Abstract

The consistent gender gap in financial inclusion over time is postulated by World Bank Findex data despite an increase in the overall financial inclusion level around the globe. Women’s financial inclusion is significant in line with the promotion of gender equality- one of the 17 Sustainable Development Goals adopted by the United Nations. Academic literatures have fragmented studies on women’s financial inclusion and there is a dearth of systematic literature review to comprehend the overall literature landscape in analyzing research gaps. This article is an attempt to conduct a structured systematic literature review to identify factors impacting women’s financial inclusion, the associated gender gap and importance of promoting greater financial inclusion for women. Literature reviews are important to map the existing landscape of a study problem and develop further knowledge. This study reviews 75 peer reviewed articles from 2000 to 2021 and presents the findings in a comprehensive manner following a conceptual model. Synthesized evidence reveal the existence of gendered financial inclusion mainly due to demand side factors. Various socio-economic and cultural factors are also seen to influence women’s financial exclusion. Based on the mapping of existing findings the study suggests future research directions where emerging themes lie in the areas related to digital finance, financial self-efficacy and financial literacy which are important for enhancing women’s financial inclusion.

Keywords

Introduction

Financial inclusion implying affordable access to formal financial services for the poor is an important policy goal for nations across the world. It is postulated to be instrumental in reducing poverty and promoting sustainable growth (Demirguc-kunt et al., 2017). Financial inclusion for women is particularly given emphasis in the current times because of the benefits it can have on society and economy at large in terms of growth and empowerment (Holloway et al., 2017). The significance of women’s financial inclusion is also in line with the promotion of gender equality—one of the 17 sustainable development goals adopted by the United Nations—emphasizing on ‘ending all discrimination against women and girls as a basic human right’. Evidence suggest the presence of gender gap in use of financial services in poorer countries (Arnold & Gammage, 2019; Johnson, 2004), and this gender gap has been one major factor obstructing growth in women-operated businesses (Chaudhuri et al., 2020; Muravyev et al., 2009). The gendered differences in accessing formal sources of finance is an issue of debate among researchers (Sholevar & Harris, 2020), and despite efforts placed in reducing the gap, there has not been promising sustainable results (Eckhoff et al., 2019; Shoma, 2019). As the Global Findex data (2011, 2014, 2017) by the World Bank points out, though there has been considerable increase in account ownership across countries among men and women, the gender gap in account ownership remains consistent at 7% points throughout these years (Demirguc-Kunt et al., 2018). A country’s regulatory arrangements play significant roles for women inclusion in the formal financial system but failure of proper redistributive measures in addressing gendered socio-economic differences would reproduce financial exclusion of women (Natile, 2019).

In the early stages, financial inclusion was identified with ‘access’ to bank accounts by the poor. This concept has gone beyond just ‘access’ and broadened with time to include ‘usage’ of different financial services as a parameter to gauge financial inclusion attainment in an economy. The different factors associated with achieving faster financial inclusion is attributed to financial literacy, digitalization, financial self-efficacy and microfinance. Microfinance has shown promising results in bringing the poor and especially women into the spectrum of financial services and promoted women empowerment through different schemes and self-help groups (Nagaraj & Sundaram, 2017; Subrahmanyam & Santosh, 2019). However, greater financial inclusion of women calls for addressing gendered barriers and investing in social norm changes (Arnold & Gammage, 2019).

