Abstract

We employ event study methodology to analyze the impact of unprecedented unconventional monetary policy (UMP) measures employed by the Reserve Bank of India to fortify monetary transmission mechanism and to restore financial stability. We find that the UMP announcements result in a decline in bond yields and yield spread as well as increase in market capitalization and sectoral portfolio of stock returns. Evaluating the relative efficacy of UMP measures, we find that targeted long-term repo operation announcements are more effective in easing bond yields than mere long-term repo operations. Our findings provide beneficial inference for day-traders and investors as asset prices increase significantly and durable goods producing stock returns found to be higher than those of non-durable goods. The lessons that can be drawn for the emerging market economy central banks, who do not have enough space to conduct conventional monetary policy and even when they do not face zero lower bound interest rate, they still can employ UMP tools to directly influence banks cost of funds, and long-term bond yields and interest rates, and in turn, portfolio of stock returns and investments to stimulate aggregate demand.

1. Introduction

Following COVID-19 pandemic severe macroeconomic disruption and financial distress worldwide, major central banks once again, based on the post global financial crisis (GFC) experience, resorted to unconventional monetary policy (UMP) tools (Potter & Smets, 2019; Yehoue et al., 2009) to stabilize financial markets and fortify monetary transmission mechanism, and in turn, cushioning aggregate demand. Most of the central banks continued with negative interest rates as a primary tool (Echarte Fernández et al., 2021; Hartley & Rebucci, 2020). In order to smoothen liquidity management, several unprecedented steps have been taken such as, lowering the reserve requirement of commercial banks, extending the maturity of typical lending operations, and relaxing the collateral norms to extend their support in credit creation. Central banks of emerging market economies (EMEs) too revised their collateral norms, extended liquidity operations, and expanded their asset purchase programs (APPs) to counter the twin shocks 1 of aggregate supply and aggregate demand arising from COVID-19 (Hartley & Rebucci, 2020).

Similarly, the Reserve Bank of India (RBI) has adopted various UMP measures to mitigate the impact of COVID-19 pandemic (Talwar et al., 2021). The most important among them are extended long-term lending operations (LTLOs), APPs, which are also known as quantitative easing (QE), and forward guidance (FG). Besides, RBI has also conducted a special type of QE measure commonly known as “operation-twist (OT)” (Das et al., 2020). We draw our motivation to study the effectiveness of RBI’s UMP measures since they differ from their developed country counterparts on several aspects. First, unlike its developed country counterparts who have resorted to UMP measures when confronted with the difficulty of pursuing monetary policy effectively at “zero lower bound” nominal interest rate, the RBI conducted UMP even when the nominal interest rates were positive and nowhere near zero lower bound. Second, while in advanced economies LTLOs, APPs, forex interventions were the main UMP policy tools, in case of India, the share of liquidity support LTLOs measures were very high both compared to advanced economies and EMEs, with three-fourth being new measures (RBI, 2022). The LTLOs auctions have been conducted with a purpose to infuse systemic liquidity in the banking system. Third and more notably, when the liquidity measures encountered risk aversion among banks on-lending the RBI’s funds to pandemic afflicted troubled entities, special refinance facilities through targeted lending operations were provided to financial institutions to ameliorate sector- and small institution-specific liquidity constraints. Fourth, additional liquidity neutral special open market operations (OMOs) of simultaneous purchase and sale of securities were carried out evenly across the yield curve facilitating monetary transmission (Patra, 2022). Fifth, targeted LTLOs for health, medical supplies, and contact intensive sectors were the additional features in India. Sixth, the size of APPs, crucial to lower the long-term bond yields as well as to narrow yield spreads, is also significantly lesser in magnitude than the developed counterparts and forex intervention measures were very meager to the overall UMP measures (Hartley & Rebucci, 2020; RBI, 2022). Finally, RBI as an EME central bank has adopted UMP measures for the very first time, making it an ideal case to study to evaluate the effectiveness of UMP measures in India. We hope that, in addition to the existing literature, our findings will be of considerable interest to policy makers and financial market participants.

The extant literature examining the effectiveness of UMP pertains mostly to advanced economy experiences. The US Fed’s QE, in response to tackling the great recession, has successfully lowered the long-term treasury yields along with the reduction of corporate bond spreads (D’Amico & King, 2013; Gagnon et al., 2010; Krishnamurthy & Vissing-Jorgensen, 2011). Swanson (2011) examining OTs’ announcement effect, finds that the OTs lowered US long-term treasury yields. However, the finding on the impact of QE on asset prices is a mixed bag. While Krishnamurthy et al. (2018), Kurov and Gu (2016), and Rogers et al. (2014) found that UMP led to an increase in bond prices and stock returns in the US and Europe, whereas Florackis et al. (2014) and Hosono and Isobe (2014) found that UMP measures in UK and Japan, respectively, worsened the economy further and in turn forcing the investors to look for alternative safe assets. Besides having an influence on asset prices, UMP announcements also impact market participants’ sentiment and expectations about future market volatility (VIX). Several studies demonstrate that UMP shocks significantly mitigate the financial market stress and boost economic sentiment (Fassas et al., 2021). The sparse literature evaluating the impact of UMP measures in EMEs during the pandemic, however, recently has garnered considerable interest. Ha and Kindberg-Hanlon (2020), Hofmann et al. (2021), and Sever et al. (2020) of IMF, BIS, and World Bank, respectively, found that the UMP measures have been more effective than the conventional monetary policy measures in lowering bond yields and sovereign credit default swap rate. In terms of methodology, several studies have used event-study methodology to analyze the impact of monetary policy surprises on financial markets (Gagnon et al., 2011; Krishnamurthy & Vissing-Jorgensen, 2011; Swanson, 2011).

Given this backdrop, the core objective of pursuing UMP by the RBI has been to restore monetary transmission mechanism and to stabilize financial market: reduce long-term bond yields and yield spreads of different maturities, and stock returns through easing monetary conditions with largescale systemic liquidity infusion. Therefore, using an event study methodology, we limit our empirical analysis to estimate the impact of UMP surprise announcements by the RBI on the financial market, that is, on bond yields, yield spread, and stock returns. Additionally, we estimate the impact of these UMP announcements on different sectoral portfolios of stocks. We also analyze the efficacy of different UMP measures in reducing bond yields and yield spreads.

