Abstract

This research investigates the relationship between central bank independence and inflation for 37 developing countries during the period from 1972 to 2019. Given that most developing countries experienced high inflation, many opted for central bank independence to enhance their focus on inflation. Central bank independence reforms were anticipated to create a higher level of independence, which would result in a low inflation rate. We employed pooled least square with the assumption of homogeneity of co-efficients; the result showed no significant relationship between central bank independence and inflation. We checked the homogeneity assumption of the panel by applying Chow and Roy–Zellner tests; results showed that the model was not homogeneous. Furthermore, we performed the panel heterogeneity model with the pooled mean group estimator which indicated that a reverse relationship exists between central bank independence and inflation. This finding is robust as we split the sample into two groups: moderate and high inflation countries; the negative relationship between those variables still exists.

Introduction

Central banks hold an essential role in achieving macro-economic stability, particularly in influencing the level of inflation. Central bank independence (CBI) signifies that the central bank is free from political interference to pursue a monetary policy goal to control the inflation rate (Berger et al., 2001). The primary aim of CBI is to address the time inconsistency problem as a consequence of the policy that is no longer optimal in response to the original plan (Barro & Gordon, 1983; Kydland & Prescott, 1977). The time inconsistency problem generates inflation bias, which occurs when a government interferes with a central bank’s operation. In this situation, if the central bank recognizes a public inflation expectation, it tends to create inflation surprise, increasing seigniorage and pushing employment. Consequently, the central bank’s credibility is reduced, and inflation becomes challenging to manage. Therefore, delegating monetary policy to an independent central bank is predicted to promote the economic agent’s trust in future monetary stability. An independent central bank is believed to be better positioned to eliminate the time inconsistency problem of monetary policy (Rogoff, 1985).

Cukierman et al. (1992) examined the relationship between CBI and inflation in developed and developing countries. Their results show that the negative relationship only exists in developed countries and failed to find the same result for developing countries. Most developing countries are often affected by an unstable political situation, hyperinflation period, and strong political interference in central bank matters, though some developing countries also experience disinflation. According to Cukierman et al. (1992), Arnone et al. (2009), and Klomp and De Haan (2010), the concept of CBI in developing countries differs from that in industrialized nations. For example, the law and actual practice in the central banks in developed and developing countries are different. Developing countries have a lower level rule of law than developed countries, which may be due to a difference between the institutional arrangement and its adherence to the law. Campillo and Miron (1997) argue that, in terms of pursuing price stability, CBI requires strong political support.

Having considered this evidence in developing countries, this study focuses on the analysis of the effect of CBI on inflation among developing countries. In most developing countries, high inflation remains one of the leading challenges to macro-economic management and requires policy intervention. Moreover, among developing countries, some have experienced hyperinflation lasting for decades. To address this problem, many of these countries have had to reform their central bank legislation and change the central bank’s objective to achieve low inflation. These reforms have been expected to create a higher level of independence to efficiently manage inflation. However, the impact of CBI on inflation varies widely across countries. This diversity reflects the different characteristics of the central bank with regard to pursuing its monetary policy goal and heterogeneity in the structure of macro-economic variables. Various reasons have been proposed to explain the cross-country heterogeneity of the effect of CBI such as financial structure, macro-economic performance, and exchange rate regime.

Empirical evidence regarding the relationship between CBI and inflation using a panel data model is inconclusive. Alesina and Summers (1993), Grilli et al. (1991), Cukierman et al. (1992), Brumm (2002), Jonsson (1995), and Acemoglu et al. (2008) conclude that there is a negative relationship between CBI and inflation. According to King and Ma (2001) and Temple (1998), the negative effect of CBI on inflation exists only if high inflation countries are removed from the sample. On the other hand, Campillo and Miron (1997), Daunfeldt and De Luna (2008), Jácome and Vázquez (2008), Posso and Tawadros (2013), Dumiter et al. (2015), and Agoba et al. (2017) find no significant association between CBI and inflation.

