Abstract

The case describes the growth challenges faced by Service Industries Limited (SIL) in the year 2014. There were a number of strategic growth options available to the firm, some related to product diversification and some related to product extension, and SIL had to devise the best plan in order to tap into these strategic growth options.

Since 2011, SIL was continuously on the growth path where its domestic and international sales had increased. This had been made possible through improving virtually every aspect of its value chain as well as activities in the market and product development sides. However, recently, the domestic sector which gave the lion’s share of its sales was undergoing a stagnation, and thus SIL was exploring new avenues of growth in both the domestic and the international markets. These avenues included venturing into tractor tyres and tubes business, auto spare parts business (in which SIL had already embarked) and export business. Each of these growth options had its own peculiarities and implications on various sections of its value chain. This might disturb the very recipe of its internal systems that had given SIL significant growth since 2011 in the first place. Arif Saeed, Managing Director of SIL Tyre and Tube Division had to take steps in a careful and cautious manner in order to further grow.

Keywords

One fine morning of April 2015, Arif Saeed, director for the Tyre and Tube Division at Service Industries Limited (SIL) arrived at his office in Lahore, Pakistan, to discuss the business performance of his division with the management team. The agenda of the meeting was to brainstorm the enablers of its success and the challenges faced ahead in achieving any future growth plans. The business had shown significant growth since 2011, considering the challenging economic conditions of the country but had still missed the targets set by the board of directors. The board had set goals related to growth in sales, exports and newer business lines for the next 5 years.

After receiving a positive response from the markets in Africa, the Far East and Europe, the exports division increased the production of the products in the current line. Arif had to decide how this momentum could be maintained to enter new markets and strengthen its position in the domestic market. The option of entering the agri-tyre business to leverage existing tyre manufacturing and channel capabilities was also under consideration. SIL had recently started manufacturing motorcycle spare parts to supply parts, under the Servis brand name. They were selling to the parts replacement market and motorcycle manufacturers by sourcing completely designed and manufactured spare parts from vendors. Arif wondered how SIL could ensure quality and avoid any negative impact on the SIL brand.

Tyre and tube manufacturing was a capital-intensive business, and high growth rate required investments in equipment to ensure not only larger production capacity and superior quality product but also investment in developing brand recognition. Arif had been able to convince the board to invest in equipment and the brand in the past 8 years. Now Servis was the number one brand in the domestic motorcycle tyre and tube market. The revenue of the tyre division had risen to 7.25 billion in 2014 from 4.2 billion in the year 2011. More recently, the growth in the local motorcycle business had slowed down, whereas the bicycle tyre and tube business was gradually falling.

Arif thought about the various growth options before he went to the meeting. He was not sure which option he should follow at this point in time or did it make more sense to pursue all of them together.

Service Industries Limited 1

The foundation of the Service Group was laid by a group of young college friends 2 who set up Service Industries in 1941 in Lahore as a small-scale business of manufacturing handbags and sports goods. During the Second World War, Service supplied boots to the British Army. In 1953, the friends started a small tannery named Halal Tanneries. Subsequently, in 1954, the group installed a shoe manufacturing plant in the industrial area of Gulberg, Lahore. This plant started production of various types of shoes in the same year. Later, the group shifted the factory from Lahore to Gujrat. In 1959, the group acquired a place for Service Factory Gujrat to set up Pakistan’s first organized shoe factory.

SIL Gujrat was established in 1964. In 1965, they decided to start their own marketing unit rather than base their manufacturing on only contracts. Hence, they made a retail company with the name Service Sales Company (SSC). According to Arif Saeed:

SSC took shops on rent and decided to put a shop of Service parallel to every shop of the multinational brand Bata. Now [in 2015] where there is a Bata shop there is a Service shop.

Between 1968 and 1984, a number of start-ups and acquisitions brought the group’s portfolio of companies to include Service Textiles and other businesses. During 1988–1989, four more factories were started: SIL Muridke, Dar Es Salaam Textile mills, a motorcycle tyre factory located at SIL Gujrat and a gas mask manufacturing factory. Muhammad Hussain and Nazar Muhammad continued to work together in business for more than 70 years. In 2007, SSC grew to have higher sales than Bata and became the largest retail company in Pakistan.

By 2010, SIL flourished; the company was manufacturing shoes, tyres and tubes. It even had rubber production facilities in Gujrat and Muridke. SIL was also the leading exporter of footwear in Pakistan. Similarly, SSC was Pakistan’s leading footwear retailer by revenue and had also diversified into other businesses such as pharmaceutical retailing. SSC had more than 450 retail outlets and a dealer base of more than 2000 in Pakistan.

In 2011, when the group’s ownership and control went to the sons and grandsons of the founders, the owners decided to split the group’s assets into two equal portions so the two families could manage it independently. According to Arif Saeed:

Servis is among the top three big brands of Pakistan. We are superior in shoes and tyre industry and the Servis brand can be used for businesses in other industries as well. Though it took more than seventy years, our elders started from scratch. In 2015, again, we are on the verge of starting new things—for example in the tyre division, the spare parts, tractor tyres, and export businesses. We should learn from our history that our company has the potential to become number one in every field that it operates in.

After the ownership and management was handed over to the next generation, Omar Saeed, Harvard MBA graduate and third-generation family member emerged as the Chief Executive Officer of SIL in March 2011. Prior to leading SIL, Saeed had run SSC as Chief Operating Officer from 2001 to 2010. In 2001, when Omar joined SSC, double-digit growth was a challenge. Omar took up several initiatives. Young managers between 30 and 35 years of age were hired to improve the average manager age of 53 years in 2002. SSC started holding an annual conference to recognize high-achieving employees. SSC adopted the policy of introducing 55 per cent new styles every year as opposed to the traditional mix of 70 per cent old and 30 per cent new. Major changes were made throughout SSC’s supply chain and retail management by launching the project ‘Project Giant Leap’ and engaging an international consulting company. SSC introduced a new format of retail stores called the Shoe Planet, where SSC displayed its own collection as well as shoes from different brands. As a result, in 2009, SSC opened a shoe store every week leading to 24 per cent annual growth in SSC’s business.

After joining SIL in 2011, Omar decided to arrange a 3-day exercise for the senior management of SIL to mutually create and set the goals for SIL’s leadership for the next 3 years. SIL sent forty senior managers to Murree (a hill station) for a 3-day exercise facilitated by a consultant who came up with a set of objectives and action plans to achieve them. The following goals were set by the end of the 3-day activity, and they were to be achieved by SIL in the next 3 years:

Tyre division sale to increase from PKR5 billion to PKR11 billion, Shoe division exports to increase from PKR2 billion to PKR7 billion, Shoe division domestic sale to increase from PKR3.8 billion to PKR7 billion.

