Abstract

Innovation enables firms to face increasing competition in the global environment, but there is variation in innovation investments across firms due to the inherent uncertainty involved in innovative activities. The strategic role of board, therefore, becomes crucial in overseeing innovation decisions. This study, hence, examines whether the relation between R&D investment and firm’s performance would vary based on the board characteristics of the company. It empirically explores this interrelationship in publicly listed Indian companies, by assessing the moderation effect of board using fixed effect regression analysis and conditional effects on a panel data of 9,031 firm years across twelve years. Board size, board meetings, proportion of women director and board leadership are found to negatively moderate the relationship between innovation and financial performance (ROE), however none of them moderates the relation between innovation and firm value (Tobin’s Q). It signifies that though board characteristics play an important role in relationship between innovation and ROE, investors fail to recognise it. Companies should focus on creating the right kind of board, investors must appreciate board’s influence in the success of R&D investments without being driven by mere compliance. Policy makers should deliberate upon the desirability of present structure of stringent laws.

Introduction

Innovation is central in today’s rapidly changing business environment to enhance the performance of firms. It helps firms create a competitive advantage and sustain long term growth. The innovative strategy is, however, experiential as well as interpretative as it involves decisions on irreversible investments carrying inherent risk in their expected results. Companies, therefore, differ in their innovation investments as management finds it difficult to allocate resources in innovative activities due to uncertainty in their returns. The decision to innovate thus becomes a matter of strategic choice of management. They may either deviate resources to avoid risk or undertake unnecessary risk, hurting the value of shareholders’ investment. The need for effective governance thus arises to ensure accountability of management towards investors, wherein the board of directors play key role in encouraging innovation while monitoring risk in the firm with the objective of maximising returns to stakeholders.

According to Porter (1990), firm’s structure and strategy is one of the crucial elements in determining the success of the firm. It is the board of directors that define the firm’s structure, and foster innovation which is an important element of corporate strategy. Directors, as the resource dependency theory purports, act as an important resource for the company by providing necessary expertise, skills and knowledge required to facilitate decision making. The innovation strategy in a company is shaped by the board’s ability in selecting and evaluating various alternative investment opportunities. They affect the resources firms devote to innovation and also assist in successful implementation of R&D projects, which in turn enhances performance. Therefore, the interplay of board and innovation needs to be acknowledged, as the extent of gainful innovation in an enterprise depends on board’s efficiency in formulating and scrutinising the strategies to enhance shareholders’ value.

But the interrelationship among board, innovation and performance has received little attention in the literature and needs to be explored. Numerous studies have established the relationship between innovation and firm performance, but have failed to recognise that investment in innovation is a strategic issue which has to be understood in the context of corporate governance. Though the moderating impact of board on the relationship between innovation and performance has been examined by few researchers (Baysinger et al., 1991; Lee & O’Neill, 2003; Sapra et al., 2014), but it is mainly done in developed countries. Thus, the study investigates the board-innovation-performance relationship in India to examine the competence of board in translating innovation into enhanced firm performance.

Using a panel of 947 Indian listed companies actively engaged in R&D investment over a 12-year period from 2006 to 2017, the article examines which board characteristics strengthen the relationship between innovation and performance. The findings imply that firms actively involved in R&D should not have a large board, too frequent board meetings, high proportion of women directors and separate the position of CEO and Chairman in order to enhance the effect of innovation on performance. The results help in understanding the relevance of corporate governance regulations especially when India has recently made amendments to its law. Regulations regarding restriction on board size and requirement to disclose skill set of directors is a right move but separation of chairperson and CEO may need to be re-examined.

The rest of the article is organised as follows—the next section describes literature review, then research approach followed by the empirical results, discussion and implications, and finally the conclusion of the article.

Literature Review and Hypothesis Development

Innovation is the mode of expansion and sustainability for companies in today’s competitive environment, that requires firms to undertake research and development (R&D) expenditures. R&D investments indicate firm’s innovation ability (Griffith et al., 2004), and has a positive impact on its market value (Parcharidis & Varsakelis, 2010). Literature has well established the linkage between R&D activities and firm’s performance theoretically as well as empirically. But the investments in R&D are risky (Munari et al., 2010), they reduce short-term earnings and their returns are neither immediate nor certain (Driver & Guedes, 2012). Innovation therefore depends on the risk appetite of management, they may under-invest in R&D or engage in unnecessary expenditure on R&D, which may hamper firm performance. The conflict of interest between managers and shareholders due to separation of ownership and control (Berle & Means, 1932), therefore, becomes acute in decisions regarding innovative investments due to their long-term horizon. Hence, innovation has to be considered as a constitutive element of entrepreneurship (Lumpkin & Dess, 1996), which is affected by decisions taken by management, and thus, has to be handled diligently.

