Abstract

This study examines the effects of share repurchase announcements on Taiwanese firms after various financial practices and decisions from 2000 to 2020. First, we discuss whether there is a significant abnormal return on the price around share repurchase announcement. Furthermore, we explore whether firms take advantage of buyback announcements to signal the outsiders that the company’s stock price is undervalued. Second, we discuss whether the repurchase announcements have abnormal returns after financing or dividend distribution decisions as companies implement these decisions in response to future operating plans. Further, we explore whether there is a conflict between these funding operation policies and the repurchase announcement.

According to our results, there is an opposing effect between seasoned equity offering and share repurchase announcements. We found the effect of the announcement of share repurchase after a cash dividend is better than a stock dividend. The results also show that the effect of a share repurchase announcement after the issuance of convertible bonds is better than an ordinary corporate bond issue, especially the firms with a low market-to-book ratio. It means that convertible bonds can reduce liabilities if the investors convert the debt into equity and improve the company’s capital structure.

1. Introduction

In the past 30 years, open-market share repurchase has become a critical financial policy of firms, as it can be used to achieve financial purposes, such as signaling information to the market and adjusting the capital structure (Andriosopoulos & Hoque, 2013; Dittmar, 2000; Grullon & Michaely, 2004; Ikenberry et al., 1995; Oded, 2005; Vermaelen, 1981). The company may engage in stock repurchase transactions for various reasons, including influencing stock prices, profit distribution, resisting takeovers, and investment opportunities. Previous studies generally find a positive market reaction to the announcement of the share repurchases. Dittmar (2000) investigated the motivation for firms to buy back stocks. He found that firms took advantage of potential undervaluation, distributed excess capital, and altered leverage ratios through the decision. According to Brav et al. (2005), share repurchases are more significant forms of earnings payout than they were in the past. Share repurchase programs by listed companies have grown in importance as a means of reducing systematic risk, particularly since the global financial crisis in 2008.

This study aims to understand if the short-term effects of share repurchase announcements are impacted by the firms’ prior financial events, including seasoned equity offering (SEO), bond issuance, and dividend distributions. In the extant literature, firms announce a share repurchase program based on several critical motivations. The first motivation is based on the theory of signaling mechanisms, indicating that firms would signal a better prospect of the firm by announcing share repurchase (Chan et al., 2004; Grullon & Michaely, 2004; Ikenberry et al., 1995; Louis & White, 2007; Vermaelen, 1981). Firms expect to reflect future operational performance in market price by announcing repurchase under a signaling mechanism. Theoretically, the firm would not be undervalued or overvalued in an efficient market since all the information of the firm has been reflected in the market price. However, mispricing may exist due to incomplete and asymmetric information. If the firm’s stock price is undervalued, the management would implement a share repurchase program to attract market attention and adjust the firm’s stock price to its intrinsic value. Thus, an open-market share repurchase announcement is viewed as a mechanism to raise the stock prices to market investors (Chan et al., 2010; Siems & De Cesari, 2012).

The second motivation is attributed to the agency theory (Grullon & Michaely, 2004; Jensen, 1986; Nohel & Tarhan, 1998; Saxena & Sahoo, 2023), indicating that firms would like to distribute excess free cash flow to shareholders by buying back the shares from the market. The announcement of a repurchase also implies the firms do not have better investment opportunities. Share repurchase and cash dividend distribution are two ways to distribute excess capital to stockholders. Specifically, share repurchase can serve as a self-imposed discipline mechanism for management and reduce the firms’ agency costs (Andriosopoulos & Hoque, 2013). Grullon and Michaely (2004) suggest that the repurchasing firms significantly decrease their capital expenditures and the market positively reacts to repurchase announcements in the following years. Consistent with the above findings, generally, share repurchases decrease the likelihood of over-investment by the management.

The third motivation is the need for capital structure adjustment (Asquith & Mullins, 1986; Bonaimé et al., 2014). Capital structure plays a critical role in firm valuation, considering taxation or not (Bradley et al., 1984; DeAngelo & Masulis, 1980; Masulis, 1983). Hovakimian et al. (2001) confirm that more profitable firms are more likely to issue debt rather than equity and more likely to buyback shares rather than retire debt. This implies that the firms would issue corporate bonds to adjust the firm’s capital structure. To maximize shareholders’ wealth and firm value, Titman and Tsyplakov (2007) proposed a continuous time-varying model, demonstrating that the firm would dynamically adjust its capital structure to increase firm value. However, Chan et al. (2004) found very limited evidence that firms would use share repurchases to adjust their capital structure. The hypothesis of capital structure adjustment is conditional on significant actual repurchase activity.

The announcement of a share repurchase is regarded as an independent event in the literature. Firms procure funds in a variety of ways to support their potential investments. It seems absurd that investors would positively support the repurchase announcement without considering the firm’s prior financial practices and decisions, especially institutional investors. Chang et al. (2010) imply this viewpoint in their conclusion that stock markets respond more positively to the announcements made by firms with better previous records. A similar conclusion could be found in Zhang (2005), indicating that the firms’ increased buyback activity would generate more positive abnormal returns (ARs).

In this study, the general market reaction to share repurchase announcements in Taiwan is examined, especially after various financial events such as SEO, straight and convertible bond issuance, and dividend distributions. We obtain some critical findings that have not been discovered in previous studies. Consistent with previous studies, share price declines prior to a repurchase announcement, and the market reaction to the announcement is generally positive supporting the signaling hypothesis. In addition, announcements from firms with lower market-to-book ratio (MBR) receive stronger market reactions.

We then categorize the repurchase announcements based on the different financial practices made in the last year. The firms’ share repurchase announcements after a prior SEO are not significant on average for firms with both a high and low MBR, except for five-day announcement performance. Similar results are found in the announcements after a prior straight bond issuance. Specifically, firms with a prior straight bond issuance and a lower MBR generally have stronger market reactions than those with a higher MBR. Surprisingly, the market reaction to the repurchase announcement with a prior convertible bond issuance is not as significant as the one with a prior straight bond issuance. In addition, the market reactions to share repurchase announcements with prior cash and stock dividend distributions are significantly positive, and the ones with a prior cash dividend distribution generate stronger reactions. We also examine the relationship between repurchase announcement effects and firm characteristics. Generally, MBR has a significantly negative effect on repurchase announcements. Debt ratio and institutional investors’ shareholding are positively associated with the firms’ announcement effects, which could be seen as a monitoring effect (Kang et al., 2011; Slovin et al., 1990).

The remainder of the paper is organized as follows. Section 2 introduces the data used in this study and the repurchase regulation in Taiwan. Section 3 describes the methodology and research procedure. Section 4 presents the empirical results and the financial implications. Section 5 concludes the paper.

2. Data

After experiencing the Asian financial crisis in 1997, the Taiwanese government offered more mechanisms to listed firms to protect investors. For example, open-market repurchase is one of the mechanisms used to protect the stock price. Listed firms in Taiwan have been allowed to buy back their shares from the market since August 2000 based on the following three reasons: transferring shares to employees, equity conversion in coordination with the issuance of securities, and maintaining the firm’s credit. The details of the share repurchase program, including the target volume to be repurchased, the target price range, and the repurchase period, need to be discussed and authorized at the board meeting. The repurchase program will then be announced in newspapers and reported on TWSE’s (Taiwan Stock Exchange) official website within two days. The period for repurchase is two months from the date the firm announced, and up to 10% of the outstanding shares can be repurchased. Until the end of 2020, 60.47% of the listed firms on the TWSE and the Taipei Exchange (TPEx) have announced, at least once, a share repurchase program.