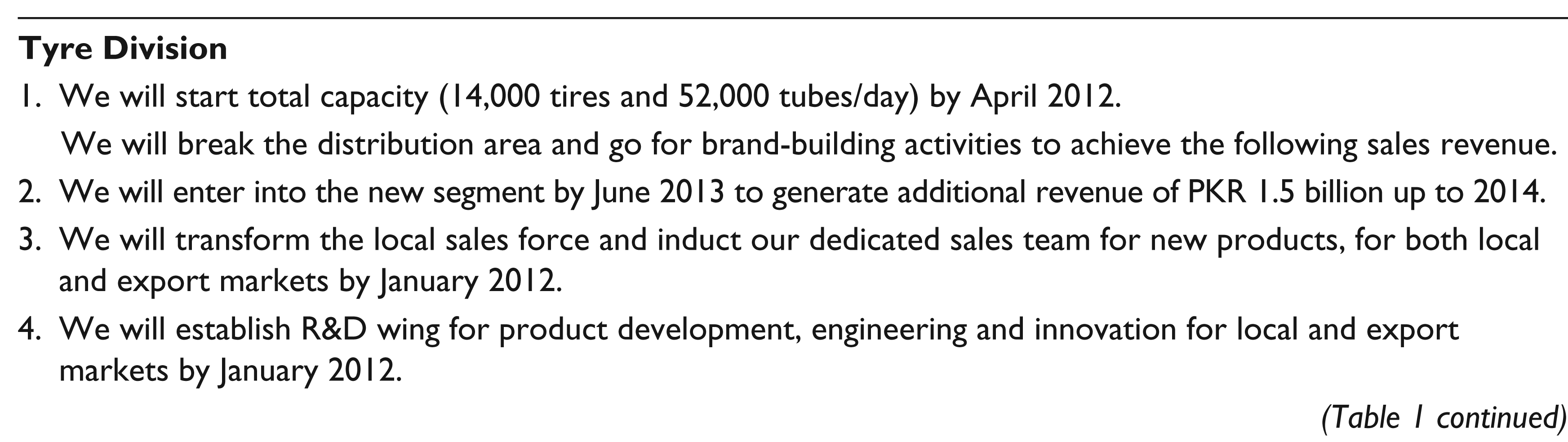

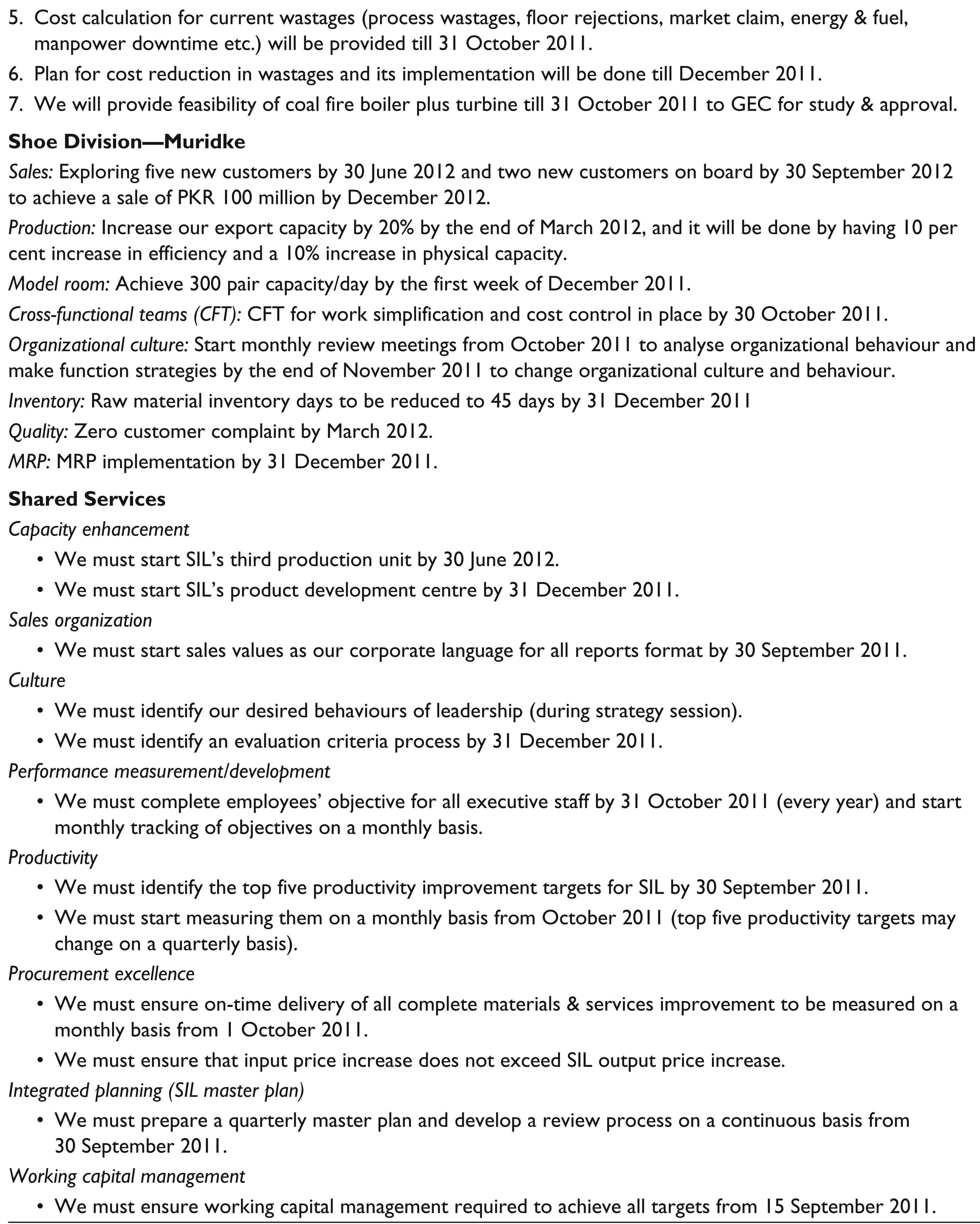

It was also decided that in order to achieve these targets a number of new initiatives would be undertaken. Table 1 provides details of the initiatives along with specific targets in different areas.

