Abstract

Using a unique dataset for Egyptian firms, we investigate the relationship between board independence, audit quality and earnings management. We test whether firm-level corporate governance provisions matter in an emerging market setting characterised by weak legal enforcement and inadequate external discipline by the market for corporate control. Our results cast doubt on the notion that a higher ratio of non-executive members is associated with lower earnings management. We find that the effect of board independence on earnings management practices is contingent on the levels of ownership held by executive directors and large shareholders, as well as the composition of audit committee. In addition, the results are consistent with the view that high-quality auditors are effective in reducing earnings management.

JEL Classification: M41, M48

Introduction

It is widely believed that reporting flexibility may provide managers with a channel through which they can opportunistically manage earnings, which in turn may adversely affect the quality of reported earnings and their use in the decision-making process (Xie, Davidson, & DaDalt, 2003). Prior research provides several explanations as to why corporate managers may tend to manipulate reported earnings. The findings from this stream of research suggest that managers attempt to manage earnings in order to achieve one or more of contractual and capital market objectives, such as, increasing their compensation, avoiding debt covenants violation, smoothing the reported earnings and meeting or exceeding analysts’ forecasts. 1

The accounting scandals surrounding several prominent large companies in the last decade (e.g., Enron, Xerox, Worldcom, HealthSouth, Tyco, Waste Management, Rite Aid and Subeam) have raised serious concerns about the effectiveness of the monitoring and governance devices employed by corporations to protect investors’ interests. 2 One of the corporate governance characteristics, which is widely viewed as desirable in mitigating costly managerial incentives, relates to board independence. It is argued that boards with a majority of independent directors in place are more effective in controlling insiders’ opportunism.

Furthermore, to ensure that objective financial information is conveyed to shareholders, company boards should be composed of a sufficient number of independent non-executive directors who are more likely to be free from the management’s influence (Karamanou & Vafeas, 2005). The findings of several prior studies conducted for the United States (US), the United Kingdom (UK) and European firms are taken as evidence of lower levels of earnings management and fraud in boards in which independent directors are in the majority (Beasley, 1996; Klein, 2002; Marra, Mazzola, & Prencipe, 2011; Peasnell, Pope, & Young, 2005).

Audit quality is another factor perceived to be effective in detecting aggressive earnings management. High-quality auditors require a high financial reporting quality in order to protect their brand name and reputation against the risk that may arise from misleading financial reports by clients (DeAngelo, 1981; Francis & Wang, 2008). It is shown that large audit firms earn considerably higher fees and use part of the audit fee premium to enhance their technological capability and hire skilled professionals to design and employ effective tools for detecting misreporting (Choi, Kim, Liu, & Simunic, 2008; Craswell, Francis, & Taylor, 1995).

Although the relationship between corporate governance and earnings management has been the subject of several studies, the issues that prior research considers relate generally to well-developed capital markets, in particular to the US and the UK in which the ownership of companies is well dispersed among outside shareholders and investor protection is relatively strong. In contrast, few studies have directly addressed the relationship in emerging countries that are characterised by both highly concentrated ownership and weaker investor protection. In addition, there is no consensus on the importance of outside directors and audit quality in reducing earnings management. It is argued that boards of publicly traded firms are generally passive and often dominated by weak non-executive directors who are charged with monitoring executives and not effective in protecting minority stockholders from expropriation by entrenched insiders (Holderness & Sheehan, 1991; Klein, 1998; Park & Shin, 2004). Although there is evidence that a higher ratio of outside directors is associated with better decisions, the evidence on the relation between outside directors and earnings management is not clear-cut (Bradbury, Mak, & Tan, 2006).

The objective of this article is to extend earlier research on earnings management by investigating the potential roles of board independence and audit quality as crucial governance mechanisms in controlling opportunistic earnings management practices in Egypt.

Given the significant differences in the legal and institutional factors between emerging countries and developed countries highlighted in previous research (see Fan & Wong, 2002; La Porta, Lopez-de-Silane, & Shleifer, 1999, among others), inferences from studies conducted for developed countries may be misleading in relation to the effectiveness of corporate governance mechanisms. Conducting this study for Egypt therefore provides us with a distinct opportunity to provide further insights into the effectiveness of corporate governance in constraining earnings management. In contrast to an Anglo-Saxon corporate governance system, the key features of the corporate governance environment in Egypt include a significant degree of ownership concentration, weak law enforcement and inadequate external discipline of the market for corporate control (Djankov, La Porta, Lopez-de-Silanes, & Shleifer, 2008; World Bank, 2009). Moreover, the compliance with corporate governance codes in Egypt is generally voluntary, limiting the potential benefits of compliance and leaving prospective investors less protected and hence reluctant to invest. This, in turn, provides controlling shareholders and top managers with a greater power and a degree of discretion to manage reported earnings and choose a board structure that serves their interests. 3

Additionally, an assumption maintained in the auditing literature is that the Big Four auditors are associated with high audit quality because they require higher earnings quality in order to protect their brand name and reputation from litigation sanctions and potential risk arising from misleading financial reports by clients (DeAngelo, 1981; Francis & Wang, 2008). The Egyptian setting provides us with an ideal opportunity to study the view that high-quality audit firms would provide lower-quality audits when it is less likely that misreporting will be detected and/or litigation is unlikely to occur.

Drawing upon a panel data of 1,005 non-financial listed Egyptian firm-year observations over the period 2005–2012, we find support for the notion that non-executive board directors and audit committee per se are not sufficient to constrain opportunistic earnings management adequately. Our analysis also suggests that firms audited by high-quality auditors are associated with a lower degree of earnings management. Specifically, we find that the impact of corporate governance mechanisms on earnings management varies with the levels of large and managerial shareholdings. At higher levels of large shareholdings and managerial ownership, dominant shareholders and managers attempt to reassure outside investors and signal their commitment to the capital market not to manage earnings. They do so, for example, by putting in place devices, such as appointing more outside members on the board, which potentially prevent the expropriation of outside investors. However, at lower levels of large shareholdings, adding more directors to the board may increase the communication and coordination problems among board directors, leading to less effective monitoring and, as a consequence, higher magnitude of earnings management. The results also reveal that high-quality auditing and higher number of non-executive directors act jointly to further reduce earnings management. In addition, we conclude that managerial ownership (large shareholdings) may play a substitution monitoring role at higher ownership levels of large shareholders (executive directors).

The analysis and the findings of the present study contribute to the existing literature in three main ways. First, using a unique (hand-collected) dataset that reflects distinct corporate governance features and settings helps us shed additional light on the role of the institutional characteristics of emerging countries in explaining the relationship between corporate governance and earnings management. The analysis of this study also provides more insights into the monitoring effectiveness and the role of corporate governance mechanisms. Furthermore, this study, to some extent, addresses the question whether there is a universal corporate governance structure that should be followed irrespective of institutional and structural differences across countries. Second, our study highlights the fact that institutional environment and the incentives faced by managers and controlling shareholders may have a greater influence in explaining the corporate governance– earnings management relationship. Third, the results also add to the auditing literature by providing evidence that high-quality auditors are effective in curbing earnings management even when the likelihood of exposure to litigation risk is very low.

The rest of this article is organised as follows. The next section presents the institutional setting in Egypt. This is followed by a section that develops the hypotheses tested in the study. The section after that discusses the data, the research design and sample characteristics. The next section provides the empirical results of the fixed-effects model estimation. The penultimate section presents robustness checks. Finally, the last section concludes.

Institutional Setting

The Egyptian Corporate Governance Code (henceforth the Code), issued in 2005, emphasises the importance of inclusion of outside directors with an appropriate mix of technical and analytical skills on the board and its committees. For example, the Code requires companies listed on the Egyptian Exchange (EGX) to have an audit committee with at least three non-executive directors to be selected by the company’s board of directors. However, the Code and the Listing Rules do not impose any regulations with regard to the structure of other board-level committees, such as nomination and remuneration committees. While the Company Law does not prohibit the chairperson from being the chief executive officer (CEO), the Code prefers that the two positions not to be occupied by the same person. In case of the necessity of combining the two positions, the reasons should be explained in the corporation’s annual reports. Regarding board size, Egyptian companies have the discretion to determine the appropriate board size that fits their needs. However, according to the Company Law, boards must have an odd number of members, not less than three, chosen by the general assembly for three years, with the exception of the first board, which is appointed by the founders for a maximum of five years (Bahaa El Din & Shawky, 2005).

The existence of the Central Auditing Organisation (CAO) is a unique feature of auditing in Egypt. The CAO is an independent organisation that helps the People’s Assembly (Parliament) achieve control over state and public entities’ funds. The CAO exercises financial, performance and legal control, as well as providing opinions on the financial statements for publicly owned companies, other state bodies and companies in which a public entity, public sector company or bank owns 25 per cent or more of the share capital.

Hypotheses Development

Board Independence and Earnings Management

There has been considerable evidence supporting the hypothesis that the likelihood of fraud and earnings management is negatively related to the percentage of outside directors. Dechow, Sloan and Sweeney (1996) provide evidence that the percentage of outside directors on the board is negatively related to the likelihood of fraud and firms charged with overstating their earnings are more likely to have insider-dominated boards of directors. In line with this view, Beasley (1996) and Uzun, Szewczyk and Varma (2004) find that the likelihood of financial fraud is lower in firms with a high proportion of outside directors. Peasnell et al. (2005) demonstrate that the possibility of making income-increasing abnormal accruals to avoid reporting losses and earnings reductions is negatively related to the proportion of non-executive directors on the board. Similarly, Klein (2002) finds a negative association between the magnitude of abnormal accruals and the percentage of outside directors on the board. Furthermore, Carcello and Neal (2003) show that audit firms are unlikely to issue going-concern reports to financially distressed clients whose audit committees lack independence. The analysis of Klein (2002) also reveals that firms with boards and/or audit committees composed of less than a majority of independent directors are more likely to have a larger magnitude of abnormal accruals. Likewise, the results of Davidson, Goodwin-Stewart and Kent (2005) indicate that earnings management is lower when the majority on the board of directors and audit committees are non-executive members. Marra et al. (2011) also demonstrate that including outside directors on the board and audit committee plays a crucial role in constraining earnings management after the mandatory application of International Financial Reporting Standards. Based on the given discussion, our first hypothesis is formulated as follows:

Hypothesis 1: Earnings management is negatively related to board independence.

