Abstract

The main purpose of this study is to explore factors determining China’s outward FDI (OFDI), with particular emphasis on the unique characteristics of China’s economy during the period of institutional transformation. The empirical results obtained in the present study show that Chinese enterprises tend to invest in countries that have a mature economy. Exports have a significantly positive effect on China’s OFDI, with the relationship between OFDI and exports in China being a complementary one. The relationship between imports and OFDI for China is one of substitution, as Chinese enterprises have often relied upon the importation of key components as a means of acquiring the technology they need. Exchange rates, monopolistic advantage, foreign exchange reserves and the level of technology intensity, all have a significant impact on China’s OFDI, while the GDP growth rate and geographical distance have not had a significant impact.

Introduction

With the continuing trend towards economic globalisation, more and more business enterprises have been investing overseas with a view to improving their growth and earnings performance. In investing overseas, firms may be seeking to secure access to natural resources, mature technology or a large market. As China has opened up, and as the capabilities of its domestic enterprises have grown, more and more Chinese firms have been expanding into other countries. From the point of view of the Chinese government, the increase in China’s outward foreign direct investment (OFDI) helps to give it enhanced political and economic leverage. The growth in China’s OFDI has been so rapid that China has already been transformed from a net recipient of FDI into a net outflow FDI country.

Before China began its process of economic liberalisation in 1978, the government had adopted an inward looking policy with emphasis on self-reliance and economic independence; it was, therefore, strongly opposed to FDI and the establishment of multinational corporations so common in the West. At that time, it was felt that the presence of Western multinationals brought no benefits to the host country. However, once China had embarked on the process of economic liberalisation and the Chinese–Foreign Joint Ventures Law was enacted in July 1979, more and more transnational corporations and other foreign enterprises began undertaking production in China, thus helping to stimulate economic development (Chen, 1992, 1996; Cheng & Kwan, 2000). As a result, China came to adopt a different attitude towards the importance of FDI, and by the late 1980s, not only had the Chinese government continued the process of liberalisation, welcoming foreign capital, technology and management experience with its open door policy, but it was also encouraging the expansion of overseas investment by Chinese enterprises, with OFDI becoming a part of the strategy for economic development based on institutional transformation. The ‘Going Out’ (zouchuqu) policy, which was officially proposed in 2000, emphasised that the Chinese government should support and encourage homeland enterprises that had a competitive advantage to compete globally through an active internationalisation process. At the same time, the Chinese government supported such enterprises by promoting their transnational operations and using resources overseas.

Furthermore, as a result of gradual institutional transformation, China’s economy has been able to grow rapidly, and China is often cited as the leading example of a successful gradualist approach to institutional change, with better results than Russia’s reforms through shock therapy, thereby driving the rapid growth in foreign outward investment (Lau et al., 2000; Smyth, 1998). China’s central government policies and regulations have played a critical role in its overseas investment. In 2011, experiments with the use of the renminbi in OFDI were permitted, reflecting the progressive internationalisation of China’s currency. The 12th Five-Year Program (2011–2015) emphasised the importance of its ‘Going Out’ strategy and OFDI was projected to increase at an annual rate of 17 per cent and hit US$150 billion by 2015. In November 2013, China unveiled an aggressive reform package after the Third Plenum of the 18th Communist Party of China’s Central Committee. The package included signing more bilateral and multilateral investment agreements for boosting China’s overseas investment.

Chinese multinational companies have played an important role in overseas investment activities. Furthermore, Chinese multinational companies are large in size; for example, China International Trading and Investment Corporation (CITIC Group), with foreign assets of US$71.5 billion, was the largest overseas investor in 2011. China Ocean Shipping (Group) Company was second with foreign assets of US$40.4 billion, followed by the China National Offshore Oil Corporation, China National Petroleum Corporation and the Sinochem Group. Indeed, China was once an insignificant OFDI country, but it has progressed to become an important source of global investment. According to the United Nations Conference on Trade and Development, China was ranked as the fourth largest source of global OFDI (after Japan, USA, Netherlands and China) in 2019, up from sixth in 2011. However, the COVID-19 pandemic could have an adverse effect on China’s OFDI.

Based on the evolution of FDI, the effects of OFDI on the home or host country’s economy will be profound, even if it has (like China) become a major exporter of OFDI in recent years, but the location choice and OFDI pattern are still the main determining factors of OFDI decisions. In terms of the geographical distribution of China’s OFDI, prior to 1990, the most important countries for such investment were the developed countries, including the USA, Canada, Australia and New Zealand. Since 1990, the major recipient nations in terms of the largest amounts of Chinese OFDI are Asian countries including Hong Kong, South Korea, Thailand, Macau, Indonesia, Singapore, Japan and Vietnam. The share in the Asian region had risen to 77.89 per cent in 2008, and then, it increased to 80.96 per cent in 2019, with Hong Kong alone accounting for 66.64 per cent of the total.