Interventions to be Taken for Achieving Targets Set in 2011

Four Years Later: A Snapshot of Service Industries Limited in 2015

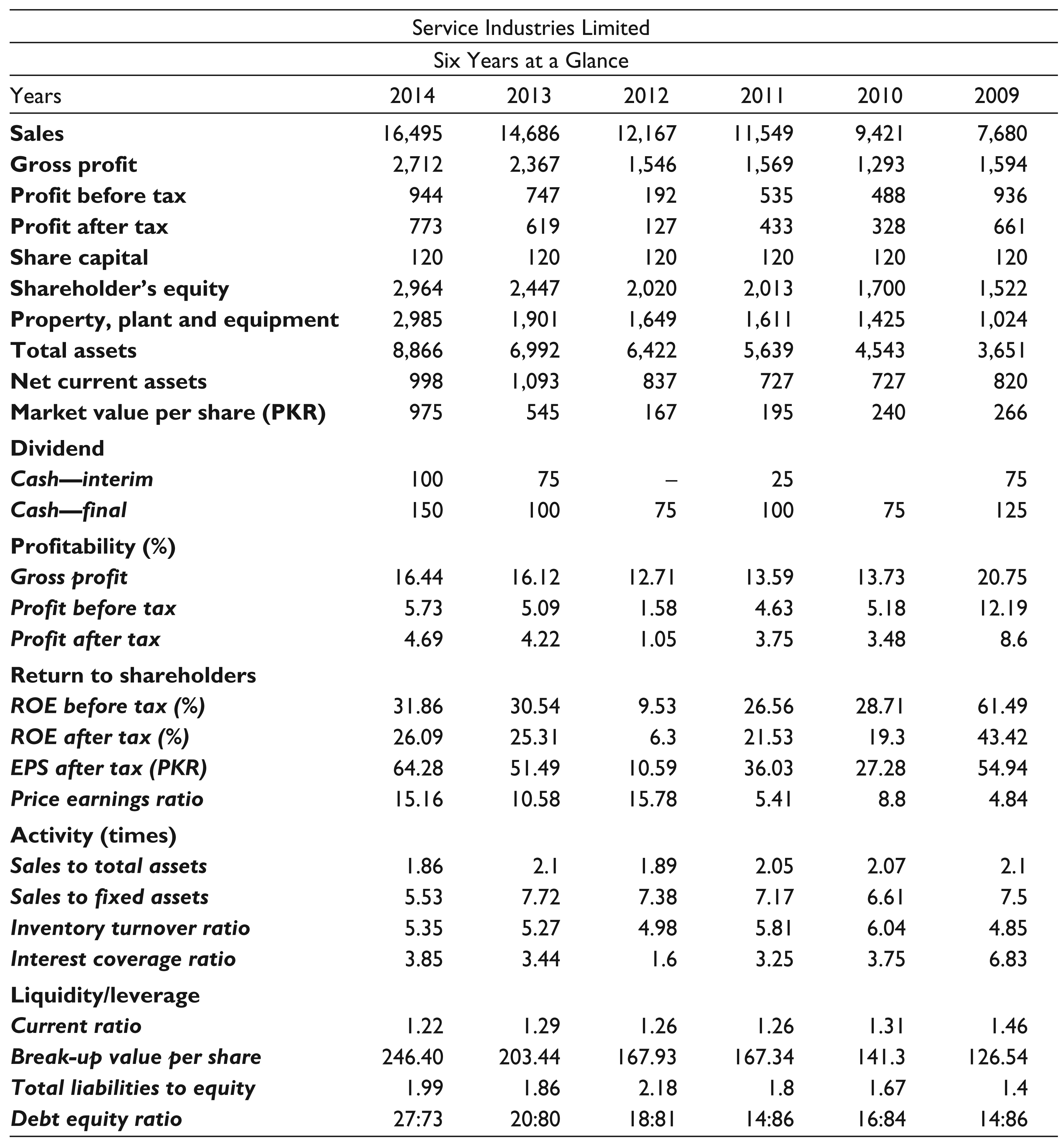

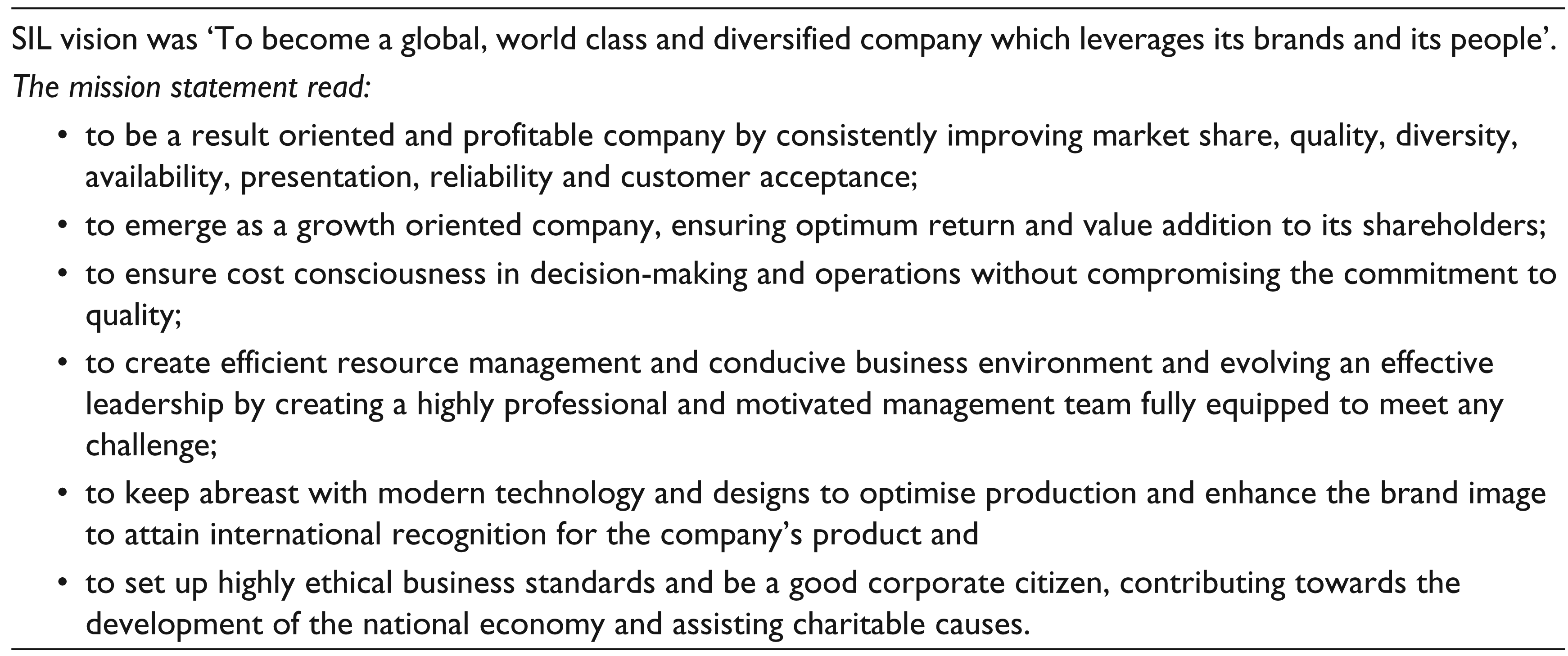

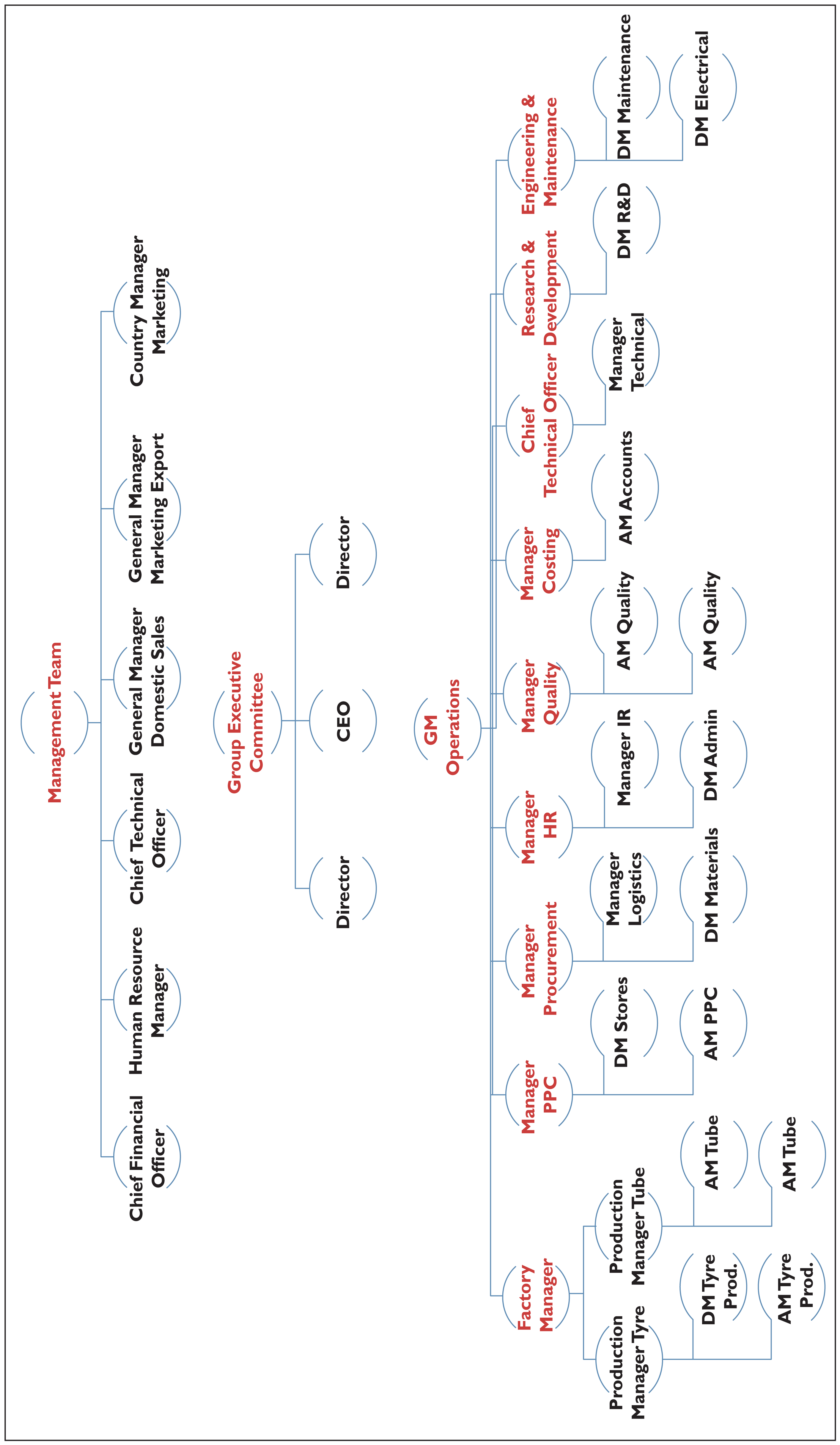

SIL, a public limited company listed in the Pakistan Stock Exchange, was Pakistan’s premium footwear manufacturer and exporter. It generated annual revenues of about PKR 16.5 billion (company financials are available in Tables 2a–2c) and was the largest manufacturer of footwear, tyres and tubes for two-wheelers and had also been the largest footwear exporter in the country for the last 10 years. The company employed more than 8,764 people in the facilities located in Gujrat and Muridke and exported its products to many destinations around the world. With a strong emphasis on product quality and innovation, SIL had built both domestic and international recognition. SIL’s vision and mission statements and organization chart are provided in Table 3 and Figure 1, respectively.