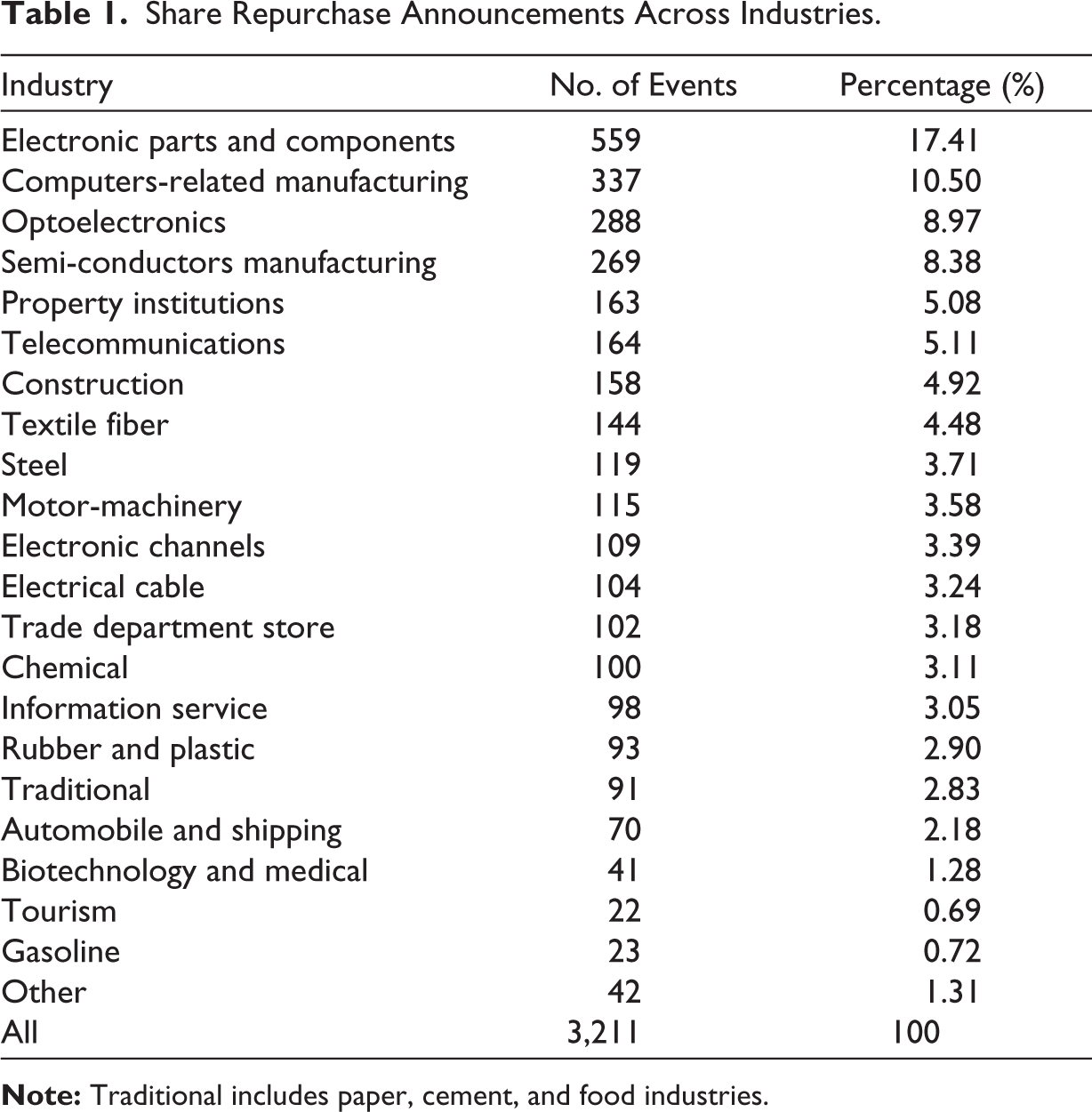

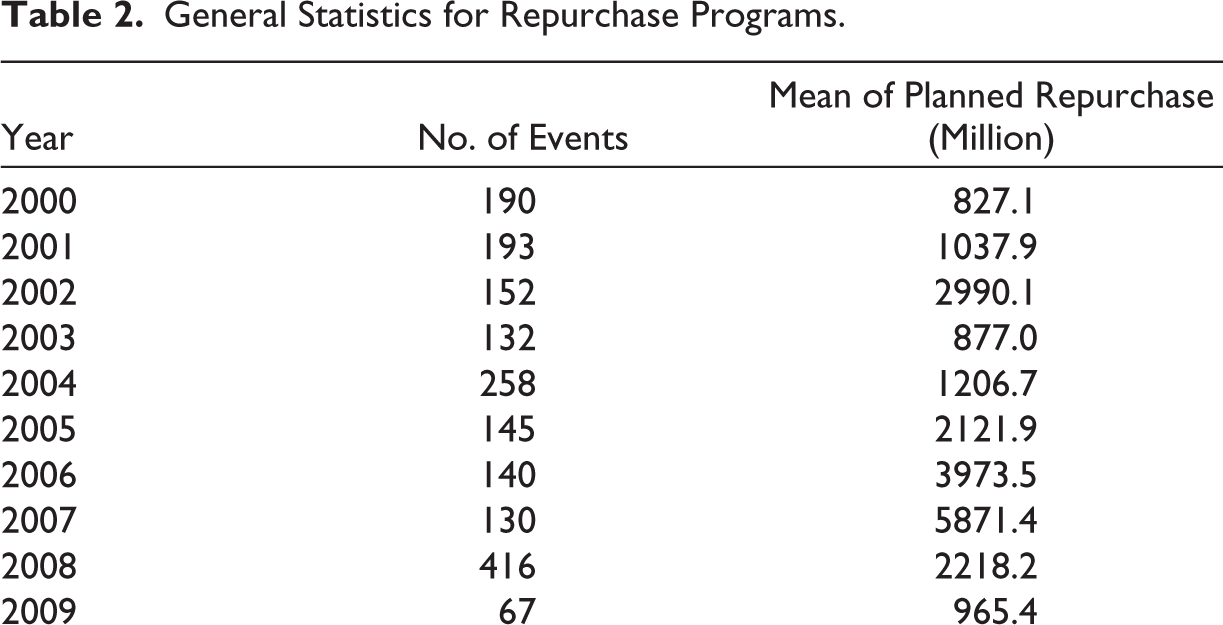

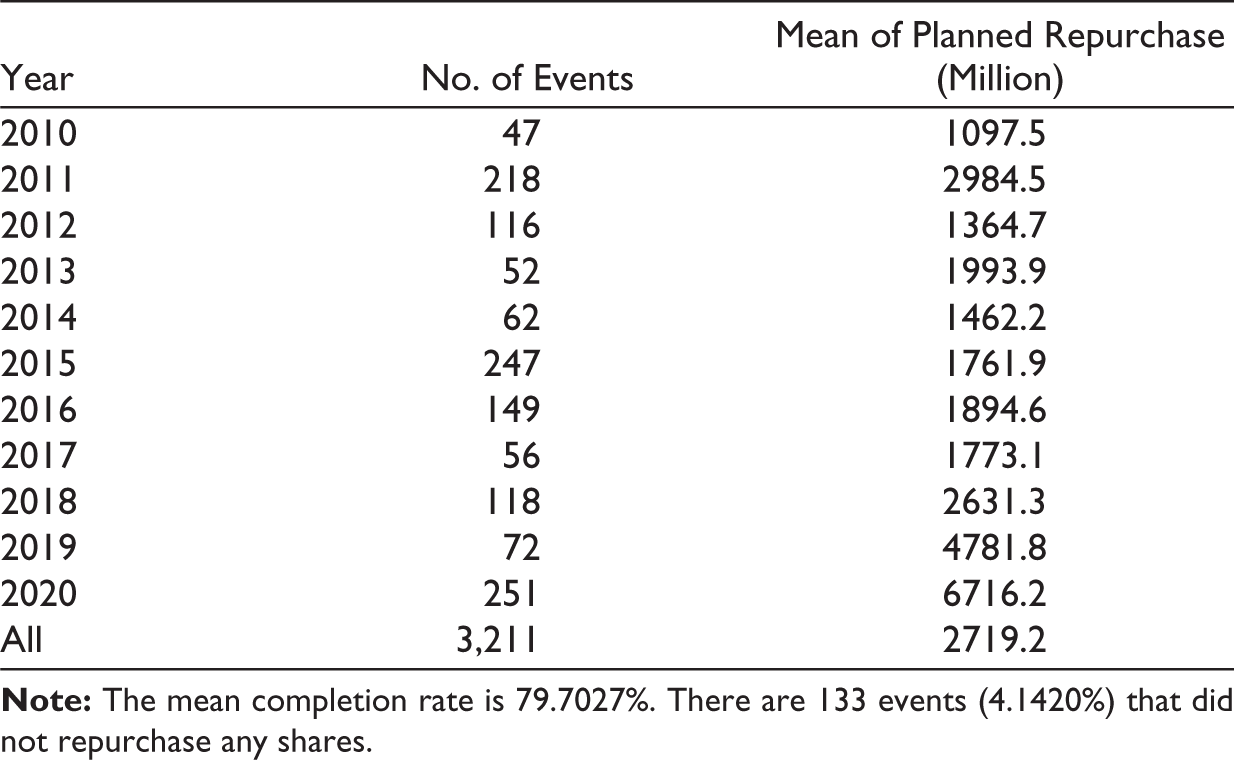

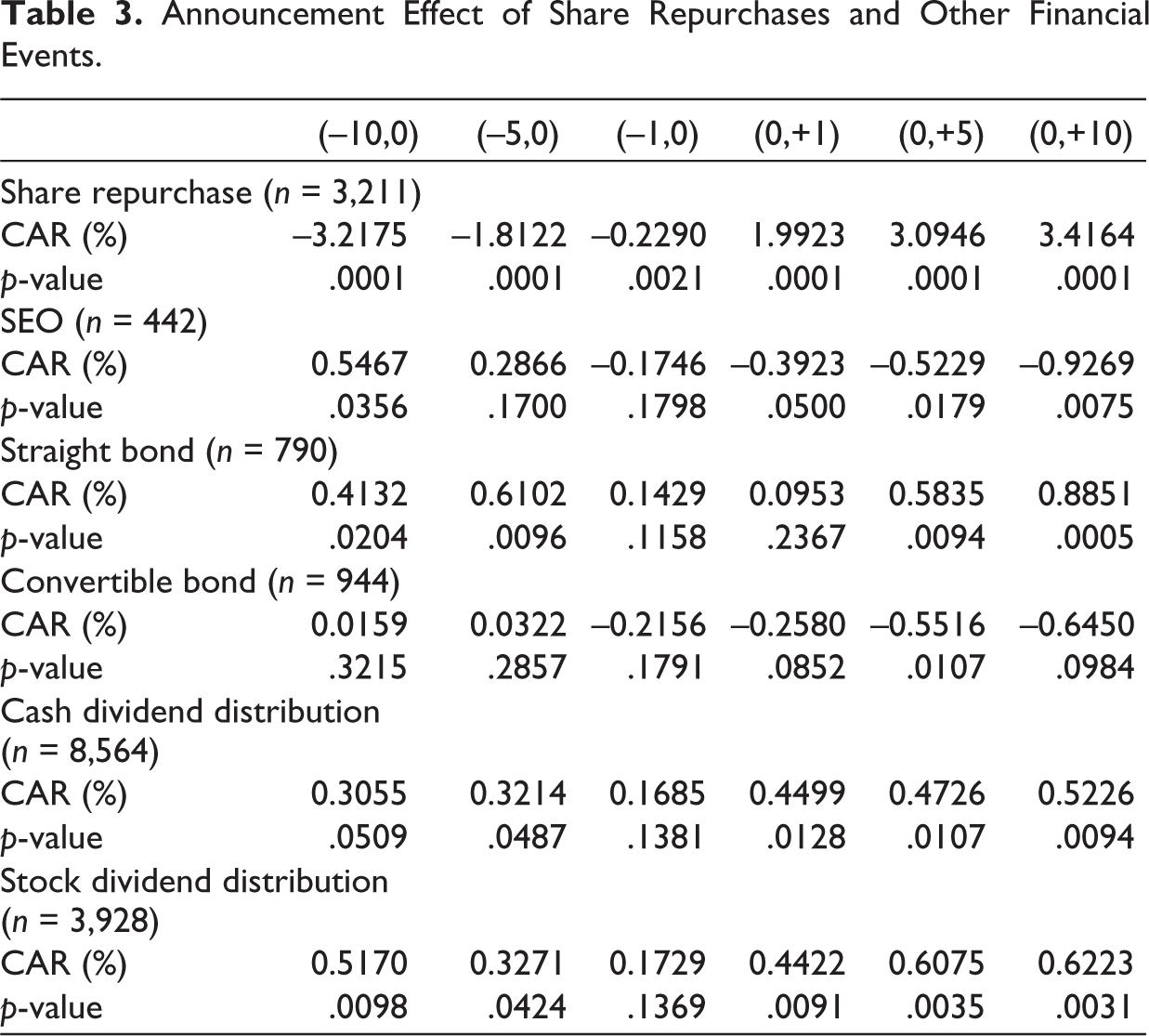

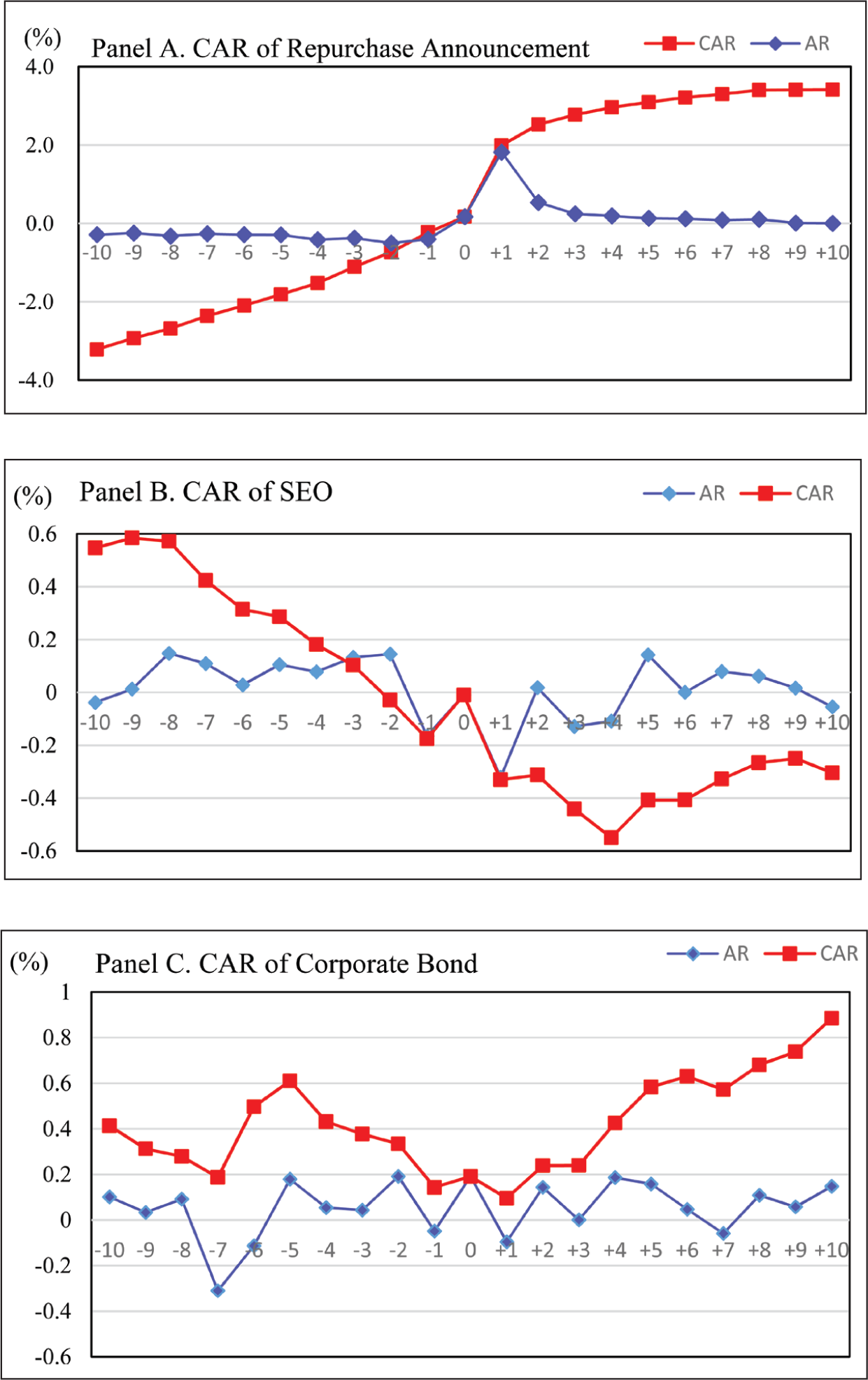

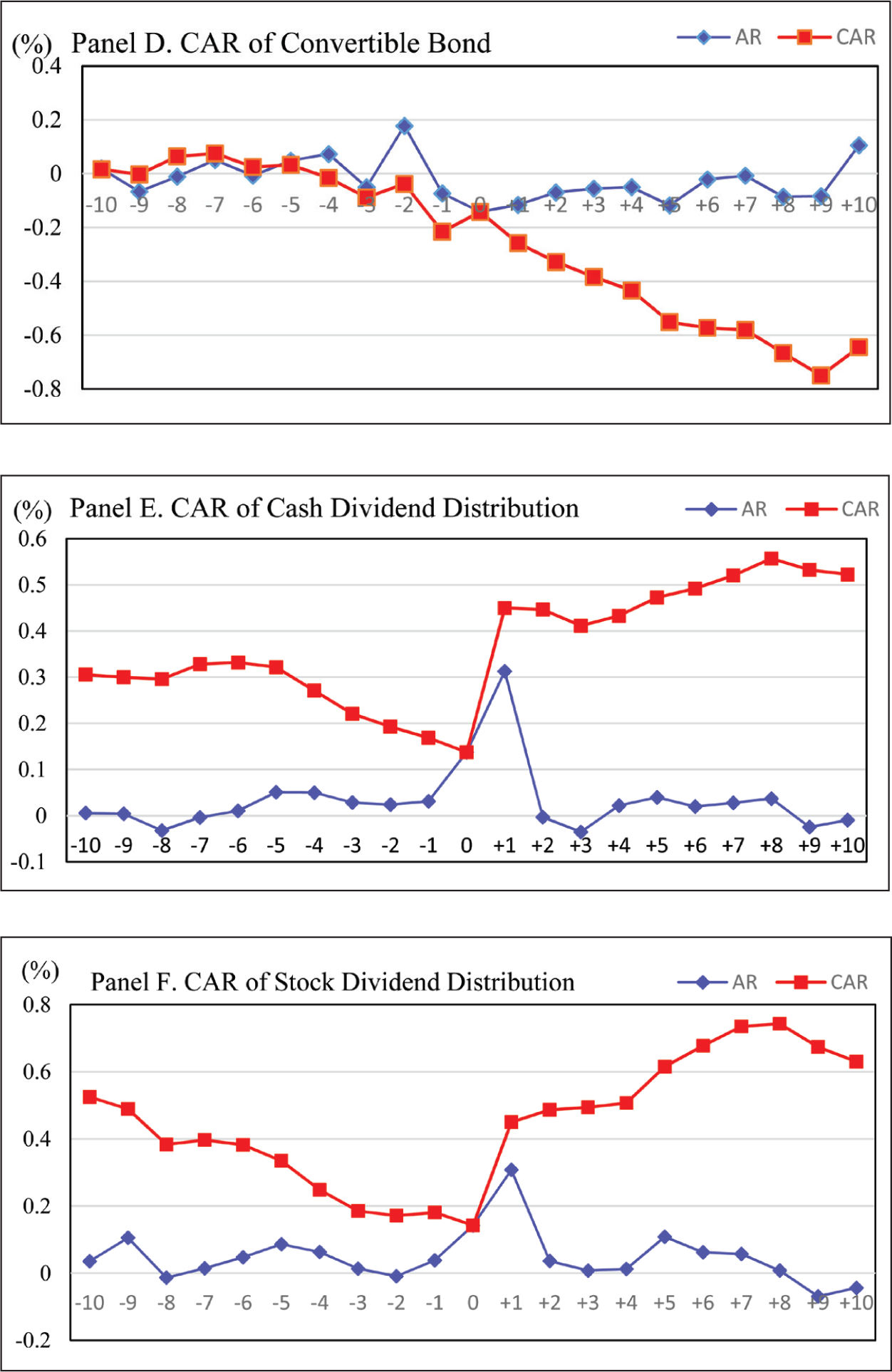

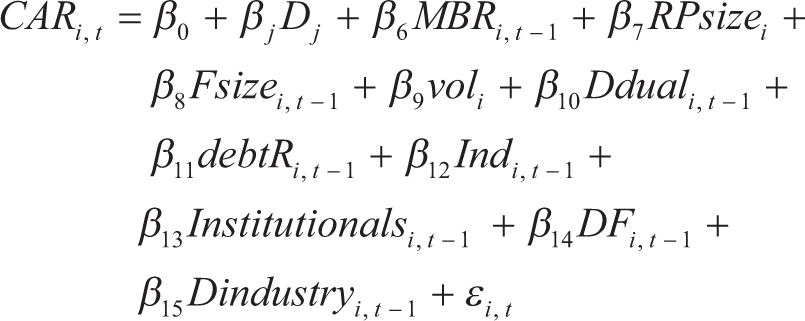

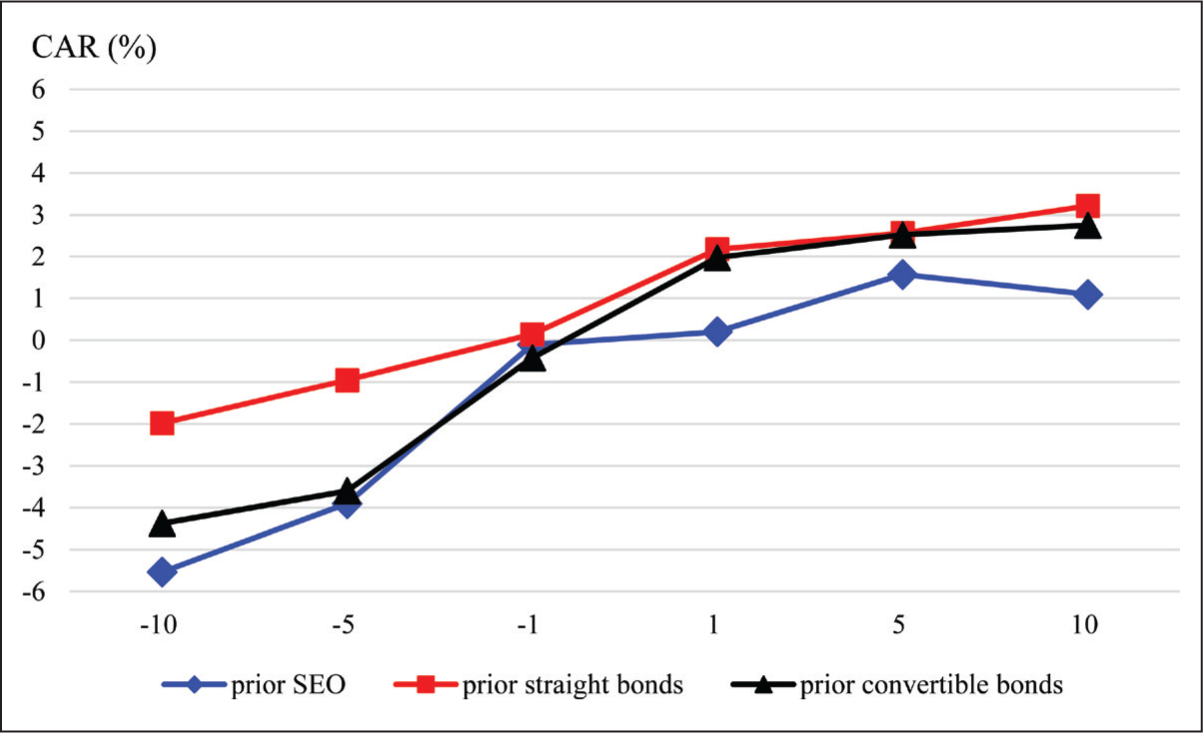

The initial sample of share repurchase announcements of the listed firms on the TWSE and TPEx were collected from the Taiwan Economic Journal database, spanning the period from August 2000 to December 2020. Excluding repeat share repurchases within one year, the announcements made by financial institutions, and observations from delisted firms, the final sample consists of 3,211 repurchase announcements, including 1,660 buybacks for transferring shares to employees, 34 cases for equity conversion, and 1,517 announcements for maintaining company credit and shareholders’ equity. Table 1 shows the number of announcing firms across industries from 2000 to 2020. Table 2 presents the general statistics of the listed company repurchase programs during the sample period. To examine if the repurchase announcement effect is influenced by the firm’s prior financial events, some important events are collected, including SEOs, the issuance of straight and convertible bonds, and cash and stock dividend distributions. The announcement effects of prior financial events are shown in Table 3, and the patterns of the average cumulative abnormal returns (CAR) are exhibited in Figure 1. In general, the announcement effects of share repurchase in Taiwan equity market are consistent with previous research (Ikenberry et al., 1995). The stock prices of announcing firms fall significantly before the announcement, ranging from –0.2290% to –3.2173%. The announcement effect of the share