Abstract

The purpose of this study is to identify the challenges of preparing sustainability reporting (SR) and the reasons for non-disclosure. A systematic review was done from two major databases Scopus and Web of Science. Existing literature related to the managers’ perception of barriers in SR was considered for this study. Results show that lack of awareness and understanding of SR is a major barrier mentioned in most of the studies, followed by lesser perceived benefits compared to cost, scarcity of resources, lack of legal requirements, government initiatives, and data collection issues as common barriers manager’s face for sustainability disclosure. Most of the barriers in developed and developing countries are found to be similar, this may be due to relative newness in the concept of SR. The present study also emphasizes the research gaps in the extant literature that can be taken forward for a better understanding of the issues in SR and enhancing reporting quality.

Introduction

The Brundtland Report of the World Commission on Environment and Development defined the concept of sustainable development as meeting the needs of the present without compromising the ability of future generations to meet their needs. 1 Later in the year 1992, United Nations Conference on Environment and Development (UNCED) also known as Rio Conference or Earth Summit was held with the purpose to promote sustainable development globally. 2 Elucidated the term sustainability as Triple Bottom Line, that is, People, Planet, and Profit. “Sustainability Reporting” (SR) also known as “Environmental, Social, and Governance (ESG) Disclosures” or “Non-financial Reporting” has gained a lot of importance in the last two decades, as it satisfies the needs of all stakeholders which was not possible through traditional financial disclosures. The main focus of Traditional disclosures was to publish only financial information which mainly realizes the shareholders’ expectations. There is also substantial growth in the number of academic studies related to SR since 2000.3, 4 SR is an effective tool for companies to communicate their ESG aspects in the form of a report. It alleviates the information asymmetry and supports companies to have a healthy relationship with their stakeholders which is necessary for the long-term viability and success of the firm. 5 SR is based on non-financial factors but it has a financial impact on the company. They might impact access to capital, risk management, market access, human capital, reputation, employee engagement, and others. 6 High-quality sustainability reports on ESG issues help companies to measure their impact and identify targets. Global Reporting Initiative (GRI) has defined SR as the efforts of the firm in reporting their positive and negative contribution publicly to environmental, social, governance, and economic aspects and towards sustainable development. 7 SR is a pertinent concern for companies today, 8 as due to the advent of the internet and digital technologies data collection and processing have become much easier, less time-consuming, and cheaper. Thus, stakeholders are becoming more aware of the companies’ activities and gradually the demand for information in non-financial disclosures is increasing. The basic purpose of SR is to improve transparency between companies and their stakeholders for better assessment of firms, 9 as stakeholders can better evaluate firms’ risks and reliability through these reports. 10 SR helps companies in enhancing brand image, minimizing risks, competitive advantage, and favourable funding situations from credit institutions. 10 Apart from building corporate image and reputation, SR plays a crucial role in the implementation of the Sustainable Development Goals (SDGs).

The demand from investors and other stakeholders has led to substantial improvement in the sustainability reports. In the past few years, policymakers and regulators of various countries have accelerated their efforts to encourage SR. To facilitate and promote the SR, there are various reporting guidelines, standards, and frameworks such as GRI, Sustainability Accounting Standards Board (SASB), International Integrated Reporting Framework (IIRC), Carbon Disclosure Project (CDP), Climate Disclosure Standards Board (CDSB), United Nations Global Compact (UNGC). Recently in 2020, five leading global frameworks for SR 11 united together to make SR more comprehensive and to guide organizations on how these frameworks can be used in a complementary and additive manner. Stock exchanges, regulators, and policymakers have increased their efforts to promote SR practices in various countries. Around 80% of the companies in the world report on sustainability issues. 12 Institutional investors are also declaring their support for ESG issues and integrating them into investment decision-making. The world’s largest asset manager BlackRock asked the companies to disclose information on the recommendation of the Task Force on Climate-related Financial Disclosures (TCFD) and SASB to cover a broader set of material sustainability issues and declared that sustainability would be their new standard for investing. 13 CEO of BlackRock Larry Fink in his annual letter to the CEO asked companies to disclose their plan about how their companies will be compatible in the world of net-zero greenhouse gas emissions. They urged companies to produce better sustainability disclosures rather than waiting for the regulators to make it mandatory. 14

There are two schools of thought when it comes to the significance of SR. According to one viewpoint, companies disclose information regarding their sustainability efforts in these reports that reflects their sustainability performance. Another conflicting viewpoint is that companies do not put genuine efforts toward sustainability and instead rely on sustainability reports to influence the stakeholders’ perception, resulting in “greenwashing.”

15

In recent years, reporting on sustainability issues has become accountable to the companies. Companies find it difficult to aggregate data required for producing SR,16, 17 deciding which issues are material, and measuring the effectiveness of the report. Multiple Sustainability Standards and frameworks also make it hard for the companies to decide which framework to follow for reporting. Corporate Social Reporting Studies can be classified into three categories, that is (a) scope and level of CSR and its determinants, (b) Manager’s perception studies, and (c) other stakeholders’ perception studies.

18

Thus, there are two types of studies on SR, either based on content analysis to determine the extent of SR8, 19 or perception-based studies20–23 through questionnaires or interviews to understand the perception of managers and other stakeholders towards SR. Review studies are there on SR,

18

its determinants,4, 24 and drivers and motivations.

3

As per the author’s knowledge, no existing study combines and analyses the studies related to the challenges faced by managers and preparers in preparing SR and the reasons why companies avoid providing sustainability reports. We add to the existing literature by answering the following research question:

RQ1: What are the challenges of preparing sustainability reports and how they can be mitigated?

