Abstract

The article tries to reconcile theoretical predictions of the two most important capital structure theories with evidences for corporate financing in India. We identify that while the pattern of leverage supports the prediction of pecking order hypotheses strongly, the key arguments of the theory are missing. We also found a significant explanation for incremental changes in debt ratios caused by mechanical stock price movement as compared to the changes caused by the overall issuance activities of firms. Firms do not seem to readjust their debt ratios to counter the drift caused by these stock-related movements in debt ratios.

Introduction

How do firms finance themselves? Is there a particular way to finance? Why would they like to finance themselves in a particular manner? Similar questions have been a critical concern of extensive capital structure literature addressing both theoretical underpinnings as well as empirical anomalies. Despite of having extensive research, these questions seem yet to be perplexing and unanswered. There is still no broad consensus on the typical theoretical frameworks or on the tests employed for testing these theoretical predictions. 1

The most important theoretical underpinning for corporate financing choices comes in the form of a pecking order theory promulgated by Myers (1984) and the trade-off hypotheses initiated by Kraus and Litzenberger (1973). The original version of the pecking order introduced by Myers (1984) and motivated by Myers and Majluf (1984) was due to information asymmetry between firms’ insiders and outsiders. 2 In order to overcome the financing difficulties owing to the cost associated with such information asymmetry, firms in need of external financing tend to prefer issuing low information-sensitive securities as far as possible. Thus, there seems to be a pecking order where firms would use their internal funds first, followed by debt and very rarely would issue equity at last, owing to its high information sensitivity.

The form of the theory, although, had a rigorous appeal, its predictions of the pecking order could be due to several other reasons. For example, Leary and Roberts (2004) found that empirically information asymmetry may not result in the form of a pecking order described by Myers (1984). Moreover, Leary and Roberts (2010) assert that whatever pecking order is observed in the US firms could be explained by several other factors apart from information asymmetry such as incentive conflicts between the managers and shareholders. Further, there can be other forms of pecking order in certain situations. For example, although smaller and high growth firms face immense information asymmetry between insiders and outsiders, they tend to issue equity mostly for their financing needs.

The trade-off version, in its classical form, says that a firm maximises its value by issuing an optimal mix of debt and equity. The firm would inherently make a trade-off between the tax shields emerging out of incremental debt and the concomitant increase in bankruptcy costs. Accordingly, one can expect a firm to have a target debt ratio to which a firm would gradually move to.

Over a period of time, the trade-off theory has witnessed several developments both in terms of theoretical descriptions and empirical testing. Starting with a static framework of a trade-off between taxes and bankruptcy in the 1980s, the trade-off theory has moved to find the optimal capital structure in dynamic settings in the last decade. Although, these frameworks were applauded quite often for their plausible effects on real time firms, the empirical evidences left enough room for alternate explanations of the capital structure dynamics.

Owing to the difficulty of measuring the tax benefits and bankruptcy costs directly, 3 the empirical testing of the static version is primarily the testing of its predictions on the effect of firm-specific variables on debt ratios of the firms. Although the static version gained adequate prominence in the late 1980s and 1990s, 4 it was later undermined as results on testing its predictions could well be envisaged with alternate explanations involving no trade-off or a different trade-off other than between the tax and cost of bankruptcy. 5 Further, these predictions varied considerably in time and space. More importantly, it could not address the dynamic nature of rebalancing of debt ratios pertaining to several costs of adjustment.

Apart from conceptual and empirical divide in testing of the capital structure theories, these theories have definite implications for financing of firms in emerging markets. For example, Booth, Aivazian, Demirguc-Kunt and Maksimovic (2001) found persistent difference across developing countries in terms of the capital structure decisions. Similarly, Fan, Titman and Twite (2012) also found cross-sectional differences in the capital structure choices for 39 developed and developing countries.

Motivated by the arguments above, the article here investigates as to what extent the extant theories can explain the financing behaviour of firms in India. The article helps to explore the typical financing pattern of firms in India and contributes towards identifying the missing links in order to reconcile the theory and the evidences. The article differs from the past literature exploring conformance of the firms in India to these theoretical frameworks by identifying the strength of correlation of debt ratios with their previously known determinants. Rather we stress more on financing choices of the firms to draw inferences for such conformances. More specifically, we test the predictions of the pecking order hypotheses by observing the variation in incremental debt ratios caused by net issuance activity of the non-financial firms in India. Here, we would like to explore the relative importance of debt and equity issuances in determining the leverage structure of these firms.

The results of this exercise shows that although debt issuances dominate the overall issuance activities of the firm, the degree of explanation is not at par with that of firms in the developed countries. Further, the core issue of adverse selection does not seem to hold an appropriate explanation of the observed pecking order. Interestingly, consistent with Leary and Roberts (2010) and in contrast to Lemmon and Zender (2010), the issuance activity of firms seems to be uncorrelated with alleviating market concerns of information asymmetry. Market assessment of these issuance activities, as reflected by the changes in the stock prices, seems to be uncorrelated with the issuance of debt or equity per se. The results can be interpreted to imply that market signalling ability, if any, due to these issuances is rather modest.

While testing the trade-off version, there seems to be no evidence that firms follow a target leverage ratio. Firms in India seem to be on a deleveraging trail. The aggregate corporate leverage shows a consistent decline post-liberalisation. Further, the results suggest that this decline cannot be attributed to the changing composition of firms. While, deleveraging can be a firm’s own choice, there seem to be enough evidences against this proposition too. For example, Chauhan (2015) shows that systematic rather than firm-specific factors are responsible for the deleveraging of firms in India. The article argues that firms in India seem to be shedding debt due to capital constraints imposed on them by systematic institutional arrangements.

