Abstract

Digitalization and intelligization is the need of the hour in today’s world. The manufacturing industry is, in fact, moving towards the fourth-generation industry, which we termed as Industry 4.0 or the Fourth Industrial revolution, which is defined as a new level of organization and control over the entire value chain of the life cycle of products; it is geared towards increasingly individualized customer requirements. Industry 4.0 is all about talking in terms of big data, technology, cyber security, the Internet of Things (IoT) and so on. This study is done to understand the new emerging technology in data exchange and automation, popularly known as Industry 4.0, in terms of banking sector with context to the Indian banking sector.

The study focuses on studying banks in a digitalized word and what are the challenges that banks face. How banks cope up with digitalization, keeping customers at priority. This study centred on incorporating articles published in recent years to establish knowledge on the topic and to further identify areas for future research.

Executive Summary

The purpose of this study was to analyse the state of banking industry in India, due to digitalization. It was a review study mainly analysing the impact of industrialization on banking sector. It focused on understanding Industry 4.0, its various phases, its impact on banking sector, global banking trends and what all will be required to be incorporated in Indian banks in case of Industry 4.0 revolution. This article is primarily based on various banking industry reports created by Deloitte, PWC, Ernst & Young, CII and so on (Capgemini, 2012, 2020; EY, 2016, 2017; PwC, 2012, 2020).

The main idea line of study was to reveal all changes that banking sector is taking place due to industrial revolution 4. We tried to understand Industry 4.0 in light of banking sector: Is this revolution affecting banking or making banks move towards industrialization or digitalization? The changing scenario of banks and how they are planning for its implementation. How big data, artificial intelligence (AI) and cloud computing will help banks ahead to sustain? How will people understand all this (Jacapo, 2017)?

Besides implementation, digitalization has already been adopted by Indian banks. However, the threat of data security and everyday scandals in banking industry is a biggest threat. To implement the industrialization with proper education and taking steps for data security, avoiding cybercrime can only be a reason for success of digitalization in banks. We still exist with people loving traditional banking more than digital and on the other hand, we have people who have no time to visit banks and for them app-based banking or mobile banking is the best solution.

The study concluded that through this article we tried to throw some light on changing banking industry, with advancement of technological development how banks are changing globally. The Indian banking industry with modernization have its new meaning in post demonetization era. The banks that were working on traditional model are now being adopting emerging technologies such as Robotic Process Automation (RPA), cloud, AI and blockchain to cut down their operating expenses and improve efficiency.

In our understanding, there is an urgent need of proper policy framework. Institution and policies play a crucial role in development of finance–banking sector (Deloitte, 2020). Perhaps preparing customer for the same is also need of the hour. In Indian banking sector despite digitalization, there are many people preferring traditional banking methods. Hence, how this new trend will be welcomed and accepted in developing economies like India is really a question to look forward at. We are hearing Industry 4.0 a lot in case of manufacturing sector; it would be great to observe its implementation in banking sector too.

Introduction

The world around us is changing at a fast speed along with human civilization. Therefore, technology and technological development are also changing. Industry 4.0 is a model that shows how industrial development takes place and how it changes with time. The term Industry 4.0 means smart factory in which digital devices are networked and they communicate with whole production cycle including people, machines and material. The industry is characterized by efficient use of resources, integration of customer and business partners (Dohale & Kumar, 2018; Rojko, 2017).

India is on the cusp of digital revolution with the upcoming of various digital technologies, growing use of mobile data and smartphones. The financial sector is also receiving a push from government and various other initiatives to move towards adoption of digital driven or technologically advanced services. This transformation will bring in viable technological differences in banks, non-banking financial companies (NBFCs), insurance companies across value chain. Indian banks, NBFCs and insurance sector are already making use of digital world by cutting down operational cost, which thereby is increasing pressure of higher provisioning and capital requirement and to deliver higher customer requirements. The Reserve Bank of India is constantly motivating and pushing banks towards digitalization (Deloitte, 2020).

The idea of ‘Fourth Industrial Revolution’ may sound the best at first, it is essential to remark that there is a multitude of challenges, risks and barriers associated with its implementation namely, defining appropriate infrastructures and standards, ensuring data security and educating employees are among the issues that need to be addressed on the road to Industry 4.0 (Hofmann & Rüsch, 2017). Therefore, it is essential to locate the status of the research as well the forthcoming opportunities in future research on Industry 4.0 (Zhou et al., 2015).

