Abstract

Culture, attitudes and perceptions have an underappreciated effect on industrial cluster policies particularly in transition economies, where long-established local social norms are confronted with hard-pressed external imperatives. This paper examines the impact of cultural and governmental peculiarities in the Russian context on the development of special economic zones and industrial parks. Based on some stylized facts about the Russian context, in-depth interviews and surveys of the managing companies and tenants of all industrial clusters in Russia, we find cultural and governmental characteristics emerge as major influences on the effective development of industrial cluster policies. We develop an adapted industrial cluster model that accommodates these factors and suggests a policy pathway for mitigation.

Introduction

Special economic zones (SEZs) and industrial parks (IPs) have been a mainstay of economic development policy since the successful export-led industrialization of the Asian Tigers and China from the 1970s. Such industrial cluster policies draw on the Marshallian concept of positive externalities from geographic concentrations of economic activities, establishing incentives for the agglomeration of firms to increased productivity and stimulate innovation by combining technology, information, specialized labour, supporting and competing firms, universities, R&D centers and other organizations (Porter, 1990).

The recent Russian experience in pursuing industrial cluster strategies, however, suggests that it is not straightforward to transfer cluster policies to different social and political contexts and that extra-economic factors have a much greater effect on outcomes than predicted by the standard model (Albekov et al., 2017; Nikolaev and Grigoryeva, 2016). This paper examines the adoption of industrial cluster policies in Russia since the 1990s, identifying factors contributing to outcomes less successful than anticipated. We argue that these factors are likely to be problematic for the pursuit of industrial clustering policies in other similar social and political contexts.

Attempts to develop SEZs and IPs came late to Russia. While there were some state initiatives to establish SEZs in Soviet times, these efforts largely perished with the economic collapse and political instability of the early 1990s (Kushnirsky, 1997). A firmer footing for SEZs came in 2005 with federal legislation (Decree 116) demarcating four types of SEZ: industrial, innovation, tourism and port and logistics zones. These would attract investors with utilities tailored to each individual potential investor, an autonomous customs zone with simplified procedures and duty-free benefits, more liberal economic and juridical regulations, potential partnerships with other companies, proximity to local companies, labour resources, new potential markets for growth and fiscal incentives (Maslikhina, 2016; Yankov et al., 2016).

IPs subsequently emerged as private, then regional government, initiatives from 2008; before this, only industrial zones without administration or delimited territory existed (Keeble and Nachum, 2002; Kihlgren, 2003). The first IP was the venture of a Swiss development firm; others were initiated by banks to dispose of assets from failed construction firms amidst the 2008 economic crisis. Later, regional governments established specific departments to cultivate IPs as tools for economic development. These were popularized by further Federal legislation (Act 233) in 2012, which provided federal funding for IP establishment and subsidies for small and medium enterprises (SMEs) who became tenants (Sandler and Kuznetsov, 2015; Volkonitskaia, 2015).

Regional governments have been the main drivers of both SEZs and IPs in Russia, ostensibly aiming to agglomerate existing resources and businesses into larger entities, modernize facilities and workplaces to create strong national enterprises and reduce import-dependency (Yankov et al., 2016). But, in practice, SEZ and IP initiatives have been motivated by a desire to overcome particular political, economic or organizational challenges, rather than as part of a coherent regional development plan. As a result, while some projects developed as exemplars, most of them struggled (Kuznetsov and Kuznetsova, 2019).

Research on transitional economies emphasizes the central role of market liberalization and the development of liberal institutional arrangements to support this (Puffer et al., 2010; Williams and Vorley, 2014). Several scholars have noted the obstacles to Russian market liberalization posed by limited changes to informal institutions related to culture, attitudes and perceptions (Kuznetsov et al., 2000; Pililyan, 2016). Standard industrial cluster theory, however, gives little attention to such broader institutional factors (Puia and Ofori‐Dankwa, 2013; Sun et al., 2009; Wolman and Hincapie, 2014). So, this asymmetry between market liberalization and informal institutional factors provides a useful analytical framework for not only the examination of industrial clusters in Russia, but the consideration of industrial cluster policy in general.

The paper is structured as follows. A literature review introduces industrial cluster theory, its main factors and how these are related to the SEZ/IP policies, and then proposes an adaptation to the standard cluster model that is more responsive to regional and differing cultural and governmental contexts. Next, the application of the adapted model to the case of Russia is discussed and data collection and analysis methods are described. The third section presents and discusses the findings, testing the adapted cluster model. The paper concludes with a reflection on the implications of the findings for future development of economic zones and industrial parks in Russia and other transitional economies.

Literature

Special economic zones and industrial parks

Beyond the general positive externalities of agglomerating or clustering related economic activities, a SEZ is distinguished by specific characteristics. Its territory is geographically demarcated, it has a managing company or single administration, it offers tax benefits within the area, it provides an autonomous customs zone with simplified procedures and duty-free benefits, and it has more liberal economic and juridical regulations than in the rest of the country (Gupta, 2008; Tantri, 2016). SEZs are normally supported by government investments in infrastructure, access to research and development capabilities, and incentives to attract internationally competitive firms, as part of direct industrial policy intervention in order to promote regional economic growth (Aritenang and Chandramidi, 2019; Zeng, 2012). However, despite the global proliferation of SEZs, many have failed to fulfill objectives such as employment growth and export diversification; successful SEZs have been those that have upgraded their competitiveness and quality of services rather than relying on fiscal incentives (Moberg, 2015; Pan and Ngo, 2016; Yeung et al., 2009).

An IP differs from a SEZ by scale and specialization, tending to be SME-oriented, city-level development projects (Behera et al., 2012; Zeng, 2019). An IP is usually located outside a city’s residential areas but is supported by well-developed transport connections (Frej and Gause, 2001; Moore and Jennings, 1993). The model is based on the idea that establishing infrastructure in a specifically restricted territory reduces certain expenses for businesses (e.g. roads, railways, electricity, water and gas), while the location of industrial zones outside the city bounds decreases their environmental impact on urban areas (Geng and Hengxin, 2009; Ratinho and Henriques, 2010). Like SEZs, a prominent characteristic of IPs is access to research and development capabilities, such as universities or research centres (Liberati et al., 2016; Phillimore, 1999).

The role of SEZs in creating agglomeration economies has been under-investigated because of the assumption that they comprise trade enclaves with few domestic linkages, largely based on low-cost, low-skilled labour (Aggarwal, 2012; Aritenang and Chandramidi, 2019). Yet, the value of a SEZ depends not only on the proximity of companies but on collaboration, interaction and the networks that they set up with the local economy (Ambroziak and Hartwell, 2018; Moberg, 2015; Zeng, 2019). The presence of competitors, suppliers and consumers stimulates significant linkages, complementarities and knowledge and technology spillovers, thus fostering innovative activity and increasing productivity and competitiveness (Delgado et al., 2016; Gomis and Carrillo, 2016; Lazzeretti et al., 2019). However, a major barrier to SEZs and IPs accessing the positive externalities of geographic agglomeration is that whereas most industrial clusters emerge gradually through a ‘bottom-up’ process, SEZs and IPs are typically established on the basis of a ‘top-down’ approach by government policies (Aggarwal, 2012; Hsu et al., 2013; Zeng, 2019). Such external imperatives leave little room for the generation of important, organic, informal and slowly-developing interactions (Zeng, 2012, 2019).

The theory of industrial clusters

Marshall (2013 [1890]) was first to theorize the benefits gained from firms geographically collocated. The benefits include access to three kinds of positive externalities: specialized workers, specialized suppliers of inputs and services, and spillovers of technology and knowledge among companies sharing a location. These externalities are generated not only by geographic proximity, but also by sectoral, horizontal and vertical agglomerations of labour division (Carpinetti and Lima, 2013). All parties involved benefit from the collective specialization that comes from operating within the same industry, resource base and supply chain (Swords, 2013). In a similar manner, firms benefit from social, cultural and institutional proximity (Becattini et al., 2003).

