Abstract

The geographies of real estate, land redevelopment and capital play crucial roles in India’s contemporary urban place-making. There is a significant knowledge gap in understanding the role of real estate development and the linkages with capital, the pre-existing propertied business class, emerging markets, and associated aspects in the rapidly changing non-metropolitan, medium-sized cities’ (MSC) context. This study analyses urban transition in Siliguri, a fast-growing MSC in eastern India. Unlike the large megacities, real estate development here has witnessed a considerable capital shift in a speculative property market. Real estate growth is primarily led by the local business and propertied class that eventually emerged as developers. The efforts have resulted in urban place-making of newly built environments, consumption spaces and gated condos through the land redevelopment process.

Introduction

Urban transformation in the Global South, particularly in India, has recently received significant academic attention (Roy & Ong, 2011; Searle, 2016; Shatkin, 2017). According to Shaw (1999), India’s new urban transition was fuelled by international capital inflow in the leading city regions. The country adopted a New Economic Policy in 1991 (NEP-1991) to embrace liberalization, privatization and globalization. Following NEP-1991, leading cities like New Delhi, Chennai, Kolkata, Bangalore and Hyderabad became important entry points for inbound foreign direct investments (FDI) in the country. Accordingly, these cities underwent a significant spatial transformation in the past three decades through various planning, policy-level interventions and practices (Banerjee-Guha, 2002; Bose, 2015; Das, 2015; Dey, Samaddar & Sen, 2016; Nijman, 2000; Shatkin, 2017; Stallmeyer, 2010). The geographies of real estate, built environment and capital played an essential role in India’s contemporary urban restructuring and place-making process (Dupont, 2016; Rouanet & Halbert, 2015; Searle, 2016). A significant shift has been observed in the government’s effort to liberalize land (Sud, 2020). It includes abolishing erstwhile urban land ceiling acts and opening FDIs in the real estate sector (Batra, 2009). Leading cities have experienced speculative real estate growth through land redevelopment influenced by transnational financial networks (Goldman, 2011; Goldman & Narayan, 2021). The period witnessed the emergence of a new urban class, gentrification and (re)production of diverse consumption spaces leading to urban spatial transformations (Bose, 2015, Brosius, 2012; Searle, 2016; Upadhya, 2009).

While big cities have already been much studied, there are limited attempts to understand the urban transition and the growing significance of real estate development efforts in the context of emerging non-metropolitan and medium-sized cities (MSCs) in India. This study argues that the effect of globalization, aka neo-liberalization, in urban place-making, is no longer limited to leading cities. It has already been outreached to many regional cities, causing significant spatial changes. MSCs are middle-range cities in the settlement hierarchy, situated between the leading cities and relatively smaller towns in a region or country (Bolay & Kern, 2019; Rondinelli, 1982). MSCs are mainly sub-regional cities with local specificities, geographical-historical embeddedness, and diverse political-economic trajectories. The study assumes that the urban transition of MSCs usually takes different pathways, along with some well-established similarities. Transnational capital may not directly drive urban transition in these cities. The real estate developer’s role may also differ regarding the economic position and control as stakeholders in urban place-making. They may also function at a much lower scale, in a different capacity and adopt local level market strategies. The study has followed a nuanced approach to examine urban transition and real estate development in Indian MSCs by taking Siliguri as a case study.

Study Area: Siliguri

Siliguri is a fast-growing city in West Bengal, India. It occupies an important geographical and strategic position (Figure 1). It is situated in India’s ‘chicken neck corridor’, a 23-kilometre narrow land strip between Nepal and Bangladesh. It connects the country’s Northeastern region with the Indian mainland. Siliguri shares international boundaries with Nepal, Bangladesh and Bhutan, making it an important commercial hub and trade corridor. Over the years, the city’s population has significantly increased, transforming it into a leading city in the region.

Study Area—Siliguri.

According to the 2011 census, the population of the Siliguri Municipal Corporation or SMC was over 0.5 million. It is currently the second leading city in India’s larger Northeastern region after Guwahati, the state capital of Assam. Siliguri’s economy mainly depends on tea, trade and transport (SMC, 2015). Over the years, its economic activities, especially trade and commerce, have been significantly rising and therefore its economic and logistical importance has substantially increased (Ghosh, 2018). Siliguri’s Bagdogra airport is the second most important airport in West Bengal after Kolkata.

Figure 2 suggests that the number of passengers arriving and departing from Bagdogra airport has increased from 327,748 in 2007–08 to 1,524,516 in 2016–2017. This means almost a five-time increase in passengers within a decade for a city with just 0.5 million population. The above analysis suggests that the Siliguri economy is rising, indicating the emergence of a new urban middle class.

The recent urban development in the city includes the rise of shopping malls, commercial complexes, real estate projects, luxury hotels, and new townships. 1 These reaffirm the city’s rapid transformation with significant investment and a recent real-estate-driven urban place-making. This study addresses the following issues of Siliguri’s urban transition: How does urban place-making take place? Who are the real estate developers? What is the nature of capital associated with the city’s urban transition in recent years? The study mainly contributes to the role of locally embedded real-estate development in emerging Indian MSCs.

Theoretical Framework

The study follows an institutional framework, which offers a suitable explanation to understand the growth of real estate in a city. This framework primarily originated from the sociologist Anthony Gidden’s work on structuration and agency theory (Giddens, 1984). Gidden conceptualizes structure, agency and institution, that is, actors, forces and their relative relationship, as the key determining factor for any social development. Healey and Barrett (1990) first contextualized this theory in the context of real estate and the property market. Krabben and Lambooy (1993) noted that ‘The built environment is the result of the relationships between agents and institutions within the local economy on the one hand, and with regional, national and (inter)national financial and development interests which are influenced by structural factors on the other hand.’ Guy and Henneberry (2000) further argued the need for integrating economic logic and social structure in urban development. As a significant agency of urban changes, locally embedded real estate developers are relatively less studied in the Global South which includes India. They simultaneously characterize a social class, spatial and built-up decision makers as investors, market risk appraisers and risk-takers, while maintaining social and political-economic linkages with other agencies and institutions. They often become critical players in urban place-making, most applicable to non-global or non-metropolitan cities. In Indian society, real estate developers’ agency building through pre-existing surplus capital, assets and social organization background are often ignored. This study primarily contributes to the locally embedded nature of real estate growth by taking Siliguri as a case study.

