Abstract

We posit a simple mathematical model to show that a profit-and-loss sharing contract can be formed between a capital seeker and capital provider as a potential alternative to institutional debt financing. The major methodological tool used is that of Nash bargaining; utilising the matching theory proposition of Pissarides (2000). Our posited model demonstrates that a ‘match’ between a capital seeker and a capital provider can occur even in the presence of embedded market frictions arising out of information asymmetries as are especially rife in the emerging markets. This is an important result especially for marginal borrowers in emerging economies and we present supporting empirical evidence that indicates profit-and-loss sharing being increasingly seen as an effective alternative financing to long-term borrowing.

Introduction

In the aftermath of the global financial crisis, ‘debt’ has become the new four-letter taboo word and capital market institutions are actively looking at alternatives to debt in business financing; that can allow for more transparent risk appraisals (Gepp, Kumar, & Bhattacharya, 2009). The socio-political unrest in a number of European Union countries following announcement of so-called ‘austerity measures’ have further emphasised the potential undesirable social effects of heavy borrowing as a means of long-term financing. That substantive socio-religious constructs could be re-engineered to address critical bottlenecks in environmentalism has already been exposited (Wolkomir, Futreal, Woodrum, & Hoban, 1997). In a study encompassing 63 ex-colonies, Grier (1997) empirically assessed that there is an impact of dominant religious beliefs on economic development. It is therefore not too far a stretch to expect similar redemptions for capitalism originating from socio-religious norms that are already in place in several cultures. ElGindi, Said, and Salevurakis (2009) have provided an empirical account of interest-free financing as an alternative form of capital generation in a longitudinal study of Malaysian banks from 1999 to 2006. Wolf, Nabin, and Bhattacharya (2012) posited the use of ‘marketable profit-and-loss sharing contracts’ in lieu of marketable corporate debt securities; where the guiding philosophy is drawn from the principle of ‘interest-free’ financing which is a predominant socio-religious norm within the Islamic culture. They have mathematically demonstrated that in the present value terms, the cash flows to the holder of such a contract can be higher than a comparable debt security even with market frictions arising out of information asymmetries. However, they left out institutional debt, which is perhaps a more practical source of borrowed capital as compared to marketable debt, given that active bond markets are not available everywhere. In this article, we take up the issue of institutional debt and formulate a simple mathematical model of Nash bargaining that demonstrates the feasibility of an ‘interest-free’ profit-and-loss sharing arrangement between capital seekers and providers even in the presence of frictions. While our posited model cannot claim to redeem capitalism from its myriad negatives, it proves that a viable alternative in fact exists to deleterious debt financing as a source of capital.

Institutional profit-and-loss sharing (hereafter PLS) contracts is an accepted form of business financing in many countries where a socio-religious taboo exists against interest-bearing debt as within the Islamic culture. A PLS contract is a partnering agreement that has traditionally been affected on a ‘goodwill’ basis where the capital seeker and capital provider are well aware of each other’s credentials (Tayyebi, 2008). However, a high growth in their demand has recently attracted several conventional financial institutions to provide this type of financing resulting in information asymmetries (Khan, 2010). Aggarwal and Yousef (2000) have already argued that engineered financial instruments that are almost indistinguishable from conventional debt instruments are a rational outcome borne out of the prevailing ‘contracting environments’. In other words, in the presence of information asymmetries, most PLS contracts would degenerate to a conventional debt contract differing only in name.

We accept that market frictions can arise out of information asymmetries (DeGennaro & Robotti, 2007). However, we argue that a pure PLS contract can be formed even in the presence of such frictions and use the matching theory framework postulated by Pissarides (2000) to model this contract formation. However, we are not claiming at this point that a PLS contract is necessarily more optimal compared to standard debt contracts from either distributional or performance efficiency points of view (as these still remain to be modelled and tested). All we are saying that we have mathematically demonstrated here is that PLS contracts can be a potential alternative to debt financing even in presence of market frictions.

The rate of debt financing is increasing in emerging economies as compared to developed Western markets as these economies push towards growth and development and compete on equal footing with the developed economies (Staikouras, 2005). Our finding is of particular importance for investment financing in emerging markets where marginal borrowers are likely to fall into a ‘debt trap’ due to the market imperfections and information asymmetries.

Matching Theory Applied to PLS Contract Formation

We assume a unit mass of individuals seeking business financing, that is, a capital seeker and an infinite number of capital providers who own and provide one unit of capital K with one ‘vacancy’ to be filled with one capital seeker. The market of capital seekers is then subject to matching frictions of the Diamond–Mortensen–Pissarides type (Pissarides, 2000). To keep the analysis simple, we have not explicitly introduced any ‘power difference’ between capital seeker and capital providers. However, a ‘power difference’ effect is implicit in the information asymmetry that leads to the market frictions, which is considered in our model. We introduce heterogeneity among the capital seekers such that not all of them are productive. 1 We assume that e ∈ [0,1] is the fraction of capital seekers who are productive (e is determined exogenously). Therefore, (1 – e) is the fraction of unproductive capital seekers.

Each period matches are formed with the following aggregate matching function that satisfies the necessary Cobb–Douglas properties:

Here, u and v are the ‘unemployment’ and ‘vacancy’ rates, respectively. We define parameter θ is the tightness of capital seeker market such that

Given the matching Equation (1), the Poisson rate that a vacancy will be filled is as follows:

Similarly, the Poisson rate that an unemployed capital seeker will be employed is as follows:

Finally, we assume that there are exogenous shocks that arrive at Poisson rate γ ≡ [λ + (1 – e)], which will destroy all the matches. 2 Here, γ incorporates two types of shock: (a) the shock from the business cycle, that is, λ and (b) the shock from not being productive, that is, (1 – e). For sake of simplicity we assume that these two are independent.