The vitality of a cluster arises from the relationship between collaboration and competition. Collaboration with companies, customers, government agencies, universities and other organizations reduce transaction costs by pooling infrastructure, generating knowledge and technology spillovers (Feldman et al., 2005). Demanding customers, venture capitalists’ support and knowledge-intensive service providers create intense pressure to innovate (Ketels, 2013). Collaboration and rivalry drive specialization, innovation, competitiveness and business formation (Delgado et al., 2014; Puppim de Oliveira and de Oliveira Cerqueira Fortes, 2014). While Marshall (2013 [1890]) emphasized the spontaneous, endogenous development of industrial clusters via congruence of concentrations of skills and proximate markets, other researchers have observed how exogenous, mainly government policy, influences can accelerate the process (Lazzarini, 2015; Lee et al., 2017). But outcomes can be positive or negative, depending largely on the robustness of government strategy, with a focus on establishing an enabling business environment more effective than direct intervention (Vernay et al., 2018; Zhong and Tang, 2018).

In his influential, now standard, model of industrial clusters, Porter (1990) summarizes the cluster determinants as a ‘diamond’ of interacting drivers of competitiveness: factor conditions; demand conditions; related and supporting industries; firm strategy, structure and rivalry, albeit conditioned by exogenous government and ‘chance’ influences. While initially proposed as an explanation of differences in national competitiveness, Porter’s diamond has been applied extensively at an industry level (Fang et al., 2018; Lazzarini, 2015). Yet, while providing a very influential contribution to the understanding of international competitiveness, there are limitations in the deployment of Porter’s diamond to different regional, cultural and governmental contexts.

Adapted cluster model

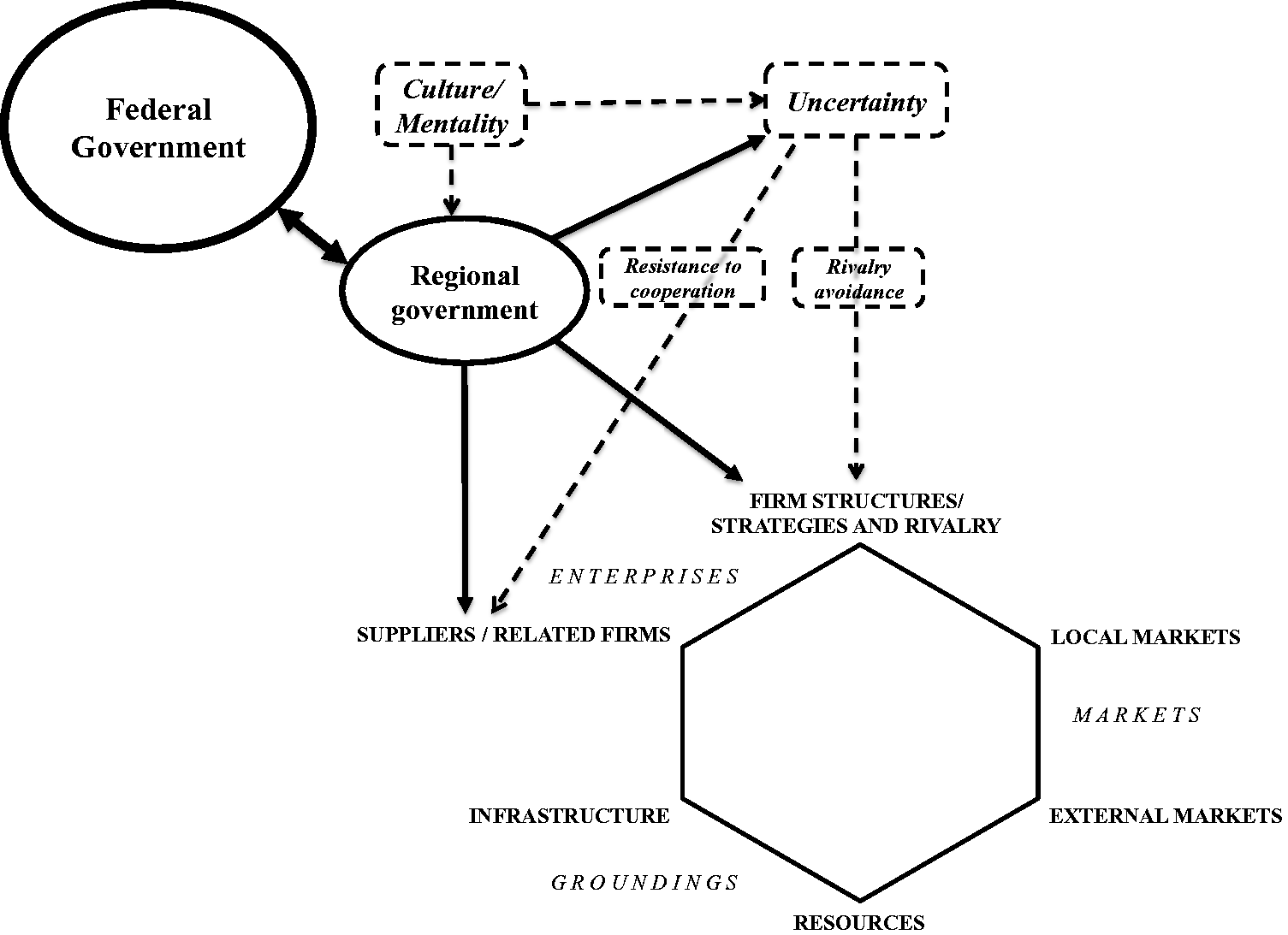

Padmore and Gibson (1998) argue it is necessary to adapt Porter’s diamond for use in a regional context. They give greater attention to regionally specific variables via the addition of infrastructure and access external markets variable. The six variables in this adapted model are grouped into Groundings (resources and infrastructure), Enterprises (suppliers and related firms, firm structures/strategies and rivalry) and Markets (local markets, and access to external markets), given the acronym GEM. Like Porter, they note the conditioning role of government in shaping the configuration of factors but particularly emphasize the way state-owned companies can have a large effect at a regional level.

Van Den Bosch and Van Prooijen (1992) criticize Porter’s model for omitting consideration of the role of national culture in cluster dynamics, a criticism that can also be applied to Padmore and Gibson’s (1998) adaption. Common language and culture are preconditions for maintaining linkages among companies and facilitating learning activities such as knowledge sharing, transfer, and absorption and greatly affects behaviour such as trust, collaboration and competition (Nestle et al., 2019). Van Den Bosch and Van Prooijen (1992) argue that Porter’s framework betrays a Western bias, which welcomes fierce competition as beneficial for productivity growth and innovation. Yet, different countries have different attitudes towards competition and cooperation (Nestle et al., 2019). In some cultures business relationships are built primarily on personal relationships and trust rather than just mutual economic benefit (Cai et al., 2013; Karhunen et al., 2018) and firms in some countries prefer to cooperate rather than compete (Gomis and Carrillo, 2016; Yuan et al., 2010). Countries also differ in their perceptions of international competition, both in openness to exporting and receptiveness to imports, related to cultural differences towards uncertainty (Trompenaars and Hampden-Turner, 2011).

Moreover, each country has its own peculiarities and specific governance structure, managerial systems and culture and legal and regulatory regime that shape the actions and responses of firms (Chandler and Hikino, 2009). Porter’s diamond assumes a limited-interventionist role for government as a policy facilitator, institutional infrastructure provider and legal regulator. Its role is to establish a stable and business-friendly commercial and socio-political climate in successful clusters with well-defined property rights, implementation enforcement of such property rights, administration of a fair and efficient legal system, low crime rates and corruption, business-government cooperation and the support of entrepreneurship, risk-taking and business innovation (Lazzarini, 2015; Vernay et al., 2018). Other national contexts may expect greater and more targeted government intervention. The capabilities of some small producers can be improved essentially through government action to strengthen the local market and for companies to seek exporting opportunities (Lazzarini, 2015; Swords, 2013). The government can also provide additional demand for locally produced goods and services through procurement policy, which may act as a catalyst for regulative institutions (Etzkowitz, 2008). Particularly during the formation and stabilization stages of an industrial cluster, the government can facilitate initial cooperation between cluster participants to stimulate knowledge flow and technology transfer (Zhong and Tang, 2018). Further, in light of the potential for national culture to affect cluster dynamics, we propose that a government may have an additional role that has not been discussed previously in the literature concerning industrial clusters, which is to intervene to mitigate these cultural effects among business-government networks at a personal level.

