Abstract

This article investigates the market timing ability of the bond–equity yield ratio (BEYR) from an international investor perspective. Consolidating data on emerging markets, we document no major international evidence that BEYR-based investing strategies, namely extreme values, thresholds and moving averages, provide higher risk-adjusted returns than benchmark buy-and-hold portfolios. However, we develop new augmented BEYR indicators by introducing the notion of US bonds as a safe investment relative to emerging market stocks and bonds. Dynamic strategies based on our augmented BEYR indicators produce significant gains in risk-adjusted returns compared with traditional BEYR and buy-and-hold benchmark strategies.

Introduction

The empirical relationship between stock and bond markets is of great importance to investors (Baker & Wurgler, 2012). In particular, market participants are interested in the returns and diversification properties of the two major asset classes. The extant literature documents a number of financial and accounting variables associated with stocks and bonds that have been evaluated and tested as a foundation for various trading rules. 1 In this study, we examine the market timing ability of the bond–equity yield ratio (BEYR) from an international investor perspective in the emerging market setting.

The underlying motivation behind using the BEYR as a relative pricing tool for allocating the capital between stocks and bonds can be described as follows: Yields on bonds and dividend yields associated with stocks should be approximately equal or at least strongly correlated in the long run, and therefore BEYR should vary around its long-run equilibrium (Maio, 2013). If equity yields fall, bonds become more attractive to investors and their prices rise, which, in turn, will cause bond yields to fall, making equity yields look attractive again (Giot & Petitjean, 2009). A decline in bond yields pushes the BEYR down from its long-term equilibrium, while a fall in equity yields drives it back up. If the BEYR were too low compared with the long-run level, bonds would be viewed as expensive relative to stocks and the traditional investing rule would suggest ‘sell bonds and buy stocks’. Inversely, if the BEYR were too high related to its long-run equilibrium, equities would be viewed as too expensive relative to bonds and the investing rule would suggest ‘sell stocks and buy bonds’.

The purpose of this article is twofold. First, by comparing the performance of BEYR-based strategies with traditional buy-and-hold bonds and stocks benchmark strategies we explore the market timing ability of the BEYR using emerging market data. This is conducted by employing three BEYR-based active investment strategies, namely extreme values, the thresholds BEYR rule and moving averages. Second, we develop two new augmented BEYR indicators, in which we introduce the US bonds as a safe haven investment relative to the emerging market stocks and bonds. Establishing new augmented BEYR indicators is motivated by the literature suggesting that emerging market bonds exhibit properties of ‘equity-like’ risky assets because of the high country risk and uncertainty in emerging economies (Kelly, Martins, & Carlson, 1998; Panchenko & Wu, 2009; Piljak, 2013). Thus, the underlying concept is that risk-averse investors, when substituting safer assets for their risky ones, prefer allocating their capital to bonds from developed countries (proxied by the US government bonds), rather than bonds in emerging markets. The performance of the augmented BEYR investing strategies is compared with the benchmark buy-and-hold and traditional BEYR-based strategies.

Our study contributes to the literature in three important ways. First, we add to the strand of literature investigating BEYR market timing (Brooks & Persand, 2001; Harris & Sanchez-Valle, 2000; Levin & Wright, 1998) by providing new international evidence from emerging markets. The literature has traditionally focused on developed markets, and this is the first study that considers emerging markets a separate category in the context of BEYR market timing. Second, by employing the US bonds as a safe asset and emerging markets’ stocks or bonds as risky assets, we construct new augmented BEYR indicators serving as a valuable relative pricing tool that can be used to dynamically allocate capital between safe and risky assets in the international setting. Third, in line with Kelly et al. (1998), Panchenko and Wu (2009) and Piljak (2013), we provide supplementary evidence that emerging market bonds should not be assigned the properties of a safe investment relative to emerging market stocks. By comparing the performance of traditional and augmented BEYR-based strategies we confirm the equity-like properties of emerging market bonds. Empirical findings from this article can benefit international investors seeking profitable trading opportunities between stock and bond markets.

The empirical findings reported in this study show that the traditional BEYR investing strategies (constructed from the emerging market bond and stock yields) do not deliver significantly higher risk-adjusted returns relative to buy-and-hold benchmark strategies. Our results are therefore casting doubt on the market timing ability of the traditional BEYR, providing further international support to the findings in Brooks and Persand (2001) and Giot and Petitjean (2009). Furthermore, all of the augmented BEYR-based trading strategies (using US bonds as a safe asset and emerging market stocks and bonds as risky assets) deliver higher risk-adjusted returns compared with the benchmark buy-and-hold bonds or stocks strategies.

The remainder of the article is organised as follows. In the second section, we describe the theoretical rationale for using the BEYR as an investing tool. The third section presents the dataset, provides descriptive statistics and describes various methods of BEYR investing. In Section 4, we present the results. Finally, the fifth section concludes the article.

Essential Theory Underlying BEYR

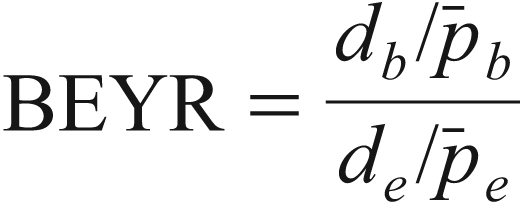

The cornerstone of BEYR market timing is the relationship between risky assets (stocks) and safe assets (bonds). BEYR is defined as the ratio of the income yield on long-term government bonds to the dividend yield on equities. 2 It has been identified by the practitioners as a useful tool for detecting relative mispricing between bonds and equities. The theoretical rationale for using the BEYR as a tool for detecting profitable trading opportunities between stocks and bonds can be seen from its basic definition:

where db represents the income stream from bonds (coupon), de is the income stream from the equity (dividend) and

where rf is the risk-free discount rate, ρ is the equity-risk premium and gb and ge are the corresponding growth in the income stream from bonds and equity, respectively. Equation (2) accordingly suggests that BEYR will diverge if

