Abstract

This article studies the effects of macroeconomic news announcements and order flow on exchange rates in Pakistan by considering both direct and indirect information channels during news announcements periods. For this purpose, it employs GARCH models by using real-time data on macroeconomic news, order flow, and exchange rates. The findings reveal that macroeconomic news directly, and indirectly affect Pak Rupee exchange rates. The results also show that the order flow drives fluctuations in Pak Rupee exchange rates indicating the role of trade signals and trading strategies of currency traders in the exchange rate determination. Hence, as part of an aggregated economic component and means of public and private information, macroeconomic news and order flow impact Pak Rupee exchange rates as an integrated determinant. When macroeconomic news strikes the foreign exchange market, it affects the decisions of market makers, influencing order flow, and then exchange rates.

Introduction

The exchange rate determination is a leading issue in international economics. In the early 1980s, numerous researchers developed new models of foreign exchange rates incorporating the role of information in analyzing the behavior of foreign exchange rates (Almeida et al., 1998; Andersen et al., 2003; Evans & Lyons, 2002a, 2002b; Glosten & Milgrom, 1985; Goodhart et al., 1993; Kyle, 1985). The macro-information-based models of exchange rates consider the role of macroeconomic news announcements in explaining exchange rate movements. Under the assumptions of rational expectations and efficient markets, these models state that the macroeconomic news announcements directly and immediately incorporate public information into exchange rates (Almeida et al., 1998; Andersen et al., 2003). These models show that the effects of macroeconomic news announcements on exchange rates are common knowledge and trading, which convey no private information that affects exchange rates. On the other hand, the micro-information-based models of exchange rates consider the role of trading in explaining exchange rate movements. These models state that order flow incorporates private information into exchange rates (Glosten & Milgrom, 1985; Kyle, 1985). These models show that the effects of trading are not common knowledge and trading conveys private information, which affects exchange rates. The hybrid-information-based models of exchange rates consider the information-aggregation role of order flow linking macroeconomic fundamentals and exchange rates (Evans & Lyons, 2002a). These models state that order flow induces the private portfolio shift effects on exchange rates that are unrelated to macroeconomic information.

A considerable amount of research has focused on the relative significance of the direct and indirect information channels during and after news announcement periods. If macroeconomic news announcements contain common knowledge information, then the direct channel accounts for most of the exchange rate movements and has the same effects on exchange rates. Conversely, if macroeconomic news announcements contain dispersed information, then the indirect channel dominates and has different effects on exchange rates. Therefore, several existing empirical studies have analyzed the direct and indirect effects of macroeconomic news announcements on exchange rates, respectively (Evans & Lyons, 2008; Savaser, 2011).

One strand of studies find that macroeconomic news announcements directly and immediately incorporate public information into exchange rates (Almeida et al., 1998; Andersen et al., 2003; Ben Omrane et al., 2020; Boudt et al., 2019; Gau & Wu, 2017; May et al., 2018). These studies find that only common knowledge macroeconomic information matters and there are rational and homogeneous market participants, interpreting public information identically and thus, uniformly calculate changes in exchange rates. In contrast, other studies find that macroeconomic news announcements indirectly incorporate dispersed information into exchange rates via order flow (Evans & Lyons, 2005, 2008; Galati & Ho, 2003; Love & Payne, 2008; Savaser, 2011; Zhang et al., 2016). These studies find that macroeconomic news releases public information creating order flow that reveals private information and incorporate dispersed information into exchange rates. Hence, the trading conveys dispersed information that affects exchange rates. These studies integrate public macroeconomic information, agents’ heterogeneous information, and dispersed information which induces market participants to revise their expectations, resulting in changes in exchange rates.

Most of the published literature on information-based models of exchange rate determination consider developed economies foreign exchange markets to investigate the link between macroeconomic news announcements, order flow, and exchange rates (Evans & Lyons, 2005, 2008; Galati & Ho, 2003; Love & Payne, 2008; Savaser, 2011; Zhang et al., 2016). However, the effects of macroeconomic news announcements on exchange rate dynamics and the role of order flow in formulating these effects for emerging economies such as Pakistan are still unexplored in the literature. Yet, there is a dire need to investigate whether these models also hold for the foreign exchange market of emerging economies as most of these are characterized by market inefficiencies and illiquidity. Further, there is a vital need to explore the effects on exchange rates if the information is revealed to all market participants publicly and simultaneously and if the information is dispersed between heterogeneous market participants in an integrated framework. There is also a need to explore the direction in which similar macroeconomic news announcements impact the different exchange rates of the underlying currency. Additionally, there is need to identify the mechanisms that are related to the exchange rate determination, as well as the mechanisms that dominate and determine the sign of the response of exchange rate to the news.

It is essential to examine whether trading signals and trading strategies of currency traders affect exchange rates and whether releases of foreign and domestic macroeconomic news trigger trading, which reveals dispersed information affecting the exchange rates indirectly during announcements periods. Understanding and explaining the exchange rate behavior by order flow and macroeconomic news announcements are very important for trade analysis and decision making by market participants like traders, investors, money managers, and corporate firms and for designing and evaluating policies by policymakers.

This article covers these gaps by investigating the effects of macroeconomic news announcements and order flow on Pak Rupee exchange rates. Specifically, it analyzes both direct and indirect information channels during news announcement periods affecting Pak Rupee exchange rates. It also investigates the role of order flow in driving movements in Pak Rupee exchange rates, which are unrelated to macroeconomic information. The article significantly contributes to the literature by exploring the mechanisms through which macroeconomic news affects exchange rates.

In this article, the subsequent section presents the literature review and the model specification. This is followed by the data description and the empirical findings, and finally the conclusion is presented.

Literature Review

On the one hand, a considerable amount of empirical literature explores the direct effects of macroeconomic news announcements on foreign exchange rates. The main finding of these studies indicates that under market efficiency and rational expectations, announcements of macroeconomic news have a direct and immediate effect on the exchange rates. These studies conclude that the exchange rates react significantly to the surprise component of macroeconomic announcements. For example, Andersen et al. (2003) examine the reaction of exchange rate returns and their volatility to macroeconomic news. They show that average effects from macroeconomic news announcements are incorporated in exchange rates immediately. They also find that exchange rates quickly adjust to scheduled macroeconomic news whereas their volatilities adjust gradually to the news. Following Andersen et al. (2003), several empirical studies show the direct and immediate macroeconomic news announcement effects on exchange rate returns and their volatilities. These studies analyze exchange rate reactions to foreign and domestic macroeconomic news announcements (Ben Omrane et al., 2020; Ehrmann & Fratzscher, 2005; Fatum et al., 2012; Gau & Wu, 2017; Omrane & Hafner, 2015; Omrane & Savaşer, 2017; Pearce & Solakoglu, 2007). Most of these studies focus on news announcements such as US news, UK news, Euro Area news, Australian news, German news, Canadian news, and Japanese news. They examine news effects on foreign exchange rates of developed economies (the United States, the United Kingdom, Germany, Japan, Canada, and Australia). However, a few studies examine the direct effect of news on the exchange rates in in emerging markets (Boudt et al., 2019; Cai et al., 2008; Caporale et al., 2018; Wong et al., 2014).

