Abstract

Effective corporate governance leads the way towards aligning the interest between managers and shareholders. Effectiveness of practicing the corporate governance of companies in Sri Lanka is debatable topic due to the variation between standard and actual practices. This study aims to examine the influence of board diversity on agency costs of companies listed in Sri Lanka as proposed by agency theory. The sample of this research consists of all companies listed in Sri Lanka, exclusive of bank and financial institutions which are practicing unique governance practices issued by Central Bank of Sri Lanka. The final sample consists of 180 companies during the period from 2013 to 2019. This study deployed panel regression analysis to test the relationship formulated in the hypotheses by using the EViews 9 software. The results showed that the board diversity-related variables such as separate leadership structure and presence of non-executive director on companies’ board are appeared to have significant influence on agency costs. Meanwhile, board size does not have direct impact on agency costs. The findings of this study regarding board diversity and agency costs have important managerial implications, that these findings are unlikely to the prediction of agency theory and best practices. Agency theory is not applicable to these companies, since the exiting corporate governance practices increase agency costs. The potential benefits of this study led to re-think the board of directors of the companies, managers, shareholder and the policymakers to re-organise the implementation of best practices.

Keywords

Introduction

Corporate governance leads the way to resolve conflict of interest between shareholders and managers in firms (Chilosi & Damiani, 2007). Effective corporate governance is vital to any organisation to resolve the agency problems (Kiel & Nicholson, 2003; Shaifali & Mittal, 2019). The best practice of corporate governance is backed by agency theory, stewardship theory etc. However, corporate governance practices of companies all over the world is differed due to the economic, political and social context (Garanina & Kaikova, 2016; Nam & Nam, 2004). The Anglo-Saxon model of corporate governance is based on the idea of agency theory that concentrate on distributed ownership and control. This model is presently practiced in the United States and United Kingdom. The other model, continental model of corporate governance is common in Continental Europe countries such as German, Japan and emerging Asian countries. It is mainly focused on the ideology of stakeholder theory and a relatively high concentration of ownership and control.

In order to have effectiveness of corporate governance in Sri Lankan listed firms, corporate governance practices were introduced in 1997, and were modified throughout the period till 2013. At present, corporate governance best practices in Sri Lankan listed firms are based on mandatory and voluntary rules which was extracted from Anglo-Saxon and continental models of corporate governance (Senaratne & Gunaratne, 2008). In 2003, Institute of Chartered Accountant of Sri Lanka and Securities Exchange Commission (SEC) jointly released voluntary codes of best practice for corporate governance. Then, all companies listed on Colombo Stock Exchange (CSE) were requested to follow the corporate governance practices as mandatory with effect from the financial year 1 April 2008.

The effectiveness of corporate governance practices of companies in Sri Lanka is debatable topic due to the variation between standard and actual practices of corporate governance (Dissabandara, 2012). Kalainathan and Vijayarani (2014) state that investors are having lack of confidence to make more investment in Sri Lanka as a result of investors’ protection index ranked as 52 out of 187 countries in 2013. Azeez (2015) states that investors are also having lack of confidence on the existence of the link between standard practices of corporate governance and its impact on firm performance in Sri Lanka. This raises a serious concern over the existing corporate governance practices on resolving agency problem in association with the best practices backed by agency theory.

Much corporate governance researches have focused on the US context (Kiel & Nicholson, 2003). Many research conducted on corporate governance practices and agency costs are based in Western countries (Elston & Goldberg, 2003; Fleming et al., 2005; Florackis, 2008; Garanina & Kaikova, 2016; Lei et al., 2013; McKnight & Weir, 2009; Mustapha & Ahmad, 2011; Singh & Davidson, 2003). Few researches have been carried out in Sri Lankan context on corporate governance and its impact on firm performance (Azeez, 2015; Dharmadasa et al., 2014), which are not directly addresses the agency costs, and no single research directly tackled on this interest. Garanina and Kaikova (2016) suggest that the primary research on corporate governance must focus on the corporate governance mechanisms that have direct influence on agency costs in association with agency theory rather than examining influence on firm performance. It is therefore important to consider the efficacy of corporate governance practices in association with agency theory, such as board diversity and agency costs. This research focuses on board diversity such as board size, separate leadership structure, proportionate of non-executive and/or independent director and mitigating agency costs in relation to agency theory and practices. This research will contribute to agency theory, and also provides framework for international policymakers who are having similar corporate governance practices in their own countries.

