Abstract

KASB Bank Limited was a small sized bank in Pakistan. Its operations did not generate sufficient profits and over the years it was unable to meet the regulatory capital as specified by the State Bank of Pakistan. The bank’s loan portfolio was infected with poor quality borrowers and this resulted in very high non performing loans which required loan loss provisions. The bank sponsor had other group companies which the KASB Bank acquired in order to meet the capital needs. The State Bank as part of compliance with BASEL rules required higher amounts of capital to protect the banking sector and had allowed KASB Bank extra time to meet the capital needs. However, the State Bank ultimately used its regulatory authority to put the bank under its supervision. The State Bank placed KASB Bank under a moratoriam so that the KASB Bank customer deposits were frozen and only withdrawls up to PKR300,000 were allowed from each account. The State Bank wanted another bank to take over the KASB Bank operations and allowed other interested banks to conduct due diligence so as to review the financial status of the bank with a view to take over the troubled bank. There were very few banks interested in taking over because KASB Bank had negative equity estimated at PKR12 to PKR14 billion. The State Bank in order to protect the interests of the 150,000 depositors and the stability of the banking system gave a concessionary loan of PKR20 billion as part of the scheme of amalgamation of KASB Bank with Bank Islami.

Discussion Questions

Fahim was a financial analyst with a local funds management company in Lahore, Pakistan. On 25 May 2015, he had been assigned the task of preparing an important report. This report discussed how the State Bank of Pakistan (SBP) had placed a moratorium on KASB Bank’s activities on 14 November 2014. Fahim also wanted to analyse how the SBP had resolved the issue of KASB Bank. The SBP had merged KASB Bank with another bank known as Bank Islami Pakistan Limited, and Fahim wanted to understand how this amalgamation had resolved the matter.

The KASB Bank Limited had PKR57 billion in customer deposits which the SBP wanted to protect, so the moratorium did not close KASB Bank, but only restricted the bank from paying certain debts. The SBP had allowed depositors up to PKR300,000 1 to operate their accounts normally. The bank would also continue to collect its loans and advances. The general public was assured by the SBP that KASB Bank was a small bank and had less than 0.7 per cent of the banking sector deposits as a whole (SBP, 2014a). There was no effect on any other bank, and all other banks were functioning normally. KASB Bank had reported losses continuously over the preceding five years; its losses for the calendar year ending 31 December 2013 were PKR1,625 million and a very high percentage of its loans and investments portfolio were non-performing. As a result, the bank had been facing severe capital shortages in terms of both minimum capital requirement (MCR) and capital adequacy ratio (CAR). As of 30 September 2014, its MCR was about PKR0.958 billion (SBP, 2015) with a CAR of negative 4.63 per cent against the required levels of PKR10 billion and 10 per cent, respectively. As KASB Bank could not meet the SBP capital adequacy requirements, this had resulted in regulatory action by the SBP—the latter had warned the bank’s board of directors that as the regulatory capital had become negative, the SBP would take action if arrangements were not made to enhance the capital base. Fahim planned to conduct the analysis of the financial statements of KASB Bank to arrive at an estimate of the capital deficit by calculating the Tier 1 capital which represented the bank’s internal resources. He also wanted to analyse the actions of the State Bank in resolving the matter.

Background

KASB Bank Limited was a public limited company which had been incorporated in 1994 (KASB Bank Limited, 2012). It was listed on all the stock exchanges in Pakistan and was licensed to undertake the business of commercial, consumer and investment banking. The bank was a holding company with many associates as part of a group of companies known as the KASB Group (see Exhibit 1). It was reporting losses due to poor profitability, as a result of which its regulatory capital was eroded and fell below the statutory minimum requirement. In order to meet the State Bank requirements of capital, the management and board of directors decided on a series of mergers with other group companies. Two major companies that were merged into the bank were International Housing Finance Limited (IHFL), in 2006, and KASB Capital Limited (KCL), in 2008, which were non-banking finance companies. Another company, Network Leasing Company Limited (NLCL), was merged by the end of 2008.

Banking Sector Outlook (2009–2014) 2

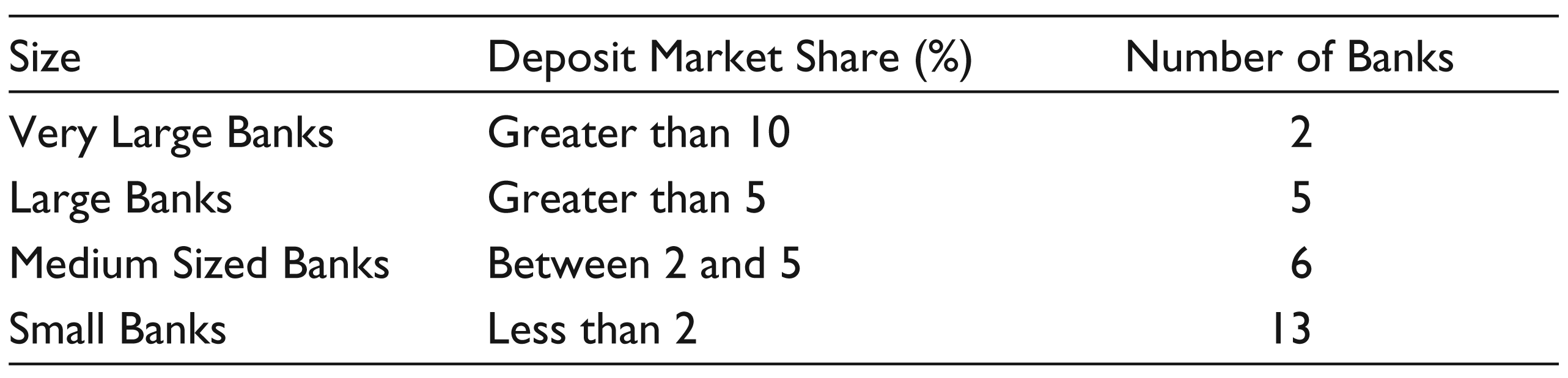

The banking industry in Pakistan had grown at a compound annual growth rate (CAGR) of 13.2 per cent over the period 2009–2014, while deposits of the industry had posted a CAGR of 14 per cent. The banks, in general, had adopted a conservative lending strategy as a result of high problem advances during 2008–2010. The banks invested in high returning government securities which ensured that profitability remained strong without exposure to credit risks. For investors, a return on equity on bank stock of 16.2 per cent was very attractive. The banking industry was divided into the various market segments, mentioned in Table 1.