While on the other hand, a considerable amount of empirical literature on microstructure explores the effects of macroeconomic fundamentals and order flow on foreign exchange rates. The main finding of these studies show that the order flow (trading flows) incorporate private information into exchange rates. They consider order flow as a proximate determinant of exchange rates that is unrelated to macroeconomic information. Evans and Lyons (2002a) find exchange rate movements are triggered by the order flow through private portfolio shifts that are unrelated to macroeconomic information. The order flow brings portfolio-balance effects on exchange rates. Following Evans and Lyons (2002a), several studies such as Chinn and Moore (2011), Duffuor et al. (2012), Breedon and Ranaldo (2013), Zhang et al. (2016), McIntyre and Harjes (2016), and Anifowose et al. (2018) estimate foreign exchange microstructure models and find that the order flow sufficiently explains movement in the exchange rates.

Several studies in the literature document direct and indirect channels that affect exchange rates through news releases (Evans & Lyons, 2008; Love & Payne, 2008; Savaser, 2011; Zhang et al., 2016). They explore the impact of macroeconomic news announcements through the order flow on foreign exchange rates. They argue that order flow is the medium through which macroeconomic information is impounded into exchange rates. Their main findings indicate that the release of macroeconomic news creates trading that reveals private information, which is dispersed between market agents and in turn affects exchange rates. Evans and Lyons (2005) and Love and Payne (2008) show that if the information is released publicly and simultaneously to all market agents, then it is effectively impounded directly and indirectly through order flow into the exchange rates. They find the reaction of exchange rates to announcements of macroeconomic news mediated by order flow. Evans and Lyons (2005) describe the average news effect as the direct effect of announcements of macroeconomic news on exchange rates and the total news effect as the sum of the direct effect and the indirect effect of announcements of macroeconomic news. They conclude that the total news effect on exchange rates must include the immediate reaction to new as well as reaction to trades.

Evans and Lyons (2008) show that when a macroeconomic news release is viewed by heterogeneous agents, it has different effects on exchange rates. Although the same announcement is observed by all, different views about macroeconomic news announcements affect exchange rates via order flow and represent dispersed information. When macroeconomic news strikes the foreign exchange market, it affects the decisions of market makers, influencing order flow, and then exchange rates. This indicates the interaction between order flow and macroeconomic news. Savaser (2011) and Zhang et al. (2016) examined the direct effects of macroeconomic news and order flow on exchange rates and the indirect effects of macroeconomic news via order flow. Their results reveal that real-time public and private information significantly affect exchange rates. However, Zhang et al. (2016) finds no interaction of order flow and macroeconomic news in the information transmission process. Savaser (2011) finds order flow intensifies macroeconomic news effects on exchange rates. Carlson and Lo (2006) and Gradojevic and Neely (2009) found a significant reaction of exchange rates to news announcements with trading. However, these studies on the direct and indirect effects of macroeconomic news examine the exchange rate dynamics of developed economies only.

Several studies in the literature examine the effect of information on exchange rate volatility, both macroeconomic news and private information (Bauwens et al., 2005; Berger et al., 2009; Cai et al., 2001; Carlson & Lo, 2006; Evans & Lyons, 2008; Frömmel et al., 2008; Zhang et al., 2016). Their results reveal that real-time macroeconomic news and private information from market makers significantly affect exchange rate volatility.

This article is distinct from previous studies in several aspects. First, it modifies the information-based models for modeling exchange rates in the emerging economy such as Pakistan by incorporating the dynamics of the emerging foreign exchange market. Second, it analyzes the direct and indirect effects of macroeconomic news announcements on Pak Rupee exchange rates. Third, it investigates the role of order flow in driving movements in Pak Rupee exchange rates that are unrelated to macroeconomic information. Fourth, it explores the nonlinear relationship between macroeconomic news and order flow through interaction between macroeconomic news and order flow which affects exchange rates. Last, instead of pooling all news announcements, it analyzes the individual effect of each different type of announcement with a longer sample period. These aspects of the article make significant contributions to the literature.

Model Specifications

This article examines the effects of macroeconomic news announcements and order flow on exchange rate returns and exchange rate volatility of the Pak Rupee using autoregressive moving average (ARMA) with univariate generalized autoregressive conditional heteroscedasticity (GARCH) models. 1 It is well-known that ARMA-GARCH models can capture the exchange rate dynamics known as stylized facts. They are skewness, fat tails, and volatility clustering. Moreover, “GARCH models increase estimation efficiency by modelling volatility clustering and providing explicit estimates of the parameters describing the time-varying nature of the conditional variance” (Engle, 1982). Therefore, several studies employed GARCH models to study the news effects on exchange rates for different countries (Hayo & Neuenkirch, 2012, 2013; May et al., 2018; Omrane & Hafner, 2015).

Macroeconomic News Announcements and Order Flow Effect on Exchange Rate Returns and Exchange Rate Volatility

According to Evans and Lyons (2002a), order flow conveys private information which is unrelated to macroeconomic news announcement effects on exchange rates. Order flow is the proximate determinant of exchange rates. It takes the form of private portfolio shifts that induce a portfolio-balance effect on exchange rates. Exchange rates reflect all publicly available macroeconomic information and private information. Therefore, the effects of macroeconomic news announcements and order flow on exchange rate returns and exchange rate volatility of the Pak Rupee are examined by following the model developed by Evans and Lyons (2002a).

To study the contemporaneous effects of news of each of macroeconomic indicator and order flow on exchange rate returns and exchange rate volatility during announcement periods, ARMA (p, q) – GARCH (p, q) model is specified as follows:

Where r i,t is each Pak Rupee exchange rate returns i at time t, h i,t is Pak Rupee exchange rate volatility, N i,k,t refers to the standardized macroeconomic news announcement (macroeconomics announcement surprise) k (k = 1, … , n) at time t, and z i,t refers to order flow at time t. The θ i,t measures the exchange rate returns reaction to the macroeconomic news announcement N i,k,t and ϑ i,k measures the exchange rate volatility reaction to the absolute macroeconomic news announcement. The Ψ i measures the exchange rate returns reaction to order flow z i,k and Ω i measures the exchange rate volatility reaction to the absolute order flow z i,t .

Macroeconomic News Announcement Indirect Effects via Order Flow on Exchange Rate Returns and Exchange Rate Volatility

According to Evans and Lyons (2008), when a macroeconomic news announcement is viewed by heterogeneous agents, it has different effects on exchange rates. Although everyone observes the same announcement, different views about macroeconomic news announcements affect exchange rates via order flow and represent dispersed information. When macroeconomic news hits the foreign exchange market, it influences market makers’ decisions, which in turn affects order flow and then exchange rates. This indicates the interaction between macroeconomic news and order flow. Therefore, the effects of macroeconomic news on exchange rates can be examined through both the direct channel and indirect channel, via the order flow. The indirect effects of macroeconomic news announcements via order flow on exchange rate returns and exchange rate volatility of the Pak Rupee are examined by following the model developed by Evans and Lyons (2008).

