Abstract

The assumption of gender neutrality of budgets continues to be challenged by feminist activists, scholars, experts and practitioners. As public finance decisions have far-reaching implications, integrating feminist approaches in budgeting can go a long way in actualising positive change in the lives of women and girls, especially those from intersectionally disadvantaged backgrounds. Gender responsive budgeting offers great potential to do so. This article makes a case for strengthening gender responsive budgeting in India as an effective public finance mechanism for empowering women and girls. FY 2024–25 marked two decades since the formal adoption of gender responsive budgeting strategies by the Government of India, which is a significant milestone in India’s progress towards gender equality goals. This article takes stock of the progress on this front to date. Further, it explores the prospects for gender responsive budgeting in ‘indivisible’ sectors where much remains to be done, and outlines some actionable policy considerations for enhancing overall implementation of this strategy at the national and the State levels. Deepening and re-envisioning ongoing efforts in this direction can accelerate India’s progress towards achieving its gender equality objectives.

Keywords

Background

Progress towards gender equality in every sphere is critical for advancing human development goals. Sen (2000) envisions development as the expansion of people’s freedoms, choices and capabilities rather than the growth of income alone. Humanity as a whole cannot achieve its optimal potential while all-pervading gender inequalities inhibit the potential of women and gender minorities to lead lives they value (Hsu & Kovacevik, 2015). Sustained commitment and action towards gender responsiveness of public policy and governance is a key enabler of human development.

The year 2023 marked the midpoint of the United Nations Sustainable Development Goals (UN SDG) Agenda 2030. This is an opportune time for a midpoint review of the progress on these goals made by India so far. Of particular significance is SDG 5 targeted towards gender equality and empowering women and girls. Emphasising the importance of data-driven governance, UN SDG Indicator 5.c.1 attempts to assess whether governments allocate and monitor public funds towards gender equality and empowering women (United Nations Statistics Division, 2023). Gender responsive budgeting practices are an important step in this direction.

Drawing from Molyneux’s (1985) typology, gender responsive budgeting can cater to practical gender interests in the short term (e.g., by improving women’s access to paid work by earmarking allocations for them under MGNREGS). Strategic gender interests can be met in the long term by enshrining feminist perspectives in policies, which, for instance, can enable more equitable distribution of unpaid care work and domestic work in the household, as well as safer working conditions and prevention of sexual and gender-based violence at the workplace, thus paving the way for achieving gender equal outcomes.

This article underscores the significance of gender responsive budgeting in India for promoting gender equality and inclusion. It illustrates how the policy strategy of gender responsive budgeting serves as a substantive entry point for integrating feminist perspectives in public finance and budgets in the country. The evolution and implementation of this strategy are examined, and policy measures are proposed for deepening it to improve outcomes for women and girls.

The structure of this article is as follows. The third section introduces gender responsive budgeting. The fourth section provides a snapshot of its evolution in India with a focus on its operationalisation. The fifth section touches upon key entry points and tools for gender responsive budgeting in India and discusses notable practices which can be replicated elsewhere. The sixth section delves deeper into the Gender Budget Statement, which is a widely and increasingly adopted entry point as well as tool or instrument for gender responsive budgeting in India. The prospects of gender responsive budgeting in ‘indivisible’ sectors are explored in the seventh section. The eighth section offers policy considerations for deepening gender responsive budgeting practices in India. The ninth section offers concluding reflections.

Method

This article is based on a review of existing academic literature and policy frameworks in the domain of gender responsive budgeting internationally as well as in India. Further, relevant budget documents are reviewed and analysed to assess the effectiveness of the existing mechanisms, methods and practices being undertaken for implementing gender responsive budgeting at the level of the Union Government. These documents include the Gender Budget Statements published by the Union Government as well as some State governments for various years. A key informant interview with a sector expert has also informed the analysis.

An Overview of Gender Responsive Budgeting

‘Gender budgeting is an approach to budgeting that uses fiscal policy and administration to promote gender equality and girls’ and women’s development’ (Stotsky, 2016, p. 1). Also referred to as gender responsive budgeting, it is a public finance strategy to make budgets count for women and girls. Heavy reliance of women and girls on public services, including education and healthcare, in developing countries such as India makes it imperative to ensure that public expenditure remains responsive to their needs. Contesting the notion of gender neutrality of budgets, gender responsive budgeting aims at incorporating a gender analysis in public finance with the objective of improving outcomes for women and girls and promoting gender equality. More importantly, the prevalence of deep-rooted patriarchy in a society could lead to a further reinforcement of gender inequalities even through publicly funded services and interventions, unless a gender perspective is consciously integrated at each stage of public finance.

