Abstract

The need for the European Union to get involved in unemployment insurance has frequently been debated in the past decade, starting from exploratory discussions and eventually becoming a political commitment by the European Commission President. This article looks back at the origins of the idea of an EU-level unemployment benefit scheme and explains the political dynamics of the concept’s evolution. Following the 2009 Great Recession and the subsequent eurozone debt crisis, a new movement for a reinforced social dimension has been pushing the EU beyond its previous red lines. The case for counter-cyclical social stabilisation at EU level is now a touchstone for a materially meaningful EU social dimension. The COVID-19 crisis triggered a giant leap to a greater EU budgetary capacity, including financial support for job-saving schemes. This article argues that these new instruments will not suffice without also creating an EU safety net for those whose jobs cannot be saved in a period of economic downturn.

In memoriam Henrik Enderlein

Introduction

The need for the European Union to get involved in unemployment insurance has frequently been debated in the past decade, with greater or lesser intensity. The case is not self-evident from either the legal or the financial points of view. The shocks of the Great Recession and the eurozone debt crisis, however, together with the experience of austerity policies triggered a new movement for a reinforced social dimension of the EU, sometimes conceptualised as a Social Union. Regardless of terminology, the discussion on EU-wide unemployment insurance or reinsurance has benefited from a snowball effect, reaching far more constituencies than in the years of financial crisis. The idea now appears to be a cornerstone of any new version of Social Europe that expects to be taken seriously.

Of course, this discussion is about much more than a social safety net for vulnerable workers. In a broader context the field of employment has been just one more example of what appears to be a more general flaw in the structure of the European Union, namely that practically all emergency and stabilisation mechanisms are located at the national instead of the Community level. The EU allows free movement, which is a central component of the Single Market. Through this, it contributes to shared prosperity, but in ‘bad times’, such as when economic recessions or other types of crisis hit the Community, the Member States can rely mainly on themselves, or on intergovernmental deals. This was experienced during the 2010 financial crisis, the 2015 migration crisis and most recently the 2020 COVID-19 crisis.

All these crises have been pushing the EU, though not without serious headwinds, towards building more emergency and stabilisation capacities, delivering ‘de facto solidarity’, as the late French foreign minister and EU founding father Robert Schuman called it. Recent developments in the wake of the coronavirus pandemic represent a new chapter in this history. An overview of the evolution of the idea of EU-wide unemployment insurance and the political debate around it can help with reflections on the future of Europe, and perhaps also the actual policy process in the EU institutions.

Early pointers on unemployment insurance

A Community unemployment fund, which is now on the agenda of EU debates in the form of a reinsurance scheme, is not a new idea. It was first outlined in 1975 by a Report authored by the former Vice-President of the European Commission, Robert Marjolin (see European Commission, 1975). The concept was also supported by the 1977 MacDougall Report (see MacDougall, 1977). These documents explored the budgetary requirements for a sustainable European economic integration which would also stretch to establishing a monetary union.

In the 1970s the European Economic Community (EEC) experimented with an early form of monetary cooperation, called the Currency Snake. 1 This was a necessary first step on a long road, triggered by the unilateral withdrawal of the United States from the stabilising function of the Bretton Woods monetary system. Once the gold parity of the US dollar was cancelled and the post-war mechanism of exchange rate stabilisation was no longer available, the six EC Member States had to take care of currency stability without the United States, but in cooperation with a number of non-EC member European countries.

While distant in time from the actual introduction of the single currency, the MacDougall Report highlighted the important link 2 between monetary union and unemployment insurance. In essence, the question has always been how the Community can help Member States to tackle cyclical unemployment, which is linked to, and aggravated by, the lack of adjustment tools at an advanced stage of monetary integration.

Those early documents of public finance analysis, the Marjolin and MacDougall Reports, considered it self-explanatory that monetary integration requires unemployment insurance as a form of de facto solidarity, in the spirit of the 1950 Schuman Declaration. Linking the stability and resilience of monetary integration to unemployment dynamics proved right, because mass unemployment did play a major role in the disintegration of the Exchange Rate Mechanism (ERM) in 1992–1993. Governments with currencies under speculative attack were forced to set priorities, and the only form of Community-level ‘unemployment insurance’ was the exit option, that is, the right to leave the ERM, until the summer of 1993, when the fluctuation bands of the ERM were widened to ±15 per cent, which in reality meant that the mission of the ERM to deliver exchange rate stability was dropped.

The Maastricht model and the Delors paradox

Unfortunately, the 1989 Delors Report and the subsequent Maastricht process ignored much of the early insight. Commission President Jacques Delors was committed to building a social dimension for the Single Market, but no similar effort was made regarding the currency union. The difference between the two is highly significant; we can thus talk about a ‘Delors paradox’ 3 here. While the Single Market–related social legislation introduced by Delors has been of great importance, giving rise to the vision of Social Europe, this architecture has been progressively undermined by the currency union, which in social terms has eventually polarised, rather than unified the Union.

