Abstract

The main goal of this study is to examine the effect of real effective exchange rate uncertainty on domestic investment for the South African economy over the sample period 1985Q1–2019Q2. To address this objective, Jordà’s (2005) local projection method is employed in this study. The generalised impulse response functions indicate that domestic investment decreases between the second and seventh quarters in response to one standard deviation shock in exchange rate uncertainty. Furthermore, high exchange rate uncertainty affects domestic investment negatively while low exchange rate uncertainty affects domestic investment positively. In other words, domestic investment declines due to a rise in exchange rate uncertainty while a drop in exchange rate uncertainty enhances domestic investment. Regarding the effects of control variables, output and export influences domestic investment positively and significantly. Inflation, however, has a negative and significant effect on domestic investment. Lastly, the Diks–Panchenko nonlinear Granger’s causality confirms bidirectional causality between exchange rate uncertainty and domestic investment.

Keywords

Introduction

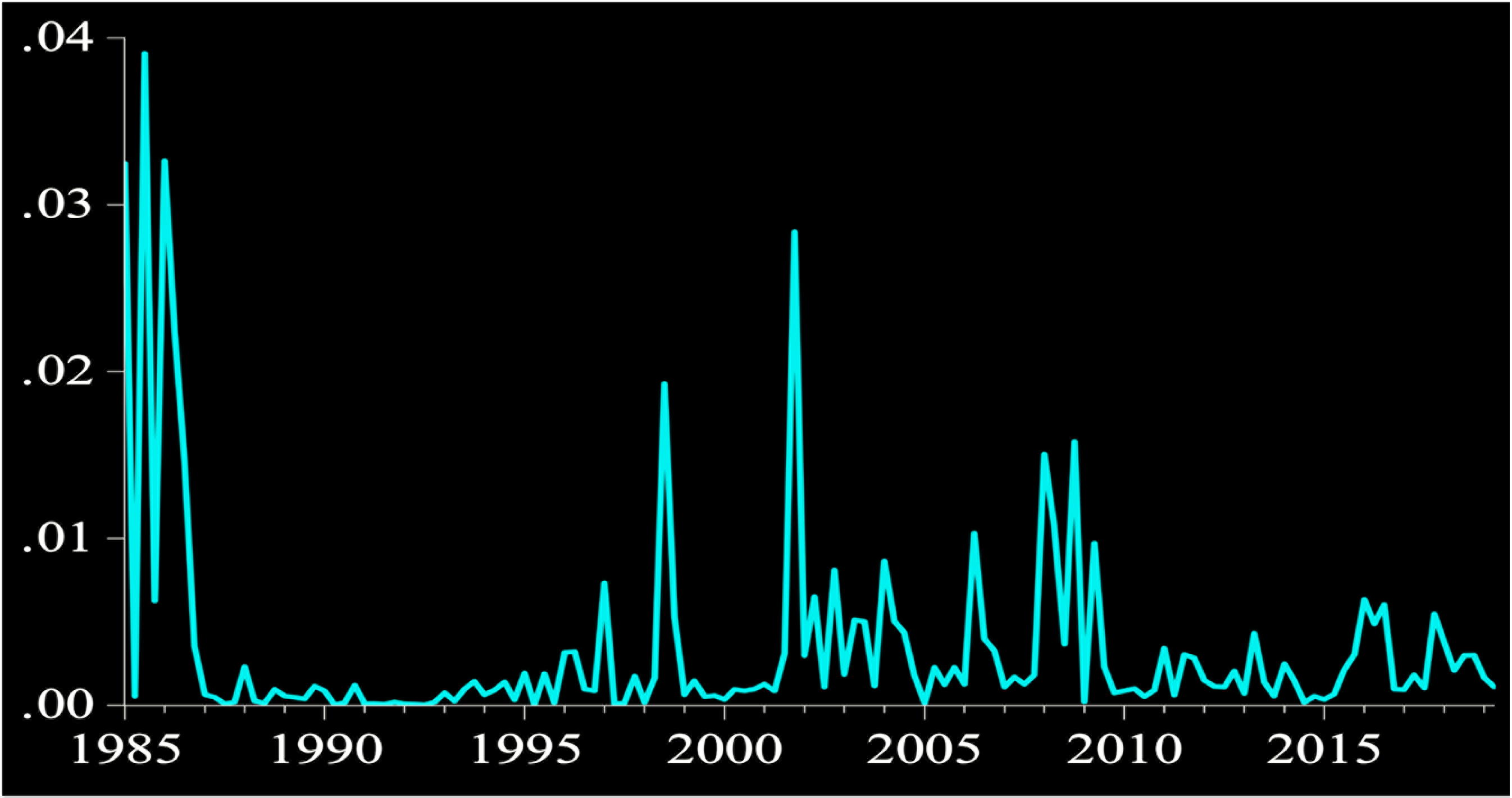

One of the major policy changes made by several countries globally was the abandonment of fixed exchange rates in favour of floating exchange rate systems mainly after the end of the gold standard system in 1971. Since then, exchange rate uncertainty has had alarming economic consequences (Ozcelebi, 2018). The exchange rate regime in South Africa has undergone various amendments over the past 30 years. Before 1970, under the Bretton Woods system, the exchange rate of the South African rand was fixed to the sterling, and this was followed by a managed float from 1970 to 2000 (Aye & Harris, 2019). Under the South African Reserve Bank’s (SARB) current inflation targeting monetary policy framework, the rand has been a free-floating currency since 2001, with its value determined by market demand and supply for the currency against foreign currencies traded for it. Such a policy has resulted in making the rand volatile and uncertain currency, given the high levels of participation by foreigners in the local markets (Khomo, 2018). South Africa’s real effective exchange rate has hence undergone considerable variations over the past few decades covering cycles of appreciation and subsequent declines (Figure 1).

Exchange rate uncertainty and its effect on economic variables such as trade, investment, inflation, employment and economic growth have become an alarming issue in South Africa (Khomo, 2018). However, investment has played a significant role in the growth of the South African economy, and since 2016, investment in South Africa has recovered from its 4.1 per cent contraction.