The study builds on the extant literature of managers’ perceptions of the challenges faced in producing SR and the reasons why companies are reluctant to produce SR. Studies from both the developed and developing countries are assessed to identify the major challenges and possible measures that can be implemented to promote the SR. Based on the level of control companies have over the issues, the challenges identified from the literature are further divided into two categories: internal and external barriers. Subsequently, the existing literature is summarized to identify gaps and propose future research agendas. Finding from the study shows that lack of understanding and awareness is the most common internal challenge that the managers encounter as a barrier to SR. This barrier leads to other negative perceptions that managers have such as reluctance to provide information, no impact of SR on performance, and confusion between focusing on short-term gains or long-term profitability. Another major barrier that is external to the company is the lack of mandatory requirements and less stakeholder readership. Government initiatives also play an important role in encouraging companies for publishing sustainability reports. This study includes literature from both developed and developing countries, results indicate that the managers of both developed and developing economies are facing almost similar challenges while reporting sustainability data, due to the relative newness of the SR concept. 25

Research Methodology

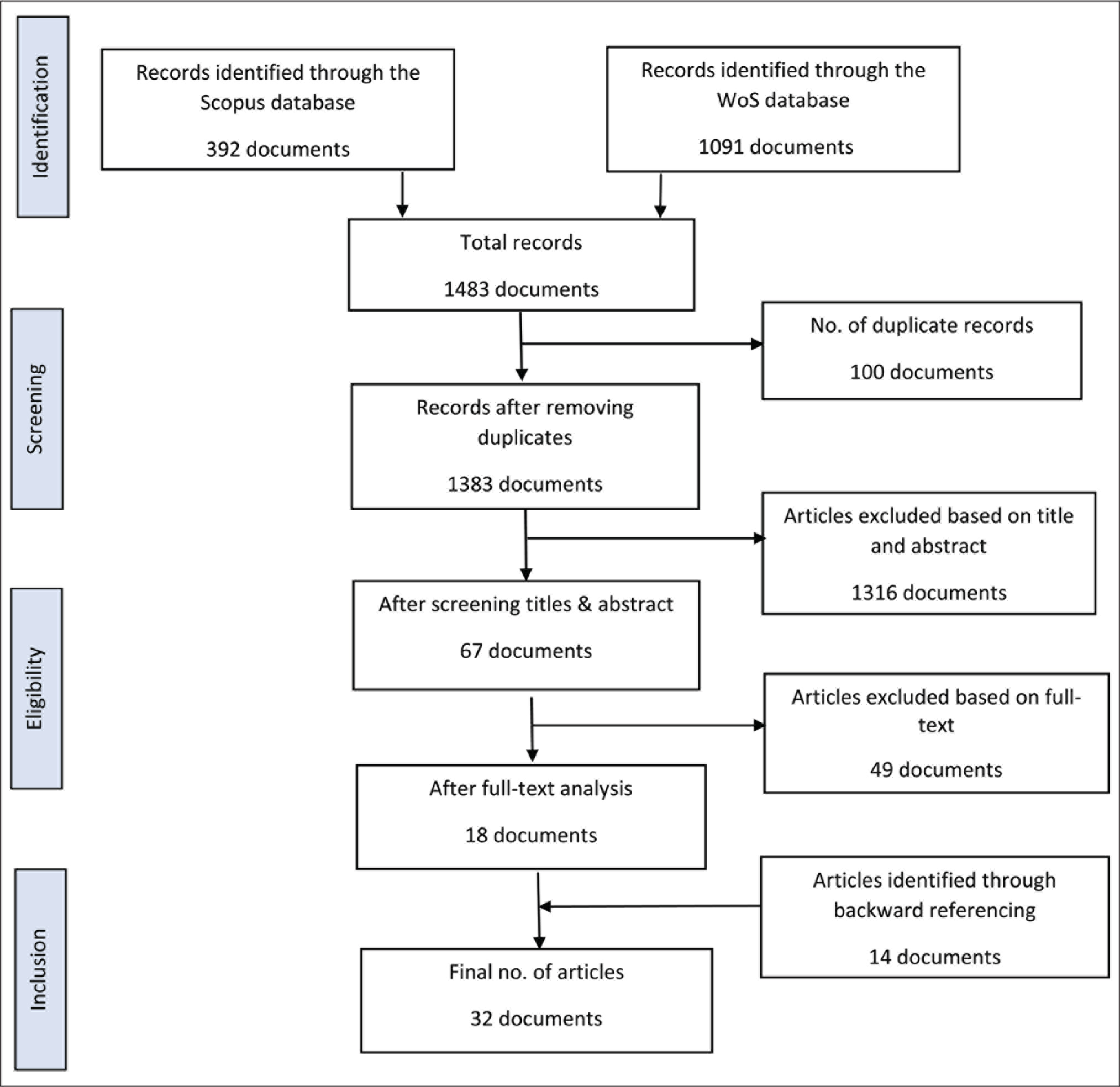

To obtain relevant research papers on the challenges of SR published in academic journals, a systematic review was conducted. Two major databases Elsevier Scopus and Clarivate Analytics Web of Science were used in the study. Both databases are among the most comprehensive electronic databases for obtaining literature, covering all important international publications. The study searched for combinations of various related keywords such as “sustainability report*.” “Integrated report*,” “report*,” “environmental report*,” “social report*,” “non-financial report*,” “challenges,” “barriers,” “impediments,” and “perception” for literature search. The expression “report*” was used to cover all the documents both with keyword report and reporting. Subject categories in Scopus databases are limited to “Business, Management, and Accounting” and “Economics, Econometrics, and Finance” and three subject categories were selected in WoS, namely “Management,” “Business,” and “Business Finance.” Further, documents published in the English language were considered for the study. Figure 1 provides an overview of the flow of methodology. Initially, data of 392 documents and 1092 documents from Scopus and Web of Science respectively were retrieved on 18 January 2022. Subsequently, documents were filtered based on the title, abstract and full-text screening. The documents after the full-text screening were excluded due to the following reasons: studies based on content analysis, stakeholder’s perception, motivation aspect only, implementation challenges of sustainability, and perception towards CSR practices. Further, backward referencing was used to identify more documents related to the study. This review study incorporates the research articles (both qualitative and quantitative) that discuss the challenges of SR from the manager’s perception. A total of 32 articles were finally considered for the detailed review. Relevant data related to barriers were extracted from papers as per the requirement of the study.

