Abstract

In countries with weak institutions, board governance becomes more important. This study uses a unique dataset from listed sub-Saharan African companies to examine the relationship between ownership composition and board compensation. It further analyses the association between board compensation and company performance. The findings indicate that board ownership and chief executive officer ownership are positively associated, whereas state ownership and concentrated ownership are negatively associated with board compensation. There is no evidence of a significant association between chairperson ownership or foreign ownership and board compensation. Finally, there is a negative but not significant relationship between board compensation and company performance.

Keywords

Introduction

Sub-Saharan African countries have weak institutional environments with the difficult enforcement of the laws and regulations (Rossouw, 2005). These weak institutions increase the managers’ degrees of freedom and call for effective board governance from directors that fulfil their fiduciary duties. In this article, we argue that the level of compensation may influence the board members’ fiduciary efforts. Using a unique dataset of sub-Saharan listed companies, we study whether the level of board compensation may be influenced by the ownership structure of the company (Connelly, Hoskisson, Tihanyi, & Certo, 2010). We further investigate the association between board compensation and company performance.

The literature highlights that directors’ effectiveness is related to their ability to monitor and advise management (Adams & Ferreira, 2007; Hahn & Lasfer, 2011; Hillman & Dalziel, 2003). More specifically, boards have the power to make, or at least to ratify, all of the important decisions, including decisions about investment policy, management compensation policy and board governance (Bhagat & Bolton, 2008). This power implies that boards can influence company performance.

Board directors are agents that represent the shareholders. As in any other principal–agent relationship, there is a potential agency problem. Bebchuk and Fried (2003) argue that just as there is no reason to assume that top management automatically seeks to maximise shareholder value, there is no reason to expect that directors will either. Moreover, as argued by Pant and Pattanayak (2010), directors’ fiduciary efforts may differ according to the ownership structure.

The conflict of interest between board members and shareholders can be mitigated through compensation (Mehran, 1995). Thus, we reason that board compensation is one of the issues that may influence the effectiveness of the board of directors. Kumar (2006) finds that dividend payout differs according to ownership structure. Likewise, Barontini and Bozzi (2011) argue that the level of board compensation could be related to ownership structure, but it could also signal the existence of agency problems or appropriate payment to high-performing directors. If an agency problem exists, there would be a negative relationship between excess board compensation and company performance. Alternatively, there would be a positive association between excess board compensation and company performance if compensation represents a premium that is paid to high-performing directors.

The empirical context of this study comprises companies listed in sub-Saharan Africa. We are motivated by the reforms undertaken by many sub-Saharan African countries (Jones, Morrissey, & Nelson, 2011; Rossouw, 2005) to attract foreign investment and to mobilise domestic savings and investment. These reforms include the establishment and adoption of good corporate governance mechanisms similar to those used in developed countries (Reed, 2002). It is argued that good corporate governance is important for economic development (Claessens, 2006) and that board governance is particularly important in countries with weak institutions such as those in sub-Saharan Africa. Nevertheless, studies on corporate governance in the African context are scarce (Adegbite, Amaeshi, & Nakajima, 2013), and, to the best of our knowledge, studies on the relationships among ownership structure, board compensation and company performance are non-existent. In this article, we aim to fill this void.

Our findings indicate that board member ownership and chief executive officer (CEO) ownership are positively associated with board compensation, while state ownership and concentrated ownership are negatively associated with board compensation. Moreover, neither board chairperson ownership nor foreign ownership is significantly associated with board compensation. These findings may be important for investors because they suggest that different ownership structures have different effects on board compensation. In regard to the effect of board compensation on company performance, we find no significant relationship between excess board compensation and company accounting performance measured by Return on Assets (ROA).

This article is organised in six sections. The second section describes the sub-Saharan African context. The third section reviews the existing literature and develops hypotheses. The fourth section describes the data and the variables. The fifth section presents and discusses the empirical results. Finally, the sixth section concludes the article.

The Institutional Context of Sub-Saharan Africa

Sub-Saharan Africa comprises 48 countries. All of these countries with the exception of Ethiopia and Liberia were colonialised by Western powers for many years. The colonisation influence is still present, as shown by the differences in languages, legal systems and memberships in the international organisations that are associated with the former colonies’ rulers. Most of these countries are prominently influenced by the British (Anglophone), the French (Francophone) and a few by the Portuguese. However, all of the countries included in our sample are under the influence of common law systems, lending a similarity to their laws and regulations that has important implications for corporate governance practices.

In recent years, several countries have undertaken many reforms with the intent of attracting foreign investment and mobilising domestic savings for investment to attain long-term economic development. Among the reforms undertaken are reforms related to corporate governance (Armstrong, 2003; Rossouw, 2005). These reforms follow the wide recognition that corporate governance contributes to the economic success of companies and their capacity for long-term sustainability (Armstrong, 2003). Furthermore, it is argued that good corporate governance can improve market discipline, corporate responsibility, transparency and reputation, which in turn can attract foreign and local investors (Armstrong, 2003; Rossouw, 2005).

Based on the expectation of benefits from corporate governance reforms, many countries across sub-Saharan Africa have established corporate governance codes. One important feature in these codes is the recommended self-regulatory approach: companies are encouraged not only to adopt the codes but also to consider good corporate governance to be a best business practice (Rossouw, 2005). Generally, the codes focus on corporate governance at the company level rather than at the regulatory level (Rossouw, 2005) and many are consistent with the international recommendations such as those articulated by the OECD (2004) and Cadbury (1992). This focus means that the objective of the codes is to assist companies in improving their internal corporate governance mechanisms. In particular, the codes address the separation of the chairperson and the CEO position and whether the boards should have a unitary or a two-tier structure. The codes for the countries included in our sample, for example, recommend separating the role of the chairperson from that of the CEO. In addition, the codes follow the unitary board structure, which includes both non-executive and executive directors.

Corporate governance mechanisms can be divided into internal and external mechanisms (Cremers & Nair, 2005), and the mechanisms can complement and/or substitute for each other. In other words, companies in practice are governed by a combination of both internal and external mechanisms. The OECD (2004) suggests that the presence of effective corporate governance systems both within an individual company and across an economy as a whole helps to provide a degree of confidence that is necessary for the proper functioning of a market economy.

The important external governance mechanisms are the legal, regulatory and institutional environments (OECD, 2004), which are considered to be weak in sub-Saharan countries (Kaufmann, Kraay, & Mastruzzi, 2009; Rossouw, 2005). The weak institutions in sub-Saharan countries challenge the companies’ governance systems and affect their performance and, therefore, their economic development in general.

Literature Review and Hypotheses Development

Jensen (1993) suggests that when external governance mechanisms are weak, the only solution is to strengthen the internal governance mechanisms. Thus, in sub-Saharan African countries, companies depend more on internal governance. The key internal governance mechanisms are the type of shareholders and the board of directors (Cremers & Nair, 2005). However, the relationship between shareholders and the board of directors leads to potential agency problems (Bebchuk & Fried, 2003). Shareholders, because they are the beneficiaries of the residuals, need to use monitoring and incentive mechanisms to induce the directors to pursue objectives that enhance and safeguard the shareholders’ interests. We argue that the application of monitoring and incentive mechanisms depend on the company’s ownership structure. Thus, the ownership structure may affect board compensation (Connelly et al., 2010).