Hong Kong has historically been the favoured host region of Chinese round-tripping OFDI, as there are incentives for Chinese companies to comply with the ‘foreign-owned enterprises’ (FOE) status. Many Chinese firms invest in Hong Kong to transform their identity, obtain an FOE status and invest in China under a different identity. Obtaining hard evidence of the actual figure of round-tripping is not easy. The estimate for round-tripping FDI from Hong Kong to China is likely to be in the range of 23–50 per cent (Li, 2013).

In reflecting on China’s status as an economy undergoing institutional transformation, it should be noted that its OFDI has a unique characteristic, namely the majority of Chinese enterprises that invest overseas are state-owned enterprises, and the government maintains extensive control over the market operations of its state-owned enterprises. Today, China possesses a group of highly competitive medium-sized multinational corporations that enjoy both an ownership advantage and internalisation advantage; companies such as the China National Petroleum Corporation (CNPC), the Haier Group and Capital Steel & Iron have all invested overseas. Other companies that lack the international brand recognition of the firms noted above, such as the CITIC Group (China International Trust and Investment Corporation) and Konka, have also undertaken overseas investment.

Whether or not traditional FDI theory can explain the OFDI activity of China’s business enterprises is an interesting question. Given China’s status as the most important transitional economy in the world, studies on China’s OFDI activity should provide valuable lessons for other countries engaged in a process of economic transformation when deciding whether or not to actively promote OFDI.

To date, the results of empirical studies on the determinants of China’s OFDI are rather mixed and many research themes remain unsolved (Paul & Benito, 2017). In terms of factors determining China’s OFDI, for example, Liu et al. (2005) pointed out that the level of economic development is the main factor explaining China’s OFDI. Buckley et al. (2007) indicated that Chinese OFDI is attracted to countries with high political risk. Cheng and Ma (2008) found that the host countries’ GDP and sharing of a common border with China had a significantly positive impact on China’s OFDI. Cheung and Qian (2009) found no substantial evidence that China invests in Africa and oil-producing countries for their natural resources, while Kolstad and Wiig (2009) suggested that China’s OFDI is attracted to large markets and to countries with a combination of large natural resources and poor institutions. Whalley and Xin (2010) argued that China’s OFDI contributes to the rapid growth of China’s economy. Huang and Wang (2011) indicated that market size, production costs and legal environment did not impact Chinese investors’ choice of location. However, Chou et al. (2011) pointed out that both the degree of economic integration and host country’s political risk have a negative influence on China’s OFDI. Ramasamy et al. (2012) documented that Chinese state-owned enterprises are attracted to countries with large sources of natural resources and high risky political environments. Dong and Guo (2013) proposed that China’s public firms are more likely to conduct cross-border mergers and acquisitions (M&A). Wei et al. (2014) pointed out that productivity, technology-based capability, export experience, industry entry barriers, subnational institutions and intermediary institutional support, all play an important role in Chinese firms’ OFDI decisions. Huang et al. (2017) found that a high percentage of China’s state-owned shares have negative effects on state-owned enterprises’ (SOEs’) OFDI. As to the impact of China’s OFDI on host country, Gusarova (2019) expressed that China’s OFDI has a very strong impact on the economic growth of BRICS countries. Hao et al. (2020) suggested that China’s OFDI increased domestic environmental pollution. This anomaly makes the empirical exploration of China’s OFDI an appealing issue.

Thus, the main purpose of this study is to explore factors determining China’s OFDI, with emphasis on the unique characteristics of China’s economy during the period of institutional transformation. Furthermore, we wish to fill a gap in the existing literature. The remainder of this article is organised as follows: the second section of the article explores the motivation and business model behind Chinese OFDI. The third section describes the empirical research methods and data sources used. The fourth section presents the empirical analysis, in which panel data are used in the empirical testing, with the F test, Hausman test and LM (Lagrange multiplier) test being used to determine whether a fixed effects model, random effects model or pooled regression model should be used in the empirical analysis. The conclusions are presented in the fifth section.

The Motivation and the Business Model Underlying Chinese Outward Foreign Direct Investment

The ultimate goal of Chinese enterprises that invest overseas is to leverage the penetration of international markets and the establishment of global reach to reduce production costs, maximise earnings and expand their scale of operations, as they seek to create true Chinese multinationals. The Chinese enterprises’ motivation for investing overseas is described in the following sub-sections (Hong & Sun, 2006; Luo et al., 2010; Wong & Chan, 2003; Wu & Chen, 2001; Yeung & Liu, 2008).