However, those studies utilized a conventional panel data approach (pooled least square or fixed effect estimations), which has some limitations. Pooled least square estimation treats the homogeneity co-efficients for all cross-sections, thus neglecting individual heterogeneity (Samargandi et al., 2015). The drawback of the fixed effect model is that it does not take into account the unobservable individual-specific effect, thus yielding a biased and inconsistent estimation (Baltagi, 2008). In the light of the ongoing debate on the relationship between CBI and inflation, we seek to contribute an empirical perspective in the following ways: first, we test the parameter homogeneity assumption of the pooled least square estimation using the Chow test and Roy–Zellner test and also test for individual fixed effect following the approach of Baltagi (2008); we then model the CBI and inflation relationship in a dynamic model, where we distinguish between the short- and long-run effects. Such a distinction is crucial since CBI need not necessarily lead to lower inflation in the short run because there is a trade-off between inflation and growth in the short term, and the government prefers high output to low inflation. Econometrics testing of the theory uncovers the proper equilibrium of the long-run parameter for the relationship between those variables. Thus, we perform the pooled mean group (PMG) estimation. According to Pesaran et al. (1999), the PMG method captures both the dynamics and parameter heterogeneity.

Our result confirms the presence of heterogeneity parameters across cross-sections in the relationship between CBI and inflation. The results of the Chow and Roy–Zellner tests reject the homogeneous assumption for the co-efficients in the pooled least square estimation. According to the PMG estimation, we find that, in the long run, CBI has a negative effect on inflation. This finding is robust since we split the sample into two groups—moderate and high inflation countries; the negative relationship between those variables still exists.

Data and Econometric Methodology

Data

For the measure of CBI, we followed the CBI index constructed by Cukierman et al. (1992). This index is based on a legal aspect of independence. The index is between 0 and 1, with higher values denoting greater CBI for the legal index. The data for the CBI index are a legal variable aggregate weighted taken from Garriga’s (2016) data set. The panel data used in this study cover 37 developing countries (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Egypt, Ethiopia, Ghana, Guatemala, Honduras, Indonesia, Kenya, Malaysia, Mauritania, Mexico, Morocco, Nepal, Nicaragua, Nigeria, Pakistan, Paraguay, Peru, the Philippines, South Africa, Sri Lanka, Suriname, Tanzania, Thailand, Trinidad and Tobago, Tunisia, Turkey, Uganda, Uruguay, Venezuela, and Zambia). The classification of developing countries is based on International Monetary Fund’s (IMF’s) World Economic Outlook. We selected the countries which have change(s) in their CBI degree. Our data set consisted of seven variables: CBI, inflation, output gap, openness, fiscal deficit, US inflation, and unemployment rate covering the period from the years 1972 to 2019. Inflation is defined as the percentage change in the consumer price index over the corresponding period from the previous year and is provided by the International Financial Statistic (IFS) from the IMF.

Descriptive Statistics.

Econometric Methodology

This study investigates the relationship between inflation and CBI. We follow Cukierman et al. (1992) models.

In model 1, we extend Equation (1) by adding control variables, output gap, openness, and a fiscal deficit. According to Kydland and Prescott (1990), output gap is one of the primary determinants of inflation. We included openness, following Romer (1993), Terra (1998), and Jácome and Vázquez (2008) who studied the relationship between trade openness and inflation. Finally, the fiscal deficit was accounted following Sargent and Wallace (1984) and Catão and Terrones (2005) who studied the dynamic relationship between inflation and fiscal deficit. The fiscal deficit is one of the substantial influencers of inflation in developing countries. It is because the developing economies have limited access to foreign debt, undeveloped domestic capital market, and a limited tax capacity.

Additionally, to make our finding robust, first, in model 2, we added US inflation since the USA is the largest trading partner for developing countries. Given that around 50% of the US trade is with developing countries, inflation in the USA can spread to developing countries. We followed Crowder’s (1996) study that domestic inflation can be influenced by inflation in other countries as an external shock. Second, in model 3, we included the unemployment rate as it is one of the necessary factors for inflation. A higher unemployment rate might increase the incentive for the government to drive economic expansion; as a result, it increases the inflation rate. Phillips (1958) reported a negative relationship between inflation and unemployment rate. Phillips (1958) described the trade-off between inflation and unemployment known as the Phillips curve. Finally, in model 4, we added both US inflation and unemployment rate to our basic model. Models 1–4 are described as follows:

where, INF is inflation, LCBI is the legal CBI index, GAP is output gap, OPEN is openness trade, FD is a fiscal deficit, USinf is US inflation, and UNP is the unemployment rate.

