Abstract

This article aims to scrutinize the antecedents and outcomes of accounting information quality (AIQ) of small- and medium-sized enterprises (SMEs) in the developing country of Vietnam. Based on the perspectives of agency theory and contingency theory, accounting information system quality (AISQ) has been considered as the main antecedent factor, and firm performance (FIP) is examined as the outcome in this article. We additionally examine the mediating role of AISQ in the context of information technology risks (ITR)–AIQ nexus. Furthermore, the moderating role of transformational leadership (TL) was considered in the context of the AISQ–AIQ nexus, and the AIQ–FIP nexus, respectively. Using the quantitative research methods with rigorous testing to determine the most accurate results and ensure reliability, this article concludes that the ITR have an appreciable influence on AISQ, and the AISQ has an appreciable favourable impact on AIQ. Additionally, the AIQ has an appreciable impact on FIP in the context of Vietnamese SMEs, and at the same time, AIQ positively mediates the AISQ–FIP nexus. Lastly, TL positively moderates the AIQ–FIP nexus.

Keywords

Introduction

Accounting data has been reviewed as one of the advantageous tools to assist internal and external users in creating applicable decisions (Abu Afifa & Saleh, 2021, 2022). Thereby, the quality of data disclosed in the financial statements of firms has become exceedingly important and it influences the decision-making efficiency of data utilizers (Nogueira & Jorge, 2017). Regarding the increasingly principal role of small and medium-sized enterprises (SMEs) in the economy, the quality of information on the financial statements of SMEs is becoming increasingly interesting for users. This is because this is the key source of information to help users make economic decisions related to SMEs, such as loans and business cooperation (Perera & Chand, 2015). Stemming from the role and importance of information, research on the quality of financial statement data has been the content that receives the attention of researchers in the field of accounting, as well as firms and professional associations in accounting (Abu Afifa & Saleh, 2021, 2022). However, most previous investigations seem to pay attention to large firms and ignore SMEs (Carraher & Van Auken, 2013). Meanwhile, for SMEs that are not required to audit by regulations, the process of equipping and presenting financial statements at these enterprises still contains many errors left undetected, leading to a decrease in the quality of data within the financial statements.