Acquiring Production Resources

Business enterprises seek to maximise their profits, while at the same time trying to ensure the maintenance of a stable supply of production resources. As China’s economy has grown and its industry has expanded, Chinese enterprises have found it increasingly hard to obtain the resources they need. Taking petroleum as an example, China had become a net oil importer by 1993. Energy shortages have had a major impact on Chinese industry and on China’s overall economic development. As a result, Chinese enterprises have been forced to look overseas for the resources they need, to compensate for the shortfall at home.

Securing Access to Advanced Technology and Managerial Expertise

In the past, China relied heavily on attracting foreign companies to invest and establish factories in China, so that China could benefit from technology transfer and from foreign companies’ managerial experience. Unquestionably, this policy did indeed help to enhance China’s overall competitiveness. Even so, Chinese firms continue to lag behind their counterparts in the developed nations in terms of technology and management expertise. In the last few years, Chinese enterprises have begun to adopt a strategy of investing in and setting up production facilities in developed nations as a means of securing access to technology and managerial experience.

Boosting Market Share in International Markets

One of the motivating factors behind the growth of China’s OFDI is the desire to boost exports and overcome barriers to trade. Setting up factories in the markets to which China exports its goods can help Chinese companies boost their market share, while also enabling them to gain access to more detailed data on supply and demand in international markets. Another factor is the rapid growth in the productivity of China’s home appliance and automotive industries since 1990. With the domestic market already saturated, and with few prospects of a dramatic increase in domestic demand in the near future, many Chinese companies have found themselves suffering from overcapacity. Investing overseas helps firms to expand their distribution channels and develop overseas markets more effectively.

Leveraging Technological Advantages

In comparison with developing countries in Africa or Latin America, China’s home appliance, textiles and food processing industries have already reached a high level of development. This disparity has encouraged Chinese firms to concentrate their overseas investment efforts on developing nations. There has also been significant direct investment in regions with large ethnic Chinese populations by firms producing ‘traditional Chinese products’, for example, Chinese herbal medicines, gardening products, ingredients for Chinese cuisine, etc.; this type of OFDI represents an effective leveraging of the technological advantage that China possesses in certain areas.

Capital Flight

China’s enterprises have the incentive to set up subsidiaries overseas to achieve a more balanced portfolio and evade the foreign exchange and other restrictions with which they are saddled at home. This is the phenomenon generally referred to as capital flight. China has recently experienced large-scale capital fight, which has been accompanied by dynamic growth and the attraction of foreign investors. According to an empirical estimate by Wang et al. (2009), the amount of capital flight from China in each year over the period 1997–2002 was greater than the sum of FDI inflows and external debt. As the process of liberalisation has continued, and as Chinese business enterprises have grown stronger, more Chinese firms have begun to consider investing overseas. The exact form that the overseas investment takes has varied depending on the capabilities of the individual firm, the industry to which it belongs and the strategy that it adopts.

Some of the main models employed by Chinese enterprises when investing overseas are outlined below (Gao, 2009; Guo, 2008; Lu & Yan, 2005; Morck et al., 2008; Wu, 2008):

With this model, a firm’s main objective when investing overseas is to build up its international distribution and sales network, so that it can market its goods directly in other countries, thereby boosting the firm’s earnings performance. The overseas investment undertaken by the 999 Group, China’s leading pharmaceuticals manufacturer, represents an example of this model. All the 999 Group’s manufacturing facilities and R&D centres are located in China, while its overseas subsidiaries focus on marketing and sales. Since 1992, the 999 Group has established sales companies in over a dozen different countries, including Hong Kong, Russia, Malaysia, Germany and the USA; these sales companies play a very important role in promoting the sale of 999 Group products in overseas markets. Other companies that have adopted this type of model for their overseas investment activities include the Fuyao Group, the Tiens Group, the Sinochem Group and the China Technology Group. The main advantage of this model is that a firm can expand the scale of its exports directly and can access market information more effectively. However, if a company’s production, purchasing and R&D functions are still located in China, it is likely to be affected by trade barriers in its overseas markets.

The term ‘offshore processing’ is used to refer to a situation where a company establishes an offshore production facility or facilities, thereby boosting exports of production equipment, technology, materials and components produced in the company’s home country. As offshore processing is ideally suited to China’s current needs as an economy undergoing transformation, over the last few years, it has emerged as an important model for overseas investment by Chinese enterprises. Most of the firms that have adopted this model are in industries such as textiles, home appliances, light industry or machinery manufacturing, which are characterised by mature technologies and over-capacity; for example, in the mid-1990s China’s textile industry found itself faced with a shrinking domestic market, severe overcapacity and trade barriers (in the form of export quotas) in international markets. The China Worldbest Group responded by establishing offshore processing facilities in Mexico, Canada and Thailand, thereby exploiting country-of-origin rules in order to develop overseas markets. The overseas investment undertaken by the Konka Group, the Gree Group and the Chunlan Group has also followed this model. Overseas investment using this model can help drive export growth, while also speeding up the transformation of China’s industrial structure.