Six-Year Financials

Profit and Loss for Tyre Division

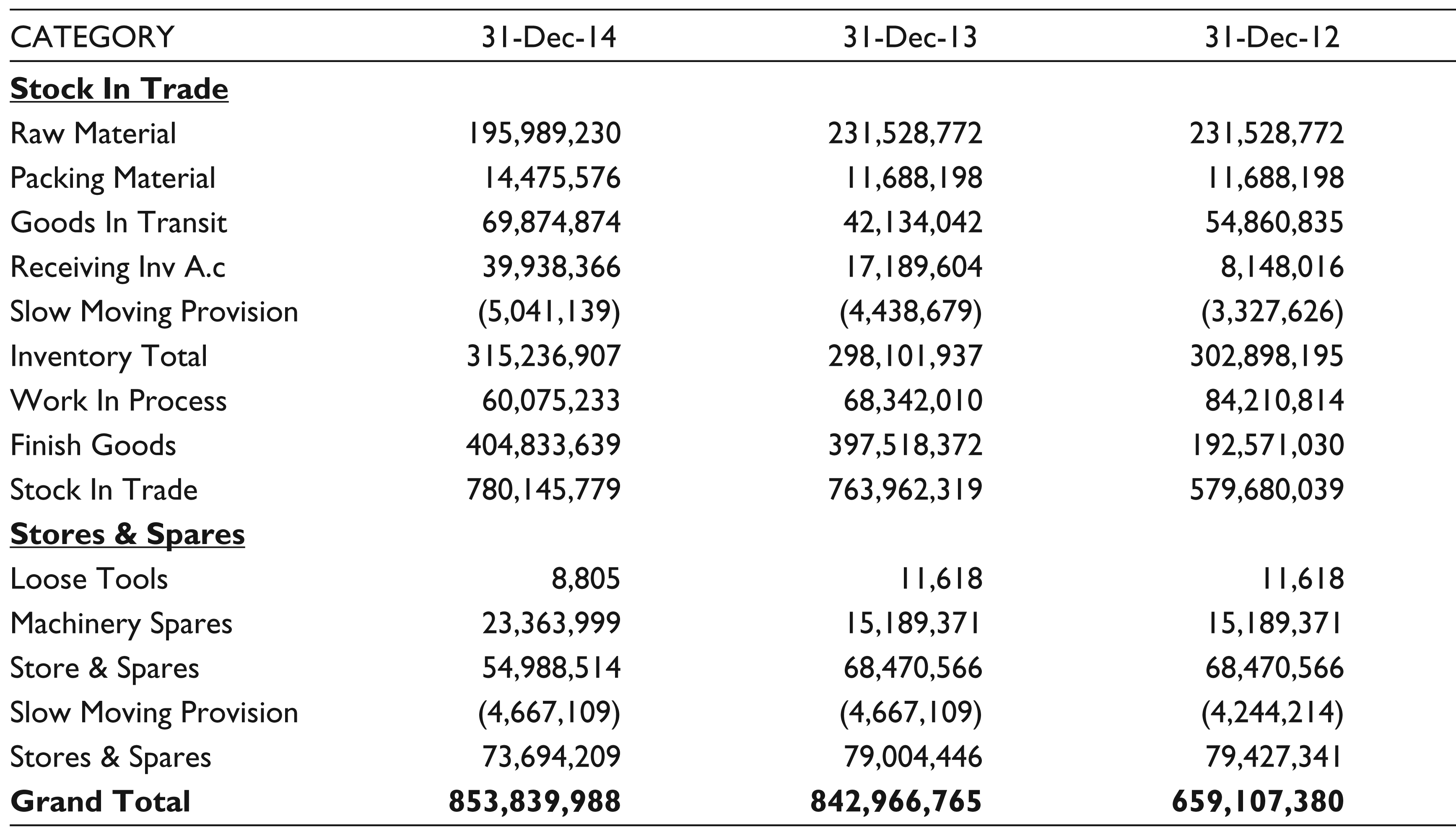

Stock in Trade as on

Shoe Division

SIL’s shoe division was the largest footwear exporter in the country. Annual revenues of the shoe division exceeded PKR 8.3 billion of which 45 per cent came from exports primarily to EU countries—namely, Germany, France and Italy. SIL’s in-house manufacturing covered all aspects of the shoe manufacturing value chain. The Gujrat plant manufactured shoes mainly for the local market (80% production by volume for the local market), and the Muridke plant manufactured mainly for the international market (80% production by volume for international market). Over time, SIL had developed a niche in the female footwear market. A total of 80 per cent of its exports comprised female footwear.

SIL’s Vision and Mission Statements

Tyre Division

SIL’s tyre division mainly produced tyres and tubes for motorcycles, bicycles and rickshaws. The tyre division reported revenues of PKR 7.3 billion in 2014, with an average growth rate of about 14 per cent in the last 3 years, and employed a workforce of about 2,500 employees. In the last 4 years, SIL had become the market leader in the tyre and tube business and a holder of majority market share of about 42 per cent. In addition, SIL was a major supplier of tyres and tubes to OEMs of motorcycles including Honda and Yamaha and other local motorcycle assemblers in Pakistan.

Tyre and Tube Business Value Chain

Research and Development

Design and development of tyres was a complex process and required considerations in tyre design and its subsequent development. The success of a tyre was measured in terms of its performance parameters of abrasion resistance, 3 wobbling and road grip, 4 which in turn depended upon tyre design and its formulation. Tyre design determined its shape according to established international standards. Besides, a tyre had to be produced in the most economical manner (because of the commodity nature of the product). For this purpose, an economic analysis of the tyre was essential that considered factors such as disposition of material in the tyre, bead wire construction, tyre construction, material composition and selection (these terms will be elaborated on in the tyre production section) as well as market claims.

In the past few years, the R&D process had formalized at SIL, and a number of new testing equipment had also been added. The R&D team underwent a few trainings, too. Abdul Qayyum, Manager R&D, had over 15 years of work experience in R&D of tube and tyre sector, especially mould making. He had been associated with SIL for 6 years, and his addition to the R&D team was good for the company. Under his supervision, they launched new product designs and improved product features like road grip, traction and product life. Qayyum reported directly to the tyre division GM.

The R&D department followed the tyre design standards of brands like JATMA 5 and ETRTO 6 to ensure good product quality and latest design features in Servis tyre and tube product range for the local and the export market. In the case of market claims, R&D would analyse the returned product to determine the root cause of a problem and introduce changes in the design or the production process in order to prevent the same problem from reoccurring in the future.

The R&D department had the latest testing lab but did not have prototyping equipment and they were, therefore, dependent on the production plant for testing and validation of the new developments. At the same time, fundamental R&D in tyre design and engineering was absent, and most tyre developments were being carried out by a hit and trial method. In 2015, R&D housed three full-time employees including Qayyum. The R&D staff was being trained on the job. Qayyum reflected on the competition in the international market:

In the export market, if our tyre price is at $13, China will be able to produce the same tyre at $12. Similarly, MRF tyres—an Indian brand has better dimensions and quality than our tyres; however, ours is probably slightly cheaper. If we want to improve our tyre, my only resolution would be the continuous training of the R&D staff. Besides, an exposure of international firms will help them develop an understanding of how things need to be done and help create mental benchmarks.

Technical

The role of the technical department included: (a) testing of materials at various stages of the production process, raw materials, work in process and finished goods and (b) development of new material formulations (or compositions) for different applications. In order to carry out the physical testing of goods or materials, the technical department was equipped with state-of-the-art testing equipment.

7

Mr Ghazanfar who was head of the technical department proudly mentioned his involvement in the development of rubber pads for the chains of Al-Khalid tank. He recalled:

These rubber pads had to be subjected to the toughest road conditions—very high road friction, uneven surfaces, high load, and required significantly high abrasive, tensile and fracture strengths. We were able to successfully develop the pads, and SIL produced and supplied these pads to the Pakistan Army.

Ghazanfar received his undergraduate degree from the University of North London. He had two engineers in his team and on average the department had more than 30 years of work experience. The role of the technical department in the tyre design was to determine the number of nylon plies, their direction and the angle, as well as control on ash content, specific gravity and abrasion resistance. The specific gravity, in turn, was controlled by adjusting the quantity of carbon and other materials in the rubber compound. These materials had different costs and different specific gravities of their own which made a tyre bulky or light. A blend of these materials would result in desired specific gravity and cost targets in an application.

Ghazanfar recalled an instant when the management gave him a target of reducing tyre cost by PKR 5 million per month. He reflected:

When we accepted this challenge, we made an analysis of high cost materials within the tyre. We made several changes in the material formulation and achieved the cost reduction targets. This was not possible if we did not have an in-depth understanding of the chemistry of the materials and testing equipment. Other organizations do have engineers and specialists as well but they do not think to the extent we think.

Ghazanfar also commented on the improvements needed in his department:

There is a need for teamwork in the department. If an individual knows something, he tends to hesitate telling it to others. People do not trust each other; however, the development work requires sharing and bouncing ideas within the team in order to develop a better understanding and reach a decision quickly. We are facing scalability and sustainability issues, and in order to address these, staff members need to be trained—two people should go for a year-long training program to learn rubber technology.

According to the General Manager (GM) of the tyre plant Mr Cheema:

Our technical department can make changes in formulations and in curing parameters in order to adjust for slight changes in raw materials.

Production

The tyre and tube plant had two sections, one for producing tyres and tubes for two-, three- and four-wheeler automobiles (motorcycles, auto rickshaw, wheelbarrows and light trucks) and another for producing tyres and tubes for bicycles. Each section was divided into two lines, one for tyre manufacturing and the other for tubes. The auto tyre section had a production capacity of 24,500 tyres a day and 80,000 tubes per day. Both production lines were operating at full capacity.