We applied the poolability test to check whether the parameter of our equation varies from one country to the other. The pooled least square model represents a behavioral equation with the same parameters over time and across groups. On the other hand, the unrestricted model has the same behavioral equation but different parameters across time and across groups (Baltagi, 2008). The restricted model for each group is as follows:

where,

where,

The null hypothesis of the poolability test is

In the case where the pooled least square estimator is not poolable due to the assumption of homogeneity not being held, we then use the pooled mean group (PMG) estimator constructed by Pesaran et al. (1999). Pesaran et al. (1999) developed the PMG estimation, which incorporates both long-run and short-run effects by adopting autoregressive distributive lag structure (ARDL) and estimating the ARDL method as an error correction model. The PMG estimator allows the intercepts, short-run co-efficients, and error variances to vary for every cross-section, but the constraint of long-run co-efficients is the same. The PMG model is based on the ARDL (p, q, q, …, q) model. Following Pesaran et al. (1999), we estimated a dynamic panel heterogeneous model based on the ARDL (pi, qi, ki, li, mi) model:

In pooled mean group estimation, Equation (2) becomes

We also employed the Hausman test to check the long-run homogeneity hypothesis of the PMG estimator. The null hypothesis in this test assumes that the PMG estimator is consistent and more efficient than the mean group estimator (Pesaran et al., 1999). If we reject the null hypothesis, then we cannot assume the same long-run co-efficients for all panels, and the restriction imposed by the PMG estimator is not valid. In other words, the mean group estimator is preferred.

Empirical Results

Pooled Least Square Estimation.

Poolability Test.

The assumption in the pooled least square model is that all of the co-efficients must be the same across country. Having estimated the pooled least square method, we performed a poolability test under the assumptions of homoskedastic and normally distributed errors. The test results are given in Table 3. First, we applied a Chow test on models 1 to 4, under