Under this model, Chinese companies that already possess strong brands make use of joint ventures, franchising or chain store operations to develop overseas markets. One example of a Chinese firm that has employed this model effectively is Tongrentang (TRT), a Beijing company that has been in existence for over 330 years. Today, TRT is a large, modern manufacturer and vendor of Chinese herbal medicines; its trademark is registered in over 50 countries and regions, and its products are sold in more than 40 countries throughout the world. A precondition for successful use of this model is that the company must already possess a strong brand and its own intellectual property; since the vast majority of Chinese companies possess neither, only a handful of firms so far have been able to make this model work for them.

With this model, a Chinese company buys voting shares in a foreign company (usually a listed company), either on the open market or by subscribing to capital increments, with a view to building up a sufficiently large stake to be able to exercise control over the company’s management. The last few years have seen a gradual increase in the number of Chinese companies making use of this strategy; for example, in 2001, the Wanxiang Group acquired Universal Automotive Industries (UAI) Company, a company listed on the NASDAQ (National Association of Securities Dealers Automated Quotations) stock exchange in the USA. Investing overseas through the purchase of shares in foreign companies is a relatively cheap form of overseas investment, as it does not require any increase in shareholders’ tax liabilities; on the other hand, a Chinese company that uses this model does have to take on the liabilities of the target company.

Empirical Model and Description of Data

The empirical model employed in the present study is based on Liu et al. (2005) and Buckley et al. (2007), whose models have been revised to conform to the objectives of the present study. The regression equation can be represented by Equation (1):

where OFDI ijt represents the outward flow of FDI from China to the recipient country at time t. PGDP jt /PGDP it represents the relative size of per capita GDP in the recipient country and in China, measuring the level of the economic development of the recipient country relative to China. If the estimated coefficient β1 is greater than zero, this would suggest that China’s OFDI flows more into developed countries than other countries. GGDP jt represents the growth rate of GDP in the recipient countries for each year and is used to measure the market potential in the recipient countries. The market growth hypothesis suggests that a region with a high economic growth rate will also offer greater opportunities for profit-making and will, therefore, attract more inward FDI (Lim, 1983). Therefore, the coefficient of the variable of GGDP jt will indicate whether China’s OFDI is motivated by a desire to expand market share in the international market.

Export ijt represents China’s export volume to the recipient country of its OFDI. Leichenko and Erickson (1997) suggested that there is a causal relationship between a country’s exports and its OFDI. An enterprise’s first interactions with overseas markets will be through exports. As exports increase, the firm may decide that it needs to establish sales companies to market its products in overseas markets. Eventually, the firm may decide to engage in direct investment in overseas markets, setting up production facilities in these countries. Thus, the relationship between OFDI and exports is a complementary one. However, China’s OFDI has mainly been undertaken with a view to avoiding barriers to trade, and so, in China’s case, the relationship between exportation and FDI is one of substitution.

Import ijt represents the volume of China’s imports from the recipient countries of its OFDI. According to the internalisation advantage theory, if the cost of importing the resources that an enterprise needs for production becomes too high, or if the firm finds it difficult to access these resources, then the firm can be expected to engage in OFDI so as to obtain the resources it needs (Buckley & Casson, 1976). DIST ij represents the geographical distance from country i (China) to recipient country j, and it is measured between capital cities. This variable is used to represent the costs of doing business in foreign countries, as suggested by the gravity model (Egger, 2008). Its expected sign is negative, since countries that are geographically close should have lower costs of making investments, and correspondingly larger levels of Chinese OFDI.

Xit is the variable that represents the characteristics of the Chinese economy, where ERATE it , BRAND it , RESERVE it and S&Tit-1 are used to measure the different characteristics of the Chinese economy during this period of institutional transformation. ERATE it represents the exchange rate of the renminbi against the US$. Summary and Summary (1995) noted that there is a pronounced relationship between the revaluation of a nation’s currency and its OFDI. China’s rapid economic growth has led to the revaluation of the yuan that has made assets, production equipment and the like in other countries relatively cheaper, thereby facilitating overseas investment by Chinese firms.

BRAND it measures the monopolistic advantage of the Chinese company. The strengthening of Chinese brands that has accompanied the growth in the scale of operations of Chinese enterprises in recent years has also contributed to the increase in China’s OFDI. According to Hymer’s (1960) ‘monopolistic advantage’ theory, when a company possesses a competitive advantage in terms of management, sales or production technology, that company will be encouraged to leverage this advantage by engaging in FDI, in order to boost its profits.