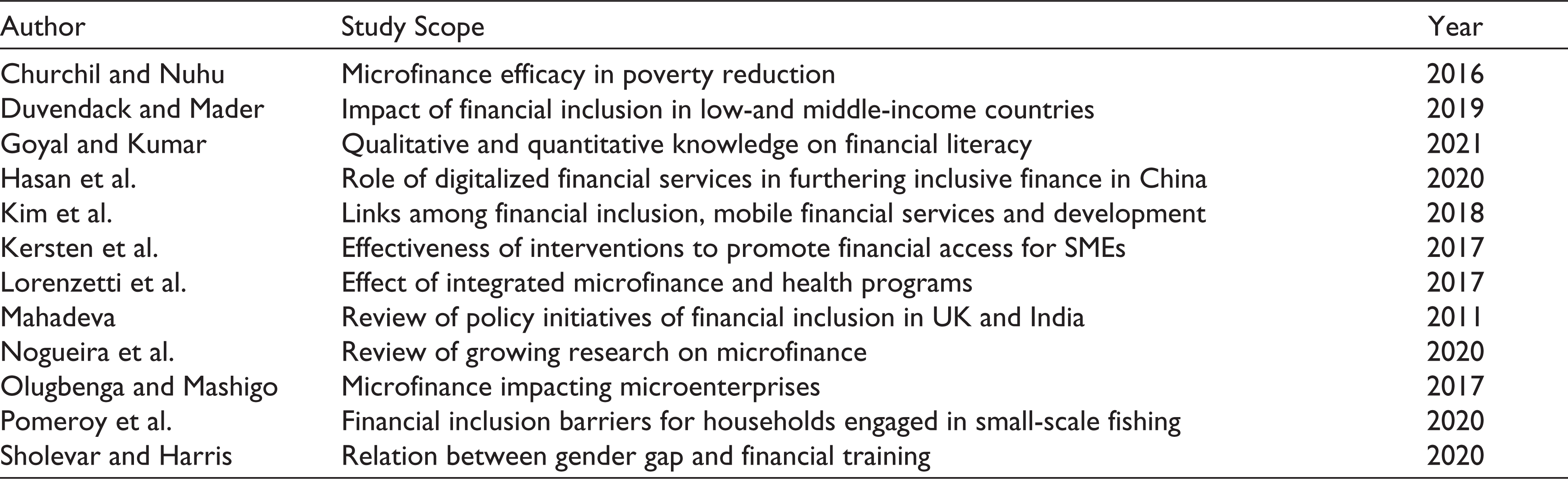

Financial inclusion for women is a broad topic, and there have been a considerable amount of studies in this area. The current academic literature, nonetheless, lacks a comprehensive and systematic review related to women’s financial inclusion and the associated gender gap. The existing reviews related to financial inclusion mostly focus on microfinance, financial literacy and digital financial inclusion (Churchill & Nuhu, 2016; Goyal & Kumar, 2021; Hasan et al., 2020; Kim et al., 2018; Lorenzetti et al., 2017). Some of the recent systematic review papers related to the financial inclusion are listed in Table 1 along with their study scope. The purpose of this study in identifying the importance of promoting women’s financial inclusion calls for determining the status of extant research and highlighting important research gaps to assist in future research endeavors. This is one of the most important purposes of a systematic review (Paul & Criado, 2020). A systematic review strengthens the foundation of knowledge by thorough inspection and synthesis of knowledge from existing research. Traditional narrative reviews are often not considered as reliable for they are not extensive and mostly not regarded as ‘genuine pieces of investigatory science’ (Tranfield et al., 2003). In this regard, this article focuses on providing a comprehensive mapping of evidence from the extant academic literatures focusing on the theme of gender and financial inclusion.

Some Recent Systematic Review Papers Related to Financial Inclusion

Geographic Scope of the Article

The prevailing gender differences in accessing different sources of formal finance is more pronounced for the poor and developing economies as compared to the developed ones (Demirguc-Kunt et al., 2015). This variation may be ascribed to, among others, differences in institutional set ups. The gap with respect to gender in bank account access is more prominent in South Asian economies, and there are also noticeable differences among high- and low-income economies in usage of banking services (Cabeza-García et al., 2019). In fact, research related to women’s financial inclusion is much more in developed countries which necessitate highlighting the context of less developed ones. In this article, the countries of Sub-Saharan Africa (SSA) and South Asia categorized under low-income and/or lower-middle-income groups have been considered for the study. The country classifications to define low- and lower-middle-income countries have been taken from country classifications (2020) by World Bank Country and Lending Groups where the classification of countries (high-income, upper-middle-income, lower-middle-income and low-income) have been done as per their level of development (measured by per capita gross national income [GNI]). According to the classification of countries by region, out of a total 48 SSA countries, 41 are classified as low- or lower-mid-income countries. Putting in other words, almost 86% of total SSA countries belong to the low- or lower-mid-income strata. Similar is the case of South Asian countries where seven out of eight countries are in low- or lower-middle-income strata. Majority of countries in other regions are high or upper-middle-income economies as shown in Figure 1. This study is focused on poor developing economics due to which the regions of South Asia and SSA deemed suitable.

Study Gap, Research Questions and Objectives

A logical synthesis of the findings of prior studies leads to the advancement of a subject (Kumar et al., 2019) achievable through a well-crafted review of the literature. This is highly helpful especially for young researchers for it has the potential to identify research gaps and providing future research directions in the current field related to methods, variables or theories. Similar thought is suggested by Marabelli and Newell (2014), in that systematic reviews are meant to impart critical examination of a set research theme through integration of the existent literature and identification of research gaps.

In the financial inclusion literature, there are ample studies exploring women’s financial inclusion or the associated gender gap, but the studies have addressed diverse themes and mixed findings which make this study topic fragmented. This diversity and abundance can be overwhelming for researchers in analyzing the gaps for different related research questions in this topic of interest which is solvable through a well-conducted systematic review. As already mentioned, while earlier reviews have assessed the associated keywords related to financial inclusion, the women’s financial inclusion and the gender gap has not been studied broadly through a systematic review in well-recognized journals. This is an addition to the existing literature landscape.

So, there are two-fold objectives for this study—one, to find answers to the research questions on women’s financial inclusion and its gender gap—questions on what different kind of barriers women face in terms of inclusive financial services in developing countries, is gender gap in financial inclusion a reality and whether it is a demand side or supply side barrier, the impacts of increasing women’s financial inclusion and ways of promoting women’s financial inclusion to contribute to sustainable development. Two, to discern the findings in analyzing the knowledge gaps and suggesting directions for future research endeavors. In this regard, this article has reviewed academic evidence on the studies related to two aspects: women’s inclusion and gender gap in formal financial spectrum.

Moreover, this article is not a traditional literature review providing just a summary of the findings from the literatures but a thoroughly inspected analysis of the diverse topics in the existing knowledge landscape where the findings are reported based on a built conceptual framework. This study, through a systematic review, tries to bring the bits and pieces together to give an insight on the existing study findings. Furthermore, the study contributes to the current knowledge state in highlighting the importance of inclusive finance for women, influence of social and cultural norms in determining women’s ability to avail formal financial services, and identifying the challenges in promoting gender inclusive finance under an umbrella and provides comprehensibility thus, opening doors especially for beginner researchers in this area.