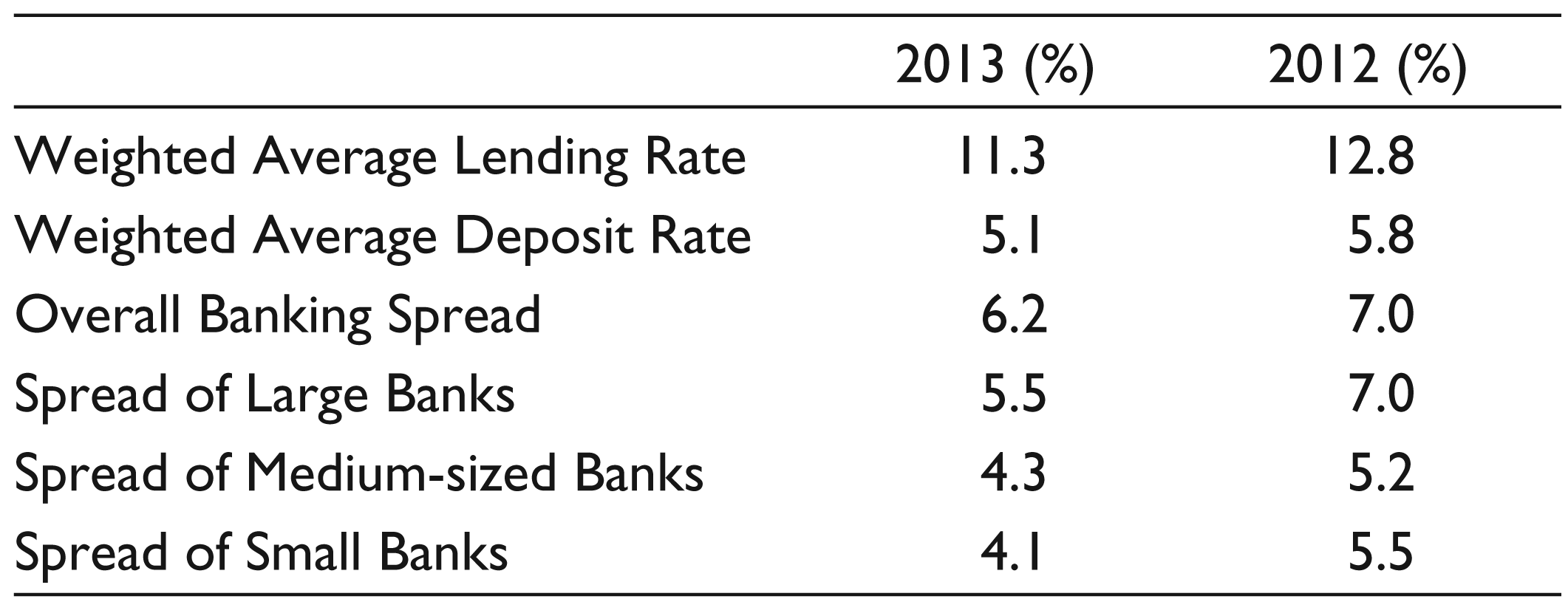

KASB Bank was among the small-sized banks and, along with its peers, was having difficulty in meeting the enhanced capital requirements of the SBP. As Basel III 3 was being implemented, the pressure on asset quality and a narrowing of spreads made the operating environment for banks having a weak financial risk profile more challenging (see Table 2). The spreads achieved by various categories of banks are shown in Table 2. 4

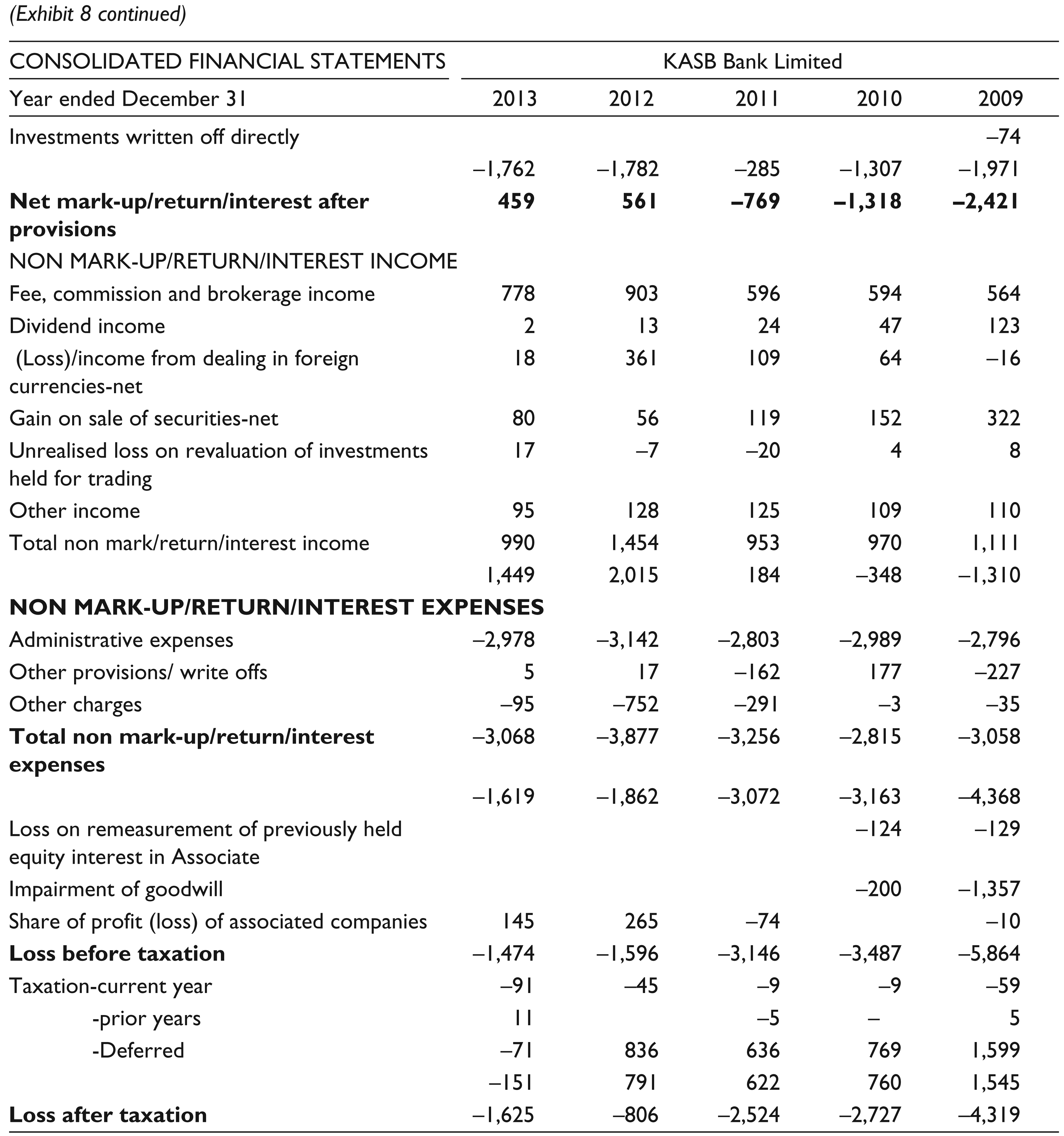

Over the years, the bank had made poor credit decisions in building its loans and advances portfolio and, as a result, its non-performing loans (NPL) were very high. The bank’s performance from 2009 to 2013 was seriously affected by the NPLs and other strategic investments that were also non-earning. The banking sector continued to operate in one of the most challenging times during 2009 due to tight liquidity conditions, distressed corporate performance and an overall weak macroeconomic situation. During 2010–2011, the bank’s investments did not generate enough earnings and the net interest margin became negative. This fact, and the amount of loan loss provisions and impairments in 2009 of PKR3,328 million and PKR1,509 million in 2010, caused the bank to report huge losses of PKR4.3 billion in 2009 and PKR2.7 billion in 2010. There were also further provisions required for subsequent years. In 2011, due to the high cost of funds, the net interest margin was again negative at PKR485 million which, together with administrative expenses of PKR2.8 billion, resulted in the bank reporting a loss of PKR2.5 billion. The bank also posted losses in dealings in foreign exchange due to a weak currency. The administrative expenses increased to a high of PKR3.1 billion in 2012 and the bank’s loss for the year was PKR806 million. The net interest margin in 2013 was insufficient to cover the loan loss provision of PKR1.18 billion and the administrative expenses of PKR2.9 billion, causing a loss of PKR1.6 billion in 2013. By the end of 2013, the accumulated loss was a massive amount of PKR12,500 million.

