Abstract

This study reconceptualizes the so far inconclusive relationship between unrelated diversification and financial performance by explaining how coordination costs can shape the amount of free cash flow and related agency problems at different levels of unrelated diversification. The study builds upon the notion that coordination requirements and associated coordination costs will vary at levels of unrelated diversification to regulate the amount of free cash flow managers will have at their disposal at each level of unrelated diversification. Based on the agency costs associated with free cash flow, we conceptualize that at different stages of unrelated diversification, the degree of managerial misuse of free cash flow can create different performance implications of the unrelated diversified firm to explain a proposed S-shaped relationship.

Introduction

Unrelated diversification (UD) refers to the extension of a firm’s business activities into an entirely different industry from its core function (Ljubownikow & Ang, 2020; Ng, 2007; Sorenson et al., 2006) and it has been considered an important way through which firms can strategically extend themselves (Singh et al., 2018; Westhead et al., 2001). However, despite decades of research into the relationship between UD and performance, the findings have been inconsistent (Palich et al., 2000; Schommer et al., 2019). In this study, we aim to conceptually explain that this inconsistent relationship is purely contextual around specific factors being considered, the extent of UD as well as managerial considerations. This contextual consideration ultimately extends the focus on linear predictions and path dependent approaches to include more complex approaches that predict complex interactions among constructs that are fundamental to the success of UD strategies (Palich et al., 2000). In answering this questions conceptually, this study conceptualizes a relationship between UD and financial performance by considering the interplay between free cash flow (FCF), coordination costs and managerial opportunism at various levels of UD.1 The interaction of these factors is overarching because they bring out managerial implications of UD management, the financial positions of UD and the challenges posed by the structure of the UD to corroborate why existing relationship between UD and financial performance may be inconsistent.

First, this conceptual argument begins by looking at the strength of UD strategy which is the internal capital market and how this internal capital market thrives on FCF. Internal capital market serves as a means of allocating funds from profitable or cash-rich business units to those with growth opportunities or in need of additional resources. In the context of the internal capital market, FCF serves as a source of funds that can be allocated to different business units based on their needs and growth opportunities. Consequently, we point out that FCF allows management to invest in projects expected to have highest potential returns which is a positive indicator. However, when agency opportunism arises, unrelated diversified firms may fail to maximize the overall value of the firm, in what is termed as agency cost of free cash.

Second, we conceptually show that the realization of the amount of this FCF depends on the coordination costs of the UD. These coordination costs typically emanate from the coordination requirements which vary at different levels of UD and can lead to different UD performance outcomes.

Third, based on the preceding considerations, we will conceptually suggest the general relationship between UD and financial performance to be S-shaped by considering three levels of UD to show how the performance of UD differ based on the specific factors and managerial response to FCF at each stage/level of the UD.

In doing so, this study contributes to knowledge in three main ways. First, it offers comprehensive insight into the effects of FCF on unrelated diversified firms, further indicating that moderate levels of UD are most beneficial for firms. Second, this study suggests that a firm should equally be concerned about an incoming danger of inefficient investment or misuse of funds when FCF is generated. Third, the study indicated that optimum benefits of FCF are realized by adhering to modalities to control agency opportunism. These contributions inadvertently determine the performance outcome of UD.

The study is organized in the following order. The second section elaborates the nature of UD, the role of FCF and mechanisms that facilitate inefficient use of FCF. This section also focusses on the emergence of the coordination cost and its significant influence on FCF. The third section focuses on how FCF and coordination cost interplay to yield different performance effects at different stages of UD. The fourth section offers possible control measures that could be applied to moderate agency effects around FCF. The fifth section covers the summary and conclusion of the study.

The Nature of UD and the Role of Free Cash Flow

UD occurs when an organization enters an entirely different business where there is no direct link with the company’s core business unit (Ljubownikow & Ang, 2020; Ng, 2007). There has been academic debate about how to precisely define UD. Literature on multi-businesses has generally taken a rigid view by only looking at those situations in which one corporation has multiple business groups that operate completely independently from each other. However, this study also highlights that aspect of UD that emphasizes the presence of managerial coordination and common ownership across divisions (Kock & Guillen, 2001). In this study, we will adhere to this latter line of argumentation, thus accepting that UD oftentimes requires the presence of common managerial and ownership ties. These managerial and ownership ties are often linked together by an interest in a central financial pool requiring coordination abilities (Guillen, 2000; Kock & Guillen, 2001).

