Abstract

This article investigates the impact of board changes on the share prices of the companies listed on the Johannesburg stock exchange (JSE) during the period 2004–2008. Four types of board changes are investigated: new appointments, resignation, retirement and joint appointments. Market participants consider a change in the composition of a company’s board as having information content and produce statistically significant change in the share prices of the company concerned. In particular, the informational effects of new appointments are perceived differently by the market from resignations from the company board. The results also provide evidence that market reacts more favourably to the appointment of an executive director in comparison to that of a non-executive director board appointment.

Introduction

A board of directors plays an important role in ensuring good corporate governance, which should benefit shareholders through improved company performance (Schooley, Renner, & Allen, 2010). In theory, the ultimate responsibility for ensuring that firms are properly managed rests with shareholders, but with the separation of ownership from control, in most major business enterprises the responsibility for strategic decisions and ensuring that top managers discharge their day-to-day duties effectively and efficiently is entrusted to the board of directors. The board of directors should, in turn, act in the best interests of shareholders who they represent while also safeguarding the interests of other stakeholders.

While the trade-offs between shareholders’ interests and the interests of other stakeholders may be subject to considerable debate, it is clear that the role of the board of directors is to act on behalf of these stakeholders to guide the company and to act as the first line of defence of stakeholders’ interests against incompetence and poor management decisions. As board members possess power and influence over firm strategy, policy and decision-making authority, a potentially significant event in any company is a change in the composition of the board with the appointment of a new member of the board or an existing member ceasing, for whatever reason, to remain on the board (Bozec, 2005).

Currently, there is no study known to the author that has investigated the impact of board changes in South Africa on share prices. The primary contribution of this article is that it provides some evidence for South African listed companies of the impact on shareholders’ wealth due to changes in the composition of the board of directors. The study, while restricted only to the South African data, will provide a basis for comparison with the existing and subsequent studies in other developing countries and also with certain English-speaking countries with which it has strong business links and also with countries having similar regulatory framework for corporate governance.

Board Changes and Shareholder’s Wealth

Changes in the composition of the board could be beneficial for a number of reasons. All directors have the potential to influence policies and objectives of the firm and, therefore, performance. A new appointee to the board can bring a fresh and dynamic impetus to the operations of the firm. Extensive experience and knowledge can also be introduced by hiring a suitably qualified and experienced executive. Second, by displacing an ineffective board member, a signal is conveyed to the capital market that the firm is initiating procedures and actions that will increase its efficiency and, consequently, improve its future performances. Since the potential contribution of an individual member to the board cannot be observed directly, the performance of a firm’s share prices could be used as an indirect measure of the information contained in the change in the composition of a company’s board (Coles & Hesterly, 2000, p. 210).

A change in the composition of a firm’s board could take the form of a new appointment or some form of removal from the board; namely, (1) a new appointment, (2) resignation, (3) retirement and (4) death. Each of the above changes may or may not be considered important by the market. Previous studies in this area do not distinguish between the informational effects ofthe different type of board changes (Mahajan & Lummer, 1993; Hillier & McColgan 2006; Warner, Watts, & Wruck, 1988; among others).

Therefore, in this study the different types of board changes are examined separately to ascertain the impact that each type of change may have on the firm’s share prices. Each board change type may even convey more than one signal. For example, the resignation of a board member may have a positive impact if the market considers that the change will result in a new and better appointment as the replacement for the vacancy on the board. If, however, the market considers that the resignation is not good for the company, the impact on shareholders’ wealth may be negative. Since it is impossible to uniquely determine, ex-ante, the direction of the market’s interpretation, what is examined in this study is whether, on an average, the wealth transfer associated with each board change type is zero. It is an investigation of whether board changes in South Africa have information content which is reflected in share prices behaviour. It may be considered a test of the hypothesis that board changes have information content, which is captured in the share prices, versus the null hypothesis that board changes have no information content.

Board Changes and Share Prices

This study will use the share prices performance as an indirect measure of the information conveyed by a change in the composition of the management board. The dynamics of board changes discussed in Zajac and Westphal (1996) are not the issues examined in this study. A change in the composition of the board can occur for a number of reasons. First, firms may appoint a new member to the board as a means of increasing organisational effectiveness. Second, the new appointees may have demonstrated particular strengths in some areas. Third, even though not all appointees may prove, in time, to have been good, it can be argued that new appointments will not be made unless it is thought it will improve the company’s efficiency. In addition, a new appointment could be made simply as a signal to the market (Bozec, 2005). Data is not available that will allow the positive identification or even to infer with a reasonable probability of accuracy, the real underlying motive for a new appointment; therefore, it was decided to group together all new appointments. But if markets are efficient, firms will be punished if they make appointments for reasons other than the betterment of the firm. Therefore, a positive average reaction is expected from the market to new appointments.

Second, resignations from the board of directors may be considered good or bad depending on whether it is thought that it may lead to an improvement in the company’s efficiency. The impact of a resignation could, therefore, be negative or positive depending on the interpretation of the circumstances. Consider some of the reasons for a resignation. A resignation could be due to completely personal reasons not associated with the company itself and may deprive the firm of a valuable board member. This would normally be expected to provide a negative signal to the market with a consequent lowering of the share prices.

Resignations could also result from power struggles within the organisation and some of these may, effectively, be a little different from the dismissals of poor directors and a positive signal to the market that the average standard of the board of directors has increased. A resignation could be due to an expression of disquiet by the resigning director about what is going on within the company and in the absence of strong form of market efficiency it could be the signal to the market that something is amiss. Such resignations could provide a negative signal, at least in the short term. However, this may ultimately be a good thing if it highlights the deficiencies and forces the firm to put its house in order. Therefore, the likely direction of any impact of resignations on share prices is not unambiguous. Third, retirement should not convey any information to the market since it will not be a new information unless the retirement is sudden and more in the nature of a resignation.