From the beginning of the 1990s, cooperation between the EU Member States in the monetary field outstripped cooperation in other areas, mainly for political reasons (in other words, by prioritising the euro’s presumed unifying role). The single currency was introduced without an EU-level system for the supervision of financial institutions operating in the Single Market, and thus without any real economic governance that could help to make development more evenly balanced, and without any uniform, solidarity-based crisis-management mechanisms to respond to shocks. 4

Establishing a minimalist monetary union, and especially one without a fiscal union in Europe was always controversial (Andor, 2013). The Maastricht model of the European Monetary Union (EMU) can be qualified as minimalist because it drops the exchange rate from the economic policy toolkit, but it does not replace it with either a lender of last resort, or a central budget able to provide fiscal stimulus, or at least coordinated policies aiming to uphold aggregate demand across Europe through a revaluation in ‘surplus’ countries. As a result, those economies experiencing balance-of-payments problems are bound to undertake internal devaluation (cuts in wages, pensions and investment as a substitute for currency devaluation) to regain cost competitiveness in times of crisis. This has adverse effects on overall growth, but also on the labour market and the social situation, leading to unnecessary economic losses and a potentially devastating social impact at the same time.

Eurozone crisis: the search for stabilisation tools

The EMU’s design flaws were brushed under the carpet for nearly two decades. However, Europe’s fragile economic architecture suffered a major blow during the 2008 global financial meltdown and the years that followed. In this period (2008–2009), countries outside the eurozone appeared to be more vulnerable, and especially those which had no capacity to respond to the financial market shock and the recession by adjusting the exchange rate of their currencies. The Baltic countries, though not yet in the eurozone, 5 implemented massive internal devaluation in the early phase of the crisis. This not only resulted in a dramatic rise in unemployment, poverty and income inequality, but also boosted the outward mobility of the workforce.

In the second phase of the European crisis (2010–2011), various countries in the eurozone periphery started to lose access to capital markets and asked for official assistance. They were helped out by other EU states, as well as by the International Monetary Fund (IMF) but only in exchange for severe austerity programmes with internal devaluation strategies at their heart. At the same time, frontloaded fiscal consolidation policy at the EU level, coupled with pro-cyclical rate hikes by the European Central Bank (ECB), created a macroeconomic framework with no exits out of the recession, and pushing the eurozone ever closer to disintegration.

When EU leaders looked into the abyss in 2012 and faced the risk of immediate eurozone collapse, the moment of truth came. Far-reaching reforms were announced, declaring the need for banking union, fiscal union, as well as political union. The Four Presidents’ report (Van Rompuy et al., 2012), the Commission Blueprint for Deep and Genuine EMU (European Commission, 2012) and the Thyssen Report (European Parliament, 2012) adopted by the European Parliament pointed in the same direction. In addition, the words of the 2012 Blueprint on automatic stabilisers were repeated in the 2013 October Commission Communication about the Social Dimension of EMU.

The eurozone crisis not only resulted in a rise in EU unemployment to record high levels, 6 but also a polarisation between countries in terms of labour market performance. In addition to the divergence of unemployment rates (between core and periphery countries), the eurozone experienced a marked excess of unemployment, even though its largest country, Germany, constantly experienced falling unemployment in 2011–2013.

Once the systemic nature of the crisis of the single currency was recognised in 2011–2012, a number of options for eurozone automatic fiscal stabilisers were proposed in the literature and in policy debates. The idea of a basic European unemployment benefit scheme has been pioneered and most clearly advocated by Sebastian Dullien, 7 and also analysed by the European Commission’s DG EMPL with the involvement of a number of external experts 8 (Strauss, 2016). A scheme based on the concept of income insurance as one option has also been explored by the Commission’s DG ECFIN.

Relaunching the debate: EMU’s social dimension

Various EMU documents in 2012 highlighted the severe social consequences of the crisis and support for ad hoc but also systemic solutions started to grow. The December 2012 European Council included in its conclusions (12.b.) the need to work on the social dimension of EMU and the social dialogue (European Council, 2012). Ahead of May Day 2013, the European Commission received representatives of the social partners at a College meeting (the first time in its history). Shortly afterwards, a heated debate took place in the European Parliament plenary about EMU’s social dimension. But the delayed 9 delivery also resulted in dilution of the Communication’s policy proposals. The original version of 2013 included an outline of European Unemployment Benefit Scheme (EUBS) options, but they were left out of the final version. 10

It is important to highlight that in 2012–2013 there was no obvious demandeur for a European Unemployment Benefit Scheme, whether among Member States, political parties or key stakeholder groups (including social partners). In July 2013, the Commission used the informal EPSCO council 11 in Vilnius to raise ministers’ awareness of EMU’s social dimension. One year later, the informal EPSCO in Milan was used to discuss unemployment insurance itself.

The social partners were not particularly enthusiastic at this time. In some countries (such as Sweden and Denmark) a focus on social dumping alone was supposed to solve Europe’s social questions. In others, and also for much of the ETUC leadership, the fear was that a shift of emphasis towards EMU’s social dimension would weaken efforts concerning the social dimension across the European Union as a whole. The German social partners sent a letter to the Commission to make it clear that they were opposed to any movement towards an EU role in unemployment insurance.

