Abstract

World-wide, there is movement toward embracing environmental, social, and governance (ESG) issues in corporate conduct and performance. These developments have led to movement toward “reimagining capitalism,” and many firms have ridden the wave of investor enthusiasm for firms that prioritize ESG disclosures. The present study examines the role of International Financial Reporting Standards (IFRS) in India on ESG and overall ESG reporting. The Indian capital markets regulator, SEBI, had made integrated reporting compulsory for listed firms to disclose information about matters that substantively affect the organization’s ability to create value over the short, medium, and long term at a time. Motivated by this episode, we examine how accounting regulations in the form of IFRS could influence ESG disclosures in India. Based on the ESG scores of 104 non-financial firms in India from 2013 to 2021, the study finds a positive relationship between ESG reporting and IFRS introduction in India. The performance of firms (return on assets) and leverage had a negative impact on ESG disclosures.

1. Introduction

The present study is motivated by the events surrounding the Sterlite Copper Plant episode in Tamil Nadu, India, in 2018. The Sterlite plant located in Tuticorin, Tamil Nadu, India—a part of the Vedanta group, accounted for 40% of India’s copper output. Despite the company’s claims of meeting global emission standards and exercising environmental stewardship, evidence of local health issues and violations of pollution norms contradicted this (The Economist, 2018). Since its commencement in 1997, the plant had been found on various occasions to violate the pollution norms and had its permit rescinded by the local pollution regulators. In May 2018, the Sterlite plant was closed by the state government after deadly protests (13 protestors lost their life in police firing) that sought the plant’s closure for alleged pollution. 1 This episode highlights the need for transparency in disclosing non-financial risks and how they can affect a company’s “social license to operate.”

The obligation for companies to do what is desirable for the purposes and values of our society can be broadly divided into three dimensions: environmental (E), social (S), and corporate governance (G), which are collectively referred to as environmental, social and governance (ESG). The International Financial Reporting Standards (IFRS, 2020) emphasize the concept of “financial materiality,” which includes non-financial (ESG) risks. The Securities and Exchange Board of India (SEBI) has been an active proponent of non-financial reporting (initially for the top 100 companies), which has to be reported in their Business Responsibility Reports. In 2017, this requirement was extended to the top 500 listed companies. A new ESG reporting framework known as the Business Responsibility and Sustainability Report (BRSR) was introduced in 2021.

IFRS standards can facilitate companies’ efforts to increase public trust via enhanced transparency in sustainability reporting. This is particularly important in the context of India’s commitment to the Paris Agreement and the estimated $1 trillion need for sustainable finance by 2030 in developing nations like India. Hence, we explore how the convergence of Indian Accounting Standards (Ind AS) with IFRS influences ESG disclosure/scores in India.

The extant literature has examined the financial consequences of IFRS on accounting quality (Adhikari et al., 2021; Key & Kim, 2020), market reaction (Armstrong et al., 2010), portfolio performance (Alankara & Scholesa, 2022; Alareeni & Hamdan, 2020), information asymmetry (Abad et al., 2018), cost of capital (Persakis & Iatridis, 2017), and so on. The convergence of Ind AS with IFRS has offered Indian corporations an opportunity to address market, stakeholder, and regulatory pressures by enhancing ESG disclosure. In 2015, the convergence was announced to be effective in 2017, and the Securities Exchange and Board of India (SEBI) also mandated integrated reporting (IR) by listed firms with the goal of improving transparency in value creation over the short, medium, and long term. Thus, our study seeks to examine the influence of these regulatory changes on ESG disclosures (scores) in India.

Our study contributes to the existing academic literature in several meaningful ways. First, it provides empirical evidence of the impact of IFRS on ESG disclosure/scores in India, a context that has remained largely unexplored. Second, our research yields robust evidence of a positive relationship between IFRS adoption and ESG scores. This finding underscores the importance of accounting standards as regulatory tools to promote sustainability reporting and enhance corporate governance practices, thereby providing support for policymaking efforts aimed at establishing more uniform ESG reporting standards. Lastly, our findings lend support to the call for a universal standard for ESG corporate disclosures. This would not only enhance the comparability of ESG scores within India and across economies but also provide a benchmark for corporations striving to improve their sustainability performance. Therefore, our research underscores the need for harmonization in ESG reporting standards, offering crucial insights for regulators, policymakers, and standard-setters worldwide.

The remainder of the paper is organized as follows: Section 2 discusses the literature and proposed research questions. Section 3 presents our sample and research design. Section 4 reports our findings, and Section 5 concludes.

2. Literature Review and Hypothesis Development

The relevance of non-financial factors as determinants of a firm’s risk and returns is increasingly acknowledged. These factors, generally categorized as ESG scores, encompass various elements from sourcing, governance, and ownership. ESG risks can lead to revenue loss, decreased customer loyalty, litigation, regulatory sanctions, and share price decline, among others (Champagne et al., 2021). Conversely, higher ESG scores have been associated with lower capital costs, reduced tail risks, and increased cash flow to creditors (Gregory, 2022a). Effective identification and management of ESG issues can therefore enhance a firm’s sustainability by mitigating risks and capitalizing on new opportunities (SASB, 2017). It is also posited that firms disclose their ESG credentials as a self-protective measure against potential ESG risks. Yadav and Bhama (2023) found little and negative associations between sustainability and stock returns during and after COVID-19 crisis.