Because UD comprises entirely different and uncorrelated business units, sharing common physical resources across different segments is severely limited, indicating limited ability to obtain synergistic benefits. So, an avenue to create a form of synergy may be important to overcome this limitation within the UD organizations (Hill & Hoskisson, 1987). To bridge this synergistic gap, UD firms tend to utilize financial resources across various segments of the UD organization for this purpose. The logic is that cash resource is flexible enough to provide UD firms a common benefit like that gained by matched portfolios of related diversified firms within the scope of resource complementarity and substitutability (D’Oria et al., 2021; Hill & Hoskisson, 1987; Park & Jang, 2013).

In the light of this, cash flows have been central common resource, which is managed and allocated by corporate managers. However, it is important to note that, during the operations of the organization, the firm may create cash flows that exceed what is required to pay for operational expenses and capital expenditure especially in times when firms make abnormal profit. This excess cash flow is important for UD firms because it introduces challenges to the organization due to greater latitude of manager’s discretion around its use (Ang et al., 2000). As a result, it is important to look at FCF as its presence is important to realizing the benefits of UD.

The role of FCF2 is valuable within UD organizations because it is liquid in nature and can be applied across all segments of unrelated diversified segments, a role that many physical resources cannot fulfil. The liquidity of FCFs makes FCF a substitutable and/or complementary resource across different business units, even those that operate differently. Hill and Hoskisson (1987) have confirmed this assertion, showing that unrelated diversified firms rarely utilize similar physical resources, R&D and common production knowledge across segments because these business segments cannot easily adapt to resources from other business units. FCF increases the potential of unrelated diversified firms to benefit from transfer and utilization of a common cash resource across segments (Palepu, 1985).

The emergence of FCF promotes a well-functioning internal capital market of an unrelated diversified firm (Khanna & Palepu, 1999; Scharfstein & Stein, 2000). In multi-business strategy, this common utilization of FCF across business units via internal capital market is generally termed cross-financing (Stiroh & Rumble, 2006). The potential to cross finance becomes valuable where there is high information asymmetry within the external capital financing domain and financial constraints (Cline et al., 2014). The initial intent of cross-financing is to allocate limited capital resources to profitable divisions to avoid situations where viable investment may be rejected due to high cost of external financing, thus serving as an alternative financial source for UD firms (Shenoy, 2021; Stein, 2003). The internal capital market theory asserts that the leverage to cross finance provides headquarters valuable flexibility to reallocate funds from less desirable segments to more desirable ones (Khanna & Tice, 2001; Stein, 1997). In addition, where external capital becomes expensive to access, an organization can benefit adequately from its internal capital base to cross finance viable investment (Kuppuswamy & Villalonga, 2016). Similarly, viable investment opportunities which may not attract funding from the external capital market can be financed internally to get the expected benefits (Matvos et al., 2018; Stein, 1997; Williamson 1975). Thus, FCF provides positive performance position for the functioning of the internal capital market.

However, scholars have noted managerial issues with the effective functioning of the internal capital market which tend to undermine the usefulness of FCFs. Previous literature suggests that cross-financing may destroy firm value rather than that which enhances it (Rajan et al., 2000) due to agency complications that trigger wasteful use of FCFs (Jensen, 1986). Agency theory defines an organizational pattern where shareholders delegate corporate decision-making to hired managers (Fama & Jensen, 1983). Often shareholders are primarily interested in their financial returns, whereas managers are more focused on their career prospects (Fama & Jensen, 1983; Katti & Raithatha, 2018). Therefore, managers may embark on the tradition of managerial capitalism, where corporate decisions tend to benefit them instead of their shareholders (Jensen & Meckling, 1976; Na, 2016). Based on these agency complications, cross-financing carried out at the discretion of corporate managers may not always benefit shareholders. For example, connection between divisional managers and CEOs as well as corporate favouritism can outweigh formal influence which tends to limit the impact of efficient capital allocation to segments (Duchin & Sosyura, 2013). Further, within the context of cross-financing, discretionary power of corporate managers provides means to elude external monitoring from actors of external market paving way for inefficient capital allocation, hence poor financial performance (Lang & Stulz, 1993; Rajan et al., 2000). In this perspective, FCF can be a disservice to UD leading to low performance.