In the following, we build on the above arguments to develop hypotheses regarding the specific relationship between different ownership structures and board compensation.

Board Ownership

The primary responsibility of the directors is to provide a link between shareholders and management to ensure that shareholder interest is enhanced and protected (Fama & Jensen, 1983). However, Kumar and Sivaramakrishnan (2008) argue that delegating governance to the board improves monitoring but creates an agency problem because the directors may avoid exerting effort and become dependent on the CEO.

A possible solution for the agency problem is to align the shareholders’ and the directors’ interests by allowing the directors to be shareholders in the company (Jensen & Meckling, 1976; Jensen & Murphy, 1990). When the directors own shares in a company, they are likely to implement actions that would help to maximise shareholder value.

Agent ownership aligns the interests of the shareholders and those of the agent. However, agent ownership could also lead to the agent’s entrenchment (Ozkan, 2007). This entrenchment increases the agent’s political power, which in turn enables the agent to control and influence the key decisions of the company. This influence implies that the directors with a high share ownership could have more controlling power and could use corporate resources to their own benefit, such as increasing their own compensation (Ozkan, 2007).

These arguments suggest that there are two possible effects of board ownership on board compensation, as stated in the following hypotheses:

Hypothesis 1a: There is a positive association between board ownership and board compensation when ownership leads to board entrenchment.

Hypothesis 1b: There is a negative association between board ownership and board compensation when ownership leads to the alignment of interests between the board and the other shareholders.

CEO Ownership

According to agency theory, the agency problems between shareholders and management can be mitigated by managerial ownership (Jensen & Meckling, 1976). Thus, when the managers have an ownership stake in the company, their interests and those of the shareholders are aligned (Jensen & Murphy, 1990). We argue that the companies with a low risk of agency problems will deploy fewer resources to monitor management’s behaviour. In other words, the degree of the directors’ involvement in monitoring top management will be relatively low in the companies where the CEOs have an ownership stake. Therefore, as the directors may be compensated for their efforts (Cordeiro, Veliyath, & Eramus, 2000), we should expect CEO ownership to be negatively associated to board compensation.

However, CEO ownership not only aligns the interests of the managers and the shareholders, but it may also lead to management entrenchment, which could potentially cause company performance to suffer (Morck, Shleifer, & Vishny, 1988). An entrenched CEO can use his/her power to influence various decisions to his/her own benefit and to the expense of the other shareholders. These benefits may include high board compensation. Thus, we expect the companies with entrenched management to have relatively higher board compensation. Taken together, the combination of the alignment and the entrenchment arguments suggests that CEO ownership can have two different impacts on board compensation. Thus, we postulate the following:

Hypothesis 2a: There is a positive association between board ownership and board compensation when ownership leads to CEO entrenchment.

Hypothesis 2b: There is a negative association between board ownership and board compensation when ownership leads to the alignment of interests of the CEO and the other shareholders.

Chairperson Ownership

A chairperson 1 who owns shares in the company will be motivated to ensure that the board makes and approves decisions that prioritise the interests of shareholders (Connelly et al., 2010). In addition, because the chairperson is the leader of the board, he/she will set the agendas for board meetings (Brickley, Coles, & Jarrell, 1997), which designate the contents, process and direction of a meeting. This responsibility implies that the chairperson can add or omit any issue from the agenda without consulting the other directors, which grants him/her a great deal of power (Brickley et al., 1997). Given this combination of power over board meetings and the chairperson’s personal interest in the company in the form of shareholdings, it is likely that the chairperson may favour decisions that increase shareholder value. In this regard, the higher the proportion of shares in the company owned by the chairperson, the greater the desire they will have to minimise the level of board compensation from the company.

There is, however, also the possibility that the chairperson will use his/her power in the board meetings and his/her shareholding influence to propose and approve high compensation. This happens when the chairperson becomes entrenched and may influence personal gains at the cost of other shareholders. In particular, in countries with the weak protection of shareholders’ rights, such as in sub-Saharan African countries, this misuse of a chairperson’s power could be more frequent.

Thus, similar to the relationship between CEO ownership and board compensation, both the alignment and entrenchment perspectives (Morck et al., 1988) also apply to the relationship between chairperson ownership and board compensation. We therefore posit the following:

Hypothesis 3a: There is a positive association between chairperson ownership and board compensation when ownership leads to chairperson entrenchment.

Hypothesis 3b: There is a negative association between chairperson ownership and board compensation when there is an alignment of interests between the chairperson and the other shareholders.

State Ownership

Li, Moshirian, Nguyen and Tan (2007) argue that state ownership has a negative influence on directors’ compensation because it is often selected from among low-paid bureaucrats to act as state representatives. According to institutional theory (North, 1990), organisations need to conform to the established norms to obtain societal legitimacy. Li (1994) argues that when the state is a major owner, it is especially important for the board of directors to appear to be legitimate and accountable to the public. State ownership should therefore have a negative effect on the directors’ compensation because the compensation must be disclosed in the financial statements (International Accounting Standards Committee Foundation, 2010), which can be easily accessed by the public.

Many state-controlled companies have a large base of assets and other resources that, in one way or another, may be consumed privately by the directors. The directors in state-controlled companies may thus be willing to receive lower compensation than they would receive from non-state-controlled companies because of the implicit benefits gained from state-controlled assets. This potential trade-off reinforces our expectation that state ownership will be negatively related to board compensation. The existing empirical evidence supports this argument. For example, Barontini and Bozzi (2011) found that state-owned companies in Italy are associated with lower board compensation. Thus, we suggest the following:

Hypothesis 4: There is a negative association between state ownership and board compensation.

Ownership Concentration

Many sub-Saharan African companies are characterised by highly concentrated ownership. The degree of ownership concentration has implications for the strategy and policies of a company. One of the policies that might be affected is compensation. In companies with a high ownership concentration, the major shareholders will have a substantial economic incentive to monitor top management’s behaviour (Busta, Sinani, & Thomsen, 2014), whereas in the companies with dispersed ownership, the individual shareholders are unlikely to have sufficient motivation to do the same (Connelly et al., 2010; Filatotchev & Wright, 2011; Shleifer, & Vishny, 1986). Close monitoring reduces the agency costs and directs decisions towards increasing firm value (Busta et al., 2014; Shleifer & Vishny, 1986). Because large shareholders maintain close control over their interest in a company, they may not need to depend as much on the directors. Thus, because compensation may be considered to be an incentive to directors but also a cost incurred by shareholders, we expect that, where possible, the shareholders will seek to minimise these costs. This is supported in the literature. For example, based on the companies listed on the Milan Stock Exchange, Barontini and Bozzi (2011) found that board compensation is lower in the companies with more concentrated ownership. Therefore, we suggest the following:

Hypothesis 5: There is a negative association between ownership concentration and board compensation.

Foreign Ownership

Privatisation and trade liberalisation reforms in sub-Saharan Africa have attracted foreign investment (Asiedu & Gyimah-Brempong, 2008). Foreign shareholders may influence various policies, including board compensation. In general, foreign investors are more likely to demand better performance from their investments (Kimura & Kiyota, 2007). To achieve this performance, the foreign investors are likely to engage the best directors (Martins, 2011), who they believe will better manage their investments and generate good performance (Firth, Fung, & Rui, 2007). However, good performance often comes with high costs because the high-performing directors are likely to demand high compensation (Oxelheim & Randøy, 2005).