repurchase is significantly positive, which fits the hypothesis of signaling. The announcements of other financial events are also investigated. The announcement effects of SEO and convertible bonds are generally negative. In contrast, the announcement effects of straight bonds, and cash and stock dividend distributions are significantly positive. The evidence of repurchase and SEO announcements is in accordance with DeAngelo et al. (2010), indicating that firms may announce a SEO when the stock price is overvalued, and a repurchase program when it is undervalued.

Share Repurchase Announcements Across Industries.

General Statistics for Repurchase Programs.

Announcement Effect of Share Repurchases and Other Financial Events.

Cumulative Abnormal Returns (CAR) of Major Financial Events.

3. Methodology

In this study, a standard event study method is applied to examine the short-term market reaction to a repurchase announcement. We define the announcement date of the event as day 0. The expected return of the announcing firm is obtained from the market-index and industry-index adjusted model with the estimation period from 270 to 20 days prior to the date of the repurchase announcement. 1 The market-index adjusted method is based on capitalization-weighted TWSE and TPEx returns. A standard event study process is applied to measure the AR and the CAR of a repurchase announcement. If the average CAR after the announcement is significant from zero, it implies there is an announcement effect to the share repurchase. In our study, the MBR is used to determine whether the stock price is undervalued. Generally, lower MBR indicates that the company’s stock price is more likely undervalued.

