Abstract

This paper opens the black box of the role of the state when regulating the process of financialization of a national economy. For this purpose, we firstly study two recent Spanish executives’ closeness and similarity to financial, insurance and real estate sectors – usually identified as the ‘FIRE sector’. We secondly study how the process of specific law production and regulation during two different political terms has significant effects in the finance, insurance, and real estate complex. Our research explains that this specific regulation is related to the evolution of the FIRE sector in Spain, something that reflects the role of state agencies to favour financialization dynamics.

Introduction

In this article we adopt an interdisciplinary approach to explore the financialization of a national economy, shedding light on key aspects that are not often discussed when treating this subject. We open the ‘black box’, studying the lesser-known role of the national state to promote the development of financialization and, especially, its main operating scheme, the so-called ‘FIRE sector’, a compound of finance, insurance and real estate enterprises (Krippner, 2005). The FIRE sector’s weight in the US and European economies has more than doubled since 1980 (Jayadev et al., 2018).

Although the evolution of the FIRE sector is influenced by a great deal of social forces, we claim that the state regulation matters, as it legitimizes economic opportunities on a national scale. Our research focuses on how the state operates within financialization, using Spain as a case study due to the severe implications of the 2008–2013 crisis.

We firstly analyze key economic and regulatory agencies across two different political periods, 2004–2008 (under the Socialist Party’s rule), and 2011–2016 (Popular Party’s). When studying the similarities between the state regulators’ profiles and the FIRE sector, we analyze the reticular proximity of both types of institutions. Secondly, we proceed to investigate the specific legislation related to the FIRE sector during the latter periods, assessing whether this legislation is significantly related to economic variables measuring long-term FIRE sector growth or contraction.

This research is structured as follows: firstly, a theoretical framework outlining financialization’s characteristics, the state’s role and influential power elites within it; secondly, a methodological section presenting the main research questions; thirdly, a data and analysis section exploring, on the one hand, the structural parallels and the proximity between key economic directors of the state and the FIRE sector; and on the other hand, how government-approved legislation affects the FIRE sector’s expansion or contraction. We conclude by summarizing findings and discussing our paper contributions.

Financialization, power and the state: A theoretical framework

The concept of financialization summarizes shifts in financial-real sector dynamics, favouring financial actors (Stockhammer, 2010). It encompasses linked, yet distinct, phenomena: globalized financial markets, increased financial investment and income (Demir, 2007, 2009; Duménil and Levy, 2004; Krippner, 2005; Orhangazi, 2008; Stockhammer, 2004); shifting corporate governance (Akkemik and Özen, 2014; Bivens and Weller, 2004; Jung and Lee, 2022; Jürgens et al., 2000; Lazonick and O’Sullivan, 2000); mounting household debt (De Vita and Luo, 2021; Kim, 2013); more crises and capital mobility (Epstein, 2005; Ertürk et al., 2008; Seccareccia, 2012).

When studying the global phenomenon of financialization, we need to highlight the central place of national states. The state exercises legislative and regulatory powers that enable the financialization process at the national level (Jayadev et al., 2018; Krippner, 2011). Thus, to analyze the phenomenon of financialization in a comprehensive way, we should speak of a phenomenon of ‘state-sponsored financialization’, in which the role of state agencies is crucial (Christophers, 2017).

Krippner (2011) sees state sponsorship as a solution to the 1970s crisis, but not in a neutral way, yielding unequal outcomes (Freeman, 2010). Financialization blends redistributive politics with rent-seeking through finance (Fligstein and Shin 2007; Tomaskovic-Devey and Lin 2011).

Massó (2016) has analyzed the role of the state legislation and public programs in the financialization of Spanish sovereign debt markets. Massó (2016) illustrates the correlation between the financialization of the Spanish government debt market and debt sustainability from 1996 to 2013. This author highlights how the financialization of these markets was strategically crafted to enhance liquidity through innovative debt policies. However, it also enabled investors to assume speculative positions based on the market’s perception of default risk. The rapid increase in public indebtedness to fund the government’s deficit and the expenses related to financial system support led to a loss of credibility in Spanish debt sustainability and government solvency.

Tullumello et al. (2020), based on Aalbers (2019), identifies four areas for housing financialization – mortgage debt, mortgage securitization, rental housing, and housing companies – and propose a framework to organize specific legislation and programs across various dimensions of housing financialization in Southern Europe. They identify several modes of financialization, each associated with specific examples of public policies implemented by the state. For instance, mortgage debt exemplifies the linkage of homeownership access to finance, driven by fiscal incentives and ‘right to buy’ programs for public housing alienation. Mortgage securitization, the use of mortgage portfolios as securities/assets, has seen regulatory facilitation by both the state and the EU. Additionally, the state has played a dual role in the privatization and financialization of social rented housing. Market rental housing has also experienced financialization, accompanied by either the privatization or transformation of public housing companies into financialized entities. Lastly, the financialization of ‘not-for-profit housing’ has emerged, facilitated by fiscal and urban policy deregulation, encouraging activities like short-term rentals and the conversion of housing into tourist facilities.

The structural role of financial revolving doors

The study of state-led financialization can benefit from an interdisciplinary approach that considers the intricate interplay between individual actors and the institutions to which they are affiliated. From this perspective we highlight the structural role of the so-called ‘revolving doors’, that consist of a movement from business to politics and then back, which tend to foster business-aligned policies (Witko, 2016).

In pursuit of comprehending the intricacies of the revolving doors phenomenon and its potential impact on state decisions, we have analyzed the main theories about political and corporate power in advanced capitalist societies. As Mills’ (1956) and Domhoff (1990, 2022) network-oriented seminal studies about power in the US have stated, corporate elites have an enormous capacity to influence state decisions. Authors like Miliband (1969), who studied the bureaucratic and corporate elites in Western Europe after 1945, claimed that an important part of corporate influence relies on several technocrats who work for the state, but whose goals and values are like those of the business world, something that influences the state measures and resolutions.