Research Questions

This research aims to address the following research questions:

Does board size influence on agency costs as proposed by agency theory? Does separate leadership structure influences agency costs as proposed by agency theory? Does proportion of non-executive and/or independent director has an influence on agency costs as proposed by agency theory?

Research Objectives

The research objectives of this study are to:

Examine the influence of companies’ board size on agency costs as proposed by agency theory? Investigate the influence of separate leadership structure on agency costs as proposed by agency theory? Examine the influence of proportion of non-executive and/or independent director on agency costs as proposed by agency theory?

Analysis of Literature and Development of Hypothesis

Introduction

The term ‘corporate governance’ refers to a structure in which businesses are directed and regulated (Cadbury Committee, 1992). Corporate governance is a mechanism and set of relationship between shareholders, board of directors, company management and other stakeholders aimed at serving the interests of company shareholders. Effective corporate governance is vital to attract investors, expand the growth of companies and to eliminate corporate scandal in order to create a healthy environment (The Institute of Chartered Accountants of Sri Lanka & Securities and Exchange Commission of Sri Lanka). Implementing best practice on corporate governance will lead to resolve conflict between the mangers and shareholders which direct to eliminate agency problem and thus to reduce agency costs of firm (Shaifali & Mittal, 2019).

According to Dissabandara (2012), corporate governance best practices affect agency costs as a result of separation of ownership and control. Corporate governance standards in certain areas are particularly important to balance the interest between company management and shareholders, and thus resolve agency problems. There are numbers of corporate governance mechanisms available in the companies such as board size, separate leadership structure and non-executive and/or independent directors which draw from agency theory.

Theoretical Perspectives of Corporate Governance

Agency theory was paid much more attention on many corporate governance-related researches (Berle & Means, 1932; Fama, 1980; Fama & Jensen, 1983; Jensen & Meckling, 1976). Agency theory proposes corporate governance best practices to resolve agency problem as result of ownership and control separation in companies which was also proposed by Fama (1980) and Jensen and Meckling (1976). They stated that corporate governance mechanisms address the issues related to ownership and control into agency problem. Agency problems are classified as the principal, agent and policy (Kiel & Nicholson, 2003; Zogning, 2017).

The agency theory related literature largely focuses on methods and systems on governing the organisation (Zogning, 2017). This leads to balance the interests of the principal and agent. Agency theory highlights the role of board of directors who are to govern the function of the board through monitoring the managers’ actions to maximise shareholders wealth through reducing agency costs to firms (Jensen & Meckling, 1976). As suggested by agency theory, board of directors should monitor the management activities who may involve in non-value adding activities which may not improve the value of firm which arise agency problems as well as agency costs (Jensen & Meckling, 1976).

Agency theory also proposes that the directors on boards should be consisting of largely of non-executive and/or independent directors to overcome agency problems (Fama & Jensen, 1983). The independent directors of board direct the firms to reduce agency costs as it enhances through monitoring the management action. The positions of chairman of board and chief executive officer (CEO) have to be separated in order to have effective operations of the companies (Fama & Jensen, 1983). The board of directors continuously monitor managerial actions on behalf of shareholders. It is suggested that the chairman of the board must be independent to management activities (Kiel & Nicholson, 2003). Agency theory predicts that CEO duality will not be an ideal corporate governance mechanism to achieve the interest of shareholders.

Corporate Governance Practices in Sri Lankan Context

In Sri Lanka, a code of best practice on corporate governance was adopted as a voluntary code of compliance. Later, it was modified as a mandatory compliance of corporate governance for companies listed in Sri Lanka. The first code of best practice on corporate governance was introduced in 1977 and was developed over a period of time. Later, minimum of corporate governance for mandatory compliance for companies was presented in 2008. The implementation of voluntary and mandatory code of compliance led the firms to enhance effectiveness of board and strengthen the company’s relationship with its stakeholders.

According to the 2013 corporate governance code of best practice, Section 1, Principle A.1 states that all listed companies in Sri Lanka should be governed by an effective board. The board should manage the companies’ activities to maximise shareholders’ wealth. The importance of separate leadership structure was identified in the 2013 code (Section 1, Principle A.2). The code also points out to separating the responsibility of the CEO and the chairman of the board. If it is to combine the posts of the CEO and the chairman as a single person, justification should be given in the company annual report.