Theoretically, all the financial practices of a firm should be consistent (Asquith & Mullins, 1986). For example, a firm’s coherent financial practice would not announce a share repurchase program following a SEO program due to the conflict between the two decisions. In general, a firm might intend to adjust its capital structure using corporate bonds to replace the equity. Chang et al. (2010) argued that a firm’s prior decisions affect the market reaction to a repurchase announcement. However, the market reactions to a share repurchase announcement with different prior financial practices are not clear. The general market reactions to various prior events are shown in Table 3 and Figure 1. All the prior events within one year of a share repurchase announcement are collected. The collected data is used to examine if the repurchase announcement effect is affected by the firm’s prior financial practice. Furthermore, we apply the Market-to-book ratio (MBRi, t–1) to measure the magnitude of under- or over-value of a firm’s stock price. Firm size (Fsizei, t–1) is measured by the natural logarithm of the total assets in the last year, and debt ratio (debtRi, t–1) is used to measure the announcing firm’s leverage:

where Dj is the dummy variables presenting the cases that repurchase announcing firms have prior financial events, such as SEO, straight or convertible bond issuance, cash and stock dividend distributions, and j = 1, 2, …, 5. In Equation (1), we also include announced repurchase plan size (RPsizei), 250-day return volatility (voli) before announcements, a dummy for the case that if the CEO is the same person as the chairman (Dduali, t–1), percentage of independent directors on the board (Indi, t–1), shares held by institutional investors (Institutionalsi, t–1), dummy for if the announcing firm is a family-owned firm (DFi, t–1) and if the firm operates in the electronics industry (Dindustryi, t–1).