The complexity of capitalism has made certain hybrid profiles more salient, as Galbraith highlighted with his notion of ‘technostructure’ (1967), a group of high-profile actors who either work for the public or for the private sector. The revolving door has proven to be a relevant economic incentive for private sector objectives (Blanes et al., 2012).

When analyzing the role of revolving doors in financialization, there are authors, in the first place, who pay more attention to the consequences in financial regulation. Wirsching (2018), from the perspective of the state, shows that central bank governors with experience in the financial sector deregulate significantly more than governors without a background in finance. Shive and Forster (2017) have analyzed this phenomenon from the financial industry point of view, concluding that financial enterprises are highly motivated to recruit US regulatory employees and to pay them good salaries for their role in reducing the risk level of their firms. In the third place, we also refer to research about financial executives and debt management (Silano, 2022), at a time when public debt has gained importance as one of the most worrying problems of advanced economies.

State-sponsored business development and financialization has been a central feature of the Spanish economic evolution from dictatorship to democracy. When analyzing financial reform during the 70s, 80s and 90s, Pérez (1997) underlines the importance of the alliance and network proximity between a group of reformers within the Bank of Spain and the leaders of the domestic banking sector. Liberal reforms were accommodated to the needs of a domestic community of interests, that would exchange personnel with the ones in charge of the state institutions (Pérez, 1997).

Revolving door technocrats can therefore be traced as a relevant empirical object of study to understand the deep and complex mechanism of interactions between private and public institutions.

Methodology: Research questions and the choice of Spain

Our approach aims to contribute to an empirical understanding the state’s role in advancing financialization. We posit that state agencies drive specific legislation enabling FIRE sector expansion, with a relative independence of political shifts in Western democracies. This process is mainly steered by technocrats, who tend to show similarities and to have ties to the FIRE sector.

This approach can be specified in the following research questions (RQ), that analyze the role of the state from two different and related points of view:

. Structural proximity between state agencies and the FIRE sector.

The specific legislation promoted by the state main economic and financial regulatory agencies relies on technocrats who are closely tied to the FIRE sector. A great deal of these public managers and directors were either recruited from Enterprises that belong to the FIRE sector or returned to this sector after leaving office. These revolving door technocrats often possess bureaucratic titles as part of a Spanish elite tradition that, over decades, has linked the bureaucratic elite to the corporate sector (Baena del Alcázar, 1999).

Governmental official and legislative support to the financialization process.

The specific legislation that is promoted by governmental regulatory agencies is related to the long-run evolution of the FIRE sector. The technical legislation which is driven by governments tends to favour the FIRE sector growth. Party politics and general economic conditions matter but they only play a secondary role in this relationship.

The choice of Spain: Why this country, and why these periods

Choosing Spain and two different governments, the 2004-2008 progressive one (Partido Socialista Obrero Español, PSOE), and the 2011–2016 liberal conservative one (Partido Popular, PP), offers insight into the impact of financialization within a specific social and political setting. These governments have been the main players of Spain’s bipartisan democratic system.

Spain became the epitome of the financialization of the real estate sector. Between 2002 and 2007, the national economy transitioned from a model characterized by high rates of homeownership and low debt levels to a prime example of the real estate sector’s financialization.

From 2002 until the 2008 housing bubble burst, heralding the Great Recession, Spain saw substantial non-financial private debt growth, majorly financed by the financial sector using housing as collateral (López and Rodríguez, 2011; Marchetti and Martínez, 2013; Medialdea García and Sanabria Martín, 2022). This surged the FIRE sector’s GDP share, climbing from 10% in early 2002 to over 14% by late 2008. Therefore, it is highly pertinent to know whether the legislative production of the government at the time, 2004–2008, was responsible for the growth of the FIRE sector.

As Spain’s Great Recession started, private sector solvency issues arose. By the end of 2008, household, corporate, and financial debt neared 306% of GDP, amid falling collateral values, which triggered a private sector economic slump. Financial institutions ceased credit and aimed to recapitalize through taxpayer funds (López and Rodríguez, 2011; Medialdea García and Sanabria Martín, 2022). Commencing from 2011, Brussels-controlled European Union governance prioritized Spanish banking sector rescue and restructuring, imposing costs on taxpayers. This requires analyzing the impact of 2011–2016 financial sector legislation on the FIRE sector’s Spanish economy weight.

Empirical results

In relation to our research questions, we propose two different analyses. Firstly, and corresponding to the first research question – that is, RQ1, Structural proximity between state agencies and the FIRE sector – we study the careers of the high-ranking officials that oversaw the most relevant regulatory agencies. Secondly, and referring to the second research question – that is, RQ2, Governmental official and legislative support to the financialization process – we analyze the legislation driven by each government and its relationship with the evolution of the FIRE sector.

Do the legislators belong to the legislated inner circles? The Revolving Technocrat Indicator

In this first stage, we address the research question RQ1 of the proximity between the state and the FIRE sector. We analyze the similarities between the regulators’ careers and the FIRE sector main branches and firms. We examine prominent officials within the Ministry of Economy and specific autonomous entities in the governments formed by PSOE in 2004 and PP in 2011. 1

These government figures are analyzed in separate databases for each administration (PSOE, 2004–2008, and PP, 2011–2016). The databases include names, bureaucratic titles (which can be influential, particularly in economic domains and Spanish political elites), roles in businesses prior to government service, and positions held in enterprises after leaving public office. 2

We develop an indicator, the Revolving Technocrat Indicator (RTI), to gauge the proximity of these key economic officials to the main FIRE sector branches. The RTI measures the concentration of revolving door regulators in each executive.