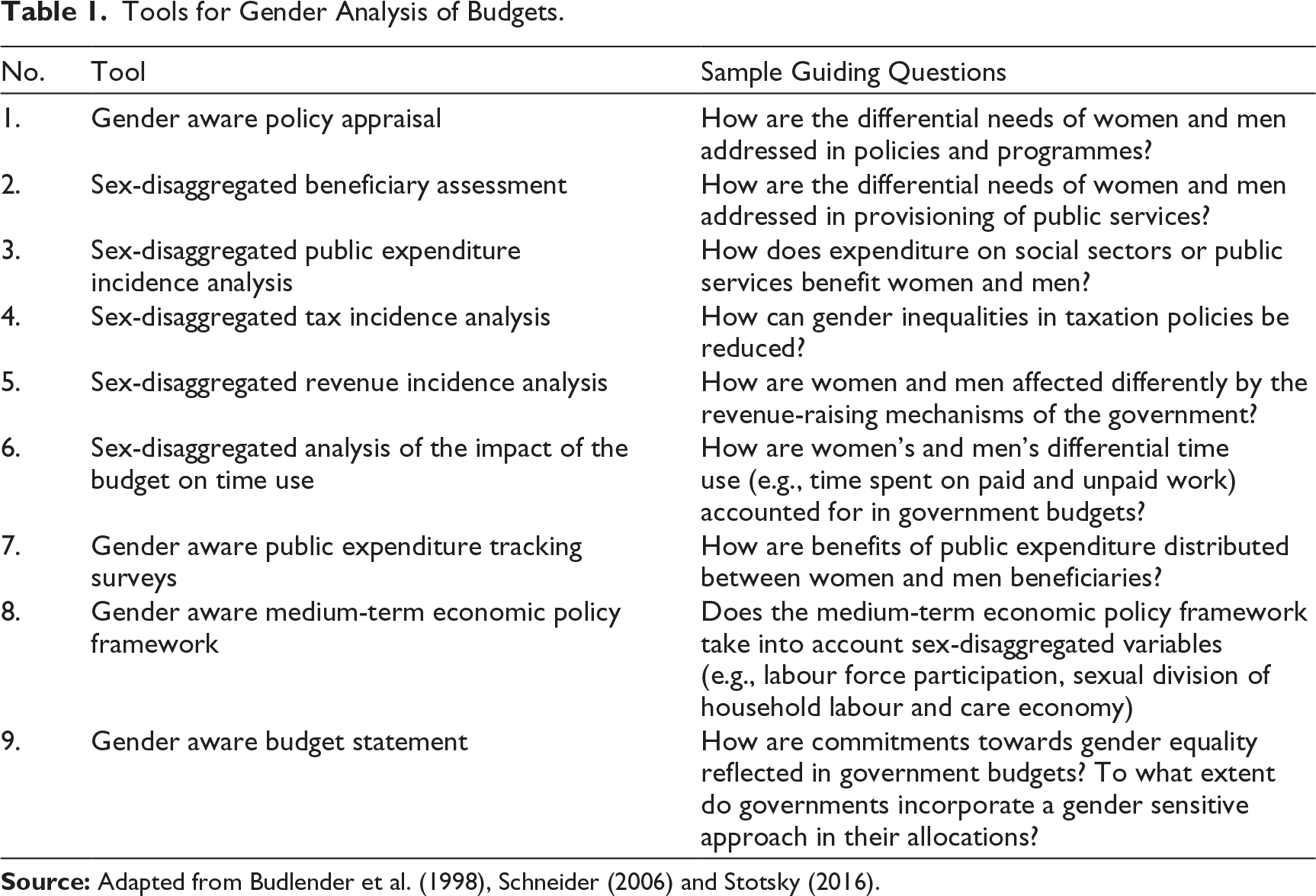

Building upon Elson’s (1997) extensive framework on making budget analyses gender sensitive, Budlender et al. (1998) and Schneider (2006) recommend several tools for gender sensitive budget analysis (Table 1).

Tools for Gender Analysis of Budgets.

Since the gender aware budget statement is the most extensively used tool for gender responsive budgeting in India, the other tools mentioned in Table 1 are beyond the scope of this article.

Gender Responsive Budgeting in India: The Story So Far

Das and Mishra (2006) trace the roots of gender responsive budgeting in India to the Seventh Five-Year Plan (1985–1990), during which allocations for 27 schemes and programmes benefiting women were tracked for the first time. The Eighth Five-Year Plan (1992–1997) of the Government of India recognised the need for targeted development programmes for women in addition to the general ones (Ministry of Women and Child Development, 2021). Subsequently, the Ninth Five-Year Plan (1997–2002) paved the way for the same with the introduction of the Women’s Component Plan under which the Union Government, as well as the State/Union Territory governments, were required to earmark at least 30% of the allocations for women in sectors related to them. The National Policy for the Empowerment of Women, released in 2001 by the Ministry of Women and Child Development, mentioned the need for gender budgeting and a gender inclusive perspective towards processes and practices (Ministry of Women and Child Development, 2015b).

The Ministry of Finance, Government of India, mandated establishing Gender Budget Cells in all the Union Ministries and Departments in 2004–05 (Ministry of Women and Child Development, 2015a). This was followed by the publication of the first Gender Budget Statement as a part of the Union Budget documents for 2005–06, which was a huge stride towards institutionalising gender responsive budgeting practices in India. Nearly two decades down the line, this juncture warrants mapping the contours of the developments hitherto and charting future directions.

It must be noted that gender responsive budgeting is not an annual one-off exercise to be performed only after the Ministry of Finance, Government of India, issues a Budget Circular to all the Union Ministries and Departments. To ensure and bolster its efficacy, it should ideally be integrated along the entire budget cycle spread across a financial year. At the initial or planning stage of the budget cycle, gender concerns need to be taken into account in scheme designs in addition to the inclusion of women in consultative policy formulation processes (Ambast et al., 2021). The budgeting stage follows the planning stage, where the composition and adequacy of the projected expenditures or the allocations need to be examined with reference to the gender priorities identified in planning. Further, a gender analysis at the implementation stage assesses the extent to which outlays translate into desirable outcomes.

Finally, at the audit stage, the Supreme Audit Institution of the country, which is the Office of the Comptroller and Auditor General (CAG) of India, conducts Performance Audits for selected Departments every year. It is essential that the CAG incorporates a gender lens in its Performance Audits of programmes and schemes. This will send a clear signal to all Departments about ‘accountability’ for gender responsive budgeting. In addition to ‘gender aware’ or ‘gender sensitised’ Performance Audits by the CAG, Gender Budget Cells of each Ministry/Department should conduct a ‘gender audit’ of the activities, outputs and services delivered by the respective Ministry/Department on an annual basis.

Entry Points and Tools for Gender Responsive Budgeting in India

Some of the popular/commonly adopted entry points for initiating Ministries/Departments (at national/State level) into gender responsive budgeting are as follows.

Institution of Gender Budget Cells across Ministries/Departments through a government order or notification.

Capacity-building programmes for the officials across Ministries/Departments.