Research Design

The study adopts a multi-stage research strategy to fulfill the research objectives. It examines the status of land redevelopment in Siliguri using the GPS survey-based Land Use Land Cover (LULC) maps for 2004 and 2019. The investigation reflects on the land redevelopment process to locate major real estate growth areas. The study followed a questionnaire-based sample survey to examine the evolution of urban built-up changes, real estate investment and patterns of land prices in the select study areas.

Finally, qualitative analysis is conducted by considering in-depth interviews of 43 key informants to examine the role of real estate developers, investors, and anchors of globalized capital brands in Siliguri’s recent transition. The key informants were interviewed in two stages between July 2019 and January 2020. The initial respondents of the study included officials, planners, policy-makers from various public institutions and members of various business organizations to understand the nature of urban transition in Siliguri. The second-stage interviews involved respondents who adequately represent the city’s organized and unorganized real estate sectors. The respondents were members of the Confederation of Real Estate Development Agencies India (CREDAI-Siliguri), the Association of Real Estate Advisors Siliguri, individual property developers, and managers of hotels, shopping malls, branded stores, restaurants, and other enterprises. All the key informants were selected following a snowball sampling methodology and used the semi-structured questionnaire. The audio-recorded interviews were transcribed and analysed for detailed content analysis using the NVivo software.

Analysis and Findings

Spatial Transformation of Siliguri

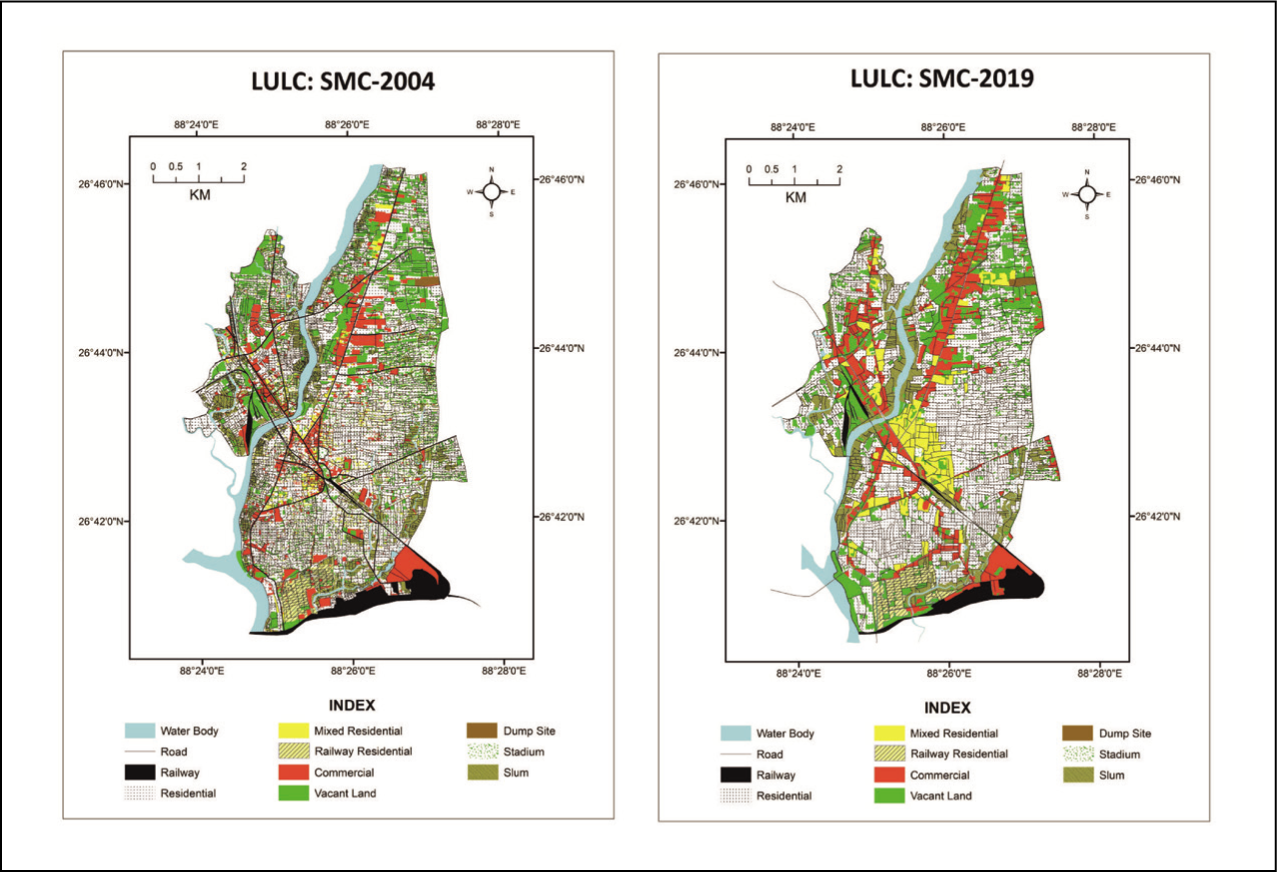

Understanding land use change has always been vital in investigating how capitalization has shaped urban spaces worldwide. In 2004, SMC prepared the city’s first detailed GPS-based survey Land Use Land Cover map (LULC-2004). The latest LULC map of the city is available for 2019 (LULC-2019), prepared by the ICLEI (ICLEI, 2019). There were a few mismatches between these LULC-2004 and LULC-2019 maps. The LULC-2004 had not covered areas such as railways, railway residential, and stadiums, unlike the LULC-2019. The other land use types adopted in both surveys were comparable, except for required alterations in selected geographical locations. The SMC boundaries of LULC 2004 and LULC 2019 were found mismatched in some areas. The study attempts to make the necessary changes in these LULC maps and used Google Earth Image to make the required changes in 178 pre-identified locations in the LULC-2004 map. In addition, a GPS-based survey was conducted in over 197 pre-identified geographical patches in 2019. After following standardized procedures, the updated LULC-2004 and modified LULC-2019 were prepared (Figure 3).