We propose two indicators to assess the degree of influence of the FIRE sector on the government: firstly, the RTI total indicator, which quantifies the number of private sector positions that each government accumulate; and secondly, the RTI average value, which considers the diversity of professional trajectories, thus allowing for a more nuanced comparison between the two executives.

Drawing from Brezis and Cariolle’s pioneering work on revolving door indicators (2014), we jointly consider three criteria to understand this phenomenon.

Firstly (a), we evaluate the former positions and backgrounds of government regulators. Four categories are established: ‘0’ for those transitioning from the public sector into government (scored as 0); ‘I’ for private CEOs (scored 5); ‘II’ for Board of Directors members (scored 3); and ‘III’ for other firm positions (scored 1).

Secondly (b), we classify the government officials based on the power of their executive positions. ‘GP’ – referring to ‘great power’ – means high-ranking officials such as ministers, state secretaries and presidents of regulatory bodies, 3 assigned a score of 5. ‘LP’ – ‘low power’ – denotes officials with comparatively lower power, like deputy secretaries and general directors (score 1).

Thirdly (c), combining these two former classifications, we observe three revolving door trajectories, therefore, three different channels of corporate influence. ‘Type 1’, public to private trajectories, which involves former members of the economic team who after leaving office moved to FIRE companies (their score is 3). ‘Type 2’, private to public, consists of former FIRE company executives recruited for significant economic director roles in the governments (scored 5). ‘Type 3’, private to public and public to private, which describes executives participating in both ‘Type 1’ and ‘Type 2’ movements (also scored 5). ‘Type 4’ means public to public movements, reflecting no revolving door shift at all (scored 0).

Among these combinations, the strongest revolving door trajectory entails a regulator who was a former CEO in a private firm, holds a ‘GP’ position within the public sector, and experiences a ‘Type 2’ or ‘Type 3’ revolving door flow, that is, either returning or not returning to the FIRE sector after leaving office. In such a scenario, the score is as follows: 5 x 5 x 5 = 125. Conversely, the least influential career involves a transition entirely within the public sector (‘Type 4’), earning a score of 0. This latter type of career relates to a great part of Spanish bureaucrats.

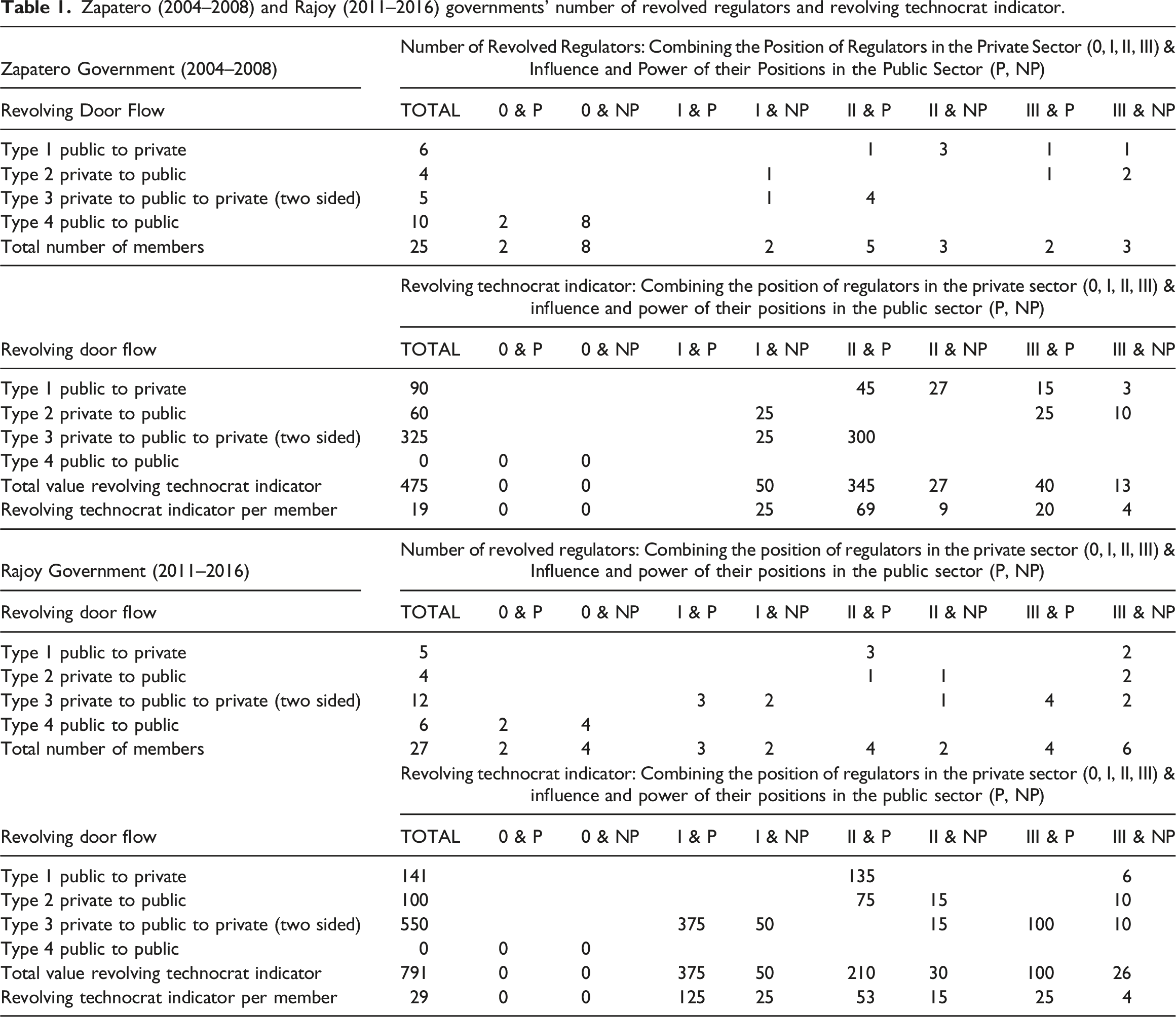

Zapatero (2004–2008) and Rajoy (2011–2016) governments’ number of revolved regulators and revolving technocrat indicator.

