Abstract

Policy initiatives and regulatory changes made during the last two-and-half decades of economic reforms have led to a considerable increase in the number of mergers and acquisitions (M&As) in the Indian corporate sector. Given the policy-induced flexibilities, while the domestic firms have taken the route of mergers to restructure their business and grow, the foreign firms have preferred to enter into specific markets through acquisitions and raise monopoly power therein. In this context, the present article attempts to examine the impact of M&As on market the structure in major industries of the Indian manufacturing sector during the post-reform period. Using a panel dataset of 34 major industries for the period 2001–2009, the article finds that M&As do not necessarily cause any appreciable adverse impact on market concentration. Instead, the degrees of sellers’ concentration are influenced by the growth of market, capital intensity, firms’ advertising efforts and their financial performance. The findings of the present article, therefore, suggest for a rethink on policies and regulations relating to M&A, international trade and intellectual property, as they play a significant role in enhancing firms’ competitiveness and restricting the emergence of a monopolistic power.

Introduction

Policy initiatives and regulatory changes made in India during the last two-and-half decades’ reforms have led to a considerable increase in the number of mergers and acquisitions (M&As) 1 (Basant & Mishra, 2016; Beena, 2008). 2 While the majority of these deals were horizontal in nature, involvement of the multinational corporations (MNCs) was substantially high with share of cross-border deals being around 34 per cent during 2000–2008 (Beena, 2015). In fact, acquisition has become the predominant channel for foreign investment inflows, with the share of such deals in equity inflows increasing from 11 per cent during 1995–2000 to 27 per cent during 2000–2012 (Rao, Dhar, Ranganathan, Choudhury, & Negi, 2014). 3 However, the share of mergers in the total number of deals has declined, especially after the mid-1990s (Basant & Mishra, 2012).

According to Beena, (2008), there are three distinct phases of M&As in India’s new policy regime. While the first phase (from 1991 till 1995) was aimed at facing foreign competition, the second wave (since 1995) had significant involvement from the MNCs. In contrast, the third phase since 2000 has been characterised by overseas acquisitions by Indian firms. The number of M&As has varied considerably across major industries (Basant & Mishra, 2016); in the 1990s, the distribution of M&As across industries was influenced by factors relating to market structure, firms’ strategic behaviour and performance, and government policies (Mishra, 2011). Given the variation in the number of M&As in different industries and the causal factors, their impact on market structure also differed.

It is commonly perceived that M&As enhance firms’ market power, leading to lower competition and higher prices by eliminating the incumbent(s) from the market. On the other hand, firms can also achieve synergy or efficiency gains, with counter-effects on prices, if the benefits are passed on to consumers. When efficiency gains compensate for the anticompetitive effects of market power, consumer welfare is likely to increase. However, if the mergers are dominated by market power effects vis-à-vis efficiency gains, post-merger entry is more likely (Cabral, 2003; Davidson & Mukherjee, 2007; Spector, 2003; Werden & Froeb, 1998), enhancing competition in the market.

Thus, M&As are likely to result in a combination of diverse forces, and the net impact of such business combinations on the market structure depends on which effect is dominant. Also, the impact of M&As on market structure is influenced by other factors. Given the trends and patterns of M&As in India’s manufacturing sector in the post-reform period, it would, therefore, be interesting to examine how such business strategies have affected the structure of various markets 4 in the sector, and the present article makes an attempt in this direction.

The article is divided into seven sections. The relevant studies are reviewed in the next section, while the third section highlights emerging research issues. The fourth section of the article specifies the functional model to be estimated and hypothesises the possible impact of the independent variables. The estimation techniques applied and sources of data used are discussed in the fifth section; and the sixth section presents and discusses the regression results. The last section summarises the major findings and concludes with a discussion on policy implications; the limitations of the article and scope for future research are also highlighted in this section.

Review of Literature

There are a number of theories that explain why a firm acquires or merges with other firms. Following Trautwein (1990), these theories can be classified into five broad categories: the efficiency theory, monopoly theory, valuation theory, empire-building theory and process theory. According to the efficiency theory, M&As are executed to reduce costs by achieving scale economies (Porter, 1985; Shelton, 1988), whereas the monopoly theory considers M&As as routes to raise market power (Chatterjee, 1986; Steiner, 1975). The valuation theory suggests that a firm bids for another when it places a higher value on the target firm (Holderness & Seehan, 1985). According to the empire-building theory, managers undertake M&As to maximise their own utility rather than shareholders’ wealth (Black, 1989; Mueller, 1969; Rhoades, 1983). Finally, the process theory considers M&As as outcomes of processes that are governed by incomplete evaluations, cognitive simplifications, organisational routines and political games (Duhaime & Schwenk, 1985; Jemison & Sitkin, 1986). However, the monopoly theory and efficiency theory are considered as the two broad strands explaining the impact of M&As on market structure.

It is generally argued that M&As lead to an increase in market concentration, which in turn gives firms the opportunity to charge monopoly prices and improve financial performance. Besides, the reduction in the number of firms following a merger also facilitates post-merger collusion (Motta, 2009). There are evidences of an increase in market concentration following M&As (e.g., Hannah & Kay, 1977; Hart, Utton, & Walshe, 1973; Liebeskind, Opler, & Hatfield, 1996; Markham, 1955). In contrast, several other studies (e.g., Goldberg, 1973; Mishra, 2005; Mishra & Rao, 2014; Mueller, 1985; Weiss, 1965) have also shown either no significant change or a decline in market concentration following M&As.

Thus, the impact of M&As on market structure is not conclusive in the literature. This is so possibly because M&As are industry-specifics (Mitchell & Mulherin, 1996), and their impact on market concentration may vary depending on industry-specific factors, such as the number and size distribution of firms in an industry, entry of new firms, import competition, market expansion, other business strategies and so on. The consequences of M&As are also influenced by stages of development and the availability of financial resources (Kaur, 2012). In addition, whether a merger or an acquisition would lead to an increase in market concentration may also depend on various firm-specific factors such as the motive of a particular synergy (Banerjee & Eckard, 1998). 5 If M&As are motivated by efficient operations, they may not necessarily lead to an increase in market concentration, at least in the short run.

According to the efficiency theory, M&As help firms in reducing costs of operation through scale economies. More specifically, mergers result in greater efficiency through reorganisation of production, efficient allocation of inputs and wider sales and distribution networks (Pesendorfer, 2003). Efficiency gains may also arise from control over key inputs, product rationalisation, cutting down R&D expenditure or combined selling efforts (Ansoff & Weston, 1962; Coase, 1937). In addition, vertical integration through M&As facilitates collective organisational structure (Williamson, 2002). Greater monopoly power through M&As can enhance technological progress and result in lower costs and prices. 6 Further, with entry of the MNCs through acquisitions, one may expect spillovers of technology and managerial competencies. Many developed economies have emphasised the efficiency aspect while designing antitrust policies. 7 According to the post-Chicago school, efficiency gains and benefits to consumers should be the criteria in judging M&As (Bhattacharjea, 2010).