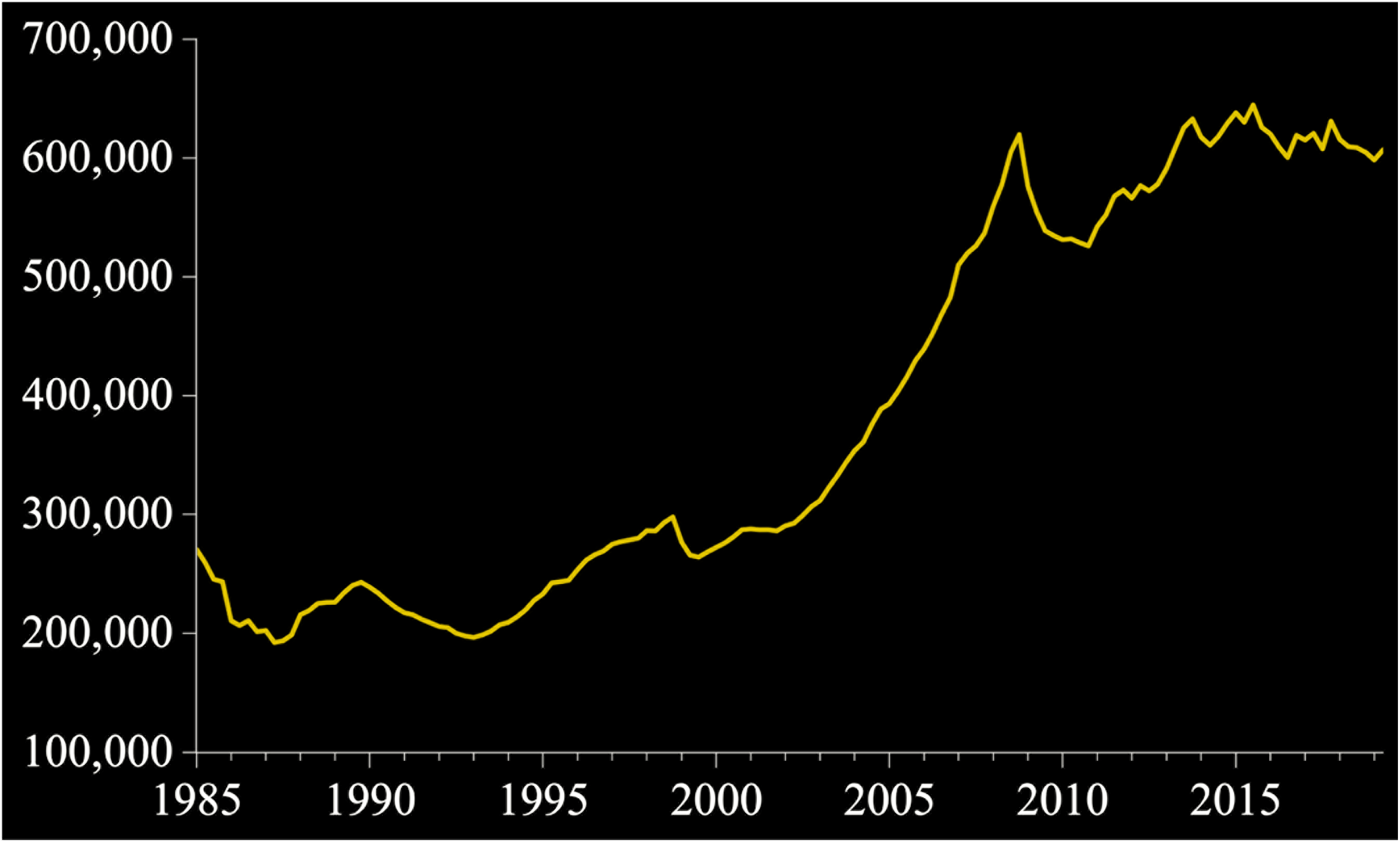

Figure 2 displays domestic investment in millions of national currency in South Africa from 1985-2019. Overall, domestic investment improves over time in South Africa, especially between 2002-2007 before it declines in 2008 and recovers again after 2010.

A number of theoretical and empirical studies have been conducted to explore the effect of exchange rate uncertainty on import and export sectors. However, recently several academicians have conducted empirical work on exchange rate uncertainty effects on investment, both domestic and foreign direct investment. The theoretical linkage between exchange rate uncertainty and investment includes both direct and inverse relationships. Studies by Hartman (1972) and Abel (1983) argue that competitive risk-neutral firms invest more in order to avoid uncertainty in the future; hence, high exchange rate uncertainty leads to higher levels of investment. In contrast, Pindyck (1991) states that investment is irreversible, and increased uncertainty slows down the investment process in risk-neutral firms. Additionally, Dixit and Pindyck (1994) claim that investment can be postponed and investment projects may not be executed due to exchange rate uncertainty, and this may lower investment.

There are also several empirical studies revealing both positive and negative effects of exchange rate uncertainty on investment. Iyke and Sin-Yu (2017) and Canbaloglu and Gurgun (2018), for example, find that exchange rate uncertainty has a positive impact on domestic investment; Safdari and Soleymani (2011), Serven (2002) and Diallo (2015) in contrast find that real effective exchange rate uncertainty has a strong negative impact on investment.

The only available empirical study for South Africa is by Maepa (2016), which showed the effect of exchange rate uncertainty on different types of investment using a multivariate Johansen cointegration approach. The results exhibit a negative long-run relationship between exchange rate uncertainty and private domestic investment. The study also finds a weak and negative long-run effect of exchange rate uncertainty on foreign direct investment and portfolio investments in South Africa. Our research extends the existing limited empirical literature on the nexus between exchange rate uncertainty and investment by incorporating mainly non-linearity into the model.

