Abstract

Dr Reddy’s Laboratories Ltd (DRL) was one of India’s success stories in the pharma space, wherein a founder’s dream turned into a reality. It had a remarkable growth over three decades, with impeccable quality and regulatory standards, as it went on to become the number-two pharma company in India by sales. However, in the last 3 years, DRL was navigating one of the most challenging times it had ever faced for various reasons. Sales were stagnated, profits had plunged, costs had spiralled and manufacturing sites grappled with US Food and Drug Administration (FDA) issues—and more importantly, its growth strategies were not delivering results. This resulted in value erosion, reduced number of new product approvals, customers doubting the capabilities, competitors doing much better, etc. Also, it questioned whether DRL continued to be the bellwether or not for the Indian pharma fraternity as competitors raced ahead. This case highlights the global and Indian context of the pharma industry, along with details of three main competitors based on secondary data sources, and analyses the ongoing issues in DRL. Finally, it concludes by highlighting the six decision buckets and the way forward to make DRL a bellwether again in the Indian pharma industry.

Discussion Questions

What is a bellwether, and why is it being used in this context? How did Dr Reddy’s Laboratories (DRL) become a bellwether in the first place?

What has the competition been doing differently in the last few years which has helped them overtake DRL?

What are the global trends emerging in the pharmaceutical industry? What does it take in the generics business space in the pharma industry to succeed?

Use Porter’s Five Forces model with reference to the Indian pharmaceutical industry. What insights do you draw from this analysis regarding industry profitability?

Who are the key competitors of DRL? What criteria would you use to identify the key competitors? What inference can you make about the key competitors from the case?

Measure the economic performance of DRL and three of its competitors (Sun, Aurobindo and Lupin) and provide insights on which one is doing the best and why?

If you were DRL’s CEO, what would you do to make DRL a bellwether again in the Indian pharma industry?

On the cold morning of January 1, 2018, when the world was still celebrating the new year, Mr G. V. Prasad (CEO of Dr Reddy’s Laboratories Ltd [DRL]) looked through the windows of his posh office in Hyderabad and pondered over the sales numbers that he had reviewed the previous night. He was upset with the fact that DRL had closed yet again with disappointing monthly and quarterly numbers, in both revenues and profits. There had been a muted top-line growth and a steady decline in the bottom line over the last 3 years (Dr Reddy’s, 2019–20) because of various reasons that were bothering him. As Prasad mulled over how to revive the company, multiple questions crossed his mind. How would he sort out the long-pending US Food and Drug Administration (FDA) issues? How should the company innovate to revive growth in sales and profit? Was there a need to reorganize the management? How could he infuse fresh thinking to boost the research and development (R&D) engine? Should the company explore the option of going back to its basics or explore inorganic avenues? What should the company’s human resources (HR) be doing differently?

Global Pharmaceutical Industry

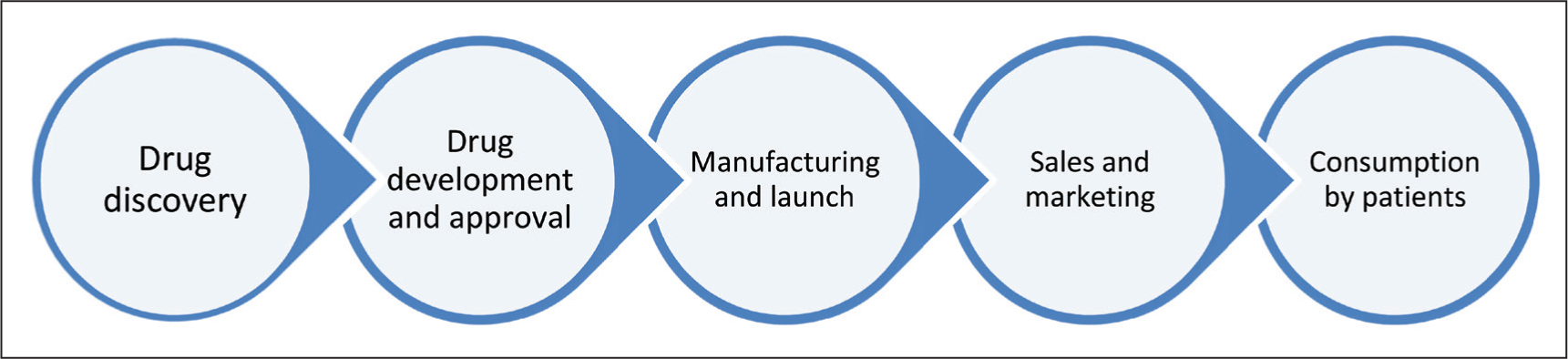

The pharmaceutical industry was one of the integral components of the healthcare sector which innovated, manufactured and supplied medicines. The global pharmaceutical industry was valued at nearly US $1 trillion in size during the year 2014 (Benson, 2015) and was steadily growing. The typical value chain involved discovery research, development research, product approvals, manufacturing and marketing before the drug reached the patients (see Figure 1 for pharma industry value chain). The global pharma industry dealt with two types of medicines (Nasdaq, 2016): prescription medicines and generic medicines. The design, development and marketing of new prescription medicines were intensive and challenging processes (often time-consuming), with a cost of almost US $2 billion (Lim, 2018), and it took over a decade to bring the medicines to the market. Even though the efforts towards research and development (R&D) of new drugs did not always guarantee success, yet the rewards were enormous.

On the other hand, the generic drug market was a different market category and varied across countries. It was dependent on prescription drugs going off-patent, and when patents expired in a particular market, generics companies sold these generic-version drugs. Generally, the first company to receive approval to sell these drugs got the first-mover advantage and maximized profits. There were several unique features of the pharmaceutical industry, and drugs could be broadly divided into prescription and over-the-counter (OTC) drugs based on the type of prescriptions (Cengage, 2018). Prescription drugs were available only based on prescriptions by doctors who decided which drug to administer based on a patient’s ailments. OTC drugs, which were predominantly for non-chronic ailments, were available in the market without any prescription, and patients could buy and consume them as per their will.