Market Segments of Banking Industry

KASB Bank Financial Performance

Asset Quality

On a quarterly basis, the bank reviewed the entire loan portfolio and made provisions for any NPL. This was in compliance with the prudential requirements stipulated by the SBP. The bank management’s focus had been mainly on the recoveries of its stuck up advances (NPLs; see Exhibits 2 and 3). The overall advances portfolio registered no significant movement, but the NPLs were very high—these increased from 21 per cent of advances in 2009 to a high of 36 per cent of the advances during 2012. This was due to an increase in the interbank rate called KIBOR (Karachi Interbank Offer Rate) which caused a large number of customers to default. These advances not only took up a lot of management time but also required different expertise to restructure them. The bank took measures to strengthen the security structure and initiated prompt restructuring and rescheduling to limit the deterioration of the loan portfolio. The prudential regulations prescribed age-based criteria for the classification of NPLs and advances as held by the bank.

The SBP Quarterly Report for the October to December 2014 quarter (SBP, 2014b) stated that the asset quality of banks, in general, continued to improve from July 2013 to December 2014 as the NPLs to loans ratio decreased by 70 basis points to 12.3 per cent. The report also noted that the operating performance of the banking industry showed a marked improvement as the profit before tax increased by 52 per cent during 2014.

However, the performance of KASB Bank was very different in 2013. While the new NPLs identified were low at PKR649 million compared to PKR2.9 billion that were recovered in cash or regularized, their total as a percentage of the entire portfolio remained high at 35 per cent. Management had set up a Special Assets Management Group (SMAG) to adopt an aggressive follow-up of NPLs. The bank had developed measures to put likely NPLs on a watch list to address and reduce the accounts being classified. The bank had a dedicated recovery team that dealt with NPLs on a regular basis. Experience showed that a substantial number of companies and customers who had been classified and were not current on advances repayment were still operating their businesses; the bank staff was in contact with such cases to restructure their facilities wherever possible.

Bank Regulatory Capital

The SBP (2013) had prescribed various levels of regulatory capital for the banks operating in Pakistan. The financial year of all the banks followed the calendar year, and the minimum regulatory capital that all the banks were required to maintain was judged on 31 December. The amount of regulatory capital had been raised in a phased manner and was PKR6 billion in 2009, which increased to PKR10 billion in 2013 (see Exhibit 4; see also SBP, 2008). Section 14 Clause (i) of the Banking Companies Ordinance 1962 stated:

No banking company incorporated in Pakistan shall carry on business in Pakistan unless it satisfies the following condition: that the subscribed capital of the company is not less than one-half of the authorized capital and the paid-up capital is not less than one-half of the subscribed capital. (SBP, 1962)

Under this overriding condition, there were the some capital standards as defined by the SBP that we will discuss here.

Minimum Capital Requirement (MCR)

MCR (SBP, 2013) was a standard that established the minimum amount of capital that had to be held by banks. No bank could carry on its business in Pakistan unless it met the nominal capital requirements prescribed by the SBP from time to time. The existing MCR standard of paid-up capital (net of losses) consisted of the sum of the following elements:

Fully paid-up common shares Balance in share premium accounts Reserve for issue of bonus shares Any other type of instrument approved by the SBP

Less

Accumulated losses/discount offered on issue of shares Negative general reserves Regulatory adjustments

This was known as Tier 1 capital and represented the internal financial resources of the bank. Tier II capital included general provisions for loan losses (up to a maximum of 1.25 per cent of risk-weighted assets or RWA), reserves on the revaluation of fixed assets and equity investments (up to a maximum of 45 per cent of the balance in the related revaluation reserves gross of any deferred tax liability), after deduction of 50 per cent of the equity investment of the subsidiary company.

Tier III supplementary capital consisted of short-term subordinated debt, which was solely for the purpose of meeting a proportion of capital required for market risks. The bank did not have any Tier III capital. The total of Tier II and Tier III capital had to be limited to Tier I capital.

Capital Adequacy Ratio (CAR)

CAR (SBP, 2013) was a ratio that indicated the level of risks faced by the banks; it was calculated on a consolidated and standalone basis. Certain deductions were required from MCR by the SBP to calculate the required eligible capital (see Exhibit 5). CAR was calculated by taking the eligible capital as the numerator and the total RWA as the denominator.

Banks were required to calculate their RWA with respect to credit, market and operational risks. This ratio was a measure of the financial strength of the bank by comparing the capital with the risk assets. Any bank which was not complying with the required CAR had to inform the SBP and state the remedial measures it had taken. The SBP could take the following actions against any bank that failed to meet the regulatory capital requirement:

Penalties that may include restrictions on business operations, including withdrawal of permission to accept deposits and any other as deemed fit by the SBP Withdrawal of the license as a scheduled bank Cancellation of the banking license if the bank failed to meet both the regulatory requirements of CAR and MCR

KASB Bank’s goals for managing capital were identified as follows (KASB Bank Limited, 2013):

To be an appropriately capitalized institution as defined by the regulatory authorities and compar-able to the peers Maintenance of strong ratings and protecting the bank against unexpected events Availability of adequate capital at a reasonable cost so as to enable the bank to expand and achieve low overall cost of capital with appropriate mix of capital elements

The required CAR was to be complied with by the bank by managing its assets more effectively. Various assets including off-balance sheet assets were subject to different risks, and the bank management was required to recognize these different risks to obtain a balanced risk portfolio. The formula of calculating CAR was prescribed by the SBP and included credit and market risks.