In recent years, the commitment of US corporations to achieve net zero emissions by 2050 has increased, not only within high-polluting industries but also in consumer-facing sectors. Concurrently, ESG considerations have started to permeate investment and credit rating strategies. For instance, BlackRock, the world’s largest asset manager, has made significant investments in the US energy sector, encompassing natural gas, renewables, and decarbonization technologies. Furthermore, several credit rating agencies have incorporated ESG factors into their methodologies and expressed commitment to responsible investment principles.

However, ESG considerations have also been criticized as a smokescreen for political agendas and perceived as harmful to fossil fuel producers. For example, Louisiana withdrew a substantial sum from BlackRock funds in response to the asset manager’s emphasis on ESG investing, arguing that it conflicted with the state’s economic interests.

The breadth of ESG disclosure is expansive, covering sustainability-related aspects typically not included in financial reporting. The implications of such disclosures for social welfare are an ongoing area of research. Current evidence suggests that ESG disclosures can improve the quality of corporate information, enhance the visibility of financial and non-financial information, signal compliance with societal norms, and contribute toward a more sustainable and inclusive economy (Fatemi et al., 2018; Raimo et al., 2021). Moreover, mandatory ESG reporting can refine a firm’s financial information environment and lead to more accurate and less dispersed analysts’ earnings forecasts (Krueger et al., 2021).

Despite accusations of “greenwashing” and backlash, ESG investing has been adopted by global investors, particularly institutional ones, as a critical dimension for capital allocation. The increasing pressure on firms to incorporate social consciousness and environmental respon-sibility into their operations has spurred academic research and entre-preneurial initiatives promoting ESG investments. Market leaders like BlackRock, State Street Corp, and Vanguard Group posit that environmentally proactive firms will reap higher profits over time. This assertion is supported by the significant increase in ESG investments, soaring from $5 billion in 2018 to $70 billion in 2021 (Pérez et al., 2022), and the reported superior risk-adjusted returns of ESG investments (Pástor et al., 2022).

The Friedman (1970) argument for firms solely prioritizing profit maximization ignited debates that still reverberate today. This “shareholder expense” perspective is contrasted with the “stakeholder value maximization” view (Freeman, 1984), advocating firms’ responsibility to society beyond their equity holders’ wealth maximization. The stakeholder capitalism model prioritizes both profits and purpose, aiming to serve employees, suppliers, government, shareholders, community, and customers. The agency problem perspective and stakeholder theory offer differing views on ESG activities, either as a means for managers to improve reputation at shareholders’ expense or as value-enhancing engagements (Benabou & Tirole, 2010; Edmans, 2011; Servaes & Tamayo, 2013). Concerns have also been raised about stakeholder protection being manipulated into a strategy for incumbent CEOs to entrench their position (Cespa & Cestone, 2007).

Previous research on ESG and IFRS has explored various aspects such as earnings quality, value relevance, financial statement impact, firm value, green stock returns, managerial characteristics, ownership characteristics, cost of capital, earnings management, and socially responsible investment. Raut and Kumar (2023) found that both economic and environmental concerns are significant predictors of a positive attitude toward socially responsible investment. Findings indicate that strong ESG preferences might lead to underreaction to negative earnings surprises and a willingness to accept lower financial performance. Firms with positive ESG ratings tend to show less negative abnormal returns in the case of a profit warning (Dayanandan et al., 2018). However, the majority of such studies focus on developed countries, leaving emerging markets relatively unexplored.

In emerging economies like India, firms have begun transitioning from short-term profit maximization to long-term sustainability involving ESG goals (Chelawat & Trivedi, 2016). The Indian GAAP’s convergence with IFRS, known as Ind AS, effective from April 1, 2016, has transformed the financial reporting landscape in India, encouraging more ESG disclosures (Weerathunga et al., 2020). Stakeholders advocate for “double materiality,” measuring the impact of firms internally (economic value creation) and externally (communities and the environment). The release of industry-based standards by the Sustainability Accounting Standards Board (SASB) in 2017 has further propelled the ESG reporting environment.

IFRS/Ind AS has emphasized more disclosures, including sustainability-related ones. Key changes include emphasis on substance over form, fair value, and consolidation. The substance over form concept encourages firms to focus on the economic reality of business transactions when choosing accounting policies. Fair value assessment includes ESG-related parameters, potentially affecting the value of assets and liabilities. From the above discussion and extant literature, it is hypothesized that

H1: There is a positive relationship between IFRS/Ind AS adoption and ESG disclosures.

Existing literature suggests a positive correlation between firm size and ESG scores, largely due to resource availability within larger firms facilitating better ESG data collection and reporting (Drempetic et al., 2020). Other potential factors include the capacity of large firms to exploit economies of scale in ESG efforts and their ability to undertake stakeholder value-enhancing activities. However, there’s also an opposing viewpoint highlighting larger firms as significant contributors to environmental damage (Gregory, 2022b).

Studies show that the adoption of IFRS has heightened the value relevance for high-value firms (Saji, 2021). In the context of India, Ray and Goel (2022) establish a positive relationship between ESG disclosure and the annual average share price of listed firms. The phased implementation of IFRS in India from April 1, 2016, was largely determined by firm size, initially targeting firms with a net worth of 500 crore ₹ or more, followed by listed firms with a net worth of less than 500 crore ₹, and eventually extending to unlisted firms with a net worth of 250 crore ₹.