The article is structured as follows. The literature review is presented in Section 2. The data type and sources are presented in Section 3. Section 4 discusses the econometric strategy. Results are presented and discussed in Section 5. In Sections 6 and 7, robustness checks and conclusions are presented, respectively.

Theoretical Framework

Theoretically, the linkage between the fluctuations in exchange rate and investment consists of both direct and opposite effects. Most theoretical studies argue that exchange rate uncertainty results in a positive or negative effect on domestic investment after it causes price uncertainty. On the one hand, studies by Hartman (1972) and Abel (1983) claimed that competitive risk neutral firms invest more in order to avoid uncertainty in the future; hence, high price uncertainty leads to higher levels of investment. In contrast, Pindyck (1991) stated that investment is irreversible and increased uncertainty slows down the investment process by risk-neutral firms.

Dixit and Pindyck (1994), based on their theory of optimal inertia, come up with another important aspect—that investments can be postponed. Information about the future can bring favourable or unfavourable scripts. In both cases, an optimum decision could be to postpone the investment project. In the case of a favourable script, the postponement avoids the low revenue operation period and investment under an uncertain environment. In the adverse script, the waiting period can have a long duration and the investment project may not be executed and lowers investment. Darby et al. (1999) later developed a theoretical model based on Dixit and Pindyck (1994). Their model tried to solve some related dilemmas of investment execution states. First, it introduced the threshold at which exchange rate uncertainty could have adverse effects on investment. Second, the model pinpointed real situations in which investment is actually killed by uncertainty. It also clearly identified conditions under which exchange rate uncertainty could have negative or positive effects on domestic investment. The condition is basically reduced to opportunity cost of postponing against the present value. If the opportunity cost of postponing is lower than the present value or the scrapping price by firms, producers will be eager to postpone rather than to invest. On the other hand, the postponing effect may disappear if uncertainty is rather low.