The pharmaceutical industry was highly regulated. The respective governments controlled the industry (Drugs Controller General of India [DCGI] in India, FDA in the United States, Medicines and Healthcare products Regulatory Agency [MHRA] in the United Kingdom, etc.); hence, every product had to pass through stringent norms before it hit the market. The regulations were more stringent in developed countries (United States, European Union [EU] countries, Japan) and relatively less stringent in developing countries (Africa, India, etc.). However, each country had its own drug approval process, and companies had to follow it to sell their products.

Industry Structure

The pharma industry structure broadly comprised the innovator (branded) and generics business (see Figure 2 for global pharmaceutical sales).

Innovator Business

In the innovator business, companies discovered, manufactured and supplied new drugs to meet patients’ unmet needs. Pharmaceutical innovation was a risk–reward game wherein the cost to develop a new product was US $2 billion from the lab to distribution. However, if a company succeeded in developing a new drug, then there were multiple ways in which the economic interests were protected, with intellectual property protection (patent) being one such way. Product patents typically ran for 20 years, whereby companies had the opportunity to be exclusive in the market to reap benefits. Beyond this period, the product became available for manufacturing and sold to other companies.

Generics Business

Generic drugs were officially approved copies of the original innovator drugs (Dirnagl & Cocoli, 2016). Companies would reverse-engineer an already innovated drug in the generics business by making a cheaper version and launching it once the innovator company’s patent expired. Since the patent term was usually long (20 years), the competition was generally high when a product was launched upon patent expiry, and due to the high competition, the drugs’ prices fell significantly once the generics entered the market. While this was a risk-free approach, there were provisions in every country’s patent system wherein a generic company could launch earlier by invalidating or non-infringing existing patents (e.g., provisions like the Hatch Waxman Act in the United States). This was a high-risk option, but the reward was also high; the generic companies went for it because of the limited competition.

Drugs of the generic companies were legally approved by the regulatory bodies and were safe for consumption, like the innovators’ products. Both products had similar inactive ingredients, dosage, dose form, route of administration and bio-equivalent. At times, the appearance, inactive ingredients and cost were different. Nevertheless, it was generally predicted that generic drugs were available at one-tenth of the innovator’s cost.