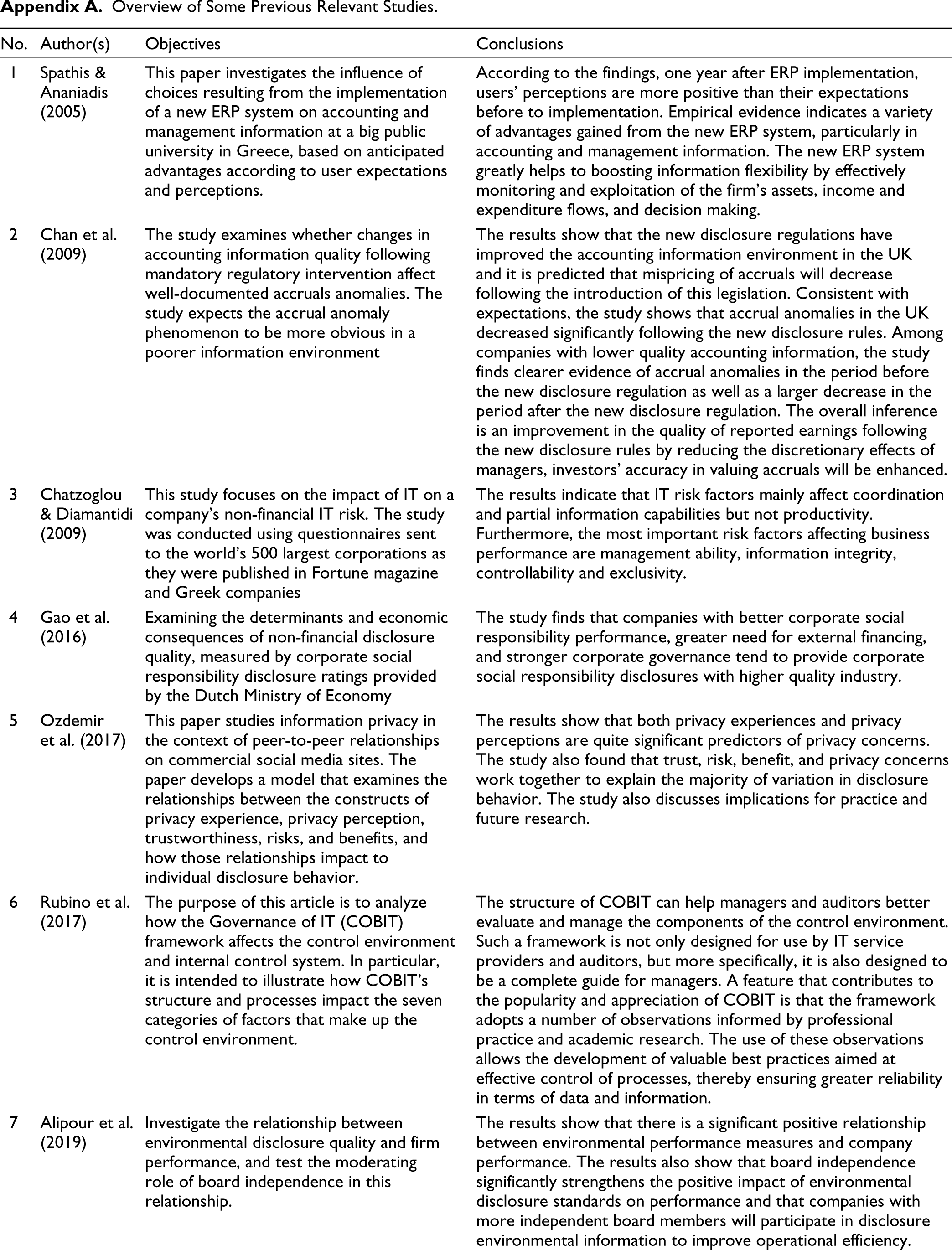

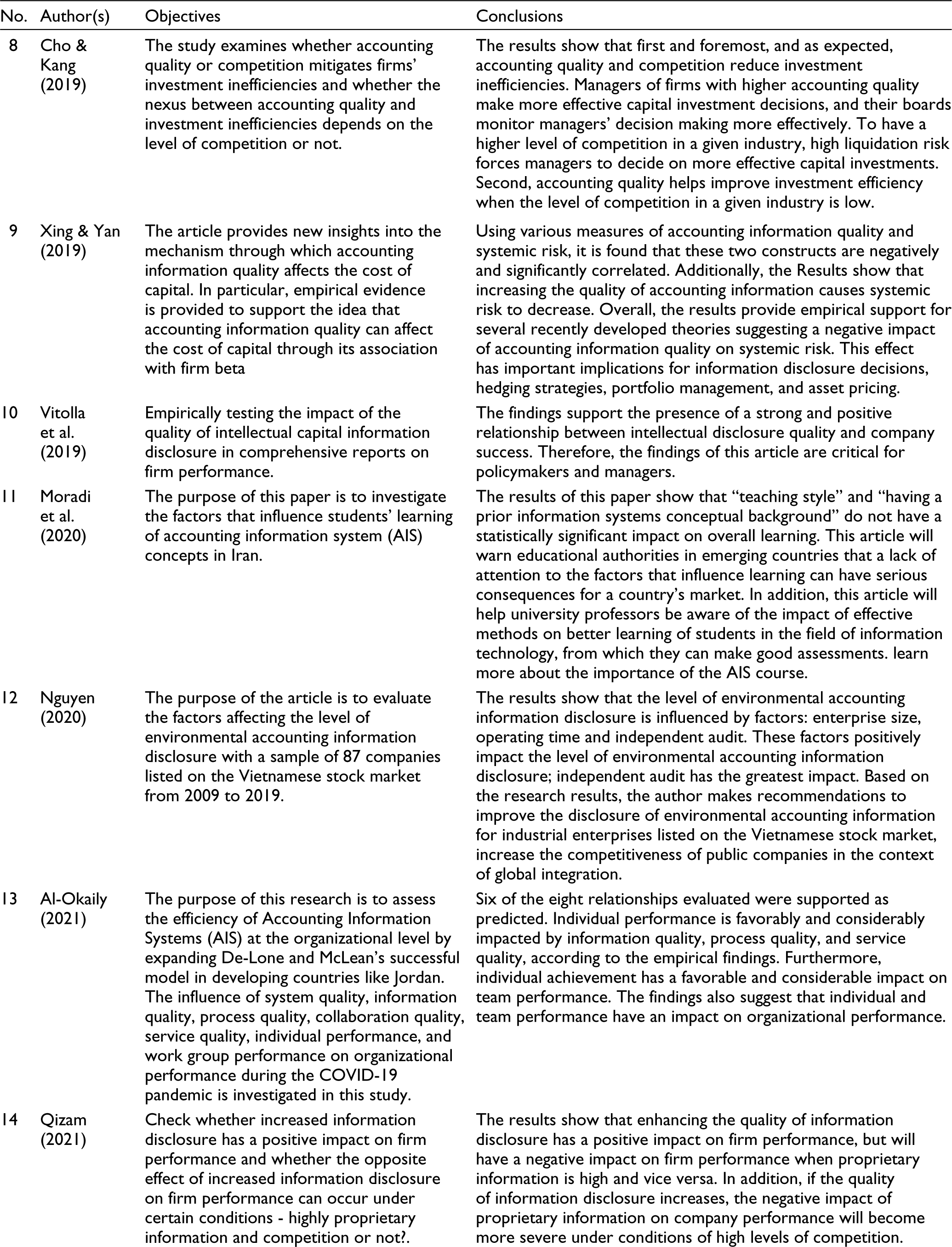

In fact, there are quite a few antecedent and outcome variables related to the accounting information quality (AIQ) (Abu Afifa et al., 2023; Ozdemir et al., 2017), but there is a lack of earlier investigations that fully integrate this issue. Some studies have paid attention to factors affecting the AIQ on financial statements with fairly consistent results (Moradi et al., 2020; Nguyen, 2020). Meanwhile, numerous previous studies have examined the influence of AIQ on some important aspects of the firm (Cho & Kang, 2019; Xing & Yan, 2019), especially firm performance (FIP) (Chan et al., 2009; Spathis & Ananiadis, 2005). A novel research stream related to technology 4.0 is to consider the influence of the accounting information systems quality (AISQ) on the AIQ (Al-Okaily, 2024). Simultaneously, there is a research direction on the influence of information technology risks (ITR) on the firm’s operations (Chatzoglou & Diamantidis, 2009), especially the AISQ (Rubino et al., 2017). However, these investigations are not targeted at SMEs and do not fully integrate these variables into the unique empirical research model (see Appendix A).

Additionally, studies on the factors affecting accounting information system quality (AISQ) and AIQ have been carried out in developing countries (Al-Hattami & Kabra, 2024; Kwarteng & Aveh, 2018), but not so much in Vietnam. Moreover, the studies on the factors affecting the AISQ and AIQ have not yet shown that there are studies with all organizational factors and information technology factors (Ghorbel, 2019). In particular, there has been a lack of study on the effect of these factors on AISQ from the perspective of ITR and the manager’s personal characteristics (e.g. transformational leadership [TL]). The integrated study of the above factors in the context of SMEs will help SMEs and stakeholders better understand the quality of accounting information on financial statements. Accordingly, SMEs and stakeholders can control ITR in the best way, helping to enhance the AISQ and in turn helping to enhance the AIQ. In the current era of global digitalization, SMEs show their importance to the economy because they account for a relatively high proportion, especially in developing countries such as Vietnam (Nguyen & Nguyen, 2019; Quoc Trung, 2021). However, reality shows that many SMEs do not properly recognize the importance of controlling information technology for its output (e.g. AISQ and AIQ) to serve economic growth (e.g. FIP). Furthermore, a large number of SMEs are targets of cyber-attacks (Armenia et al., 2021), but they still do not appreciate the role of ITR in their survival and development.

Thereby, this article goes further by scrutinizing the influence of AIQ on the FIP of SMEs in regard to Vietnam. We additionally explore the antecedent variable impacting of AISQ and ITR in the circumstances. Besides, we employ TL as a moderating factor in the study model. The main study results manifest that there has been a favourable and notable influence of AIQ on FIP of SMEs in accordance with agency theory. Furthermore, AISQ and ITR serve as significantly antecedent variables consistent with the contingency theory. Additionally, TL positively moderates the AIQ–FIP nexus. As a result, this study has several theoretical and practical benefactions as follows. First, earlier investigations focused more on factors that directly affect AIQ rather than intermediate and antecedent effects. Meanwhile, this article focuses on this issue in the circumstances of SMEs, especially the role of ITR and TL. Second, the findings of this article provide decision-makers with more in-depth explanations of the influence of AIQ on FIP. Decision builders, such as current and later investors, can use these insights to create the right decisions by utilizing AIQ as an indicator to forecast a firm’s later accomplishment. Furthermore, policy-builders can use these results to provide guidance that may enhance FIP by paying attention to upgrading accounting data systems and reducing ITR.

The following sections of the article are introduced as follows. The ‘Theoretical Background and Hypotheses’ section is a theoretical background and hypotheses. The ‘Methodology’ section is more about data and methodology, while the ‘Results and Discussion’ section presents experimental findings and discussion. The ‘Conclusion’ section presents the main conclusions, limitations of the present article and future research directions.

Theoretical Background and Hypotheses

With the context of this topic, agency theory is utilized to describe and forecast the selections of SMEs with accounting practice. Agency theory postulates that accounting selections are likely to be specified by those at the top of the firm looking to have an impact on revealed returns and equity structure in defective markets (Chen et al., 2012a). Adopting an accounting information system is the accounting selection that leaders want to improve both the quality of earnings and FIP (Abu Afifa et al., 2023). In line with this theory, accounting data systems reduce the issue of data asymmetry and increase the AIQ by enhancing the accuracy of the statements. Furthermore, this theory has been the foundation for assessing the influence of AIQ on FIP (Alipour et al., 2019).

Contingency theory had been used in information systems research to describe how individual and organizational characteristics have been related to create efficient systems (Dewett & Jones, 2001). The perspective of this theory in information technology and data systems has been in line with the rule that no unique data system may be universally adopted with all firms in all circumstances (Abu Afifa & Saleh, 2021, 2022). This theory shows that the accounting data system relies on the characteristics of a firm expressed through the environment, technology, organizational structure, individuals and leadership characteristics. Accordingly, the factors of management, organizational culture, human resources and information technology factors are considered to be related and affect the AISQ (Stoel et al., 2012).

In the perspective of the converging between the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB), the standards for AIQ have been agreed upon, including relevance (predicting and confirmed value), faithful substitute (absolute, unbiased and non-error) and verifiability (comparing, understandability and timeliness) (Alali & Cao, 2010). Then, IASB adds to the standard framework for AIQ the materiality attribute, to emphasize and further explain the relevant attribute (Al-Dmour et al., 2023; Tarca, 2020). Data are considered material if its exclusion or misrepresentation might impact decision-makers who use financial statements. Although there are some differences among researchers on the characteristics of information quality (Fan et al., 2023; Song & Zhou, 2021; Yang et al., 2021), in general, these views are similar to the harmonized and agreed views on the format of the IASB AIQ standards and FASB. Applied in this article, the standards of AIQ of IASB and FASB are selected as the theoretical basis for measuring AIQ because of its large and far-reaching global influence, as well as its high level of reference and citation.

Over the past decade, there have been many different views on AISQ. Darma (2018) argues that AISQ includes reliability, integration and accessibility. In addition, Al-Dmour and Abbod (2018) point out that the AISQ attributes include efficiency, integrity, compliance, efficiency, availability and security. According to Napitupulu (2020), AISQ is identified through the characteristics of integration, flexibility, reliability and efficiency. Hutahayan (2020) also mentioned that AISQ is related to efficiency, integration and timeliness. Additionally, Al-Hattami (2021) emphasizes three attributes of flexibility, efficiency and accessibility. However, in general, the Petter et al. (2008) model has a reliable theoretical basis and relates to the field of data technology and information systems. The measurement characteristics in this model have many similarities and cover most of the views of other researchers about AISQ, including ‘Net Benefits’ becoming ’Net Effects’, with the authors implying that the output is negative or positive, but the term ‘Benefits; usually refers only to what is positive. In addition, feedback loops are also added with feedback arrows going from ‘Usage’, ‘User Satisfaction’ to ‘System Quality’, ‘Information Quality’ and ‘Service Quality’. Therefore, in this article, the model of Petter et al. (2008) is taken as the basis for measuring AISQ, but we only inherit the properties of the component system quality.