More importantly, while efficiency gains are expected to result in monopoly power in the long run, existing studies are not conclusive in this regard. For example, according to Schmalensee (1987), the cost-reducing effects of M&As may outweigh their collusion-enhancing impacts, whereas Williamson (1968) is of the opinion that the market power effects of a merger may sometimes result in a price increase across a wider class of firms. 8 There are also evidences of a decline in efficiency after mergers (Beena, 2015). Similarly, investigating the pricing effects of M&As in Italian banks, Focarelli and Panetta (2003) find that the short-run effects cause negative price changes for consumers, but the efficiency gains have favourable impacts on prices in the long run. On the other hand, there are evidences (Hannan & Prager, 1998; Kim & Singal, 1993) that merging banks do not pass their efficiency gains on to consumers, and there may also be M&As which can reduce efficiency and welfare even without raising market power.

Research Gaps

From the aforementioned review of literature, it is evident that the nature and extent of the impact of M&As on market structure is not conclusive, and needs further scrutiny, especially on the following grounds: First, the existing literature on competition is based on two predominant views, namely, the static and dynamic views of competition. While the static view considers competition as a state of affairs that result in the optimum allocation of resources for a given set of technological opportunities, dynamic competition is generally seen as technology-driven rivalry for markets rather than price- and output-based competition within a market. Such innovation-driven competition may cause disequilibrium in markets, particularly when entry and exit are free (Mueller, 1990). Hence, competition should be viewed as a dynamic process of rivalry (Vickers, 1995), and understanding the impact of M&A requires a dynamic framework. However, such dynamic aspects of competition following M&As have remained largely unexplored in the Indian context. Instead, antitrust policies generally focus on a static analysis limiting in-depth understanding of the impact of M&As on market concentration. For example, the studies by Khanna (1997), Roy (1999) and Mishra (2005) examine overall changes in market structure in the 1990s and do not capture the dynamics of competition. 9

Second, there are variations in mergers across industries (e.g., Basant & Mishra, 2016; Harford, 2005; Mulherin & Boone, 2000), which can be caused by both firm-specific objectives such as gaining synergy (Maquieira, Megginson, & Nail, 1998), increasing value (Bradley, Desai, & Han Kim, 1988), enhancing efficiency (Rhoades, 1998), having excess cash debt capacity (Bruner, 1988), as well as industry-level factors like economic, regulatory and technology shocks (Mitchell & Mulherin, 1996), capacity utilisation (Andrade & Stafford, 2004) and so on. Deeper understanding of the impact of M&As on market concentration, therefore, requires controlling the influence of factors relating to other structural aspects of market, firms’ strategic behaviour (other than M&As), their performance and policies of the government.

Third, while the monopoly theory postulates that firms aim at raising their market power through M&As and there are evidences of an increase in market concentration following such business strategies, in many cases, market concentration either declined or remained largely the same in the Indian context (Mishra & Rao, 2014). There are evidences of significant decline in market shares for plants acquired in horizontal mergers (Baldwin & Gorecki, 1990). Similarly, Pesendorfer (2003) found 74.1 per cent of merging firms losing market share. Such findings in the literature raise the need to re-examine the impact of M&As on market structure using a dynamic framework and controlling for the influence of other factors in the Indian context.

Finally, in contestable markets, potential competition may restrain monopoly pricing (Morrison & Winston, 1987) and incumbents may fail to raise market concentration through M&As. With the introduction of liberal policies relating to trade and investment, greater market contestability was expected to restrict incumbents’ monopolistic behaviour. But this aspect has remained largely unexplored in the Indian context. Further, recent amendments to the Indian Patent Act (1970) were expected to provide an incentive for innovation, and in-house R&D intensity (although still low) has grown significantly in recent years (Basant & Mishra, 2016). Since innovation influences market structure, the impact of M&As should be re-examined for the potential role of these amendments.

Given that the existing studies are inconclusive, and the frameworks used are not comprehensive, it is necessary to revisit M&A–market structure relationships in the Indian context using a dynamic framework. The present article is an attempt in this direction. The objective of this article is, therefore, to examine the impact of M&As on market concentration in major industries of Indian manufacturing sector during the post-reform period. This is important as the rationale of efficiency gain through competition has been instrumental in shaping India’s economic policies in the new policy regime, and the strategy of M&As, particularly integration with the MNCs, may be crucial in this regard. While the Competition Act (2002) was enacted to ensure that M&As do not have any appreciable adverse impact on competition in relevant markets, empirical evidences show that market concentration may decline or remain by and large the same following M&As (See Hart & Clarke, 1980 for the details). Since the process of economic reforms has deepened in areas like international trade, FDI and intellectual property protection, a deeper understanding of the impact of M&As on market structure is necessary for fine-tuning competition law and policy.

In the initial years of reforms, many of the country’s leading business houses were actively involved in M&As to restructure their businesses and correct inefficiencies (Basant, 2000). Since mergers enhance efficiency (Pesendorfer, 2003), 10 the competitiveness of participating firms seems to have increased. It is found that export competitiveness has increased during the post-reform period (Basant & Mishra, 2016), which can largely be attributed to M&As (Mishra & Jaiswal, 2012). Besides, there is little evidence of an improvement in financial performance (Basant & Mishra, 2016), whereas a large number of industries have recorded either a decline or no change in market concentration during the post-reform period (Mishra & Rao, 2014). Even wherever market concentration has increased, it might not have influenced financial performance as the concentration–markup relationship is not significant in a dynamic context (Mishra, 2008). There are evidences of no significant relationships between M&As and profitability at the firm level as well (Mishra & Chandra, 2010). In this perspective, re-examining the impact of M&As on market structure in the Indian context is expected to help fine-tuning of competition law and policy, especially in respect of the regulation of M&As.