To address this discrepancy, shareholders want corporations to be governed with oversight mechanisms in order to align manager’s interest with their interests. In that context, the composition of board acts as a signal to market participants about the robustness of the corporate governance mechanisms in place (Fama & Jensen, 1983). Board of directors hold the greatest power in strategy formulation, and thus, are central to corporate innovation. As it involves qualitative and subjective judgement, the effectiveness of innovation is determined by board characteristics of the company (Rabi et al., 2010). Ineffective boards are found to negatively affect the relationship between innovation and performance (O’Connor & Rafferty, 2012). A proper board would ensure appropriate level of R&D investment by curtailing managers’ tendency to pursue inefficient strategies (Jensen & Meckling, 1976), and thus, lay the foundation for successful innovation. This study therefore explores the moderating effect of board characteristics on relationship between R&D investment and performance.

Board of directors are responsible for making critical strategic decisions, they act as important resource in providing the required expertise, knowledge and skills to companies. The composition of board and their activity thus form important parameters to assess the efficacy of company’s board on its performance. Supporting resource dependency theory, researchers have found empirical evidence on positive association between board size and performance (Jackling & Johl, 2009; Pearce & Zahra, 1992). But Yermack (1996) has established negative relationship between the two due to coordination problems. Moreover, size of the board has significant negative association with product innovation (Galia & Zenou, 2012). Shapiro et al. (2015) found no evidence on relation between board size and innovation, and Rabi et al. (2010) found no moderating effect of board size on R&D performance relation.

Board leadership, according to stewardship theory, should rest with CEO of the company but separate position for CEO and board chairperson is found to enhance innovation (Hill & Snell, 1988; Wu, 2008). Ben and Dwivedi (2013) also observed negative effect of duality on innovation due to undue influence of one dominant person in strategic decisions. Findings of Driver and Guedes (2012), Hirshleifer et al. (2012) and Hung and Mondejar (2005), however, found risk-taking preference and zeal to undertake new initiatives in CEOs who hold position of chairman as well. Researchers have also considered the influence of appointment of independent directors and found that monitoring and expert advice provided by them leads to higher R&D and Tobin’s Q (Chen & Hsu, 2009; Chung et al., 2003; Lacetera, 2001). Chang et al. (2015), however, reported negative association between independent directors and risk. Faleye et al. (2011) too provided evidence for negative impact of board independence on innovation. David et al. (2001) found that outside directors have no moderating effect on relationship between R&D investment and performance.

Gender diverse boards are also found to bring positive impact on firm performance (Carter et al., 2003; Daily & Dalton, 2003), but others have reported no relation between the two (Chapple & Humphrey, 2014; Rose, 2007). Miller and Triana (2009) found a positive relationship between gender diversity and innovation; they stated that women bring different perspectives and working styles, and ideas which helps to identify new innovative opportunities. Torchia et al. (2011) argued that presence of women directors enhances organisational innovation, but Tseng et al. (2013) found no effect of women directors on firm’s innovative activities. According to researchers, female directors have inadequate management experience (Peterson & Philpot, 2007), are more sensitive, more risk averse (Eckel & Grossman, 2008), and less competitive than men in general (Croson & Gneezy, 2009), which could have adverse effect on allocation of funds for innovation.

Apart from board composition, board activity measured through frequency of board meetings and participation of directors therein also acts as an important determinant for effective innovation investment (Rabi et al., 2010). Active board improves performance (Lipton & Lorsch, 1992), but negative association between frequency of board meetings and R&D–performance relationship has also been reported (Li, 2012). It highlights that the proficiency of the decisions is conditional on active participation of board members in meetings. The power of independent directors depends on their readiness to act and participate rather than their credentials (Liu et al., 2016). It is therefore crucial for directors to attend and actively contribute in board meetings. Multiple directorships, however, tend to adversely affect directors’ active participation in board meetings. Directors were found to be more active as against their less busy counterparts in terms of attending board meetings regularly (Sarkar & Sarkar, 2009). Busyness of directors is found to negatively affect company’s performance (Fich & Shivdasani, 2004; Jiraporn et al., 2009). Pfeffer (1972), on the contrary, contends such directors as valuable resource for the companies. He stated beneficial aspects of their networks to access suppliers and customers, Balsmeier et al. (2014) too argued positive impact of experience possessed by these directors on firm’s innovation activities that is beneficial in improving performance.

