Abstract

Abstract

Socially responsible investing (SRI) is fast catching the imagination of the ever increasing social consciousness of the investor community. Emergence of SRI can be traced back to the 1970s to few socially conscious investors who wanted to invest in bonds other than war, arms and ammunition and alcohol. Traditionally, SRI has focused on the economic social and governance (ESG) areas. Dieckmann (2007) who authored; Microfinance an emerging investment opportunity as a part of the Deutsche Bank Research, indicates that the SRI sector is witnessing the emergence of novae entrants like the microfinance (MF). The report also states that MF is scanning the environment for new funding opportunities by securitising MF opportunities and moving to the extent of going public. The scenario suggests microfinance to be robust, low risk profiled and growing investment avenue, which is fast emerging in the field of SRI. The purpose of the present article is to explore into the different dimensions of this emerging phenomenon and understand the emerging opportunities for banks in creating value using the synergy of SRI and MF.

Keywords

Introduction

Growth in sustainable investing has prompted the business world to adopt a non-conventional approach to designing investment portfolios. It is no longer considered to be quixotic or overtly philanthropic act for people in business to invest in socially relevant areas and socially responsible products. The concept of socially responsible investing (SRI) is not new to the business world. Driven by ethical considerations avoidance of business areas such as alcohol, tobacco, arms and ammunition by certain enlightened business houses, though few and far between, has always existed. Lack of a popular social perception of the right and wrong business to be involved in may also have been a reason for majority of the entrepreneurs to disregard ‘value caring’ while making investment decisions and focusing primarily only on the profit potential as advocated by Friedman (1970). However, the change in the profile of investors in the area of SRI as well as the various products that were eligible to be considered as socially responsible is very conspicuous in recent years. Traditionally, SRI has focused on the economic social and governance (ESG) areas. The Deutsche Bank research on microfinance and socially responsible investing on SRI indicates that the SRI sector is witnessing the emergence of novae entrants such as microfinance (MF) Dieckmann (2007). The MF investors are in a transition process from a donor-driven NGO-dominated framework towards an increasing involvement of capital markets (Dieckmann, 2007). The report also states that MF is scanning the environment for new funding opportunities by securitising MF loan portfolios and some MF institutions have gone public (ibid.). This emerging trend indicates MF to be robust low-risk investment avenue, which is fast being included in the gamut of SRIs. The purpose of the present article is to explore into the different dimensions of this emerging phenomenon.

Objectives of the Study

The present study is an attempt to examine the emerging profile of MF as a socially responsible investment avenue. The study endeavours to trace the growth and development of the MF investments and to understand the merger of the two concepts of MF and SRI. It also aims to critique the emerging opportunity for MF as attractive SRI avenue for banking institutions (BI), which has only of late made attempts to understand the MF market. Drawing on the theoretical base of the social capital theory, my work seeks to forge a link between the MF and corporate financial institutions. An attempt has been made to develop a MF–BI value chain for sustainable and socially responsible business. The study relies on the secondary sources of data collected from publications of various national and international organisations.

Development of SRI Thought–A Review

From very humble beginnings in 1970s, today the MFIs have emerged as a major global force which according to the microfinance information exchange (MFI) lend to more than 57 million population worldwide (Rhyne, 2009). The concept of SRI emerged in 1970s in the USA when Reverend Luther E. Tyson along with two other investors was inspired by a lady parishioner who asked him for a mutual fund that does not invest in war. Finding there was none that did not, he with two more investors decided to float a mutual fund, which unwittingly triggered the movement for SRI (Galema, 2011). The movement within a decade spread to the UK (Nybom, 2012). Yet, the concept did not evolve in a similar strain across the globe. A review of literature throws up various nomenclatures like Green investment, ethical investment, sustainable investment, screened investment, ESG based investment, socially responsible investment, etc., (Norup & Gotleib, 2011; White, 1995; Cowton, 1998 as quoted in Bosh et al., 2008). The UN and forums like Social Investment Forum of the USA and Social investment organisation in Canada brought about some level of uniformity in its 2006 recommendations and these efforts gave a fillip to SRI in sustaining as a mainstream strategy on the major capital markets (Norup & Gotleib, 2011).

Initial attempts to define the SRI had led to pitting of SRI with Ethical Investing (EI). From among the authors who have contributed to differentiating the concepts of SRI and EI are Cowton and Sparkes (2004 as quoted in Norup & Gotleib, 2011) in their joint article consider the two terms interchangeable. Sparkes (2001) defines SRI as the less stringent concept that covers all those investments, which emphasise on ethical matters, but may not be defined as 100 per cent ethical—for example, because of an additional focus on profit-making (Norup & Gotleib, 2011).

Impact investing is all together a different proposition, which makes similar claims of responsible investing. But where responsible investing focuses on the ESG factors, impact investing supported by global impact investing network requires making investments in socially economically profitable areas (Lapenu & Brusky, 2010).

Kinder (2005) classified SRI into three categories based on the value function of SRI. They are value-based SRI, value-seeking SRI and value-enhancing SRI. Value-based SRI reflects the investor’s personal and ethical priorities while value-seeking SRI is practiced by those investors who seek to align investments with the socially accepted and norms and criteria but still aim to benefit in terms of financial returns. Value-enhancing SRI is made by those investors who align to their professional interests of financial gain with value generation and those who patently adhere to the norms of corporate governance (Kinder, 2005, as quoted in Norup & Gotleib, 2011).