The code emphasizes that the companies must balance executive and non-executive directors of company’s board (Section 1, Principle A.5). It further states that a company’s board of directors should have at least two non-executive directors or a number equal to one-third of the total number of directors, whichever is higher. The outside directors must contribute significantly in the board’s decision. Non-executive directors should represent majority of the board members when the chairman and CEO is represented as a single person (Section 1, Principle A.5.1).

The confidence of the investors widely depends on the rapid development of the financial markets. As a result of the government’s economic reform process, Sri Lanka’s economy expanded at an average rate of 4.79% in 2015 (Gunathilake et al., 2011). Rapid development of the capital market and economic reform process led the economy to perform better in South Asia with effective corporate governance systems which enhance the performance of the listed companies and thus increases the confidence of investors. Corporate governance practices in Sri Lanka have been improving with the expansion of business and the development of governance systems of listed companies to resolve conflict of interest.

The successful application of corporate governance practices is lacking in Sri Lanka due to ownership concentration issues. Ownership concentration raises serious concerns to the appointment of board of directors, such as executive and non-executive company’s directors, which challenges the protection of minority shareholders rights in Sri Lanka (Denis & McConnell, 2003). Extend of conflict of interest regulation index is weak in Sri Lanka, which shows that there is a need to protect investors in Sri Lanka (Kalainathan & Vijayarani, 2014). Dissabandara (2012) states that there is a lack of transparency in the board’s appointment which leads to ineffective corporate governance features in Sri Lanka. The standard practice of corporate governance is felt as essential elements to enhance the wealth of the shareholders which is lacking in Sri Lankan context. He further states that the variation between standard practice and actual practice of corporate governance in Sri Lanka is noteworthy (over all variation—56%; firm level variation—maximum 69% and minimum 39%; industry level variation—48%–61%). This study shows that the existence of agency problem in Sri Lankan listed companies. Further it explains that board of directors of companies in Sri Lanka are ineffective in monitoring and evaluating management actions and having the relationship with key stakeholders (Dissabandara, 2012).

Previous Research on Corporate Governance: Global Context

Corporate governance research has become a vital area in the recent past due to corporate scandals and firms’ failure (Karasneh & Bataineh, 2018; Mustapha & Ahmad, 2011). Much research on corporate governance was focused on the US context (Kiel & Nicholson, 2003). There was few research conducted on the European context to investigate the effectiveness of European board (Denis & McConnell, 2003). Among the corporate governance researches, many research findings associated with corporate governance practices and mitigating agency costs are based on Western countries (Elston & Goldberg, 2003; Fleming et al., 2005; Florackis, 2008; Garanina & Kaikova, 2016; Lei et al., 2013; McKnight & Weir, 2009; Mustapha & Ahmad, 2011; Singh & Davidson, 2003). But little research was carried out to measure the agency costs on the US context (Garanina & Kaikova, 2016; McKnight & Weir, 2009).

In Si Lanka, few corporate governance-related researches were conducted (Azeez, 2015; Dharmadasa et al., 2014). These researches are not directly address the issues related with agency costs and the application of agency theory on corporate governance practices in Sri Lanka. Garanina and Kaikova (2016) stated that the primary research on corporate governance must focus on the corporate governance practices that are having direct influence on agency costs rather than examining the influence on performance of companies. It seems that there is no single research directly tackles on this interest such as agency costs and the application of agency theory in developing countries such as Sri Lanka.

Garanina and Kaikova (2016) state that corporate governance mechanisms vary country to country such as United States, Norway and Russia depending on the economic, political and social context of those countries, and differs across companies and industries (Dharmadasa et al., 2014). The current corporate governance model for Sri Lankan companies is based on both mandatory and voluntary corporate governance compliance. It was developed in conjunction with the Anglo-Saxon and Continental corporate governance models, which are respectively based on agency theory and stakeholder theory (Senaratne & Gunaratne, 2008).

Directors of companies are considered as the most important element of corporate governance mechanisms. All companies in CSE should be governed by an effective company’s board which is responsible to manage the companies’ activities. Singh and Davidson (2003) stated that effective board and its size are most important in any governance systems to formulate strategic decision. Florackis (2008) suggests that effectiveness of a board depends on its size. From agency theory perspective, larger board tends to reduce agency costs, as a larger number of directors will be monitoring the actions of management of companies. Reddy and Locke (2014) argued that larger board tends to balance the right skills and expertise with smaller boards. Kiel and Nicholson (2003) state that board size of company is positively associated with market-based performance of firm. It is indeed requiring a larger board to have better management and enhance performance of the organisation (Nguyen et al., 2020). Therefore, the first null hypothesis of this study is:

H1: Board size of company does not influence agency costs.