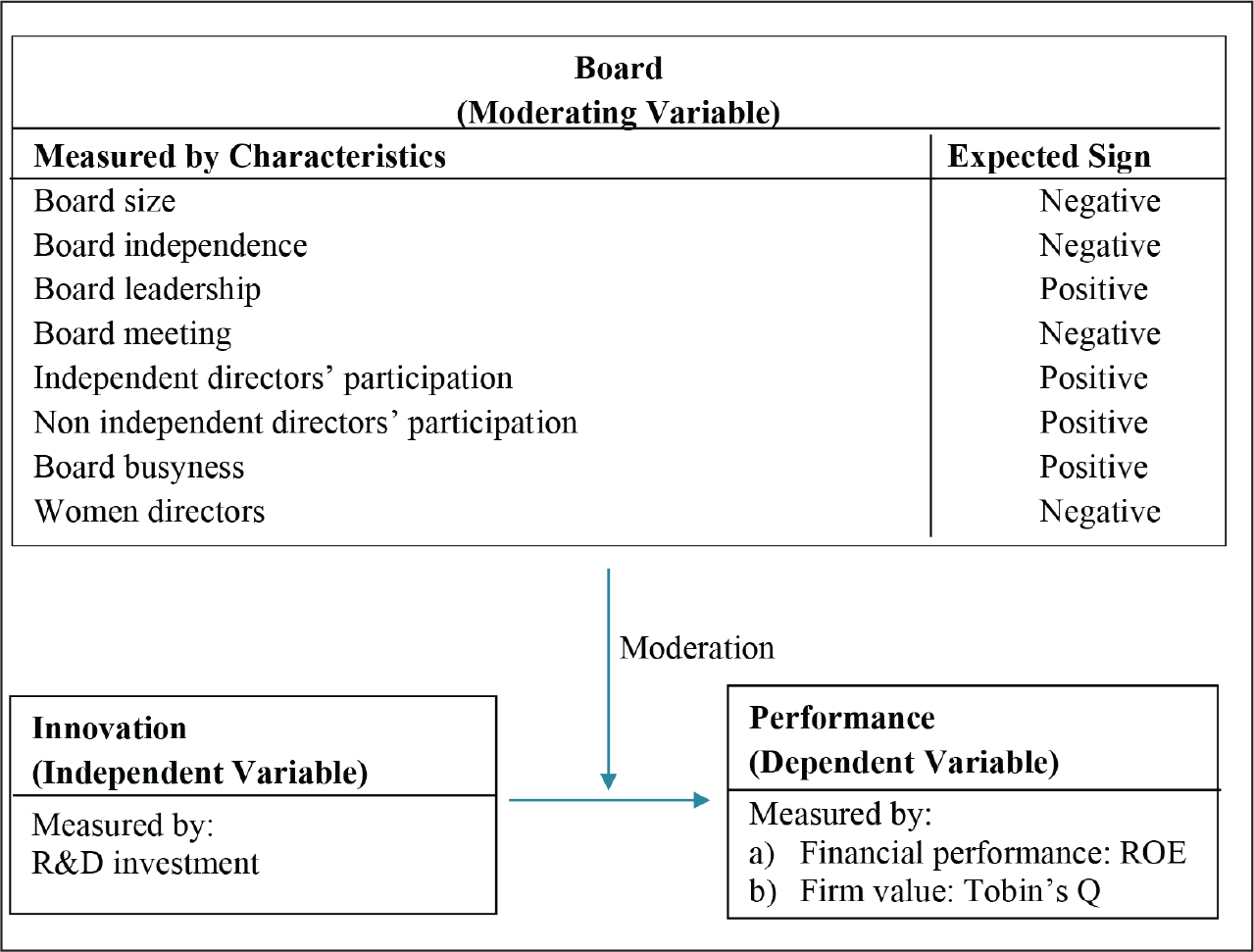

Since the limited number of studies examining the moderation effect of board characteristics on innovation–performance relation provides inconclusive findings, the study makes an attempt to explore the moderating effect of board size, its leadership, presence of independent directors, gender diversity on a company’s board, board meetings, participation of directors in meetings and multiple directorships held by directors on shareholders’ return through innovation strategy. The conceptual model is presented in Figure 1.

Data and Methodology

The sample selection, data sources, measurement of variables and methodology is elaborated as follows.

Sample Design

From a population of 5,477 companies listed on the Bombay Stock Exchange (BSE), only those which have incurred R&D expenditure and had data available on governance and performance variables were taken resulting in a final sample of 9,031 firm years. The data for the period 2006–2017 is extracted from Prowess IQ, the corporate database maintained by Centre for Monitoring Indian Economy (CMIE), and also from the respective websites and annual reports of the companies.