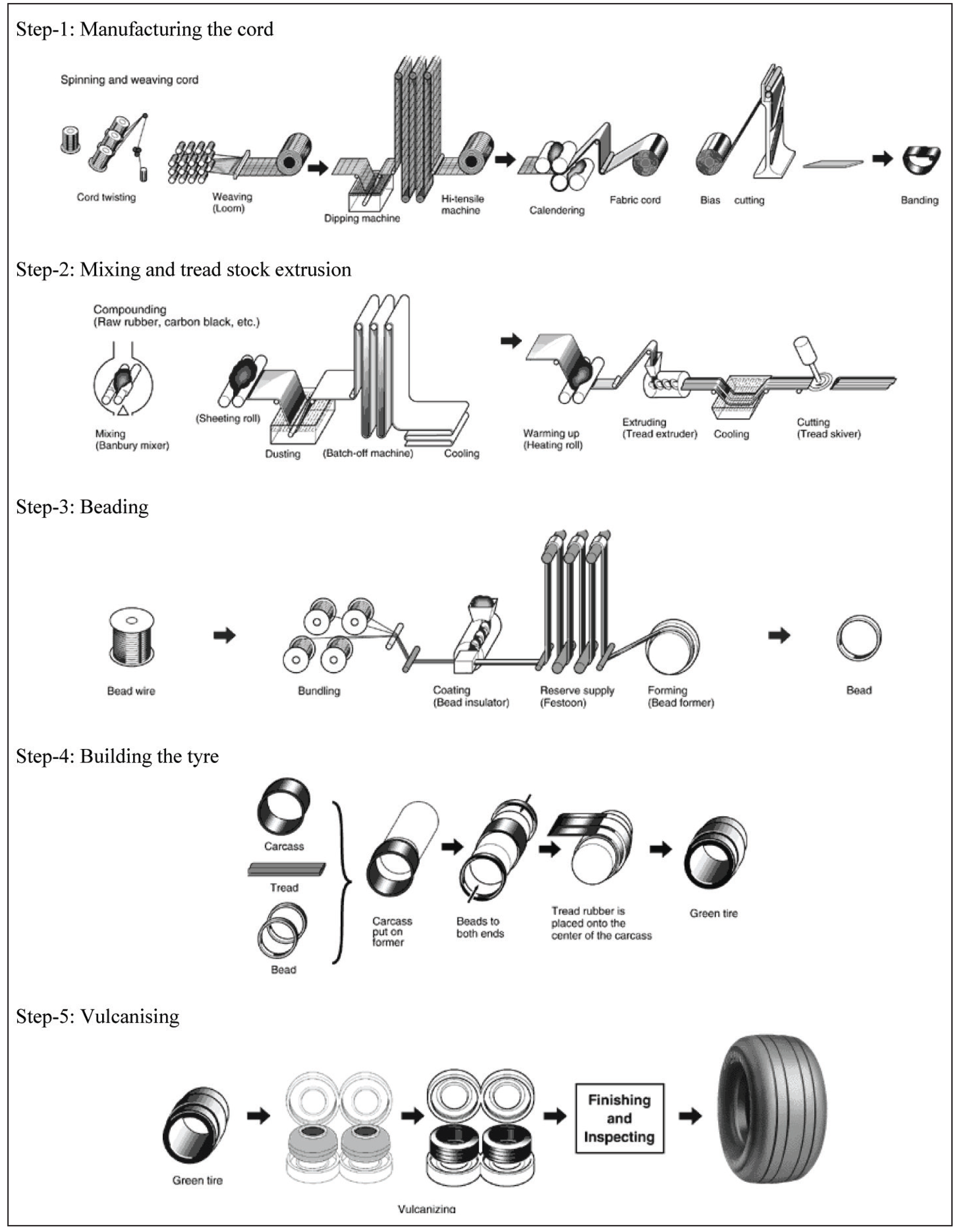

The tyre production process consisted of the following steps: tyre production process consisted of five major steps, namely manufacturing the cord, mixing and tread stock extrusion, beading, building the tyre and vulcanizing as shown in Figure 2. The process began with spinning and weaving the nylon cord and converting it into a band or carcass by passing it through rubber coating and calendaring processes. In the second step, rubber and other raw materials were mixed in varying proportions depending on the type of product. The materials were heated to soften in the warming process and then turned into sheets during extrusion. Thus, a tread was formed using nylon fabric and rubber in four-ball calendaring. In the third step, the bead that would make the sides of a tyre was formed. In the fourth step, the construction of a tyre (a green tyre) was completed by putting together the carcass, the tread and the bead produced in the previous steps. Finally, the vulcanizing process passed the green tyre through a heated mould under a specified pressure and produced the final tyre. The tyre went through a finishing and inspection process before sending it to packaging.

The tube production process was much simpler compared to the tyre production process. 8 A workforce of 844 people worked in the auto tyre production and packing facility. A workforce of 740 people worked in the auto tube production and packing facility. A total of 149 personnel were involved in the quality assurance and control process.

The bicycle tyre and tube manufacturing process was similar to the auto tyre and tube manufacturing process, but the machines were less sophisticated in comparison. The bicycle production facility had a workforce of 116 including tyre and tube manufacturing and quality assurance and control personnel.

According to the General Manager of the tyre plant Mr Cheema:

The greatest strength of the production facility was its trained workforce. Some of whom have been with the company for over thirty years and their skill and knowledge have played a major role in the success of the company.

The production facility at SIL tyre division had the latest machines, also used by some of the top European and Japanese manufacturers. Since 2007, the company had invested heavily in upgrading the production facility to ensure high quality products that would enable SIL to compete in the competitive export markets (refer to Figure 3). To ensure that the product quality was consistent and met quality standards, the tyre division had one of the most advanced testing labs in the tyre and tube industry in Pakistan. Products were tested at various stages during the production, gauges were installed in various equipment and a monitoring and control system was in place.

Key personnel in the tyre and tube plant were able to bring about improvements in the production process. As an example, de-bottlenecking of the calendaring operation was carried out by the tyre division staff themselves in a very short period of time and increased its capacity from 22,000 to 27,000 units per day. However, the engagement of foreign consultants for this project would have consumed substantial money and time. The tyre division productivity figures, as well as its rejection rates, were better than its main competitors as shown in Table 4. With respect to continuous process improvements, Raja Imran, Production Manager Tyre Division, elaborated:

In the past, we have carried out a number of projects that caused substantial improvements in the processes. For example, there was a problem in the motorcycle tube production process which was causing a 5%-6% rejection rate and the production process was very slow—three moulds were being handled by one operator. We made a slight change in the nozzle design of the tube by converting it from Z-type to L-type, removed one production process step and adjusted production process parameters in such a way that a very less skilled operator could now operate the equipment, the production process became quicker and the rejection rate decreased. In another project, we refurbished the rice husk boiler resulting in lower energy cost. Though we have carried out these projects either by taking self-initiative or by higher management’s orders but the process improvements in our plant are not being done in a structured manner. We currently lack a structured process for continuous improvements which is absolutely important to protect our competitive advantage against the competitors. We do not have quality circles.

Tyre Plant Productivity Compared to Competitor

While emphasizing the need for future planning, Raja Imran emphasized on making a 5-year plan for capacity enhancement. He also wanted to carry out seasonal planning for inventory build-up which could be used in high-demand seasons. He also emphasized the need for management training for managers. This was important to understand the role played by various functions like production in the overall scheme of things at SIL. At the same time, it was considered important to better manage the production workforce and cost control. This would also develop professional management skills in individuals, and thus the relationships among different departments would be more professional. Another issue faced by production management was that their job descriptions had not been reviewed for quite some time. During this time, the roles of the management staff had evolved that needed to be accorded.

High turnover of production workforce was another issue which was important for plant management. This was not only causing SIL management the hassle of looking for new workers but also affected the quality of output and productivity. The plant management was contemplating testing a female workforce on some production operations under the belief that managing women would be relatively less demanding. HR policies of SIL with regard to worker welfare and social security were good; however, there were concerns regarding the cooling systems on the production floors. The regulated cooling system would help workers feel less fatigued at work.

Quality Control

The tyre division had established a strong system for quality control and assurance. There was a quality inspection before and after each major step of the production process, that is, raw material, production, packaging and pre-delivery. The purpose of this inspection system was to control defective units to be passed to the next stage in the production process. On the other hand, the purpose of the quality assurance system was to ensure that no defective units were produced in the first place. For this purpose, control gauges and instruments were installed on each piece of the equipment in order to control process parameters that were known to affect the quality of the product at the respective processing step.

The quality control department at the tyre plant employed 102 personnel 9 —50 per cent each for quality control and quality assurance purposes, 4 executives and 12 quality supervisors. These people carried out their duties in three shifts of operations of the tyre plant. The quality assurance individuals were responsible for taking readings of different parameters on equipment and helped to adjust the equipment. The quality control staff inspected the outcome from each process step, allowed passing the correct parts to the next step and recirculated the defective parts to the previous stages for reprocessing (where possible).

Quality Manager, Mr Faisal, was quite satisfied with the performance of his department. He reflected on the quality system:

The actual implementation of a quality system depends upon, (1) top management commitment which provides resources, (2) the immediate boss who delegates authority to make decisions and establish procedures, and (3) objective criteria to assess and control quality.

He also reflected that 30–35 per cent of the causes for defective units were uncontrollable, while the remaining causes were controllable. The controllable factors included: material compound problems, worker operations and worker turnover.

Faisal reflected that a major challenge to ensure quality at the plant was high employee turnover. Some of the reasons might include tough working conditions—high temperature, especially in the summer season, low salary and too many checks. The system needed to be further improved, and managers and supervisors needed to be given training on the latest quality and safety management systems such as total quality management. The production and quality managers admitted that there was a dire need to implement quality circles and 5S methodologies in order to establish a continuous improvement system in the organization. They also concurred that:

Quality should not be the responsibility of a few individuals in the organisation. Quality is a way of life, a discipline that everyone in the organisation should follow. The need and urgency of quality have to be inculcated in the minds of the workers and the managers alike so that a quality culture could be developed.