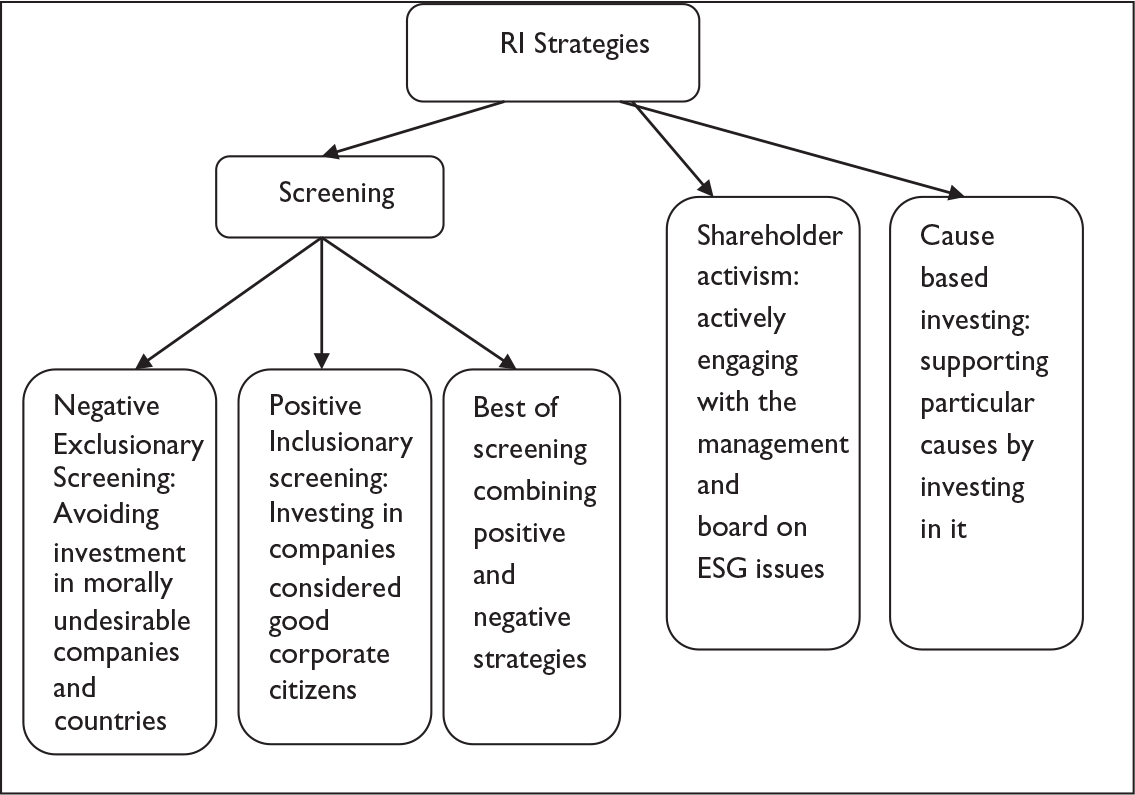

The emergence of socially responsible investments created a need for various agencies to assess these funds and to declare their social quotient. The Domini social index founded by Kinder Lyndengerg and Domini and company devised a capitalisation weighted index model to undertake the task (Statman, 2000). Some of the areas encompassed under sustainable investing are negative screening, positive screening, norm-based screening, integration of ESG, sustainability-themed investing, impact/community investing, corporate engagement and shareholder’ activism (Figure 1).

Region-wise Increase of the SRI Assets Worldwide

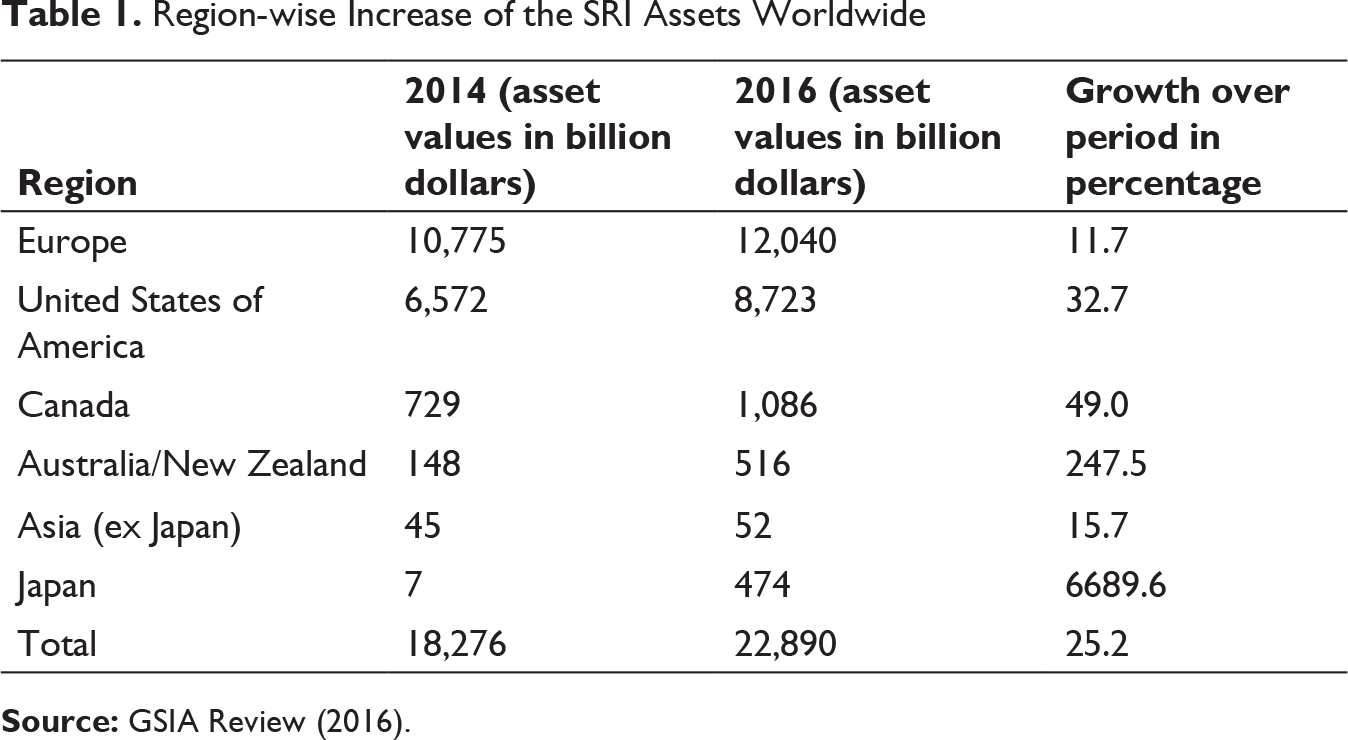

The GSIA Review (2016) states that negative screening is the most preferred, followed by ESG integration, corporate engagement and shareholder activism. A rich corpus of research suggests that ESG factor is being considered as a necessary element to be integrated into a company’s financial performance. One interesting example is the European ESG Analyzer developed by UBS Investment Research (Taiana, 2012). Sustainable investment therefore receives high patronage from value-driven business ventures. The SRI assets worldwide have grown by around 25 per cent from 2014 to 2016 indicating burgeoning of social orientation among business enterprises (Table 1). The GSIA Review (2016) provides a geographical region-wise and area-wise dispersion and investment patterns in SRI, wherein the negative exclusionary screening seems to be most-practised across various countries, followed by ESG integration. Corporate engagement and shareholder activism also seem to be emerging as an important factor being considered for SRM-based investment.

SRI and Social Capital Theory—Theoretical Framework

The role of the social capital theory cannot be gainsaid in the development of the thought of SRI. The philosophy of SRI can be traced back to the basic tenets of social capital, which place their faith in popular participation in any activity leading to maximum good to the society. Earliest references of social capital are traced back to Hanifan (1916) as quoted in Woolcock and Narayanan (2002), who made references to the tangible contributions made by basic social relations, which paved the way for ease of operations in numerous situations. Putnam (1993) was the first researcher to suggest the importance of the influence exerted by the social structures on the organisational dynamics. The concept was further refined encompassing social relations, social communications, conflicts and considerations. The World Bank calls family, community, ethnicity and gender as the primary associations of social capital (Rankin, 2002). The well-being and active involvement in these associations will necessarily impact an organisation for profit and its strategic business decisions as there is an undeniable ‘mutual embedding of economic and social life’ (Bourdieu, 1977).

Notwithstanding the word capital, social capital was treated as a non-economic entity impacting the mainstream policy and decision-making only minutely (Sabatini, 2005). Such conclusion may be highly intuitive as the word social denotes social relationships like friends and family structures and questions the impact of these structures on policy and decision-making (Woolcock & Narayan, 2000). The writings of Bourdieu’s and Coleman two of the very initial contributors to social capital theory made clear the technical dimensions of social capital to be a network of different types of multidimensional structures leading to creation of ‘aggregate of actual potential of resources’ resulting in recognition and mutual benefit (Hazelton & Kennan, 2000). A critical understanding of the definition entails that social capital is a complex network of personal and organisational structures in which social relationships are used for accruing benefits. The economic models of social capital are based on the premise that social support systems in the guise of social obligations, cooperative norms and social sanctions play a crucial role in the event of failure of market forces and governmental systems (Wallis, Killerby & Dollery, 2004). Essence of social capital theory and its inextricable association with MF lies in the simple argument that social networks hold the key for creation of associational life as support systems for organisations to undertake various initiatives or decisions (Rankin, 2002).

