Abstract

The role of health insurance in expanding Universal Health Coverage is to ease the access to healthcare services and reduce the risk of unexpected health expenditure burden. In order to examine this role, this article assesses the contribution of enrolment in health insurance on the utilisation of healthcare services and out-of-pocket expenditure for working-age Indians. Investigation into these two issues, addressing the self-selection/endogeneity problem in buying health insurance, is uncommon in the literature. Against this end, the probability of utilising healthcare services and the incurred out-of-pocket expenditure has been estimated using National Sample Survey (2017–2018) data in India. Empirical findings reveal evidence of endogeneity in health insurance enrolment for hospitalisation, which indicates the presence of self-selection in health insurance enrolment. Addressing the endogeneity problem, this study has found a higher probability of utilising hospitalisation and lower out-of-pocket expenditure among insured individuals than others. Socio-economic and demographic variables like household income, education, gender, religion and state of residence are important to determine the utilisation of healthcare facilities. On the other hand, while out-of-pocket expenditure incurred for hospitalisation significantly varies with age, gender, social caste, religion, working status, state of residence, nature of ailment and type of hospital, household income and health status have no significant effect on out-of-pocket expenditure. Poor people are less likely to be hospitalised, and compared to males, females have a higher probability of utilising healthcare services at their reproductive age. State-level health policies and health insurance schemes play a crucial role in determining health insurance participation and utilisation of health services.

Keywords

Introduction

Achieving Universal Health Coverage (UHC) is a major target of Sustainable Development Goal 3 (SDG 3) adopted by the United Nations in 2015. Access to healthcare facilities, protection against the risk of healthcare costs and healthcare coverage for everyone are the three major steps each nation needs to follow towards achieving UHC. While access to healthcare defines an individual’s ability to get healthcare services according to need, utilisation of healthcare presumes access and implies the formulation of a healthcare plan during a healthcare encounter. Out-of-pocket (OOP) expenditure is the net expenditure generated after cashless treatment or the reimbursement amount realised from health insurance. Therefore, financial protection can be provided to individuals if their OOP healthcare expenditure can be reduced. Health insurance plays a crucial role, particularly in lower-middle income countries, in improving the utilisation of healthcare among the members and providing protection against financial catastrophe.

Despite the existence of several government-sponsored, employer-supported and private health insurance plans, the rate of enrolment in health insurance programmes for Indians is still less than 20 per cent (NSS report, 2020). Hence, a significant proportion of healthcare spending in India is OOP expenditure. The average OOP medical expenditure spent for treatment in each hospitalisation case was ₹15,937 in rural areas and ₹22,031 in urban areas in 2017–2018 (NSS report, 2020). Against this backdrop, the present study investigates whether the existing health insurance schemes in India are effective in increasing the utilisation of healthcare and providing financial protection against OOP expenditure. The rest of the article has been arranged as follows: We explore the existing literature and find out the specific objectives of the study. Subsequently, we discuss the methodology and data sources and then present the results of the analysis with the importance of the findings, followed by the conclusions of the study.

Literature Review

The effectiveness of health insurance schemes in increasing the utilisation of healthcare and in protecting households from financial catastrophe has been addressed by many researchers across the globe (Dugan, 2020; Erlangga et al., 2019; Hooda, 2017; Jutting, 2003; Sriram & Khan, 2020). Compared to insured individuals, uninsured individuals had 40 per cent lower emergency visits and 61 per cent lower inpatient hospitalisation in the USA (Anderson et al., 2012). Al-Hanawi et al. (2020) have reported that participation in health insurance increases the probability of medical check-ups for people in the Kingdom of Saudi Arabia. A study by Thuong (2020) found that in Vietnam, health insurance caused a rise in both outpatient and inpatient visits in hospitals among enrolled individuals. In a recent study, Helmsmuller and Landmann (2022) have found that the insured individuals more frequently opt for private hospitals in Pakistan. Both private and public health insurance policyholders have reported higher use of physician services compared to the uninsured; however, the use of emergency care is lower among privately insured individuals than publicly insured individuals (Dugan, 2020).

Several community-based health insurance programmes have been found effective in increasing hospitalisation and lowering expenditure among the poor and informal sector people in developing countries (Galarraga et al., 2010; Jutting, 2003). Improved health schemes should be developed with expanded benefit packages and redesigned cost-sharing policies (Li et al., 2014, 2012). Expansion of health insurance coverage benefits the poorer sections of society as well as individuals who incur large health expenditures (Tirgil et al., 2019). Jowett et al. (2004) concluded that though health expenditures are affected by income, these expenditures can be reduced in significantly higher proportion among the poor members than the rich members of health insurance. Wirtz et al. (2012) observed that in Mexico, the major component of OOP expenditure, which is expenditure on medicine, can be reduced by purchasing health insurance, though the extent of reduction varies across the types of insurance plans. Both contributory and non-contributory insurance have caused an increase in the number of hospital visits in antenatal care and a reduction in average OOP expenditure in Indonesia (Aizawa, 2019). Kronenberg and Barros (2013) suggested that OOP expenditure related to medical care should be exempted to protect vulnerable groups from catastrophic healthcare spending in Portugal.

