Abstract

This study examines the impact of foreign direct investment (FDI) on the total factor productivity (TFP) of host countries. Extensions of the new growth theory provide a framework in which FDI increases the growth rate of a host country through technology transfer, diffusion and spillover effects. We construct four new series of TFP using the framework of neoclassical growth models. We also address the issue of endogeneity using the generalized method of moments. Our estimations using a balanced panel of 77 low- and middle-income countries suggest that FDI could not promote TFP in the countries studied. Our sensitivity analysis, in terms of alternative estimation methods, data, models and time period, reinforces the findings. We observe that the lack of absorptive capacity is likely to be an important reason for not having a direct relationship between FDI and TFP.

Keywords

Introduction

Neo-classical growth theory postulates that foreign direct investment (FDI) finances capital formation, increases the stock of capital and promotes economic growth in the short run. In the long run, the host economy converges to the steady state due to diminishing returns to capital, and FDI does not leave any permanent impact on economic growth. The neo-classical model also suggests that foreign investment is as productive as domestic investment and has the same impact on economic growth. However, according to the endogenous growth theory, foreign investment is more productive than domestic investment as it brings not only capital but also technology and know-how to the host county (Borensztein, De Gregorio, & Lee, 1998). These FDI-related technological spillovers offset the effects of diminishing returns to capital and promote economic growth both in the short run and in the long run. FDI not only increases the stock of knowledge of the recipient country through training of workers, but also introduces innovative management practices and organizational arrangements (De Mello, 1997).

Since the postulation of the endogenous growth theory by Romer (1986), various extensions of the theory have been developed by hypothesizing how FDI-related spillovers and technological diffusion promote economic growth. These theories identify numerous channels, such as demonstration by foreign firms and imitation by local firms, labour mobility, exports, competition and backward and forward linkage with domestic firms, through which FDI promotes economic growth (Görg & Greenaway, 2004; Laborda, Salem, & Moreno, 2014).

Anecdotally, much has been done in the literature assessing spillover effects by estimating the impact of FDI on gross domestic product (GDP). Yet, due to the limited availability of appropriate TFP measures and rigorous statistical inferences, less has been established in the literature. Some studies claim that the positive relationship between FDI and economic growth is conditional on pursuing export promotion and/or financial development of host countries (Alfaro, Chanda, Kalemli-Ozcan, & Sayek, 2004; Balasubramanyam, Salisu, & Sapsford, 1996). On the other hand, others have found that for a vast majority of countries, FDI does not have any positive impact on economic growth (Carkovic & Levine 2005; Herzer, Klasen, & Nowak-Lehmann, 2008). While it is more appropriate to use TFP to assess the impact of FDI-related spillovers, most of the existing studies use economic growth as a proxy for TFP (Alvarado, Iñiguez, & Ponce, 2017; Li & Liu, 2005). The lack of availability of TFP measures is one of the major reasons for this.

Existing studies that investigate the relationship between FDI and TFP are based on homogenous panel data methods, which assume independence of cross-sectional units and parameter homogeneity across the countries (Baltabaev, 2014). If the cross-sectional units are dependent, the traditional panel data models do not produce consistent estimates. Since countries have experienced greater economic and financial integration and linkages in the last few decades, they are exposed to common institutional, political, and social shocks, spatial spillover effects, and externalities. These common shocks are likely to generate cross-section dependence in errors. Homogeneous panel data models also assume parameter homogeneity across the countries. However, if the true slope coefficients are heterogeneous, these estimators may produce inconsistent and misleading estimates (Pesaran & Smith, 1995).

This article seeks to construct four TFP measures and estimate the impact of FDI on these measures using a variety of econometric methods that can account for endogeneity, cross-section dependence, heterogeneity of parameters, non-stationarity of variables, and control for unobservable factors that influence the estimates. The construction of four different TFP series allows us to measure the impact of FDI on different types of factor productivity. It also helps to estimate the direct impact of FDI on the host countries. The scatter plots using four different TFP measures and FDI are reported in Figures A1–A4 in Appendix. Using the newly constructed TFP series, we address the following questions in our study: Does FDI promote economic growth in low- and middle-income countries? Does this relationship remain valid after controlling for endogeneity?

The key findings of our study suggest that FDI fails to promote TFP in the recipient countries. The results remain valid irrespective of the TFP measures used in this study. Our findings are statistically robust as our parameters are stable and errors are well-behaved despite the change in model structure, TFP measures, and sample period. However, our findings suggest that an increase in the absorptive capacity of the economy is likely to facilitate optimizing the productivity of local firms from FDI.

In the next section, we provide a brief outline of the voids in the existing research. Section 3 provides a detailed theoretical and quantitative outline of the construction of TFP series and estimation strategy. We present the results and analyse the findings of this study in Section 4. Section 5 presents the concluding remarks.

Literature Review

Theoretical Underpinnings

Various theoretical and empirical models explain how FDI promotes productivity and growth in a host country through transfer, diffusion and spillover of technology. Proponents of these models argue that FDI brings capital and best management practices, facilitates the use of advanced technology, promotes exports and creates employment opportunities (Ozturk, 2007; Forte & Moura, 2013). The indirect benefits may come through efficiency and productivity enhancement of domestically owned enterprises. When multinational enterprises (MNEs) use technology, this generates positive externalities for local firms. Such positive externalities are known as ‘spillovers’ that increase productivity. Higher productivity generated through spillovers may come from various channels including demonstration/imitation, labour turnover, and backward and forward linkage with local firms, competition and exports (Laborda et al., 2014; Saggi, 2002).

The presence of foreign firms can also benefit local firms through exports (Görg & Greenaway, 2004). The local firms can learn exporting strategies, such as how to penetrate into new markets, from their foreign counterparts by collaboration and imitation. This will enable them to exploit scale economies and increase productivity (Görg & Greenaway, 2004). Spillover from MNEs may also occur through labour turnover (Fosfuri, Motta, & Ronde, 2001). The spillover of knowledge from foreign firms to indigenous firms may take place if MNEs establish backward linkages with local firms. Javorcik (2004) argues that MNEs directly transfer know-how to their suppliers and force them to improve the quality of their products and deliver on time, which encourages local suppliers to upgrade their technology or improve their managerial capability. The increased demand for intermediate products also enables them to take advantage of scale economies. These increase productivity in backward-linkage (upstream) industries. Similarly, productivity of domestic firms may increase through forward-linkage (downstream) industries if they can make use of new, advanced and cheaper inputs produced by MNEs (Javorcik, 2004).