Fourth, death of an existing board member deprives the firm of a, presumably, valuable board member and should usually elicit a negative signal. But it is possible that the market response to the management board changes due to the death could be good or bad depending on the circumstances. A death following a long period of ill health may be both (a) more in nature of a retirement and (b) an opportunity to introduce new dynamism into the firm’s management by providing the opportunity to appoint a fully functioning member of the board to replace a director who may be suffering ill health and possibly performing below par or not at all. In an efficient market the death of a board member will be processed according to the information content of the event and can be expected to be fully and speedily reflected in the share prices.

While the impact of changes due to resignations, retirements and death are not capable of being considered, ex-ante, a clear directional signal like new appointments to the board provide a great opportunity to convey the message of new dynamism into the management of the firms. The average effects of new appointments should, therefore, be positive. A smooth transition should also have some positive impact on the firm’s value.

The reaction of the share prices to a board change will indicate whether the market considers such a change significant or not. Since it is difficult to study the motives of a particular change, the relationship between the different types of board changes and the change in the average share prices is studied. The behaviour of abnormal share returns is examined. If the board member changes have no impact on the prices, the average effect of any type of change should be zero.

This study also examines the impact of non-executive director board changes in the light of the King (2002) recommendations that firms should appoint to their boards, non-executive directors. Non-executive directors are intended to bring independent judgement to bear on the issues of strategy, performance, resources, including key appointments and standards of conduct (Helland & Sykuta, 2005). The recommendation of the King 2 Report was for a significant number of non-executives to be appointed such that, their views can carry a significant weight in the decisions of the board. This study, examines the impact of board changes involving executive and non-executive directors. It is hypothesised that, if the appointments of non-executive directors are perceived as value relevant, the public announcement of such appointments should induce significant positive abnormal returns.

Previous Studies on Management Changes and Firm Value

Most of the studies on the effects of board changes on shareholders wealth are based on the United States data and report mixed results. Some studies report significant positive abnormal returns around the management change (Bonnier & Brunner, 1989; Furtado, 1986; Furtado & Rozeff, 1987; Rosenstein & Wyatt, 1990; Weisbach, 1988). However, there are also studies that report no significant abnormal performance (Borstadt, 1985; Klein, Kim & Mahajan, 1985; Reinganum, 1985; Warner et al., 1988). Mahajan and Lummer (1993) and Warner et al., (1988) also found no significant abnormal performance on the announcement of management change.

Bhana (2003) investigated the share market response to announcements of the CEO dismissals by companies listed on the JSE Securities Exchange during 1975–1999. It was found that investors react favourably to those announcements where the replacement of the dismissed executive was an outsider. The positive interaction between the origin (inside or outside) and the CEO appointment suggested that an outside appointment to a CEO position highlights the perception of the share market of the benefit from the break with the firm’s past policies.

Two opposing opinions have emerged with regard to the impact of non-executive directors on a firm’s performance: a positive view and a negative one. Empirical studies on the relationship between the appointment of non-executive directors and financial performance have supported both viewpoints (Cho & Kim, 2007).

Despite a clear trend among the United States firms towards a greater non-executive representation, there has been some debate regarding the effectiveness of non-executive directors as a governance mechanism (Judge & Dobbins, 1995; Rosenstein & Wyatt, 1990). It has been argued that non-executive directors often lack the time and information to meaningfully contribute to the complex management process (Aram & Cowen, 1983; Mintzberg, 1983). It has also been argued that boards are superfluous because the market provides powerful incentives for managers and shareholders to align their interests (Hart, 1983). The dominant role played by the CEOs in choosing non-executive directors also invite scepticism about the ability of the latter to make independent judgements related to the firm’s performance (Waldo, 1985).

Conversely, several studies posit that non-executive directors have a positive impact on the firm’s performance (Long, Dulewicz & Gay, 2005; Pearce & Zahra, 1992; Rosenstein & Wyatt, 1990). Lin, Pope and Young (2003) investigated non-executive directors’ appointment announcements in the UK over the period 1993–1996. The average market reaction was indistinguishable from zero, consistent with the view that shareholders do not automatically benefit from the appointment of non-executive directors.

Sample Selection and Research Methodology

Sample Selection and Hypotheses

Data for the study covers the five year period from January 2004 to December 2008. The time period chosen is mainly due to using the latest available data and resource constraints. All changes in the composition of the management board for firms that met the following criteria were collected from Business Day and the database of JSE Stock Exchange News Service (SENS). First, the date of the board change must be available. Second, there must not be any other major news announcement in the two week period surrounding the board change such as earnings and dividend announcements, mergers and major contracts. This criterion was to ensure that other variables that could affect the price around the period of management change are eliminated. Third, the price data necessary in the examination of shareholder wealth effects must be available from the McGregor BFA database. The sample that met the data selection criteria totalled 890 over the five year period. The final sample of board change announcements used in the study was 873 after excluding the observations for deaths due to the small sample size.

Table 1 presents the summary statistics of the distribution of different types of board changes investigated during the study period. The following hypotheses were tested:

Distribution of Board Changes by Year and Type of Change

H1: Board members possess power and influence over company strategy, policy and decision-making authority. Market participants would consider a change in the composition of a company’s board as having information content and will produce positive or negative share price reaction depending on the nature of the board change.

H2: Non-executive directors are perceived to be important monitors of the management and the providers of relevant expertise. Announcements related to the appointment of non-executive directors are regarded by capital markets as having information content and a discernable positive effect on the share prices of the affected companies can be expected.

Research Methodology

The test of shareholder wealth effects around the time of a company’s board changes is structured as an event study. This study examines the excess daily returns that accrue to shareholders around the announcement of the board change. For the purpose of this study it is assumed that if the board change contains no unexpected information, the abnormal returns can be expected to be zero. The test of the information content in the board change is, therefore, achieved by examining whether the abnormal returns in the test period are significantly different from zero. The methodology employed in this study is essentially a variance methodology which has been used in a number of previous studies as reported by Opong (1996). The main thrust of the methodology is that if board changes contain information that alters expectations concerning future cash flows, the release of such information will cause a change in investors’ estimates of the probability distribution of the firms’ future share prices and this may result in a change in the current price.