Steps Taken to Improve the MCR

Merger with International Housing Finance Limited

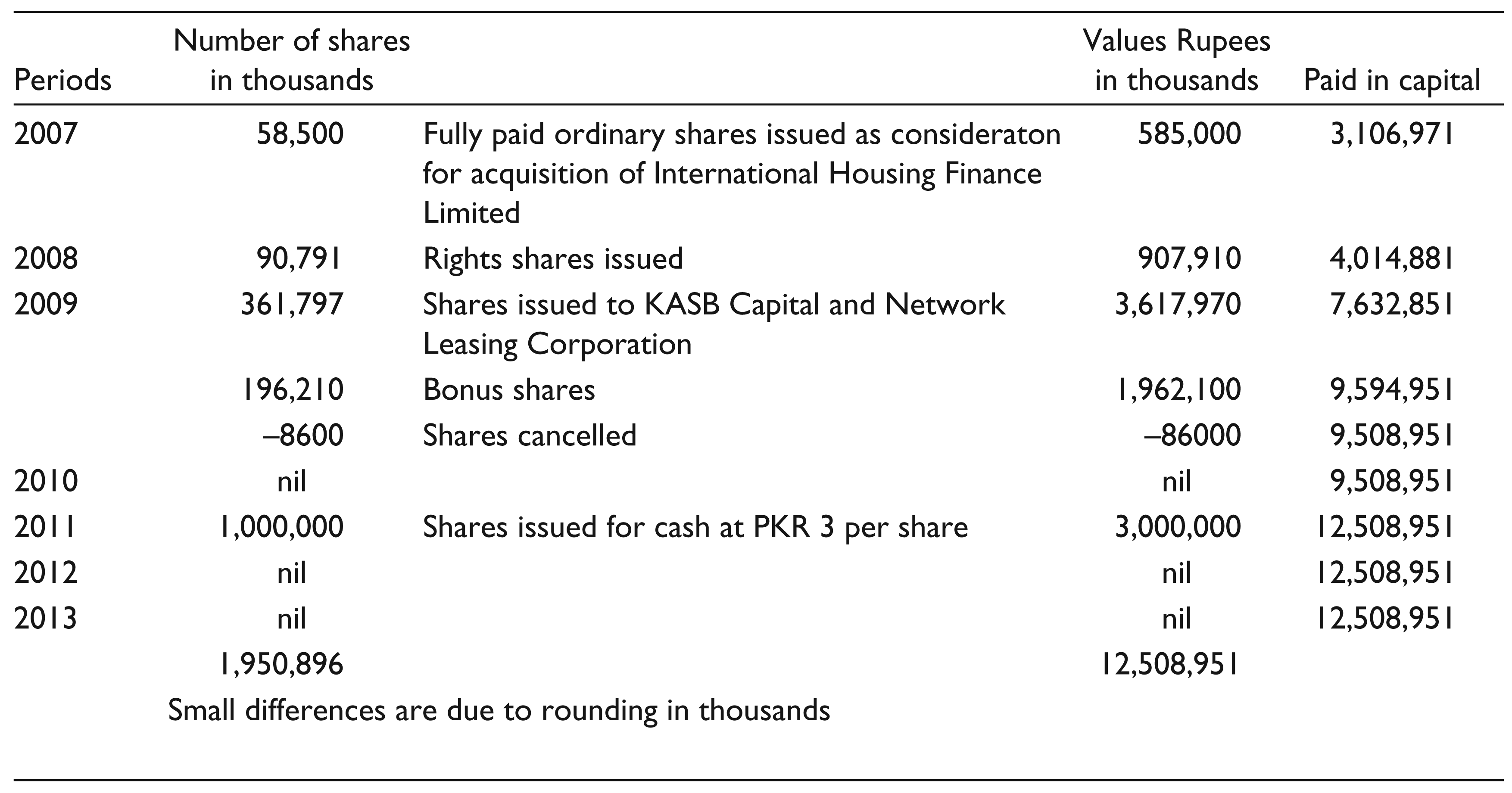

The bank sponsor, Mr Nasir Ali Shah Bukhari, was a major shareholder in a public company called IHFL (KASB Bank Limited, 2007). This company provided mortgage financing in the housing and non-residential sector. The bank was in need of regulatory capital, and during a meeting on 27 October 2006, the bank’s board of directors decided to merge with IHFL. The SBP granted ‘in principle’ approval on 30 October 2007 to the merger. It also granted a period up to 31 March 2007 for the bank to meet the minimum capital of PKR3 billion needed by 31 December 2006. The scheme of amalgamation of IHFL with the bank was a share swap that resulted in additional capital of PKR585 million which raised the bank’s paid in capital to PKR3,106.9 million (see Exhibit 6) on 31 December 2007.

The merger was considered a strategic decision as it was expected to jump-start the business of mortgage finance, a product that the bank management had already approved. The merger added a robust amount of PKR522 million in advances to the existing bank portfolio. After the year ended, 31 December 2007, a rights issue amounting to PKR907.9 million increased the paid in capital to PKR4,014.8 million on 31 December 2008.

Merger with KASB Capital Limited and Network Leasing Company Limited

During 2008, there was a significant restructuring of the KASB Group which involved separating the group’s non-banking financial businesses from the bank. This resulted in the formation of a non-banking financial conglomerate called KASB Capital. The bank invested in 68 million shares of KASB Capital which was 27.5 per cent shareholding of the new entity. As a result of the global financial crisis in 2008, the economic scenario for the banks changed drastically, and the board of directors and management were required to act quickly. The board decided to amalgamate with the two group companies, that is, KCL and NLCL, and the scheme of amalgamation was approved by the SBP (KASB Bank Limited, 2008). KCL and NLCL were both non-banking finance companies and provided investment and lease finance services, respectively. The bank held 27.5 per cent shares of KCL, and KCL held 78.84 per cent of the shares in NLCL.

By 31 December 2008, the bank had also acquired the remaining 72.5 per cent of KCL shares to merge it with the bank. Because of this amalgamation, the bank became the holder of 78.84 per cent of NLCL. It then acquired the remaining 21.16 per cent of shares to merge NLCL into the bank.

After the issue of shares worth PKR3,618 million upon the amalgamation of KCL and NLCL into the bank, the paid-in capital was increased to PKR7,632 million. The bank then recognized a share premium of PKR1,989 million in the bank’s books. The bank’s board of directors later decided on 28 August 2009 to issue bonus shares of 26 ordinary shares for every 100 shares by utilizing the share premium of PKR1,989 million. All the shareholders of KCL and NLCL were also eligible for the shares under the amalgamation agreement. The additional shares were issued in two tranches—first 3,618 million shares were issued as fully paid ordinary shares as the purchase consideration by the bank. The balance of 1,962 million bonus shares was against the share premium recognized on the amalgamation of the KCL and NLCL; this raised the bank’s paid in capital to PKR9,508 million as of 31 December 2009.

Issue of Rights Shares

A rights issue of one billion shares with each share at a discounted price of PKR3 per share was planned by the board, as this would increase the capital by PKR3 billion. Additionally, the bank holding company had planned to augment the capital by issuing subordinated debt up to PKR1,500 million. In 2011, the bank offered the one billion rights shares at PKR3 per share. In accordance with the underwriting agreement, the unsubscribed rights were claimed by KASB Finance Private Limited. The subscription of the rights shares increased the paid-up capital from PKR9,509 to PKR12,509 million (net of discount) as of 31 December 2011 (see Exhibit 6).

Capital Investment by Asia International Financial Limited

By 31 December 2010, due to accumulated losses, the regulatory capital of the bank amounted to a negative of PKR1,078 million, while its CAR stood at negative 2.2 per cent and did not meet the SBP requirements (see Exhibit 4). In view of the continuing deficiency in regulatory capital, the bank’s sponsors entered into an agreement with a foreign investor whereby equity investment was to be made into the bank. In 2010, the KASB Group sponsor, Nasir Ali Shah Bokhari (NASB), introduced a restructuring proposal whereby a Chinese company M/s Asia International Financial Limited (AIFL) would be given 50 per cent shareholding against injection of funds in the group holding company KASB Finance Private Limited (SBP, 2015). The funds were to be used for capital injection into the bank and to purchase certain group companies. Later in 2014, the SBP was informed that the AIFL ownership structure had changed without SBP approval, which violated the SBP regulations; hence, the scheme was rejected.

Management Initiatives

Management had diversified its approach in 2013 and was pursuing new ideas which included converting over 20 branches into business branches (KASB Bank Limited, 2013); this separated these branches from typical branch banking. The objective was to reduce branch losses and serve customers at their doorstep by offering full banking services. There was a new focus on the growth of non-funded income by strengthening existing relationships with exchange companies regarding remittance. The bank reviewed its correspondent banking and cash management services and started offering mobile banking to tap unbanked markets.