Since BEYR represents a ratio of bond yield, which is a nominal variable in nature and equity yield, which is a real variable, it is evident that the BEYR is exceptionally sensitive to expected inflation. Specifically, while firms can raise their prices in response to inflation, bond coupons stay fixed in nominal terms. The positive effect of inflation on equity yields (also known as the ‘money illusion error’) can be attributed to distort corporate earnings and capital gain taxes (Asness, 2003). Thus, investors demand higher-risk premiums and expected returns with high inflation, causing equity yield to rise (Giot & Petitjean, 2009). The growth rate is also affected by anticipated inflation caused by the restrictive monetary regime that results from rising inflation expectations (Levin & Wright, 1998). To consolidate the impact of expected inflation on the real value of bond coupons (which is a constant in nominal terms), the following BEYR equation is derived:

where (1 + R)(1 + π) = 1+ r; (1+ G)(1 + π) = 1+ g; and (1 + ρr)(1 + π) = 1 + ρ represent Fisher equations for the relationship between the nominal and real variables. R represents the real interest rate, G is the real growth rate in the income stream and ρr depicts the real equity-risk premium.

The relationship between bonds and stocks is shaped by two effects. First, the ‘discount rate effect’ suggests a negative relationship between bond and equity yields driven by the rationale that cost of equity depends on prevailing interest rates and accordingly rising (falling) bond yields lead to the lower (higher) stock prices (Giot & Petitjean, 2009). An alternative view called the ‘cash flow effect’ proposes a positive correlation between stock prices and bond yields motivated by the argument that rising inflation drives bond yields as well as the growth of future nominal cash flow from equities up, which in turn raises equity prices as well. Nevertheless, the general agreement in stock–bond literature is that the ‘discount rate effect’ should prevail during expansion periods while the ‘cash flow effect’ is more important during contractions periods (Andersson, Krylova, & Vähämaa, 2008; Boyd, Hu, & Jagannathan, 2005).

The fluctuations of the economy between periods of expansions (growth) and contractions (recession) have an impact on market participants’ risk aversion, thereby also affecting the prices of stocks and bonds simultaneously (Andersson et al., 2008; Baur & Lucey, 2009; Connolly, Stivers, & Sun, 2005; Gulko, 2002). Government bonds, by definition, are deemed to be safe haven assets relative to stocks in developed markets. During times of financial turmoil, investors engage in ‘flight-to-safety’ as they substitute risky assets (stocks) for safer assets (bonds). However, the relationship between stock and bond prices is altered in emerging markets. Specifically, prices of both assets tend not to move in opposite directions during crisis periods. Subsequently, due to the specific country risk in emerging economies, domestic bond returns show patterns of ‘equity-like’ securities and, in turn, the ‘flight-to-quality’ phenomenon does not exist (Kelly et al., 1998).

In a nutshell, the relationship between the stock and bond yields is fairly sophisticated, and the overall picture is further complicated in the emerging market setting. Moreover, the ability of BEYR to work as a trading rule foundation in emerging economies is challenged by the country-dependent co-movements in stock and bond prices and the risk premium. Thus, no definite proof in support of the BEYR approach exists (Giot & Petitjean, 2009).

Several studies discuss the market timing properties of three models associated with bonds and stocks: the Fed model, the BEYR and the bond–stock earnings yield differential (BSEYD). Studies such as Asness (2003), Gwilym, Seaton, Suddason, and Thomas (2004) and Maio (2013) address the Fed model, which uses the yield gap, the difference between equity yields on stock market indexes and long-term yields on treasury bonds. Other studies such as Levin and Wright (1998), Brooks and Persand (2001), Giot and Petitjean (2009) and Harris and Sanchez-Valle (2000) focus on BEYR, which is defined as the ratio of bond yields over the equity yields (dividend or earnings yields). Finally, Berge and Ziemba (2003) and Lleo and Ziemba (2017) focus on BSEYD, defined as the ratio between long-term government bonds yields and earnings yields on stocks. All of the models are essentially based on the same underlying theory that stocks and bonds are interchangeable investment assets with their yields being highly correlated in the long run.

The literature on market timing of the BEYR offers miscellaneous explanations and inconclusive results on whether the BEYR can be used as a profitable trading rule. A summary of the literature including the countries investigated and the results on whether a model associated with stocks and bonds can be used as valuable market timing tool is reported in Table 1. Clare, Thomas, and Wickens (1994) and Harris and Sanchez-Valle (2000) investigate a number of BEYR-based trading rules that in turn deliver higher average returns and lower standard deviations than buy-and-hold strategies. Additionally, Levin and Wright (1998) introduce the threshold values for BEYR market timing strategy in determining whether the equities and bonds are cheap or expensive and conclude that the BEYR model is superior to all other benchmark portfolios. Conversely, Brooks and Persand (2001) and Giot and Petitjean (2009) find no international evidence that BEYR-based trading strategies deliver significantly higher risk-adjusted returns than buy-and-hold stocks or bonds portfolios. Owing to the general disagreement in the literature, Giot and Petitjean (2009) argue that future research is warranted to investigate how BEYR might be best modelled and implemented.

Summary of the Prior Literature

Summary of the Prior Literature

Monthly data on stock index dividend yields and income yields on government bonds were obtained from the Thomson Reuters Datastream. 4 The empirical part focuses on 13 emerging markets, namely Argentina, Brazil, Bulgaria, China, Colombia, Ecuador, India, Mexico, Peru, the Philippines, Russia, Turkey and Venezuela as well as the USA. The sample data cover the period January 1994 until September 2014. We incorporate the longest available dataset for each country in the study. 5 The selection of the emerging markets in our sample is based on the country composition of both the Morgan Stanley Capital International (MSCI) BRIC Index 6 and the J. P. Morgan Emerging Market Bond Index Plus (EMBI+). 7 Stock market indexes for each emerging market are provided by MSCI. The inclusion of the US market in the study was due to its role as a global factor in the international financial markets. The US bond market is represented by 10-year government bonds. All of the stock and bond indexes are denominated in US dollars.