This structured systematic review is done through 75 peer-reviewed articles, and the results portray the extant literature addressing topics categorized into two major clusters: ‘the backward linkages’ and ‘the forward linkages’ of women’s financial inclusion. These are further classified into sub-groups addressing firm-level and household-level studies as well as analyzing impact studies on various social and macro-economic factors. The second section outlines the methodology used in extracting the research articles for the structured review followed by the detailed analysis of findings in the third section. A discussion on research gaps and future research directions is put forward in the fourth section while the fifth section concludes the study.

Methodology Used for the Study

Tranfield et al. (2003) have identified a three-step approach for conducting a systematic review, also followed by (Kim et al., 2018). This approach has been considered as the base methodology in carrying out the process of review in this article with the following stages:

Planning of the review—Identifying search strategy and determining the inclusion/exclusion criteria Execution of the review—Study search and data abstraction Reporting of the results

Planning

Determining the Search Strategy

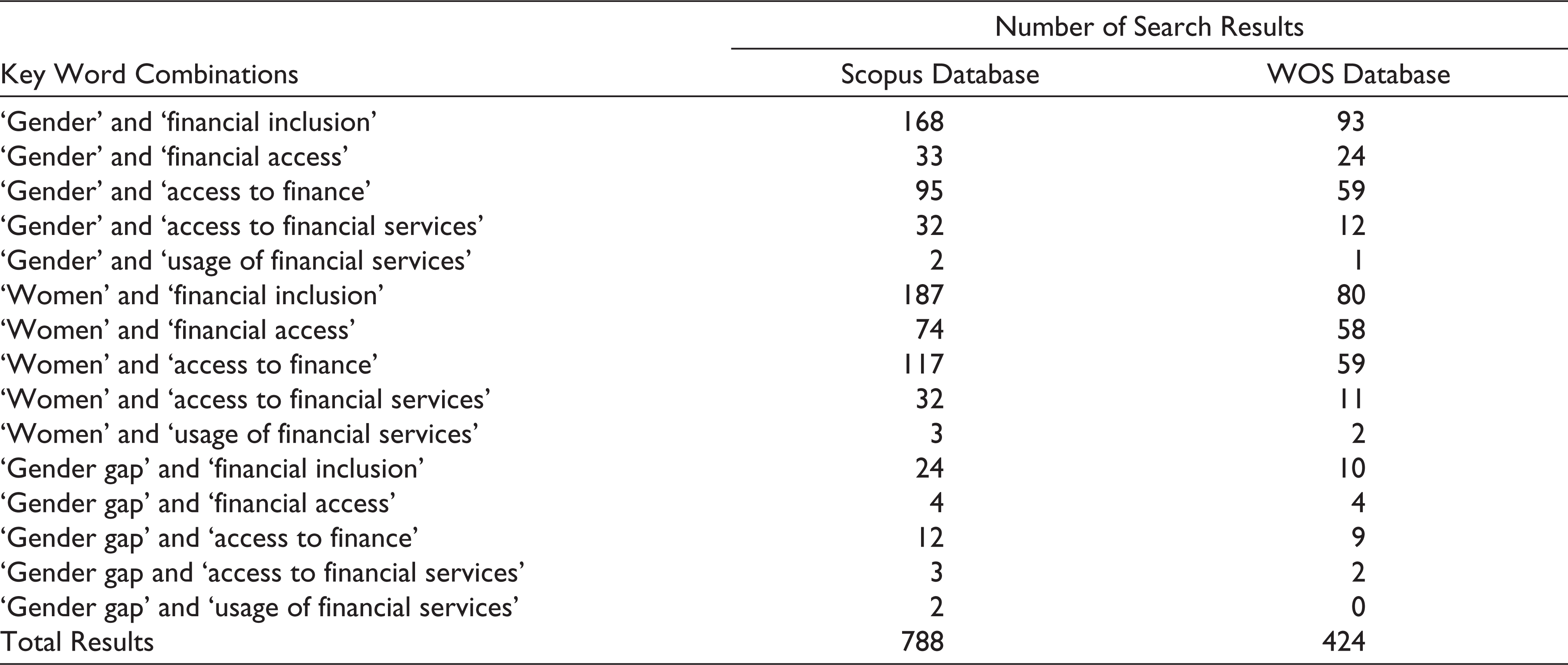

Three key words have been identified for extraction of relevant studies: women, gender gap and financial inclusion. Financial inclusion has various alternative terms used interchangeably among which the most commonly used terms are financial access, access to finance, access to financial services and usage of financial services. This has led to 15 combinations of search key words: ‘gender’ and ‘financial inclusion’; ‘gender’ and ‘financial access’; ‘gender and access to finance’; ‘gender’ and ‘access to financial services’; ‘gender’ and ‘usage of financial services’; ‘gender gap’ and ‘financial inclusion’; ‘gender gap’ and ‘financial access’; ‘gender gap’ and ‘access to finance’; ‘gender gap’ and ‘access to financial services’; ‘gender gap’ and ‘usage of financial services’; ‘women’ and ‘financial inclusion’; ‘women’ and ‘financial access’; ‘women’ and ‘access to finance’; ‘women’ and ‘access to financial services’ and ‘women’ and ‘usage of financial services’.

