Abstract

Since the beginning of gold standards, gold is always preferred over paper currency. Over the years, gold has been found to have a peculiar linkage with different asset classes. The current study is an attempt to analyse the probable relationship of gold prices with crises. The current study highlights as to how gold could act as a saviour during the time of global crisis like the current pandemic (COVID 19). Additionally, it conducts a comparative assessment of gold returns vis-à-vis equity market returns and inflation over the last decade. Finally, the study concludes with alternative gold investment options and policy remarks.

Unanimously, each one of us will agree with the golden rule of investment of not parking all funds in one pocket. Ironically, the current scenario teaches us quite the contrary. The equation so far has depicted a remarkably high sensitivity of gold (yellow metal) prices vis-à-vis any situation of a global crisis. The fundamental question that emerges here is, ‘Could Covid-19 qualify under the above equation?’ And if the answer is ‘Yes’, then, ‘Does the current move of the nations across the globe to stockpile their gold reserves yield the desired outcomes, with the prospective of changed dynamics?’ Gold serves as the saviour to enable nations to manage as the last resort. Since ancient times, gold has been serving as the common medium of exchange to replace the barter system and is now acting as a store of value to ensure stability during crises and better prospects for global trade.

Could Gold Prove to Be a New Saviour in Dealing with the Pandemic?

Right since the First World War and till the coronavirus disaster, globally, every nation and central bank has confined its trust in gold as an investment hedge to protect wealth. In the prevailing scenario, the inherent strength of any nation and its future potential depend to an extent upon the gold reserves that the nation holds. Most nations (such as India) have a history of using gold as collateral to raise funds from international markets. India raised US$400 million in 1991 from Bank of Japan and Bank of England against its gold reserves. The US Federal Reserve System has a history of continuous addition to its gold reserves since their inception (1913), with the buying spree continuing till 1939 to stockpile as much as to 19,000 tons. During the First World War and Second World War, the United States added 650 tons of gold to its reserves in 1913, followed by a 1,000-ton addition between 1915 and 1920.

Significance of Gold Reserves for a Country

For any nation, to ensure the system’s liquidity is a matter of grave concern. During a time of crisis, for maintaining liquidity in the system, gold becomes the obvious choice, due to its easy and convenient liquidation without value weakening. It was only after the 2008 financial crisis that the global platform started recognizing gold as a better ‘medium of exchange’ than the dollar, probably the only viable solution to manage any difficult situation. Additionally, a well-governed nation must have its inflation under check. Nations use gold reserves as a hedging tool to contain inflation. Moreover, unanimous acceptance of gold across the world further strengthens the case for why nations need to increase their respective gold reserves. Since gold has the unique feature of not losing its intrinsic value with time, it minimizes the prospective risk that may emerge due to underlying uncertainty. It is quite clear that since the recent COVID-19 disaster, nations have started acknowledging the significance of gold as the ultimate saviour. Undoubtedly, the current time could be considered as the ‘gold-en era’ where nations may find themselves gradually shifting from trade (cold) wars to end up contesting ‘in terms of inventory of gold reserves’. The same is witnessed in the ever increasing and quite aggressive production of gold and gold reserves by nations over the last two decades. Recent statistics indicate that China is ranked the highest in production of gold across the globe, holding a 11.54% share in the world’s gold production in 2018, followed by Australia at 8.99% .

For a nation like India, gold has an added relevance for its ethnic value as a custom. Ancient India (around the tenth century) is often referred to as a ‘golden sparrow’. Probably, this is the reason why India features among the top 10 consumers of gold and in the top 10 nations with the largest gold reserves.

Let us begin the discussion with the key affiliates that essentially and logically associate gold prices with any global crisis, like the current one. Any global crisis does leave its footprint on the stock markets of nations. Crises and stock markets move hand in hand, whereby any positive news creates a positive sentiment, and vice versa. Alternatively, it could be inferred that there is an inverse linkage between the equity market and gold prices (refer to Figure 1).

From Figure 1, the inverse association between gold prices and the equity market can be observed. Also, the gap between the two lines broadens during the crises phases—first in January 2008 (global financial crisis) and then in May 2020 (COVID-19).