While the 2013 October Communication (European Commission, 2013) was, in a way, a setback, the Commission cooperated with the incoming Italian presidency to make the necessary next step and discuss unemployment insurance among employment, as well as finance ministers. At the time of the Italian presidency, a debate was organised in both the ECOFIN 12 and EPSCO councils. The latter generated a lot of interest and support, while in 2014 in ECOFIN the mood remained lukewarm. At the September meeting of finance ministers, Italy more or less stood alone as an advocate. At the press conference after the informal EPSCO council in Milan, however, the Italian government representative voiced the need for a Green Paper on EMU unemployment insurance.

Creating an epistemic community

Since 2011–2013, a great deal of analysis, produced by the Commission itself and a host of think tanks and independent experts, has explored the problems of asymmetry and divergence. Simulations have also been run. In 2013–2014, the European Commission, in cooperation with the Bertelsmann Foundation (Noack, 2014), held two public conferences about the possibility of EU-level unemployment insurance.

For most analysts of EMU, unemployment insurance had not been among the most important issues. For critics of the Maastricht model, such as Joseph Stiglitz, Paul Krugman or Paul de Grauwe, it was more important to point out that monetary union without a fiscal union was folly. Implementing the Banking Union and developing a common fiscal capacity, ideally in some form of mutualisation of public debt, were seen as the real priorities. From the point of view of fiscal stabilisation capacity, eurobonds are the right solution; everything else is ‘plan B’ at best. Nevertheless, unemployment insurance has been mentioned more and more frequently as a necessary EMU reform, alongside various forms of eurobonds. Nobel Memorial Prize laureate Joseph Stiglitz also endorsed the idea in his book about the single currency (Stiglitz, 2016) and also in a public debate with eurozone president Jeroen Dijsselbloem.

While not listed by most economists among the top three elements of necessary EMU reform, unemployment insurance was increasingly recognised as a possible step towards both economic and social stabilisation. 13 In discussions surrounding EMU’s social dimension, it was stressed that the stabilisation capacity can be built in such a way that it does not become a one-way support channel. Focusing fiscal transfers on the need to mitigate asymmetric cyclical shocks means that, over the long term, all participating Member States are likely to be both contributors and beneficiaries of the scheme. This of course would not mean full symmetry, and even if the balance is not exactly zero after a certain period of time, the system’s capacity to reduce the depth and duration of economic crises would provide a more stable macroeconomic environment for all, sustain aggregate demand and therefore improve growth prospects for the whole eurozone.

Early research in national context

In 2014, the debate on automatic stabilisers entered the political arena, feeding into EMU reconstruction. Research and policy debate also started in national contexts, especially in the most influential countries of the eurozone.

The French ministries of finance and the economy published a brief in June 2014 (Lellouch and Sode, 2014) supporting the establishment of common basic unemployment insurance, to consolidate eurozone integration, improve macroeconomic and financial stabilisation and move towards enhanced coordination of labour market policies. They suggested that such a scheme would need to be implemented in stages.

In November 2014, the Bank of Italy published a paper identifying the broad characteristics that a shock absorber based on unemployment should have in order to be incentive-compatible and politically feasible (Brandolini et al., 2014). The study empirically describes the combination of activation thresholds, experience rating, eligibility criteria and benefit generosity such a system would need, giving rise to macro cross-national transfers, activated by a trigger and with partial experience rating. The results of the simulations conducted suggest that even systems that do not redistribute resources between countries can have a considerable stabilisation impact in the medium term.

In Germany, Dolls et al. (2014) analysed different alternatives for a common unemployment insurance system for the eurozone, quantifying the trade-off between stabilisation effects and degree of cross-country transfers. They suggested that contingent benefits could limit the degree of cross-country redistribution, but might also reduce the desired insurance effects.

Deutsche Bank also published a research briefing on this topic (Vetter, 2014), stressing the problems of moral hazard among participating countries. It argued that mechanisms to prevent it would automatically reduce the scheme’s stabilisation impact, and that the difficulties of establishing ‘an equilibrium between net contributors and net beneficiaries in the long term’ would reduce the chances of achieving political acceptance. Moral hazard remained one of the critical points of relevant research, usually leading to consideration of various clawback instruments. Shafik and Weichenrieder (2016) analysed various clawback mechanisms that had been suggested in the literature as ways of limiting redistribution, but concluded that clawbacks were undesirable, as they would essentially destroy the insurance value of a fiscal union. Instead, they proposed that a clearly defined exit option as a guarantee against involuntary redistribution could make entry into a stronger fiscal union less risky and hence more attractive for Member States.

Exploring alternative models

Following the initial moves by the Commission and the expert community across Europe, economic, social, financial and legal studies discussed the potential role and feasibility 14 of an EU-wide unemployment benefit scheme. While recognising some barriers and risks, all such studies point to the overwhelming economic and social benefits of such automatic fiscal stabilisers. If researchers had any doubts they concerned the legal basis for automatic social stabilisers within the existing Treaty, or the political support for cross-country transfers, especially if they looked set to become lasting and systemic.

The fact that major think tanks started to work on policy options on EU unemployment insurance indicated the importance of the issue for the policy agenda. Bruegel came forward with important studies ahead of the Council meetings in 2014, providing input to ministerial discussions (see Claeys et al., 2014a). Bruegel even presented a ‘do it yourself’ unemployment insurance scheme on its website to allow visitors to choose their preferred parameters and see what the direction and intensity of cross-country transfers would be in different models (Claeys et al., 2014b).