The steady state unemployment rate is defined as follows:

Here, γ(1 – u) is the mean number of employed capital seekers who become unemployed; and eθq(θ)u is the mean number of unemployed capital seekers who become employed. Next, we derive the steady state mean unemployment by setting

Equation (5) explains that, for any given value of θ, if e = 1 then there still exists unemployment, that is,

To complete our analysis, we need to analyse both capital provider’s and capital seeker’s decision calculi. So, we derive two key equations—the job creation and wage equations:

Capital Provider’s Decision Calculus

A capital provider’s analyses two crucial aspects to make a decision and these are: (a) asset value of the vacant job and (b) asset value of the occupied job. In so doing, a capital provider, with one vacancy, incurs cost c in searching for a productive capital seeker. If he finds the productive capital seeker a match will occur, and this produce one unit of output, that is, y = 1. This output will generate and a gross return to the capital provider p.

3

However, the capital provider will need to pay the capital seeker his share of ‘wage’

Let us assume that V and J are the present discounted value of expected profit from a vacant job and an occupied job, respectively, which are also constant. Therefore, the asset value of a vacant job to a capital provider will be as follows 4 :

Here,

Similarly, we derive the asset value of an ‘occupied job’ for a capital provider as follows:

The first term of right-hand side of the equation explains the net return from ‘occupied job’ and the second term of the right-hand side of the equation explains the net return when the state has changed. By using equilibrium condition V = 0 and the Equations (7) and (8), we obtain the job creation equation, which is written as follows:

Here, as obtained by Pissarides (2000), L is negatively related to θ. However, in this model our focus is on the relationship between productive capital seeker and L curve. Therefore, it can be demonstrated that, for any given value of θ and for all values of e ∈[0,1],

This implies that L is concave with respect to e. This solution is intuitive in so far as that in the presence of an exogenous shock λ, ‘job creation’ will increase at a diminishing rate when the number of productive capital seekers rise.

The expected return of a ‘jobless’ capital seeker (i.e., when he has no access to investable capital) is as follows:

Here, z is the reservation wage of a jobless capital seeker and the second term of the right-hand side of the equation shows the net return earned when his state has changed.

The capital seeker’s expected return is as follows:

The share of capital seeker, that is,

Note that, here U and V are the disagreement points of capital seeker and a capital provider, respectively; β ∈[0,1] refers to bargaining power; for example, if

Equation (13) is also interpretable as a classical wage equation. Like the traditional model of Pissarides (2000), this ‘wage equation’ is also upward sloping with respect to θ. However, for any given value of θ and for all

We assume that an interior solution exists and posit the following propositions:

Proposition 1:

For any given value of θ, there exists e* such that if e < e* then no matching will take place at equilibrium; and if e ≥ e* then the matching will take place at equilibrium.

Proof:

From Equations (9) and (13), we know that for all values of e ϵ[0,1], L is upwardly sloping and

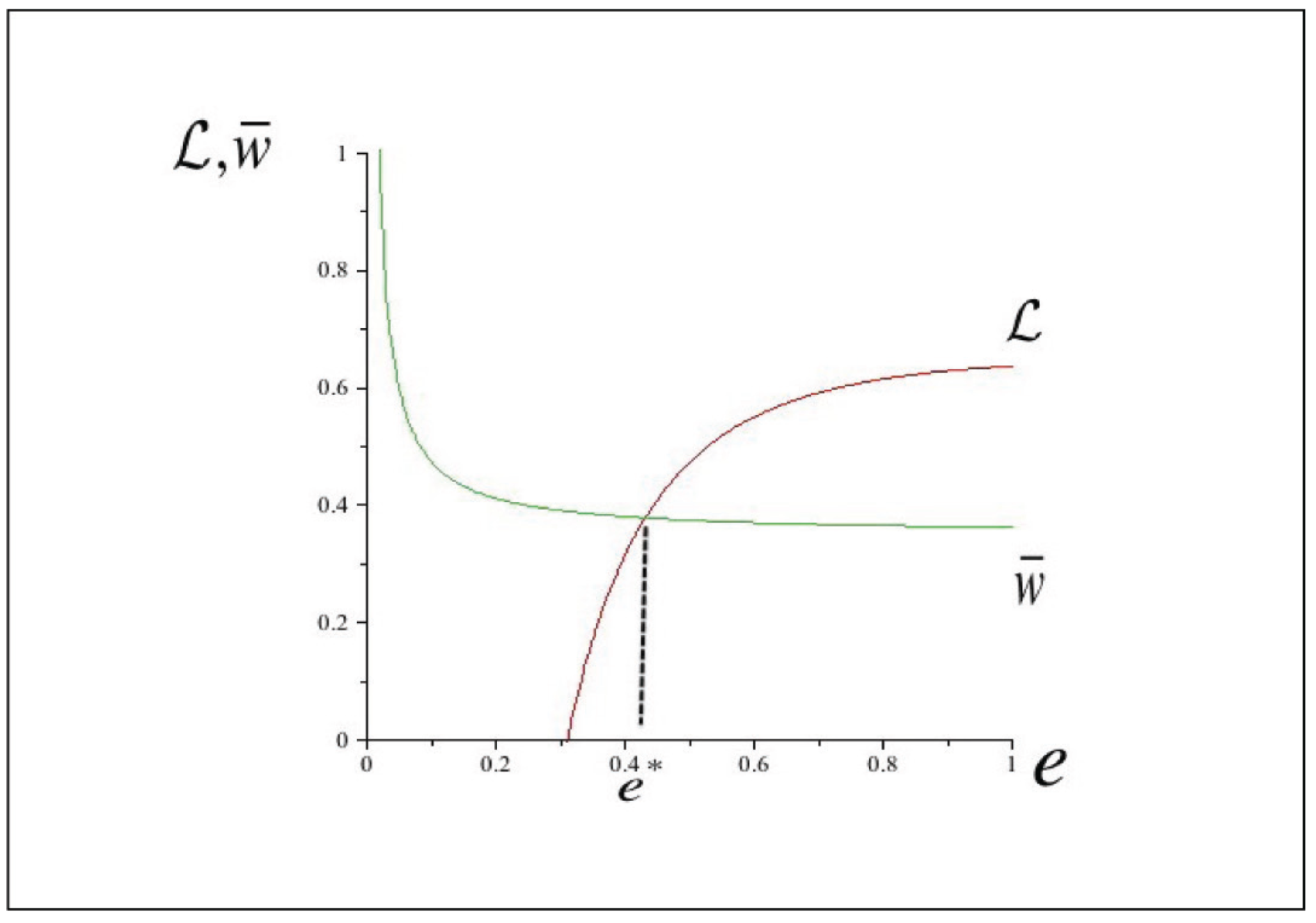

Proposition 1 implies that there exists a critical mass for productive capital seekers; and if the economy fails to achieve this critical mass then a PLS contract will not come into existence. Figure 1 illustrates Proposition 1 for the following parameter values:

p = 1, c = 0.01, δ = 1, λ = 0.01, θ = 0.5, z = 0, α = 0.5, β = 0.35

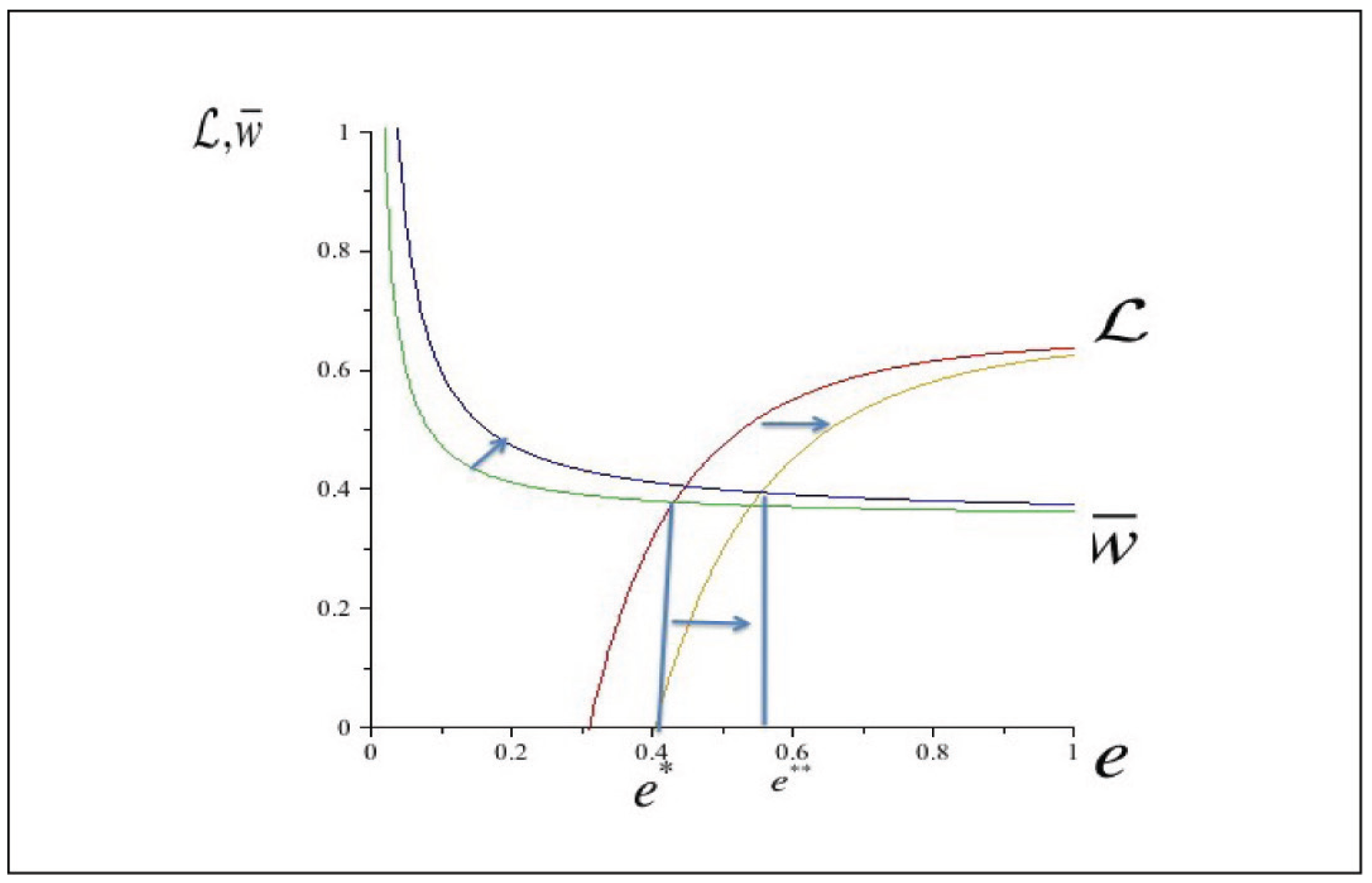

Note that an increased value of c and λ will increase the critical value of productive mass, that is, e*. In other words, an increase in search cost and exogenous shock will increase the critical mass of productive capital seekers that might make the PLS a less attractive form of financing. Figure 2 demonstrates the effect of an increase in the value of c.

Figure 2 illustrates that an increase in search cost c will force L and

Proposition 2:

Assuming the interior solution exists, there exists c such that an increase in c leads to increase in e*.