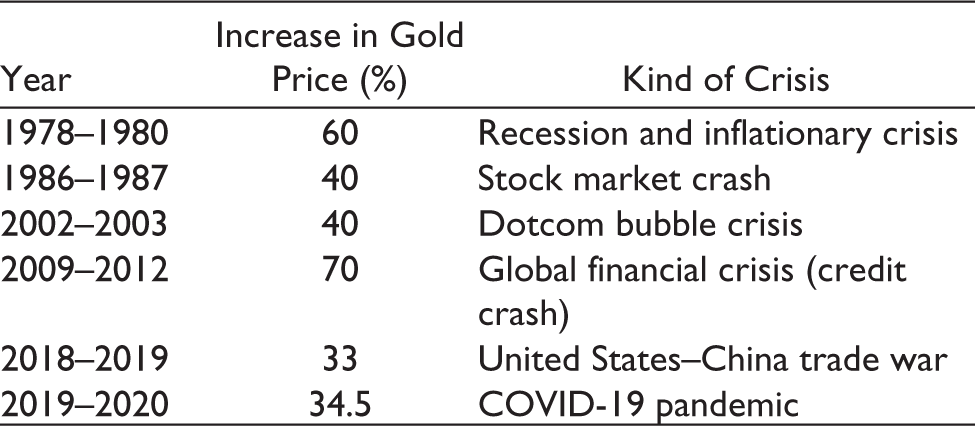

Historical evidence during recessionary and inflationary trends between 1978 and 2018 confirms the inverse linkage between any crisis and gold price (refer to Table 1), where gold prices have skyrocketed, jumping by 29% in 1978, 120% in 1979, 29% in 1980, 24% in 1987, 40% in 2002–2003, 70% in 2009–2012, 33% in 2018–2019 and 34.5% in 2019–2020. Be it the dotcom bubble, the global financial crisis in 2008, the US trade wars with such nations as Iraq, Afghanistan (2002–2008) and China (in 2018) or the COVID-19 pandemic—all have led to an expansion in gold reserves, with a pertinent buying push over the last 5 years.