Model Specification

Specification of the Econometric Model

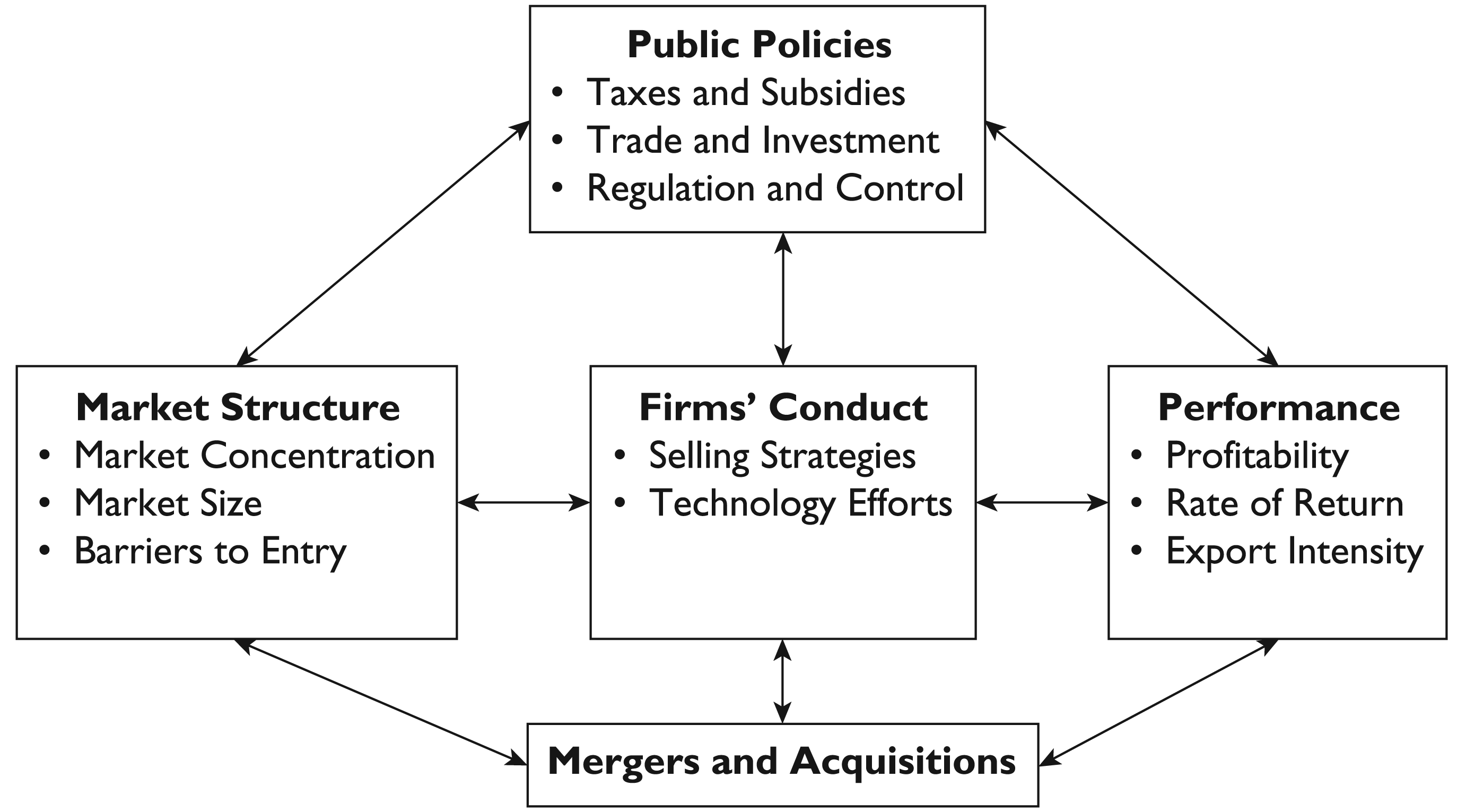

In the present article, the functional model is specified using the structure– conduct–performance (SCP) framework based on Scherer and Ross (1990). This multidirectional SCP framework recognises dual causalities between structure and conduct, between conduct and performance, and between structure and performance along with the influence of public policies as shown in Figure 1.

Given this framework, we assume that the degree of sellers’ concentration (CON) 11 in a market depends on the rate of growth of sales (GROWTH), presence of the MNCs (MNC), capital intensity (KIR), advertising intensity (ADVT), technology intensity (TECH), number of M&As (M&A), import–export ratio (IMP) and returns on capital employed (ROCE). Since examining the impact of M&As on market concentration requires a dynamic framework, the regression model envisaged also includes a lagged dependent variable as an independent variable, that is,

Here, GROWTH, MNC and KIR stand for other structural aspects of markets (other than market concentration); ADVT, TECH, M&A and IMP for strategic behaviour of firms; and ROCE for financial performance. In addition, ADVT can be a proxy for the structural aspects of markets with respect to product differentiation. Similarly, IMP can influence market competition. Further, while MNC and M&A are partly outcomes of investment and competition-related policies, IMP can capture the impact of trade policies. Similarly, TECH is a proxy for the effects of technology-related policies including regulation of intellectual property. One may also expect KIR to capture the effects of trade and technology-related policy changes.

Here, the two alternative measures of market concentration, that is, the Herfindahl–Hirschman index (HHI) and the GRS index (GRSI) are used to ensure robustness of the findings as the additive measures of market concentration suffer from various limitations (Mishra, Mohit, & Parimal, 2011). While the HHI is a widely used measure of market concentration, the GRS Index gives the most accurate measure of market concentration for the Indian manufacturing sector (Mishra et al., 2011). Hence, the use of these two alternative measures would help in ensuring robustness of the findings.

Although understanding the impact of M&As on market structure requires capturing the size of deals, non-availability of systematic data restricts us from controlling this aspect. However, with industry being the unit of analysis and the size of industry being controlled, this may not be a serious limitation. Further, some of the existing studies in the Indian context have used either a dummy variable (i.e., Dummy = 1 for firms undertaking M&A activity and Dummy = 0 otherwise) (e.g., Vyas, Narayanan, & Ramanathan, 2013) or the number of deals (e.g., Basant & Mishra, 2014) or both (Vyas et al., 2012) to examine various implications of M&As. There are also studies that have applied logarithmic transformation on the number of deals (e.g., Di Giovanni, 2005; Piñeiro, Chaitany, & Tamazia, 2008; Wang, 2008), as it is done in the present article, to measure the extent of M&As.

Better insights on the impact of M&As on market concentration also require controlling for types of deals (i.e., horizontal, vertical or conglomerations). One could even classify deals according to the nature of ownerships of firms involved (i.e., private or state-owned enterprises) or the country of origin (i.e., Indian or foreign). However, non-availability of detailed systematic data on these aspects restricts us from carrying out such an exercise. The present article examines the impact on market concentration taking all types of deals together. Since most of the deals are horizontal in nature and many involve the MNCs as well, these issues are expected to be adequately captured in the article.

Further, in the present article, all the independent variables are computed as a simple moving average of the previous 3 years of the respective measure, with the year under reference being the starting year. This makes the dataset more consistent over time, particularly when there are missing observations, and helps in controlling the dynamics of the adjustment process and potential endogeneity problem. Details on the measurement of the variables are given in the Appendix. What follows next is a discussion on the likely impact of independent variables on market concentration.

Data and Methodology

The model is estimated with a panel dataset of 34 major industries from Indian manufacturing sector over the period 2001–2002 to 2008–2009. The study period was selected for three reasons. First, since M&As during 1995–2000 significantly involved the MNCs, which have a distinct edge, the market structure was likely to be affected in subsequent years. Second, there were three important amendments to the Indian Patent Act (1970) since the late 1990s, namely, the Patent First Amendment Act in 1999, the Patent (Second Amendment) Bill in 2002 and the Patent (Amendment) Bill in 2005. These amendments were expected to incentivise firms to innovate, influencing their competitiveness. Third, stable economic conditions and changes in macroeconomic policies since the early 2000s were likely to influence the market structure. Thus, examining the impact of M&As on market structure during 2001–2009 is expected to provide comprehensive insights.