Foreign investment may create more challenges for the directors because they must simultaneously address the demands of the foreign shareholders and the local environment. For example, Oxelheim and Randøy (2005) suggest that the management of a company under foreign influence will be exposed to a clash between two corporate cultures and that the need to reconcile two or more systems will pose new challenges and tasks. Furthermore, the degree of international influence over a company is an important determinant of the complexity that it will face (Filatotchev, Stephan, & Jindra, 2008). Foreign shareholders who invest in countries with volatile institutions (Peng, Wang, & Jiang, 2008), such as many sub-Saharan African countries, could face more information asymmetry and may find it difficult to manage the risks associated with an uncertain institutional environment. In such environments, foreign shareholders may depend more on the directors to run the business, which may lead to higher director compensation.

It is more common to find foreign experts on the boards of companies with foreign shareholders. Normally, foreign experts are paid higher compensation than local employees in developing countries. For example, Leung, Zhu and Ge (2009) found a large compensation gap between local and expatriate employees in China. Given the prevalence of low compensation in sub-Saharan African countries (Asiedu & Gyimah-Brempong, 2008), we expect the companies with a high level of foreign ownership to pay higher board compensation than other companies. Thus, we suggest the following:

Hypothesis 6: There is a positive association between foreign ownership and board compensation.

Data and Variables

Data Collection and Sources

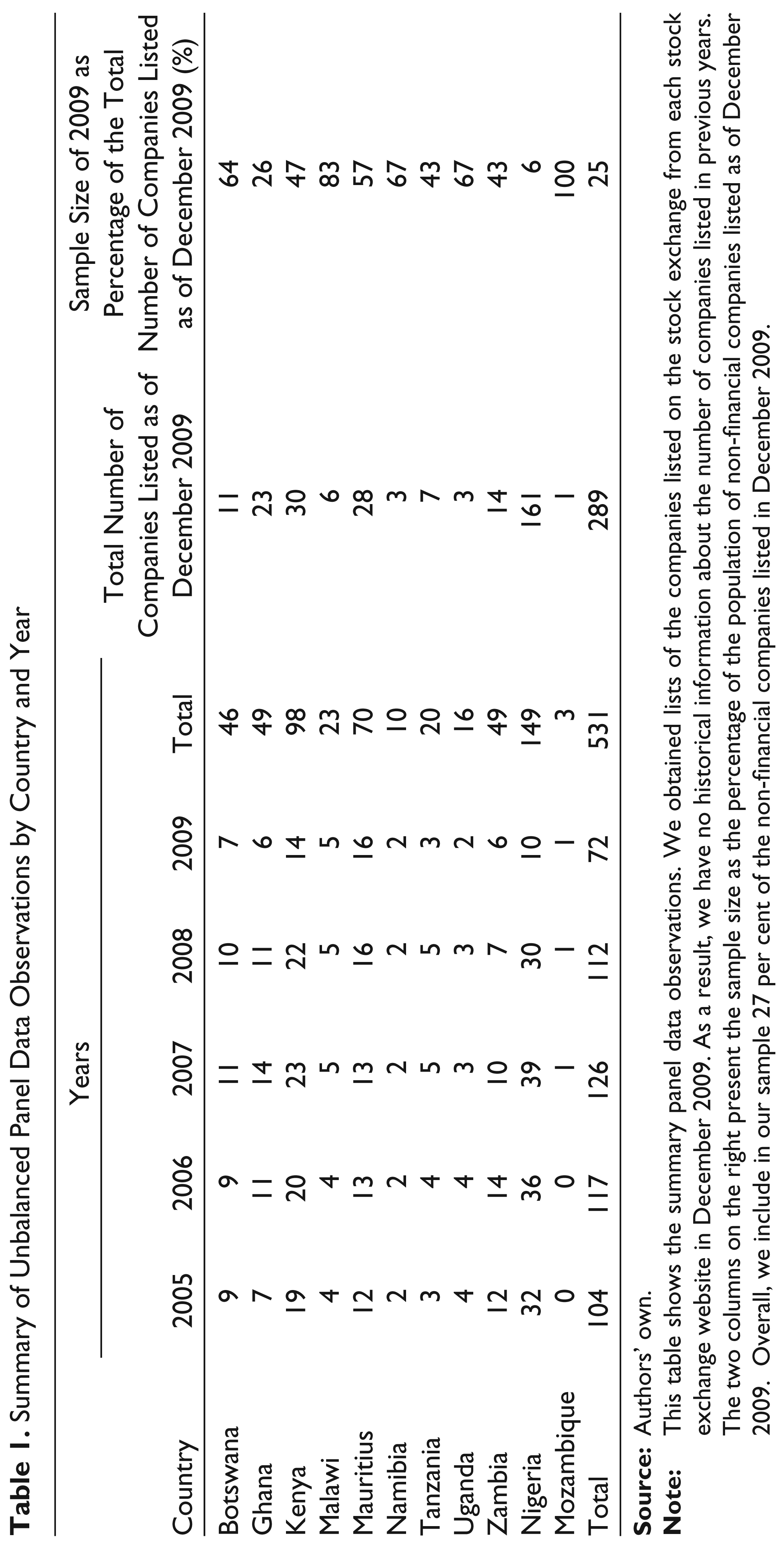

Former corporate governance studies from listed sub-Saharan firms have been single country studies (Barako, Hancock, & Izan, 2006; Ezeoha & Okafor, 2010). We bring the literature forward by presenting evidence from multiple countries. Our sample includes listed non-financial companies from countries that had active stock exchanges as of December 2009. However, we exclude South Africa, Zimbabwe and Côte d’Ivoire. South Africa is excluded because it has a relatively highly developed stock market in terms of market capitalisation and the volume of shares traded compared to other sub-Saharan African countries. Zimbabwe is excluded because of the hyperinflationary economic condition during the years for which the data of this study were collected. Côte d’Ivoire is excluded because their stock exchange is operated in French and we are unable to translate the information into English.

The names of the listed companies were obtained from the websites of the stock exchanges in each country. The dataset includes all companies listed as of December 2009.

2

Focusing on the non-financial companies, we then search for each company’s website using the Google search engine. Depending on availability, annual reports are downloaded from the companies’ websites. We also obtain annual reports from

Summary of Unbalanced Panel Data Observations by Country and Year

Many of the companies in our sample prepare their annual reports using the local currency. Therefore, we translate the financial data into US dollars using the yearly average exchange rate according to each country’s Central Bank.

Variables and Measures

Dependent Variables

Average cash compensation: the total cash compensation of all directors divided by the total number of directors. This measure of board compensation has been used in previous studies (e.g., Andreas, Rapp, & Wolff, 2012; Barontini & Bozzi, 2011). To reduce heteroscedasticity, we use the natural logarithm of the average cash compensation as the dependent variable in the regression analysis.

Independent Variables

Board ownership: the shares owned by all directors, excluding those owned by the CEO and the chairperson, divided by the total shares outstanding at year end. CEO ownership: the shares owned by the CEO divided by the total shares outstanding at year end. Chairperson ownership: the shares owned by the chairperson divided by the total shares outstanding at year end. State ownership: the shares owned by the state divided by the total shares outstanding at year end. Ownership concentration: the proportion of shares owned by shareholders who own at least 5 per cent of all of the shares outstanding at year end. Foreign ownership: the shares owned by foreign shareholders divided by the total shares outstanding at year end.

