Abstract

Trade finance is integral for international trade as it offers fluidity and safety to the movement of merchandise and services globally. After the financial crisis of 2008–2009, there has been an increase in the use of open accounts, which enhances the possibilities for availing factoring for international trade. International factoring has witnessed considerable growth in the last decade. This article examines the relationship between international factoring and cross-border trade using Granger causality. It also examines the causal relations of international factoring with disaggregated data of cross-border trade of imports and exports. We find a unidirectional causal flow from international trade to international factoring, and a unidirectional casual flow from exports to international factoring.

Introduction

Cross-border trade is indispensable in a globalised world. International trade varies from domestic trade in several dimensions. For a start, time-to-ship, that is, the time required for goods to ship and reach their destination, is longer in international trade as against domestic trade. Djankov et al. (2010) found that the median time-to-ship in cross-border trade is 21 days. Further, it is more difficult to enforce contracts across borders and risk exposures are high (Schmidt-Eisenlohr, 2013, p. 98). Prominent risks include insolvency risk, transportation risk, exchange rate and political risk (Auboin, 2007, p. 5).

As trade partners engage in international trade, they have to decide among the various terms of financing available to support cross-border trade. Prominent among these are letters of credit, cash in advance, working capital loans and overdrafts, open accounts, and forfaiting or international factoring (Antras & Foley, 2015, p. 6; Auboin & Meier-Ewert, 2003, p. 1; Schmidt-Eisenlohr, 2013, p. 96). These financing modes can be categorised into bank-mediated and non-bank forms of financing.

Around 90 per cent of the world trade relies on trade finance (Auboin, 2009, p. 37). Payment contracts or mode of payments can influence prices, quantities and patterns of cross-border trade (Schmidt-Eisenlohr, 2013, p. 106). Constraints in trade finance negatively affect international trade—a contraction of credit due to the financial crisis of 2008–2009 adversely affected trade (Auboin, 2009, p. 37; Berman et al., 2013; Paravisini et al., 2014), and it was followed by a shift in the preferred modes of trade financing. Bank-mediated financing declined considerably, whereas the use of open accounts and cash in advance have been heavily used post-financial crisis (Antras & Foley, 2015, p. 1). It is expected that the use of other forms of financing, such as international factoring, also subsequently increased, as open accounts are generally bundled with other modes like factoring and export credit insurance (Schmidt-Eisenlohr, 2013; Open Accounts, n.d.).

Developments in banking and financial institutions, especially in the exporting country, also facilitate the use of international factoring (Manova, 2013, p. 27). Factoring can encourage firms to engage in cross-border trade on open accounts without fear of bad debts and offer immediate cash to the exporting firm. Another key point to note is that it also helps the importing firm in availing a credit period.

Factoring companies offer exporting firms credit protection, working capital financing and collection services. These bundled services might also allow local exporters to enter new and riskier overseas markets (Klapper, 2006a). The past decade witnessed tremendous growth in international factoring compared to domestic factoring. The average growth of international factoring was 11.81 per cent as against 7.2 per cent for domestic factoring for the period 2009–2018. The share of international factoring to total factoring in terms of volume of transactions has also steadily improved in the period 2008–2019 (Factors Chain International, 2014). Auboin et al. (2016) attributed the growth of factoring in cross-border trade to two phenomena: rising global supply chains through the growth of open account trade, involving ecosystems of small and medium-sized enterprises (SMEs); and receding bank-mediated trade finance since the financial crisis.

This article aims to examine the relationship between international factoring and international trade using the Granger causality approach. We investigate the causal influence of international factoring on international trade and vice versa. It contributes to the existing literature on trade finance by examining the causal relationship between international factoring and international trade. Though trade finance is the fundamental element of international trade, many aspects of trade finance remain unexplored (Schmidt-Eisenlohr, 2013, p. 106). Second, most of the previous studies have concentrated on the influence of trade finance on international trade. In contrast, the influence of cross-border trade on the use and demand for trade finance has been overlooked. The findings of this study show the need for more studies on this aspect. Third, it also contributes to the literature on factoring, wherein studies on international factoring are scarce.

The remaining section of this article is divided as follows: Section 2 provides a review of the literature. Sections 3 and 4 present the research methodology and empirical results, respectively. Finally, Section 5 offers the conclusion and policy implications.

Review of Literature

Trade Finance and International Trade

From the international finance literature, the influence of finance on cross-border trade can be categorised into two classes. The first class of literature concentrates on effects of trade credit on cross-border trade (Berman & Martin, 2012, pp. 329–364; Iacovone et al., 2019; Ronci, 2004, pp. 3–19). The results on this have been mixed, whereby some showed a positive influence while others indicated a negative or no association. Trade credit refers to the sale of goods or services for which payment will be received later (Amiti & Weinstein, 2011, pp. 4–5). The second area of research concentrates on the effects of trade finance on cross-border trade. Trade finance refers to working capital loans and other means of financing trade credit (Amiti & Weinstein, 2011, p. 5); it includes credit, insurance and guarantees and is considered to be the lifeline of international trade (Auboin, 2007, p. 1). It can be of short term, medium and long term, but short-term financing is considered more crucial in financing international trade (Auboin & Meier-Ewert, 2003, p. 1).