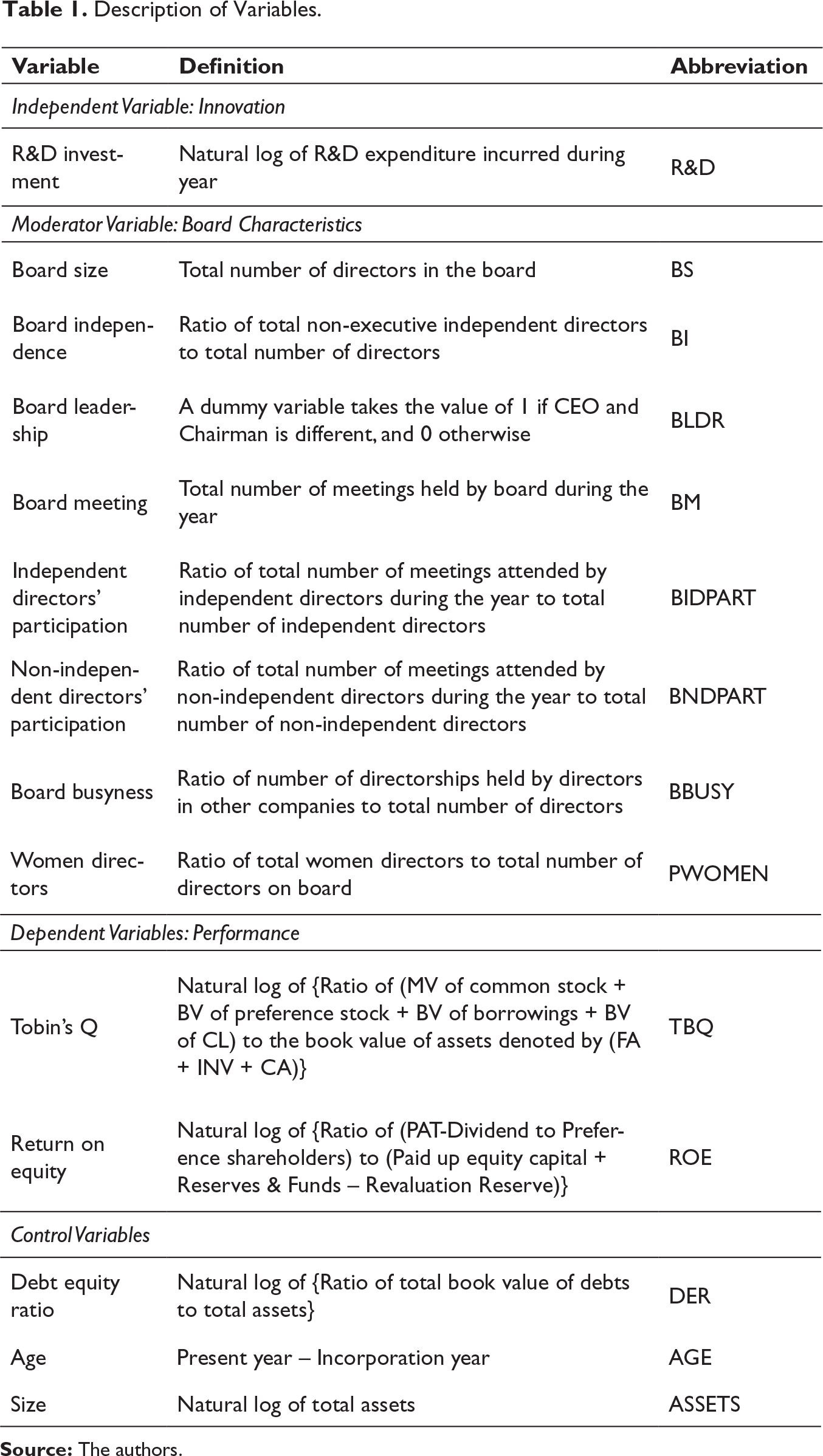

Variable Measurement

Description of Variables.

Source: The authors.

Empirical Model and Data Diagnostics

The study employs moderation approach by Baron and Kenny (1986) to test moderation effects, while running fixed effect regression in panel data set. With statistically significant chi-square (Prob > chi2 = 0.000) found while assessing the consistency of estimation results with fixed effects and random effects models, Hausman test confirmed the applicability of fixed effect regression in panel data. Moderation method requires independent and moderator variable to precede dependent variable, therefore lagged values for performance is used in the model. It also allows board and innovation the required time to reveal their impact in generating returns (Chen & Hsu, 2009; Pakes & Schankerman, 1984). The moderation effect is tested by significant coefficient of the interaction term (XM) between independent variable (X) and moderating variable (M) added in the model. Further, conditional effects for significant moderation effects are computed.

Empirical model used by study is:

Performance Indicatorit = α0 + β1R&DInvestmentit–2 + β2CGit–2 + β3Interactionsit–2 +β4Cit–2+ vit

Where, performance represents Tobin’s Q and ROE, CG is vector of board characteristics, interactions denote product of R&D investment and board characteristic with C as vector of control variables for firm i at time t, and vit is the error term.