Control Variables

We include several control variables that can affect a company’s board compensation policy.

Company performance: High-performing companies have the ability to generate more resources, which can be utilised to pay higher compensation. Thus, we expect a positive association between company performance and board compensation. We use ROA (i.e., the operating profit divided by total assets) to measure company performance.

Company size: According to the literature, there is empirical evidence that company size is related to board compensation (Tosi, Werner, Katz, & Gomez-Mejia, 2000). Thus, larger companies are likely to pay higher compensation. We measure company size by the logarithm of the book value of the total assets.

Leverage: The literature suggests that leverage can be used as a corporate governance mechanism to control the performance of agents (Jensen, 1986). The companies with external debt are normally monitored by the debt holders; this monitoring helps limit high compensation. Moreover, debt obligations reduce free cash flows that could otherwise be used to pay higher compensation. We measure company leverage by the ratio of the book value of the total debts to the book value of the total assets.

Company growth: Complex companies require qualified directors who are capable of assuming the responsibilities that come with complexity. If the shareholders prefer a high-quality board that can effectively and efficiently monitor and advise management, they must be willing to pay compensation that is commensurate with the qualifications of the board members (Liu & Fong, 2010). Thus, we expect board compensation to be related to the complexity and the growth opportunities of a company. We measure company complexity and growth by the ratio of sales in the current year to sales in the prior year.

Ratio of foreign directors 3 : As argued in the hypothesis, foreign experts may be better paid than local directors. We therefore control for the percentage of foreign directors in the board which is measured as the ratio of number of foreign directors to the total number of all directors.

Institutional environment: This study covers different countries across sub-Saharan Africa, all of which have different institutional environments that might influence the relationship between the ownership structure and board compensation differently. Institutions are considered strong if they support free exchange between different parties in the market but weak if they fail to support an effective market (Meyer, Estrin, Bhaumik, & Peng, 2009). We expect strong institutions to support the effective functioning of various corporate governance mechanisms, including helping directors to conduct their duties in the most effective ways possible. Institutional environment is multidimensional, so we use multiple measures: a corruption index, gross domestic product and the percentage of the stock market capitalisation on gross domestic product.

Corruption: Corruption is a central and unfortunate institutional issue in most developing countries such as those in sub-Saharan Africa. Corruption is related to agency problems (Pinto, Leana, & Pil, 2008) and is therefore relevant when studying the relationship between ownership structure and board compensation. The corruption literature suggests that in the principal–agent model, the agent, in exchange for compensation or some sort of gain, has an incentive to favour a third party at the expense of the principal (Pinto et al., 2008). We argue that corruption could affect the board compensation either positively or negatively. Corruption could have a positive effect if the shareholders believe that they must pay the directors more to persuade them not to behave in a way that is corrupt. However, the effect of corruption could be negative if the shareholders perceive that they should be more involved in the business and would therefore not need to pay high compensation to the directors. To measure corruption, we use the Transparency Corruption Perceptions Index (TCPI) from Transparency International (Catrinescu, Leon-Ledesma, Piracha, & Quillin, 2009; Transparency International, 2011). This index ranks countries in terms of the degree to which corruption is perceived to exist (Transparency International, 2011). The higher the score, the lower the perceived corruption in the country.

Country economic performance: Specific country economic performance is likely to affect wages and salary levels, including board compensation. We use Gross Domestic Product (GDP) from the World Bank Development Indictors reports to measure a country’s economic performance.

Financial market development: Financial market development influences economic development (Enisan & Olufisayo, 2009; Ghirmay, 2004) and is related to the effectiveness of companies’ corporate governance systems and the companies’ performance. We expect high financial market development to reduce agency problems, which include controlling the directors’ ability to obtain high compensation. We measure financial market development by the percentage of stock market capitalisation on gross domestic product (La Porta, Lopez-De-Silanes, & Shleifer, 2006). We obtain this information from the World Bank Development Indicators reports.

Index of economic freedom: Finally, to control for the institutional environment, we include the index of economic freedom. The countries with high economic freedom are more likely to have low uncertainty and smaller agency problems, which are typically associated with high uncertainty. We expect the boards to be better compensated in the countries with a higher economic freedom index score. This information is obtained from the 2012 Index of Economic Freedom report, which is prepared by the Heritage Foundation.

Other control variables: Finally, we include the proportion of executive directors to control for the effect of the number of executive directors on the average board compensation. Where necessary, we also include country dummies, industry dummies and year dummies to control for country, industry and year fixed effects (FE), respectively.

Regression Method

Our dataset consists of unbalanced panel data with five years of observations. With this type of dataset, we can conduct regressions using pooled ordinary least squares (OLS), the FE method or the random effects (RE) method. To select the better method between the FE and the RE, we run a Hausman test (Hausman, 1978), which tests the null hypothesis that the coefficients estimated by the efficient RE estimator are the same as those estimated by the consistent FE estimator. The results of this test, which are not presented here, reject the null hypothesis, meaning that the RE method is consistent and efficient in this case. Additionally, we test for RE in the model using the Breusch–Pagan Lagrange Multiplier (LM), to decide between the RE regression and the OLS regression. The LM tests the null hypothesis that the variances across entities are zero. The results of this test, which are not reported here, reject the null hypothesis, so we conclude that the RE method was more appropriate than OLS. However, as a robustness check, we run the OLS regressions as well.

