Abstract

This case study is about ZARA’s transformation from conventional stores for women’s apparel brands to omnichannel concept stores to provide a seamless shopping experience inside its stores. This case is about the time when, in 2019, ZARA’s Indian subsidiary was on the verge of adapting to a new concept store model. The challenges ZARA faced in transforming its Indian stores from brick-and-mortar stores into omnichannel stores, and ZARA’s entry strategies adopted across markets and its plan to convert from the current multi-channel strategy to omnichannel stores are all elaborated on in the case.

Keywords

Discussion Questions

What are the adaptation challenges ZARA faced in pursuit of growth?

Do a SWOT analysis for ZARA with respect to an existing strategy, capabilities and competitive advantage.

What are the challenges faced by ZARA while changing its marketing mix?

What kind of technological, digital and cultural capabilities does ZARA need to succeed in omnichannel?

Describe the customer journey experience using all touch points from the customer’s point of view.

It was a cold, windy morning in October 2019 in Delhi, and Mr Ashish Dash, ZARA’s Managing Director of Indian Operations, was about to inaugurate a store. His visit was scheduled for two purposes: first, to inaugurate the store, and second, to explore the possibility of providing a unique shopping experience for its regular customers. Omnichannel provided a seamless, integrated shopping experience and interface for retailers and their customers. However, it had complexities related to IT and logistics. The women’s apparel market was witnessing a fierce battle in the UK and other European markets. Many retailers started to build infrastructure to support omnichannel retailing, but they were unsure about the factors that impacted shopping behaviour. During 2015, it was more like a test-and-iterate retail marketplace. He had to decide if he should invest in omnichannel technology because investment in this new technology would imply many changes for logistics, IT and the present culture.

Introduction

ZARA operated in more than 59 countries and was among the fastest-growing fashion retail brands. This was a flagship brand of its parent company Inditex (Industria del Diseño Textil, SA). The parent company was headquartered in Galicia, northwest Spain. The company ZARA was established in 1975. In a short span of time, Inditex had become the world’s most famous clothing retailer and ranked second in the fashion retail business. By the end of 2006, ZARA had 2,692 retail showrooms across 62 countries. ZARA accounted for 66% of Inditex’s turnover in 2005. Apart from ZARA, Inditex owned seven other clothing chains, namely Kiddy’s Class (children’s fashion chain), Pull and Bear (youth casual clothes chain), Massimo Dutti (quality and conventional fashion chain), Bershka (avant-garde clothing chain), Stradivarius (chain of trendy garments for young women), Oysho (chain for undergarment) and ZARA Home (household textiles chain).

ZARA’s Business Model

ZARA’s strategy was to streamline fashion trends by providing the latest fashion at moderate quality and affordable prices, as Inditex founder, Amancio Ortega, explained. ZARA’s business model focused on the turnaround time compared to its competitors and its concept stores as a hub for information. ZARA had approached lean manufacturing (Castellano, 1993, 2002). ZARA’s turnaround time was less than four weeks. The clothing line on display changed within two weeks and was faster than the industry average ( The Economist, 2005 ). ZARA mainly focused on its private labels on display as its ‘live collections’, contributing to almost half of its total production, and outsourced the remaining clothing lines that did not witness seasonal variation. Every year, around 11,000 new offerings were launched ( Ghemawat & Nueno, 2003 ).

Apart from acting as a point-of-sale, ZARA’s stores also influenced the launch of new designs and the pace of production. The manufacturing of apparel started with experimenting with newly launched designs of clothes with its customers, collecting information from its field executives who extensively travelled to fashion cities to observe the shopping behaviour of customers who visited the stores and tracking publications with trends related to customer buying pattern (Fabrega, 2004). ZARA’s strength was the feedback that its managers collected from their customers who visited the stores (Roll, 2021). Store managers were responsible for daily reporting customer demand and sales trends to headquarters. The designers used the feedback given by the customers to create new clothes (Crawford, 2000; Martinez, 1997). Around 60% of its clothing lines were replenished regularly; the remaining 40% varied once every 2 weeks. ZARA’s customers visited the store 17 times a year, compared to around four visits for competing stores (Castro, 2003).