In January 2015, the European Commission launched a major study to examine details and explore possible implications of EMU unemployment insurance. The consortium of researchers led by the Brussels-based Centre for European Policy Studies (CEPS) delivered multiple simulations and analysis explaining the justification, as well as the feasibility of a reinsurance mechanism (Beblavý et al., 2015, 2017). The positive predisposition of this consortium’s lead researchers was displayed in a study by Beblavý and Maselli (2014), which proposed an unemployment benefit scheme open to all EU countries, not restricted to the eurozone, of a maximum duration of 12 months, triggered by an increase of 2 percentage points in the difference between the unemployment rate and the non-accelerating wage rate of unemployment (NAWRU), and included a clawback mechanism to prevent permanent transfers.

During these years of reflection, the partial pooling of unemployment benefit schemes, as proposed by Sebastian Dullien, was understood to be a better form of integration, while a US-inspired reinsurance model was seen as better matching the European approach respecting subsidiarity, but adds further layers with a clear added value if justified by extraordinary circumstances. The competing perspectives agreed on one key point: if either of these insurance mechanisms had existed in EMU from the launch of the single currency, all Member States would have been beneficiaries at least once for a shorter or a longer period.

European Parliament focus on fiscal capacity

The European Parliament elections in 2014 gave evidence of public discontent with the long crisis. Various far-right groups managed to boost their representation, and the ruling parties of the centre-left and centre-right suffered losses, except, for example, in Italy, where the ruling Democratic Party under new leadership presented itself as a disruptor of the status quo.

Leading voices supporting the Juncker Commission remained focused on necessary reform of EMU, focusing on issues such as the completion of the Banking Union. A European Parliament report by Pervenche Berès (French Socialist) and Reimer Böge (German CDU) confirmed the need for a central fiscal capacity 15 with a counter-cyclical stabilisation function.

In the process of producing the Berès/Böge report, the European Parliament repeatedly heard arguments for automatic stabilisers, including unemployment insurance. Some invited researchers continued to favour fiscal stabilisation unrelated to unemployment. One such study was presented to the Parliament by Heikki Oksanen, following in the footsteps of Henrik Enderlein, who put forward an output gap–based mechanism (Enderlein et al., 2013) at the 2013 Commission–Bertelsmann conference (Oksanen, 2016).

In the 2014–2019 European Parliament, progressive MEPs playing a leading role in economic affairs, such as Roberto Gualtieri (Italy), Pervenche Berès (France) and Jakob von Weizsäcker (Germany) voiced their support for one or another form of common unemployment insurance in the EU. This signalled not only an evolution of thinking about EMU reform but also a deeper connection between economic and social policy reform.

A concrete model for unemployment reinsurance was designed in 2018 with the support of a German and a Spanish MEP, Jakob von Weizsäcker and Jonas Fernandez. The model 16 they presented in the European Parliament combined modest transfers with loans, effectively trying to force Member States to save in good times in order to be able to secure long enough and generous unemployment coverage in bad times.

Political iteration games

French President François Hollande promised to put an end to austerity in Europe in 2012. A real chance for convergence in the German and French positions on economic governance, however, emerged only after the German SPD entered a Grand Coalition with the CDU-CSU after the 2013 elections. Economy ministers Sigmar Gabriel and Emmanuel Macron developed a robust discourse, and to some extent also a policy agenda, on investment. 17 To create a supportive environment and provide useful inputs for the convergence of French and German policies, including on EMU reform, the Eiffel and Gleinicker Groups of distinguished economists played a major role in these years.

Once the Italian presidency was over, and the vision of substantial EMU reform was replaced by – often vague – rhetoric on investment, Italian finance minister Pier Carlo Padoan embarked on a seemingly Quixotic campaign, arguing in favour of an unemployment insurance fund embedded in the EU’s Multiannual Financial Framework (MFF) (Padoan, 2015). In October Padoan (2015) stressed the need for ‘a European mechanism to mitigate cyclical unemployment and its consequences’, and proposed an unemployment insurance scheme that would be feasible within the limits of the current Treaties (MEF, 2015). Such a scheme would increase convergence in labour market regulation, consolidate medium-term growth and prevent hysteresis effects. The key feature of the Italian proposal is its sense of urgency, accompanied by the argument that ‘such an instrument could be established without Treaty changes’.

When Padoan stepped down as a minister in 2018, former Hamburg mayor (and now German Chancellor) Olaf Scholz took over the finance portfolio in Berlin in the Grand Coalition of the centre-left and the centre-right. Scholz also took over from Padoan coordination of the centre-left political group in ECOFIN, and came out with his own version of unemployment insurance. It was based on loans rather than transfers, which risked presenting a more symbolic than substantial version of solidarity (Andor, 2018b). But at least from that standpoint it was no longer a Germany-against-the-rest type of EU political debate, but an internal German debate. This was a major step towards practical reform. Scholz gave an interview to Der Spiegel in June 2018 (Reiermann and Sauga, 2018) in which he committed to the idea of unemployment reinsurance, which hitherto had been anathema in German government circles.