Instructing various Ministries/Departments to start reporting in a Gender Budget Statement to be published by the respective Ministry/Department of Finance, along with the annual Budget documents.

Setting up an Inter-Departmental Monitoring Committee to provide leadership for gender responsive budgeting as well as enforce accountability of the Departments.

Of these, the most common entry point has been asking Ministries/Departments to start reporting in a Gender Budget Statement.

The following are some of the popular/commonly adopted tools or instruments for operationalising gender responsive budgeting in India.

Incorporating a gender responsive budgeting related task or requirement for all or most Departments in the Budget Circular/Budget Call Circular issued by Finance Departments every year to commence the budget preparation process for the ensuing financial year.

Publishing a Gender Budget Statement along with other budget documents.

Preparing State Action Plans for gender responsive budgeting, which some States have prepared with technical assistance from multilateral agencies such as UN Women.

Manuals and training modules for gender responsive budgeting, developed by the Ministry of Women and Child Development, Government of India; UN Women, and the Centre for Budget and Governance Accountability, India.

The Gender Budget Statement is arguably the most crucial entry point and tool for operationalising gender responsive budgeting in India. However, it is a double-edged sword; if a Department views the task of reporting in the Gender Budget Statement as the end objective of carrying out gender responsive budgeting, its efforts in this direction might hit a dead end here itself. Every Department which reports in a Gender Budget Statement needs to view the task of reporting only as a means towards larger ends. What each Department is meant to achieve through gender responsive budgeting needs to be developed and documented systematically in the form of their own goals, milestones and roadmap for gender responsive budgeting.

Notable Practices

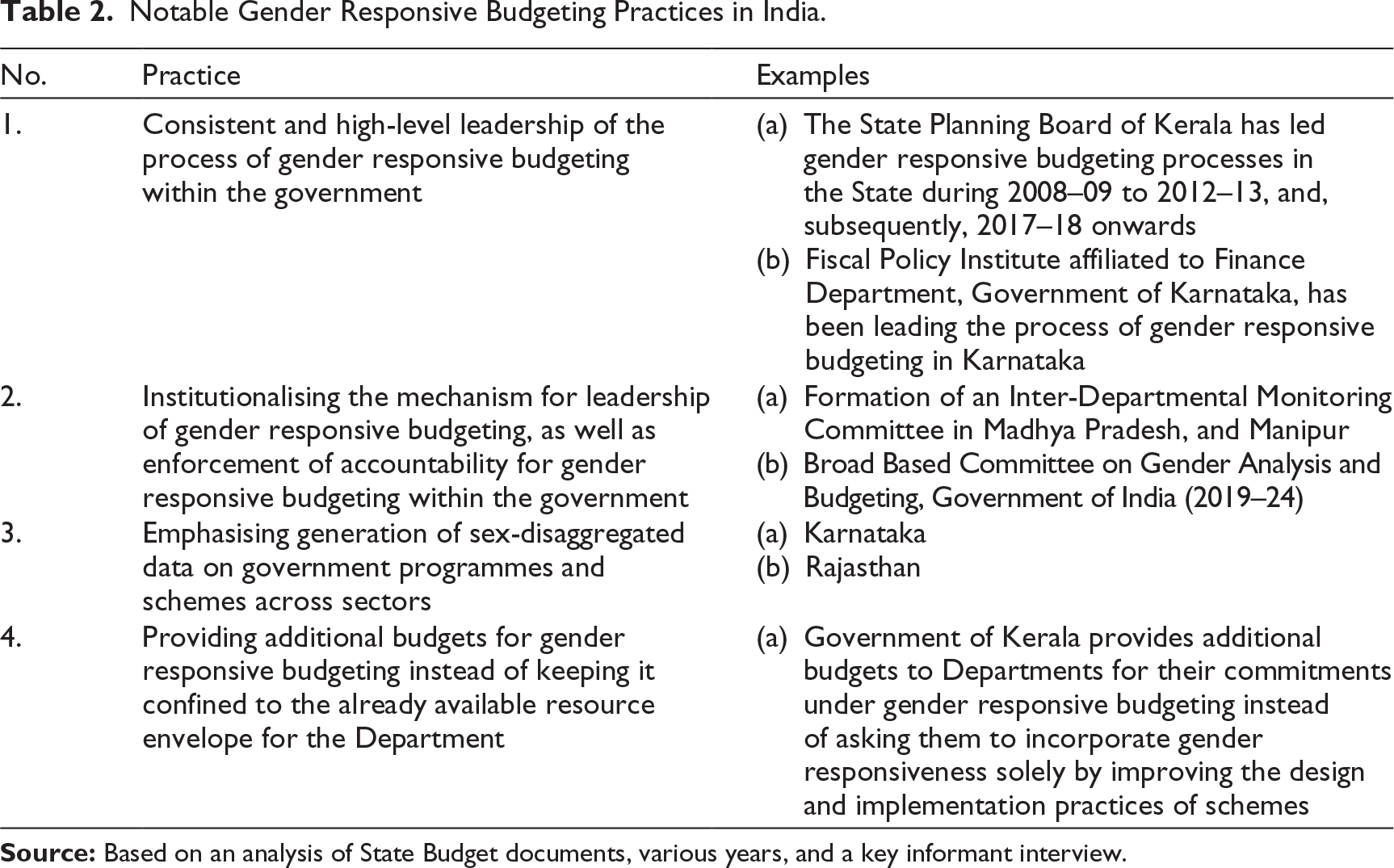

While there is no standard format followed by all State governments, it is worth noting some examples from States which can be replicated elsewhere as well as at the Union level. For example, Kerala has bifurcated its Gender Budget Statement in a manner that Part A includes interventions with 90%–100% of their allocations earmarked for women. Part B allows reporting of all interventions with less than 90% of their allocations beneficial for women (without any floor level proportion of schemes’ allocations, such as a minimum 30%). Short explanatory notes on entries in Parts A and B are provided, and a brief Transgender Budget Statement is also included.