To test the contemporaneous effects of news of each of macroeconomic indicator through order flow exchange rate returns and exchange rate volatility during announcement periods, ARMA (p, q) – GARCH (p, q) model is specified as follows:

Where Φ i,k measures the exchange rate returns reaction to the macroeconomic news announcement N i,k,t via order flow and ψ i,k measures the exchange rate volatility reaction to the absolute macroeconomic news announcement N i,k,t via order flow.

For the estimation of GARCH models, the maximum-likelihood (MLE) method is used. The Gaussian conditional distribution is followed by residual term.

Data Description

Variables Definitions, Construction, and Sources

Exchange Rates

This article uses daily Pak Rupee exchange rate data to investigate the effects of macroeconomic news announcements on exchange rates. The daily Pak Rupee exchange rate data were collected from January 2008 to December 2018, obtained from the State Bank of Pakistan. Moreover, it takes nominal exchange rate of the Pak Rupee relative to the US dollar, UK pound, Japanese yen, and Euro quoted as domestic currency per unit of foreign currency. The exchange rate returns are the first logarithmic difference of exchange rates of successive periods as the continuously compounded returns.

Scheduled Macroeconomic News Announcements

In this article, the real-time data on announcements of important macroeconomic indicators reflecting real-time information for the United States (US), the United Kingdom(UK), Euro Zone (EZ), Japan (JP), and Pakistan (PAk), and their market expectations based on survey data were used. The monthly data on real-time reporting of released macroeconomic indicators and their forecasts from January 2008 to December 2018 were used. The monthly data of released macroeconomic indicators and their forecasts were obtained from the investing.com database. Further, this article selects those macroeconomic indicators that are available with their actual release as well as forecast and widely used in literature. It selects a time period base on the availability of market expectation data (forecasts).

The macroeconomic news announcements are standardized to compare the coefficients of macroeconomic news announcements with different units of measurement, by taking the difference of forecasts from the released and dividing them by the sample standard deviation of the difference (difference of its released and forecast values). The standardized macroeconomic news announcements are “close to zero mean and have a unit standard deviation” (Andersen et al., 2003).

For empirical analysis, the announcement of each news is added at every point of each exchange rate series. Therefore, for estimation, those observations (r t , N k , t) are considered where an announcement was made at time t (Almeida et al., 1998; Andersen et al., 2003).

Order Flow

“Order flow is a measure of buying/selling pressure. It is the net of buyer-initiated orders and seller-initiated orders” (Evans & Lyons, 2002a, 2002b, 2005, 2008). The order flows are signed trades between dealers of foreign exchange cumulated over time. Trades are signed depending on whether the initiator sells or buys. A purchase (sale) of 1 unit of a currency initiated by a trader on a dealer’s quote, order flow is 1(−1). Evans and Lyons (2002a, 2002b) measure order flow as “the difference between the number of buyer-initiated and seller-initiated trades.” They take a number of transactions/trades (buying and selling) for measuring order flow. This study uses the daily data of foreign exchange transactions of Pak Rupee between dealers in terms of traded contracts from January 2008 to December 2018. The data were obtained from the barchart.com database. This study follows the convention of signing a trade using the direction of the market order. For every trade executed, “the data set contains a time-stamped record of the transaction price and a bought/sold indicator. The bought/sold indicator allows to sign trades for measuring order flow” (Evans & Lyons, 2002a, 2002b).

Descriptive Summary

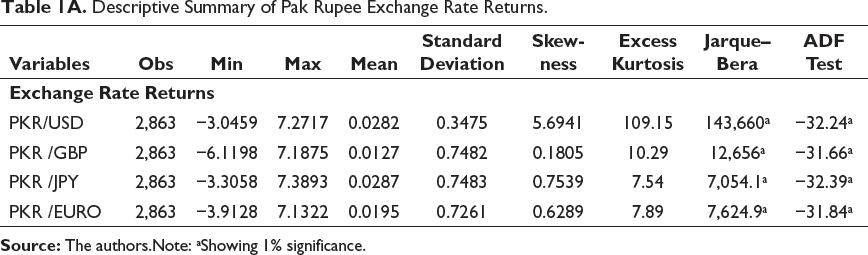

Table 1A presents summary statistics of daily exchange rate returns of the Pak Rupee. The daily exchange returns means are positive, indicating exchange rates increase over time. This implies Pak Rupee depreciates against foreign currencies over time. The standard deviation of daily exchange returns exhibits a similar degree of volatility. Positive skewness and excess kurtosis in exchange rate returns indicate heavy-tailed and leptokurtic distribution. The significant Jarque–Bera test statistic shows non-normality in the exchange rate returns of the Pak Rupee. The stationarity of Pak Rupee exchange rate returns checked through the augmented Dickey–Fuller (ADF) test indicates that all Pak Rupee exchange rate returns are stationary at their levels and provide strong evidence that they are integrated of order zero, I(0). The standardized macroeconomic news announcements are close to zero mean and have a unit standard deviation.

Descriptive Summary of Pak Rupee Exchange Rate Returns.

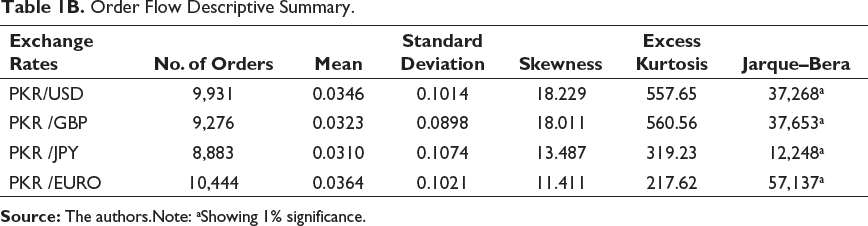

Order Flow Descriptive Summary.