A handful of studies in India have reported that enrolment in government-sponsored health insurance schemes increases the incidents of inpatient healthcare use among poor individuals (Selvaraj & Karan, 2012; Sriram & Khan, 2020). Conducting a study in Birbhum district in West Bengal, Mukherjee (2005) reported that participation in a private health insurance scheme improves access to formal healthcare services and reduces OOP expenditure. On the other hand, government-sponsored schemes have not been found effective in reducing catastrophic health expenditure and impoverishment in India (Fan et al., 2012; Shahrawat & Rao, 2012). Rashtriya Swasthya Bima Yojana (RSBY) (2008), the largest central government-sponsored scheme before the implementation of Pradhan Mantri Jan Arogya Yojana (2018), has been criticised in respect of its low coverage ratio and inappropriate usage patterns (Taneja & Taneja, 2016). According to Shahrawat and Rao (2012), protection of poor people from impoverishment would not be possible without providing insurance coverage for medicine and outpatient care for the poor and near-poor. Sriram and Khan (2020) also advocate that coverage of health insurance should be extended to outpatient services as well, to reduce the overconsumption of inpatient usage. Both insurance coverage and hospital care usage are lower among women having chronic health diseases and vulnerable community people, such as elderly people, compared to their counterparts. Whereas, compared to urban people, rural people have lower enrolment in health insurance but higher use of healthcare in India (Sengupta & Rooj, 2019). Moreover, OOP expenditure varies for the nature of the ailment; the probability of incurring distress financing in India is very high among patients with cancer and tuberculosis (Kastor & Mohanty, 2018).

Another factor that must be addressed while analysing the use of healthcare facilities is the problem of information asymmetry in the enrolment of health insurance schemes. People having poor health status are more likely to enrol in health insurance (Wang et al., 2006), which may lead to adverse selection and moral hazard in the insurance market (Sengupta & Rooj, 2019). Waters (1999) obtained that people working in the formal sector with severe illness prefer to opt for private healthcare services and self-select themselves in health insurance programmes; this selection bias leads to an endogeneity problem. In Chile, the independent and dependent workers self-select themselves for private and public insurance, respectively, whereas the event of moral hazard among insured individuals is significantly high in terms of medical visits (Sapelli & Vial, 2003). However, some studies have not obtained any evidence of self-selection in health insurance enrolment in relation to the probability and cost of hospitalisation (Jutting, 2003; Mukherjee, 2005).

Research Gap and Objectives of the Study

Most of the studies in India have explored whether participation in public health insurance schemes accelerates the utilisation of healthcare among the poor or not. However, the effectiveness of health insurance should be explored not only for the poor but also for individuals of different income levels. Moreover, the existing government-sponsored health insurance schemes target the poor as well as the non-poor households. Some state-sponsored health schemes have been implemented exclusively for poor households, for example, Bhamashah Swasthya Bima Yojana in Rajasthan provides health insurance coverage for BPL families. Dr. YSR Aarogyasri scheme of the Government of Andhra Pradesh (2020) serves households having an annual income of up to five lakh rupees. Again, a permanent residential certificate, not income, is the eligibility criterion for enrolment in the Swasthya Sathi scheme of the Government of West Bengal (2016). While Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY), launched by the Government of India, aims at providing health coverage to the families that form the bottom 40 per cent of the Indian population, the erstwhile RSBY was for the BPL population only. Further, there exist several government-employer supported schemes such as Employee’s State Insurance Scheme (ESIS), Central Government Health Scheme (CGHS), as well as health schemes supported by private employers to cover employees and their dependents; these types of schemes are mandatory for the employees in most of the cases. Furthermore, individuals may purchase health insurance coverage from insurance companies by paying the premium.

Self-selection in joining a health insurance plan, which is one of the potential causes of information asymmetry in the insurance market, is not much explored by the literature in the Indian context. Some unobservable factors like the health condition of the individuals, choice of joining the insurance and eligibility for being enrolled in the health insurance are the main reasons behind this selection bias. The individuals who self-select themselves into health insurance have a higher probability of utilising healthcare facilities. Therefore, in the presence of self-selection bias, the actual effect of health insurance becomes overestimated, which ultimately leads to the problem of endogeneity. The present study considers enrolment in government-sponsored schemes as well as voluntary health insurance schemes. The membership of employer-supported health insurance plans has been excluded from our analysis as it is a mandatory enrolment for employees and their families in most of the cases, so this type of insurance does not indicate any self-selection in enrolment. Against this backdrop, this study has the following objectives: First, this study examines the presence of self-selection, if any, in the decision to enrol in health insurance schemes affecting the individual’s behaviour of utilising healthcare services and its expenditure. In addition to that, we explore the socio-economic and demographic factors affecting the decision to take enrolment in the health insurance schemes. If the enrolment in a health insurance plan is endogenous, we would address the problem. Finally, we study the effect of enrolment in health insurance, along with some socio-economic and demographic factors, on getting access to healthcare facilities and its expenditure in India.