We use the ratio of non-executive directors on the board, NEXECD, as a proxy for board independence.

Audit Quality and Earnings Management

It is widely believed that high audit quality is associated with less earnings management and higher quality of earnings. Clients of higher quality auditors are expected to have smaller abnormal accruals. This is because high-quality auditors are more likely to detect aggressive earnings management and report material misreporting (Francis & Wang, 2008; Francis & Yu, 2009). It is found that big audit firms with brand names are associated with higher-quality audits (Becker, DeFond, Jiambalvo, & Subramanyam, 1998; DeAngelo, 1981; Gul, Fung, & Jaggi, 2009). As they have more to lose in terms of clients and audit fees, high-quality auditing firms have stronger incentives to reduce the risk of litigation and protect their reputations. Under this perspective, one would expect to observe a negative association between the magnitude of earnings management and audit quality.

4

Based on the given discussion, the following hypothesis is formulated:

Hypothesis 2: Earnings management is negatively related to audit quality.

In light of the high auditing quality provided by CAO, audit quality is measured using a dummy variable, BIG4, that takes the value of 1 if the firm is audited by Big Four or CAO, and zero otherwise.

Data and Variables

Data

The data examined in this study are drawn from a unique dataset, representing a sample of non-financial publicly listed companies in Egypt over the period 2005–2012. The financial statements were hand collected from EGX and the Capital Market Authority (CMA). Data on ownership structure, board variables, audit committees and auditors was also hand collected from Egypt for Information Dissemination (EGID) and the annual disclosure book issued by EGX (various issues). Market value of equity was extracted from the monthly and yearly bulletins issued by EGID (various issues). To be included in the sample, firms have to meet the following requirements. First, firms must have sufficient data during the sample period to estimate the discretionary accruals. Second, firms should not be involved in any merger or acquisition events. Third, firms should not belong to the financial or regulated sectors because their disclosure requirements, accruals, generation and earnings management incentives are likely to be different from those of firms in other industries. Furthermore, we cleared outliers in the dataset (on the basis of 1st and the 99th percentiles for each variable). This process yields a final sample of 1,005 firm-year observations, representing about 125 firms over 8 years.

Variables Measurement

Earnings Management

Drawing on prior research, this study uses discretionary accruals as a proxy for unobservable earnings management behaviour. The performance-adjusted discretionary accruals approach suggested by Kothari, Leone and Wasley (2005) is used to measure the discretionary accrual component. We measure discretionary accruals (DA) in two stages. First, we estimate non-discretionary accruals (NDA) as a function of changes in cash revenues and the level of property, plant and equipment and the lagged return on assets using the following ordinary least squares (OLS) industry-year model:

where ΔREV represents the change in net revenues for firm i between years t − 1 and t; ΔREC is the change in receivables between years t − 1 and t; GPPE is gross property, plant and equipment; ROA is the ratio of net income before extraordinary items to total assets; TA is the firm i’s book value of total assets in year t;

where ACC represents total accruals, calculated as earnings before extraordinary items and discontinued operations minus cash flows from operating activities; and ε is the error term. Second, discretionary accruals are defined as:

We have modified the original performance-adjusted discretionary accruals model in two main ways. First, as we have no particular event to examine, we adjust firm discretionary accruals by subtracting the changes in accounts receivable from the changes in revenues in the two stages (Kasznik, 1999; Teoh, Welch, & Wong, 1998). This is done mainly because ignoring the effects of receivables in the first stage is likely to reduce the power of the test (McNichols, 2000). Furthermore, there is no reason to think that earnings management is expected to be observed only in the second period (McNichols, 2000). Dechow et al. (1995) argue that it is easier for managers to exercise discretion over the recognition of revenue on credit sales than on cash sales. They also claim that when a firm does not manage earnings in the first stage and manages receivables in the second stage, the accruals of credit sales are normal in the first stage and abnormal in the second stage. Second, we include an intercept term without scaling by lagged total assets. This is because there is no theoretical reason for forcing the regression through the origin (Peasnell, Pope, & Young, 2000), or to believe that total accruals will be zero when changes in cash sales and gross property plant and equipment are zero. 5

Corporate Governance and Control Variables

Our analysis considers several corporate governance mechanisms discussed in prior studies that examined the earnings management– corporate governance relationship, namely, insiders’ ownership, board size, CEO duality and audit committee composition.

The literature on corporate governance offers two competing views with respect to the role of insiders’ ownership. On the one hand, insiders may have incentives and the ability to take actions that are not necessarily in line with the interests of minority investors and creditors. The weak protection of minority shareholders may allow insiders to have influence over the management to misuse corporate resources, generating benefits that might not be shared with minority shareholders, and hence leading to wealth expropriation (Dyck & Zingales, 2004; Thomsen, Pedersen, & Kvist, 2006). On the other hand, insiders may also have an interest in monitoring and reducing the risk of managerial opportunism (Jiraporn & Gleason, 2007), lowering the probability of earnings management. This possibly occurs due to the high costs of extracting benefits, which increase with ownership as insiders would bear a larger share of the decline in firm value resulting from opportunistic earnings manipulation. We include the ownership of the large shareholders, LARGHOLD, defined as the percentage of common equity held by the largest shareholder who owns 5 per cent or more of a firm’s ordinary shares, and executives’ ownership, EXECOWN, defined as the percentage of common equity owned by the CEO and executives of the firm, in an attempt to capture the effects of insiders’ ownership on earnings management.

A number of studies suggest that larger boards may be less effective than smaller boards (Jensen, 1993; Lipton & Lorsch, 1992). Kao and Chen (2004) show that earnings management is positively related to board size. Additionally, Dechow et al. (1996) find that board size is larger for firms engaging in earnings management than for those not engaging in earnings management. Xie et al. (2003) claim that small boards may be less burdened with bureaucratic problems and may provide better financial reporting oversight. In contrast, it is argued that large boards may be able to draw from a broader range of experience as they offer better environmental links and more expertise; help support the link between corporations and their environments; and provide advice on the strategic options for the firm (Pearce & Zahra, 1992). Board size, BODSIZE, is measured by the total number of directors on the board.

Under the agency framework, the ability of a firm’s board to perform its monitoring role is weakened when the CEO and chairman of the board (COB) positions are held by the same person, mainly due to the concentration of power (Beasley, 1996; Jensen, 1993). Managers may be more likely to abuse their power by engaging in fraudulent activities and taking decisions that may not be in the best interests of minority shareholders (Chen, Firth, Gao, & Rui, 2006; Elsayed, 2010). To capture the effect of CEO and COB duality, we use CEODUAL, defined as a dummy variable that takes the value of 1 if the roles of chairperson and CEO are held by the same person, and zero otherwise.

Audit committee independence is also considered a vital and dominant characteristic for an audit committee to fulfil its oversight and monitoring role in the financial reporting. The non-executive directors serving on audit committees are more likely to be free from management’s influence in ensuring that objective financial information is conveyed to shareholders (Karamanou & Vafeas, 2005). It is found that firms with audit committees composed of less than a majority of independent directors are more likely to receive a going-concern audit report modification (Carcello & Neal, 2003), to have a larger magnitude of abnormal accruals (Klein, 2002) and to be associated with lower levels of fraud (Beasley, 1996). To control for the possible effect of audit committees’ independence on our results, we incorporate in our analysis AUDCOM, defined as a dummy variable that takes the value of 1 if the audit committee is composed entirely of non-executive directors, and zero otherwise, as a proxy for audit committee independence. 6

Our analysis also includes some other control variables discussed in prior earnings management studies. It is found that the risk of audit failure is expected to be higher in the early years of tenure as incoming auditors are unlikely to have client-specific expertise and knowledge (Jaggi & Leung 2007; Johnson, Khurana, & Reynolds, 2002). Audit tenure, AUDTEN, defined as a dummy variable that takes the value of 1 if the client–auditor relation started at least three years previously, and zero otherwise, is hence incorporated in order to control for the likely negative association found in prior studies between audit tenure and earnings management (e.g., Heninger, 2001; Johnson et al., 2002).