Challenges of Sustainability Reporting

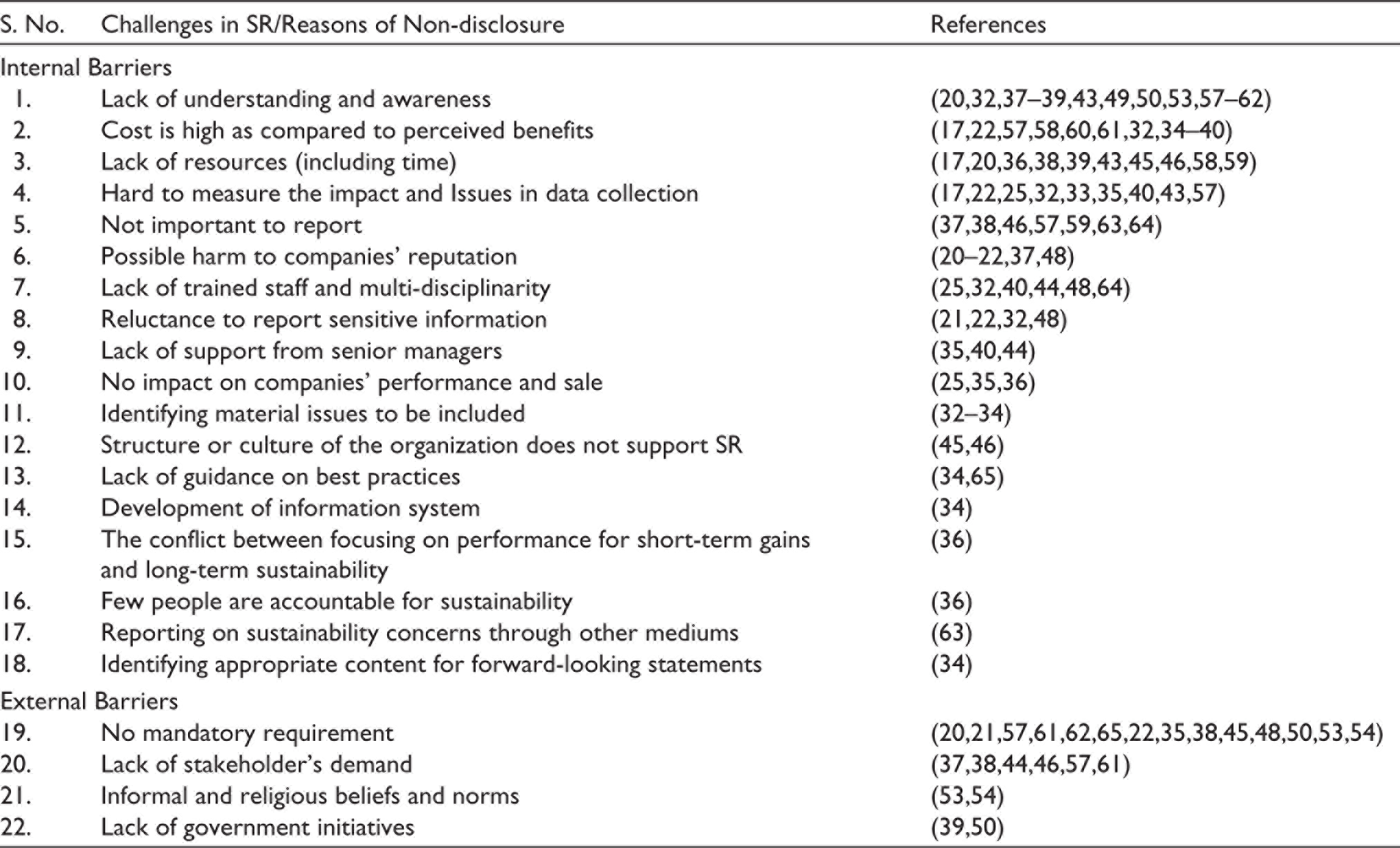

Disclosing information on Sustainable issues has numerous benefits for the company such as it makes the company more transparent, 17 enhances corporate reputation,22, 26, 27 stakeholders get information from authentic sources which prevent them from believing in false information, 28 and many others. There are two different perceptions of SR, the first perception considers SR as a standard practice of disclosure to follow the global norms while in the other perception SR is regarded as a tool for corporate communication to enhance companies’ reputation and image among local stakeholders. 17 Many companies consider sustainability disclosures as an attempt to legitimize their corporate behaviour.8, 17, 22, 29 To enhance the extensiveness, quality, quantity, and comprehensiveness of the reports, it is, therefore, essential to identify the reasons for non-disclosure. 30 Issues need to be recognized and addressed that prevent organizations from making disclosures on Sustainability issues. This is important to frame policies and adapt practices to promote SR.22, 31 Table 1 shows the summary of some common barriers the managers experience in preparing SR and the reasons why companies avoid providing a dedicated report for disclosing information on sustainability issues.

Summary of Some Common Barriers

Internal Barriers

Internal barriers are those that can be influenced by the firm, a company can work upon these barriers to overcome the challenges of SR. It is apparent from Table 1 that the lack of awareness and knowledge is the most common barrier which was highlighted in the majority of the studies. Managers that are involved in the process of SR are not well aware of the guidelines and standards that are to be followed and critical issues that need to be addressed in preparing sustainability reports.32–34 The lack of understanding is also one of the major reasons for the negative perception of managers toward SR and their fear of disclosing information in reports. They perceive that the report on the social and environmental issues that are prepared by the company has little or no impact on the share price and the overall performance of the company25, 35, 36 and also the information disclosed might affect the reputation of the company.21, 22, 32 The conflict between focusing on short-term profits or attaining long-term goals of sustainability is also the result of the lack of knowledge among the SR preparers. Managers perceive that SR does not have any positive impact on the companies’ performance35, 36 and considered it as not an important practice,37, 38 because of their focus on the short-term gains rather than long-term benefits. 36 Thus, the lack of awareness and knowledge of SR among managers is a major reason for the many other barriers they encounter. Therefore, it is important to educate and train managers about the importance of SR to motivate them and improve the quality of data reported. Awareness programmes should be organized by the standard setters and the government to increase awareness about the tangible benefits of the SR to reduce the managers’ aversion to reporting on sustainable issues. However, understanding and engaging in SR may take some time for all employees, especially when there is a high turnover of employees in the organization as the entire process of familiarization will be started from scratch. 39