Another theoretical approach that explains the interaction between the exchange rate and investment is the modern portfolio theory that emphasises on how exchange rates are determined in cases where financial assets other than money are available. According to the portfolio balance approach, exchange rates, that is the opportunity cost of holding money, is the direct output lost from holding other imperfect domestic and foreign financial substitute assets. Accordingly, other variables remaining constant, a decrease in the supply of domestic money increases the domestic interest rate, which in turn increases the demand for holding domestic assets, and decreases holdings of foreign assets (Van der Merwe & Mollentze, 2012).

The other approach called the monetary approach explains the link between the exchange rate and investment, arguing that the exchange rate is determined by the demand and supply of money between two countries; and that domestic and foreign bonds are perfectly substitutable to each other (Husted & Melvin, 2007). Furthermore, the theory assumes that there is a positive and stable long-run relationship between the demand for money and level of national income.

Empirical Review

A number of empirical results are found for the effect of exchange uncertainty on investment revealing both positive and negative linkages. Some empirical studies showed a positive relationship between exchange rate uncertainty and investment in general and domestic investments in particular, while others disproved this result and indicated a negative linkage.

Iyke and Sin-Yu (2017), for instance, using annual data for Ghana covering the period 1980–2015 found that in the short run the current level of uncertainty enhances investment while lagged levels of uncertainty dampen investment. In the long run, however, exchange rate uncertainty has a positive impact on domestic investment. Canbaloglu and Gurgun (2018) examined the effect of exchange rate uncertainty on domestic investment for 25 emerging markets and developing economies and the effect was found to be positive and significant.

On the other side, Diallo (2015) assessed the link between real exchange rate uncertainty and domestic investment by using panel data cointegration techniques for 51 developing countries (23 low-income and 28 middle-income countries) and illustrated that real effective exchange rate uncertainty has a strong negative impact on investment. Safdari and Soleymani (2011) also analysed the relationship between uncertainty of exchange rate and domestic investment using panel data for six countries and the generalised autoregressive conditional heteroskedasticity (GARCH) (1,1) approach, and obtained a negative relation between uncertainty of exchange rate and domestic investment. Serven (2002), using large cross-country time-series data and the GARCH-based measure of real exchange uncertainty, showed a negative and highly significant effect of real exchange rate uncertainty on private investment.

Bahmani-Oskooee and Hajilee (2013) assessed the short-run and long-run effects of exchange rate uncertainty on domestic investment in 36 countries using the bounds test approach; the results indicated that exchange rate uncertainty has a significant short-run effect on domestic investment in 27 countries. De Oliveira (2014) compared the relationship between different exchange rate regimes and investment scenarios and showed that a crawling peg exchange rate regime has advantages over the other regimes. The regime stability implies that fewer currency fluctuations are necessary to stimulate investment.

Maepa (2016) examined the effect of exchange uncertainty on different types of investment in South Africa from 1970 to 2014 using a multivariate Johansen cointegration approach. The study revealed a negative long-run relationship between exchange rate uncertainty and private domestic investment. It also documented a weak and negative long-run relationship effect of exchange rate uncertainty on foreign direct investment and portfolio investments in South Africa. However, the short-run interaction was found to be small and not significant enough to cause disruptions to the exchange rate and to the inflow of investments into the country.

Data Type and Source

We use quarterly data that extends from the period 1985Q1 to 2019Q2. This period incorporates important events in the history of South Africa. The beginning year of our sample marks the formal ending of the fixed exchange rate regime, after which the South African economy became highly liberalised following the De Kock Commission in 1985, and the post-democratisation period, when economic sanctions were lifted and South Africa began to interact with the global economy.

The variables of interest in our estimated model are domestic investment as the dependent variable and real effective exchange rate uncertainty as the main independent variable. Following Aye and Harris (2019), the quarterly data real effective exchange uncertainty is captured in

Where rt is the monthly return (natural logarithm of the first difference, i.e., lnrt – lnrt–1) for month i within quarter t, and i = 1…T where T is the total number of monthly observations within a quarter. Other control variables such as real gross domestic product (RGDP), exports and inflation (the first difference of the consumer price index in our case) are included in the study. The data are obtained from SARB and International Monetary Fund.