Our study contributes to the literature in three ways. First, our study is one of the first that examines the impact of UMP surprises on the changes in bond yields of different maturities and stock returns since the beginning of the pandemic; comprehensively extending the study by Talwar et al. (2021) who narrowly examined the bond market only. Second, we examine the impact of UMP on the sectoral portfolio of stock returns to get further insights on the sectoral impact. Finally, we examine the efficacy of LTLOs and OT announcements in reducing bond yields and yield spread, respectively. In the first set of results, estimating the impact of UMP surprises on bond yields and stock returns, we find that expansionary UMP surprises reduce bond yields and increase stock returns. In our second set of results on the impact of expansionary UMP surprises on the sectoral portfolio stock indices, our findings are consistent with earlier results for most of the sectors (see Table 4). Finally, after evaluating the efficacy of different UMP tools employed by the RBI, we find that TLTLOs are more successful in decreasing bond yields than LTLOs, and OTs have a significant impact on yield spread as well. Our findings have wider global policy implications both for central banks as well as investors of EMEs as well. Investors can earn significant returns, since asset prices increase significantly following UMP announcements. The EME central banks, who do not have enough space to conduct conventional monetary policy and even when they do not face zero bound lower interest rate, can also adopt UMP tools to stimulate aggregate demand.

The rest of the article is organized as follows. The second section outlines the monetary transmission channels through which UMP measures affect the financial market. The third section highlights the Indian experience with UMP. The methodology employed for the study is discussed in the fourth section. The fifth section describes the data source. The sixth section estimates the impact of UMP surprises on bond yields and stock returns including its impact on sectoral portfolios. The seventh section estimates the impact of LTLOs and OTs announcements on bond yields and yield spread, respectively. The robustness checks are considered in the eighth section. The final section concludes the findings and discusses policy implications.

2. Channels Through Which UMP Measures Affect Financial Market

The emergence of UMP has its origin in the Keynesian liquidity preference theory. As interest rates become “zero-bound,” public prefers to hold cash rather than alternative financial assets. Consequently, as and when the economy is in a liquidity trap, any attempt by the central bank to inject additional liquidity through the monetary system to increase the level of spending in the economy, on the contrary, results in public passively holding additional liquidity without incremental consumption or aggregate demand. Therefore, monetary transmission mechanism through the conventional interest rate channel fails to affect aggregate demand and asset prices at low interest rates, and hence, the central banks needed to employ UMP tools to stabilize financial markets, stimulate aggregate demand and output in the economy.

The extant literature on the operation of UMP tools identifies within the interest rate transmission channel, three main sub channels: signaling, portfolio balance (PB), and liquidity channel (Bowdler & Radia, 2012). The signaling channel enables the central bank to effectively communicate to restore market confidence and alter public perception of prospective monetary policy changes (Cecioni et al., 2019). Following the UMP announcement, if investors anticipate that the central bank will maintain lower interest rates for longer, then the announcement will influence long-term interest rates by reducing expected future short-term interest rates (Lloyd, 2017). Through the PB channel, a central bank can influence the financial market by purchasing long-term assets both from the public and private sectors. The purchase of the long-term assets by the central bank from the private sector increases the private sectors’ holdings of short-term reserves. So long as investors view these assets as imperfect substitutes the price of long-term assets increases and yields decrease. Thus, the changes in the relative holdings of the two asset classes result in portfolio rebalancing and movement in asset prices (Bowdler & Radia, 2012). The third, liquidity channel refers to the increase in asset prices due to increase in market liquidity because of APPs; especially when the financial market is under stress. An increase in liquidity provides consistent buyers for assets resulting in an increase in assets prices and decrease in bond yields (Lloyd, 2017).

The comparative importance of these channels is empirically investigated by several studies. Krishnamurthy and Vissing-Jorgensen (2011) found that both the signaling channel and the portfolio channel are considerably effective in reducing long-term asset yields. Gagnon et al. (2011) also found that the majority of yield changes caused by the Fed’s large-scale asset purchases are transmitted through the PB channel. Since the main objective of our study is to examine the impact of UMP measures on both the bond market and portfolios of stocks, the PB channel becomes a potent channel in explaining the monetary transmission mechanism as it operates through the changes in the composition of assets in the financial market. Therefore, we are primarily investigating the effectiveness of the PB channel as one of the key transmission channels for the UMP in India.

3. Indian Experience with Unconventional Monetary Policy

During the pandemic, the key UMP measures adopted by RBI to minimize the disruption in the monetary transmission mechanism are LTLOs, OTs, APPs, and FG. Under LTLOs, RBI has provided liquidity support to the commercial banks for up to three years at the repo rate, which is much lesser than the market rate. In this series, RBI has made five long-term repo operation (LTRO 2 ) announcements, each amounting to ₹25,000 crore. The liquidity support amounting to ₹125,117 crore has been facilitated by the commercial banks to improve the credit flow in the economy. However, due to the increase in the credit demand caused by the pandemic and in turn to reduce the cost of funds, banks have repaid ₹123,572 crore (about 98.8% of total funds availed) much before its maturity.

Further, another series of four targeted long-term repo operation (TLTRO 3 ) announcements each amounting to ₹25,000 crore has been made to provide liquidity support to targeted sectors, particularly public sector entities facing liquidity stress. RBI deployed a liquidity support of ₹100,050 crore to the commercial banks to lend/invest in PSUs (Talwar et al., 2021). While TLTRO 2.0 notified an amount of ₹25,000 crore, mainly focused on microfinance institutions and NBFCs, but only ₹12,850 crore issued due to a lack of demand for additional liquidity. In the special series of liquidity, RBI announced three additional LTLOs, one on-tap long-term repo operation (OTTLTRO) and two special long-term repo operations (SLTROs) of ₹100,000 crore and ₹1,000 crore, respectively, to provide liquidity support to the banking system.

Under APP, RBI employed a special type of QE termed as OT, which refers to the simultaneous purchase and sale of government securities. Throughout the entire pandemic period, RBI conducted a total of 24 special purchase operations of amount ₹10,000 crore each (Talwar et al., 2021). RBI also purchased state government securities, commonly known as state development loans. FG became a prominent tool of RBI’s communication strategy regarding its intention on setting the future policy rate path to reassure the market players that it will take any required step to sustain a comfortable liquidity environment and ensure stability in the financial market.

Table 1 summarizes the list of all the announced measures undertaken by RBI that we analyze with its events’ dates. These events also include all the Monetary Policy Committee (MPC) meetings as the proxy for the FG along with the actual FG bulletin. In total, our event study includes a total of 91 monetary policy announcements ranging from December 2019 to December 2021.