Full Sample

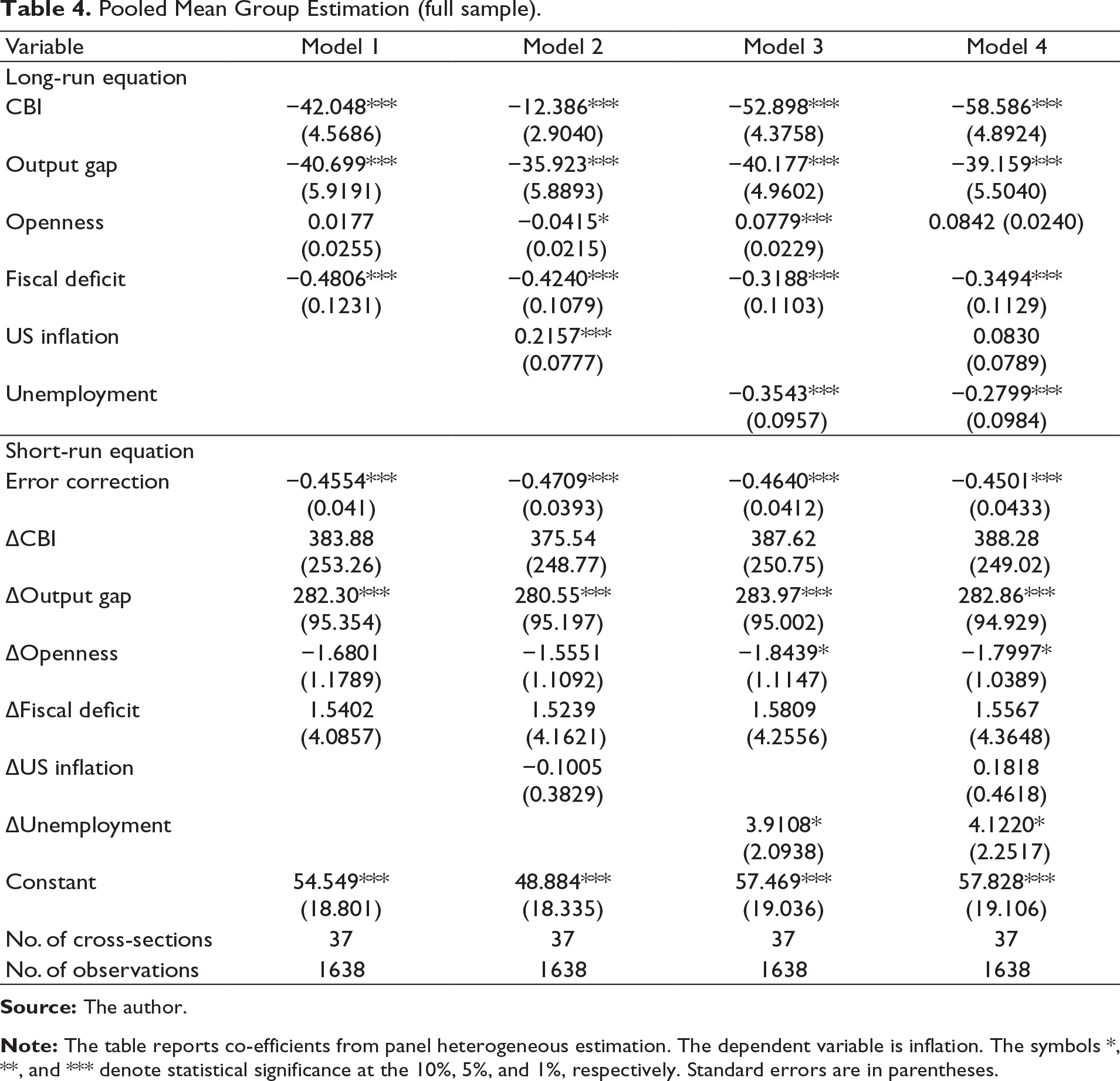

Pooled Mean Group Estimation (Full Sample).

To choose the optimal lags for each variable in the long run and the short run, we applied the Akaike info criterion (AIC). We estimated the ARDL (1, 1, 1, 1, 1), which is preferred in this model. In the PMG estimator, the error correction term (ECT) is statistically significant and has a negative sign, so there exists a long-run relationship between inflation and its essential determinants. This negative and significant co-efficient implies that, in response to a shock, inflation adjusts to the long-run equilibrium, the explanatory variables in the model bring about a correction in the opposite direction. The co-efficients of the ECT are in the range from −0.4840 to −0.4983 and significant at 1%. This implies that the disequilibrium in the short run will be corrected annually by between 48.40% and 49.83%, and a long-run equilibrium exists after about two years for the PMG estimator.

The long-run parameter estimates can be explained as follows: we find a statistically significant negative long-run relationship between CBI and inflation with co-efficients ranging from −4.2971 to −33.987 for the four models. This finding is supported by the theoretical view of CBI, whereby delegating monetary policy to an independent central bank will reduce inflation. Our finding is supported by Grilli et al. (1991), Cukierman et al. (1992), Jonsson (1995), Brumm (2002), and Acemoglu et al. (2008), who found a negative and significant effect of legal CBI on inflation. Loungani and Sheets (1997) state that most economists agree that CBI helps to reach the long-term goal of price stability.

Split Sample

We divided the sample countries into moderate inflation countries and high inflation countries. The results of the PMG estimator for the moderate and high inflation countries are reported in Table 5. Focusing first on the moderate inflation economies, the adjustment co-efficient for the PMG estimator is negative and significant at 1%. The speed of the adjustments is −0.4740, −0.4759, −0.4839, and −0.4833 for model 1, model 2, model 3, and model 4, respectively. These co-efficients indicate that around 47% to 49% of the disequilibrium in the short run is corrected in the long run for the moderate inflation countries. These adjustments suggest that any deviation in inflation from the long-run equilibrium relationship will be corrected in the opposite direction in 2.1 to 2 years. Our finding for the high inflation group reveals that the long-run co-efficient of convergence is negative and significant at the 15 level, with co-efficients of −0.6095, −0.6128, −0.6206, and −0.6198 for model 1, model 2, model 3, and model 4, respectively. These co-efficients indicate that around 60% to 62% of the disequilibrium in the short run is corrected in the long run for the high inflation group of countries. The adjustment time for inflation to achieve long-run equilibrium is approximately 1.6 years. Based on the result attained from the ECT co-efficient, it can be inferred that inflation in the high inflation countries achieves long-run equilibrium faster than in the moderate inflation countries. Therefore, the impact of CBI on reducing inflation in high inflation countries is more efficient and faster than in the moderate inflation countries. According to Loungani and Sheets (1997), high inflation countries experience hyperinflation; this creates a high degree of aversion to inflation, which may establish a high degree CBI index and also result in lower inflation than in moderate inflation countries.