ZARA’s Stores’ Locations and Layout

First, ZARA’s key focus in domestic and international markets was its store location. ZARA’s shops were situated in prime locations. The locational decision was based on a combination of a comprehensive design that explored niche opportunities for ZARA’s clothing line in those markets, the price of its competitor’s offerings and the recommended price proposed by their local managers and industry experts to optimize profitability (Bonache & Cerviño, 1996). The location of its stores was meticulously planned near main commercial areas in every fashion city in all markets where they operate. Once the store location was decided, local managers began to hire executives for store operations. Initially, ZARA sent its Spanish managers to replicate the management practices in their country of origin (Fabrega, 2004). However, they faced difficulty operating in countries like Mexico and France (Bonache & Cerviño, 1996), which made ZARA adapt locally by recruiting executives from the host country to better understand the prevailing market preferences (Martinez, 1997). ZARA ensured their knowledge and know-how in drawing market insights, designing clothing lines and robust supply chain procedures and transferring corporate values to other markets (Bonache & Cerviño, 1996).

Second, the store’s interior layout was designed to provide a unique shopping destination to its customers with striking window displays. They focused on the quality of in-store customer service, intrinsic benefits such as soothing music in the background, the temperature in the store and layout as a combination. ZARA adapted approaches like ‘mystery shopper’ as a regular activity to gain insights into how the customer felt while shopping in-store (Fabrega, 2004; Monllor, 2001).

ZARA’s Marketing Strategy

ZARA followed their pricing primarily based on a market assessment of their regular buyers’ willingness to pay. The prices of ZARA’s clothing lines were different in all the markets they operated in and were higher than their counterparts, whereas it offered the lowest prices in its home market. Prices were set centrally based on a market-oriented approach. Prices in international markets were generally higher due to the longer cycle of their distribution networks. They adopted reverse budgetary planning by allocating the cost of material, production and suppliers per the target price set and the profit margin they decided for each clothing line (Bonache & Cerviño, 1996; Mazaira et al., 2003).

ZARA applied a similar promotion strategy in both domestic and foreign markets. Stores used to spend around 0.3% of their annual turnover on advertisement campaigns only at the beginning of the season or during the opening of a new store. ZARA mainly focused on in-store promotions (Ghemawat & Nueno, 2003).

Initially, ZARA followed an ethnocentric approach by replicating its international stores similar to those in its home market (Alexander & Myers, 2000; Bonache & Cerviño, 1996). However, due to cultural resistance and differences in buying patterns, ZARA adopted a geocentric approach. They started adapting local preferences related to store format and local preferences about clothing lines.

ZARA as a Brand

ZARA’s clothing lines were built domestically and then launched internationally. Their multi-brand portfolio helped ZARA to serve their target segments effectively. However, this branding strategy had its complexities. They used a combination of proper product strategies with separate target segments, different promotional strategies and retail images to differentiate the brands of clothing lines.

In over 30 years, Inditex had transformed ZARA from a local brand to a global brand by building a brand portfolio (see Table 1 and 2 for details) through brand acquisitions and developing existing brands. They acquired major brands like Massimo Dutti in 1991 and Stradivarius in 1999. In contrast, Inditex developed brands like ZARA in 1975, Pull & Bear in 1991, Kiddy’s Class in 1993, Bershka in 1998 and Oysho in 2001. They also extended brands by adding ZARA Home. ZARA avoided linking its brand portfolio with its origin, which had helped convey a global image (See Table 3 for details).