Another recent entrant in the gender responsive budgeting domain, Manipur, has also not stipulated any floor in Part B of its Gender Budget Statement. State Departments are encouraged to report all interventions with less than 100% of pro-women allocations in Part B, which widens the scope of the exercise. Table 2 mentions some other promising examples.

Notable Gender Responsive Budgeting Practices in India.

The Gender Budget Statement: A Boon or a Bane?

As of FY 2025–26, in the context of the Government of India, Statement 13 of the Expenditure Profile publication in the Union Budget documents is referred to as the Gender Budget Statement. It is a document reporting all schemes and programmatic interventions which have a proportion of their allocations earmarked for girls and women. It is divided into two parts. Part A mentions all schemes and programmatic interventions with their entire allocation earmarked for women and girls. Examples include the scheme for the safety of women on public road transport under the Ministry of Road Transport and Highways, and the Prime Minister’s girls’ hostels under the Department of Higher Education.

Schemes and programmatic interventions with anywhere between 30% and 99% of their total allocation targeted towards the welfare of women and girls are included in Part B. Examples include, the Mahatma Gandhi National Rural Employment Guarantee Scheme under the Department of Rural Development, which also provides employment to women workers, and the Scholarships for Students with Disabilities under the Department of Empowerment of Persons with Disabilities, whose beneficiaries include female students with disabilities.

Years of advocacy by gender responsive budgeting experts culminated in the much-needed introduction of a Part C with less than 30% allocations earmarked for women and girls in the Gender Budget Statement published by the Union Government in FY 2024–25. Ministries and Departments should be encouraged to undertake a gender analysis of their interventions, particularly those pertaining to indivisible sectors, for their inclusion in Part C of the Gender Budget Statement. In addition, this move is expected to promote objective and fact-based reporting in the Gender Budget Statement by Ministries and Departments which do not have divisible schemes.

Importance

Ever since its maiden publication in the Union Budget 2005–06, the Gender Budget Statement has remained the key instrument for gender responsive budgeting in India. The number of Union Ministries and Departments reporting in the Gender Budget Statement has steadily increased from 9 in 2005–06 to 45 in 2025–26 (Ministry of Women and Child Development, 2025).

Ambast et al. (2021) emphasise the significance of the Gender Budget Statement as a tool for tracking, evaluation, transparency and accountability. It helps to analyse the trends over time in the total scheme expenditure as well as Ministry/Department-wise expenditure on components beneficial for girls and women. Moreover, it aids Ministries and Departments to assess their allocations for schemes and programmatic interventions from the perspective of gender inclusion. The Gender Budget Statement also ensures accountability because it is tabled in Parliament alongside other budget documents and is available in the public domain.

In practice, the Gender Budget Statement is a useful indicator of government’s priority towards bringing about positive changes in the lives of women and other genders. This bestows it with the potential of being a gender transformative public finance strategy. The effectiveness of the Gender Budget Statement can be improved by deploying it in conjunction with other gender responsive budgeting strategies (such as gender aware policy appraisal) and the Outcome budget (Ambast et al., 2021).

Persistent Gaps

By 2021, the Gender Budget Statement had been adopted by 37 Union Ministries and Departments, and 27 State/Union Territory governments (Pandit, 2021). Notably, the number of Union Ministries and Departments adopting the Statement had increased to 49 by 2025–26. State Nodal Centres for capacity-building on gender budgeting had also been established in 21 State/Union Territory governments by the same year (Ministry of Women and Child Development, 2021). However, several gaps have been observed which restrict the scope and purpose of this tool. These are briefly discussed as follows.

Largely An ‘Ex-post’ Exercise

The preparation of the Gender Budget Statement is not simultaneous with the formulation stage of the budget cycle. Rather, it remains an ex-post exercise wherein reporting is an end in itself (Kaul & Shrivastava, 2013). Gender concerns tend to be taken into account after the funds have been allocated for the various programmes and schemes across the Ministries and Departments (for the ensuing budget), mainly for the purpose of reporting in the Gender Budget Statement, rather than before these budgetary allocations for various programmes and schemes are made (ex-ante). The preparation of the Gender Budget Statement after the allocation of budgets for schemes limits its potential to include gender concerns as a policy and budgetary priority at the planning stage (United Nations Economic and Social Commission for Asia and the Pacific, 2018).

Unclear Rationale

The format of the Gender Budget Statement developed by the Government of India and several State governments is largely quantitative, with no qualitative explanations justifying the inclusion of certain entries in either Part. For instance, from the Union Government’s Gender Budget Statement 2025–26, it is unclear why three Autonomous Bodies under the Ministry of Ayush (National Institute of Ayurveda, Central Council for Research in Siddha and Central Council for Research in Ayurvedic Sciences) have been reported in Part A when these are not exclusively meant for women, or the Department of Higher Education included grants for promotion of Indian languages in Part B. Moreover, there is little clarity or explanation regarding how the proportion of allocations included in Part B is computed by each Ministry/Department.

Exclusion of Indivisible Sectors

A large number of Ministries/Departments whose interventions potentially benefit women and girls are excluded from the ambit of the Gender Budget Statement. As of 2025–26, these include the Ministry of Environment, Forests and Climate Change and the Ministry of Law and Justice. Despite the well-acknowledged disproportionate impact of disasters and environmental degradation on women, neither disaster management nor climate change finds a mention in the Gender Budget Statement.

Sectors considered indivisible, such as infrastructure and transport, also tend to exclude themselves from the Gender Budget Statement on the grounds that their benefits to women cannot be measured or quantified. However, roads can be made more women-friendly through adequate lighting and improving connectivity, especially in rural areas, among others (Dewan, 2012). Similarly, improving the quality of public transport to make these more accessible and safer for women, including those who are pregnant, menstruating and have disabilities, are gender responsive components for which funds can be proportionally allocated. These concerns are revisited and elaborated upon in the next section ‘Prospects: Gender Responsive Budgeting in Indivisible Sectors’.