Significant legislation has been enacted to promote sustainability in India, including the corporate social responsibility (CSR) provision in the Companies Act 2013 and the Business Responsibility Reporting norms by the SEBI. These regulations mandate 2% of the average net profits of the preceding three financial years toward CSR and the release of a BRSR by the Top 1,000 listed entities, based on market capitalization, for ESG disclosure in financial year 2022–2023. Thus, ESG-related disclosures were initially prescribed for larger firms, and ESG reporting has been made compulsory following the implementation of these policies. Therefore, drawing upon the above literature, the following hypothesis is proposed:

H2: There is a positive relationship between firm size and ESG disclosures.

3. Sample and Methodology

To measure the extent of companies ESG disclosures, we use a third-party (rating agency’s) ESG score. Data on ESG scores are based on scores provided by Thomson Reuters’s Refinitiv (formerly ASSET4) database. The scores are based on publicly-reported data and measure a firm’s ESG performance. The overall ESG scores, as well as the sub-scores (ESG), are percentile rank scores and are scaled to range between 0 (the minimum score) and 100 (the maximum score). The environment sub-score thereby received a weight of 34% in the total ESG score, the social sub-score of 35.5%, and the governance sub-score of 30.5%. REFINITIV has the most individual indicators with 282, followed by Sustainalytics with 163 (Berg, 2022). ESG scores from the REFINITIV database are widely used, both in academic research and in the investment management industry. Moreover, REFINITIV ESG data are used by major asset managers, such as BlackRock, to manage ESG investment risks.

We started our search for ESG data based on firms included in the NSE-500. We were able to collect ESG data for 115 firms for the period 2013–2021. After excluding banking firms, our sample contains 104 firms. The market capitalization of these 104 firms accounts for 85% of the market capitalization of the NSE 500 firms. We downloaded the data for 104 Indian firms from the REFINITIV ESG database provided by Thomson Reuters on September 1, 2022. After merging the data with S&P Capital IQ, we obtained 936 firm-year observations with an ESG score. The financial and stock price data are also sourced from S&P Capital IQ. The IFRS dummy assumes a value of one for firms that adopted IFRS. See Table A1 for a detailed description of the variables.

We estimate the following regression model:

where IFRS refers to dummy variable capturing the adoption of the IFRS/Ind AS, SIZE refers to the size of the firm, and Xit refer to the control variables. Equation (1) is estimated separately for the environment (E), social (S), governance (G), and overall (ESG) scores. Equation (1) is estimated using the fixed-effects model, which accounts for the individual heterogeneity of firms. Based on the hypothesis (1), we expect a positive relationship between IFRS and the overall ESG score. Similarly, we expect a positive relationship between SIZE and ESG scores. We also provide estimates based on OLS, generalized method of moments (GMM), and system GMM to check the robustness of the estimates. The GMM empirical framework is presented in two varieties: differenced-GMM from Arellano and Bond (1991) and system-GMM estimator from Blundell and Bond (1998, 2000). The differenced GMM estimator derives the coefficients from moment restrictions on the co-variances between the regressors and the error term. The differenced GMM controls for endogeneity. The system GMM estimator uses, in addition to lagged levels, also lagged first differences as instruments for equations in levels. By adding the original equation in levels, Blundell and Bond (1998, 2000) argued that the system GMM estimator performs well as predicators for the endogenous variables in the model even when the series are very persistent. They found substantial improvements in efficiency and significant reduction in finite sample bias as compared with the difference GMM estimator.

The validity of the instruments is evaluated using Hansen’s (1982) J-statistics. The J-statistic is a test of overidentifying restrictions that checks the instruments’ validity.

Based on the extant literature, we include a number of control variables in the panel regression model, such as performance (return on assets [ROA]), leverage, market risk, news, loss, MVBV, Big 4, audit fee, and asset turnover ratio (ATR). For the control variables, we expect a negative relationship between ESG and its components, as argued from the agency perspective (Bènabou & Tirole, 2010). We consider ROA as a proxy for firms’ financial performance. Since ESG investing focuses on firms’ long-term and sustainable financial returns rather than short-term speculation in the stock market, ROA is a more appropriate proxy for performance than any other measures. Alareeni and Hamdan (2020) investigate whether there are relationships among ESG and firm performance and show that ESG disclosures positively affect ROA. Among the ESG sub-components separately, they show that environment and social are negatively associated with ROA. Rahman et al. (2023) find that ESG and all of its separate dimensions—environmental, social, and governance—exert a significant positive impact on ROA. Thus, existing literature documents a mixed relationship between ROA and ESG. Similarly, leverage is also expected to negatively influence the ESG score (Broadstock et al., 2021).

The market risk could have positive and negative impacts on ESG and the overall ESG score. Lioui (2018) observes that the estimated market risk associated with the ESG factor is negative, which implies that more highly rated ESG securities have lower expected returns. On the other hand, higher market risk could also lead to more ESG disclosure. The news variable (NEWS) is expected to have a negative impact on ESG score. The MVBV variable is considered to control long-term financial performance and is expected to positively or negatively influence the ESG score (Fatemi et al., 2018). Few of the studies (Alareeni & Hamdan, 2020; Rahman et al., 2023) document a positive relationship between MVBV and ESG. It is observed that the accounting numbers of Big 4 clients contain more value-relevant financial measures and assurances to shareholders than those of non-Big 4 auditors (Bakarich et al., 2023; Lin et al., 2009). Similarly, Burke et al. (2019) find that negative ESG-related media coverage is associated with a higher likelihood of auditor resignation and increased audit fees. Thus, we consider audit interface variables—Big 4 and audit fee—which proxies audit quality, to have a positive impact on the ESG score. The ATR is expected to have a negative impact on the ESG score.

