Abstract

It was the start of November 2015. Muhammad Ejaz, the CEO of Arif Habib Dolmen REIT Management Limited (AHDRML), was preparing for a presentation to the Board of AHDRML for the following week. The presentation was to recount the story of Dolmen City REIT (DCR), launched a few months back in June 2015, highlighting the regulatory and legal challenges faced during the process and many lingering issues still confronting this nascent sector. Ejaz realized that the group, as a leading player in the sector, had a crucial role to play in lobbying for further changes in the regulation to pave the way for future launches. More importantly, Ejaz wanted a nod from the Board for launch of a different REIT structure in 2016 to capitalize on the immense opportunity in the real estate sector of Pakistan.

Keywords

Introduction

As Ejaz was jotting down notes, memories of this historic journey went through his mind. The satisfaction evident on his face was a reflection of the effort that he and his team had put in over the past several years to achieve something as big as the launch of Pakistan’s first-ever Real Estate Investment Trust (REIT). A copy of the recently published financial statements of the Dolmen City REIT (DCR) was resting on his workstation as he occasionally referred to it to reaffirm some of the factual details for the presentation. His noticeable attention to detail in preparing the presentation was a clear indication of the significance of the upcoming meeting with the Board. Ejaz realized that his presentation could possibly sway the Board’s opinion regarding the future launch of another REIT by the Group in 2016.

Ejaz organized his presentation into different phases, from conception to launch, starting from as early as 2005 when the idea of introducing a REIT Regime in Pakistan was floated by the government, to the eventual initial public offering (IPO) of Pakistan’s first REIT in June 2015. He planned to address the regulatory issues that delayed the launch of REITs in Pakistan and how the regulatory framework evolved over time to pave way for the launch of DCR. While the REIT regulations had significantly evolved over the years, several challenges remained or resurfaced constricting the development of the REIT sector. Ejaz; however, was very optimistic about the future of REITs in Pakistan. As he conceptualized the upcoming presentation, Ejaz reflected on the global trends and developments in REITs to underscore the immense potential in this sector of Pakistan. Exhibit 1 provides an overview of REITs, common REIT structures, Islamic REITs (iREITs) and the historical perspective on the development of REITs.

Pakistan’s Commercial Real Estate Market

Pakistan’s commercial real estate sector 1 had generally remained underdeveloped and failed to attract significant long-term investments because of security concerns and an unstable political environment. Although the situation was unlikely to change dramatically in the short term, significant opportunities existed to expand and modernize Pakistan’s stock of commercial real estate, offering investors high yields and considerable growth potential in the long term. Improved law and order situation could give a significant boost to the commercial real estate sector of Pakistan. In addition, a more favourable regulatory environment for the creation of REITs could further pave the way for increased investment in this sector through pooled funds and provide Pakistani investors a valuable channel to direct their investments into the home market rather than seeking opportunities overseas.

The office properties segment had seen robust demand, offering investors fairly high yields. The retail real estate sector was expected to be supported by a young and increasingly urban population, and with low organized retail segment penetration levels, there was plenty of room for growth. However, generally low-income levels and the preference of many Pakistanis to shop in traditional smaller outlets for grocery purchases had deterred many international retail chains from entering the Pakistani market. Most shopping malls and Western-style retail stores were primarily located in more affluent neighbourhoods in major cities.

The industrial segment of commercial real estate, comprising warehousing and industrial facilities, was likely to get a major boost from improvements in the country’s cargo shipment facilities, by way of port expansions and new rail links, especially due to CPEC (China–Pakistan Economic Corridor), the demand for premium-quality space in industrial zones and growing demand for manufacturing and logistics space.

Arif Habib Group and Dolmen Group Forging a Partnership

AHL had a significant market share in the financial services business. The company provided financing and investment solutions related to equity and debt capital markets, mergers and acquisitions, financial advisory and structured finance. MCB Arif Habib Savings and Investments Limited was a leading asset management company in Pakistan catering to institutional and retail investors.

Pakistan’s first REIT, DCR, was launched by AHDRML. The IPO took place on 12 June 2015 with the stock listed on all three stock exchanges of Pakistan. The successful launch of a REIT in Pakistan was the outcome of a long period of regulatory adjustments by the SECP and concerted efforts made by Arif Habib Group and Dolmen Group.

REIT Regulatory Evolution and Issues

Activities to establish a REIT regulatory regime in Pakistan started in 2005, when Prime Minister Shaukat Aziz showed interest in bringing this global investment vehicle to Pakistan. While the real estate market in Pakistan was growing, the sector remained capital starved. A need was felt to provide finance to this sector through the capital markets and to provide investment opportunities in real estate to small investors. REITs seemed to be a suitable vehicle for these objectives. In an attempt to introduce this instrument in Pakistan, the REIT Regulations 2008 were issued by SECP. However, no REIT could be launched under these regulations which were considered very stringent for the sponsors and fund managers. Ejaz described the situation thus:

REIT Regulations 2008 were not very practical. The minimum fund size required was PKR 5 billion, which was quite large. The regulations also required that the real estate property must be approved by SECP prior to bringing it into the REIT Scheme. This was problematic since public knowledge of strong interest in the property before the transaction was likely to impact the negotiation dynamics and property prices. This requirement was seen by major investment bankers as over-regulation and detrimental to the development of REITs in Pakistan. Due to some of these regulatory and technical issues, the regulatory framework failed to generate sufficient interest of property owners, REIT management and property management companies to establish REITs in Pakistan.