Unconventional Monetary Policy Tools and Announcement Dates.

4. Econometric Model and Identification Strategy

The econometric framework consists of two different event study models to investigate the relationship between UMP surprises and financial market performance capture through bond yields and stock returns. In our first event study econometric model, we use a similar approach as Bernanke and Kuttner (2005), Rogers et al. (2014), and Haitsma et al. (2016) to estimate the overall impact of UMP surprises. As we are interested in estimating the response of stock returns and the changes in the bond yields, we estimate the following model:

where dependent variable Ri, t, reflects both the return on day t of a stock indices or portfolios i in the stock market as well as changes in the bond yields of different maturities. The intercept α is a constant, MPS t represents the UMP surprises on day t, X t is a vector of control variables on day t and εt is the error term on day t. The coefficient β represents the impact of monetary policy surprises on stock returns and the changes in the bond yields. We also consider control variables in order to capture the plausible impact of any other variable on the dependent variable. The vector of control variables consists of VIX, financial stress index (FSI) of the emerging market, 4 Nifty 50 stock returns, and S&P 500 stock returns. Following Mukherjee and Roy (2016) and Heath and Kopchak (2015), we include S&P 500 stock returns as a control for international shocks.

The estimation of the model (1) follows three crucial steps. We first calculate the individual stock returns as well as returns of portfolio of stocks as follows:

where Pi, t reflects the closing price of a given stock index or portfolio of stocks i on day t.

We then calculate the change in the bond yields of different maturities using the following equation:

where, Xi, t is the daily bond yields of different maturity.

The final, and most important step in estimating model (1), is the identification of UMP shocks. We identify UMP shocks (MPS) following Wright (2012) and Rogers et al. (2014) identification techniques. We use the RBI’s UMP announcement dates as event dates and compute UMP shocks (MPS) as the first principal component of the intraday changes in the front-month futures contract 5 price of the 5-, 10-, and 15-year government bonds (Fischer, 2020). In a similar vein, Gagnon et al. (2010) and Krishnamurthy and Vissing-Jorgensen (2011) measured monetary policy shocks directly from intraday changes in asset prices. However, unlike Wright (2012) and Rogers et al. (2014)’s who have estimated the changes using high-frequency intraday data around the Federal Open Market Committee announcement time, we use intraday net changes 6 on the day of the UMP announcement. This is for two reasons. First, due to the unavailability of exact time of UMP announcements by RBI and second, UMP surprise announcements often result in lengthy adjustment periods in the financial markets (Carlson & Lo, 2006; Gagnon et al., 2010), therefore, we proceed with “one-day” policy windows and further use “two-day” policy windows to check the robustness. In addition, we also estimate the impact of UMP shocks on the volatility of stock returns and on the investor’s sentiment as well.

Further, in order to analyze the effectiveness of each of the UMP tools employed by the RBI, we use our second event study model similar to Brown and Warner (1985). Post-GFC, several studies have used such an event study framework to analyze the impact of UMP measures employed by the central banks across the world (Breitenlechner et al., 2021; Hartley & Rebucci, 2020; Krishnamurthy & Vissing-Jorgensen, 2011). The basic objective is to discover the abnormal changes attributed to the event by compensating for the changes due to overall market fluctuation. Following the mean-adjusted return model, we compute the abnormal changes (ARi, t) in the bond yields as follows:

where

where for each of the event day the cross-section average abnormal changes of N securities are obtained as follows

and the SD is computed over an estimation period of T0 days. Thus,

While the event study method has been used by many studies, yet it is strictly based on some fundamental assumptions. Following Neely (2015), we highlight three key underlying assumptions. First, the policymakers must have a prior knowledge of asset price movements. Second, the changes in expectations of the financial markets must happen during the UMP surprise announcement event windows only. Third, any other news during the event windows must have a minimal overall impact.