Capital constraints faced by firms also explains the low explanatory power of issuance activities in explaining the variation in incremental debt ratios. It is possibly the reason why firms could allow their debt ratios to drift overtime. The consequences of such capital constraints are manifested in higher corporate taxes being paid by firms overtime Chauhan (2015).

The discussions in this article also highlights that the complementary effects of sound equity markets to enable corporate financing are meagre. The effect of equity issuances on incremental debt ratios is only marginal at best. Further, good equity markets do not substitute well for low availability of capital in India. This is in contrast to the findings in Demirguc-Kunt and Maksimovic (1996) which shows that the development of stock markets is complementary for the development of credit markets for the developing countries.

The article is arranged as follows. The second section discusses the observed pattern of leverage for firms in India. This section puts forward the results of the econometric analysis for testing the pecking order and trade-off versions of the capital structure theories. The third section discusses the implications for the observed pecking order and the relative trade-off. The fourth section concludes and provides the future direction of the research.

The Financing Choice of Debt versus Equity

The pecking order hypotheses put forth a hierarchical view of firm financing in the order of retained earnings, debt and equity. In this section we intend to test the relative importance of this order by observing the effect of debt and equity issuances on incremental debt ratios of non-financial firms in India. The data in this article is constituted of all non-financial listed firms available in the Centre for Monitoring of Indian Economy (CMIE) between 1992 and 2013. We have used the methodology suggested by Welch (2004) to see the impact of the issuance activities on incremental debt ratios of firms. While Welch (2004) has employed Fama-Macbeth regression to estimate this impact, we intend to use fixed-effect models 6 for this purpose. The advantage with fixed-effect models is that they can control the time-invariant firm-specific factors and thus, control the changing sample composition of firms’ overtime.

The basic idea is to test whether changes in actual debt ratios correspond well with the issuance activity of any firm. This can be seen by isolating the effect of change in leverage due to stock price movement and that due to the issuance of debt and equity. For US firms, Welch (2004) has identified that changes accruing due to stock-related movement in debt ratios are less in magnitude as compared to changes accrued due to the issuance related activities.

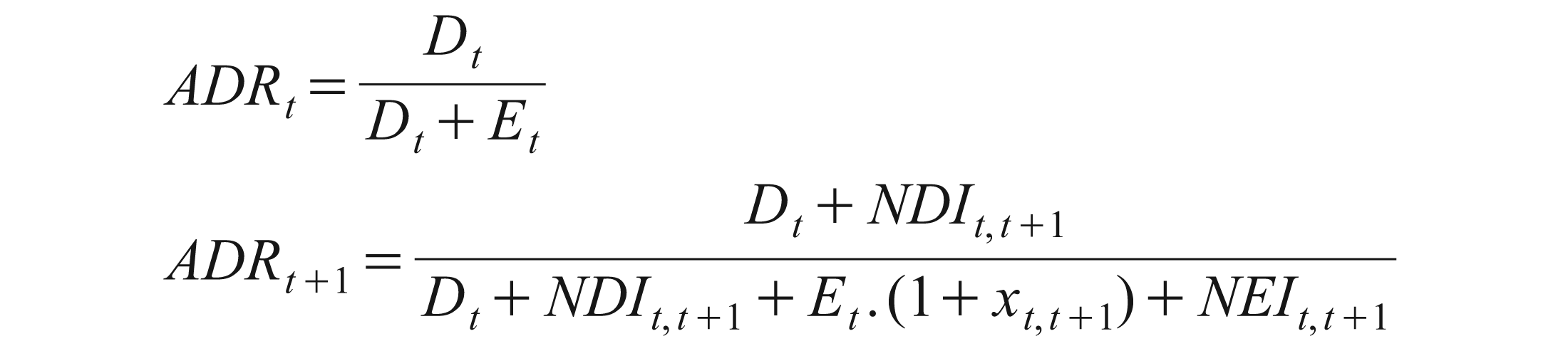

We have made use of the basic identities described in Welch (2004) to address the variation in incremental debt ratios. These identities are enumerated here for reference:

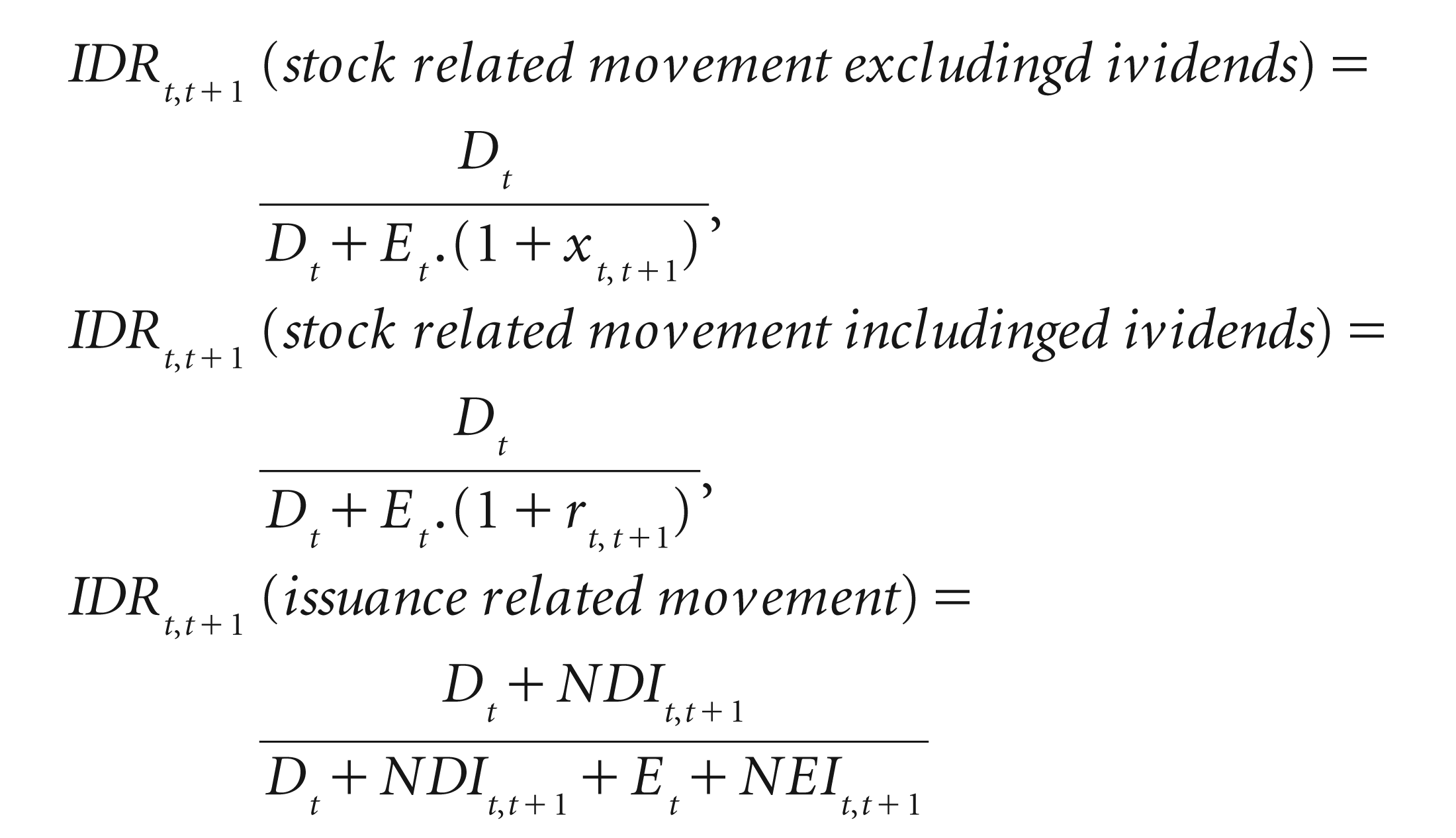

where ADRt denotes the ratio of book value of debt over the sum of book value of debt and market value of equity; Similarly ADRt+1 denotes the next period debt ratio. IDRt,t+1 denotes the next period implied debt ratio that would surface solely due to the equity returns or due to the net issuance activities in the form of equity and debt. ADR and IDR are estimated as follows:

where Dt = book value of debt at t = 0,

Et = market value of equity at t = 0,

xt,t+1 = equity returns excluding dividends,

rt,t+1 = equity returns including dividends,

NDIt,t+1 = net debt issued in a given year,

NEIt,t+1 = net equity issued in a given year,

From equation (1), the incremental change in debt ratios can be given as:

The fixed-effect model controls the changing sample composition by estimating within-firm changes and also controls the time invariant factors influencing the model. The model in the modified form becomes:

where Firmi is the within-firm time invariant effect. In our sample of more than 4300 listed firms, we have a panel of 53,168 firm-year observations. The data is winsorised at 0.5 percentile for all the measures of debt ratios at each tail so that the effect of outliers can be eliminated.