Theoretical and empirical research has shown the significance of trade finance on cross-border trade. The effect of financial market imperfections on international trade flows was examined by Manova (2013) who showed that credit constraints impede firm-level exports. Weak financial institutions lead to fewer destination markets, lower aggregate trade volumes and a reduction in export product variety. Berman and Héricourt (2010), using a cross-country firm-level database of emerging economies, showed the importance of access to finance on a firm’s entry decision into the export market. Paravisini et al. (2014) showed that negative shocks to bank credit have adverse effects on export volumes. Felbermayr and Yalcin (2011) looked at the effects of export credit guarantees on export, and found that an increase in credit boosts exports. The impact of credit was seen to be higher in lower-income countries. Minetti and Zhu (2011) found that credit-rationed firms are less likely to export and are likely to export less. Amiti and Weinstein (2011) concluded that negative financial shocks played an important role in the decline of exports. Chan and Manova (2015) established that exporting firms follow a pecking order in terms of destinations, but financial constraints cause disruptions to their decisions to enter foreign markets. Based on a theoretical model, Chaney (2016) showed that even firms which could profitably export could be prevented from exporting due to financial constraints.

While the studies discussed above approached the influence of trade finance on cross-border trade from the perspective of exports, relatively fewer studies have viewed the issue from the imports perspective. Auboin and Engemann (2014) found that increasing trade credit to a country increased real imports of that country. Castello and Gruber (2015) found that negative shocks resulted in a fall in the trade-to-GDP ratio, as the shocks reduce the capability of importing firms to purchase, and a contraction in credit worsens the ability of importing firms to access foreign suppliers. Muûls (2015) reported that firms which are less credit-constrained, and have greater productivity and profitability, have a higher probability of importing. Bernard et al. (2007) and Muûls and Pisu (2009) showed that importing firms share many similar characteristics with exporting firms.

In addition to the above studies examining the influence of trade financing on international trade, another stream of the literature concentrates on the relationship between financial development and international trade. Beck (2002) found that financial development causes an increase in exports. Hur et al. (2006) showed that countries with higher levels of financial development have higher export and trade balances in industries with more intangible assets. Becker et al. (2012) also found a positive association between financial development and exports.

It can be observed from the literature on trade finance that most of the studies have focused on investigating the influence of trade finance on international trade. In contrast, the research examining the effect of international trade on trade finance is limited.

International Factoring

Factoring is a supplier financing mechanism, where the seller avails immediate financing by selling its accounts receivables at a discount. As the underlying asset in factoring is accounts receivables, the quality of receivables resulting from the creditworthiness of the buyer is vital. Factoring can be on a recourse or a non-recourse basis; however, most of the transactions are undertaken on a non-recourse basis, whereby the factor bears the risk of non-repayment. Another essential characteristic of factoring is its implications on the firm’s balance sheet, whereby no liabilities are created despite offering working capital. Factoring is not just a medium of financing but also offers other services such as credit protection, bookkeeping and collection services (Klapper, 2006a, p. 1, 2006b, pp. 3111–3113).

Factoring can be categorised as domestic and international factoring based on the occurrence of the sale of receivables. Domestic factoring is the one in which the supplier assigns the receivables indebted by the domestic buyer(s) to the factor, whereas in international factoring the receivables are sold by the supplier primarily owned by the buyer from another country. The three major types of international factoring are the two-factor system factoring, direct import and export factoring, back-to-back factoring, and disclosed and unclosed factoring (Glinavos, 2002, pp. 4–6; Mizan, 2011, pp. 248–251).

For international trade, factoring can be of immense help to the exporter as it allows for selling on open account terms, besides covering the credit risk, and enables the exporter to avail of immediate working capital financing. It is especially highly beneficial for SME exporters, as it is resilient to SMEs’ main problems of information asymmetry, lack of collaterals and perception of high risk as the underwriting is based on the quality of the receivables (Klapper, 2006b, p. 3112). It may also help in facilitating trade credit to importers as the availability of the option of factoring could increase the confidence of the exporter in selling goods or services on credit.

Despite the benefits, there are several challenges which can arise in the facilitation of international factoring compared to the domestic counterpart. As international factoring involves parties from different countries, language and communication problems arising from different commercial traditions can create difficulties for the exporter. Assessing the creditworthiness of an importer also could be more difficult. Exchange rate volatility and political risks can act as big hurdles in international factoring (Glinavos, 2002, p. 7). However, the biggest hurdle would be issues in the creation of valid assignments in different legal systems. Different legal systems may ascribe different treatments for the assignment of transactions. Factors may need to grapple with different rules and regulations, as the types of assignment valid in one country may not be considered so in another (Glinavos, 2002, p. 7; Milenkovic-Kerkovic & Dencic-Mihajlov, 2012, pp. 432–435; Salinger, 2007, pp. 7–9). These problems may be more prevalent in the case of civil law countries (Milenkovic-Kerkovic & Dencic-Mihajlov, 2012, pp. 433–435).

To overcome the problems of assigning receivables due to different legal systems internationally, and thus improving the facilitation of international factoring, the UNIDROIT Convention was established in 1988. It recognises the significance of uniform rules by providing a legal framework that will enable international factoring to take place smoothly (Glinavos, 2002, pp. 8–9; UNIDROIT Convention on Factoring, 2020). In recent times, development efforts to unify the law on receivables assignment came in the form of the United Nations Convention on the Assignment of Receivables in International Trade (UNCITRAL). Formed on 12 December 2001, it aims to encourage the use of international receivables financing as a mode of financing international trade by reducing the cost and uncertainty involved in the process (Milenkovic-Kerkovic & Dencic-Mihajlov, 2012, p. 432; United Nations Convention on the Assignment of Receivables in International Trade, 2001).

Current State of Research on International Factoring

The literature on international factoring may be categorised into two groups. The first set of literature focuses on the role of international factoring in facilitating international trade. Huu-Phuong and Soo-Jiuan (1990) studied how export factoring can be used as a strategic financing alternative by small exporters in Singapore using data from interviews and surveys. Later, the role of factoring in financing exports was discussed by Klapper (2006a) through a conceptual study. Auboin et al. (2016) investigated the influence of international factoring on SMEs’ trade using panel data and found that increase in the availability of factoring leads to an increase in real trade flows. The second set of literature focuses on the legal and regulatory aspects of international factoring. It can be seen that more studies have been devoted to this area of international factoring (Glinavos, 2002, pp. 3–25; Milenkovic-Kerkovic & Dencic-Mihajlov, 2012, pp. 428–435; Mugarura, 2016, pp. 507–521; Salinger, 2007, pp. 7–9; Velentzas et al., 2013). In general, it can be observed that studies concentrating on international factoring are limited.