A number of studies explain the negative or neutral impact of FDI on productivity growth. They argue that domestic firms have a relatively higher marginal cost compared to their foreign counterparts, which enjoy lower marginal costs due to firm-specific advantages and proprietary knowledge. Due to these cost disadvantages, local firms lose market share to MNCs, lose output and move up along the average cost curve (Aitken & Harrison, 1999). Thus, due to the presence of foreign firms, since local firms lose their market share, operate on a less efficient scale, and experience higher production costs, they become unable to invest in new technologies. This creates an adverse impact on the productivity of local firms.

Negative knowledge spillover can also be caused by a negative backward-linkage effect. If MNCs procure fewer inputs in a host country than the domestic firms they displace, an increase in FDI may reduce the input variety produced by local firms and lower productivity in the host country. MNCs may also restrict the flow of their firm-specific knowledge to domestic firms. This may prevent any knowledge spillovers from MNCs (Görg & Greenaway, 2004). Spillovers also depend on labour quality—the education and experience of the workers (Globerman, 1979). An increase in the quality of labour increases their absorptive capacity—their ability to learn, imitate and adopt technology used by MNEs, which positively influences knowledge spillovers. If the quality of labour is poor, the gap in technological know-how between local and foreign firms will be too wide and therefore it would be difficult for local workers to learn from foreign firms resulting in no significant spillovers from MNCs (Wang & Blomström, 1992). Kokko (1994) also observes that a large technology gap between local and foreign firms lowers spillovers.

Empirical Literature

The empirical literature related to FDI and productivity can be classified into two categories: country-level macro-studies and firm-level micro-studies. Firm-level studies often suggest that FDI does not have any positive impact on economic growth. Görg and Greenaway (2004) summarize the findings of 25 panel studies on productivity spillovers in manufacturing industries in developing, developed and transition economies. In only six studies, evidence is found for positive spillovers, and none of them are developing countries. Aitken and Harrison (1999) in their study on Venezuela find evidence of negative spillovers. Similar studies pursued in other countries also report insignificant or negative externalities from FDI including: Djankov and Hoekman (2000) for the Czech Republic, Kathuria (2000) for India, Damijan, Knell, Majcen, and Rojec (2003) for eight transition economies, and Hu and Jefferson (2002) for China. Girma, Greenaway, and Wakelin (2001) using a panel of 2,342 UK firms find that there is no positive impact of a foreign presence on the productivity of local firms either in level or in growth.

Despite significant scholarship in the area of FDI and TFP, there are major gaps in the existing literature. First, a majority of the existing studies have estimated spillover effects by analysing the impact of FDI on GDP. Since FDI is assumed to benefit an economy by causing technological change, in order to study technological change driven by FDI, it is more appropriate to study TFP and use it as a dependent variable in the growth regressions rather than the growth rate of GDP. Moreover, it is well documented that the TFP accounts for 50–70 per cent of cross-country differences in income (Hsieh & Klenow, 2010). TFP growth is also identified as the main driver of a long-run increase in the standard of living (Hall & Jones, 1999). Second, data on TFP is a major issue. The TFP series made available by Penn World Tables (PWT) is not long enough and exists for fewer countries. Third, existing studies measure foreign presence by FDI flows as a percentage of GDP. The use of FDI flows in a growth regression may introduce endogeneity due to reverse causality between FDI flows and GDP (Nunnenkamp & Spatz, 2004). FDI flows also suffer short-term fluctuations due to changes in macroeconomic conditions. Such flows also do not give any idea about the market share of foreign investors because FDI flows can be very insignificant when the entire market is captured by foreign investors. Moreover, often existing time-series studies employ co-integration techniques developed by Johansen (1995). Due to the small sample size, the method of cointegration has a tendency to reject the null of no cointegration inaccurately (Herzer et al., 2008). In panel cointegration, in the presence of cointegration across countries, the null of no cointegration can be falsely rejected when no or very few within country relationships are cointegrated (Banerjee, Marcellino, & Osbat, 2004).

This study addresses the aforementioned issues in the following manner. First, we use TFP as our dependent variable as opposed to GDP growth. Second, to address the issue of missing data, we construct four different TFP series following the underlying theoretical models. We collect the necessary data to construct our series from PWT 7.1 and 8.1. Our data set also includes some series from Castellacci and Natera (2011). The novelty of this data set is that this is a balanced panel with no missing values. Gaps in the data are filled using multiple imputations developed by Honaker and King (2010). To the best of our knowledge, no study has so far developed such a data set to analyse the impact of FDI on factor productivity. Third, we address the issue of endogeneity and other estimation-related issues by using the generalized method of moments (GMM) estimation method proposed by Holtz-Eakin, Newey, and Rosen (1988) and subsequently extended by Arellano and Bond (1991), Arellano and Bover (1995), and Blundell and Bond (1998). This estimation method is capable of controlling for the endogeneity problem and the omitted variable bias in growth regressions. We employ instruments to overcome the issues related to endogeneity. Hence, we claim that this study minimizes the void in the literature in a more robust way.

Empirical Framework and Estimation Methods

Construction of TFP Variables

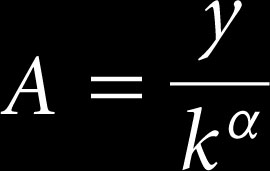

Our construction of four different TFP series is originated from the simple Solow–Swan growth model. We assume the following Cobb–Douglas production function:

where Y is real GDP, K is real physical capital, L is total labour force, α is the share of capital in total output and A is total factor productivity (TFP).

Dividing both sides of Equation (1) by L, output per worker can be written as

where

This is our first estimate of TFP. Let us denote it as tfp1.

For estimating tfp1, we construct a series on capital stock K. We calculate the initial level of capital stock following the steady-state relationship of the Solow model suggested by Harberger (1978) (Beck et al., 2000; King and Levine, 1994; Nehru and Dhareshwar, 1993):

where I0 is the initial investment, g is the average geometric growth rate of GDP over the period and δ is constant depreciation rate of capital stock. We assume 5 per cent rate of depreciation (Bosworth & Collins, 2003). Investment data is taken from the PWT 7.1 to construct the series on K. We use the perpetual inventory method to construct the series on capital stock:

where It is investment and δ is the depreciation rate. 1

Following Caselli (2005), we construct the series on output, investment and labour from PWT 7.1. We estimate Y, I, L and size of the population to calculate initial and subsequent stock of capital and TFP. As part of the TFP calculation, we need information on income share of labour, which is not readily available. Exiting literature suggest that income share of labour varies from 0.65 to 0.8. For our TFP1, we assume fixed labour share of 0.65 (Bernanke & Gurkaynak, 2001; Gollin, 2002).