5. Data Source

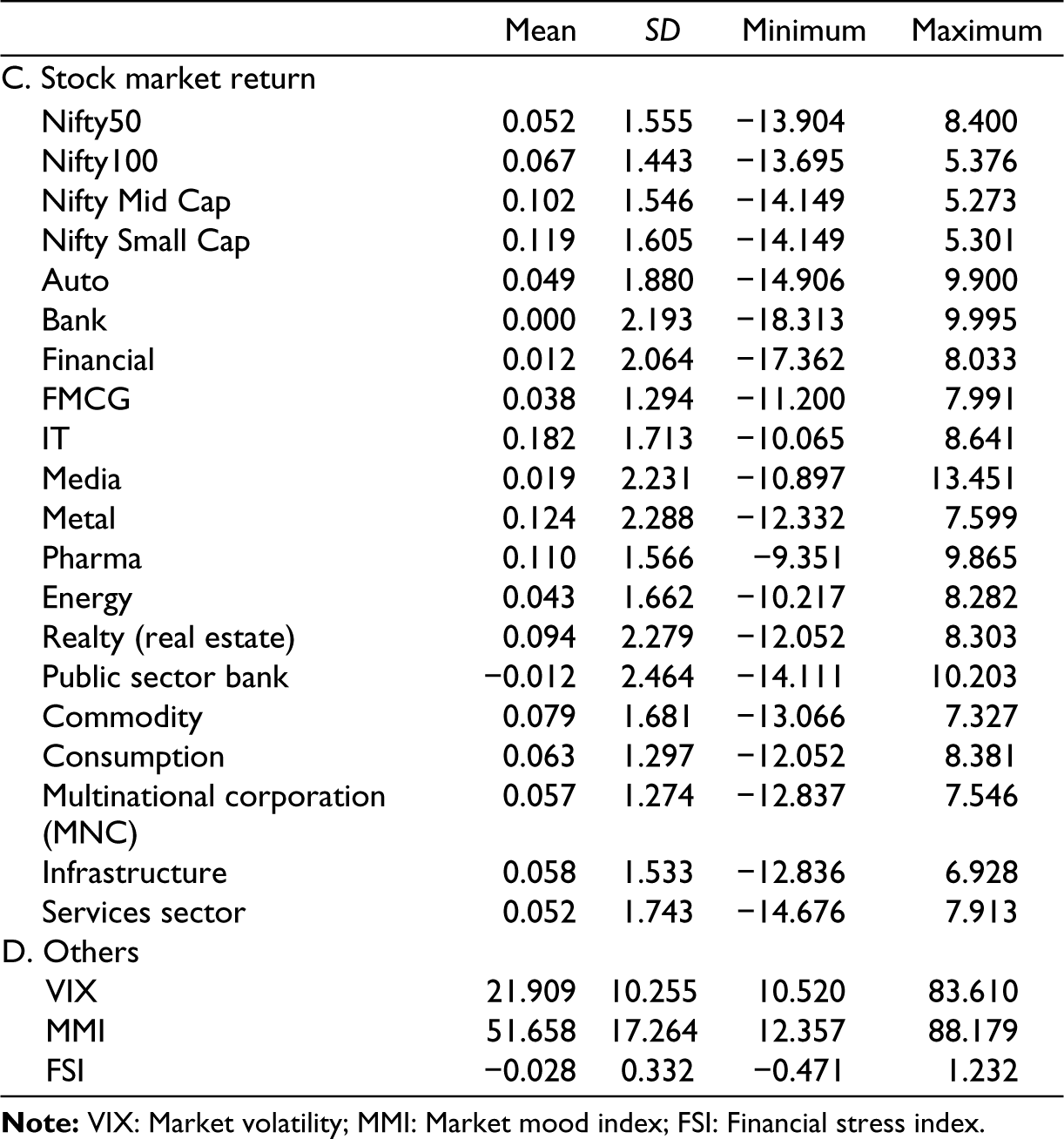

We use the data from December 1, 2019 to December 31, 2021 covering all the UMP announcements during pandemic period for our analysis. The data for bond yields of different maturities are collected from Bloomberg database and have been used to estimate the bond spreads. 7 The National Stock Exchange provides the historical data of the Nifty 50 stock index and the other sectoral indices. 8 We use 10 major sectoral portfolio indices and 5 highly influential thematic indices based on the market capitalization. We have also considered other stock portfolios such as, Nifty100, mid-caps, and small-caps. To assess the impact of UMP on VIX we have used VIX which measures VIX based on NIFTY index option prices. In order to measure the investor sentiment, we use market mood index (MMI) 9 developed by Smallcase in collaboration with ET Now. To control the spill-over effect of US monetary policy, we use Standard and Poor’s 500 (SP500) daily returns provided by the Bloomberg database. Finally, we use the FSI of emerging markets provided by the Office of Financial Research as a control variable for the financial market condition. The descriptive statistics of all the variables used for the analysis is given in Table 2.

Descriptive Statistics.

6. Empirical Analysis

Before proceeding with the analysis, we find out the correlation between financial asset prices. We find that the bond yields are negatively correlated with NIFTY50 stock returns. Surprisingly, we also find bond yields and NIFTY50 stock returns are negatively correlated with VIX. As expected, we find that UMP announcement surprises are negatively correlated with bond yields and positively correlated with NIFTY50 stock returns. We also find a positive correlation between NIFTY50 stock returns and the investor sentiment index.