4. Empirical Results

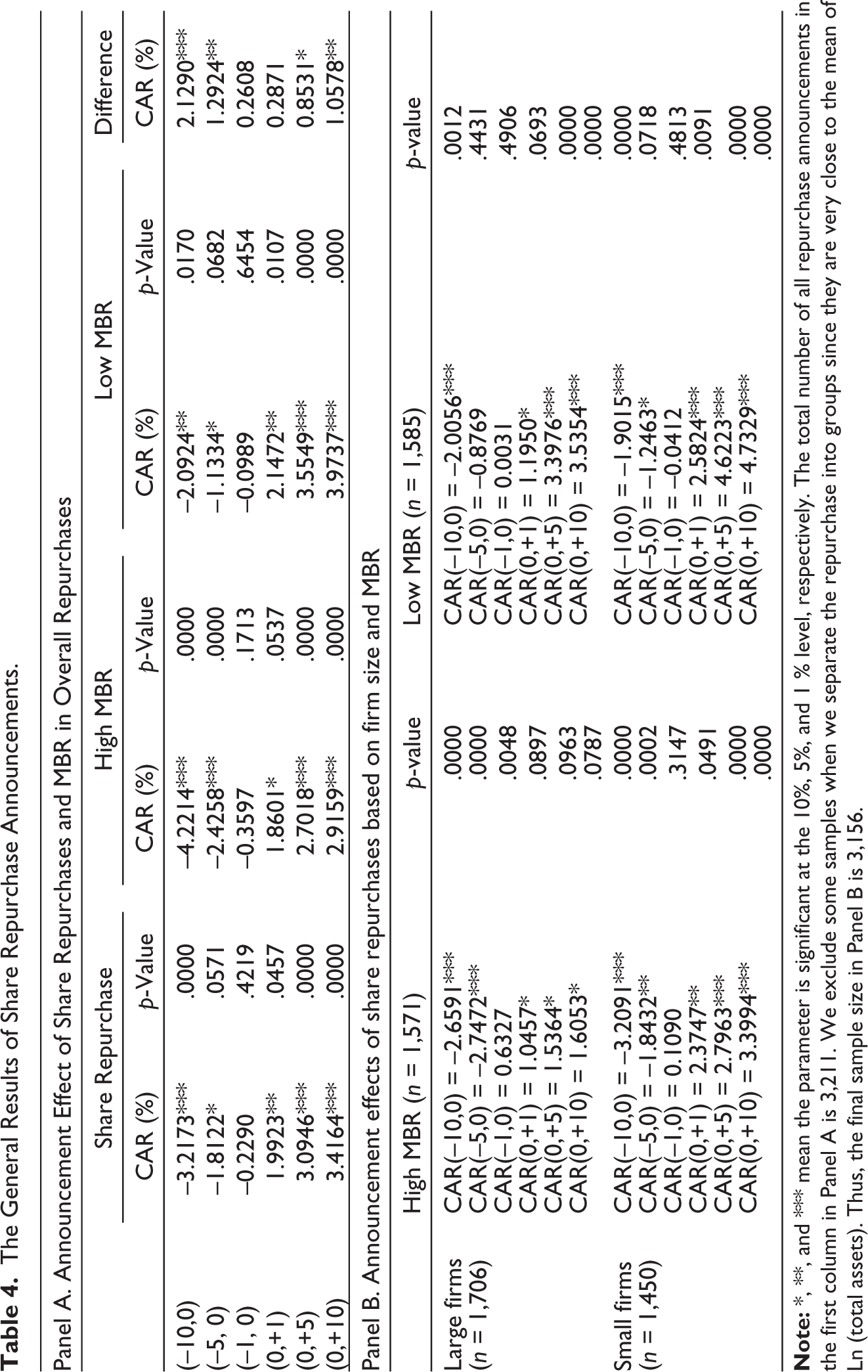

Table 4 provides the general results of the CAR of the share repurchase announcements. In panel A, CAR ranges between –3.2173 and 3.4164, indicating the stock prices are in a downward trend prior to the share repurchase announcement and that they generally ascend after the announcement. It demonstrates that repurchase announcements deliver some information to the market, and investors respond positively. The general results deliver the same information as in Firth and Yeung (2005). In addition, we investigate if under- or over-valuation leads to a significantly positive CAR with various MBRs. The evidence in Panel A of Table 4 shows that CARs of repurchase announcements of firms with lower MBR are larger than the ones with higher MBR (difference CAR(0,+10) = 1.0578%), which is consistent with Ikenberry et al. (1995). Specifically, the repurchase announcement effects of undervalued firms are significantly stronger than those of overvalued firms. In Panel B of Table 4, we examine the repurchase announcement effects based on firm size and MBR. The evidence shows that the repurchase announcement effects on smaller firms with lower MBR are strongly significant. For example, CAR (0,+10) in the right-bottom and left-upper cells of Panel B are 4.7329 and 3.3994. It implies that repurchase announcements of small and undervalued firms are more positively significant than those of large and overvalued firms. Another explanation for this is that small (large) firms’ having less (more) attention in the market directly causes them to be undervalued (overvalued).

The General Results of Share Repurchase Announcements.

4.1 Repurchase Announcement After SEO and Bond Issuances

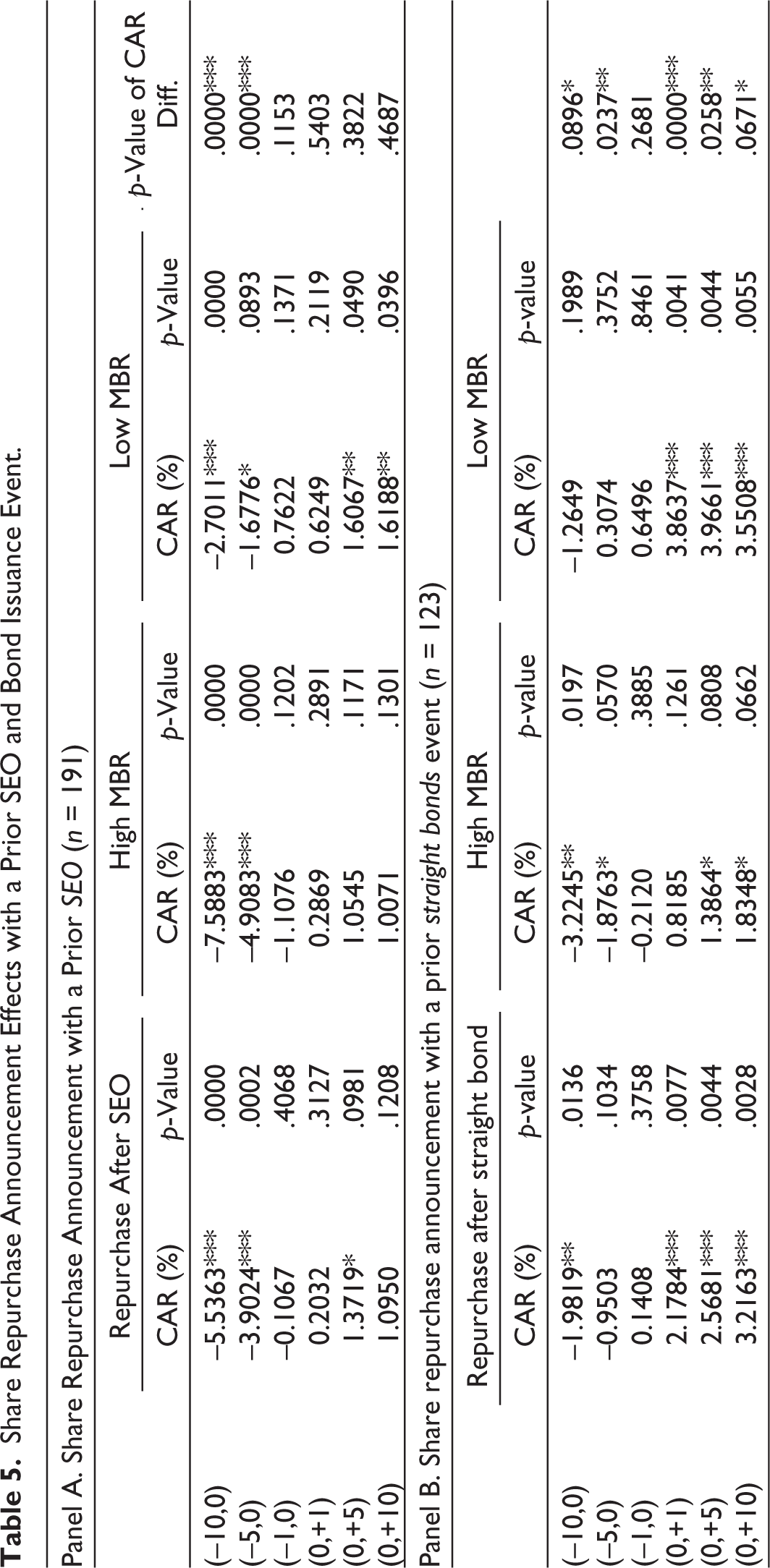

This section examines the effects of a repurchase announcement after a SEO or a bond issuance announcement. SEO is a common method for listed firms to raise capital (Hess & Frost, 1982; Marsh, 1982), since they might have new investments and opportunities. However, firms might announce a SEO and then announce a share repurchase within one year to reduce the number of shares. Theoretically, firms’ SEO announcements deliver an overvalued image to the stock price (Chen et al., 2001; Corwin, 2003; Lucas & McDonald, 1990). However, the repurchase announcement provides an undervalued appearance. The former event inflates the firm’s capital, while the latter shrinks the firm’s equity. It is a puzzle that a listed firm might operate these two contrary financial practices consecutively within a short period. In general, the evidence shown in Panel A of Table 5 (as well as in Figure 2) indicates that the repurchase announcement with a prior SEO event generally has a weak market reaction. A potential interpretation of the results is that market investors do not identify the motivation of share buyback, particularly with a prior SEO event. In other words, the firms announcing share repurchases with a prior SEO event could not receive a positive market response in general since the SEO and repurchase are incompatible. The evidence in Panel A also shows that firms’ announcements with high (overvalued) MBR are not significant, but the announcements in the low (undervalued) MBR column are generally significant.

Share Repurchase Announcement Effects with a Prior SEO and Bond Issuance Event.

Share Repurchase Announcements with Various Prior Financing Announcements.