The need for expense rationalization was addressed by setting up a central budget control cell and placing a freeze on hiring except staff for new products. There was a new focus on service quality and human resource initiatives such as the following:

Monitoring of service quality Focusing on training and development Recognizing and rewarding people Improving corporate communication Reengineering processes to enhance efficiency

Branch Banking

The bank’s management was aware of the role that technology played in running a large branch network. The volume of transactions was very high and the transaction processing system had to be reliable and efficient. To improve the systems in use, in 2007, the management of KASB Bank decided to upgrade its banking software and implemented the Misys packaged solution (a well-known global banking software). They expected that the software would allow access to information for the purposes of monitoring and provide timely information to business managers. It would also enable the branch staff to offer complex financial solutions.

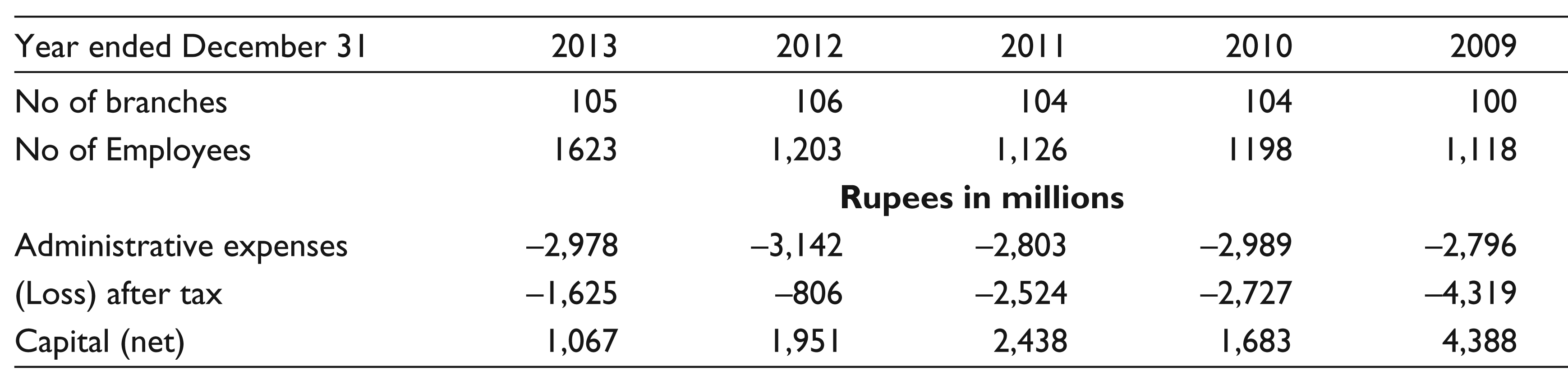

An annual branch expansion plan was required to be submitted to the SBP for approval. The bank’s management delayed submitting its plan for 2009 until the effects of the mergers in 2008 had stabilized. The bank opened 27 new branches towards the end of the third quarter of 2009 so that the network of branches amounted to 100 (see Exhibit 7). The expanded network of 100 branches performed for the first 12 months in the year ending on 31 December 2010 and had a positive impact as the overall cost of deposits declined to a single figure. The bank had 105 branches by 2013, and these continued to generate non-interest bearing deposits that reduced the cost of the bank’s funds.

Future Plan

To address the capital deficiency and financial condition (see Exhibits 8 and 9), the board of directors approved a plan that envisaged the following:

Reshaping the bank through a demerger process by separating core banking assets from the non-core businesses and assets Re-capitalizing the demerged core by either direct equity injection or amalgamation with another bank

The bank’s board of directors had also prepared a forward plan covering the period from 2014 to 2018. However, achieving the results included the following risks:

Maintaining asset quality, retaining customers and meeting forecast net interest margins Raising additional capital as envisaged under the restructuring mentioned earlier Failure in meeting the minimum regulatory capital (the bank was exposed to action by the SBP as the regulator under the banking laws) Assessing the appropriateness of using the going concern as the basis for accounting was also relevant under the risks mentioned previously

Capital Injection Proposal of Cybernaut Investment Group

After filing a writ petition in the Islamabad High Court, KASB Bank’s major shareholder NASB sent a letter in March 2015 to the SBP that they had identified an investor, namely, Cybernaut Investment Group (CIG), and requested for approval to carry out due diligence. The SBP, in response, requested that complete information be provided about the CIG to establish its being a bona fide party and including the arrangement of funds of PKR5 billion. The CIG staff requested to meet the SBP officials, and, at the meeting, they were informed that as per the existing laws, any investor who intended to acquire 5 per cent or more stake in a Pakistani bank was required to establish its fitness and propriety before conducting due diligence. In April 2015, NASB sent a letter to the SBP that Cybernaut had proposed to inject USD 100 million by the end of the year 2015; however, the letter from Cybernaut to SBP only mentioned an amount of USD 50 million. The SBP felt that Cybernaut had not been able to establish its bona fide intention and their request for due diligence was declined.

State Bank Regulatory Action

On 14 November 2014, the central bank, that is, SBP, had placed KASB Bank Limited under a moratorium for six months in order to protect the interests of depositors and other stakeholders. This restrained the bank from payment of certain obligations and debts while it continued to receive all payments/recoveries due to the bank.

The SBP had clarified that offices and branches of KASB Bank would remain open as per routine because the bank’s operations had not been suspended. In a press release on 16 November 2014, the SBP said it had already advised KASB Bank to begin making payments of up to PKR300,000 to its account holders. Consequently, 92.3 per cent of the bank’s depositors would be able to withdraw their total deposits if they so desired. The rest of them would be able to withdraw up to PKR300,000.

The SBP then held discussions with different banks, such as, Allied Bank Limited (ABL), Habib Bank Limited (HBL), Bank AL Habib, Saudi American Bank (SAMBA) and National Bank of Pakistan (NBP), regarding merger or takeover of KASB Bank Limited. However, none of them showed any interest and did not formally approach the SBP for even due diligence due to proscribed Iranian $200 million in the bank, which was subsequently frozen. An official of the SBP added that four banks, that is, JS Bank, Sindh Bank, Askari Bank and Bank Islami, had shown interest in the possible acquisition of KASB Bank. Accordingly, the SBP allowed these banks to conduct due diligence of the defunct bank.