One of the limitations of the aforementioned production function in Equation (1) is that it does not take into account human capital as an input. After incorporating human capital as an input, we consider the following production function:

where h is human capital per person and Lh is human capital adjusted labor force (i.e., number of workers multiplied by their average human capital).

Dividing both sides of Equation (6) by L, output per worker can be written as

where

This is our second estimate of TFP. We denote it as tfp2.

The relationship between human capital h and education S is designed in a way where more weight is attached to the workers with a higher level of education (Hall & Jones, 1999; Klenow & Rodriguez-Clare, 1997). We assume a log-linear relationship between wage and schooling. Hence, our human capital function becomes

where S is average years of schooling. More explicitly the labour quality index for human capital h can be written as follows:

where φp, φs and φt are the Mincerian returns to an additional year of schooling at primary, secondary and tertiary levels and sp, ss and st represent average years of schooling at primary, secondary and tertiary levels, respectively. 2 The construction of index h is based on data on S from the Barro and Lee education data set.

When we calculate tfp1, we assumed a constant income share of labour and capital. We have improved our estimates of tfp1 by assuming different income shares of labour and capital over time and across countries. We use data on income share of labour from PWT 8.1 to construct another series on TFP from Equation (3). We call it tfp3. Our fourth series, tfp4, is an extension of tfp2 with varying level of income share from PWT 8.1. The construction of four different TFP series accommodates the flexibility in TFP and covers a wide range of TFP estimates.

To examine the impact of FDI on TFP, we estimate the following model (Baltabaev, 2014; Kose, Prasad, & Terrones 2009; Woo, 2009):

Alternatively, we can write it as

where i is country index,t is time index, y is TFP (tfp), FDI is the stock of FDI per capita, X is a vector of explanatory variables that affect TFP, η i is unobserved country fixed effects, λ t is time fixed effects and ε it is the usual error term.

Following the existing literature, our X includes investment as a percentage of GDP, distance to the technology frontier (dtf), inflation rate, population growth rate, exchange rate, average years of schooling, domestic credit to private sector by banks as a share of GDP, kof index of globalization as a measure of openness, internet users per 1,000 people as an indicator of infrastructure and an index to measure the impact of institutional development. Our dtf is the relative TFP gap between the technology leader and sample countries. Assuming USA as the technology leader, dtf is measured by TFPUS / TFPi, where TFPUS is TFP of USA and TFPi is TFP of a country in the sample. Following Benhabib and Spiegel (1994), we assume that countries further from the technology leader achieve higher TFP growth. Autonomous transfer of technology from the leader country to follower countries helps them achieve faster growth and catch up to the technology frontier. Inflation is an indicator of uncertainty and macroeconomic instability. Inflation decreases the return on capital and discourages investment. So, an increase in inflation is expected to have a negative impact of productivity.

Average years of schooling measures human capital. Improvement in human capital increases the ability to develop technology and assimilate technology developed elsewhere, which increases productivity growth. Domestic credit to the private sector is expected to increase productivity if such credit facilitates investment in capital intensive state of the art technology. The kof index of globalization measures the three main dimensions of globalization: economic, social and political. An increase in globalization enhances access to foreign technologies and facilitates learning of advanced technologies. Openness to imports lowers tariff and non-tariff barriers, facilitates import of varieties of capital goods and gives opportunity to learn foreign technology embodied in foreign goods (Madsen, 2009). Thus, openness strengthens technology learning and aids catching up to the technology frontier. We also hypothesize that an improvement in infrastructure is expected to improve productivity. Population growth rate is expected to influence TFP growth positively. An increase in the size of population is expected to generate more ideas and leads to more innovations, which will increase productivity (Jones, 1995; Kremer, 1993).

We measure institution combining two indicators published by Freedom House: political rights and civil liberties. Each of these indicators is measured on a scale of 1–7, where larger numbers indicate fewer rights and liberties. We construct a single indictor for institution following Busse (2004):

This single indicator will lie between 0 when there are no political rights and civil liberties and 1 when a country has the highest degree of political rights and civil liberties.

We also examine whether absorptive capacity is a potential candidate behind no relationship between FDI and TFP. If the interaction term between FDI and dtf is negative and significant, we could claim that absorptive capacity plays an important role in increasing TFP from FDI. We also add an interaction term between FDI and inflation to assess how macroeconomic volatility influences the impact of FDI on the growth rate of TFP.