The methodology compares the abnormal returns in the test period with those of the estimation period when no board changes are made. Each firm is analysed in two time periods namely (1) a non-board change or estimation period followed by (2) a board change or test period. The estimation period covers a period of 134 days up to 16 days before the board change. The test period starts from 15 days before the announcement of management change through to 15 days subsequent to the management change. Time period zero is the day of the announcement of the management change. Normal daily returns were generated using the standard market model developed by Brown and Warner (1985). The market model is given by:

where R it and Rmt are the daily return to shareholders of firm i at the time period t and daily returns on the JSE All Share Index at the time period t , ϵ it is the abnormal return of firm i in time period t which is assumed to have a zero expectation and α and β are market model parameters.

The method employed by Cohen, Hawawini, Maier, Schwartz and Whitcomb (1983) to overcome the problem of beta underestimation caused by serial correlation was used when calculating the beta values for companies in the sample. Bradfield and Barr (1989) conducted a sensitivity study of the beta values of JSE listed companies. They showed that there is a statistical significance for two lagged terms, the contemporaneous term and one leading term. The Bradfield and Barr procedure was, therefore, used to calculate the beta values for companies identified as events.

Actual returns were subtracted from the corresponding normal returns to obtain excess returns according to the following:

where R

it

is the actual return of firm i in the period t, R

mt

is the return on the JSE All Share Index for the time period t and

The market model parameters in the estimation period are generated using the 134 daily price observations (from day -149 to day -16) before the release of the news about the management change.

One significant anomaly relating to the security generating process is the tendency of small capitalised stocks to outperform larger ones. The event study methodology should consider whether an appropriate adjustment for size needs to be made. However, Dimson and Marsh (1986) present evidence that where the measurement interval is short, the impact of size on the event study methodology is not significant. In the current study the measurement interval is 15 days on either side of the release of the information concerning management change and therefore the potential problem of size is considered so slight that it can be ignored.

The daily excess returns were averaged across the observations according to:

where ARt is the average across observations for the particular day t and e i,t is the excess returns for firm i for day t. These averaged daily excess returns were tested for significance using t-statistics according to:

where Sei,t = [var (ARt)]2 with var estimated over 134 days, –149 to –16.

The average values for the excess returns are cumulated over the test period days in order to observe the behaviour of excess returns over the test period given by:

where CARt is the cumulative excess return on announcement day t and ARt is as defined previously.

A test based on ranks is performed on the absolute values of the excess returns for each management change announcement over the test period. The mean rank for each trading day in the event window is compared with the expected value following Walmsley, Yadav and Rees (1992) and Opong (1996). The rationale for the non-parametric rank test is threefold. First, aggregating signed values may remove some or most of the effect of interest and will bias the test towards the acceptance of the null hypothesis that the management board changes have no shareholder wealth effects beyond what the market expect. Second, as pointed out by Patell (1976), equation (4) is not appropriate if the residual share price is not zero. Third, a small number of large values could affect the averaging process using equation (3). Since the sample size is large, this may not be a severe problem.

This non-parametric procedure based on ranks is described as follows:

Let xi,t be the rank of excess return for firm i on day t

Therefore, under the null hypothesis that successive xi’s are independent,

The test statistic used to judge the significance of xt, the mean ranking for a particular day t in the event window is:

Under the null hypothesis, Zt is a unit normal variate.

Discussion of Results

Initially, a total of 890 board changes were available for the study. Of these about 52 per cent were new board appointments and about 24 per cent were resignations. Only 2 per cent, a total of 17 observations, concerned death. The death category was excluded from the analysis due to the small sample size and, therefore the final sample was reduced to 873 board change observations. There is a steady increase in the number of new appointments over the study period and this could partly be explained by the publication of the King 2 Report (2002) which recommended that firms should also appoint non-executive directors to their boards. The number of firms and the distribution of announcement types during the period of the study are reported in Table 1. Out of the 873 board changes in the study about 53 per cent were new board appointments and about 25 per cent were resignations. Retirements (12 per cent) and joint appointments (10 per cent) make up the remaining categories of board changes shown in Table 1.