Researchers and practitioners offer a variety of meanings and measurements for FIP, and it has been a way of measuring a firm’s success in the industry both financially and non-financially (Abu Afifa & Saleh, 2022). There have been dissimilar variables to quantify FIP in SMEs, and some researchers utilize financial indicators to quantify it (Shu et al., 2020). Both financial and operating performances are commonly used to measure a firm’s accomplishment in the area of understanding management (Al-Sa’di et al., 2017). Although the financial aspect has been considered to be the core of a firm’s performance (Nuryakin & Ardyan, 2018), it cannot represent a firm’s performance alone. Numerous researchers have recommended that the operational aspect has been a key driver of success (Huo et al., 2021; Ramirez et al., 2021). Thereby, this article selects the operational aspect to quantify FIP to specify how well the firm is managed (Chaithanapat et al., 2022).

Rather than just obtaining compliance, transformational leaders motivate their teams to achieve unexpected outcomes by changing their opinions, principles and practices (Maaitah, 2018). This management style stresses employee development in accordance with the overall goals of the firm (Kim, 2014). Transformational leaders are concerned about their teams and promote enthusiasm and good work to improve their performance (Gilmore et al., 2013). Managers using this approach will encourage good employee behaviour, resulting in improved organizational performance. Previous studies indicate that some of the successful international businesses have attained their objectives by employing the TL method (Maaitah, 2018). Moreover, several studies show that TL plays a significant role in achieving individual and firm goals (Gyensare et al., 2017) and the TL components (i.e. idealized impact, inspirational motivation, intellectual stimulation and individualized consideration) have an indirect effect on management system and FIP (Khan et al., 2018; Para-González et al., 2018). Accordingly, TL is a composite interaction from which a shared impulsion for activity and shift arises when diversified actors interact in a network, which creates innovating categories of behaviour or new modes of operation.

Agency theory has been interested in identifying a mechanism by which the owner with less data may best profit from the attempts of the agent who has more data and various benefits. AIQ has not been good due to data asymmetry making financial statements undependable. Simultaneously, the AIQ will influence the utilizers of the data on the financial statements to assess the FIP. Thus, the AIQ has been principal in the process of observing the operations of the leadership (the board of directors) so that the firm may have better accomplishments and improve the benefits of related parties. Consequently, the theory emphasizes the role of AIQ on FIP. Earlier investigations had indicated a notable favourable nexus between AIQ and FIP indicators (Qizam, 2021; Temiz, 2021). Furthermore, with a specific feature such as quality of environmental accounting information (Alipour et al., 2019), quality of non-financial accounting data (Gao et al., 2016) or quality intellectual capital accounting information (Vitolla et al., 2019) all show a positive impact on FIP. It leads to frame the following hypothesis:

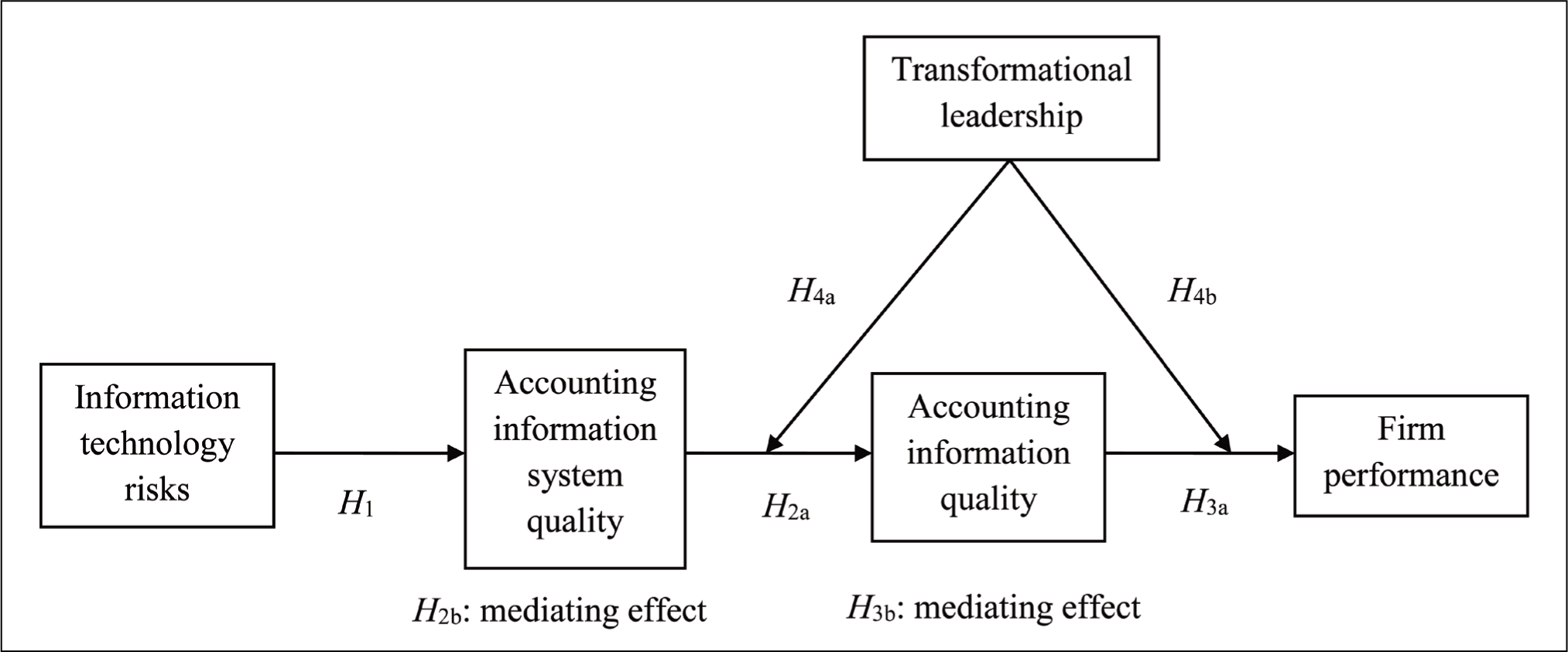

H1: AIQ has a favourable influence on FIP of SMEs.

An accounting data system has the ability to copy, account, save and process information to generate data for business decisions (Alkan, 2022). Some scholars stated that information systems assist managers in performing management functions by providing the information needed (Meiryani et al., 2023). Meanwhile, others state that the intention of an accounting information system has been to supply data about the resources used by the firm, and to provide information relevant to management decision-making, and help employees perform their duties efficiently and effectively (Belfo & Trigo, 2013; Trigo et al., 2016). A study by Sajady et al. (2008) which evaluates the effects of an accounting data system shows that the performance of the system leads to improved quality of financial statements and faster transaction processing. Another conclusion of prior investigations describes the link between accounting data systems and reporting based on the quality characteristics of accounting data, such as accuracy, reliability, timely accessibility, update and availability (Latifah et al., 2021; Trigo et al., 2016). Finally, the accounting data system has been recognized as an important reporting system that provides stakeholders with quality accounting information to make useful decisions (Blackburn et al., 2014; Huy & Phuc, 2020). Therefore, the below hypotheses have been constructed:

H2a: AISQ has a favourable influence on AIQ of SMEs. H2b: AIQ mediates the impact of AISQ on FIP of SMEs.

In the circumstances of data technology, the increasing amount and complexity of data has led to increased attention on the risks and control related to both emerging technologies and governance approaches (Colicchia & Strozzi, 2012; Kardes et al., 2013). With the achievement of the accounting data system, data quality has been very important as it ensures effective improvement within the firm (Paula Monteiro et al., 2022; Silvola et al., 2016). Several scholars also argued that the accuracy of data has a relationship with the success or failure of the resource planning system operation (Alshurideh et al., 2022; Hasan et al., 2019). There has also been the point of vision that the incompleteness and inaccuracy of data can harm firm competition abilities, as poor data quality seriously affects the output of the accounting data system (Abrardi et al., 2022; Calvano & Polo, 2021). Additionally, firms that need to have a plan to remediate a data problem if it occurs strengthen the role of data quality audit and data encryption to give information systems reliability, security and safety. Moreover, it has been necessary to focus on threats to the firm’s data from both internal and external sources (Moon, 2013; Prajogo & McDermott, 2014).

