Abstract

Global private equity (PE) investments continue to increase at unprecedented levels over the last two decades, as investors are increasingly thriving over the potential of funded firms. The purpose of this study is to provide an understanding of determining factors that guide the flow of private equity investment in target firms. The existing academic research concerning selection determinants of private equity investment is restrictive and unstructured. These determinants are diverse and observe inconclusive results in extant literature. To identify the firm-level determinants of private equity investment, understand the current gaps in the literature and direct the future scope of work, the authors conduct a systematic literature review of empirical private equity investment studies. The results pointed out the open issues in private equity literature focusing on drivers of investment decisions and extracted the most frequently observed selection determinants of private equity investments along with their causal relationship. The review also acknowledges that there exists a coherence among private equity and M&A investment decisions and thus, expands the scope of research by including empirical studies on M&A determinants. The study creates a comprehensive database and identifies shortcomings in the relevant literature addressing private equity.

Introduction

For decades, private equity firms have provided operational and strategic guidance to their portfolio companies along with the financial capital they require. The private equity market is imperative in financing start-up firms, private firms, public firms’ buyouts and firms with financial constraints. Private equity has gradually developed as a source of corporate finance and become the fastest-growing market over public equity and bond markets (Nary & Kaul, 2021; Stulz, 2020). Private equity funds/firms raise funds from high-net-worth individuals and institutional investors and invest them in both public and private companies (Boone et al., 2019). It makes professionally managed equity investments in the unregistered securities of private and public companies (Fenn et al., 1997).

A large proportion of research circling private equity examines the effect of private equity investments on the growth, performance and successful exits of PE-backed firms. Acharya et al. (2009) examined private equity portfolio companies that generate higher un-levered returns and improve profitability above their matched peers. The deals show high operational stability during PE ownership since they have statistically significantly lower volatility than their sectors and similar peers. Chemmanur et al. (2011) suggest that the overall efficiency of VC-backed firms is higher than that of non-VC-backed firms due to the screening and monitoring ability of private equity investors. Peneder (2010) finds that the average annual growth of firms with venture capital financing is significantly higher than other firms in terms of sales revenue and employment. Bernstein et al. (2019) also show that PE-backed companies experience higher growth in their assets along with a greater flow of investment in the post-crisis years.

Another section of research acknowledges how private equity investors possess selection superiority and the post-investment performance may have selection bias resulting in higher performance for PE-backed firms in comparison to non-PE-backed firms (Baum & Silverman, 2004; Bertoni et al., 2016, 2019; De Bettignies & Brander, 2007). Peneder (2010) studies the selection and value-adding impact that venture capital financing has on the innovation and growth of firms showing significant difference in innovation output and annual growth in VC-financed companies is due to VC selection effects. Baum and Silverman (2004) also determine whether the success of investee firms is a result of the positive sorting effect or treatment effect and gives a joint logic combining the VC roles of picking winners and building winners for the superior performance of VC-backed companies. This empirical research stream focuses on the positive sorting effect, which is both economically relevant and statistically significant in the US.

Croce et al. (2013) examine whether the outperformance of VC-backed firms is a consequence of screening or value addition by VC investors, and find an increase in productivity growth only after the VC round providing evidence for the value addition effect and excluding the screening effect. Colombo and Grilli (2010) also studies the scout and coach function of VC investors for new technology-based Italian firms finding support for the coach function, while no support was documented for the scout function as the main task performed by VC investors. More specifically in Europe, the VC markets are relatively thinner due to a scarce supply of VC financing resulting in young high-tech firms self-selecting out of the VC market, with no positive signs of sorting mechanism by VCs (Bertoni et al., 2011; Colombo & Grilli, 2010; Croce et al., 2013).

The empirical literature reflects the significance of positive selection effect in the US markets (Chemmanur et al., 2011; Sørensen, 2007), as experienced PE/VC investors equip them with the expertise to select better targets. Conversely, this positive selection effect is not as widely present in European markets (Bertoni et al., 2016), as the investee companies may face high opportunity costs for seeking investors due to the thinness of VC markets.

Considering the selection and monitoring effects of private equity firms on the portfolio firms’ performance, the selection characteristics of target firms influencing the investment decision of private equity funds become imperative. Most existing studies in this regard focus on value creation drivers in private equity investments by studying the factors contributing towards a higher shareholder value. Such factors that exhibit the superior performance of portfolio firms may work well as selection determinants for private equity investments. The extant literature has not identified and summarized the target firm characteristics that increases their propensity to gain private equity investment.

A Review of literature in the past has studied private equity from diverse perspectives of performance, returns, and ownership (Gohil & Vyas, 2016; Köhn, 2018; Schickinger et al., 2018). While systematic reviews studied VC internationalization (Devigne et al., 2018) and family firm–private equity partnership (Schickinger et al., 2018). There is no systematic review on selection determinants of private equity investment, focusing on the significance of determinants for the presence and performance of private equity. This study aims at mapping various firm-specific determinants that are responsible for private equity financing in target firms. Furthermore, the study also observes the determinants of M&A investment decisions, regarded as closely related to PE investment decisions. The authors create a comprehensive database of explanatory variables concerning determinants of private equity investments from the existing empirical research and identify M&A as a related field of research, providing scope for future private equity studies.