Further, we carry out a set of empirical experiments aimed at evaluating traditional and augmented BEYR performance as a relative pricing tool for allocating funds between risky and safe assets. In the traditional BEYR evaluation, we compare two basic benchmark rules, namely buy-and-hold equity and buy-and-hold bonds, with a number of BEYR-based active trading strategies. Specifically, we employ the extreme value strategy, the thresholds BEYR rule and the moving averages investing strategies. In addition to the traditional BEYR, we create two new augmented BEYR variables, integrating the US bonds in the calculation as a proxy for safe investment relative to risky emerging market stocks and bonds. Inclusion of US bonds as a safe asset relative to emerging market stocks and bonds is motivated by the literature treating the emerging market bonds as risky ‘equity-like’ assets because of high country risk and uncertainty in emerging economies.

Trading rules for the traditional BEYR are based on the basic principle of shifting the capital between the competing assets: stocks (risky assets) and long-term government bonds (safe assets). Deviations from the long-term equilibrium are used as a signal in the trading rules. In situations where bond yields are exceptionally low relative to equity yields, and therefore the BEYR is too low compared to its long-term equilibrium, we shift our position from bonds to stocks. Correspondingly, we shift from stocks to bonds if the BEYR is too high or stock yields are much higher than bond yields.

Further, for our augmented BEYR-based trading strategies we shift between the US bonds (safe assets) and the emerging market stocks or bonds (risky assets). If the augmented BEYR is too high, we shift the funds out of emerging market stocks or bonds into US government bonds. Correspondingly, if the augmented BEYR is too low, we shift the capital from US government bonds to emerging market stocks or bonds. Following the prior literature, we initially place our capital into equity for all of the strategies used.