Empirical Results

Direct Effects on Exchange Rate Returns and Exchange Rate Volatility

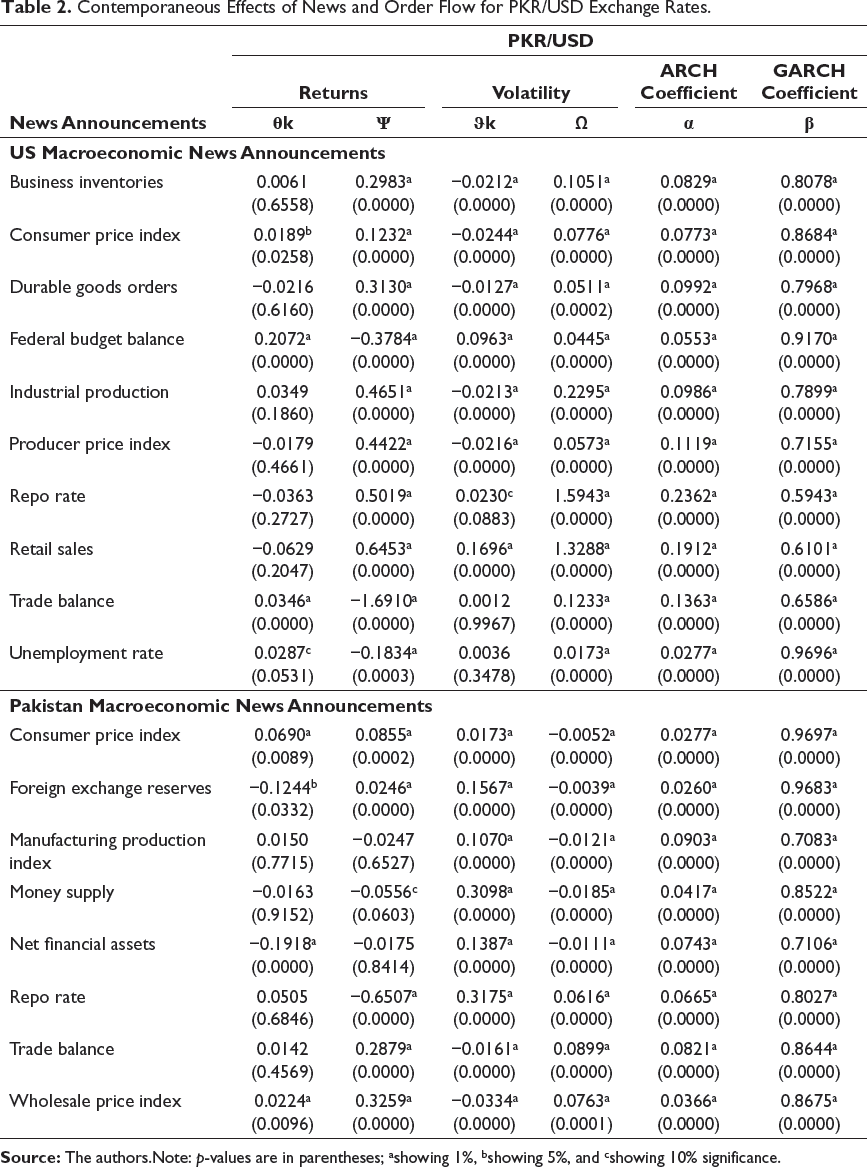

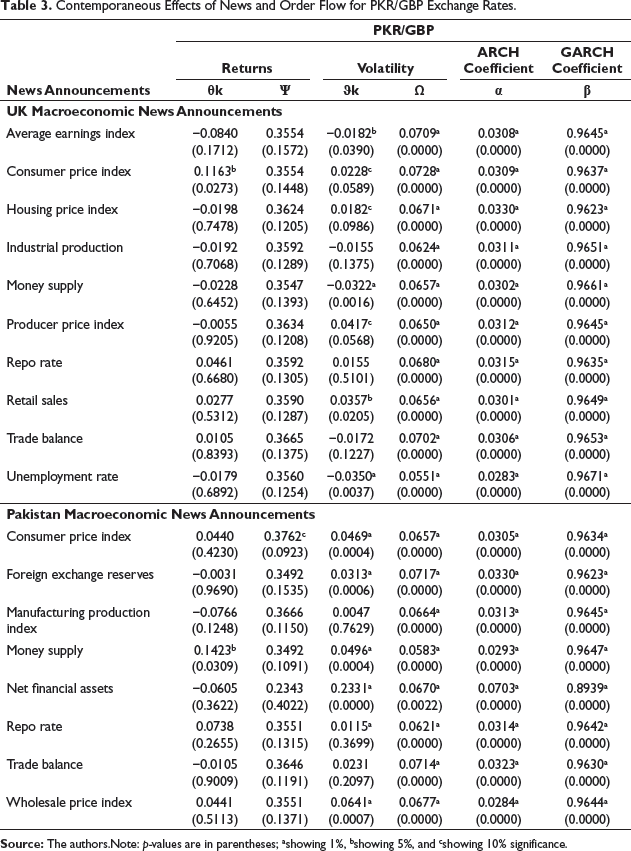

To examine the contemporaneous effects of each of macroeconomic news and order flow for each foreign currency on exchange rate returns and exchange rate volatility during announcement periods, Equations (3) and (4) are estimated. Tables 2–5 present the estimated contemporaneous effects of each of macroeconomic news and order flow for each foreign currency on Pak Rupee exchange rate returns and their volatilities during announcement periods. For Pak Rupee exchange rate returns, different ARMA (p, q) specifications are selected for incorporating serial correlation in exchange rate returns. For Pak Rupee exchange rate volatility, GARCH (1, 1) model is used. The significant ARMA (p, q) specifications indicate that the Pak Rupee exchange rate returns series show prediction of exchange rate movements based on past information. These findings imply market inefficiency. The significant coefficients of ARCH and GARCH terms imply that the volatility of each exchange rate reacts significantly to its own past squared shocks and to its own past volatility, respectively. These estimates exhibit volatility persistence.

In the return equation, the positive coefficient of macroeconomic news announcement indicates positive effects on Pak Rupee exchange rate returns implying good news (positive surprise) leading to an appreciation of Pak Rupee exchange rates and vice versa for bad news (negative surprise). The negative coefficient of macroeconomic news announcement indicates negative effects on Pak Rupee exchange rate returns implying good news (positive surprise) leading to a depreciation of Pak Rupee exchange rates and vice versa for bad news (negative surprise). However, the positive coefficient of order flow dominated in foreign currencies indicates positive effects on Pak Rupee exchange rate returns implying net purchase of foreign currency, which in turn causes an appreciation of Pak Rupee exchange rates. The negative coefficient of order flow indicates negative effects on Pak Rupee exchange rate returns implying net sale of foreign currency, which in turn causes depreciation of Pak Rupee exchange rates.

In the variance equation, the positive coefficient indicates that good news (positive surprise) raises the Pak Rupee exchange rate volatility while the negative coefficient indicates that good news (positive surprise) reduces the Pak Rupee exchange rate volatility. Whereas the positive coefficient of order flow indicates that order flow that is the net purchase of foreign currency raises the Pak Rupee exchange rate volatility, while the negative coefficient of order flow indicates that order flow that is the net sale of foreign currency reduces the Pak Rupee exchange rate volatility.

The magnitude of estimated coefficients of foreign and domestic macroeconomic news announcements suggest a surprise of one standard deviation in foreign and domestic macroeconomic indicators leading to appreciation/depreciation of Pak Rupee exchange rates. The Pak Rupee exchange rate returns react significantly to a few of the foreign and domestic macroeconomic news announcements. However, the Pak Rupee exchange rate volatility reacts significantly to most of the foreign and domestic macroeconomic news announcements. The direction of the contemporaneous effects of news of macroeconomic indicators depends on exchange rate determination models and news reactions by the monetary authorities (Almeida et al., 1998).