To examine the effect of real effective exchange rate uncertainty on domestic investment in South Africa, Jordà’s (2005) local projection (LP) method is used. The LP method requires running a sequence of predictive regressions of a variable of interest on a structural shock for different prediction horizons. The impulse response is then obtained from the sequence of regression coefficients of the structural shock (Aye & Harris, 2019). The method can produce the response of domestic investment to real effective exchange rate uncertainty at different horizons. As clearly explained in Auerbach and Gorodnichenko (2013), Ramey and Zubairy (2018) and Aye and Harris (2019), this method has some advantages compared to vector autoregressive impulse responses. First, the estimation relies on robust standard errors and is simple to implement. Second, it is robust to misspecification of the data generating process. Third, joint or point-wise analytic inference is simple. Fourth, it can more easily accommodate non-linearities. Last but not least, impulse responses from LP are consistent and asymptotically normal.

According to Hamilton (1994) and Koop et al. (1996), impulse responses function, the difference between two forecasts, is a drive in a dynamic system used to scale the impact of shocks on expected or future value of economic variables at a time horizon. According to Koop et al. (1996), the generalised impulse response function of yt at horizon h is defined as follows:

Where, δ is an n × 1 vector representing shocks, 0 is an n × 1 veector matrix of zeros, vt is an n × 1 veector of additive random shocks, Ωt–1 is the information block of value of the variables up to t – 1 and E (.|.) is a mean predictor. Jordà (2005) proposed to recover the multiplier from the set of regression coefficients

Domestic investment, the endogenous variable interest, is represented by yt; xt is the shocks from exchange rate uncertainty, with mean zero and variance

Beyond the estimated model in Equation (3), the specification of the asymmetric effect model to estimate the asymmetric response of domestic investment to exchange rate uncertainty is handled. Two dummy variables are incorporated in the model to capture the asymmetric effects of both higher and lower exchange rate uncertainty. High uncertainty is calculated by multiplying aggregate exchange rate uncertainty with the first dummy variable, which takes the value of one if uncertainty is above the mean, and zero otherwise; and low uncertainty by multiplying aggregate exchange rate uncertainty with the second dummy variable, which takes the value of one if uncertainty is below the mean, and zero otherwise.

xt, the exchange rate uncertainty now is either to be high or low. The higher exchange rate uncertainty that includes the values of exchange rates one if uncertainty is above the sample mean and zero otherwise is indicated by

Finally, a nonlinear causality test—the Diks and Panchenko (2006) nonlinear Granger’s causality—is also used to check the causal relationship between exchange rate uncertainty and domestic investment over the sample period for the South African economy.