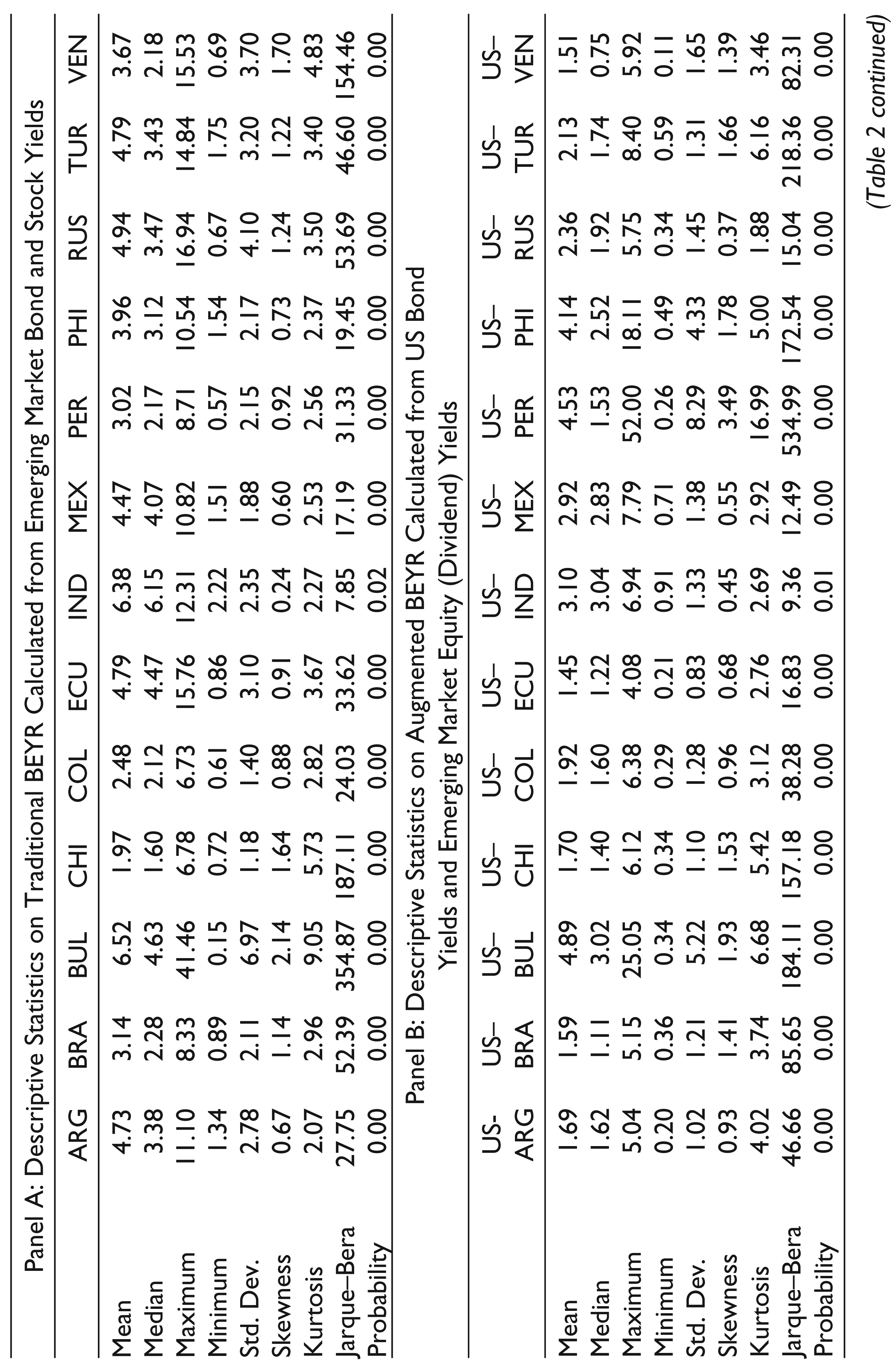

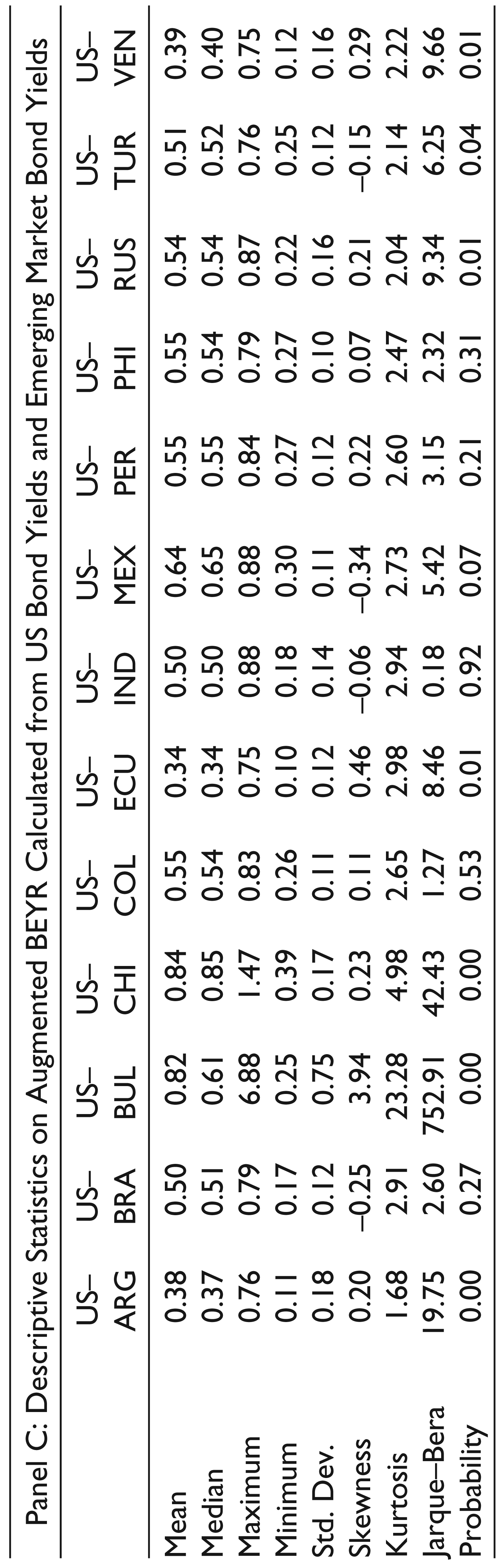

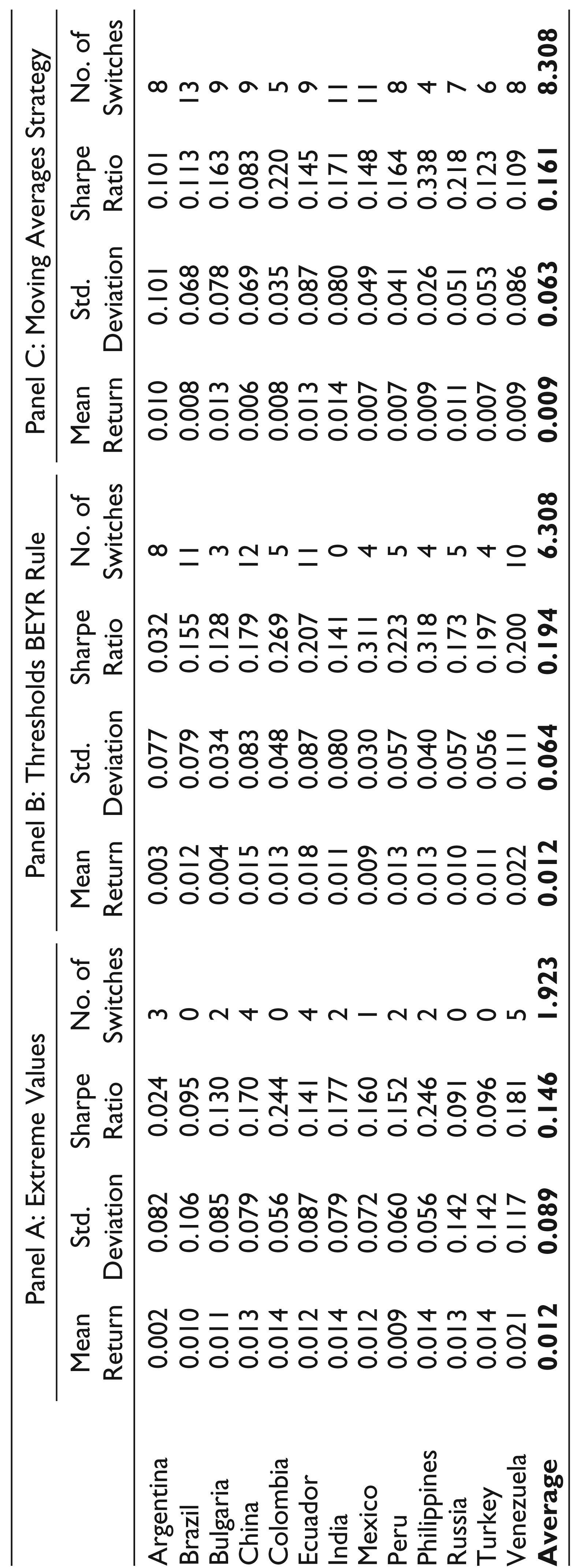

Table 2 presents the summary statistics for the three versions of the BEYR used in the study. We construct three different versions of the BEYR to use in further analysis: (a) Figure A1 represents the summary statistics for the traditional BEYR calculated by taking the ratio of bond and equity yields from the same country, that is, the bond yield divided by the equity dividend yield; (b) Figure A2 shows the descriptive statistics for the first augmented BEYR calculated as a ratio of US bond yield (safe) over the equity dividend yield from the emerging markets (risky); and (c) Figure A3 presents the second augmented BEYR, calculated as a ratio of US bond yield (safe) over the emerging market bond yield (risky). Based on Jarque–Bera normality and kurtosis test statistics, we reject the hypothesis for the normality for all of the BEYR and augmented BEYR series, which gives further motivation for using the active strategy switching models for our trading rules.