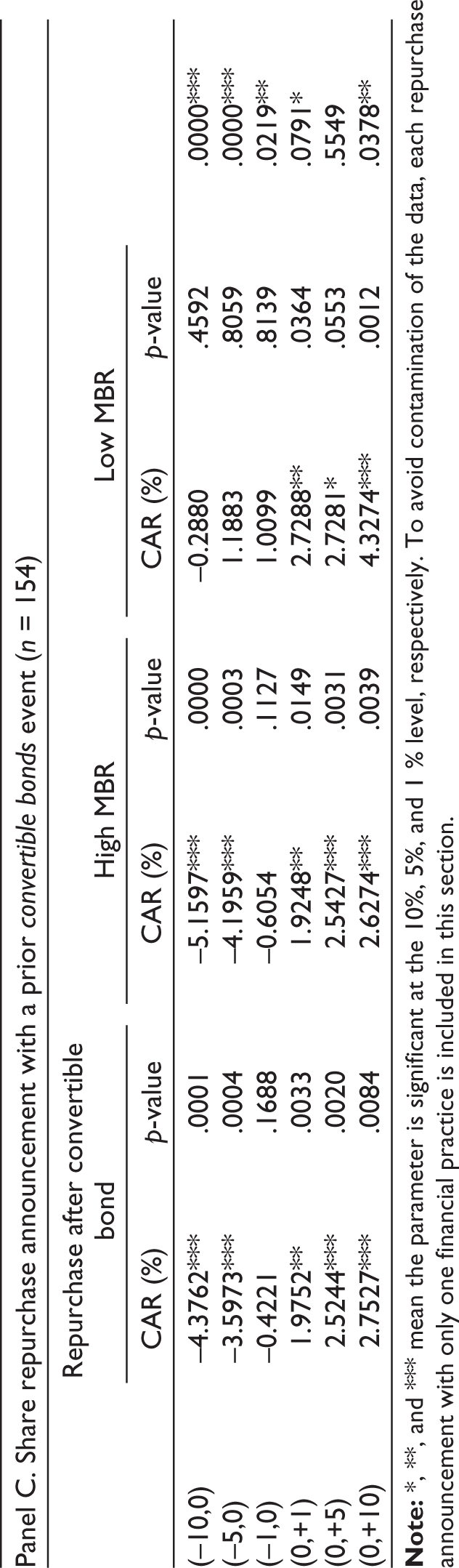

Corporate bond is an alternative of long-term financing and widely used by listed firms. Thus, we also examine the announcement effects of the share repurchase with a prior corporate bond issuance, including straight and convertible bonds. The results in Panels B and C of Table 5 generally exhibit significantly positive CAR. In Panel B, repurchase announcements with a prior straight bond issuances have strong effects, implying that the market investors accept the repurchase programs and the consecutive policy. Similar results can be found in Panel C. Generally, share repurchase announcement effects with a prior convertible bond issuance are significantly positive. However, a convertible bond might expand the firm’s outstanding shares in the future. Furthermore, repurchase announcements with a prior convertible bond issuance of low MBR firms generally react strongly and even have similar effects to those issuing straight bonds, which has no expanding effect. On average, lower MBR firms with a prior straight and convertible bond issuance have stronger and more significant repurchase announcement effects than those with a prior SEO event. In addition, lower MBR firms’ share repurchase announcements with both prior bond events generally have a more positive market response.

4.2 The Effect of Share Repurchases After Different Dividend Policies

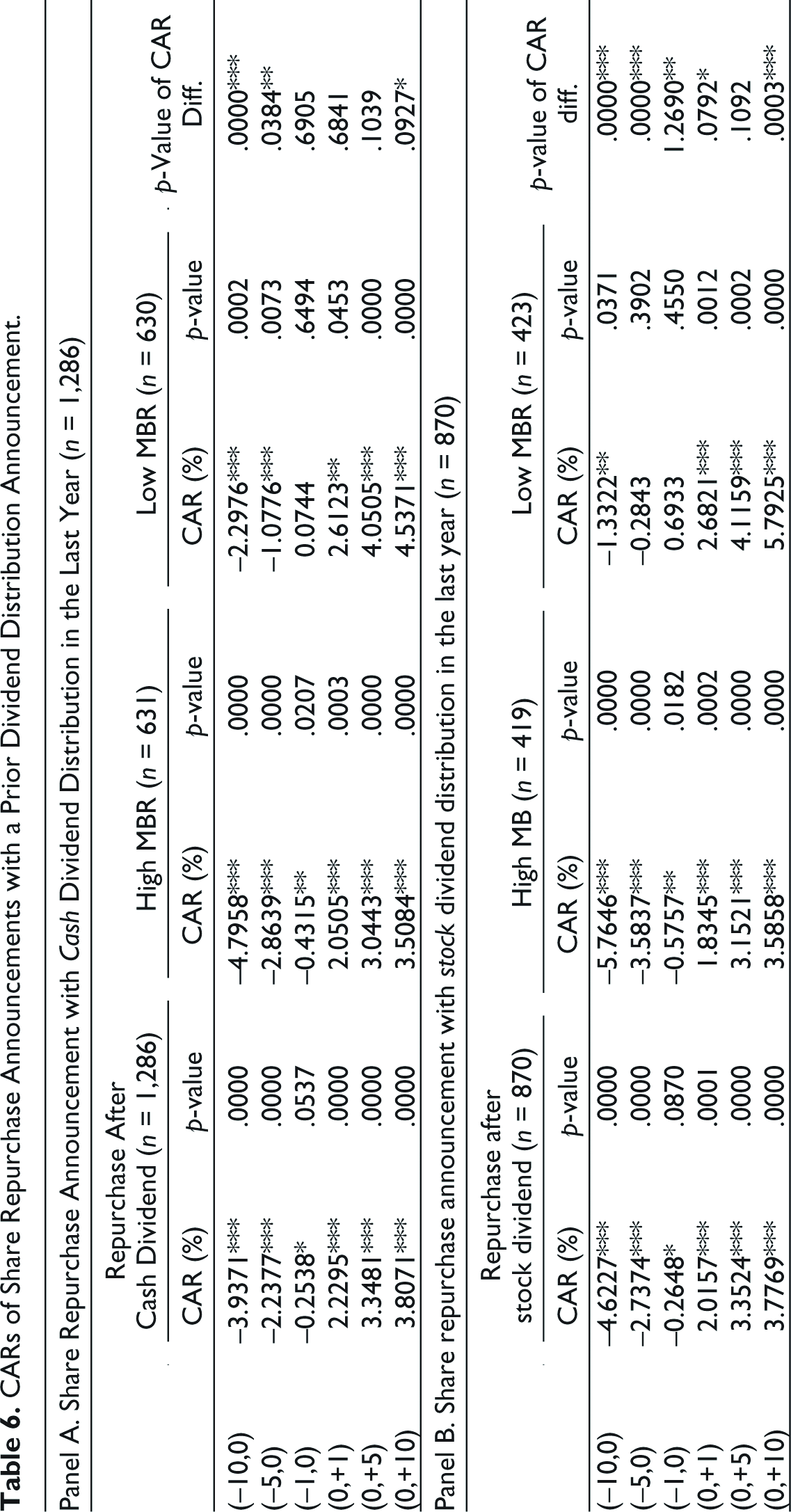

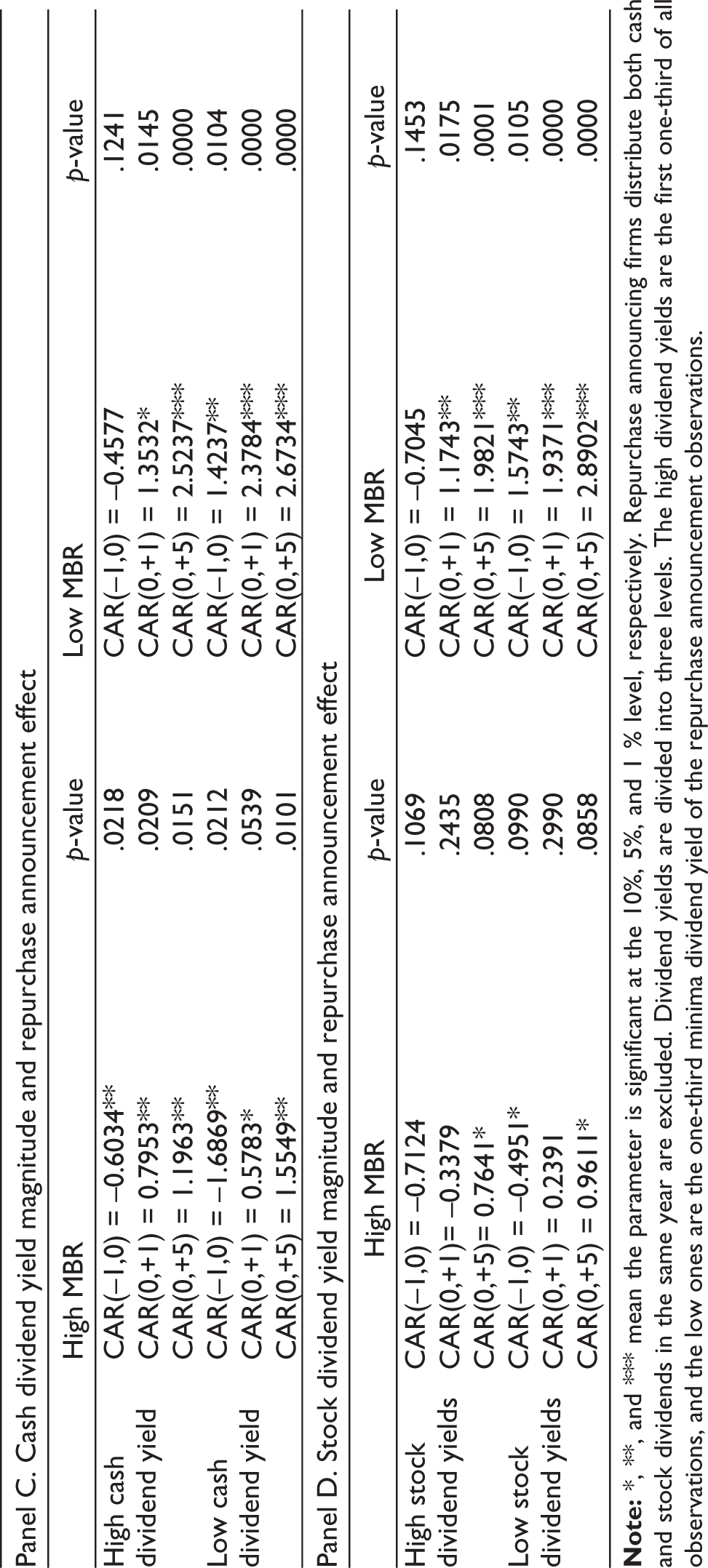

Dividend policy is critical to listed firms since it is associated directly with the share price. This section examines if the cash and stock dividend distributions might affect the firm’s repurchase announcement effect. Share repurchase announcement effects with a prior cash and stock dividend distribution are shown in Table 6. Generally, repurchase announcements with cash and stock dividend distribution are significantly positive, indicating that market investors prefer firms that distribute dividends in the previous year and then announce a repurchase program. In addition, the positive repurchase announcement effects of firms with a prior stock dividend distribution are slightly stronger than those with a cash distribution. Similar results could also be found in the low-MBR firm column. The possible explanation for this is that investors in emerging markets, like Taiwan stock market, prefer to receive stock dividends rather than cash dividends (Jain, 2007). Another potential reason for the results is that more listed firms distributing stock dividends are young electronics companies, and the electronics firms prefer distributing stock dividends to support their future growth.