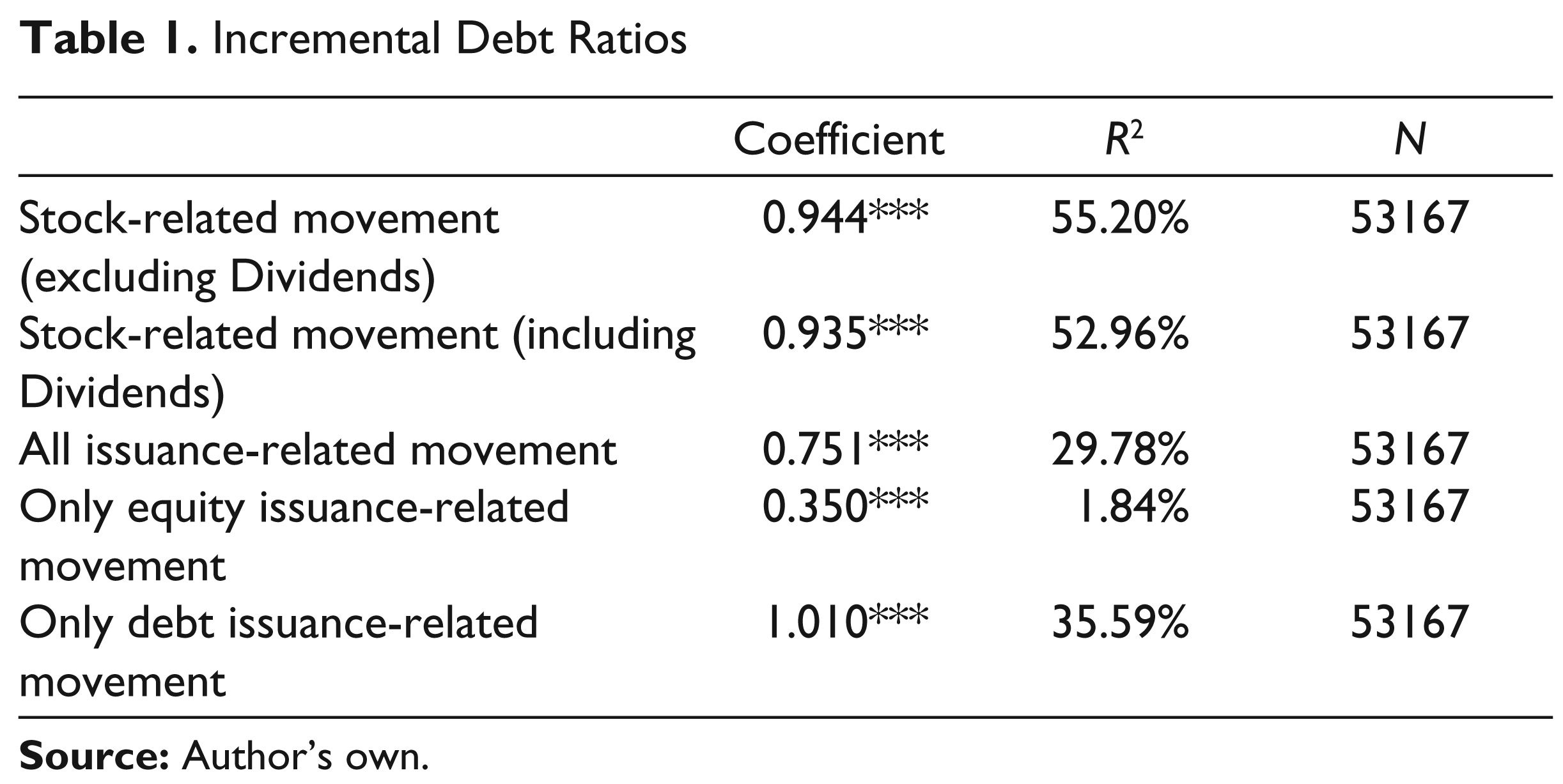

In our first attempt, we try to see how much of the variation in change of actual debt ratios are explained by stock-related movements during the year. Subsequently, we repeat the analysis for stock returns including the effect of dividend yields. Later we observe the effect of issuances in the form of equity and debt. Table 1 shows the summary of the results for the model described by equation (3) for the said effect of stock price and the issuance-related movements.

Incremental Debt Ratios

The results show that the stock price related movement, which is nothing but a mechanical drift in debt ratios, explains more than half of the variation. This implies that, on an average, most firms are not attempting to arrest the drift in debt ratios caused by equity returns in a given year. Further only 37 per cent variation in debt ratios are explained by the total issuance activity. Consistent with the predictions in the pecking order hypotheses, most of the variation caused by issuances is due to the issuance of debt. The effect of equity issuance is very low despite of the fact that India is endowed with a sound secondary equity market and not-so-good debt market when compared to the developed countries. The model in equation (3) controls the changing sample composition over the year; results reported in Table 1 are within-firm effects.

The percentage variation explained by stock-related mechanistic changes and those due to issuances are in contrast to the findings in Welch (2004). For US firms, the issuance activity explains more variation than which can be explained by stock-related movements.

The trade-off theory, in its classical form, did not find any place in Modigliani-Miller (1958) proposition. The static trade-off theory says that firms are actively maximising values through changes in their capital structure. At the root of this value creation is the trade-off between debt tax shields and firm-specific distress costs. Overtime there has been several updation regarding the static trade-off version in the form of dynamic models explaining the trade-off by including transaction costs, market frictions and speed of adjustments. 7

With regard to the predictions of the trade-off theory, an important idea is the adjustment of debt ratios to retain the relative debt-related advantage. A high degree of explanation due to mechanistic stock-related movements, as depicted in Table 1, shows that actual within-firm debt ratios are consistently drifting from their original values at the start of a year. On an average, half of the firms are just not readjusting their debt ratios in a given year.