In order to accommodate regional, cultural and governmental differences that are likely to be encountered in distinct national contexts we propose an adaptation of Padmore and Gibson’s (1998) model of industrial cluster competitiveness, sensitive to informal institutional structures. In this adapted model (Figure 1), we emphasize the distinctive role of regional government to localized industrial clusters and the additional conditioning role of national culture, particularly attitudes towards uncertainty. As discussed above, these attitudes have considerable potential to affect the central mechanisms of cluster dynamics in the standard model, the interaction between collaboration and competition. Further in this paper, we present our findings within the categories of our adapted GEM model: Groundings (resources and infrastructure), Enterprises (suppliers and related firms, firm structures/strategies and rivalry) and Markets (local markets, and access to external markets). We discuss our results according to each of the category of this model with specific focus on two dimensions of the category – Enterprises (Figure 1). We argue that low tolerance for uncertainty may generate resistance to cooperation and avoidance of rivalry, impacting on firm structures, strategies and rivalry and on the relationships between suppliers and related firms. Further, the adapted model illustrates the potential for regional government to mitigate attitudes to uncertainty by providing timely funding, building personal relationships among participants and potential investors, and providing political guarantees.

Adapted GEM model.

Summary

SEZs and IPs have been identified as valuable mechanisms for regional economic development, drawing on an influential industrial model highlighting the reinforcing effects of the interaction of cooperation and competition in geographic agglomerations. Cluster policies drawing on this model have been widely adopted worldwide. However, limitations in the standard model suggest its implementation in some non-Western contexts may not be as effective as expected. In particular, an adaptation is needed to apply the model more effectively in a regional context and in differing national cultural and governmental contexts.

Research setting

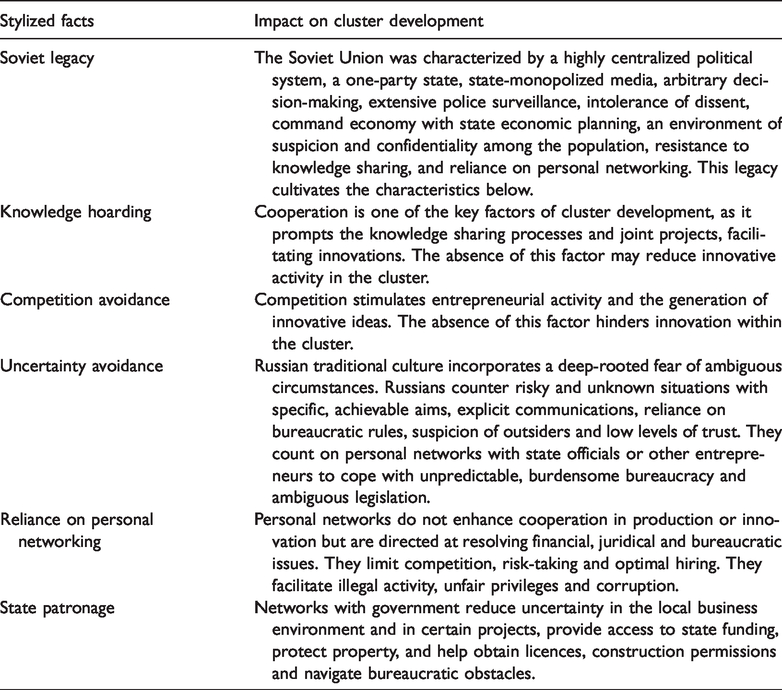

We employ our adapted model to examine the adoption of industrial cluster policies in Russia (Mindlin et al., 2016; Rodionova et al., 2018), a considerably different cultural and governmental context to that normally discussed in the cluster literature (Delgado et al., 2014; Lazzarini, 2015). Factors highlighted by this examination are likely to be relevant to other similar social and political contexts. This study is the first substantive examination of cluster policies in this research setting. We discuss the research setting via a set of stylized facts, which emerged as recurrent themes in our reading of the literature on the contemporary Russian business environment. These comprise: the legacy of the Soviet period in Russia (Oxenstierna, 2015); reluctance to share knowledge (May and Wayne Jr, 2013); avoidance of competition (Kuznetsova and Roud, 2014); avoidance of uncertainty (Liuhto et al., 2017); reliance on personal networks (Ledeneva, 2013); and the importance of relationships with state institutions (Sharafutdinova and Turovsky, 2017).

Soviet legacy

The contemporary Russian Federation emerged from the main remnant of the collapse of the Soviet Union, a federation of socialist states between 1922 and 1991. The Soviet Union was characterized by a monolithic political system, a one-party state, state-monopolized media, arbitrary decision-making, extensive police surveillance and intolerance of dissent (Albats, 1995). All these generated a climate of suspicion and confidentiality among the population (Pauleen, 2007) that continues to hamper knowledge sharing in contemporary Russia (Michailova and Hutchings, 2006). The inability to rely on legal protection from arbitrary decisions forced people to protect their interests by cultivating relationships with those with power (Ledeneva, 2013).

The Soviet economy had been characterized by: (1) a highly centralized command economy, in which the government determined what goods should be manufactured, their quantity, and the price at which they should have been offered for sale (Sakwa, 2008); (2) state economic planning, in which investments, manufacturing and distribution of means of production were carried out in accordance with national or regional economic plans (Liuhto et al., 2017); (3) rapid growth of large-scale state-prioritized enterprises alongside bottlenecks, inefficiencies and goods shortages (Andrianov, 1997; Barkhatova, 2000); (4) personal consumption amidst shortages was maintained by ‘blat’, a friendly exchange of favours and support with state personnel enjoying privileged access to goods (Karhunen et al., 2018). Consequently, experience with market mechanisms, private ownership, competition and entrepreneurship were very limited (Resnick and Wolff, 2013). Norms, values, social customs practiced during the Soviet period continue to dominate everyday practice, particularly hampering entrepreneurial behaviour (Williams and Horodnic, 2015).

Large parts of the Soviet economy were concentrated in large conglomerations, including firms in the energy sector, the oil and gas industry, aluminium, the airspace industry, strategic defence and the exploitation of waste natural resources. While these were internationally competitive, this was achieved mainly by considerable support from the central government in the form of state funding provision and legal protection (Oxenstierna, 2015; Tsygankov, 2014). This concentration left smaller firms highly dependent on maintaining close relationships with the industry leaders and little scope for entrepreneurial initiative.

Competition avoidance

The Russian economy and political system remain highly centralized, with government greatly embedded in the business environment (Becker and Oxenstierna, 2018). The largest corporations are state-owned or closely directed by the state, seen to contribute to defence of national interests in the international political arena (Tsygankov, 2014). This generates a business environment in which even SMEs are essentially dependent on Russian state-owned MNEs. Their key consumers or suppliers are state monopolies that give them exclusive partnership contracts and, thus, dictate the conditions of the deal; if they do not operate in this way, SMEs risk losing vital partners (Ross, 2014).

Geographical factors also play a part. Markets are geographically far away from each other due to the great size of the country and its uneven infrastructure (Tsukhlo, 2007). If a firm is located in a region with poor transport connections, then it possesses some local monopoly power because its rivals are located far away in other regions (Brown and Earle, 2000; Mau, 2017). Each region or a federal zone, such as the Urals, Siberia, Altai, the Caucasus, etc., can be perceived as a separate market with its own dominant players (Shtanchaeva et al., 2015). These conditions limit the scope for entrepreneurial activity and reduce potential benefits to efficiency and productivity from competitive activity. Russian entrepreneurs also actively avoid competition because they perceive as a threat due to the inability to work in such environment as a consequence of the centralized economy (Pavroz, 2017; Tsygankov, 2014). For this reason, they rarely see competition as a benefit or know how to extract benefits from it (Oxenstierna, 2015).