The board of directors provide effective leadership to the company within the code of best practice on corporate governance which enables to reduce agency costs of firm. Cadbury Committee (1992) argued that the balance of power and authority will be ensured by separating the position of chairman and CEO of company which will enhance the power of decisions. Research findings indicate that separate role of CEO and chairman can lead to better performance and hence fewer agency costs (Florackis, 2008; Gul et al., 2012). On the other hand, CEO duality in UK firms does not influence on mitigating agency costs (McKnight & Weir, 2009). It is suggested that chairman of the board should be independent of corporate management (Kiel & Nicholson, 2003). Agency theory predicts that CEO duality will be against to fulfil the interest of the shareholders. Therefore, the second null hypothesis of this study is:

H2: Separate leadership structure does not influence agency costs.

As per the agency theory, the board should have higher number of outside directors who will bring information to the board and be able to provide important resources in creating and sustaining competitive advantage (McKnight & Weir, 2009). Non-executive and/or independent directors of appropriate calibre who contribute substantially to the board’s decision should be included on the company’s board. Non-executive directors on boards with a higher proportion are more effective at controlling management behaviour. They can restrict managerial opportunism, resulting in improved firm performance (Florackis, 2008; Garanina & Kaikova, 2016; Nguyen et al., 2020). Kiel and Nicholson (2003) state that the influence of non-executive directors on agency costs is statistically significant. Therefore, the third null hypothesis of this study is:

H3: Higher proportionate of non-executive and/or independent director does not influence agency costs.

Data Source and Methodology

Conceptual Framework

The conceptual framework demonstrates the relationship that is used in this study between theoretical perspective, corporate governance variables and agency costs. Empirical findings from different studies showed that the relationship between corporate governance mechanism (board diversity) and agency costs are influenced by many corporate governance variables. In the previous section, the relationship between board composition and agency costs, as proposed by agency theory, is discussed. The conceptual model involves internal variables of corporate governance, such as the board diversity, which are considered essential in mitigating the agency costs. Board size, separate leadership structure and proportion of non-executive board directors are part of board diversity referred to in this study. The agency costs measured in this study are the ratio of assets utilisation and selling, general and administrative expenses (SG&A) to sales ratio (Chilosi & Damiani, 2007; Tchouassi & Nosseyamba, 2011).

Variables Measurement

This section describes the operationalisation of the variables. In order to test the influence of board size, this study includes the variable, that is, total number of directors on boards (Florackis, 2008; Garanina & Kaikova, 2016; Gul et al., 2012; Kiel and Nicholson, 2003; Premepeh & Odartei-Mills, 2015; Reddy & Locke, 2014).

Corporate governance research related to leadership structure widely used dummy variables to operationalise the board leadership structure (Donaldson & Davis, 1991; Florackis, 2008; Gul et al., 2012; McKnight & Weir, 2009; Reddy & Locke, 2014). Therefore, dummy variables for the separate leadership structure will be used in this study. If the position of chairman and CEO is appointed by one person, it will be known as combined management and will be coded ‘0’. If two separate persons hold the positions, it will be known as separate management and will be coded ‘1’.

The number of non-executive and/or independent directors on board divided by the total number of directors of company will be used in this study (Florackis, 2008; Gul et al., 2012; Kiel & Nicholson, 2003; McKnight & Weir, 2009; Premepeh & Odartei-Mills, 2015). Leverage is considered as controlling mechanism in this study which may be associated with agency costs. The ratio of total debt to total assets is calculated as leverage of company (Florackis, 2008; Garania & Kaikova, 2016; McKnight & Weir, 2009; Premepeh & Odartei-Mills, 2015; Singh & Davidson, 2003). Firm size can be considered by taking book value of total assets of the firm (Florackis, 2008; Premepeh & Odartei-Mills, 2015; Singh & Davidson, 2003).

As far as agency costs concern, the previous research on corporate governance practices has used the assets to sales ratio (Fleming et al., 2005; Florackis, 2008; Garanina & Kaikova, 2016; Gul et al., 2012; Karasneh & Bataineh, 2018; McKnight & Weir, 2009; Reddy & Lock, 2014; Singh & Davidson, 2003) and assets liquidity ratio (Garanina & Kaikova, 2016; Henry, 2006; Siddiqui et al., 2013) as a measurement for agency costs. In addition, SG&A to sales ratio has also been used as proxy for measuring agency costs (Fleming et al., 2005; Florackis, 2008; Florackis & Ozkan, 2004; Reddy and Locke, 2014; Singh & Davidson, 2003).