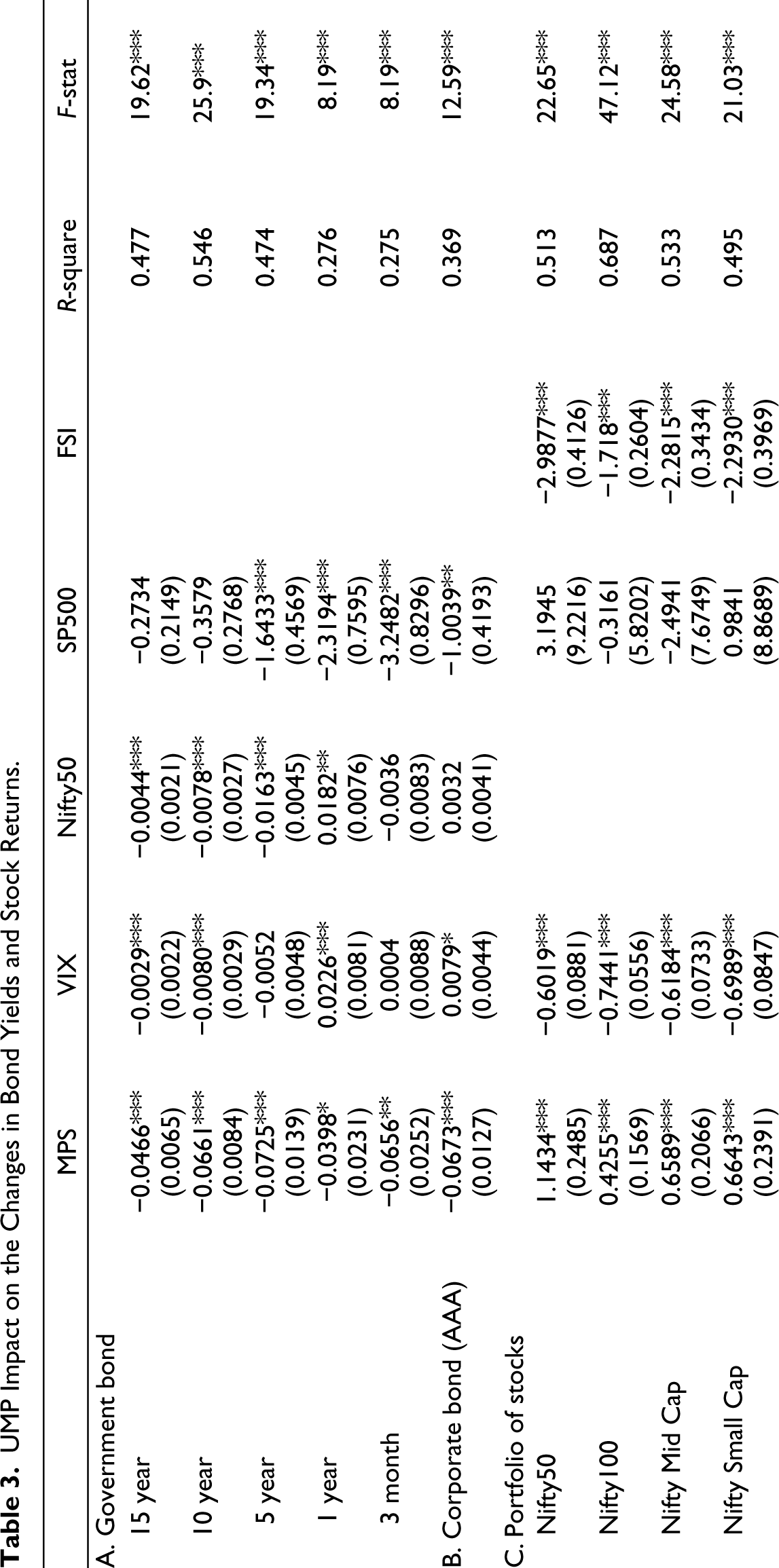

Finally, we estimate Equation (1) and discuss the UMP impact on stock returns and bond yields. Table 3 presents the regression result of changes in the bond yields and stock returns, along with VIX, MMI, and bond spreads. The negative coefficients of MPS for bond yields suggest that UMP surprises reduce bond yields. Specifically, a one SD UMP shock reduces the 10-year government bond yields by six basis points. This result is similar to Wright’s (2012) findings of Fed’s one SD monetary policy shocks lowers 10-year US Treasury yields by 12 basis points. We also find that 10-year corporate bond yields reduce by 6.5 basis points; which is in line with Wright (2012). The 5-year government bond yields are reduced by about seven basis points (one basis point more than the 10-year government bond yields), whereas one-year government bond yields reduce by only about four basis points. Similarly, 15-year government bond yields reduce by five basis points and 3-month treasury yields reduce by six basis points. This reduction in long-term bond yields is only possible through UMP measures since the sudden outbreak of COVID-19 pandemic gripped the Indian economy with twin shocks of aggregate supply and aggregate demand, and consequently collapse of financial markets. RBI cut the policy repo rate unprecedently by 115 bps within the first three months and kept it at record low of 4 percent, reverse report rate by 155 bps, cash reserve ratio by 100 bps and infused liquidity through OMOs to cushion aggregate demand; leaving no room for the use of conventional monetary policy any further. To overcome the persistence risk of further reduction in nominal interest rate to restore monetary transmission mechanism, asset prices and aggregate demand at low interest rates, RBI employed UMP tools to lower the banks’ cost of funds and to reduce the long-term bond yields and interest rates more directly to stimulate aggregate demand. All the estimated regression results are statistically significant (see Table 3(A, B)).

UMP Impact on the Changes in Bond Yields and Stock Returns.

Standard errors are in parenthesis and heteroscedasticity robust.

Yields are in percentage points.

Returns are 100 times log returns.

The positive coefficients of NIFTY50 stock returns and other portfolio of stocks indicate that UMP surprises lead to an increase in stock returns (see Table 3(C)). Specifically, one SD UMP shocks increase Nifty50 stock returns by about 1.14 percentage points. The results are similar to the Rogers et al. (2014) findings of Fed’s one SD monetary policy shocks increase S&P stock returns by 0.94 percentage points. The results also indicate that both NIFTY mid-cap and small-cap stock returns increase by 0.66 percentage points, followed by Nifty100, which increases by 0.42 percentage points. We also find that UMP surprises increase the India VIX volatility index by 0.85 percentage points and MMI by 1.91 percentage points. The positive coefficient of MMI indicates that the investor gets greedier following UMP announcements. The results also show that yield spread between 10-year and 3-month maturity government bond yields reduces by five basis points.