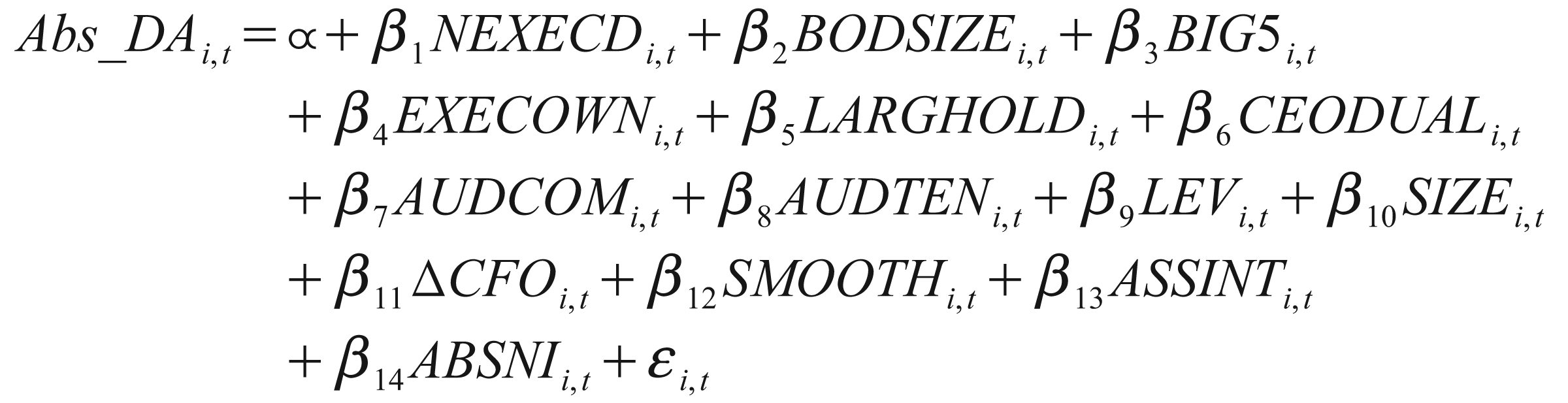

In an attempt to control for the possibility that managers may use abnormal accruals to increase the reported income to avoid debt covenant violation (see, e.g., DeFond & Jiambalvo 1994; and Sweeney, 1994), firm leverage, LEV, measured as the ratio of total debt to total assets, is included in the analysis. It is also found that the magnitude of discretionary accruals reported by large firms is lower as they are likely to be exposed to a higher litigation risk, political intrusion and public pressure (Ashbaugh, LaFond, & Mayhew, 2003; Xie et al., 2003), which may influence their accounting choices. We use the natural logarithm of total assets, SIZE, as a proxy for firm size. Following Darrough, Pourjalali and Saudagaran (1998) and Young (1999), change in cash from operations, ΔCFO, is used to account for the smoothing inherent in accrual generation, while SMOOTH, defined as a dummy variable taking the value of 1 when unmanaged earnings are above earnings benchmark, and zero otherwise, is used to account for the possibility of managing earnings being used to achieve earnings targets. The ratio of gross fixed assets to total market capitalisation, ASSINT, is used to control for the effects of depreciation on the estimations of discretionary accruals (Young, 1998), while the absolute current year earnings, ABSNI, defined as the absolute value of net income scaled by lagged total assets, is used to control for firm performance (Frankel, Johnson, & Nelson, 2002). We employ a fixed-effects estimator to examine the impact of board independence, board size and audit quality on earnings management. Our specified model is as follows:

where Abs_DA is the absolute value of discretionary accruals as measured in equation (3). Since this study does not examine earnings management on a particular event and borrowing extensively from prior studies (see, e.g., Ashbaugh et al., 2003; DeFond & Jiambalvo, 1994; Francis & Yu, 2009; Frankel et al., 2002; Gul et al., 2009; Kasznik, 1999), we use the absolute (unsigned) value of discretionary accruals as the main dependent variable in the analysis to capture the effects of both income increasing and decreasing adjustments.

Sample Characteristics

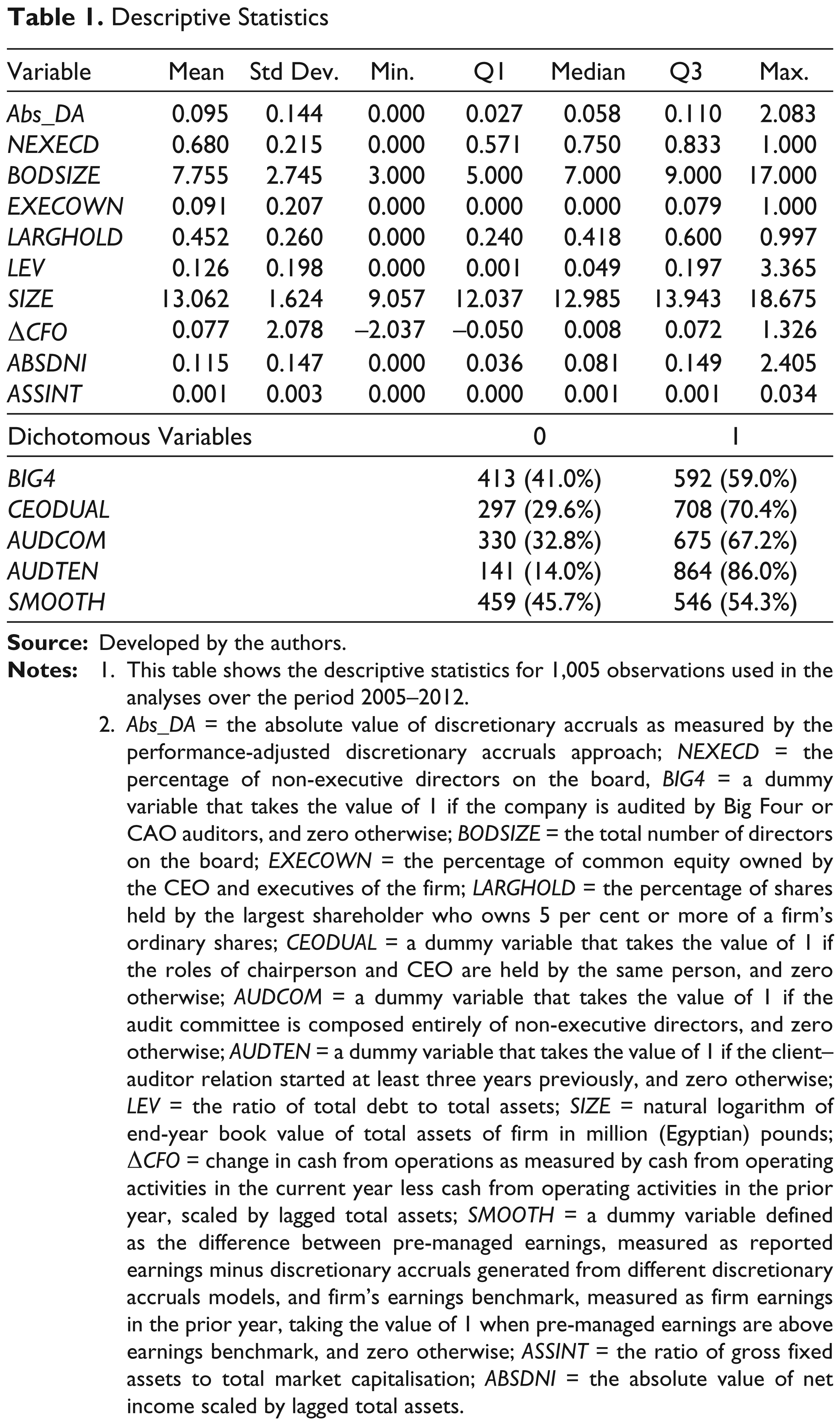

Table 1 reports summary descriptive statistics for discretionary accruals and other variables used in the study. The absolute value of discretionary accruals is on average 0.095, with a median value of 0.058. The average number of directors on the board is just below eight. The majority of board members are non-executive directors, suggested by the average and median values of the ratio of non-executive directors on the board, which are respectively 68 per cent and 57.1 per cent. The positions of COB and CEO are held, on average, by the same person in 70.4 per cent of the sample firms. Additionally, 67.2 per cent of firms have audit committees composed entirely of outsider members. The analysis also indicates that those firms that are audited by Big Four auditors represent 59 per cent of the firms in the sample. In addition, the average ownership by executive directors is 9.1 per cent. 7

Descriptive Statistics

2. Abs_DA = the absolute value of discretionary accruals as measured by the performance-adjusted discretionary accruals approach; NEXECD = the percentage of non-executive directors on the board, BIG4 = a dummy variable that takes the value of 1 if the company is audited by Big Four or CAO auditors, and zero otherwise; BODSIZE = the total number of directors on the board; EXECOWN = the percentage of common equity owned by the CEO and executives of the firm; LARGHOLD = the percentage of shares held by the largest shareholder who owns 5 per cent or more of a firm’s ordinary shares; CEODUAL = a dummy variable that takes the value of 1 if the roles of chairperson and CEO are held by the same person, and zero otherwise; AUDCOM = a dummy variable that takes the value of 1 if the audit committee is composed entirely of non-executive directors, and zero otherwise; AUDTEN = a dummy variable that takes the value of 1 if the client–auditor relation started at least three years previously, and zero otherwise; LEV = the ratio of total debt to total assets; SIZE = natural logarithm of end-year book value of total assets of firm in million (Egyptian) pounds; ΔCFO = change in cash from operations as measured by cash from operating activities in the current year less cash from operating activities in the prior year, scaled by lagged total assets; SMOOTH = a dummy variable defined as the difference between pre-managed earnings, measured as reported earnings minus discretionary accruals generated from different discretionary accruals models, and firm’s earnings benchmark, measured as firm earnings in the prior year, taking the value of 1 when pre-managed earnings are above earnings benchmark, and zero otherwise; ASSINT = the ratio of gross fixed assets to total market capitalisation; ABSDNI = the absolute value of net income scaled by lagged total assets.