Land Use Land Cover Maps of SMC for 2004 and 2019.

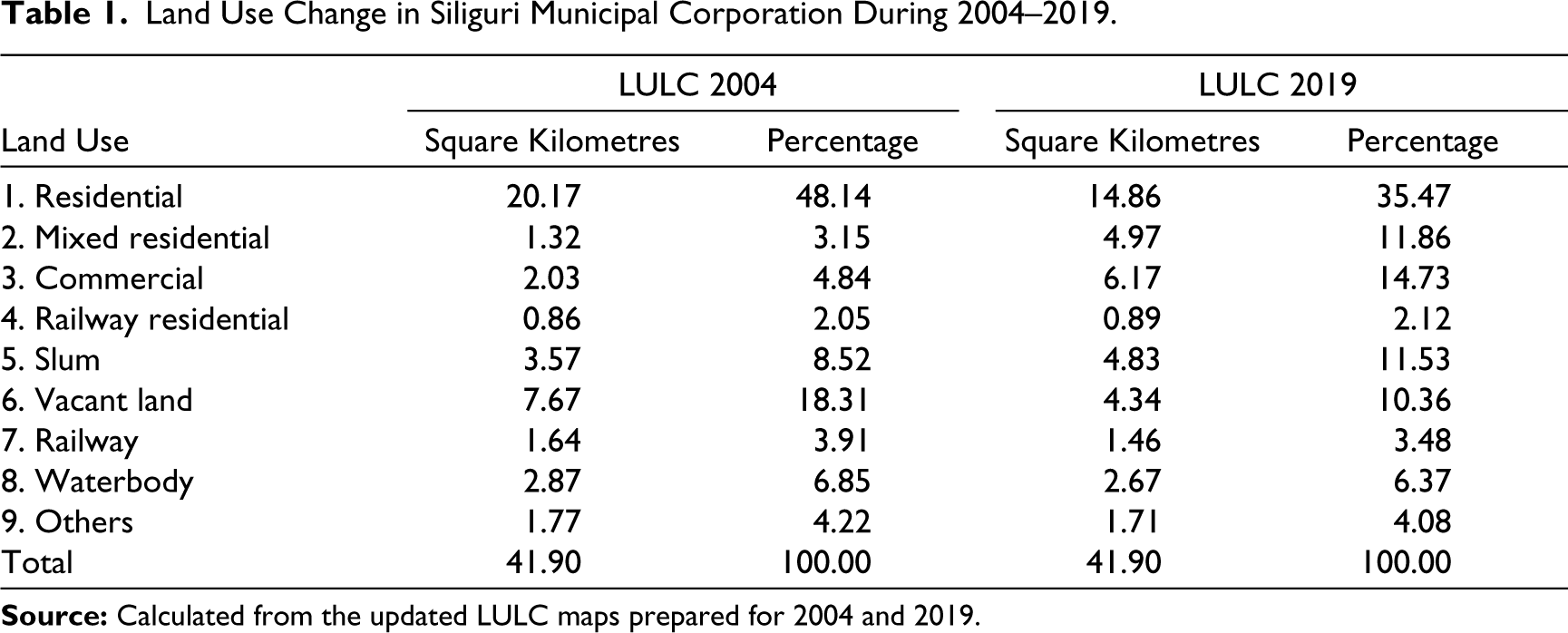

The comparison of LULC map details in Table 1 suggests the following changes in land utilization and land redevelopment practices in SMC between 2004 and 2019.

Land Use Change in Siliguri Municipal Corporation During 2004–2019.

The residential areas have declined by nearly 5 sq. km. The reduced residential areas primarily changed into commercial zones.

The city has noticed a significant growth of mixed residential areas and commercialization of land use.

The commercialization of the land use process has intensified mainly along the city’s three arterial roads or corridors that is, Sevoke Road, Hill Cart Road and Bardhaman Road.

Sevoke Road has emerged as the city’s new commercial area, attracting maximum investment during the last 15 years.

Siliguri has limited vacant lands, just 10% of the area. Limited vacant land and high demand have increased land prices in the city. The following section will further highlight this aspect.