The dominance of state-related monopolies in the economy sustains and is reinforced by a prevailing perception and acceptance that power holders are very distant from ordinary society and there is a huge gap between powerful and less powerful people; Russia has a high power distance culture (Hofstede et al., 2010). This leads to attitudes of deference to authority, goal attainment through appeals to the powerful, and suspicion of others, all driving individual passivity and fatalism (Ledeneva, 2013).

Uncertainty avoidance

Russian traditional culture is marked by a deep-rooted fear of ambiguity (Grigoriev and Dekalchuk, 2017). Russians attempt to counter ambiguous or unknown situations with specific, achievable aims, explicit communications, reliance on bureaucratic rules, suspicion of outsiders and low levels of trust (Leppänen et al., 2012). Hofstede et al. (2010) describes this as ‘uncertainty avoidance’. Uncertainty avoidance differs from risk aversion; ‘uncertainty is to risk as anxiety is to fear’ (Hofstede et al., 2010: 197). Risk expresses the probability of a certain event occurring, an expected outcome; risk aversion is the pursuit of a more probable outcome to reduce the fear of failure. Uncertainty has no probability of happening, anything can potentially occur. When uncertainty becomes a risk, it stops being a source of anxiety. Instead of leading to risk reduction, uncertainty avoidance leads to ambiguity reduction. Hofstede et al. (2010) suggest that people in cultures with high level of uncertainty dimension seek increased structure in their organizations, institutions, and relationships that make the procedures clear, explainable and predictable. In Russia, for example, one of the most complicated bureaucracies in the world was created (Leppänen et al., 2012). Also, negotiations are well prepared and commonly focused on relationship building; possessing context and some background information is favourable (Grigoriev and Dekalchuk, 2017). Russians prefer to build personal relations in business to avoid uncertainty. Trust and relationships with individuals have more importance than legal contracts (Trompenaars and Hampden-Turner, 2011).

Knowledge hoarding

A consequence of uncertainty avoidance is a reluctance to share knowledge, prefer to work only with people with whom they are familiar and avoid outsiders; sharing knowledge is perceived as potentially harmful (Puffer and McCarthy, 2011). Knowledge hoarding in Russia is reinforced by three features: uncertainty about how the receiver will use the shared knowledge; accepting and respecting a strong hierarchy and formal power; and anticipated and experienced negative consequences of sharing knowledge, part of the Soviet legacy (May and Wayne Jr, 2013).

In management, Russians tend to associate knowledge with formal, position-based power, rather than seeing knowledge as a necessary condition and organizational resource for taking optimal managerial decisions. Russians often talk in terms of subjugating people rather than leading them and consider this one of a manager’s most important roles. Russian managers believe they should always be more knowledgeable than their employees (Michailova and Husted, 2003). This prevents managers from approaching employees as sources of ideas and reliable knowledge or believing they can learn from their employees (Fey and Shekshnia, 2011). Knowledge hoarding and minimal disclosure of company information undermines effective corporate governance and knowledge sharing (Estrin and Prevezer, 2011; Puffer and McCarthy, 2011), key components of the cooperation contributing to the vitality of industrial clusters.

Reliance on informal personal networks

Following the fall of the Soviet Union in 1991, the formerly allocated relationships between suppliers and producers collapsed (Gurkov, 1996), being replaced by supply relationships formed through informal personal networks (Ledeneva, 2013). In addition, entrepreneurs find it difficult to protect property rights and resolve business disputes as while legal processes are formally in place, the rules are implemented inconsistently (Tonoyan et al., 2010; Williams and Horodnic, 2015). Interpersonal networks continue to be important in the face of an uncertain and unstable economic and legal environment, as interpersonal trust mitigates risk and reduces the influence of turbulent macro-environmental changes and arbitrary legal decisions (Grigoriev and Dekalchuk, 2017; Klarin and Sharmelly, 2019). The economic reliance on informal networks, the need to navigate the corridors of state power, combined with a desire to avoid uncertainty and low-trust environment leads to a strong emphasis on personal networking. In Russia, it is important to establish useful networks and contacts in order to gain access to people who can help overcome problems in conducting business activities and cope with bureaucratic procedures (Becker and Oxenstierna, 2018; Tsygankov, 2014).

With the post-Soviet market reforms, the ‘blat’ exchange of favours was monetarized and transformed into bribing (Hsu, 2005; Ledeneva, 2013). The term has become interchangeable with ‘svyazi,’ which means ‘connections’ or ‘networks’ (Karhunen et al., 2018). Entry into networks provides access to additional favours from other members of the network, beyond market transactions. These include price benefits, the opportunity to obtain goods and services without payment in advance, inter-firm credit, and overcoming administrative barriers and bureaucracy (Karhunen et al., 2018; Ledeneva, 2013). Competition in Russian markets now typically represents competing networks rather than competing independent companies (Pililyan, 2016). This emphasis on establishing useful networks and contacts is valued more than hard work and talent as drivers of success (Kuznetsov et al., 2000). But these relationships do not enhance cooperation in manufacturing or innovation but are rather merely directed at resolving financial, juridical and bureaucratic issues (Klarin and Sharmelly, 2019). Furthermore, personal networking results in limited competition, difficulties in hiring the best employees, illegal operations, limited risk-taking, unfair privileges and corruption (Butler and Purchase, 2004; Ledeneva, 2013; Michailova and Worm, 2003).

State patronage

A crucial part of Russian business strategy is to develop and maintain relationships with reliable supporters within state institutions, such as in the tax and customs offices, to protect the interests of the business (Ross, 2014). These relationships with officials sometimes involve bribes; more often it is about an exchange of favours (Ledeneva, 2013). State officials reassure entrepreneurs that their interests will be represented and there is no reason to worry; later, entrepreneurs are contacted and asked for a favour in return, and this request will be perceived as a commitment (Rochlitz, 2014). As a result, in the conditions of the dominance of national state-owned manufacturers, SMEs do not work independently. Their key consumers or suppliers are the state monopolies that through personal networks award them exclusive partnership contracts and, thus, dictate the conditions of the deal; if they do not cooperate, SMEs risk losing their key partners (Tsygankov, 2014). Hence, the current business environment in Russia encourages entrepreneurs to avoid competition and instead build useful networks for successfully conducting business activities.

Personal networking also takes place in the intergovernmental vertical hierarchy in Russia. While the federal government in Moscow makes fiscal decisions centrally, regional governments are not simply subordinated local agents of the federal government (Sharafutdinova and Turovsky, 2017). Rather, the situation is one of mutual dependence; some regional governors have been in power in their regions for a long time and have developed significant networks of support both locally and in Moscow; others had come from Moscow with existing support at the federal level. Governors with such strong networks and best lobbying skills are the most successful in attracting federal financial support into their regions (Sharafutdinova and Turovsky, 2017). Regional authorities need to mobilize all their networks with influence in federal institutions, whereas in their own region they must organize a strong team of state managers capable of generating ideas and projects and deliver solid results when the initiatives are implemented (Sharafutdinova and Steinbuks, 2017).

Business investment decisions in this context are not those of standard risk assessment of expected returns but assessment of the conditions characterized by the dominance of personal networks and arbitrary application of formal rules and regulations, in which any political change may revoke all former agreements and relationships generating uncertainty and unpredictability for regional businesses (Ershova, 2017; Liuhto et al., 2017). In Russia, many of these companies count on the goodwill of the regional authorities for gaining licences, construction permissions and avoidance of bureaucratic procedures related to doing business. Others may rely on political networks to gain access to state-funded contracts and projects (Demidova and Yakovlev, 2012; Sharafutdinova and Steinbuks, 2017). And there is refuge in numbers; Feldman et al. (2005) suggest that co-locating firms reduces uncertainty as it increases the awareness of emerging trends: innovation clusters spatially in locations where knowledge externalities lower the costs of discovery and commercialization.