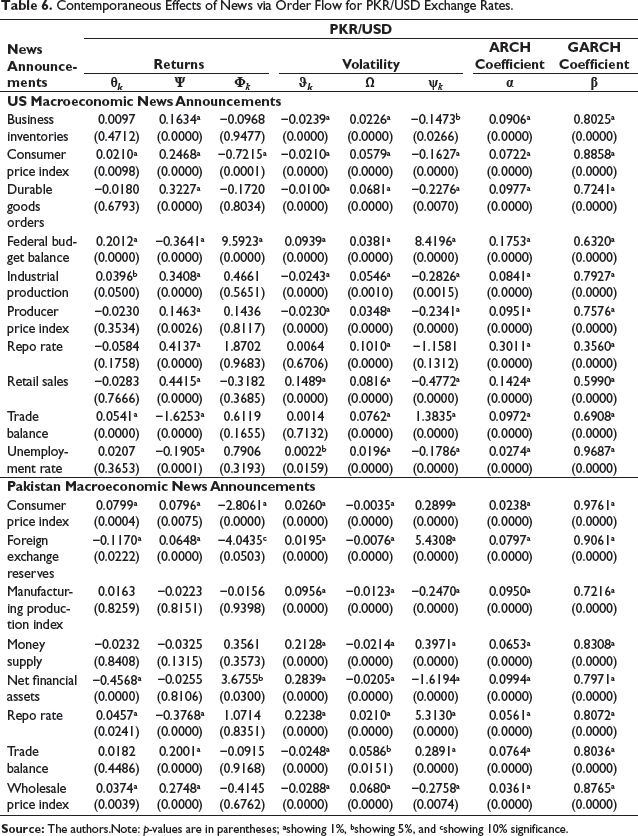

The PKR/USD exchange rate returns react positively and significantly to macroeconomic news such as US consumer price index, US federal budget balance, US trade balance, and US unemployment rate, PAK consumer price index, and PAK wholesale price index and negatively and significantly to PAK foreign exchange reserves, and PAK net financial assets. That is, PKR/USD exchange rate appreciates with news of improvement in the US federal budget balance and US trade balance, rise in the US consumer price index, US unemployment rate, PAK consumer price index, and PAK wholesale price index and depreciates with news of increase in PAK foreign exchange reserves, and PAK net financial assets.

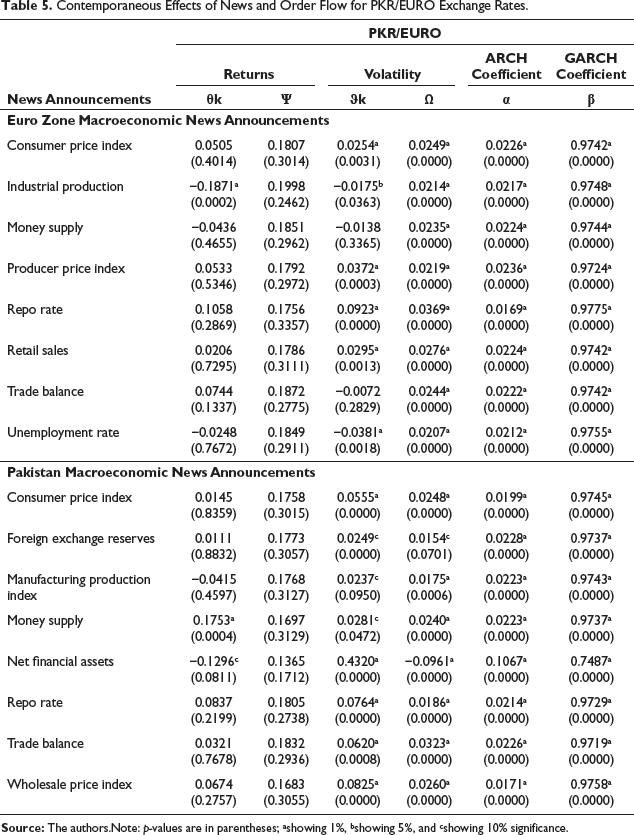

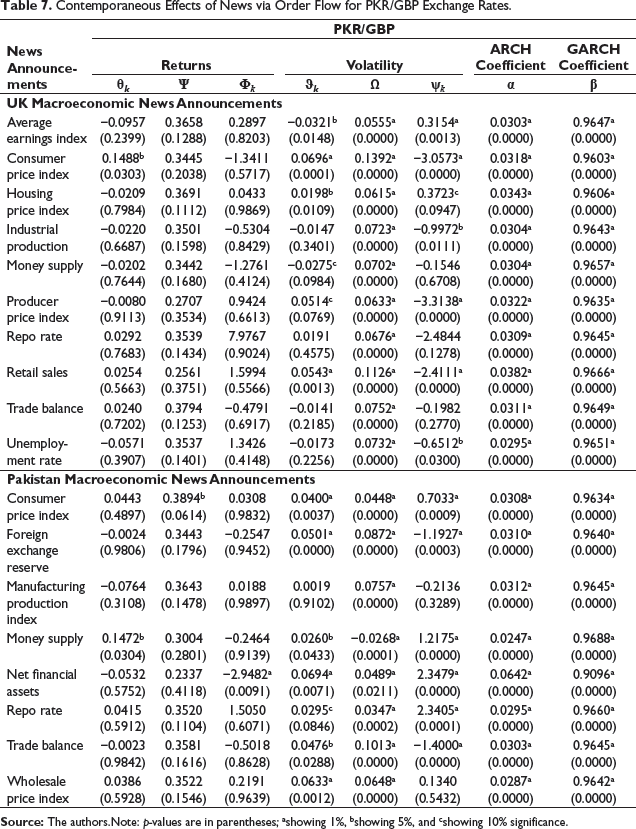

The news of the UK consumer price index and PAK money supply positively and significantly affects the PKR/GBP exchange rate returns. In other words, the PKR/GBP exchange rate appreciates with news of a rise in the UK consumer price index and an increase in PAK money supply. The PKR/JPY exchange rate returns react positively and significantly to macroeconomic news such as JP retail sales, PAK repo rate, and negatively to JP consumer price index and PAK net financial assets. It implies PKR/JPY exchange rate appreciates with news of an increase in JP retail sales and a rise in PAK repo rate and depreciates in with news of a rise in JP consumer price index and increase in PAK net financial assets. The PAK money supply news positively and significantly affects the PKR/EURO exchange rate and news of EZ industrial production and PAK net financial assets negatively and significantly affect the PKR/EURO exchange rate. It implies PKR/EURO exchange rate appreciates with news of an increase in PAK money supply and depreciates with news of a rise in EZ industrial production and an increase in PAK net financial assets.