Methodology and Data Source

Like the studies (Jutting, 2003; Mukherjee, 2005; Wang et al., 2005; Waters, 1999), this study has developed a two-part model, where the first part deals with the estimation of the utilisation of healthcare services, and the second part focuses on estimating the expenditure of healthcare for those who have had accessed the service. In the first part, a probit model will be constructed to estimate the probability of utilising formal healthcare, which is captured by the binary variable ‘whether the individual has been hospitalised at least once during the last year or not’. In the second part, a log-linear model will be framed to assess how the health insurance policy holding reduces OOP expenditure of individuals who have been hospitalised in the last 1 year. The OOP expenditure is calculated as the difference between the direct medical expenditure incurred by the individual during hospitalisation and the reimbursement amount by the insurance provider.

A handful of studies (Jutting, 2003; Mukherjee, 2005; Waters, 1999) have addressed the issue of endogeneity in evaluating the effects of health insurance on getting healthcare access and its expenditure. This endogeneity is caused because of the omitted variable bias in the model due to the presence of self-selection by some individuals in the health insurance and thus, the observed effect of the health insurance enrolment on the utilisation and expenditure of healthcare does not reflect the true effects. To investigate how the purchase decision of health insurance affects getting access to healthcare and its expenditure, we first examine whether the health insurance enrolment is exogenous or not, following a methodology applied by Waters (1999) and later used by Jutting (2003). In this method, initially, a reduced-form equation for enrolment in health insurance will be estimated. From this equation, the predicted values of enrolment will be obtained. Then, both the predicted and observed values of health insurance enrolment will be taken as explanatory variables in the equations of estimating the effect of health insurance on healthcare utilisation and healthcare expenditure. If the coefficient of ‘predicted enrolment’ is obtained as significant, the health insurance enrolment is endogenous; otherwise, it is exogenous. Hence, to test the exogeneity of the enrolment variable, we first explore which factors affect the choice of enrolling in a health insurance scheme. The decision to purchase a health insurance plan by an individual is a binary variable that takes the value ‘one’ if the individual has a health insurance policy and ‘zero’ otherwise. This study formulates a binary probit model where the outcome variable is whether the individual has purchased health insurance or not.

The socio-economic and demographic factors, such as household income, health status, age, gender, educational level, marital status, religion, caste, occupation, household size, sector and state the person resides in, affect the decision to purchase health insurance (Jutting, 2003; Mukherjee, 2005). On the other hand, household income, age, gender, education level, marital status, religion, caste, occupation, sector and state the person resides in, along with the enrolment of health insurance scheme, determine the probability of utilising the hospitalisation facility when the situation arises and the OOP expenditure. Some other variables such as duration of stay in the hospital, nature of the disease for which the person is hospitalised, and whether the person is hospitalised in public or private medical institutions also affect the OOP expenditure (Sriram & Khan, 2020). We now specify the variables selected for the present analysis.

Decision to get health insurance enrolment (HIE): It is a dichotomous variable indicating value ‘one’ for the individuals currently enrolled in any health insurance scheme; otherwise, ‘zero’.

Hospitalisation of individuals (HOSP): It measures the utilisation of formal healthcare facilities by the individual, which takes the value ‘one’ for the individual who experienced hospitalisation at least once during the last 365-day period, and ‘zero’ otherwise.

Out-of-pocket expenditure (OOPE): We construct the OOP expenditure for healthcare as the medical expenditure (including the package component, doctor’s fees, costs of medicines and diagnostic tests, bed charges) incurred by the person during the last 365 days (including multiple events of hospitalisation) over the total reimbursement by the health insurance provider. It is a continuous variable measured in rupees. The log of the OOPE has been taken as the outcome variable in the second part of the analysis.

Per capita household income: The income effect on having access to healthcare and its expenditure must be analysed like the demand function of any goods and services. Since the data on income are not available, expenditure is taken as a proxy for income. National Sample Survey (NSS) provides data on a household’s usual monthly consumption expenditure, which has been converted into monthly per capita household consumption expenditure (MPCE) by dividing it by the respective household size. The present study considers the log of per capita monthly expenditure, which is suitable for measuring the diminishing marginal effect of income on demand for healthcare services and income elasticity of OOP expenditure.

Age of the individual (AGE): It is expected that as age increases, the utilisation of healthcare increases among people. On the other hand, as age increases, enrolment in health insurance diminishes, for which OOP expenditure is likely to be high among the elderly. In order to examine these assumptions, this study incorporates age and square of age (in years) as explanatory variables in the analysis.

Gender: NSS data (2017–2018) have reported three categories for the gender of the individuals: male, female and transgender. As the number of transgender is only 0.01 per cent in the sample, this study takes one dummy for gender, indicating ‘one’ for female (FEM) and ‘zero’ otherwise. The study takes an interaction variable between gender and age (FEM*AGE) to assess how the outcome variables change with respect to the simultaneous change in age and gender.