Pooled Mean Group Estimation (Split Sample).

This finding implies that CBI could be helpful for countries facing a high level of inflation. Our result shows that the co-efficient of the relationship between CBI and inflation is high, particularly in the high inflation group of countries. This high co-efficient is due to the fact that we use the level of inflation that is calculated by the difference in consumer price divided by the previous consumer price. Previous studies have transformed inflation or used the logarithm of average inflation. Other studies treat high inflation as an outlier and removes it from the sample data. The co-efficients associated with the high inflation countries (from −86.435 to −92.135) are roughly 10 times larger than those of the moderate inflation countries (−3.8242 to −10.631); this is due to the fact that the decrease in inflation is larger in high inflation countries. This finding is supported by Jonsson (1995), who argued that CBI is the most crucial variable during a high inflation period. The more independent the central bank, the more freedom central bank has to set and implement monetary policy to reduce inflation.

On the other hand, in the short run, the co-efficients of the PMG estimator reveal a different pattern. This is because, in the short run, the co-efficients are not restricted to being the same across countries. Hence, there will be no single common estimate for any co-efficient. The average short-run effect can be estimated by considering the mean of the corresponding co-efficients across countries. We cannot establish a significant impact of CBI on inflation in all of the sample countries or in the moderate and high inflation countries. This shows that there is a delayed effect of CBI that can reduce inflation in all four models. The reason why there is no significant effect of CBI on inflation in the short run is due to the trade-off between inflation and output. According to Walsh (1995), CBI strengthens the effect of monetary policy on real activity, and the trade-off between output and inflation is more significant in countries with a more independent central bank. This implies that countries with a more independent central bank have a larger short-run effect on real output and employment. This suggests that, in the short run, monetary policy seeks to pursue high output and employment rather than inflation. Another reason is that, in the short run, prices are sticky, and expected inflation is unchanged; therefore, the monetary policy will not affect inflation in the short run.

Robustness Test

In this part, we implemented a robustness check for the effect of CBI on inflation by performing instrumental variable (IV) estimation. To control for potential endogeneity, we employed the first difference generalized method of moments (FD-GMM) estimator of Arellano and Bond (1991). The CBI is considered endogenous and instrumented with lagged values in the FD equation. The control variables are considered exogenous, being instrumented in the level.

Panel IV Estimation (Full Sample).

Conclusion

This research provides new evidence for the effect of CBI and some control variables on inflation from the perspective of both long-run equilibrium and short-run dynamics. In this study, we argue that the typical assumption of parameter homogeneity in panel data that has been used in previous empirical studies on the relationship between CBI and inflation does not hold. Since the previous works did not meet the validity of the parameter homogeneity, this implies that their results were biased. Given that our panel consists of heterogeneity across countries, we performed PMG estimations in a panel of 37 developing economies. We also divided the panel into two groups, moderate and high inflation countries to gain an insight into the nature of this heterogeneity. The ECT for the PMG estimators is statistically significant and has a negative sign, suggesting that a long-run relationship exists between these variables. The speed of adjustment of inflation from the long-run equilibrium is corrected in the opposite direction. It takes around 1.6 years in the high inflation group and 2.1 years in the moderate inflation group. Some further implications follow from these findings. We confirm that there is a long-run negative relationship between CBI and inflation. If we distinguish between moderate and high inflation countries, we find that CBI has a higher impact in high inflation countries. This suggests that the role of central bank reforms is more efficient in reducing inflation in countries with a high inflation rate.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflict of interest, with respect to research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.