Methodology

As the main aim of this study is to examine the causal relationship between international factoring and cross-border trade, we employed the Granger causality approach. The possibility of bivariate Granger causality can be studied using the Vector Autoregressive (VAR) model to estimate whether the lags of one variable explain the current value of some other variable, and to describe the dynamics of the data (Brooks, 2019, pp. 410–421; Kumar et al., 2012). The VAR model for data series integrated on the order of 0, that is, I(0) can be estimated as

Where x and y are two-time series, α and β are the parameters for estimation, k is the lag order, N is the number of members in the panel (j = 1,…, N), t is the time period (t = 1,…, T), VN,t is an error term.

When the data are found to be integrated on the order of 1, that is, I(1), then the Granger causality can be estimated using the VAR model:

Where ∆ is the difference operator, x and y are two-time series, α and β are the parameters for estimation, k is the lag order, N is the number of members in the panel (j = 1,…, N), t is the time period (t = 1,…, T), and VN,t is an error term.

If the series of the variables are found to be integrated on the order of I(1), then a co-integration test is required to check the long-run relationships between the variables. If the co-integration between variables is confirmed, then the error correction term is required in testing Granger causality, as pure VAR in differences will be misspecified (Engle & Granger, 1987, p. 259; Granger et al., 2002).

Variance decomposition and impulse response functions are applied to examine the effect shocks on the endogenous variables. The impulse response function is used to examine the impact of innovation in one variable on the past and future values of another variable. Generally, the Cholesky decomposition, that is, the orthogonalised response function is used as it solves the issue of serial correlation of error terms in VAR, which leads to correlation in the impulse responses. This makes interpretation of the impulse response difficult. However, the Cholesky decomposition requires the ordering of variables in the system and finding an appropriate ordering of variables can be difficult. One of the ways to avoid this is to use the response function that does not depend on the ordering of variables in VAR (Kumar et al., 2012, p. 217). The generalised impulse response function as proposed by Pesaran and Shin (1998) is one way to avoid the difficulties of ordering the variables. Thus, following Kumar et al. (2012) we use generalised impulse response to analyse the shocks. On the other hand, the variance decomposition analysis offers information about the relative importance of each random innovation in affecting the variables in the VAR.

Empirical Results

Data

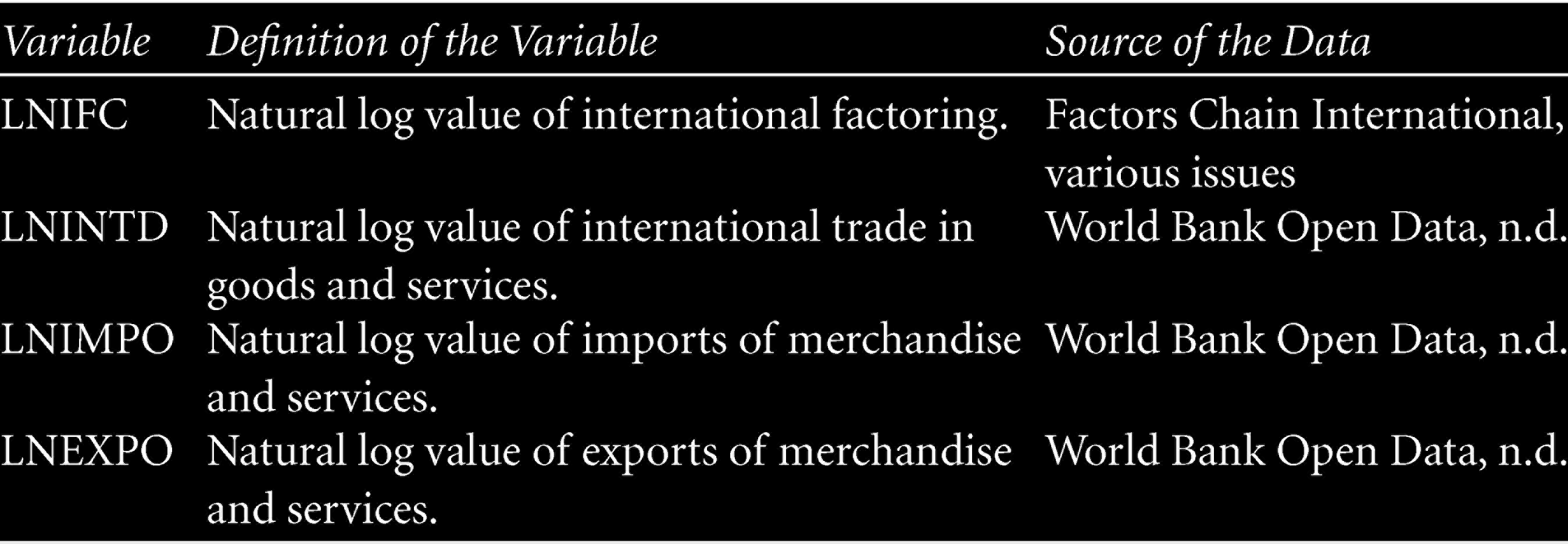

The data for the present study are obtained from Factors Chain International (FCI) and the World Bank. FCI is an international body representing factoring and receivables in the finance industry. We have used international factoring volume from the FCI and international trade data from the World Bank. These variable and data have been widely used in previous studies, thus indicating the appropriateness and reliability of the same (Auboin et al., 2016, pp. 6–7; Ronci, 2004, pp. 4–7). The list of countries included in the study is given in Table A1. The data used for the study covers the period 2008–2019. The description of the variables is given in Table 1.