Official caste: The official caste of a person is a categorical variable that states the person as belonging to a specific official caste, that is, General Castes, Other Backward Classes (OBC), Scheduled Castes (SC) and Scheduled Tribes (ST). Therefore, three dummies have been used, where General Caste individuals are taken as the reference category.

Religion: The study has formulated four dummies for the religious status of the individuals: Muslim (MUSLIM), Christianity (CHRIST), Sikhism (SIKH) and other religions (including Buddhism, Jainism, Zoroastrianism and others) (ORELG), respectively, taking Hinduism as the reference category.

Marital status: Marital status is taken as a categorical variable with different categories, namely currently married, never married, widowed and separated. Since the number of widowed and separated are only 4.65 per cent and 0.27 per cent in the sample, the study takes one dummy (MARRIED) for marital status, which takes the value ‘one’ if the individual is currently married and ‘zero’ otherwise.

Education: To examine the effect of education standards on healthcare access and its expenditure, we categorise the education level of the individuals. Considering ‘Graduation or equivalent and above’ as the reference category, six dummy variables have been constructed, namely ‘Not literate (NLIT)’, ‘Below primary (BPRIM)’, ‘Primary (PRIM)’, ‘Middle school (MSCHL)’, ‘Secondary or equivalent (SECOND)’ and ‘Higher secondary or equivalent (HS)’.

Principal activity status: Principal activity status implies the activity in which the individual has spent major amount of time in the last 365 days. The categories of usual activity status have been combined into the following categories, namely ‘Salaried employee’, ‘Self-employed individuals (SELFE)’, ‘Casual workers (CWORKER)’, ‘Unpaid family workers (UPWORKER)’, ‘Individuals attending some educational institutions (AEDU)’, ‘Pensioners and/or remittance recipients (RETD)’, ‘Individuals performing domestic duties (PDOD)’ and ‘Persons having other occupations (begging etc.) (OOCC)’. Seven dummies have been included for principal activity status, with ‘Salaried employee’ as the base category.

Household size: The household size is taken as a binary variable (HSIZE), which takes the value ‘one’ if the size of the household the individual belongs to is greater than five and ‘zero’ otherwise. Household size can be considered as a proxy for the cost of insurance; the larger the household size, the higher will be the premium paid to purchase health insurance.

No chronic ailments: To control the self-selection bias in health insurance purchase, we need to incorporate health status as an explanatory variable in the model. Chronic health disease is an indicator of health status. A dummy variable has been created considering value ‘one’ if the individual does not have any chronic ailment (NCA) and ‘zero’ otherwise.

Type of medical institution: The analysis considers a dummy variable for this factor, which takes the value ‘one’ if the admission has been taken in a government hospital (GHOS) and ‘zero’ otherwise (private or NGO-run hospitals).

Sector: The binary variable for a sector (RURAL) takes the value ‘one’ if the person resides in a rural area and ‘zero’ otherwise.

State of residence: State dummies (SDUM) have been considered in the present studies with twenty-six states, while all other states like Jammu & Kashmir and union territories (UTs) are taken as reference categories. Clustered-standard errors across states have been considered to perform each regression analysis.

Duration of hospitalisation: This is a discrete variable that measures the total number of days spent by the person for inpatient care in a hospital (DHOS).

Nature of ailment: NSS (2017–2018) data have reported a number of ailments for which people have been hospitalised during the last 365 days. We have constructed dummy variables for the following diseases: Psychiatric and neurological (PSYNEU), Cancers (CANCER), Cardiovascular (CARVAS), Gastrointestinal (GASTRO), Musculoskeletal (MUSC), Injuries (INJR) and Obstetric (OBST). All other ailments are taken as the reference category.

The probability of health insurance enrolment has been estimated by Equation (1):

Equation (2) gives the model for the probability of hospitalisation of an individual:

The model for the OOP expenditure for the hospitalisation case is given by Equation (3):

Some researchers (Waters, 1999; Winkelmann, 2012) have used bivariate probit model to address the issue of endogeneity in health economics. In our study also, if health insurance enrolment is found to be endogenous in the equation of hospitalisation, a seemingly unrelated bivariate probit model is formulated with Equations (1) and (2). The presence of endogeneity indicates that the unobservable factors that affect health insurance participation also influence the probability of getting access to healthcare. Therefore,

The 75th round NSS data (2017–2018) of the Household Social Consumption Survey (Health), a nationally representative data set, have been used to perform the analysis in the present study. Our sample consists of 357,195 individuals who belong to the working-age population (15–64 years). However, some individuals were hospitalised more than once during the last 365 days. Some factors like the nature of the ailment and the type of hospital where treatment has been made are expected to differ for the multiple hospitalisation cases. To capture the effect of health insurance on OOP expenditure, we consider the data set of hospitalisation events, which consists of 67,616 data points. Therefore, for Equations (1) and (2), the number of individuals is 357,195, and for Equation (3), the number of hospitalisation events is 67,616.