Empirical Results

Univariate Analysis

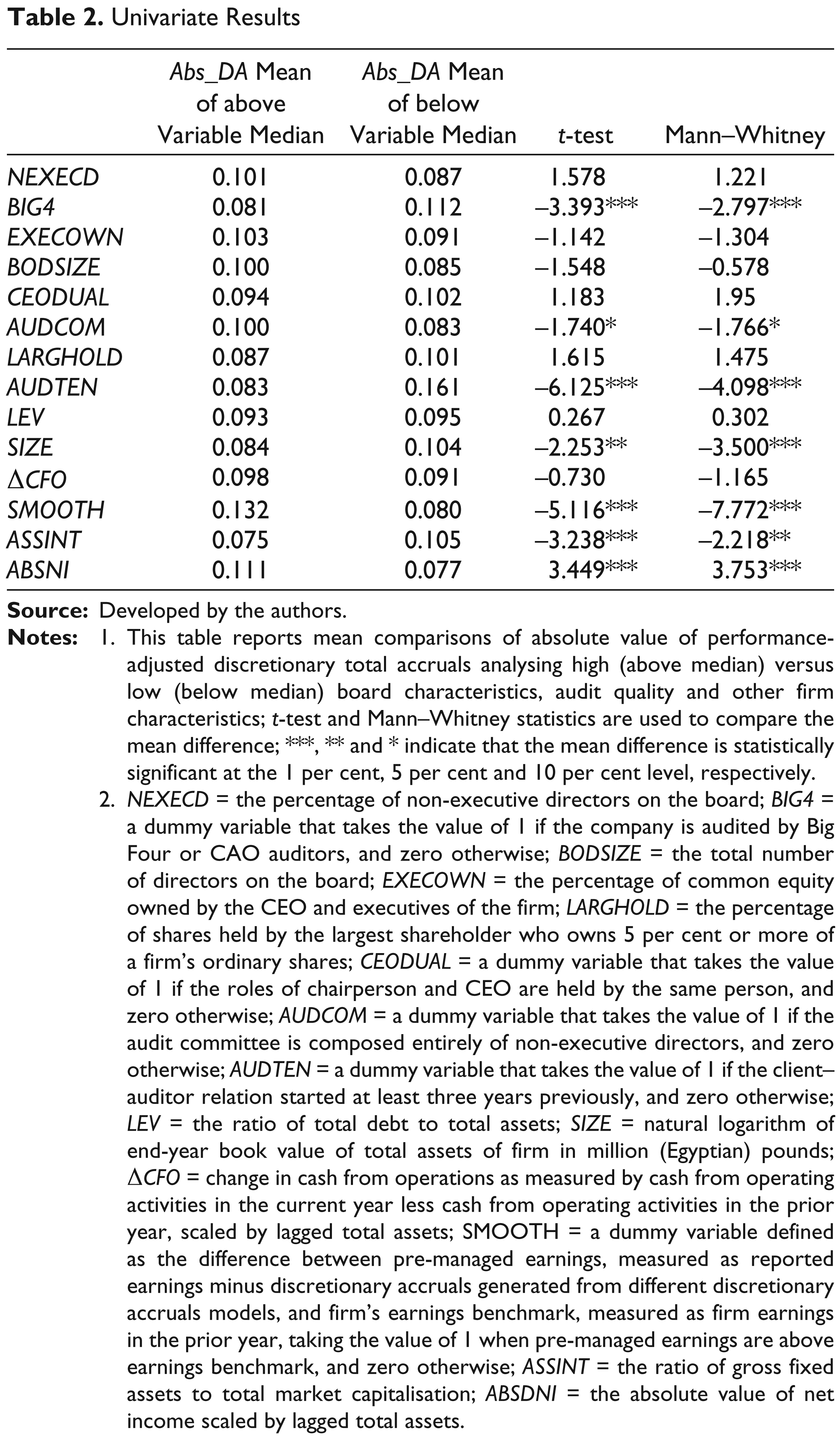

The univariate analysis includes a mean (median) comparison test of the subsamples of firms using t-test (Wilcoxon–Mann–Whitney test). The samples of Abs_DA are designed on the basis of the median of each explanatory variable in the case of scale variables, or using the two categories in the case of dichotomous variables. We test the hypothesis that firms with above median values of corporate governance characteristics, audit quality and other firm characteristics differ from firms with below median values with respect to the absolute value of discretionary accruals.

We find that firms with above median values for BIG4, AUDTEN, SMOOTH and ASSINT have relatively lower magnitudes of discretionary accruals. These results are statistically significant at the 1 per cent level. In addition, we find that larger firms have lower earnings management relative to smaller firms. The difference between the means is statistically significant at the 5 per cent level. However, we find that firms with above median values of ABSNI have relatively greater extent of discretionary accruals. Contrary to our prediction, the results in Table 2 reveal that equity ownership levels of large shareholders and executive directors are not significantly associated with earnings management. In particular, it appears that firms with above median executive ownership (large shareholdings) have absolute abnormal accruals of 0.103 (0.091), while firms with below median executive ownership (large shareholdings) have absolute abnormal accruals of 0.087 (0.101). Additionally, there is no evidence that firms with larger board and in which the roles of CEO and COB are separated have higher earnings management relative to those with small board size and in which the CEO and COB positions are held by the same person. There is also weak evidence that firms in which audit committees are composed entirely of non-executive directors have a lower magnitude of earnings management. This result is statistically significant at the 10 per cent level.

Univariate Results

2. NEXECD = the percentage of non-executive directors on the board; BIG4 = a dummy variable that takes the value of 1 if the company is audited by Big Four or CAO auditors, and zero otherwise; BODSIZE = the total number of directors on the board; EXECOWN = the percentage of common equity owned by the CEO and executives of the firm; LARGHOLD = the percentage of shares held by the largest shareholder who owns 5 per cent or more of a firm’s ordinary shares; CEODUAL = a dummy variable that takes the value of 1 if the roles of chairperson and CEO are held by the same person, and zero otherwise; AUDCOM = a dummy variable that takes the value of 1 if the audit committee is composed entirely of non-executive directors, and zero otherwise; AUDTEN = a dummy variable that takes the value of 1 if the client–auditor relation started at least three years previously, and zero otherwise; LEV = the ratio of total debt to total assets; SIZE = natural logarithm of end-year book value of total assets of firm in million (Egyptian) pounds; ΔCFO = change in cash from operations as measured by cash from operating activities in the current year less cash from operating activities in the prior year, scaled by lagged total assets; SMOOTH = a dummy variable defined as the difference between pre-managed earnings, measured as reported earnings minus discretionary accruals generated from different discretionary accruals models, and firm’s earnings benchmark, measured as firm earnings in the prior year, taking the value of 1 when pre-managed earnings are above earnings benchmark, and zero otherwise; ASSINT = the ratio of gross fixed assets to total market capitalisation; ABSDNI = the absolute value of net income scaled by lagged total assets.

Multivariate Analysis

The results of univariate analysis reveal a weak association between the majority of board characteristics, audit quality and earnings management. The univariate analysis, however, does not control for the effects of other variables that may be related to abnormal accruals and/or corporate governance mechanisms. The potential relation may, in turn, confound the earnings management–corporate governance relationship. Accordingly, the rest of the empirical results are derived from multi-variate analysis.