Slow motion under Juncker

The Juncker Commission (2014–2019) did not launch any significant EMU reform, and even discussions about the need for reform were toned down. The Five Presidents’ Report (Juncker et al., 2015) was less clear-cut about the necessary elements of a genuine and sustainable EMU than the original Four Presidents’ Report. The necessary third pillar of the Banking Union, deposit insurance (EDIS), was not delivered. A commitment to fiscal union was replaced by vague talk about fiscal capacity. Concerning unemployment insurance, the Commission did organise a major conference on the subject, with two Commissioners (Marianne Thyssen and Pierre Moscovici) attending, but despite the merits of the idea being presented by the CEPS-led consortium, legal barriers were invoked and no new initiative followed.

In 2016, the Slovak Council Presidency brought unemployment insurance back into the policy debate and organised a high-level conference on it in Bratislava (TASR, 2016). They also relaunched the ECOFIN debate on the issue. Opinion among finance ministers was much more balanced than under the Italian presidency. This did not have a discernible impact on the Juncker Commission, however, even though a smart move on unemployment insurance could have made the European Pillar of Social Rights (EPSR, see European Council, 2017) – a flagship Juncker initiative on the EU social dimension – more meaningful. At the very end of his mandate, Juncker declared that he was, under certain conditions, in favour of introducing an unemployment insurance scheme. In the years when he could have done something about it as Commission president, however, he showed no interest in promoting it.

The most important documents produced by the Juncker Commission on EMU reform, and the 2017 Reflection Paper on the future of EMU (European Commission, 2017) in particular, highlighted the danger of economic and social divergence in the eurozone, but in the absence of political momentum, only very modest reform proposals were put forward, especially concerning risk-sharing. In May 2018, Juncker proposed a new Multiannual Financial Framework (MFF) which would have embedded facilities serving the EMU stabilisation function into the seven-year EU budget but with tools that did not turn out to be convincing because of their size or profile (Andor, 2018a). Juncker’s gadgets 18 were silently dropped in 2020 when the EU had to produce a serious new model budget to face the COVID-19 crisis.

Surprise return with Ursula von der Leyen

Following her nomination as Commission president, Ursula von der Leyen 19 announced that during her mandate the Commission would introduce an unemployment reinsurance scheme. This promise was then included in the mission letter of two EU Commissioners: Nicolas Schmit (Jobs and Social Rights) and Paolo Gentiloni (Economy). Without underestimating the political complexity of the case, Schmit and Gentiloni had been among its natural supporters. Nicolas Schmit had acted as coordinator of the Socialist group among EPSCO ministers for years, and hosted a high-level event in 2018 in Luxembourg to boost the debate and policy process on the EU and EMU social dimensions (Fernandes, 2019). Paolo Gentiloni had been a colleague and then boss of Pier Carlo Padoan, a long-time standard bearer of EU-wide unemployment insurance.

Von der Leyen’s nomination by the European Council surprised many, following the inconclusive result of the 2019 European Parliament elections, which saw a further decline in support for the European People’s Party, but also the Socialists and Democrats. Parliamentary arithmetic and the hostility of some social democrats meant that von der Leyen had to work hard to win the support of the centre-left and green MEPs for her election. She thus integrated a long list of key elements of the social democratic and green agenda in her presidential programme.

Neither the centre-left 20 nor the greens had been truly firm and united on the question of EMU unemployment insurance, however. It had not featured among the main discussion points of the 2019 European Parliament election campaign either. On the other hand, the European Economic and Social Committee (EESC) was keen to promote the concept of unemployment insurance, although it focused on the definition of minimum standards 21 as opposed to risk mutualisation and directly linking the issue to EMU reform (Röpke, 2019).

Von der Leyen, who was German Minister for Labour and Social Affairs at the time of the initial (2013) debates on EMU’s social dimension, was not known to be a supporter of EU-level unemployment insurance or reinsurance. Nevertheless, she represented the strongly pro-European wing of the CDU, with coalition experience with (economic) liberals, as well as social democrats. She had no difficulty in taking the idea of unemployment insurance on board, but was open to alternatives when the EU economy entered an unexpected recession.

COVID-19 recession: rolling out SURE

When in March 2020 EU Member States were suddenly overwhelmed by the COVID-19 pandemic, the Commission put forward a proposal for the creation of a European instrument for temporary support to mitigate unemployment risks in an emergency, entitled ‘Support to mitigate Unemployment Risks in an Emergency’ or ‘SURE’ (D’Alfonso, 2020; European Council, 2020). When the new SURE initiative was announced by Commission President von der Leyen, the justification for this innovative instrument was embedded in the context of unemployment reinsurance. The differences between the two concepts were also quickly understood, however.

While it has significant potential 22 , SURE does not qualify as unemployment insurance or reinsurance. According to Fernandes and Vandenbroucke (2020), SURE can be best characterised as a job insurance scheme. It is a safety net for jobs, but not for the unemployed. The distinction between the two is meaningful. In unemployment insurance schemes, the unemployed are provided with cash, not a loan. SURE, by contrast, distributes loans, not cash, and not to the unemployed, but to those who might be threatened by unemployment. This threat is mitigated by short-time working arrangements. On the other hand, national unemployment benefit schemes are a better bet for reducing unemployment than SURE.