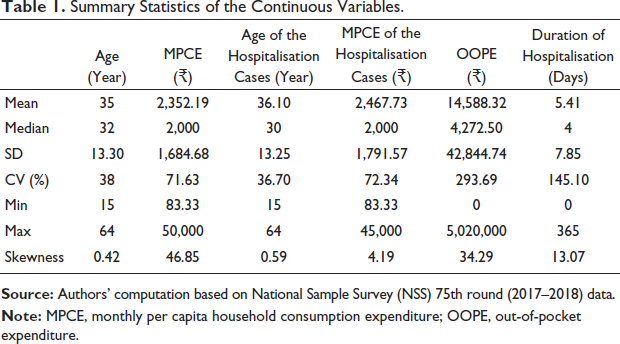

Table 1 reveals that the mean age of the respondents for the full sample is nearly 35 years, while the median age is 32 years. Therefore, the proportion of the younger population is higher in our sample. The average MPCE is ₹2,352.19, which is greater than the median MPCE. The OOP expenditure for hospital admission takes the mean value of ₹14,588.32 and varies widely across different events of hospitalisation. The mean age of hospitalisation is nearly 36 years, while the mean MPCE of the hospitalised person is ₹2,467.73. The average duration of stay in hospital for hospitalised persons is 5 days, which ranges from 0 to 365 days.

Summary Statistics of the Continuous Variables.

Summary Statistics of the Continuous Variables.

The proportion of insurance enrolment among the working-age Indians is only 14.84 per cent, despite the availability of several government-sponsored free health insurance schemes (Table 2). Among them, 13.01 per cent of individuals are covered by government-sponsored schemes and the rest 1.83 per cent of people are enrolled in the voluntary health coverage plans arranged by the households (Table 2). Table 2 shows that the proportion of hospitalisation is higher among the individuals who joined a health insurance scheme relative to the individuals without health insurance. Relative to others, persons having chronic diseases have much higher participation in health insurance schemes. However, the joining rate of women is slightly higher than that of men. Among the respondents following different religions, Christians and Sikhs, respectively, have the highest and the lowest proportion of participation in different health insurance plans. The individuals from the tribal community have a higher rate of insurance enrolment than others. The percentage of enrolment in health insurance is slightly higher among the people having lower educational qualifications compared to the people with higher educational qualifications. The informal sector workers and retired persons have a higher joining rate in the health insurance programme than the others. People residing in rural areas have higher enrolment in health insurance. It may be a consequence of the extensive implementation of government-sponsored free health schemes across the states.

Frequency Distribution of the Categorical Variables (n = 357,195).

The proportion of hospitalisation among insured individuals is 19.90 per cent, which is higher than that of the individuals who are not insured (Table 2). As expected, individuals having chronic ailments have been hospitalised more than their counterparts. Compared to males, the occurrence of hospitalisation is higher among females which due to the event of childbirth (Table 2). For different categories of education, the proportion of hospitalisation is also different. Among people belonging to different activity statuses, pensioners, persons performing domestic duties and persons of other working statuses have higher events of hospitalisation (Table 2). The average MPCE is higher among those who are enrolled in health insurance schemes. It indicates that rich people are more likely to purchase a health insurance policy. The mean OOP expenditure is higher among the non-insured group compared to the insured group (Table A1). Average OOP expenditure is significantly higher among the non-insured group compared to the insured group for the hospitalisation cases of cancers, musculoskeletal, injuries and infectious diseases (Table A2).