Buy-and-hold Bonds and Stocks

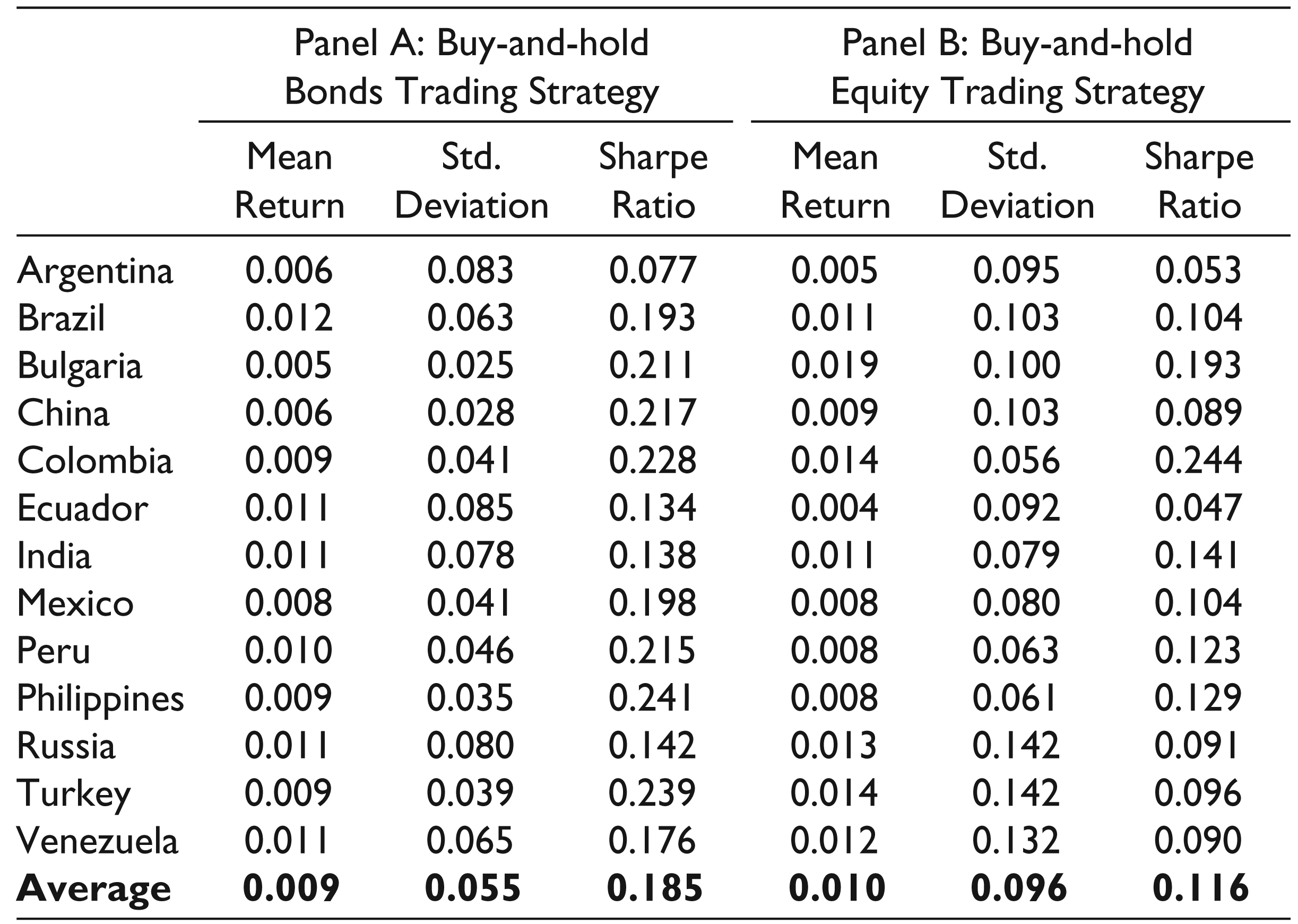

The passive buy-and-hold (stocks and bonds) strategy is the most appropriate benchmark for comparison purposes with active traditional and augmented BEYR-based strategies. It represents the highest possible return for the given level of risk with no active management (Levin & Wright, 1998). In this basic investing strategy, we buy bonds or stocks and hold them for the entire sample period, regardless of the fluctuations in the market. Conventional investing experience from developed markets suggests that stocks render a higher return than bonds over longer time horizons.

The Extreme Value Strategy

The extreme value strategy compares the current levels of traditional and augmented BEYR with the extreme values extracted from its historical distribution. Specifically, this strategy identifies those months when investors should switch their positions between risky and safe assets based on the thresholds that are set to the 10th and 90th percentiles of the unconditional distribution of the BEYR. To spot the deviation from the long-term equilibrium, the percentiles are set according to the first 60 months of observations and then rolled forward 1 month at a time. Thus, we employ the following trading rule: when the current value of the traditional BEYR is lower than the 10th percentile of its unconditional distribution, we would shift the funds from bonds to equity, and inversely, if the current value of the traditional BEYR is above the 90th percentile of its unconditional distribution, we would shift the funds out of stocks and into bonds. In this fashion we could identify the months when investors should be out of equities (or bonds) as the stock market (bond market) is too expensively priced.

Descriptive Statistics

Descriptive Statistics

Accordingly, when the current value of the augmented BEYR is lower than the 10th percentile of its distribution, we would shift the funds from US bonds to emerging market stocks or bonds. Inversely, if the current value of the augmented BEYR is above the 90th percentile of its distribution, we would shift the funds out of risky emerging market stocks or bonds into safe US bonds.

The thresholds BEYR rule is based on the Hoare Govett thresholds strategy. This active trading strategy typically used by investment managers employs fixed thresholds for incrementing the portfolio towards either the total equity return index or the return on government bonds (Levin & Wright, 1998). The selected fixed thresholds of 2.0 and 2.4 are commonly used by practitioners arbitraging between stock and bond markets in the UK.

The thresholds BEYR uses the following trading rules: A traditional BEYR value lower than 2.0 results in the decision to switch the position to equity, while a traditional BEYR value over 2.4 results in the decision to shift the funds back to bonds. Correspondingly, if the current value of the augmented BEYR is lower than 2.0, we would switch the position to risky assets (emerging market stocks or bonds), while the value of BEYR over 2.4 would result in the decision to shift the funds back to safe assets (US bonds).

Moving Averages Strategy

The moving averages investing strategy uses a crossover type of signal for switching the capital between bonds and stocks. Specifically, when a short-term average crosses the long-term average of BEYR, the signal is given for switching the positions. For executing the moving averages strategy in our empirical analysis, we consider 6 months as the short-term period and 24 months as the long-term period.