Indian Pharmaceutical Industry

Evolution

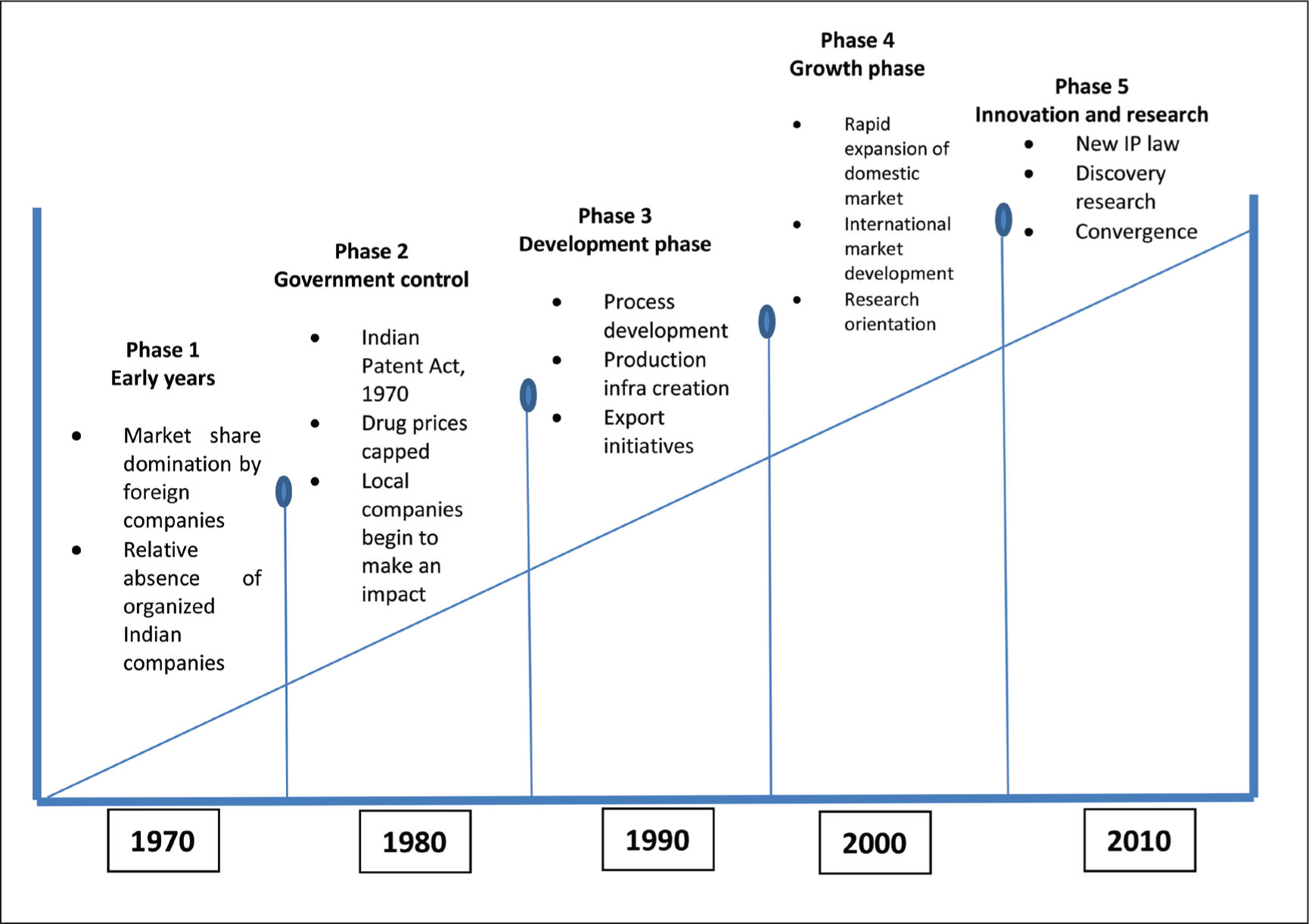

The Indian pharmaceutical sector’s evolution broadly went through five stages (see Figure 3 for the flow of events from the 1970s onwards). First, in the 1960s, there was little or no presence of home-grown companies. Foreign companies ultimately met the Country’s demand through imports. The government took the initiative to set up research institutions and promoted private players to establish companies to enhance India’s pharmaceutical industry. Second, in the 1970s and 1980s, multiple entrepreneurs started companies that were predominantly manufacturing active pharmaceutical ingredients (APIs). The third phase was the 1990s and 2000s, when the Indian pharma industry and market started witnessing robust growth in both volume and value. Several Indian players sprung up as foreign multinational majors and started vertical integration and diversified into niche areas. The government’s liberalization schemes enabled the industry to grow further. The Indian pharma industry was a significant force in the global pharma arena, especially in the generics space, boasting the largest generic-medicine manufacturers.

Industry Structure

The Indian pharma industry was mainly involved in the manufacture and supply of generic medicines and export of APIs. India was not a primary market for innovators because of the legacy of the patent regime, but the patent structure changed in 2005 (Dogra, 2018) and saw a shift to discovery services. India was also a global destination for pharmaceutical outsourcing in contract research and manufacturing services (CRAMS). In addition to that, biosimilars comprised another emerging business for the Indian pharma industry. The Indian pharma industry (Nahar, n.d.) consisted of five different businesses (see Figure 4 for different types of Indian pharma businesses).

The size of the Indian pharma industry was 3% (in value) and 20% (in volume) of the global pharma industry in 2017 (Invest India, n.d.). The industry was dominated by generic formulations (>70%), and the rest spread across API and custom manufacturing sales. The Indian pharma industry was also an export-intensive sector, with a 50% contribution from it, which was valued at US $17 billion of the total US $33 billion in 2017 (Pharmaceuticals, n.d.). Major contributors in the export were the United States (40% and a major importer), EU (20%) and Africa (20%) (Mahalingam & Gopalan, 2019). The Indian pharma industry was a highly fragmented fraternity, with over 3,000 pharma companies and over 10,000 manufacturing facilities (Invest India, n.d.) catering to both the local market and exports.

Current Challenges

While the Indian pharma industry carved out a niche in the global map and was recognized as the ‘pharmacy of the world’, there were many stumbling blocks along the road impacting the sector’s growth. Some of the critical problems plaguing the Indian pharma industry were as follows:

Key Indian Competitors

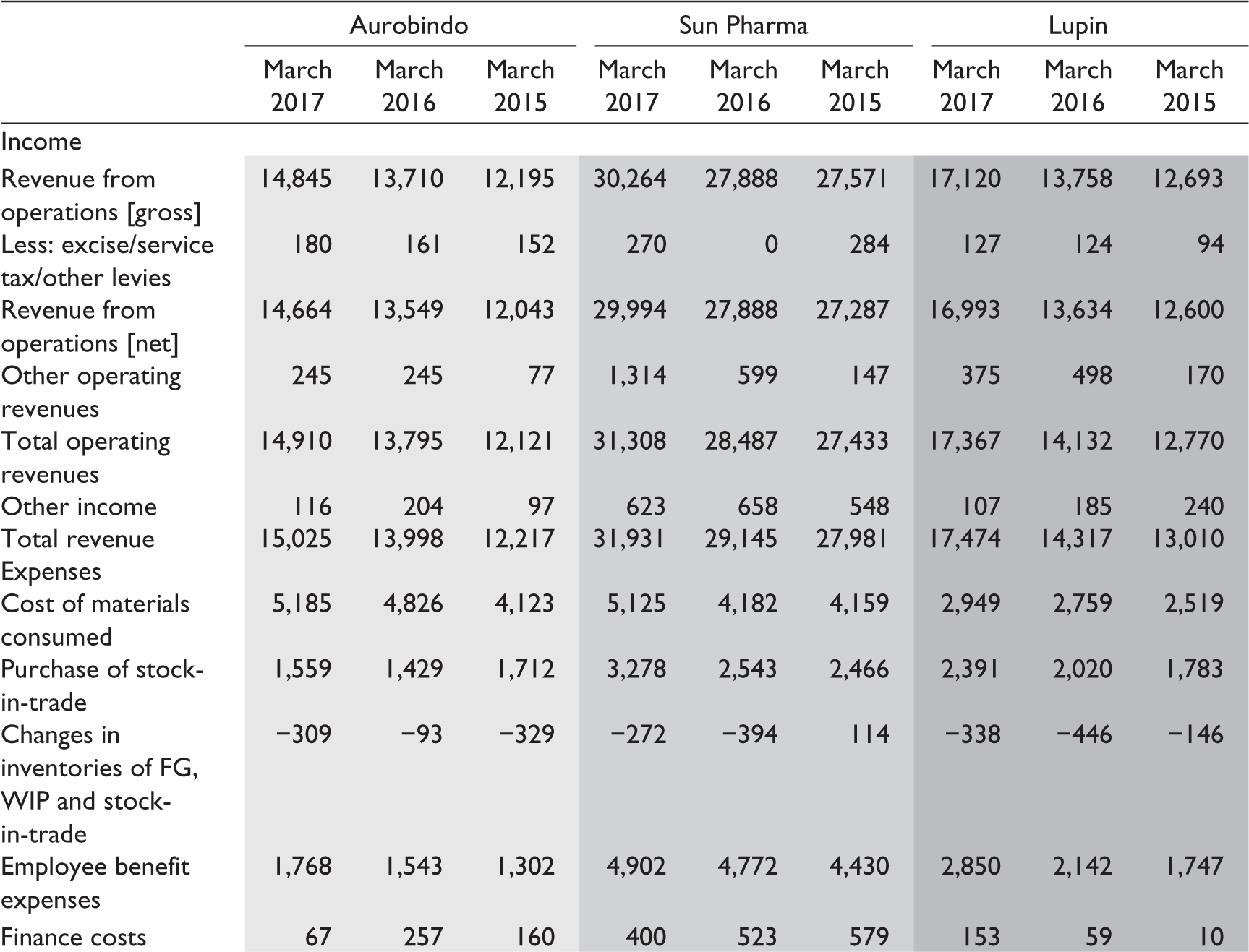

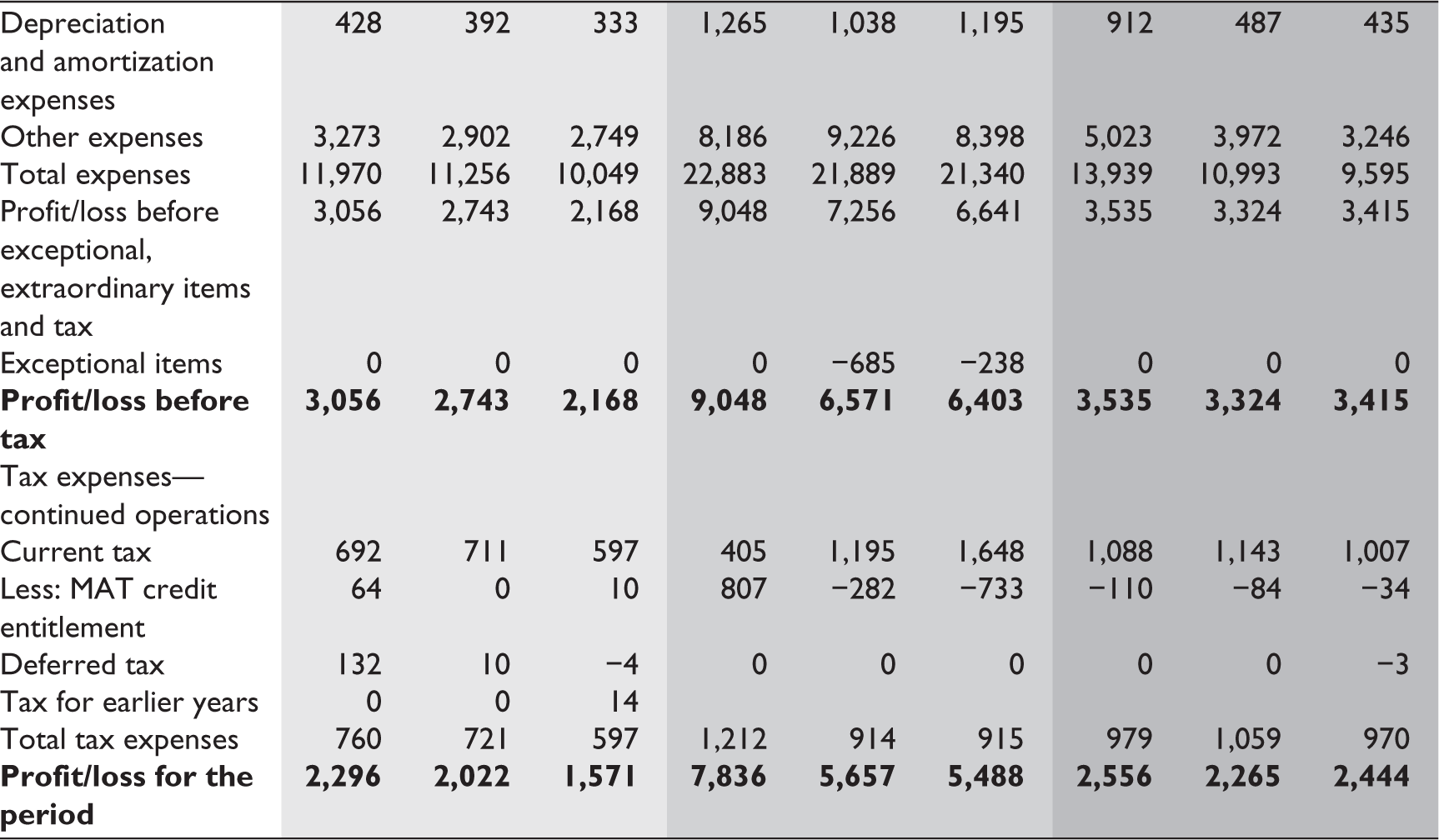

The Indian pharma industry was a crowded and fragmented space with over 10,000 manufacturers in the market. Some of the key big players were Cipla, Cadila, Intas, Glenmark and Wockhardt, to name a few (Buffer, n.d.). However, Sun Pharma, Aurobindo and Lupin were the ones that competed with DRL because of the business and market operating lines (see Table 1 for their financials).