Summary

Table 1 summarizes these stylized facts about the Russian business environment and how these impact on the standard industrial cluster model. Each of the factors resulting from the institutional behaviour of the Russian mentality coming from traditional culture and the Soviet past, reinforced by the post-Soviet rapid market liberalization impacts on business behaviour in industrial clusters.

Stylized facts about Russia and its culture in relation to industrial cluster model.

Methodology

In order to examine the impact of political and social context on the dynamics of industrial clusters, we undertake a detailed study of industrial SEZs and IPs established in Russia since their start in the mid-1990s. Previous studies of cluster policies in Russia are limited to descriptive accounts (Maslikhina, 2016; Sandler and Kuznetsov, 2015; Yankov et al., 2016) reliant on secondary data about the SEZs and IPs that had been implemented from 2005 (Kuznetsov and Kuznetsova, 2019; Turgel et al., 2019; Zhukovskaya et al., 2016). Our study is more comprehensive and involves primary data. We employ a multiple-method approach, which both examines relationships between variables quantitatively and also enriches and contextualizes findings. We analyse the business performance of the zone and park management companies and their tenant firms, drawing on financial data, questionnaires and interviews with a large sample of managers. We then utilize our adapted model to attempt to account for the business performance of the SEZs and IPs in the light of the management responses and the stylized facts about the Russian business environment.

Pilot study

The first stage of our fieldwork (December 2015 – January 2016) was an exploratory pilot study, comprising 14 two-hour semi-structured interviews within six SEZs (Titanium Valley, Alabuga, Lipetsk, Togliatti, Moglino and Kaluga), the manager of each, two tenants from each of the first three, and two representatives from the Association of Industrial Parks (AIP) in Russia. Three types of interview for three groups of respondents were composed. We gained a preliminary understanding of the background of SEZ development in the country in general through semi-structured interviews. These were especially well-suited to the pilot data collection stage because there was little pre-knowledge of the phenomenon that was to be investigated, and there was uncertainty about whether the questions asked were appropriate and correct (Denzin and Lincoln, 2017). The interviews were face-to-face meetings undertaken at the participants’ offices. Participants were general directors, deputy directors and research managers. The SEZ tenants belonged to the following industry sectors: titanium production, the production of components and equipment for metallurgy and mechanical engineering, and the manufacturing of plastics, rubber and chemicals. Interviews were conducted in Russian and subsequently reviewed and translated into English.

Main study: sample for field research

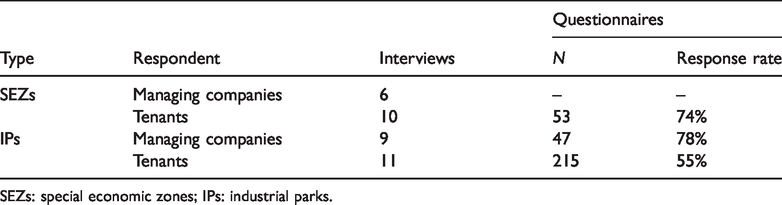

Our starting point for field research was the entire population of industrial SEZs and IPs in Russia. This was compiled from a list of all six Russian industrial SEZs 1 from the website of the state-owned JSC Special Economic Zones managing company and a list of all 120 legally certified IPs from the 2015 annual report of the AIP (Sytchev et al., 2015). The managing companies of SEZs/IPs and their tenants were screened using data from the official websites of SEZs and IPs, the SPARK-Interfax database, and direct enquiries via email or phone. During the main data collection process (November 2016 – June 2017), we discovered that many parks did not exist yet or comply with the AIP accreditation criteria. They were merely traditional industrial zones without any managing company or governance, mutual resources or infrastructure, while some tenants listed on the websites of the IPs did not yet operate on the territory of the park. This reduced the overall size of the park population. Tenants were selected where they: (1) were currently functioning on the territory of the zone or park; (2) had signed a contract with the managing company of the zone or park and be in the process of constructing buildings and manufacturing facilities on the territory of the zone or park; (3) were not operating as a sole trader, sole entrepreneur, sole proprietorship or self-employed individual; (4) were engaged in production or manufacturing activity, not simply trading. This resulted in a population of 60 managing companies and 390 tenants in IPs and six managing companies and 72 tenants in the SEZs. Questionnaires were distributed by email to all tenants of SEZs and IPs and IP management companies that met the selection criteria, addressed to the Director, Deputy Director or Head of Investor Relations. Non-respondents were followed-up by phone calls. Table 2 summarizes the responses. 2

Number of interviews conducted, and questionnaires completed.

SEZs: special economic zones; IPs: industrial parks.