There is a belief among businesses that the cost of preparing the SR outweighs the benefits and it takes a lot of time and efforts of managers involved in the process due to which companies inhibit the allocation of limited resources of the business for SR.39, 40 Lack of resources (both personnel and time resources) is another major cause of non-disclosure. The process of SR is time-consuming, this issue further increases when there is a shortage of skilled staff. Providing training to the staff and having a dedicated team for the SR process will reduce the time and may enhance the quality of sustainability reports. Identifying the material issues to be reported is another pertinent barrier in preparing SR.32, 33 The concept of materiality in SR is vague as the users of SR are more heterogeneous than in financial reporting. 41 Companies struggle to identify the issues that are essential for preparing the reports. 41 They fail to conduct materiality analysis appropriately and misuse it to decide the content of the report without considering the interests of the diverse stakeholders’ groups. 42 The material issues can be determined with the use of international standards such as GRI, SASB, and IIRC that are largely followed by different industries to incorporate all the material issues related to a specific industry. Further, companies should conduct rigorous materiality analysis to determine significant issues that are critical for the company and also fulfil the information needs of the diverse stakeholder group. Additionally, companies should also focus on the reporting aspect of the material issues apart from identifying the material stakeholder groups and topics to enhance stakeholder engagement. 42

Measuring the environmental impact of the companies in the form of hard data and collecting credible data to be reported is another common barrier.17, 43 Few studies such as35, 40, 44 also highlight the lack of support from the top management as another impediment to reporting. The senior managers doubt the benefits of reporting on sustainable issues and act as “wet blankets.” 40 A study on MNCs having subsidiaries in Sri Lanka 45 specified that structures and processes also caused internal barriers for the companies. Companies consider sustainability as part of their culture but do not feel the need to report it in a form of a dedicated report. 46

The most significant implementation challenge as highlighted by Steyn 34 is selecting appropriate content for the forward-looking statements in a study of South African listed companies. Three key factors have been identified by Al-Shaer, Albitar, and Hussainey 47 that determine the content of SR; first, external governance-related factors, which comprise voluntary assurance of SR, selection of assurance provider; second, internal governance factors, that is, the presence of CSR and sustainability committee, board characteristics; third, reporting behaviour of the companies that include the choice of international standards and quality of reporting. Companies try to provide suitable content to the report users without jeopardizing business confidentiality. Companies are afraid to provide any sensitive information in the reports,21, 48 as it might harm the reputation of the companies and can be misused by the competitors. 22 A case study of four Indian companies 49 indicated that managers perceive that Integrated Reporting may lead to inconsistency among the annual reports. These internal barriers to SR in companies can be curtailed by increasing awareness among companies and managers regarding the benefits of SR and further training employees for preparing sustainability reports.

External Barriers

External barriers are those that are beyond the company’s control yet affect the quality of sustainability disclosures. These challenges may be due to the regulatory environment, social and religious norms, stakeholders, and others. The most common external barrier is the lack of legal and mandatory requirements which is highlighted in most of the studies,21, 45, 50 especially in developing countries. Apart from the absence of legal requirements, the lack of government initiatives also acts as a hindrance39, 50 for the companies that are publishing sustainability reports. Government should take steps to provide incentives and educate managers about sustainability issues to encourage them for SR. Although in recent years there is a rise in SR in developing nations, they still lag behind developed ones. 31 Therefore, there is a need for the mandatory regulatory requirement for the sustainability disclosure to promote SR. The fact that there are so many sustainability standards and frameworks also makes it difficult for businesses to determine which one to use for reporting. While GRI is the most preferred framework for preparing sustainability reports 12 because of its uniformity, flexibility, and its emphasis on continuous improvement, 51 companies are also following other standards such are SASB, <IR>, TCFD, and CDSB for reporting. A large number of key performance indicators (KPIs) in a framework also pose a challenge for managers to select suitable KPIs for the reporting, especially for the companies operating in developing economies. 51 These international SR standards have also started banding together to improve clarity and create a comprehensive reporting framework. Another major reason is the lack of stakeholders’ demand for sustainability information. A low level of stakeholder readership does not motivate management to devote time and resources to prepare SR. 44 There is a need to raise awareness and educate stakeholders to make them aware of the significance of non-financial information in decision-making. Companies also need to identify the stakeholder groups that are striving to be heard and are involved in the decision-making of the companies. 52 Their recommendations should be considered seriously by the companies to enhance transparency and stakeholder engagement. Cultural and religious belief is a unique challenge that is being identified in the studies concerning Bangladesh.53, 54 A study on Bangladeshi MNC subsidiaries 53 highlighted that around 87% of interviewees agreed that CSR reporting could be considered negative as per Islamic beliefs as it does not allow self-presentation of good deeds. A person is accountable to God and philanthropic activities are aimed to satisfy God rather than any other individual or stakeholder. 54 In an opposed statement,55, 56 mentioned that the Islamic notion of accountability demands complete disclosure of information to all stakeholders, be it financial or non-financial information.

Discussion

Reporting on sustainability issues is one of the major challenges companies experience while implementing sustainability. 66 Table 1 shows the comprehensive list of internal and external barriers faced by SR preparers in various developed and developing countries. Out of 32 studies, around 15 studies used the interview method while another 15 studies used only a questionnaire survey for collecting data from the companies, and two studies39, 58 used both (survey and interview) methods of data collection. The sample size of the interview study was small as compared to questionnaire survey studies because it is more time-consuming and difficult to gather large data from interviews. Interviews can be more useful for such studies as researchers can get detailed and thorough data. Interviewers also might get to know new perceptions from the managers towards SR.

Country-specific environmental and social issues play a crucial role in Corporate SR practices.30, 54 Existing literature shows that most of the studies from developed countries found a lack of support from senior management, less expertise in SR, and more cost than incentives as major challenges.36, 37, 40, 44, 59 The biggest reason for less disclosure or non-disclosure in emerging economies is due to lack of legal obligation or mandatory requirement for SR.20, 21, 38, 50, 53, 54, 57 Lack of awareness/knowledge, lack of resources, and less expertise are found to be the other obstructions for SR in developing countries and a few developed countries. The purpose of SR practices in developing countries is different from those in developed countries, as socially sensitive issues such as poverty, child labour, and corruption are more relevant issues in emerging economies as compared to developed countries. 54 Research shows developing countries still lag behind developed countries in terms of SR. 31 Vives 58 and Moneva and Hernández-Pajares 59 studied SMEs in a combination of developed and developing countries and reported almost similar challenges of time and resource constraints, less awareness among managers, and a lack of interest from SMEs to legitimize their actions.