Banks Interested in KASB Bank Limited

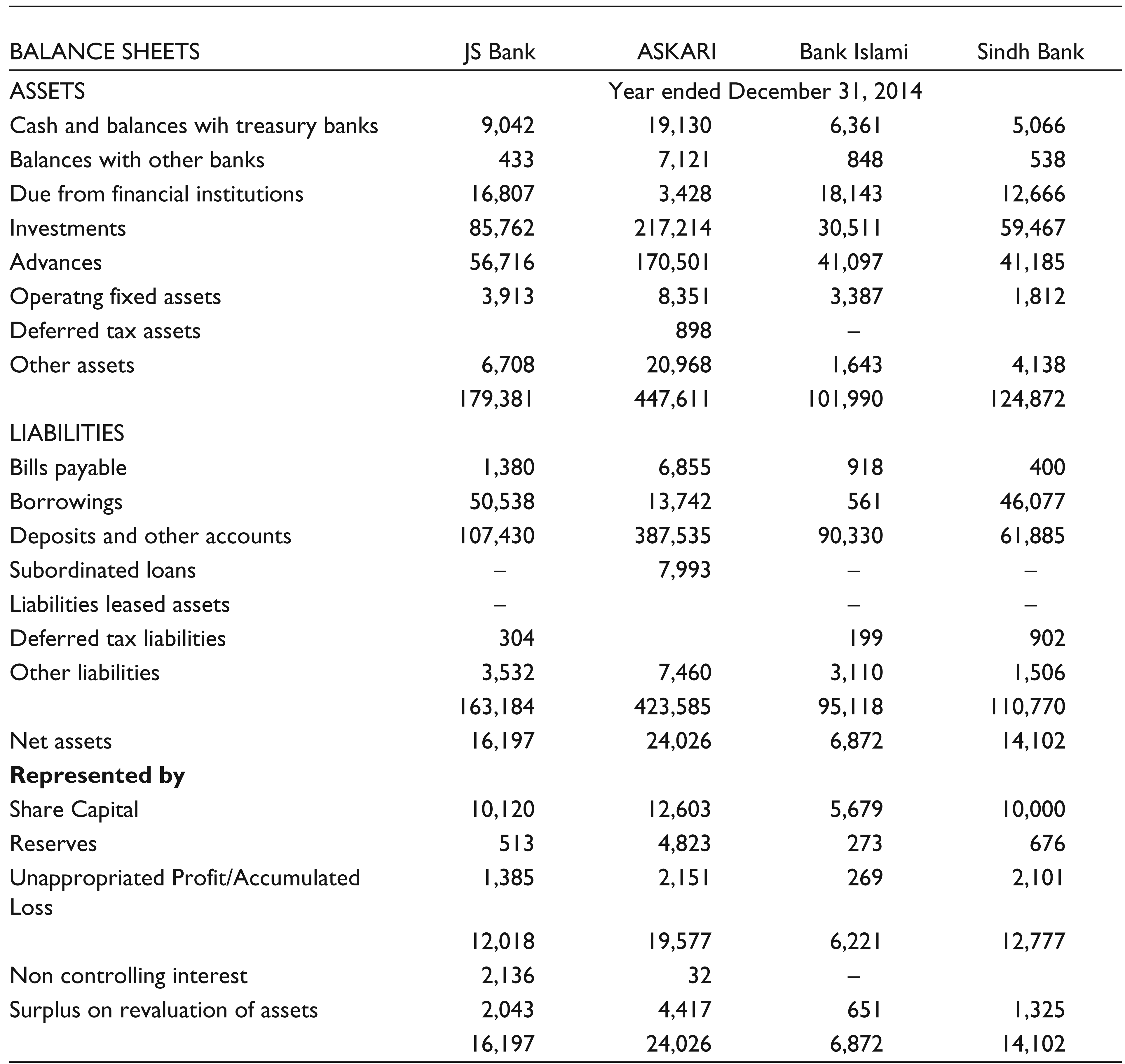

Four banks had responded to the opportunity to conduct due diligence prior to a decision of taking over KASB Bank Limited. Their recent brief results and capital adequacy are discussed here in brief (see Exhibits 10 and 11).

Askari Bank

Askari Bank had been incorporated in 1991 and in 2014, had a network of 321 branches/sub-branches including 53 dedicated Islamic banking branches. It had an equity of PKR23.7 billion on 31 December 2014, an MCR 5 of PKR26.7 billion and CAR 6 of 13.3 per cent.

JS Bank

JS Bank Limited (JSBL) was incorporated on 15 March 2006 and in 2014, it had 238 branches across 122 cities. On 19 February 2014, the bank issued 150 million unlisted, convertible, irredeemable, perpetual, non-cumulative and non-voting preference shares of PKR10 each, which qualified for Tier I capital under Basel III requirement. As a result of this transaction, the paid up capital of the bank had increased by PKR1.5 billion and the bank was in compliance with the MCR prescribed by the SBP. The paid-up capital (free of losses) of the bank as of 31 December 2014 stood at PKR10.119 billion. In addition, the bank was also required to maintain a minimum CAR of 10 per cent of its risk-weighted exposure. The Bank’s CAR as of 31 December 2014 was 16.73 per cent of its RWA.

Sindh Bank

The Sindh Bank had 225 branches in 111 cities and these included 5 dedicated Islamic banking branches. The bank had reported a profit of PKR1.07 billion in 2014 up from PKR665.9 million in 2013. The paid-in capital (free from losses) was PKR10 billion in compliance with the MCR, and the CAR was 22.57 per cent.

Bank Islami

Bank Islami was incorporated in Pakistan under the Companies Ordinance, 1984, as a public limited company on 18 October 2004 to engage in the business of an Islamic commercial bank. The SBP issued a license of a ‘Scheduled Islamic Commercial Bank’ (Bank) and the bank commenced operations from 7 April 2006. It was mainly engaged in corporate, commercial, consumer, retail banking activities and investment activities. Bank Islami had 213 branches at the end of 2014 with total equity of PKR6.2 billion. Its profit after tax for 2014 was PKR313.6 million, up by 69.3 per cent from the preceding year’s earnings.

Bank Islami Capital Adequacy History

Earlier, the SBP circular no. 07, dated 15 April 2009, had increased the MCR for banks to PKR10 billion, which was to be achieved in a phased manner by 31 December 2013. The capital of Bank Islami at the time was below PKR6 billion (see Exhibit 12) that was required to be achieved by the bank before 31 December 2009. In order to meet the requirement of PKR6 billion, the board of directors had decided in their meeting on 7 February 2011 to issue rights shares, but this issue was delayed till 2014.

The SBP, through its various letters, granted extension in time for meeting the MCR of PKR6 billion till 31 March 2013 and required Bank Islami to submit a time-bound capital injection plan to comply with the requirements. In 2013, the board of directors approved a plan for capital injection which was submitted to the SBP. Subsequently, the SBP, in its letter dated 12 March 2014, increased the CAR requirement of the bank to 18 per cent so long as the banks regulatory capital was below PKR6 billion. During 2014, the bank obtained permissions from both the SBP and the Securities Exchange Commission of Pakistan (SECP) to issue 47.9 million shares at a discounted price of PKR8.35, thereby increasing the paid-in capital by PKR400 million (net) to PKR5.68 billion.

In order to meet the next MCR limit of PKR10 billion, the board held a meeting on 29 October 2014 and decided to raise the paid-in capital by a further PKR4.3 billion through a second rights issue. To enable this increase, the bank obtained permissions from the SBP and the SECP. Approval from the SECP was required to grant relaxation from the requirement of Rule 5(i) of the Companies (Issue of Capital Rules) Rules, 1996, which related to the second issue of shares within a year by a company. These approvals were granted by the SBP and SECP vide letters dated 5 November 2014 and 2 December 2014, respectively.

After receiving the two approvals, the board of directors in their meeting on 30 December 2014 approved the issuance of 432,040,000 rights shares to all the shareholders in the ratio of 75.0236 shares for every 100 shares held. This rights issue was fully underwritten, and it would enable the bank to meet the MCR requirement of PKR10 billion by the second quarter of the calendar year 2015. The board of Bank Islami in its meeting on 10 January 2015 approved issuing Tier II capital up to PKR3.5 billion in tranches of PKR500 million.

Due Diligence by Banks

The four banking companies interested in taking over KASB Bank, after conducting due diligence, indicated a possible negative equity gap of around PKR10–12 billion in the bank, in addition to the shortfall of PKR10 billion in capital requirements. After conducting due diligence, apart from Bank Islami, none of the other three banks showed interest in acquiring KASB Bank.