Limiting EU solidarity to those workers whose jobs can be saved is hard to justify. During the recession triggered by the COVID-19 pandemic, unemployment was tamed but was bound to rise simply because some companies go out of business and so cannot retain workers even if subsidies are offered. Furthermore, many people were on temporary contracts when the crisis hit, and in the circumstances most were simply not renewed. As a result, a lot of people became unemployed without being dismissed either de facto or de jure. Most of those employees would be unlikely to be considered for short-time work schemes, similarly to the self-employed. It is therefore particularly important that the SURE initiative is open to programmes designed for the self-employed. Even so, it remains an exclusive, not an inclusive support tool.

While it is clear that SURE is not an unemployment reinsurance scheme, the question is whether it can be developed into one by incorporating elements that provide additional support to the unemployed. Such possibilities certainly exist. In justification, one could argue that in case of a sudden rise in unemployment it takes time to organise short-time working and it is not equally possible in every sector and every company. In case of a stronger than average increase in unemployment, a grant component could be introduced and the recipient government allowed to start repayment after a delay. This type of compromise solution (drawing on the spirit of the earlier Fernandez—von Weizsäcker scheme) would require the establishment of a grant fund, a definition of the trigger (a certain percentage-point increase in the level of unemployment), and an outline of constructive conditionalities (for example, that the quality of unemployment insurance cannot decline in the recipient country while it is receiving EU support).

The COVID-19 crisis has apparently propelled the EU to a new level of integration, while once more unemployment reinsurance does not appear to be considered urgent, given the rollout of SURE and the €750bn Next Generation EU. In spring 2021, under the Portuguese Council presidency, the EU moved to a major campaign to strengthen its social dimension, based on an Action Plan (European Commission, 2021) published in March and popularised during a Social Summit held in Porto in May. The fact that EU-wide unemployment reinsurance did not appear among the commitments, however, raised concerns, not least on the part of the ETUC, which by this time was a stronger supporter of this policy than previously.

Fiscal rules and unemployment insurance

At the outbreak of the COVID-19 crisis and the resulting recession (in March 2020), the European Commission activated the escape clause of the Stability and Growth Pact (SGP). Member State governments were allowed to implement fiscal expansion to maintain domestic demand and thus prevent a downward spiral of the real economy. Together with other crisis measures, the question of the exit from crisis measures became an important debate. On the other hand, the question was not only when but also whether the EU should return to the established rules of fiscal policy coordination.

It became clear and was widely discussed that for a viable recovery and a transition to a more sustainable economic model, the EU’s inherited fiscal rules must be reformed. Most obviously, the debt ceiling (public debt was not permitted to be higher than 60 per cent of a country’s GDP) became unrealistic for Europe’s post-COVID conditions. In fact, the Commission had already launched a review of the fiscal rules in early 2020. And on 8 July 2021, the European Parliament approved a parliamentary report from the Socialists and Democrats (S&D) calling for urgent reform of the EU’s economic governance architecture (Socialists and Democrats, 2021). To address well-known shortcomings of the system, they proposed a country-specific debt adjustment approach. 23

Connecting SGP reform with elevating social policy would throw light on the need for EU-wide unemployment insurance, emphasising its potential beyond economic, social and institutional stabilisation. EMU unemployment insurance or reinsurance could contribute to economic stabilisation by shifting demand and purchasing power to countries and regions that would otherwise need to implement internal devaluation. Second, social stabilisation would also follow as a result of directing the flow of funds towards more vulnerable social groups and helping to curb rising poverty, especially among the working-age population. Institutional stabilisation is a third dimension. Unemployment insurance could be a deal-maker should the EU want to relaunch a (reformed) set of fiscal rules after the post-COVID-19 recovery takes hold.

Conclusion: the case for stabilisation capacity linked to unemployment

The rationale for setting up a fiscal stabilisation capacity within EMU is compelling. The idea of connecting fiscal stabilisation to a mechanism that helps to boost unemployment insurance across the EU is almost half a century old. Options have been clarified, the political debate is mature and the institutional commitment to deliver has been expressed.

As we have seen in two recent economic crises, national fiscal stabilisers might not be sufficient to smooth the cycle within individual countries, maintain economic convergence and deliver the optimal fiscal stance for the eurozone as a whole. This was very much the case during the 2011–2013 crisis when national budgets, even in countries with sound and resilient underlying fiscal positions, were overwhelmed by the severity of the crisis. The lack of adequate national fiscal stabilisation capacities, and the complete lack of such a capacity at the EU level, harmed the economic performance and social cohesion of the whole eurozone.

According to the reformist logic, an automatic stabiliser at EMU level would help uphold aggregate demand at the right time, and without delays. Most importantly, it would prevent short-term crises from unleashing longer-lasting divergence within EMU. Such a fiscal stabiliser would not represent ‘more Europe’ for its own sake, and certainly not more intrusion of ‘Brussels bureaucracy’ into national policy-making. It would rather constitute a mechanism to strengthen the autonomy of each Member State precisely by stabilising EMU and making it more resilient on the basis of transparent rules.

While the overall dynamics of unemployment will remain functions of the fiscal and monetary mix, various structural interventions and institutional innovations can have mitigating effects and a positive influence on working conditions. From this point of view, the EU can use the coronavirus crisis to deepen solidarity among its Member States, accelerate the transfer of better practices between them and make efforts to ensure that the constructive effects of crisis response measures survive the emergency. Any new initiative for an EU-wide unemployment insurance or reinsurance scheme can fall back on a decade-long debate and a massive body of expert analysis demonstrating the merits of the proposal.