Based on the market response and feedback, SECP amended the REIT regulations in June 2010. Under these amendments, some of the stringent requirements were relaxed for the REIT Management Companies (RMCs). For example, the fund size and capital requirements were reduced. However, many problems still remained. There was a restriction on REITs borrowing, which could hinder their growth. In addition, Ejaz commented:

Under the REIT regulations 2010, 20 per cent of the real estate fund had to be owned by the RMC, effectively making a fund manager a significant investor as well. If a real estate was to be brought into a REIT scheme, payments for it could generally be made either through cash or issuance of REIT units. However, the regulation restricted ownership by any single investor to a maximum of 10 per cent. Hence, a REIT could not issue more than 10 per cent units for any property and payment had to be made mostly in cash. This was another impediment in establishing REITs. It became obvious that an outside property could be brought into a REIT scheme primarily through direct ownership of property.

AHDRML submitted an application under the 2010 amended regulations in an attempt to provide lead in this important catalyst of real estate development in Pakistan. However, a major challenge for the RMC was to offer an attractive yield to excite investors’ interest in the REIT. Recalling his professional experiences, Ejaz observed:

Throughout the world rental REITs yield 150–200 basis points above the five-year government bonds. In the case of Pakistan, the yield on five-year Pakistan Investment Bonds (PIBs) in 20102 was between 12 per cent– 14 per cent. This was a tough benchmark for any rental REIT to meet. For a Developmental REIT, risks were even greater since the project had to be developed first before any income was generated, which under the interest rate scenario would be even less attractive for investors. Hence, this attempt to launch a REIT by Arif Habib-Dolmen did not materialize and in fact no other REIT could be launched in Pakistan even after the regulatory amendments.

Based on the experience and fund managers’ reluctance to launch REITs under the 2010 regulatory framework, SECP repealed the earlier regulations and replaced them with the REIT Regulations 2015. 3 REIT Regulations 2015 brought down the minimum fund size requirement in line with the listing requirement on the stock exchanges. Other regulatory changes provisioned an REIT scheme to be registered before the transfer of property, enabling the REIT to carry out the purchase transaction by issuing units to the seller of the real estate. The RMCs unit-holding requirement was also reduced from 20 per cent to 5 per cent. According to REIT Regulations 2015, an ‘REIT Scheme’ had to be a listed closed-end fund. Mortgage REITs were not allowed. Only equity REITs classified into the following three categories were permitted to fund sponsors: Developmental REIT, Rental REIT and Hybrid REIT.

Ejaz lauded the new regulations as a significant advancement over the previous, and a step in the right direction. However, he noted that there were several areas in the regulatory framework that still required improvement. Ejaz reflected:

For example, there is still a lacuna—minimum 25 per cent of the units must be issued through an IPO. If someone transfers a real estate to the REIT, only 75 per cent of units could be issued to it, remaining consideration (in cash) could be paid after the IPO and it takes about 2–3 months for the process to complete. Another area that required to be revisited by the regulator was the SECP approval requirement before a property could be brought into the REIT. SECP as a regulator should provide the necessary guidelines related to property acquisition, but leave the business decisions to the fund managers—removing the requirement of SECP approval before it could be incorporated in the REIT. In addition, not allowing the use of leverage under the new regulations significantly limited the financing opportunities for REITs.

AHDRML filed the application for the registration of DCR, comprising Dolmen Mall and Harbour Front properties, two premier properties in Karachi’s Clifton area. However, many challenges had to be overcome in launching the first listed REIT in Pakistan.

Other Challenges

During the development of the real estate projects, many challenges emerged for Arif Habib Group and Dolmen Group. The model for the two properties was built-to-rent. Recalling those circumstances, Ejaz said, ‘In our experience, if you develop and sell a plot, after five years the adjacent undeveloped plot’s value would be the same as the developed property, thus reducing incentive for developers’, referring to the steep upward trend in real estate prices in Pakistan. Traditionally, the general preference of small local businesses in Pakistan was to own shops rather than rent them. Even if a business was not very successful, the rise in the real estate price would generate positive returns. Hence, starting a shopping mall and corporate tower based on the rental model, especially on such a large scale, was the first-of-its-kind project involving significant risks. During Dolmen City Mall’s construction there were widespread concerns regarding its commercial viability. The project was a testimony to the two groups’ resolve. The first corporate tenant, Engro, moved into the Harbour Front building in 2008, and rented six out of seventeen floors of the building, while it took five years to fill the remaining eleven floors.

The challenges encountered in launching of the REIT were even more daunting. Transfer taxes that accrued on the transfer of a property to the REIT scheme were quite high, reaching around 5 per cent– 6 per cent of the value of the property. If the property was transferred on the basis of valuation tables, taxes would amount to about PKR 225 million, while if it was transferred on the transaction value basis, taxes would amount to as high as PKR 1 billion, making the transaction unfeasible. To facilitate the launch of DCR, the first REIT Scheme in Pakistan, the government of Sindh approved concessionary tax rates on property transfer to the REIT, which made the transaction feasible.

Another challenge was to inform the public and stimulate investor interest in the REIT units. Traditionally, investor dynamics in the real estate sector and the capital markets of Pakistan were quite different. There were relatively few investors participating in the capital markets compared to the real estate sector, which had a bigger and diverse investor base. REITs; however, blended some of the features of both markets. To offer such an instrument for the first time and attract investors was not easy. The timing of the launch compounded the problems, considering the fact that the yields on risk-free government securities were quite high compared to rental yields. Structuring the offer to yield attractive returns was another challenge. A capitalization rate of 10 per cent was; therefore, used for the valuation of the property based on income capitalization.