Proof: Since

For any e > e*, an individual capital provider will find that the return L is higher than the ‘wage’

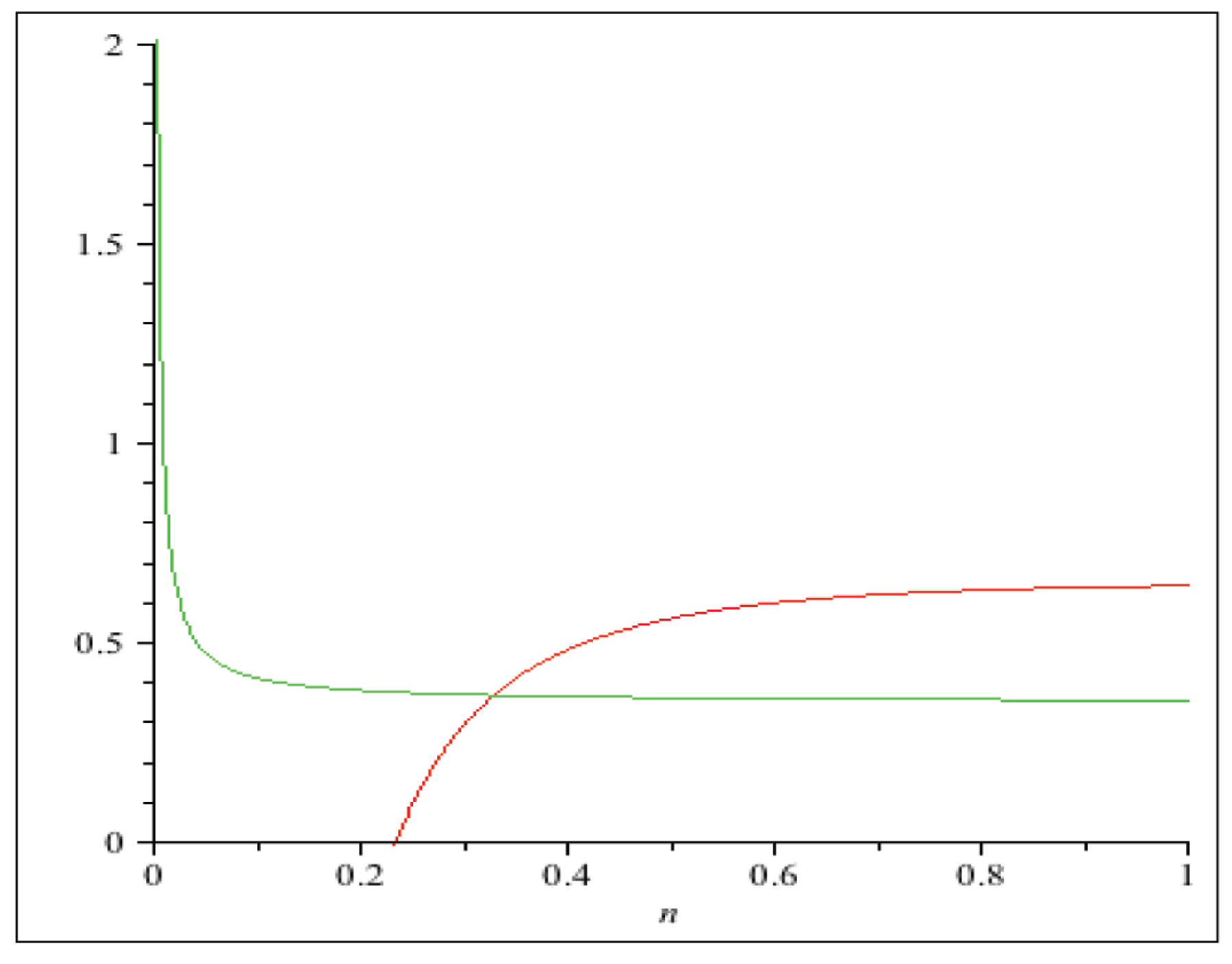

Keeping all other parameters unchanged but only increasing c to 0.05; yields Figure 3.