RESERVE it denotes the foreign exchange reserves owned by China. China has experienced rapid growth in its foreign exchange holdings. Indeed, China’s huge foreign exchange holdings have led to imbalances in its economy. One of the policies adopted by the Chinese government to mitigate the negative effects of China’s large foreign exchange holdings has been to encourage both state-owned and private sector enterprises to engage in overseas investment.

S&Tit-1 represents the level of technology intensity in China. The new growth theory holds that technology is one of the most important factors contributing to FDI, and the relationship between technology and FDI was investigated by empirical studies. Trevino et al. (2000) found that the higher the level of a company’s technology intensity, the more international experience its managers possess, the higher its earnings, and the more oriented it will be towards overseas investment. Aliber (1970) suggested that when a country whose currency is increasing in value possesses an advantage in technology, that country’s business enterprises will start to re-orient themselves away from undertaking original design manufacturing (ODM)/original equipment manufacturing (OEM) production for foreign vendors towards establishing production facilities overseas. Spending on technology constitutes an important foundation for building technological capabilities; however, the benefits from investment in technology generally take some time to make themselves felt. Therefore, a one-period lag value of spending on technology is used as a proxy variable for measuring the technology intensity level in China.

The global financial crisis of 2008 slowed down global economic growth, therefore, the empirical research in the present study uses data for 40 of China’s major OFDI recipient countries (all of which have had intensive investment relations with China over an extended period) for a restricted period of 5 years from 2003 to 2007. Nevertheless, our dataset is still valid and worthwhile for empirical testing and implication. 1

The volumes of China’s OFDI to major countries between 2003 and 2007 are taken from China’s Ministry of Commerce (2009); the values for GDP and per capita GDP are obtained from the World Bank (2009) dataset and China Statistical Yearbook 2004–2008 (National Bureau of Statistics, 2004–2008); and the volumes of China’s exports and imports with its trading partners between 2003 and 2007 are taken from China Customs (2009). The geographical distances between countries are taken from the ‘distance calculator’ found at