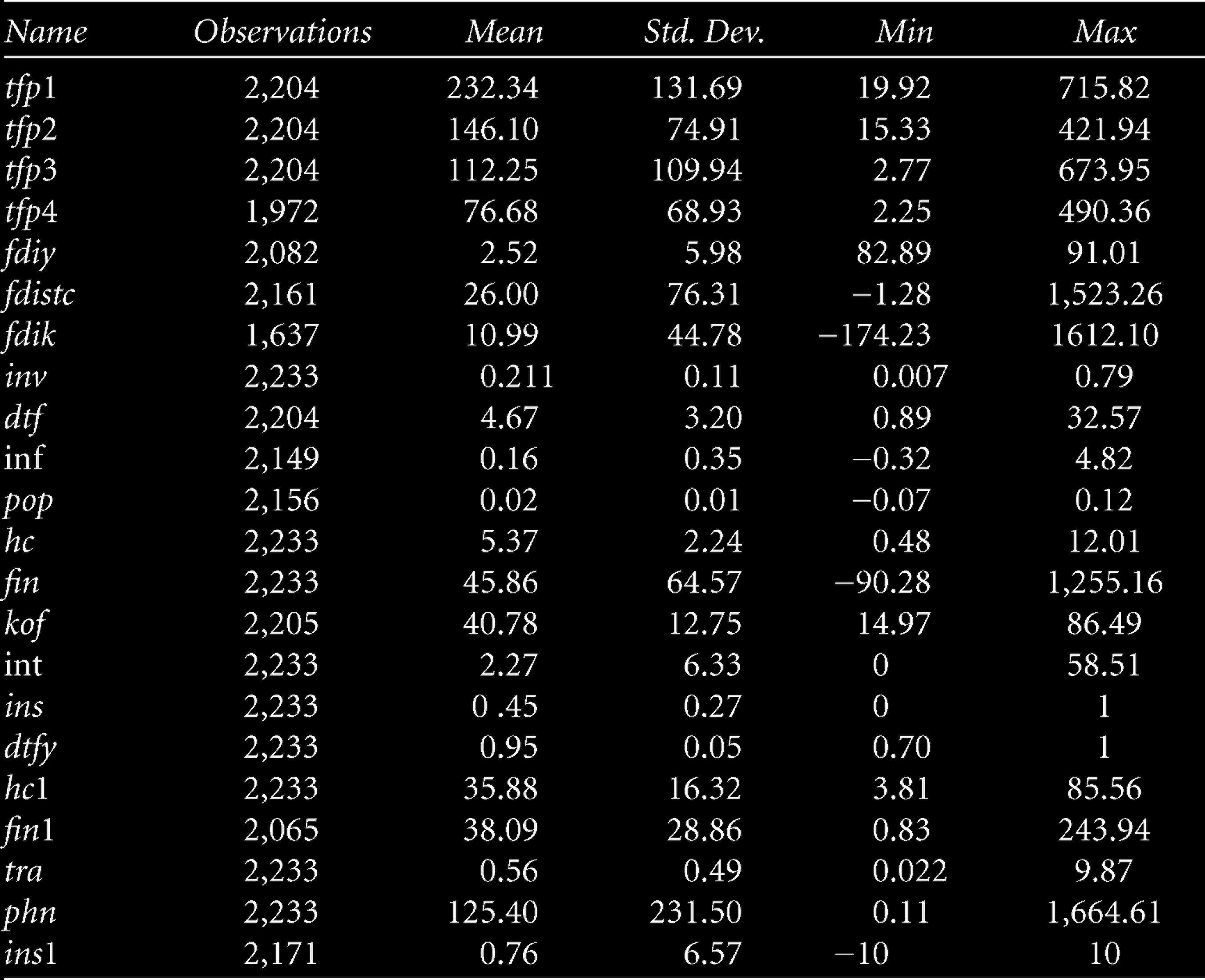

Our sample period ranges from 1980 to 2008 and includes annual data on the variables. 3 In order to avoid business cycles, the data values are averaged over a 3-year period. Our sample includes 77 low- and middle-income countries. The data are collected from various sources such as PWT 7.1 and 8.1, World Development Indicators (WDI), Freedom House, External Wealth of Nations Mark II database, UNCTAD, Center for Systemic Peace and the Swiss Economic Institute. Summary statistics of the variables included in the models are reported in Tables A1–A3.

We estimate our model (Equation (12)) by the system GMM method. We employ the two-step estimator GMM estimator as it is more efficient than the one-step estimator due to optimal weighting matrices (Roodman, 2009). To test the consistency of the GMM estimator, we employ both Hansen J test of overidentifying restrictions and serial correlation test (AR1 and AR2) in the disturbances.

As part of the robustness test, instead of using FDI stock as a percentage of GDP as a measure of FDI, we also employ FDI inflows as a percent of GDP and FDI inflows as a percent of gross capital formation. Moreover, following Li and Liu (2005), we also generate the DTF variable on the basis of income differential as follows:

where y is real GDP per capita of the country under consideration and real GDP per capita of the United States is used as y max

t

. We also reconstruct the human capital variable using the weighted average of enrolment ratios in primary, secondary and tertiary education. Our alternative specification of human capital is constructed as follows (Karimi, Yusop, Hook, & Chin, 2013):

where PRI, SEC and TER are enrolment ratios in primary, secondary and tertiary education, respectively. This index assigns different weights to different schooling enrolment rates. The higher weights are assigned to higher levels of education because higher education develops higher skills for technical and managerial innovation. The existing literature proposes various alternatives to the financial development, globalization, infrastructure and institution. Hence, we also replace Credit to GDP ratio with M2GDP ratio, trade (sum of import and export) as a percent of GDP instead of kof index of globalization. We use telephone subscriber (fixed-line plus mobile) per 1,000 inhabitants as a measure of infrastructure. For institution, we also use POLITY IV variable, which ranges from +10 (strongly democratic) to −10 (strongly autocratic) instead of political rights and civil liberties.