The internal heuristics of social capital have close linkages with socially responsible investment in letter and spirit. While the theory of social capital aims to use the synergy of social networks and social relations for the business success, socially responsible investment seeks to ensure positive and ethically motivated investment to benefit the general society. The success of MF systems stands as an abundant proof of a successful amalgam of the twin thoughts of social capital and SRI. The movement of MF paves the way for financial inclusion of the hitherto excluded groups by motivating them to undertake initiatives leading to financial independence and meaningful social participation.

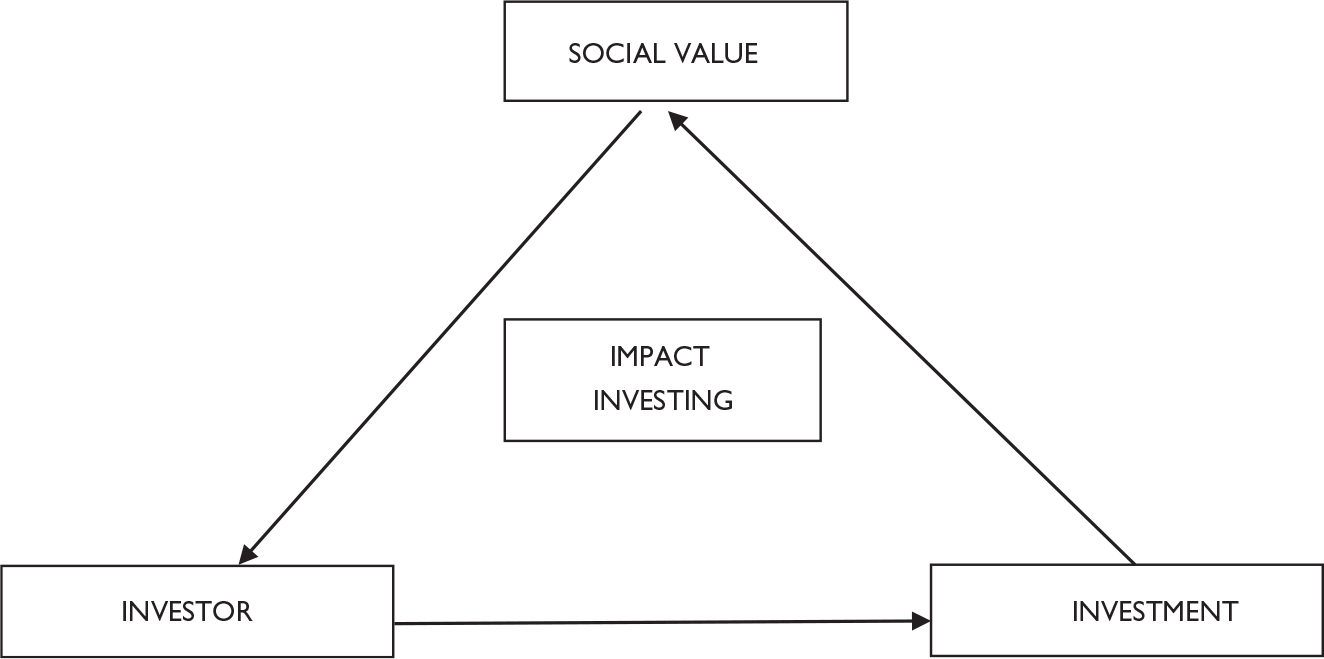

Impact investments that also considered as an important avenue of socially responsible investments are made by social investors, philanthropic individuals, financial institutions and individuals with high net worth in products that have a social or environmental impact beyond financial return and thereby contribute to the society (Oʼdonohoe, et al., 2010). Brest and Born (2013) have formulated three specific impact investment parameters, namely, enterprise impact, investment impact and non-monetary impact. These three impacts focus on the investor, investment and social value as a tri-dimensional entity (Figure 2).

The term impact investing was first used by the Rockfeller foundation in 2009 in their signal report titled ‘Impact Investing—An Emerging Asset Class’, indicating the desire of the investor to gain a result beyond the financial returns for their investment (Phillips, 2016). Marco (2011) had provided an inventory of activities related to impact investing undertaken in different countries. These activities included providing courses for employability, selling of reusable cloth, embarking on need-based product development like low-cost incubators etc., which can be treated as areas of impact investing. The role of social consciousness in the investment decisions has thus always been a moot point with certain segments of society and is expanding in its scope and dimension due to mounting social awareness among consumers and investors alike.

The Microfinance Scenario: Understanding the Bottom of the Pyramid (BOP) Market

Muhammad Yunus flagged off the movement of MF in Bangladesh in the 1970s leading to a revolution in the lending practices. The banking system till then was familiar only with lending for small holdings and agricultural purposes. In a major break with tradition, the MFI introduced the process of lending for non-agricultural activities (Galema, 2001). The MF may be called an umbrella term for the types of investments that are not covered by mainstream financial providers (Dieckmann, 2007). The original philosophy behind MF was to save the small time business people from loan sharks and high interest rates and often offering loans without the traditional requirement of collateral (Brau & Woller, 2004). The traditional collateral is substituted by the control exerted by the social groups and by the need to maintain their social standing in the community and being recognised as a prompt payer (Woolcock, 2010). These loans are more of group loans rather than the individual loans (ibid.). Traditionally, these investments are earmarked for small time business in the informal sector with the goal of economic empowerment through financial inclusion. In addition to their original lending practices, the MFIs are offering additional products, such as savings, consumption or emergency loans, insurance and business education (Brau & Woller, 2004). The MFI today is accepted as a unique product on the investment portfolio, which serves to assuage the social and ethical sensibilities of investors. The MF also projects a strong belief and trust in the ‘Bottom of the Pyramid’ (BOP) market in its ability to involve in economic revival and repayment ability. Delfiner and Peron (2007) have classified the target group of MF as poor who are not in a position to involve in any economic activity to economically active poor, who have the potential to involve in micro-business to low- and middle-income consumers. This classification allows the microfinance investment vehicles (MIV) to design appropriate financial assistance programmes to suit the target group. The products being offered therefore extend to a range of loans that aim to empower the BOP segment and eradicate poverty.