On the other hand, unskilled staff is also believed to be the cause of failure in operating information systems (Moon, 2013; Safdar et al., 2022), and the competence of accountants is also considered to be the key to the success or failure of the accounting data system. Additionally, people are the most important and are even more important than the system. Human factors have a much larger impact on the AISQ and information technology staff cannot create all the controls to put into the system, as they still need people to enforce the rules and controls. However, the commitment of managers and the capacity of users have affected the accounting information systems quality (Ibrada et al., 2022; Thoa & Nhi, 2022). The users are the ones who produce the results and are responsible for making the system work as expected. Furthermore, the lack of proper training and coaching may lead to serious problems for the firm (Dikert et al., 2016) by having an impact on the AISQ and AIQ. It leads to frame the following hypotheses:

H3a: ITR have an adverse influence on AISQ of SMEs. H3b: AISQ mediates the impact of ITR on AIQ of SMEs.

Leadership disengagement and non-cooperation are significant obstacles in the relationship between AISQ and AIQ, making it harder to reach FIP (Qatawneh, 2023). Put differently, the evolution of AIQ can be improved if leaders set an ideal and voluntarily apply new technologies in accounting information systems (Bowen et al., 2007; Chang et al., 2003; Gorla et al., 2010). In addition, the stronger the consciousness, the faster the leaders move from the traditional style to the transformation. In that context, TL will promote the impact from the AISQ to the AIQ. In terms of cause, TL is a method for achieving higher workplace process efficiency (Kissi et al., 2013; Walumbwa & Hartnell, 2011), therefore, improving the AISQ and thereby enhancing the AIQ. On the contrary, a low level of leadership may have unpredictable effects on the system’s data management and pose risks to the AIQ (Li & Lin, 2006; Otley & Pierce, 1995). Furthermore, risk management has been the foundation of a flexible data system with multiple growth orientations (Arnold et al., 2015). Therefore, the lack of TL will have an adverse influence on both the development orientation of the system and lead to an adverse effect on the AIQ. In such a case, the safety and effectiveness of the system will decrease due to lack of timely leadership. This is indirectly reducing the AIQ.

Another advantage of TL is that the manager improves the ability to evaluate functional flows and the overall goals of the firm (Birasnav, 2014; Burmeister et al., 2020), thereby making decisions more efficient and fostering trust between internal managers (Chen et al., 2012). These benefits will enhance the AIQ, which in turn will promote improved FIP. In this context, employees will follow the leadership example, contributing to the growth of AIQ. In addition, TL helps firms with high AIQ to increase the practice of quality-improvement activities, which leads to a stronger relationship with FIP. Obviously, when TL is high, the impact of AIQ on FIP will be improved. In contrast, in the case of managers with low TL, it is difficult for firms to establish policies to promote activities to improve employee performance (Khan et al., 2018; Nijstad et al., 2014). This will somewhat have an adverse influence on AIQ, leading to a reduction in FIP. Therefore, the below hypotheses are constructed:

H4a: TL moderates the impact of AISQ on AIQ of SMEs. H4b: TL moderates the impact of AIQ on FIP of SMEs.

Finally, we can show the research model through Figure 1.

Research Model.

Methodology

Quantitative methods were utilized in this article. In line with earlier studies, the scale variables and questionnaires were built in accordance with the research context of SMEs in Vietnam. This context was chosen because of the following reasons. First, accounting data in Vietnam was inadequate for creating decisions due to the system quality and the data quality not being absolute (Binh et al., 2022). Therefore, empirical studies were needed to more clearly define the internal problem in this country with respect to AIQ. Second, the current understanding of accounting innovation (e.g. increase in AIQ) and its economic influence (e.g. increase in FIP) had still been limited when it related to evolving countries (e.g. Vietnam). Wadho and Chaudhry (2018) argued that much of the absence of skilfulness could be ascribed to the fact that firm-specific data on renewal procedures were not available in these countries. Therefore, it was necessary to clarify this issue so that firms had the right strategy when they wanted to improve FIP. Finally, SMEs account for a large proportion in developing countries such as Vietnam (e.g. Nguyen & Nguyen, 2019; Quoc Trung, 2021). However, there is a paucity of empirical studies on SMEs both in terms of AIQ (e.g. Al-Hattami & Kabra, 2024) and FIP (e.g. Chin et al., 2014) for this context. Therefore, this article will fill this gap and want to go further in integrating AISQ, AIQ and FIP in the same experimental model. This adds to current theoretical knowledge and tackles important practical issues in developing-country SMEs.

The questionnaire was released as an experiment and received feedback and then was edited and used as a data collection tool for formal research. We used a web-based e-mail survey form to gather the information. The e-mail replies had been gathered from the homepage of firms, the Department of Planning and Investment of Vietnam and the Entrepreneurs Association. The non-probability conveniences approach was used to choose firms in each sector. However, our business selection was based on (a) the proportion of SMEs to all firms in Vietnam and (b) the ratio between small and medium firms within SMEs. These ratios were in line with the results of the 2021 Enterprise Census conducted by the Vietnamese General Statistics Office (General Statistics Office of Vietnam, 2021). Consequently, it nonetheless assured that our sample was representative of the research population.

Reference letters with questionnaire links were sent to corporate or personal e-mails of 500 respondents. Reminders were sent twice to encourage the response. Specifically, 255 complete responses were collected. We removed 22 incomplete responses and 15 outliers. Our analysis unit was each SME, so survey respondents should be managers representing their respective SME. Besides, we had an extra step to test the rest of the feedback forms. Specifically, we had reviewed and removed feedback from the same firm. Thus, 198 final valid responses had been eventually utilized for data examination, reaching a rate of 39.6%. These responses had been utilized for data analysis and our sample size fits the quantitative research criteria (Hair et al., 2019).

Based on the theoretical review, we designed a survey that included each aspect examined. Question items in our survey had been adapted from previous studies (see Appendix B). All the structures used in our theoretical framework had been operated as reflective structures. Specifically, we measured AIQ inherited from accounting conceptual framework for accounting information quality (as recommended by IASB and FASB in 2010; Abu Afifa et al., 2023), including nine indicators. FIP was measured through six items which Wang and Wang (2012) developed. We measured AISQ against four adjusted metrics from the component system quality of Petter et al. (2008). Next, the ITR variable was measured by a secondary order inherited from Zhang et al. (2003), covering two aspects related to SMEs, namely data risks (four items) and human resource risks (three items). In addition, the measure of TL consisted of five items inherited from Alonso-Almeida et al. (2017). Finally, we also used a firm type as a control variable for both AIQ and FIP in the study model.

We had used Harman’s test (Malhotra et al., 2006) and marker variable (Lindell & Whitney, 2001) to minimize the common method bias (CMB). These findings demonstrated that CMB is not a reason for alarm. To test the non-response bias, we saved the subject response timestamps to divide the survey sample into many groups. The t-test was then utilized to differentiate the two groups (the earliest and newest responses). According to the findings, there has been no notable distinction in the mean value of any factor between the two groups (p > .05). Following that, the χ2 test was tested to investigate demographic variations among respondents. The findings also revealed that no statistically notable divergence existed between any two groups of respondents (p > .05).

Collected data was analysed and corrected by SPSS, including descriptive statistics of variables, CMB tests and non-response bias tests. Smart–PLS was utilized to evaluate the proposed hypotheses using partial least squares structural equation modelling (PLS–SEM). We utilized PLS–SEM for analysis because it is appropriate for predictive research with precisely sequential phases (Hair et al., 2019). Furthermore, to investigate the impact of the mediating and moderating variables, we used the bootstrap technique interval.

Results and Discussion

According to the descriptive results of the study sample characteristics, the sample includes 63.6% in the industry and construction sector, 29.8% in the agriculture, forestry and fishery sector and 6.7% in the service sector. The ratios have been appropriate to the GDP ratios of the aforementioned industries in 2021 (65%, 31.5% and 3.5%, respectively). Besides, the sample includes 28 (14.14%) medium firms and 170 small firms (85.86%), and these ratios are consistent with the ratios of small and medium firms listed in Vietnam according to the 2021 Enterprise Census. Therefore, the selected sample is guaranteed to be identical to the research population.