One of the sectors that is going to be impacted by Fourth Industrial Revolution (Industry 4.0) is financial banking sector. Achievement in various other sector will not only lead to developing of finance–banking sector, but it will also be raising issues related to development of banking sector (Cộng Sản et al., 2019).

This article is structured as follows. In the second section, Industry 4.0 origin and concept will be discussed. Section 3 will discuss about adaptability of Industry 4.0 in global perspective. Section 4 will through some light on Indian banking sector and adaption of industry 4.0. Section 5 will talk about emerging trends in banking sector with adaption of industry 4.0 in banking sector. Section 6 will discuss various issues and challenges in implementation. In the last section, conclusions are drawn and general topics are discussed.

Industry 4.0 Origin, Concept and Definition

The ‘Industry 4.0’ is often referred to as Fourth Industrial Revolution, in fact two terms are often used interchangeably. ‘Industry 4.0’ refers to the concept of factories in which machines are augmented with wireless connectivity and sensors, connected to a system that can visualize the entire production line and make decisions on its own (Fettermann et al., 2018; Rojko, 2017).

The Industry 4.0 concept originates from Germany and it is not surprising at all because Germany has the most competitive manufacturing industry in the world or perhaps we can grade them as leaders in an area (Ghobakhloo, 2018). The basic concept was first introduced in Hannover Fair in the year 2011. Since then, it began as one of the most talked about topic of research.

The basic idea line is to exploit the potentials of new technologies and concept such as:

Availability and use of Internet and IoT. Integrating technical and digital process. Digital mapping and virtualization of real world.

Industry 4.0 refers to recent technological advances where the Internet and supporting technologies (e.g., embedded systems) serve as a backbone to integrate physical objects, human actors, intelligent machines, production lines and processes across organizational boundaries to form a new kind of intelligent, networked and agile value chain (Prause & Atari, 2017).

The German interpretation of smart production, Industry 4.0, goes even further than by additionally tackling energy and resource efficiency, as well as increasing productivity and shortening innovation and time-to-market cycles (Kagermann et al., 2013). Internet-based linked machine-to-machine interaction paves the way to networked manufacturing systems and cross-company production processes that enable the design and control of the product’s entire supply chain during its full life time (Buer et al., 2018; Brettel et al., 2014).

According to Brunelli et al. (2017), nine tools were identified as influencing tools for manufacturing sector, such as robots, augmented reality, simulation, addictive manufacturing, vertical and horizontal system integration, IIoT, Cloud computing, big data and cyber security. To avail benefits of digitalization, it is of prime importance for companies to implement and manage information system within organization effectively. In such environment, integration, migration to cloud technology and building cyber resilience is important. As mentioned by Hercko and Hnat (2015), the successful implementation of industry 4.0 depends on the use of six principles such as interoperability, virtualization, decentralization, capacities in real time, service orientation, modularity and re-configurability.

What is Industry 4.0?