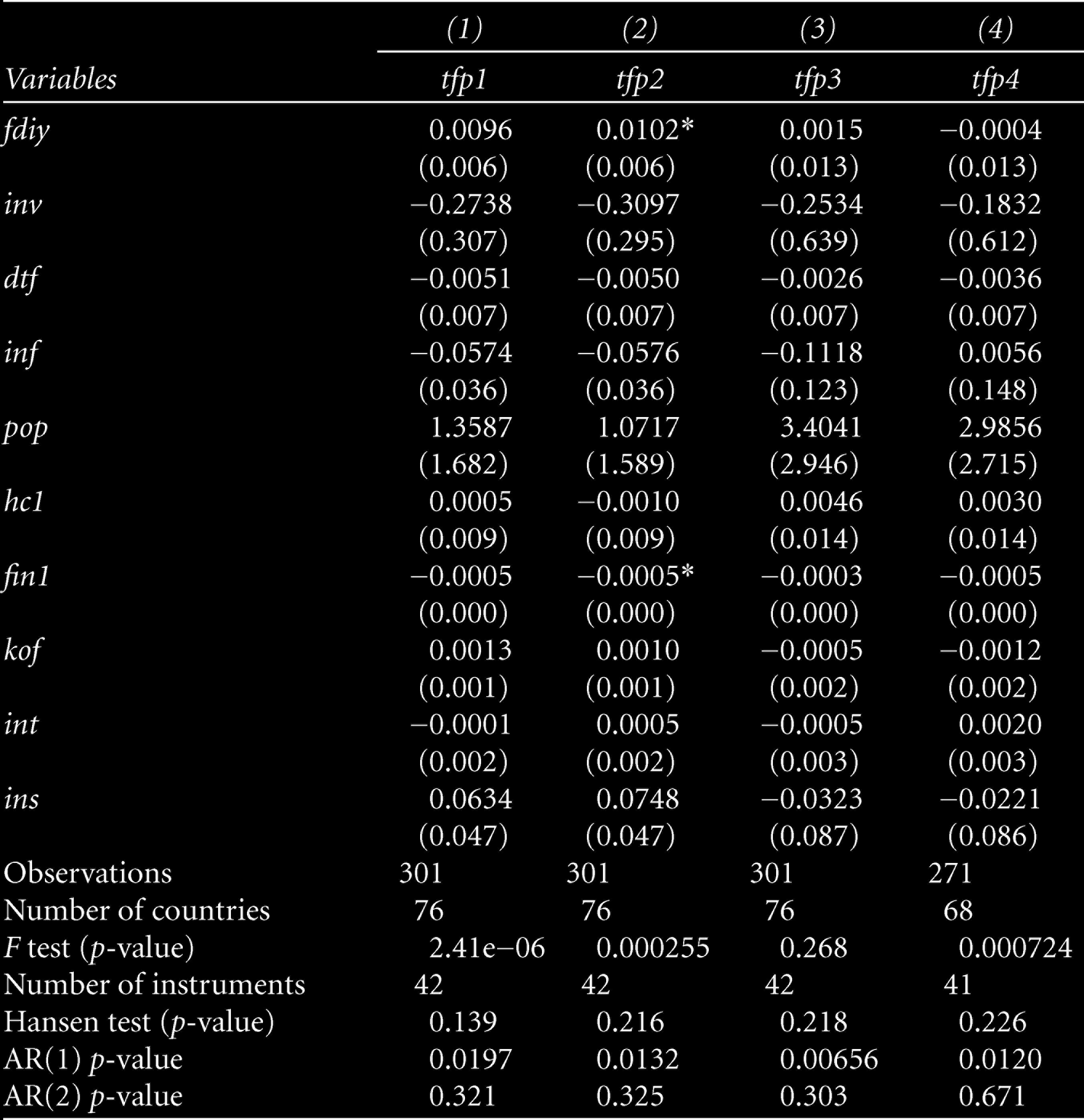

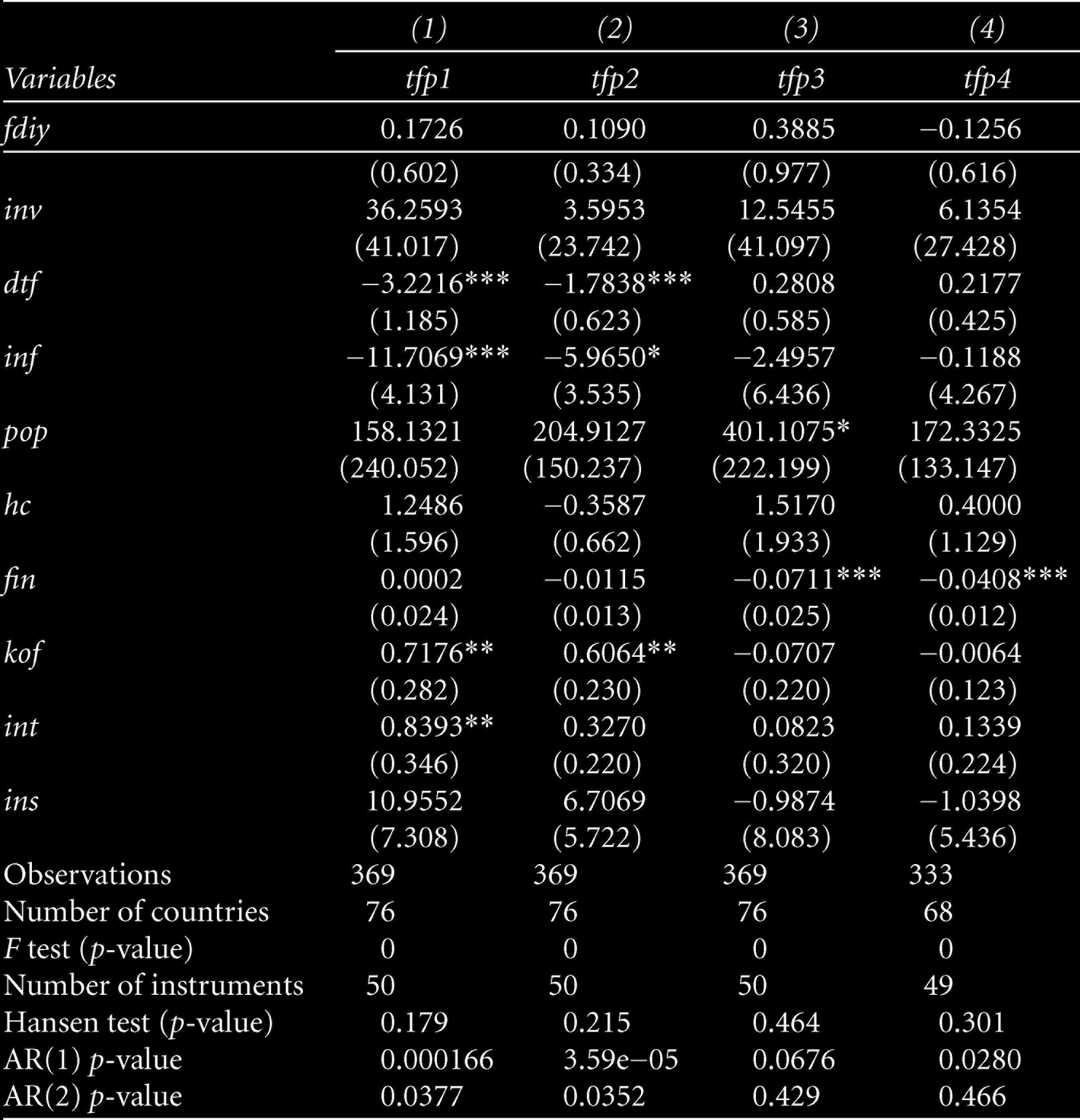

Table 1 reports the results of the GMM estimation of Equation (12). We estimate four models based on the four different TFP series. In Model (1) we use the first measure of FDI (FDI inflows as a percentage of GDP) as an independent variable. Our estimates in most cases provide evidence that FDI does not have any direct influence on the growth rate of TFP. Our findings support Carkovic and Levine (2002), Herzer et al. (2008), and Herzer (2012). Low absorptive capacity could be an important factor explaining the non-existence of a positive relationship between FDI and TFP. Low absorptive capacity may restrict spillovers of knowledge from foreign firms (Wang & Blomström, 1992). If local firms are not capable of making investment to absorb foreign technologies, knowledge spillovers will be limited or may not take place at all. MNEs may not apply advanced technology in a host country where the quality of human capital is low, which restricts the scope improving productivity from foreign firms (Kokko & Blomström, 1995). Foreign firms can also take steps to protect leakage of technology to local firms. MNEs may also offer a very high wage to their employees to prevent turnover of their workers and restrict the diffusion of technology (Lipsey & Sjoholm, 2004). Geographic proximity is also a condition to facilitate knowledge spillover. If MNEs operates in ‘enclaves’ where technology used and products produced by foreign firms are different from those of local firms, there is little scope for local firms to learn from foreign firms, and there will be no positive impact on labour productivity (Kokko, 1994). The adverse competition effect may also drive local firms out of the market. For these reasons, knowledge spillovers may be very weak and may not take place at all.