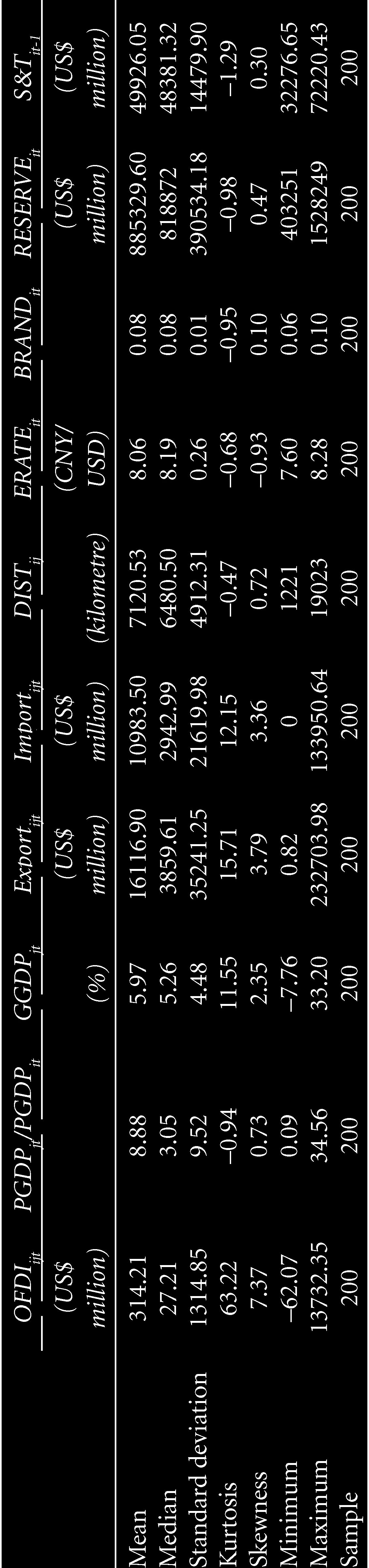

Summary Statistics of Variables Used for Empirical Testing

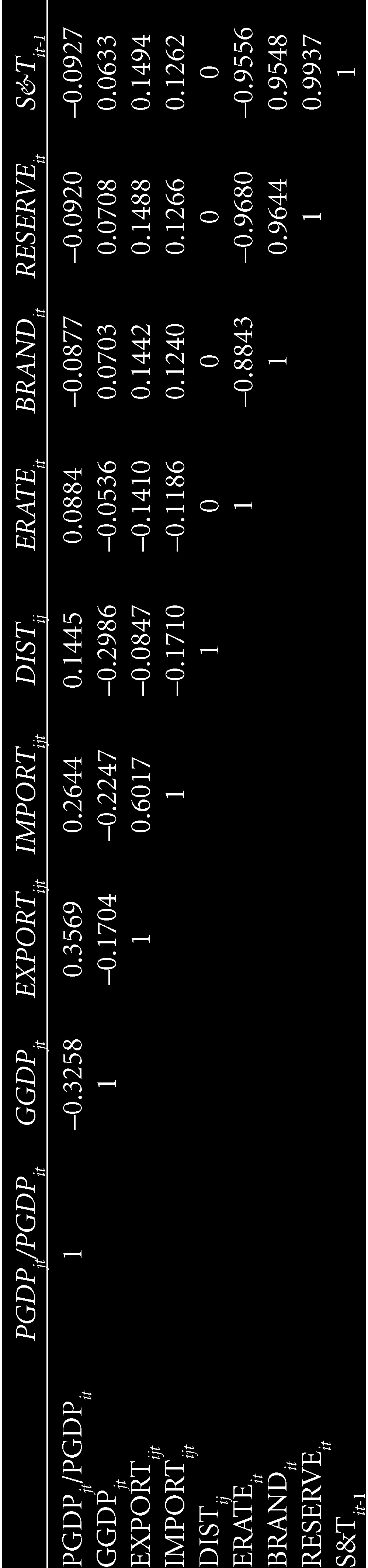

Pairwise correlation coefficients were calculated for all the explanatory variables to avoid the risk of multicollinearity. The absolute values of the correlation coefficients for most independent variables were found to be within the range of 0.0536–0.6017, but the pairwise correlation among BRAND, ERATE, RESERVE and S&T was found to be rather high (see Table 2). In such a case, we should be careful regarding the issue of multicollinearity and consider only one of these variables in the regression model at a time. Moreover, sensitivity tests are used to develop a more robust set of empirical results for the empirical model. According to the sensitivity tests, if the coefficients are not sensitive to the inclusion of different variables, for example, the coefficients do not change signs or become insignificant, then the variables can robustly affect the dependent variable. Only the robust results of the empirical model are presented.