Board Independence, Audit Quality and Earnings Management

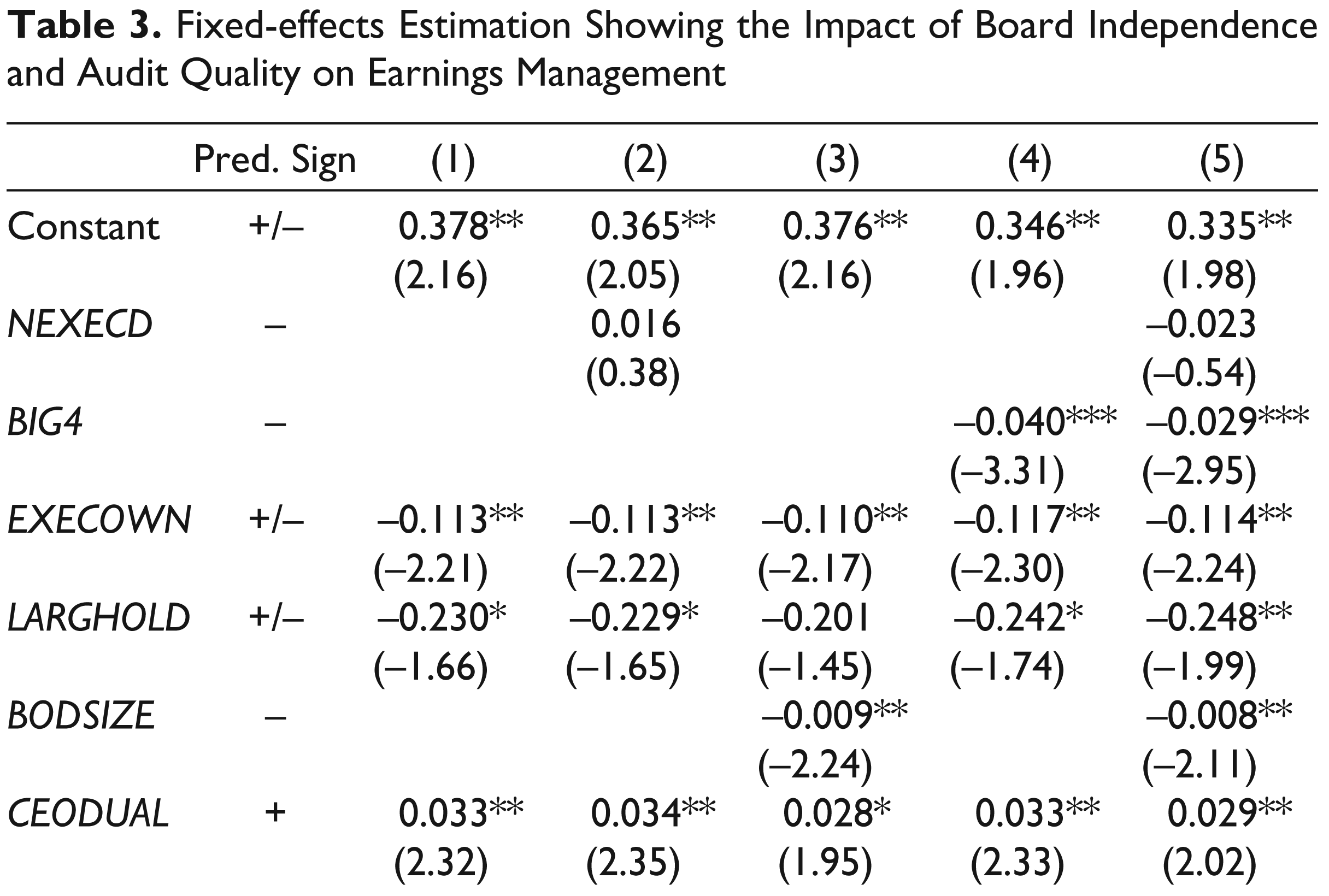

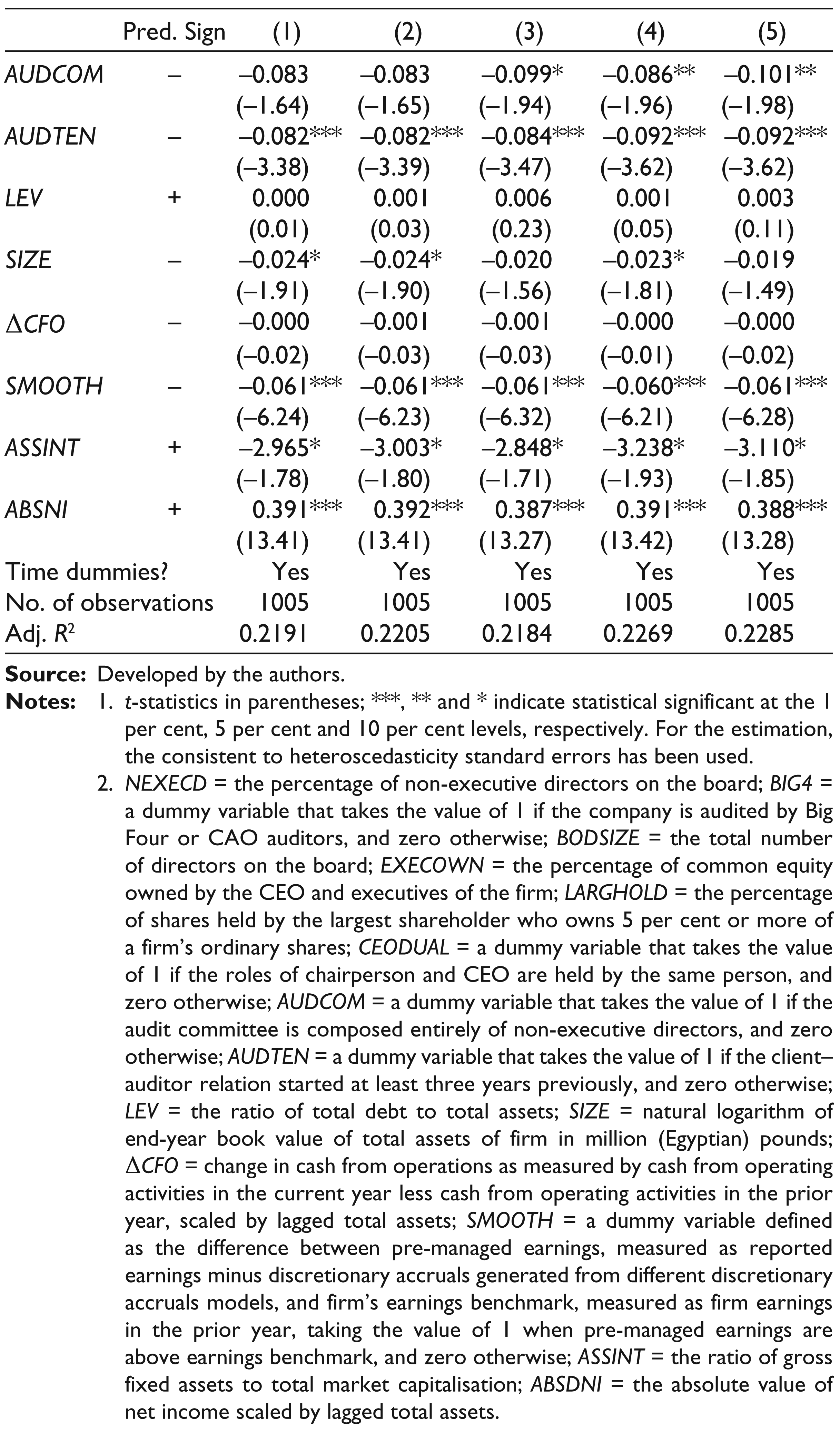

Table 3 reports the results of the absolute value of discretionary accruals tests using a fixed-effects estimation methodology with robust standard errors to correct for heteroscedasticity. In contrast to our expectations, the results in Table 3 reveal that the estimated coefficient of NEXECD is not significant, implying that non-executive directors in general play no monitoring role in the earnings management reduction. One plausible explanation is that non-executive directors are added to the board for their advisory duties such as special expertise and contacts, or merely to comply with regulations (Peasnell, Pope, & Young, 2003; Siregar & Utama, 2008), rather than their monitoring function. The results in Table 3 show that the coefficient of AUDCOM is negative and statistically significant at the 5 per cent level. This result suggests that firms with audit committees composed solely of non-executive directors are less likely to undertake earnings manipulation activities.

Fixed-effects Estimation Showing the Impact of Board Independence and Audit Quality on Earnings Management

2. NEXECD = the percentage of non-executive directors on the board; BIG4 = a dummy variable that takes the value of 1 if the company is audited by Big Four or CAO auditors, and zero otherwise; BODSIZE = the total number of directors on the board; EXECOWN = the percentage of common equity owned by the CEO and executives of the firm; LARGHOLD = the percentage of shares held by the largest shareholder who owns 5 per cent or more of a firm’s ordinary shares; CEODUAL = a dummy variable that takes the value of 1 if the roles of chairperson and CEO are held by the same person, and zero otherwise; AUDCOM = a dummy variable that takes the value of 1 if the audit committee is composed entirely of non-executive directors, and zero otherwise; AUDTEN = a dummy variable that takes the value of 1 if the client–auditor relation started at least three years previously, and zero otherwise; LEV = the ratio of total debt to total assets; SIZE = natural logarithm of end-year book value of total assets of firm in million (Egyptian) pounds; ΔCFO = change in cash from operations as measured by cash from operating activities in the current year less cash from operating activities in the prior year, scaled by lagged total assets; SMOOTH = a dummy variable defined as the difference between pre-managed earnings, measured as reported earnings minus discretionary accruals generated from different discretionary accruals models, and firm’s earnings benchmark, measured as firm earnings in the prior year, taking the value of 1 when pre-managed earnings are above earnings benchmark, and zero otherwise; ASSINT = the ratio of gross fixed assets to total market capitalisation; ABSDNI = the absolute value of net income scaled by lagged total assets.

As the likelihood of the litigation risk that audit firms might face is low in Egypt (Fawzy, 2003; Sourial 2004), one would expect no differences between the quality of auditing provided by Big Four and non-Big Four. However, the estimated coefficient of BIG4 is highly significant and negatively associated with earnings managements at 1 per cent level. This result is in line with the view that firms audited by Big Four auditors are unlikely to engage in earnings management practices due to the higher quality of auditing provided by those auditors (e.g., Becker et al., 1998; Francis, Maydew, & Sparks, 1999).

The findings in Table 3 also show that firms with higher managerial ownership and large shareholdings are likely to have a lower magnitude of earnings management. This is possibly because top managers at higher ownership levels are less likely to engage in value-destroying activities such as opportunistic earnings management. Furthermore, the results in Table 3 reveal that the coefficient of BODSIZE is negative and significant at the 5 per cent level or better. This result suggests that a large board is more effective in reducing earnings management. This is possibly because larger boards may benefit from greater representations of outsiders on the board and audit committees and increase the diversity of different expertise which, presumably, leads to less earnings management (Cheng, 2008; Klein, 2002; Xie et al., 2003).

Turning to other variables, the estimated coefficient of CEODUAL is positive and significant at the 5 per cent level. This result is in line with the agency argument that CEO duality is likely to weaken the firm’s board monitoring role. The results in Model (5) indicate that the coefficients of several control variables are significantly associated with the magnitude of earnings management at the 5 per cent level or better with their expected signs, where the exceptions are the estimated coefficients of LEV and ΔCFO, which are not significant. The leverage result is inconsistent with the view that firms with debt covenants may have greater incentives to disguise the firm’s economic performance and inflate reported earnings to prevent debt covenants violation (e.g., DeFond & Jiambalvo, 1994; Healy & Palepu, 1990). However, this result is in line with the assertion that highly leveraged firms are unlikely to make income-increasing accounting choices in an attempt to reduce the possibility of default (see, e.g., DeAngelo, DeAngelo, & Skinner, 1994; Heflin, Kwon, Wild, & Building, 2002). Using a sample of Egyptian firms, Khalil and Simon (2014) find no evidence that supports the assertion that managers of highly leveraged firms are likely to manipulate abnormal accruals upward to increase the reported income to prevent debt covenant violation. They find that income smoothing objective is dominant in the Egyptian setting. As Table 3 shows that the estimated coefficient of SMOOTH is negative and statistically significant at the 1 per cent level, it seems that earnings smoothing is more likely help management to achieve contractual objectives, including avoid debt covenant violation, and/or gain personal advantage. This also helps management keep their jobs (Fudenberg & Tirole, 1995), increase their compensation and reduce the probability of governmental intervention. Equally, it can help management signal their ability to the capital market and build their reputation. Thus, the weak evidence of leverage might be captured by the strong effects of income smoothing.

Furthermore, ASSINT is marginally significant at the 10 per cent with a sign different than expected while SIZE is also marginally significant at the 10 per cent level. It also seems that firms with longer audit tenure have lower earnings management. More specifically, the estimated coefficient of AUDTEN is negative and statistically significant at the 1 per cent level.