A ‘buy bonds and sell stocks’ signal arises when the short-term average crosses above the long-term average of traditional BEYR indicator, and correspondingly, the ‘buy stocks and sell bonds’ signal is triggered by a short-term average crossing below the long-term average. Subsequently, when a short-term average crosses above the long-term average of augmented BEYR indicator, the ‘buy US bonds and sell emerging market stocks or bonds’ (move the capital into safe assets) signal is given. Finally, the ‘buy emerging market stocks of bonds and sell US bonds’ (move the capital into risky assets) signal is triggered by a short-term average crossing below the long-term average of the augmented BEYR indicator.

Empirical Results

First, we turn to the question of whether or not the traditionally calculated BEYR variable can be used as a successful trading rule in emerging markets. In particular, we investigate the performance of traditional BEYR-based active strategies (extreme values, fixed thresholds rule and moving averages) relative to passive buy-and-hold bonds and equities strategies. To do so, we examined the mean returns, standard deviations and Sharpe ratios for each strategy. Additionally, we report the number of switches in placing the capital between stocks and bonds for each active trading strategy. Further, we expanded our empirical tests to the augmented BEYR-based strategies, compared their risk-adjusted returns to the benchmark buy-and-hold strategies, and examined whether or not they generate significantly higher average returns in comparison to the traditional BEYR-based strategies.

Table 3 presents the performance results for the benchmark buy-and-hold bonds and buy-and-hold equity strategies. On average, the emerging markets deliver a mean return of 0.9 per cent and 1.0 per cent per month for passively investing in bonds and stocks, respectively. Importantly, the risk-adjusted returns for the corresponding buy-and-hold bonds and stocks portfolios provide monthly Sharpe ratios of 0.185 and 0.116, respectively, across the emerging markets included in the sample. More specifically, emerging countries with the highest risk-adjusted returns from the buy-and-hold bonds strategy are Columbia and Turkey, while the highest Sharpe ratios among the emerging countries for the buy-and-hold equity strategy are delivered by Bulgaria and Colombia. After setting the benchmark strategies results, we proceed by comparing their performance with active BEYR-based investing strategies.

Passive Buy-and-hold Trading Strategies

Passive Buy-and-hold Trading Strategies

Next, we explore whether or not a traditional BEYR can be used as a profitable market timing tool for investing in emerging markets. Table 4 provides summary results of traditional BEYR-based investing returns, standard deviations, Sharpe ratios and number of switched positions between bonds and stocks. Specifically, we employ three active BEYR-based trading strategies, namely extreme values (Figure A1), fixed thresholds rule (Figure A2) and moving averages (Figure A3) to guide us on investing decisions about whether to place the funds in bonds or equity in emerging markets. The results indicate that the fixed thresholds rule is the only traditional BEYR trading strategy that delivers both the mean returns and Sharpe ratios compared with benchmark strategies. Specifically, countries with the highest risk-adjusted performance are Mexico and the Philippines with the respective Sharpe ratios of 0.311 and 0.318. Moreover, the extreme values and moving averages strategies exhibit higher average returns than the equity benchmark portfolio but not the bond benchmark portfolio. On average, the buy-and-hold bond portfolio demonstrates a superior performance measured in a higher Sharpe ratio (0.185) than both the extreme values (0.146) and the moving averages strategies (0.161). The emerging market countries with the highest risk-adjusted returns based on extreme values and moving averages BEYR-based strategies are Colombia and the Philippines. Although some active trading strategies do provide higher risk-adjusted returns than buy-and-hold strategies for certain emerging market countries, the overall result of whether or not the traditional BEYR is a useful market timing tool in emerging markets is negative. The passive buy-and-hold bonds strategy delivers higher risk-adjusted returns than many of the BEYR dynamic strategies.

Traditional BEYR Active Trading Strategies

The results thus far cast a doubt on traditional BEYR-based strategies’ performance as trading rules in emerging markets. We observe that basic passive strategies outperform traditional BEYR active strategies in many cases. We offer the following explanation for this finding. Emerging market bonds are not safe assets relative to emerging market stocks and therefore do not offer a hedging opportunity for investors in times of falling stock markets. 8 Therefore, investors with positions in emerging market stocks might prefer shifting their funds to developed market bonds instead (proxied by US bonds in our sample). Consequently, we create two new augmented BEYR measures in which we combine the US bond yields with emerging market stock and bond yields and investigate whether or not these new augmented BEYR strategies deliver higher risk-adjusted returns than buy-and-hold strategies as well as the traditional BEYR.