Human Resources

The total number of employees at the tyre plant was 2,266. A total of 76 executive and 249 non-executive personnel worked in the head office in Lahore. Some of the HR functions were performed by the production department—payroll, compensation and HR planning were managed by the GM of production. Shop floor workers were permanent employees, and SIL offered attractive benefits—annual profit sharing, group life insurance and social security coverage were all part of the package.

Shop floor worker retention was a challenge at the tyre and tube plant owing to tough working conditions in some of the processes as well as socio-economic issues. The company paid a 10 per cent heat allowance for the summer months and had worked with the staff and management to improve the working conditions such as adjusting the cool draft of air on workstations where workers had to work in front of heated moulds. The HR department worked closely with line managers and the production supervisors to come up with policies that would encourage employees to stay associated with the tyre and tube plant for a longer period of time.

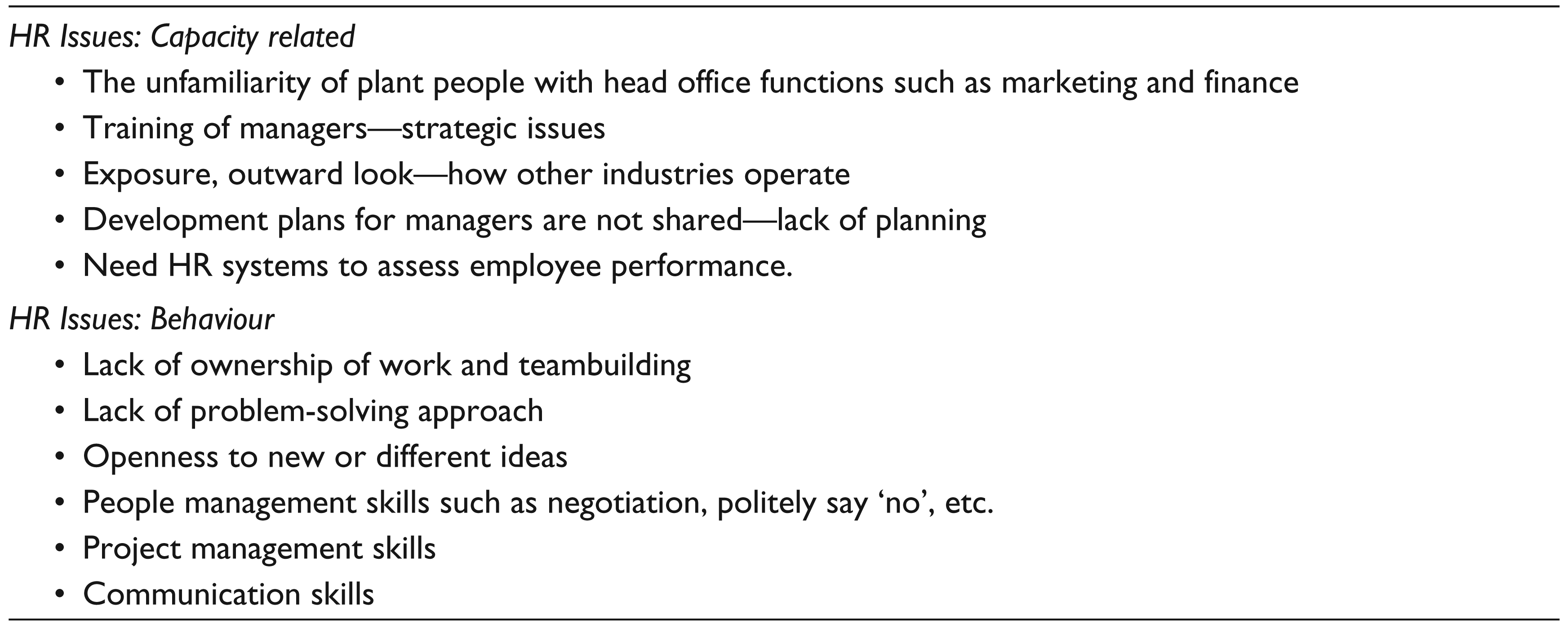

At the managerial level, a number of departmental managers at the tyre and tube plant identified challenges that hampered their ability to function well in the organization. They felt that these issues needed to be addressed. They are summarized in Table 5.

HR Issues at the Tyre Plant

According to Mr Noman Faisal—head of the HR department:

A major goal for the HR department was to turn SIL into a progressive organisation hence the decentralisation of resources and functions was important. Bringing transparency and accountability to each role in the organisation was also important. People were receptive to change and new ideas and various interventions from the HR department were taken positively such as mandatory safety trainings for the supervisors, performance appraisals, standardised entry level test at the time of recruitment. Experienced workers are promoted to supervisor rank without any managerial training. There is a high employee turnover at the worker level. At the same time, training and retention of workers coming from other organisations is a challenge. For the managerial ranks, SIL provides a compensation structure. SIL offers medical insurance, leave fare assistance (LFA), performance bonus, 10%–12% increase in salary every year, and a stable (or permanent) job.

Hassan Shahid, an HR executive expressed his dismay in general about the production plants:

There is a difference in approach to recruitment policies between plants and the HR department. Plant people do not want change in structure and practices, they want to employ experienced and local workers whereas HR wants to employ relatively young people. Appraisal feedback is not provided to employees, there is hardly any succession planning, and no career paths are discussed with subordinates.

Sourcing Raw Materials

Tyre and tube production was dependent on rubber as the main raw material. Rubber formed about 60 per cent of the total cost of the tyre and tube and all of it was imported. Rubber, being a commodity, faced price fluctuations throughout the year and posed a major source of variability in the planning process of the tyre division. There were twenty people in the commercial department responsible for procurement, imports and vendor development. The commercial department worked in close coordination with production planning and finance departments.

The rubber purchase decisions were mainly taken by Arif Saeed, director of the tyre division. He had 15 years of experience in the cotton industry primarily focusing on commodity purchase and sale. He was known to have an instinct about when to buy or not to buy a commodity based on fluctuations in dollar value and other economic indicators. He said:

We have beaten our competition a number of times by taking positions in buying commodities, i.e., spot or forward buying.

Sales and Distribution

SIL took pride in its long-term relationship with its distributors, which was based on mutual trust. SIL competed with local and international brands, and the channel relationship was very important. In 2014, SIL had twenty-one distributors

10

for motorcycle tyres and eleven distributors for bicycle tyres. Other tyres were sold through dealers’

11

network. SIL had a wide sales network with over 7,000 wholesale and retail outlets in Pakistan. It had worked with its channel partners to improve their processes and systems. According to Salman Riaz, Deputy Manager of Distribution:

SIL’s main strength is its distribution network. Its distributors stand with SIL through thick and thin. SIL also ensures their profits are paid. There are distributors who are with SIL for more than fifty years and they are treated like family members of the founders.

SIL had audit teams whose role was to provide trainings to distributors and dealers as well as to check adherence to company policies. Distribution was completely a credit market with 30 days of credit terms, and distributors had to fill a 15-day inventory.