Description of Variables

Description of Variables

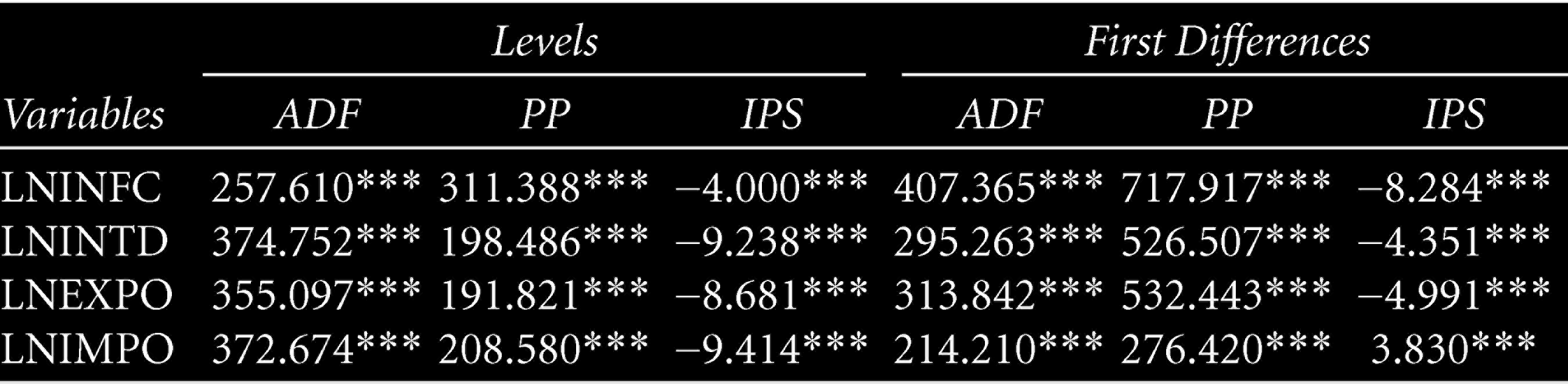

Testing the stationary of the data using the unit root test is required to avoid spurious regressions. We used Augmented Dickey–Fuller (ADF) and Im, Pesaran, and Shin (IPS) test procedures for testing the unit root of the panel data. We tested the stationarity of the data at level and at first difference with intercept and trend. With respect to the selection of lags, we used the Schwarz Info Criterion (SIC) and lag 1 for all the variables.

Table 2 shows the results of the unit root test using ADF, Phillips–Perron (PP) and IPS. It can be observed that both LNINFC and LNINTD are stationary at levels and first difference at the 1 per cent level of significance. Examining the results of the unit root tests, we consider the panel data to be integrated on the order of I(0).

Unit Root Test

Unit Root Test

*** signifies significance at the 1% level.

As the variables are integrated on the order of I(0), the Granger causality test based on unrestricted standard VAR was applied. The lag order is determined using the SIC. The optimal lag order is 3 for the relationship between LNINFC and LNINTD as well for the disaggregate data for international trade, that is, LNIMPO and LNEXPO.

To check the robustness, we tested for serial correlation in the relationship between LNINFC and LNINTD at lag 3, using Breusch–Godfrey Lagrange Multiplier Test (LM), and found no presence of serial correlation at lag 3 (see Table 3). Similarly, the LM test was performed to check for the relationship between international factoring and the disaggregated data for international trade, that is, imports and exports, and there was no serial correlation at lag 3 for the relationship between LNINFC and LNEXPO. However, the results show the presence of serial correlation between LNINFC and LNIMPO at lag 3 (see Table A2). As such, the lag order was increased to 4, and there was no serial correlation at lag 4 (see Tables A3 and A4).

LM Test for Serial Correlation Between LNINFC and LNINTD

*Edgeworth expansion corrected likelihood ratio test.