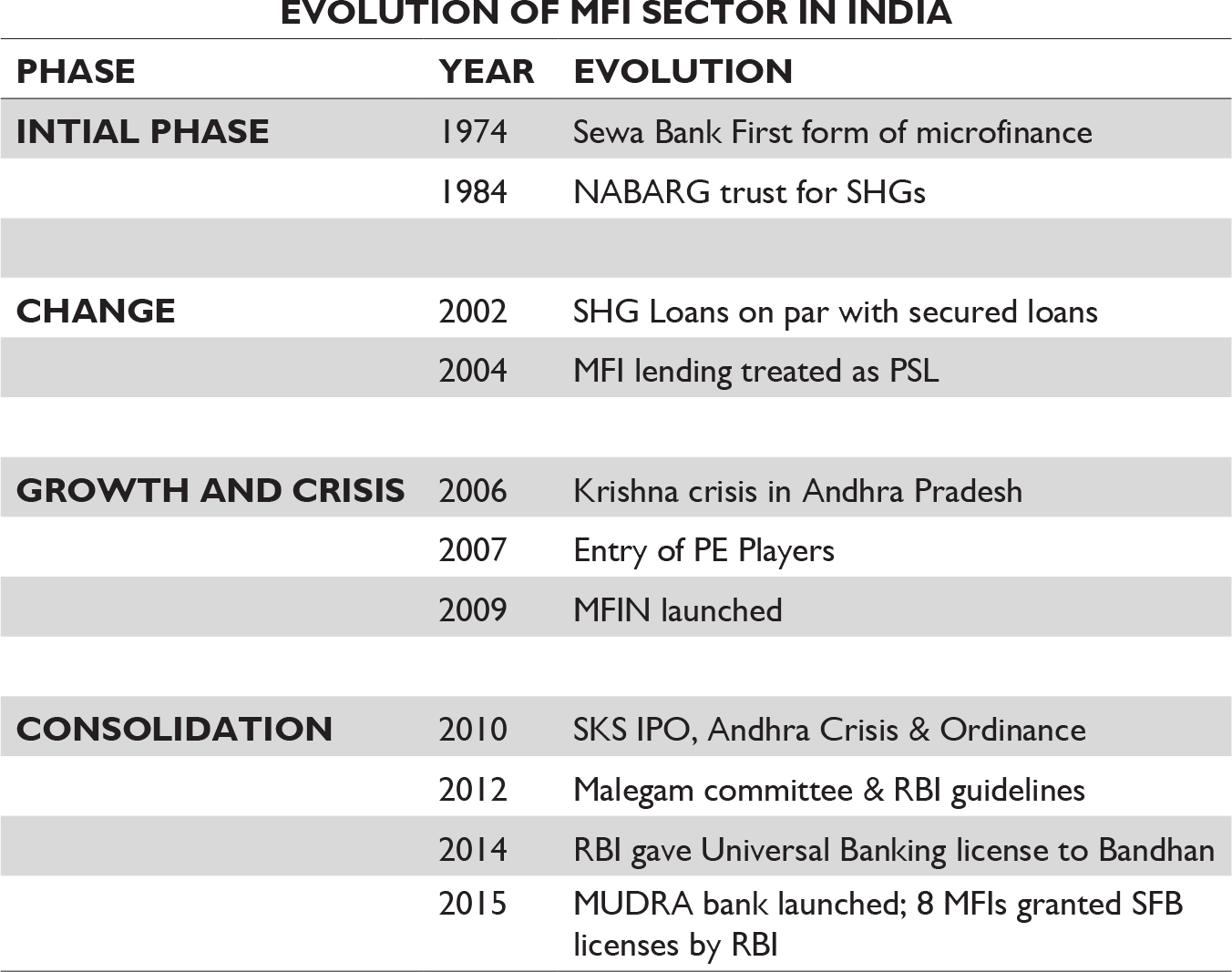

Microfinance in India

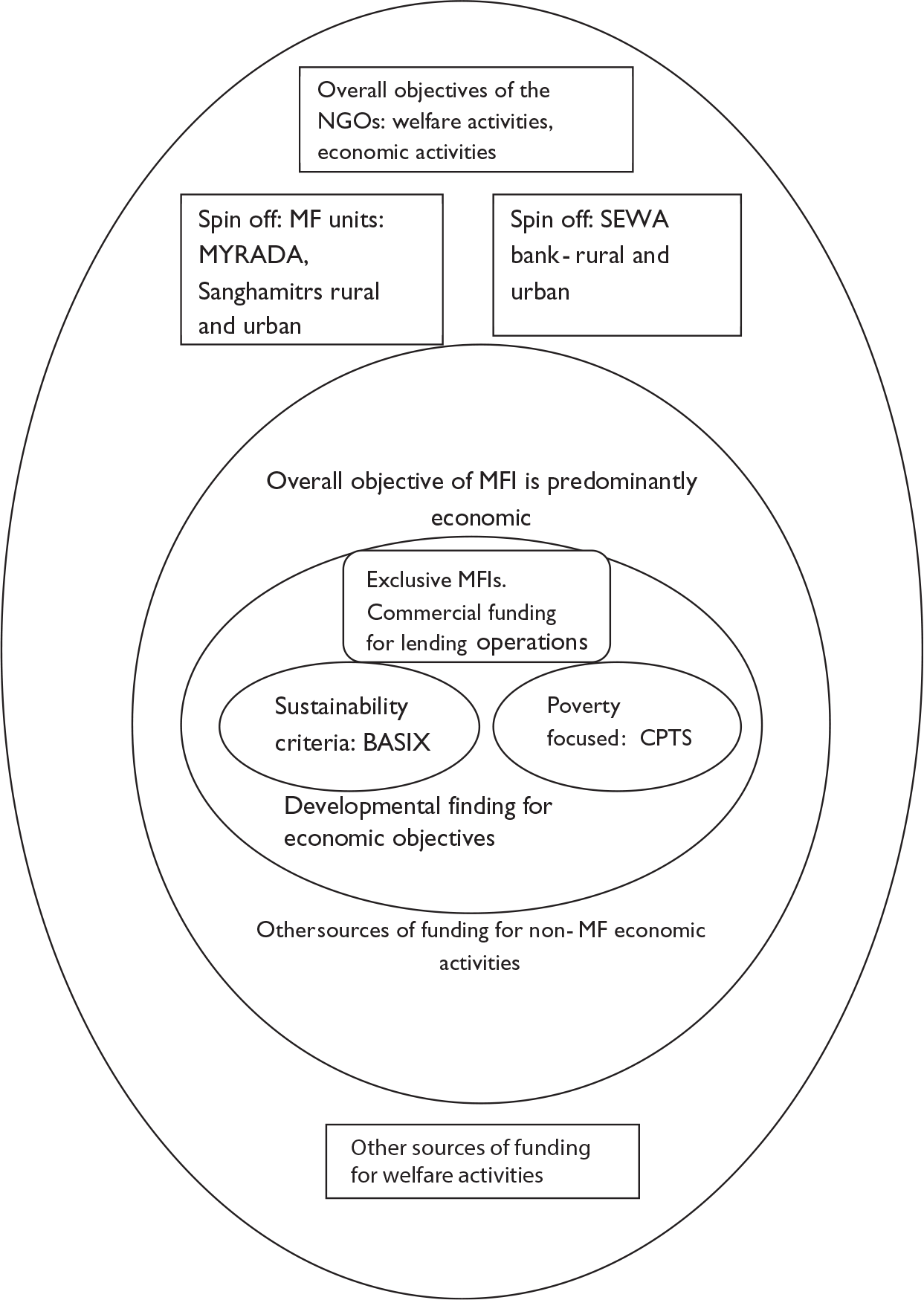

Microfinance in India was taken up as an act of welfare state philosophy and painstakingly honed as a strategic tool to fight poverty. Gradual and sustainable empowerment is also one of the goals envisioned for MF in India. The concept of course gained prominence only with the Grameen bank experiment of Yunus and came to be regarded as the ‘alternative sector’, an alternative sector which is forsaken by government or by the corporate (Sriram & Upadhyayula, 2002). The authors have given the definition of MF in a pictorial format, which they call the Microfinance Egg (Figure 3).