Selection of Search Database

Two major electronic databases viz. Scopus and Web of Science (WOS) have been considered for searching relevant articles. These global citation databases include publications in top-tier journals, and are used and trusted widely by a huge number of academic, corporate and government institutions for producing quality research.

Inclusion/Exclusion Criteria

Financial inclusion was more pronounced and gained formal importance in policy interventions since early 2000s. Thus, studies prior to 2000s have not been considered for this review. This restricts the articles by publication years from 2000 to 2021. Additionally, the articles considered for this review have met the following inclusion/exclusion criteria:

Exclusion of articles written in languages other than English Exclusion of articles having study areas other than countries of SSA and South Asia under ‘low’ and ‘lower-middle’ income groups. However, some of the cross-country studies have been considered for the review given that these studies include the above-mentioned economies Inclusion of only peer reviewed articles Exclusion of books or book chapters Studies not assessing women’s financial inclusion or gender differences in financial inclusion as main theme are also excluded

According to the World Bank definition, ‘Financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs—transactions, payments, savings, credit and insurance—delivered in a responsible and sustainable way’. In line with the above definition, financial inclusion in this article will be referred to ‘access’ and ‘usage’ of an array of formal financial services such as bank account, savings, credit, postal accounts, payments and remittances, and also include microfinance and digital financial services like mobile banking or mobile payments.

Execution

The execution stage consisted in searching of studies using the key word combinations as determined in the planning stage. In the next step, studies have been screened and filtered according to the inclusion/exclusion criteria decided at the planning stage.

Study Search and Screening

A systematic search of literatures have generated a total of 1212 search results—788 from Scopus and 424 from the WOS, as displayed in Table 2, out of which 637 duplicate articles in total have been eliminated. The remaining 575 articles have been screened according to some of the inclusion/exclusion criteria resulting in 156 eliminations. The process of execution is shown in Figure 2. An abstract review on the remaining articles resulted in further 328 exclusions which do not consider financial inclusion of women or gender gap in financial inclusion as major themes in their study. The screening of remaining 91 articles resulted in elimination of 16 more articles. Finally, a total of 75 articles have been extracted for full paper review.