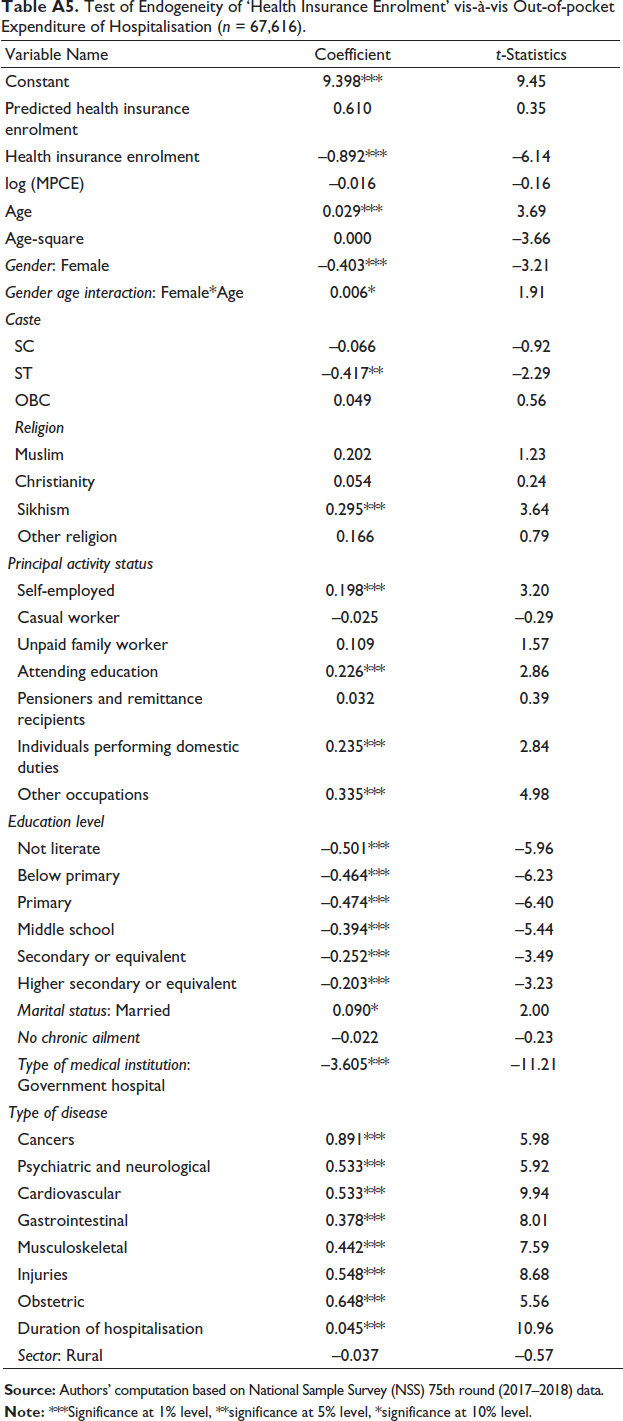

In order to examine the exogeneity of the enrolment in health insurance, we first estimate Equation (1) for enrolment in health insurance. The results of the probit model formulated for this purpose have been presented in Table A3. Then, the predicted probability of insurance enrolment has been calculated from this model. The predicted probabilities can take any value between zero and one. After that, both the predicted and the observed values of the insurance enrolment variable have been taken as regressors in Equations (2) and (3), that is, as a regressor in the two separate models of estimating the healthcare utilisation and the OOP expenditure. The coefficient of the predicted enrolment has been obtained as significant in the equation of estimating the utilisation of healthcare (Table A4), which indicates that the health insurance enrolment is endogenous in determining the use of healthcare services. However, the coefficient of the predicted enrolment has been found insignificant in the equation of estimating the OOP expenditure of hospitalisation (Table A5), and we can conclude that the insurance enrolment is an exogenous variable while estimating the OOP expenditure for hospitalisation. The OOP expenditure is expected to be lower among the participants of health insurance; however, enrolment in health insurance is not determined by the OOP expenditure for hospitalisation. There is no two-way relationship between health insurance enrolment and the extent of OOP expenditure, and hence, health insurance participation is found to be exogenous in the OOP expenditure mode, which has also been found by a few literature (Jutting, 2003; Mukherjee, 2005).

The presence of endogeneity has been addressed by estimating a bivariate probit model with Equations (1) and (2), where Equation (2) is taken as the primary equation and Equation (1) is considered as the reduced-form equation, that is, the secondary equation.

Bivariate Probit Regression for Hospitalisation and Endogenous Health Insurance Enrolment (n = 357,195).

Let us now explain the results of the bivariate probit model (Table 3). We have obtained ρ, the correlation coefficient between the error terms of the two equations, which is statistically significant, indicating that health insurance enrolment has been considered as an endogenous regressor. The coefficient of health insurance enrolment is positive and statistically significant after addressing the endogeneity problem through estimating the bivariate probit model. The marginal effect of health insurance enrolment shows that the probability of access to healthcare services is 16 percentage points higher for insured persons compared to that for non-insured persons. Now, we need to discuss other socio-economic factors that affect the likelihood of an individual being hospitalised. MPCE, which is taken as a proxy for household income, significantly affects the probability of hospitalisation of the individual if necessary. Keeping all other variables constant, an increase in MPCE by 10 percentage points causes a rise in the average probability of utilising healthcare services by 0.37 percentage points. Females have a higher average probability of hospitalisation than males, but this reduces as the age of the females increases. The proportion of younger women is higher in our sample, and also, we have seen that 38.88 per cent of hospitalisation cases are on account of childbirth (Table A2). Therefore, females have a higher rate of hospitalisation at their reproductive age. Among individuals of different religious communities, compared to Hindus, Muslims and Sikhs have a lower likelihood of hospitalisation if necessary. However, the people of the SC community have a higher average predicted probability of hospitalisation. People belonging to different working classes have a higher average predicted probability of taking hospital admission than salaried employees, while married people take more hospital admissions than others. Compared to the persons having graduation level education, individuals with lower levels of education have a higher average probability of getting hospitalised in case of health encounters. We have found that compared to urban people, rural people are more likely to use hospital services. This has been made possible largely because of the implementation of the National Rural Health Mission (NRHM) programs in 2005 long before the implementation of the National Urban Health Mission (NUHM) programs in 2014. The main NRHM program, such as the Janani Suraksha Yojana, a conditional cash-transfer scheme, encourages rural women for giving child birth at hospitals. Moreover, limited opportunities to visit medical professionals in outdoor clinics, rural people mostly try to get access to inpatient healthcare. Among the effects of included state dummies (SDUM), which have not been reported in table, the highest average probabilities of hospitalisation have been found for two states: Tamil Nadu and Odisha. These findings justify the arguments of high-level health awareness and wide availability of healthcare facilities in Tamil Nadu, while Odisha is coming up as an emerging state with good healthcare services in eastern India.