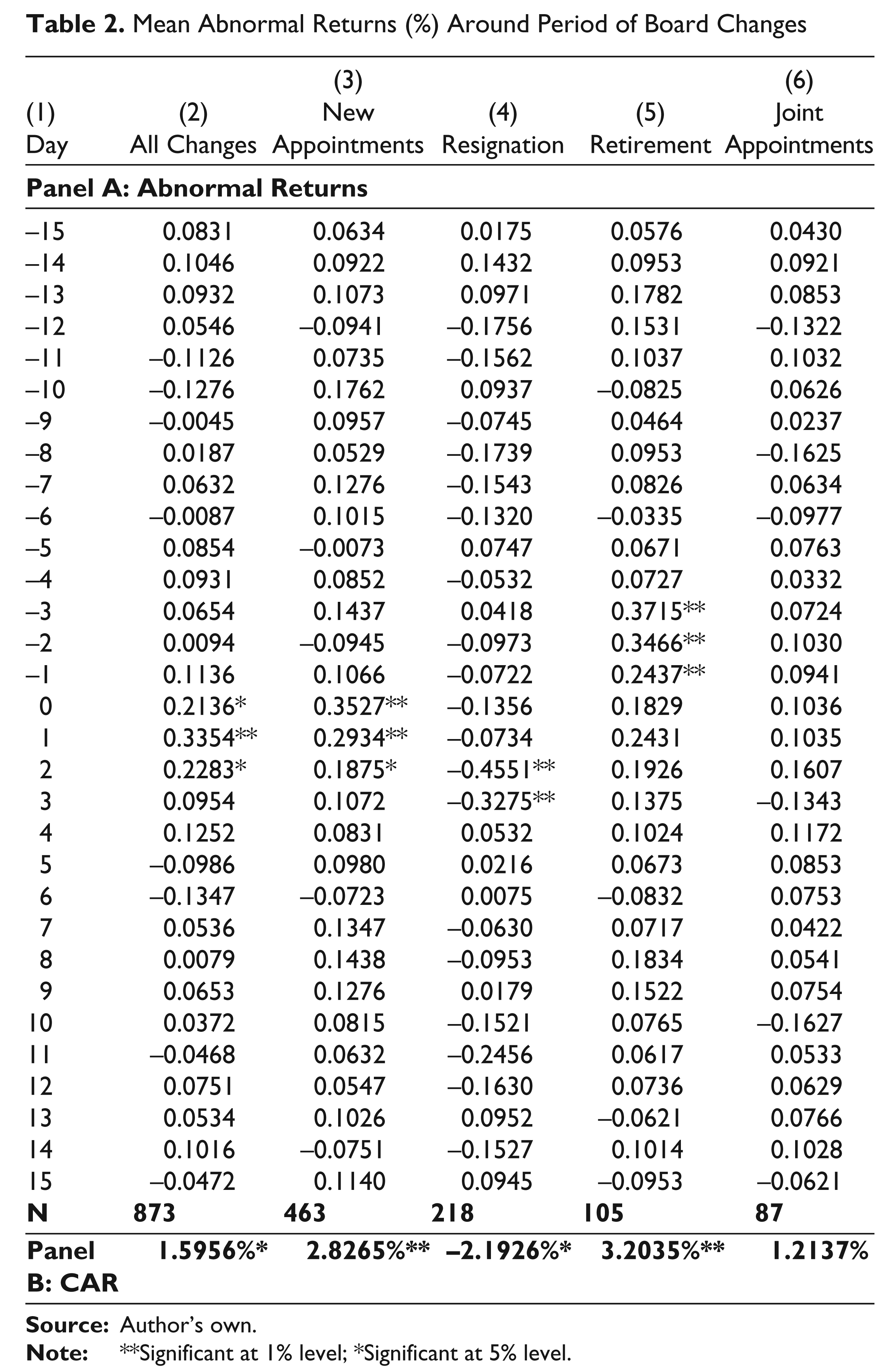

If the securities market is efficient, the positive as well as the negative abnormal returns are expected in the test period. The abnormal returns should not be statistically significant from zero. However, if board changes do contain price sensitive information then a significant price reaction is expected if such information had not been anticipated by the market. The shareholder wealth effects for all sampled firms are reported in Panel A of Table 2. Column 1 in Table 2 represents the day in the test period. Columns 2 to 5 represent the mean abnormal returns in the test period for the various types of announcement of board changes. The t-statistics associated with the mean abnormal returns reported in Table 2 are computed using equation (4). The t-statistics for the test period days that are statistically significant are shown with asterisks. Over the 31 day test period, the abnormal returns were statistically significant on the day of the announcement of all board changes at the 5 per cent significance level (column 2). Statistically significant abnormal returns are also observed for two days following the announcement of all board changes. On the days that the abnormal returns are statistically significant, they are also positive. This appears to indicate that shareholders experience positive wealth changes on an average when board changes take place. The market perceives board changes as something that is good for the firm. Similar results have been reported by Weisbach (1988) and Bonnier and Brunner (1989).

Board changes are also analysed according to the type of announcement. The result of the separate analysis of all new appointments is reported in column 3 of Table 2. The results appear to indicate that the market, on an average, takes a positive view of new appointments. Small but statistically significant positive abnormal returns are experienced on the day of the announcement as well as on the next two days subsequent to the public announcement of the new appointment.

The results of the board resignations are reported in column 4. It is noteworthy that only the statistically significant abnormal returns occur after the announcement of resignations from the board. This appears to indicate that shareholders suffer negative wealth effects but not until days two and three after the announcement; which also implies that the market takes some time to digest the information signals provided by the resignations.

The average perception of the market is that the board resignations probably signal some form of disquiet about what is happening in the firm. Resignations from the board may also be viewed as a public expression of some disapproval of policies being pursued by the firm. The results do not seem to support a different view that would imply that the board resignations may in the end be good for the firm. The results in Panel B of Table 2, column 4 shows a CAR value of –2.19 per cent and clearly support the alternative view that resignations are generally not considered a positive signal.

Mean Abnormal Returns (%) Around Period of Board Changes

Retirements from the management board are reported in column 5. The results show that significant positive abnormal returns are experienced by shareholders during the three days before the announcement of retirements from the management board. This might indicate that the market has anticipated the formal announcement. The positive shareholder wealth effects may be explained by the fact that retirements may be used to appoint new members, thereby bringing fresh and dynamic impetus into the firms operations. The fact that no significant abnormal returns are experienced on the day of the announcement of retirement shows that the market discounted the informational effects. This is not surprising since details of the retirement are usually released well in advance of the formal announcement.

Column 6 shows the results of mixed announcements where more than one announcement of different types are made on the same day. The results indicate that the impact of these combined changes is generally positive but not statistically significant. In fact, the CAR value for joint announcements is the lowest of the five different types of board announcements shown in Panel B of Table 2.

These results can be seen more clearly by examining the cumulative abnormal returns shown in Panel B of Table 2. Both new appointments (2.83 per cent) and retirements (3.20 per cent) produce fairly large positive and significant returns. Joint appointments (1.21 per cent) and all board changes (1.59 per cent) each produce small positive changes. Resignation (–2.19 per cent) is the only category of board changes to produce a negative and significant impact. It is noteworthy that a substantial part of the cumulative abnormal returns associated with retirements occur during the three days immediately preceding the official announcement.

Results of the non-parametric rank tests for each announcement type are reported in Table 3. Columns 2 to 5 represent the mean ranking for the highest values of the abnormal returns for each day in the test period. Given that there are 31 days in the test period, the expected value of the mean rank for each day in the test period is 16.