Financials of Ccompetition (Sun Pharma, Aurobindo, and Lupin)

Sun Pharma

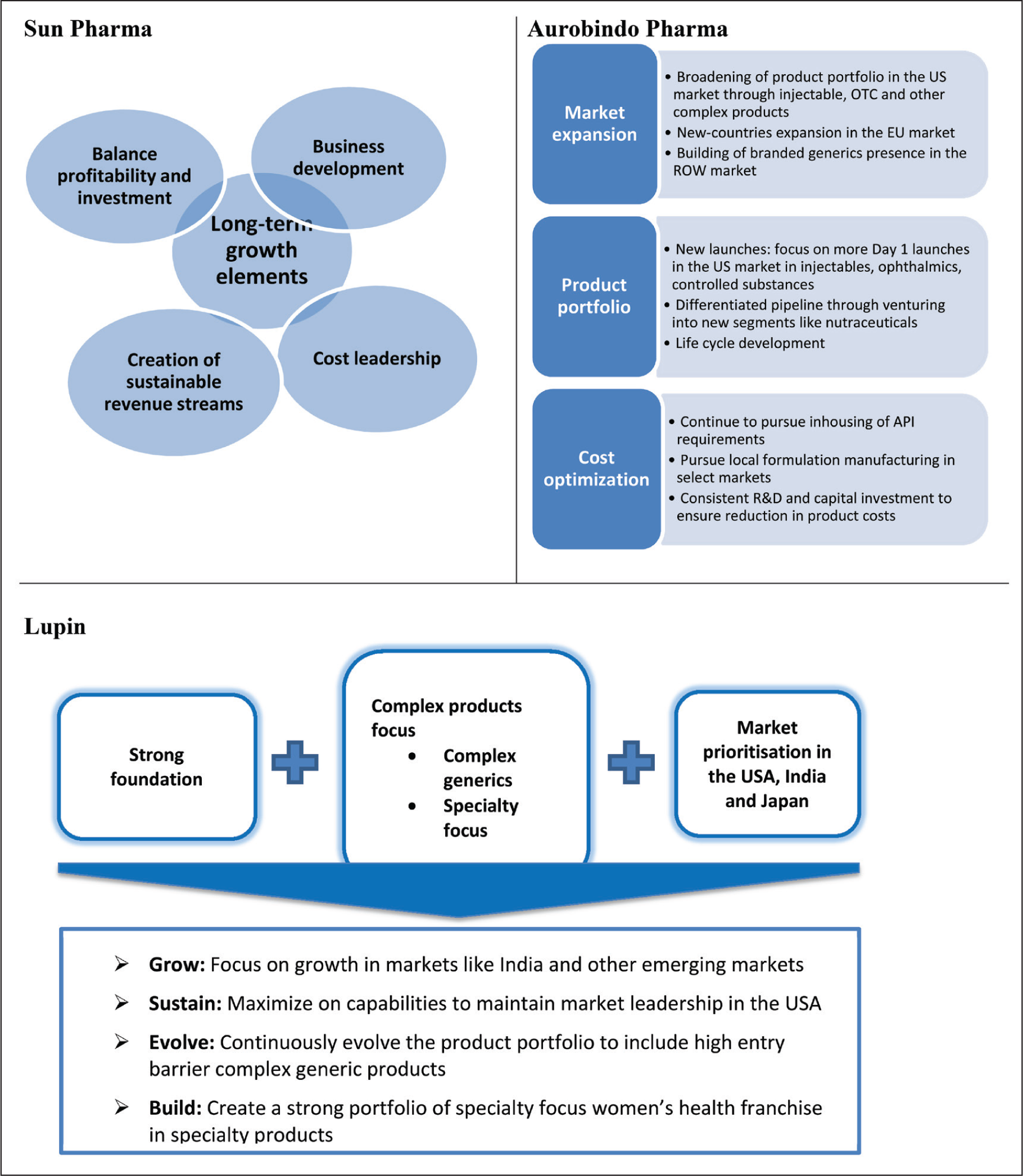

Sun Pharma, the most prominent Indian pharma company in sales and market capitalization, was based in Mumbai with a global manufacturing and marketing presence. Founded by Dilip Sanghvi in the early 1980s, it had grown significantly since then. Like DRL, Sun Pharma had its business lines across the pharma value chain and the globe. It had grown organically and inorganically through acquisitions over the years, with notable ones like Taro and Ranbaxy.(Sun Pharma, n.d.) While unveiling the company’s long-term strategic growth path, Dilip Sanghvi mentioned that the upcoming big things for Sun Pharma were speciality (Business Standard, 2017) and complex products (Business Standard, 2019a). The key elements of the long-term growth strategy identified are depicted in Figure 5.

The key strengths of Sun pharma were:

Strong pipeline of products in key geographies, like the United States; Strong portfolio presence across various therapeutic areas in the Indian market; Acquired and turnaround companies; and Strong financial discipline and cost control.

Aurobindo Pharma

Aurobindo Pharma was yet another offshoot of a Hyderabad-based entrepreneur’s dream come true in the pharmaceutical space. Founded in the mid-1980s by Ramprasad Reddy and Nithyananda Reddy as a small bulk-drug manufacturer, it grew at a rapid pace, closing in on sales of US $3 billion. Along with DRL, Aurobindo always had been a big force in the pharma space. It was one of the top five pharma companies in the US market (the toughest one) by prescriptions. Aurobindo was vertically integrated with 70% of its API requirements supplied in-house, making it one of the most attractive vertically integrated pharma companies. Its revenue mix was 80% formulations and the remaining API (Aurobindo, n.d.). In revenues, the United States accounted for the largest share of formulations business at 40% (Business Standard, 2019b); the rest came from Europe, Rest-of-the-World (ROW) and anti-retroviral businesses. The key elements of the long-term growth strategy of Aurobindo pharma are identified and depicted in Figure 5.

The key strengths (Motilal Oswal, 2016) of Aurobindo Pharma were:

Strong vertical integration (>70% API supplied in-house); Status of the fifth-largest pharma company in the US market by prescriptions; A strong and diversified product category portfolio, including complex generics, peptides, enzymes, nutraceuticals, etc.; and Regional presence across the globe without any overdependence.