The Reserve Bank of India has declared MF sector as a key initiative for inclusion drive recognising the fact that MFIs have emerged as the most acceptable and viable alternatives for extending financial services to low-income group population (EY Report, July 2016). Yet, the development of the MF sector has not been a sudden growth but a painstaking process of gradual evolution moving from initial cautious acceptance to active belief. Initially, the MFIs had been extending only small ticket loans aimed at basic income generation, which have gradually moved to consumption loans with larger ticket size with the customers maturing over extending loan cycles leading to developing higher sense of confidence in the investment (EY Report, 2016). The non-government organisations or the NGOs as they are popularly called have played a vital role in implementation of the MF initiative by forming self-help groups (SHGs). Indian SHGs are primarily dominated by women and have gained some measure of empowerment through self-employment due to credit provided to them (Ghosh, 2005). A timeline of the growth is given in Figure 4.

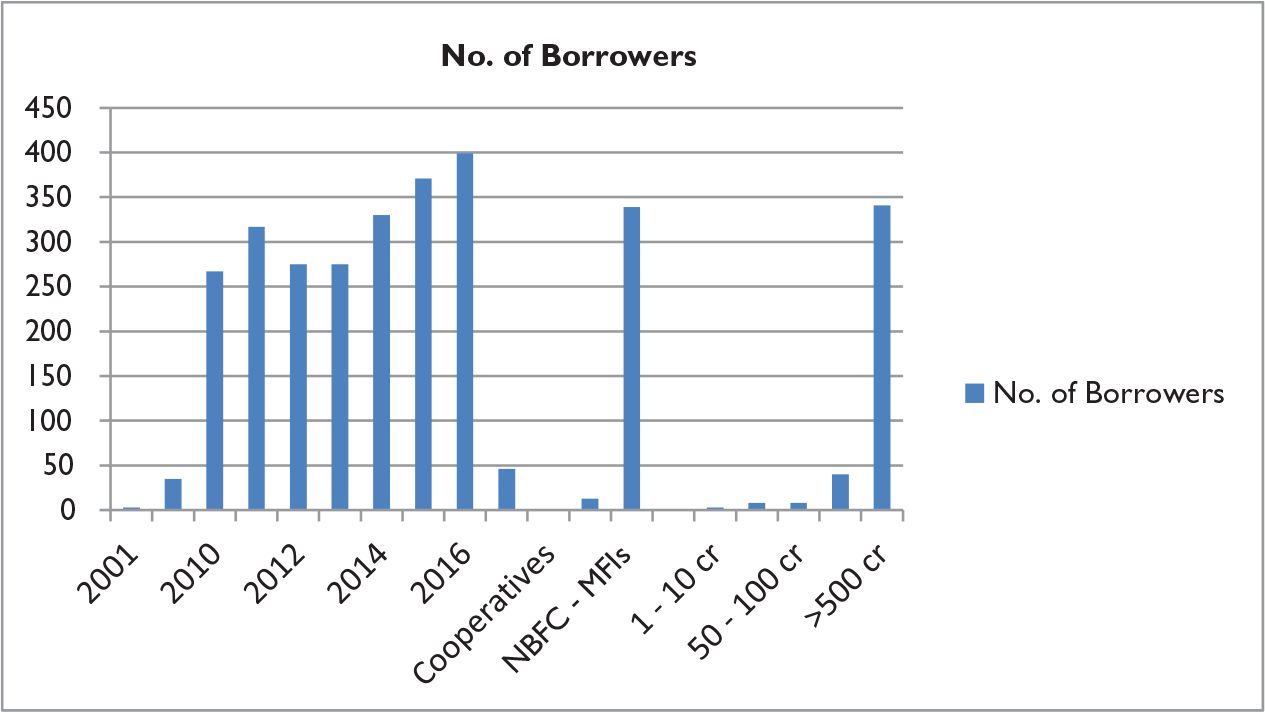

The NGOs and MFIs were primarily dependent on various financial institutions for their source of funds. Of late banks and other insurance companies have gained cognizance of the large market of the low-income group households traditionally viewed as bad for credit areas. As NGOs offer a gateway to these income groups, a number of corporate are now entering into the realm of micro-credit by establishing alliance with NGOs as clearly observed in the case of the ICICI bank (Srinivasan & Sriram, 2003). The arena of MF now stands expanded with the emergence of new players and higher level of competitiveness (Figure 5).

The SRI–MFI Connect

Microfinance by its very conceptualisation is a socially responsible investment in view of its tri-dimensional agenda that seeks positive screening, shareholder activism and sustainable development of the below-poverty line population. Similarly, MFI can be said to have a triple bottom line agenda comprising economic empowerment, financial inclusion and social upliftment of the economically active poor. Despite the ESG focus, MFI is increasingly viewed as a strategic tool by many investors who aim to do impact investing or SRI as MFI has ‘limited exposure to systemic risks due to low correlation to international capital markets’ (Krauss & Walter, 2008). This feature makes MFI a strategic investment which has a proven record of substantial returns while at the same time offers a typical social responsible avenue of investment thereby integrating both social and financial considerations (Galema, 2011).

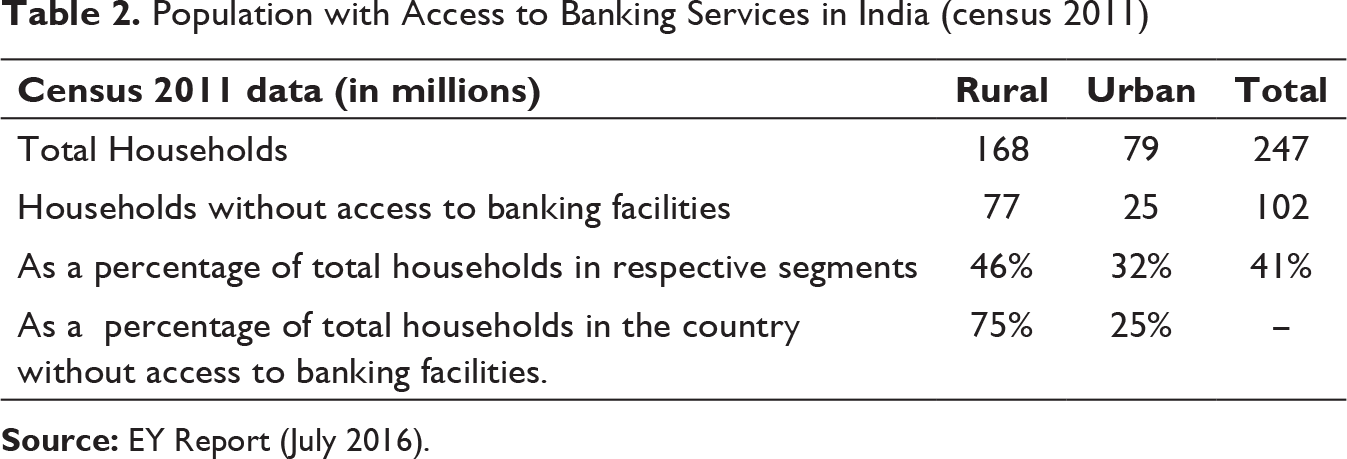

Commercial Banks in Microfinance—Emerging Vistas

Population with Access to Banking Services in India (census 2011)