This article does not consider the data period beyond 2008–2009 as the pace of M&As slackened during 2008–2014 (Basant & Mishra, 2016). Further, due to the global slowdown since 2009–2010, consideration of this phase may cause unusual truncation in the envisaged relationships.

Since competition is a dynamic process (Hayek, 1948; Vickers, 1995), the present article estimates the following Arellano-Bond dynamic panel data model:

The estimation techniques in Arellano–Bond dynamic panel data model are based on the generalised method of moments (GMM). Compared to the application of the method of instrumental variables (e.g., Balestra & Nerlove, 1966; Bhargava & Sargan, 1983), the GMM estimators can bring in more information on data (Ahn & Schmidt, 1995). The Arellano and Bond (1991) GMM estimators are also consistent and more efficient than the Anderson and Hsiao (1982) estimators and have generalisations that can address the issue of heteroscedasticity, specification tests and so on. They uncover the joint effects of explanatory variables on the dependent variable and control potential bias due to endogeneity. 12 In order to control the endogeneity bias further, one-year lagged values of explanatory variables are used as instruments. 13 Such a lagged structure also helps in capturing non-instantaneous relationships.

The article uses market size (MSZ), marketing and distribution intensity (MDI) and profitability (PROF) as additional instruments. In addition, the presence of autocorrelation and validity of the instruments are tested by applying the Arellano–Bond test for autocovariance and the Sargan test (1958) of over-identifying restrictions. We use both the one-step and two-step estimators. While the two-step estimates are used for model specification and overall significance of the estimated model, inferences on individual coefficients are based on the one-step estimates, as their asymptotic standard errors are unbiased and reliable.

In addition to the dynamic model, static panel data models with a proportionate change in market concentration as the dependent variable are also estimated for confirming the results. Three models, namely, the pooled regression model, the fixed effects model (FEM) and the random effects model (REM) are estimated. In order to select the appropriate model, three tests, that is, the restricted F-test, the Breusch–Pagan Lagrange multiplier test (1980) and the Hausman specification test (1978) are carried out. The restricted F-test is used to make a choice between the pooled regression model and the FEM, whereas the Breusch–Pagan Lagrange multiplier test is applied to make a selection between the pooled regression model and the REM. In the event that both the REM and the FEM are chosen over the pooled regression model, the Hausman specification test is applied to select between the two.

The data are sourced from various databases of the Centre for Monitoring Indian Economy (CMIE). While information on M&As are compiled from the Business-Beacon database of the CMIE, data on the rest of the variables are collected from the Prowess database of the organisation.