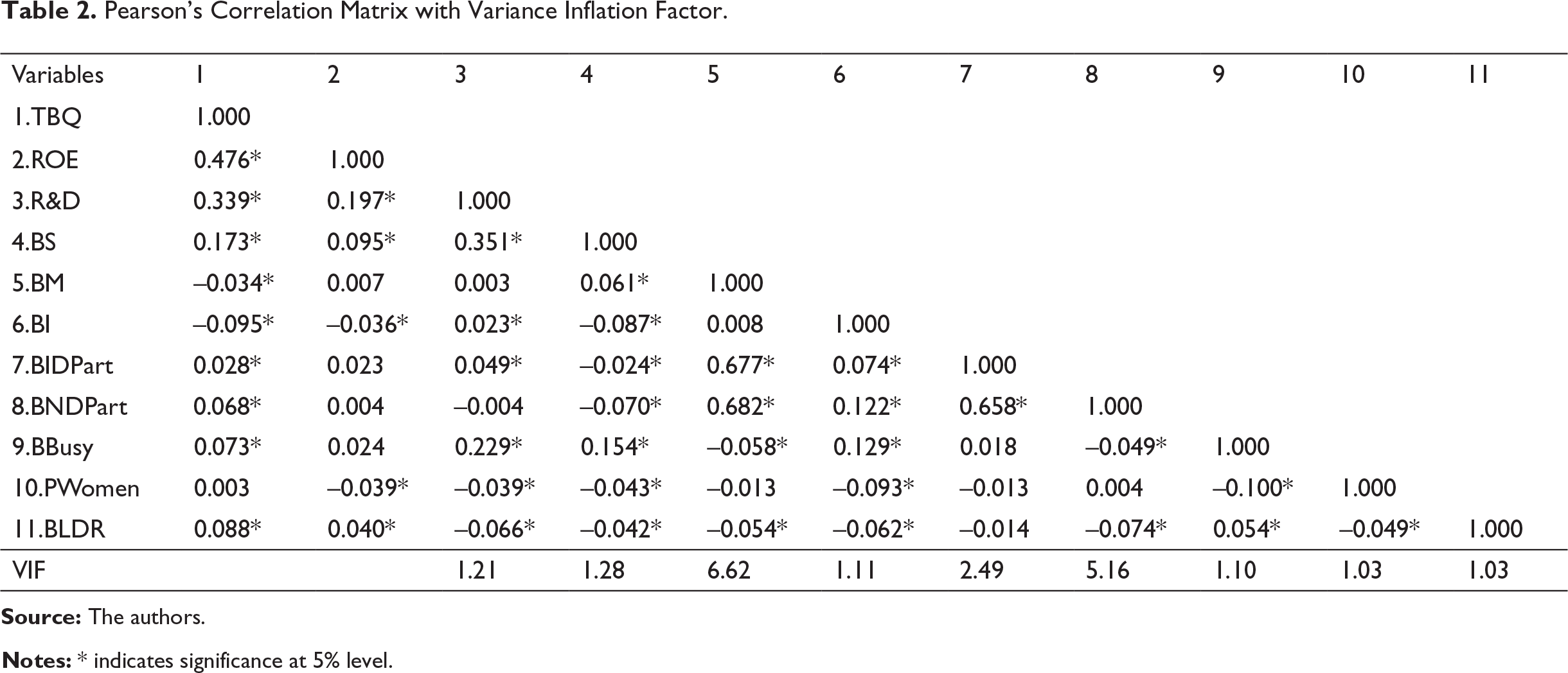

Diagnosis tests for heteroscedasticity and autocorrelation are employed using ‘Wooldridge test for serial correlation’ and ‘Modified Wald statistic for groupwise heteroskedasticity’ in the residuals of fixed effect regression. The tests confirmed presence of both, hence, cluster-robust standard errors are computed to obtain consistent regression estimates (Cameron & Trivedi, 2009; Wooldridge, 2002). To detect presence of multicollinearity, variance inflation factor (VIF) and pair-wise correlation matrix is drawn in Table 2. With correlations below 0.70 and VIF less than 8, multicollinearity is non-existent. Additionally, mean-centred values for R&D investment and board characteristics are used for computing the interaction term (Aiken & West, 1991) to increase the power of detecting the moderation effects.

Data Analysis and Results

Descriptive Statistics

The descriptive statistics in Table 3 displays mean, standard deviation, minimum and maximum value of the variables. Average size of board is 9 and more than half of the board is independent. Average participation of directors is 4 out of 6 board meetings held during the year. They do not appear to be busy as on average they hold 3 directorships. The proportion of women director is very low with 0.05%, but it has increased after appointment of at least one woman director was made mandatory in India from 2013. The board leadership at 0.62 indicates that for every 100 CEOs, 62 of them are not serving as board chairman. Companies have voluntarily separated the position of CEO and chairman, indicating good governance beyond the requirements of law.