Measurement Model

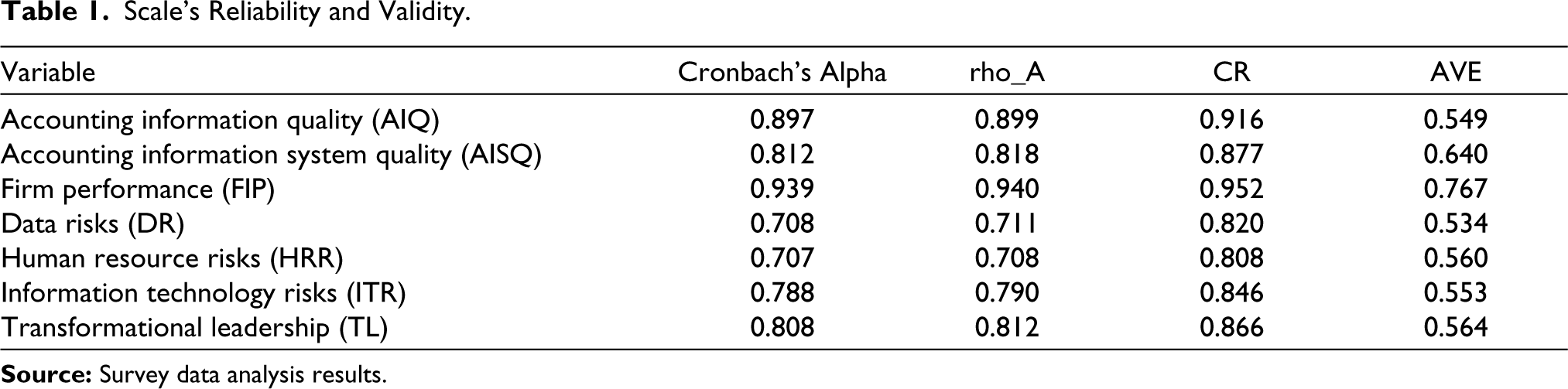

We hypothesize the inner consistency’s reliability using the composite reliability (CR) index in which certain indicators have been excluded because the outer loading is less than 0.4 and the t-bootstrap is less than 1.96. Moreover, the average variance extracted (AVE) indexes of all constructs have been over 0.50 in Table 1; therefore, the convergent validity reach expectations. The CRs of all latent variables are more than 0.7. Furthermore, Cronbach’s alpha is more than 0.7 in all scales, implying that the measurement model really reaches inner consistent reliability.

Scale’s Reliability and Validity.

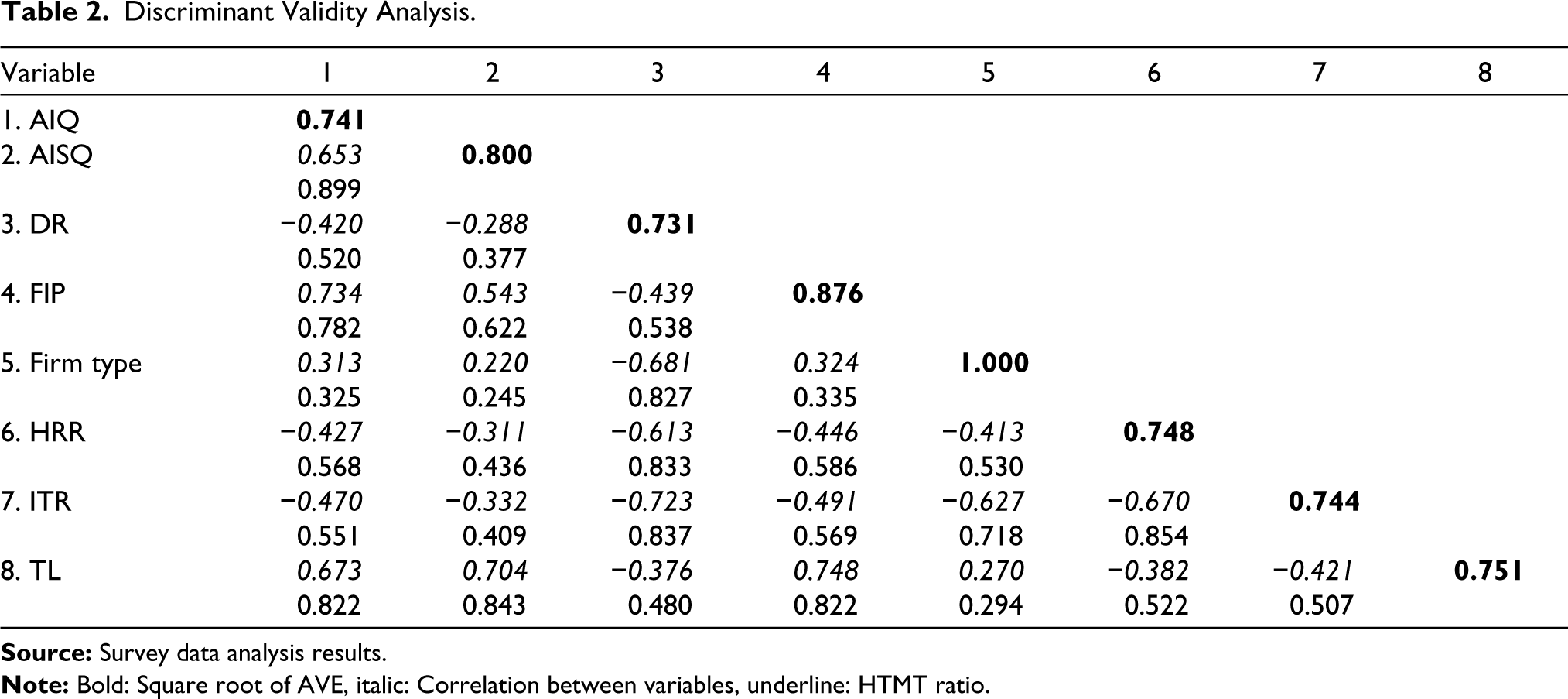

Next, we used the process proposed by Fornell and Larcker (1981) to assess discriminant validity. The square roots of the AVEs of the significant constructs in Table 2 are all greater than the equivalent correlation coefficients. Moreover, HTMTij ratio is less than 0.9 in each pair of scales. So, study pairs of scales are eligible to employ the bootstrapping process of HTMT ratio test (Henseler et al., 2015). According to the 5,000 bootstrapping results, the 95% confidence interval of the HTMT ratios has been less than one. As a result, the measurement models of this article obtain a high level of discriminant accuracy.

Discriminant Validity Analysis.