Timeline of Gold Prices along with Global Crises

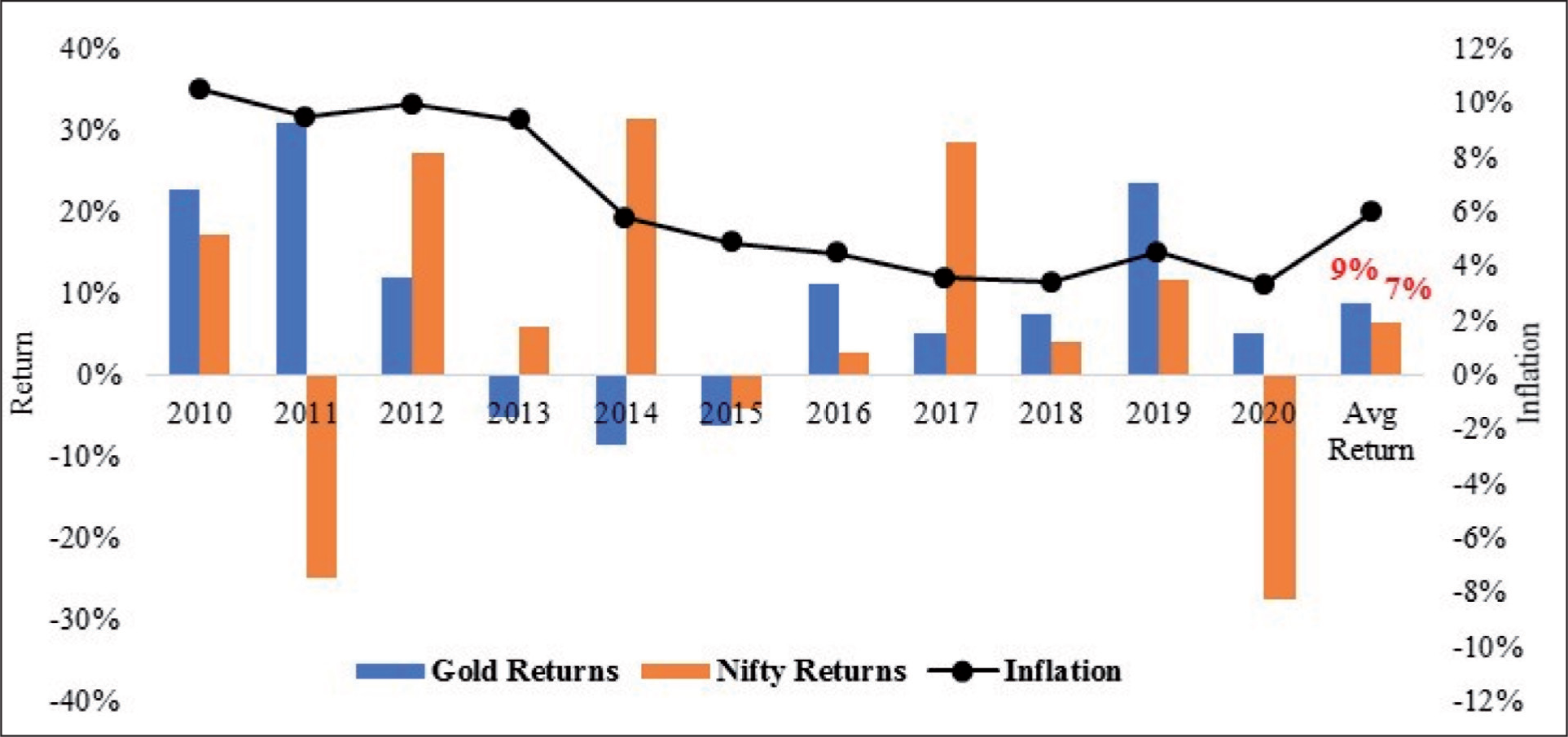

Additionally, the fundamental, behavioural and technical factors play a vital role in determining the relationship between gold and real rates (returns minus inflation). In general, there is an inverse relationship between gold prices and real interest rates, further indicating gold to be preferred over USD. Hence, the behavioural factors indicate gold as an ‘alternate currency’ in the long term, whereas the technical factors are dependent on the demand and supply of gold. Ideally, the central objective of any investment shall be to maximize the real returns (returns minus inflation) in order to beat inflation. Therefore, it is essential to compare and understand two asset classes—equity and gold returns—over the last decade, along with inflation. Figure 2 depicts the movement of gold returns vis-à-vis Nifty returns (equity market).

From Figure 2, the following key observations emerge:

Both asset classes are found to be volatile in the respective movements of the returns over the years; During the eventuality of any crisis, these two asset classes tend to move in opposite directions (refer to 2020 in Figure 2); Over the last decade, the average returns from gold are found to outperform equity by 2%; and Over the last decade, returns from gold have contained inflation a greater number of times than those from equity, with average performance by both asset classes.

Also, an investor who is willing to invest in gold and chooses to obtain benefits from gold price adjustments has several options for investing in gold in the following forms.

Investment in gold stocks could be treated as a different investment avenue with an easy and wider reach. Basically, these stocks belong to gold mining companies. An investor can decide to invest in these gold mining companies instead of lodging direct investments in gold. These days, even mutual fund houses are enabling the above by opting to invest in gold mining stocks or gold-related instruments.

Unfortunately, we can only wish for better awareness of investors through opting for gold ETFs and gold bonds over conventional methods of investing in gold. Since gold prices are highly volatile, with great responsiveness to the nation’s macroeconomic/micro-economic factors, investors should invest prudently and strategically in gold in order to ensure safety and long-term stability.

Gone the times when Gold used to be acknowledged only as a medium of exchange but now the time has come where gold is going to function more as a store of value and unit of currency in the future. Since gold and wealth are two sides of the same coin, undoubtedly, gold has a bright future ahead. There is a famous adage that goes, ‘pressure creates diamond and fire refines gold’. This shall hold its practicality for nations post the pandemic in a more pronounced way, so much as to ensure the very survival of humanity, as: ‘Real gold (Humanity) does not fear the Furnace (Pandemic)’.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Disclaimer

Views are independent of institutional affiliation.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.