Land Prices in Siliguri

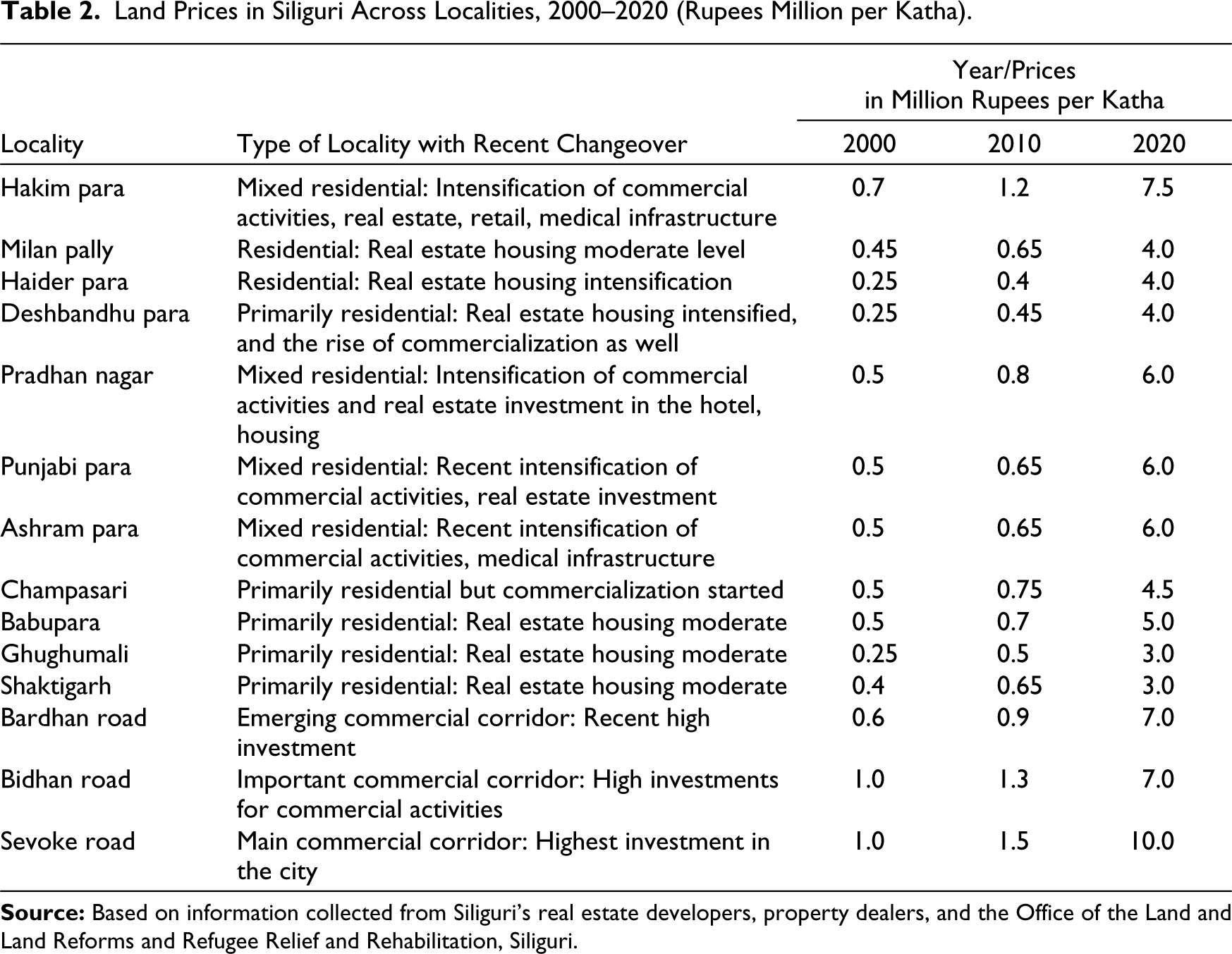

Land prices in Siliguri sustained a considerable increase over the years (Table 2). In the early 2000s, Siliguri’s residential areas had an average land price of rupees 0.25–0.5 million per katha (i.e., 720 sq. ft). Land prices of the same locality reached 0.4 to 0.7 million in 2010, marked by an overall 40–50% growth in valuation. The current land prices have touched the bracket ranging from rupees 3.0 to 4.0 million per katha in these areas. In the last decade, along with the real-estate-based housing market expansion, many residential areas witnessed the invasion of numerous commercial activities, including nursing homes, hotels, retail stores and market complexes. The process contributed to a brisk increase in land valuation and the gradual changeover of these neighbourhoods into emerging mixed-residential areas.

The mixed residential areas are primarily located near main commercial activities, where land valuation increased multiple times over a shorter duration. The land prices in mixed residential areas increased from rupees 0.5 to 0.7 million in 2000 to 6.0–7.5 million per katha in early 2020. Along one of the major commercial corridors, Bardhaman Road, the land prices increased from rupees 0.6 to 1.0 million to over 7.0 million. In the last decade, land prices in Sevoke Road have grown to over rupees 10 million per katha in 2020. Sevoke Road has witnessed a phenomenal physical and land use transformation through a massive investment drive. Many large shopping malls, restaurants, and retail stores have immensely transformed it.

Land Prices in Siliguri Across Localities, 2000–2020 (Rupees Million per Katha).

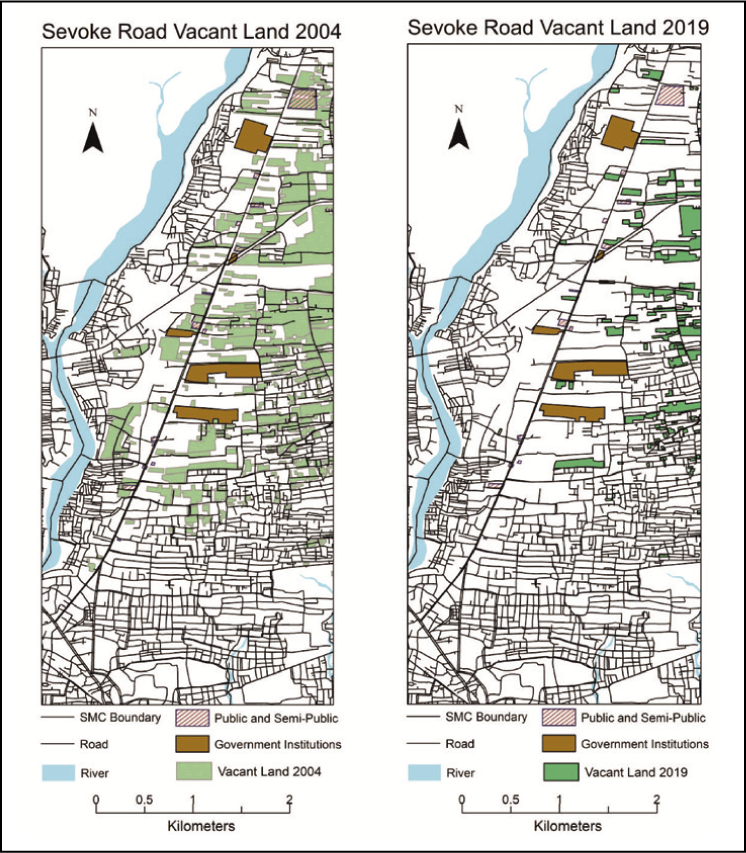

Transformation in Siliguri’s Sevoke Road (SRD)