Lack of Disaggregated Data

The absence of sex-disaggregated data impacts the quality of allocations. For instance, while the National Crime Records Bureau releases data on crimes against women in its annually published reports, data disaggregated by sex, caste, age, disability status, income and other social attributes is scarcely available (Kaul & Shrivastava, 2013). Data disaggregated at various levels can help not only to design schemes and programmatic interventions for addressing intersectional forms of gender-based violence but also route budgetary priorities accordingly prior to determining outlays.

Prospects: Gender Responsive Budgeting in Indivisible Sectors

Physical infrastructure, transport and mobility, road connectivity and power comprise some of the sectors considered ‘indivisible’ owing to the difficulties in measuring, quantifying, distributing and disaggregating their utilisation and benefits. The assumption of gender neutrality of infrastructural sectors ought to be challenged due to gendered differentials in patterns of demand and use of infrastructure (The Solutions Lab, n.d.).

Zhang et al.’s (2022) large-scale household survey in six Indian states finds evidence of intra-household gender inequalities in energy services, manifested in the form of awareness deficit, difficulties in access and differences in usage patterns of women vis-à-vis men. Moreover, intersectional disadvantages stemming from various social identities and ascribed characteristics have a bearing on not only women’s necessities but also their access to various resources, services and facilities.

Dewan (2012) argues that ensuring availability, affordability and access is key to addressing gender inequalities in physical infrastructure, transport, mobility and road connectivity, among others. To illustrate, mobility patterns show variations for women and men in terms of the purpose, patterns, distance, frequency, time, mode and safety of travel; more so as women frequently have to travel with children or other dependents (Dewan, 2012; Ollivier et al., 2022). Pregnancy, menstruation, disability and other medical conditions place significant constraints upon women’s mobility, especially in rural areas where road connectivity may be poor and public facilities are located at further distances. Such specificities point towards the need for targeted investments and budgetary priorities towards making physical infrastructure gender responsive, and eliminating various barriers impeding women’s access.

How can concerns of gender inclusion and responsiveness be incorporated in urban infrastructure, transport and mobility? Suggested design and policy measures include constructing and maintaining wide and well-lit footpaths with clear signages for pedestrians, adequate seating arrangements for women, children, the elderly and persons with disabilities in public spaces used round-the-clock such as bus stops and train stations; as well as the provision of functional restrooms segregated by gender, including gender neutral restrooms and those accessible for persons with disabilities (Ollivier et al., 2022). Incorporating such gender responsive and inclusive components in urban infrastructure design alongside their maintenance requires sustained investments, for which gender responsive budgeting has an integral role to play.

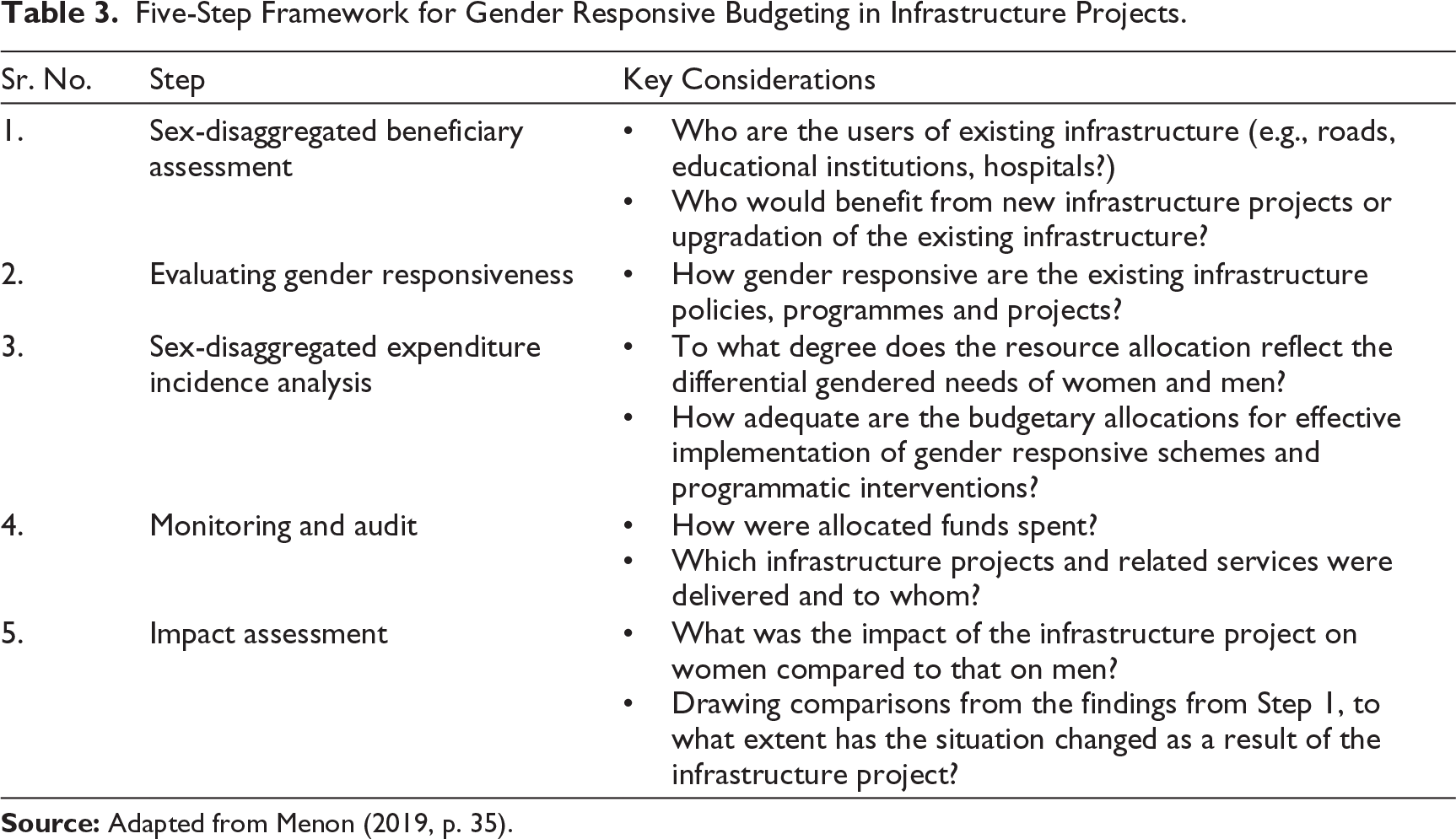

Drawing from the five-step framework discussed by Budlender (2002), Menon (2019) proposes the following measures for implementing gender responsive budgeting in the infrastructure sector (Table 3).