*** and ** signify significance at the 1% and 5% levels, respectively.

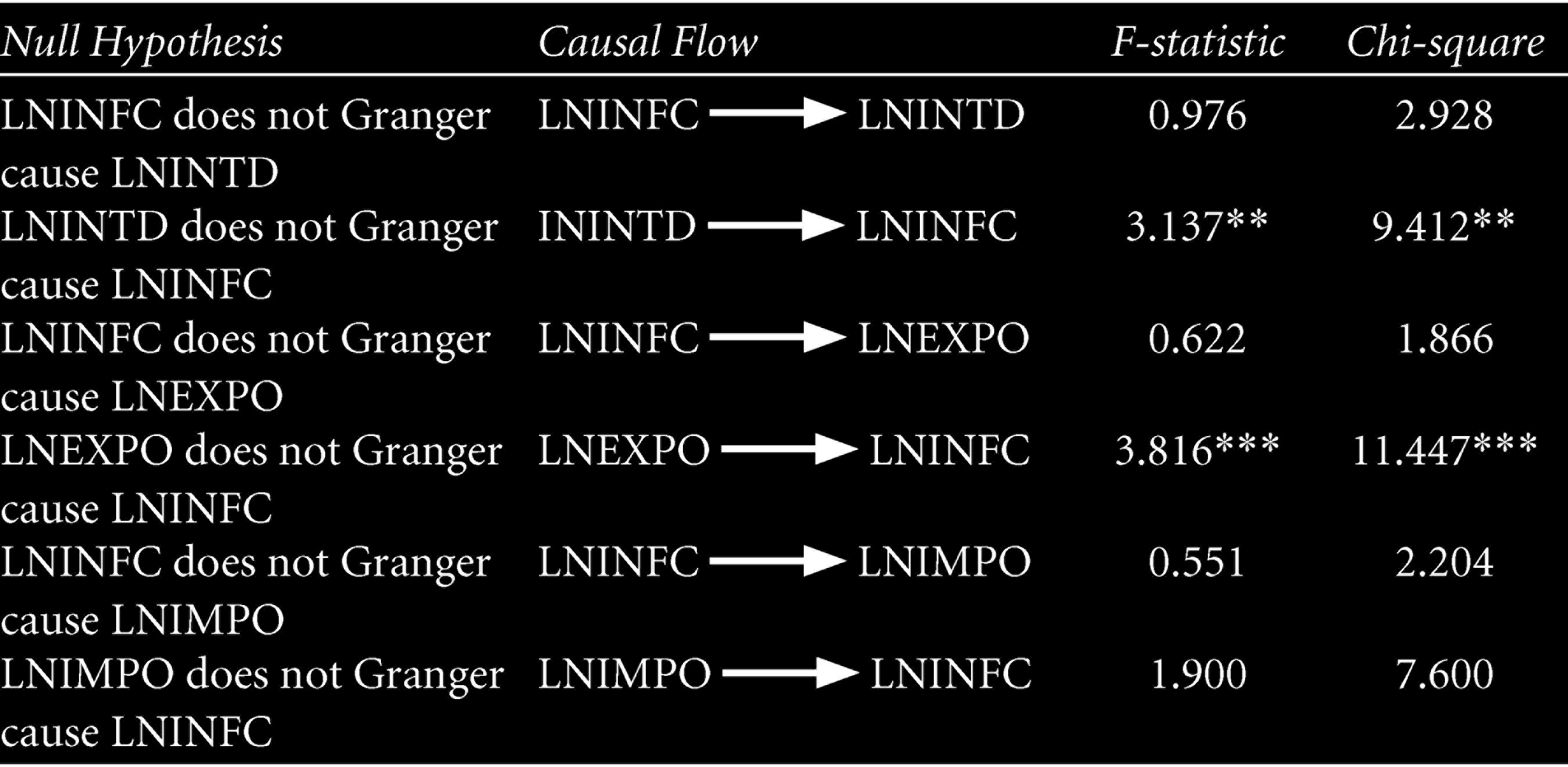

The Granger causality test was performed to analyse the causal relationships between the variables. The results show that there exists a unidirectional causal flow from LNINTD to LNINFC, implying that the lagged values of international trade influence international factoring; however, international trade is not influenced by the lagged values of international factoring. Similar observations can be seen for the relationship between LNINFC and INEXPO, where there is a unidirectional flow from LNEXPO to LNINFC. However, we found no causal relationship between LNINFC and LNEXPO (see Table 4).