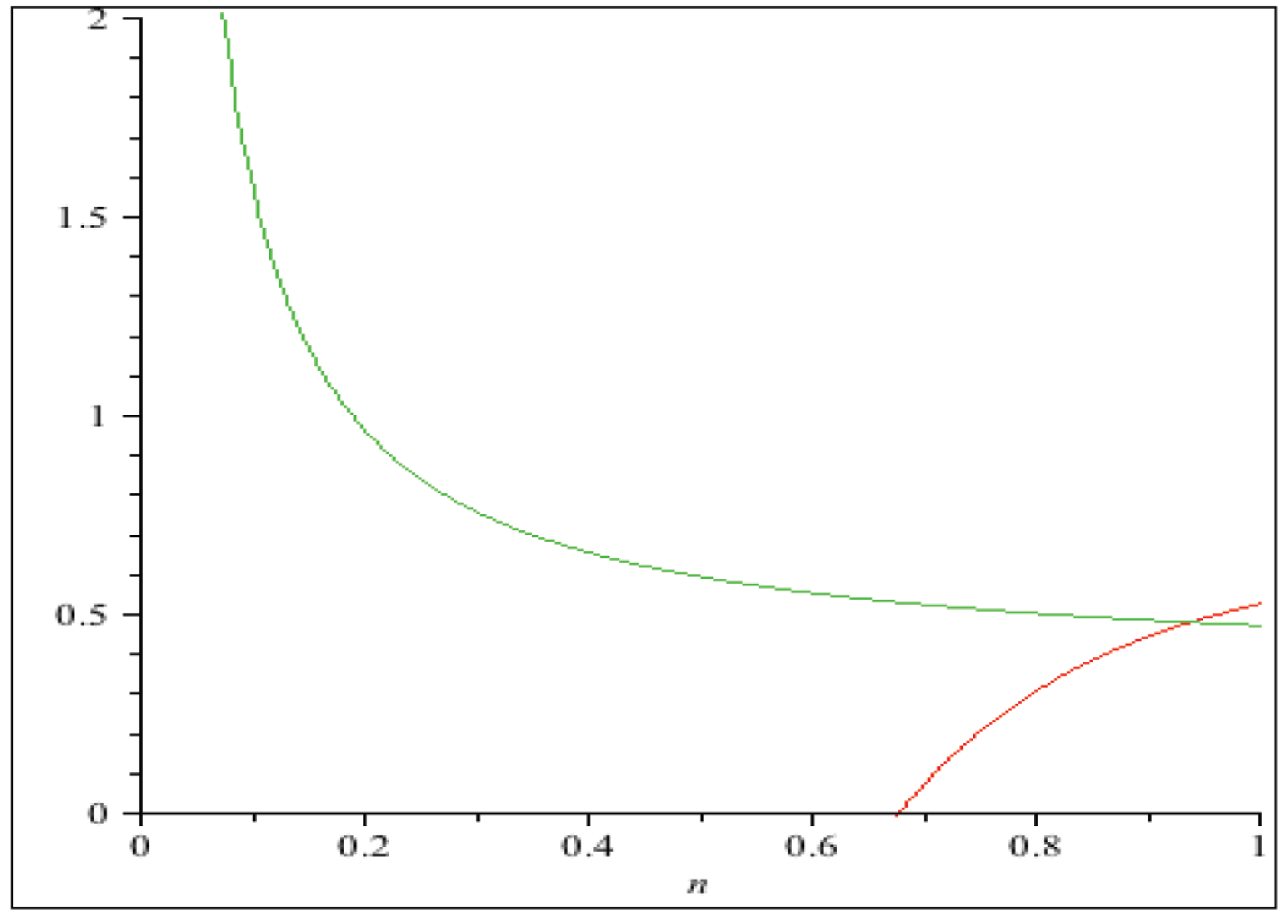

Keeping all other parameters same but only bumping c up to 0.99; yields Figure 4.

As it is apparent from the set of Figures 1–4, the value of c ranging from 0.01 to 0.99 will produce an equilibrium e for which a PLS contract can take place, that is, our matching model will be valid throughout this range of c values (though it can also be valid outside this range). It is important to note that Equation (14) confirms that an increase in c will lower J * as

The growth of financial institutions that typically offer PLS-type financing have outmatched that of conventional financial institutions in the first decade of the present century although there has been a current slowdown in that growth not due to waning popularity but because of saturation of the traditional markets (i.e., the regions where an Islamic culture predominates).

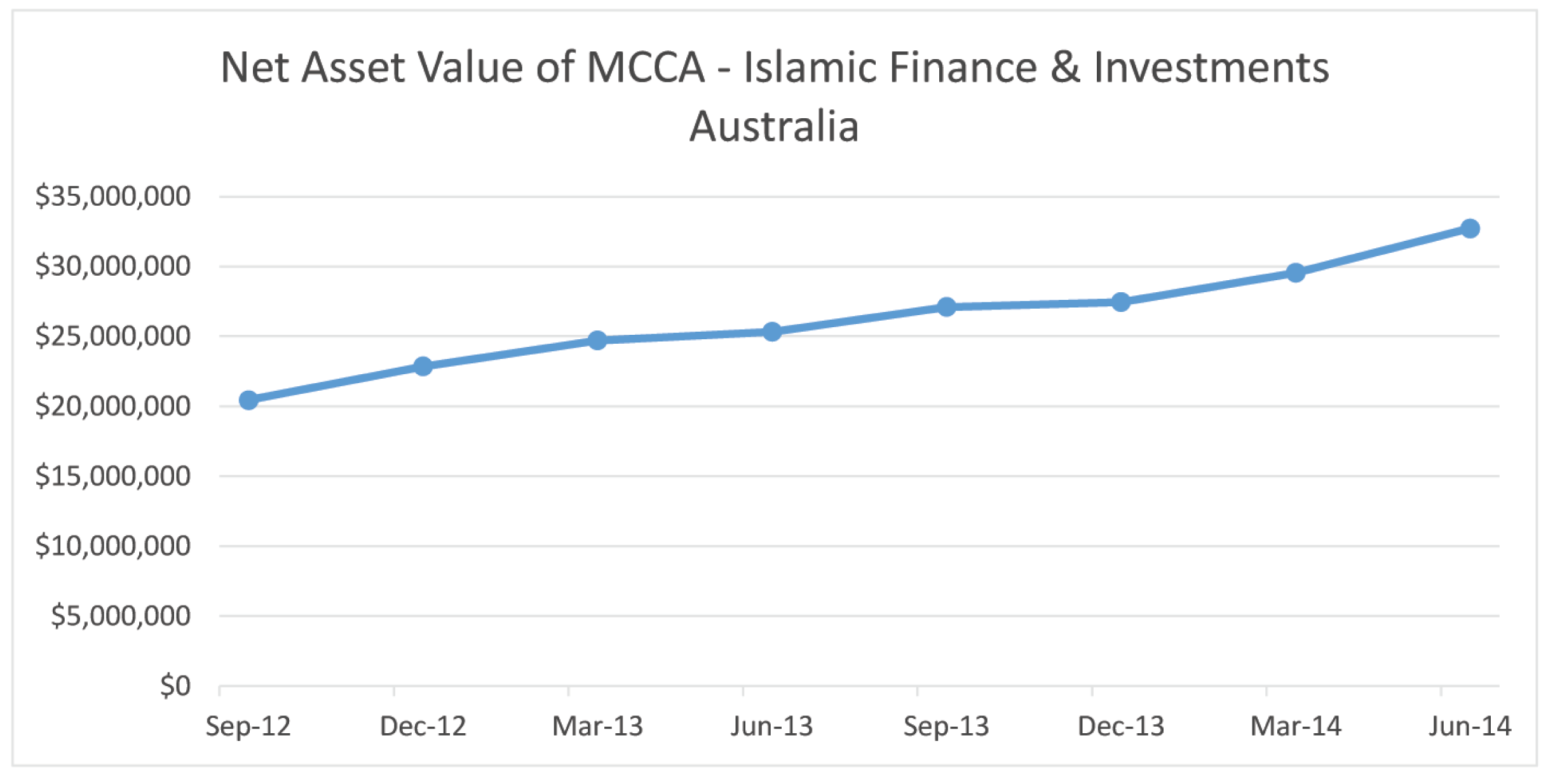

However, the growth rate is set to pick up again as this form of long-term capital sourcing gains popularity in other regions with different socio-cultural structures where these sorts of financing arrangements were not hitherto available to the capital seekers. In fact, the fast growth of financial institutions offering PLS-type financing in OECD countries actually herald a stronger support for our posited model given that it is likely that the capital seekers in these countries are more ‘productive’ compared to less developed countries. So, the net impact on the differential cash flows to the capital provider is likely to be positive. For example, in Australia, the growth of PLS-type financing is rising in recent times as per the net asset value (NAV) trend of the leading institution that offers such financing (Figure 5).