Amalgamation

To protect the lifelong savings of depositors of around PKR57 billion and to protect the jobs of 1,200 employees, as well as to ensure the stability of the financial system as a whole, amalgamation of KASB Bank with and into Bank Islami Pakistan Limited was considered the most appropriate option. Bank Islami was going to take over KASB Bank in line with an amalgamation scheme prepared by the SBP. The SBP’s confidential scheme would result in the acquisition of KASB Bank, the country’s smallest lender, by Bank Islami (see Exhibit 13) at a ‘token nominal value’, according to the statements released by the two banks. Following international practices, the SBP set a notional value of PKR1,000 for the amalgamation. The decision had come as a surprise to bankers and banking experts in the country, who believed that Bank Islami did not even deserve permission to conduct due diligence. They noted that the financial strength of Askari Bank and Sindh Bank was much better comparatively, and they could acquire a troubled bank.

At the end of 2014, Bank Islami was in the process of increasing paid-in capital by issuing rights shares amounting to PKR4.3 billion to cover the shortfall of approximately PKR4 billion in paid-up capital (see Exhibit 12). It had failed to meet the SBP deadline of 31 December 2014 to raise its capital of PKR10 billion despite repeated warnings by the SBP, which had strictly directed banks to comply with the directives of the International Monetary Fund (IMF). Other banks such as Summit Bank and SAMBA had raised their respective paid-up capital before the set date, with the help of the injection of billions of rupees from their investors. The two banks left were KASB Bank and Bank Islami, who could not meet the MCR by the year ended 31 December 2014.

KASB Group at Year Ending 31 December 2013

Moratorium Lifted

The SBP issued a press release on 7 May 2015 informing all the depositors of KASB Bank Limited that the scheme of amalgamation 7 of the bank had been approved by the federal government. KASB Bank had been merged with and into the Bank Islami Pakistan Limited. Accordingly, the moratorium placed on what was previously KASB Bank Limited had been lifted. The depositors of the bank had become depositors of Bank Islami Pakistan Limited, and were free to operate their accounts maintained at the respective branches of the former KASB Bank Limited.

After the merger, the SBP granted PKR20 billion to Bank Islami, consisting of a concessionary loan of PKR5 billion at a low rate of 0.01 per cent and PKR15 billion for temporary liquidity. As there was no competitive bidding for this facility, the market considered that this grant raised transparency issues. Bank Islami, on the first day of its operations after taking over KASB Bank, paid billions of rupees to the depositors. The biggest payment was made to Bahria Town which amounted to PKR2.5 billion.

As Fahim started organizing his report, he first prepared the amount of Tier I regulatory capital available to the KASB bank management from the financial statements so as to arrive at an amount of the shortage. He also wondered what the impact would be on the banking industry as a result of the incorporation of KASB Bank into one of the smallest banks in Pakistan.