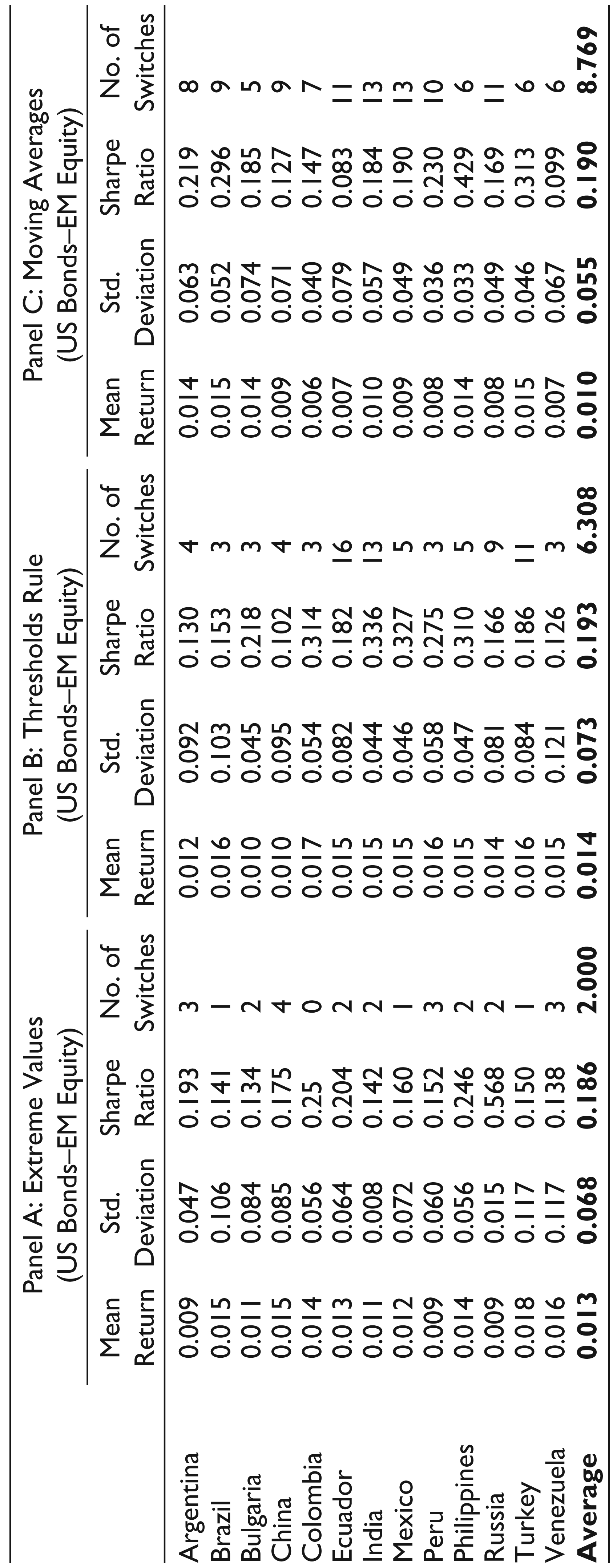

Table 5 shows the performance for the first augmented BEYR strategies incremented each period based on extreme values, the fixed thresholds rule and moving averages trading rules (accordingly displayed in Figures A1–A3). The augmented BEYR is composed from the US bond yields representing a safe asset and the emerging market equity yields as a risky asset. The results in Table 5 demonstrate that all of the investing strategies based on the augmented BEYR deliver both higher mean and higher risk-adjusted returns compared with all of the benchmark strategies. On average, Sharpe ratios for the augmented BEYR trading rules for extreme values (0.186), fixed thresholds rule (0.193) and moving averages (0.190) exceed the risk-adjusted returns of buy-and-hold strategies. Additionally, these strategies deliver higher risk-adjusted returns relative to traditional BEYR strategies with the exception of the fixed thresholds strategy. The number of switches for placing the capital between the US bonds and emerging market equities increases compared to the traditional BEYR strategies. More specifically, the augmented BEYR calculated from combining the US bonds with stocks from Russia gives the highest risk-adjusted returns for the extreme value strategy, stocks from India provide the highest returns for fixed thresholds rule and, finally, stocks from the Philippines deliver the highest returns for the moving averages strategy.

Augmented BEYR Active Trading Strategies: US Bonds–EM Stocks

Next, we combined the US bonds (safe) with the emerging market bonds (risky) to create a second augmented BEYR indicator and tested it against the benchmarks and the traditional BEYR strategies. In so doing we used the emerging market bonds as a risky ‘equity-like’ asset for timing the market. The results from Table 6 yield similar conclusions about the profitability of the augmented BEYR-based strategies. The risk-adjusted returns reported in Figures A1–A3 on extreme values, fixed thresholds and moving averages strategies are significantly outperforming the benchmark buy-and-hold as well as the traditional BEYR strategies. On average, dynamic strategies utilising US bond yields (as a safe asset) and emerging market bond yields (as a risky asset) deliver Sharpe ratios of 0.235 for the extreme values, 0.244 for the fixed thresholds rule and 0.207 for the moving averages strategy. On the individual country level, the augmented BEYR trading strategies provide the highest risk-adjusted returns when combining US. bonds with bonds from the following emerging market countries: The Philippines and Russia (for the extreme values and fixed thresholds strategies) and the Philippines and China (for the moving averages strategy).