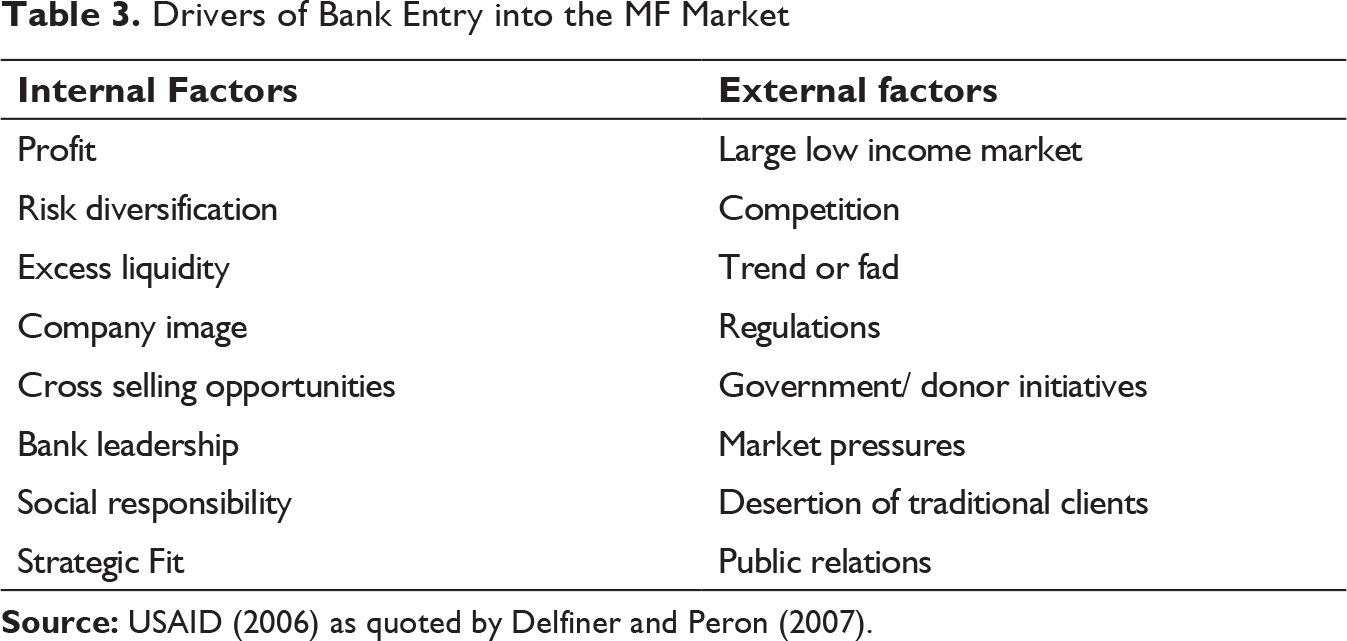

Drivers of Bank Entry into the MF Market

The Reserve Bank of India has introduced the use of the services of third parties called business correspondents (BCs) to enhance the outreach services of the bank whereby the banks can expand their financial products to include micro-products like micro-loans, micro-savings, micro-insurance etc. (Mas et al., 2012). The banking industry worldwide has started taking notice of the potential of the small time borrower. This may be due to the need to diversify in the face of stiff competition in the existing market or gaining cognizance of the NGOs turned banks, which are making potential profits in the market.

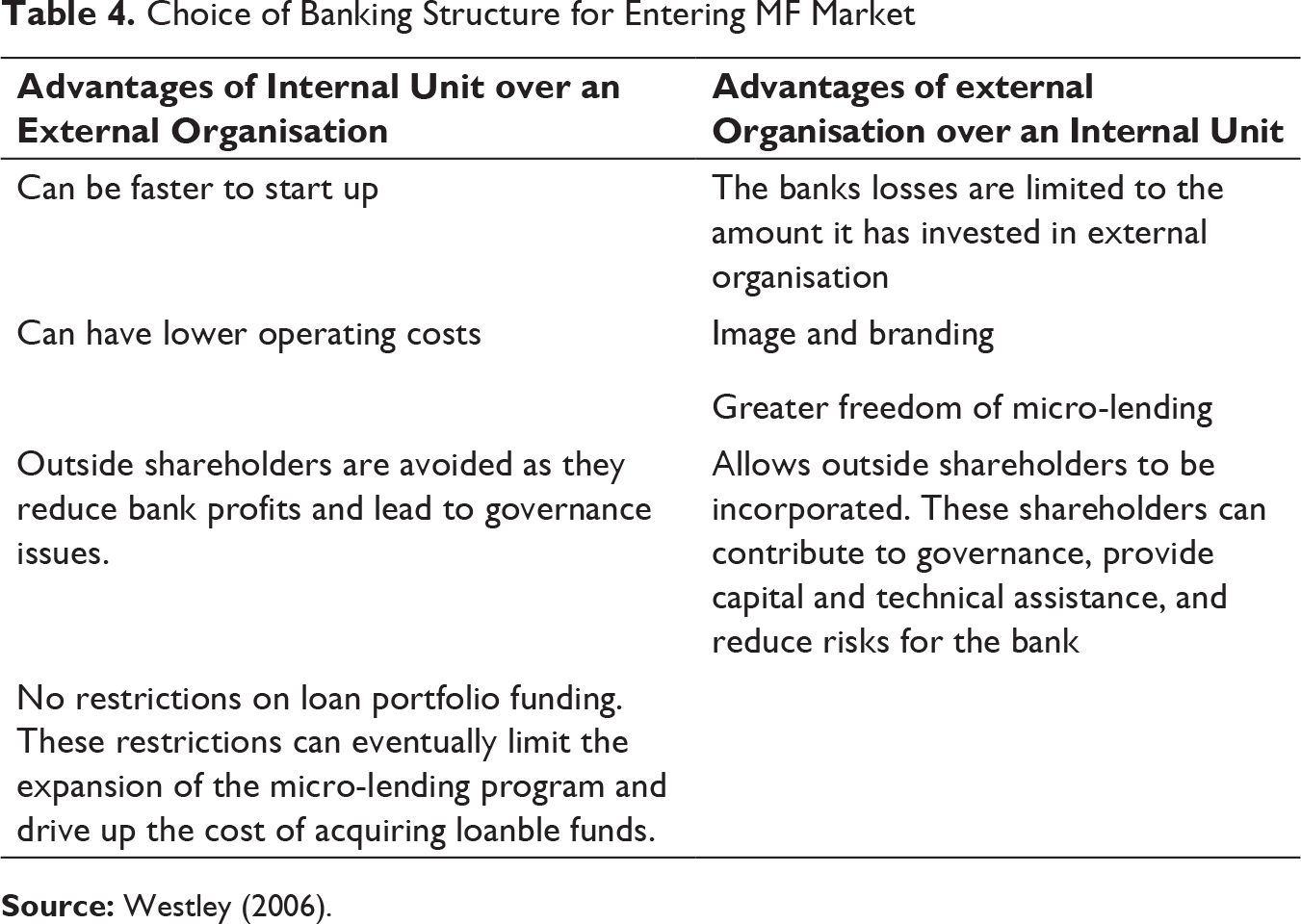

The act of catering to the hitherto ignored lower level consumer is called as downscaling, wherein the bank establishes a branch of MF within the gamut of its regular operations (Rhyne, 2009). The advantages of banks vis-à-vis MFIs as identified by Baydas, Graham and Valenzuela (1997) and Westley (2006) are: physical technical and human infrastructure, brand name and image that evoke credibility, access to plentiful and low cost funds, low cost structure and market knowledge.