Agency cost is usually high where managers amass excessive powers within the organization to make suboptimal choices (Duchin & Sosyura, 2013). This occurs where ownership concentration is low with lower oversight responsibilities, therewith allowing managers to engage in more self-serving behaviour (Chari et al., 2019). Where this agency cost is high, it creates inefficiency of the internal capital market through a suboptimal utilization of the FCF (Aggarwal & Samwick, 2003). In this context, inefficiency pertains to financial decisions where managers of FCF engage in wasteful expenditures, usually feasible due to agency complications (Chari et al., 2019) and capital market imperfection (Hubbard, 1998, 2001). Considering how agency problems can disrupt value maximization of FCFs during financial allocation, it is important to recognize that this agency disruption can lessen performance. This performance reduction may occur via the mode of utilization of FCF, as well as inefficiencies surrounding processes leading to the accumulation of FCF (Oded, 2020; Stellian & Danna-Buitrago, 2019).

The above considerations can conceptually point out that the role of FCF within the UD organization can be both negative and positive. However, what has not been fully recognized to date is that the potential for these negatives and positives will depend on the level of UD, as the amount of FCF will vary with coordination cost and agency opportunistic behaviour at each level of UD. Given these interrelationships, this study conceptually suggests that benefits from FCF will conceptually create a horizontal S-shaped link between UD and firm performance.

Emergence of Coordination Cost

The role of a central financial pool for UD firms with FCF creates significant challenges for organizations. This is in respect of how they coordinate a range of different functions across variety of business units on how to efficiently allocate this free cash resource from the central financial pool. Literature on UD suggests that success of UD largely depends on how to efficiently coordinate its segment’s financial activities regarding the intra firm capital allocation, i.e., redistribution of FCF (Duchin & Sosyura, 2013). This makes coordination function inevitable for UD firms despite being separate business units (Gulati & Singh, 1998; Jones & Hills, 1988). In this perspective, coordination costs can be described as costs incurred by diversified firms while managing task relating to financial interdependencies of UD firms (Rawley, 2010; Zhou, 2011). These costs are important because they influence the profit function of the diversified firm. As part of coordination functions, headquarters strategically intervene in the activities of segments to apply key changes in the operating procedures of the business units (Aggarwal & Samwick, 2003). These interventions are generally meant to coordinate activities to facilitate efficiency in capital allocation and joint planning of the miniature internal capital market to enhance disciplinary financial roles of redistributing resources across segments (Aggarwal & Samwick, 2003).

To successfully coordinate linkages of common financial resources within firms, it is imperative to recognize that such coordination function is not frictionless as it may require reformulation of existing formalized routines and practices (Kaplan & Henderson, 2005). To the extent that change can be met with organizational rigidity and other bureaucratic barriers triggered by agency costs (Amihud & Levi, 1981; Shleifer & Vishny, 1989), coordination may eventually be difficult and complex leading to higher coordination costs (Rawley, 2010).

Further, the push to establish new segments where FCF is accumulated can increase coordination burden (Rawley, 2010). Because these new establishment are not correlated with existing corporate functions, a considerable coordination burden is expected due to unfamiliarity in the new business domain which may in turn increase coordination cost (Rumelt, 1982; Sorenson et al., 2006).

Additionally, coordination costs of UD are driven by the need to process information and communication, joint planning and effective decision-making (Im et al., 2013). During allocation decisions, corporate headquarters may cross-subsidize wrongly in non-performing segments given the possibility that segment managers may withhold key information (Aggarwal & Samwick, 2003). These decision constraints, and the possibility of making value reducing allocation, requires information processing and joint planning which tends to increase cost of coordination (Cottrell & Nault, 2004).