Differences between the mean for each day and the expected mean of 16 are tested for statistical significance using equation (9). The values marked with asterisks show the values that are statistically significant. The data for all sampled firms reported in column 2 of Table 3 indicates that the only day in the period around the management board change that shareholders experienced significant wealth changes beyond the market expectation is the day that the board change announcement was made public. Whereas the results in Table 2 column 2 indicate that shareholders experienced significant abnormal returns in test period days 0, 1 and 2; the reported results in column 2 of Table 3 indicate that significant abnormal returns are experienced only on the announcement day. The reported results in Table 2 could have been affected by a small number of large values of the abnormal returns whereas the mean ranking non-parametric test will not be sensitive to a small number of large values and thus provide a further check of the results reported in Table 2. The rank test indicates that shareholders experience wealth changes on the day of the announcement of a new appointment to the management board as well as on the day immediately following the announcement of the new appointment to the board.

It is important to note that whereas the negative but insignificant abnormal returns are experienced on the announcement of resignations from the management board reported in Table 2; the rank test reported in column 4 in Table 3 indicates that the mean abnormal return experienced on the announcement day is significant. A notable feature of the rank test is that the announcement day excess returns are significant for all board change types on the announcement day. It appears from Table 3 that significant excess are experienced nine days before the public announcement of resignations from the board. A reference to Table 2 indicates excess returns for day 9 for resignations are negative. A feature of column 4 in Table 2 representing resignations is the preponderance of negative values which is clearly shown by the CAR amounting to –2.1926 per cent.

Mean Ranking of Days Around the Period of Board Changes

Expected mean rank for each day is 16.

The results in Tables 2 and 3 support hypothesis 1, that market participants consider a change in the composition of a company’s board as having information content and produce an appropriate response in the share prices of the company concerned.

A further examination is conducted for changes that involve non-executive directors. The importance of non-executive directors stems from the concern about the system of corporate governance in South Africa which led to the King 2 Report (2002). Since the appointment of non-executive directors is a key recommendation of the King 2 Report, the impact of board changes involving non-executive directors is worth examining.

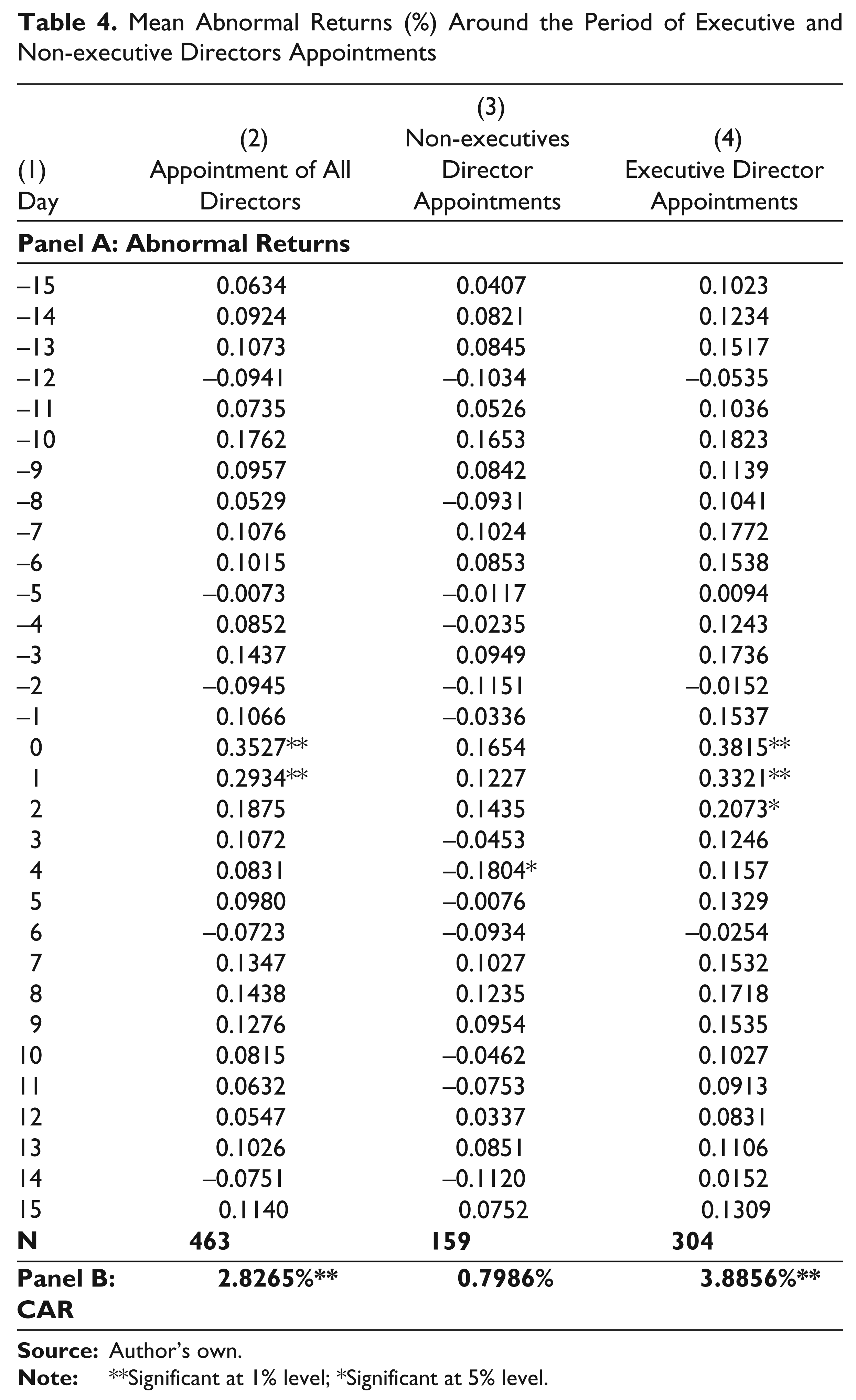

The results of the mean abnormal returns associated with the appointment of different categories of directors are shown in Panel A of Table 4. Column 1 in Table 4 represents the days in the test period as defined previously. Column 2 of Table 4 represents the mean abnormal returns for the appointment of all directors (executive and non-executive). Columns 3 and 4 show the abnormal returns associated with the appointment of non-executive and executive directors respectively. The appointments of all directors produce positive and significant abnormal returns on the announcement day and the following day (day 1). However, the appointments of new non-executive directors appear not to induce any significant returns on the announcement day. This appears to indicate some degree of scepticism on the part of the market as to whether non-executive directors could have any real impact in shaping policies of sampled firms. However, public announcement of new non-executive director appointments appear to induce significant negative abnormal returns at the 5 per cent significance level four days after the announcement, as shown in column 3 of Table 4. It also implies that the market takes some time to digest the information signals provided by non-executive director appointments.