Sevoke Road (SRD), one of Siliguri’s main arteries, has significantly transformed. It connects the city’s central business district that is, Bidhan market, with the National Highway 31C that leads to Sikkim, the Dooars and Bhutan. SRD’s transformation started primarily from 2005 onwards (Figure 4). Until 2004, SRD mainly constituted several commercial buildings, offices, warehouses, garages and different government organizations. A large parcel of land remained vacant or unused. In 2005 the local real estate developers first initiated property development on erstwhile vacant lands for diverse projects like housing, malls, commercial complexes and hotels. The expanding real estate gradually lessened the pre-existing vacant lands along the SRD.

Land Redevelopment and Declining Vacant Land in SRD, 2004–2019.

Changing Built-up Characteristics in SRD

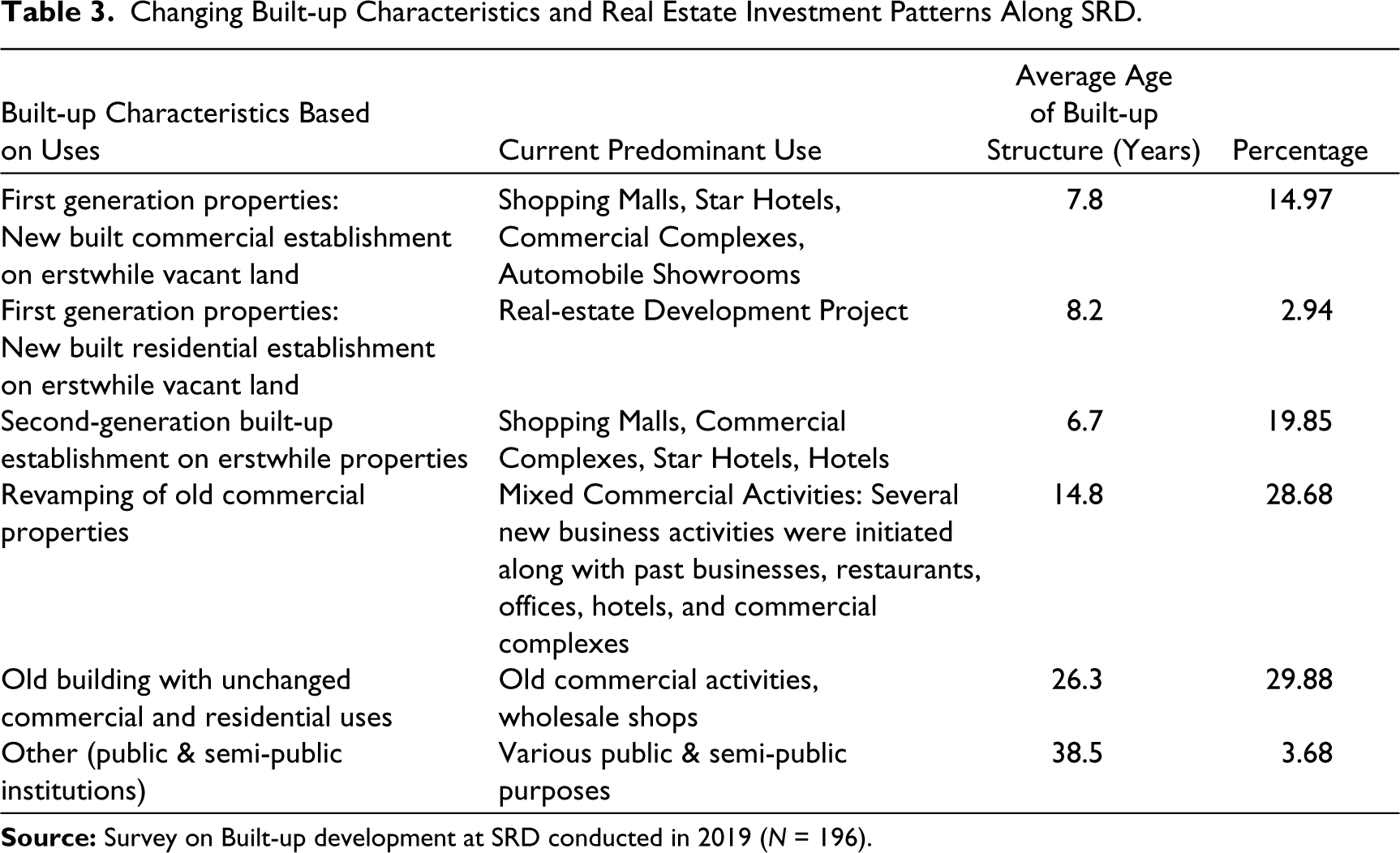

The study conducted a sample survey in 2019 by taking 196 samples (N) of built-up establishments along the SRD to examine the specific nature of changes regarding land utilization, physicality or built-up modifications, and new economies by replacing the former utilization of the spaces. The detailed differences in built-up characteristics with current use suggest that changing investments, specific demands in the real-estate sector, and emerging consumption spaces in SRD have evolved in recent years (Table 3).

Changing Built-up Characteristics and Real Estate Investment Patterns Along SRD.

The transformation in SRD followed three intrinsically linked built-up development processes: (a) first-generation or newly built development in the erstwhile available vacant lands; (b) second-generation built-up properties on erstwhile construction or properties; and (c) revamping of old commercial properties for new ventures.