As cost component minimizes available cash flow, this study uses coordination cost as a determinant of the amount of cash flow expected to be available for a firm. The coordination requirements and associated costs will vary at different levels of UD. As a result of varying coordination costs, the amount of available FCFs will vary, such that where coordination cost is high, free cost decreases and vice versa. This (increase/decrease) in FCF in turn determines the amount of agency cost leading to different UD-performance link at various levels of UD.

Agency Cost and Coordination Cost

Coordination function becomes inevitable for unrelated diversified firms because of separate business units that perform functions under a single corporate umbrella (Gulati & Singh, 1998; Jones & Hills, 1988). However, organizational rigidity and other bureaucratic barriers triggered by agency reasons (Amihud & Lev, 1981; Shleifer & Vishny, 1991) hinder the coordination processes, which eventually makes coordination difficult leading to higher coordination costs (Rawley, 2010). Consequently, where agency complication is high, associated rigidity and bureaucratic barriers tend to increase coordination cost burden of the unrelated diversified firm.

Performance Implication at Various Levels of UD

Based on the above considerations, this study describes performance implication of unrelated diversified firms at low, moderate and high levels on the basis of the interactions of FCF and coordination cost of UD, while applying agency cost of FCF across these three levels.

Low Level

The dispersion of segments determines the level of coordination requirements of a UD firm which may in turn influence the amount of coordination cost to incur (Chen et al., 2017). Hashai (2015) have shown that segment activities at low levels are not extensive and, therefore, very simple to coordinate leading to a lower coordination cost (Hashai, 2015). A significant feature of this coordination cost is its potential to increase the cost component of a UD firm (Rawley, 2010). Stellian and Danna-Buitrago (2019) have shown that firms that have higher cost component of their operations achieve less FCF, an indication of an inverse relationship between FCF and cost elements of a firm. At low level of UD where firms are characterized by lesser number of segments, lesser coordination requirements and low coordination cost, the potential to create FCF is expected to be high.

Agency cost argument on FCF however states that, where there are FCFs, a firm’s performance may be below due to possible misuse of FCF (Richardson, 2006). For example, Chen et al. (2016) have shown that overinvestment which is common in the presence of FCF tends to reduce performance. Biddle et al. (2009) have established a positive association between FCF and overinvestment in both negative and positive net present value projects. According to agency theory, the main reason for investment inefficiency centres on the private gains of managers to create large corporate empires for job security (Duchin & Sosyura, 2013). Consequently, at low levels where FCF is high, firms can encounter misuse of funds which lessens the benefits in the use of FCF (Jensen, 1986; Richardson, 2006) as corporate managers are attracted to push for larger, unprofitable and inefficient investments (Titman et al., 2003).

Taken together, this study builds three key ideas regarding low levels of UD. First, the number of segments (size) of unrelated activities is few, whereby coordination demands tend to be low and lead to a low cost of coordination. Second, low coordination cost further serves as cost cut, which in turn releases FCF. Third, as FCF is generated, the expected benefits from FCF are mitigated by agency costs factors, which in turn limit benefits of FCF, and this may reduce the performance of the firm.

Moderate Level of UD

Excess capacity hypothesis supports the notion that when firms attain equilibrium capacity, marginal resource requirements and capacity to utilize them reach a stable state (Di Carlo, 2020). Regarding cash flows, UD organizations at moderate levels reach a point where available financial resources and financial demand may be of the same magnitude. The implication of this market condition is that firms are unlikely to create any form of financial redundancy and hence limited potential to declare FCF (Stellian & Danna-Buitrago, 2019). The absence of FCF eradicates managerial opportunism and inefficiencies in overinvestment as contended by agency cost of FCF (Chen et al., 2016).