Population and Sample

Sample of this research consists of all listed companies on CSE in Sri Lanka, with the exception of companies with specific ownership and different governance structures, such as banks and financial institutions. The research period consists of the last seven years, from 2013 to 2019. The final sample is made up of 180 companies. The reason for the selection of the said period was that corporate governance principles which were adopted in 2003 and that, four years later, in 2007, the corporate governance code has to be extended to companies reporting on or after 1 April 2008. Later, in 2013, code of best practice on corporate governance was updated and reviewed. In the meantime, corporate governance practices of Sri Lankan companies were criticised by many researchers during the period 2009–2015 (Dissabandara, 2012; Kalainathan & Vijayarani, 2014; Senarate & Guneratne, 2008). For this reason, the 2013–2019 period was a significant period to evaluate the efficacy of the board diversity in terms of mitigating agency costs as proposed by agency theory.

Method of Analysis and Model Estimation

Data collected for this research were from the sources of CSE website and audited annual reports of listed companies in Sri Lanka. From the annual report, which published data on all financial details relating to the performance and financial position of the organisation, data on the board structure and agency costs were extracted. Details relating to corporate governance practices, board composition, were also extracted from the annual report.

The EViews 9 statistical software was employed to evaluate the relationship in the hypotheses described in the conceptual framework. Descriptive statistics, Spearman’s correlation, stationary test, auto correlation, multicollinearity, tests of heterogeneity and multiple regression analysis were included in the analysis. The data set of this analysis will be known as a panel of data. It consists of information from both time series and cross-sectional components. Baltagi and Levin (1986) suggest that the particular benefit of panel data allows a large number of data accessible and encourages further prediction accuracy. To analyse panel data, there are different econometric models/estimation techniques available. Generally, they are empirically validated models of pool ordinary least squares regression, Fama–Mac Beth regression model, panel regression fixed effect (FE)/random effect (RE) and dynamic panel regression model. FE/RE panel regression model was the subject of this analysis.

Models 1 and 2 (Agency Costs and Board Structure)

Fixed Effect

Random Effect

where agency costit is the dependent variable of the study, it represents ratio of asset utilisation or SG&A to sales ratio for firm i at period t as alternative estimation.

Validity and Reliability of Data

Secondary data have been the data base of this analysis. The data were collected from the audited annual report of the company and the handbook issued by the CSE. As the data have been audited and the publication has been carried out by listed companies, the data are highly credible and accurate.

Empirical Findings and Discussion

Descriptive Statistics

Summary of Descriptive Statistics.

The mean value for assets to sales ratio was 0.876, and the range for this variable is from 5.350 to 0.000. SG&A is being recorded a mean value of 0.316, with maximum value 28.460 and minimum value 0.000. The standard deviation of both dependent variables is having greater variation. Mean value of assets to sales ratio is less than 1, which indicates the firms’ in-ability to manage its resources to generate sales. The mean value for board size of Sri Lanka companies is 8. The range of the companies’ board size is from 2 to 15. The average companies’ board size listed in Sri Lanka is based on the suggestion by Jensen (1993). Descriptive statistics of the separate leadership structure reports that 96.8% of the companies listed in Sri Lanka separate the position of management as proposed by agency theory. It is noted that less than 3% of companies in Sri Lanka are having CEO duality of the board. The average of non-executive directors’ representation on board is 42.6%, which is closer to the recommendation of code of best practices issued in 2013. On the other side, agency theory proposes that a board must consist of majority of non-executive and/or independent directors on board to monitor the management actions. Maximum percentage of leverage on total assets is 87.3%, which shows that the existence of highly levered companies in Sri Lanka. The average value for log of total assets is 21.681, which indicates the enhanced investors’ confidence in companies in the sample.

Spearman’s Correlation Analysis

Spearman’s Correlation Analysis.

Board size of companies is positively correlated with assets to sales ratio and negatively correlated with SG&A, which is reported as weak correlation. The other board diversity-related variables such as non-executive directors on board are positively correlated with SG&A and then negatively correlated to assets to sales ratio. The association between these variables is also reported as weak.