The average RTI value in the PP government (2011–2016) is notably higher at 29.3, while the PSOE government (2004–2008) records a RTI of 19. The conservative administration of 2011 features a prevalent trajectory of FIRE sector regulators emerging from the private sector, primarily ‘Type 2’ and ‘Type 3’. These regulators are either former CEOs who, during the political term for which they were recruited, hold less conspicuous regulatory roles or individuals who, having held less decisive private sector positions, were recruited for a relevant regulatory responsibility.

Among these revolving door actors, significant bureaucratic affiliations exist, particularly state lawyers, who often specialize in fiscal and financial regulation -and who have the highest frequency of movements towards the private sector. This bureaucratic group held prominence in the 2011 conservative government. State economists also played a notable role in 2011 and 2004 executives, reflecting an influence that was transversal to politics.

Some specific examples of revolving door technocrats shed light on the latter. The Minister of Economy during the 2011–2016 PP period exemplifies ‘type 2’, transitioning from the private sector to the public one. Although not an official militant of the Popular Party, he had served under conservative governments from 1996 to 2004. Holding the civil servant title as state economist, he worked for various FIRE sector companies, including international investment banks such as Lehman Brothers and Nomura, as well as a Spanish savings and loans firm. After leaving office, he assumed the role of vice president of the European Central Bank. Concurrently, the vice minister of Economy (Secretary of State) exemplifies ‘type 3’ (private to public to private). Being a state economist, he had worked for Lehman Brothers and Barclays Bank before having been recruited by the conservative government. After leaving office, he returned to the private sector as the Spanish representative of Rothschild’s Bank.

In the PSOE government, the average RTI is lower due to higher number of ‘type 1’ careers. However, the average RTI for this executive reveals a distinct state-FIRE sector relationship. The most frequent career is that of a public regulator who, after leaving office, moves to the private sector as a CEO. Another common average trajectory involves a regulator who comes from the public sector, holds a significant regulatory role, and later enters the private one in a non-key capacity. An additional average RTI scenario includes a regulator who comes from a private firm’s board but does not acquire a leadership role when recruited for the government. In short, although the average RTI indicator is lower in the PSOE government, a deeper analysis of its composition suggests that the revolving doors effect is also relevant.

In relation to the PSOE government, the minister of Economy during 2004–2008 typified a ‘type 1’ case, moving from public to private. A state economist, he was not a Socialist Party militant, but had held a PSOE parliamentary seat in 1996 and had been the European Union vice president and financial commissioner (1999–2003). After leaving office, he joined the boards of Barclays Bank and Caixa Bank. The vice minister of Economy embodies a ‘type 3’ example (private to public to private). He arrived from a notable Spanish financial broker and a bank, returning to the latter after the end of his term in office.

In both governments, there is a notable weight of revolving door technocrats. This weight is greater in the case of the PP one, but it is also relevant in the PSOE. However, and as it was mentioned above, it should be stressed that, on the one hand, the PP government has more actors from the private sector who end up in less influential government positions, therefore exerting a lower degree of public influence. On the other hand, the PSOE has fewer revolving door actors, but includes a high number of managers who, after exercising relevant public responsibilities, end up in FIRE sector boards.

In the PP government, there are more revolving doors, but they are relatively less important; in the PSOE, there are fewer, but they seem to be more decisive. This marks an ideological difference between the two major parties of Spanish democracy: the senior officials of the PP, conservatives, reflect a stronger influence from the FIRE sector; however, the exercise of public power brings those of the PSOE notably closer to those of the PP, reducing the ideological gap. Public and private leaders with bureaucratic titles predominate in both cases, especially state lawyers in the conservative one, and state economists and tax inspectors in the two governments.

The following section studies whether the data analyzed here materialize in a legislative activity that affects in a different manner the relative size of the FIRE sector, and with it, the degree of financialization of the Spanish economy.

Do Spanish Governments Legislate in favour of the FIRE Sector? An econometric analysis

This section analyses, according to RQ2 – Governmental official and legislative support to the financialization process – whether both governments bolstered the FIRE sector through specific legislation.

A brief overview of Spain’s legislative process is therefore pertinent. Spanish laws, fundamental state sources, are divided into Organic Laws requiring Parliament’s absolute majority and Ordinary Laws not needing such majority. A specialized parliamentary commission, including Deputies and Senators from major parties, can debate and approve these laws.

In contrast to laws passed by democratic chambers, certain regulations hold law status, such as Royal Decree Laws and Royal Decrees, which are common under specific circumstances. Unlike laws, Royal Decree Laws and Royal Decrees are issued by the government due to extreme and urgent necessity (art. 82-86 CE, Generales (1978)).