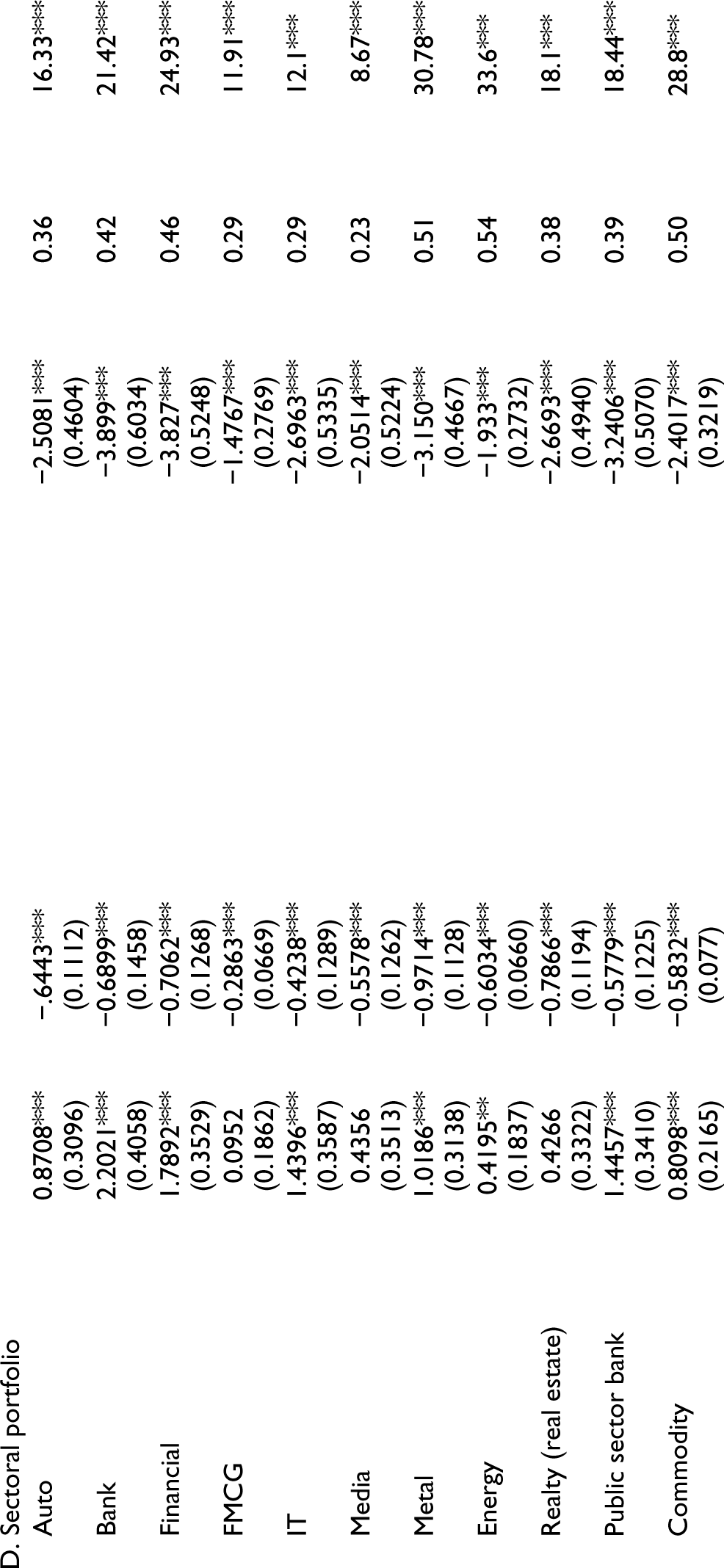

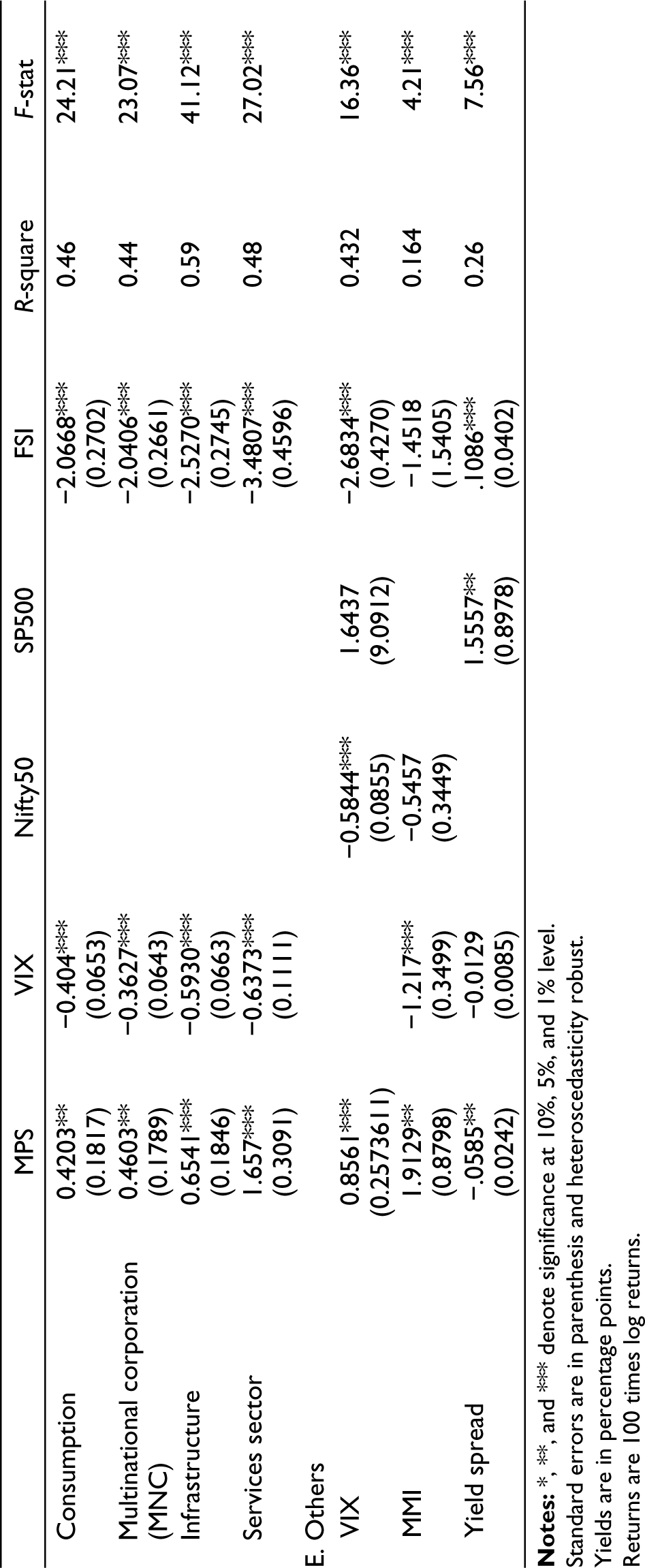

Table 3(D) reports the regression output for ten major sectoral portfolio indices and five highly influential thematic indices. Similar to the previous results, we find that the estimated coefficients of UMP surprises to be positive for all the sectoral indices indicating an increase in stock returns. The impact of UMP surprises found to be the most for the banking, financial and service sectors. This indicates that UMP surprise announcements eased financial market conditions. A SD UMP surprise leads to an increase in banking sector returns by about 2.20 percentage points, whereas financial and service sector stock returns increased by 1.78 and 1.66 percentage points, respectively. Further, durable goods-producing sectors such as, automobile, IT, metal, and real estate have higher coefficients while sectors producing non-durable goods such as, fast-moving consumer goods (FMCG) and media have lower and insignificant coefficients. Monetary policy operates through the compositional effect on aggregate demand by stimulating interest-sensitive long-term business investments and households’ expenditure on consumer durable goods. A higher return on durable-goods sector indicates the relative efficacy of monetary policy transmitting through UMP measures taken to reduce the cost of borrowing encouraging businesses to increase long-term investments and households to spend on durable goods; which in turn reflects in higher stock returns for investors. Since the change in demand for nondurable goods may not show significant variation, so will the returns on them. These findings are similar to Haitsma et al. (2016) that durable goods producing sectoral stock returns are higher than those of non-durable goods. We also find that both the control variables FSI and VIX used in the regression model are statistically significant (see Table 3(E)). The negative estimated coefficients of FSI indicate that heightened financial stress reduces the sectoral portfolio stock returns. Similarly negative coefficients for VIX suggest that heightened volatility reduces the sectoral portfolio stock returns.

7. Effects of Different UMP Announcements

We estimate Equation (5) and discuss the impact of different types of UMP announcements on bond yields and yield spread. The primary objective of conducting LTLOs is to bring down bond yields, whereas OTs are conducted to reduce the yield spread between the long-term and short-term maturity bonds.

7.1. Impact of LTLO Announcements on Bond Yields

Table 4(A) reports the changes in government bond yields of different maturities ranging from 3 months to 15 years. We also report the impact of LTLO announcements on changes in AAA 10-year corporate bond yields. We find that LTROs, TLROs, and SLTROs impact differently on the announcement date (day zero). TLTRO announcements have been more effective in lowering bond yields compared to LTROs. The cumulative reduction of bond yields is found to be higher for 1-year maturity compared to government bonds of longer maturity. Cumulatively eleven LTLO announcements have softened the 1-year government bond yields by about 112 basis points (bps), compared to the reduction of 76 bps and 53 bps for the 3-year and 5-year bond yields, respectively. However, surprisingly we find that the cumulative reduction of 10-year government bond yields is of only nine basis points, which is substantially lesser compared to the government bond yields of 3- and 5-year maturity. The LTRO announcements are found to be more effective in softening the yields compared to other LTLO announcements. In contrast, the cumulative reduction in 10-year corporate bond yields is significantly higher, that is, 73 basis points.