Descriptive Statistics

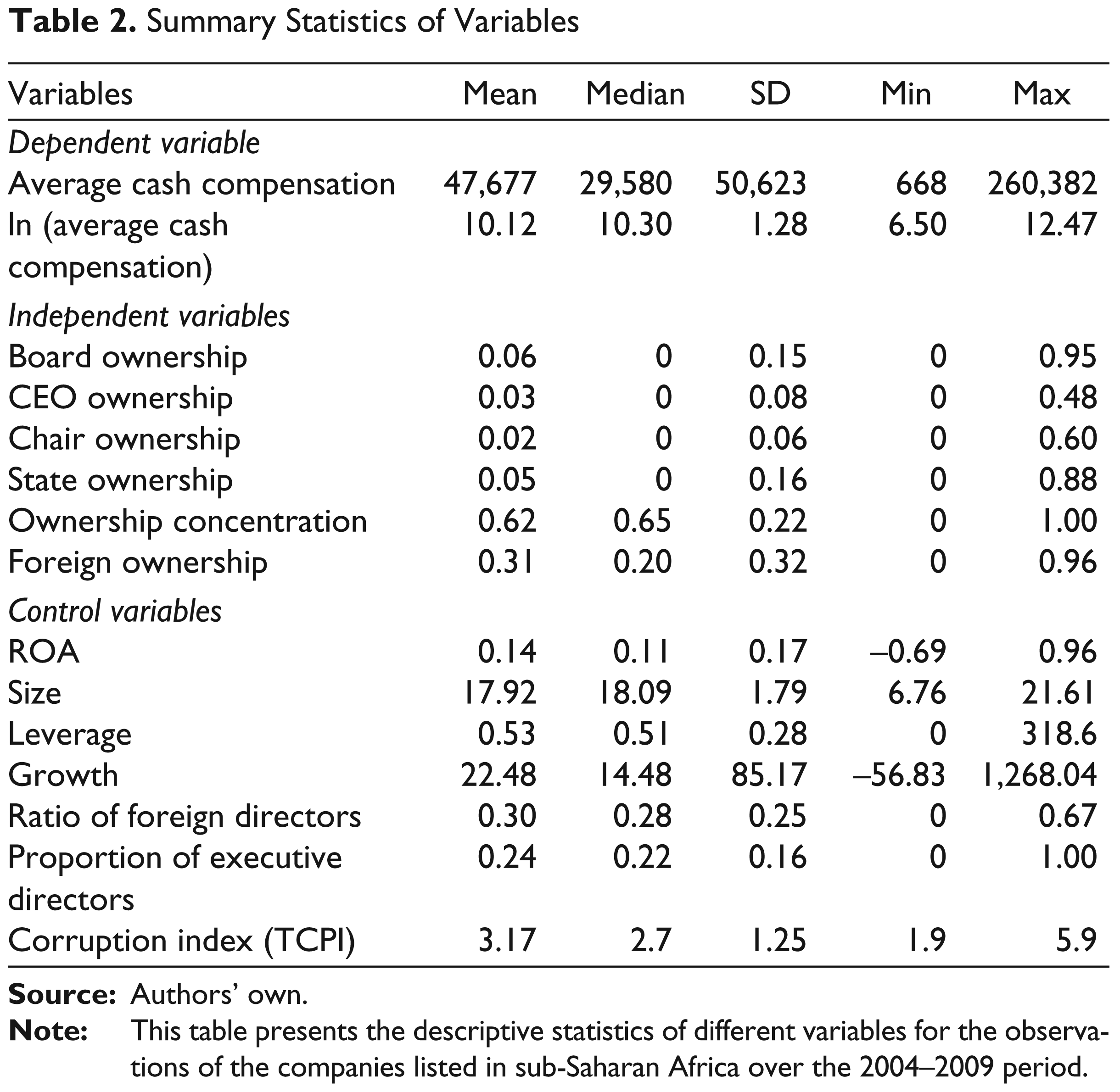

Table 2 presents the summary statistics for the overall sample. The table shows that the average compensation of the boards in our sample is US$47,677 with a median value of US$29,580, a minimum of US$668 and a maximum of US$260,382. This result indicates that there is high variation in the board compensation offered by the companies in our sample. The percentages of shares held by the board, the chairperson, the CEO and the government range between 2 and 6 per cent. Ownership concentration has a mean of 62 per cent and a median of 65 per cent suggesting that there is a high concentration of share ownership in the companies listed in sub-Saharan African countries. Foreign ownership has a mean of 31 per cent and a median of 20 per cent, indicating the importance of foreign investors in sub-Saharan African companies.

Summary Statistics of Variables

On average, the companies appear to be profitable with a mean ROA of 14 per cent. The mean leverage is 0.53 and the median is 0.51. This suggests that the debt holders may influence company matters, especially those related to the use of cash flow including board compensation. Our sample shows a high variation in sales growth, which ranges from –57 percent to 1268 per cent, with a mean of 23 percent. Finally, our sample shows that the groups of executive directors and foreign directors each represent approximately one quarter of all directors.

Table 3 shows a simple correlation matrix. Board compensation is negatively and significantly correlated with chair ownership and ownership concentration. In relation to the control variables, Table 3 indicates that board compensation has a positive and significant correlation with company size, company performance (Tobin’s Q), sales growth and the proportion of executive directors. As we see, none of the correlation coefficients are at a level that would indicate problems with multicollinearity in our regressions.

Simple Correlation Matrix

Empirical Results

The Relationship between Ownership Structure and Board Compensation

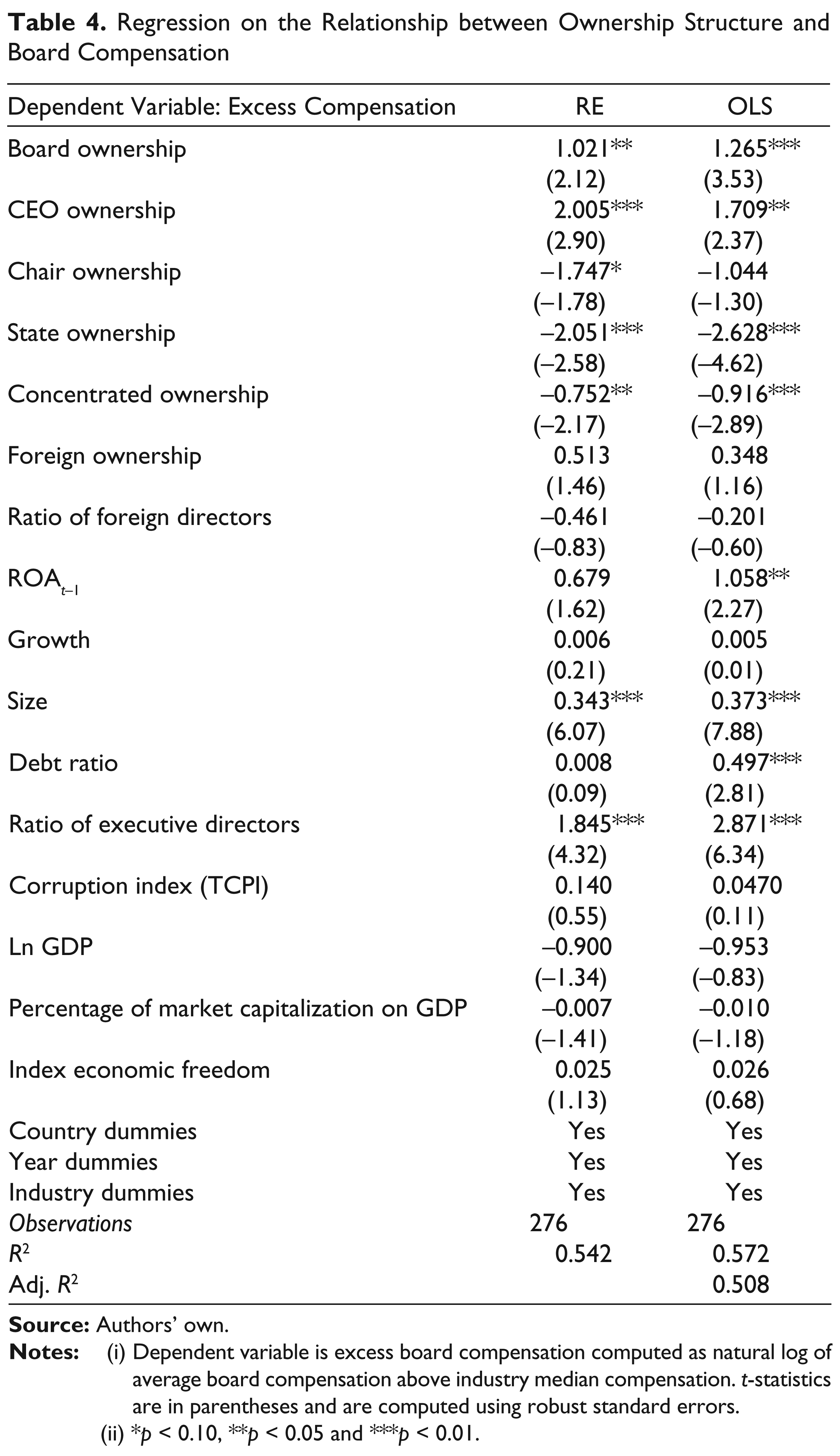

In this section, we discuss the results of the RE regression that are shown in Table 4. We use robust standard errors in the regression (Gujarati, 2003). The OLS regression results are also shown in Table 4 as a robustness check, but our discussion is based on the RE regression results. Nevertheless, there are few differences between the RE and the OLS regression results, which indicate that our results are robust.