The Intervening Effect of Large Shareholdings, Executives’ Ownership and Audit Committee Independence

The conclusion from the above-mentioned results is that the role of board characteristics in reducing earnings management is not significant. However, we believe that the monitoring role of non-executive directors in Egypt is more likely to be contingent on the equity ownership levels of large shareholders and executive directors. The premise underpinning our argument is that in a setting characterised by weak legal protection of shareholders, dominant owners may have different incentives at various levels of ownership. At lower levels of ownership, large shareholders and top management may tend to expropriate firm resources for their personal consumption by taking self-interested actions that may not necessarily be optimal for other shareholders. These actions include, for example, managing the reported earnings aggressively and choosing weak boards. However, greater levels of ownership can be seen as a governance mechanism that helps prevent the potential expropriation of minority shareholders. Thus, at higher levels of equity ownership, controlling shareholders and/or powerful managers may tend to reduce opportunistic earnings management as they would bear a larger share of the decline in firm value resulting from opportunistic earnings management.

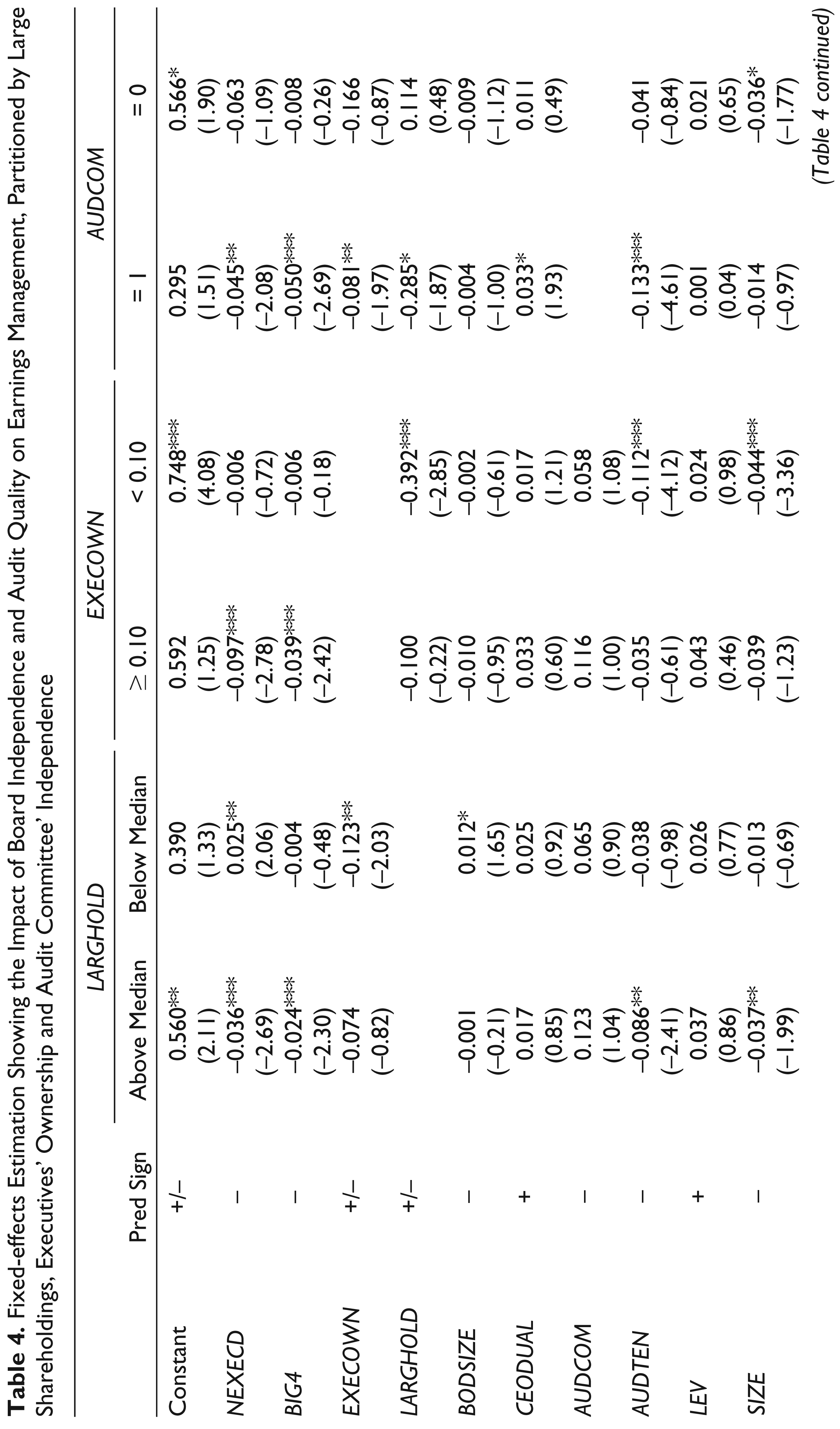

This argument potentially suggests that the structure and the monitoring role of the board and audit quality are likely to interact with and be shaped by the equity ownership of large and executive shareholders. Thus, it would be useful to test the extent to which the ownership of large and executive shareholders, as well as audit quality, interact to reduce or exacerbate the magnitude of earnings management. Such analysis is likely to provide additional insights into the conditional monitoring roles of corporate governance in a country with weak legal protection of shareholders. To do so, we first split the full sample into two sub-samples based upon the level of the median value of ownership of large shareholders.

At lower levels of large shareholdings, Table 4 shows that the NEXECD coefficient is significantly positive at the 5 per cent level. This result reflects an important feature of the Egyptian setting. Although the majority of board members are on average from non-executive directors, existing voting rules entitle the controlling owners to elect members to represent dominant shareholders’ interests. It is found that the majority of Egyptian board members are usually chosen from family, close relatives and friends (Sourial, 2004). This is no doubt due to the absence of cumulative voting that enables minority shareholders to elect their representative on the board. This, in turn, is more likely to lead to weak boards whose members lack financial knowledge and facilitate resource expropriation, enabling large shareholders to enjoy private benefits that are not shared with other shareholders. Presumably, the weak Egyptian legal protection of minority shareholders allows controlling shareholders to benefit from corporate resource expropriation via, for example, earnings management to obtain more private benefits if they believe that these benefits outweigh the costs of extracting such benefits. In addition, large shareholders may exaggerate the capital market pressure in the short term by managing the reported earnings in order to meet earnings targets (e.g., Guthrie & Sokolowsky, 2010). Thus, weak boards are likely to be the preferred choice of dominant shareholders, which enable them to act in their own best interests by exploiting minority shareholders.

Fixed-effects Estimation Showing the Impact of Board Independence and Audit Quality on Earnings Management, Partitioned by Large Shareholdings, Executives’ Ownership and Audit Committee’ Independence

2. NEXECD = the percentage of non-executive directors on the board; BIG4 = a dummy variable that takes the value of 1 if the company is audited by Big Four or CAO auditors, and zero otherwise; BODSIZE = the total number of directors on the board; EXECOWN = the percentage of common equity owned by the CEO and executives of the firm; LARGHOLD = the percentage of shares held by the largest shareholder who owns 5 per cent or more of a firm’s ordinary shares; CEODUAL = a dummy variable that takes the value of 1 if the roles of chairperson and CEO are held by the same person, and zero otherwise; AUDCOM = a dummy variable that takes the value of 1 if the audit committee is composed entirely of non-executive directors, and zero otherwise; AUDTEN = a dummy variable that takes the value of 1 if the client–auditor relation started at least three years previously, and zero otherwise; LEV = the ratio of total debt to total assets; SIZE = natural logarithm of end-year book value of total assets of firm in million (Egyptian) pounds; ΔCFO = change in cash from operations as measured by cash from operating activities in the current year less cash from operating activities in the prior year, scaled by lagged total assets; SMOOTH = a dummy variable defined as the difference between pre-managed earnings, measured as reported earnings minus discretionary accruals generated from different discretionary accruals models, and firm’s earnings benchmark, measured as firm earnings in the prior year, taking the value of 1 when pre-managed earnings are above earnings benchmark, and zero otherwise; ASSINT = the ratio of gross fixed assets to total market capitalisation; ABSDNI = the absolute value of net income scaled by lagged total assets.

At lower level of large shareholdings, the Big Four do not seem to play a significant role in constraining earnings management, suggested by the insignificantly estimated coefficient of BIG4. With respect to the impact of managerial ownership, the results in Table 4 suggest that executive ownership may act jointly as effective governance mechanism to curtail opportunistic behaviour of dominant shareholders at lower levels of ownership. In addition, the estimated coefficient of BODSIZE (NEXCED) is positive and significant at the 10 (5) per cent level. We argue that while larger boards might lead to a greater representation of outsiders, and hence provide the CEO with better advice (Coles, Daniel, & Naveen, 2008), adding more directors to the board is more likely to increase the coordination and communication problems as well as the director free-rider problem related to larger boards (Fama & Jensen, 1983; Jensen, 1993). These results suggest that large shareholders may use their voting power to appoint directors who serve to provide expertise and advice, rather than for monitoring purposes, possibly due to higher monitoring costs.

However, it seems that other board characteristics, namely, CEO duality and audit committee independence, play no role in reducing earnings manipulation. This is possibly because managerial ownership may provide a sufficient monitoring role of opportunistic earnings manipulation at higher ownership levels of large shareholders.

Arguably, at higher levels of large shareholder ownership, the results in Table 4 suggest that the monitoring role of outside directors becomes effective as the coefficient of NEXECD is negative and significant at the 1 per cent level. Presumably, at such higher ownership levels, outside shareholders may expect that earnings management can be used as a mean of resource diversion, and they are more likely to protect their interests by, for example, paying a lower price for firm shares. This is, in turn, likely to have adverse effects on the firm value and on the wealth of managers and large shareholders. As a result, dominant shareholders tend to signal their commitment to outsiders to refrain from the diversion of the firm’s resources to serve their own interests by putting in place effective credible devices, such as adding more outside members to the board. This might be an important part of a broader strategy that improves their transparency if improved transparency allows them, for example, to access external capital at a lower cost or facilitates cross-listing (Gopalan & Jayaraman, 2012). Doing so may reduce the diversion of corporate resources and enhance firm value, thereby increasing the wealth of dominant shareholders.