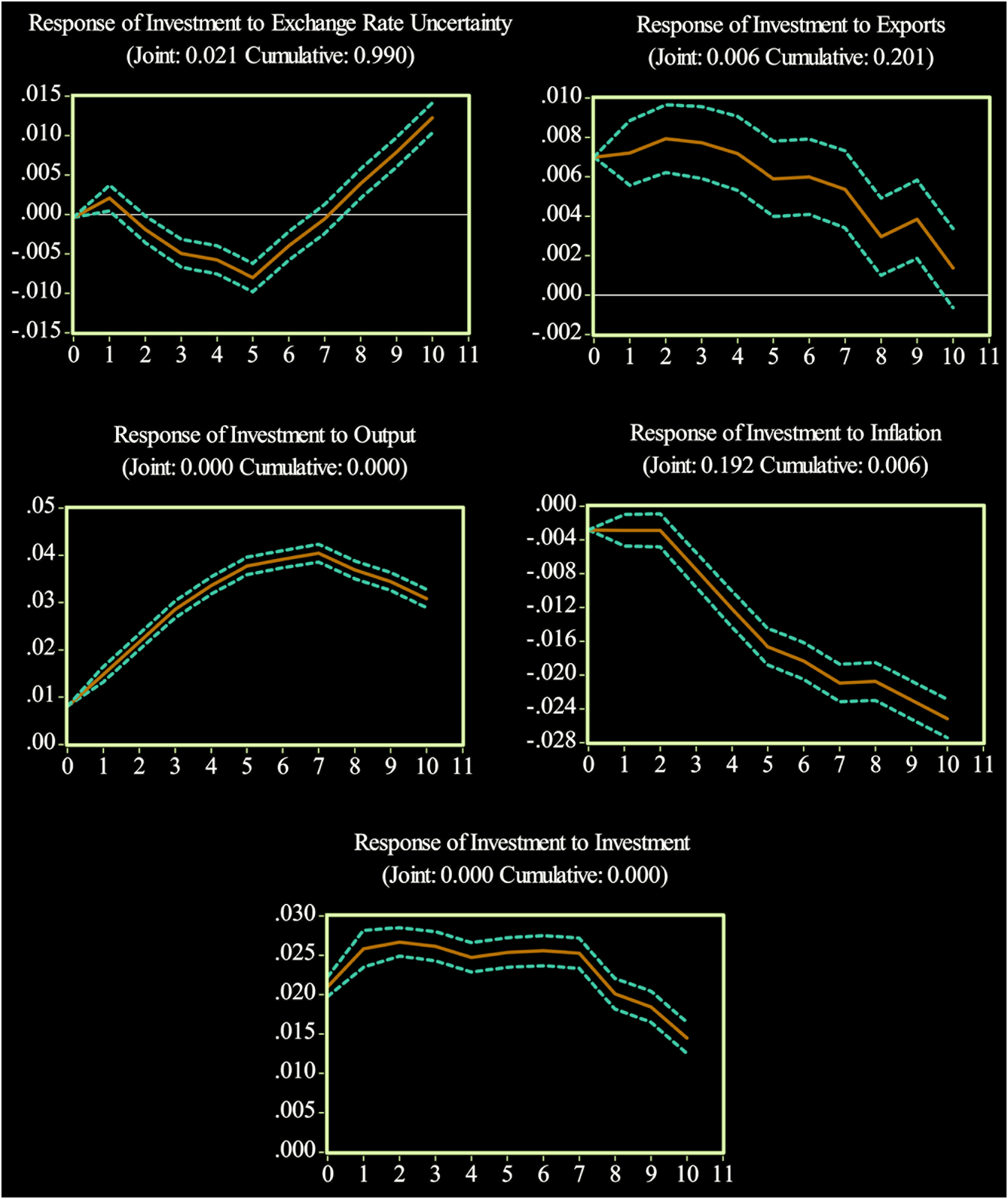

The generalised impulse response functions over 10 horizons for the symmetric and asymmetric effects of exchange rate uncertainty on domestic investment are provided in Figures 3 and 4, respectively. To begin with, our main variable of interest, Figure 3 reveals that exchange rate uncertainty has a negative significant effect on domestic investment from the second quarter to the seventh quarter. Domestic investment declines by about 0.8 per cent in the fifth quarter in response to a one standard deviation shock in exchange rate uncertainty. This result is consistent with the theory by Pindyck (1991) who argued that investment is irreversible and increased uncertainty slows down the investment process by risk-neutral firms; and with the empirical findings of Safdari and Soleymani (2011), Serven (2002) and Diallo (2015) who obtained a negative relation between uncertainty of the exchange rate and domestic investment. This is because when investors are uncertain about the future movements in an exchange rate, they are more likely to move their investments to a period they perceive to have more a stable and healthy investment environment or to completely change their minds and not invest at all.

As the South African exchange rate is a floating exchange rate, the flexibility gives producers the option to adjust international production patterns to the realisation of shocks, at the cost of carrying the extra productive capacity. Hence, a less volatile exchange rate is more conducive for the enhancement of domestic investment relative to a volatile exchange rate. This conclusion applies for both real and nominal shocks. This is because less volatile (or more or less certain) exchange rates are capable of better isolating real wages and production from monetary shocks, and thus are associated with higher expected profits. The higher expected income, in turn, supports higher domestic investment (Aizenman, 1992).

Dixit and Pindyck (1994) also argued that volatility affects the costs of investment indirectly as it influences international trade in goods, their prices and flows of assets. Since uncertainty in exchange rates brings risk for both exporters and importers, it leads to higher cost of production and nominal wage rate. These factors in return lead to lower investment.

Domestic investment, however, increases in response to a one-standard deviation shock in exports up to the 10th quarter considered in our study. Domestic investment also positively responds to output shock. A one-standard deviation shock in RGDP invokes a significant expansion in domestic investment across the entire time horizon considered. The joint and cumulative responses of domestic investment to RGDP shock are statistically significant. A one-standard deviation shock in inflation results in a fall in domestic investment in the deliberated horizon. Lastly, investment shock is persistent.