We provide t-statistics in the parenthesis in order to check the statistical significance of the changes in yields. We find that the changes in yields after TLTRO announcements are mostly significant compared to LTRO announcements. The impact of SLTRO announcements is found to be statistically insignificant for changes in the government bond yields of all maturities.

Impact of Different UMP Announcements.

Standard t-statistics are in parenthesis.

7.2. Impact of OTs on Bond Yields Spread

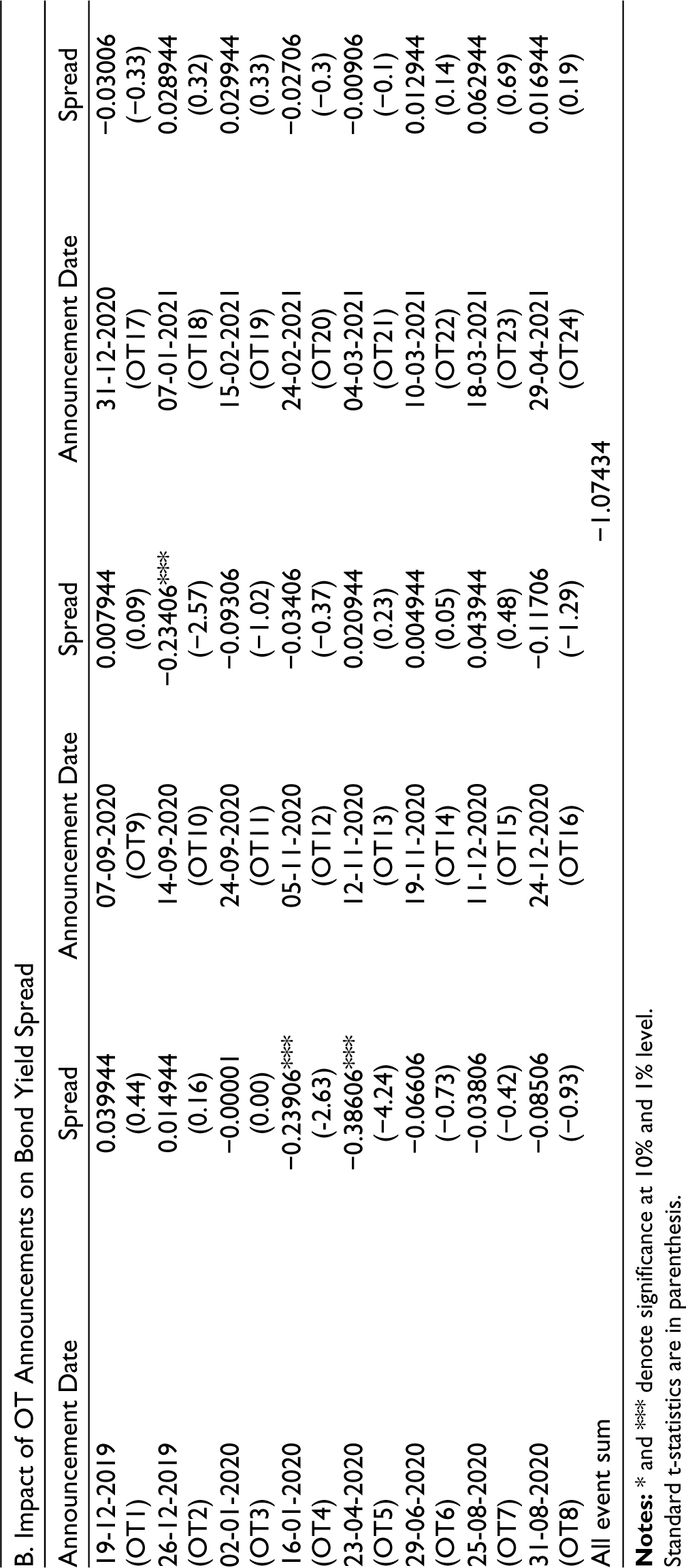

Table 4(B) reports the impact of the OT announcements on the changes in the yield spread between 10-year and 3-month maturity government bonds. As monetary authority, the main objective of conducting OTs is to reduce the yield spread. The results suggest a cumulative reduction of yield spread by 107 bps due to all OT announcements. During the pandemic period, RBI announced a total of 24 OTs. The finding suggests that out of 24 OTs, eleven of them have given counterintuitive results. One of the primary reasons for these theoretic results is due to the occurrence of the other significant events near the announcement dates such as, anticipation of fiscal stimulus, higher expected inflation, and uncertainty about OMOs. Besides, the loss of confidence in the ability of the government to tackle the pandemic could also be the reason for the rise in yield spread. However, the increase in the yield spread is found to be statistically insignificant, suggesting, therefore, a successful conduct of OT.

Similar to the LTLOs results, we also report the t-statistics in order to check the statistical significance of the changes in the yield spread. We find that the changes in the yield spread after OT announcements are statistically significant for the few initial OT announcements only.