These results are coherent with the flexible-price monetary model (FPMM), Keynesian model, and monetary approach to the balance of payments and also consistent with the market belief about the reaction function of the monetary authority. These results are consistent with the findings of Almeida et al. (1998), Andersen et al. (2003), Ehrmann and Fratzscher (2005), Pearce and Solakoglu (2007), Cai et al. (2008), Fatum et al. (2012), Caporale et al. (2018), Cheung et al. (2019), and Ben Omrane et al. (2020).

The PKR/USD exchange rate volatility reacts significantly to US macroeconomic news announcements such as US business inventories, US consumer price index, US durable goods orders, US federal budget balance, US industrial production, US producer price index, US repo rate, and US retail sales. The PAK macroeconomic news announcements such as PAK consumer price index, PAK foreign exchange reserves, PAK manufacturing production index, PAK money supply, PAK net financial assets, PAK repo rate, PAK trade balance, and PAK wholesale price index significantly affect the PKR/USD exchange rate volatility.

The UK macroeconomic news announcements such as UK average earnings index, UK consumer price index, UK housing price index, UK money supply, UK retail sales, UK unemployment rate significantly affect the PKR/GBP exchange rate volatility. The PKR/GBP exchange rate volatility reacts significantly to PAK macroeconomic news announcements such as PAK consumer price index, PAK foreign exchange reserves, PAK money supply, PAK net financial assets, PAK repo rate, and PAK wholesale price index.

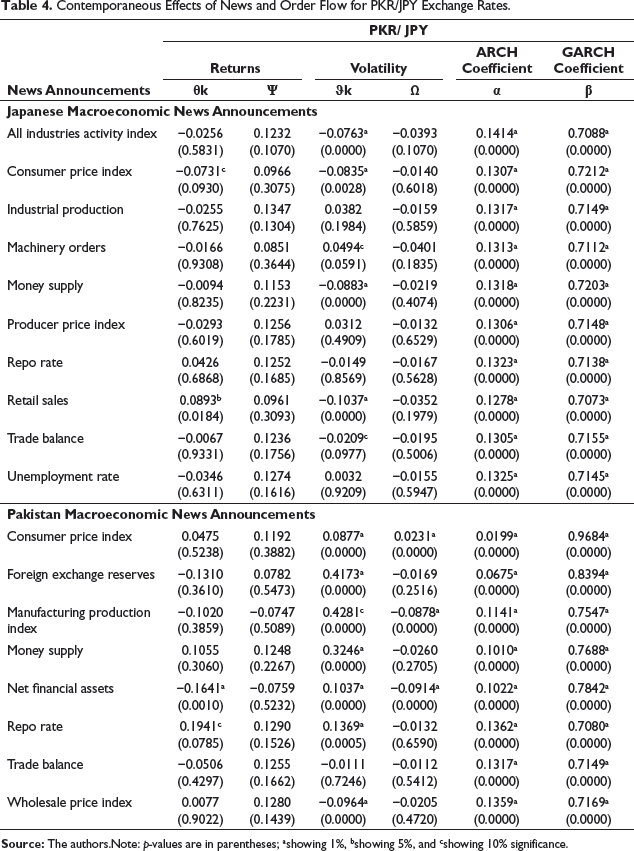

The PKR/JPY exchange rate volatility reacts significantly to JP macroeconomic news announcements such as JP all industries activity index, JP consumer price index, JP money supply, JP machinery orders, JP retail sales, and JP trade balance. The PAK macroeconomic news announcements such as PAK consumer price index, PAK foreign exchange reserves, PAK manufacturing production index, PAK money supply, PAK net financial assets, PAK repo rate, and PAK wholesale price index significantly affects the PKR/JPY exchange rate volatility.

The EZ macroeconomic news announcements such as EZ consumer price index, EZ industrial production, EZ producer price index, EZ repo rate, EZ retail sales, and EZ unemployment rate significantly affects the PKR/GBP exchange rate volatility. The PKR/EURO exchange rate volatility reacts significantly to PAK macroeconomic news announcements such as PAK consumer price index, PAK foreign exchange reserves, PAK manufacturing production index PAK money supply, PAK net financial assets, PAK repo rate, PAK trade balance, and PAK wholesale price index.

Most of the macroeconomic news announcements affect exchange rate volatility via money demand and capital or current account. These results are consistent with the findings of Ederington and Lee (1994, 1995), Andersen and Bollerslev (1998), Andersen et al. (2003), Pearce and Solakoglu (2007), Cai et al. (2008), Evans and Speight (2010), Neely (2011), Omrane and Hafner (2015), Omrane and Savaşer (2017), Maserumule and Alagidede (2017), Caporale et al. (2018), Cheung et al. (2019), and Ben Omrane et al. (2020).

The magnitude of positive coefficients of order flow for Pak Rupee exchange rate returns for each macroeconomic news suggests a hundred more purchases than sales of foreign currencies, which induces an increase in Pak Rupee price of foreign currencies. However, the magnitudes of negative coefficients of order flow for Pak Rupee exchange rate returns for each macroeconomic news suggest a hundred more sales than purchases of foreign currencies, which induces a decrease in Pak Rupee price of foreign currencies. The magnitude of estimated coefficients of order flow varies considerably with macroeconomic news flow for PKR/USD exchange rates. However, the magnitude of estimated coefficients of order flow is more or less the same with macroeconomic news flow for PKR/GBP, PKR/JPY, and PKR/EURO exchange rates.

The order flow significantly affects Pak Rupee exchange rate returns and their volatilities during announcement periods. The significant effect of order flow implies that order flow can explain contemporaneous fluctuations in the Pak Rupee exchange rates. Further, the role of order flow to convey private/incremental information unrelated to macroeconomic information is identified in Pak Rupee exchange rates determination. These findings align with Evans and Lyons (2002a, 2002b, 2005), Love and Payne (2008), Gradojevic and Neely (2009), Chinn and Moore (2011), Savaser (2011), McIntyre and Harjes (2016), Zhang et al. (2016), and Anifowose et al. (2018).

The effect of order flow on PKR/USD exchange rate returns is positive and significant corresponding to each US macroeconomic news such as US business inventories, US consumer price index, US durable goods orders, US industrial production index, US producer price index, US repo rate, and US retail sales. The positive effect implies the net purchase of USD which in turn causes an appreciation of USD against PKR. The effect of order flow on PKR/USD exchange rate returns is negative and significant corresponding to each US macroeconomic news such as US federal budget balance, US trade balance, and the US unemployment rate. The negative effect implies the net sale of USD which in turn causes depreciation of USD against PKR.

The effect of order flow on PKR/USD exchange rate volatility is positive and significant corresponding to each of US macroeconomic news. The positive effect implies that the order flow raises the PKR/USD exchange rate volatility corresponding to each US and macroeconomic news such as US business inventories, US consumer price index, US durable goods orders, US federal budget balance, US industrial production index, US producer price index, US repo rate and US retail sales, US trade balance, and US unemployment rate.