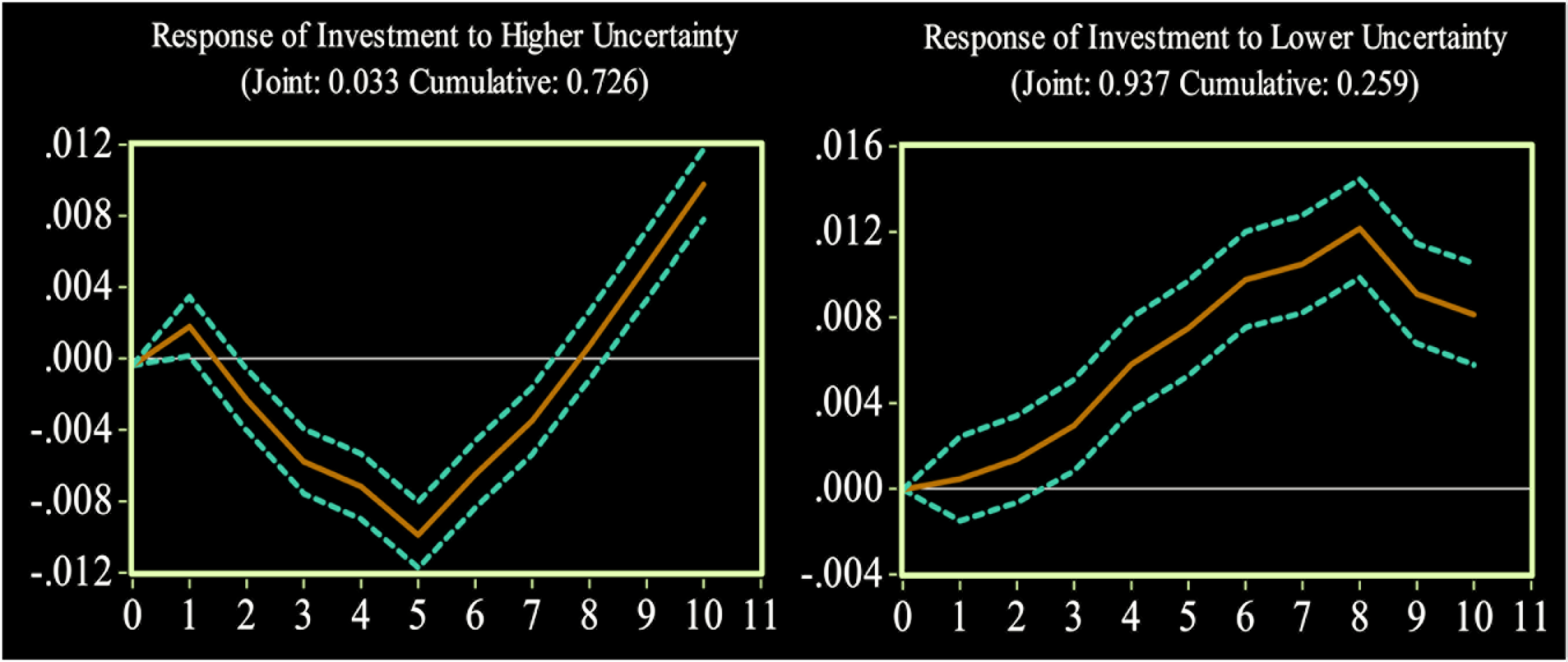

Figure 4 shows that domestic investment significantly declines as a result of high exchange rate uncertainty from the second quarter to the seventh quarter, before it increases continuously for the remaining quarters. This means that domestic investment significantly falls in response to a rise in exchange rate uncertainty. Regarding the response of domestic investment to low exchange rate uncertainty, domestic investment increases across the entire time horizon considered, though a significant enhancement begins from the third quarter onwards. In other words, a fall in exchange rate uncertainty yields a significant boost in domestic investment. This signifies that there is an asymmetric effect of exchange rate uncertainty on domestic investment for the South African economy. It is important to note that for brevity, responses to the other control variables are omitted, since they are exact replications of those in Figure 3.