Discussion

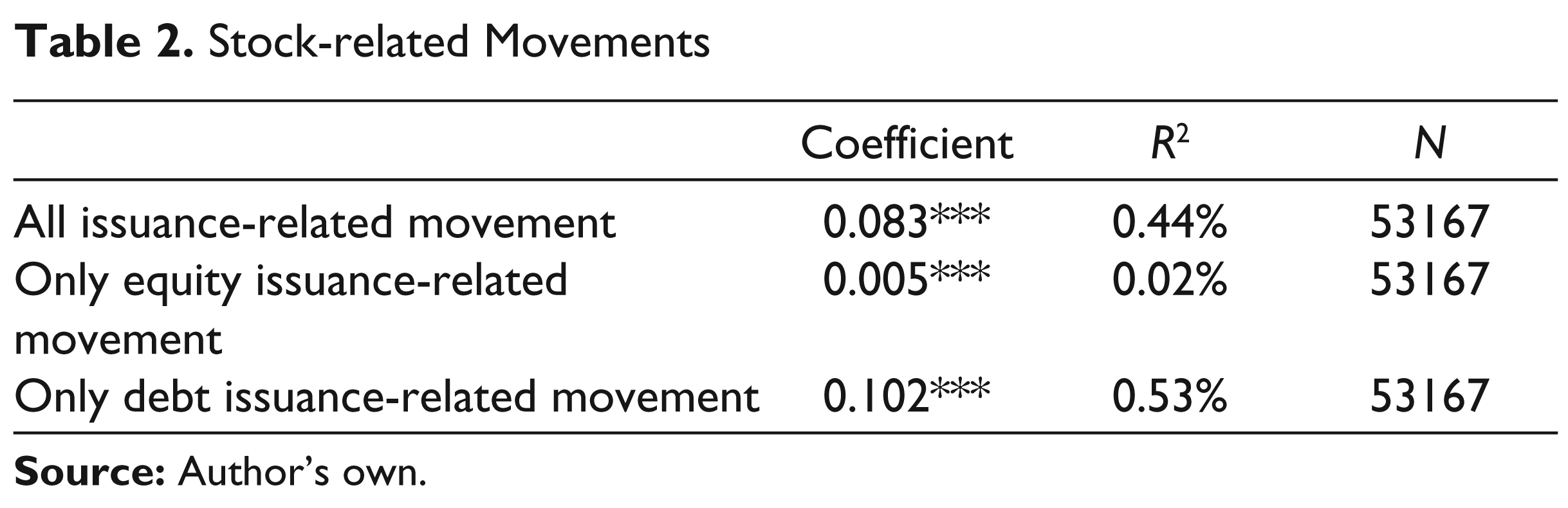

The results in the previous section reveal some important insights about the corporate financing pattern of firms in India. For a typical firm, if earnings are assumed to correlate with stock returns, the results are very much in line with the pecking order predictions. However, at the core of the pecking order hypotheses, the underlying idea is of information asymmetry between the lenders and the borrowers. Thus, issuances in the form of equity or debt should affect the equity returns of a typical firm. In other words, stock-related movement and the issuance-related movement of debt ratios should be correlated. Table 2 shows the results for within-firm regression of stock-related price movement on issuance-related movement of debt ratios. Quite surprisingly, the two movements in debt ratios are not at all correlated.

Stock-related Movements

Uncorrelated stock-related movements and the issuance-related movement of debt ratios highlights a theoretical challenge in accepting the predictions of pecking order hypotheses for firms in India. Issuances do not seem to be motivated by market reactions. In other words, the necessary signalling effect for alleviating information asymmetry is missing from the evidences.

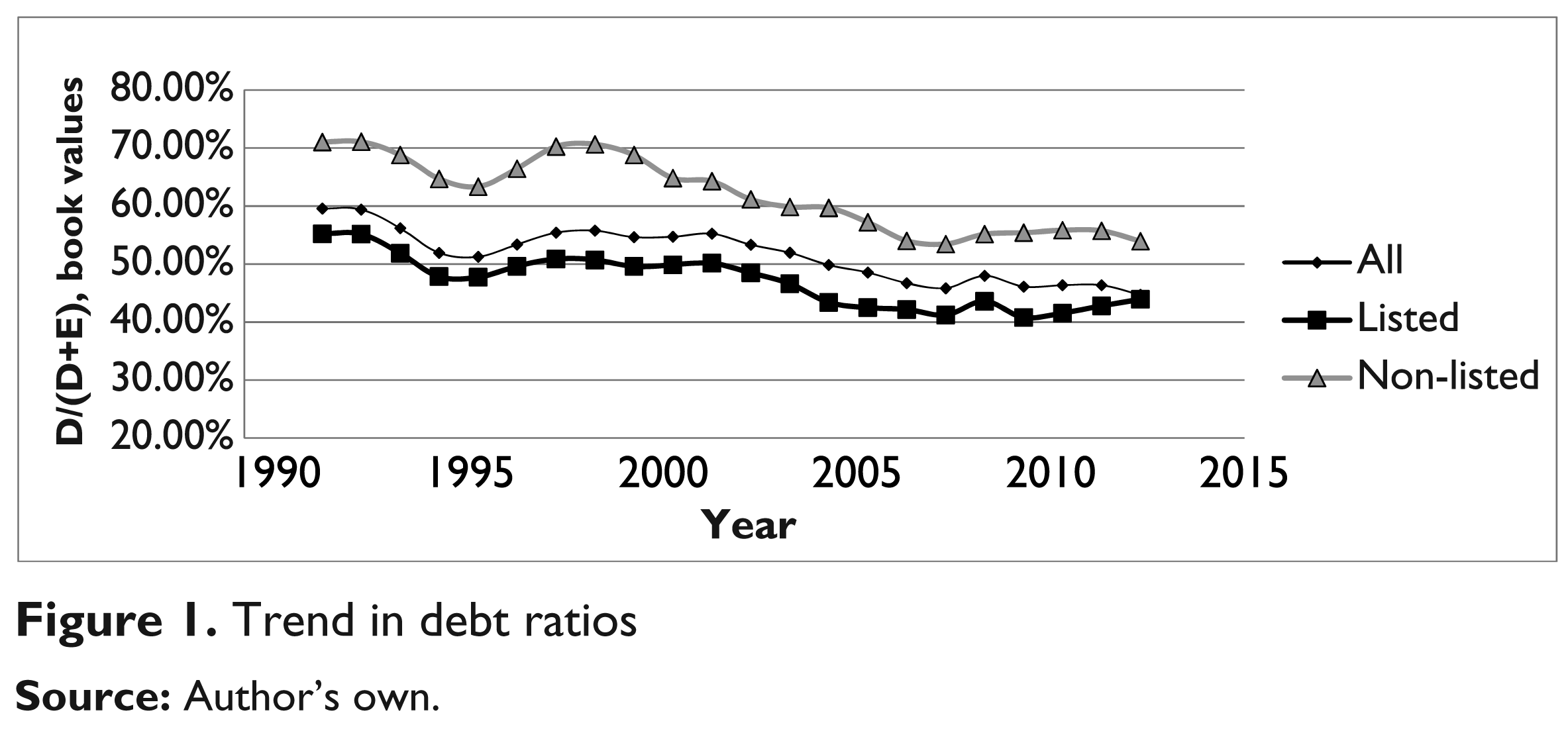

Uncorrelated movements also signify that firms do not issue to readjust their debt ratios or their issuance motives are definitely not related to adjust debt ratios toward an optimal. This becomes even alarming when we could see the trend in leverage for firms in India. Figure 1 shows that the trend in aggregate debt ratios is non-stationary and declining for the listed as well as non-listed firms. This confirms that firms are not chasing a defined target ratio for themselves.