Methodology

This qualitative research aims to review the contributions of quality peer-reviewed publications on private equity investment and its determinants. A systematic literature review synthesizes the existing literature and offers a comprehensive and structured view of the relevant empirical evidence. The majority of private equity studies show a dominant focus on the performance of portfolio firms. There are, however, themes other than performance such as value drivers, determinants and sources of value creation in private equity, which require academic attention in a manner, that is systematic and structured. A structured approach has the potential to comprehensively identify and assess the determinants of private equity investment from extant literature and form grounds for future research. A systematic literature review is therefore recognized as an appropriate method to study private equity determinants.

To conduct systematic research, certain features of the PRISMA Statement (Moher et al., 2009) have been adopted. The authors developed the following methodological approach:

Identify the need and strategy for the review, and design the review protocol. Select the studies, assess the quality, extract data and synthesize the data. Report the results of the review.

Identifying Studies

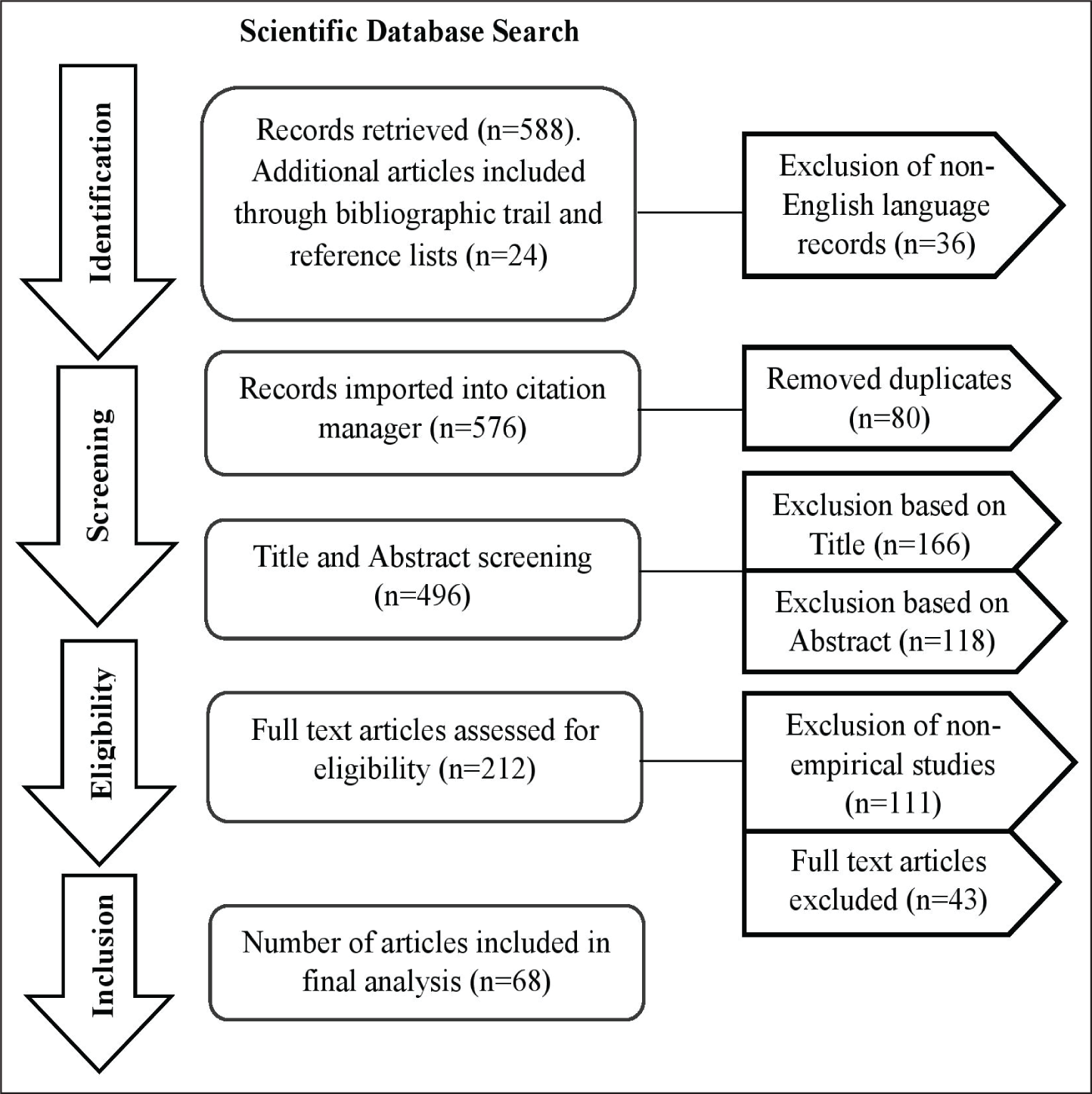

A systematic literature search was undertaken in February 2021 without restrictions on the timeframe, the results were subsequently updated in August 2021. This search was tailored from the Scopus database, using the following keywords: ‘private equity’, ‘private equity determinants’, ‘private equity investment’, ‘M&A drivers’ and ‘M&A performance’. Additional searches using the snowball effect (i.e. referenced works of relevant articles) were also included. The search focused on mapping the existing literature on the determinants of private equity investment in the field of financial studies, business economics and business strategy. We then narrowed the search area to business venturing, alternative investments and corporate investment. The research contemplated articles from 1985 to 2021, covering 36 years. A flowchart of the search strategy is presented in Figure 1. Where the abstract of a particular study was not available, the full article was retrieved and evaluated for relevance. Further, all relevant articles were retrieved in full text.