Five-Step Framework for Gender Responsive Budgeting in Infrastructure Projects.

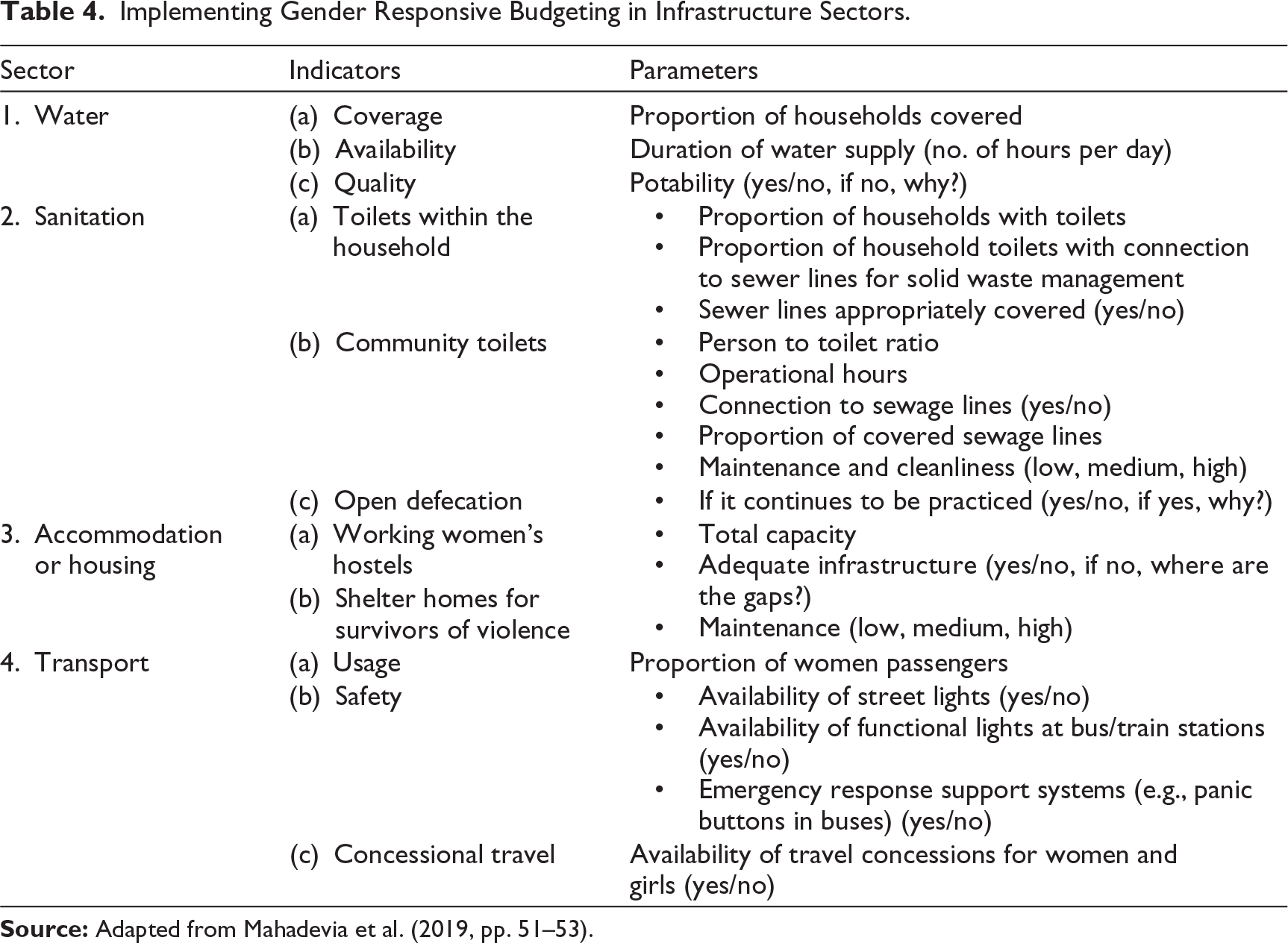

In the Indian context, Mahadevia et al. (2019) examined select aspects of urban development from the lens of gender responsive budgeting in two metropolitan cities. Based on the sectors, indicators and parameters they identified, a framework is proposed to guide ex-ante gender responsive budgeting in infrastructure (Table 4).

Ex-ante gender responsive budgeting entails identifying the needs of women and girls before allocating funds. Collecting data using the indicators and parameters can inform evidence-based budgeting, which can also be more gender responsive. It should be noted that the framework in Table 4 is illustrative and can be used to inform the design of sector-specific surveys to capture the required information.

Implementing Gender Responsive Budgeting in Infrastructure Sectors.

A notable case study is the gender policy lab (GPL), a first-of-its-kind initiative launched by the Greater Chennai Corporation using the Nirbhaya Fund in 2022. A 2021 gender gap assessment in Chennai shed light on the lack of gender sensitive infrastructure in public transport, including buses, train stations and terminals, which impede women’s mobility (Nikore et al., 2024). Recommendations included setting up a nodal agency for streamlining the interventions under Nirbhaya Fund and strengthening coordination among all implementing agencies. This gave rise to GPL as a component of the Chennai City Partnership between the government of Tamil Nadu and the World Bank.