The survey results suggest significant construction through newly built properties in recent years. Nearly 18% of the built-up development includes first-generation properties on erstwhile vacant lands. It includes the new commercial and residential units developed with an average property age under eight years.

The second generation of new built-up developments recorded nearly 20% of the overall built-ups, primarily constructed through replacing the previous structure.

The first- and second-generation properties are utilized for new economic spaces, including shopping malls, star hotels, commercial complexes, automobile showrooms, and mixed commercial purposes.

The revamped properties, that is, reinvestments on the existing old commercial building, were recorded to be nearly 29% of the overall property stock. These properties are primarily used for mixed commercial activities.

The share of old built-up developments accounts for 30% of the total property stocks. These properties mostly continued with the past commercial activities, such as wholesale shops and offices. The average age of old built-up structures is 26 years.

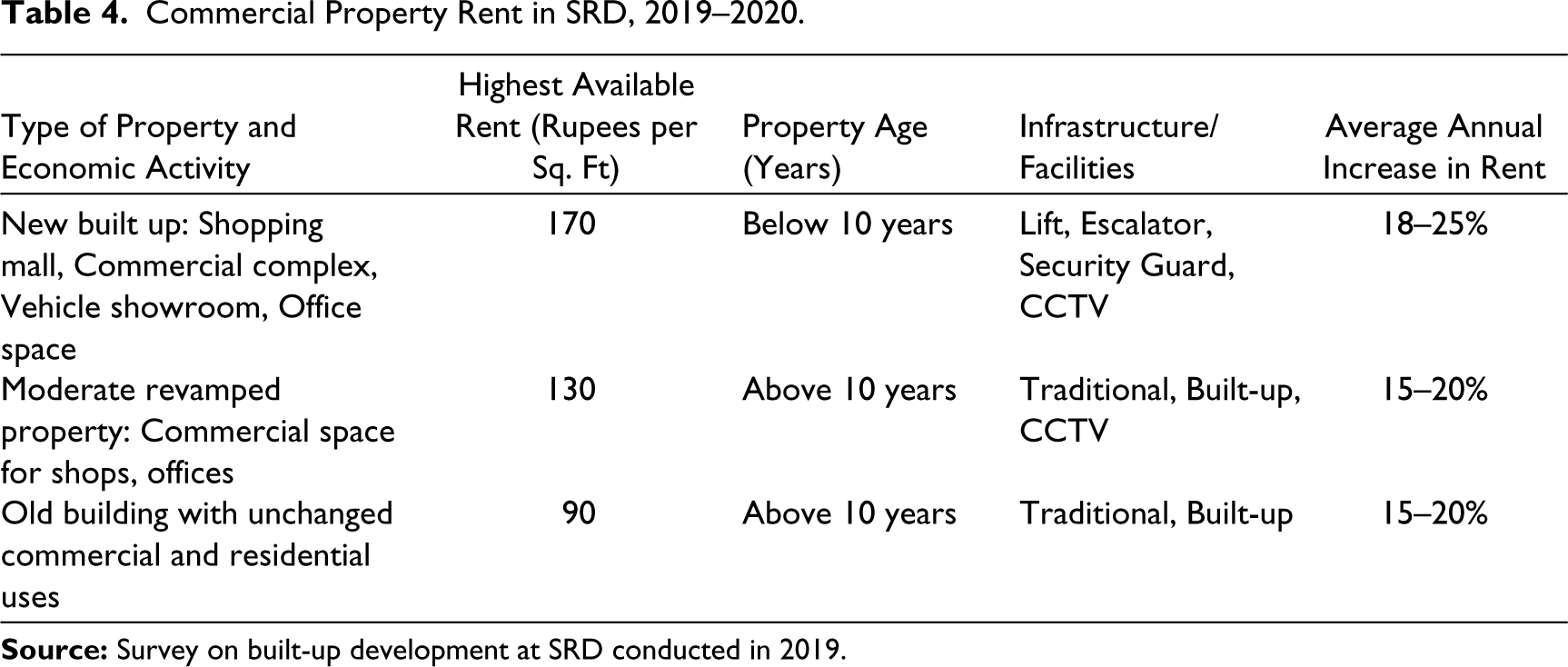

Property Rent and Rentier Capital

In 2019, property rents on SRD reached rupees 170 per square foot for the newly developed prime commercial spaces like shopping malls, showrooms and offices (see Table 4). Commercial rents, irrespective of the property age, have increased annually by 15–20% in SRD from 2010 to 2020. This has led to a massive revamping of older properties by the property owners.

Commercial Property Rent in SRD, 2019–2020.

The interviews with prominent real estate developers provide a valuable account of the flourishing rental market along SRD. Siliguri’s leading real estate developers, said that commercial property demand mainly started rising in Siliguri after 2010.

The commercial rent gradually started rising post 2009–2010 onwards. Siliguri’s first shopping mall started at SRD in 2009–10. Many retail brands started coming up from 2013–2014, which escalated the demand for more commercial spaces and property rents. (A real estate developer)

Business connections soon began to develop between the local propertied class and the country’s expanding globalized consumer economy. The analysis suggests a rising rentier capital in Siliguri’s urban transition, which leads to a massive investment in real estate properties. The following section will further reflect on this.