Structural Model

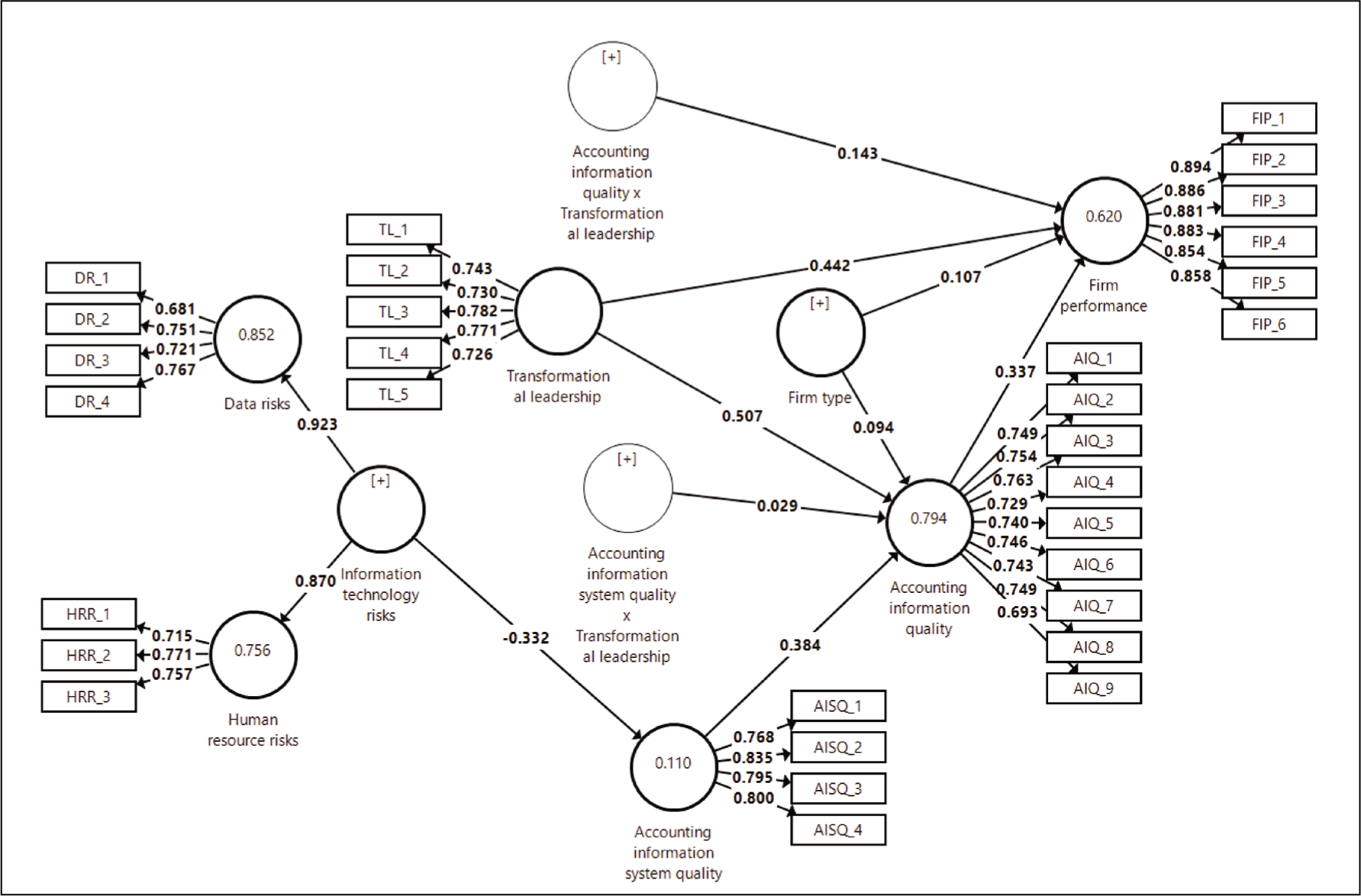

Due to the variance inflation component coefficients of all variables being less than 5, multicollinearity is unlikely in this study model. According to the results of Figure 2, AISQ, AIQ and FIP have R2 equal 0.110, 0.794 and 0.620, respectively. Therefore, ITR have a low level of effect on AISQ and AISQ has a high level of impact on AIQ, as well as AIQ having a high level of influence on FIP. Additionally, all f2 coefficients are more than 0.02, so all factors have high level of explanation. Specifically, ITR have low explanatory power for AISQ. In contrast, AISQ has high explanatory power for AIQ. Similarly, AIQ has high explanatory power for FIP.

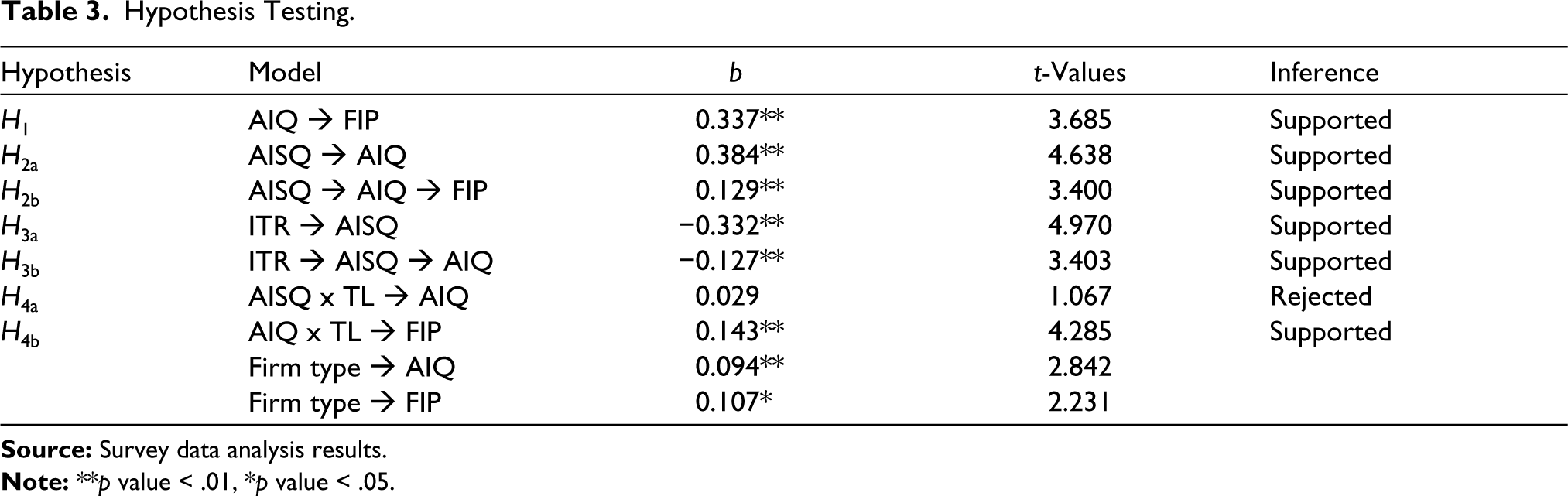

Additionally, the dependent variables in the study model have Q2 > 0, demonstrating the predicting power of the model. Specifically, the study model has medium predicting powers for AIQ and FIP (Q2 = 0.427 and 0.458, respectively). Table 3 indicates that the study hypotheses are statistically significant with 95% confidence. Thereby, AIQ positively affects FIP, and AISQ positively impacts on AIQ. Conversely, ITR negatively affects AISQ. Besides, AIQ positively mediates the AISQ–FIP nexus. Additionally, AISQ negatively mediates the ITR–AIQ nexus. Finally, TL positively moderates the AIQ–FIP nexus.

Hypothesis Testing.

Particularly, H1 predicts that AIQ has a beneficial effect on FIP. The findings reveal that β = 0.337 (p < .05) and the t-value is above 1.96. Consequently, H1 is accepted. According to H2a, AISQ has a beneficial effect on AIQ. The findings reveal that β = 0.384 (p < .05) and the t-value has been above 1.96. Therefore, H2a is accepted. H2b predicts that AIQ mediates AISQ–FIP nexus. The findings show that β = 0.129 (p < .05) and the t-value is above 1.96. Thereby, H2b has been approved. H3a predicts that ITR negatively affect AISQ. The results show that β = −0.332 (p < .05) and the t-value has been above 1.96. Thus, H3a is supported. H3b predicts that AISQ mediates ITR–AIQ nexus. The findings show that β = −0.127 (p < .05) and the t-value is above 1.96. Therefore, H3b has been approved. Next, H4a and H4b predict that TL moderates AISQ–AIQ nexus and AIQ–FIP nexus, respectively. The results indicate that β is 0.029 and 0.143, respectively, but only H4b is supported due to p <.05 and t-value >1.96. Finally, the control variable has a positively significant influence on both AIQ and FIP.