Screening and Study Selection

The admissibility of the retrieved articles was examined independently by the authors based on predefined exclusion and inclusion criteria. The initial search scanned from database inception until 2021 without the restriction of the study period, and included journal articles, research reports, review papers; and identified 612 papers published in a different area of private equity and M&A studies.

In the next stage, all the duplications were filtered thoroughly. The titles and abstracts of these records were studied for the analysis and segregation of articles to ensure the relevance of literature included in the review. In this process, studies addressing performance measures, value creation, value drivers, selection determinants and the private equity investors’ motivation were included. A considerable number of studies are drawn towards the growth, governance and economics of the private equity market. Such records were excluded from the final sample if found irrelevant concerning the research objective. From these, studies that have carried out empirical work were shortlisted, and 68 articles were considered for the final assessment in this study (Figure 1).

A synthesis is prepared from the 68 selected articles and organized according to the following categories: explanatory variable, dependent variable (with causal direction), study period, sample size and region. This synthesizer identifies the frequently observed variables as well as their impact and relationship with the research subject, thus creating a comprehensive compilation of the findings of the selected empirical studies.

Determinants for Private Equity Investments

Literature focusing on determinants of PE investments is a mix of macro-level and firm-level determinants. The macroeconomic determinants are the external variants influencing the private equity investment activity such as GDP growth, industry growth, legal environment, inflation and unemployment. These determinants largely depend on factors neither in control of private equity firms nor the investee companies and vary distinctively from one country to another. Conversely, the firm-specific determinants are not external to the operations of private equity firms and their investee companies. These are characteristics that a target company must possess to get acquired by a private equity investor. This article predominantly focuses on the firm-specific determinants of private equity investment.