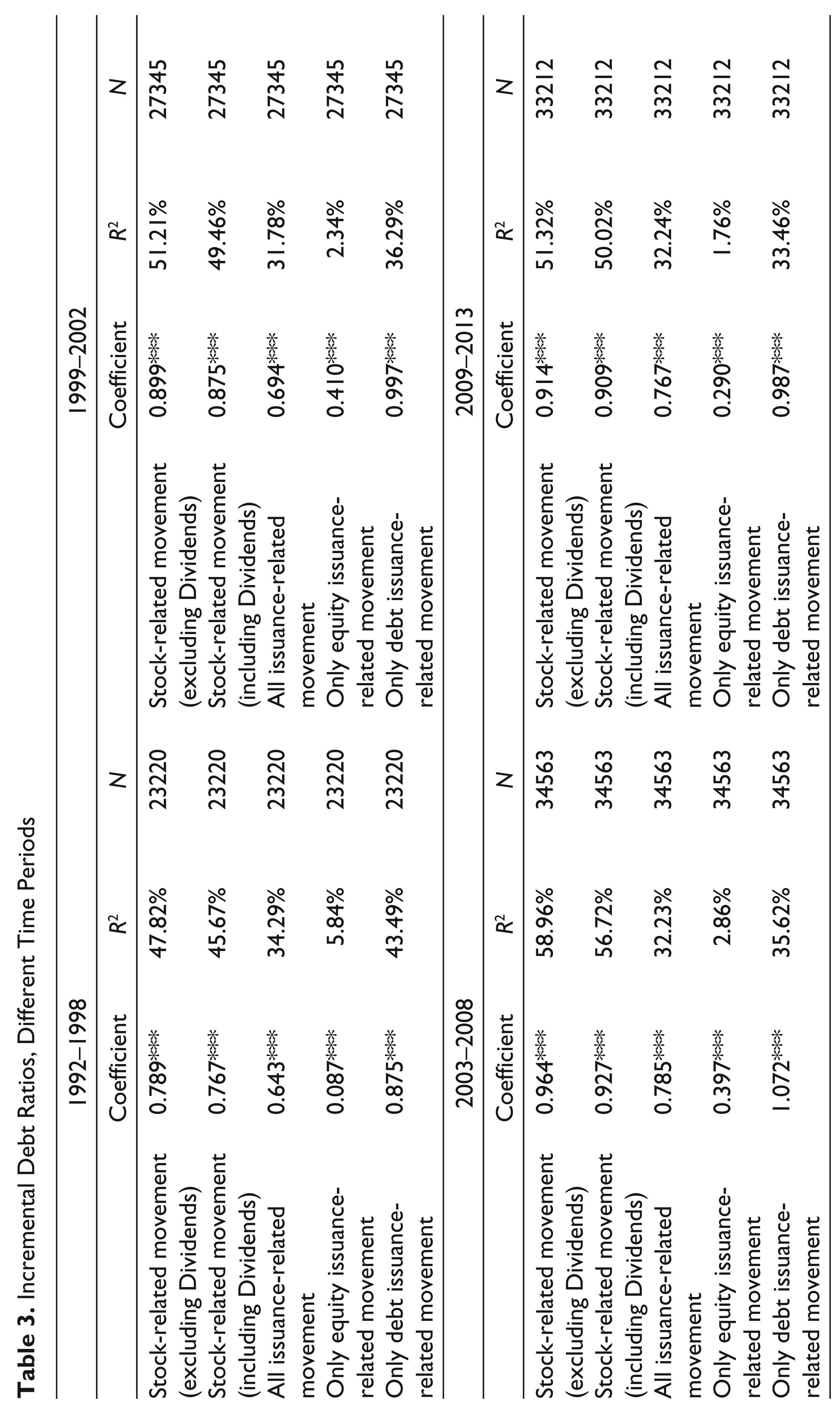

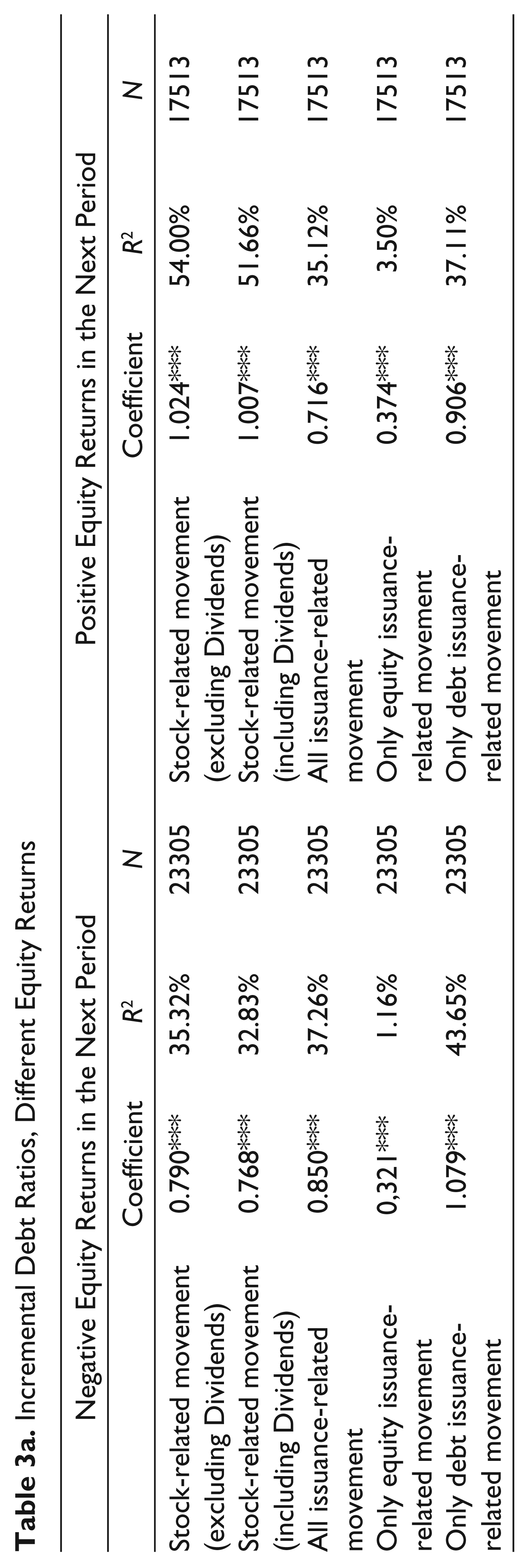

The results in Table 1 are robust to different time period chosen for the analysis. Table 3 shows results for different time periods. Further, the results are also robust for negative and positive equity returns for firms during a given year. Table 3a shows the results. Quite interestingly, during booms (e.g., 2003–2008 period) and when firms are facing positive equity returns, when it can be expected that firms do have lot of resources to readjust their debt ratios, they often do not readjust; rather the drift is very strong. Issuances would lose much of their relative significance to explain incremental changes in debt ratios during booms.

Incremental Debt Ratios, Different Time Periods

Incremental Debt Ratios, Different Equity Returns

Funds Issued as a Percentage of Total Asset

A major challenge surfaces in the form of a modest effect of the issuance activity on incremental debt ratios. Why issuances are not being able to influence the debt ratios as they would do for firms in a developed market setting? Further, why stock-related movements in debt ratios are uncorrelated with issuance-related debt ratios?

Looking into the results and experience of Indian firms vis-à-vis the US firms, these problems may arise due to capital constraints faced by the firms. Constrained firms may not be able to issue adequate debt or equity when facing difficult times in stock markets. Also, while facing good market returns, firms issue equity as well as debt simultaneously nullifying the effect on incremental changes in debt ratios. Correlation of debt and equity issuances is found to be significant at 54 per cent for the data we have captured in this article. This again reaffirms that firms are not chasing any defined target.