Impact of FDI on TFP Growth—Dependent Variable: Growth Rate of TFP

Impact of FDI on TFP Growth—Dependent Variable: Growth Rate of TFP

Inflation is found to have a negative impact on the growth rate of TFP in a number of cases. This is expected since higher inflation increases uncertainty, reduces the real rate of return to investment and discourages investment and factor productivity. We do not find any significant impact of domestic investment, the distance to the technology frontier, population, openness, education and institutions on the growth rate of TFP. In terms of the impact of human capital, we find no significant impact of schooling on TFP, which is in line with Bils and Klenow (2000) and Prichett (2001).

Our dtf variable suggests that there are no discernable differences in productivity between countries. If the absorptive capacity of the workers of the FDI recipient countries is very poor or firms do not have the financial strength to invest in absorbing foreign technologies, these countries will not benefit from the knowledge spillovers from FDI; they will not be able to assimilate or imitate foreign technology. Even MNEs may abstain from investing in high-tech industries in these countries due to lack of skilled workers. In that case, technology learning will be slow, the convergence process will be weak, and we may have an insignificant or negative coefficient for this variable. Our findings are in line with Herzer (2012), Li and Liu (2005), and Woo (2009). We also observe that democracy does not have any impact on TFP. This is consistent with findings of the previous studies (Doucouliagos & Ulubaşoğlu, 2008). All of our models pass the diagnostic tests of the system GMM method and assures that the models are correctly specified. Our test results confirm that instruments as a group are exogenous and valid. The consistency of the estimations is proved by the AR1 and AR2 test results. Empirical evidences allow us to reject the null of the absence of the first order serial correlation (AR1) and not to reject the null of the absence of the second order serial correlation (AR2), which is expected for consistency of the GMM estimators.