Value Creation Drivers

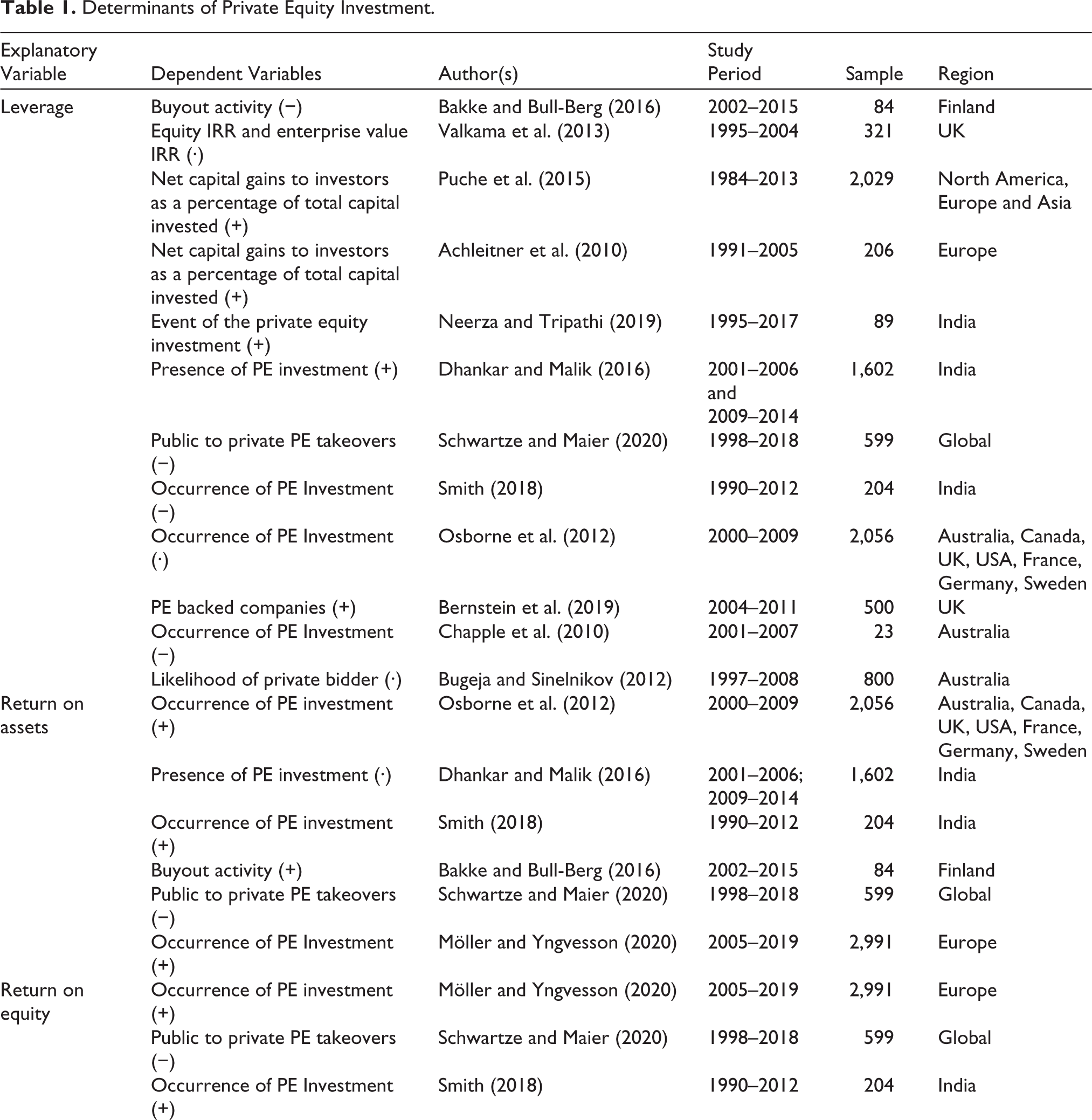

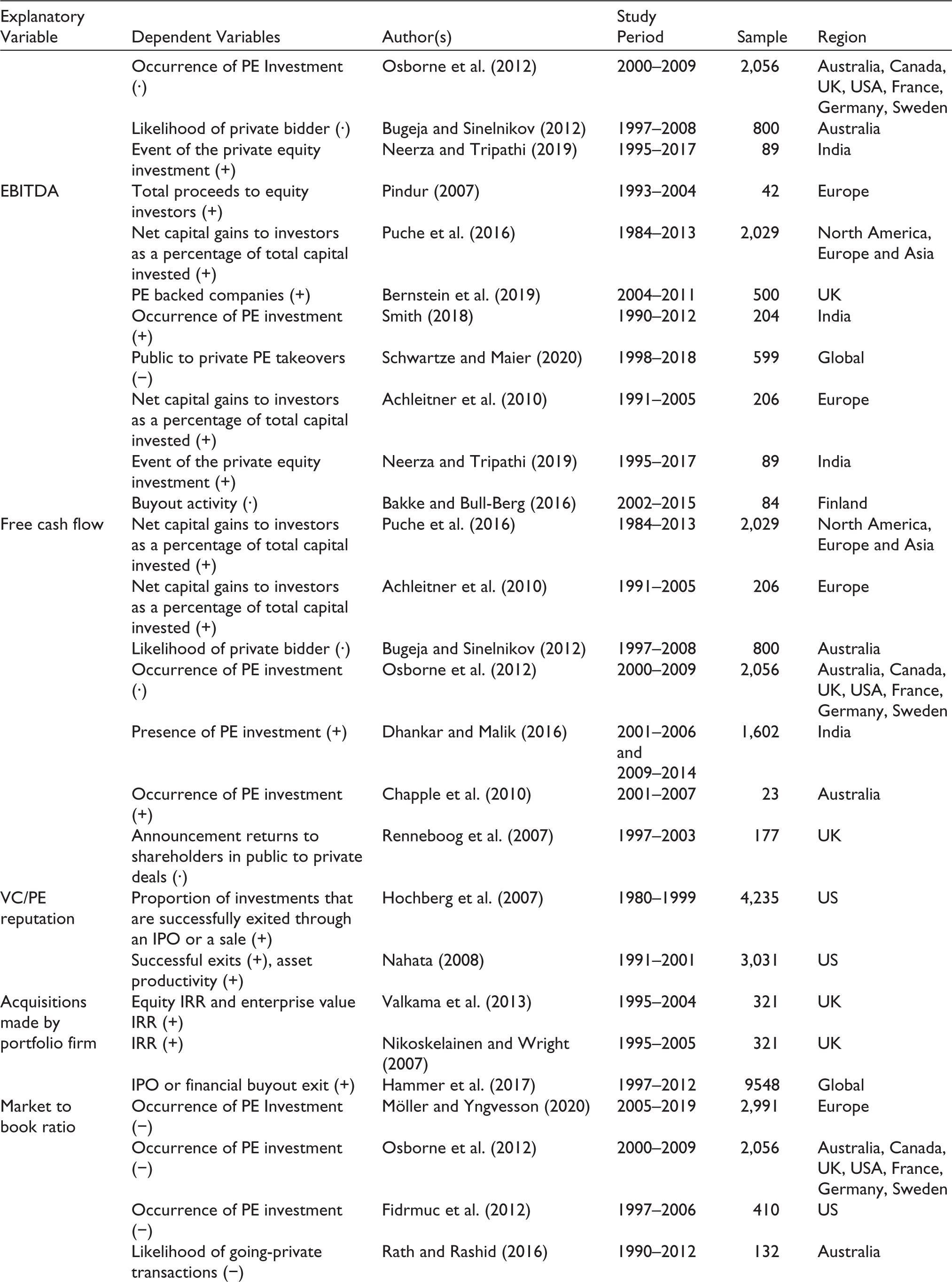

Most existing literature addresses the closely related question of value drivers—the driving factors that create value for PE investee firms. These value drivers can also be characterized as important selection determinants for PE investors, as their ultimate aim remains value creation through the selected investee firms. Pindur (2007) concludes the growth of earnings before interest, tax, depreciation and amortization (EBITDA) as the main driver of value for PE investments over the life of the investment, this suggests that a low EBITDA might be considered as a selection determinant. Loos (2007) shows that deleveraging and multiple effects contribute to over 80% of the internal rate of return generated. Haarmeyer (2008) observes operational performance, leverage increase and interest coverage as the main contributors to the success of private equity funds, implying that companies with relatively low ratios can be suitable targets for PE firms.