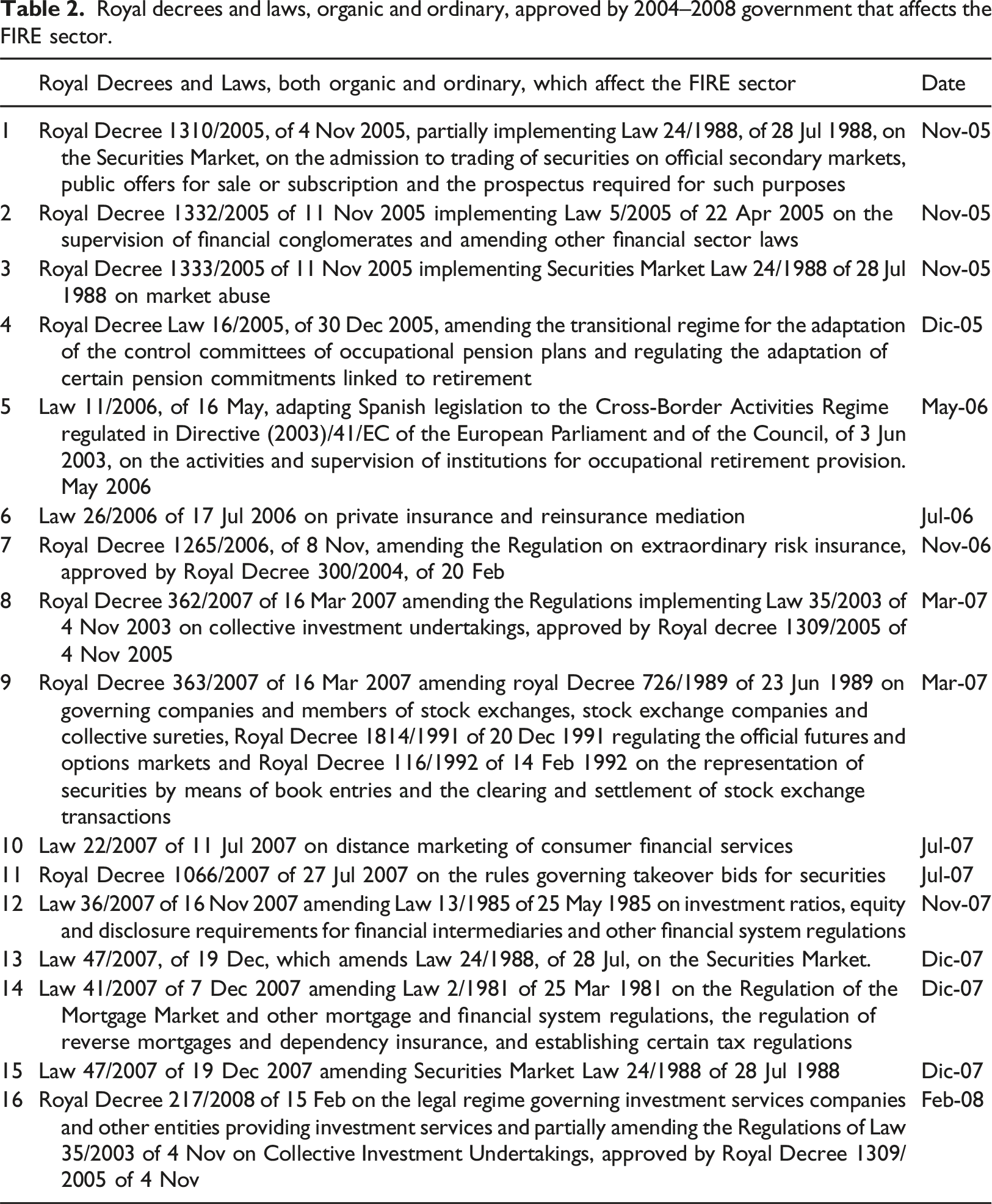

These latter norms are often employed when a majority government aims to expedite approval, bypassing discussion in a Congress of Deputies’ delegated commission (art. 75.2 CE, Generales (1978)). This pattern is evident in our data: 56.25% of FIRE sector-related legislation was processed as Royal Decrees during the Socialist Party’s (Partido Socialista Obrero Español, PSOE) rule (2004-2008), rising to 100% in the Popular Party’s (Partido Popular) 2011-2016 term. Notably, the conservative 2011-2016 government held an absolute majority in both Congress and Senate. Meanwhile, the progressive 2004-2008 government had a simple majority in both chambers.

Sanz and Sanz’s (2020) research aligns with these findings on Spanish democracy’s Royal Decree usage. They studied 574 Royal Decrees passed in Spain from 1978 to 2018, establishing a link between Royal Decree quantity and the political, economic, and social context. A negative correlation emerged between Royal Decree count and annual national GDP growth rate, particularly regarding economic and financial matters. Its use upsurges during economic crises, amplifying legislative impact (Sanz and Sanz, 2020). Additionally, this legislative approach is more prevalent when a government commands an absolute parliamentary majority.

Royal decrees and laws, organic and ordinary, approved by 2004–2008 government that affects the FIRE sector.

Royal decrees and laws, organic and ordinary, approved by the 2011–2016 government that affects the FIRE sector.

Despite Spain’s EU membership since 1986 and the inherent intertwining of its FIRE sector legislative framework with the EU’s, notable discretion remains in financial legislation development and implementation, following a tradition of arrangements between the Spanish Central Bank reformers and the domestic banking sector (Pérez, 1997). European norms in our database mainly involve transposed directives, adapting community regulations to national law (Mangas and Liñán, 2020).