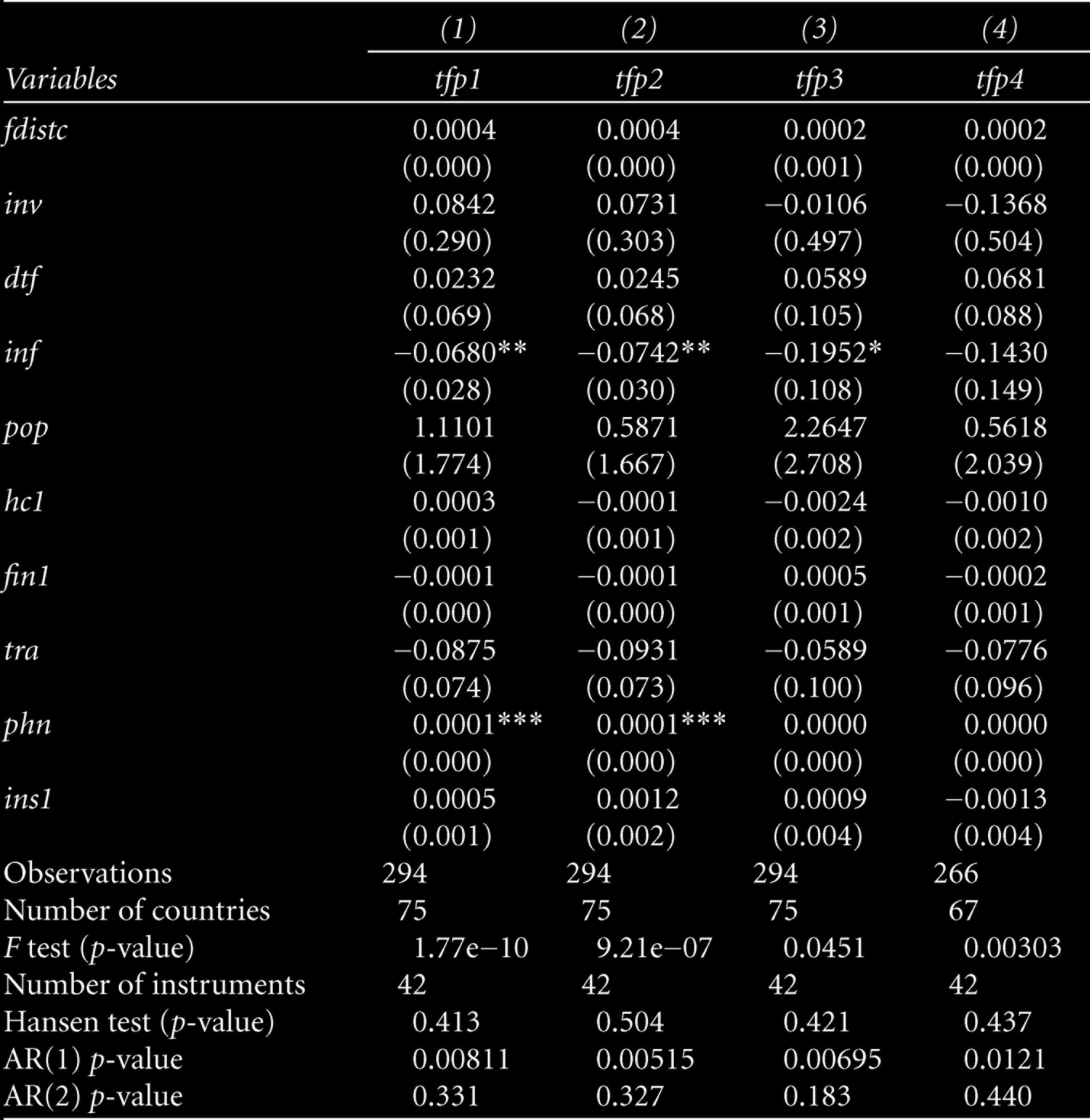

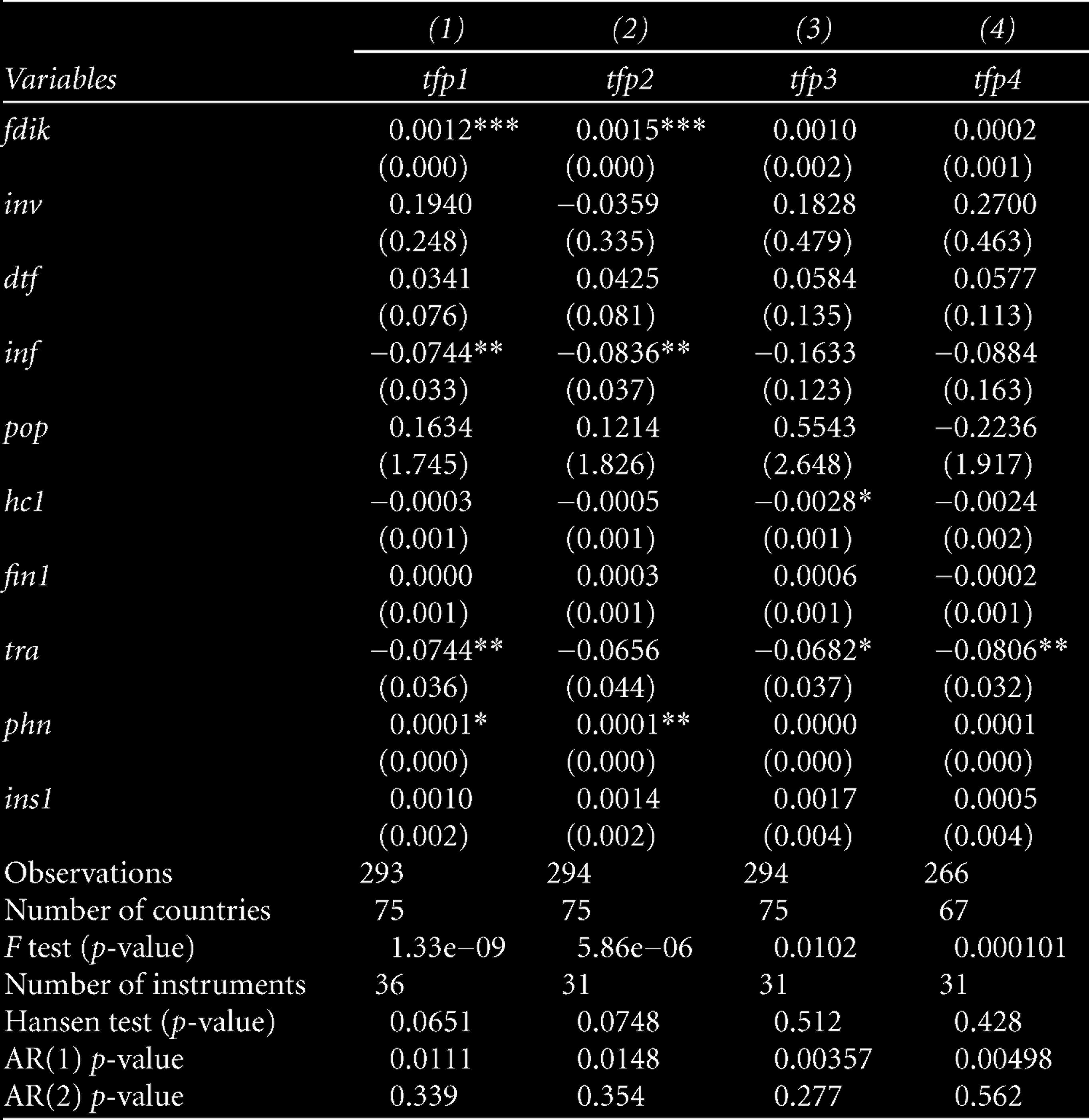

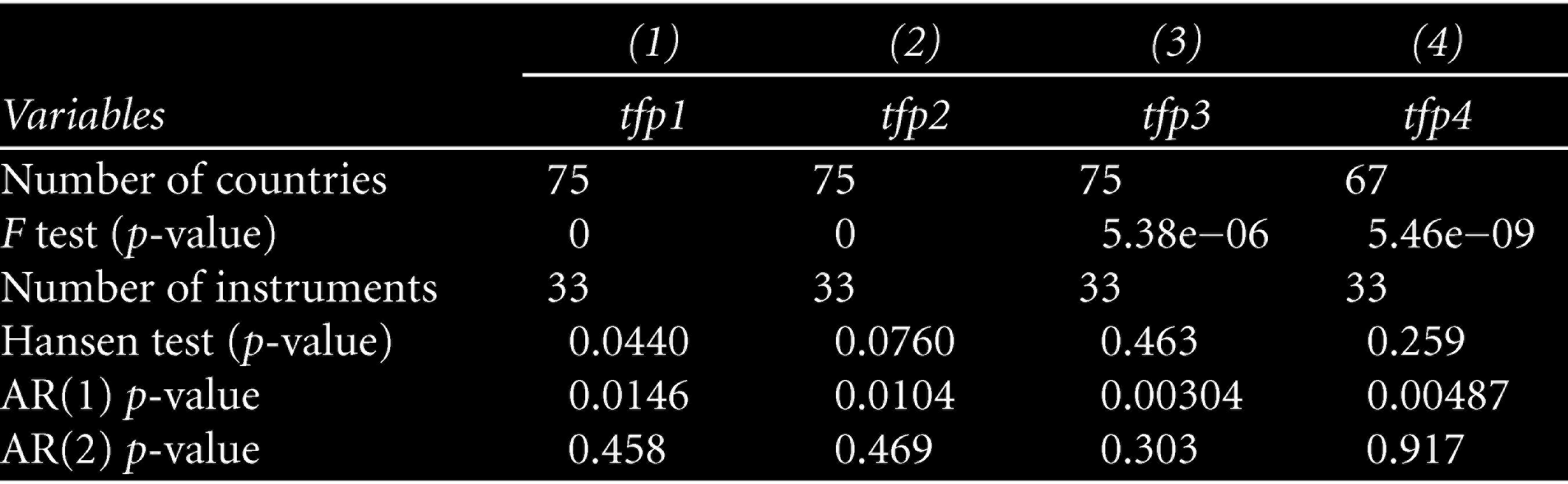

Tables 2 and 3 present the coefficients of our regressions with alternative specifications using an alternative set of explanatory variables. In Table 2, we use FDI stock as a percentage of GDP as a measure of foreign capital. In Table 3, we use FDI inflows as a percentage of gross fixed capital formation as a variable to measure foreign capital. The coefficients of the variables in Tables 2 and 3 support our previous findings: FDI does not have any statistically significant impact on the growth rate of TFP. The results for most of the variables are in line with our previous findings. We observe that in the first two models, presented in Table 3, FDI has positive influence on the growth rate of TFP. But these findings are not robust, because these two models are not well specified. In both models, p-values of the Hansen test are very low (0.065 and 0.075, respectively). These p-values produce very weak evidence that the instruments as a group are exogenous. In the other two models, where the Hansen J statistic is valid, we find that FDI does not have any statistically significant influence on the growth rate of TFP.