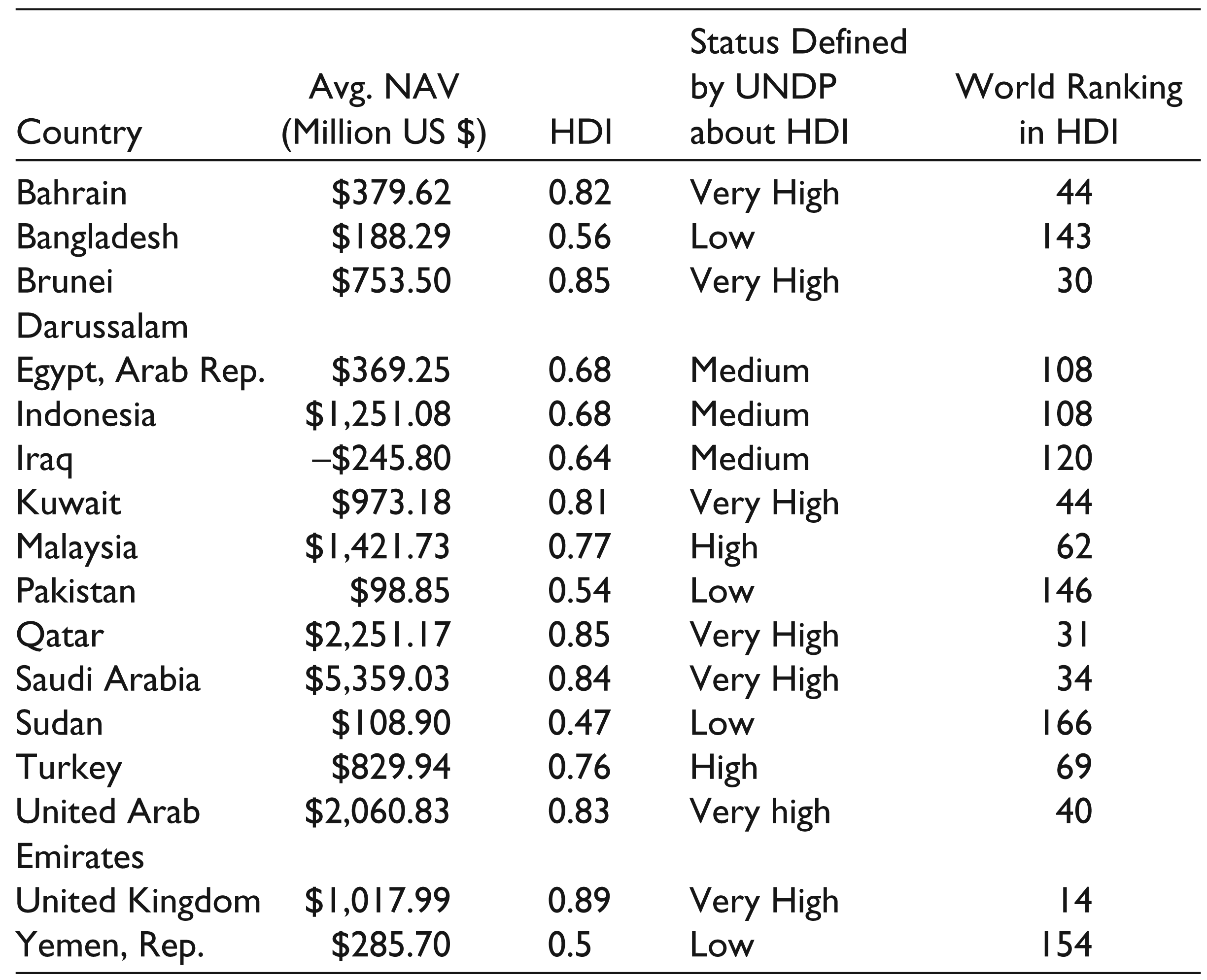

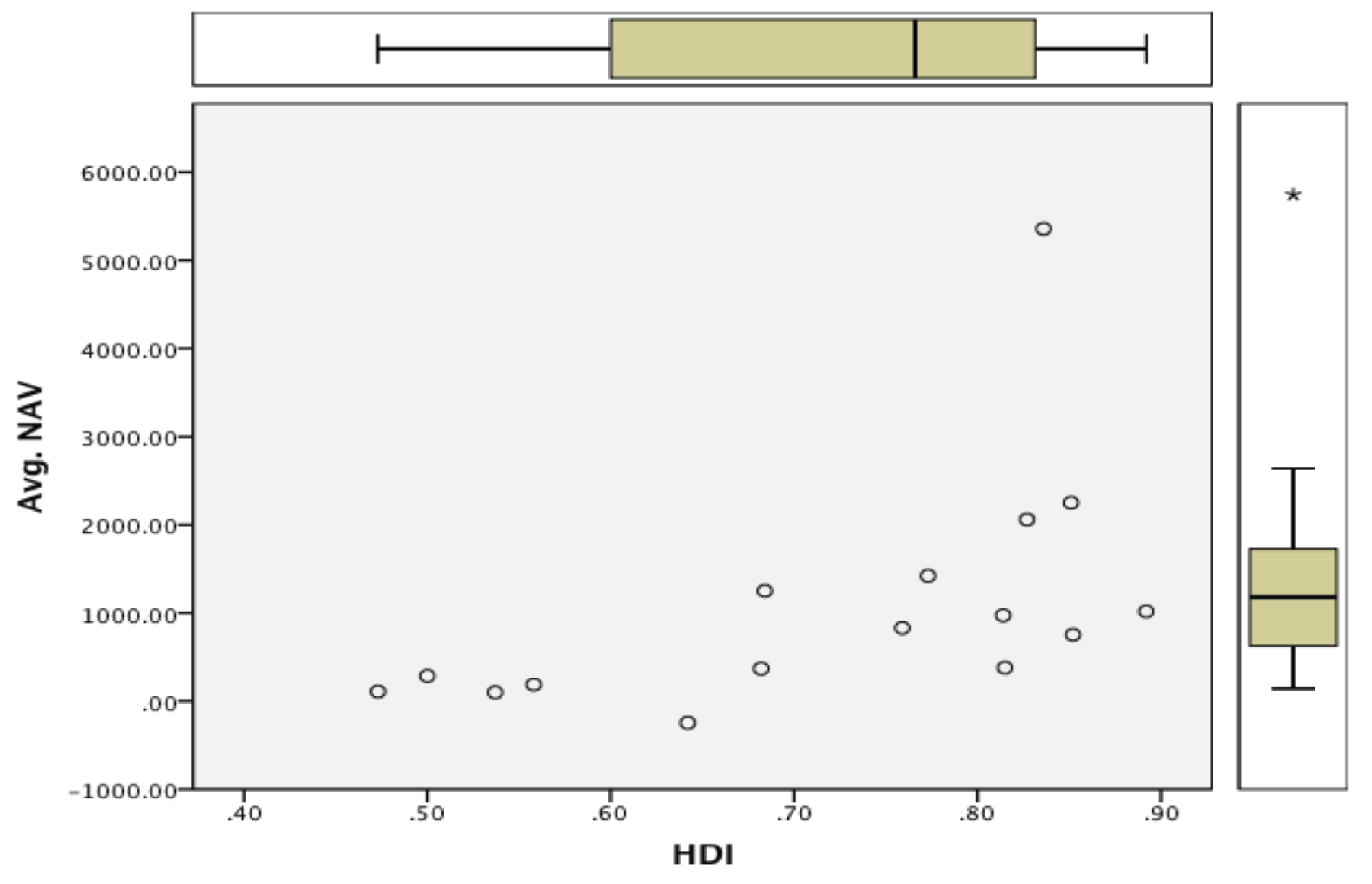

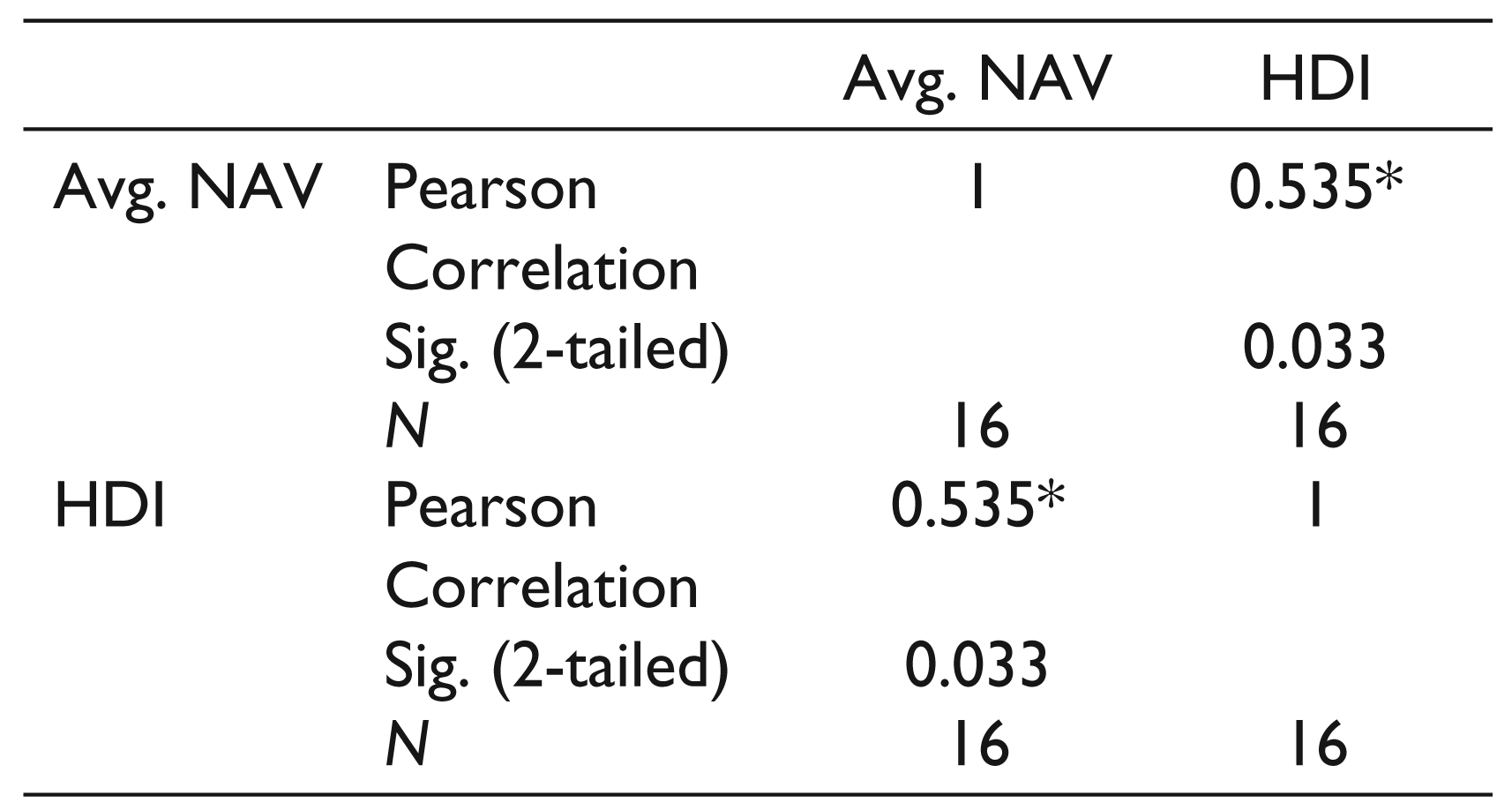

World Bank Reported NAV and UNDP reported HDI of Sixteen Countries with PLS-type Institutional Financing