Achleitner et al. (2010) analyse the value creation drivers for PE buyouts in Europe and the UK by attributing them to operational, market and leverage effects. They associated two-thirds of value creation with operational and market effects, and the rest with the leverage effects. Similarly, Puche et al. (2015) distribute the total value created as a percentage of total capital invested in components, such as financial risk, increases in operating cash flow, growth in the transaction multiple and free cash flow (FCF) effect. Valkama et al. (2013) studies the drivers of holding period firm-level returns for PE buyouts and concluded that returns are driven by leverage, industry growth, size of the buyout and acquisitions made by the portfolio company during the holding period. Bakke and Bull-Berg (2016) examine the drivers of value creation post-PE buyout to their benchmark group across four dimensions-operating performance, insolvency risk, employment and total factor productivity (TFP).

PE Investment Drivers

Acharya et al. (2009) identify the selection pattern for PE targets, documenting stable operating performance and nonlinear profitability (EBITDA margin) in companies acquired by PE firms. Several studies conduct relative studies for determining firm-specific factors in selecting PE targets and corporate targets (Chapple et al., 2010; Osborne et al., 2012; Rath & Rashid, 2016). Chapple et al. (2010) emphasize that private equity targets possess greater financial slack and financial stability along with higher free cash flow, and a lower growth potential relative to corporate targets; Osborne et al. (2012) examine higher market-to-book ratio, greater abnormal operating income, firm size and lower stock volatility as significant internal drivers for attracting PE investment relative to tender/merger targets. Moreover, they iterate the importance of firm-specific factors in selecting targets over country-specific factors. While Rath and Rashid (2016) analyse PE targets against public mergers and find market undervaluation as a dominant factor in private equity takeovers.

Some studies have focused on the firm characteristics preferred by different set of buyers at the time of private equity investment. Fidrmuc et al. (2012) undertake a relative study on targets acquired by private equity vs strategic buyers and conclude that PE funds aim for targets with lower market-to-book ratios, more tangible assets and lower R&D expenses than targets pursued by strategic buyers. While Bugeja and Sinelnikov (2012) study the bidding firm listing status, that is, public vs private buyers against the preferred characteristics of target firms. They claim that private equity targets have a less independent board, are more undervalued, are relatively smaller, have higher management ownership, lower cash flows and lower growth than targets of public bidders. Möller and Yngvesson (2020) compare the target firm characteristics between financial and strategic buyers for the public to private transactions in Europe and finds that PE targets display high profitability (measured as returns on assets and equity), and low price-to-book ratios in comparison to their strategic competitors.

Few recent studies have observed the role of target characteristics in the likelihood of PE acquisition or deal performance. Schwartze and Maier (2020) identify the determinants for selecting public companies to become PE takeover targets by grouping investors into different levels of risk aversion. It has been emphasized that PE investors with long-term orientation are drawn to strong growth potential and a high asset base, while risk-seeking PE investors focus on return on equity and return on assets, and a high trading turnover. Wilson et al. (2022) study the determining characteristics of PE targets that affect the probability of PE acquisition and identify that targets with cash generation, profitability and high-interest coverage ratio on existing debt are likely to get acquired by PE funds. They also find that established companies in terms of age and size, and a higher proportion of tangible assets are the potential targets of PE funds. Burth and Reißig-Thust (2019) focused on the importance of pre-acquisition determinants for deal performance, where they find that asset lightness and management experience increase the likelihood of earning higher returns. Whereas Block et al. (2019) dealt with PE investment criteria for different types of PE investors, that is, venture capitalists, business angels and family offices and found revenue growth, value-added of product or service, management team’s track record and profitability as important criteria. Family offices, growth-equity funds and leveraged buyout funds value profitability, while venture capital funds give higher preference to revenue growth, business models and company investors.