The effect of order flow on PKR/USD exchange rate returns is positive and significant corresponding to each PAK macroeconomic news such as PAK consumer price index, PAK foreign exchange reserves, PAK trade balance, and PAK wholesale price index. The positive effect implies the net purchase of USD, which in turn causes depreciation of PKR against USD. The effect of order flow on PKR/USD exchange rate returns is negative corresponding to each PAK macroeconomic news such as PAK money supply and PAK repo rate. The negative effect implies the net sale of USD, which in turn causes an appreciation of PKR against USD.

The effect of order flow on PKR/USD exchange rate volatility is negative and significant corresponding to PAK macroeconomic news such as PAK consumer price index, PAK foreign exchange reserves, PAK manufacturing production index, PAK money supply, and PAK net financial assets. The negative effect implies that the order flow reduces PKR/USD exchange rate volatility. The effect of order flow on PKR/USD exchange rate volatility is positive and significant corresponding to PAK macroeconomic news such as PAK repo rate, PAK trade balance, and PAK wholesale price index.

The order flow insignificantly affects PKR/GBP exchange rate returns corresponding to each UK and PAK macroeconomic news. However, the order flow positively and significantly affects PKR/GBP exchange rate volatility corresponding to each UK and PAK macroeconomic news. The positive effect implies that the order flow raises the PKR/GBP exchange rate volatility. The order flow insignificantly affects PKR/JPY exchange rate returns corresponding to each JP and PAK macroeconomic news. Similarly, the order flow insignificantly affects PKR/JPY exchange rate volatility except corresponding to the news of PAK consumer price index, PAK manufacturing production index, and PAK net financial assets. The order flow insignificantly affects PKR/EURO exchange rate returns for each EZ and PAK macroeconomic news. However, the order flow positively and significantly affects PKR/EURO exchange rate volatility corresponding to each EZ and PAK macroeconomic news released. The positive effect implies that the order flow raises the PKR/EURO exchange rate volatility.

Contemporaneous Effects of News and Order Flow for PKR/USD Exchange Rates.

Contemporaneous Effects of News and Order Flow for PKR/GBP Exchange Rates.

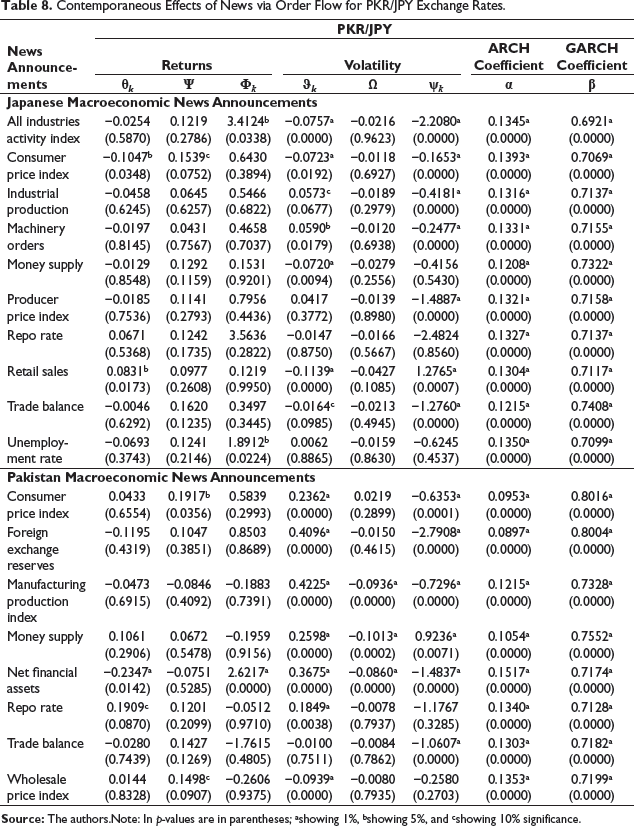

Contemporaneous Effects of News and Order Flow for PKR/JPY Exchange Rates.

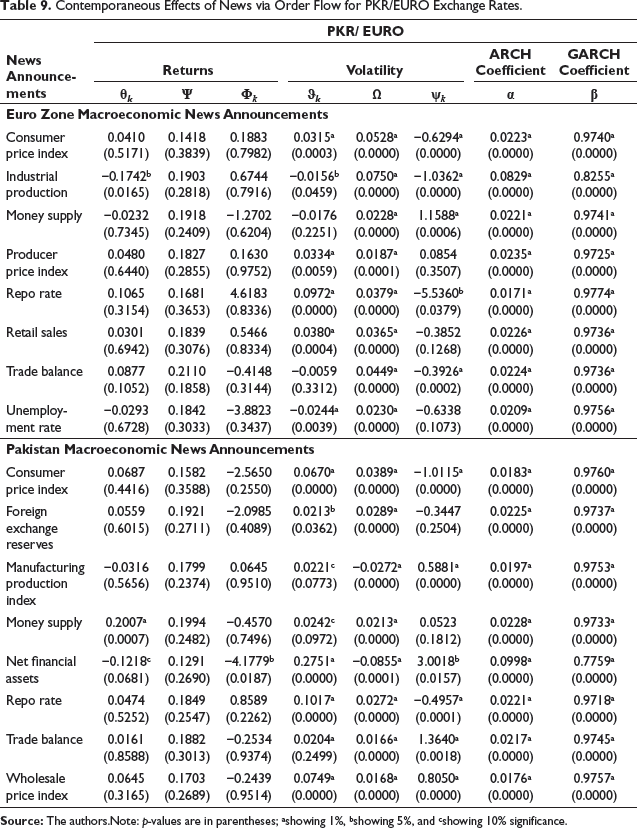

Contemporaneous Effects of News and Order Flow for PKR/EURO Exchange Rates.

Indirect Effects on Exchange Rate Returns and Exchange Rate Volatility

To examine the contemporaneous effects of each of the macroeconomic news via order flow on exchange rate returns and exchange rate volatility during announcement periods, Equations (3) and (4) are estimated. In return equation, the positive coefficient of interaction between macroeconomic news and order flow indicates positive effects on Pak Rupee exchange rate returns implying good news (positive surprise) that causes net purchase of foreign currencies, which leads to an appreciation of Pak Rupee exchange rates and vice versa for bad news (negative surprise). The negative coefficient of interaction between macroeconomic news and order flow indicates negative effects on Pak Rupee exchange rate returns implying good news (positive surprise) that causes net sale of foreign currencies, which leads to depreciation of Pak Rupee exchange rates and vice versa for bad news (negative surprise). The estimated interaction coefficients indicate the impact of dispersed information on Pak Rupee exchange rates. In the variance equation, the positive coefficient indicates that dispersed information leads to an increase in Pak Rupee exchange rate volatility while the negative coefficient indicates that dispersed information leads to reduced Pak Rupee exchange rate volatility.