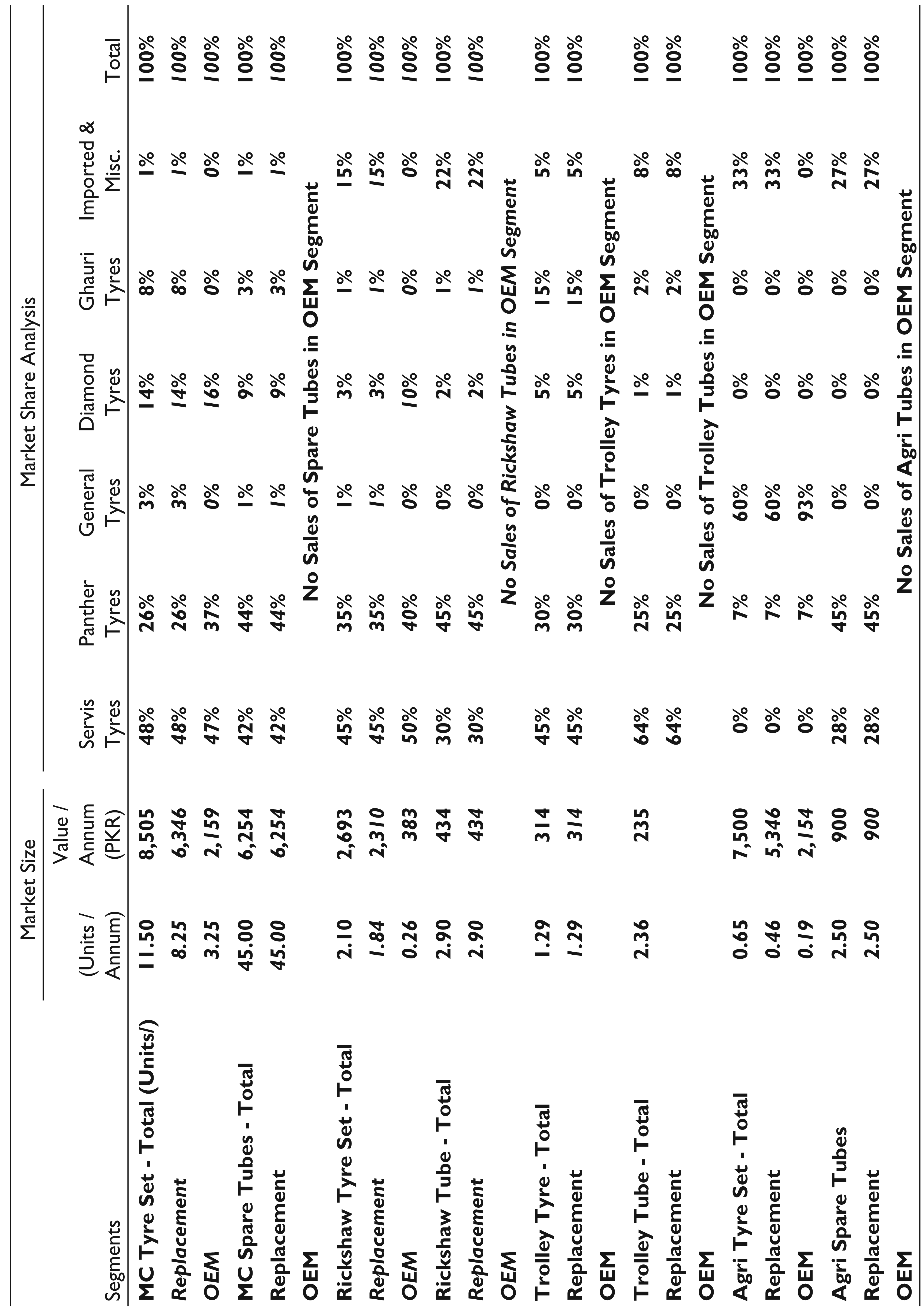

The bicycle tyre market had faced a decline in sales in the last few years because the customers were now preferring locally assembled motorcycles. SIL faced stiff competition in this segment with four to five major players besides the smaller players. This was because bicycle tyres could be manufactured in the cottage industry, and there were many producers in Pakistan. Bicycle tyre manufacturing was a PKR 2.5 billion market in 2014, and SIL had the second highest market share (25%), after Ghauri (35%). Ghauri, on the other hand, worked on the dealership network.

In 2007, SIL had a 58 per cent share in Motorcycle OEM market and provided tyres and tubes to foreign brands (Honda, Yamaha, etc.,) and local assemblers. The only other player was Panther. According to Atif Khatana, Manager of OEM sales:

In 2009, Diamond Tyres entered the market and focused on establishing itself in the OEM market. For OEM, price and credit facility was very important. To enter the market Diamond offered the lowest prices. As a response Panther started offering credit facility.

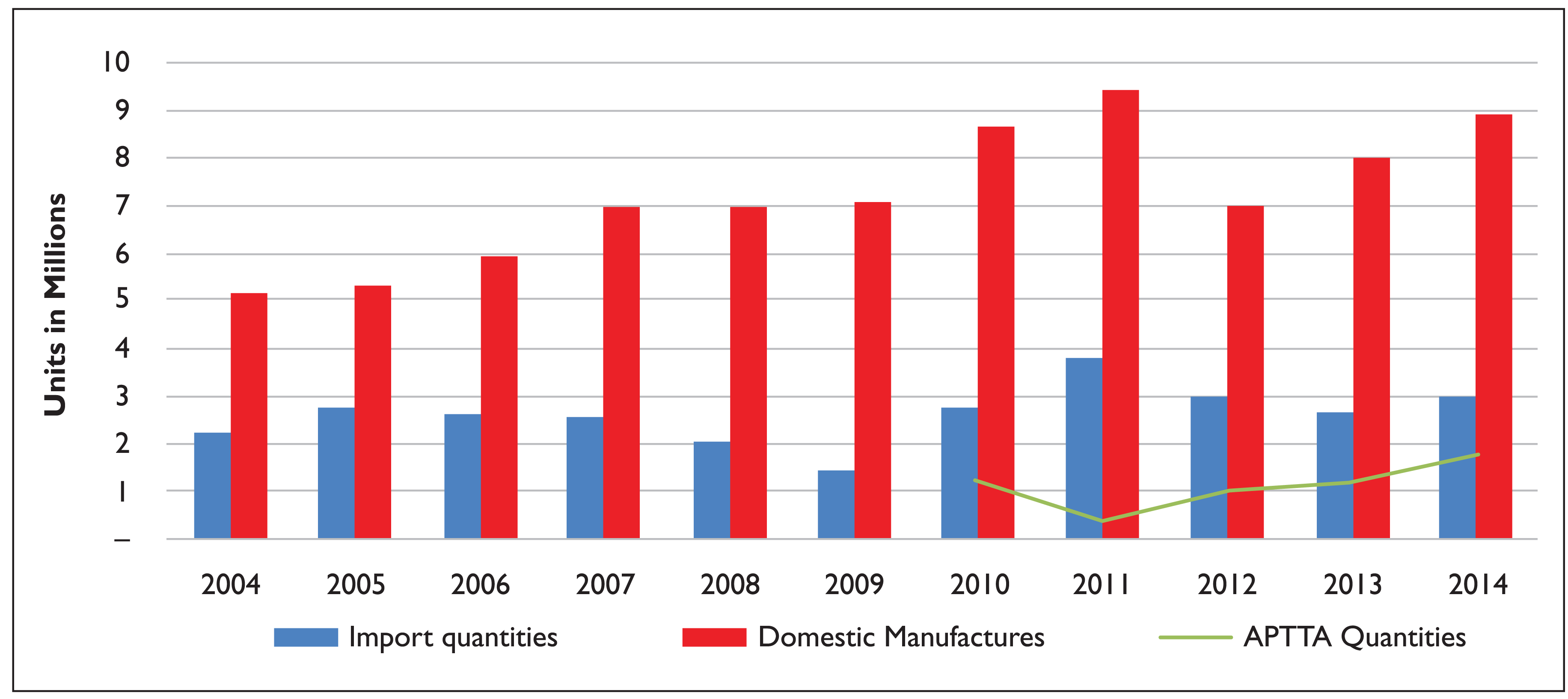

In the OEM motorcycle market, Honda Atlas had a major market share and brand recognition. Honda purchased 48 per cent of tyres from SIL, and SIL was also an exclusive supplier for some of the local assemblers like Ravi, SuperAsia and Ali Raza. In 2014, SIL had a market share of 47 per cent in the OEM motorcycle tyre segment, while Panther had 37 per cent and Diamond 16 per cent (Figure 4a). The OEM business worked on 36 days of credit. SIL closely monitored the financial health of its OEM customers and the economic conditions of the country before deciding on the specific credit policies for its customers. Motorcycle production had been stagnant for the past few years; the market showed only 1–2 per cent increase which meant that the tyre sales to OEM were also stagnant. This meant that SIL had to maintain its goal to retain its current market share for the next few years.

Motorcycle tyre sales in the replacement market formed a significant part of SIL’s business. In this market, SIL leveraged its distributor network, superior product quality and brand recognition. SIL was able to sell at a 5 per cent premium over the competition. It enjoyed a market leadership position, and its share increased from 41 per cent to 48 per cent in the past year.

SIL was also exporting its products to Africa, the Far East and European markets. Chinese firms posed the biggest competition because of their low cost. Thus, SIL was trying to establish its brand in these markets with its superior quality. The export business improved from PKR 243 million in 2011 to PKR 399 million in 2014.

Marketing

Marketing efforts in the tyre division had increased significantly in recent years. Since 2007, SIL had been investing in ATL and BTL advertising activities to increase company profile, brand perception and product value, and the current leadership position in the face of competition was a result of it. The marketing budget increased from PKR 2.5 million in 2007 to PKR 150 million in 2014.

SIL started advertising in the media in 2012, a first in the motorcycle tyres market. There were 10,000 retailers of SIL tyres and tubes of which 7,500 were distributors’ own retail shops. These shops were used for branding. Similarly, vulcanizers who were the major opinion builders of the end consumer were engaged in branding activities such as the provision of water coolers, sunglasses, P-caps, tools and tags bearing Servis logo as well as advertisement posters. Talking about the challenges faced by SIL, Muhammad Ejaz, the Country Manager (Marketing) said:

The major challenge faced by SIL is the unethical practices of competitors who are involved in tax evasion. SIL with a history of giving tax since its inception continues with ethical practices and thus faces challenges in the marketplace. Besides, our marketing and branding strategy needs to improve and marketing budgets and resource needs should drive from there.