The results reported in column 4 of Table 4 indicate that board changes involving the appointment of executive directors induce positive and significant wealth changes on the day of the public announcement and the two days subsequent to the public announcement. The CAR values in Panel B of Table 4 provides further evidence that market participants strongly prefer the appointment of executive directors over the appointment of non-executive directors. The CAR value (3.89 per cent) for the appointment of executive directors is large and statistically significant, whereas non-executive director appointments generate a CAR value (0.80 per cent) that is small and not statistically significant. The results reject hypothesis 2 which predicts that shareholders would prefer the appointment of non-executive directors because they are important monitors of the management and also providers of relevant expertise which is supposed to generate positive shareholder wealth effects. However, the impact of non-executive director board membership requires further study before any strong conclusion can be drawn.

Mean Abnormal Returns (%) Around the Period of Executive and Non-executive Directors Appointments

A key recommendation of the King 2 Report was for a significant number of non-executive directors to be appointed so that they can carry a significant weight in issues related to corporate governance. Intuitively, it seems that non-executive directors provide more effective governance due to their independence and lower self-interest in the benefits to be derived from the company’s performance. However, the results of this study show that investors tend to react more favourably to the appointment of executive directors. Investors appear to reason that the cost of self-interest and lack of independence on the part of the executive board members are outweighed by the benefit of the additional operational and strategic knowledge that executive board members provide to the deliberations of the board (Schooley et al., 2010).

Sector Specific and Institutional Shareholding Effects of Board Change Announcements

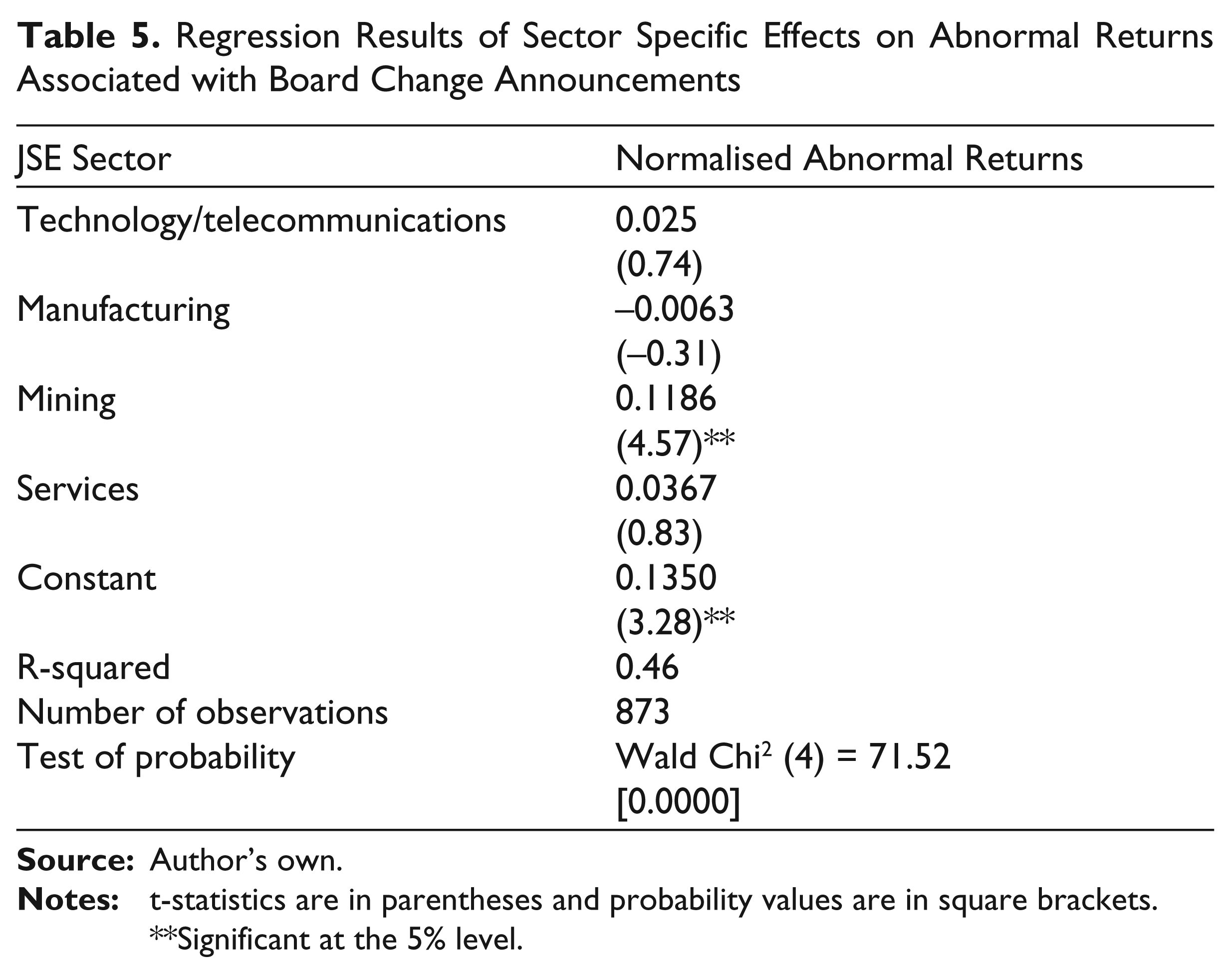

An analysis of sector category variables is undertaken to ascertain whether the specific sectors of the JSE classification of listed companies have any significant impact on shareholders’ reaction to board change announcements. Of the 108 companies representing the 873 board change announcements, 32 were in the industrial sector, 23 in the mining sector, 25 were in the mining sector, 10 in the technology/telecommunications sector and 18 in the service sector. This distribution is proportionate with the sectors representing all companies listed on the JSE.