In a few developing countries, many corporate managers are not aware of GRI guidelines, 60 inexperienced managers and reporters do not understand the concept of sustainability completely and relate it with the concept of being just “green.” 44 Training and guidance are the prerequisites for corporate managers in developing countries to attain the required skills and awareness to commence with SR. They should be trained by professional firms and associations to enhance the quality of SR. 67 Necessary efforts are required from Sustainability Standard Setters, regulators, policymakers, and companies to spread awareness regarding the usage of international standards in SR. Many companies prefer not to disclose sensitive information or harmful environmental and social information in reports because of the fear of negative reactions from stakeholders.20–22, 37 Companies fear misinterpretation and avoid disclosing even positive information, this can be explained through the political economy of accounting. 20 Adams, Coutts, and Harte 29 used political economy to explain that companies refuse to disclose more information than required. Adams, Coutts, and Harte 2 mentioned that non-disclosure is an effective means of intervention and doubt when accounting reports fail to communicate information that is in the self-interest of the business. There is a need to educate employees to make them aware of SR practices and make them appreciate the advantages of SR. 67 Educating companies’ management might reduce their fear of misinterpretation. Apart from the managers, it is also important to educate stakeholders to make them aware of SR and its significance in decision-making. Another major barrier to SR is the lack of resources, be it financial or human resources. Corporate Managers view SR as costly and less beneficial for the company.22, 37–40, 61 Existing managers found difficulty in balancing SR roles apart from their existing work,40, 44 and a shortage of human resources in a company results in overburdened managers. Farooq and Villiers 44 indicated that delegating the responsibility of data collection and report drafting to content owners (below mid-level managers) will reduce the work of overburdened managers. Apart from these factors53, 54 also brings informal norms and religious beliefs as another reason for non-disclosure.

Recommendations for Future Studies

Results presented in the study reflect that the research on non-financial reporting has been ongoing for quite some time. The number of published articles related to the barriers has grown in the last few years. The critical evaluation of the available literature reveals some observations related to the impediments in preparing SR as well as potential areas for future research.

First, the majority of the reviewed articles have studied the negative aspects of SR from a manager’s perspective. A very few studies have studied positive determinants apart from the negative ones in their study.22, 28 There is a need to study the opportunities and the benefits that managers perceive from publishing SR.

Second, the impact of external drivers on SR is different for developed and developing nations. In the case of developed countries, some crucial external drivers motivate companies to publish sustainability reports such as increasing trend of ethical consumption while these external drivers are not that powerful in the case of developing countries 39 as there are more critical issues of poverty, inequality, corruption39, 54 that matter more than environmental and social concerns. Comparative studies concerning both developed and developing nations may provide better comprehensive outcomes. Further, nations differ from each other in terms of the political climate, environmental condition, and economic situation. 64 The majority of studies are focused on one country; cross-country studies can be done in the future to observe the impact of economic and political situations on the SR.

Third, the listed companies are more accountable to society and publishing non-financial information28, 68 as they are using public funds as compared to the unlisted firms. Public organizations follow GRI guidelines more frequently and are more likely to publish sustainability reports as compared to private firms. 69 Managers’ perception of publishing separate sustainability reports might be different in the case of listed firms. Therefore, a comparative study can be done between listed and unlisted companies. Similarly, comparisons can be made among the perception of government-owned, state-owned, and privately-owned organizations, MNCs, and national companies. Small and medium-sized enterprises (SMEs) have also started publishing sustainability reports in the last few years and are different from corporates as they have limited market reach and sources of revenue. Research studies exploring the perception of SMEs towards SR may provide new observations.

Fourth, all the studies are cross-sectional, which reflects the managers’ perception at a single point in time. A longitudinal study can be done to understand the change in perception of the managers towards SR over a period of time. Further, a case study approach can be adopted to get better insights into the sustainability practices of the companies. Perception of both managers and stakeholders towards specific companies’ sustainability reports can be studied to identify the gaps between the information that is provided by the companies and the information which stakeholders need. This can help the managers to understand better what information is important to report and how to report it.

Fifth, Method-wise, more than half of the studies used questionnaire surveys for studying managerial perception, only a few studies have considered both methods, that is, interviews and questionnaires.38, 39, 58 Both techniques of data collection have their own merits and demerits, thus, more future studies can be done using both techniques. Further, the focus group method can also be adopted for data collection for obtaining in-depth information.

Sixth, there is a dearth of studies concerning the perception of other stakeholders apart from managers towards SR. 17 Future studies may explore the perception of various other stakeholders, such as investors, assurers, analysts, employees, and customers to understand the views of recipients of the sustainability information.

Conclusion

SR reflects the sustainability performance of the companies. 15 The motivation and involvement of corporate managers and report preparers is a significant aspect of SR. This research extends prior reviews on sustainability by recognizing and classifying the challenges of SR based on existing studies of managerial perception. To attain this objective, published work related to the managerial perception of SR was retrieved from Scopus and WoS databases. The results indicate that lack of mandatory requirements is one of the major external barriers for the companies while lack of awareness and understanding of sustainability reports is a common internal barrier among companies. Due to the lack of mandatory regulatory requirements, companies seek to choose metrics that can be measured and disclosed easily and ignore the aspects that could present the darker side of the companies in terms of the sustainability initiatives. 70 Although SR practices vary according to the organization’s size, culture, and nation, 30 the extant literature does not show any major difference in the barriers faced by management in developing and developed countries. Literature from both countries has shown less knowledge and awareness, lack of resources and time, fear of negative publicity, difficulty in data collection, lack of mandatory requirements, and higher cost over benefits as significant challenges. This may be due to the relative newness in the concept of SR that both countries are facing similar kinds of barriers. 25 The research gaps and future research agenda reveal that more studies are needed in this aspect to understand the barriers faced by companies of different nations.