Search Results from the Databases

Reporting the Results

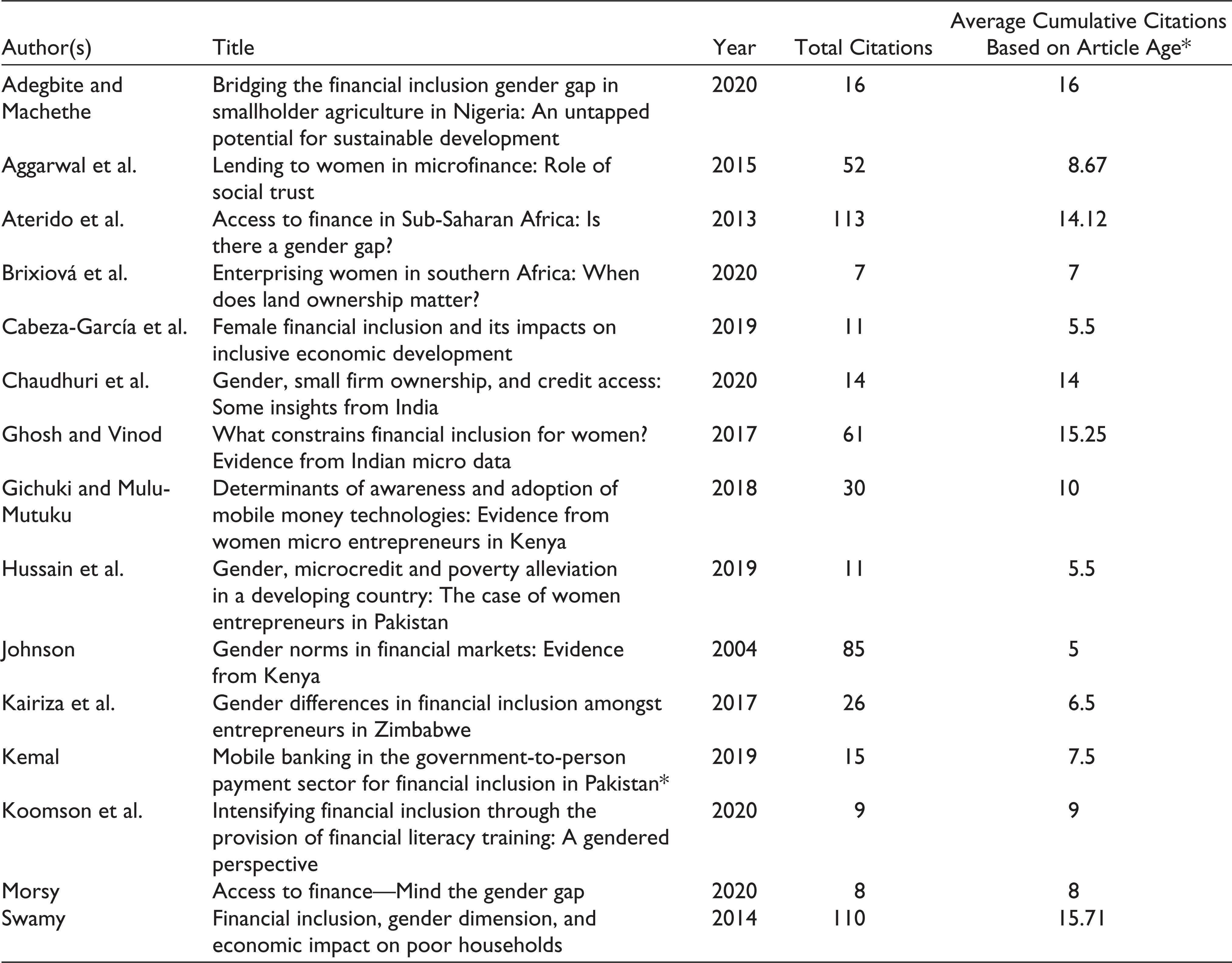

The descriptive summary of studies is presented through bar and pie charts in this section. Additionally, the extracted papers for this review have also been assessed on the basis of average cumulative citations based on article age, and some of the highly cited papers are displayed in Table 3.

Some of the Frequently Cited Papers

The study search has been conducted from 2000 to 2021. The trend of publication in time shows limited research in the early 2000s. The timeline of publications does not show a perfect trend. There have been an upsurge of studies from 2016, and the highest number of research articles has been published in 2019 as shown in Figure 3.

Figure 4 depicts the number of studies in different countries along with percentages of studies in different regions. Nearly, 44% of studies are from the South Asian region while 28% are from the SSA region. However, among 20 cross-country studies, six are cross-country studies of the African region.

There are 18 qualitative and 57 quantitative papers (Figure 5). Among them, 28 studies used primary data sources while there are 43 articles using secondary data sources while the remaining four studies used both primary and secondary data sources (Figure 6). Most of the primary studies have used multistage random sampling for data collection, while focus group interviews are also common in a handful of studies. There are several secondary data sources among which World Bank Global Findex, World Bank Enterprise Survey and Finscope Consumer Survey are the most common ones. The quantitative studies have most commonly used logit and probit models for analysis.

Findings

The search results generating 75 articles for full paper review address different interventions. The articles are categorized on the basis of the conceptual model as shown in Figure 7 describing the backward and forward linkages of women’s financial inclusion. Backward linkages describe the different factors determining or impacting women’s financial inclusion. The forward linkages describe the impacts increased women’s financial inclusion has on different factors. Financial inclusion as defined can be seen in terms of access to or use of different financial services such as bank account ownership, savings and credit, post office account, microfinance or digital financial services.

Few of the literatures which do not study factors of women’s financial inclusion, rather only consider significance of demographic variables determining financial inclusion in general have been excluded (Dar & Ahmed, 2020; Irankunda & Bergeijk, 2019; Mala & Vijayarangan, 2019; Musweu et al., 2018; Oluwatayo, 2014; Soumaré et al., 2016).

Backward Linkages of Women’s Financial Inclusion

The studied literatures examine the backward linkages at two data levels: firms and household/individuals.

Findings from Studies at Firm Level

The firm-level studies mostly focused on ‘access to credit’ as financial inclusion measure and explained various factors and constraints affecting demand and supply of financial access. Majority of the studies on firm level are from the SSA region in the sampled articles. The studies reviewed mostly examined factors that affect women’s access to finance negatively, pointing out to the constraints. Woldie et al. (2018) studied perception of women entrepreneurs of small and medium enterprises (SMEs) in Congo on various factors posing as challenge for accessing credit and found majority of them stating lack of collateral, complicated procedures, high interest rates and unfavorable business environment impeding SMEs to secure finance from formal external sources. Women-owned firms face challenges while availing formal credit and lack of collateral is one of the constraints specific to female-owned firms as compared to the male counterparts (Singh & Dash, 2021). Thus, a supportive and enabling environment would prove useful in determining smooth facilitation of financial access for female firms in their respective countries (Ahmad & Arif, 2015). A finding on the same line is found in Nigeria showing weak financial condition and dearth of collateral as constraints in accessing finance for start-up and growth of business by women entrepreneurs (Adesua-Lincoln, 2011). In addition, the same study found socio-cultural factors like inferior status of women and gender discrimination due to tribal norms to be factors that negatively impact women’s financial inclusion. Adetiloye et al. (2020) also examined issues constraining financial access in the Nigerian MSME sector and postulated loan conditions and education as significant determinants, suggesting easier loan conditions and targeted female education in assisting the female entrepreneurs to have sustainable credit access. Naegels et al. (2017) in his survey study in Tanzanian women-owned enterprises found that women perceive financial access to be troublesome due to high collateral requirements, high interest rates, personal guarantee requirements and lack of access to financial knowledge. In a different study of female-owned informal enterprises (FOIEs) in India Maurya and Mohanty (2016) signified owner characteristics, firm characteristics and financial characteristics as determining factors for access to credit. Through probit estimation, they found factors such as firm location, firm size and age, whether the firm involves in multiple businesses and maintenance of accounting records as salient factors affecting credit access for FOIEs. Apart from access to credit as a financial inclusion measure, two studies in Kenya and India (Gichuki & Mulu-Mutuku, 2018; Keloth et al., 2020) determined factors determining access to digital financial services by females. Both of the studies found education to be significant in creating awareness about mobile applications. However, statistical evidence of awareness leading to adoption of mobile financial services has not been found (Keloth et al., 2020).