GPL aims to enhance safety and gender responsiveness in public spaces and public transport through research, safety audits, training and capacity-building, campaigns and collaborations to strengthen policy, infrastructure and services (Greater Chennai Corporation, n.d.). Key achievements in its first year included the installation of 65 street lights, as well as the sanctioning of 425 street lights in 152 locations by the Electrical Department; in addition to proposals being floated for enhancing the safety of numerous public toilets, approach roads, bus stops/terminuses and railway stations (Ollivier & Srinivasan, 2024). Moreover, findings of studies by GPL led to the allocation of ₹12 crore for 81 new bus stops and ₹4 crore for three pedestrian pathways (Nikore et al., 2024). The GPL model offers an example of gender informed transport planning and budgeting, which can be replicated in other cities.

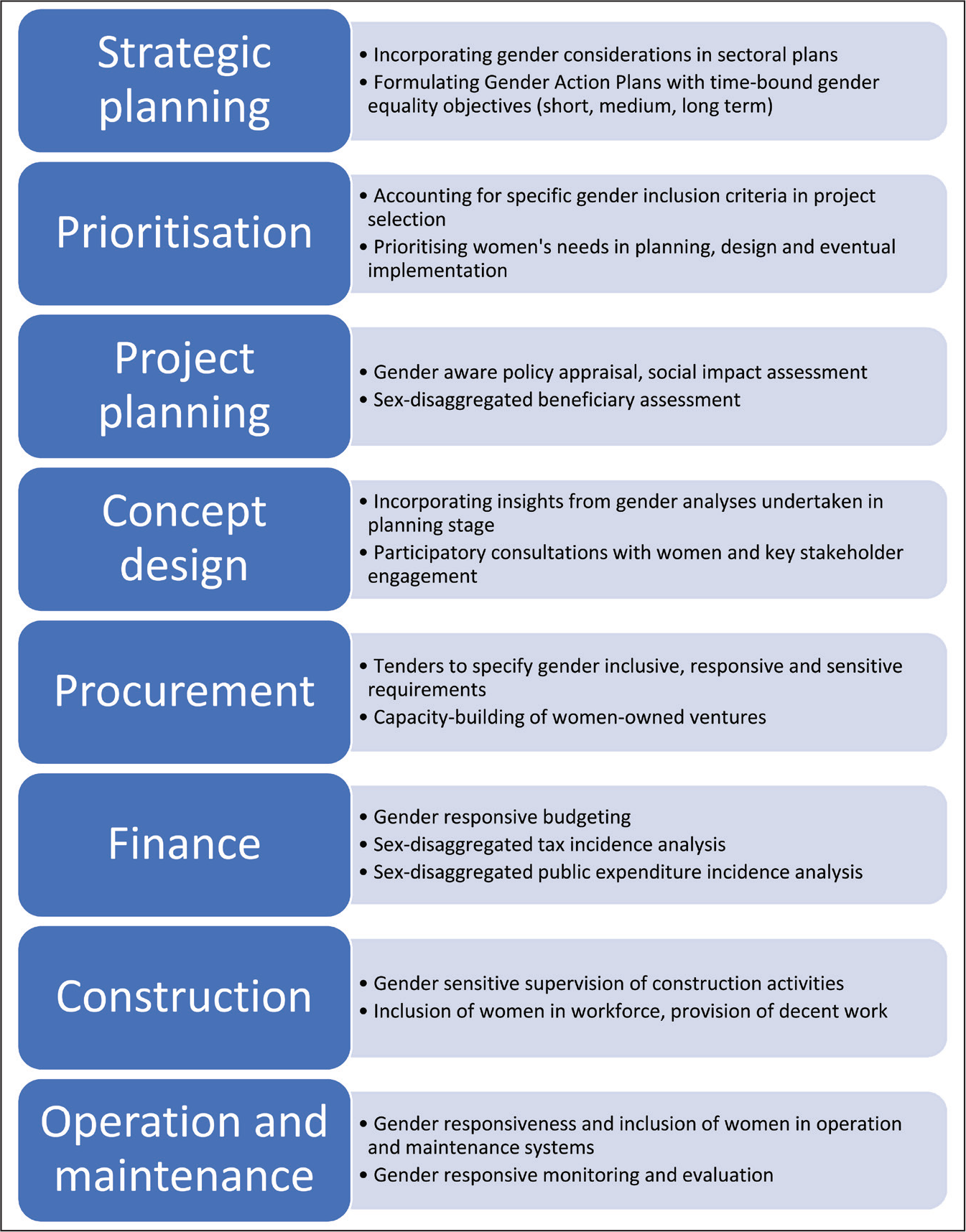

For promoting gender responsiveness in budgeting for infrastructure as well as indivisible sectors more broadly, gender considerations need to span the entire lifecycle rather than the strategic planning phase alone (Figure 1).

Alongside consistent engagement with varied analytical and evaluation tools to inform gender responsive budgeting practices, suggested complementary and cross-cutting actions include obtaining sex-disaggregated data, participatory consultations with women and other stakeholders, women’s skilling and capacity-building, addressing gender gaps in pay and workforce participation, and gender sensitisation and training of government and other functionaries (The Solutions Lab, n.d.).

It can be argued that the hitherto isolation of a large number of indivisible sectors from gender responsive budgeting processes in India has been an instance of two-way exclusion. On the one hand, the lack of a gender inclusive perspective in policy design and discourses pertaining to such sectors results in Ministries/Departments failing to adequately account for their gendered dimensions. On the other hand, the formats, structure and methods of gender responsive budgeting practices, most importantly the Gender Budget Statement, have also, to a certain extent, deterred Ministries/Departments from adopting gender responsive budgeting.