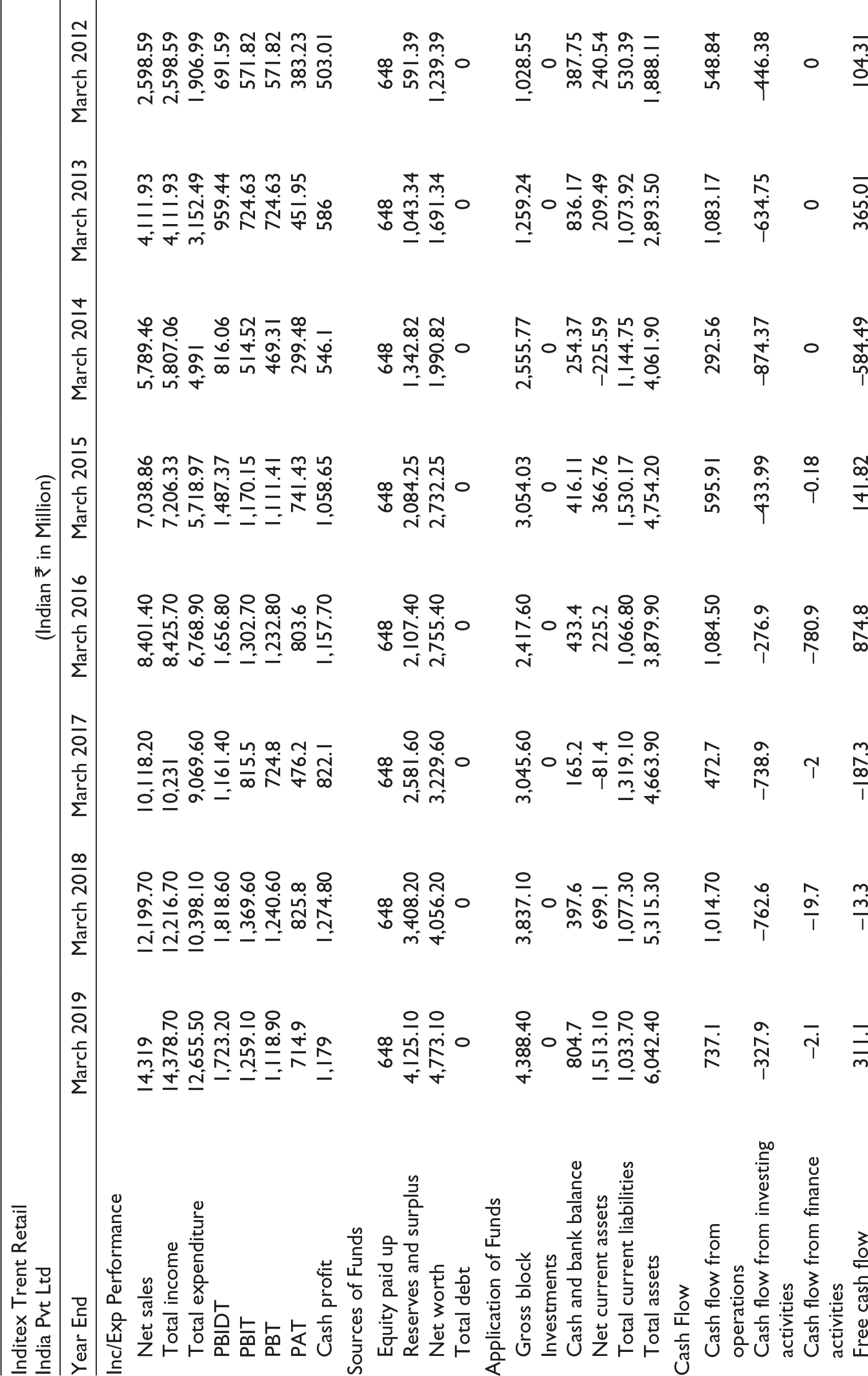

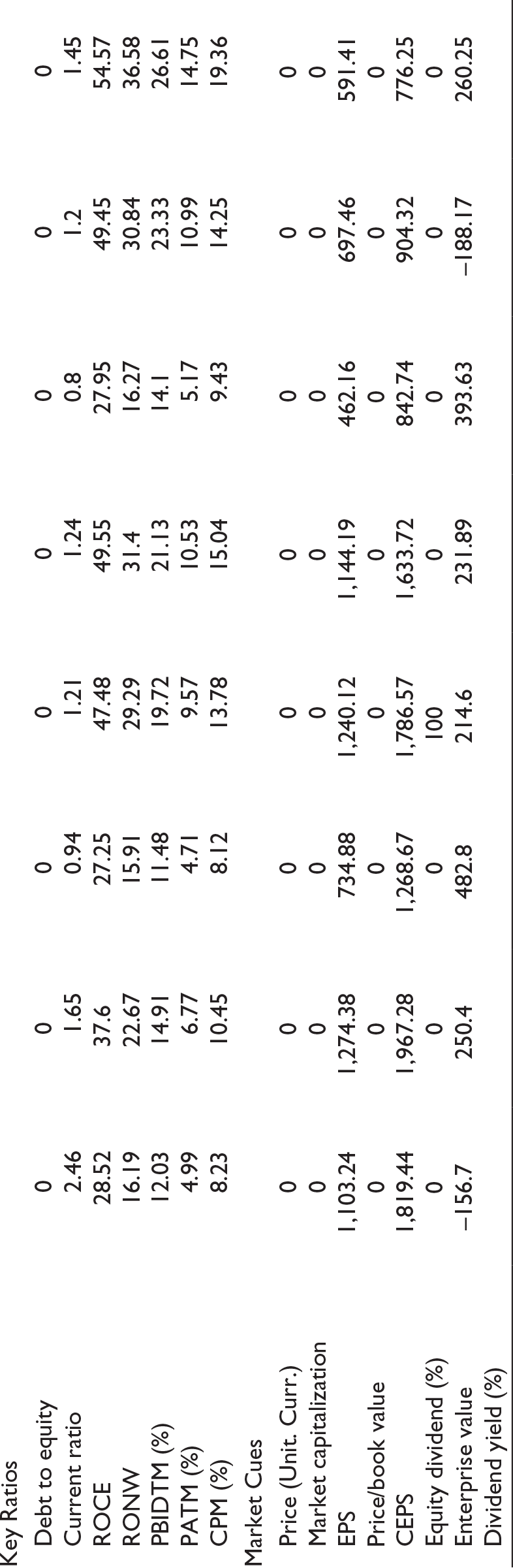

Financial Ratio of ZARA.

Case Flow.

Global Brand Value.

ZARA’s Market Expansion Strategy

In 1975, ZARA started its flagship store in northwest Spain. During the 1980s, ZARA rapidly expanded its store network in all major cities in Spain, with a population of approximately 100,000 (Ghemawat & Nueno, 2003). In 1988, ZARA opened its first international store in Oporto, Portugal, as it was one of the most attractive and familiar markets due to its geographical and cultural proximity to Spain. By the end of January 2006, ZARA had a presence in 59 countries with 852 stores. They had 664 stores in Europe, of which 259 were in Spain, 112 in America, 45 in the Middle East and Africa and 31 in Asia.

The Birth of Omnichannel

Some industry experts claimed that omnichannel started around 2003. Initially, retailers had focused more on customer centricity. Best Buy was the first retail store chain to have customer-centricity as its main strategy. During 2003, retailers were struggling due to the dominance of major players like Walmart and were clueless about how to compete. Best Buy was clear in its strategy to not compete with Walmart on price. They shifted their focus more on the customer experience.

McKinsey Research and Harvard Business Review found that omnichannel retail customers spent an average of 4% more on every shopping occasion in-store and 10% more online than single-channel customers.

Omnichannel: Retailer’s Dilemma

Retailers often faced the dilemma of serving shoppers who shopped online for convenience but asked for tangible benefits from brick-and-mortar stores. Recent studies revealed that around 48% of shoppers ordered products online and picked them up in the physical store, 37% used the internet to search for offers but bought through the physical store and 35% ordered the products online but returned them in the physical store. Around 88% of Millennia had at least one retailer app on their mobile phones, and 86% of these cohorts accessed those apps at least once per week.

There were extraneous factors that contributed to their expansion. The Spanish market was maturing and started witnessing a change in consumer buying patterns and preferences, a shift in their spending pattern more on travelling and education than clothing, the inclusion of Spain in the European Union in 1986, globalization of economies and emerging homogeneous consumption patterns across markets.