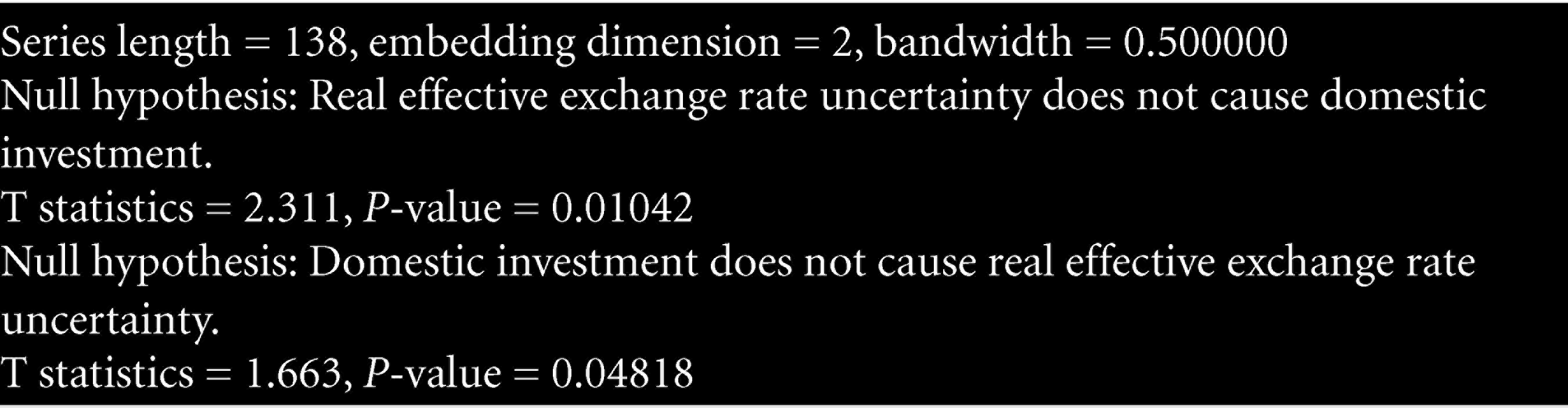

A nonlinear Granger causality test using Diks and Panchenko (2006) nonlinear Granger’s Causality is also conducted to see if there is a nonlinear Granger causal relationship between exchange rate uncertainty and domestic investment. The outcome of the test is given in Table 1.

Diks–Panchenko Nonlinear Granger Causality

The P-values of the hypotheses are found to be less than 5 per cent confidence coefficient, which enables us to reject the null hypotheses and we conclude that there is nonlinear Granger causality between exchange rate uncertainty and domestic investment. Hence, exchange rate uncertainty nonlinearly Granger causes domestic investment and domestic investment also nonlinearly Granger causes exchange rate uncertainty. This result indicates the presence of a bidirectional causal relationship between the two variables.

To see the relationships between exchange rate uncertainty and domestic investment in cyclical patterns levels, a band-pass filter of exchange rate uncertainty and domestic investment series is applied and the cyclical components are extracted. Figures 5 and 6 reveal the symmetric and asymmetric impulse responses of cyclical investment against the controlled variables and cyclical exchange rate uncertainty, respectively. Finally, the cyclical relationships between domestic investment and exchange rate uncertainty are compared with the normal relationships of the variables in Figures 3 and 4 as a robustness checks.

We find that the impulse responses are broadly the same with our baseline model results. We also observe that there is an abrupt movement in the exchange rate uncertainty and investment relationships in both the symmetric and asymmetric cases.

This study examines the symmetric and asymmetric effects of exchange rate uncertainty on South African domestic investment using Jordà’s (2005) LP method over a sample period, 1985Q1 up to 2019Q2. Following Koop et al. (1996), the generalised impulse response functions are generated to see the effects of the variables of interest on the dependent variable. The result of the symmetric model shows that exchange rate uncertainty affects domestic investment negatively and significantly between the second and seventh quarters. The effect of inflation shock on domestic investment is also negative and significant. Domestic investment, however, positively responds to export and output shocks.

From the asymmetric model, we observe that domestic investment falls with a rise in exchange rate uncertainty. Unlike high exchange rate uncertainty, low exchange rate uncertainty boosts domestic investment, that is, a fall in exchange rate uncertainty induces high domestic investment.

To conclude, uncertainty of the real effective exchange rate in South Africa, resulting from a free floating exchange rate policy, has both symmetric and asymmetric effects on domestic investment. In both cases, the more uncertain the exchanges rate the lower the level of domestic investment. This might be due to the risk-averse nature of domestic investors in South Africa, who postpone investment projects or completely stop investing under uncertain conditions. This is consistent with the theoretical argument of Dixit and Pindyck (1994) that investment can be postponed and investment projects may not be executed due to exchange rate uncertainty, and this may lower investment. Our findings imply that South Africa needs to boost investment to enhance economic growth and output. At the same time, there is a need to formulate and implement careful exchange rate policies so as to promote investment flows and output growth.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.