Implications of the Study

The study discusses the challenges that companies experience while preparing sustainability reports. Although there are multiple international standards and frameworks for promoting and increasing awareness about the benefits of SR. Companies are still apprehensive about revealing information on sustainability issues in reports. The present study indicates that there is a need for the proper training and awareness programme for managers to attain the requisite skills and positive attitude towards SR, leading to enhanced quality of reporting. Training of senior managers from professional firms will help the businesses to incorporate the SR culture in the system and convince them to consider SR as a value-added activity rather than a business impediment. 39 Apart from managers, stakeholders are also required to be educated and aware of the SR and its significance in their investment decision-making. This will further create stakeholder pressure on the companies to provide comprehensive and quality information in the sustainability reports. Policymakers especially in developing nations should make disclosure of SR a mandatory requirement to promote as it was found to be one of the key barriers in developing countries.45, 50 Additionally, countries and regulators may collaborate with international standards to enhance the regulatory framework for environmental and social concerns. Furthermore, incentives and rewards could be presented from the government to the companies with exemplary sustainability performance to promote the culture of SR.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Appendix

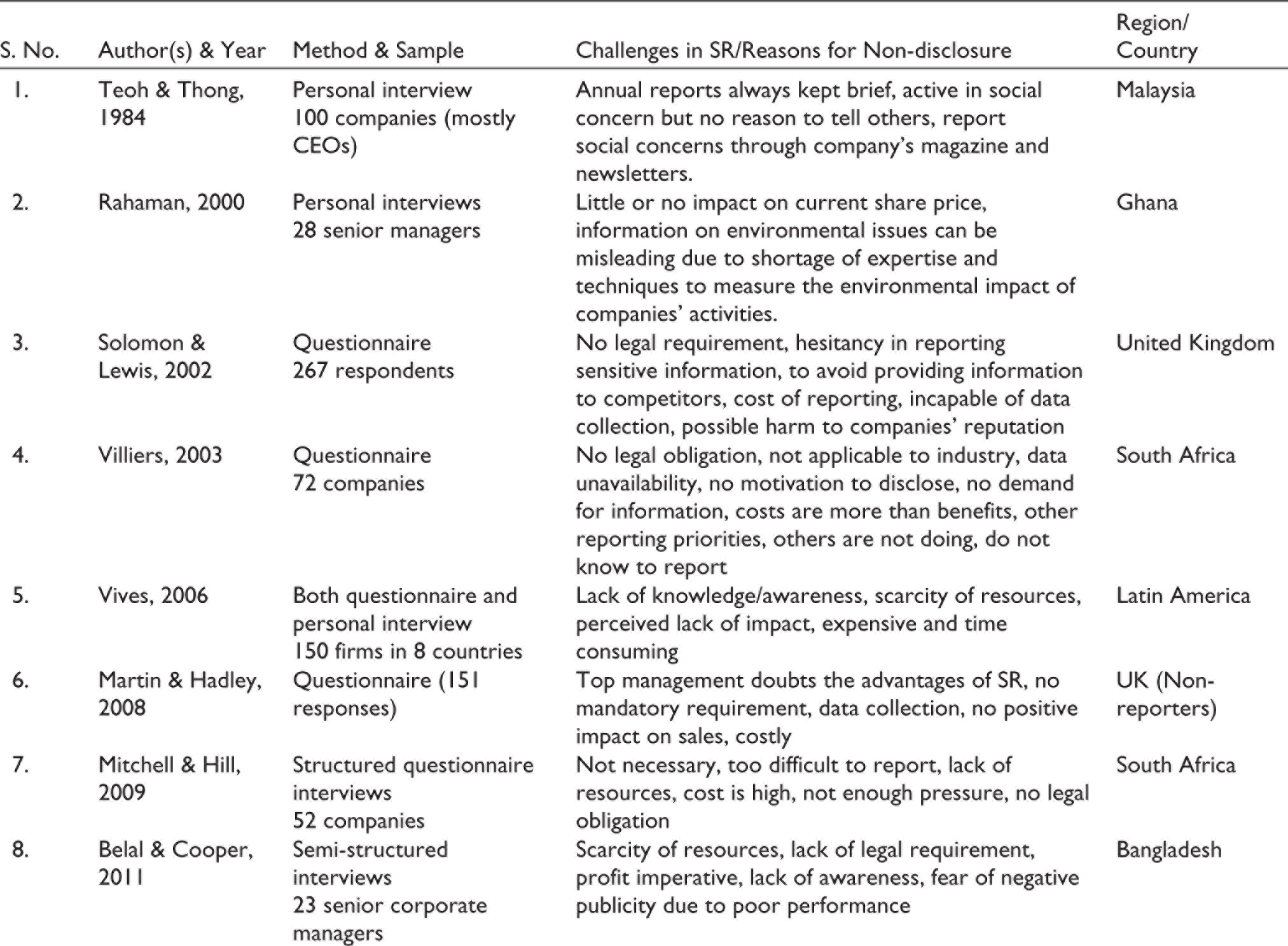

Details of Existing Literature

| S. No. | Author(s) & Year | Method & Sample | Challenges in SR/Reasons for Non-disclosure | Region/ Country |

| 1. | Teoh & Thong, 1984 | Personal interview 100 companies (mostly CEOs) |

Annual reports always kept brief, active in social concern but no reason to tell others, report social concerns through company’s magazine and newsletters. | Malaysia |

| 2. | Rahaman, 2000 | Personal interviews 28 senior managers |

Little or no impact on current share price, information on environmental issues can be misleading due to shortage of expertise and techniques to measure the environmental impact of companies’ activities. | Ghana |

| 3. | Solomon & Lewis, 2002 | Questionnaire 267 respondents |

No legal requirement, hesitancy in reporting sensitive information, to avoid providing information to competitors, cost of reporting, incapable of data collection, possible harm to companies’ reputation | United Kingdom |

| 4. | Villiers, 2003 | Questionnaire 72 companies |

No legal obligation, not applicable to industry, data unavailability, no motivation to disclose, no demand for information, costs are more than benefits, other reporting priorities, others are not doing, do not know to report | South Africa |

| 5. | Vives, 2006 | Both questionnaire and personal interview 150 firms in 8 countries |

Lack of knowledge/awareness, scarcity of resources, perceived lack of impact, expensive and time consuming | Latin America |

| 6. | Martin & Hadley, 2008 | Questionnaire (151 responses) | Top management doubts the advantages of SR, no mandatory requirement, data collection, no positive impact on sales, costly | UK (Non-reporters) |

| 7. | Mitchell & Hill, 2009 | Structured questionnaire interviews 52 companies |