A different set of studies have analyzed if female ownership in firms determines access to credit (Aterido et al., 2013; Chaudhuri et al., 2020; Hansen & Rand, 2014; Seema et al., 2021). Interestingly, the studies provide conflicting results. While the studies like Chaudhuri et al. (2020) and Seema et al. (2021) established that ownership of firms significantly determine access to credit, and there is more denial for credit for firms that are women-owned than if they are men-owned, Aterido et al. (2013) found that applications of loans by firms are neither discouraged nor rejected based on gender of ownership. However, traces of unconditional gender gap are found in terms of usage of credit which might be attributed to demand-side factors. Similarly, Hansen and Rand (2014) found insignificant gender differences for credit use. Few other studies have also found gender to be extraneous to financial institutions in granting financial access (Adesua-Lincoln, 2011; Kairiza et al., 2017; Woldie et al., 2018).

Summarizing the findings, it is found that negative perceptions of women about supply side of financial inclusion negatively determine women’s access to formal financial sources. Thus, simplification of procedures, reduction of interest rates for loans and alternatives for collateral requirement can positively impact women’s financial access and help in promoting greater financial inclusion for them. Demand side factors like addressing gender-discriminatory, socio-cultural factors and increasing female-targeted education can have promising results in furthering financial inclusion of women. However, while examining the impact of firm ownership on financial inclusion, conflicting results are found regarding supply side factors impacting access to credit for women-owned firms.

Findings from Studies at Household/Individual Level

The studies at household or individual level consider numerous financial inclusion indicators such as account ownership, savings, borrowings and digital services unlike the studies at firm level where maximum studies had used access to credit as financial inclusion measure. Almost all of the studies use more than one indicator.

Among the selected studies at household level, majority of the studies measure the impact of gender of the household head (for household studies) or gender of an individual (for individual studies) on women’s financial inclusion, and the results are not conclusive. Two similar studies in Indian context (Ghosh & Vinod, 2017; Kaur & Kapuria, 2020) analyzed the significance of ‘gender’ of the household head for accessing finance, controlling for different household and state-level controls. Both the studies posit similar results in that female heads are likely to opt for informal finance than institutional sources, as compared to male heads. Girón et al. (2021) shared the same view in that the probability of a female possessing an official financial account is lesser than that of a male and women are likely to be dependent on informal financial sources. Doss et al. (2019) also found more men acquiring financial assets through market in contrast to women. Additionally, similar findings are found in two more cross-country studies (Chakraborty, 2014; Morsy, 2020) which conclude that being a female impact the probability of being financially included as compared to being a male. However, while the findings by Chakraborty (2014) is significant even after all country level controls, Morsy (2020) postulates that level of female exclusion depends on various bank level and country level indicators. Ghosh and Chaudhury (2019) found gender of an individual to be significant in explaining women’s financial inclusion. Bhuyan et al. (2018) found gender as an important factor in determining financial awareness which impacts the probability of being financially included.

The impact of an individual’s gender on financial access also varies with indicators defining financial inclusion. For instance, Ndoya and Tsala (2021) reported gender gap in all six financial inclusion indicators related to access and usage taken in their study when examined for Cameroon while the study in Tanzania (Mndolwa & Alhassan, 2020) found gender dummy to be negative and significant for determining formal savings, positive and significant for formal credit while insignificant for account ownership and mobile money accounts. Another study examining mobile money as a financial inclusion instrument in the context of Ghana found that males are less inclined to use mobile money when compared to females. This is contrary to the findings on traditional financial sources where being a female is negatively related to use of formal finance (Lotto, 2018). Aterido et al. (2013) found no significant conditional impact of gender on usage of financial services, when controlled for household characteristics. Kulkarni and Ghosh (2021) however found constrained financial inclusion for women in terms of mobile banking and digital literacy, income, societal barriers and lack of confidence to be the factors affecting their digital financial inclusion.

Some of the studies have also analyzed the impact of household characteristics, individual characteristics, socio-economic and socio-cultural characteristics on female financial inclusion (Adegbite & Machethe, 2020; Kemal, 2019). Patriarchal societal structures impose barriers to women’s financial access and employment in formal economy is a key determinant of increasing their inclusion in formal financial sector (Manta, 2019). Doss et al. (2020) postulated that value of physical assets and household physical wealth of a woman are determining factors of having formal savings. Another study showed that mere value of assets is not detrimental to women’s inclusion in all financial services. Possession of land can increase account ownership and savings, but women are provided formal credit only in case of joint land ownership with men (Balasubramanian et al., 2019). Additionally, out of two similar studies analyzing the socio-economic factors impacting credit demand through logistic regression, one (Fatima, 2009) found cultural background of the family to be significant in determining the probability of borrowing in Pakistan. The study further established that increase in household income or assets reduce the probability of borrowing. The other study in Indian context (Malik et al., 2020) also found household income and expenditures to be significant determinants of credit demand in addition to education and employment. Gender difference along with other socio-economic factors such as access to education, ethnicity, income and lack of trust also hinders women’s financial literacy and inclusion (Girón et al., 2021; Mishra et al., 2021).