As per the regulations, the real estate had to be approved by the SECP which was quite a tedious process. To establish the ownership of the property, SECP required a written confirmation from Karachi Development Authority (KDA), the lessor of the property. It also required a confirmation about whether construction was completed as per requirements of the Sindh Building Control Authority. Apart from this, No Objection Certificate (NOC) from environmental protection agencies and confirmation of the property being encroachment-free were also required. Hence, complying with the regulatory approval requirements made the process long and complex. Since the confirmations were required from government authorities and offices, the approval processes took a long time. In the case of Dolmen City Project, two out of the five buildings were to be acquired under the REIT, which resulted in undivided share of land. This further delayed the approval process.

The Offering of First REIT in Pakistan

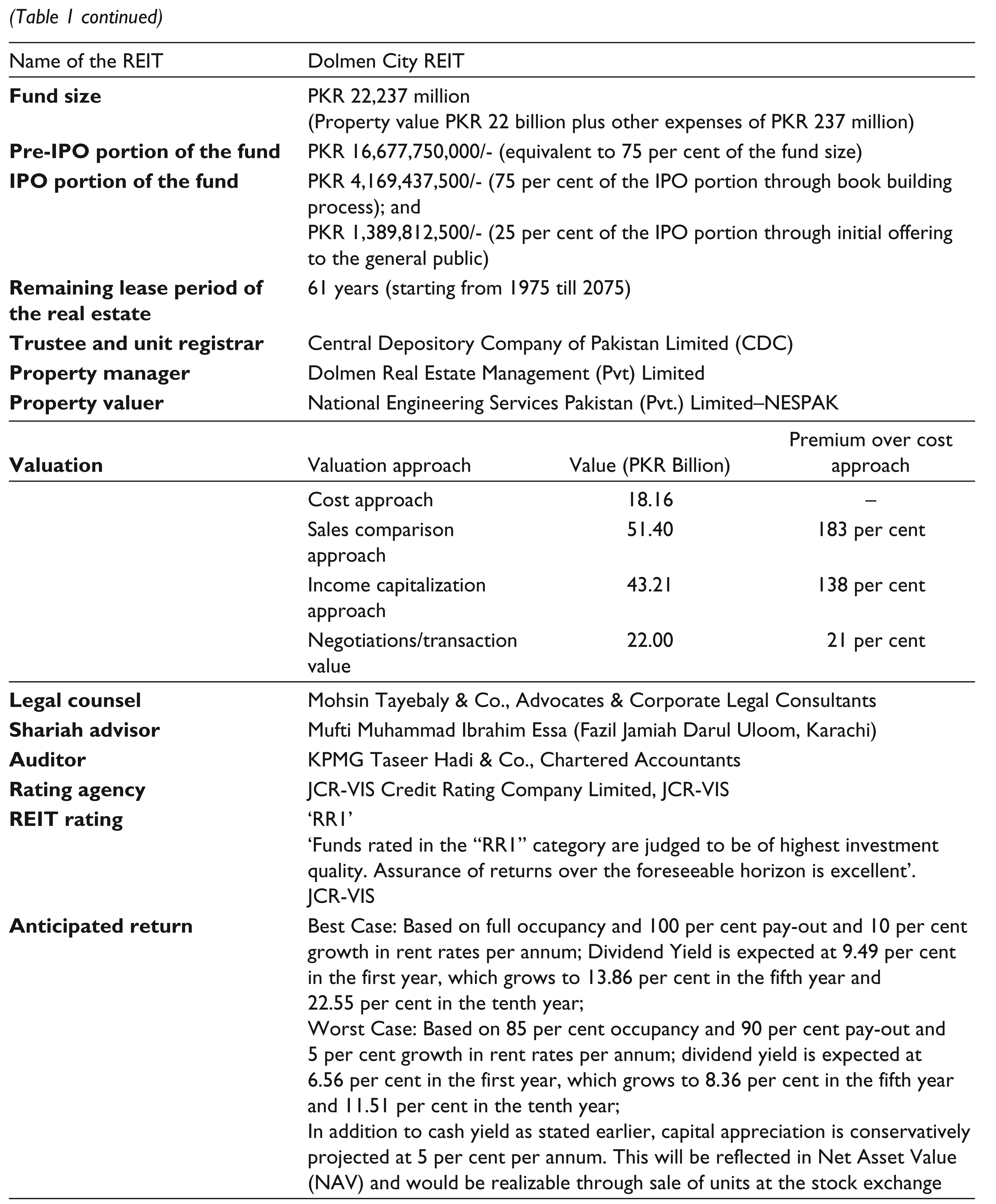

Arif Habib Group had a stake in the Dolmen Mall and Harbour Front through a 20 per cent shareholding in International Complex Projects Limited (ICPL), the original holder of the properties (while the other 80 per cent was with Dolmen Group). The Mall became operational in 2011 and was almost fully occupied by 2014. This raised the Group’s confidence that these state-of-the-art properties would be ideal for a REIT. As a result, Arif Habib Dolmen REIT Management remained committed to the launch of the DCR. One of the impediments to the launch of the REIT earlier was the prevailing high interest rate scenario in the country which made the return on a rental REIT unattractive for investors. The falling interest rates in 2014–2015; however, created a favourable environment for the launch of the REIT. The combined capital market expertise of Arif Habib Group and real estate expertise of Dolmen Group (the property manager) also contributed to investor confidence in the REIT venture.