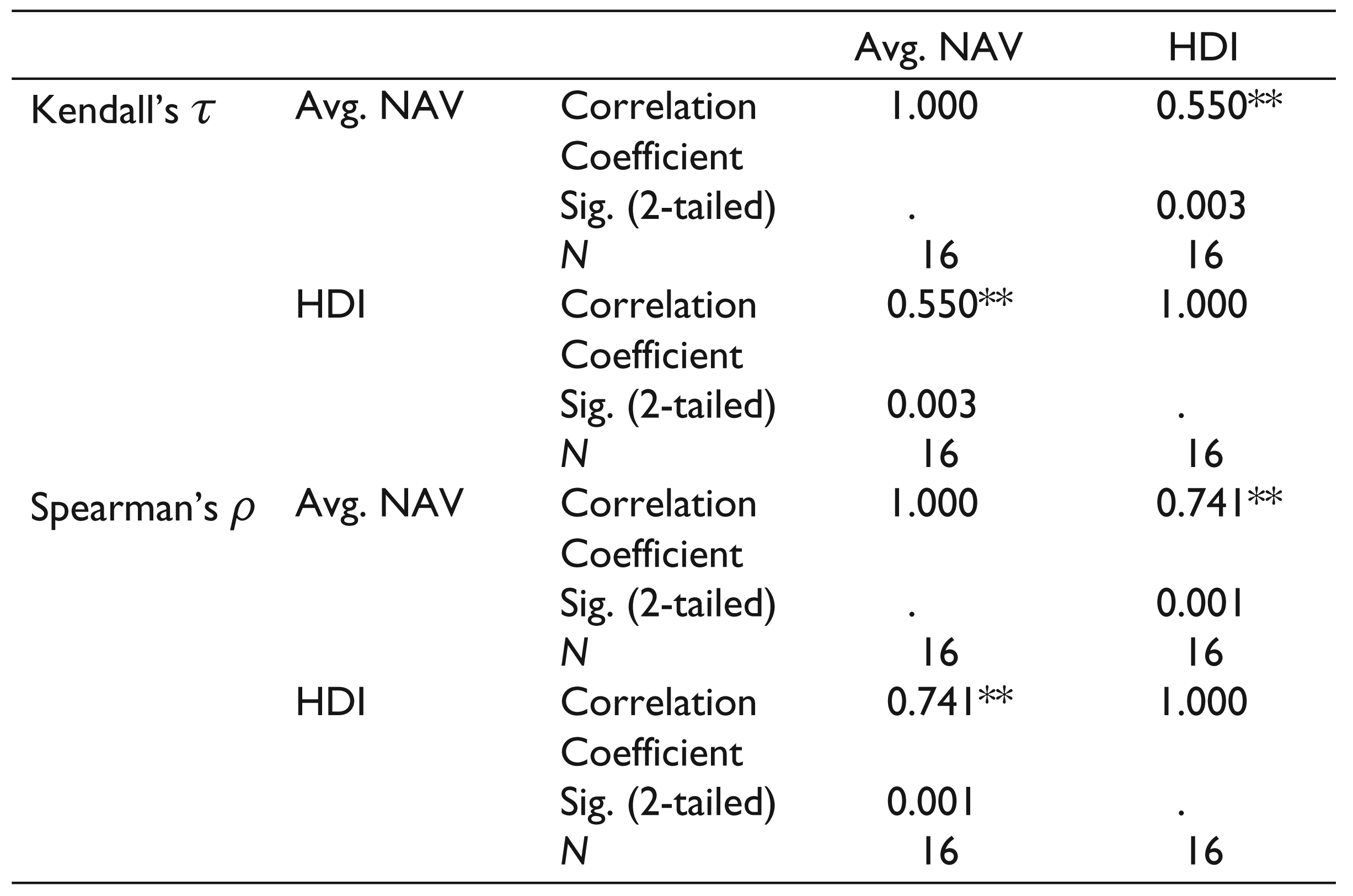

Even within the countries where PLS-type institutional financing has proliferated most significantly due to amicable socio-religious factors, we have detected a statistically significant positive correlation between the NAV (calculated as total reported assets minus total reported external liabilities) of the financing institutions and the human development index (HDI) (as extracted from 2013 UNDP World Development report). The extracted data is presented in Table 1 and the results of statistical analysis are presented in Tables 2–3 and Figure 6. This empirical finding helps provide anecdotal evidence in support of our posited model. With higher HDI, it is expected that more capital seekers would be productive and therefore a PLS-type financing arrangement will also be more beneficial from the standpoint of the capital providers (i.e., the financing institutions). Indeed, as PLS-type financing grows further in OECD countries we hypothesise this significant positive correlation to become even more evident. As a direction of future empirical research, one could look at panels of countries categorised in accordance with their HDIs and the financial performance of standard debt financing versus PLS-type financing institutions, which can throw further light on this under-researched topic.

Correlation Analysis—Parametric

Correlation Analysis—Non-parametric

We have demonstrated that even in the presence of market frictions arising out of information asymmetries, a PLS contract can be formed—which is a radical mode of long-term financing that can have a far wider, pan-global socio-cultural desirability as compared to traditional borrowing. Stated formally, we have shown that even in the presence of matching frictions of the Diamond–Mortensen–Pissarides type (Mortensen & Pissarides, 1994; Pissarides, 2000), a Nash bargaining set-up can lead to a viable PLS contract formation between capital seeker and capital provider; with the result being of particular relevance for marginal borrowers in emerging markets. One could argue that one of the shortcomings of our analysis as earlier is that we have implicitly assumed that whether a capital seeker is productive or not is essentially a ‘zero-one’ case and that by introducing a ‘degree’ to the productiveness of the capital seekers (so that some are more productive than others) one may explore the effects of any adverse selection within our posited framework. While it is a valid point, it could, however, cause the article to become too long-drawn if we were to try and accommodate this within a single article. We therefore have chosen to leave this as an open research problem for future researchers wishing to build further on our model. Furthermore, our model establishes a theoretical framework that now opens up the issue for more focused, incisive empirical analysis that was not possible hitherto given that there was no real support for the position that PLS contracts could exist in presence of market frictions. Our work arguably effects a radical change on the way debt financing is conceived in future.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.