ZARA’s expansion was meticulously planned by entering the market with geographical and psychological proximity. In 1990, ZARA opened its first store in Paris, a fashion capital and culturally close city. They then expanded to other markets like Belgium and Sweden in 1994 (Bonache & Cerviño, 1996). It entered Mexico in 1992, being a geographically distant but culturally close market. This helped ZARA to gain insights into the South American market. The next move was to open their stores in Greece, Malta and Cyprus in 1993, 1995 and 1996, respectively. During this time, ZARA opened its first store in New York in 1989, although being in a culturally distant and competitive market. This was a strategic move to reinforce its brand value and build global brand imagery.

Apart from culturally close markets, ZARA also moved to geographically and culturally distant markets. In 1997, ZARA opened its store in Israel. Following 3 years, ZARA consolidated its position in the European market rather than focusing on new markets. ZARA also opened retail outlets in countries such as Costa Rica, Monaco, the Philippines and Indonesia. By 2006, ZARA had a presence in 59 countries.

ZARA’S Entry Strategies

During expansion, ZARA adopted three modes of market entry:

ZARA’S Subsidiaries

ZARA had adopted this strategy for most European and South American countries as these markets were perceived to possess high growth potential and low business risk (Flavian & Polo, 2000).

Joint Ventures with Others

In 1999, ZARA did a joint venture with the German firm Otto Versand Trading Group due to its immense knowledge of the European market and strong distribution network. Then went for another joint venture with Gruppo Percassi in 2001 to help overcome the administrative barriers related to the dominance of local trades and knowledge of the property market in Italy (Expansion, 2001). In 1998, ZARA entered into a joint venture with Biti in Japan, as this company had experience tracking trends related to clothing preferences and knowledge of the property (Castro, 2003). All the ventures were of 50/50 partnership.