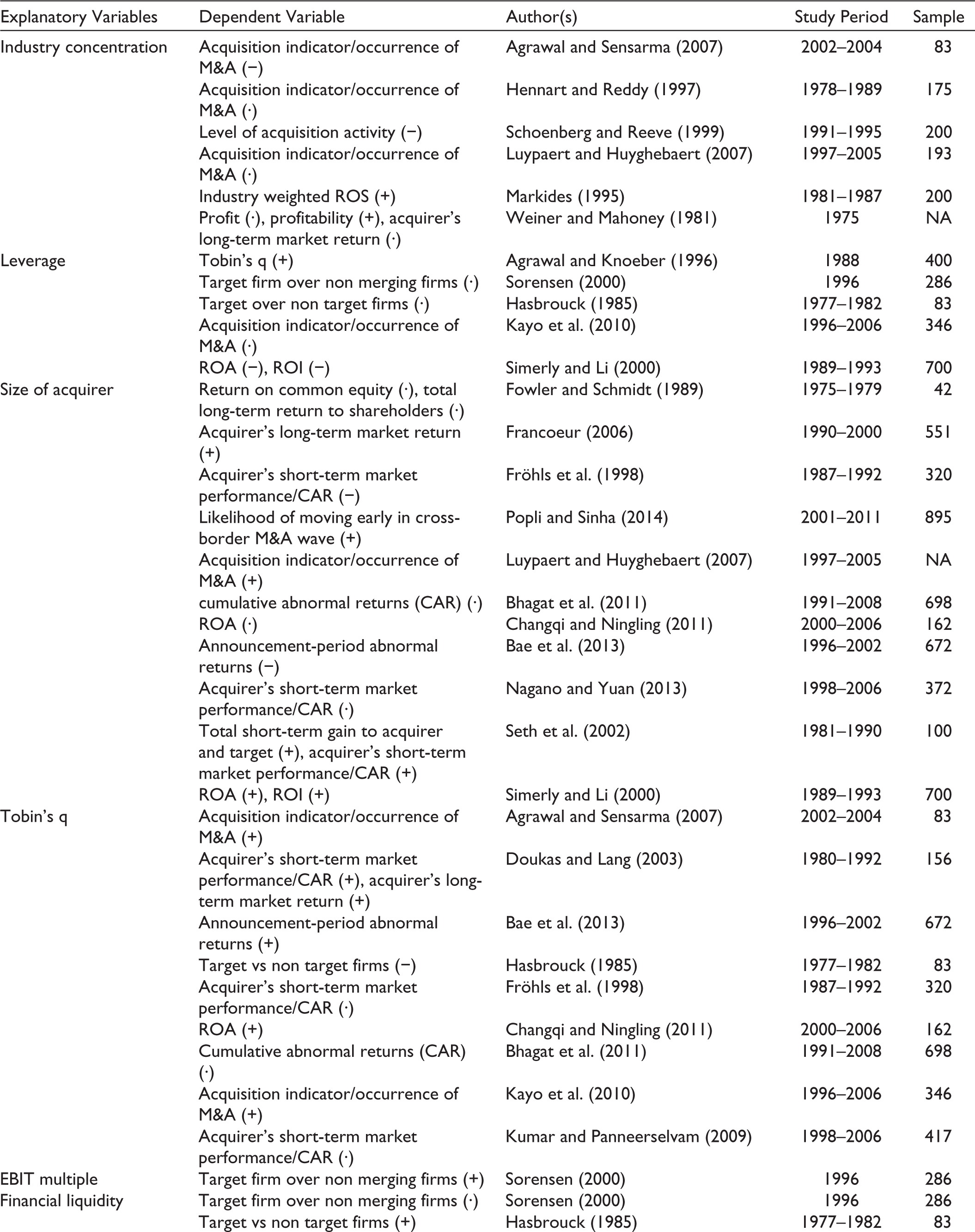

This section analyzes the explanatory variables influencing the private equity investment used in different studies and summarize the firm-level variables along with their study period, the target firm’s geographic region and sample size. It also documents the causal direction of explanatory variables identified in the selected studies. Table 1 provides details of the explanatory variables that are frequently studied across the literature along with their respective dependent variables and causal direction as found in studies.

Determinants of Private Equity Investment.

Mergers and Acquisitions Drivers

Mergers and acquisitions are the key strategic decisions, undertaken with critical due diligence, as in case of private equity investment decisions. The literature on M&A has extensively focused on factors driving M&A activity and M&A performance (Agrawal & Sensarma, 2007; Das & Kapil, 2012; Kayo et al., 2010; Popli & Sinha, 2014; Sorensen, 2000). Though strategic approach and synergies differ, both private equity investments and M&A focus on selecting targets that facilitate successful transfer of ownership and resources, suggesting a coherence in the determinants of private equity and M&A investments decisions.

The characteristics that drive merger and acquisition activity emphasize both, target and acquirer characteristics (Bhagat et al., 2011; Kayo et al., 2010; Sorensen, 2000). The focus has also been made on the determinants that create value or improve the acquirer’s performance post acquisition (Changqi & Ningling, 2010; Hummel & Amiryany, 2015; Kumar & Panneerselvam, 2009). Some studies observe the drivers that affects the acquirer’s choice between public and private targets (Bae et al., 2013; Capron & Shen, 2007), while others examine the cross-border merger waves (Popli & Sinha, 2014). The variables explaining the performance of M&A deals and the variables used for defining characteristics of targets and acquirers, serve as determinants to merger and acquisition activity or indicate the likelihood of M&A occurrence. Table 2 consolidates the determinants (explanatory variables) that influence the M&A activity or performance. This exercise will further contribute towards building literature on determinants of private equity investment considering the congruity among the two investment decisions.

Determinants of M&A Activity and Performance.

Open Issues and Discussion

The extant literature covers the topic selectively and remains away from the entirety of the subject. As the influx of private equity investments come through domestic as well as international means, most studies focus on country-level factors influencing private equity investment (Bernoth & Colavecchio, 2010; Kelly, 2012; Ndlwana & Botha, 2018; Oberli, 2014). This implies that researchers focus predominantly on macro-level factors for screening private equity investment targets. The strategic decision however also requires closely scrutinizing the firm-level factors, and past literature has sparsely studied the relationship between firm characteristics and the presence of private equity investment. Future studies can thus explore whether firm-level determinants affect the propensity of private equity firms to invest.