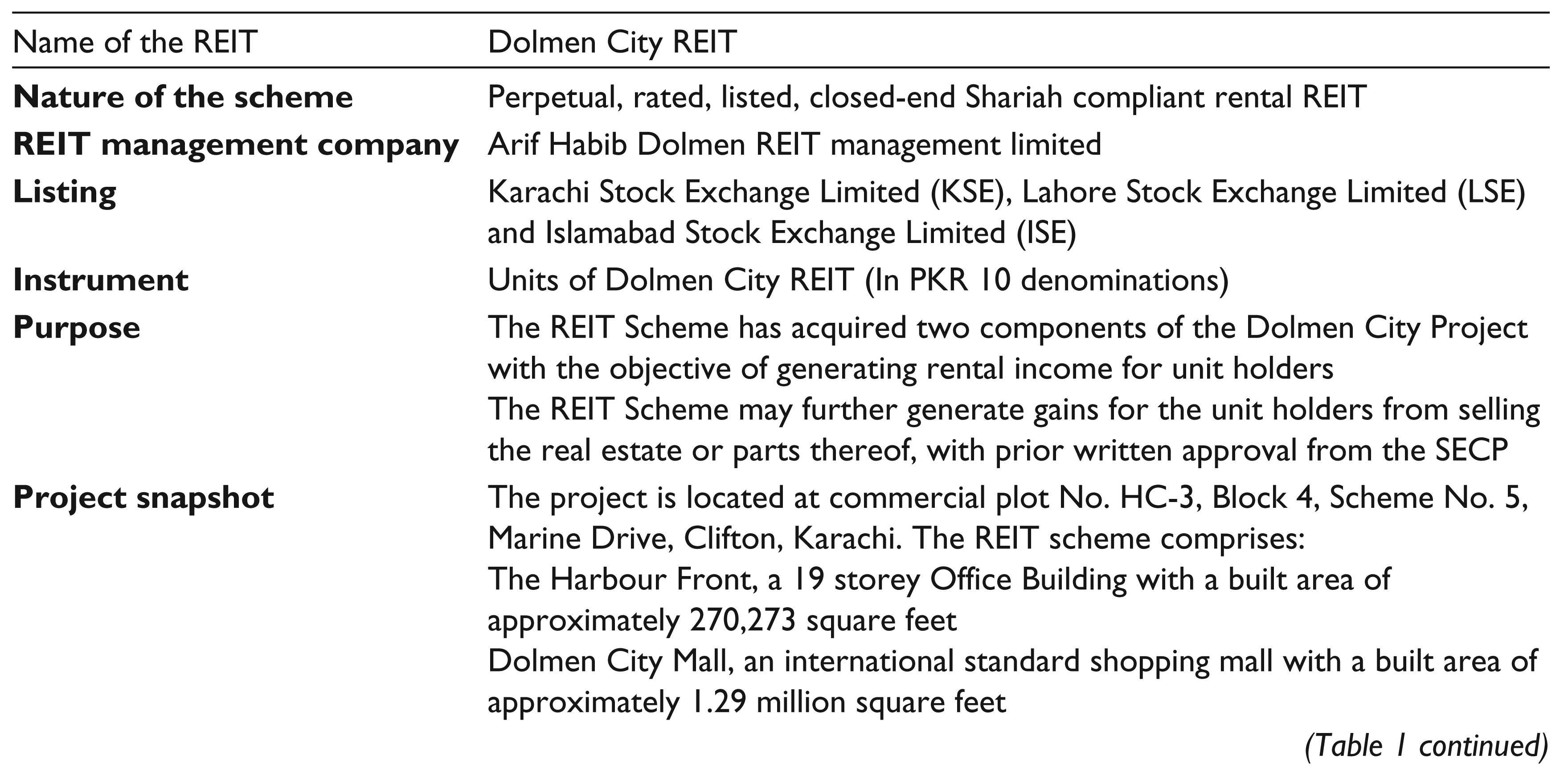

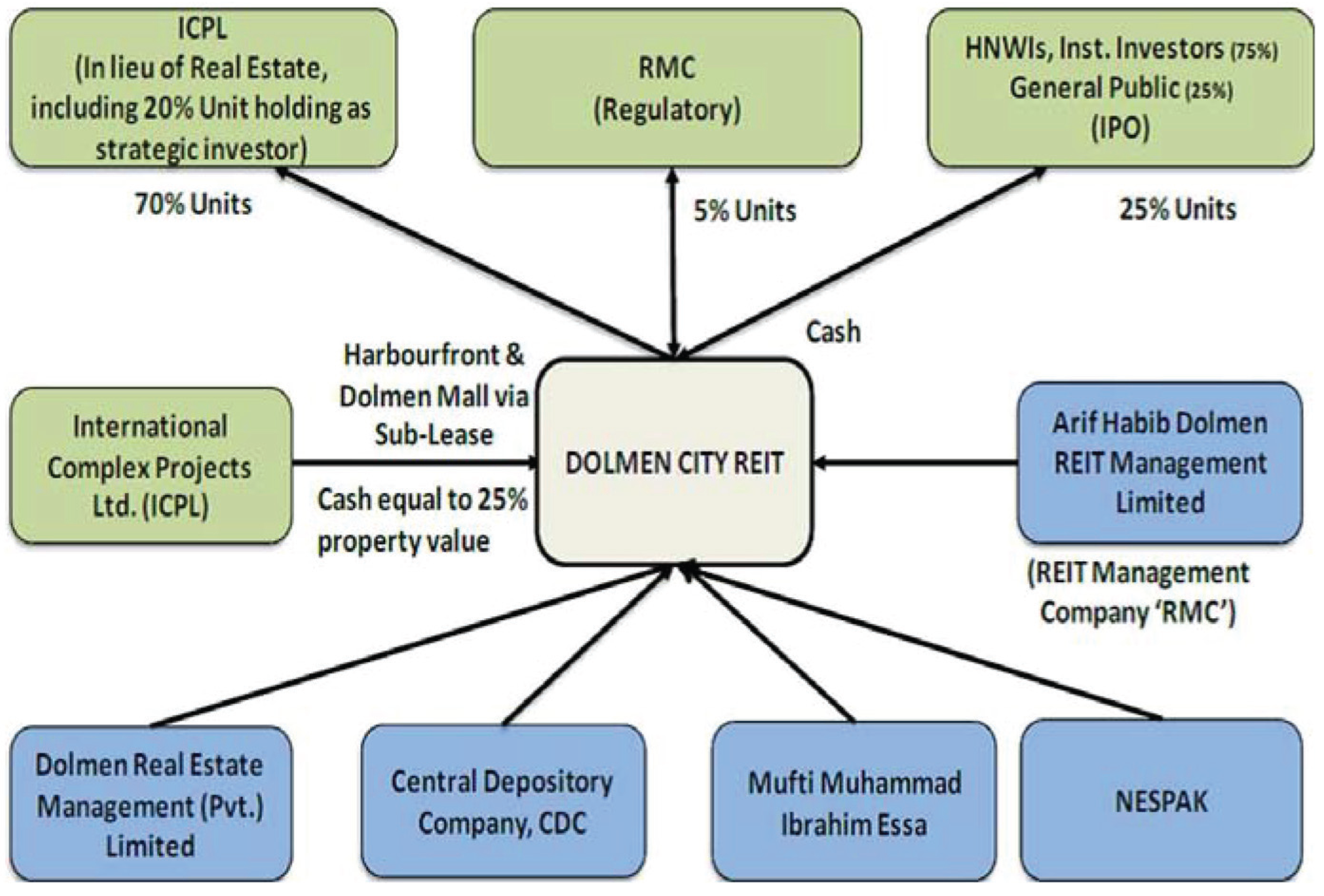

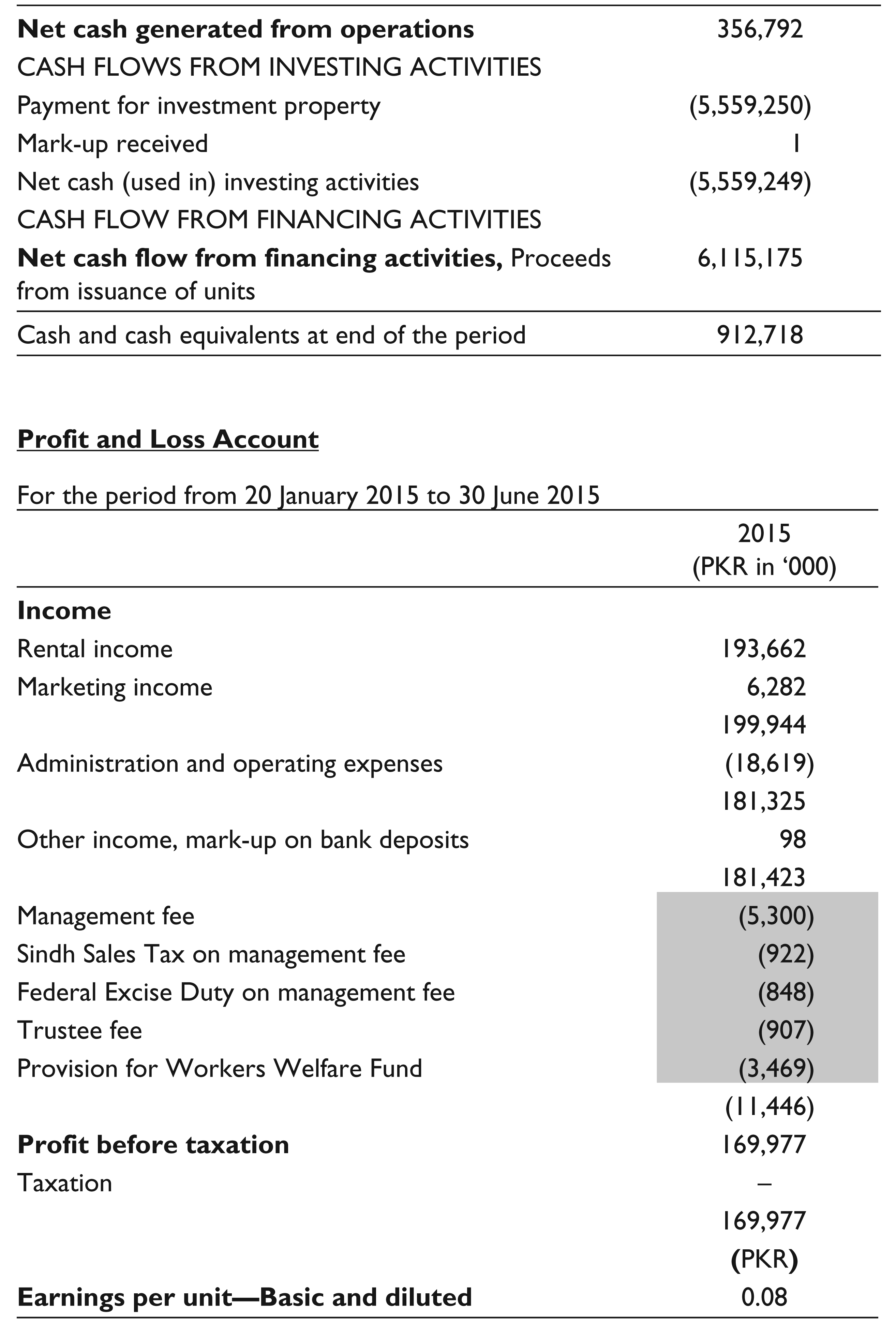

The REIT registration documents were subsequently filed with the SECP and approved in June 2015. The book building and the IPO process commenced in the same month. Limited roadshows were conducted primarily targeting institutional investors who were believed to be major potential investors in the IPO. The book building portion of the IPO of DCR was conducted during 8–9 June 2015. The issue was oversubscribed 1.7 times, resulting in the strike price of PKR 11 per unit. Banks with provisional allocation of 63.7 per cent units were the largest recipients of units in the book building phase. The IPO shares were