Lupin

Lupin was another home-grown pharmaceutical multinational that carved a niche for itself in the growth story of Indian companies. Founded five decades ago by Dr Desh Bandhu Gupta, fondly called DBG, with an aspiration to put India on the global map, it was started as a small chemical and trading company. It grew into a fully integrated pharmaceutical company with a presence across the globe in over 100 countries. Lupin believed in the inorganic route for growth, evident from its high-profile acquisitions like Gavis, Kyowa, etc. in the recent past. Its acquisition of Gavis, a United States-based speciality products manufacturer, at US $880 million was the largest overseas acquisition by an Indian pharma company. Lupin had received a warning letter from the United States Food and Drug Administration (USFDA) when two of its manufacturing facilities ran into compliance issues. While it had tough years, Lupin was still one of the companies that invested consistently in R&D over the years, with its R&D investment peaking at 13.5% (Lupin, n.d.) of sales in 2018. The strategic vision of Lupin was to become a well-diversified pharma company (Healthworld, 2018; Nair, 2019) (see Figure 5 for the key elements of its long-term growth strategy).

The key strengths of Lupin were:

Ability to achieve a market share in the chosen markets like the United States (top-five ranking); Strong domestic presence in the Indian market; Series of successful acquisitions; and Early diversification into complex generics, speciality and biosimilar products.

Dr Reddy’s Laboratories: The Torchbearer

History

DRL’s journey started in 1984 (Dr Reddy’s, 2019–20) through the vision of its iconic founder, Dr Anji Reddy, who had always been the torchbearer in the scientific diaspora of pharma, to bring affordable medicines to patients through DRL (see Figure 6 for a brief outline of the journey of DRL). In summary, DRL transformed itself from an ingredient manufacturer with a local presence into a multinational patient-centric healthcare organization over the years.

Major Businesses

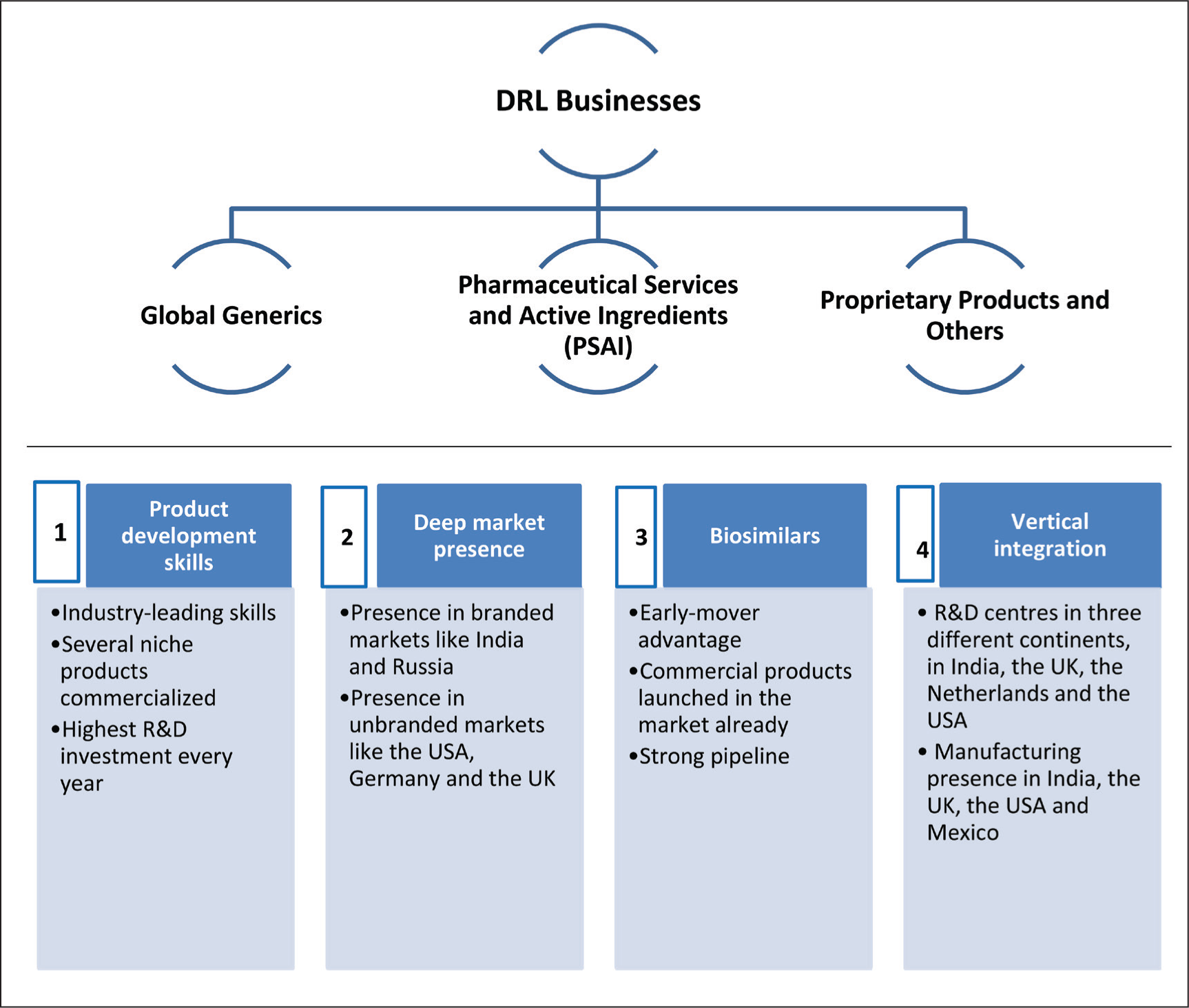

The major business lines of DRL (Dr Reddy’s, 2019–20) and its key strengths and capabilities that defined its success so far are outlined in Figure 7. First, the generic global business that supplied generics formulations across the globe was the company’s main driver and contributed 80% of the net revenues. Second, Pharmaceutical Services and Active Ingredients (PSAI) was the division that manufactured and supplied APIs across the globe, contributing 16% of the net revenues. Lastly, proprietary products and other businesses that focused on differentiated formulations contributed 4% of the revenues.