A modified version of the regression model by Wen, Rwegasira and Bilderbeek (2002) is employed to determine the existence of sector specific effects. The modification of the model involves inclusion of sector category variables. This enables us to capture the impact of sector specific effects on the abnormal returns associated with board change announcements. The empirical model is specified as follows:

where i = 1, 2.. .. 108; t = 1, 2. . 5; Yi,t is a normalised measure of the abnormal returns for firm i at time t; β0 is the intercept; Z’i,t is a 1x k vector of observations on k explanatory variables for firm i at time t; β1 and β2 are the k x 1 vector parameters; and λi is the specific sector variable, and εi,t is the error term.

Table 5 presents the results of a categorical regression model run to ascertain the effect of the specific JSE sectors on the abnormal returns associated with board changes during the 2004–2008 period. In this model the industrial sector is used as the reference point to which all the other sectors are compared. The results show that the mining sector attains a higher abnormal return compared to the industrial sector. This confirms the empirical evidence that the mining sector is associated with relatively higher profits and thus is in a position to provide better abnormal returns to shareholders. Following closely are the technology/ telecommunications and services sectors which also appear to be providing higher abnormal returns to shareholders when compared to the industrial sector. However, the results are not statistically significant. The manufacturing sector on the other hand provides less abnormal returns to its shareholders compared to the industrial sector. These results are consistent with the relative profitability of specific JSE sectors. The shareholder reaction to board changes in the company appears to be in line with their perception of the profitability of the sector to which the company belongs.

Regression Results of Sector Specific Effects on Abnormal Returns Associated with Board Change Announcements

**Significant at the 5% level.

A regression analysis model is used to determine the extent to which institutional shareholding affects the abnormal returns arising from board change announcements. The regression model is specified as follows:

where i = 1, 2……..873; t = 1, 2…5; Yi,t is the predicted abnormal returns; b0 is the intercept; b1 is the regression coefficient; Xi,t is the percentage institutional shareholding in share i in the period t and ei,t is the error term.

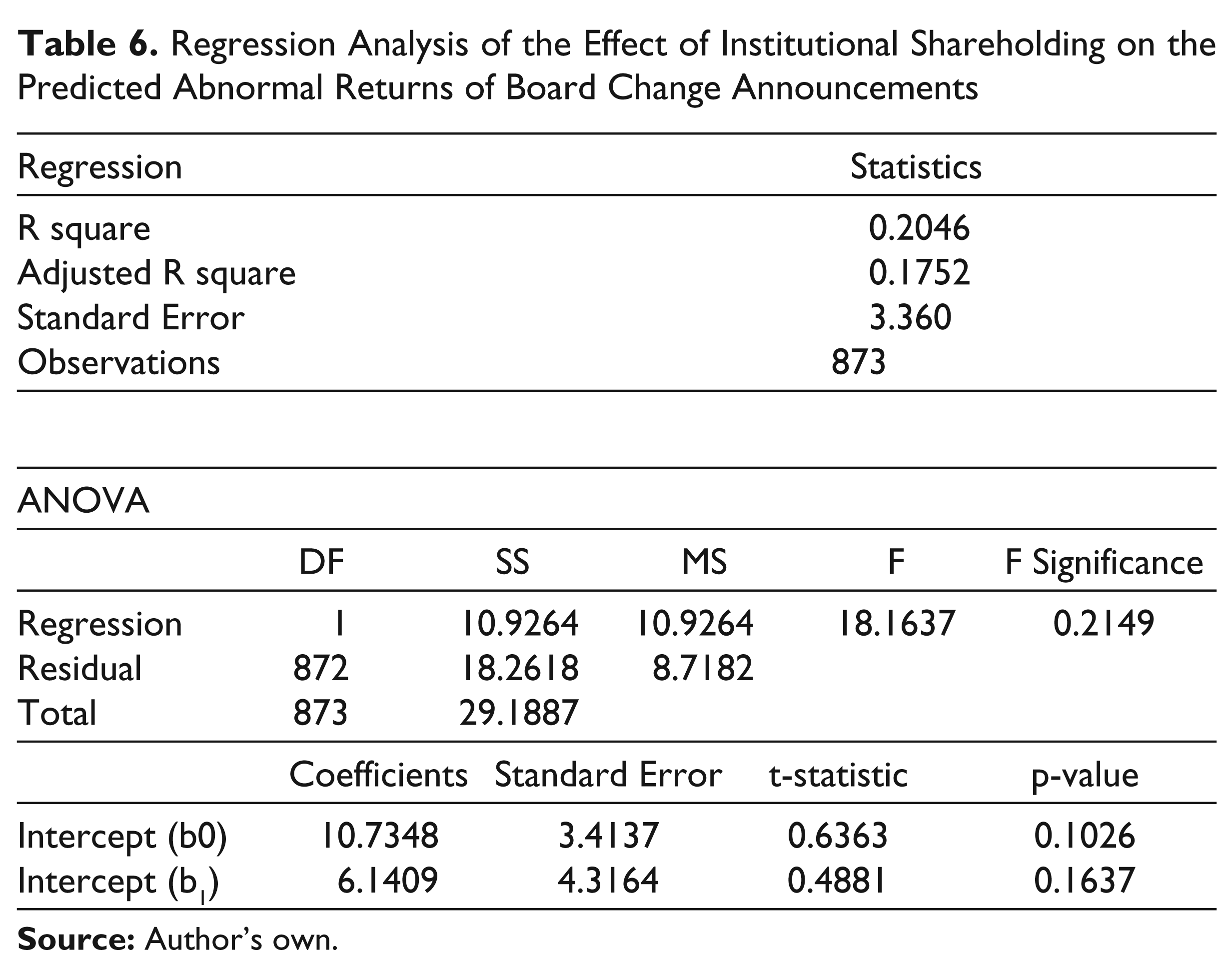

The results of the Excel output for the regression analysis are presented in Table 6. The results reveal that only about 17, 52 per cent variation in the abnormal returns can be explained by the institutional shareholding effect in a typical market reaction to the board change announcement. This is apparently low because more than 82 per cent of the variation remains unexplained. There are several reasons for this and one of them is that there might be some other influencing variables that have not been included in the regression model tested.