Notably, gender responsive budgeting in indivisible sectors remains under-researched in India and has not garnered enough policy attention. Alongside initiating and eventually institutionalising it at the national level, there is a need for developing standardised, evidence-based and actionable formats and methods that State governments can also emulate.

Policy Considerations

Neither do all Ministries/Departments report in the Gender Budget Statement published by the Union Government, nor do all State governments publish a Gender Budget Statement. A larger number of Ministries/Departments need to undertake gender impact assessments and report gender responsive components of their interventions in the Gender Budget Statement. Several other areas of improvement are highlighted as follows.

Ex-Ante Gender Responsive Budgeting

While both ex-post and ex-ante approaches are adopted, the latter should be the norm wherever possible so that Ministries/Departments can identify the required gender inclusive and responsive interventions before allocating funds rather than the other way round. This will also deter the reduction of the Gender Budget Statement to a reporting instrument. The ends must not be reporting alone, rather the achievement of positive outcomes indicating advancement towards gender equality goals.

Zero-based Budgeting

The less likelihood of acquiring additional funds for making their sectoral interventions gender responsive compels Ministries/Departments to carry on undertaking piecemeal efforts towards gender responsive budgeting that the ongoing incremental budgeting processes allow. Hence, a gradual transition from incremental budgeting to zero-based budgeting in some of the indivisible sectors needs mulling over.

Providing Qualitative Information with Supporting Rationale for Entries in the Gender Budget Statement

Reinstating an introductory narrative or summary note (discontinued from FY 2016–17), besides providing explanatory notes/endnotes qualifying each entry in the Gender Budget Statement, will add value to the quality of reporting therein. Indivisible sectors can consider including qualitative notes explaining the potential benefits to girls and women and how the allocations were apportioned.

Collection of Sex-disaggregated Data

Differential patterns in use and demand, particularly in the case of indivisible sectors, necessitate the collection of sex-disaggregated data on needs as well as factors constraining access (Dewan, 2012). Management Information Systems storing beneficiary data should be programmed in a manner that data disaggregated by sex and other socio-economic characteristics are collected at source. This can facilitate evidence-driven budgetary prioritisation and inform gender responsive allocations such that the needs of girls and women from intersectionally disadvantaged categories can be better addressed.

Linking the Gender Budget with the Outcome Budget

Several Union Ministries/Departments report gender-specific indicators, targets, outcomes and outlays for a number of schemes in the Output-Outcome Monitoring Framework of the Union Government. Budgetary allocations for achieving these targets and outcomes can be reported in the Gender Budget Statement (Centre for Budget and Governance Accountability, 2021), thus mapping outlays to gender-specific outcomes. Such an integration of the gender budget and outcome budget shall not only ensure allocations towards well-defined gender-specific targets but also enable tracking of expenditure and monitoring of outcomes. In the long run, it may enable greater convergence among sectors as well as among departments.

Capacity Building of Government Officials

Establishing a robust institutional architecture for gender responsive budgeting will go a long way in enhancing its implementation. One of the means for achieving this is capacity-building via regular and refresher trainings of all government officials by the Gender Budget Cells, especially of those officials who collate data for the Gender Budget Statement. Standardised training can also help to reduce inconsistencies in reporting across Ministries/Departments.

Additionally, supplementing the (usually one-off) capacity-building and training interventions with medium to long term technical handholding can augment the competencies of Ministries/Departments handling indivisible sectors, in the long run. For this, research and training around gender responsive budgeting in the indivisible sectors must be prioritised.

Concluding Reflections

Gender responsive budgeting involves integrating a gender approach throughout the budget cycle with a view to achieving gender equality and women’s empowerment objectives. An increasing number of global calls for investing in women and girls reinforce the importance of adopting gender responsive budgeting as a key public finance strategy at the national as well as the State levels in India.

The significance of integrating and institutionalising feminist principles, practices and perspectives in policy and public finance can hardly be overstated. There is a strong case for strengthening gender responsive budgeting as a feminist intervention to realise gender transformative outcomes from public financial management. It has the potential to serve both strategic and practical gender needs of women and girls.

While gender responsive budgeting can be said to have been institutionalised at the Union as well as the State levels in India (Chakraborty, 2016) over the past 20 years, there is still room for deepening its processes and practices. The feminist analysis of its processes and practices undertaken in this article, particularly with regard to the Gender Budget Statement, points towards persistent gaps which have repercussions on the gender responsiveness of allocations in different States and across various sectors.

In addition to the suggested policy measures, prioritising research and training for gender responsive budgeting in ‘indivisible’ sectors will be key imperatives for strengthening the implementation of gender responsive budgeting in India. Sustained efforts would be critical for gender equality commitments to reflect in budgetary priorities, and engendering a conducive ecosystem with multiple stakeholders to enable significant improvements in gender equality outcomes.

Feminist discourses continue to evolve over time. For gender responsive budgeting to keep pace with these developments, as well as retain its feminist character and transformative potential, it should adopt an intersectional feminist approach. Further, its focus and ambit would have to widen and become responsive to issues of not only women but also various marginalised gender identities. While noteworthy progress towards feminist goals has been achieved in its first two decades, the future roadmap should envisage further evolution of gender responsive budgeting as an intersectional feminist and inclusive ‘fiscal innovation’ (Chakraborty, 2014, p. 2) over the next two decades.

Footnotes

Acknowledgements

The author expresses her deepest gratitude to Mr Subrat Das, former Executive Director of Centre for Budget and Governance Accountability, for his invaluable guidance and suggestions. An earlier draft of this article was presented at Global Conclave 2024: ‘Advancing Human Development in the Global South’, organised by Institute of Human Development, New Delhi, in partnership with NITI Aayog, Government of India and Research and Information System for Developing Countries (RIS).

Declaration of Conflicting Interests

The author declares no potential conflict of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article: The author received no financial support for the research and authorship of this article. Open access publishing was supported by the University of Sheffield.