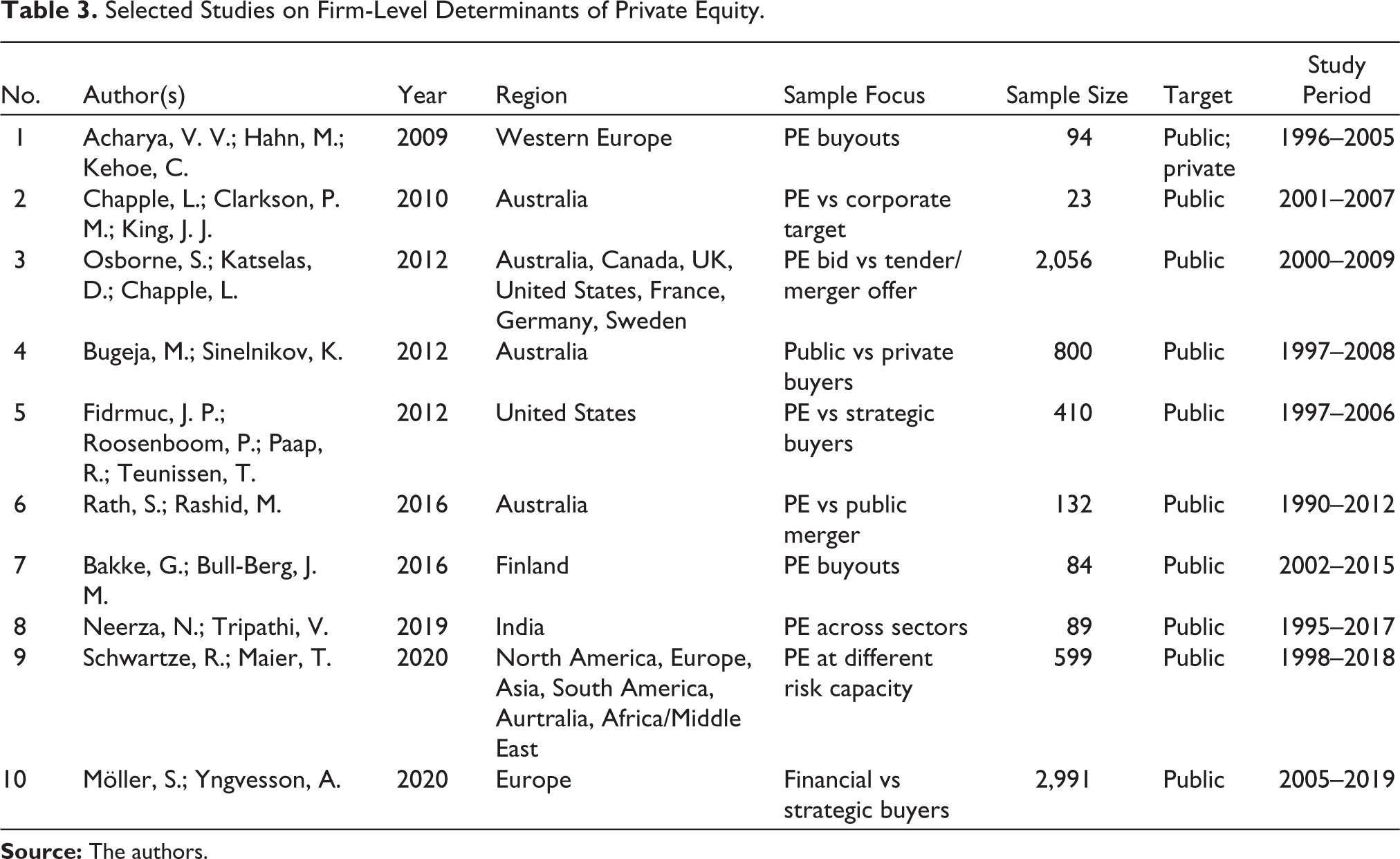

The authors observe that majority of research on private equity investments is based in developed countries (Chapple et al., 2010; Möller & Yngvesson, 2020; Rath & Rashid, 2016) as these countries attracted private equity early on and gained researchers’ attention on growth, performance and successful exits of private equity; while in emerging countries the investment in private equity has recently gained momentum and there is only modest research yet (Table 3). The limited view on private equity can also be attributed to the lack of comprehensively recorded data on private equity transactions in emerging countries (De Lima Ribeiro & Gledson de Carvalho, 2008; Neerza & Tripathi, 2019). However, as structured data sources are emerging, future studies possess the potential to cover private equity transactions in emerging countries. Given the differences in institutional setting and capital market development such studies may be able to determine unique target characteristics, different from those identified in developed countries. This further enables the researchers to draw a contrast between the private equity activity of developed and emerging countries.