4. Empirical Results

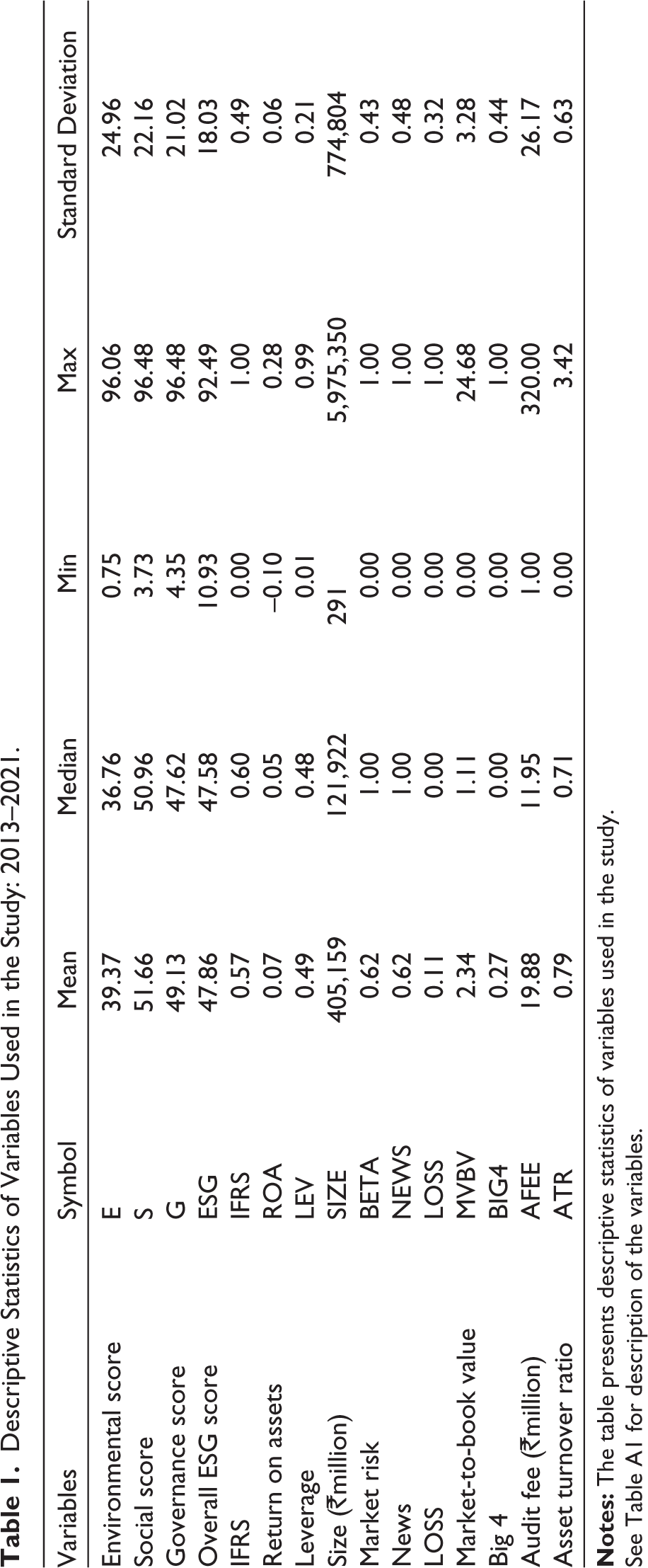

Table 1 provides descriptive statistics of the data used in the study (2013–2021). Among the ESG components, the average environment score (E) of Indian firms in the sample was relatively low around 39.37, with the median at 36.76. There was large variation in the E score, with the minimum value at 0.75 and a maximum value of 96.06 show a relatively high standard deviation as high as 24.96. The average social score (S) among the firms in the sample was also low at 51.66, with the median slightly low at 50.96. The minimum and maximum values in the sample were 3.73 and 96.48, respectively, with a high standard deviation of 22.16. The average governance score (G) was also lower at 49.13 (the median at 47.62) and had a similarly large variation in its score in the sample (minimum of 4.35 and a maximum of 96.48). The total ESG score among sample firms was consequently lower at 47.86, with a median close to 47.58, and they are only in the second quartile of the distribution of ESG scores provided by REFINITIV. Overall, the ESG scores and their components were low in India and showed wide variation, reflecting the low performance of Indian firms in this area.

Descriptive Statistics of Variables Used in the Study: 2013–2021.

See Table A1 for description of the variables.

The average IFRS proxy dummy (firms that have adopted IFRS since 2017) was 0.57 or 57% with the median slightly higher at 0.60. The financial parameters (ROA, leverage, size, and so on) also showed larger variation in the sample. The average ROA was 0.07 or 7% with large variation in performance (low as –0.10 and high as 0.28). The average MVBV of equity was higher at 2.34 (median at 1.11), indicating firms on average experienced 2.34 times the market value of equity compared with its book value. The ATR, which basically shows how the firm was able to translate their total assets into sales, had an average value of 0.79, which means that for every one Rupee of total assets the firm created, it was able to translate into sales 0.79 paisa (median slightly lower at 0.71). Thus, going by ROA, ATR, and market value of equity to book value of equity, the firms in the sample had recorded better performance.