Key Strengths and Capabilities

DRL had always been termed the ‘first mover’ and had a model organization to follow for many companies. Some of the notable ‘firsts’ (Dr Reddy’s, 2019–20) achieved by DRL as a first Indian pharma company are as follows:

Listing in the New York Stock Exchange; Export of bulk drugs to Europe; Formulations entry in Russia; and Leveraging of 180-day market exclusivity in the United States.

Challenging Years

DRL has grappled with multiple challenges since the beginning of FY15. The top three are:

Issues related to FDA warning letters; Pricing pressure in the United States; and Macroeconomic changes in key emerging markets.

FY15 and FY16 were challenging years for DRL, as during this period it ran into a series of FDA issues. In FY15, three of its manufacturing facilities (two in API and one in formulations) underwent an FDA audit, which resulted in a warning letter (Siddiqui, 2015) to these facilities because of a breach in the compliance standards (Mint, 2015). The warning letter (Sridhar, 2018) prohibited the company from receiving any new product approvals in the US market while the current business could continue. Lack of new product approvals significantly affected the growth plans, as the United States was the biggest market for any new product. Moreover, customers in the West started doubting the organization’s credibility and hesitated to start a new business. The US market also witnessed huge price erosion because of increased competition and consolidation of buyers, leading to increased buying power. This had a spiralling effect on the business as well. The North American market was an important market for DRL, as it contributed over 45%. By FY17, DRL’s North American business declined by 16% in revenues, which summed up the effect (Kapoor, 2018).

DRL also grappled with issues in emerging markets. By FY17, DRL’s emerging market declined by 11%, which further complicated the issue. Two major issues that affected it were the macroeconomic conditions in Venezuela (The Pharma Letter, 2016) and the currency devaluation in Russia. Russia was its biggest market among emerging market countries, and because of the Russian rouble devaluation, DRL’s revenue declined by 29% in FY16. Venezuela used to be a profitable market for DRL as it had a huge unmet need. However, the foreign exchange constraints imposed by the government in Venezuela led to significant scaling of operations. DRL was on a market expansion spree in emerging markets over the years, which led to complexity in internal issues as well. As Satish Reddy, Vice Chairman of DRL, mentioned (Mahalingam, 2013), the aggressive market expansion (over 48 countries) led to internal complexity in operations, leading to supply disruptions.

Is It Going to Be an Unfinished Agenda?