Regression on the Relationship between Ownership Structure and Board Compensation

(ii) *p < 0.10, **p < 0.05 and ***p < 0.01.

Table 4 indicates that there is a positive and significant association between board ownership and board compensation (z = 2.12, p < 0.05). Hence, hypothesis 1a is supported, while hypothesis 1b is rejected. This result suggests that owning more shares is not a sufficient incentive to induce directors to accept low compensation. Thus, the directors’ shareholding leads to entrenchment rather than to alignment between the directors’ and the other shareholders. The directors in sub-Saharan African listed companies, on average, use their shareholding power and influence to obtain excess compensation from the company.

In relation to hypothesis 2, we find that there is a significant and positive association between CEO ownership and board compensation (z = 2.90, p < 0.01). This result supports hypothesis 2b, that is, that CEO ownership could lead to CEO entrenchment. Our results indicate that a high percentage of shares held by CEOs does not motivate them to protect the interests of shareholders, at least not by limiting the cash outflow that is paid as board compensation.

For hypothesis 3, we find that the coefficient of chairperson ownership is significantly negatively associated with board compensation (z = 1.78, p < 0.10). Thus, we find support for the alignment argument.

Hypothesis 4 suggests that state ownership is negatively associated with board compensation. This hypothesis is supported (z = –2.58, p < 0.01). Thus, the companies in which the state has a greater influence pay lower compensation than other companies. This result may suggest that these companies are operating under political constraints that limit the level of compensation paid to directors.

Hypothesis 5 states that the ownership concentration is negatively associated with board compensation. This hypothesis is supported (z = –2.17, p < 0.05). This finding supports the substitution argument that ownership concentration is a substitute for board services. When shareholders assume responsibility and become involved in the affairs of the business, they reduce their dependence on the services provided by the board, leading to lower board compensation. This finding is similar to those from Barontini and Bozzi’s (2011) study which found that more concentrated ownership is associated with lower board compensation in Italian companies.

Hypothesis 6 posits that foreign ownership is positively associated with board compensation. The results indicate that the coefficient of the foreign ownership is positive but not significant.

As for the control variables, we find, as expected, that company size is significant and positively associated with board compensation. Likewise, the results indicate that the proportion of executive directors is significant and positively associated with board compensation. The other control variables included in our regression model do not indicate any significant association with board compensation.

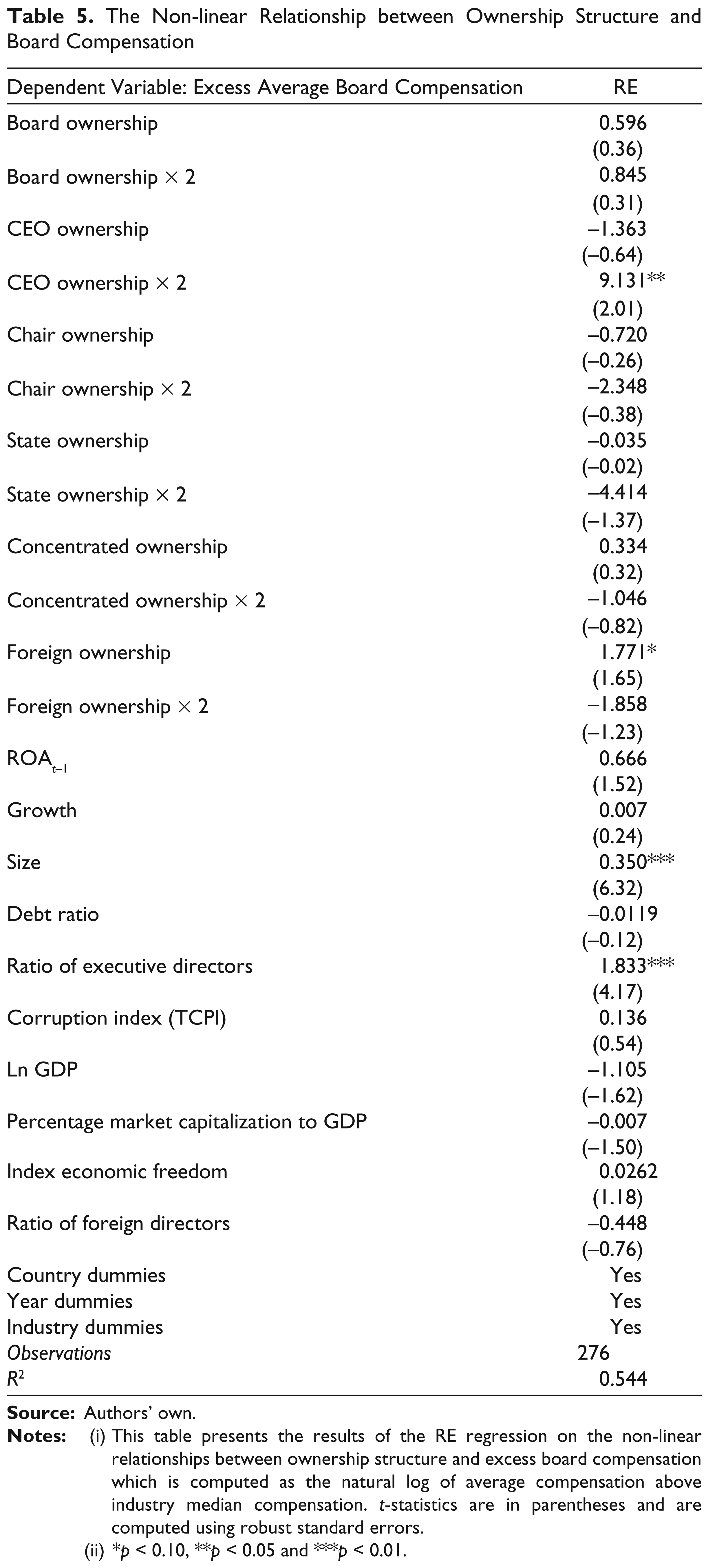

In our hypotheses and in Table 4, we only consider the possible linear relationship between ownership characteristics and board members’ compensation. It can, however, be argued that there could be a non-linear relationship between the variables. For example, it can be argued that when the state owns a low percentage of shares, there could be a positive relationship with compensation, while when the state has a high percentage of shares, the relationship becomes negative. Likewise, it can be argued that the negative relationship with compensation proposed for ownership concentration and foreign ownership only takes effect when the level of ownership is high (Li et al., 2007). Thus, to test for these possibilities, we now run an RE regression to examine the non-linear relationships between ownership characteristics and board compensation.

As shown in Table 5, the only significant quadrant relationship between ownership structure and excess board compensation is found for CEO ownership. However, the corresponding linear relationship is negative but not significant. This implies that there is no significant curvilinear relationship; rather, there is a minima point of CEO ownership beyond which CEOs become entrenched, and as a result, directors will receive high compensation.