However, the leverage of firms in the sample was around 0.49 (median close at 0.48), which is relatively high as compared with US firms (Kanoujiya et al., 2023). The variation in leverage is also very high (0.01 minimum and maximum 0.99). The average size of the firm (in ₹million) was 405,159, with the median substantially low (121,922), indicating the presence of a large number of firms below the average size. The average market risk of the firms (as proxied by beta) in the sample was 0.62, with the median market risk around 1.00, indicating the stock price movement closer to the market index. The NEWS variable, captured by a binary value of 1, if the net income of the firm was greater than the previous year, showed an average value of 0.62 (median value 1.0), indicating majority of the firms in the sample had net income exceeding the previous year. The average value of LOSS (indicating a net income loss) was only 0.11. The quality of the audit of financials is reflected in the (a) number of firms audited by the Big 4 audit firms (Deloitte, PricewaterhouseCoopers, Ernst & Young, and KPMG) and (b) audit fee. If firms are audited by Big 4 audit firms, earnings quality is considered superior. The higher the audit fee, the better the audit quality. On average, only 27% of the firms in the sample are audited by the Big 4. The average audit fee comes to ₹19.88 million, with the median low at ₹11.95 million. In sum, the average ESG scores (independently and together) were relatively modest in Indian firms. But their financial performance (ROA, MVBV, and ATR) was relatively better. The leverage of firms in the sample was relatively high. The audit quality reflected in the proportion of firms audited by the Big 4 was relatively low.

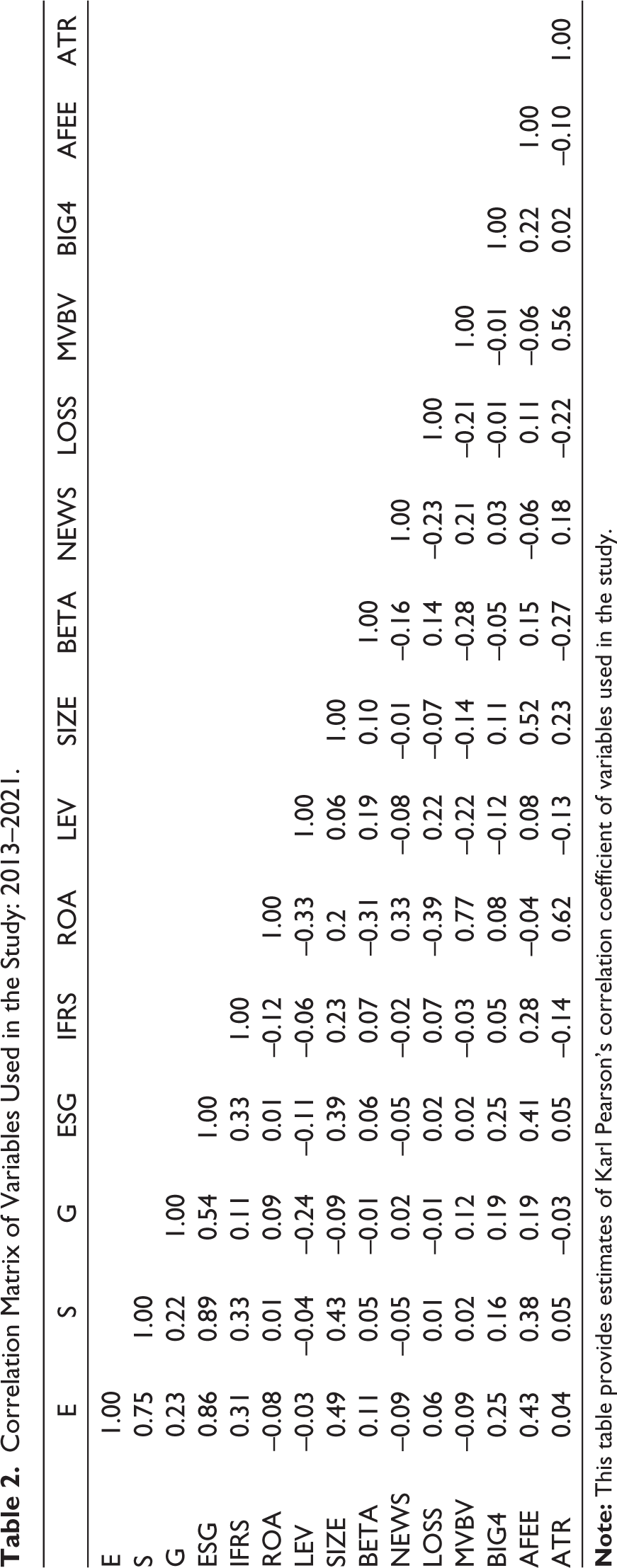

Table 2 displays the correlation coefficients of the variables implemented in this study. There is a high correlation (0.75) between environmental score (E) and social score (S). On the other hand, social score (S) has a low correlation (0.23) with governance score (G). The correlation matrix also reveals a relatively substantial correlation between the adoption of IFRS and the scores of the environmental, social, governance, and overall ESG categories, validating our proposed hypothesis. Furthermore, the firm size (revenue) displayed moderate correlations ranging from 0.39 to 0.49 with the environmental, social, and overall ESG scores. Interestingly, the governance score exhibited an inverse correlation with the firm size. A significant positive correlation (0.77) was observed between the ROA and the MVBV, indicating an association between the sample firms’ performance and their respective market valuations. Additionally, a correlation of 0.52 was established between firm size (revenue) and audit fees. Lastly, the ATR, a measure of management efficiency, demonstrated a high positive correlation (0.62) with the firms’ performance, further enhancing our understanding of the relationships between these financial metrics.