Moderation Analysis

Pearson’s Correlation Matrix with Variance Inflation Factor.

Source: The authors.

Notes: * indicates significance at 5% level.

Descriptive Statistics.

Source: The authors.

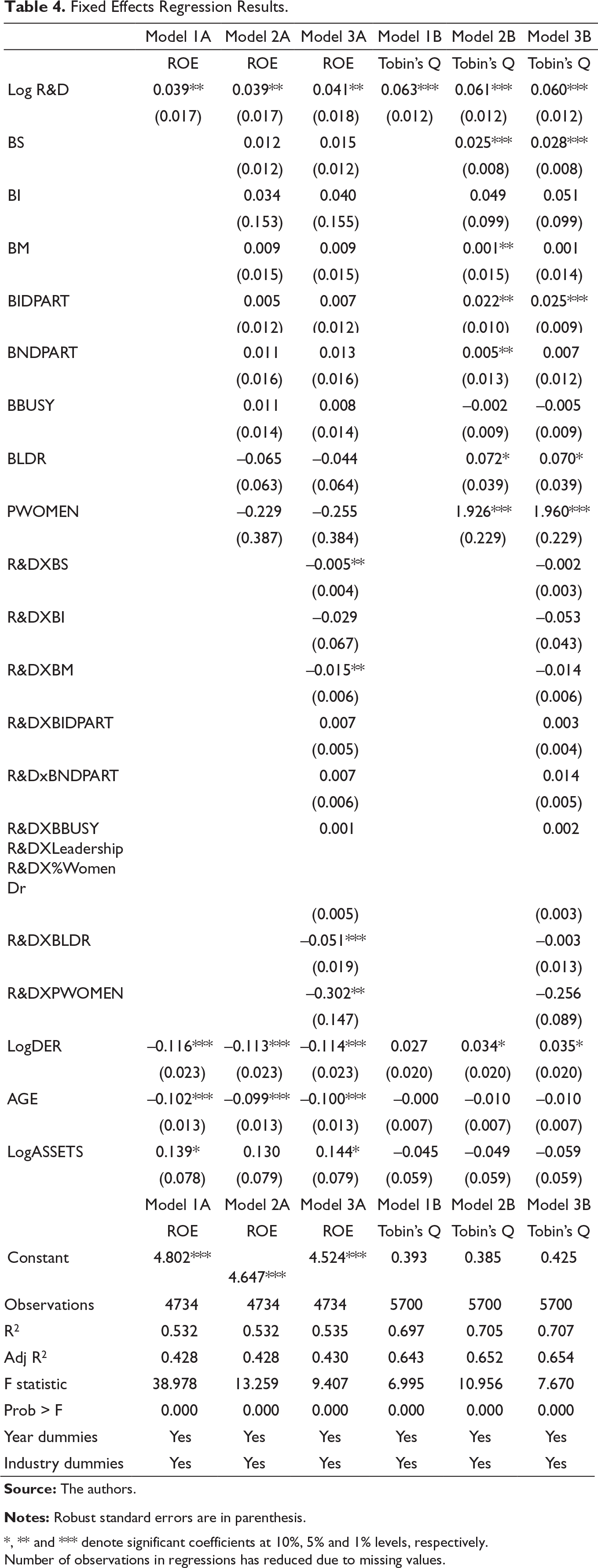

Fixed Effects Regression Results.

Source: The authors.

Notes: Robust standard errors are in parenthesis.

*, ** and *** denote significant coefficients at 10%, 5% and 1% levels, respectively.

Number of observations in regressions has reduced due to missing values.

Table 4 shows negative moderating effect of board size, board meetings, proportion of women director and board leadership on the relationship between R&D investment and ROE, but none has significant direct effect on it. However, all board variables except board independence and board busyness have significant positive effect with Tobin’s Q, but none of them moderates the relationship between R&D investment and firm value. The contradictory results between two performance measures clearly indicates investors’ failure to recognise the influence of board on the relationship between innovation and performance.