Franchising

ZARA followed this strategy for culturally distant countries with small markets with low sales forecasts, like Saudi Arabia, Kuwait, Andorra or Malaysia (Flavian & Polo, 2000). ZARA’s franchisees implemented the marketing strategy by identifying a store location, deciding the store’s interior design, logistics and human resources. However, these franchisees had the autonomy to decide how much to invest in fixed assets and recruit the staff. ZARA had also given provision to its franchisees to return their merchandise and decide on their own regarding the exclusivity in their geographic area, but with the condition that ZARA could open its exclusive stores in the same location (Castellano, 2002). ZARA owned almost 90% of the stores in these markets (Ghemawat & Nueno, 2003).

After deciding the entry mode for a particular country, ZARA followed a pattern of expansion known in the company as ‘oil stain’ (Castellano, 2002). In this context, ZARA first opened its flagship store strategically to get deeper insights about the market and acquire expertise. The experience gained in the process guided ZARA in the expansion phases in that country (Blanco & Salgado, 2004).

ZARA in India

Omnichannel Strategy

The strategy adopted by ZARA was to share revenue with the mall owners. This was an outcome-based strategy, where the mall owners would get a commission based on their sales. This helped ZARA because the customer pull was generated by the advertisements done by the retailers and mall owners. Based on local preferences, the advertisements targeted the customers well and helped them experience the sale in different channels.

From just one store in Mumbai, ZARA could use this strategy to expand to 13 stores in India rapidly. The indicator sales per square foot were the highest in India for ZARA.

ZARA’s Supply Chain

ZARA used lean manufacturing to reduce the design cycle time—from concept to design to the market. It set a record by making its go-to-market strategy with 15 days lead time. Using an economy of scale and automated manufacturing systems, it also sourced its apparel from global and local markets. Using the local designs, the finishing touches were given at the local stores, which helped with contemporary designs and set the trend for fashion.

This strategy helped increase net income, growing at 20% and increasing its retail offline presence at more than twenty locations in India (See Table 4 for details).

Finished Products.

ZARA’s Competition in India

ZARA experienced success shortly after entering India, registering double the revenue per store (average) than its closest rival, Hennes & Mauritz, that is, H&M (Bidwe, 2019). At the same time, Japanese fashion brand Uniqlo planned to launch its first store in New Delhi.

ZARA faced stiff competition from national and international fashion brands like H&M, GAP, Uniqlo and Aeropostale, but due to their effective customer-centric strategy, they could retain their customer base. A few of their closest competitors were (Verma, 2020):

H&M: This was a Swedish fashion company, and like ZARA was one of the fastest-growing fashion companies globally. Their pricing strategy was similar to that of ZARA. However, the quality standard set by ZARA for its apparel brand portfolio was superior to H&M. GAP: An American fashion-based company with a value proposition of offering simple and fashionable apparel lines. However, the expertise of ZARA in consumer data analytics that assisted the designers in mapping the line of apparel to be launched based on consumer preference patterns was unmatchable. UNIQLO: This Japanese fashion company followed a similar strategy to ZARA’s. However, the only differentiating factor was the new product experience provided to customers, which reduced product stock and increased sales revenue.

According to a recent study in the USA (Tyler, 2018), H&M was seen as more cluttered, and that was the cause of the major inventory problems in their store. However, from a customer’s perspective, the store had a lot of great offerings and depth in variety (styles) all by themselves. ZARA was slightly more premium priced. Their depth was also not what H&M gave regarding basics, beauty products and accessories.

In India, ZARA’s average sales per store exceeded those of top apparel brands such as Louis Philippe, Levi’s and Marks & Spencer and even slightly higher than department store chains like Shoppers and Lifestyle (Malviya, 2016) (See Table 5 for details).

ZARA Versus Industry Comparison.

Shifting to Omnichannel

On 4 October 2017, ZARA entered India’s fashion e-commerce competition with the launch of its website. This marked the beginning of adapting to a multi-channel approach.

Because of its fast go-to-market strategy and usage of omnichannel, ZARA could deliver apparel between two and four days in Ahmedabad, Hyderabad, Kolkata, Mumbai, Chennai and Delhi. This helped ZARA because its competitors took longer to reach their targeted customers. This sales increase happened despite ZARA charging the delivery cost to the customers.

IT Challenges for ZARA

ZARA was never tech-savvy in its business operations. For a long time, they used DOS-based systems. Moving to a specialized channel required the employment of IT professionals who would integrate present systems into the new system. The management felt that all the customers would have the same needs and follow the same path for purchases and deliveries.