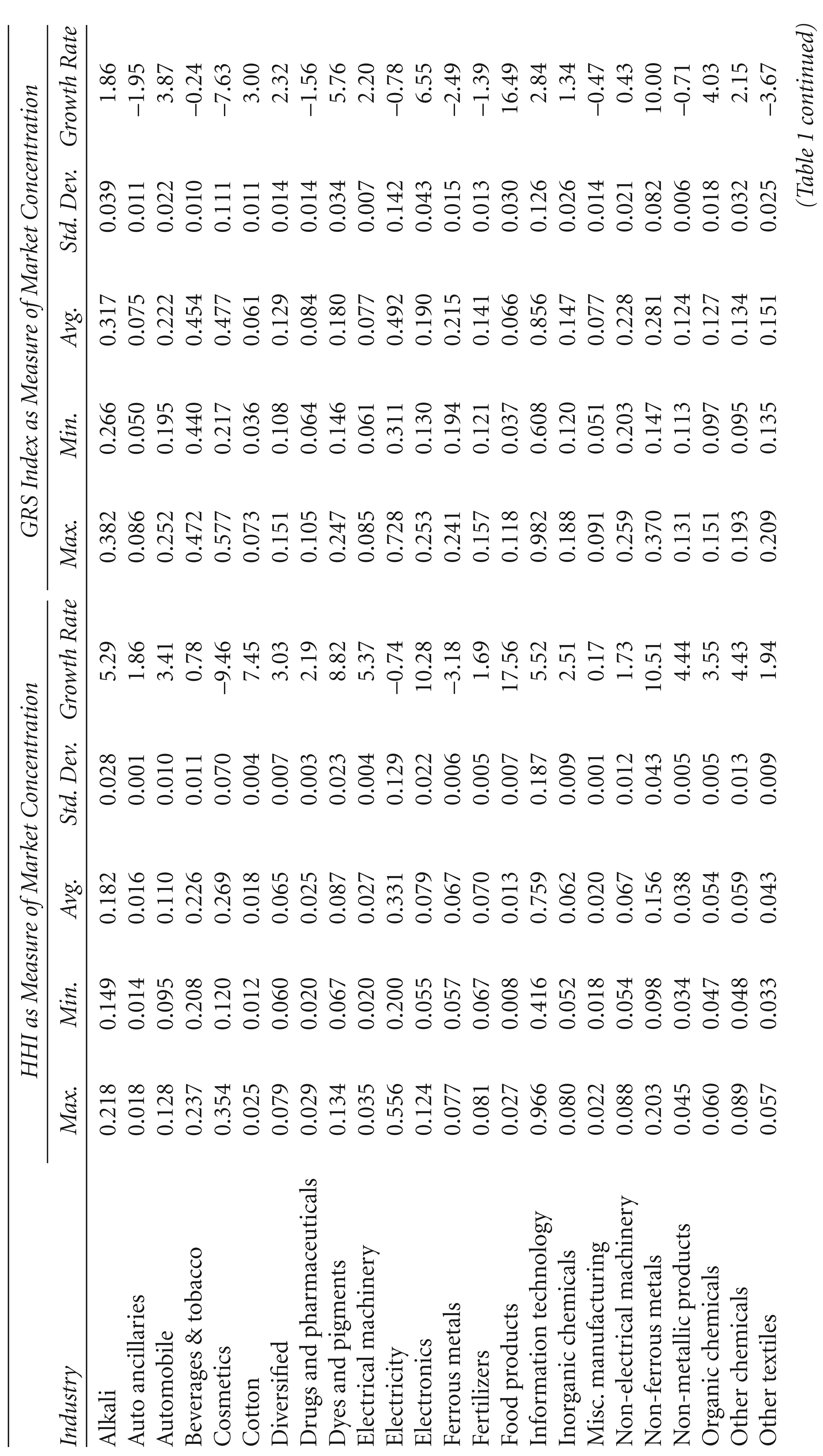

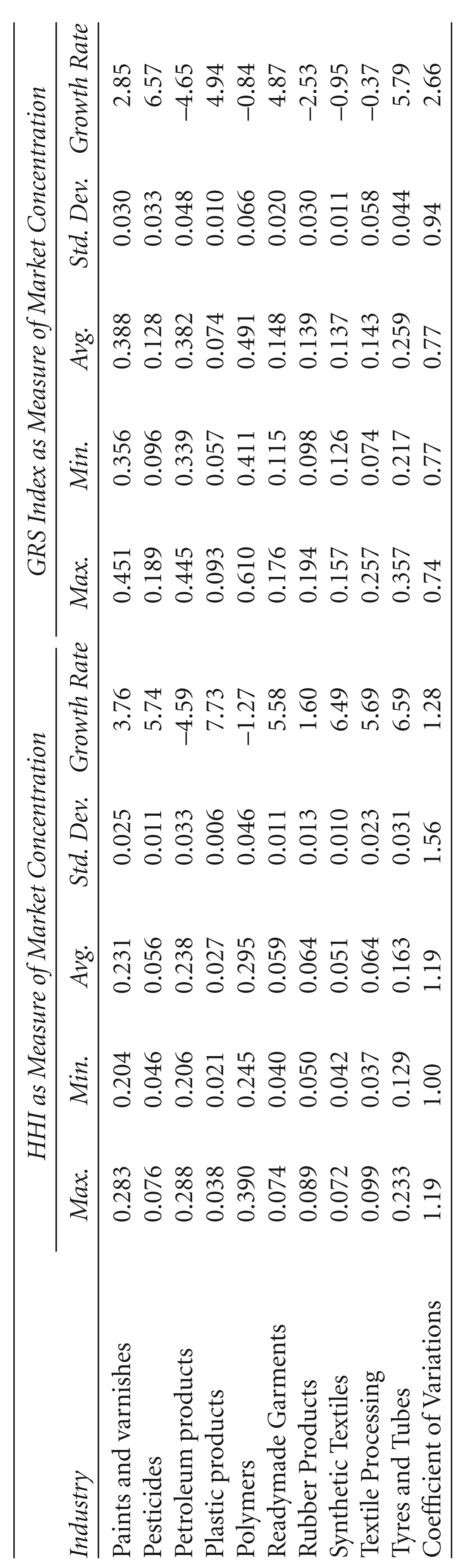

Table 1 shows the levels and changes in market concentration in major industries of Indian manufacturing sector during 2001–2008 across their alternatives measures. It is observed that the levels and changes in market concentration differ across industries. For example, while market concentration has increased for majority of the industries during 2001–2008, there are industries like cosmetics, ferrous metals, petroleum products and so on, where both the indices have recorded negative growth. Further, while market concentration in electronics, food products, non-ferrous metals and so on, has increased at a very high rate, the rate of growth is marginal in many industries. Such inter-industry variations in level and changes in market concentrations are well reflected in high value of coefficient of variations. It is, therefore, necessary to examine how M&As have contributed to such differences/changes in market structure. What follows next is an attempt in this direction.

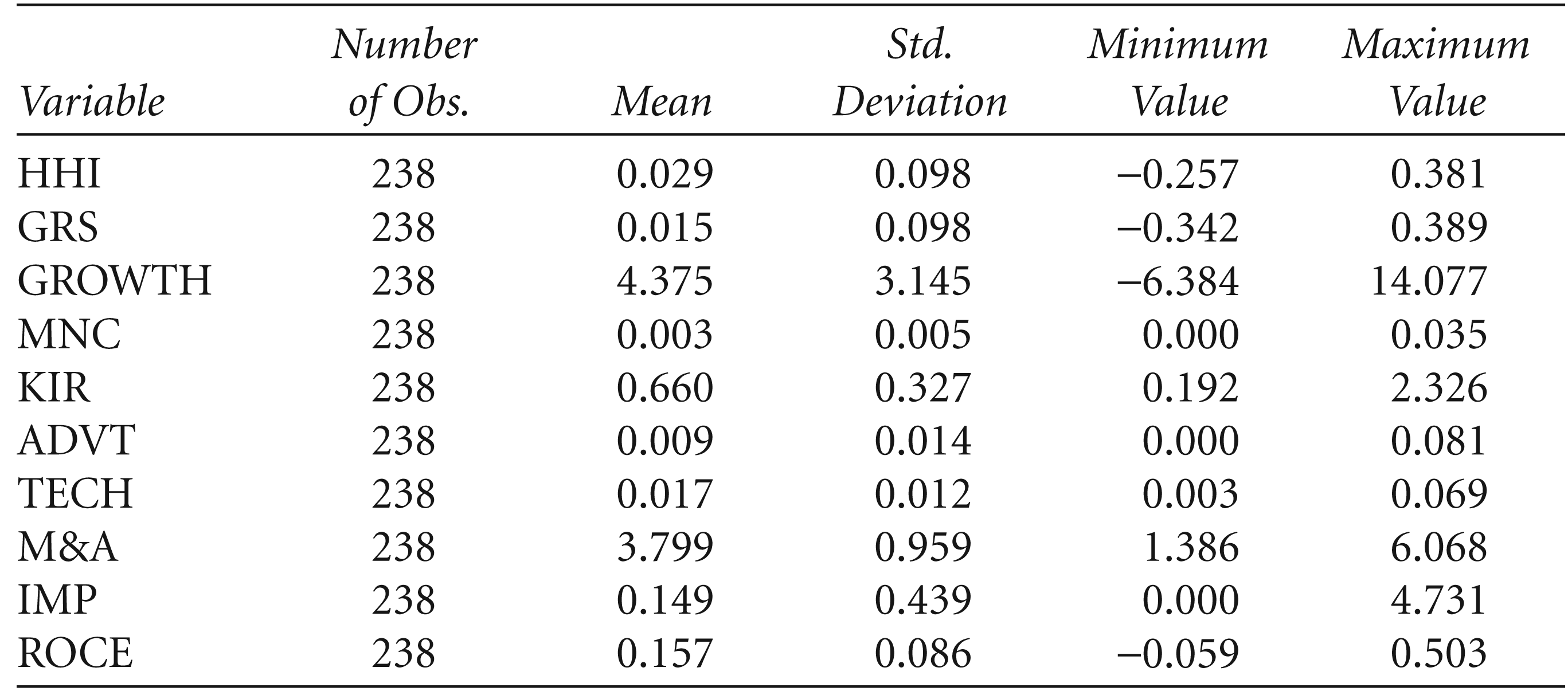

Summary statistics of variables used for estimating the static panel data models are given in Table 2. Table 3 presents the test statistics for selection of appropriate model. Since the restricted F-statistic is statistically significant, the FEM is selected over the pooled regression model. The Breush–Pagan Lagrange multiplier test also suggests that the REM is preferred to the pooled regression model. However, following the Hausman test, the FEM is finally selected and the results of this model as given in Table 4 are used for analysis of individual coefficients.

It is observed that the estimated FEMs are statistically significant. However, the low value of R2 is not a problem here as it has a very modest role in the regression analysis (Goldberger, 1991). The t-statistics for individual coefficients are computed using White’s (1980) robust standard errors to control for heteroscedasticity.