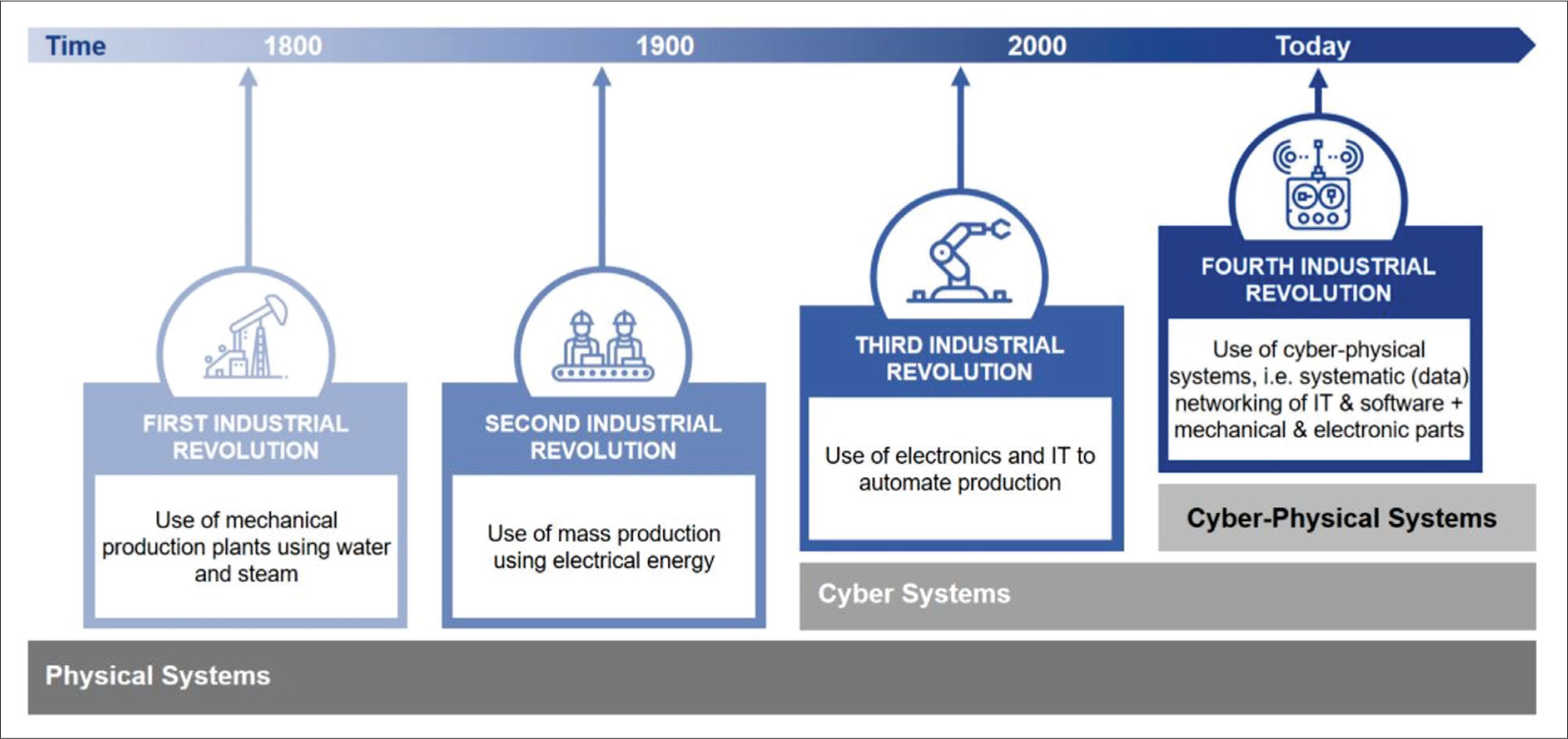

While Industry 3.0 focused on the automation of single machines and processes, Industry 4.0 focuses on the end-to-end digitization of all physical assets and integration into digital ecosystems.

The first modern transformation saw Britain move from farming to factory production in the nineteenth century. The second phase spread over the period from the 1850s to the First World War and started with the introduction of steel, electrical industrialization and mass production, and spouts of large-scale manufacturing (Mourtzis, 2016). Finally, the Third Revolution refers to the change from simple, mechanical and electronic innovation to advanced innovation that occurred from the late 1950s to the late 1970s. The fourth, at that point, is the move towards digitization. Industry 4.0 uses the IoT and digital physical frameworks, for example, sensors to gather tremendous measures of information that can be utilized by manufacturers and producers to break down and improve their work.

Industry 4.0 is the concept relating to the idea of ‘industrial revolution’ whose main objective is the integration of production processes with the information technologies and techniques (Dohale & Kumar, 2018). It combines production methods with information and communications technology. It assumes that products can be manufactured based on the individual needs of customers. Industry 4.0 makes it possible to produce items that are unique in excellent quality and at a price equal to that of mass-produced goods. Smart, digitally connected systems and production processes serve as the technical basis for this concept. Industry 4.0 also defines the entire life cycle of a product: from idea to development, manufacturing, use and maintenance, and ending on recycling of the product.

Industry 4.0 was initially developed by German industries in order to maintain their competitiveness on global markets. The main features of Industry 4.0 are:

Industry 4.0 Adaption in Banking Sector [Global Prospective]

In the ever-changing work and copying with the requirement of customer, corporates today are moving towards end-to-end connection. This creates pressure on banks to be available for them anywhere anytime to cater to their ever-growing business needs. Corporates now expect their banks to provide optimized, friction-free and digitalized processes across the full range of customer journeys, for example, account opening including Know Your Customer (KYC) checks, credit applications and the set-up of cash pooling structures including associated legal documentation.