made available for general public subscription on 12 June 2015. Table 1 shows the factsheet of DCR and Exhibit 2 shows the initial set of financial statements of DCR. Figure 1 shows the structure of DCR REIT.

Factsheet of Dolmen City REIT

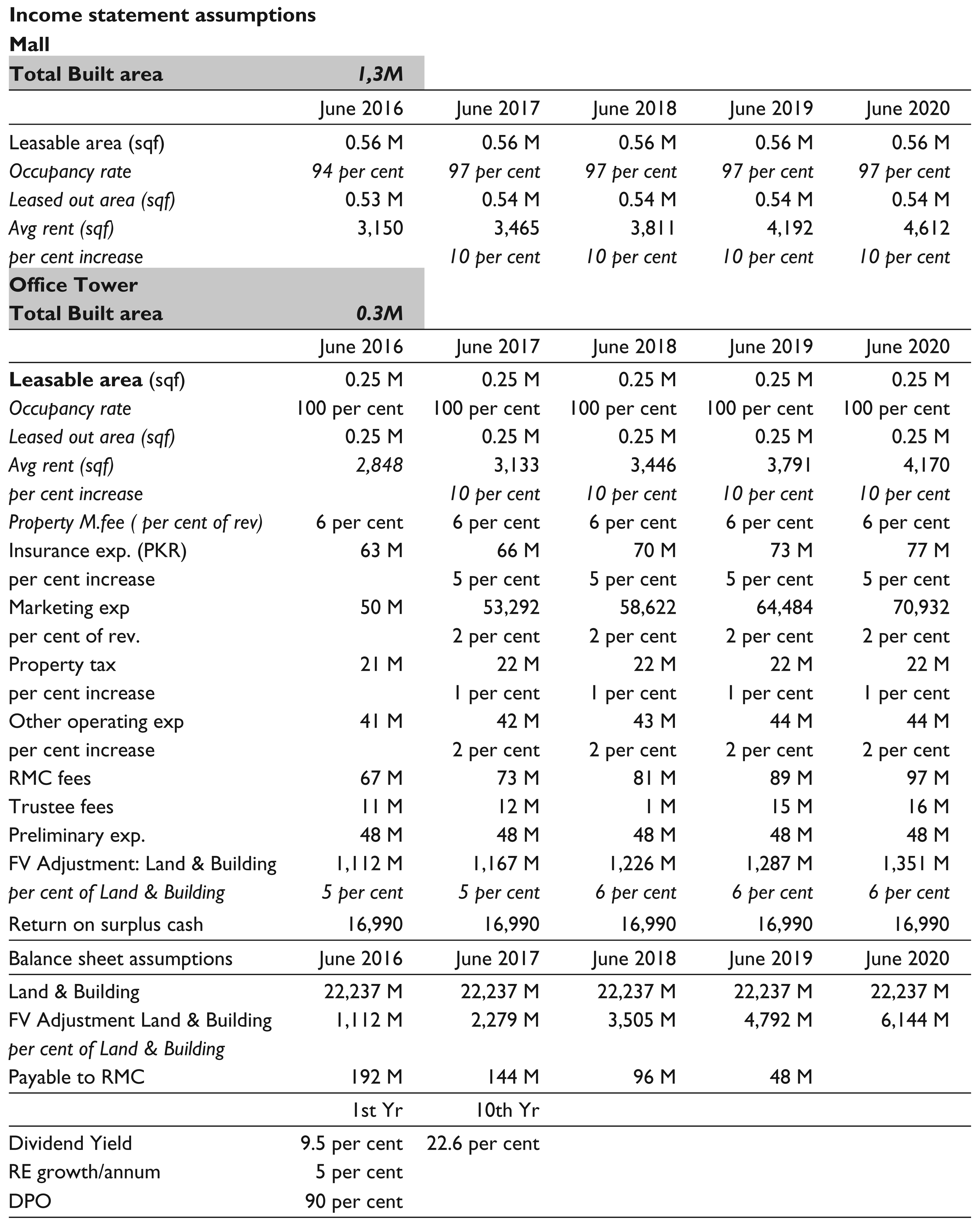

The total fund size was PKR 22.237 billion with property value comprising PKR 22 billion; other expenses accounted for the remaining PKR 237 million. The pre-IPO portion of the fund was PKR 16.677 billion (equivalent to 75 per cent of the fund size), whereas PKR 4.169 billion (75 per cent of the IPO portion) was raised through the book-building process. The remaining PKR 1.389 billion (25 per cent of the IPO portion) was raised through offering to the general public. The expected return on the REIT in the best case scenario was estimated at around 10 per cent per annum. The optimistic scenario assumed full occupancy, 100 per cent pay-out with rent rates growing at 10 per cent per annum. Dividend yield was expected at 9.49 per cent in the first year, which would grow to 13.86 per cent by the fifth year and 22.55 per cent in the tenth year. On the other hand, in the pessimistic scenario, the expected return was based on 85 per cent occupancy, 90 per cent pay-out with rent rates growing at 5 per cent per annum. In the pessimistic case, dividend yield was expected at 6.56 per cent in the first year, which would grow to 8.36 per cent in the fifth year and 11.51 per cent in the tenth year.