Dependent, independent and control variables

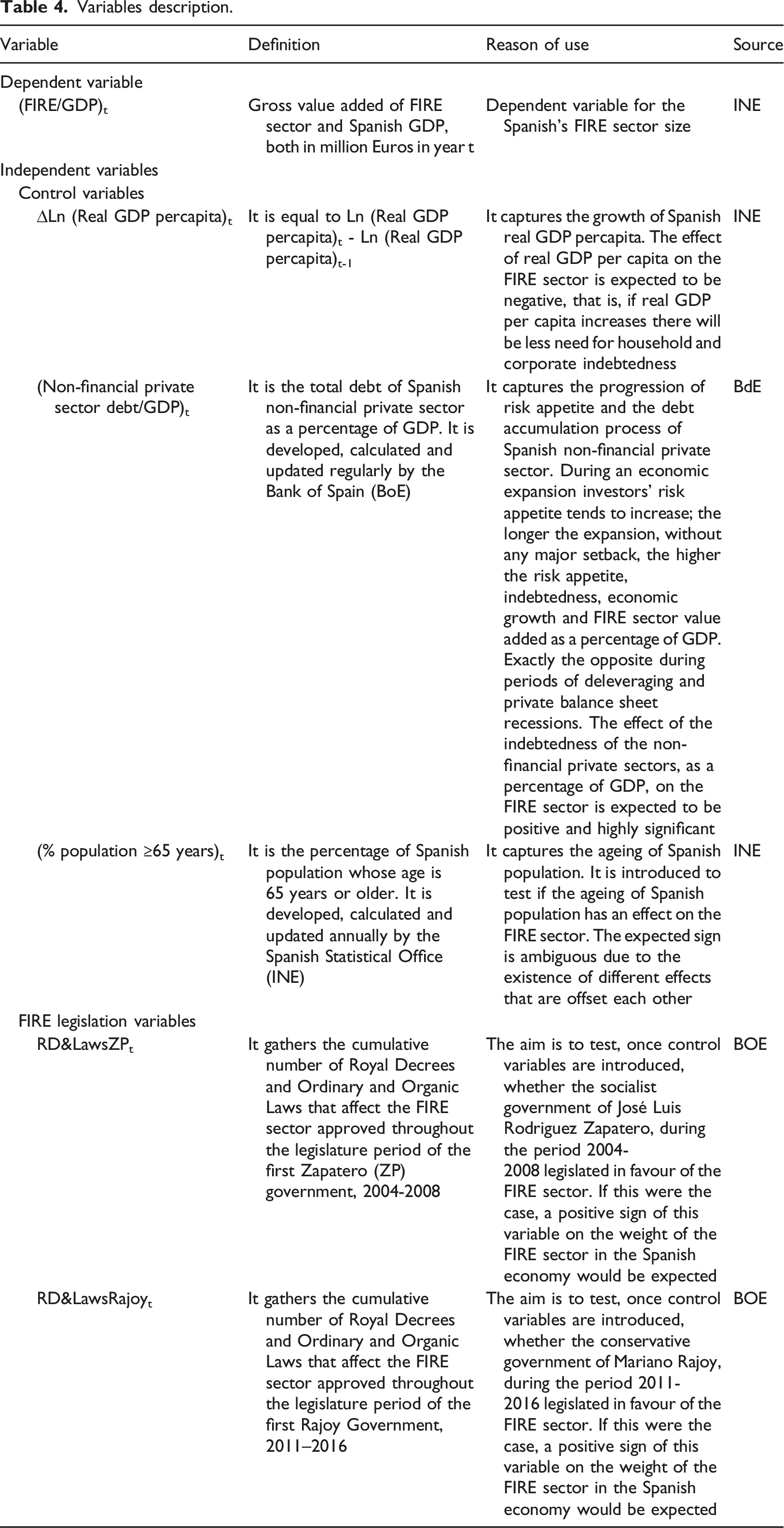

To answer the second research question -and thus to prove whether national legislation helps or hinders the expansion of the FIRE sector-we will use a regression model in which the dependent variable is the gross value added of the FIRE sector as a percentage of Spanish GDP, with a quarterly frequency, since the first quarter of 1996 to the first quarter of 2022. We create two variables that count approved royal decrees and laws, both organic and ordinary, quarterly and cumulatively for each government. They are ‘0’ until the governments issue the first legislation related to the FIRE sector. Recent cumulative data are used until the database’s last quarter from Q1 1996 to Q1 2022.

Control variables, known to affect FIRE sector growth over GDP, are necessary. The goal is to show that the formulation of FIRE sector-specific legislation significantly boosts the expansion of the FIRE sector in two different time periods, under governments of different political parties, independently of business and credit cycles. The choice of control variables, therefore, in addition to summarizing legislation, allows for control of the economic, credit, and demographic cycles to avoid spurious correlations. The variables chosen are widely used in the literature to control for business, financial and demographic cycles.

The first of these control variables is the real GDP per capita. Rising real GDP per capita tends to decrease household and corporate indebtedness. The second one is the private debt volume of non-financial sectors expressed as a percentage of GDP, which is crucial in explaining the FIRE sector’s weight. This variable predictive power during the Great Recession, aligned with Minsky’s financial instability hypothesis (Minsky, 1992), is evident. Private debt to GDP ratio’s persistence across OECD countries and macroprudential policy’s significance are empirically confirmed (Caporale et al., 2021). Non-financial private sector indebtedness as a percentage of GDP positively affects the FIRE sector.

Lastly, the demographic variable of population aged 65+. Population ageing influences the FIRE sector have unclear effects (Imam, 2013). Older households reducing their debt have a negative impact on the credit channel. It deflates collateral value, weakening monetary transmission. However, longevity risk exposure and its pension-related implications can impact sovereign debt, equities, and financial institutions positively or negatively. Empirical analysis will clarify ageing’s effect on the FIRE sector’s share. 5

Variables description.