The global banking sector is changing into each a lot of strategically centred associate degreed technologically advanced to reply to consumer expectations, whereas attempting to defend market share against an increasing array of competitors. A good deal of stress is being placed on digitizing core business processes and reassessing structure structures and internal talent to be higher ready for the longer term of banking. This transformation illustrates the increasing want to become a ‘digital bank’.

The innovation and developing new solutions that take advantage of data, advanced analytics, digital technologies and new delivery platforms have never been more important. We are seeing organizations innovate in targeting, expanding services, re-configuring delivery channels, delivering proactive advice, integrating payments and applying blockchain technology.

Countries around the world have different approach to Industry 4.0 in general and in finance–banking 4.0 in particularly. We can divide the response of countries in two parameters—active and passive. Those who deal with active change often interact with creator of change to capture new developments in financial technologies, legal obstacles to overcome the challenges. They work to develop overall policies, abide by the legal environment. In most of the cases, these countries are usually the advanced countries having developed markets and high innovation and technology (Rojko, 2017).

The countries dealing with passive change, this is usually a case where Industry 4.0 has not yet caused big impact to their markets. These countries are usually the ones, which have many legal and IT restrictions in human resource development. All these factors lead to obstacles in innovation and implementation of Industry 4.0 technology.

In order to overcome such issues, certain countries have already developed their legal framework (an important security software). Major financial corporations around the world have paid more attention to infrastructure in international payment, for example, the six largest banks in the world established the ‘Block Chain Utility Settlement Coin’ project, allowing stock transactions without money transfers, or inter-national payment provider (PSP) network, such as Earthport, allowing quick payments to all bank accounts in more than 65 countries around the world.

KPMG Banking Systems Survey (2018) mentions about the new Industry 4.0 innovation in finance sector which is called Payment Services Directive II (PSD2). This is likely to become a huge game changer in banking sector. It is the concept of ‘open banking’ where, banks will share customer transaction and account data with third parties, including retailers, telco providers, payments services and financial account aggregators. PSD2 will be a trigger to open up the current banking landscape to new players in financial arena, with moving towards new customer experiences, bringing possible disruption to banks. RatingsDirect reveals of the usage of new concepts like ‘cryptocurrency’ in banking. Cryptocurrencies are digital currencies that use encryption techniques to regulate the generation of units of currency and verify the transfer of funds.

According to Rajan and Kuder (2017), banks use AI to improve customer service by learning from customer behaviour and delivering more precisely on customer preferences in tailoring the customer journey. Thus, these technologies can be used to respond customers efficiently via cognitive call centres. The use of these advance technologies will help banks to improve the accuracy of the operations while reducing human errors.

Industry 4.0 Preparedness in Indian Banking Sector

The banking sector plays a vital role in the economic growth of an economy not only by converting your savings into investments but also by efficiently utilizing available economic resources. The Indian banking sector have witnessed a huge transformation under various financial sector reforms taking place over a decade.

Technology has touched almost all aspects of human development. The digitalization has reached to a level where we cannot imagine our lives without digitalization. As times goes by, traditional banking system will become obsolete.

The need for digitalization was felt in banking in 1980s in order to improve customer satisfaction and maintaining accounts and ledgers and MIS reporting. In 1988, RBI developed a committee for digitalization under Dr C. Rangarajan. Banks began to use standalone PCs and further moved on to LAN network. With further advancement, banks adopted core banking system (CBS). CBS was a step towards customers comfort through anywhere anytime banking.

RBI has been a guiding force in giving recommendations and improving banking sector for better serving people. Today banks aim to provide fast, accurate and quality banking experience to their customers. Today, the topmost agenda for all the banks in India is digitization. Implementation of electronic payment system such as NEFT (national electronic fund transfer), ECS (electronic clearing service), RTGS (real-time gross settlement), cheque truncation system, mobile banking system, debit cards, credit cards, and prepaid cards have all gained wide acceptance in Indian banks.

Stages of Banking Technology Revolution in India

These are all remarkable landmarks in the digital revolution in the banking sector. Online banking has changed the face of banking and brought about a noteworthy transformation in the banking operations.