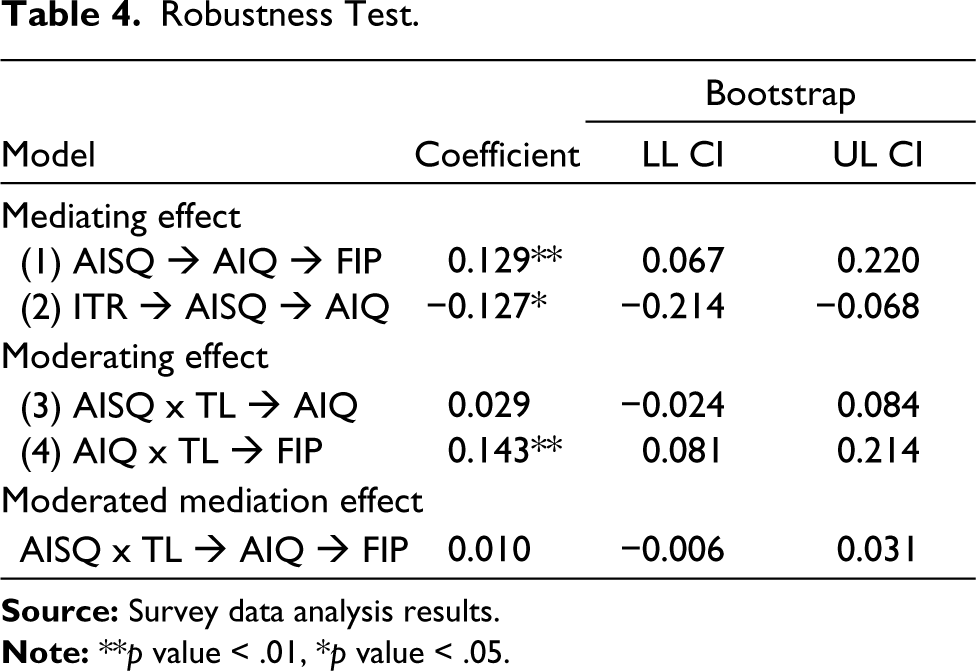

Robustness Test

Table 4 shows the mediator factor roles at the 95% significance level in the models. Particularly, the coefficient of model (1) AISQ → AIQ → FIP is equal 0.129, and the effect confidence interval is totally above zero. The coefficient of model (2) ITR → AISQ → AIQ is equal −0.127 and the confidence interval is totally below zero. Thus, AIQ positively mediates the AISQ–FIP nexus, and AISQ negatively mediates the ITR–AIQ nexus. Regarding the two moderating effects, TL only exhibited a significant moderating role for AIQ–FIP nexus (coefficient of model (3) is 0.143 at the 95% significance level), whereas it was not statistically significant for AISQ–AIQ nexus. Finally, the moderated mediation effect is not statistically significant in this study model. In summary, H2b, H3b and H4b are once again accepted, while H4a was actually rejected.

Robustness Test.

Discussion

The results of this study show that except for hypothesis H4a, the remaining hypotheses are accepted. The results suggest a positive antecedent impact of AISQ on AIQ, and a positive outcome of FIP from AIQ in the Vietnamese context. Simultaneously, this article confirmed the mediating role of AISQ for the ITR–AIQ nexus, as well as the role of AIQ mediating for the AISQ–FIP nexus. In addition, this article found evidence that TL moderates the positive AIQ–FIP nexus. This result demonstrates the importance of the above factors in modern accounting practice in relation to quality culture, especially in the developing country context.

In fact, this article is a continuation of previous research on AIQ (Alkan, 2022; Latifah et al., 2021; Qizam, 2021; Temiz, 2021; Trigo et al., 2016) and AISQ (Abrardi et al., 2022; Calvano & Polo, 2021; Ibrada et al., 2022; Moon, 2013; Safdar et al., 2022; Thoa & Nhi, 2022). The results of this study support Petter et al. (2008) when affirming the proper aspect of system quality. The findings are also similar to prior studies (e.g. Qizam, 2021; Temiz, 2021), when confirming that AIQ positively affects FIP. Additionally, the results complement previous studies on the positive mediating and antecedent role of AISQ. In order to manage strategies well and achieve business goals, managers must pursue and maintain a quality accounting information system in their firms, especially in an environment that requires the application of information technology in management increasingly (Alipour et al., 2019; Vitolla et al., 2019).

Simultaneously, organizational risks along with ITR have also had a significant impact on the AISQ (Abu Afifa & Nguyen, 2023). Therefore, the management implications from this study partly suggest to firms the orientations on controlling ITR to increase the AISQ, thereby contributing to the increase of the economic data quality in firms, especially data risks and human resource risks for SMEs. Additionally, this article shows the importance of both AISQ and AIQ for SMEs’ FIP. It can be seen that SMEs should change their management thinking, step by step standardize their working processes towards modernization, accumulate sufficient financial resources, and pay attention to monitor the continuous progress of new technologies so that when appropriate, they will make appropriate investment decisions for development.

Furthermore, the findings of this study have been consistent with some earlier studies showing that TL may support firms to achieve better performance (Chan et al., 2009; Samad, 2012; Spathis & Ananiadis, 2005) through significantly moderating the impact from AIQ to FIP, especially within accounting practice in today’s risky environment (Pillai & Williams, 2004). Following that, this article also extends a limited research stream on the indirect effects of TL on accounting practice. It can be seen that all four aspects of TL have an indirect impact on accounting practices in today’s risky digital age (Han et al., 2016). However, previous research has often focused on direct effects, leaving out the fertile research background for indirect effects in the absence of research in this direction. This article contributes to suffice the above gap in the context of Vietnamese firms, an emerging market that has paid attention to the quality of accounting, but the efficiency has not been adequate.

Finally, agency theory is often used for large firm contexts, but our study results contribute to supporting its use for SMEs, and therefore complementing the findings of previous studies (e.g. Chen et al., 2012; De Massis et al., 2015). The study results manifest that there has been a favourable and notable influence of AIQ on FIP of SMEs in accordance with agency theory. Specifically, this shows that accounting data systems reduce the problem of data asymmetry and increase AIQ by improving reporting accuracy, thereby enhancing FIP (e.g. by reducing agency costs). Clearly, applying an accounting information system is a choice that leaders want to improve both income quality and FIP (Chen et al., 2012). In this case, the application of an accounting information system with significant power will affect AIQ, thus reducing information asymmetry for private gain, leading to a reduction in agency problems.

Conclusion

This article aims to determine the influence of numerous antecedent and outcome variables in order to clarify the role of information quality in the financial statements of SMEs in Vietnam. The current article examines the AISQ–FIP nexus through the mediating role of AIQ. Similarly, AISQ is tested as a mediator variable in the ITR–AIQ nexus. We use necessary techniques to overcome the non-response bias and CMB phenomenon. The main results of this article show that ITR have a notable influence on AISQ. Furthermore, the AISQ has an obvious favourable impact on the AIQ on the financial statements of SMEs. In addition, the AIQ in the financial statements of SMEs has a favourable influence on FIP in the context of Vietnam.

The current article has a useful outlook of academic and practical implications as follows. Regarding the academic aspect, we determine the impact of antecedent variables (e.g. ITR and AISQ) and output variables (e.g. FIP) on AIQ in a developing country (i.e. Vietnam). Furthermore, this article determines the effects of the above variables in an integrated reality model. The authors additionally integrate the moderation effects of TL in the model. The results imply that AISQ negatively mediates the ITR–AIQ nexus, and AIQ is a positive mediator of the AISQ–FIP nexus. We also investigate that TL significantly moderates AIQ–FIP nexus. Finally, the results of this article contribute to confirm, strengthen and extend the previous theoretical and empirical literature on these structures in the context of developing economies.

From another perspective, ITR and AISQ are two important prerequisites of AIQ towards a strong FIP of the firm. Therefore, managers need to focus the firm’s resources on these issues. Accompanying today’s outstanding technological development are ever-expanding technological risks. Therefore, the firm should have a strategy to limit this risk, on the basis of limiting data risk and human resource risk. In particular, adequate training and training must be given to staff in the necessary skills to participate in the use of the accounting data system at the firm. It has been necessary to motivate all employees of the firm to change their attitude and consciousness in a positive direction to boldly apply new technology to work, all for the common goal of the firm. There should be a data recovery plan, such as having a mechanism to back up the data regularly, dealing with data errors, and especially an audit of the data in use. Moreover, there must be a mechanism to strictly control behaviours that threaten businesses, for example, dishonest employees, computer crimes and unfair competitors.