Table 4 shows that the coefficients of GROWTH, IMP and ROCE are statistically significant. While the coefficients of IMP ROCE are positive, those of GROWTH are negative. Thus, in a static framework, change in market concentration depends directly on the ratio of imports to exports and returns on capital employed but inversely on the growth of sales of markets. The coefficients of M&A, MNC, KIR, ADVT and TECH are not significant. Thus, the static panel data models show that M&As do not have any significant impact on changes in market concentration.

Changing Structure of Markets in Major Industries in the Indian Manufacturing Sector, 2001–2008

Changing Structure of Markets in Major Industries in the Indian Manufacturing Sector, 2001–2008

Notes: Max.: maximum, Min.: minimum, Avg.: average.

Summary Statistics of Variables Used in Static Panel Data Models

Tests for Selection of Appropriate Model for Variations in Return on Assets

Note: *statistically significant at the 5% level.

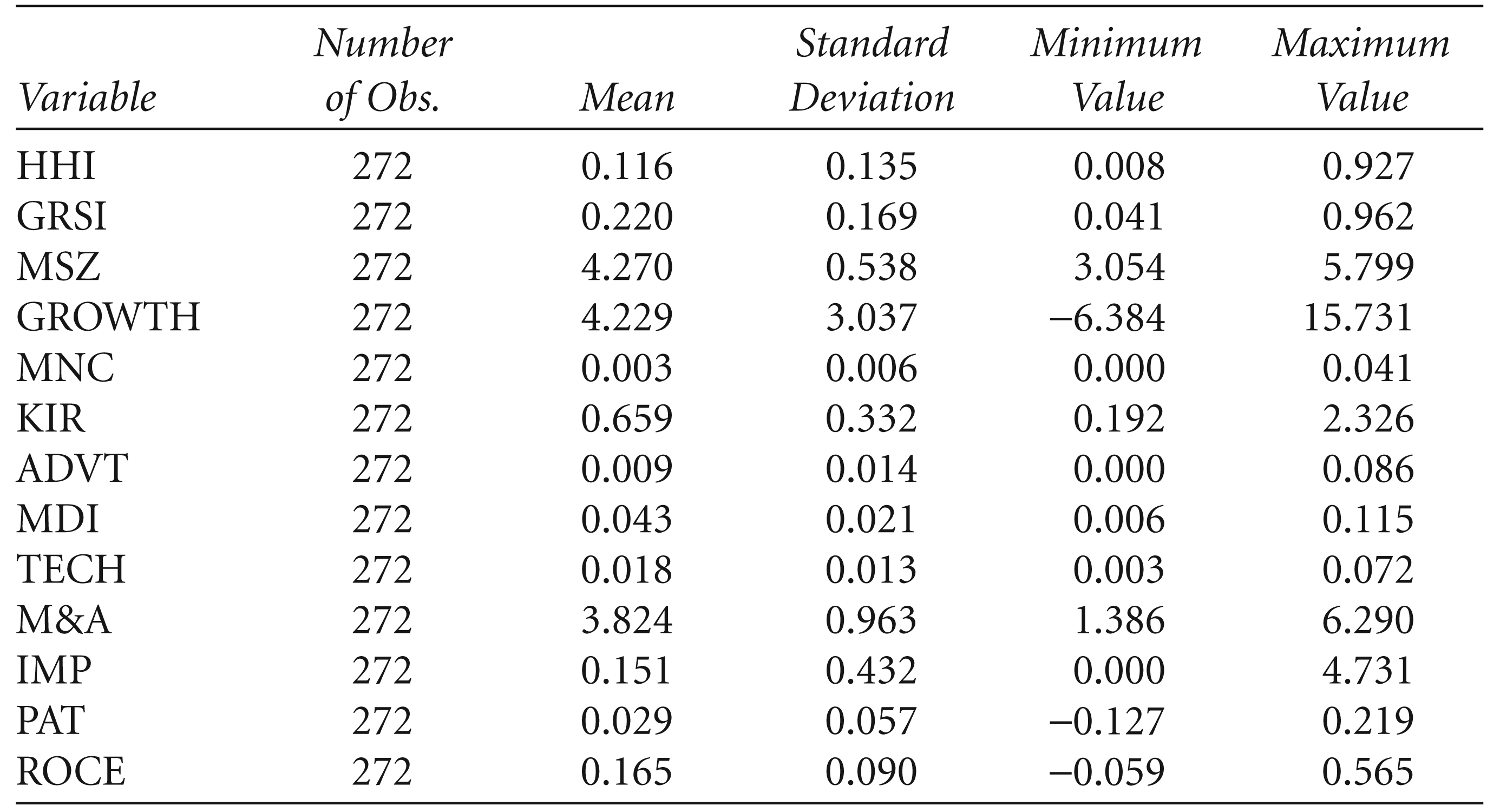

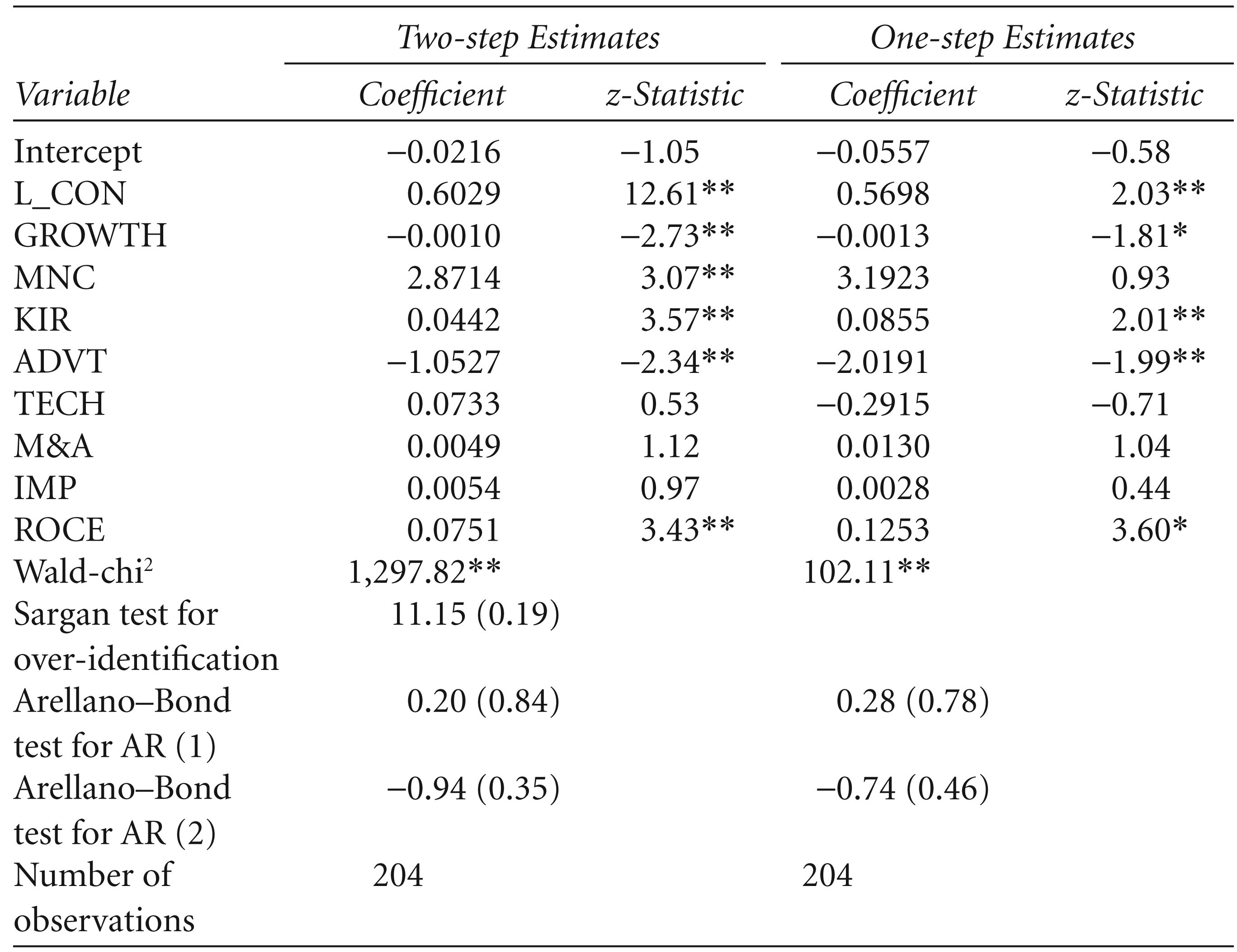

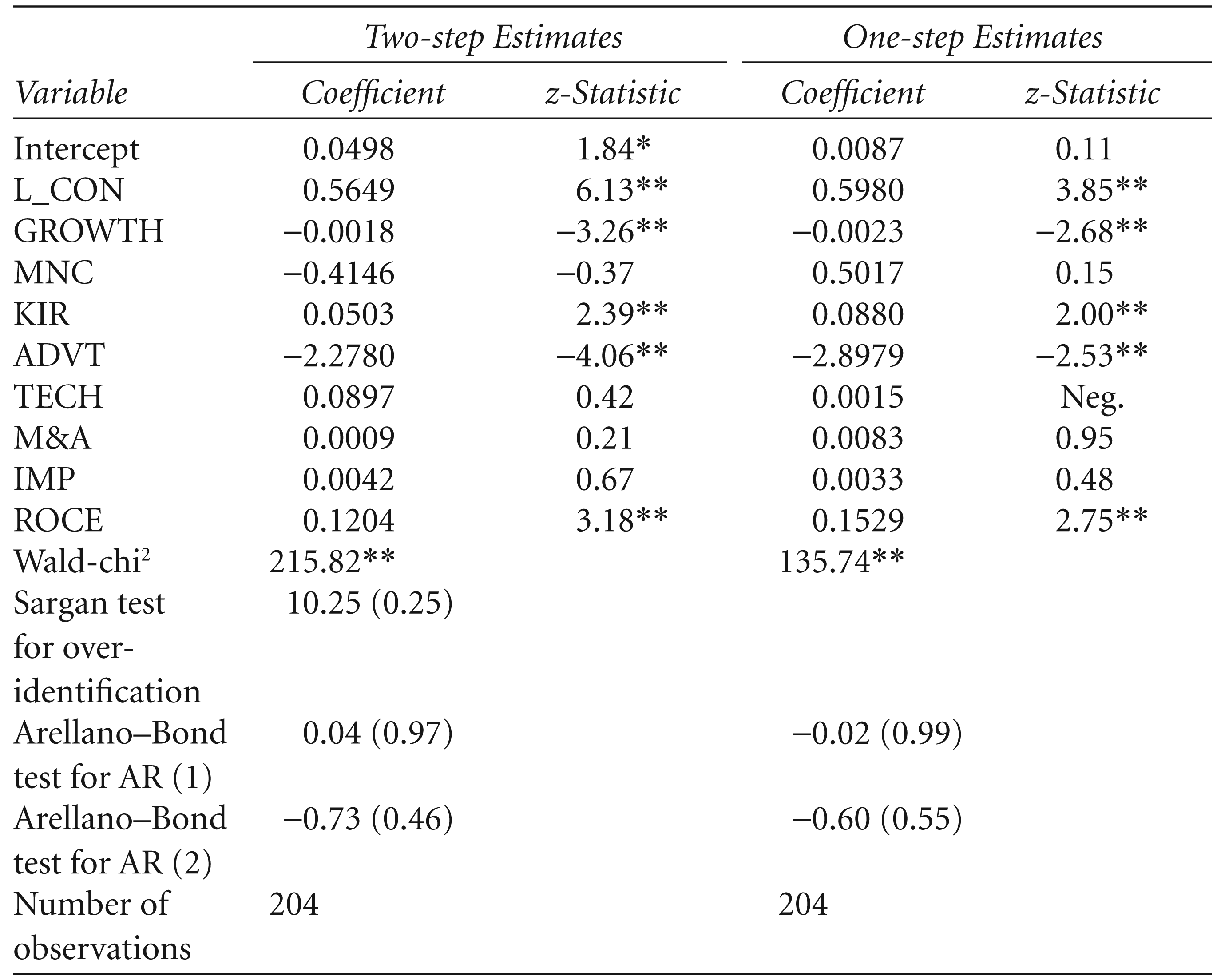

As regards estimation of the dynamic model, summary statistics of the variables are provided in Table 5, whereas Tables 6 and 7 present the regression results along with the statistics used for testing autocorrelation and the validity of instruments. The Wald-chi 2 is significant, implying validity of the estimated models. Further, the Sargan test suggests that the estimated models do not have the problem of over-identified restrictions. In addition, the statistics for the Arellano–Bond tests of AR (1) and AR (2) indicate that all the estimated models are free from autocorrelation.

Regression Results for Fixed Effects Models

*Statistically significant at the 5% level.

Summary Statistics of the Variables

Regression Results with HHI as a Measure of Market Concentration

The one-step estimates suggest that the coefficients of L_CON, GROWTH, KIR, ADVT and ROCE are significant. Further, while the coefficients of L_CON, KIR and ROCE are positive, those of GROWTH and ADVT are negative. This means that current market concentration is higher in industries where the market is already concentrated, capital intensity is high or existing firms realise higher rates of returns on capital employed, whereas industries with higher growth of sales or greater efforts towards advertising have less concentrated markets.