There was limited coordination among production, R&D and procurement, which caused delays with regard to response to customer queries and claims.

Competitive Situation for Tyre Division

With bicycle tyre and tube businesses not growing, SIL had set its focus on the auto tyre (tyres other than a bicycle) and tube market for growth. SIL was the market leader in motorcycle and rickshaw tyre segments in Pakistan according to the market share analysis conducted by the SIL marketing department (Table 6). With only five major players, the industry was concentrated. Long-time competitor Panther was in the second place in both these segments.

Competition and Segment-wise Presence in 2014

SIL was the first choice vendor for major motorcycle OEMs like Honda Atlas, Yamaha and local assemblers. It was the brand of choice in the replacement market and was sold at a premium of 3–5 per cent on price though it had a 10 per cent premium on quality. No price premium was charged on the tube.

The motorcycle tyre and tube markets in Pakistan had not seen major growth in the past few years, and the competition in this segment was going to be tougher in the future (Figures 4a and 4b). This meant that SIL had to actively look for other avenues of growth.

Recent Growth Initiatives

The strategy team for the tyre division was looking for growth opportunities, which could be either product extension or diversification. The following business development opportunities were being pursued in 2015:

Agri-tyre Business

To leverage its experience in manufacturing auto tyres and tubes, SIL saw an opportunity in the agri-tyre business, especially tractor tyres (front and rear) for the local and international markets. Pakistan being traditionally an agricultural economy meant that the agri-auto sector offered a good source of business growth in the long term. 12

According to a market research conducted by SIL, the agri-tyre was an approximately PKR 12 billion annual market in 2014. General Tyres and Panther Tyres were the major players in this segment in Pakistan. General Tyres with the lion’s share of 60 per cent was the biggest and the oldest player in the market. 13 Its product offered reasonable pricing, after sales service, low claims and quick adjustment of claims. Its brand recognition was the highest, and it was the first choice for the customers. General Tyres had developed a strong network of dealers across Pakistan and offered a complete range of products in the agri-tyre business. However, in the agri-tube business, General was not able to develop its reputation because of quality problems and had thus discontinued that business. It was; therefore, selling imported tubes under its own brand name. Market communication with customers in this area was also minimal.

Panther, on the other hand, was able to capture about 7 per cent of the market share owing to its credit policy. However, Panther suffered from poor quality, high claims and slow adjustment of the claims. Besides, it did not have service centres. Panther was not offering a full range of agri-tyre products and was reputed for selling imported tyres with its brand name.

Imported tyres filled the remaining market demand in the agri-tyre market. Imported tyres were priced higher than those from General and lacked after sales service and warranty. Rana Saeed, Head of Marketing and Sales in the domestic tyre business, felt that an opportunity existed to enter the market. He reflected:

We would need to keep our prices lower than General Tyres. We already have a reasonable market share in the Agri tube business and have developed a dealership network. We would leverage our brand value and dealership network to sell agri tyres as well. If we would ensure our product quality and offer after sales service, we would have a very good opportunity to grab a reasonable market share. However, we might need to sell on credit at the start as well as invest in market communication.

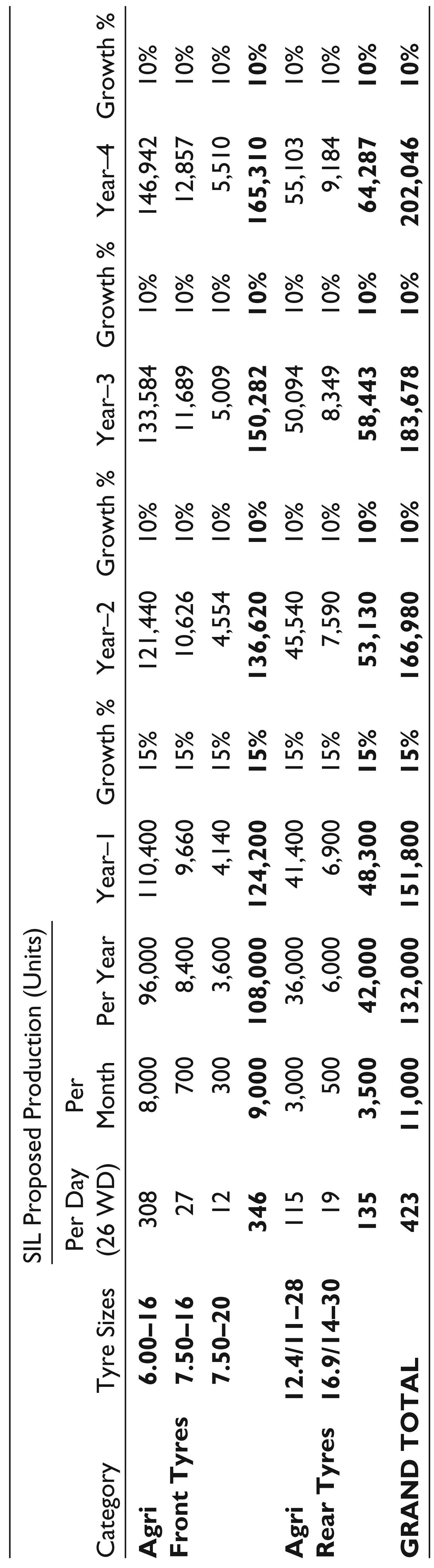

Agri-tyre production would require major investment in the plant and equipment. Besides, the dealership network would have to be rejuvenated, and relationships would need to be further strengthened. SIL hoped that it would be able to gain about 10 per cent of the market share in the tractor tyre industry in the first year. Sales projections are shown in Table 7.

Sales Projections for Agri-tyre

Auto Parts

Motorcycle parts replacement market was a PKR 58 billion market in 2014, 14 which included functional auto parts (market size of PKR 23 billion) such as batteries, air cleaners, chain sprockets, brake shoes and so on, and auto body parts (market size of PKR 17 billion) such as rims, headlights, spokes, fenders and so on. The remaining was the engine oil market. The wholesalers and retailers of auto parts and tyres and tubes had merged over the years, and 80 per cent of the retailers sold both auto parts and tyres and tubes.

Honda Atlas was the market leader in this segment and charged a 10 per cent premium over the competition. The other major player was Crown Lifan which like Honda Atlas was also a motorcycle manufacturer. Besides these, there were importers of Chinese brands. All vendors supplying to Honda Atlas and other assemblers were also marketing the products under their own brands. Auto parts market share and various brand positions are shown in Table 8 and Figure 5, respectively.

Auto Parts Market Players and Their Share

In order to leverage its brand equity and distribution channel in the auto parts business, SIL entered the market in 2012 with wheels and spokes. The wheels and spokes were a PKR 2.5 billion market in 2012. To further grow this line of business, SIL not only had to develop partnerships with auto part manufacturers but also develop in-house product design capabilities.

This line of business did not require major financial commitment as SIL was only marketing these products under its brand without the need of any manufacturing facilities. SIL sourced the products on a longer credit period and sold them on a shorter credit period. This could also benefit the distributors because they could use their current resources to increase sales volume. The bargaining power remained with SIL owing to its brand equity. However, this also posed a risk since the Servis brand would be at stake if something went wrong. SIL needed to ensure product quality and delivery reliability of its vendors, and for that matter, systems were needed to be put in place. At the same time, it may perhaps be important in the future to develop SIL’s own design capability of the auto marts if it were to contract manufacture parts from suppliers.

Exports

Export markets had been SIL’s focus since 2011, and it had set a goal of doubling exports every year. This required a major effort from the sales and marketing team. Besides, to compete with other international players, SIL had to improve its product quality and increase product range in accordance with market demands.

SIL already had certifications 15 from various markets in order to supply tyres in those markets. SIL preferred to export under its own brand name or co-branded products to establish its brand recognition in the export markets. In 2014, SIL was exporting to countries in Asia, Africa, Europe and North America. The export business comprised about 5 per cent of the total tyre and tube business at the time. However, there existed tremendous opportunities to supply bicycle and motorcycle tyres in many countries across the world.

SIL also had to increase its production capacity for increasing exports. Quality had to be improved, for which purpose SIL had imported European machinery to replace and enhance production capabilities. This required major capital investment in the current line of business. As a matter of fact, SIL was continually investing in state-of-the-art equipment since 2006 in order to ensure consistency and quality of its products.

Future Challenges

As Arif glanced through the market research data for growth options, he knew that achieving the growth targets would require developing new strategic capabilities in the value chain. He also wondered how new capabilities would interplay with the existing capabilities in the value chain and what would be the course of action for their potential alignment. Besides, he was also unsure about the potential of each growth option. Should he focus on only one of these options or all of them simultaneously? Convincing the board to trust him and his team for significant financial investments in the tyre division would not be easy. With that thought in mind, Arif prepared himself for the meeting.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this case.

Funding

The author received no financial support for the research, authorship and/or publication of this case.