The REIT was rated by JCR-VIS as RR1 which represented the highest fund quality. Different valuation models yielded different values for the REIT. The value estimated (in PKR billion) ranged from 18.16, 22, 43.21 and 51.4 based on cost basis, negotiations/transaction value, income capitalization approach and sales comparison approach, respectively. Exhibit 3 presents an outline of two approaches commonly used for the valuation of REITs. Exhibit 4 provides the relevant forecast assumptions useful in the valuation process. The property value assessor of the REIT was National Engineering Services Pakistan (Pvt.) Limited (NESPAK).

Since the launch of DCR, the unit price hovered at around PKR 10, as markets generally came under selling pressure.

The Way Forward

As Ejaz reflected on the experience of the past several years and successful launch of the first rental REIT in Pakistan, he recognized the immense potential for different REIT structures that would appeal to investors in Pakistan. He mused, ‘Unleashing the full potential; however, in Pakistan would require improvement in the REIT regulations and a supportive environment.’ He also deliberated on the impact of high tax rates on property transfer for the future REITs in Pakistan. His compliance team had sent him two new provisions introduced through the Finance Act 2015 which could have an impact on new REIT offerings. These were:

Through addition of second proviso in Clause 99A of Part-1 of the Second Schedule, Income Tax Ordinance, government had limited the exemption of income tax on profit and gains on sale of property to ‘Developmental REITs for Residential purposes’ only till 30 June 2020. This exemption was previously available to all types of REITs till 30 June 2015. Under the Second proviso of Division III of Part-1 of the First Schedule, Income Tax Ordinance, the word ‘REIT Scheme’ was added, making dividend received by a company from a collective investment scheme, REIT Scheme, or a mutual fund other than stock fund be taxed at the rate of 25 per cent, for tax year 2015 and onwards. Also the Division I of Part-III of the First Schedule on Advanced Tax on Dividends had introduced the word ‘REIT Scheme’ together with mutual funds, making dividends received by companies liable to deductions at the rate of 25 per cent.

While Ejaz focused on the regulatory aspects, he asked his research team to prepare a detailed analysis of an alternative REIT structure that would appeal to investors in Pakistan and make economic sense. In addition, he asked the team leader to prepare a preliminary fundraising teaser for the fund sponsors within the next two days so that he could incorporate the relevant analysis and recommendations in his presentation to the Board.

Exhibit 1. Overview of REITs

1.1 REIT Structures

REITs were companies that own or finance income-producing real estate properties. REITs were modelled after closed-end mutual funds and operated under specified guidelines to qualify for REIT status. They facilitated widespread public ownership of commercial real estate and provided investors with the benefits of diversification, regular income streams and long term capital appreciation. REITs usually pay out almost all of their income as dividends to unit holders.

The units of a REIT were traded on stock exchanges like company shares, and provided investors opportunity to own shares in a pool of real estate without purchasing or managing property themselves. REITs were exempted from corporate income taxes, subject to meeting the specified regulatory requirements, and only unit-holders of a REIT pay tax on their dividends. The two main types of REITs found globally were Equity REITs and Mortgage REITs. Equity REITs owned properties and generated regular income primarily through the collection of rent on these properties. Equity REITs market were classified into different property subsectors: rental apartments, offices, malls and shopping centres, storage, industrial facilities, etc. Globally, equity REITS represented a major category of REITs in terms of market capitalization. Broadly, equity REITs can be classified as:

Developmental REIT: A REIT Scheme to develop real estate for industrial, commercial or residential purpose through construction or refurbishment. Rental REIT: A REIT Scheme investing in commercial or residential real estate to generate rental income. Hybrid REIT: A REIT Scheme that had both a portfolio of buildings for rent and property for development.

Mortgage REITs invest in mortgages or mortgage-backed securities tied to commercial and/or residential properties. Regulations in Pakistan did not allow offer of Mortgage REITs till 2018.

1.2 Islamic REITs (iREITs)

In recent years, Shariah Compliant REITs or iREITs had become an important alternative to conventional REITs for investors seeking Shariah compliant exposure to real estate. The unique characteristic of iREITs was that they invest primarily in income-producing Shariah-compliant real estate or in single-purpose companies whose principal assets were Shariah-compliant real estate.

iREITs had started gaining mainstream acceptance as a viable alternate for Shariah compliant investment. Nevertheless, the extent to which iREITs would enter the trillion dollar Islamic Finance industry remained to be seen in the future. An iREIT was unique in that it invests primarily in income-producing, Shariah-compliant real estate and/or single-purpose companies whose principle assets comprise Shariah compliant real estate. The iREIT model was easily comparable to the Ijarah financing (sale and leaseback financing) in Islamic banking and finance. Some guidelines for iREITs issued by Malaysia, one of the major Islamic REIT Regimes, are as follows:

Non-permissible activities must not yield more than 20 per cent of rental incomes iREIT cannot own any property where all tenants run non-permissible activities Shall never accept any new tenants who participate in fully non-permissible activities Non-permissible activities must not acquire more than a fifth of the area. Decisions on non-space utilizing activities must be made using Ijtihad All investment, deposit and financing instruments must comply with Shariah principles. Property insurance must only be based on takaful schemes, unless no such schemes are available.