Impact of FDI on TFP Growth—Dependent Variable: Growth Rate of TFP

In order to take into account the cross-section dependence, heterogeneity of parameters and unobservable factors that influence the estimates, we also estimate our models using four common correlated effects (CCE) estimators and found similar results. 4

Impact of FDI on TFP Growth—Dependent Variable: Growth Rate of TFP

In the aforementioned models, we consider the growth rate of TFP as the dependent variable, since it measures the dynamic transfer of technology. However, the level of TFP measures the stock of technology. In order to measure the influence of foreign presence on the stock of technology, here we consider TFP level as the dependent variable in our models. Table 4 reports the estimates of all four models where the level of TFP is considered as the dependent variable.

Again, the estimates in all four models in Table 4 report similar findings: FDI does not have any impact on the level of TFP. Investment does not influence TFP in the level equations. Internet has a positive influence on the level of TFP in the first model. The results for inflation and financial development are mixed. Analogous to the previous findings, we could not claim any significant relationship between human capital and TFP of the host countries. However, we observe that dtf negatively influences the levels of TFP, as evident from the first two equations.

Impact of FDI on TFP—Dependent Variable: TFP Level

In Table 5, we reproduce all four TFP models based on Equation (12) after adding two interaction terms. The interaction term between FDI and dtf (dtffdi) is created by multiplying FDI stock as a percentage of GDP and the distance to the technology frontier based on the income of a country. On the other hand, the interaction term between FDI and inflation (inffdi)) is created by multiplying FDI flows as a percentage of gross capital formation and inflation.

Impact of FDI on TFP Growth—Dependent Variable: Growth Rate of TFP

Our findings of the interaction term for absorptive capacity (fdidtf) reflect mixed outcomes. While in some cases, the coefficient of the interaction term appears to be negative and significant, in other cases, it is insignificant. The negative interaction term asserts that better absorptive capacity will lead to a positive relationship between FDI-induced factor productivity. On the other hand, the insignificant interaction term implies that the lack of absorptive capacity is not a barrier to realizing higher TFP from FDI. 5 In this case, some other reasons may be responsible for the neutral effect of FDI on TFP. It is likely that the foreign enterprises have not used advanced technology in the host countries or that they have protected leakage of their technology to the local firm. Hence, the productivity of local enterprises may not increase from the operation of MNEs in the host country. Our interaction term between FDI and inflation is insignificant, implying that macroeconomic instability does not influence the growth rate of TFP from FDI. It neither reinforces nor weakens the transfer of knowledge from FDI to the recipient countries.

Extensions of the new growth theory provide a framework in which FDI permanently increases the growth rate of a host country through technology transfer, diffusion and spillover effects. Existing empirical studies mostly assess spillovers by estimating the impact of FDI on GDP and report mixed findings. Since FDI is believed to cause technological changes in host countries, we estimate the impact of FDI on both the level and growth rates of TFP, to assess such spillovers. Our results show that FDI has an insignificant impact on the level and growth rate of TFP.

The contributions of our study to the debate on FDI and productivity are as follows. First, in order to estimate productivity, we construct four different TFP series. We construct those series from the residuals of the Cobb–Douglas production function. The first series is constructed following the standard neoclassical approach from a Cobb–Douglas aggregate production function assuming constant shares of labour and capital. The second series is derived from the neoclassical production function incorporating human capital as an input in the production function with the assumption of a constant share of labour and capital. In the third series, we assume different factor shares for different countries in the production function that includes only labour and capital. The fourth and final series includes human capital in the production function and is based on the assumption that the income share of labour and capital varies across countries. The use of TFP allows us to capture productivity more precisely as opposed to the use of other proxies, that is, GDP growth. Second, it is likely that TFP, investment and FDI are endogenous. Using instruments and employing the GMM, we address the issue of endogeneity. Moreover, our use of the two-step GMM produces more efficient estimates. Third, our estimates are robust to alternative explanatory variables, time periods and estimation methods. Fourth, our results indicate that the lack of absorptive capacity could be a limiting factor to a positive impact of FDI on economic growth in developing countries; however, these results are not robust and we suggest further investigation in that regard.

Footnotes

Acknowledgements

The authors are grateful to John Loxley and John Serieux for their valuable comments. We are also indebted to the anonymous reviewers for their valuable comments on the earlier version of the manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix Figures

Appendix Tables

Summary Statistics of Variables

| Name | Observations | Mean | Std. Dev. | Min | Max |

| tfp1 | 2,204 | 232.34 | 131.69 | 19.92 | 715.82 |

| tfp2 | 2,204 | 146.10 | 74.91 | 15.33 | 421.94 |

| tfp3 | 2,204 | 112.25 | 109.94 | 2.77 | 673.95 |

| tfp4 | 1,972 | 76.68 | 68.93 | 2.25 | 490.36 |

| fdiy | 2,082 | 2.52 | 5.98 | 82.89 | 91.01 |

| fdistc | 2,161 | 26.00 | 76.31 | −1.28 | 1,523.26 |

| fdik | 1,637 | 10.99 | 44.78 | −174.23 | 1612.10 |

| inv | 2,233 | 0.211 | 0.11 | 0.007 | 0.79 |

| dtf | 2,204 | 4.67 | 3.20 | 0.89 | 32.57 |

| inf | 2,149 | 0.16 | 0.35 | −0.32 | 4.82 |

| pop | 2,156 | 0.02 | 0.01 | −0.07 | 0.12 |

| hc | 2,233 | 5.37 | 2.24 | 0.48 | 12.01 |

| fin | 2,233 | 45.86 | 64.57 | −90.28 | 1,255.16 |

| kof | 2,205 | 40.78 | 12.75 | 14.97 | 86.49 |

| int | 2,233 | 2.27 | 6.33 | 0 | 58.51 |

| ins | 2,233 | 0 .45 | 0.27 | 0 | 1 |

| dtfy | 2,233 | 0.95 | 0.05 | 0.70 | 1 |

| hc1 | 2,233 | 35.88 | 16.32 | 3.81 | 85.56 |

| fin1 | 2,065 | 38.09 | 28.86 | 0.83 | 243.94 |

| tra | 2,233 | 0.56 | 0.49 | 0.022 | 9.87 |

| phn | 2,233 | 125.40 | 231.50 | 0.11 | 1,664.61 |

| ins1 | 2,171 | 0.76 | 6.57 | −10 | 10 |