The results in Table 4 point to possible complementary monitoring roles at higher levels of large shareholdings between high audit quality and a greater representation of non-executive directors on the board to reduce earnings management. Put differently, in firms, a high percentage of large shareholders, high-quality audits and non-executive directors on the board possibly work jointly to provide protection against opportunistic earnings management.

In a similar manner, we split the sample based on executives’ ownerships at the 10 per cent level. Similar to the results reported earlier, Table 4, at greater levels of executive directors’ ownership, reveals that the coefficient of NEXED becomes more significant. Since they would bear a larger share of diversion costs, top management is less likely to take suboptimal decisions or consume perquisites to deviate from shareholder wealth maximisation to gain more private benefits (Jensen & Meckling, 1976). Thus, managers may seek to add more non-executive directors to the board in an attempt to protect their interests and signal the commitment not to divert corporate resources to themselves and/or to the dominant owners. The results also may indicate a possible incentive alignment between the interest of management and that of minority shareholders.

Similar to the complementary role just explained, high-quality auditors are more likely to detect aggressive earnings management when the monitoring by executives and dominant shareholders is inadequate. In Table 4 (columns 7 and 8), we examine the interactions between board characteristics and audit quality and audit committee independence. The results suggest that high-quality auditors and non-executive directors work jointly to reduce earnings management when audit committee is composed entirely of outside directors. That is, adding more non-executive directors to the boards is more effective in reducing earnings management. This is possibly because additional outsiders are likely to lead to strong boards and better governance practices and, as a result, lower earnings management. In addition, high-quality auditors are associated with lower earnings management.

The Impact of Global Financial Crisis on Corporate Governance–Earnings Management Relationship

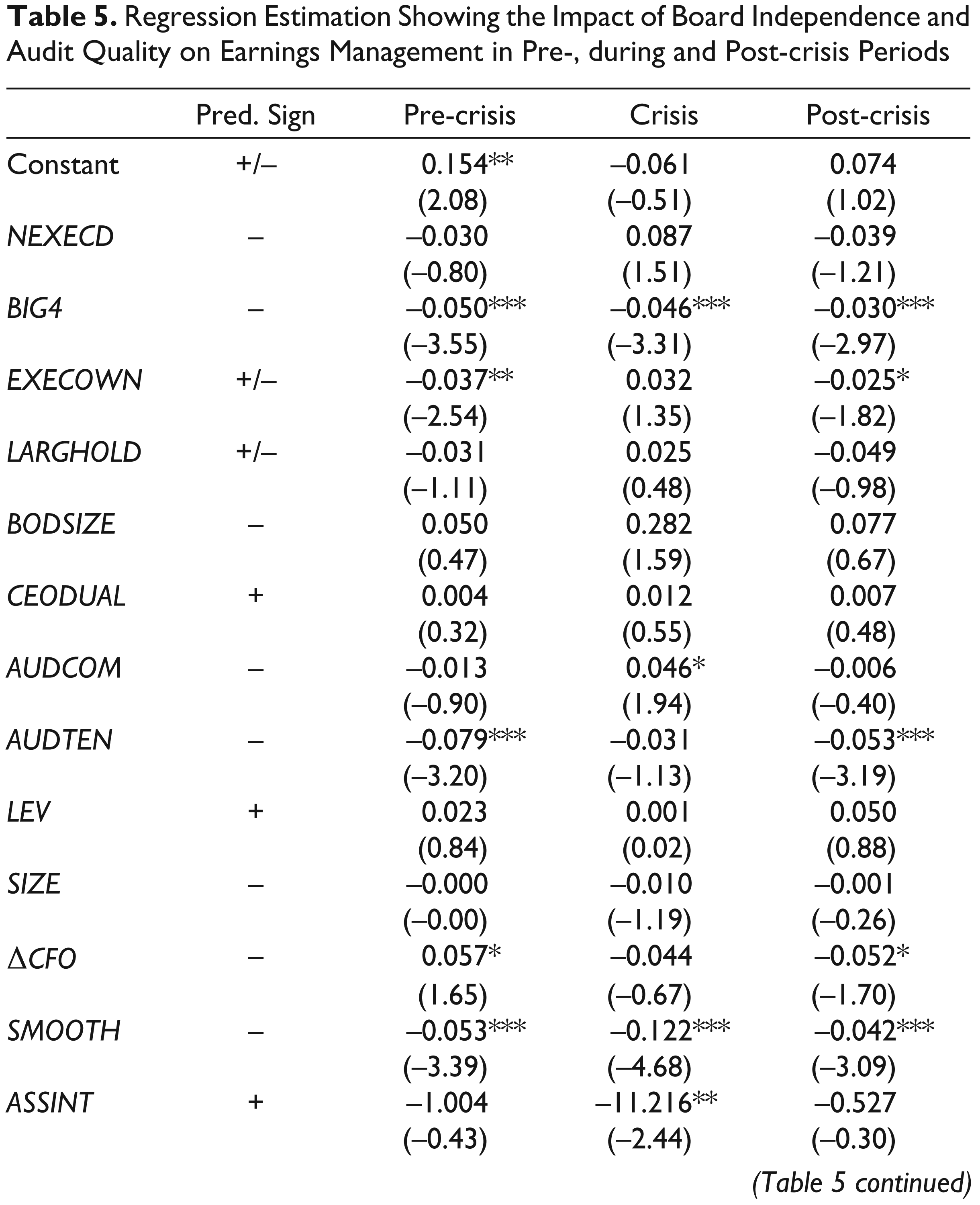

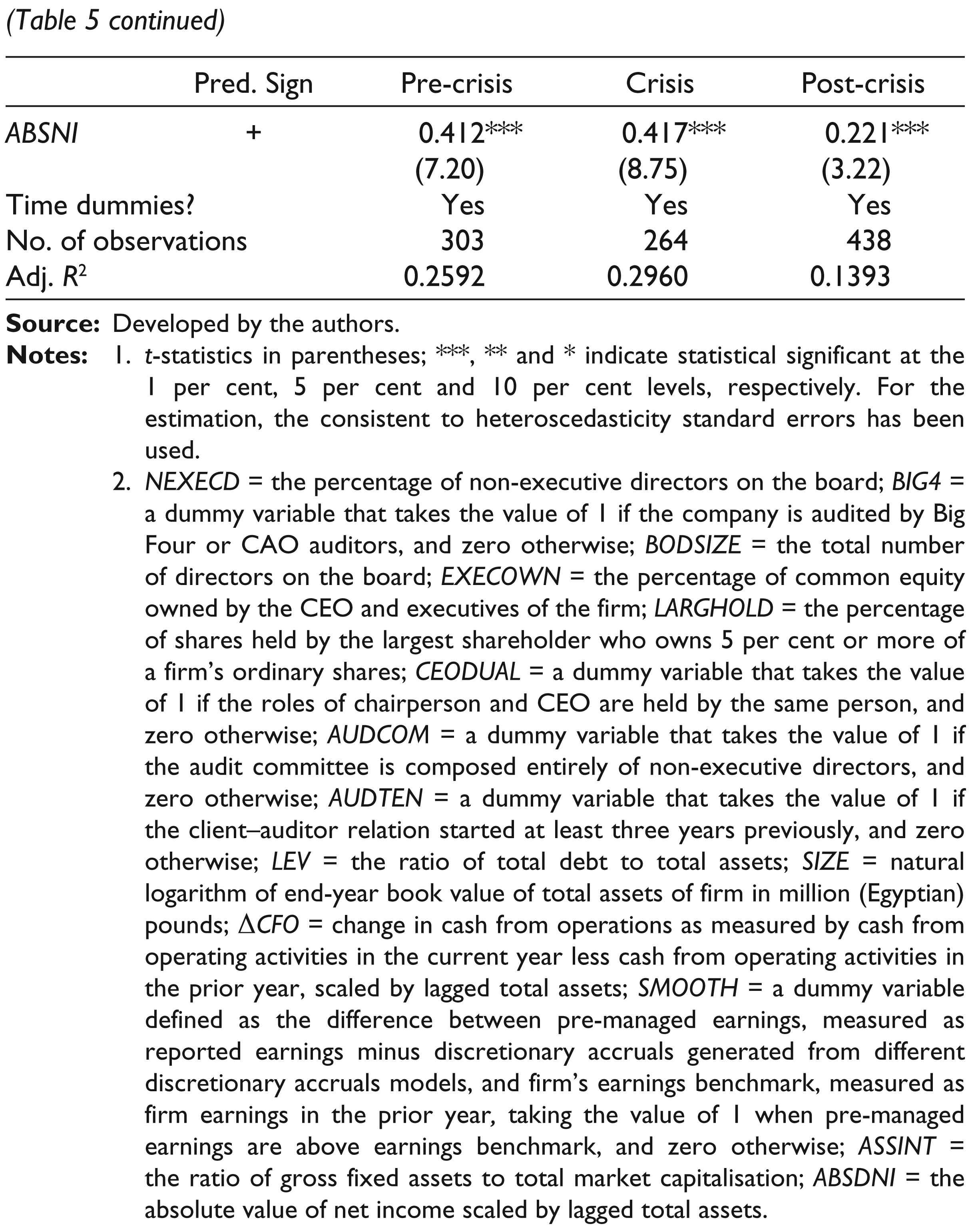

Recent research shows that financial reporting did not adequately monitor and disclose the influence of risk-taking on financial statements (e.g., Barth & Landsman, 2010; Magnan & Markarian, 2011). Thus, we acknowledge that the effectiveness of corporate governance in reducing earnings management activities may depend on the period, especially in relation to the global financial crisis of 2007–2008. A number of studies provide supportive evidence to the assertion that senior managers are more likely to manage reported earnings aggressively during the financial crisis in an attempt to meet or beat earnings targets, and hence influence the market’s evaluation of the survival of their firms (Bartov, Givoly, & Hayn, 2002; Kasznik & McNichols, 2002; Matsumoto, 2002). However, another strand of research suggests that financially distressed firms are unlikely to engage in earnings management. This is because aggressive earnings management practices are costly in terms of the loss of management’s reputation, legal responsibility of managers and other penalties that regulators and auditors can impose on the firm. Given the weak legal enforcement and inadequate external discipline by the market for corporate control in the Egyptian setting, we expect that corporate governance mechanisms will play negligible or no role in constraining earnings management during the financial crisis. To test this prediction, we run regression models by dividing the sample period into three sub-periods, namely, the pre-crisis period (i.e., 2005–2006), the crisis period (i.e., 2007–2008) and the post-crisis period (i.e., 2009–2012). Table 5 reports the results related to the three periods.