Regression Results with GRS Index as Measure of Market Concentration

Notes: (i) Neg.: negligible (<0.005); (ii) the z-statistic in a one-step estimation is based on robust standard errors; (iii) figures in parentheses indicate level of statistical significance of the respective test statistic; (iv) *statistically significant at the 10% level; (v) **statistically significant at the 5% level.

However, M&As do not have any significant influence on market concentration, thus they do not necessarily alter the structure of a market. This is so possibly because whether a particular merger or an acquisition will raise market concentration depends on a variety of other factors including initial structure of the market, barriers to entry, extent of competition from imports, other business strategies of the firms such as advertising and their financial performance. These factors influence the impact of M&As on market concentration in different directions. When these diverse forces are balanced, market concentration may not change significantly following M&As. There are evidences of no significant change or decline in market concentration following M&As (e.g., Mishra, 2005; Mueller, 1985; Weiss, 1965).

Further, mergers can be influenced by low market concentration, high cash flows and high Tobin’s q (Agrawal & Sensarma, 2007). According to Mishra (2011), inter-industry variation in M&As in Indian manufacturing sector in the 1990s were caused by a set of factors relating to market structure, other business strategies, performance and policies. Given such diverse objectives of integration and industry-specific aspects, it is very likely that M&As do not have any significant impact on market concentration in many industries.

The present article finds the market less concentrated in industries with a high rate of growth of sales. This is consistent with the findings of Ghose (1975) and Bhattacharya (2002). Possibly, fast-growing industries create more opportunities for existing firms to expand (Basant & Saha, 2005). Further, a high rate of growth of the market induces the entry of new players (Duetsch, 1984; Highfield & Smiley, 1987; Saikia, 1997). Thus, when there are more entries following the growth of the market, the degree of sellers’ concentration is likely to decline.

Market concentration is high in capital-intensive industries possibly due to high sunk costs (McDonald, 1999); high capital intensity in an industry is likely to reflect the existence of large sunk costs that create entry barriers, thereby giving rise to monopoly profit (McDonald, 1999). Besides, capital market imperfections may lead to discrimination by offering preferential lending rates to large established firms in capital-intensive industries. This higher cost of capital makes small firms less competitive and thereby restricts them from entering the industry (Basant & Saha, 2005). Given the limited entry, capital-intensive industries are likely to have a more concentrated market.

Further, the ratio of imports to exports does not influence market concentration, because higher exports make the domestic market more competitive (Chou, 1986), whereas import competition can reduce market concentration (Mishra & Behera, 2007). The combined effects of exports and imports may leave market concentration largely unchanged. Similarly, technology strategies also do not have a significant impact on market concentration. It is possible that the R&D base of domestic firms is low due to their limited financial and intellectual capabilities for development of indigenous technologies, making overall technical change adaptive in nature (Kumar & Siddharthan, 1994). This is true particularly for small and medium firms in developing countries that do not have in-house R&D facilities (Brouwer & Kleinknecht, 1993). As a result, market concentration may not change following such strategies.

It is interesting to note that, contrary to the findings in many existing studies (e.g., Comanor & Wilson, 1974; Das et al., 1993; Martin, 1979; Shepherd, 1982), the present article finds that the market is less concentrated in industries where firms make a greater effort at advertising. Whether this signals greater product differentiation and wider choices for consumers requires further scrutiny. It is also possible that greater access of consumers to information on product quality and prices through advertising has reduced sellers’ control over the market.

In the context of the wave of M&As in Indian manufacturing in the post-reform period, the present article attempts to examine the impact of such business strategies on market concentration. Using panel data estimation techniques, we do not find any statistically significant influence of M&As on market concentration, so they do not necessarily alter the structure of a market. Instead, market concentration is influenced by growth of the market, capital intensity and firms’ advertising efforts and financial performance. While the market is less concentrated in industries with growing markets and greater advertising efforts, higher capital intensity and better financial performance raise market concentration. This study does not find any significant influence of firms’ technology strategies on structure of different markets. It is also found that competition from imports vis-à-vis exports does not have any significant impact on market concentration.

The findings of this study call for a rethinking on policies and regulations on the following aspects relating to M&As, international trade and intellectual property. First, if there is need to regulate M&As, particularly when they are not necessarily anticompetitive. Instead, the integration of (weaker) firms through M&As could be encouraged to enhance their competitiveness and restrict the emergence of monopoly power. Second, the need for uniform thresholds for assets and turnovers in regulating M&As across industries should be revisited, given that the nature and extent of their impact on market concentration may differ depending on industry-specific factors. Third, the need for flexibility in the Competition Act for objective-specific assessments of M&As requires further scrutiny considering that a merger or an acquisition may not lead to an increase in market concentration, particularly when such a deal is motivated by increasing the efficiency of operation. However, since a high rate of sales growth makes the market less concentrated, priority may be given to expansion of existing markets and developing new ones to restrict firms’ monopoly power. Designing appropriate public policies and institutions are crucial in this regard.

In addition, there is a need for the integration of policies and regulations as the process of economic reforms has deepened in the areas like FDI, privatisation and disinvestment, intellectual property regulation and so on, over the years. For example, a considerable portion of FDI inflows in recent years has taken the route of M&As. With the introduction of liberal FDI policies one may, therefore, expect significant spillover of technologies and expertise that can potentially reduce production costs and improve the quality of products. Similarly, innovation and the introduction of new products give consumers a wider range of choices without any adverse impact on market concentration. Policies and regulations may, therefore, be designed to encourage firms to undertake greater in-house R&D. While these issues are important, addressing them require detailed analysis at the firm level to have better insights and hence clearer direction.

However, the findings of this article are tentative and robust conclusions may require further exploration. As mentioned earlier, a better understanding of the impact of M&As on market structure should also emphasise the size (i.e., value) of deals along with their numbers; this study fails to capture this aspect due to a lack of systematic data. Future studies could be directed at re-examining the impacts of M&As on market structure by controlling for the size of deals. In addition, efforts should be made to understand the impact on market structure by type of the deal, that is, whether the M&As are horizontal, vertical or conglomeration in nature.

More importantly, while the present article undertakes an industry-level analysis which can capture impacts on the average firm in an industry, drawing implications for competition law and policy more directly would require detailed scrutiny of relationships at the firm level, because market power or efficiency is more relevant at the firm level. A firm-level analysis can also help in controlling strategic conjectures following M&As along with examining the impact on performance in the broader perspective of changes in product quality and prices, consumers’ position in the market (in terms of access to information, choice, etc.), firms’ efforts towards innovation, and so on, and role of the regulatory agencies in this regard.

Footnotes

Measurement of the Variables

Acknowledgements

The author is grateful to conference participants for their useful comments and suggestions and to Professor Rakesh Basant for his valuable comments and suggestions at various stages of writing this article. Thanks are also due to the anonymous referee for useful comments and suggestions that helped immensely. The usual disclaimers apply. An earlier version of this article was presented and published in the proceedings of the International Conference on Economics and Finance held at Kathmandu, Nepal during 26–28 February 2015.