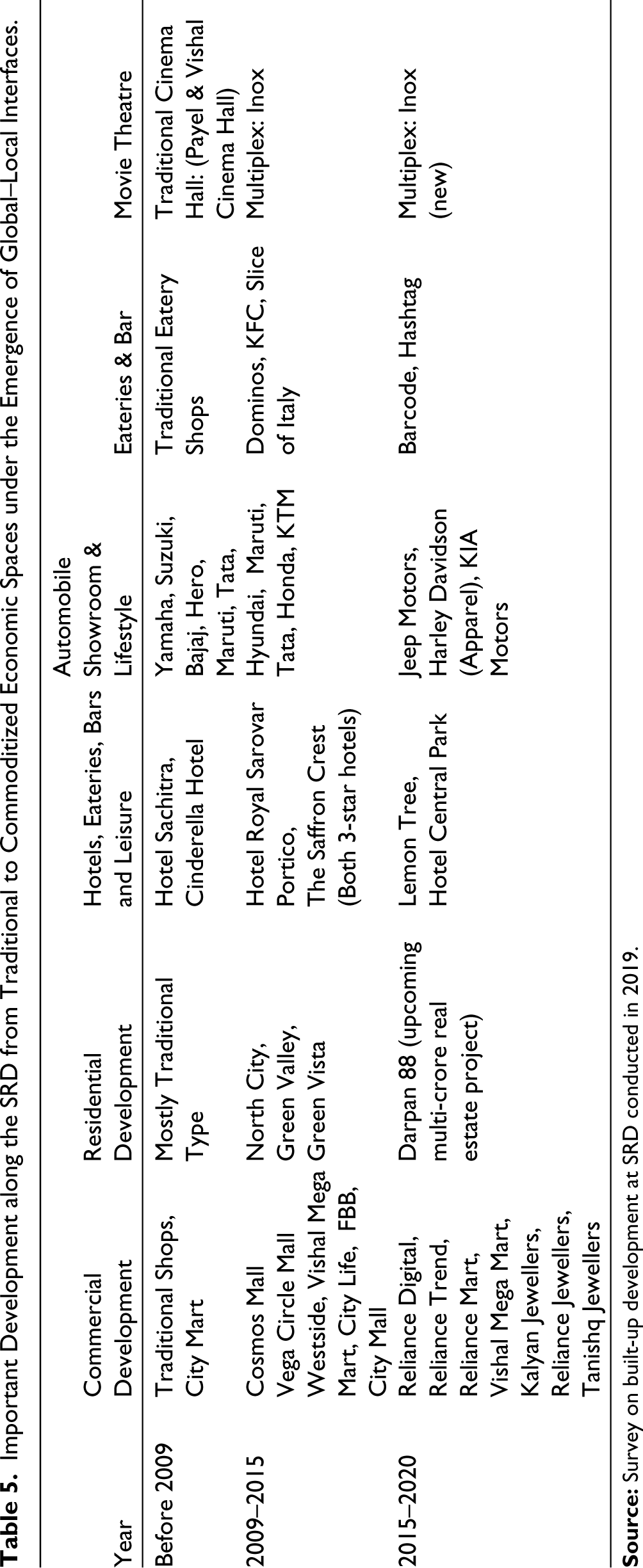

Emergence of New Economic Spaces, Anchoring of Globalized Brands and Rapid Commoditization of SRD

Investing in real estate and anchoring globalized brands are two critical attributes of recent urban change in SRD. Table 5 reflects the nature of commoditization and built-up changes in SRD. Before 2009, most of the built-up and commercial spaces remained traditional, like-local eateries, hotels and cinema halls, as typically found in India’s provincial urban landscape. From 2009–10 onwards, significant commoditization occurred through investment in more buildings and qualitative changes in land or property uses. The emerging economic spaces in SRD include the gradual opening of multiple shopping malls and retail outlets of branded merchandise, a few luxury hotels, vehicle showrooms, restaurants, bars and new offices. Siliguri’s first shopping mall Cosmos Mall started in 2009–2010. The Big Bazaar, the largest hypermarket chain in India, took the lease of one of the most significant real estate properties spread across over 325,000 square feet of area.

Important Development along the SRD from Traditional to Commoditized Economic Spaces under the Emergence of Global–Local Interfaces.

According to the Marketing Manager, Future Group, Cosmos Mall:

This building was just constructed in the year 2009–10. It was developed by a local developer. The developer probably considered building it as a shopping complex, not a mall. The building was well-constructed, well-planned and had a perfect location. It was almost at the city’s heart and connected with national highways leading to hills, the Dooars and Bhutan. Because of its potential, it started as the first mall in Siliguri.

From an investor’s point of view, the Big Bazaar was an immediate hit in Siliguri. It recorded an annual business of over 1 billion rupees immediately after its launch. The average daily footfall in the Cosmos Mall measured over 15,000 in the initial years. In the following years, one by one, multiple shopping malls and merchandise stores of some leading brands started opening. The local investor’s realized the market potential of Siliguri’s burgeoning consumer class and floating commuters from the surrounding regions. The Vega Mall, the city’s second-largest shopping mall, was inaugurated with over 350,000 square feet in 2014. The new mall was owned and operated by the same developer who owns the Cosmos Mall. Enchanted with the success story of the Vega Mall, the manager said:

The mall now provides some of the best luxury brands that only some of Kolkata’s selective malls can offer.

Vega Mall receives a daily footfall of nearly 8,000–10,000 people. It currently offers some of the leading lifestyle brands available only at very selected malls in India. The mall is entirely occupied, with no vacant space available, providing further scope for a new store. In fact, the management had to deny some of the exclusive international brands willing to open stores in Siliguri. The Westside, Vishal Mega Mart, City Life, FBB, City Mall, and many other branded merchandise outlets started to operate on SRD.