Further, this capacity alignment also supports the idea that at moderate levels of UD, there is equal capacity of management to coordinate an organization’s coordination requirements. This justifies that a firm’s coordination demand is equivalent to management’s coordinating capacity and hence little or no coordination complexity is expected. Consequently, the effect of coordination cost determining the amount of FCF is dissipates at moderate levels of related diversification.

The striking question is how the UD firms improve performance given the absence of FCF at this stage? When organizations reach moderate levels of UD, the impact of agency cost/complications on the use of financial resources reduces because managers are forced to identify viable investments and appropriate resource mix (Zahavi & Lavie, 2013). The logic is that closeness in the gap between liquidity requirements and availability limits the latitude of agents discretionary. This tight financial position may limit variations in investment, capital adjustment cost and cross-equity financing among segments (Bakke & Gu, 2017). Additionally, at the moderate level of UD, conglomerates can reach a stable state where divisions operate almost independently on their segment cash flows, thereby limiting large internal allocations of resources (Bakke & Gu, 2017). An implication for this reduction in allocation of funds across segments is a subversion of agency intricacies within unrelated diversified corporations (Duchin & Sosyura, 2013). Subsequently, cross-financing within the internal capital market becomes efficient, as cross-subsidization is rarely implemented (Lamont & Polk, 2002).

In sum, at moderate level of UD, a diversified entity is expected to be better off than low level as coordination cost effect dissipates due to management’s coordination capacity–coordination demand alignment, a situation that potentially limits redundancy (Duchin, 2010). Management attention is not dispersed by the effect of size and number of segments (Vermeulen & Barkema, 2002). There is also capacity and resource alignment which removes formation of FCF and its associated agency cost which invokes agency opportunism and inefficient investment of funds (Chen et al., 2016). As a result, the performance of UD is expected to be high at this stage.

High Level of UD

Our conceptual theorization regarding low levels and medium levels of UD strategy is based on the notion that high coordination cost reduces the accumulation of FCF. This means that high coordination cost from extremely extensive UD puts strain on cash level and creates low or no FCF. However, from moderate to high level of UD, non-performing assets are common as capacity of assets reaches the point of diminishing return to scale (Brue, 1993; Markides & Williamson, 1996). The emergence of non-yielding assets potentially triggers the decision to withhold further investment decisions in existing projects with low productivity assets (Almeida et al., 2004; Machokoto & Areneke, 2021; Riddick & Whited, 2009), leading to creation of FCF (Oded, 2020; Stellian & Danna-Buitrago, 2019). Also, firms at this stage are usually rigid as they are usually old (Loderer et al., 2017). As free cash is accumulated, Jensen (1986) and Kothari et al. (2009) have predicted negative agency effects around FCF, which accordingly decreases UD’s financial performance at high level of UD.