The Non-linear Relationship between Ownership Structure and Board Compensation

(ii) *p < 0.10, **p < 0.05 and ***p < 0.01.

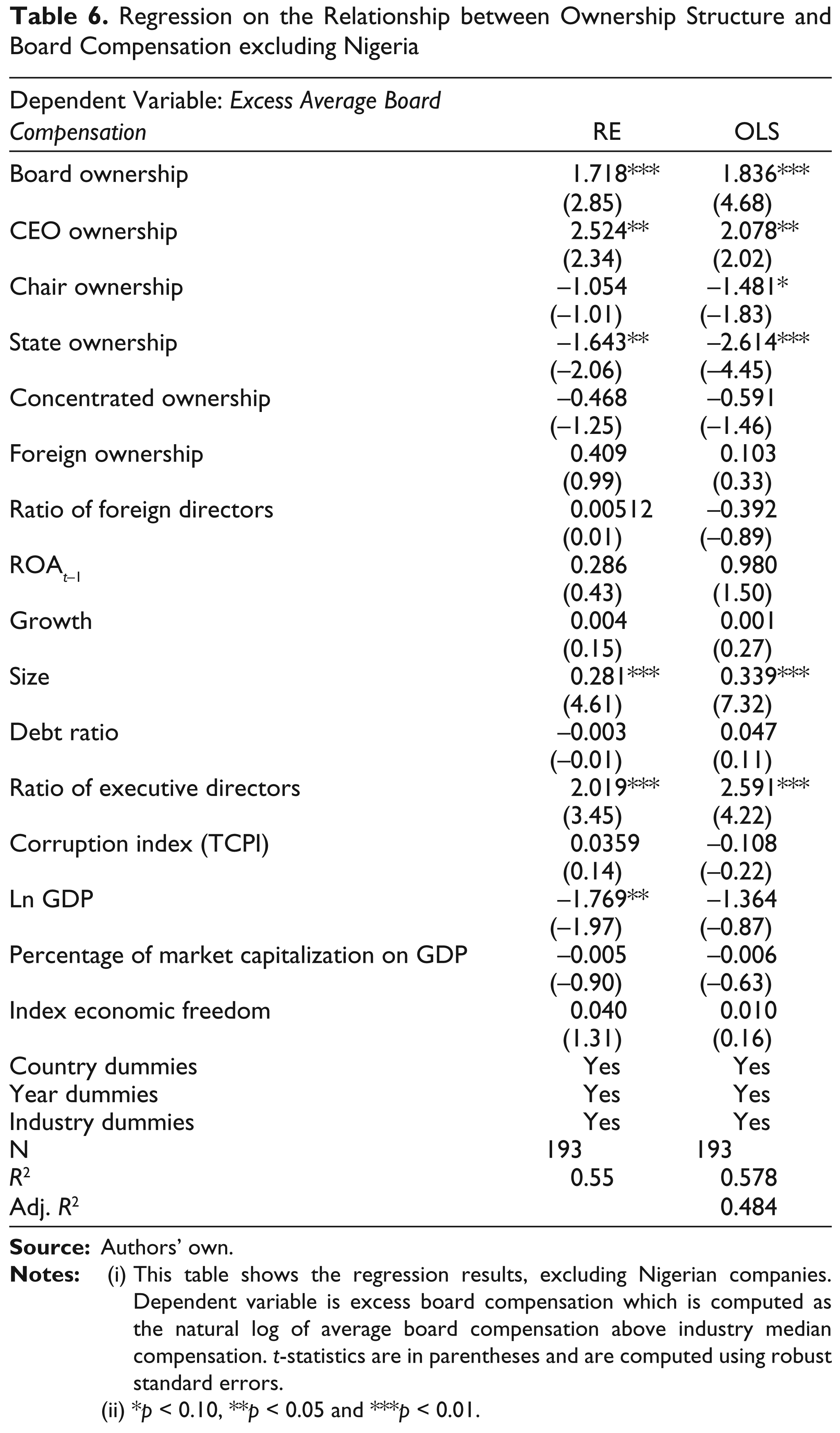

In the results presented in Table 4, Nigerian companies represent 28 per cent of the observations. This large proportion could influence the results. Therefore, we run similar regressions but exclude Nigerian companies to test whether the results in Table 4 still hold. The results of the regression excluding Nigerian companies are indicated in Tables 6.

Regression on the Relationship between Ownership Structure and Board Compensation excluding Nigeria

(ii) *p < 0.10, **p < 0.05 and ***p < 0.01.

As shown in Table 6, the results reported in Table 4 are upheld when excluding Nigerian companies in the regression. The only important difference is the coefficient of concentrated ownership, which is no longer significant. Overall, these results suggest that the Nigerian companies are not driving the results reported in Table 4.