ZARA’s supply chain managers operated each channel simultaneously as a separate process. This was because their key performance indicator (KPI) was related to the performance of the channel as a stand-alone process. So, while an executive was in charge of store delivery, he was measured against store performance only. As a result, he gave less importance to customers who came for delivery against online orders. This led to dissatisfaction among customers. This led to the isolation of channels, such as revenue generation targets, that pushed each channel to increase its sales volume regardless of any impact on other channels.

As the results suggest, ZARA needed to set up cross-functional teams to design and implement the omnichannel journey. The cross-functional team would include executives from marketing, customer service, supply-chain finance, brick-and-mortar store operations, strategic planning, e-commerce and IT.

ZARA also did not decide how to segregate the online delivery model from the traditional brick-and-mortar mode of servicing customers. As a result, displays of several products were duplicated in different channels, resulting in a waste of resources and display pages. The franchisees and retail customers had different expectations; their interests and demands were for separate designs. While franchisees wanted fast-moving fashion lines, customers wanted new trends and offbeat products. The franchisees often refused to deliver the products ordered online, as that would mean eating up the storage and display space of the franchisee’s store. Moreover, these online customers were never loyal to the franchisees, so they (the franchisees) never serviced online customers properly.

The franchisees often felt that online customers should be serviced directly from company-owned stores rather than taking up the storage space of franchisees. Some executives felt ZARA should partner with separate franchisees if they did not own the stores. This meant that these franchisees would sign a separate contract for online customers.

ZARA used the same third-party logistics partners for both online customers and franchisees. This helped them reduce the delivery cost but increased the service time for online customers. In addition, the returns from the direct customers were not handled separately, resulting in long lead times and customer dissatisfaction. No separate service centres, collection stores and return places confused all partners. They never used analytics to find customers’ changing tastes and buying behaviours, accurate forecasting by handling local customs and seasonal effects. Different level of inventory planning was not done to take care of the demands of different customers, and inventory management was also not fine-tuned.

Social media played a big role in demands and attracting new millennials to the company. However, ZARA did not put up an effective strategy for collecting comments from social media and judging the users’ moods. Sometimes the customers felt that more was promised and less was delivered, as evident from updates on Facebook and Twitter. Smaller orders could not be serviced effectively, and many times there was more excitement about new designs, but the company could not cash in on the demands that were changing fast and were different from different locations. It also took a long time for the marketers at ZARA to decide on the price of new products, resulting in a loss of opportunities and lost sales.

Challenges

The concerns seen early in the omnichannel strategy, namely uncertainty, continuity of operations, working capital and culture, had to be addressed. ZARA had to enhance the adaptability of its current employees not only to utilize new technology, but also for various systems including logistics, warehousing, and tracking customer experience data, in order to boost customer engagement. Ashish had to design communications to emphasize to the employees the necessity for change, the benefits to the company and the stakeholders and the need for the new strategy (omnichannel strategy) so that the customers could be engaged.

This was concerning because it was not just about advanced technology in the factory and marketing alone. Instead, this strategy was going to touch all aspects of the business.

Transition Plan

ZARA did not have an effective roadmap for transforming the company from traditional brick-and-mortar to multi-channel servicing. It did not plan for proper resources, resulting in chaos and ill will. The culture of old ZARA would have given way to new tech-savvy processes. Instead of rolling out the entire components of omnichannel in one go, they should have implemented the online channel first. This would help them to find new third-party channel partners for tech-oriented online customers. After the successful implementation of this channel, they should have integrated all channels.

A pilot run could have given insights into many issues not foreseen earlier. The learning would have helped implement a robust strategy with each pilot in different countries. Training sessions were not conducted for the old executives to change their mindset for creating an environment and culture for an inter-functional approach.

The Way Forward

ZARA had experienced a transformation from a national retail store chain in northwestern Spain to a global brand. However, due to the fast adoption of sophisticated IT and supply chain standards in the global apparel market, company officials were apprehensive about whether their strategy would work. To mark the future road map, Mr Ashish Dash decided to use a two-pronged strategy: (a) Balancing their presence both in online and offline channels and enhancing their share-of-wallet by implementing a multi-channel strategy; (b) Adapting to the omnichannel standards and providing a seamlessly integrated experience in their Indian stores.

Another decision was to start with metropolitan cities (tier 1), as they offered relatively better supply chain support, or to serve tier 2 and tier 3 cities in India, as major population density resided in these geographical locations.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.