The equation (1) on the determinants of the weight of the FIRE sector in the economy is formulated as follows:

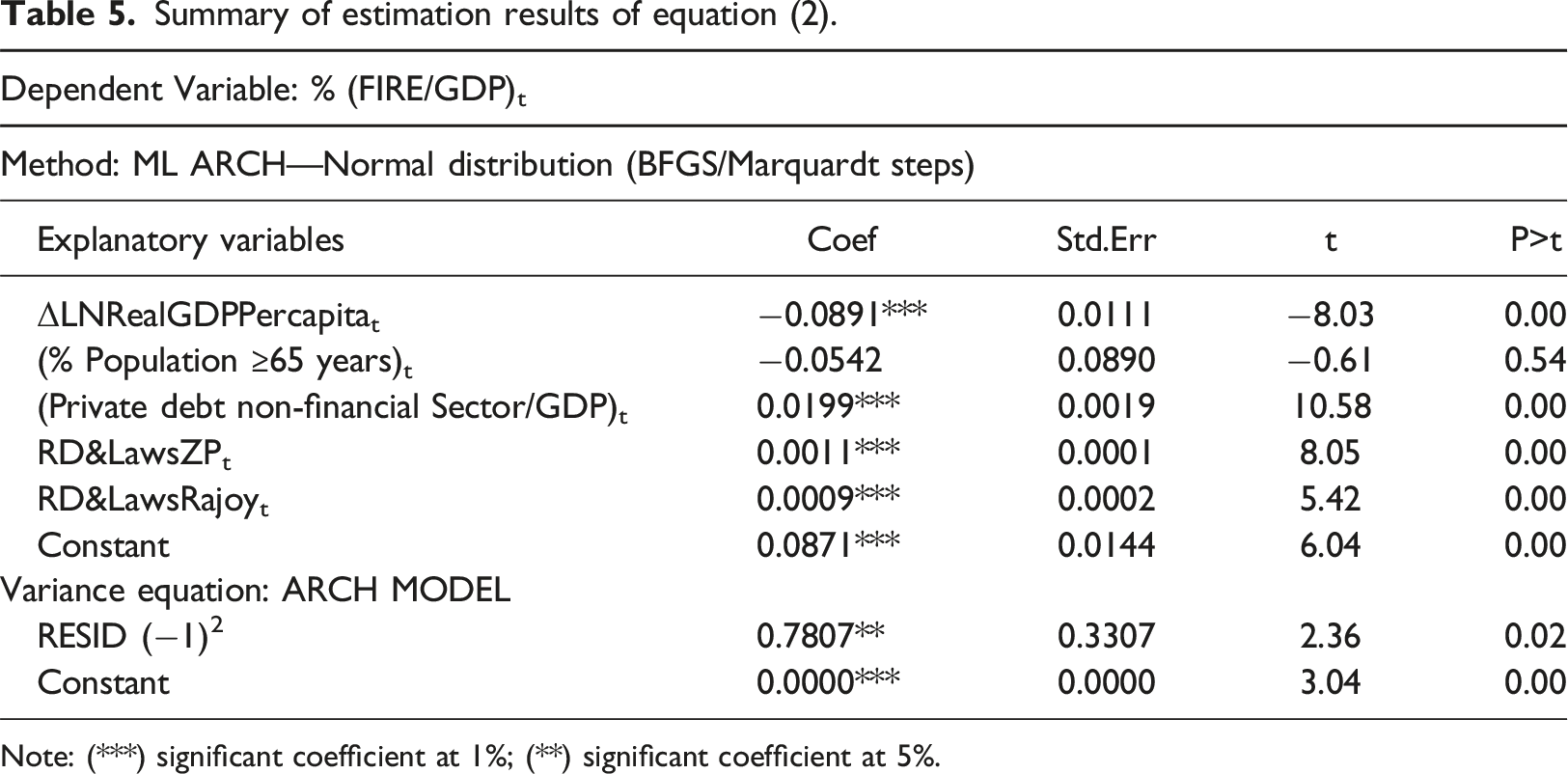

Equation (1) was initially planned for OLS regression. However, despite insignificant correlations among explanatory variables, residual assessments reveal non-normality (Bera-Jarque test), autocorrelation (Durbin-Watson test, Durbin alternative test, and Breusch-Pagan test with different lags), and heteroskedasticity with ARCH. effects (White test, LM test for ARCH. effects). The estimation method, guided by autocorrelation and heteroskedasticity correction tests, opts for a generalized autoregressive conditional heteroskedasticity model, ARCH. (1), for residual variance – selected through Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC). Hence, the approach employed is maximum likelihood. Equation (1), investigating determinants of the FIRE sector’s weight in the economy, is reformulated as follows in equation (2):

Summary of estimation results of equation (2).

Note: (***) significant coefficient at 1%; (**) significant coefficient at 5%.

Private debt as a percentage of GDP has a positive and noteworthy influence on the FIRE sector. During economic upswings, risk appetite among investors typically rises, fuelling debt growth and FIRE sector’s share of GDP. This trend reverses during deleveraging and private balance sheet recessions. Real GDP per capita negatively affects the FIRE sector. However, the final control variable, the population percentage aged over 65, lacks significance.

With these economic and financial cycle-related factors controlled for, focus shifts to the variables addressing FIRE sector-related legislation during both political terms. The coefficients of these variables are positive and significant, meaning that such legislation heightens the FIRE sector’s portion in the economy as a whole, regardless of the business and credit cycle timing of its enactment. Hence, the formulation of FIRE sector legislation significantly boosts its expansion in both periods.

We reinforce our findings’ robustness by applying equation (2) not only to the entire FIRE sector but also to its subcomponent, Real Estate (RE), given Spain’s unprecedented housing boom. Coefficient signs and statistical significance for explanatory variables in RE remain unaltered, underscoring the model’s explanatory skill.

Complementing this analysis, a Granger causality test is conducted. Note that causality does not imply direct causation but rather a temporal sequence. Granger causality is a tool to assess whether one time series helps to predict another. It is a statistical concept that deals with temporal relationships and predictive power, but it does not provide insights into the underlying mechanisms or the presence of a direct causal link. Researchers and analysts should interpret Granger causality results cautiously and consider additional evidence and context when drawing conclusions about causation.

Granger causality tests are executed in an unrestricted VAR for a multivariate analysis, where the variables (Fire/GDP) t , (Non-Financial Private Debt/GDP) t , R&DLawsZP t and R&DLawsRajoy t are treated as endogenous variables. Conversely, ΔLn(RealGDP percapita) t , and (%Population ≥ 65years) t are introduced as exogenous variables. Consequently, we have estimated a four-equation VAR(1) model. To determine the lag order of this multivariate VAR model, in this case 1, we use different information criteria and other methods. 7

VAR granger causality wald test.