Finally, the results of this article should note a number of limitations. Despite our efforts to prevent the CMB phenomenon, causality problems among variables may develop due to insufficient control variables. Thus, future research might investigate this study model using more control variables. In addition, this article only focuses on the ITR associated with the inner environment of the firm, without considering the outside environment. Subsequent studies may consider expanding to the external environment and uncovering new ITR factors.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

Overview of Some Previous Relevant Studies.

| No. | Author(s) | Objectives | Conclusions |

| 1 | Spathis & Ananiadis (2005) | This paper investigates the influence of choices resulting from the implementation of a new ERP system on accounting and management information at a big public university in Greece, based on anticipated advantages according to user expectations and perceptions. | According to the findings, one year after ERP implementation, users’ perceptions are more positive than their expectations before to implementation. Empirical evidence indicates a variety of advantages gained from the new ERP system, particularly in accounting and management information. The new ERP system greatly helps to boosting information flexibility by effectively monitoring and exploitation of the firm’s assets, income and expenditure flows, and decision making. |

| 2 | Chan et al. (2009) | The study examines whether changes in accounting information quality following mandatory regulatory intervention affect well-documented accruals anomalies. The study expects the accrual anomaly phenomenon to be more obvious in a poorer information environment | The results show that the new disclosure regulations have improved the accounting information environment in the UK and it is predicted that mispricing of accruals will decrease following the introduction of this legislation. Consistent with expectations, the study shows that accrual anomalies in the UK decreased significantly following the new disclosure rules. Among companies with lower quality accounting information, the study finds clearer evidence of accrual anomalies in the period before the new disclosure regulation as well as a larger decrease in the period after the new disclosure regulation. The overall inference is an improvement in the quality of reported earnings following the new disclosure rules by reducing the discretionary effects of managers, investors’ accuracy in valuing accruals will be enhanced. |

| 3 | Chatzoglou & Diamantidi (2009) | This study focuses on the impact of IT on a company’s non-financial IT risk. The study was conducted using questionnaires sent to the world’s 500 largest corporations as they were published in Fortune magazine and Greek companies | The results indicate that IT risk factors mainly affect coordination and partial information capabilities but not productivity. Furthermore, the most important risk factors affecting business performance are management ability, information integrity, controllability and exclusivity. |

| 4 | Gao et al. (2016) | Examining the determinants and economic consequences of non-financial disclosure quality, measured by corporate social responsibility disclosure ratings provided by the Dutch Ministry of Economy | The study finds that companies with better corporate social responsibility performance, greater need for external financing, and stronger corporate governance tend to provide corporate social responsibility disclosures with higher quality industry. |

| 5 | Ozdemir et al. (2017) | This paper studies information privacy in the context of peer-to-peer relationships on commercial social media sites. The paper develops a model that examines the relationships between the constructs of privacy experience, privacy perception, trustworthiness, risks, and benefits, and how those relationships impact to individual disclosure behavior. | The results show that both privacy experiences and privacy perceptions are quite significant predictors of privacy concerns. The study also found that trust, risk, benefit, and privacy concerns work together to explain the majority of variation in disclosure behavior. The study also discusses implications for practice and future research. |

| 6 | Rubino et al. (2017) | The purpose of this article is to analyze how the Governance of IT (COBIT) framework affects the control environment and internal control system. In particular, it is intended to illustrate how COBIT’s structure and processes impact the seven categories of factors that make up the control environment. | The structure of COBIT can help managers and auditors better evaluate and manage the components of the control environment. Such a framework is not only designed for use by IT service providers and auditors, but more specifically, it is also designed to be a complete guide for managers. A feature that contributes to the popularity and appreciation of COBIT is that the framework adopts a number of observations informed by professional practice and academic research. The use of these observations allows the development of valuable best practices aimed at effective control of processes, thereby ensuring greater reliability in terms of data and information. |

| 7 | Alipour et al. (2019) | Investigate the relationship between environmental disclosure quality and firm performance, and test the moderating role of board independence in this relationship. | The results show that there is a significant positive relationship between environmental performance measures and company performance. The results also show that board independence significantly strengthens the positive impact of environmental disclosure standards on performance and that companies with more independent board members will participate in disclosure environmental information to improve operational efficiency. |

| 8 | Cho & Kang (2019) | The study examines whether accounting quality or competition mitigates firms’ investment inefficiencies and whether the nexus between accounting quality and investment inefficiencies depends on the level of competition or not. | The results show that first and foremost, and as expected, accounting quality and competition reduce investment inefficiencies. Managers of firms with higher accounting quality make more effective capital investment decisions, and their boards monitor managers’ decision making more effectively. To have a higher level of competition in a given industry, high liquidation risk forces managers to decide on more effective capital investments. Second, accounting quality helps improve investment efficiency when the level of competition in a given industry is low. |

| 9 | Xing & Yan (2019) | The article provides new insights into the mechanism through which accounting information quality affects the cost of capital. In particular, empirical evidence is provided to support the idea that accounting information quality can affect the cost of capital through its association with firm beta | Using various measures of accounting information quality and systemic risk, it is found that these two constructs are negatively and significantly correlated. Additionally, the Results show that increasing the quality of accounting information causes systemic risk to decrease. Overall, the results provide empirical support for several recently developed theories suggesting a negative impact of accounting information quality on systemic risk. This effect has important implications for information disclosure decisions, hedging strategies, portfolio management, and asset pricing. |

| 10 | Vitolla et al. (2019) | Empirically testing the impact of the quality of intellectual capital information disclosure in comprehensive reports on firm performance. | The findings support the presence of a strong and positive relationship between intellectual disclosure quality and company success. Therefore, the findings of this article are critical for policymakers and managers. |

| 11 | Moradi et al. (2020) | The purpose of this paper is to investigate the factors that influence students’ learning of accounting information system (AIS) concepts in Iran. | The results of this paper show that “teaching style” and “having a prior information systems conceptual background” do not have a statistically significant impact on overall learning. This article will warn educational authorities in emerging countries that a lack of attention to the factors that influence learning can have serious consequences for a country’s market. In addition, this article will help university professors be aware of the impact of effective methods on better learning of students in the field of information technology, from which they can make good assessments. learn more about the importance of the AIS course. |

| 12 | Nguyen (2020) | The purpose of the article is to evaluate the factors affecting the level of environmental accounting information disclosure with a sample of 87 companies listed on the Vietnamese stock market from 2009 to 2019. | The results show that the level of environmental accounting information disclosure is influenced by factors: enterprise size, operating time and independent audit. These factors positively impact the level of environmental accounting information disclosure; independent audit has the greatest impact. Based on the research results, the author makes recommendations to improve the disclosure of environmental accounting information for industrial enterprises listed on the Vietnamese stock market, increase the competitiveness of public companies in the context of global integration. |

| 13 | Al-Okaily (2021) | The purpose of this research is to assess the efficiency of Accounting Information Systems (AIS) at the organizational level by expanding De-Lone and McLean’s successful model in developing countries like Jordan. The influence of system quality, information quality, process quality, collaboration quality, service quality, individual performance, and work group performance on organizational performance during the COVID-19 pandemic is investigated in this study. | Six of the eight relationships evaluated were supported as predicted. Individual performance is favorably and considerably impacted by information quality, process quality, and service quality, according to the empirical findings. Furthermore, individual achievement has a favorable and considerable impact on team performance. The findings also suggest that individual and team performance have an impact on organizational performance. |

| 14 | Qizam (2021) | Check whether increased information disclosure has a positive impact on firm performance and whether the opposite effect of increased information disclosure on firm performance can occur under certain conditions - highly proprietary information and competition or not?. | The results show that enhancing the quality of information disclosure has a positive impact on firm performance, but will have a negative impact on firm performance when proprietary information is high and vice versa. In addition, if the quality of information disclosure increases, the negative impact of proprietary information on company performance will become more severe under conditions of high levels of competition. |

| 15 | Temiz (2021) | Investigating the impact of corporate information disclosure quality on firm value and firm performance | The study finds that the quality of information disclosure by companies has a positive and statistically significant impact on company value. However, it has a negligible impact on firm performance |

| 16 | Abu Afifa et al. (2023) | This study intends to investigate if perceived utility (PU), perceived ease of use (PE), and availability to embrace technology (AET) impact the intention to adopt an enterprise resource planning (ERP) system in Jordanian enterprises. It also investigates the impact of ERP system acceptance on ERP system adoption. More importantly, the current study fills a gap in previous research by investigating the impact of implementing an ERP system on accounting information quality as influenced by firm size. | Empirical data analysis shows that PU, PE, and AET impact ERP system acceptance, and that there is a positive relationship between ERP system acceptance and ERP system adoption. Furthermore, ERP system adoption has a beneficial impact on the relevance and faithful representation of accounting information, however this is moderated by firm size. |