Granger Causality Test

Granger Causality Test

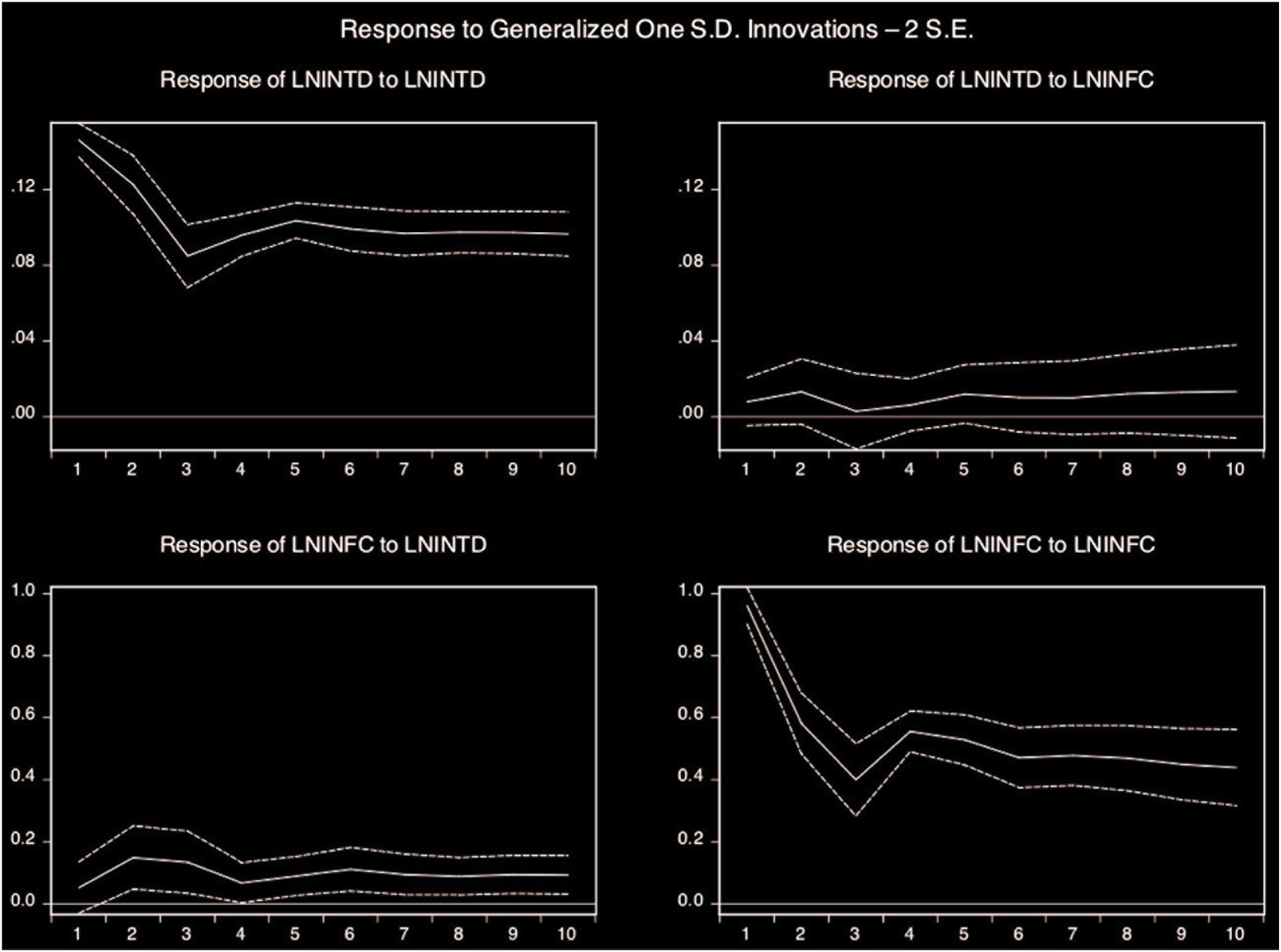

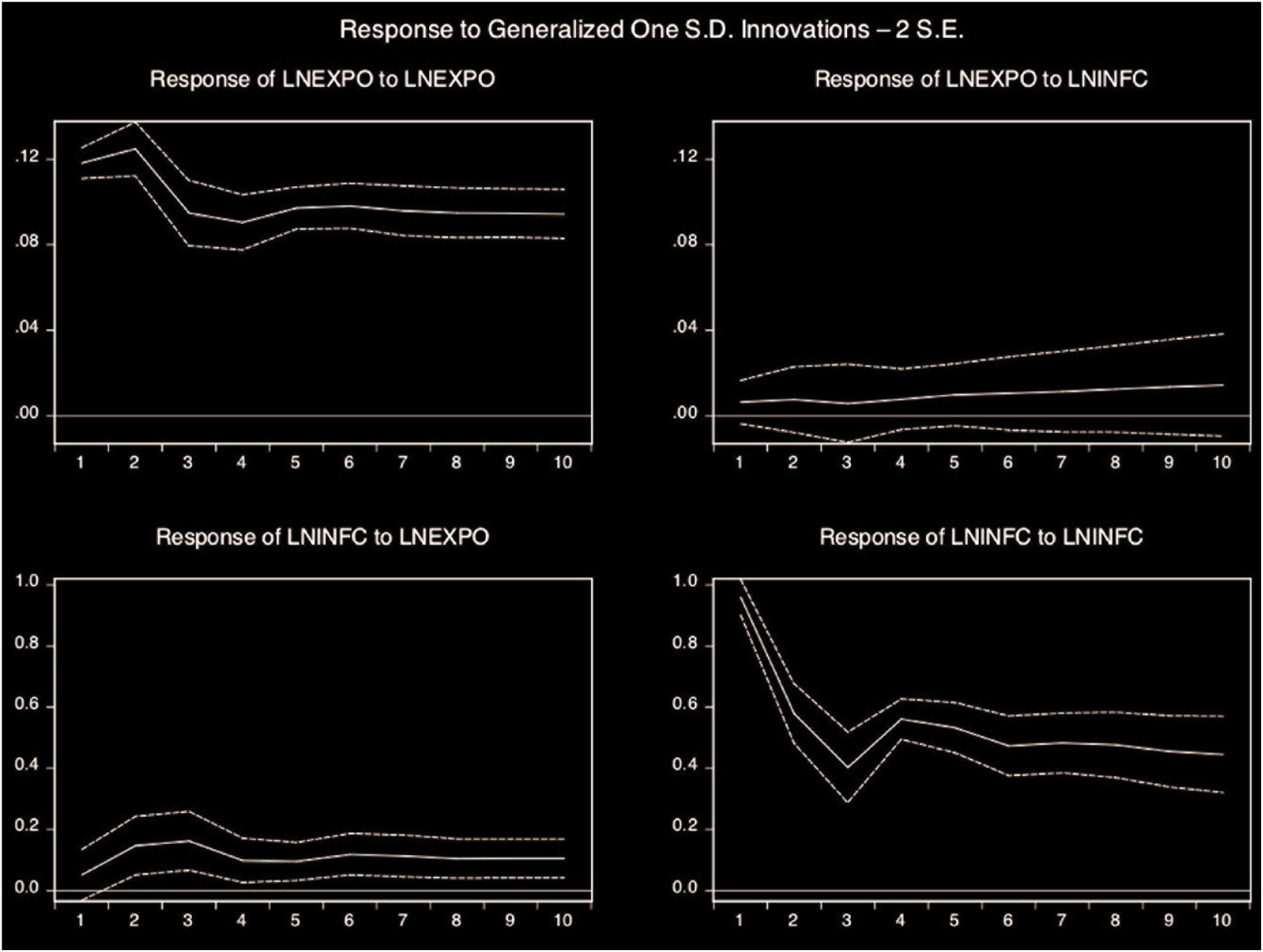

We checked the impulse response to see the impact on current and the future values of one variable caused by shocks in the other variable. The impulse response is performed only for the relationships between variables, where the causal flow is observed, as such relationship between LNINFC and LNIMPO was excluded. It can be observed from Figure 1 that LNINFC responses positively to shocks in LNINTD, thereby an increase in LNINTD in the current period will have a positive effect on LNINFC in the future. On the other hand, LNINTD also responses positively to shocks in LNINFC, but the response is rather weak. Similar observations can be seen from the relationship between LNINFC and LNEXPO, where LNINFC responds positively to shocks in the LNEXPO (Figure 2).