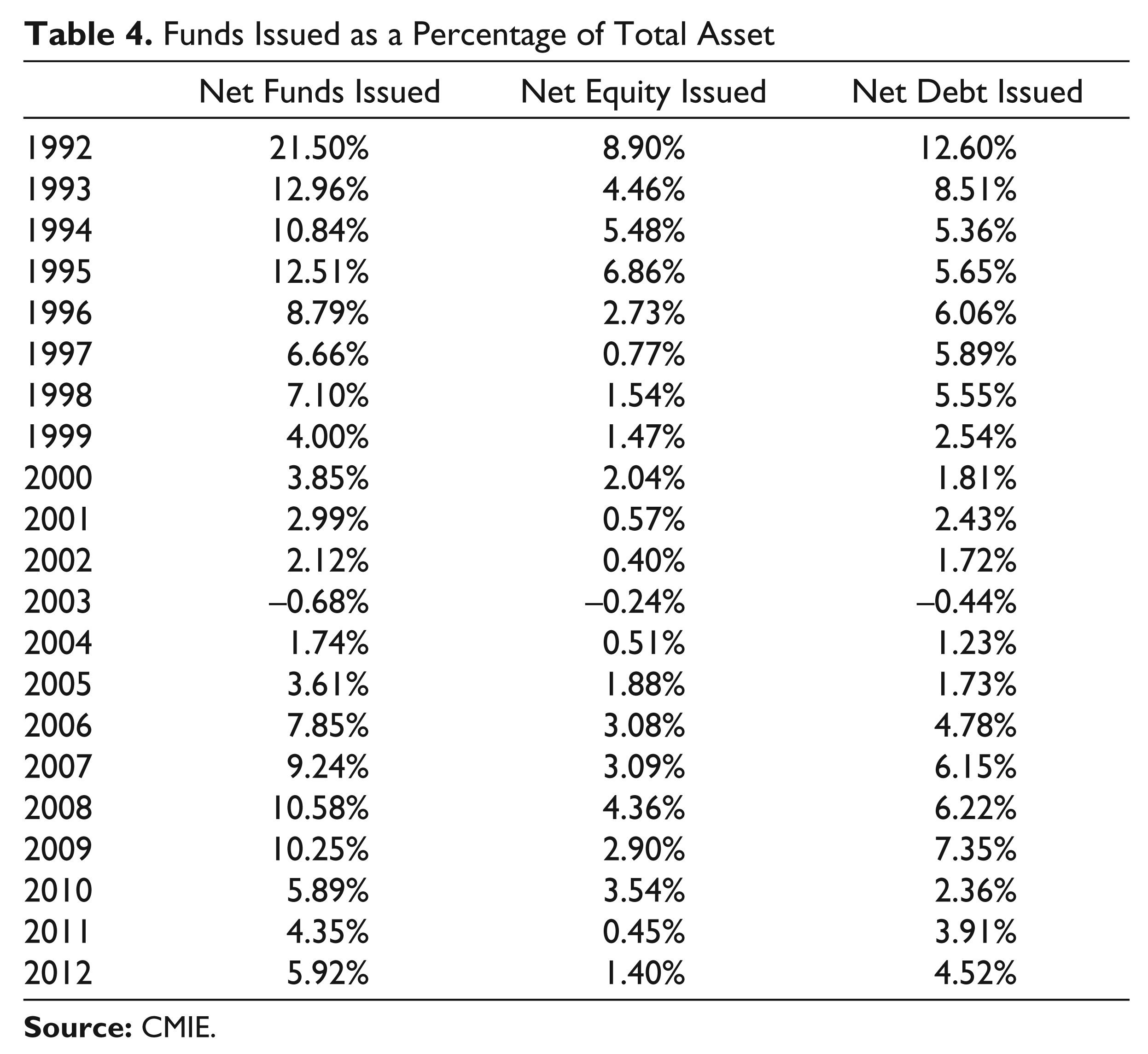

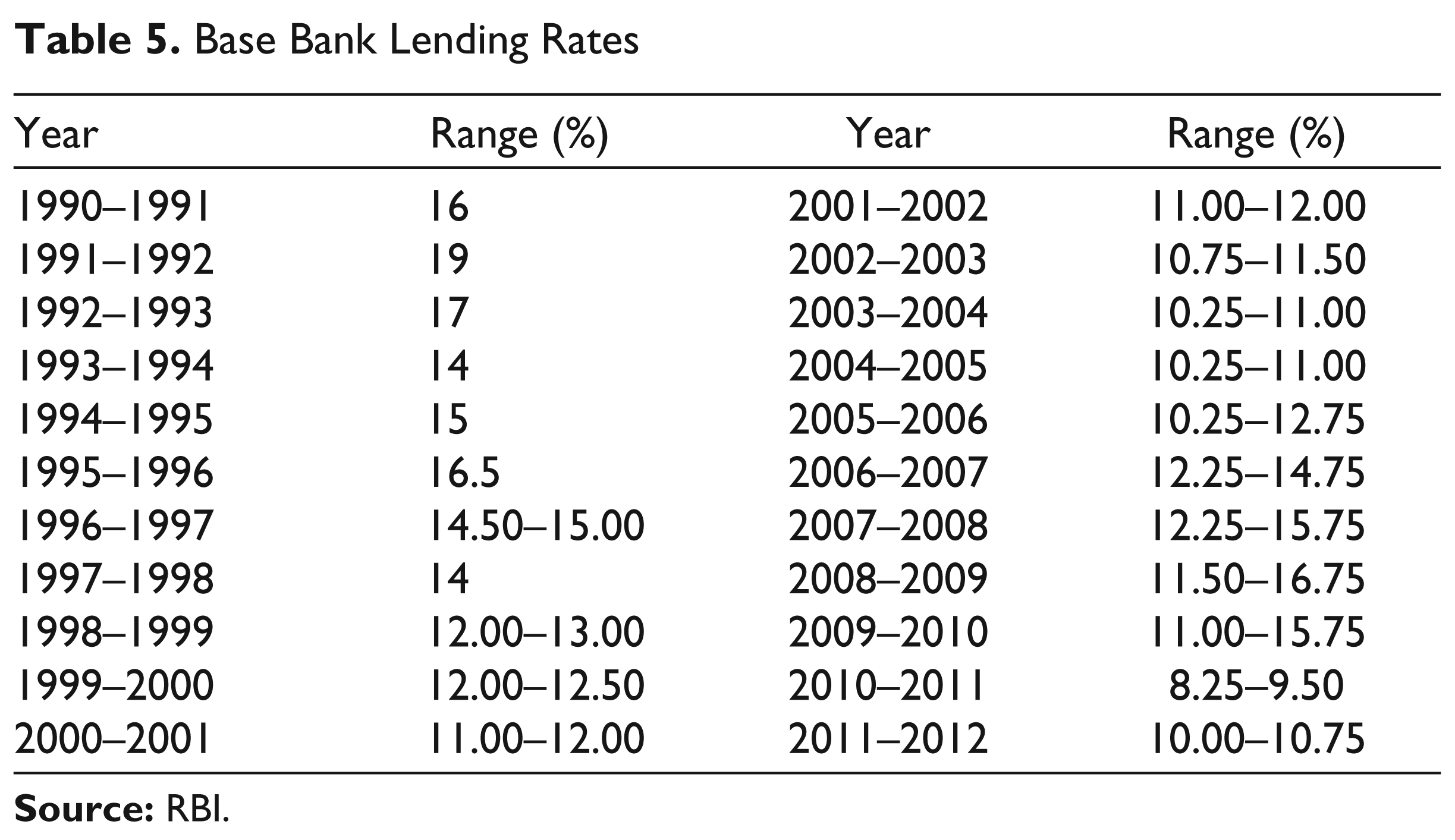

Capital constraints can be seen by looking into aggregate trend in debt and equity issuances for firms in our sample as a percentage of total assets overtime. Table 4 shows that both debt and equity issuances as percentage of total assets are going down over the years. Adding to these constraints are the higher costs of funds faced by Indian firms. Table 5 shows that the base or minimum lending rates remained high and were seldom less than 10 per cent per annum in India.

Base Bank Lending Rates

Low issuance activity and higher cost of funds indicate that even though we have sound equity markets in place, the much anticipated complementarities of these markets on overall financing of firms, especially debt, are still missing. However, this is not the case with other emerging markets (Demirguc-Kunt & Maksimovic, 1996).

Conclusion

The article is trying to explore the direction and magnitude of predictions put forward by the capital structure theories. More emphatically, we observe a strong support for the pattern of financing as predicted by the pecking order theory. However, the fundamental ground of information asymmetry, on which the theory rests, itself is missing. Issuance activities of the firms do not convey any information to markets. In other words, issuances are not motivated by the market reactions. Thus, no signalling can be expected by issuances of security for firms in India.

Results in this article show that incremental changes in debt ratios due to equity returns do not correlate with changes caused by net issuances of firms. Further, the explanation due to net issuance activities is modest as compared to similar explanation for US firms. This implies that firms do not chase a target debt ratio as predicted by the trade-off theory. Further, firms may be facing severe capital constraints in the form of availability and higher costs of funds.

Further work in this area would explore quantitatively if capital constraints are affecting firms to issue less and thus leading for modest explanation of incremental changes in debt ratios due to net issuance activities. Also, we would like to see how much of these capital constraints are industry specific. In other words, we would like to know which industries are most affected by capital constraints.