Non-performing Loans and Provisions

Financial Performance Summary

Capital Requirements

Regulatory Capital Deductions

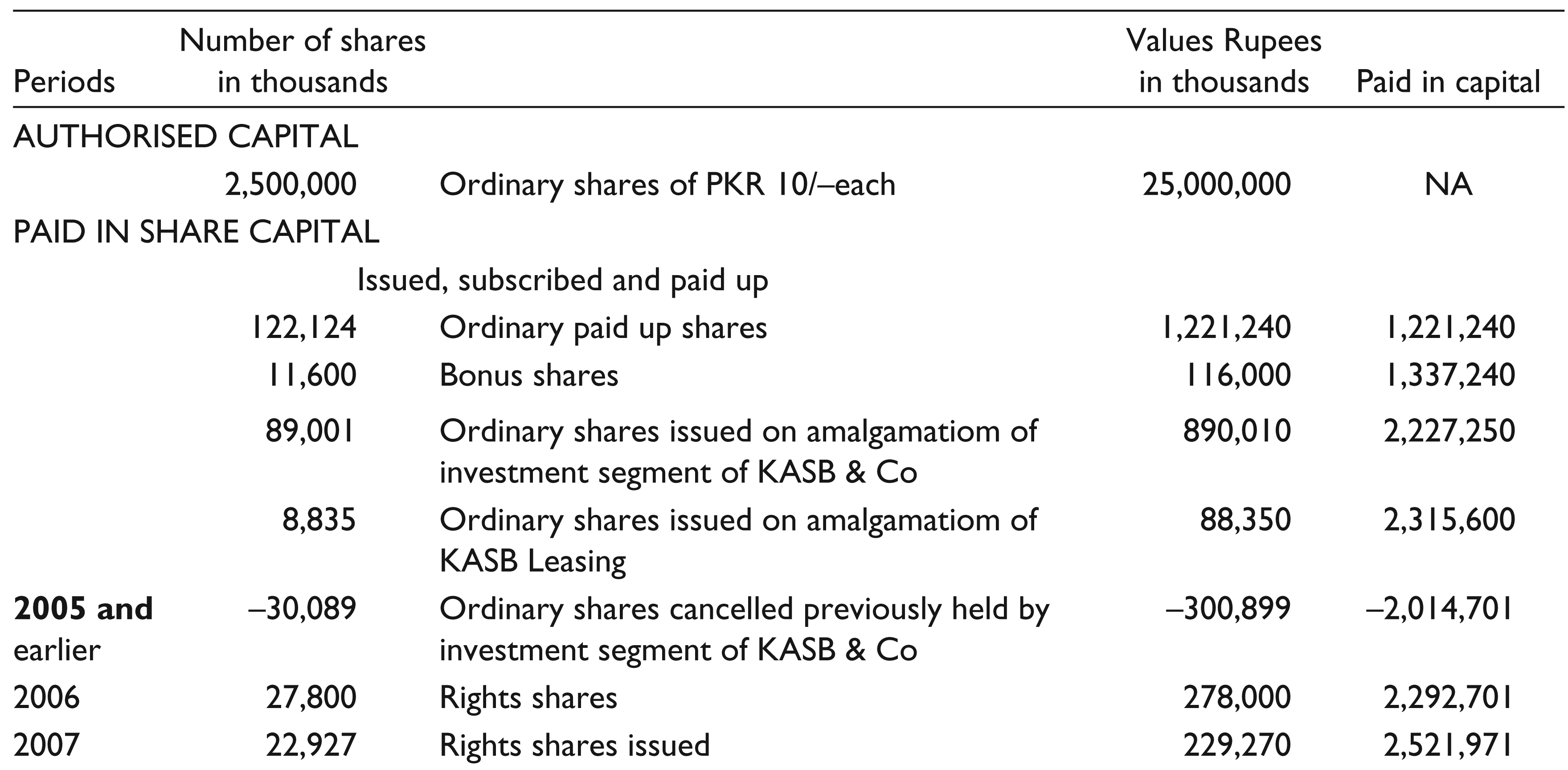

Summary of Various Categories of Shares Issued

Summary of Branches and Employees

Five Year Profit & Loss Accounts

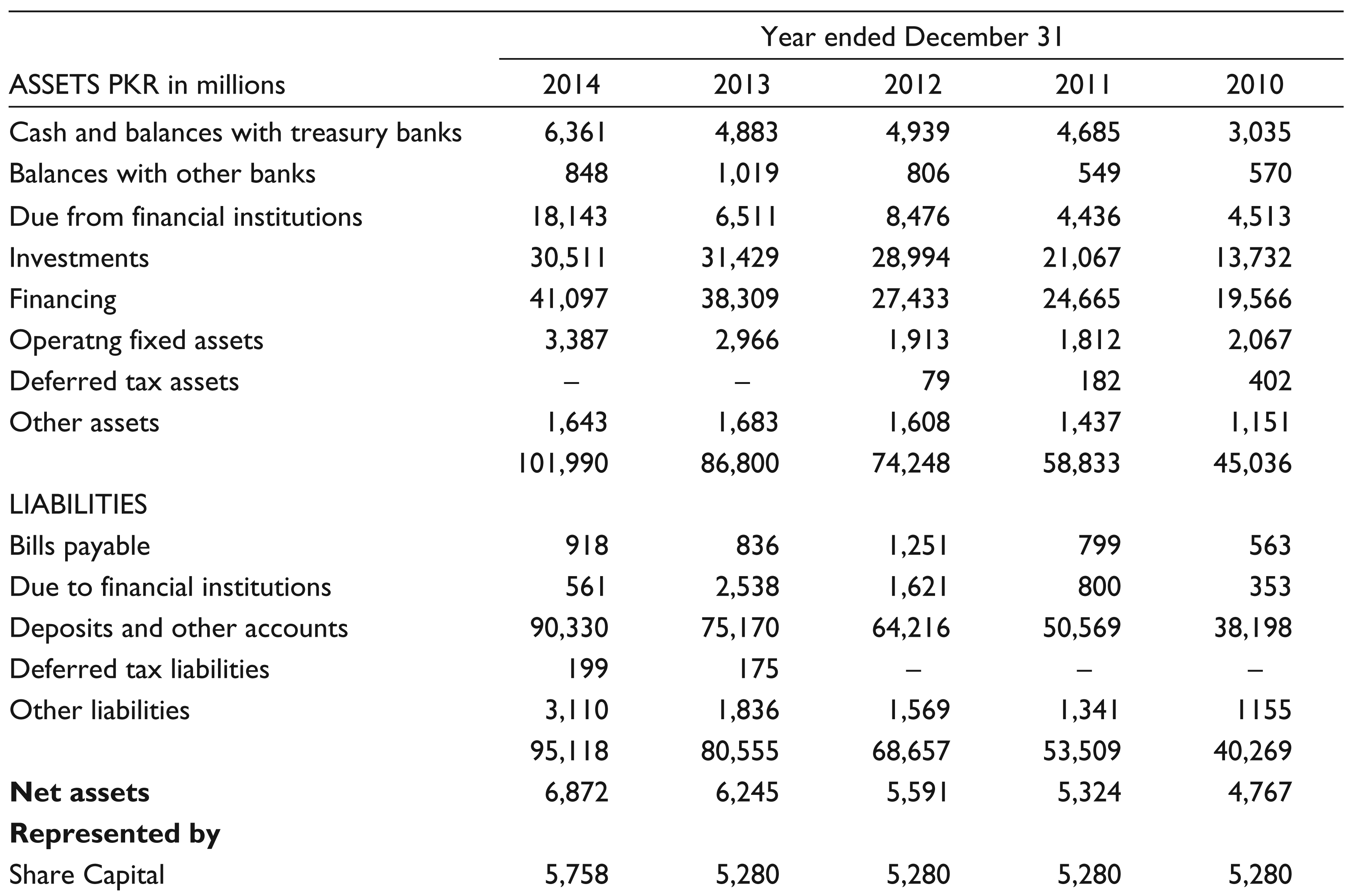

Five Year Balance Sheets

Comparative Financials (Consolidated)

Comparative Financials (Consolidated)

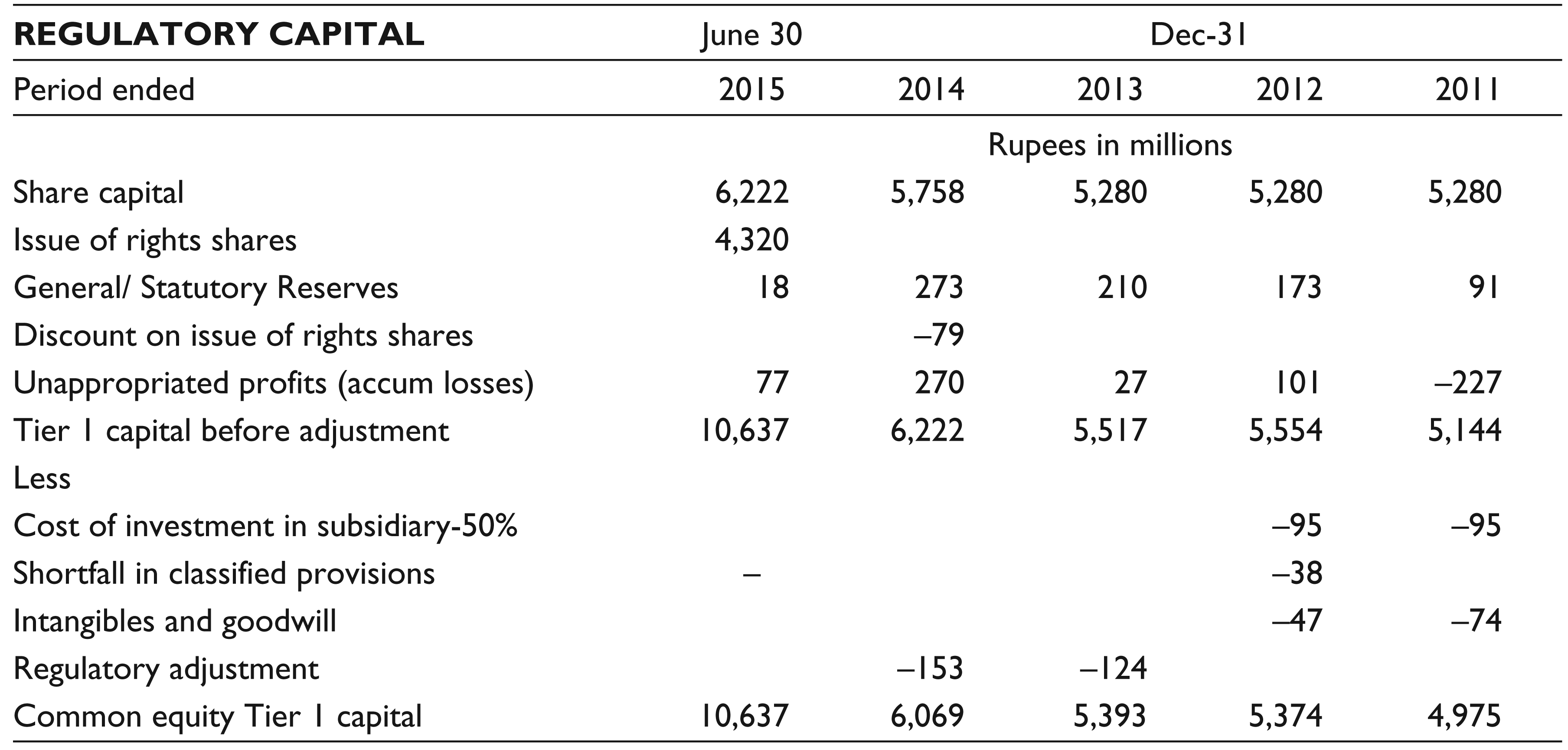

Bank Islami Tier 1 Regulatory Capital

Bank Islami Five Year Financials