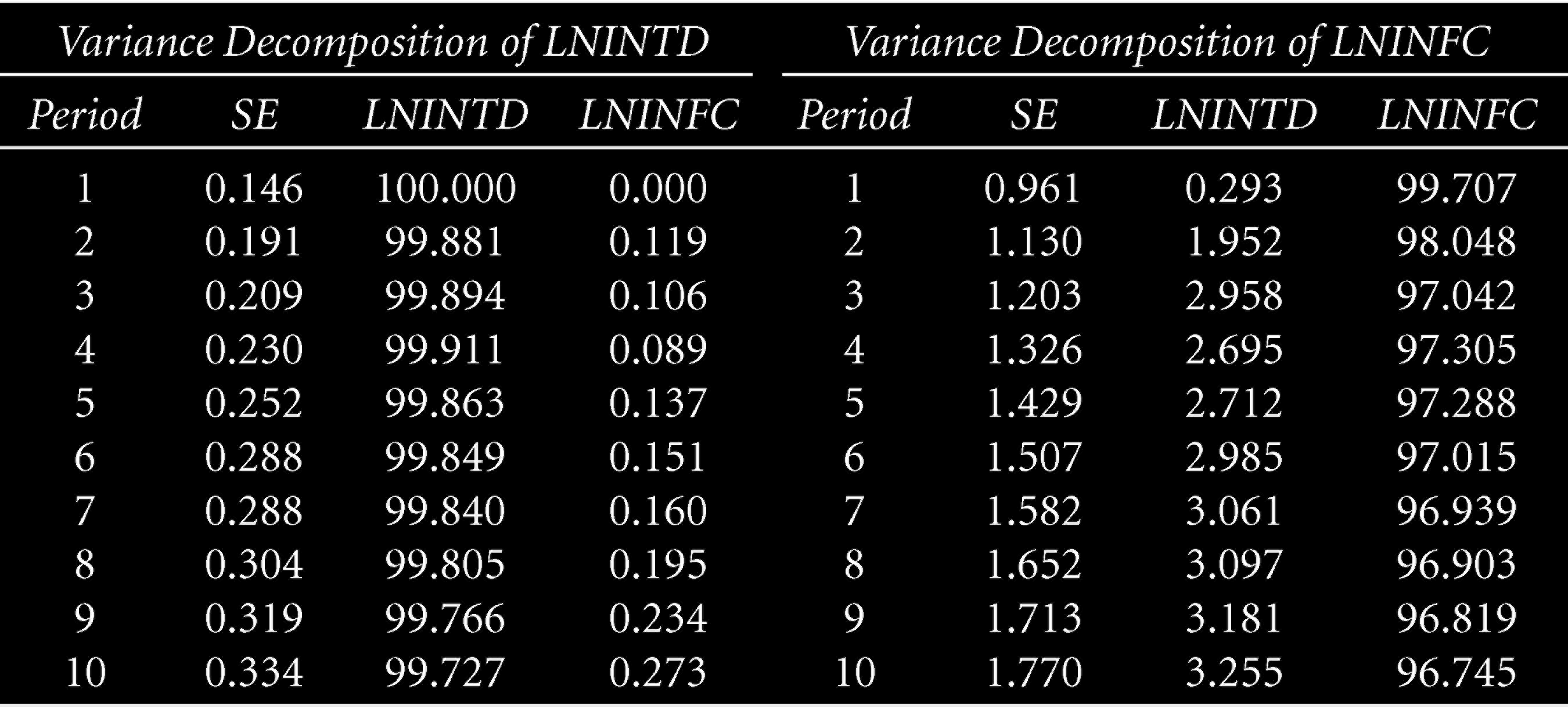

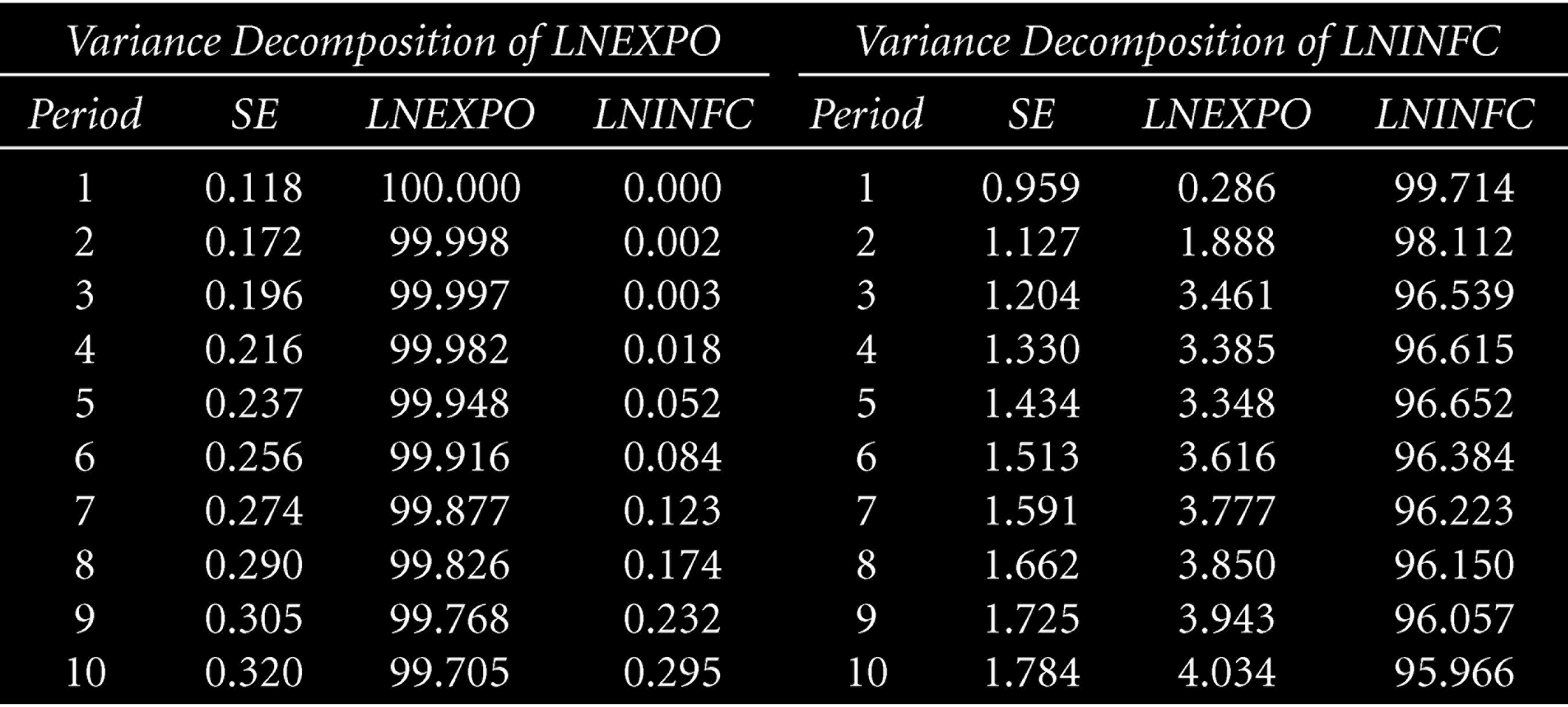

Variance decomposition was performed to check the proportion of movement of variables to its own shock compared to shocks from other variables in a sequence. We observed a greater influence of international trade on international factoring in the long run compared to the influence of international factoring on international trade. Fluctuations in international trade can explain the volatility of international factoring from 0 per cent to 3.26 per cent. On the other hand, changes in international trade due to international factoring is much lower—only 0–0.27 per cent of the volatility in international trade can be explained by fluctuations in international factoring (Table 5). Further, Table 6 shows that the influence of exports on international trade is substantial, particularly in the long run. The 0–4.03 per cent volatility in international factoring can be explained by fluctuations in exports. In contrast, only 0–0.3 per cent of the volatility in exports can be explained by fluctuations in international factoring.

Variance Decomposition Analysis Between LNINFC and LNINTD

Variance Decomposition Analysis Between LNINFC and LNINTD

Variance Decomposition Analysis Between LNINFC and LNEXPO

Trade finance is crucial for the operation and growth of international trade. It plays a key role in providing the necessary fluidity and security to the movement of goods and services worldwide. It can influence the prices, quantities and patterns of cross-border trade. Credit constraints can significantly affect trade between countries, as witnessed after the financial crisis of 2008–2009.

We examined the relationship between international factoring and international trade using panel data. The Granger Causality test showed a unidirectional causality flow from international trade to international factoring. Similar results are obtained for the relationships between international factoring and exports, but we found no causal relationship between international factoring and imports, possibly because factoring is supplier-led financing and is utilised more in exports by exporters. The impulse response analyses showed that international factoring responds positively to shocks in overall cross-border trade as well as in export value.

Further, the variance decomposition analyses revealed that 0–3.26 per cent of the volatility in international factoring could be explained by fluctuations in overall international trade. In comparison, fluctuations in exports explain about 0–4.03 per cent of the volatility in international factoring. Most papers on trade finance have examined its influence on cross-border trade, while the reverse influence has not been thoroughly examined. However, some studies on the influence of trade on financial development confirmed that trade influences financial development (e.g., Huang & Temple, 2005, p. 21; Yucel, 2009, pp. 38–39), and our study confirms the findings of those studies.