Field data collection

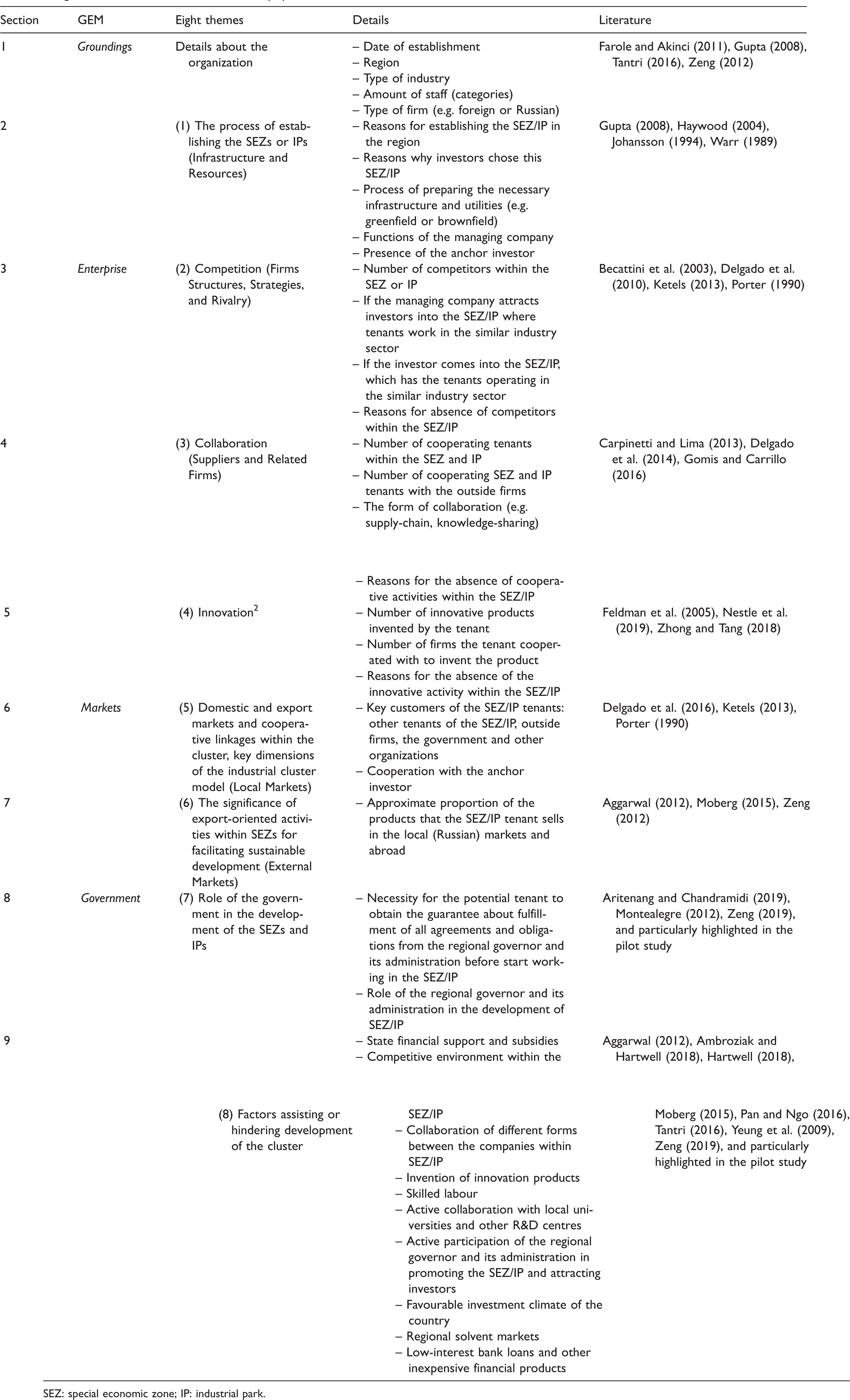

Profiles of each managing company and tenant were compiled from data drawn from the SPARK-Interfax database and the official websites of SEZs and IPs. These included the date of firm establishment within the SEZ/IP, industrial sector, employees, annual revenues, debts, subsidiary status of companies, foreign ownership, ownership structure, competitors, collaborators, legal actions and connections with state institutions. These profiles helped to triangulate, enrich and complete the data obtained via interviews and questionnaires. A questionnaire and interview protocol were developed around eight themes drawn from the literature review and a pilot study (Table 3). We asked similar questions to the managing companies and tenants but from different angles depending on the type of participant. For example, how the managing company established the infrastructure for the tenants or how the regional government helped the development of the zone/park and its tenant versus how the tenants described the process of the infrastructure establishment for them and how the regional government helped the development of their zone/park and their enterprise. Similar topics for interviewing and questionnaires enabled the comparison and confirmation of the qualitative and quantitative results as well as revealing inconsistencies in responses. The questionnaire predominantly comprised ranking and rating questions, together with some quantitative questions and one open question at the end, to allow participants to provide a fuller response in their own words. Participants were asked to take part in a follow-up interview.

Eight themes of the interview and survey questions.

SEZ: special economic zone; IP: industrial park.

Drawing on Lancaster (2017), we prepared carefully for the interviews with ‘elite’ participants from state-owned organizations and industry representatives, which required preparatory work, giving particular attention to trust building when organizing meetings and conducting interviews (Ostrander, 1993). Some relationships needed careful management both before and after the interview. Some participants were enthusiastic about sharing their experience, perspectives, and time for research. Access barriers with other participants related to the cultural and political context of the country; there is an informal division between those who favour adopting a Western lifestyle and absorbing Western knowledge and technology and those who push for an all-Slavic way of life and favour the development of specifically Russian science, trade and technology (Gurkov, 2016). As we were representing a western university, some participants perceived us a threat, fearing disclosure of potentially valuable knowledge. The influence of work culture was particularly noticeable in connection with meetings with participants working in state-owned managing companies and their tenants. Our participants were informed that we were collecting data from other similar organizations within the zone or park, but we avoided providing precise names of these or details of their responses to preserve participant confidentiality. We used numerical codes when recording the data and gave assurances that only these rather than names would be used throughout the analysis.

Data analysis

Summary statistics of responses were compiled from the questionnaire data and organized by each of the four main categories of our adapted GEM model: Groundings, Markets, Enterprises and Government. These were supplemented by a thematic analysis of the interviews. We used a predominantly deductive approach to analyse interview responses, coding and theme development directed by the eight topic categories, which had been drawn from the literature review and pilot study. After an initial familiarization read-through, the interview transcripts were systematically coded in NVivo11, sentence by sentence, to the eight topics, supplemented by emergent themes, which were added to the coding table. This involved the identification of word repetitions, key-indigenous terms, and key-words-in contexts (Denzin and Lincoln, 2017). The codes were then reviewed for overlaps and combined where there were few occurrences (Miles et al., 2014). After the initial coding, the transcripts were then re-examined in the light of the emergent codes and recoded, re-reading until few substantial new themes emerged (Glaser and Strauss, 2017). We used axial coding (Corbin and Strauss, 2015) to identify the relationships between codes emerged from different types of respondents. Through this process, we created 19 sub-categories within the eight themes (Online Supplemental Table 1) with circa 120 codes. The codes in each sub-category were also cross compared among all four types of respondents and put in a specific logic order so that afterwards that qualitative data were interpreted.

Findings

We present our findings within the principle categories of our adapted model: Groundings, Markets, Enterprises and Government.

Groundings

The industrial clusters studied were generally well-provided in terms of Groundings, that is, factor conditions, resources and infrastructure. The SEZs and IPs were established to leverage regional concentrations of resources (Turgel et al., 2019; Yankov et al., 2016). Questionnaire responses revealed that the dominant industry sector in both SEZs and IPs was general manufacturing of various goods, equipment and components: 49% among SEZs and 56% among IPs. The second most frequent was mechanical engineering (23% among SEZs and 15% among IPs), the focus of the Togliatti SEZ and an automotive manufacturing cluster in the parks of the Kaluga region. The third most prevalent industry was chemical engineering (13% among SEZs and 10% among IPs), predominantly due to the chemical cluster in the Republic of Tatarstan. Textile firms were overwhelmingly located in the Ivanovo region. The pharmaceutical sector was mostly located in the Kaluga and Belgorod regions.

SEZs offered greenfield

3

modes of investment to their potential tenants, whereas in IPs, tenants could choose between greenfield and brownfield

4

(Kuznetsov and Kuznetsova, 2019; Sandler and Kuznetsov, 2015). According to survey results, there were notable differences between zones and parks in terms of these different investment modes. As summarized in Table 4, zones comprised greenfield projects only and only in 11% of cases utilities had already been established in advance. Parks offered their potential investors both greenfield and brownfield opportunities; in both, utilities were almost always in place. Tenants reported greater delays than anticipated in the provision of utilities and other infrastructure. The standard model suggests that infrastructure should be created first in order to attract investors (Tantri, 2016; Zeng, 2019). Nonetheless, Russian SEZs and IPs attempted to attract tenants or receive primary contractual obligations during the first stages of development; only later did they begin to build the necessary infrastructure. In some cases, zones and parks began preparing infrastructure for specific tenants while the latter were building their facilities on site. One of the SEZ managing companies stated:

5

We cannot build the infrastructure first. This approach does not suit our realities. What happens if we prepare the infrastructure for the entire SEZ territory and do not manage to attract all the investors straight away? Who is going to cover the costs of unused areas? We need to get initial contractual obligations from the investor that shows their serious intentions and financial capacity for the project. Afterwards, we start establishing the infrastructure in a certain delimited area specifically for that investor.

The process of infrastructure preparation for SEZ and IP tenants.

SEZ: special economic zone; IP: industrial park.

The general uncertainty of the Russian economic environment evident in the idealized facts in the section ‘Research setting’, created a climate in which SEZ/IP managing companies did not want to risk spending their budget on the construction of an entire infrastructure without seeking certain obligations or promises from investors first. At the same time, neither foreign nor local potential tenants wanted to make these promises, as they faced the real risk of losing their investments if the projects failed. High levels of uncertainty and the risk that contractual obligations would remain unfulfilled put investors off entering zones. In the questionnaire, 42% of tenants reported that infrastructure had not been prepared in time for the opening of the zone or park due to insufficient state funding (e.g. in the Titanium Valley SEZ); 17% complained that managing companies failed to monitor the workability of existing infrastructure effectively (e.g. the Orel IP), or charged tenants additional or significantly increased fees (e.g. in the Pro-Business Park IP). Provision varied between regions because of differences in timely provision of infrastructure funding guarantees by regional governments and the extent to which managing companies were responsible for monitoring the efficiency of infrastructure.

Markets

This dimension evaluates the categories of local markets and access to external markets within the GEM model. Economic zones are expected to stimulate and diversify export-oriented activities in the host country by establishing the networks between foreign and local businesses and gaining access to global value chain (Hartwell, 2018; Tantri, 2016). The SEZs and IPs were located in 25 different regions that produced a wide variety of resources and local markets. SEZs and IPs located in the western part of the country had the potential to access European borders and partners from the Middle East. However, few tenants took advantage of these opportunities. In the questionnaire responses, the majority of tenants in the SEZs and IPs were foreign subsidiaries (35%), newly formed Russian companies (34%) and Russian subsidiaries (23%) (Table 5). Most tenants joined SEZs (32%) and IPs (29%) because of the proximity of the zone or park to potential domestic (Russian) markets (Figure 2). Also, Table 5 confirms that most SEZ and IP tenants of all types (foreign and Russian firms) did not export. For example, 42% of newly formed Russian, 29% of foreign and 22% Russian subsidiaries operated in local Russian markets only.