Choice of Banking Structure for Entering MF Market

SRI–MFI and Banking Operations—the Strategic FIT

Microfinance has rechristened itself into a strategic investment opportunity, which also has the inherent potential to maintain focus on the ESG, social consciousness and social quotient of the industry. This is quite evident from the fact that there has been significant increase in the global volume of MF investments during the late 2000s leading to foreign capital investments of more than 10 billion dollars by December 2008 (Reille & Forster, 2008, CGAP report). Mostly, such investments are carried out by the MIV, which is a private entity that acts as intermediary between investor and MFI (Galema, 2011). Dieckmann (2007) in the Deutsche Bank report quotes that while they allow investors to adopt a social investment strategy geared towards poverty alleviation they offer an attractive risk-return profile at the same time. The reason may also be to develop a social-friendly public image (Baydas et al., 1997).

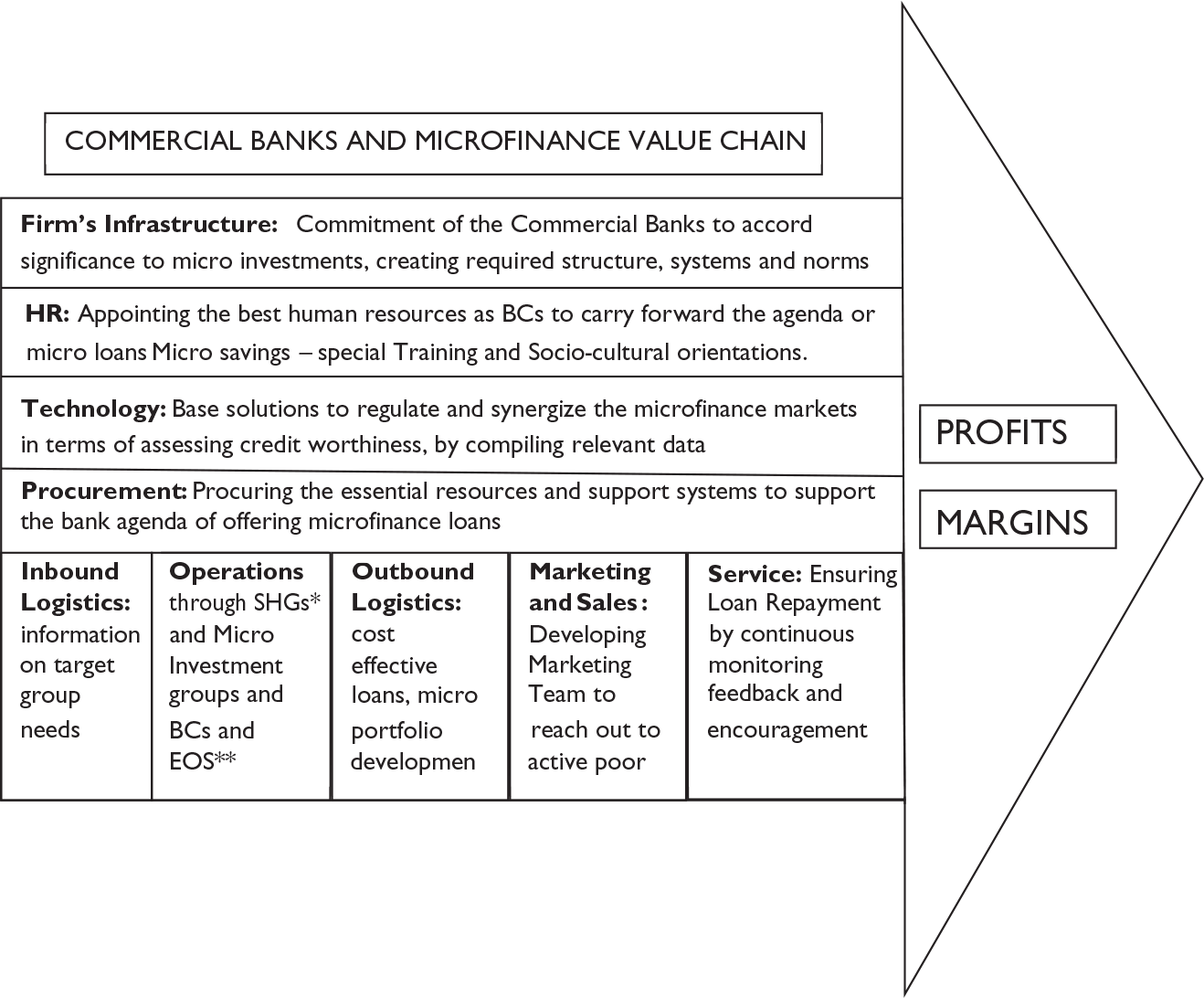

Value chain analysis is a strategic analysis tool created by Porter (1985) for strategising the organisation by analysing and understanding its value proposition in his book titled Competitive advantage—creating and sustaining superior performance. Porter (1998) classifies activities of an organisation into primary and secondary. The primary activities are called the inbound logistics, which refer to what comes into an organisation; for example, raw material. Operations refer to the actual production of either goods or services in the organisation. Outbound logistics refer to the final product which is sent into the market to be sold, an activity undertaken by the marketing and sales function whose primary role is to place promote and sell the product. Finally, the service function refers to the after sales service. These activities are considered to be vital for the organisation and therefore need to be infused with value to ensure value orientation in each and every activity of the organisation. The primary activities need to be supported by the secondary activities to derive holistic value for the organisation. The secondary activities are the firms’ infrastructure which is represented by the firms’ vision-mission and philosophy of the organisation. Identification of the best human resource to carry the vision forward is the next secondary activity, followed by procurement function which encompasses procurement of all the vital resources of the organisation whether tangible or intangible in the most cost-effective and value-driven manner. Finally, technology is the major enabler which cannot be denied in the present day organisations. An organisation’s value chain is accrued by the perfect synchronisation between the primary and secondary activities. The value chain is driven by the organisation’s attempt to enhance the value in all the activities undertaken by an organisation.

The value chain proposed in the study as shown in Figure 6 is an attempt to embed the MF as a credit instrument into the fabric of the commercial banks so as to generate value for the bank from the BOP clients or borrowers. The inbound logistics in this case are the information about the target group and their credit requirements. The banks presently need to spotlight their focus on the BOP consumer and their types of credit requirements. This may require the commercial banks to break-free from their traditional valuation of credit worthiness and develop systems to understand the inherent value of the BOP customer, which could be hidden and may not be visible to the traditional techniques.

The next primary activity of the value chain is to ensure operational efficiency after the gaining information about the target consumer group from the inbound operations. Here, the BC proposed by the RBI may be put to use. The BC model proposed by the RBI aims to arrive at a win-win situation, for both the banks and the MFIs (Mas et al., 2012). The banks on one hand gain access to a hitherto ignored segment of customers who have been sufficiently tempered by the MFIs to form a significant chunk of customers for the bank. The MFIs on the other hand gain access to the structure, technology, systems and support resources of the bank leading to a mutually beneficial partnership. The model thus provides a scope for balancing both financial and social returns. The banks need to identify the target customer value proposition and design a relevant business model (Mas et al., 2012).

The banks as a part of the outbound activities need to focus on creating micro-credit portfolio and then market it using media that can effectively reach out to the target consumer who may not be very comfortable with the traditional advertising techniques like electronic and print media. The banks may have to heavily depend on individual promotion and door-to-door promotion. Self-help groups may be roped in for this purpose.