Tables 6–9 present the estimated contemporaneous effects of each of the macroeconomic news via order flow for each foreign currency on Pak Rupee exchange rate returns and their volatilities during announcement periods. The results show that a few of the macroeconomic news via order flow significantly affect Pak Rupee exchange rate returns and their volatilities during announcement periods. However, most of the macroeconomic news via order flow significantly affect Pak Rupee exchange rate volatilities during announcement periods. They also show a significant impact of order flow following the announcement of macroeconomic news on Pak Rupee exchange rates. Further, the role of order flow to convey private/incremental information with the release of public news, which increases information asymmetry among market agents is identified in the Pak Rupee exchange rate determination.

The PKR/USD exchange rates appreciate with the announcements of the US federal budget balance news due to the net purchase of US dollars and depreciate with the announcements of US consumer price index news, PAK consumer price index news, and PAK foreign exchange reserves news due to net sale of US dollars. The appreciation occurs because large foreign budget deficit surprises raise real foreign interest rates, which raise the demand for foreign currencies. The depreciation occurs because higher foreign consumer price index surprises decrease foreign demand for money, which reduces the demand for foreign currencies and higher domestic consumer price index surprises increase demand for domestic currencies via capital account. The depreciation also occurs because PAK foreign exchange reserves surprises reduce the demand for foreign currencies.

The PKR/USD and PKR/JPY exchange rates appreciate with the announcements of PAK net financial assets news due to the net purchase of US dollars and Japanese yens. However, the PKR/GBP and PKR/EURO exchange rates depreciate with the announcements of PAK net financial assets news due to the net sale of British pounds and Euros. The appreciation occurs because an increase in net financial assets surprises leads to increased risk premium or expected rate on returns and hence increases the demand for foreign currencies. The depreciation occurs because an increase in net financial assets surprises leads to an improvement in the export competitiveness and hence decreases the demand for foreign currencies. The PKR/JPY exchange rates appreciate with the announcements of JP all industries activity index news and JP unemployment rate news due to the net purchase of Japanese yens. The appreciation occurs because higher foreign real activity surprises increase foreign demand for money, which raises the demand for foreign currencies and higher foreign unemployment surprise decreases foreign price level, which raises the demand for foreign currencies.

The PKR/USD exchange rate volatility raises with the announcements of foreign macroeconomic news such as US federal budget balance, and US trade balance due to net purchase of US dollars. However, the PKR/USD exchange rate volatility reduces with the announcements of foreign macroeconomic news such as US business inventories, US consumer price index, US durable goods orders, US industrial production, US producer price index, US retail sales, and US unemployment rate due to the net sale of US dollars. The PKR/GBP exchange rate volatility raises with the announcements of foreign macroeconomic news such as the UK average earnings index and the UK housing price index due to the net purchase of British pounds. However, the PKR/GBP exchange rate volatility reduces with the announcements of foreign macroeconomic news such as UK consumer price index, UK industrial production, UK producer price index, UK retail sales, and UK unemployment rate due to net sale of British pounds.

The PKR/JPY exchange rate volatility rises with the announcements of foreign macroeconomic news such as JP retail sales due to the net purchase of Japanese yens. However, the PKR/JPY exchange rate volatility reduces with the announcements of foreign macroeconomic news such as JP all industries activity index, JP consumer price index, JP industrial production, JP machinery orders, JP producer price index, and JP trade balance due to the net sale of Japanese yens. The PKR/EURO exchange rate volatility rises with the announcements of foreign macroeconomic news such as the EZ money supply due to the net purchase of Euros. However, the PKR/EURO exchange rate volatility reduces with the announcements of foreign macroeconomic news such as EZ consumer price index, EZ industrial production, EZ repo rate, and EZ trade balance due to the net sale of Euros.

The PKR/USD and PKR/GBP exchange rate volatilities rise with the announcements of domestic macroeconomic news such as PAK consumer price index, PAK money supply, and PAK repo rate due to net purchase of US dollars and British pounds. The announcement of PAK foreign exchange reserves news and PAK trade balance news raise the PKR/USD exchange rate volatility due to net purchase of US dollars and reduce PKR/GBP and PKR/JPY exchange rate volatilities due to net sale of British pounds and Japanese yens. The announcement of PAK manufacturing production index news reduces the PKR/USD and PKR/JPY exchange rate volatilities due to net sales of US dollars and Japanese yens and raises PKR/EURO exchange rate volatility due to net purchase of Euros. The PKR/JPY and PKR/EURO exchange rate volatilities reduce with the announcements of PAK consumer price index news due to the net sale of Japanese yens and Euros. The announcement of PAK trade balance news raises PKR/EURO exchange rate volatility due to the net purchase of Euro.

Contemporaneous Effects of News via Order Flow for PKR/USD Exchange Rates.

Contemporaneous Effects of News via Order Flow for PKR/GBP Exchange Rates.

Contemporaneous Effects of News via Order Flow for PKR/JPY Exchange Rates.

Contemporaneous Effects of News via Order Flow for PKR/EURO Exchange Rates.

Conclusion

This article studies the effects of macroeconomic news announcements and order flow on exchange rates in Pakistan. The analysis first shows the effects of foreign and domestic macroeconomic news releases on Pak Rupee exchange rate returns and their volatilities during announcement periods. It points outs average effects correspond to the direct channel for price impact, which is reflected in exchange rates immediately which is consistent with Andersen et al. (2003). Second, analysis shows that order flow drives movements in Pak Rupee exchange rates and induces portfolio–balance effects on exchange rates that are unrelated to macroeconomic information. It indicates the role of trade signals and trading strategies of currency traders affecting exchange rates. These results align with Evans and Lyons (2002a). Third, the findings show that releases of foreign and domestic macroeconomic news trigger trading, which reveals dispersed information affecting Pak Rupee exchange rate returns and their volatilities indirectly during announcement periods. It points out total effects correspond to the indirect channel for price impact, which is reflected in exchange rates. They also show that the order flow effect varies with the macroeconomic news announcements. Further, the finding also reveals that order flow intensifies the effects of macroeconomics news substantially, which is in line with Evans and Lyons (2008), Savaser (2011), and Zhang et al. (2016).

The results suggest that both macroeconomic news and order flow explain movement in exchange rates especially in PKR/USD exchange rates. Both direct and indirect information channels work during news announcement periods for Pak Rupee exchange rate movements. Hence, as part of an aggregated economic component and means of public and private information, macroeconomic news and order flow impact Pak Rupee exchange rates as an integrated determinant. When macroeconomic news strikes the foreign exchange market, it affects the decisions of market makers, influencing order flow and then the exchange rates. Based on the findings, it is recommended that policy and decision-makers in Pakistan should plan and implement policies and instruments for stabilizing the exchange rates and making foreign exchange markets efficient. The efficient foreign exchange markets lead to efficient intermediation of trading flows and news. For making financial markets efficient, efforts should be made for the organization and regulation of trading in foreign exchange markets which in turn has important implications for the price formation process.

It is also recommended that trading mechanisms and rules in foreign exchange markets, which include the direct market and the indirect market, should be explicitly defined. The centralized trading arrangement should coexist in foreign exchange markets in Pakistan to liquidate foreign exchange transactions.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.