Not necessary, too difficult to report, lack of resources, cost is high, not enough pressure, no legal obligation | South Africa |

| 8. | Belal & Cooper, 2011 | Semi-structured interviews 23 senior corporate managers |

Scarcity of resources, lack of legal requirement, profit imperative, lack of awareness, fear of negative publicity due to poor performance | Bangladesh |

| 9. | Bellringer et al., 2011 | Semi-structured interview 5 city councils |

Lack of support from senior managers, cost involved is more than benefits, difficulty in gathering information, training staff and multi-disciplinarity | New Zealand |

| 10. | Momin & Parker, 2013 | Semi-structured interview 39 senior from 7 MNC subsidiaries |

Informal beliefs and norms, very less expectation for CSR reporting, no strict reporting regulation, low level of implementation of the law | Bangladesh |

| 11. | Chiat et al., 2013 | Questionnaire, 21 corporate managers |

High cost, negative consequences of SR, not useful for non-listed companies, investors only require financial information, lack of knowledge/awareness about SR Standard Setters. | Singapore |

| 12. | Beddewela & Herzig, 2013 | In-depth interviews 18 managers |

Lack of mandatory regulatory framework, limited financial resources, structures, and processes of reporting | Sri Lanka |

| 13. | Pedersen et al., 2013 | Interviews (10 respondents) | Limitation of resources (time and financial), lack of awareness, hard to measure the impact of initiatives, diverse interpretation of new regulation | Denmark |

| 14. | Stubbs et al., 2013 | Semi-structured interviews 23 companies |

Irrelevant, lack of stakeholder’s demand, not a mandatory thing to do, lack of resources, structure or culture of the organisation does not support SR | Australia (about non-reporters) |

| 15. | Steyn, 2014 | Questionnaire (50) | Forward-looking approach required in SR, cost associated to satisfy reporting requirements, development of information system, lack of guidelines, identifying material issues | South Africa |

| 16. | Hossain et al., 2015 | Semi-structured interviews 25 senior managers of companies listed on Dhaka Stock Exchange |

No regulatory framework, religious and socio-cultural factors (such as Islam belief suggests that individuals are accountable to God and any philanthropic activity is aimed to satisfy God rather than influencing other individuals or stakeholders.) | Bangladesh |

| 17. | Özçelik et al., 2015 | Questionnaire survey 55 companies |

Lack of incentives related to sustainability performance, very few people are accountable for sustainability, lack of resources, the conflict between focusing on performance for short-term gains and long-term sustainability | Turkey |

| 18. | Habek & Wolniak, 2015 | Questionnaire (38 respondents) | High cost, lack of knowledge, lack of stakeholder’s interest, not a mandatory requirement, lack of awareness | European Union |

| 19. | Hu & Karbhari, 2015 | Questionnaire survey (156 respondents) | Lack of staff, no legal obligation, possibility of damage to company’s reputation, resistance to publish sensitive information, avoiding to provide information to competitors | China and Malaysia |

| 20. | Kumar Mitra et al., 2015 | Questionnaire (520 respondents) | Absence of legal framework, lack of guidance on best practices | India |

| 21. | Dobbs & van Staden, 2016 | Questionnaire online survey (16 respondents) | Cost Vs. benefit, understanding of value of SR, items to be included and excluded, data collection, resistance sensitive information, employing suitable personnel, incorporating CSR targets in to governance framework | New Zealand |

| 22. | Moneva & Hernández-Pajares, 2018 | Semi-structured interview 7 SMEs |

Lack of knowledge, lack of economic resources, time-consuming | Spain and Peru |

| 23. | McNally et al., 2018 | Interviews (26 managers based in 9 organisations) | Push-down approach in IR stifles proactivity, managerial attitude, doubt about what to report, balance between qualitative and quantitative information, data collection issues | South Africa |

| 24. | Matta et al., 2019 | Structured questionnaire 64 companies |

No legal obligation to report, ignore providing confidential and sensitive information, avoid possible damage to companies’ reputation | India |

| 25. | Mahmood et al., 2019 | Semi-structured interview 20 individuals and organizations |

Lack of interest and awareness in sustainability matters, lack of enforcement and regulation, lack of political will, weak government structures | Pakistan |