Emerging Trends in Banking 4.0

The Indian financial sector continues to rapidly embrace digitalization due to government push. This trend has been a further push by the emergence of Fintech players, who are playing a significant role in value chain creation.

The diversified Indian financial sector is at the verge of change. The change is inevitable and an embedded part of growth in any organization. The emerging trends are supposed to bring some useful features in the industry by updating the operational procedures with innovative technologies, maximizing the satisfaction level of both the customers and service providers and boosting the industry growth factors. Some of these trends as figured out by CII report are as follows:

A consortium of India’s 11 biggest banks including ICICI Bank, HDFC Bank, Yes Bank, Standard Chartered Bank, Axis Bank and so on have launched the first ever blockchain-connected loan framework in FY19. This framework can be utilized for automatic account opening process, finishing KYC formalities, international payments and so on. However, the system is new but it is expected to cross US $ 5 billion across all sectors in India in next five years. Adoption of AI will help banking sector by establishing innovative product and services. Humanoid Chatbot interface to interact with customers. OCR or optical character recognition system for capturing documents. Use of Bot Advisors for managing the client’s personal portfolio by analysing risk and return on investment. Image/Face recognition facility in ATMs by using real camera with advance AI techniques to prevent frauds. Thought just like other innovations, AI is at its primary stage, but its use can be effective for banking sector. Multiple banks in India like HDFC and ICICI banks have started using chatbots for customer service. Last year, Canara bank installed robots in some of its offices to interact with customers. According to CII, financial services report 2019, the appropriate use of AI expects to add nearly US $1 trillion in the Indian Economy by 2035. However, key challenges like availability of person with proper skills of data science, inserting details of 150+ languages in the robots and system can be hectic. Cloud service is considered as one of the finest methods comparing to hard drives. Under this service, information is encrypted and backed up continuously. The cloud-based service can be used for accounting, inventory, human resource and customer relationship management. The capital expenditure and ongoing operational cost can be reduced. Besides, data stored in cloud can be easily accessible. It also allows user to choose the service required on pay as you go basis. Cloud computing enables bank to switch over to changing customer need and demands. Citibank wealth management replaced its fragmented CRM system with a unified cloud-based solution for providing customer a better experience. Yes Bank also moved all its applications on cloud-based service in 2011. Greater usage of this will speed up work, increase efficiency, performance and security. Those kind of role of APIs guide the bank to add suitable feature in the procedure of online banking, customer data, cards, payments and accounts and strengthen their revenue structure. In India, Yes Bank was one of the first bank to launch API banking services to digitize B2B supply chain. Moreover, ICICI, RBI, Kotak bank, DCB bank and Citibank have seemed to be adopted this approach. ICICI Pockets is India’s first digital bank. These banks are attracted by customers only because of technological advancement and cost-effective operational models. Banking industry in India is rapidly evolving facilitated by mobile and internet penetration in the country and technological innovations disrupting the established processes. In the last couple of years, technologies such as digital wallets, EMV chip-based cards and two-factor authentication via SMS-based one-time password (OTP) have become mainstream in India. These innovations were designed to make payment transactions convenient and more secure. According to a report, between 2008 and 2017, Indian banks faced INR 700 billion worth of cyber fraud cases. The banking system needs to prepare itself to address the risks and challenges. Proper IT system, regular scrutiny for appropriate policy and supervisory intervention, offsite monitoring mechanism, structured audit management system, active cyber security cell with advanced infrastructure are highly required.

Industry 4.0 Issues and Challenges for Indian Banking Sector

In a country like India where issues like digital literacy, financial inclusions and Internet, penetration poses a deep challenge for banks. To ensure success, they need to disrupt existing systems and patterns with innovative solutions that ensure quick and prompt user adoption. Constantly changing regulations also pose another hurdle for these institutions to overcome, along with other challenges such as how banks carry out KYC processes, preserve digital identities, handle data storage, ensure cyber security and carry out customer communications.

In India, while new generation wants digitalization in everything they do, the old or middle age still, prefer the traditional banking model. In India, branch banking is often considered as an outing prospect for old-aged or superannuated people, they prefer to visit banks and meet old friends and staff. Despite these, the need of an hour demands banks to move towards digitalization.