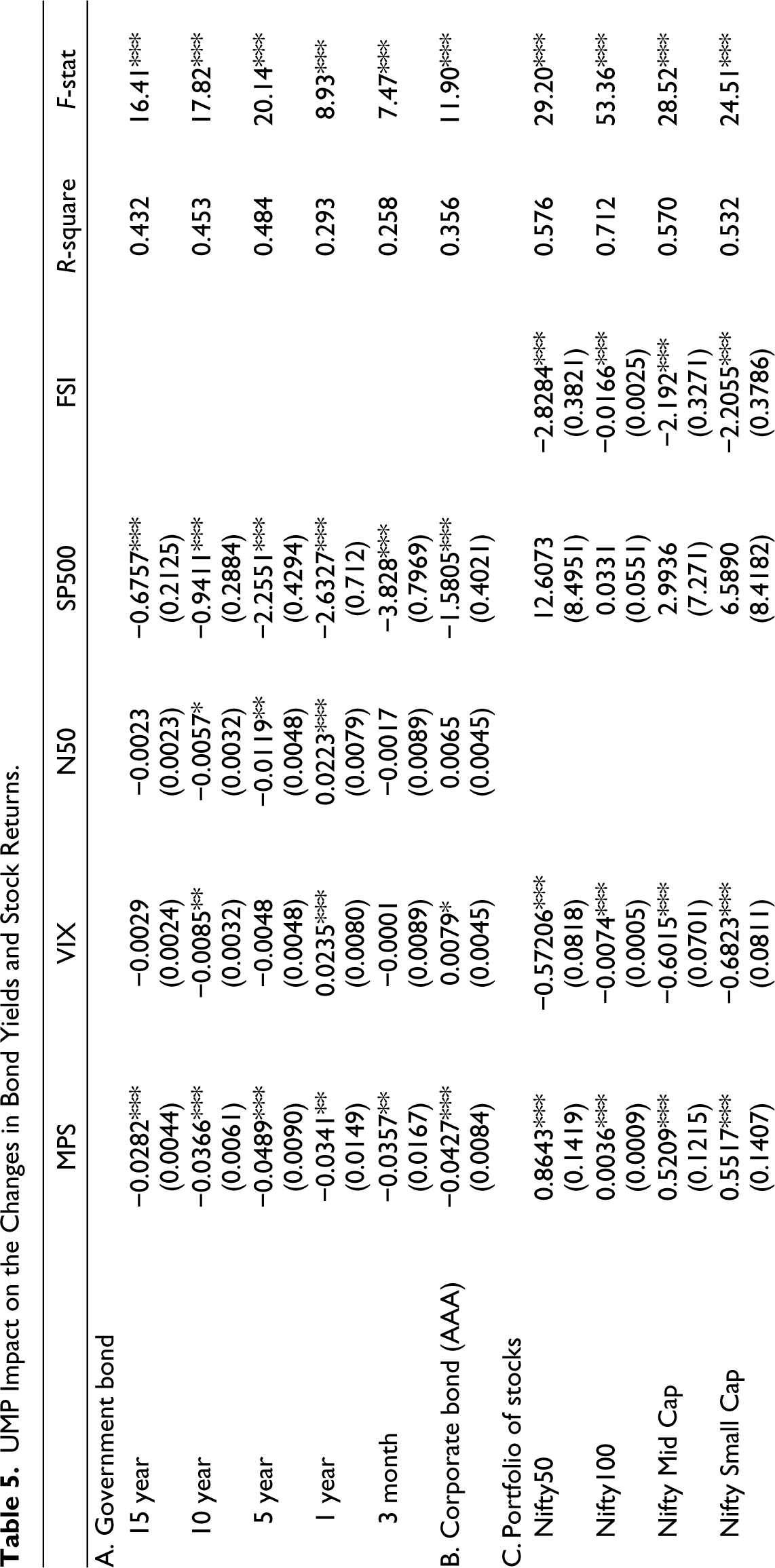

8. Robustness Check

In order to check for robustness of our results, we once again compute the UMP shocks (MPS) as the first principal component of the two-days cumulative changes in the front-month future contract of 5-, 10-, and 15-year government bonds. Using Equation (1), we re-estimate the impact of UMP surprises on changes in the bond yields of different maturities and stock returns, along with VIX, MMI, and bond spread. The estimated results (reported in Table 5) are found to be similar to the earlier results; although they differ in the magnitude of their impact both on changes in the government bond yields and stock returns. The findings suggest that an UMP shock of one SD lowers the 10-year government bond yields by about four basis points; which is two basis points less than our primary findings. This discrepancy might be due to the increase in the event window size from intraday to 2 days. We observe comparable discrepancies in other government bond yields as well. However, one SD UMP shocks lead to an increase in Nifty50 returns by about 0.86 percentage points compared to the 1.91 percentage points in our earlier finding, while the impact on investor sentiment remains insignificant.

UMP Impact on the Changes in Bond Yields and Stock Returns.

Standard errors are in parenthesis and heteroscedasticity robust.

Yields are in percentage points.

Returns are 100 times log returns.

Further, we also estimate Equation (1) to measure the impact of UMP surprises on different sectoral portfolio of stock return indices. The estimated results, as reported in Table 5(D), indicate a similar impact but of a lesser magnitude for all the sectors. Similar to the primary findings, the results indicate that the durable goods-producing sectors have given higher stock returns compared to the non-durable goods producing sectors.

9. Conclusion and Policy Implications

The objective of RBI, as a central bank, is to fortify monetary transmission mechanism and ensure financial market stability. Toward this end, through UMP measures¸ it has been able to grease the financial markets with the infusion of large amount of liquidity. In this article, we have analyzed the impact of various UMP measures on bond yields, yield spread, stock returns and investor sentiment. We find that UMP shocks of one SD reduce 10-year government and corporate bond yields by 6.0 and 6.5 bps, respectively. These changes are also consistent with the changes in government bond yields of different maturities. We also find that a SD UMP shock results in an increase in Nifty50 stock returns by about 1.14 percentage points and increases investors sentiment (MMI) by 1.91 percentage points. In terms of the impact of expansionary UMP shocks on sectoral portfolio stock indices as well as on the stock portfolios based on market capitalization, we find that both NIFTY mid-cap and small-cap stock returns increase by 0.66 percentage points, followed by Nifty100, which increases by 0.42 percentage points. The results also indicate that the durable goods-producing sectors such as, automobile, information technology, metal, and real estate yield higher stock returns than the sectors producing non-durable goods such as, FMCG and media. Finally, in terms of the relative effectiveness of LTLOs and OTs in reducing bond yields and yield spread, respectively, out results show that TLTRO announcements have a more significant impact on bond yields than LTRO announcements. We also observe that OTs have a cumulative reduction of 107 bps in the yield spread.

Our empirical evidence has a wider global policy implication both for central banks as well as EME investors as well. The ability of the central bank to enhance liquidity in the financial market when it purchases long-term government bonds depends on the pass-through of the resulting reduction in government bond yields to other asset prices. The UMP measures have a considerable spillover effect on the other asset prices, that is, by purchasing a particular government bond, the central bank not only lowers the yield of that particular bond but also has an effect on the bond yields of different maturity too. For instance, Krishnamurthy and Vissing-Jorgensen (2011) found that mortgage-backed securities (MBS) purchases by Fed were crucial for lowering MBS yields as well as corporate credit risk and thus corporate bond yields. Our findings also have a direct implication for the EME central banks, who do not have enough space to conduct conventional monetary policy and even when they do not face zero bound lower interest rate, can also adopt UMP tools to stimulate aggregate demand. By employing UMP measures, central banks can affect aggregate demand and asset prices at low level of interest rates.

Our findings also provide a beneficial inference for the day-traders and investors looking for significant returns, since asset prices increase significantly following UMP announcements, investors can earn significant returns. Further, our results also suggest that investors stay invested in durable goods producing sectoral stocks. Besides, our findings have significant political economy implications as well. If a central bank can quickly tackle and achieve the desired objective using UMP tools during any crisis, this can result in the deferment of necessary structural reforms on the part of the elected government (Rogers et al., 2014).

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.