CARs of Share Repurchase Announcements with a Prior Dividend Distribution Announcement.

In Panels C and D of Table 6, we examine the magnitude of the influence of dividend yield in the last year on the repurchase announcement effect. The observations are divided into four groups by the magnitude of dividend yield and MBR. Obviously, firms’ share purchase announcement effects are influenced by the degree of dividend yield, specifically, the ones with low MBR and low dividend yield (both cash and stock dividend yields) in the last year have significantly stronger effects. In other words, the repurchase announcements of firms with a low dividend yield deliver strongly positive information that their stock prices are undervalued compared to their intrinsic values. In contrast, the market reactions to lower-MBR firms’ repurchase announcements with higher dividend yields are generally weak since the good news from the announcements has been reflected in the high-dividend news. Similar to the results above, the repurchase announcement effects of the firms who have higher MBR are lower than the ones that have lower MBR, which is consistent with previous results shown in Section 4.

4.3 Regression Analysis of Repurchase Announcements and Robustness Analysis

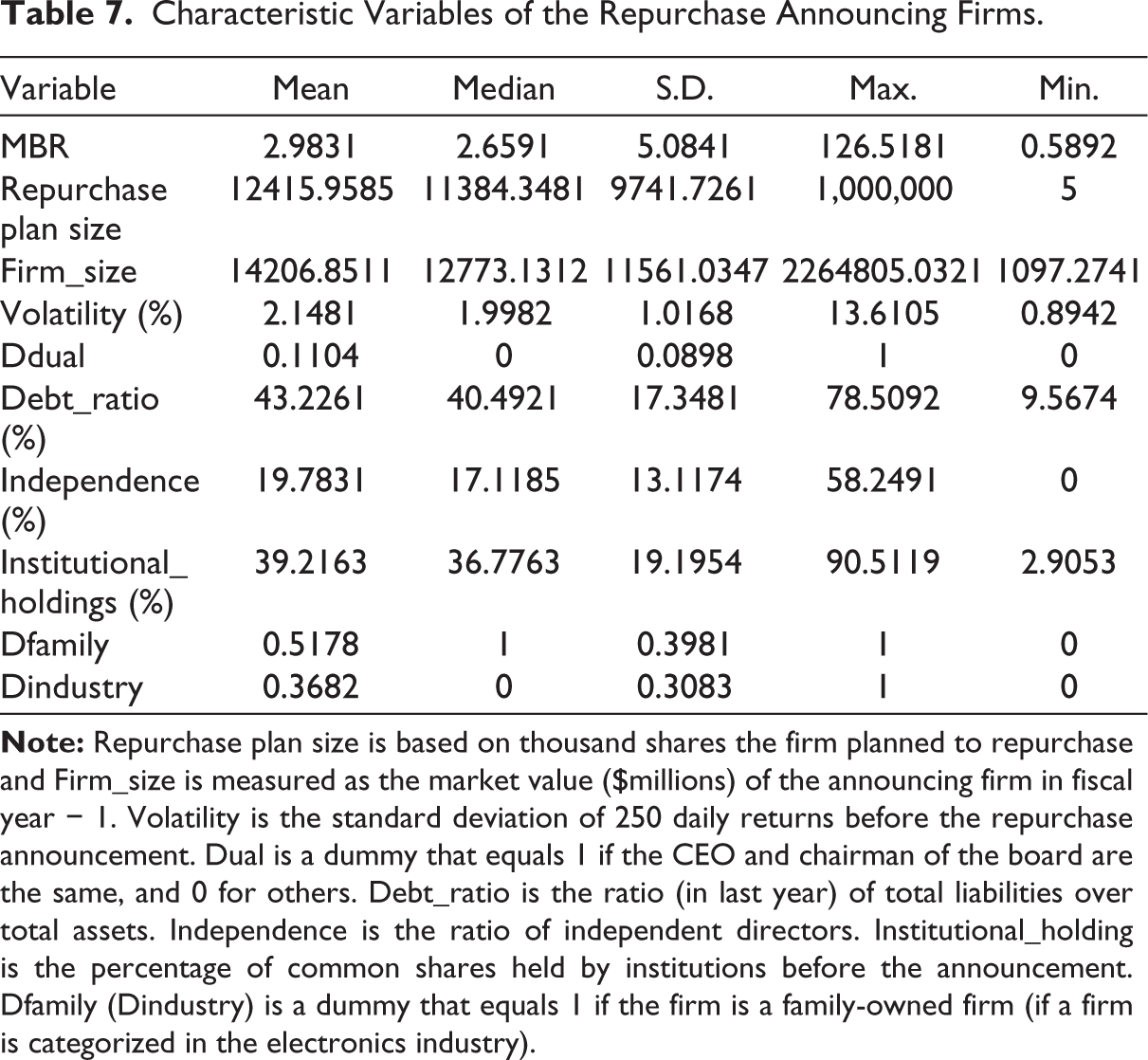

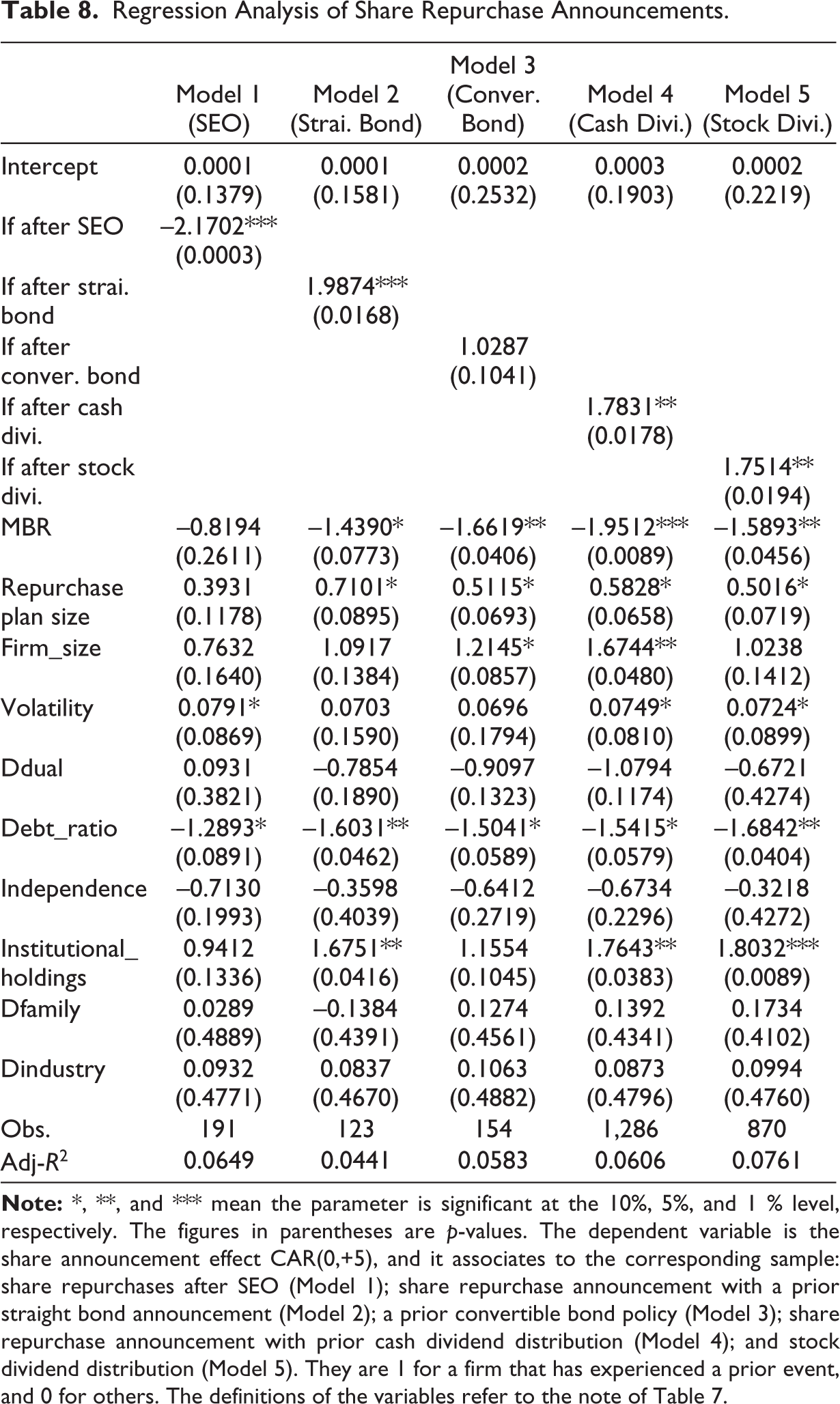

In this section, we investigate the role of prior financial practices on repurchase announcements. The characteristics of the announcing firms in Table 7 are also collected to enhance the robustness of our results, and the results of the regression analysis are displayed in Table 8. The results in Table 8 indicate that the announcement effects of share repurchase are associated with the prior financial practices. Specifically, the investors reacting to the firms’ repurchase announcement are affected by the firms’ past financial practices. For example, the repurchase announcement effects are negatively related to the firms’ prior SEO event (–2.1702). When the repurchase announcing firms have a SEO announcement, the repurchase announcement effect is significantly negative. This result also implies that investors do not support the firm’s expanding equity by using SEO and reducing it with a repurchase program in the next year, since the two financial decisions are conflicting.