Emergence of technological advancement has resulted into expansion of more fintech collaboration across the country.

The technologies have made mobile just not as a means of communication, but an important device to perform all banking task.

It is turning more challenging for banks with upcoming of advanced technology to serve their customers at best and to retain customers well.

Getting advanced is leading to employment of skilled staff that can operate and deal with technology.

Besides, installation of ATMs, Cash Deposit Machine, Cheque Deposit Machine and Passbook Printing Machine across innumerable corners of the country have made the banking work easy.

Interest of moving towards 5G technology has increased.

With the advanced, fast and unique features, each of the trends is capable to bring revolution in the Indian banking industry. However, many remote parts of this country are still unbanked, and a significant portion of the population is comfortable using the traditional banking system. Hence, smooth expansion of all the mentioned trends might take some time. Hopefully, with the increase in number of digitally literate people and better digital infrastructure sector, will have better growth momentum.

AI, Cloud Computing and Blockchain Adaptability in Banking Sector in India

India, being at emergence of adopting technology, can lead to it fastest development. Indian banks have begun to adopt AI. Globally the AI and blockchain are used extensively for back office operation and while dealing with customers. In India, some of the leading financial services are collaborating for adoption of these services. This interface is adopted by four leading banks in India.

Blockchain technology, also known as decentralized distributed ledger technology, has gained importance in India. Many banks India have started investing in technology in order to serve their customers in best possible manner. Blockchain is one of most popular weapons in terms of some of popular issues like fraud and loss of data, completing KYC; this is emerging as a biggest solution. Blockchain is also considered as a technology behind cryptocurrencies.

Let us consider the case of cross border transactions. These transactions take more than usual time in processing, a transaction has to pass on through lot of intermediaries for authentication before it reaches finally customer. Whole of this process leads to wastage of time and incur high costs, further it also leads to risk of money laundering, as true source of transaction is inaccessible. Blockchain helps in elimination of these intermediaries and helps in speeding up the transactions. It also uses the common decentralization ledger; this facility eliminates the intermediary and help in clearing and settling securities faster.

The use of blockchain technology has been beneficial in bringing accountability in the trade financing, as there has been unending NPA in banking sector. A blockchain exchange for NPAs can help banks in maintaining these documents related to assets at one place. The consortium of 11 banks including Kotak Mahindra bank, ICICI, Yes Bank, Axis, HDFC, standard chartered, RBL, South Indian Bank was formed to introduce and run a blockchain-linked loan system for small and medium enterprise. Whereas SBI, Bank of Baroda and IndusInd are outside members.

With more and more banks, moving towards its implementation, somehow this has become all the more important to understand its actual advantage. The financial industry with blockchain technology is providing us with a real-time solution. This has increased transparency and enabled banks in making real-time fraud analysis that further helps financial sector in building trust. This all is purely at implementation stage but, looking at the positive side, this will help financial sector in becoming more transparent and reliant.