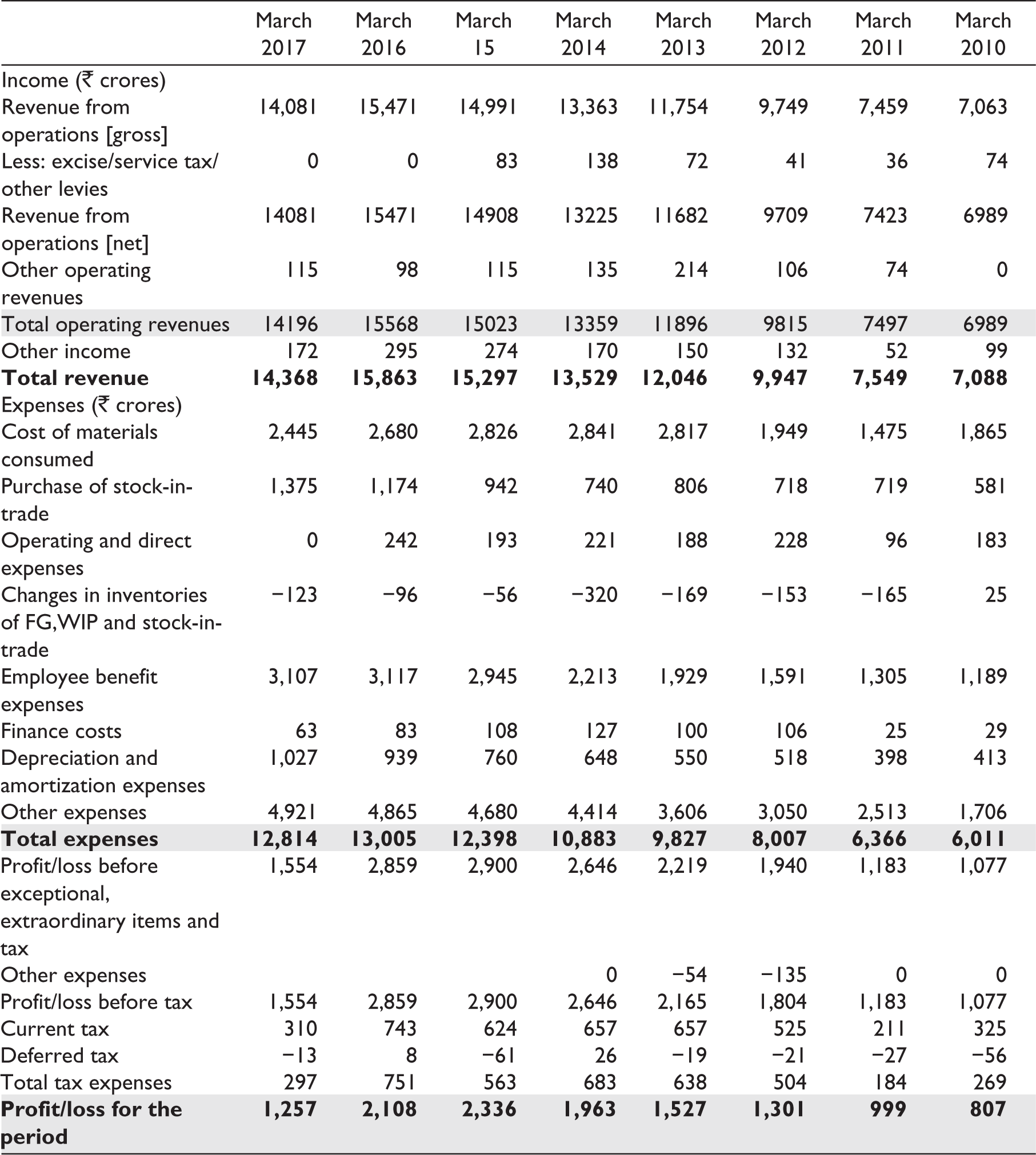

DRL had been rapidly ascending for more than a decade and been a torchbearer for the Indian pharma industry for over two decades. This was evident from the multiple milestones it had achieved and, more recently, from the fact that its gross revenue doubled and profit increased by more than two times from 2010 to 2014 (see Tables 2 and 3 for DRL’s financial statements). After this growth, DRL was expected to grow at the same speed, but then it faced stagnated revenues and declined profits. DRL attributed part of it to the ongoing FDA issues, but the rest could be attributed to increased competition, price pressure and, more importantly, increased costs.

Dr Reddy’s Laboratories Financial Statement (FY10–FY17)

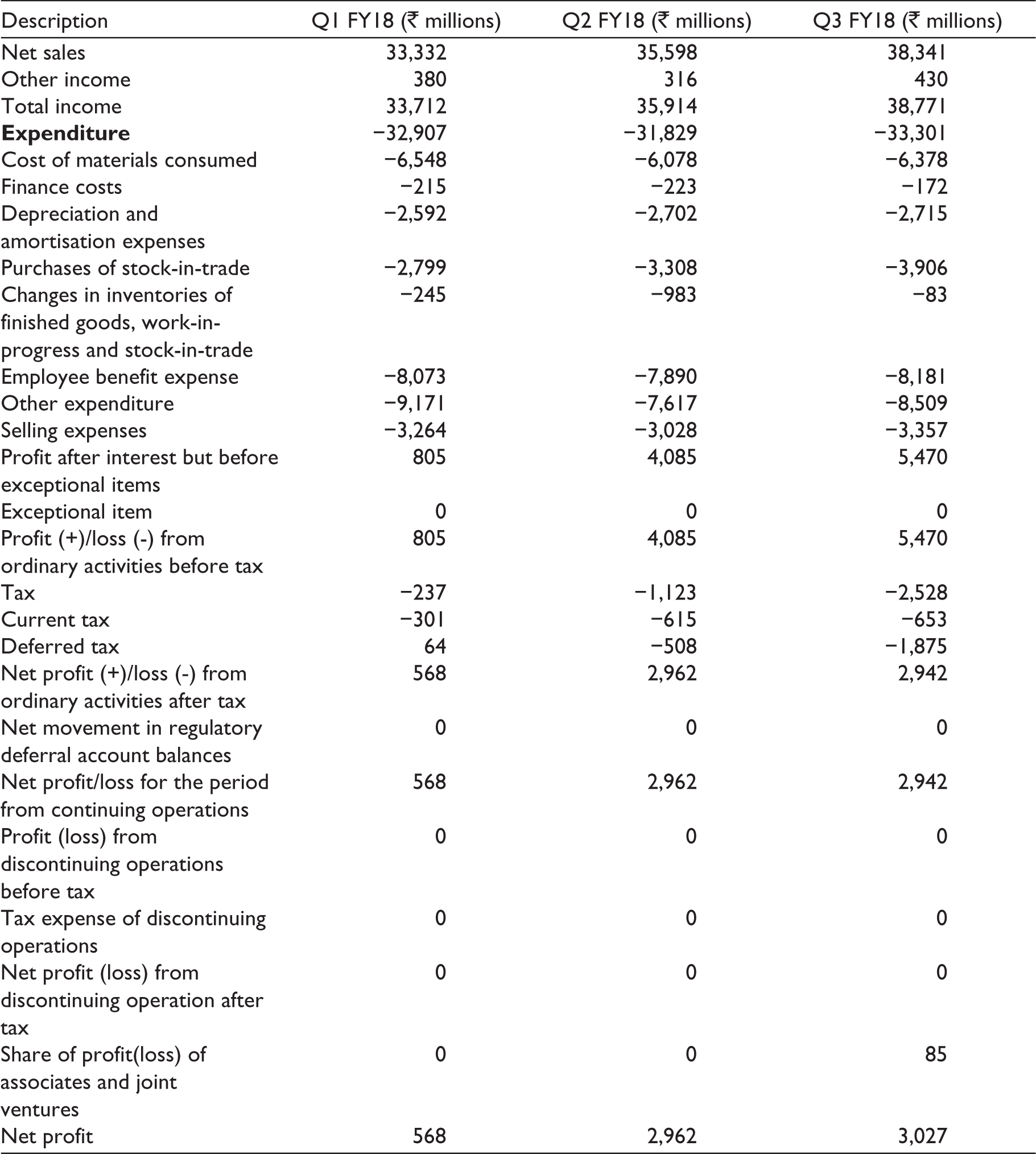

Dr Reddy’s Laboratories Financial Statement (YTD Q3 FY18)

Way Forward

While the whole world was still celebrating the new year, Prasad was in deep thought about how to wade through this ‘Perfect Storm’, as he called it in one of his letters to shareholders. He realized that this was the time for bold moves to bring the company onto a growth path in a sustainable way (see Figure 8 for the six key decision buckets and the way forward). Some of the key focus areas and the decisions surrounding him are as follows:

The time was ripe for Prasad to press the execution button while the above-mentioned key questions were in front of him to see how 2018 and beyond would pan out for DRL. The key questions on Prasad’s mind were: How should DRL sort out the long-pending FDA issues and simultaneously create and execute its emerging-market strategy? How should they innovate and infuse fresh thinking to boost the R&D engine to see growth in sales and profit? Should the company explore the option of going back to its basics or explore inorganic avenues? More specifically, what should the company’s HR strategy be, and how should they align the company’s structure with its business strategy?

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.