Several policy implications emerge from this study. As growth in international trade, particularly exports, create demand and the need for international factoring, the policymakers should create a conducive ecosystem for the facilitation of international trade through factoring. Offering competitive payment terms for increasing sales in foreign markets, accelerating cash flows, providing liquidity and protection against bad debts, improving operational process flows, and transacting in a secure environment are some policy intervention areas. Initiatives to boost export capability, depending on the comparative advantage of the country, need appropriate execution. Some measures may include offering reliable and reasonable infrastructure in terms of transport, power, telecommunications and so on; a sound institutional environment in terms of legal and judiciary systems, taxation, custom procedures and so on; setting up of trade support institutions and export promotion agencies for offering services such as trade information, marketing, export support services (technical assistance, training, capacity building, etc.); among others. A lack of uniformity of laws acts as a major barrier in the assignment of receivables. As such, policymakers should take measures to implement international conventions such as the UNCITRAL Convention to reduce or eliminate divergence in laws and regulations on the assignment of receivables between the countries. Generally, factors would prefer to purchase receivables on a recourse basis when there is difficulty in assessing the credit quality or the quality of receivables is poor, whereas suppliers would prefer to avail factoring on without recourse basis. These differences in preferences can inhibit the implementation of international factoring. Against such a scenario, governments or policymakers can help in improving the use of international factoring by offering support such as credit guarantee for export financing via factoring. Such credit guarantees can encourage both the suppliers and factors to implement international factoring.

It is expected that the findings of this study may not apply to all countries. The causal relationship between international factoring and trade may vary between countries. However, due to limitations in the data, we could not examine the causal relationship at the country level, and it will be worth exploring using country-level data in the future. More studies on the influence of cross-border trade on trade finance in general and factoring in particular need to be explored.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

LM Test for Serial Correlation Between LNINFC and LNIMPO (Increasing by Lag 1)

| Lag | LRE* Stat | Rao F-stat |

| 1 | 43.802*** | 11.169*** |

| 2 | 5.024 | 1.258 |

| 3 | 28.784*** | 7.288*** |

| 4 | 5.019 | 1.257 |

*** signifies significance at 1% level.