Correlation Coefficients of the Independent Variables

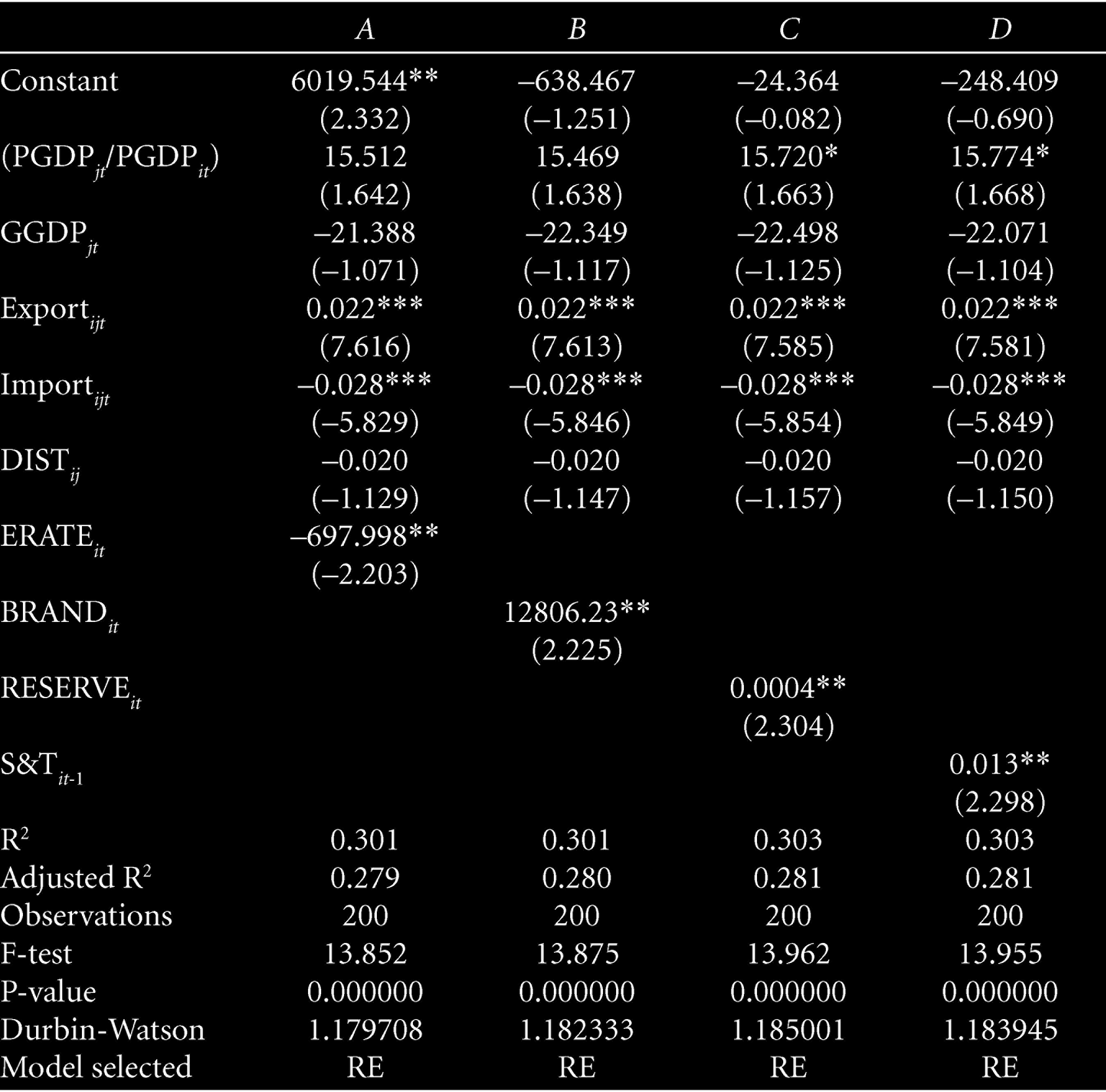

Pooled cross-section and time-series data are employed for the empirical estimation. As the data used consist of panel data, the pooled regression model, the fixed effects model and the random effects models have been estimated (Hsiao, 1986). To obtain the most suitable models, we have employed the F-test, Hausman test and LM test. F-test is used to choose between the fixed effects model and the pooled regression mode; the Hausman test is used to choose between the fixed effects model and the random effects model; and the LM test is performed to choose between the random effects model and the pooled regression model. The robust results of the empirical models are shown in Table 3. As the pairwise correlations among BRAND, ERATE, RESERVE and S&T are rather high, to avoid multicollinearity, we consider only one of these variables in the regression model at any one time. The regression results for the alternative models are presented in columns A–D, respectively.

Regression Results of China’s Outward FDI

Regression Results of China’s Outward FDI

The empirical results show that the coefficients for ERAT, BRAND, RESERVE and S&T are statistically significant (columns A–D); hence, these four variables play important roles in determining China’s OFDI. Furthermore, China’s OFDI to the recipient countries is significantly related to China’s export (Export ijt ) and import (Import ijt ) relationships with those countries. The relative sizes of the per capita GDP in the recipient country and in China (PGDP jt /PGDP it ) are statistically significant at the 10 per cent significance level. The GDP growth rates of the recipient countries (GGDP jt ) and geographical distance (DIST ij ) have no effects on the determination of China’s OFDI.

More details of the empirical results with the insight that they provide are illustrated as follows. First, the significance level of the coefficient for (PGDP jt /PGDP it ) can somewhat provide evidence that China’s overseas investment has been mainly targeted at developed economies such as the USA, Canada and Australia. The main purpose of this investment has been to acquire advanced managerial experience and technology. One example here is the acquisition by the Wah Lee Industrial Group of the CDMA (Code Division Multiple Access) R&D division of Philips’ US subsidiary.

The coefficient of GGDP jt is not significant, suggesting that the GDP growth rates of recipient countries have nothing to do with the determination of China’s OFDI. The results of the estimation seem to show that the main motivation underlying China’s OFDI is not the desire to achieve higher profits or grow market share in overseas markets, but rather the desire, for instance, to secure ready access to raw materials, technology, labour, and so on (Wheeler & Mody, 1992); for example, China has invested heavily in Africa to help make up for its domestic shortages of minerals and petroleum. Chinese investment in developed nations is normally undertaken to gain access to advanced technology rather than to achieve direct earnings growth.

China’s volume of exports to its trading partners has a significantly positive effect on its OFDI to that trading country. According to Vernon’s (1966) product life cycle theory, the relationship between FDI and exports is a relationship that may display aspects of both complementarity and substitution, depending on the motivation underlying the individual firm’s FDI activity, the category to which the firm belongs and the stage of development that it has reached. Broadly speaking, the relationship between FDI and exports in China is a complementary one; exports are one of the factors that lead to changes in FDI. The idea that exports can drive FDI conforms to international business theory. The internationalisation of a business enterprise is a gradual process that starts with exportation; once a company has built up a strong brand or a high market share in its export markets, it may decide to undertake direct investment if there are profits to be made. In China’s case, China has already built up significant export competitiveness in the years since the process of economic reform began; as a result, Chinese enterprises have gradually acquired the capabilities needed to engage in OFDI.