Mindra et al. (2017) postulated that women’s self-efficacy is a significant factor for women’s financial inclusion. Literacy is one of the significant contributors towards greater financial access but women are behind men in attaining literacy which leads to the gender gap in financial inclusion in developing countries (Cicchiello et al., 2021). Sabherwal et al. (2019) also attribute low access to information and lack of financial literacy as factors constraining financial inclusion of women. Sholevar and Harris (2020) points out cultural barriers and policy measures limiting financial literacy of women and suggests financial training as a determining factor in promoting financial inclusion of women. The positive impact of financial literacy training on intensifying women’s inclusion (Koomson et al., 2020) is supported where it is found that women beneficiaries of training have a greater propensity to own an account, save and receive payments.

Forward Linkages of Women’s Financial Inclusion

Enhancing financial inclusion of women through different ways such as access to formal financial services, microfinance and digital financial services have various social and economic impacts. The studied literatures according to their research themes have been classified into groups assessing financial inclusion impacts on empowerment, macro-economic factors and entrepreneur-ship or firm performance.

Empowerment

The impact on empowerment has been majorly studied from the lens of microfinance. Only one study has examined the impact of digital finance on women empowerment through inferential statistics (Gupta & Arya, 2020). Interestingly all the studies addressing the impact of different financial services on empowerment in our sampled articles are in South Asian region. The studies are all conclusive in asserting the positive impact of financial inclusion on different empowerment measures. Microfinance outreach is powerful in enhancing women empowerment for poor households (Laha & Kuri, 2014), however the outreach is variable across regions. So, microfinance is especially important for empowering women in states with low level of financial inclusion. Bhatia and Singh (2019) found huge increment in social, political and economic empowerment of women due to the penetration of different financial inclusion schemes in urban slums of India. Datta and Sahu (2020) advocated that access to microfinance has positive significant impact on empowering women not only economically but also politically, psychologically and socially. Nagaraj and Sundaram (2017) also showed increase of women’s economic and social empowerment in terms of growing monthly savings, expenditure and decision-making power in households by acquiring microfinance. A study from Bangladesh (Murshid, 2018) established that women participants in microfinance having control over household resources have increased decision-making power. A different study (Kumari & Azam, 2019) in Sri Lanka has showed financial literacy and financial inclusion making significant impact on women’s economic empowerment.

Macro-economic Factors

The examined studies document the relationship between female financial inclusion and different macro-economic factors such as poverty, inequality and economic growth.

On examining the impact of financial programs on poverty reduction, Swamy (2014) identified gender disparity in the impact levels of financial inclusion programs. The impact leaned strongly and positively towards women in terms of change in income of poor women and contributed to significant increase in savings level of household. Two similar studies in Pakistan (Hussain et al., 2019; Mahmood et al., 2014) found positive impact of microfinance on poverty reduction of female entrepreneurs. Both of the studies have similar findings in that the reduction of poverty of women entrepreneurs depends on the size of microfinance loan. Additionally, Mahmood et al. (2014) finds that microfinance loan has no impact on family health which is validated by Hussain et al. (2019) in finding no impact of microfinance loans on human poverty.

A cross-country study showed econometric evidence of decreased gender inequality owing to the increased participation of women in microfinance (Zhang & Posso, 2017). A qualitative study in Pakistan (Zulfiqar, 2017) examining the role of microfinance in enhancing gender equity in access to finance concluded worsening of gender inequalities due to excessive commercialization in the microfinance sector. Another cross-country study (Fouejieu et al., 2020) found that improved formal financial access to women leads to significantly reduced income inequality. In a cross-country study of 91 countries, Cabeza-García et al. (2019) advocated for increasing women’s financial inclusion owing to its positive impact on economic development. Subrahmanyam and Santosh (2019) in a qualitative study in India also advocated for the positive effects of women’s participation in microfinance (through self-help groups) on rural development through self-employment and increase in income, increased standard of living and poverty alleviation.

Entrepreneurship or Firm Performance

A few of the studies have considered examining the impact of increased financial inclusion on entrepreneurship or firm performance. Goel and Madan (2019) found financial inclusion positively and significantly impacting women entrepreneurship. However, inadequate education and lesser usage of banking facilities impede their knowledge and awareness of the different schemes. Credit constrains of the female-owned firms have negative impacts on their firm performance in terms of labor productivity (Nwosu & Orji, 2017) pressing the need for increasing access to credit. Brixiová et al. (2020) found lesser financial access to be one of the prime constraints for female entrepreneurs in Africa. Increasing formal credits prove to be useful—especially for smaller-sized women-owned firms—in increasing firms’ performance.

Most of the existing literatures assess the impact of women’s financial inclusion on different factors from the lens of microfinance. Overall, the findings from different studies favor the enhancement of women’s financial inclusion for its positive impacts on women’s empowerment. The importance of gender justice in microfinance, equitable access and appropriate design of financial products (Mayoux, 2010) in empowering women cannot be denied. Microfinance is a good channel for financial inclusion as it has better outreach into remote areas. In fact, evidence shows higher proportion of female clients associated with greater repayment rate (Ogunleye, 2017) which is consistent with an earlier study by (Aggarwal et al., 2015) showing countries with lower social trust targeting higher proportion of women borrowers.