Now we explain the second part of the bivariate probit model, which estimates the probability of enrolment in health insurance. The higher the income of the individual, the higher the average probability of being enrolled in health insurance schemes. Keeping all other variables unchanged, a 10 percentage point increase in MPCE causes a 0.29 percentage point increase in the average predicted probability of joining health insurance. Compared to those who have any chronic health disease, persons with no chronic health problems have a five percentage point lower average probability of purchasing health insurance. Therefore, health status is a more important factor than income in deciding the demand for health insurance. The impact of age is insignificant in determining the probability of health insurance enrolment, but as the age increases, females have a higher probability of taking health insurance than males, which indicates the success of the implementation of female-specific free government-provided insurance schemes. The predicted probability of enrolment in health insurance is lower for Muslims than Hindus, and higher for ST people than General Caste people. The likelihood of joining increases as the level of education attained by a person increases. Casual workers and self-employed people have a higher probability of health insurance enrolment than the salaried employees’ category. Furthermore, people residing in rural India have a higher likelihood of enrolment in health insurance schemes. These results confirm the wide and effective implementation of different government-sponsored free health insurance schemes across the states, particularly in rural areas. However, marital status and household size have no significant effect on the decision to purchase health insurance. Taking states like Jammu & Kashmir and the UTs as the reference category, a higher likelihood of health insurance enrolment has been found in states such as Kerala, Rajasthan, Chhattisgarh, Telangana and Andhra Pradesh. Apart from RSBY, these states have implemented state-sponsored health insurance schemes. The health infrastructure is well-developed, and health consciousness among the people is high in Kerala. Moreover, there exist free health schemes like Karunya Arogya Suraksha Padhathi (KASP) in Kerala. Different state-funded health schemes like Dr. YSR Aarogyasri scheme of the Government of Andhra Pradesh (2020), Bhamashah Swasthya Bima Yojana in Rajasthan and Aarogyasri of Telangana are the reasons for the higher probability of health insurance enrolment in these states.

Log-linear model for Estimating Out-of-pocket Expenditure (OOPE) of Hospitalisation (n = 67,616).

Next, we interpret the estimate of the OOP expenditure incurred for inpatient hospitalisation (Table 4). The coefficient of health insurance enrolment is negative and statistically significant, which implies that for insured people, the OOP expenditure for hospitalisation is 88 per cent lower than that for non-insured people. However, household income and health status have no significant effect on the OOP expenditure for hospitalisation. OOP expenditure increases with the age of the individuals. For females, the OOP expenditure incurred is lower than for males; however, as the age increases, females suffer from more OOP expenditure than males. However, although the chance of hospitalisation for elderly women is lower than that for elderly men, they have to bear a higher amount on account of OOP expenditure than elderly men. Among different official castes, individuals belonging to the General Caste face higher OOP expenditure than the other categories. Among different religious communities, only Christians spend a lower proportion of OOP expenditure than Hindus, which follows from a higher rate of insurance purchase of the Christian community people. Compared to salaried people, people having different employment statuses have a higher OOP expenditure. Compared to the individuals belonging to the highest category of education, others incur a lower OOP expenditure. Again, marital status and sector of residence of a person do not have a significant effect on the extent of OOP expenditure. As we expect, the OOP expenditure incurred is significantly lower for the patients in government hospitals. The OOP expenditure varies across the nature of diseases. The persons who received treatments for cancers, cardiovascular diseases, injuries, obstetric problems and others have suffered from a higher burden of OOP expenditure. The average OOPE of the hospitalization cases is lowest in Tamil Nadu followed by Delhi compared to the reference state and UTs. Improved healthcare facilities, including government-provided healthcare services, in these states is the main reason for lower OOP expenditure in these states.