Footnotes

Appendix

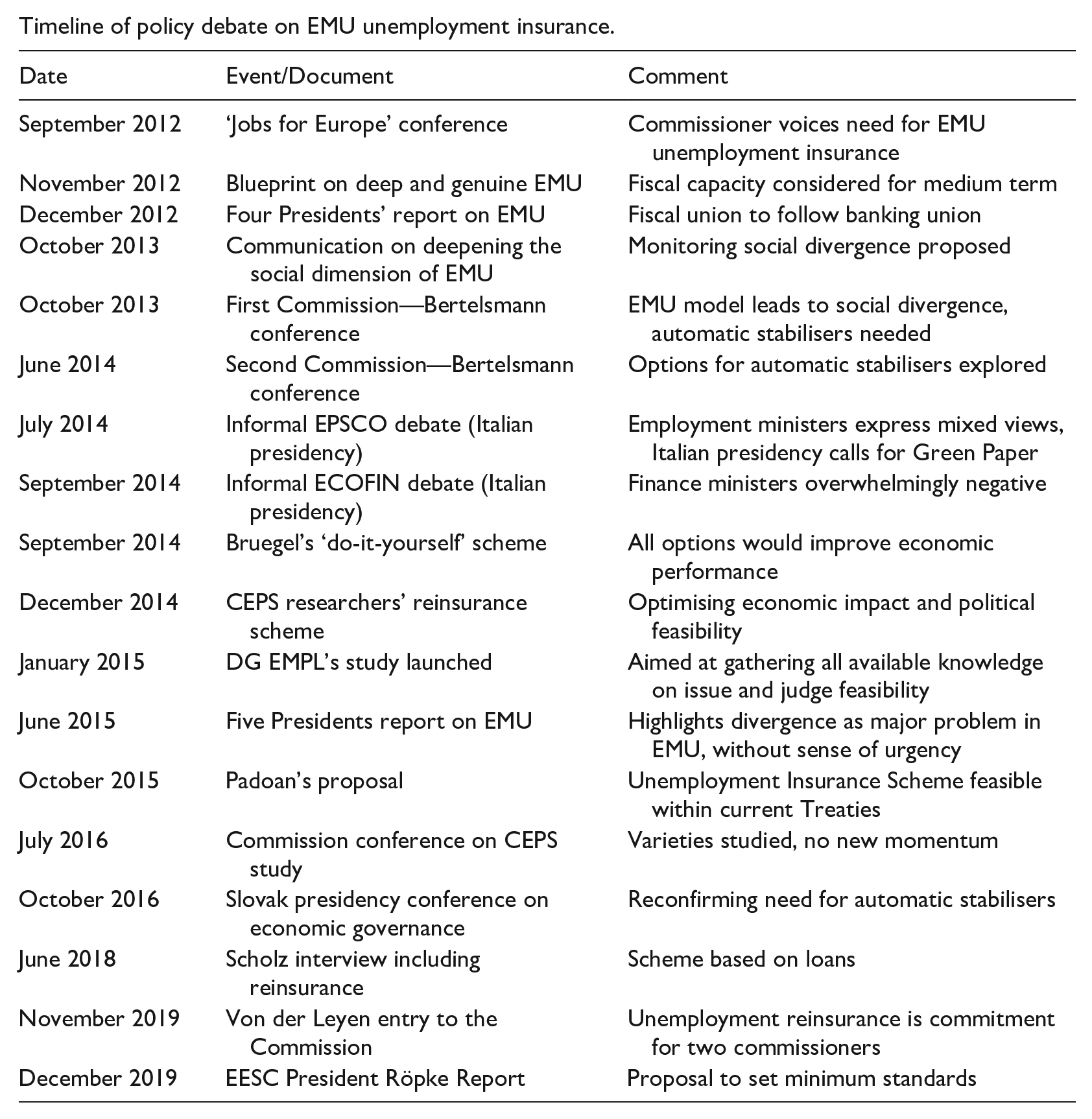

Timeline of policy debate on EMU unemployment insurance.

| Date | Event/Document | Comment |

|---|---|---|

| September 2012 | ‘Jobs for Europe’ conference | Commissioner voices need for EMU unemployment insurance |

| November 2012 | Blueprint on deep and genuine EMU | Fiscal capacity considered for medium term |

| December 2012 | Four Presidents’ report on EMU | Fiscal union to follow banking union |

| October 2013 | Communication on deepening the social dimension of EMU | Monitoring social divergence proposed |

| October 2013 | First Commission—Bertelsmann conference | EMU model leads to social divergence, automatic stabilisers needed |

| June 2014 | Second Commission—Bertelsmann conference | Options for automatic stabilisers explored |

| July 2014 | Informal EPSCO debate (Italian presidency) | Employment ministers express mixed views, Italian presidency calls for Green Paper |

| September 2014 | Informal ECOFIN debate (Italian presidency) | Finance ministers overwhelmingly negative |

| September 2014 | Bruegel’s ‘do-it-yourself’ scheme | All options would improve economic performance |