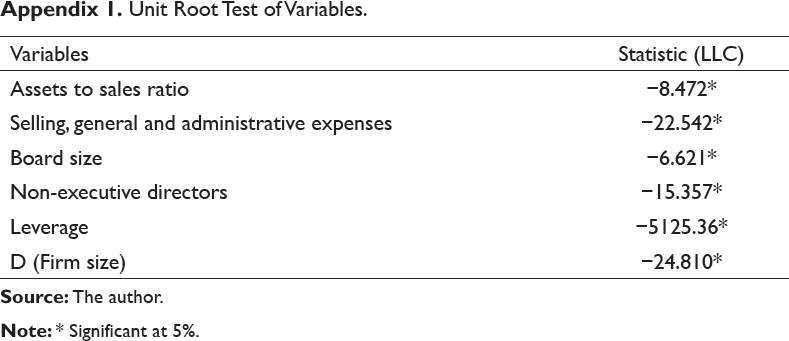

The stationary of data set can be evaluated by using scrutiny of the time series for a unit root. The test proposed by Levin et al. (2002) was used to test the stationary data in this research. Appendix 1 summarizes the unit root test of variables and the statistics Levin, Lin, Chu (LLC) along with the probability value. It can be inferred, based on the results, that the null of a unit root is rejected for all variables. The LLC model has confirmed that the variables are stationary at a 5% significance level.

Regression Analysis

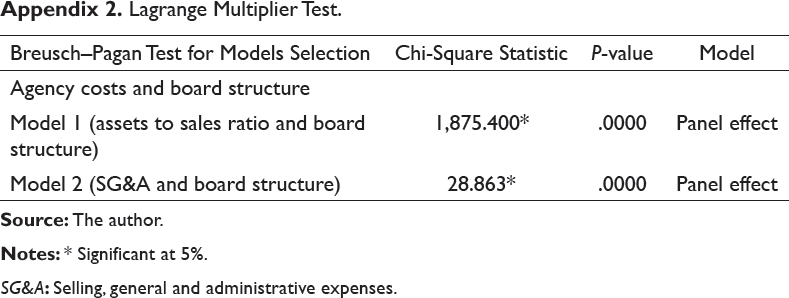

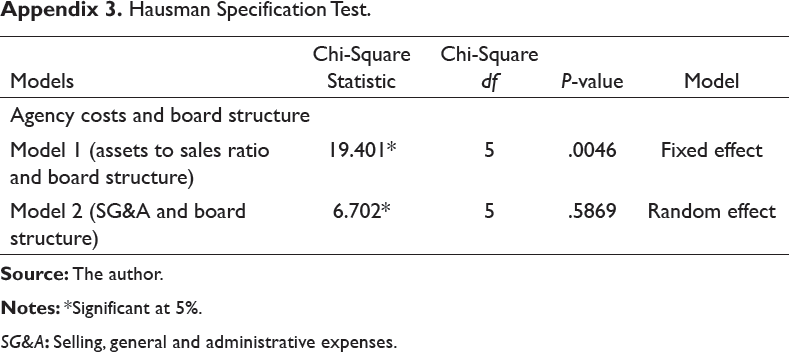

Appendix 2 summarizes Breusch–Pagan Lagrange multiplier statistical test results for Models 1 and 2 to determine whether the data contains panel effect or not. The chi-square statistics for both models are very high and statistically significant (p < 0.05) at 5% level. Therefore, the models 1 & 2 are considered as panel effect. Hausman (1978) test was performed to select the relevant model whether the models are FE or RE. Appendix 3 shows the Hausman Specification Test results. According to the results, Model 1 is preferred by FE, and then Model 2 is preferred by RE.

Breusch–Pagan Lagrange multiplier test was performed for the appropriateness of the ordinary least square regression model. It is chosen as panel regression effect. The overall F-test of Models 1 and 2 are 45.298 and 4.425 significant at 0.0000 and 0.0025 (5% level). The p-value for the overall F-test is less than 5% significant level (p = 0.00 < 0.05). Therefore, it concludes that Models 1 and 2 provide better fit with the data. R-square in the regression Model 1 shows the 92.58% of the effect from selected variables while the regression Model 2 accounts only for 4.21% of the effect in agency costs, respectively.