Rental activities classified as non-permissible are:

Interest (riba) based financial services Gambling/gaming Production or sale of haram products Conventional insurance Shariah non-compliant entertainment activities Manufacture or sale of tobacco-based or related products.

1.3 Historical Perspective on REITs

On 14 September 1960, a legislation was passed in the United States that created the legal framework for REITs, which, for the first time, brought the benefits of commercial real estate investment to all investors—benefits that previously had been available only through financial intermediaries and to high net worth individuals and institutions.

Over time, investors responded to this opportunity and more than five decades after the first listing of REITs on the US stock exchanges, the industry had grown to a $1 trillion market capitalization and nearly $2 trillion in real estate assets as per the National Association of Real Estate Investment Trusts (NAREIT).

REITs had become an investment of choice vehicle for pooled investments in real estate. REITs provided investors with an opportunity to invest in large-scale diversified portfolios of real estate property. REITs gained extensive recognition during the 1990s in the United States when banks and the government used REITs to liquidate non-performing real estate of financial institutions. Widespread acceptance of REITs enhanced real estate markets growth, liquidity and performance over time. Figure 2 shows the rapid growth of the US REIT market between 1971 and 2010.

A REIT was a tax-efficient company that owned income-producing properties. Three main types of REITs in terms of investor access were: publicly listed, non-listed public and unlisted private REITs with limited owners. Publicly listed REITs were the most transparent and visible, whereas unlisted REITs were less transparent. Listed REITs shares were traded on the exchanges like other stocks, whereas unlisted REITs shares were not traded on exchanges and therefore lack liquidity. The key differences in these three categories were in terms of liquidity, transaction costs, management, minimum investment amount, independent directors, investor control, corporate governance, disclosure obligation and performance measurement.

As of 2015, more than thirty-eight countries around the globe had introduced REIT regimes and their widespread acceptance improved the liquidity of investment in real estate. Globally, REIT regulatory requirements varied in terms of the minimum share capital requirement, allowed leverage and minimum profit distribution obligations.

The United States was the largest REIT market measured by market capitalization as of 2015, representing 61 per cent of the global market (Figure 3). The FTSE NAREIT All REITs Index, a market capitalization-weighted index that included all tax-qualified REITs that were listed on the New York Stock Exchange, the American Stock Exchange and NASDAQ had a market capitalization of $890 billion. 4 As of November 2015, 198 REITs traded on the New York Stock Exchange. The twenty-year compound annual total return on the FTSE All REITs Index was 10.41 per cent, compared with 8.91 per cent for S&P 500. In addition, the low correlation of real estate with other asset classes had been a valuable source of portfolio diversification. REITs generally did not have a high leverage; the average debt ratio of the US Equity-only REITs was 32.3 per cent while that for Equity-and-Mortgage REITs was 43.5 per cent, showing low credit risk for these investment vehicles. 5

Figure 4 compares the total return on the FTSE NAREIT All Equity REITs Index, an index comprising top US Equity REITs with the S&P 500 and the Russell 2000 indices, from December 1989 to June 2015. REIT index clearly outperformed the equity indices, with 1,259.12 per cent total return over the period compared to 905.74 per cent for the S&P and 971.63 per cent for the Russell 2000 index.

Source: NAREITs.

Exhibit 2. Financial Statements for 2015

Exhibit 3. Valuation of REITs

The use of traditional valuation metrics was not appropriate for the valuation of REITs. There were; however, two main approaches used in the industry for valuation of REITs: (1) Funds from Operations (FFO) and (2) Net Asset Value (NAV) based approach.

Funds from Operations (FFO) Approach

The Funds from Operations (FFO) is a commonly used metric for the valuation of REITs. FFO is calculated as follows:

Net income computed in accordance with GAAP + Depreciation on real estate + One-time losses on real estate – One-time gains on real estate = Funds from Operations (FFO)

This figure approximated the cash flows from operations. However, one weakness with this measure was that it did not adjust for capital expenditures used to maintain the existing portfolio of properties. As such, FFO did not reflect the true residual cash flows since all expenditures have not been accounted for. The Adjusted-Funds from Operations (AFFO) metric, which deducts capital expenditures for property maintenance from FFO, overcomes the deficiency. Analysts focus on AFFO because it was a better measure of residual cash flows to shareholders and provided a better base number for the estimation of value. These metrics can be used for valuation through Discounted Cash Flow (DCF) as well as in relative valuation methods.

Discounted Cash Flows (DCF). Project the expected stream of AFFO based on growth estimates and discount the cash flows at an appropriate discount rate to determine the present value. The cost of equity capital is typically used for discounting FFO and AFFO cash flows.

AFFO multiple = price/AFFO (benchmarked against industry peers). Other relative measures of valuation were also widely used in practice.

A primary weakness of the AFFO approach was that it did not incorporate property appreciation or depreciation. In periods of falling property values, separating depreciation from the analysis could inflate REIT shares and hide risks posed to investors as a result of falling prices.

Net Asset Value (NAV) Approach

Most analysts use the Net Asset Value (NAV) as a metric for the valuation of REITs. This was calculated as the market value of the assets of a REIT minus the value of all liabilities and divided by the number of units outstanding. The value of the real estate assets was generally calculated by taking the REIT’s forward Net Operating Income (NOI) and dividing it by an appropriate capitalization rate. Then other assets were added to arrive at the market value of assets. A REIT can trade at or below/above NAV; however, in the long run the average discount/premium to NAV for the market has been roughly 0 per cent. The NAV per share is a widely used metric to assess the value of a REIT.

Exhibit 4. Forecast Assumptions

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this case.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this case.