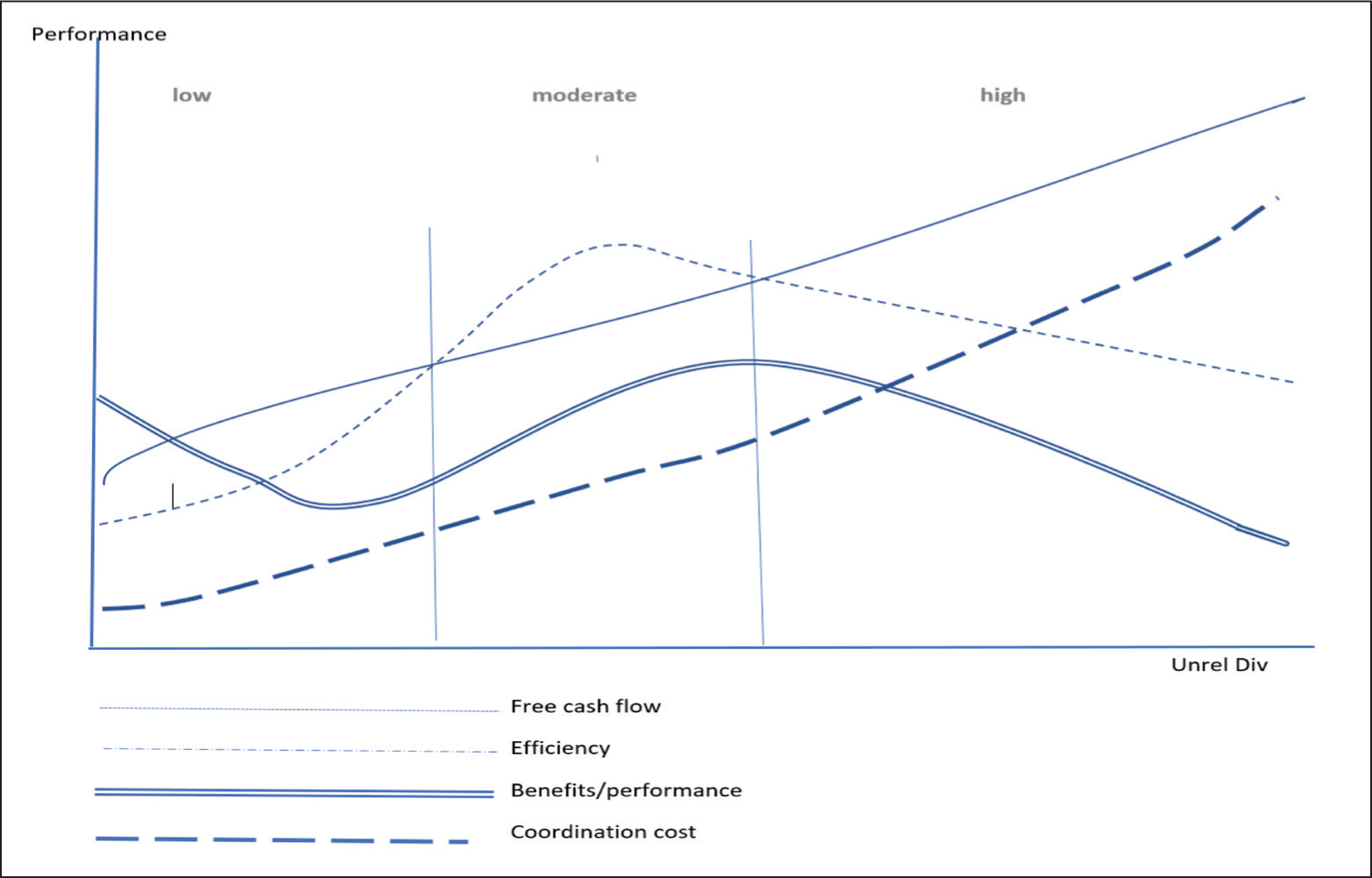

The logic of this study has been graphically shown in Figure 1 to show how the selected variables interact to create the performance effects at different levels of UD. The performance curve shows a horizontal S-shaped relationship which reflects the work of Hashai (2015) within industry diversification and Lu and Beamish (2004) regarding multinational international diversification.

Our graph indicates low-level efficiency at both low level and high levels of UD. This is demonstrating that UD at both low and high levels have limitations with regards to efficiency, hence the declining performance curve at both levels. However, the efficiency curve attains its peak at moderate levels of UD, an indication that resources in terms of cash flows can be meticulously utilized to enhance firm performance. Even though FCF curve tend to rise a bit at moderate level, corresponding high efficiency subverts the possible inefficient use of this FCF, hence the rising performance curve.

Further, in both low and high levels of UD, Figure 1 indicates low coordination costs and higher FCFs; however, a key limitation at both stages is that efficiency is below FCFs, an indication that free cash flow may be suboptimized due to this limited efficiency. Correspondingly, coordination cost curve is below FCF at high and low level of UD, suggesting that a cash is freed at low level and high level. Our logic is that this FCF which lies below the efficiency curve attracts inefficient investment according to principles of agency cost of FCF.

Even though coordination costs keep rising at moderate levels given the increase in level of UD from low to medium, the presence of high efficiency which reflects an efficient use of free cash implies that UD firms at moderate stages benefit from FCF. Similarly, higher efficiency curve implies that FCF can be absorbed optimally, thereby limiting agency misuse of FCFs. Consequently, our performance curve of UD at moderate level rises to show an improvement in UD at moderate levels. Thus far, Figure 1 is a graphical representation of the interactions of factors that form the S-shaped relationship between UD and performance.