Durbin Watson statistics is used to test the autocorrelation in the residual from Models 1 and 2. The statistics accounts for 1.5237 for Model 1 and 2.4287 for Model 2. It shows that there is no cause for autocorrelation. The variance inflation factors statistics for Model 1 is accounted for 7.671 and Model 2 is 2.032. The result of variance inflation factor reveals that there is no existence of multicollinearity between the independent variables in the regression models. Wald-test determines the joint significant of independent variables in the regression model. In addition, chi-square value of Wald test results reveals that determinants used in this study can be considered. Appendix 4 shows the results of heterogeneity of residual. Breusch–Pagan–Godfrey test shows that theta (2.76) is less than chi-square test statistics of 13.16 degree of freedom (5d.f) for Model 1 and the theta for Model 2 is 2.81 less than chi-square test statistics of 13.16 (5d.f), which proves that there is no heteroscedastic problem in the regression model.

Results and Discussion of the Study

Board Size and Its Influence on Agency Costs

Mixed results were reported from the results of the panel regression analysis between board size and costs of agency of companies listed in Sri Lanka. The positive relationship between board size and assets to sales ratio is shown in Table 3. This implies that larger boards are associated with a higher ratio of assets utilisation and thus lower agency costs in the companies. A negative relationship is recorded between the size of the board and SG&A in the second model. It implies that larger boards are associated to lower agency costs. However, relationship of both models is not significant with coefficient 0.0209 (p = 0.2526 > 0.05) for Model 1, and then with coefficient −0.1290 (p = 0.0843 > 0.05) for Model 2. Therefore, do not reject the null hypothesis. since both models are having insignificant relationship. It can be concluded that board size has insignificant influence on agency costs of companies listed in Sri Lanka.

Previous researches on best practices of corporate governance mainly suggested the effectiveness of companies’ board of directors to monitor the management actions to maximise shareholders wealth to resolve the agency problem. Jensen and Meckling (1976) stated that the responsibility of directors on board is to govern function of board of companies through effectively monitoring the management actions to enhance wealth of the shareholders. In order to maintain the board’s effectiveness, board of directors is responsible to implement corporate governance guidelines to achieve the corporate objectives. Agency theory also highlights the way to make the board as effective in companies to resolve agency problem.

The result of this study based on Sri Lankan context reveals that board size does not influence on agency costs. The finding is consistent to prior research that board size is not significant to agency costs (Singh & Davidson, 2003). The reason for the insignificant relationship is that the board of the companies is headed mainly as a legal fiction which are highly dominated by management. The influence of management on board affairs makes ineffective in mitigating agency costs due to inability of the board to harmonise agency problems, and failure to safeguard corporate assets (Kalainathan & Vijayarani, 2014). On the other hand, the result is inconsistent to agency theory concept which argue that larger board would be effective to achieve the objectives of companies. Kiel and Nicholson (2003) argue that larger boards would be effective to monitor management action and then to resolve agency problems. They argued in favour to the larger board and its influence on agency costs.

Separate Leadership Structure and Its Influence on Agency Costs

The findings in Table 3 show a negative relationship between the separate leadership and assets to sales ratio. This suggests that separate leadership structure is related to lower assets utilisation level of company and therefore higher agency costs in firms. Hence, the relationship was significant with coefficient −0.3123 (p = 0.0379 < 0.05) for Model 1. As for Model 2, a positive relationship between the separate leadership and SG&A is stated. It implies that separating the position of CEO and chairman of board is associated with higher costs of agency which is statistically insignificant with coefficient 0.1834 (p = 0.6418 > 0.05). Therefore, based on the findings in Model 1, null hypothesis (H2) is rejected. It is to accept the alternative hypothesis. It can be concluded that separate leadership structure has significant positive influence on agency costs of companies listed in Sri Lanka.

The findings of the study reveal that separate leadership structure leads to inefficient management of assets which leads to higher agency costs of companies. The results of this study are not supported by prior research (Cadbury Committee, 1992; Florackis, 2008; Gul et al., 2012). Florackis (2008) stated that having two offices for CEO and the chairman can lead to reduce agency conflict. Similar argument from Gul et al. (2012) stated that separate leadership structure is associated to mitigating agency costs. The findings are also against to the view from agency theory perspective which proposes separating the position of CEO and the chairman of the board to resolve agency problem. If the CEO retains the dual position of chair, it is expected that the needs of the owners will not be achieved. Kiel and Nicholson (2003) also state that agency theory enhances the companies to separate the position for effectiveness to monitor the management action.

However, separating the leadership structure causes higher agency costs is due to the higher management costs, weak in managing assets, and weak in leadership (Dissabandara, 2012). Majority of shareholders influences the appointment of board of directors and the CEO to nominate their representatives to the board which dominate the board decision-making (Denis & McConnell, 2003). This enhances the managers to pursue managerial opportunisms at the interest of shareholders (Gunathilake et al., 2011). This implies that separate leadership structure does not fit to the company due to the inability of the chairman to formulate proper strategies to the companies.