Correlation Matrix of Variables Used in the Study: 2013–2021.

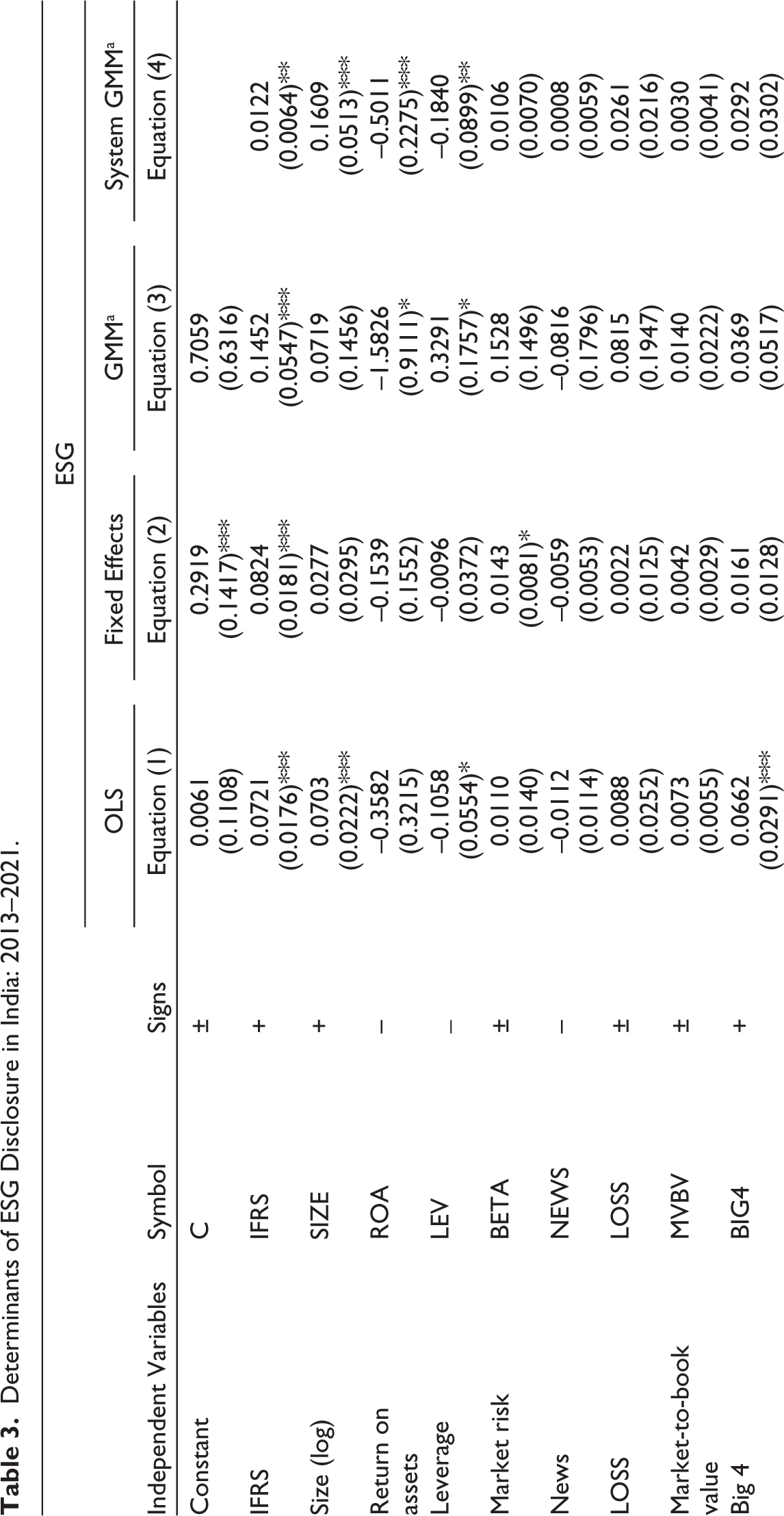

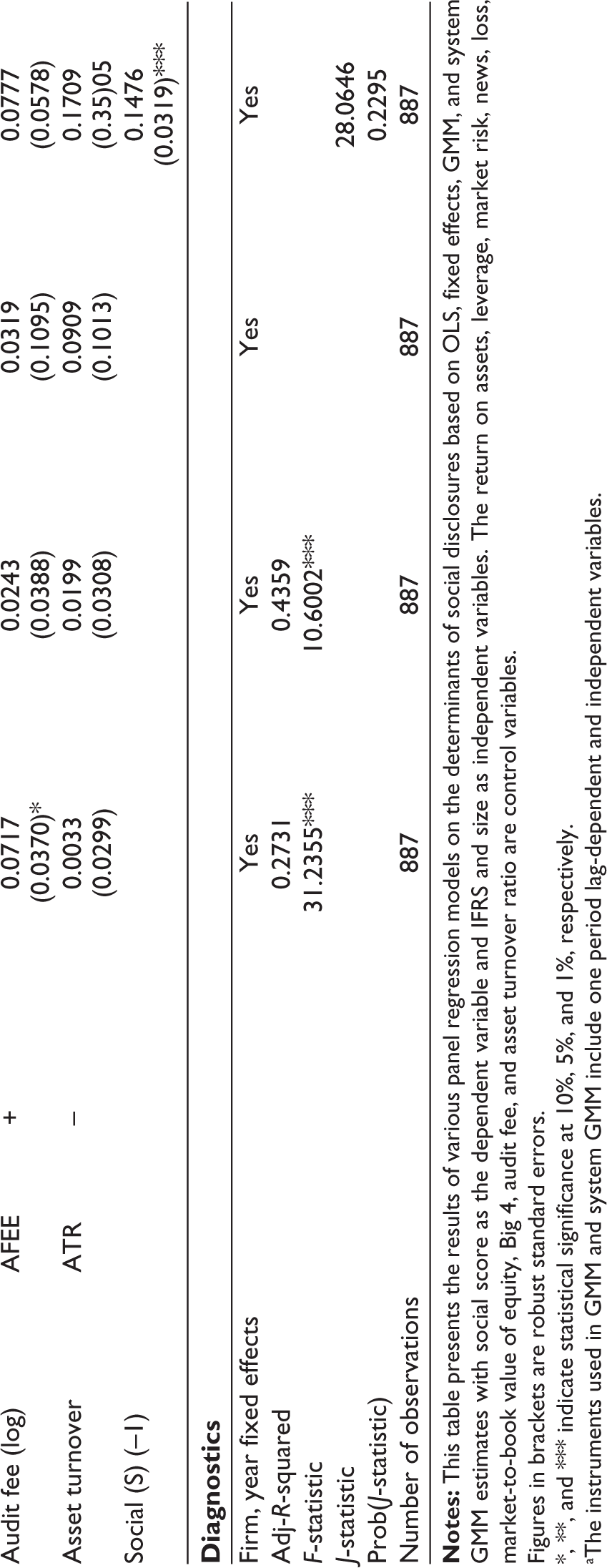

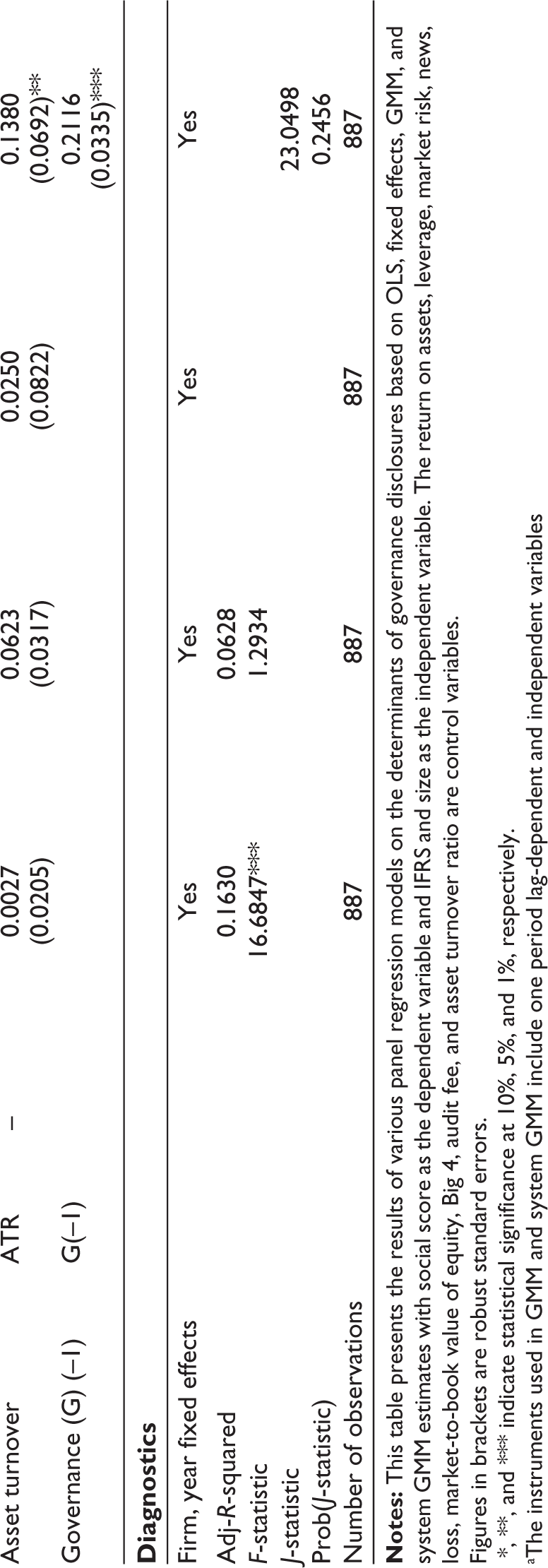

Table 3 presents the results of the various estimation procedures—OLS, fixed-effects, GMM, and system GMM estimation procedures for Equation (1) for ESG. The choice between the fixed-effects versus random-effects model estimation procedure was made on the basis of the Hausman test. The test rendered a significant outcome at the 7% level, suggesting that the fixed-effects model was the more suitable choice for our study. Regarding the ESG equation (equation (1) in Table 3), the IFRS variable exerted a positive and statistically significant influence on the overall ESG score at the 1% level. Similar results are observed for environmental, social and governance scores (Tables 4–6), thereby validating hypothesis 1 that the adoption of IFRS had a positive bearing on ESG scores in India. From an environmental perspective, the positive relationship with IFRS suggests that the adoption of these global accounting standards leads firms to be more conscious of their environmental footprint and disclosure. Given that IFRS has a more extensive focus on fair value and requires more extensive disclosures than local accounting standards, it leads to better reporting of environmental risks and impacts. As for social and governance scores, the positive impact of IFRS adoption might be attributed to enhanced transparency and stakeholder engagement. These standards require firms to provide more comprehensive and reliable information, fostering improved corporate governance and more effective interaction with stakeholders, including the workforce, customers, and the community. Better disclosure practices, such as those required by IFRS, can reduce the information asymmetry between management and stakeholders, leading to improved corporate governance. Additionally, increased transparency might enable firms to better manage their social responsibilities, leading to higher social scores.