Cross-tabulations: Types of tenant in the SEZs and IPs vs. percentage of sales in local (Russian) markets.

Key reasons why tenants selected a particular SEZ or IP, %.

One IP tenant, a Russian firm, specified: We are small and medium companies here in the parks. All we need is the established infrastructure, utilities, and access to local (Russian) markets. We don’t have financial capacity and competitive advantage to operate abroad. Large local companies can but they also cooperate with foreign firms here in Russia. But we don’t – our business doesn’t require this. We do not need them, and they do not need us. We produce and sell locally, and that is enough for current state of affairs.

Enterprises

Enterprise factors involve the elements of cooperation (suppliers and related firms) and competition (firm structures/strategies and rivalry) in the GEM model. However, in the Russian SEZs/IPs these did not work well to stimulate productivity and innovation, with limited competition and collaboration widely evident.

Firm structures/strategies and rivalry

The questionnaire responses demonstrate that competition was actively avoided in SEZs and IPs: 70% of SEZ tenants and 77% of IP tenants claimed that they would not enter the zones and parks with existing competitors. Also, zone and park management companies explicitly rejected the creation of a competitive environment as they did not see any benefits in it.

Three main reasons were cited by tenants in the questionnaire responses to explain the absence of a competitive environment in zones and parks (Figure 3). Firstly, potential tenants did not want to enter zones that contained existing competitors and the existing tenants of zones negotiated with their managing companies to ensure that companies operating in the same market segment would not be attracted to their zone (31% among SEZ and 34% among IP tenants). Managing companies opted to agree to, or even anticipate, such requests. Secondly, managing companies and state officials did not want to create a competitive environment in their regions or around the zones, for fear of chaos (29% among SEZ and 19% among IP tenants). In order to manage this, potential investors were assessed by a group of experts to check that they would not compete with existing tenants. Thirdly, some of the tenants’ rivals were operating in other regions of Russia (18% among SEZ and 24% among IP tenants). One SEZ tenants explained:

Reasons for the absence of competition in SEZs and IPs: Comparison of responses from SEZ and IP tenants, %.

It is difficult to say who initiates that. Competition simply does not exist in this zone. We did not ask the managing company to refuse our competitors entry. But, as far as I know, the managing company has certain selection criteria for tenants, so they may have some control over this. But we carried out research before coming to this zone and did not want to go where our competitors were already in operation. Now, we do not care, but our competitors do not enter this zone. It seems they have done the same way we have.

Tenants try to avoid competition for the reasons discussed in the section ‘Research setting’; they have no substantial experience operating in such an environment and instead rely on cultivating relationships with key customers and suppliers via local monopoly positions in geographic isolation.

Suppliers/related firms

At the same time, there is very limited cooperation within the SEZs and IPs. In the interviews, two SEZ managing companies discussed strategies to create supply chain cooperation, and some economic zones initially planned to create a cluster (e.g. a titanium cluster in the Titanium Valley SEZ, automotive manufacturing in the Togliatti SEZ and parks in the Kaluga region). However, tenants seldom engaged with such cooperative strategies. Questionnaire responses show tenants wanted to cooperate but did not have any opportunity to do so (33%) or tenants did not want to cooperate because they did not see any benefit in it (30%). In the first situation the management companies did not see benefits from attracting complimentary tenants; in the second, the tenants did not see benefits in cooperation. This reluctance to cooperate with outsiders is characteristic of the uncertainty avoidance and knowledge hoarding in Russia, discussed in the section ‘Research setting.’ The limited competition and cooperation within the clusters provides an explanation for the low level of innovative activity reported. In the questionnaire responses, 17% of SEZ and IP tenants reported inventions or patents, with medians of 0% and 4.2% and standard deviations of 16.2% and 4.6% among regions, respectively. The only outlier was the Lipetsk SEZ, with 36.4% of tenants being innovative. Again, tenants mainly cited seeing little benefits in innovation as they were satisfied with their position in the market (31%); SEZs, IPs or tenants were not sufficiently developed to innovate (25%); or the tenants’ parent, located either elsewhere in Russia or abroad, did not allow them to innovate (18%). An IP tenant explained: We do not see any point in modernising our products or inventing anything new. We simply buy equipment and make products. These are very simple and primitive products that do not need any adjustments. Our clients do not need anything new. We produce what they ask for. Perhaps something can be done in the manufacturing process, but it does not concern us. Besides, innovation is costly and involves cooperation, which is too much of an effort.