Augmented BEYR Active Trading Strategies: US Bonds–EM Bonds

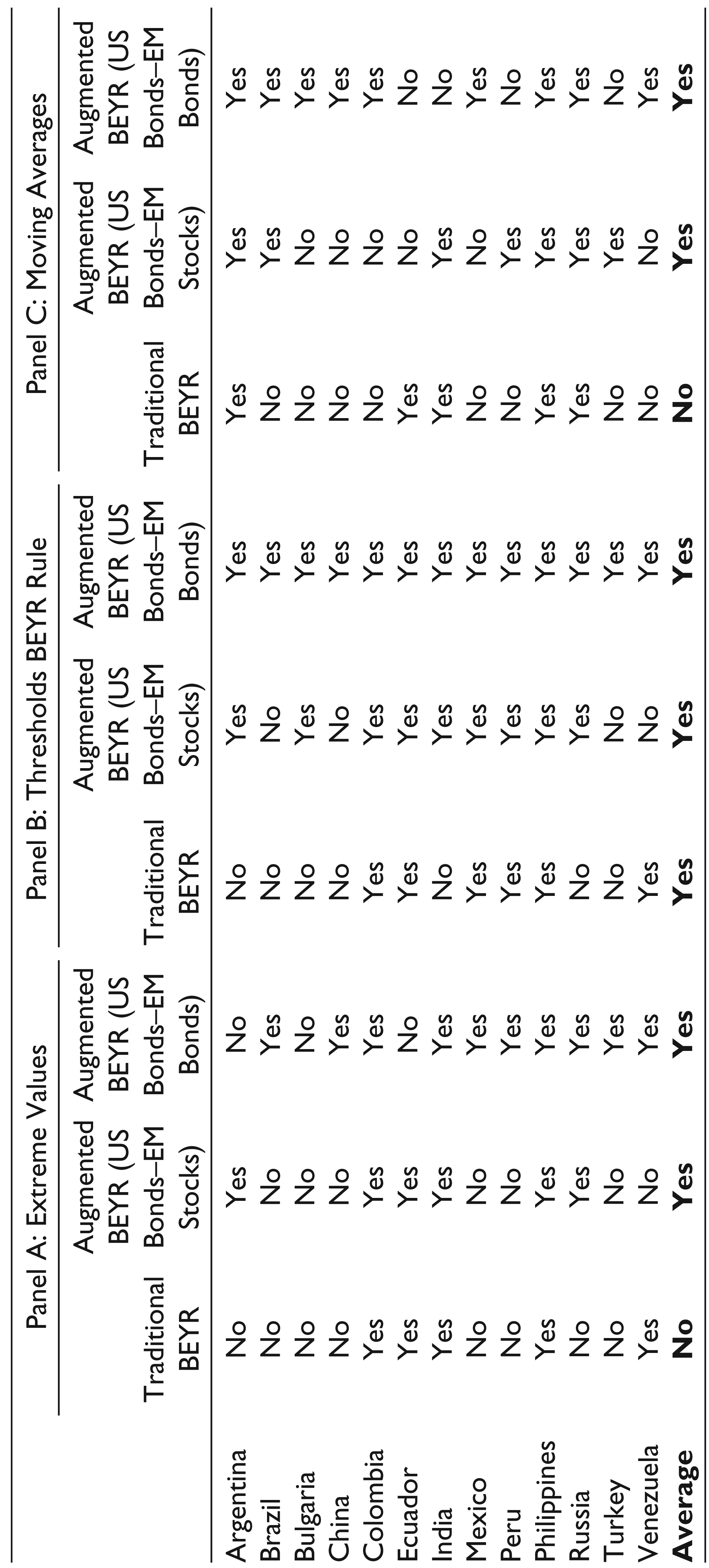

For ease of exposition, Table 7 summarises the results of the empirical tests and evaluates the performance of the traditional BEYR and the two augmented BEYR-based strategies relative the benchmark buy-and-hold stock and bonds strategies. Each emerging country from the sample is evaluated individually and compared with the benchmark strategies. Additionally, the averages across the emerging markets are calculated and compared as well. On the basis of risk-adjusted returns, we provide the answers to whether or not a particular active trading strategy outperforms both buy-and-hold bonds and buy-and-hold stocks benchmarks.

Summary of the Market Timing Profitability for Traditional BEYR and ‘Augmented BEYR’ Strategies

The summary of results reported in Table 7 suggests that, on average, the traditional BEYR strategies do not outperform benchmark strategies. On the other hand, all of the augmented BEYR-based trading rules deliver higher risk-adjusted returns than benchmark portfolios across emerging markets. This finding is far more evident in the case of the second augmented BEYR indicator that combines the US bonds with the emerging market bonds, giving further confirmation that emerging market bonds can be treated as ‘equity-like’ assets.

For the further comparison purposes between the traditional and augmented BEYR trading strategies relative to buy-and-hold bonds and stocks strategies, we create hypothetical portfolios with the initial value of one. We increment each portfolio every month according to the outcome determined by the trading rule. The mean return results for each portfolio are summarised in the figures provided in the Appendix. Finally, the tables in the Appendix present the robustness tests results of BEYR-based trading strategies. 9

Motivated by the inconclusive empirical evidence about the market timing ability of the BEYR, this study investigates the profitability of BEYR trading strategies in an international framework. By utilising the data from the emerging markets, we empirically examine the performance of various BEYR-based active trading strategies relative to the performance of benchmark buy-and-hold portfolios. Additionally, given the previous evidence that emerging market bonds have equity-like properties because of the specific country risk in emerging economies, we create new augmented BEYR variables combining the US bonds (proxy for safe assets) and emerging markets stocks and bonds (proxies for risky assets). Our results contribute to the literature in three important ways: First, our article provides new international evidence on market timing of the BEYR from the emerging markets. Specifically, traditional BEYR trading strategies do not deliver higher risk-adjusted returns relative to the benchmark buy-and-hold bonds and stocks strategies. Second, by employing the US bonds as a safe asset and emerging markets’ stocks or bonds as risky assets we construct the augmented BEYR indicator serving as a valuable practical tool that generates risk-adjusted returns persistently exceeding the returns of both buy-and-hold and traditional BEYR-based strategies. Third, we extend the literature on emerging market bonds by providing supplementary evidence that these assets possess ‘equity-like’ properties because of the specific country risk in emerging markets.

The empirical findings reported in this study show that the traditional BEYR investing strategies do not deliver significantly higher risk-adjusted returns relative to benchmark strategies. However, all of the augmented BEYR-based trading strategies (constructed from the US bonds as a proxy for safe assets and emerging market stocks and bonds as risky assets proxies) deliver higher risk-adjusted returns compared with the benchmark buy-and-hold bonds or stocks strategies. Empirical findings from this article can benefit those international investors seeking profitable trading opportunities between stock and bond markets.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: Vitaly Orlov gratefully acknowledges financial support from the OP-Pohjola Group Research Foundation (grant 201500087) and the Marcus Wallenberg foundation.

Footnotes

Acknowledgements

We thank the participants of the 2016 FMA European Conference and INFINITI Conference on International Finance for helpful suggestions.

Hypothetical Portfolio Values Based on Trading Rules Used

Hypothetical portfolios with the initial value of one are incremented every month according to the outcome determined by the trading rule. The mean return results for each portfolio are summarised in following graphs.

The results of robustness tests are summarised in Table A1. Essentially, the results of the analysis based on the alternatively specified aggregate strategies are very similar to those reported in Tables 3–7. Traditional BEYR strategies (Panel B) do not provide significantly higher risk adjusted returns relative to benchmark buy-and-hold stocks and bonds strategies (Panel A). Furthermore, incorporating US bonds as a safe asset relative to the emerging market stocks and bonds (Panels C and D) provides significantly higher Sharpe ratios relative to benchmark strategies (Panel A). Thus we confirm the previous findings giving further confirmation that emerging market bonds can be treated as ‘equity-like’ assets.

Note: The empirical analyses throughout this study are focused on the dollar-denominated emerging market securities. It is important to stress that dollar-denominated securities are highly financially integrated with US markets and therefore the risk of unpredictable fluctuation in the foreign currencies is completely eliminated as a factor that could impact the results. Thus, further research is warranted on the BEYR style investing by using financially less integrated local-currency assets as the role of currency risks, capital constraints in the form of taxes and the investment quotas might play an important role in impacting the results.