Discussion

Anatomy of the Studies by Subjects

Looking at the findings from the structured literature review, it is found that the studies focusing on backward linkages of women’s financial inclusion have firm-side studies as well as household-side studies. In case of firm side studies, the majority of the studies focus on financial inclusion as access to credit/loans. The firm side studies are mostly from Sub-Saharan region using both primary and secondary sources of data. Four studies are from South Asian region (India) and one cross country, focusing on credit as financial inclusion measure. Only one study in Indian context is on digital financial services but results are indicated using inferential statistics. Overall, almost all of the studies use logit or probit models for analysis. The household/individual side study has a different anatomy. There are nine studies in SSA context, 12 in South Asian context and seven cross-country studies. Excepting four studies which are theoretical, all the others have used econometric methods such as logit, probit or tobit models, structural equation modelling (SEM) and principal component analysis (PCA). The studies on household side majorly have used secondary data sources (mostly using Global Findex database of the World Bank). Figures 8 and 9 have displayed the anatomy of the studies on the firm and household side for backward linkages of women’s financial inclusion. The figures in the brackets indicate the number of studies.

Next on analyzing the studies on forward linkages, we find impacts of women’s financial inclusion with three components: women empowerment, macro-economic factors and entrepreneurship and firm performance. There are no studies in SSA in our sampled articles assessing the relationship of financial access with women empowerment or macro-economic factors. Three studies are found in SSA which determines whether access to finance to women firms would have an impact on firm’s performance. The flow chart depicting the anatomy of forward linkage is shown in Figure 10 for view at a glance. As evident from the flow chart, majority of the studies have focused on microfinance impact on empowerment or macro-economic factors and majority based on primary data. However, impacts on entrepreneurship and firm performance are mostly based on secondary data sources. The studies on forward linkages of women’s financial inclusion have majorly used econometric tools (mostly OLS or logistic regression) for their data analysis.

Future Research Directions

Assessing the anatomy of the existing literature findings by subjects, important insights about research gaps in the current academic literature have been observed. The important factors which influence financial inclusion of women positively also reflect different supply side or demand side constraints of women’s financial access. While constraints pertaining to socio-economic or cultural factors are established by studies at both sides, the impact of gender gives conflicting results. The existing literature has focused more on the household-side studies and portrayed similar results regarding gender gap in financial inclusion.

The firm side studies however have posited conflicting results. The firm-side studies mostly establish no supply side gender discrimination but few of the studies show women to be at a disadvantageous position while approaching for loans owing to their gender. Thus, future studies may focus more on the firm-side and analyze the differences in supply side and demand side constraints of women’s financial inclusion owing to gender differences. This requires combined interactive demand and supply side studies, to determine what is more prominent in explaining women’s financial inclusion.

Moreover, while much have been done to assess microfinance impacts on different factors, many research areas on the impacts of fin-tech or digital financial services are at a nascent stage or not investigated yet. More researches are possible analyzing the impacts of different fin-tech projects on population cohorts and the potential of digital financial inclusion in reduction of gender gap in financial inclusion. More study is also required in the areas of financial literacy, financial awareness and financial self-efficacy which play a crucial role in the enhancement of financial inclusion for women.

Additionally, the extant academic literature has econometric evidence on the subjects discussed in previous sections but not much has been done on causation. Many studies state this as their limitations. The current research landscape has established well that gender of firms’ ownership, household head or individual (in case of firms) impacts women’s financial inclusion but not much has been done to establish whether ‘gender’ is a cause for women’s constraint to financial services. While relationship between variables is important, understanding causality is necessary to clearly understand gender-gap in financial inclusion. An increase in the overall level of financial inclusion does not indicate closure of gender gaps. Clearly, the institutional set-ups and regulatory policies influence the level of financial inclusion differently across economies and across different regions in an economy. Various cross-country studies have validated the significance of country-level controls in explaining women’s financial inclusion. But for better addressing the issues of gender gap, regional studies within countries is more important necessitating micro-level primary surveys and understanding the real scenario. In the extant research, issues pertaining to women’s financial inclusion have been discussed and empirically established through regression models, but empirical demonstrations of actual benefits of different policy measures is lacking. Future academic researches might consider assessing about the actual impacts of different financial inclusion projects and schemes at micro levels through primary surveys to understand the gap between theory and practice. This might help in addressing the gender gap in financial inclusion better.

Summing up, as per analysis from the extant academic literature, the identified topics having future scope of study lie in the areas of digital finance, financial literacy, awareness and self-efficacy. Moreover, regional-based studies are important for target-based policy initiatives.

Conclusion

Gender inequality is not a new issue. Promoting women’s financial inclusion has positive repercussions on women empowerment and bridging gender gap in financial inclusion. This review has provided insights on what factors can affect women’s financial inclusion and what impacts women’s financial inclusion have on different factors. Socio-economic and cultural constraints are most common barriers found in many of the researches. Findings also reveal the existence of gender gap in women’s access to finance. However, it is not conclusive whether gendered differences are supply-sided or demand-sided. This review brings together different study fragments related to financial inclusion of women and presents a comprehensive framework of study findings by grouping them into backward and forward linkages. The importance of enhanced financial access to women cannot be denied and recognizing the role of target-based approaches for faster gender-inclusion is of importance to policymakers. Moreover, various challenges such as lack of education, financial literacy and constrained financial opportunities for entrepreneurship needs to be addressed through SDG5 to encourage women’s financial inclusion and reduction of gender inequalities.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.