The observed studies contain limitations in terms of private equity deal coverage as the studies have not considered all kinds of private equity deals, such as venture capital deals, PIPE, acquisition buyouts, early-stage expansion, later stage expansion (Acharya et al., 2009; Bakke & Bull-Berg, 2016). These studies focus on certain kinds of private equity henceforth, providing a restricted view of the private equity industry. Another noteworthy limitation stands in selecting the target firm sample, which is observably concentrated among public target firms, while the majority of private equity investments are made in private firms. The selected studies (except Acharya et al., 2009) consider publicly listed target firms in their research, leaving aside the carve-out deals, where only part of a company is acquired, and deals where a non-listed business is acquired (Table 3). For such deals, the size is relatively smaller and profitability varies from the widely studied public to private deals. Future studies can capture the effect that all kinds of deals have on the likelihood of receiving private equity investment. Given the proportion of private firms in a private equity portfolio, taking a sample of all the target firms into account (i.e. both public and private firms), will have a higher chance of producing true results in future research.

Selected Studies on Firm-Level Determinants of Private Equity.

Further, most private equity studies have performed a relative analysis with specific objectives of studying the likelihood of investment in private equity targets against merger/corporate targets. The literature also performs relative comparison among different kinds of buyers, thereafter analyzing their investment choices. The decisions made by a public buyer are different from a private buyer (Bugeja & Sinelnikov, 2012); that of a financial buyer from a strategic buyer (Möller & Yngvesson, 2020); and buyers with different risk capacities choose differently (Schwartze & Maier, 2020).

The studies under review are observed to be conducted either for a pre-acquisition period or a post-acquisition period. The post-acquisition studies observe the performance of private equity-backed firms while the pre-acquisition studies focus on the target selection pattern of private equity. The authors examine that most studies are inclined towards post-acquisition period, assessing the performance of private equity-owned firms during the PE ownership phase. This leaves scope for future PE studies to consider both pre-acquisition as well as post-acquisition phase in their assessment and provide a comprehensive view of the selection and performance of private equity deals.

The authors collate the explanatory variables that determine either the presence or performance of private equity deals and find that leverage and EBITDA have been studied most frequently among the existing studies. The study also emphasizes on the causal direction of the explanatory variables and notice inconclusive significance for most of the considered variables. Further, an analysis of dependent variables (PE occurrence and performance measures) suggests cumulative announcement return, internal rate of return (IRR), net capital gains to the acquirer and a binary variable indicating presence of private equity investment, as the most frequently studied variables. These findings provide a basis for future studies on private equity determinants to confirm the past results and build further on the causal relationship between firm-level determinants and private equity investment.

Though the choice of control variables is not included in this study, it is observed to be diverse across the studies. A lack of appropriate control variables may result in potential confounding effects. Most studies in our analysis have created a matched sample based on control variables to effectively compare the target sample with their matched peers. These matched peers range from 1 to 10 against one target sample.

Finally, the study focuses on the premise that determinants of M&A investment have a close coherence with determinants of private equity investment and therefore contribute towards identifying explanatory variables in this field. This kind of association between M&A and private equity gives rise to the question of whether determinants of M&A investment can work as determinants of private equity investment. In this study, the authors articulate that majority of explanatory variables for M&A occurrence and performance match those identified in private equity transactions, though their causal direction varies (Tables 1 and 2). This indicates that determinants for private equity investment can be borrowed from M&A literature and studied from the private equity perspective in future studies.

Limitations

The selection of relevant studies has been done in a transparent and reproducible manner, inclusion of other databases may affect the selection of studies for the systematic review. The keyword combination constructed for the preliminary search may have excluded some relevant studies from the selected collection of articles. Though the researchers ensured the inclusion of relevant studies through screening of referenced work, there remains a possibility for the non-inclusion of some relevant studies.

Further, the risk of subjectivity bias lies in the prejudiced judgment of the researchers where the gaze of each researcher could be different. To avoid subjectivity bias, the selection of studies is conducted rigorously with the help of independent researchers. However, the authors’ viewpoint on studying the firm-level determinants of private equity may hold certain biases.

This study is limited to published academic studies, which is biased towards publicly listed companies and published financial data—due to its reliability and ease of availability. Consequently, this review is also biased towards public companies’ results. It is possible that important aspects of private equity investment criteria have not yet been covered by academic research.

Concluding Remarks

Global private equity investments have been increasing at an unparalleled pace over the last decade, drawing much attention from researchers and practitioners. There has been academic evidence on the growth and prominence of the private equity industry (Jovanovic et al., 2020; Lerner et al., 2016), indicating the potential it has for stimulating innovative business models and entrepreneurial spirit. Past research has explored this potential through the lens of finance, strategy and organizational development, where the findings are sparse and lack integration.

A wide stream of literature has been concentrated towards the performance of PE investments and their successful exit providing an assessment post-investment, while there is limited research on selection determinants that guides the flow of investment into portfolio firms and studies portfolio firms’ characteristics prior to the investment deal. It is imperative to understand the selection patterns of PE acquirers, as it will eventually facilitate positive post-acquisition performance of PE-backed firms. This study underlines the relevant work from extant literature which focuses on selection determinants of private equity investments, drawing special attention towards firm-level determinants. The authors analyzed existing gaps in selected empirical studies to explanatory and dependent variables and revealed significant differences and limitations across the observed studies. Additionally, the authors capture the coherence between M&A and private equity determinants, signalling a possible correlation among them.

The performance of portfolio firms during the holding period and value creation post-investment largely depends on the selection determinants considered by private equity investors. This emphasizes the relevance of private equity determinants, while simultaneously taking cues from M&A literature.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.