Digital Transformation in India

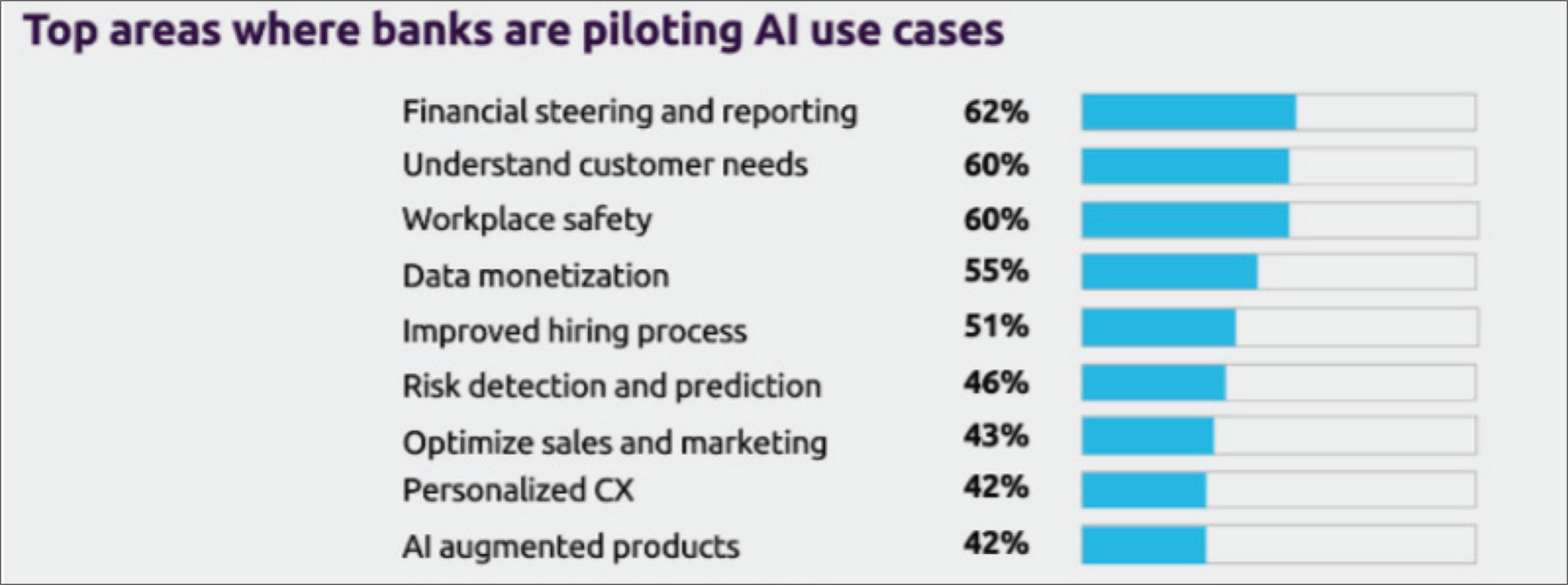

AI is growing at a sharp speed in India. As per recent report of Capgemini (2020), we can see a remarkable trend in Indian usage of AI. Further, there are some specific areas where the banks are using AI extensively.

The data clearly depict that 62 per cent of the banks financial steering and reporting is done using AI (Figure 2). Whereas approximately 60 per cent of banks understands customer needs with the help of AI, which in self is a big chunk of data. Whereas for improved hiring process 51 per cent banks rely on AI, whereby 46 per cent rely on risk detection with the help of technological development (Capgemini, 2020; Deloitte, 2020).

The banking sector is taking an upward turn based on new and innovative technology. Today banking sector is standing at the verge of development and advancement and they are trying to capture maximum consumer interest and satisfaction. It will be exciting to monitor the journey of banking sector in terms of various upcoming technologies and developments. Digital and advanced banking is replacing our tradition brick and mortar banking to a green banking. Digitalization has helped largely in reducing errors. This is a boon to a banking sector as it helps in increasing banking efficiency, further to customer at large it is a biggest benefit.

Conclusion and Future Work

We tried through this article to throw some light on the changing banking industry, with the advancement of technological developments and how banks are changing globally. The Indian banking industry with modernization has a new meaning in the post-demonetization era. Banks working on a traditional model are now adopting emerging technologies such as RPA, cloud, AI and blockchain to reduce their operating expenses and improve efficiency.

There is no doubt that the ongoing push towards digitalization is quickly affecting customary banking models. It has also expanded organizations to increasing cyber security dangers and vulnerabilities. Banks are progressively taking a gander at rising advancements, for example, blockchain and analytics in making a functioning guard component against cybercrimes.

With the help of this article, we tried to explore various avenues in the implementation of Industry 4.0 in the finance–banking sector. What could be the desired challenges for banks, what are their constraints and how will they implement it?

The banking sector is on the verge of expansion, and digitalization will not only make it easier but will also increase its profitability. Further banking today has moved beyond the traditional banking model. It will be interesting to see how upcoming technologies will be adopted by customers, implemented by banks and regulated by the government.

In our understanding, there is an urgent need for a proper policy framework. Institutions and policies play a crucial role in the development of the finance–banking sector. Perhaps, preparing the customer for the same is also a need of the hour. In the Indian banking sector, despite digitalization, many people prefer traditional banking methods. Hence, how this new trend will be welcomed and accepted in developing economies like India is really a question to look forward to. We are hearing about Industry 4.0 a lot in the case of the manufacturing sector; it would be great to observe its implementation in the banking sector too. Further, it would be great to have a comparative analysis of these technologies in terms of two Indian banks, private or public sector banks and so on.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.