Regression Analysis of the Effect of Institutional Shareholding on the Predicted Abnormal Returns of Board Change Announcements

The poor predictability of institutional shareholding is confirmed by the insignificant t-statistics and p-values and also the insignificant F-test carried out in analysis of variance (ANOVA). These results are unexpected because the JSE institutional shareholders are dominant players in share trading and their involvement would normally have a major influence on the share prices. However, the results confirm the passive role that institutional shareholders play in share dealing on the JSE (Mkhize & Msweli-Mbanga, 2006). Institutional shareholders in South Africa prefer to remain neutral when voting on company matters at annual and other company meetings. In the cases where they are dissatisfied with the direction taken by a company they would rather sell their shares than seek a confrontation with the company management. The results of the regression analysis confirm the lack of influence of institutional shareholders in company’s internal matters such as the appointment of the board members.

Conclusion

This study provides some evidence on shareholder wealth effects of management board changes for companies listed on the JSE. The study distinguishes the wealth effects of different types of management board changes. The results of the study indicate that significantly positive wealth effects are experienced during the announcement period of the management change with the exception of resignations from the management board which are associated with negative wealth effects. The results also indicate that the share market discounts some information about board changes such as the announcement of retirements. Since board members possess power and influence over firm strategy, policy and decision-making authority, changes in the board’s composition could affect the policies and strategies that firms adopt. The policies that firms adopt will have cash flow implications that will affect the wealth of shareholders.

This study also has policy implications in the recommendation by the King 2 Report, that company boards should also include non-executive directors, who are expected to play a key role in corporate governance issues. However, the appointment of non-executive directors appears not to generate an enthusiastic response by the market, instead there seems to be a preference for the appointment of executive directors. However, further research is called for regarding the role of non-executive directors on the management boards. Since the securities market appears to discount information about management board changes, studies involving different types of board changes and its impact on company’s profitability would be of major interest.

Previous researches have indicated the existence of an expectation gap regarding the role of non-executive directors in addressing the issue of corporate governance (Fich & Shivdasani, 2006). The findings of this South African study seem to confirm several previous overseas studies showing that there appears to be no significant positive market reaction to the appointment of non-executive directors. Despite the importance of non-executive directors as a control mechanism to reduce the potential divergence between corporate management and shareholders, research concerning the role of non-executive directors is still in its infancy (McNulty, Roberts, & Stiles, 2005). Doubts have also been expressed regarding non-executive directors’ independence and limitations due to lack of information and lack of time to enable them to play a proper role in corporate governance. A suggestion to help improve corporate governance is to develop an international code of conduct for non-executive directors (Hooghiemstra & van Manen, 2004). Such a code of conduct may increase the understanding of what non-executive directors’ responsibilities are and how they have to perform their duties.

The poor shareholder reaction to the appointment of non-executive directors reinforces the views of many commentators on business and management who have suggested that non-executive directors tend to be friends and cronies of the chairman or chief executive and that non- executive directors were likely to have neither the time nor the intimate knowledge of the business to be able to act as an independent force on the board (Helland & Sykuta, 2005). Cai, Keasey and Short (2006) have suggested that the control of a large company is such a complex activity and a non-executive board member can have insufficient expertise and operational know-how about the business to be useful as a director, and consequently is reduced to be a figurehead. Stern and Westphal (2010) have shown that flattery, opinion conformity and ingratiatory tactics also play a role in board appointments and this may have influenced the poor market reaction to the appointment of non-executive directors.

A key finding of this study is that the market responds favourably to the appointment of executive directors and that the corresponding appointment of non-executive directors induces no significant wealth changes. However, several studies such as D’Aveni (1990), Kim (2007) and Ungson, Steers and Park (1997) have shown that non-executive directors provide social capital and external resources, which will have a positive effect on firm value. Social capital of non-executive board members will provide an organisation with exposure to information and knowledge of the external environment. With regard to the resource dependence role, non-executive directors in particular, can be regarded as a vital source for facilitating the acquisition of resources crucial to the firm’s success due to the linkages they have established.

To the extent that they are appointed to act as monitors of management, the governance benefits of non-executive directors are likely to depend to a large degree on the perceived agency problem. Lin et al. (2003) have shown that the market response to the appointment of non-executive directors is jointly determined by the magnitude of the agency problem and the monitoring incentives of the appointee. With respect to the agency problem, all things being equal, the greater the firm’s agency problems, the more beneficial non-executive directors are likely to be. However, the existence of agency problems alone, do not appear to be a sufficient condition for ensuring that shareholders will always benefit from the appointment of directors. It appears that non-executive directors must also possess the necessary time, expertise and incentives to carry out their board duties effectively. In the absence of such qualities, the appointment of non-executive directors may actually serve to destroy firm value by reducing board effectiveness. The use of proxies based on detailed information about the required characteristics and monitoring incentives of individual board members, therefore, offers a fruitful avenue for future researches.

This study has shown that the sector specific effects have an impact on the abnormal returns associated with shareholder reaction to board change announcements. The results are in agreement with a study by Kyereboah-Coleman (2007) which showed that the sector specific effects have an impact on shareholder wealth maximisation for South African companies listed on the JSE. Institutional shareholders do not appear to have an influence on the abnormal returns associated with board change announcements on the JSE.