Non-executive and/or Independent Directors on Boards and Its Influence on Agency Costs

A negative relationship is stated between the proportion of non-executive board directors and the asset to sales ratio. This means that a higher proportion of on-board non-executive directors is correlated with a lower assets utilisation ratio and therefore contributes to higher agency costs in companies. But, the relationship with a coefficient of −0.2401 (p = 0.1871 > 0.05) for Model 1 was not statistically significant. As for the second model, a positive relationship is reported between the proportion of non-executive board directors and SG&A. This means that higher proportion of non-executive board directors is correlated with higher agency costs, which is statistically significant with coefficient of 0.4611 (p = 0.0309 < 0.05). Based on the findings on modes l and 2, the third null hypothesis (H3) is rejected, and then alternative hypothesis of this study is accepted. It can be concluded that the higher percentage of non-executive board directors has a statistically significant positive impact on agency costs for companies listed in Sri Lanka.

Summary of Regression Analysis.

SE: Standard error, SG&A: Selling, general and administrative expenses, VIF: Variance inflation factors.

Agency theory highlights that majority of non-executive directors on board would overcome the agency problem and then reduce agency costs (Fama & Jensen, 1983). The result of this study is inconsistent to the theoretical expectation (agency theory) and also to the previous research (Garanina & Kaikova, 2016; Gul et al., 2012; Kiel & Nicholson, 2003; Nguyen et al., 2020; Reddy & Locke, 2014; Roudaki & Bhuiyan, 2015). Gul et al. (2012) state that the lower percentage of non-executive board directors has lower costs of agency. Reddy and Locke (2014) reported that higher the percentage of non-executive board directors is negatively correlated to agency costs.

Conclusion

This study investigated how board diversity influences agency costs, as it is highlighted by agency theory. Agency theory highlights the way to set corporate governance mechanisms to resolve the conflict of interest and the way to reduce agency costs. Corporate governance best practices were introduced in 1977 in Sri Lankan companies and then has been developed throughout the period till 2013. This was led the companies to have effective governance practices and monitoring the managerial activities to fulfil shareholders’ interest. Even though the stock market has been performing well, many corporate failures and scandals in Sri Lanka reveal the inability of the board functions and weak leadership structure in dealing the business affairs effectively and efficiently. It is also noted that the existing corporate governance best practices in Sri Lankan companies are not meeting the standard.

The results show that the board size does not influences agency costs. The findings indicate that board size was not an effective corporate governance mechanism to resolve agency problems. Results in relation to the separate leadership structure and agency costs were statistically significant and positively correlated on agency costs based on measures assets to sales ratio. The finding indicates that the agency costs increase when the position of CEO and the chairman of the board are separated. It reveals that the board leadership structure is weak at monitoring and evaluating of management action. Regression analysis shows that non-executive directors’ representation on board has significant influence on agency costs such as positive relationship reported based on the measures SG&A. The results reveal that higher proportionate of non-executive directors’ representation on board tends to increase agency costs.

Based on agency costs measures used in this study, the findings show that the board diversity-related variables such as separate leadership structure and presence of non-executive directors on board are appeared to significantly influence agency costs, and thus it increases costs of agency. The results of this research are unlikely to theoretical prediction (agency theory) in which it expects that corporate governance mechanisms tends to reduce agency costs. In addition to above, board size does not have direct impact on agency costs. The potential benefits of this study led to re-think the board of directors, managers, shareholders and policymakers to re-organise the implementation of corporate governance best practices.

This study has not covered other corporate governance mechanisms, included in the code of best practices issued by Chartered Accountant of Sri Lanka and Securities Exchange Commission such as women on boards, interlocking directorship, ownership structure, sustainability reporting, directors’ remuneration, accountability and audit committee, as these are not proposed by agency theory. This can be extended to future research by adding more variables to examine the effectiveness of corporate governance best practices in companies in Sri Lanka.

Appendices

Unit Root Test of Variables.

Lagrange Multiplier Test.

SG&A: Selling, general and administrative expenses.

Hausman Specification Test.

SG&A: Selling, general and administrative expenses.

Results of Heterogeneity.

SG&A: Selling, general and administrative expenses.

Footnotes

Declaration of Conflicting Interests

Funding

The author received no financial support for the research, authorship and/or publication of this article.