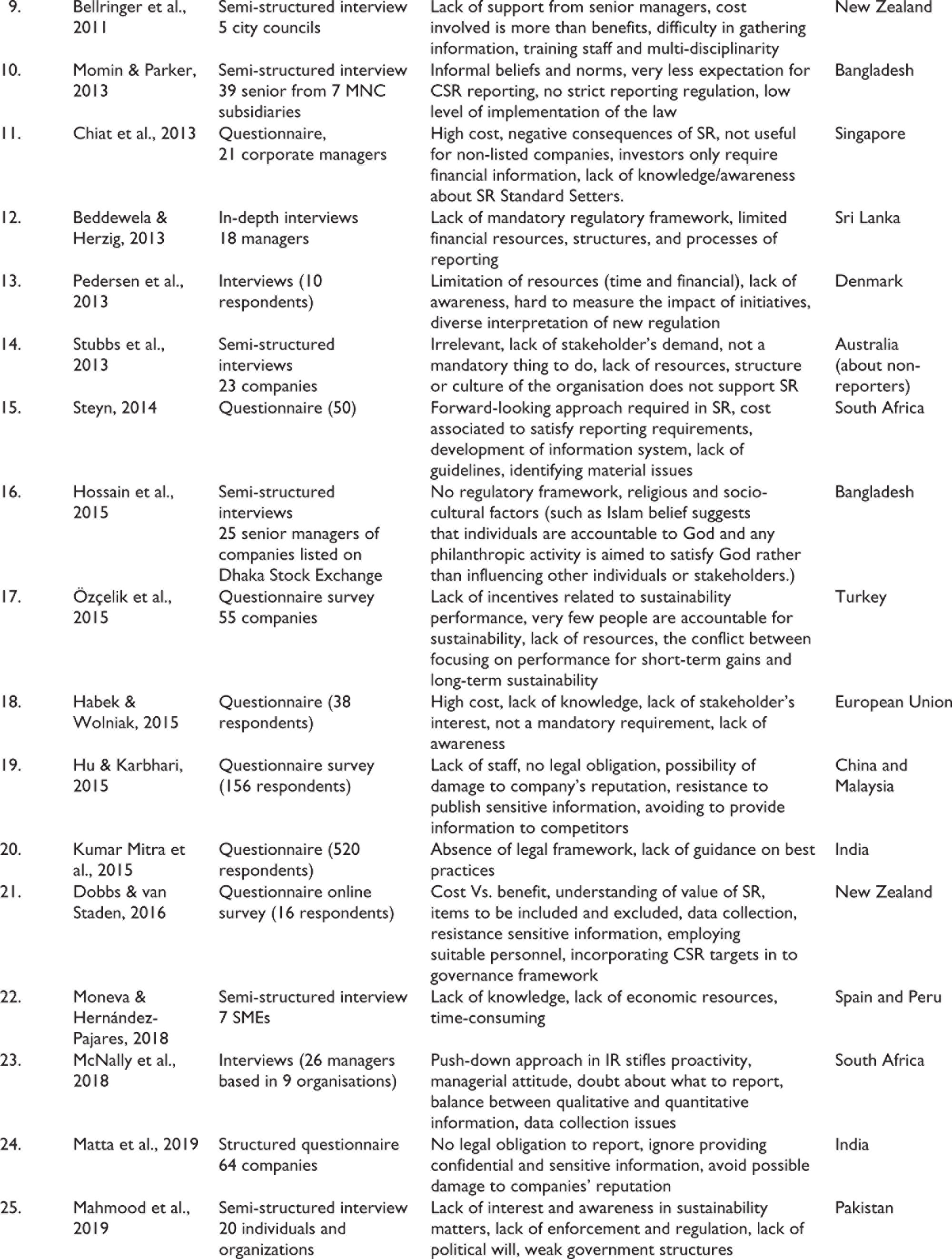

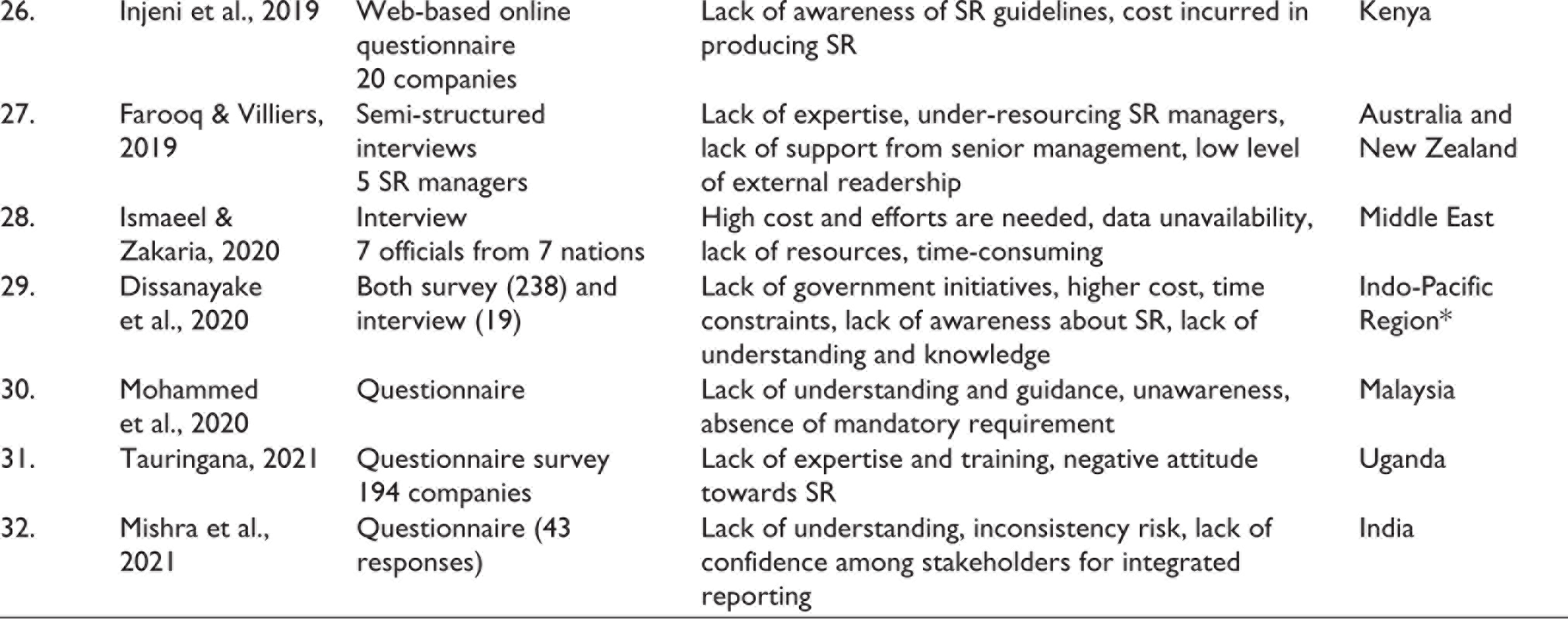

| 26. | Injeni et al., 2019 | Web-based online questionnaire 20 companies |

Lack of awareness of SR guidelines, cost incurred in producing SR | Kenya |

| 27. | Farooq & Villiers, 2019 | Semi-structured interviews 5 SR managers |

Lack of expertise, under-resourcing SR managers, lack of support from senior management, low level of external readership | Australia and New Zealand |

| 28. | Ismaeel & Zakaria, 2020 | Interview 7 officials from 7 nations |

High cost and efforts are needed, data unavailability, lack of resources, time-consuming | Middle East |

| 29. | Dissanayake et al., 2020 | Both survey (238) and interview (19) | Lack of government initiatives, higher cost, time constraints, lack of awareness about SR, lack of understanding and knowledge | Indo-Pacific Region* |

| 30. | Mohammed et al., 2020 | Questionnaire | Lack of understanding and guidance, unawareness, absence of mandatory requirement | Malaysia |

| 31. | Tauringana, 2021 | Questionnaire survey 194 companies |

Lack of expertise and training, negative attitude towards SR | Uganda |

| 32. | Mishra et al., 2021 | Questionnaire (43 responses) | Lack of understanding, inconsistency risk, lack of confidence among stakeholders for integrated reporting | India |