Government

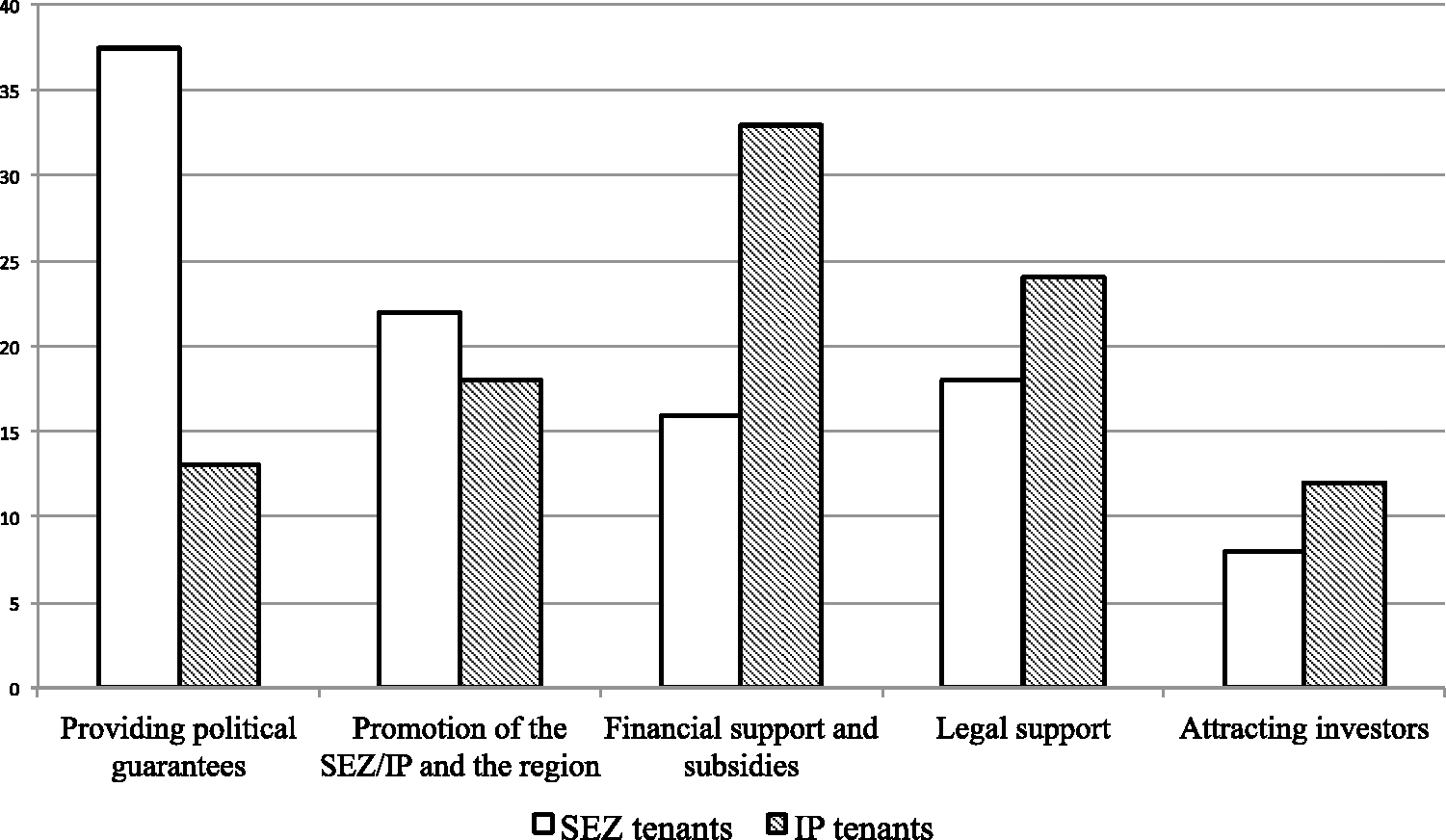

Underpinning the limited competition and cooperation in the SEZs and IPs was considerable evidence of uncertainty avoidance. In the questionnaire responses 60% of potential tenants had requested personal meetings to obtain political guarantees before investing. Interviewees reported that a major concern when considering investing was fear that the SEZ or IP projects were money-laundering schemes for the regional elites. A SEZ tenant stated: It perfectly reflects the reality of doing business in Russia. Either personal networks with the managing company of a particular SEZ or building warm relations with regional authorities impact our (tenants’) final decision. Obviously, the location and proximity to resources play an important role as well. But when the subject of negotiations concerns the investment of hundreds of millions of U.S. dollars, we require guarantees that the project is feasible and contractual obligations will be fulfilled. For big corporations, personal networks play a vital role in the selection of an economic zone. You do not just need proximity to markets: most of the parks are in the western part of Russia anyway. You need trust and feasible SEZs and IPs. Otherwise, you know how it can happen: they establish the park, get the state funding, and then disappear.

Major government roles within the development of SEZs and IPs in Russia, %.

Interviewees reported that the managing companies established zones and parks with the help of personal networks established between federal and regional governments. Such networks provided regions with privileges, including assistance with resolving financial issues, accelerated processes for obtaining necessary permissions and opportunities to promote IP projects at international political forums, sports events and in SEZs. Managing companies expected their regional governments to help attract investors, especially big, foreign firms, as government involvement expedited investors’ decisions. Having useful networks at the federal level, regional governments received necessary financial support. At the same time, the majority of both SEZ and IP tenants claimed that they had requested a political guarantee from the management of zones and parks before making the final decision to set up business there. This mostly took place among foreign firms in state-owned parks. These political guarantees involved personal meetings and, in some cases, the building of personal relationships with regional state officials, often governors or deputies. An IP managing company manager said: The regional government plays a crucial role in establishing both SEZs and IPs in a region. It is not only about funding, but also about bringing MNEs into the region through personal networks, which subsequently help to attract other good investors to the project. A good example is the Kaluga region, where the regional governor managed to attract several large investors to its parks, such as Volkswagen, L’Oréal, Continental, Samsung, etc. As a result, it greatly facilitated the development of all IPs in the Kaluga region, boosted the local economy and improved the general investment climate.

Summary

Thus, while some elements of Padmore and Gibson’s (1998) regional industrial cluster model are evident in the development of Russia’s SEZs and IPs, it is clear that uncertainty avoidance and enhanced government activity are critical additional elements in this context. This is consistent with the adapted model proposed, presented in Figure 1. As discussed in the section ‘Research setting’, the historical, cultural and attitudinal peculiarities of Russia elevate an uncertainty factor, which in our fieldwork we found weakens the Enterprise dimensions in clustering: suppliers and related firms, and firm structures/strategy and rivalry. This in turn, prompts recourse to enhanced and particularized activity of regional government as a personal guarantor of risk, well beyond the neutral facilitator in the standard model.

The influence of regional government on cluster policy need not simply compensate for particular effects of uncertainty avoidance, as seen in Russia. We suggest that an enhanced role of regional government could be to anticipate the effects of uncertainty and design ameliorating mechanisms into policy and regulations. Uncertainty could be reduced by relationship- and trust-building procedures in early stages of tenancy, a requirement on management companies to provide legally enforceable guarantees of infrastructure investment, financial incentives at various investment thresholds and incentives for related and supporting cooperation. The positive externalities available from cooperation and competition in agglomerations could be promoted and exemplars popularized. In such ways, governments could actively address weaknesses in cluster design.

Conclusion

In this paper, we have analysed how the cultural and political environment influences the development of industrial clustering, using the Russian case to illustrate limitations of the standard industrial cluster model. Although the formal institutions of standard cluster models have been introduced in Russia, culture, attitudes and governmental particularities have hampered their implementation. We have argued that not only can an adapted cluster model accommodate such environmental influences but also indicate how enhanced roles of government can address these influences.

Industrial clusters in Russia suffer from cultural and attitudinal idiosyncrasies, which create a high level of uncertainty, resulting in reluctance to cooperate and an avoidance of competition, key drivers of the standard cluster model. We have found that aspects of Russian culture, attitudes and governmental peculiarities have inhibited the development of SEZs and IPs. The most important aspects are uncertainty avoidance and the extensive role of government in economic activity. In such circumstances, Russian entrepreneurs avoid competitive environments and knowledge sharing, choosing instead to rely on personal networks with state officials or other entrepreneurs in order to cope with unpredictable, burdensome bureaucracy and ambiguous legislation. The findings clearly demonstrate similar concerns raised by Williams and Vorley (2014) about transitional economies in general, that if there is an asymmetry between formal and informal institutions, business activity and entrepreneurship can be hampered, which can hinder economic development. A formal economic policy has changed, culture, norms and governmental peculiarities have not, but this is a situation that through carefully designed policies, governments can influence.

This research makes three major contributions. First, this has been the first systematic research undertaken on SEZs and IPs in Russia. The multiple methods data collection generating a unique high-quality dataset with a novel analysis is an advance over previous discussion. Secondly, the detailed case has allowed the examination of important limitations of the standard model of industrial cluster policy, highlighting the important influences of distinctive cultural and governmental characteristics on cluster dynamics and the potential for an enhanced role for government policies in mitigating these influences. This academic contribution underpins the third contribution, implications for policy.

The research suggests that in contexts where the dynamic interplay of cooperation and competition are weak, government should go beyond the establishment of a level playing field and proactively reduce uncertainty. In the Russian case, central and regional governments should provide timely financial guarantees for infrastructure development and broker personal relationships with core local and foreign investors, but also cultivate personal networks to allow members to resolve bureaucratic challenges, such as obtaining necessary approvals and permits, providing personal political guarantees of the feasibility of SEZs and IPs and generating interest in their developments.

This research provides a substantive study of SEZ and IP development in Russia. Nevertheless, several limitations and unanswered questions warrant further discussion. Firstly, the research design was cross-sectional and necessarily restricted to management companies and tenants who had successfully established themselves in zones and parks, excluding those who had not. A longitudinal design would allow the identification of a wider range of success factors and dynamics. Secondly, the zones and parks established to date are relatively sparsely populated. As these grow and accommodate a more fully operating tenants, there would be scope to use social network analysis to examine the social relations among individuals and organizations constituting these agglomerations and accompanying knowledge spillovers in more detail. Thirdly, despite our preservation of confidentiality and anonymity throughout out the primary data collection process, some of our interviewees (especially, from the state organizations) seemed wary that the information they disclosed could potentially expose them to embarrassment, jeopardize organizational partnerships or disrupt delicately balanced politicized policy practices. It was evident that some participants self-censored, trying to express their expression to find an ‘acceptable’ way to say it. As regional governors and administrations play a crucial role in the development of regional SEZs and IPs, a further course of action could involve investigation of the personal characteristics and skills that these state authorities must have. Given the extent of its influence, further research into and broader investigation of the blat phenomenon would be valuable in this context. Finally, the adapted model we have developed is ripe for application in other national, and potentially regional, contexts opening scope for a series of comparative case studies.

Supplemental Material

sj-pdf-1-cch-10.1177_1024529420949491 - Supplemental material for The effects of culture, attitudes and perceptions on industrial cluster policy: The case of Russia

Supplemental material, sj-pdf-1-cch-10.1177_1024529420949491 for The effects of culture, attitudes and perceptions on industrial cluster policy: The case of Russia by Sergey Sosnovskikh and Bruce Cronin in Competition & Change

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.