Regression Estimation Showing the Impact of Board Independence and Audit Quality on Earnings Management in Pre-, during and Post-crisis Periods

2. NEXECD = the percentage of non-executive directors on the board; BIG4 = a dummy variable that takes the value of 1 if the company is audited by Big Four or CAO auditors, and zero otherwise; BODSIZE = the total number of directors on the board; EXECOWN = the percentage of common equity owned by the CEO and executives of the firm; LARGHOLD = the percentage of shares held by the largest shareholder who owns 5 per cent or more of a firm’s ordinary shares; CEODUAL = a dummy variable that takes the value of 1 if the roles of chairperson and CEO are held by the same person, and zero otherwise; AUDCOM = a dummy variable that takes the value of 1 if the audit committee is composed entirely of non-executive directors, and zero otherwise; AUDTEN = a dummy variable that takes the value of 1 if the client–auditor relation started at least three years previously, and zero otherwise; LEV = the ratio of total debt to total assets; SIZE = natural logarithm of end-year book value of total assets of firm in million (Egyptian) pounds; ΔCFO = change in cash from operations as measured by cash from operating activities in the current year less cash from operating activities in the prior year, scaled by lagged total assets; SMOOTH = a dummy variable defined as the difference between pre-managed earnings, measured as reported earnings minus discretionary accruals generated from different discretionary accruals models, and firm’s earnings benchmark, measured as firm earnings in the prior year, taking the value of 1 when pre-managed earnings are above earnings benchmark, and zero otherwise; ASSINT = the ratio of gross fixed assets to total market capitalisation; ABSDNI = the absolute value of net income scaled by lagged total assets.

As we can see from the table, the coefficient of BIG4 is negative and statistically significant at the 1 per cent level. This result indicates that Big Four auditors provide an effective governance mechanism against earnings manipulation over the three periods. In addition, managerial ownership seems to play an effective role only in the pre-crisis and post-crisis periods. More specifically, the coefficient of EXECOWN is negative and statistically significant at the 5 (10) per cent in the pre- (post-)crisis period. However, there is no effective role for managerial and large shareholders ownership and board characteristics during the crisis period. These results possibly are consistent with the argument that, when the overall economy is down, managers are more likely to prefer accounting choices that enhance firm’s profitability and survival (Graham, Harvey, & Rajgopal, 2005). There is also evidence that adding more outside directors to audit committees may exacerbate earnings management activities during the crisis period.

We also partitioned the sample based on the ownership levels of managers and large shareholders and whether an audit committee is composed entirely of non-executive directors to test the conditional role of board independence and audit quality. 8 Overall, we find supportive evidence for the argument that firms audited by Big Four are less likely to engage in earnings manipulation at higher ownership levels and when an audit committee is composed entirely of independent directors. However, the role is more pronounced during the pre-crisis and post-crisis periods than the crisis period. As discussed earlier, this reduced role of audit function is possibly due to the absence of the complementary roles of other governance mechanisms (Magnan & Markarian, 2011). Interestingly, we find that, at higher levels of large shareholdings and managerial ownership, a greater representation of non-executive directors on the board and audit committee exacerbates earnings management activities during the financial crisis. Thus, the results suggest that large shareholders and managers are likely to prefer weak boards whose directors lack sufficient background (Magnan & Markarian, 2011), leading to higher earnings management. Management may prefer weak boards over strong ones to enhance firm’s profitability and boost future earnings prospects possibly until the economy recovers.

Robustness Checks

It is widely believed that it is easier for managers to manipulate current accruals relative to non-working capital accruals as they can exercise more discretion over the choice of regular revenue and expense items (DeFond & Jiambalvo, 1994). To test the sensitivity of the results after excluding depreciation, our regression is re-examined using the current discretionary accruals. The results are qualitatively similar to those documented earlier. Arguably, it is also possible that the results reported earlier result from the abnormality of absolute value of discretionary accruals. To correct for this possibility, the natural logarithm of discretionary accruals is used as a dependent variable. Our inferences drawn earlier do not change and the results are qualitatively similar to those found earlier.

Hribar and Nichols (2007) demonstrate that using absolute discretionary accruals as a proxy for earnings management might bias tests for rejecting the null hypothesis of no earnings management. Against the concern that the prior results might be driven by the usage of the unsigned discretionary accruals, the sample is partitioned into two subsamples based upon the sign of discretionary accruals, resulting in a Pos_DA subsample, which includes firms with positive discretionary accruals, and a Neg_DA subsample, which includes those with negative discretionary accruals. We find that Big Four auditors are effective in monitoring both income-increasing and income-decreasing accruals alike, although they are more effective with regard to income-increasing than income-decreasing accruals. However, adding non-executive directors is not related to positive or negative accruals.

In order to test the possibility that the relation between executive ownership as well as large shareholdings and earnings management is non-linear, the regressions are re-estimated after including the squared term of executives and large equity ownership. The results show no indication of such a non-linear relationship. Additionally, the sample is partitioned according to the median value of firm size. The results indicate that non-executive directors (Big Four auditors) play an in(effective) role in reducing earnings management irrespective of the firm size. In addition, executive ownership does not seem important in reducing earnings management in small firms.

Despite the careful treatment of the variables used in the analysis and the methodology adopted, the results of this study are subject to some caveats. First, as in any accruals-based earnings management study, a key issue regarding the explanation of results concerns the ability of earnings management proxies to adequately capture earnings manipulation activities. It is well known that measurement errors related to abnormal accruals measurement are of a concern. Although alternative discretionary accruals models and different measurement error-related variables are used, the findings are still not totally free of this concern. Second, the classification of directors into executive and non-executive directors is based on the information available in the financial reports of sample firms and that collected from the EGID. Accordingly, the reliability of this information depends in turn upon the reliability of its sources. Third, the corporate governance variables used in the empirical analysis are treated as exogenous. However, it is possible that the discretionary accruals and some of those variables are endogenously determined. Finally, it is worth noting that board monitoring and audit quality are only limited dimensions of corporate governance that could be used as effective mechanisms to constrain opportunistic earnings management. Therefore, ignoring other corporate dimensions could cause a correlated omitted variable problem if these dimensions (such as financial literacy of outside members, number of board meetings and number of audit committees’ meetings) are correlated to those included in the analysis.

Concluding Remarks

This study investigates the monitoring and disciplining roles of board independence and audit quality in constraining opportunistic earnings management in Egypt characterised by high ownership concentration and weak shareholder protection. Using a sample of 1,005 non-financial Egyptian firm-year observations, over the period 2005–2012, we find support for the notion that increasing the ratio of non-executive directors on the firm’s board of directors or its audit committee may not be enough to adequately constrain opportunistic earnings management. This evidence is inconsistent with the view that greater representation of non-executive directors on the board is likely to be associated with stronger monitoring and hence, lower earnings management. We also find that the impact of the presence of non-executive directors on earnings management is likely to be contingent on the ownership levels of large shareholders and managers. Our explanation for this interaction is that at higher levels of ownership, large shareholders and managers attempt to signal their commitment to the wider public of not to manipulate earnings opportunistically by putting in place good corporate governance practices, including the appointment of more outside members on the board. We also demonstrate that firms audited by high-quality auditors are associated with lower magnitude of earnings management.

Our findings also show that corporate governance mechanisms are unlikely to act in isolation. At higher ownership levels of large shareholders, high-quality auditing acts jointly with non-executive directors to further reduce earnings management, while managerial ownership plays an effective monitoring role in reducing opportunistic earnings management when ownership levels of large shareholders is low. The result at lower ownership levels of large shareholders suggests a possible substitution role between executives’ ownership and large shareholdings. In a similar vein, non-executive directors and high-quality auditing act together to further reduce earnings management when managerial ownership is high and audit committee is composed entirely of non-executive directors.

The findings of our study should be of substantial interest to regulators and policymakers in emerging countries, and highlight the fact that there is no unique and universal corporate governance system that fits all and that the Anglo-Saxon model of corporate governance may not always be the optimal to follow. Thus, each country should design its corporate governance code in a way that matches its institutional, legal and political needs. Our results oppose the conventional wisdom that greater representation of non-executive directors on the board is necessarily associated with lower earnings management. The results also reveal that much of the weakness related to corporate governance in emerging countries may result from inadequate enforcement of the law and the weak legal protection of minority shareholders. In the Egyptian context, there is a need to put more emphasis on proper enforcement that protects minority shareholders’ rights, such as adopting cumulative voting to give minority shareholders the chance to elect their representative.

Footnotes

Acknowledgements

The authors gratefully thank the anonymous reviewers and the editor for useful comments and suggestions. The helpful comments of the participants at the 2013 European Accounting Association Annual Congress and the 2012 British Accounting and Finance Association Conference are also gratefully acknowledged.