These primary activities of the bank need to be supported by the secondary activities like reengineering the vision-mission and philosophies of the banks to show commitment and confidence in micro-credit as a viable credit instrument. Any lack of trust in the top management with the MFI can defeat the purpose even before it is implemented. Further the bank needs to engage the right manpower to develop and sell the MF products.

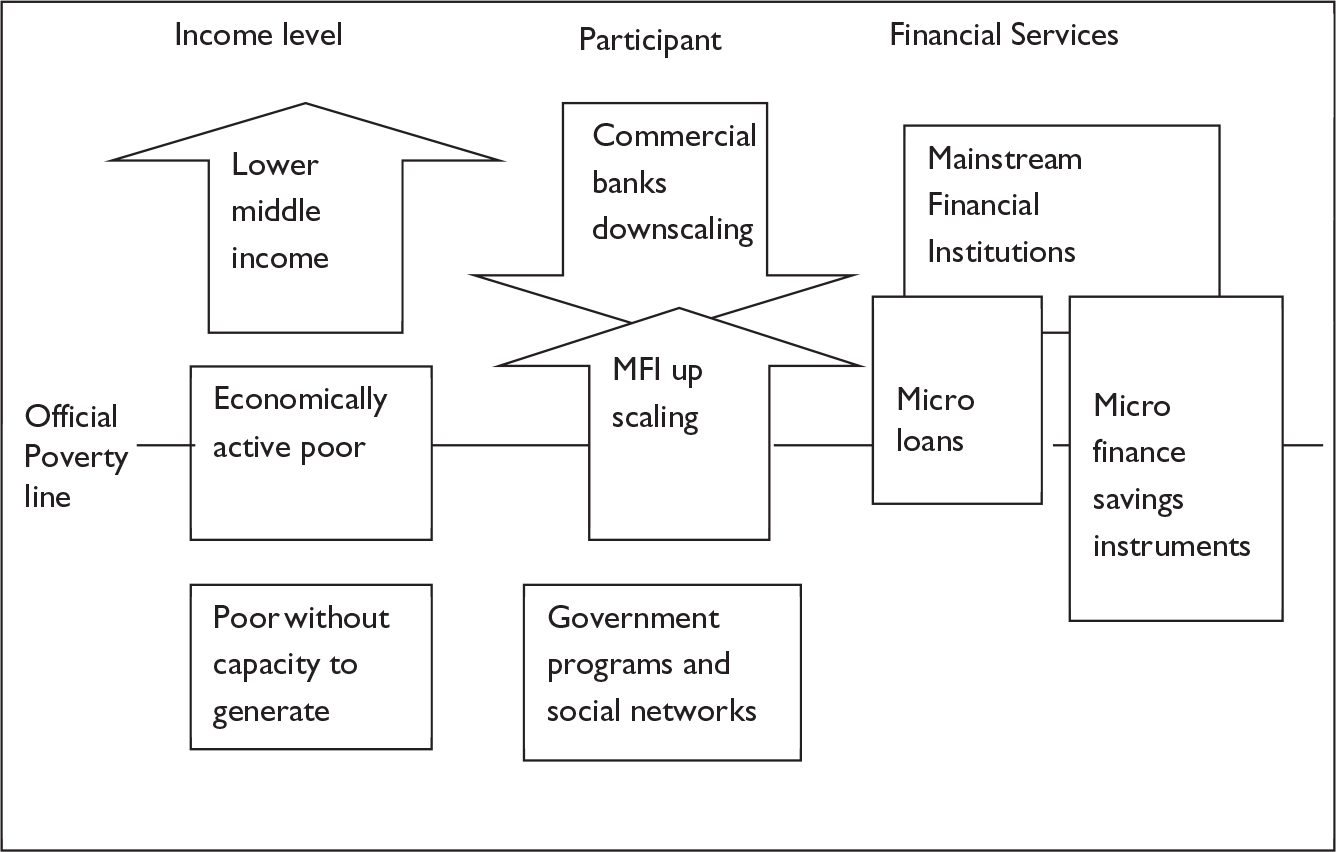

The model suggested by Delfiner and Peron (2007) elucidates the fine line of balance that needs to be arrived at the commercial banks and MFIs to contribute fruitfully to poverty alleviation. In their study, the authors classify the target consumers into lower middle class, economically active poor and below poverty line who have no scope for income generation. It is the economically active poor that need to be targeted to achieve financial inclusion and economic empowerment of this segment. Suitable technological systems need to be developed and such systems need to be made user-friendly for the most unaware user.

In this context, the model (Figure 7) developed by Delfiner and Peron in 2007 may be quoted wherein the customer of the bank have been delineated as lower and middle income group customer, economically active poor and poor without income generation capacity. The authors recommend the banks to concentrate on the economically active poor. Second, the authors recommend the banks to downscale their area of operation and the banks to upscale their area with adequate support from the government. Thus, finally the banks can be encouraged to develop micro-loans and MF savings instruments. Swanson (2007) in his paper titled ‘Role of International Capital Markets in Microfinance’ makes a case for the need for capital markets to fund MF as it is considered profitable, low risk and an expanding financial opportunity, when properly conducted. This study argues that MF has finally emerged as a major financial instrument with a positive risk profile encouraging the capital markets to involve in ‘banking with the unbankable’ (ibid.). The success of the ICICI bank in implementing a model has been much touted and quoted as example.

ICICI—The Microfinance Debut—A Case study

Michael Hokenson and Todd J. Markson (2003) developed a case study of ICICI bank’s MF initiative under the digital dividend—what works series with the combined partnership of the information for development program (Infodev) of Microsoft and the Columbia, Michigan and Kenan Flagler business schools. This case study traces out the attempts of the ICICI bank to economically empower women from lower income households by encouraging regular monthly savings, fund for emergencies and short-term group loans. This is done by the bank in a highly professional manner by appointing social service consultants who initiate the formation of the SHGs, who are further manned by coordinators. A bank project manager is appointed to manage the whole process. As the interest rates charged by ICICI (18%) are lower than the traditional money lender’s rates, the programme has more than 8,000 SHGs in its fold and is expanding. The ‘direct service model’ of the ICICI has been helpful in developing self-confidence in women and fostering group solidarity. Thus the bank, according to the case study, has been successful in merging the twin goals of social commitment with a keen focus on innovation for profitable business.

Conclusion

There is a need for both the financial institutions like banks and the MFIs to collaborate together to take benefit from the BOP market and at the same time give benefit to the BOP market. The area of MF is also attracting large institutional and direct foreign investment as per the CAGP report 2008 (Reille & Forster, 2008). The MFIs themselves are identifying avenues to transform into ‘for profit social businesses’ (ibid.). This may usher in a new era in the MF narrative. Syndicate bank was one of the primary banks in India to have initiated the concept of encouraging micro-deposits and also sanctioned micro-loan (short) periods like on daily and weekly basis (Mahanta, Panda & Sreekumar, 2012). The banks need to reengineer themselves to the new product requirements and design relevant systems to accommodate needs like small and frequent EMIs. The consumer on the other hand needs to be made comfortable with the formal banking system as the micro-financing is more in tune with the traditional money-lending system. The question of individual and group lending also needs to be addressed as the traditional banks are more equipped to cater to the needs of individual loans in contrast to the group loans methodology adopted by the MFIs. The triple bottom line of economic empowerment, financial inclusion and social uplift of the economically active poor can be well achieved if the agenda is strategised to undertake the transformation with equal focus on the needs of both the banking sector and MFIs.