China’s volume of imports from its trading partners has had a significantly negative effect on its OFDI to those trading countries. Chinese enterprises have often relied upon the importation of key components as a means of acquiring the technology they need. For some years now, Japan has been China’s main source of imports; China imports large quantities of semiconductors and other electronic components, as well as high-end automotive components, etc., from Japan. Given the high cost of investing in Japan, it makes more sense for Chinese companies to obtain advanced technology from Japan in this way than to undertake direct investment in Japan. In this sense, the relationship between imports and OFDI for China is one of substitution.

The coefficient of geographical distance (DIST ij ) is not significant, apparently having no effect on the determination of China’s OFDI. The viewpoint of the gravity model cannot be confirmed in the Chinese case. The motivation underlying Chinese enterprises’ overseas investment does not appear to be influenced by the geographical distance between China and the country being invested in 2 ; for example, the regions that have received large quantities of Chinese investment aimed at ensuring a stable supply of production resources for China include Australia, Brazil and South Africa (mineral resources), the USA, Argentina and East Africa (marine resources) and Central Asia and Africa (petroleum) (Liu et al., 2005; Pannell, 2008). Most of these countries and regions are located at considerable distances from China, and China does not seem to be particularly sensitive to the rising costs of transporting these resources. The main targets for OFDI where the aim is to gain access to technology and managerial expertise are Europe and the USA. It can, thus, be seen that there is no significant relationship between geographical distance and OFDI in China’s case.

The lower value of the exchange rate between the renminbi and the respective foreign currency has a significant positive effect on Chia’s OFDI to that country. Having run a huge trade surplus for many years, China has seen a steady increase in its foreign exchange reserves and has been under pressure from other members of the international community to revalue the yuan. The rise in the value of the yuan has fuelled housing and stock market booms; at the same time, Chinese enterprises have been able to take advantage of the revaluation to purchase overseas assets and acquire foreign firms at lower cost. Acquisitions represent the fastest and most effective way for Chinese companies to establish themselves in overseas markets; the revaluation of the yuan has helped many Chinese corporations to acquire technology, human talent and distribution networks by acquiring foreign companies.

The coefficient of monopolistic advantage (BRAND) is statistically significant; hence, this variable plays an important role in determining China’s OFDI. Traditional FDI theory holds that firms that possess an ownership advantage can be expected to undertake overseas investment so as to boost their profits. The empirical results obtained in the present study provide evidence of a positive correlation between the possession of brand advantage by Chinese firms and OFDI. As Chinese enterprises grow and develop a stronger brand image, they acquire the capabilities needed to undertake overseas investment; thus, traditional FDI theory does help to explain OFDI behaviour in China.

The volume of foreign reserves (RESERVE) held by China has a significantly positive effect on the OFDI behaviour of China; that is, the empirical results indicate that the rapid growth in China’s foreign exchange holdings in the past few years has contributed to the increase in OFDI. According to data compiled by China’s State Administration of Foreign Exchange, as of the end of March 2009, China’s foreign exchange reserves had increased five-fold since 2003. This dramatic increase is attributable mainly to the large inflows of foreign capital that China has received and to China’s huge trade surplus. From China’s point of view, the growth in the nation’s foreign exchange reserves increases the amount of influence that China is able to exert in international affairs, boosts China’s international payments ability and helps China to combat risk. It also gives Chinese enterprises an enhanced ability to engage in OFDI.

The level of technological intensity is statistically significant, and it has a positive effect in terms of explaining China’s OFDI. The ongoing increase in the amount that Chinese enterprises spend on technology has led to a gradual strengthening of Chinese firms’ technological capabilities, which in turn has enhanced their ability to internationalise their operations through FDI.

The rapid increase in FDI activity by multinational corporations since the 1960s has been one of the most important factors contributing to the process of economic globalisation. Rising OFDI has helped China to compete more effectively at the international level and to participate in the process of economic globalisation. The empirical results obtained in the present study point to a number of salient findings and implications. Chinese enterprises tend to invest in countries that have a mature economy. OFDI enables Chinese firms to acquire advanced technology and equipment, thereby helping to enhance these firms’ overall competitiveness. Exports have a significant positive effect on China’s OFDI, and the relationship between FDI and exports in China is a complementary one. China has already built up significant export competitiveness in the years since the process of economic reform began; as a result, Chinese enterprises have gradually acquired the capabilities needed to engage in OFDI. The relationship between imports and OFDI for China is one of substitution, as Chinese enterprises have often relied upon the importation of key components as a means of acquiring the technology they need.

It is interesting to note that four key variables—exchange rates, monopolistic advantage, foreign exchange reserves and technology intensity level—have a significant impact on China’s OFDI. The revaluation of the yuan, the growing strength of Chinese brands, the upgrading of the technology level of Chinese firms and the steady increase in China’s foreign currency reserves have strengthened the competitiveness of Chinese business enterprises to the point where they are in a position to engage in OFDI on a large scale.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.