Characteristic Variables of the Repurchase Announcing Firms.

Regression Analysis of Share Repurchase Announcements.

In contrast to repurchase announcements with a prior SEO event, repurchase announcement effects are positively associated with a prior straight bond issuance (1.9874), prior cash dividend distribution (1.7831), and prior stock dividend distribution (1.7514). However, it is surprising that repurchase announcement effects are not significant if the firm has a prior convertible bond issuance announcement. A potential explanation for this depends on the likelihood of convertible bonds becoming common shares in the future. If the convertible bonds convert into common shares, then the role of convertible bonds is similar to SEO. The evidence shows that repurchase announcement effects are positively associated with the firms’ prior cash or dividend distributions. Both prior cash and stock dividend distributions lead to a significant repurchase announcement effect, particularly for a prior cash dividend announcement (1.7831). In fact, dividend distribution implies that the firm has better operational performance, and the following repurchase announcements are alternatives to the payout policy. This could be a potential factor that repurchase announcements with both prior dividend distributions receive positive reactions. In Table 8, the coefficients of MBR in all models are negative, implying that the firm’s repurchase announcement effect is negatively associated with its magnitude of overvaluation.

To enhance the robustness of our results, the announcement effect of shares repurchase with various prior financial events are adjusted based on equal-weighted stock index return (as opposed to value-weighted in Table 8). 2 The robustness tests are shown in Table 9, and we obtain similar results from Table 8, that generally, the announcement effects of the share repurchase with a prior SEO event are negative. Share repurchase announcements with other financial events such as straight bond, convertible bond, cash, and stock dividend distribution normally have significantly positive market responses. On average, share repurchase announcement with a prior cash dividend distribution has a positively stronger effect. In addition, other characteristic variables of the announcing firm also exhibit some interesting results in Table 8. The repurchase announcement effects are negatively associated with MRB in general, which is consistent with the results in Table 4. Similar to Ikenberry et al. (1995), the results show that the repurchase announcement effects of overvalued firms (higher MRB) are negative. Consistent with Bonaimé (2012), the results in Table 8 also indicate that the announcement effect is positively associated with the size of the repurchase plan and firm leverage.

Robustness Tests of Share Repurchase Announcements.

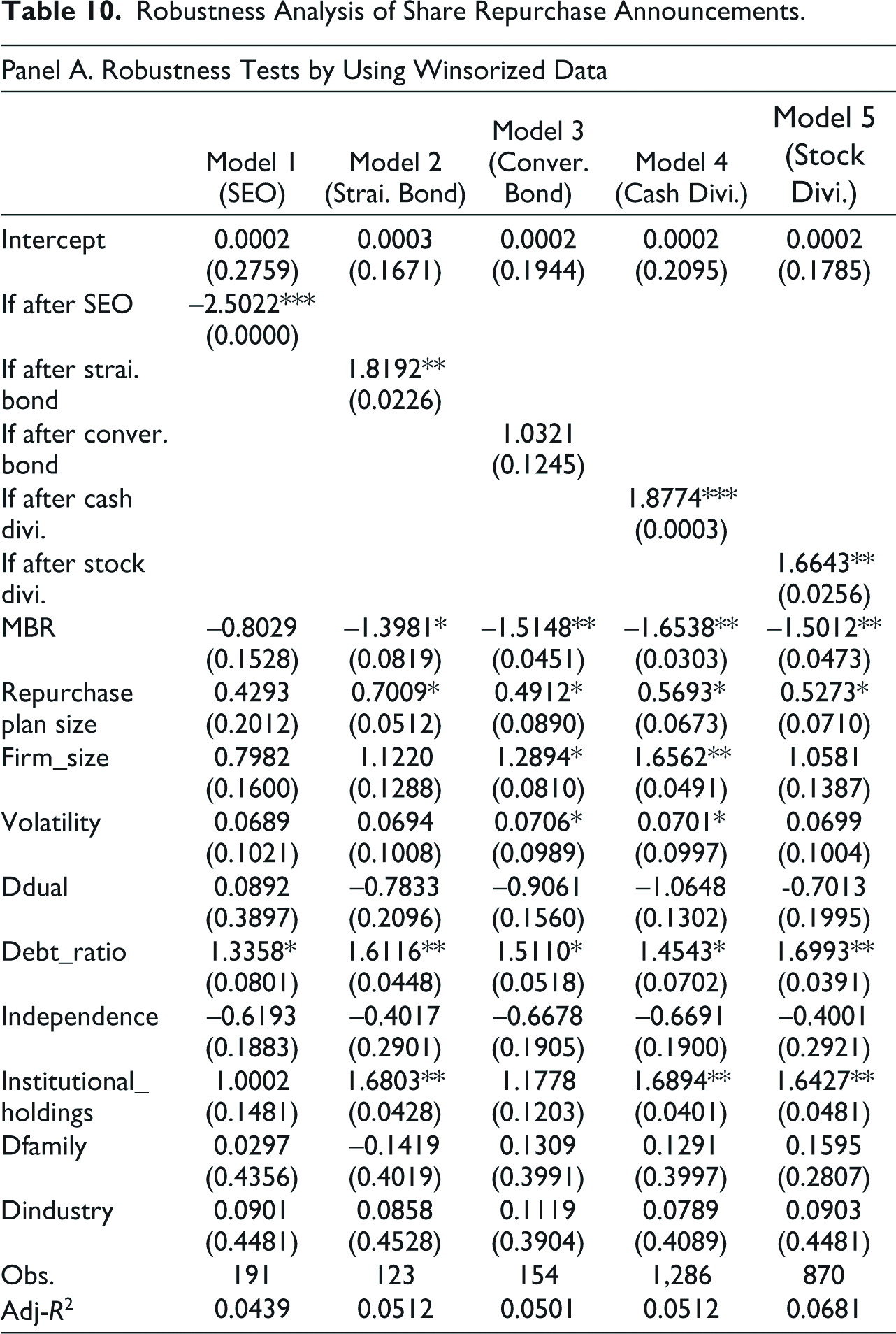

This section further examines if the results in Table 8 are affected by the extreme observations and endogeneity, and the results are presented in Panels A and B of Table 10. Following Grullon and Michaely (2004), Chen and Wang (2012), and Bonaimé et al. (2016), the dependent variable CAR (0,+5) is winsorized at the first and the 99th percentiles to mitigate the effect of outliers. 3 The results of winsorized data are generally consistent with the results using the full sample in Table 8, indicating that the prior SEO event is negatively associated with the current effects of the share repurchase announcement. The firms’ repurchase announcements with other prior financial practices, for example, straight or convertible bond issuances and cash or stock dividend distributions, normally have positive effects.

Robustness Analysis of Share Repurchase Announcements.

We also examine the endogeneity by using the two-stage regression method of Heckman (1979). The probit regressions with the dependent variables (a binary variable if the announcing firm has a prior financial event) are estimated in the first stage model. For example, a dependent (binary) variable, if the announcing firm has a prior SEO event, is used in Model 1, and independent variables, such as MBR, repurchase plan size, firm size, volatility, dummy variable for chairman/CEO duality, debt ratio, board independence, institutional investors’ holding, and the two dummy variables, are included in the first-stage regression model. In the second stage, we run the regression of repurchase announcement returns on the dummies, that is, if the announcing firms have prior financial events, the firm characteristics, and the inverse Mills ratio obtained from the first-stage regression model. As shown in the evidence in Panel B of Table 10, share repurchase announcement effects are generally associated with the firm’s prior financial events. The inverse Mills ratio is not significant across various prior financial events, indicating that our results are robust without the issue of endogenous self-selection.

5. Conclusion

All financial practices and decisions in a firm are horizontally consistent with each other. Share repurchase is a critical financial practice that could be used to adjust firm’s a capital structure and as a part of corporate payout policy. This study mainly examines whether the announcement effects of the share repurchase are affected by the firm’s prior financial events. We investigate the influence of a firm’s prior financial practice on the repurchase announcement effect in the Taiwan equity market with long-range data. Some prior financial practices, such as SEO, straight and convertible bond issuance, and cash and stock dividend distributions are included.

Similar to previous studies, the stock prices of the announcing firms present a downward tendency before the repurchase announcement and a significantly positive effect afterward. The evidence indicates that a firm’s repurchase announcement with a prior SEO event is more likely insignificant, though the announcing firms with lower MBR have few positive reactions. Moreover, the regression analysis further shows a negative relationship between the repurchase announcement effect and the prior SEO event. This result implies that market investors are less likely to support firms that raise equity and then scale the equity down by using a share repurchase program. In sum, the two conflicting financial practices are not supported by investors.

Compared to the results above, we also investigate if prior bond issuance had an influence on the effect of the share repurchase announcement. In general, a share repurchase announcement after a prior straight or convertible bond issuance has a significantly positive effect, especially for firms with lower MBR. Surprisingly, the announcements with prior convertible bond issuances have stronger market reactions. This phenomenon implies that the investors in the Taiwan stock market prefer having a likelihood of receiving stock in the future if it is worthwhile to convert a bond to a share. In addition, we examine if prior dividend distribution is a factor affecting the repurchase announcement effect, including both cash and stock dividends. We find repurchase announcements with a prior dividend distribution, either cash or stock dividends, have a significantly positive effect. Furthermore, dividend yield plays a critical role as firms with lower MBR and lower cash or stock dividend yields have higher repurchase announcement effects. The regression analysis also indicates that prior cash dividend distribution announcements contribute more to the repurchase announcement effect than stock dividends. There are many factors affecting the effectiveness of stock repurchase announcements, and we found solid evidence that prior financial practices and decisions are the critical factors considered by market investors.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.