Summary and Conclusion

Fundamentally, this study purports that low coordination costs enable cash accumulation leading to FCF. Our framework shows that the accumulation of FCF may not be beneficial to the firm for two significant reasons. First, we refer to the agency cost of FCF to corroborate this assertion by referring to several findings of positive relationship between FCF and overinvestment in bad projects by corporate managers (Chari et al., 2019). Second, this study uses the excess capacity hypothesis to contend that accumulation of FCF possibly signifies inefficiency on the part of the firm at each stage as FCF is considered as redundant resource of the firm. Operating full capacity (optimization) means corporate resources are fully engaged, and excesses (resource redundancy) can be associated with firm’s inability to put available resource to use. This can create severe penalties due to possible backlog of unutilized resources (Cruz et al., 2018; Häckel et al., 2020; Manne, 1961).

Low levels of UD are not extensive in nature (low number of segments); hence, they have less coordination demand, less coordination costs and more FCFs, hence low performance. At moderate levels of UD, this study theorizes that firm performance increases. Moderate levels of UD fulfil the tenets of the excess capacity hypothesis where UD firms operate at optimum capacity, practically devoid of organizational slack, that allows them to match resource demand and resource availability at equilibrium. By extension, FCF accumulation is technically not feasible. High levels of UD are characterized by their extensive and diverse nature, creating high coordination demands on unrelated diversified firms which are bound to reduce FCF. However, this study argues that at high levels of UD strategy, firms cut down investment because of diminishing returns on assets and corporate rigidity, which subsequently accumulate FCF. As FCF is formed, managerial discretion and the attendant self-serving tendency on FCF then follow, therewith reduce firm value.

In the build up to this conceptual study, we relaxed the assumption of loose constellation of business units held together by informal control ties (Ghemawat & Khanna, 1998; Guillen, 2000), since the concept of diversification requires the presence of managerial coordination and ownership ties (Guillen, 2000; Kock & Guillen, 2001). This article focused on limitations of UD studies on UD corporations that fail to differentiate the comparative benefits regarding independent firms and UD firms (Khanna & Palepu, 1999). Further, the relevance of this conceptual paper may be strongly applied in the context of emerging markets, where the formation of business segments and groups in unrelated areas are suitable for augmenting incomplete markets and weak institutional environments and where external capital markets are expensive (Purkayastha et al., 2012; Ramaswamy et al., 2018), and agency effects within organizations are prominent (Khanna & Palepu, 1999).

Suggested Future Research

In this study, the modelled conceptual framework provides a unique explanation regarding UD and performance link using FCF and coordination costs. This study systematically provides a stance to contend that coordination costs and FCF jointly influence performance differently according to a corporation’s level of UD. This study finally conceptualizes that performance is low at low levels, high at moderate levels and then declines again at high levels, supporting an S-shaped diversification-performance link. Similarly, Lu and Beamish (2004) and Hashai (2015) have shown S-shaped diversification performance links but used different conceptual characteristics for diversification. Hashai (2015) has applied industry diversification, while Lu and Beamish have used geographical diversification, an indication that a linear relationship between diversification and performance generally appears to be an oversimplification of the concept, because many conceptual ideas and variables tend to impede the linear dependency approach of such a relationship.

Future research may be promising in empirically testing the conceptual implications made in this study using empirical data. Further, in this study, the debate on S-shaped relationships between UD and firm performance is generalized, notwithstanding differences in institutional differences and economic development of countries where this strategy may be implemented. Other studies could replicate this study by considering the impact of institutional development on agency and internal capital market in this S-shape relationship, as agency costs and internal capital markets appear to depend on the institutional development of a country.

This study is important as it offers practical insight to CEOs of firms embarking on UD to move beyond low levels of UD, because performance tends to increase beyond this stage but should be clear on the point of inflexion where the strategy begins to expand beyond moderate levels.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.