Determinants of ESG Disclosure in India: 2013–2021.

The return on assets, leverage, market risk, news, loss, market-to-book value of equity, Big 4, audit fee, and asset turnover ratio are control variables.

Figures in brackets are robust standard errors.

*, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

aThe instruments used in GMM and system GMM include one period lag-dependent and independent variables.

Determinants of Environmental Disclosure in India: 2013–2021.

Figures in brackets are robust standard errors.

*, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

aThe instruments used in GMM and system GMM include one period lag-dependent and independent variables.

Determinants of Social Disclosure in India: 2013–2021.

Figures in brackets are robust standard errors.

*, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

aThe instruments used in GMM and system GMM include one period lag-dependent and independent variables.

Determinants of Governance Disclosure in India: 2013–2021.

Figures in brackets are robust standard errors.

*, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

aThe instruments used in GMM and system GMM include one period lag-dependent and independent variables

Our research found that the size of a firm, as gauged by its revenue, has a significant and positive influence on governance scores, affirming the second hypothesis specifically in the context of governance (Table 6). However, this relation does not hold for the environmental scores, where the influence of firm size surfaced as statistically insignificant. This finding contradicts the prevalent assumption that larger firms tend to demonstrate higher levels of sustainability than smaller entities.

Among the other factors controlled in this study, the ROA of a firm consistently had a negative impact on ESG, E, S, and G but was not statistically significant. Similarly, leverage also exhibited a negative relationship with ESG metrics, but was not statistically significant. In terms of risk exposure in the market, our analysis revealed a positive correlation across the scores but was not statistically significant. Similarly, other control variables like NEWS, LOSS, MVBV, and audit quality (Big 4 audit, audit fees) were also not statistically significant.

In terms of model fitness, the R-squared values ranged from 0.30 to 0.41, indicating that a significant portion of the variation in the dependent variable can be explained by our model. Furthermore, the F-statistic, which evaluates the combined significance of independent and control variables in the equation, dismissed the null hypothesis that all regression coefficients are equal to zero, thereby confirming the statistical validity of the model.

The possibility of endogeneity, a situation in which an explanatory variable is correlated with the error term in a regression model, could potentially emerge if the decision to adopt IFRS was somehow impacted by a firm’s ESG scores, or vice versa. However, this prospect may not pertain to our study. The adoption of IFRS was not a decision made by individual firms based on their unique situations or ESG scores. Rather, it was a regulatory directive enforced by the market regulator, applicable to all eligible firms, irrespective of their ESG scores. However, to test the potential endogeneity problem, we also performed GMM and system GMM using the 1-year lagged values of dependent and independent variables, which are presented in Tables 3–6. The validity of the instruments was tested using Hansen’s (1982) J-statistics, under which the null hypothesis is that the instrument used are valid. The prob(J-statistic) for GMM and system GMM do not reject the null hypothesis that instruments used in the estimates provided in Tables 3–6 are valid.

Given this context, the phenomenon of IFRS adoption transpires ahead of the assessment of ESG scores. Upon adopting IFRS, firms start reporting their operations pursuant to these standards. Consequently, ESG scores are ascertained based on these reports. Thus, ESG scores, being a resultant outcome of IFRS adoption, cannot retroactively influence the decision to embrace IFRS.

5. Conclusion

Our research examines the implications of the adoption of the IFRS on ESG scores within the Indian context. The advent of Ind AS, a convergence with IFRS in 2017, mandated these global standards in the country. Additionally, SEBI, the regulatory authority for the Indian capital market, necessitated IR for listed entities, which involves the disclosure of information regarding factors that materially impact the organization’s capacity for value creation in the short, medium, and long term.

Prompted by these regulatory alterations, our analysis delves into the influence of such normative shifts, particularly the implementation of accounting standards (Ind AS/IFRS), on ESG scores in India. Drawing upon the ESG ratings of 104 non-financial firms in India for the period from 2013 to 2021, the study delineates a positive association between the adoption of Ind AS/IFRS and ESG scores within the country. These findings underscore the necessity for a broader consensus on the formulation of uniform standards for ESG corporate disclosures. Such consensus would foster the comparability of ESG scores, both within India and across diverse economies globally, thereby enhancing the transparency, reliability, and relevance of these critical non-financial metrics.

The study brings into focus the role of accounting standards—IFRS—in ESG disclosures in India and is the first attempt in this direction. The present study is based on a regime when ESG reporting was made voluntary by the regulator. With the mandate of BRSR reporting by the top 1,000 companies from 2022 to 2023 onward, future research may focus on examining the validity of these results. ESG disclosures, especially in the area of environmental area, depend on scope 1 (direct emissions), scope 2 (indirect emissions), and scope 3 (emissions emanating from supply chain). A detailed analysis of the impacts of IFRS on these emissions (scopes 1–3) could be an agenda for future research.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.