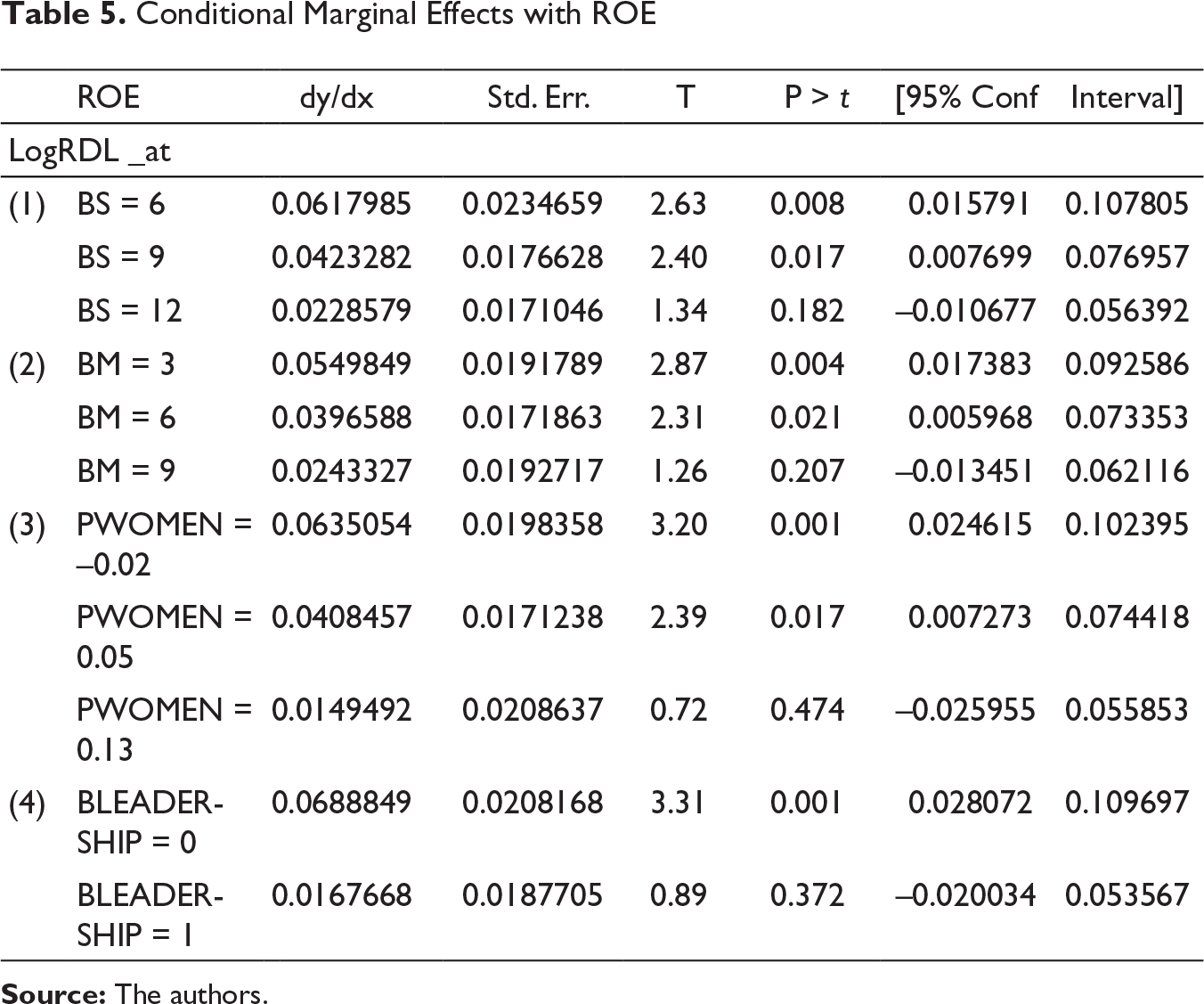

Conditional Marginal Effects

The conditional effects in Table 5 depicts magnitude of change in ROE with one unit change in R&D expenditure at different levels of board characteristics, that is, one standard deviation below its mean value, at its mean value and at one standard deviation above the mean value.

Table 5 shows significant marginal effects of R&D expenditure on ROE when board consists of 6 or 9 directors, however, it becomes insignificant once the number of directors in board becomes 12. The effect of R&D expenditure on ROE reduces from 6 percentage points to only 2 percentage points when board size increases from 6 members to 12. Similarly, the marginal effects of R&D expenditure on ROE are significant when board holds fewer meetings and diminishes as board meeting increases. It becomes insignificant as the number of board meetings reaches 9 (reducing to 2 percentage points from 5 percentage points), which is much higher than the prescribed minimum number of 4 meetings.

Conditional Marginal Effects with ROE

Source: The authors.

Discussion and Implications

The empirical results of R&D intensive Indian listed companies undertaken to explicitly investigate the interrelationship among board, R&D investment and performance using panel data set of 947 Indian listed firms over a 12-year period is attention-grabbing. The study clearly shows that board characteristics determine the extent to which innovation gets translated into performance, by revealing the negative moderating effect of large board size, frequent board meetings, high proportion of women directors and separate position of CEO and board chairman on the strength of relationship between innovation and financial performance. Investors, therefore, need to realise that mere compliance with governance regulations will not automatically lead to good returns, rather they should appreciate board’s strategic role in determining the success of R&D investments.