| December 2014 | CEPS researchers’ reinsurance scheme | Optimising economic impact and political feasibility |

| January 2015 | DG EMPL’s study launched | Aimed at gathering all available knowledge on issue and judge feasibility |

| June 2015 | Five Presidents report on EMU | Highlights divergence as major problem in EMU, without sense of urgency |

| October 2015 | Padoan’s proposal | Unemployment Insurance Scheme feasible within current Treaties |

| July 2016 | Commission conference on CEPS study | Varieties studied, no new momentum |

| October 2016 | Slovak presidency conference on economic governance | Reconfirming need for automatic stabilisers |

| June 2018 | Scholz interview including reinsurance | Scheme based on loans |

| November 2019 | Von der Leyen entry to the Commission | Unemployment reinsurance is commitment for two commissioners |

| December 2019 | EESC President Röpke Report | Proposal to set minimum standards |

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

1

The so-called ‘snake in the tunnel’ was the first attempt at European monetary cooperation in the 1970s, aimed at limiting fluctuations between different European currencies. The currencies of the six participants were only allowed to fluctuate against each other by a margin of 2.25 per cent, like the undulations of a snake.

2

The relevant quote from the MacDougall Report: ‘Apart from the political attractions of bringing the individual citizen into direct contact with the Community, it would have significant redistributive effects and help to cushion temporary setbacks in particular member countries, thereby going a small part of the way towards creating a situation in which monetary union could be sustained.’ ![]() : 13).

: 13).

4

The connection between shock absorption and fiscal risk-sharing was examined in the post-Maastricht period by Italianer and Pisani-Ferry (1994) and ![]() .

.

5

The three Baltic States, Estonia, Latvia and Lithuania, had pegged their national currencies to the euro in currency board arrangements, which allow increases in the domestic money supply only in proportion to increases in foreign exchange or gold reserves.

6

The EU unemployment rate peaked at 11 per cent in 2013 and the eurozone unemployment rate reached 12 per cent at the same time. Youth unemployment rates peaked at a level more than twice as high, on average.

7

Dullien (2013a, 2013b, ![]() ) suggested a scheme based on payroll tax, directly insuring the unemployed across Europe, and giving rise to a specific European fund that could run surpluses and deficits, according to need, therefore including the possibility of issuing debt. This would enhance the system’s stabilisation effects. The annual cost would range between 0.3 and 0.6 per cent of GDP.

) suggested a scheme based on payroll tax, directly insuring the unemployed across Europe, and giving rise to a specific European fund that could run surpluses and deficits, according to need, therefore including the possibility of issuing debt. This would enhance the system’s stabilisation effects. The annual cost would range between 0.3 and 0.6 per cent of GDP.

8

External experts contributing to the Commission analysis included Delpla (2012). The French interest in the topic in the same period is also demonstrated by ![]() from the perspective of the EMU social dimension.

from the perspective of the EMU social dimension.

9

Originally, this Communication was meant to appear ahead of the European Council meeting scheduled for June, but was then postponed to October (that is, after the Bundestag elections in Germany).

10

President Barroso was not opposed to the idea of a European Unemployment Benefit Scheme, but believed that the Commission would need to concentrate on EMU reform proposals that were already on the table, and the Banking Union in particular. He opined that the European Unemployment Benefit Scheme could be included in a legacy document of the Barroso II Commission (source: author’s recollection).

11

The Council configuration of employment and social affairs ministers.

12

The Council configuration of finance ministers.

13

Unemployment insurance from a social stabilisation perspective is considered by Corry (2013); Timbeau (2014); Fattibene (2015) and ![]() .

.

17

18

In the 2018 MFF proposal submitted by Juncker’s budget commissioner Günther Oettinger, the eurozone section includes two new items: a Reform Support Programme (RSP) for the amount of €25bn, and a European Investment Stabilisation Function (EISF) for the amount of €30bn. Neither of these proposals managed to make a breakthrough in the two-year debate that followed, however.

19

Previously in charge of the labour and social affairs portfolio in the Federal Government of Germany, von der Leyen had been a very active minister during the previous crisis. She consistently supported EU efforts to improve job opportunities and working conditions, though on issues overlapping financial and monetary questions she would not have challenged her cabinet colleague, finance minister Wolfgang Schäuble.

20

Having delivered the Pillar of Social Rights, as well as a targeted review of the Posted Workers Directive in the previous European Parliamentary cycle, the socialists moved on to new frontiers, and unemployment reinsurance moved up the policy ladder. From an internal political point of view, this must have been helped by the relative strengthening of the Italian delegation in 2014 and the Iberian dominance of the group in 2019.

21

The EESC report by President Oliver Röpke suggested that the minimum standards of unemployment insurance should be defined according to (i) the net replacement rate, (ii) coverage, (iii) duration of unemployment benefit entitlement, and (iv) the right to (re)qualification and training. Targets in these fields would be monitored in the context of the European Semester.

22

The potential of SURE is assessed by Alcidi and Corti (2020); Andor (2020); Vandenbroucke et al. (2020) and ![]() .

.

23

This country-specific debt adjustment would work by creating an expenditure rule in order to better tailor policies to the economic reality in each country and reflect the degree of debt sustainability for different countries.