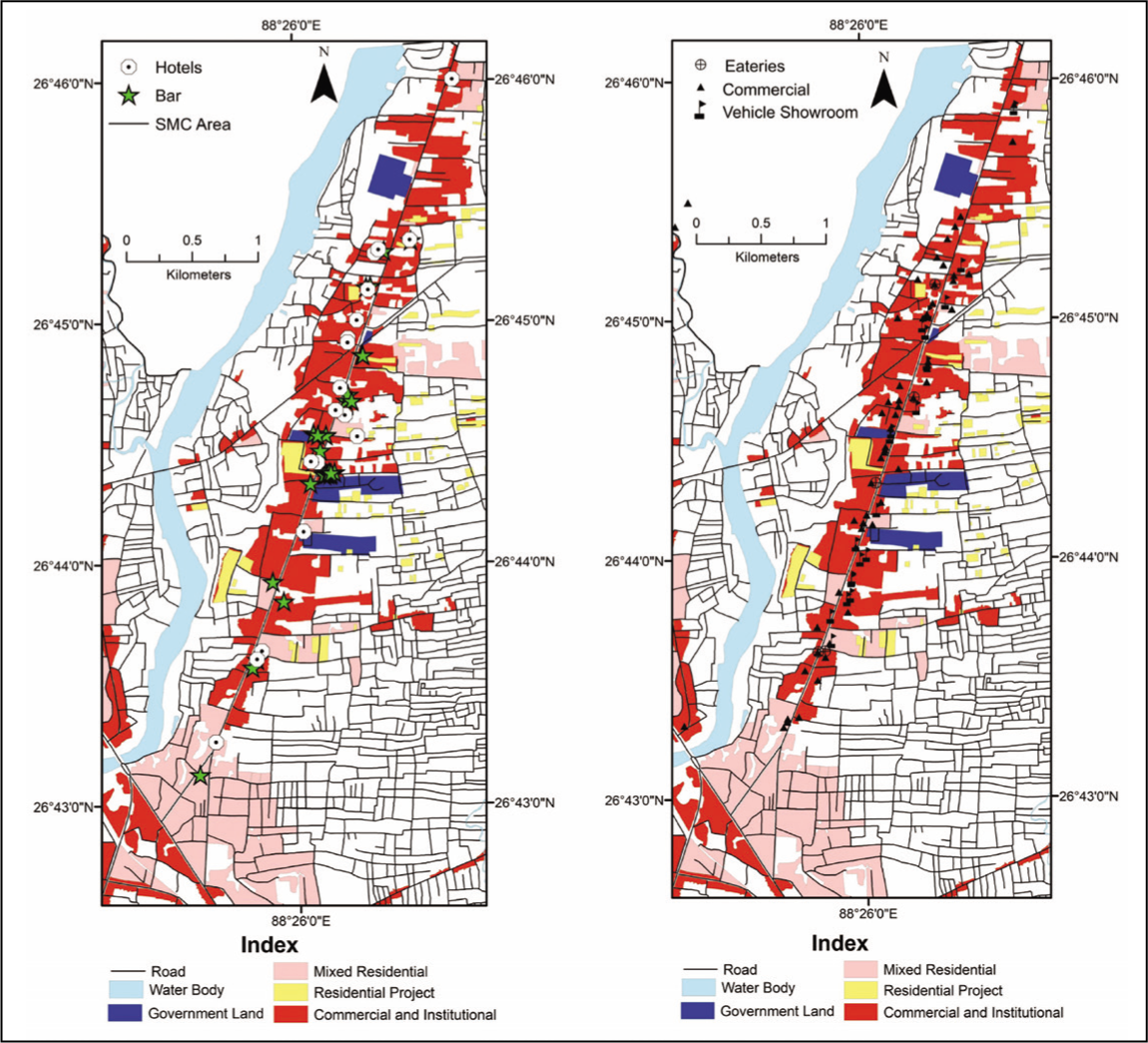

The city’s new star hotel, a 14th-floor residential luxury condominium, was developed in 2015. SRD witnessed more development in shopping malls and real estate in the next 5 years. Three more luxury chain hotels, at least a dozen new branded retail outlets, shopping malls and commercial complexes, new vehicle showrooms, and nearly a half dozen bars all developed and immensely transformed Sevoke Road (Figure 5).

Urban Place-makers in Siliguri

A subset of the survey (N = 48) on built-up development covers information on leading real estate properties and other enterprise’s investment backgrounds at SRD. Table 6 suggests that nearly 65% of investors are of local origin, and 18.8% are corporate sources. The remaining investors are mainly regional (i.e., within North Bengal), inter-state and of other state origin.

Real Estate Investors in Sevoke Road: Type and Origin.

The detailed analysis of in-depth interviews with real estate developers, investors, and franchisers of leading hotels and globalized branded outlets further suggests that Siliguri’s growing real estate industry is mainly driven by local businesses and the propertied class (LBPC). The Confederation of Real Estate Development Agencies India (CREDAI-Siliguri) and the Association of Real Estate Advisors Siliguri, are the city’s two most significant associations for the organized real estate industry. LBPC entirely represents these two organizations. LBPCs are traditionally based on tea planation, trade and transport sectors with substantial possession of accumulated wealth. They significantly influence the city’s economy and are well-connected to local politics and administration. They consider real estate as an emerging business opportunity. The accumulated surplus is hence invested in real estate. LBPC controls floor prices, rent, and types of projects to sustain real estate growth.

Conclusion

The study reflects on the spatially embedded nature of the real estate and new urban transition in a fast-growing MSC. Siliguri’s transition shows hyper real-estate growth, a speculative property market, and rapid built-up development. All are manifested in new urban place-making processes. Unlike any leading megacity, transnational capital networks have played a limited direct role here in developing the city’s real estate. The city’s urban transition has been primarily driven by the local business and propertied class, who saw a business opportunity in growing the real estate market and consumption sector. Local developers also established formal agencies to set market rules, projects and investment decisions. Urban transition is complex and it is important to understand the local social structure and evolving spatial processes. The study argues that urban scholarship must address the social structures, agencies, institutions and geo-historical specificities to comprehend India’s diverse urban transition process under the current wave of globalization in the non-metropolitan cities.

Footnotes

Acknowledgements

I am grateful to Dr Subhanil Chowdhury, Professor Shrawan Acharya, and Professor Sachidand Sinha for their suggestions on this research. Thanks to Siliguri Municipal Corporation, ICLEI for the data support and Radhika Bhanja for the assistance. I am also indebted to the anonymous reviewer for the comments and to the editor of the journal.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.