Along with useful insights for investors, important managerial and policy implications have also emerged from the results of the study. First, in contradiction to the resource dependency theory, larger boards are found to act as a constraint to the efficacy of R&D investment. Since larger groups are associated with high levels of cognitive conflicts and coordination problems, the decision on innovation investments is hampered. The lack of consensus among board members also prevents prompt corrective action on problematic investments, reducing the returns from R&D investments. Jensen (1993) and Lipton and Lorsch (1992), also insisted upon benefits of smaller boards and suggested an optimum board size of 7–9 directors. As shown by conditional effects, board size should be less than 12 to enhance the impact of R&D on performance, hence restriction of board size to fifteen directors in the Companies Act, 2013 acts as a benchmark in the right direction.

Second, the negative moderating impact of board meetings shows that frequency of meetings does not guarantee board’s attentiveness. Much of the meetings’ time is spent on routine tasks leaving little for deliberation on matters of strategic importance. Moreover, frequent meetings lead to wastage of company’s resources in expenses such as directors’ sitting fees, travel and refreshments, which also creates pressure on performance of firms. Hence, the board should hold 4–6 well planned board meetings during the year with the agenda to focus on strategic issues. When directors are provided necessary reports beforehand, and they come prepared to critically evaluate R&D projects and review investment decisions it will certainly improve the efficiency of innovation related decisions.

Third, women directors are found to be ineffective in augmenting the positive impact of R&D investment on financial performance. This could be due to several reasons. From 2015, the law compelled companies to appoint at least one women director. As a result, many of them were first time directors with inadequate boardroom exposure. In family-owned businesses, in most cases the female family members were appointed as directors to comply with the law. Majority of them did not have the relevant credentials, experience & understanding about market vulnerabilities which are essential in the context of innovation. As women directors are generally not appointed on positions of leadership such as chair or member of a prominent board committee, they lack adequate exposure to complex decision processes. Further, behavioural research suggest that women are risk averse. This implies they are less likely to support innovations as they perceive them to be high risk investments. These factors adversely affect the contribution of female directors in generating returns from innovation. Hence firms, particularly, those involved in innovative activities should appoint women director based upon necessary experience and expertise required for pursuing innovation, rather than as a compliance exercise. The requirement to disclose expertise/skills/competence of board of directors from March 2020, as provided in Listing and Obligation and Disclosure Requirement (LODR) would ensure selection of competent women who are better positioned to perform their role as director.

Fourth, in support of the stewardship theory, the results indicate that when the same person holds both the position of Chairperson and CEO it is beneficial. It enhances the impact of R&D investment on financial performance. On separation, there is division of power between two individuals which reduces control over board decisions. In family-owned Indian companies, the two positions even if separated are often held by different members of the same family leading to concentration of power. Absolute power along with required experience enables them to invest in and effectively manage complex and risky R&D projects, resulting in higher returns from innovation. Therefore, SEBI’s amendment to separate the powers of the chairperson and CEO needs to be reviewed.

Contrary to expectations, the presence of independent directors, directors’ participation in meetings and diverse knowledge of directors based on their multiple directorships did not produce desired outcome. It simply signifies symbolic presence of independent directors in company merely to abide by law, and passivity of directors in meetings. The companies should re-examine the process of selecting independent directors and evaluation of their contribution before reappointment. The regulators are also recommended to take measures for enhancing accountability of independent directors, without which their presence will continue to be ineffective. The companies, along with regulators, should focus upon building the character of board rather than creating legally perfect board structures to ensure successful translation of innovation into performance.

Conclusion

Based on the above results, it can be concluded that board and innovation complement each other such that relation between R&D investment and firm’s performance varies with the kind of board the company has. Given that there is enactment of more stringent regulations in Indian corporate governance (SEBI, 2018), the policy makers need to acknowledge that one size fits all approach of governance would be detrimental to R&D intensive companies, and they should be given flexibility to adopt guidelines suitable for them. The results confirm that firms actively involved in innovation should maintain optimum board size, make board meetings more effective, choose competent women directors, and combine the role of CEO and Chairman to enhance the effect of innovation on performance. In addition, the investors need to give due consideration to relevance of the board, as a sound board can bring higher rewards from innovation investments which is unlikely if companies follow tick the box approach to governance measures. Unless action is taken by companies and regulators to enhance the accountability of board, especially independent directors, they will continue to be ineffective in enhancing firms’ performance. Firms should aim to structure the board in a manner that creates a conducive environment that brings out the best from directors, as it takes the right kind of board to successfully translate innovation into performance.