The main contribution of this study is the investigation of the effect of health insurance enrolment on the probability of hospitalisation as well as on the extent of OOP expenditure, addressing the problem of endogeneity in health insurance enrolment in India. Considering a two-part model, the present study assesses the effectiveness of health insurance in increasing the utilisation of healthcare and reducing the OOP expenditure for healthcare among working-age Indians of different economic backgrounds. While the government-sponsored health schemes cover both poor and non-poor sections, middle-income and high-income people arrange voluntary health insurance from insurance companies. Unlike employer-supported schemes, other health insurance are non-mandatory in most of the cases; hence, participation in health insurance schemes is determined by some unobservable factors along with socio-economic and demographic factors. Our analysis indicates that several factors, namely household income, health status, religion, social category, activity status, education and state of residence, significantly affect the probability of joining health insurance schemes. However, the effect of health status is strongest among all factors; persons having chronic ailments enrol themselves more in health insurance schemes. The higher participation of this type of people may lead to the problem of self-selection in health insurance participation in the use of healthcare and in reducing the OOP expenditure of healthcare usage. Empirical findings in our study indicate the presence of endogeneity in health insurance enrolment with respect to healthcare utilisation. Therefore, people who know that their likelihood of hospitalisation is high, self-select themselves in health insurance and become hospitalised during a health encounter. The presence of self-selection or endogeneity over-estimates effects of enrolment in insurance program on health care utilisation. This problem has been addressed by estimating the bivariate probit model for utilisation of health care and enrolment in health insurance. However, the study has not found endogeneity in health insurance enrolment in determining OOP expenditure of hospitalisation. Finally, this study finds that enrolment in health insurance significantly accelerates access to formal healthcare services and sufficiently protects people from the catastrophic burden of healthcare costs in India. While household income directly affects their probability of hospitalisation, the OOP expenditure incurred by the persons does not depend on the income level. Women at their reproductive age incur higher hospitalisation as well as high OOP expenditure on the account of childbirth. Compared to Hindus, the Muslim population has a lower likelihood of purchasing health insurance, which has been found by previous researchers also (Chakrabarti & Shankar, 2015). A significantly high participation in health insurance and lower OOP expenditure has been observed for the ST community in India, which may be a consequence of the implementation of government-sponsored schemes in the tribal belts. Education acts as a significant driver of taking the decision to purchase health insurance. In our model, household size has been taken as a proxy for the cost of health insurance; however, the study has not found any significant impact of household size on health insurance purchase. Moreover, there exists inter-state variation in health insurance participation, hospitalisation and OOP expenditure incurred for hospitalisation. As a consequence of the central government-sponsored health scheme like RSBY and other schemes launched by the state governments, the likelihood of health insurance participation is higher in a few Northeastern and Southern states. Again, in the states having better public infrastructure, we can observe higher rates of hospitalisation events and lower OOP expenditure for hospitalisation. Admission to government hospitals is a crucial factor in lowering OOP expenditure. Finally, the nature of the disease plays a significant role in deciding the OOP expenditure; the health insurance does not create a significant difference in the OOP expenditure incurred between the insured and non-insured groups for some diseases.

Conclusion

Health insurance is definitely an important tool in removing the inequality in utilisation of healthcare services particularly in the lower- and lower-middle-income countries. Our analysis, based on the unit-level data of NSS (2017–2018), reports evidence of endogeneity in the health insurance enrolment with respect to hospitalisation for working-age Indians. The estimates addressing endogeneity clearly show that enrolment in health insurance significantly increases the utilisation of healthcare and reduces the OOP expenditure for hospitalisation in India. Higher-income people have a higher ability to get health insurance enrolment and to utilise formal healthcare services. From our estimates, we can say that people having chronic diseases tend to join health insurance more, which should be identified and addressed by the health insurance provider in order to improve the effectiveness of health insurance. Hence, the premium component is to be decided carefully for persons having bad health status to reduce the problem of self-selection in health insurance. On the other hand, the OOP expenditure for hospitalisation is a burden for both poor and non-poor people of Indian society. This OOP expenditure is higher for severe diseases like cancers and significantly higher in hospitals other than public medical institutions. Hence, better implementation of government-sponsored health insurance schemes for all is the first step towards increasing affordable healthcare facilities across the regions. In this regard, special focus should be given to increasing the health insurance coverage for the poor and the aged people of the country. Some low-cost health insurance schemes must be introduced by the government or public insurance companies for the benefit of the middle- and lower-middle-income population to protect them from the burden of OOP expenditure. Moreover, the health infrastructure, particularly the government health facilities, must be improved so that people can get access to healthcare facilities according to their needs. However, some other relevant behavioural factors that can affect health insurance participation, like insurance literacy, attitude towards health insurance and perceived risk related to health insurance, have not been incorporated into the analysis as these variables are not available in the NSS data set. Exploring these behavioural factors would be an extension of this study towards designing the appropriate health insurance scheme and expanding health insurance participation in India.

Appendix

Mean Difference of Some Continuous Variable for the Non-insured Versus Insured Group for Different Hospitalisation Cases (n = 67,616).

Frequency and Mean Difference of Out-of-pocket (OOP) Expenditure for Different Ailments for the Non-insured Versus Insured Group for Different Hospitalisation Cases (n = 67,616).

Determinants of the Enrolment in Health Insurance Schemes (n = 357,195).

Test of Endogeneity of ‘Health Insurance Enrolment’ vis-à-vis Hospitalisation (n = 357,195).

Test of Endogeneity of ‘Health Insurance Enrolment’ vis-à-vis Out-of-pocket Expenditure of Hospitalisation (n = 67,616).

Footnotes

Acknowledgement

The authors are grateful to the editors and the anonymous referees for their valuable comments and suggestions. The authors acknowledge the National Sample Survey Organisation (NSSO) for making available the NSS 75th round data on ‘Household Social Consumption: Health’ for further research.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.