Note: (***) significant at 1%; (**) significant coefficient at 5%; (*) significant at 1.

Causality is evident between Non-Financial Private Debt/GDP and Royal Decrees and Laws during the PSOE government (2004–2008). However, in contrast, no substantial causal link emerges between Non-Financial Private Debt/GDP and the Royal Decrees and Laws introduced during the conservative government of 2011–2016. This is due to the Spanish economy being in a phase of deleveraging in the private sector with the consequent negative effect on the health of the financial system. Legislation in this period focused on the clean-up and sale of real estate assets to bail out banks at the expense of taxpayers.

Henceforth, the underlying causal mechanism that connects legislative actions with the augmentation of worth within the FIRE sector can be outlined like this: the implementation of precise regulations governing select facets of the FIRE domain exerts an impact on the magnitude of Private Non-Financial Debt in relation to Gross Domestic Product (GDP). This, in turn, exerts an influence on the value added within the confines of the FIRE sector.

To reinforce the conclusions from a qualitative point of view, we will subsequently detail examples of how a specific legislative change creates more demand for services in the FIRE sector. The analysis of some cases of legislation to explain the mechanism of causality are framed within the literature of ‘process tracing methods’ (Beach and Pedersen, 2013; Rohlfing, 2012), that is, a set of qualitative research methods that aim to discover and understand the causal mechanisms and processes that link an independent variable or treatment to a certain outcome.

Let us examine some instances of legislation, relating to both the period of the PSOE government and that of the PP executive, where in two distinct economic scenarios, the FIRE sector was favoured. During the last real estate boom (1996-2007), there was a substantial influx of foreign capital into the Spanish real estate system. This process, driven not only by the implemented monetary and credit policies but also by the Law of Securitization Vehicles of 1992, prompted commercial banks to securitize their mortgage portfolios, transforming the Spanish mortgage market into one of the most securitized in the whole Europe (Aalbers, 2009; Aramburu, 2015). Subsequent legislation, under the PSOE government of 2004 to 2008, further amplified these dynamics. A key illustration of this argument is the Royal Decree 1310/2005, of 4 November 2005, on the Securities Market, which explicitly addresses the admission to trading of securities on official secondary markets, including mortgage-backed securities. In summary, this legislation contributed to creating a situation where readily available credit upsurged aggregate demand, housing prices, and excessive indebtedness.

In the second example, under the PP government, legislation also favoured the banks. The mortgage crisis affected the entire Spanish banking sector, leading to the establishment of the SAREB (Company for the Management of Assets Arising from Banking Restructuring) to cleanse bank balances. During the Rajoy government, legislation was developed to regulate this process: Royal Decree Law 2/2012 of 3 February on the restructuring of the financial sector, and Royal Decree Law 18/2012 of 11 May, on the reorganization and sale of real estate assets in the financial sector, among others. The state intervened to rescue banking institutions, at the expense of taxpayers and without imposing a haircut on creditors, issuing more debt at a time when significant budget deficits stemming from unemployment and the economic crisis needed large-scale public debt issuance. Massó (2016) argues that the institutional mechanisms allowing the transformation of the banking crisis into a sovereign debt crisis are rooted in the microstructure of government debt markets and their degree of financialization. For this author, legislation played a key role in the financialization of Spanish sovereign debt markets.

We can also cite other cases where legislation favoured the financialization, boosting the FIRE sector. An example is Law 41/2007 of 7 December 2007, which, through financial instruments, can turn householders’ rights into liquid assets further fuelling the real estate bubble. The same analysis can be applied to insurance or pension fund legislation, where, to promote and improve the liquidity and risk analysis of these instruments, ultimately, it facilitated a financialization of health and pensions.

Discussion and conclusions

We propose a methodology to study the role of the state in the process of financialization. We obtained enough information to answer the two questions that guided our research.

The RQ1, ‘Structural proximity between state agencies and the FIRE sector’, analyses the similarities between the directors of the main regulatory agencies, on the one hand, and the FIRE sector main branches and firms, on the other. The Revolving Technocrat Indicator (RTI) shows that the PP government (2011–2016) has stronger links to the FIRE sector. The PSOE (2004–2008) relies on fewer FIRE managers, employing them for higher-level roles. Politics, and the ideological tendency of the parties that form the government, matter in the trajectories of government high-ranking officials.

The RQ2, ‘Governmental official and legislative support to the financialization process’, questions whether legislation helps or prevents the growth of the FIRE sector. The results of the regression model led us to conclude that the creation of technical and specific legislation, mainly based on the simpler and quicker Royal Decree formula, favoured the expansion and growth of the FIRE sector. This legislation had an impact on the size of the Spanish FIRE sector in relation to the GDP in both periods: 2004-2008, PSOE government; 2011–2016, PP government.

We enhance this analysis using a Granger causality test. The causal connection linking legislative actions with increased value in the FIRE sector can be outlined as follows: enacting specific regulations for aspects of the FIRE sector affects Private Non-Financial Debt relative to Gross Domestic Product (GDP). Consequently, this affects the value added within the FIRE sector. Finally, we detail some instances of legislation, belonging to both the PSOE government period and the PP government one; underlining that, in these two distinct economic scenarios, the FIRE sector was favoured.

In summary, our results show that political shifts, which have a certain influence, do not change a relatively homogeneous tendency to legislate favouring the FIRE sector. This way, state-sponsored financialization overcomes political changes.

We expect our findings will allow for a more nuanced understanding of the multifaceted role of the state, as well as revolving doors, in enabling, promoting, and shaping the financialization of the economy.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.