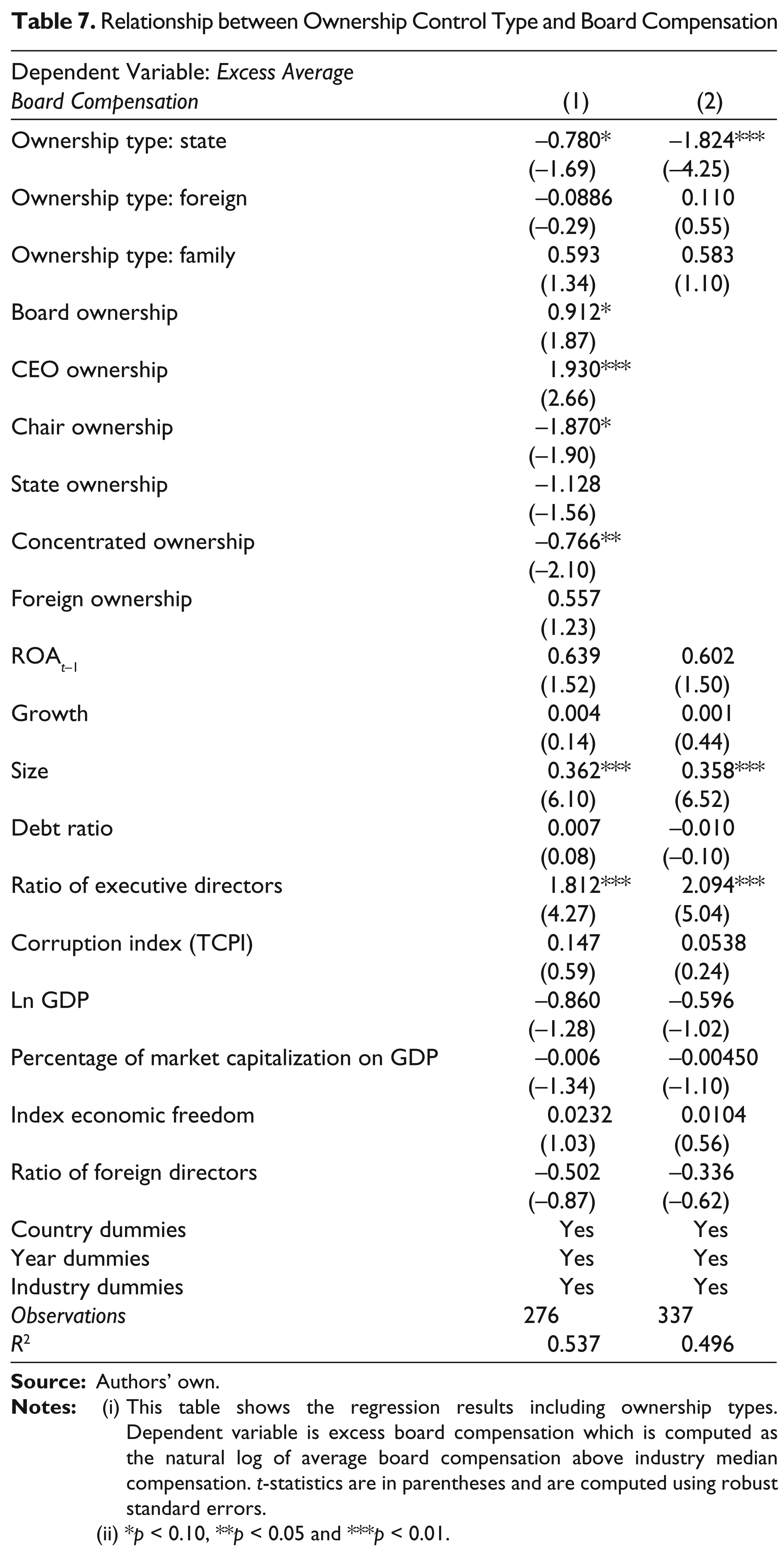

In hypothesis 5, we argue that ownership concentration may influence board compensation and the results in Table 4 indeed indicate that ownership concentration is negatively related to board compensation. However, it is also possible that the existence, whether large or small, of certain kinds of ownership may be related with board compensation. To test for this possibility, we examine whether the existence of state, foreign and family ownership in a firm is associated with the board compensation. Thus, we introduce dummy variables for state, foreign and family ownership and use dispersed ownership type as control group. The results are reported in Table 7.

The results presented in Table 7 are interesting since they show that it is the existence (the dummy) of state ownership that influences board compensation and not whether the state holds a larger or smaller percentage of the firm. Thus, firms with the state as a shareholder pay lower board compensations. For the foreign and family ownership types, the results are not significant. The results remain also when we run the regression without the ownership variables (column 2).

Relationship between Ownership Control Type and Board Compensation

(ii) *p < 0.10, **p < 0.05 and ***p < 0.01.

The Relationship between Board Compensation and Company Performance

Now, we examine the association between board compensation and company performance. We test this relationship by regressing company performance on excess board compensation, ownership structure and other company characteristics. Specifically, we examine whether excess board compensation, measured as a residual of the regression equation used in Table 4, is systematically related to company performance, measures of corporate governance and other characteristics of the company. In testing this relationship, we check whether the excess board compensation is a form of rent extraction caused by principal–agent problems between the directors and the other shareholders or whether excess compensation is a form of premium paid to the high-performing directors.

The relationship between company performance and board compensation could be susceptible to endogeneity concerns. With a panel dataset, endogeneity can be addressed by FE estimates with instrumental variables. To take this step, we must look for a valid instrument. However, in governance regressions, it is usually difficult to find an instrument that can pass the stringent test of validity. This difficulty occurs because in corporate governance studies, the variables that are considered to be the most correlated with the endogenous variable are the other governance characteristics that are already (or should be) included in the regressions (Adams & Ferreira, 2009). In this regard, we examine the relationship between excess board compensation and company performance by using the general method of moments (GMM) estimator, which specifically addresses endogeneity by using the lagged values of both the endogenous and the exogenous variables as instruments. This method is more appropriate in a situation where it is difficult to find instruments to address the endogeneity problem (Wintoki, Linck, & Netter, 2012).

The important consideration in the application of the GMM estimator is to ensure the consistency of the estimator, which depends on the validity of the instruments. Arellano and Bond (1991), Arellano and Bover (1995) and Blundell and Bond (1998) suggest two specification tests to test the validity of the instruments. The first test is the over-identification restrictions test, the Hansen test, which tests the null hypothesis that the instruments are valid. If this test result cannot reject the null hypothesis, the instruments are valid. The second test is the autocorrelation test, which considers the presence of second-order autocorrelation in the residuals from differenced equations (Arellano & Bond, 1991). If the test result p-value is large, it suggests that there is no second-order autocorrelation.

We measure company performance using the ROA. 4 We use the residual compensation from the regression model in Table 4 as the primary independent variable. We control for governance structure, company characteristics and year dummies. Furthermore, we test for the non-linear relationship between company performance and ownership structure.

Table 8 presents the GMM regression results. Our findings indicate a negative but not significant relationship between excess board compensation and company performance. These results suggest that excess board compensation in the companies listed in sub-Saharan African countries represents neither a form of rent extraction nor a premium paid to high-performing directors.

The Relationship between Board Compensation and Company Performance

(ii) Asterisks denote significance at the 0.01 (***), 0.05 (**) and 0.10 (*) levels. Company performance is measured using the ROA.

In relation to the ownership structure, we find that there is a linear negative and significant association between chairperson ownership and company performance. This finding supports the arguments in hypothesis 3, which suggest that chairperson ownership could lead to entrenchment, which could lead company performance to suffer.

The results in Table 8 further show that there is a negative non-linear significant relationship between CEO ownership and company performance. These results suggest that a high proportion of CEO ownership could lead to CEO entrenchment, which then negatively impacts the company performance. These results correspond indirectly to the results shown in Table 4, where there is a positive association between CEO ownership and board compensation.

Finally, Table 8 shows that with the exception of the lag company performance measures, there is no other variable with a significant coefficient.

Conclusions

This study examines the determinants of board compensation and the effect of board compensation on company performance for companies listed in sub-Saharan African countries over the 2005–2009 period. We examine board ownership, CEO ownership, chairperson ownership, state ownership, concentrated ownership and foreign ownership and examine their association with board compensation. We find that board ownership and CEO ownership both have a significant positive association with board compensation, while state ownership and concentrated ownership have a significant negative association with board compensation. Neither chairperson ownership nor foreign ownership is associated significantly with board compensation. We find no significant relationship between board compensation and company performance.

In a context with weak institutions, such as in sub-Saharan Africa, companies benefit little from external governance mechanisms. Thus, internal governance, and in particular, board governance, becomes important. In this regard, this study contributes to the literature on the link between ownership structure and board compensation and the effect of board compensation on company performance. In a practical sense, our findings are important for both current and potential shareholders. In particular, our results are important for companies, and stakeholders of companies, listed in sub-Saharan African countries.

Board members’ characteristics such as their experience and educational background may influence the level of compensation received. Unfortunately, we do not have access to this information and recommend it for future research. Furthermore, board compensation could be categorised into executive and non-executive directors, but we lack sufficient information to separate the compensation in this way. Although the same approach is used by others (e.g., Barontini & Bozzi, 2011), we believe that it would have been better if these categories were differentiated. In addition, our dependent variable only includes the cash compensation paid to directors as reported in the annual reports of the companies. However, a director may accept a position on a board because of stock options or the expectation of other benefits associated with directorship, such as substantial reputation enhancement and networking. The literature suggests that the value of a directorship lies in the opportunity to develop a reputation as an expert in decision control (Fama & Jensen, 1983) as well as a loyalist to the CEO (Hermalin & Weisbach, 1998), thereby increasing the value of the director’s human capital. Future studies could therefore consider that directors may receive benefits other than cash compensation.