Abstract

This paper focuses on a neglected yet crucial feature of public investment policies in the European Union (EU): the politics of statistical harmonization and off-balance-sheet policymaking. Drawing upon the instrument-centred approach and the sociology of quantification and accounting, it refines the concept of ‘fiscal ecosystem’ by highlighting the controversial and evolving nature of the boundary between on- and off-balance-sheet recording. It is argued that the accounting aggregates giving effect to EU fiscal rules favour marketized and privatized modes of public service delivery, including ‘market-based but state-led’ off-balance-sheet investment tools such as public–private partnerships. However, the effectiveness of this policy has decisively hinged upon the work of harmonizing public finance statistics carried out by Eurostat, the Statistical Office of the EU. This contested process has led to acute power struggles between statistical agencies and governments, and a substantial increase of Eurostat’s power in the wake of the Eurozone crisis. The comparison of the two main Belgian regions highlights contrasting responses to this European strategy of governing (sub)national investment policies through fiscal rules and statistical harmonization: while Flanders has consolidated the financialization of its investment policy, Wallonia has so far opposed this trend. This demonstrates that although financialization of public investment is promoted by EU fiscal integration, it is not inevitable; governments do have some leeway to follow an alternative path. As Wallonia also benefited from extraordinary economic and political circumstances, it remains to be seen whether its distinctive investment policy will withstand rising interest rates and tighter fiscal rules.

Keywords

Introduction

This paper focuses on a neglected yet crucial feature of public investment policies in the European Union (EU): the politics of statistical harmonization and off-balance-sheet policymaking. Drawing on the sociology of public policy instruments (Lascoumes and Le Galès, 2007) and the sociology of quantification and accounting (Chapman et al., 2009; Mennicken and Espeland, 2019), it refines the concept of ‘fiscal ecosystem’ (Guter-Sandu and Murau, 2022) by highlighting the controversial and evolving nature of the boundary between on- and off-balance-sheet recording and its productive effects on domestic public investment policies. It also stresses the inherently multi-level nature of the European Investor State (EIS), by considering the complex interactions between the European, national and regional levels. 1

I argue that the accounting aggregates giving effect to EU fiscal rules have favoured privatization and marketization of public service delivery, including ‘market-based but state-led’ (Mertens and Thiemann, 2018) off-balance-sheet investment tools, such as public–private partnerships (PPPs) and financialized state-owned utilities. As a result, public investment policies in Europe are more and more subject to financialization, understood as ‘the increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies’ (Epstein, 2005: 3). 2

Yet the effectiveness of this way of governing public investment ‘through financial markets’ (Braun et al., 2018) has crucially hinged upon the work of harmonizing and monitoring national public finance statistics carried out by Eurostat, the Statistical Office of the EU. 3 Far from being self-evident, this process has been characterized by acute power struggles between Eurostat, national statistical institutes (NSIs) and governments. Through such struggles, Eurostat shapes public investment policies in Europe while also carving out its power – thereby delineating the room to manoeuvre left to member states to invest in a fiscally constrained context.

The empirical part of the paper analyzes the controversies between Eurostat and the two main regions of arguably the most decentralized EU country (Belgium) over the on- or off-balance-sheet recording of selected investment techniques, and their effects on investment policies. Between the mid-2000s and 2014, Flanders and Wallonia fought a protracted struggle with Eurostat over the recording of contested investment devices. Faced with Eurostat’s strengthened powers, both regions responded very differently to the European strategy of governing (sub)national investment policies through fiscal rules and statistical harmonization: while Flanders has consolidated the financialization of its investment strategy, Wallonia has so far actively opposed this trend. This example demonstrates that the financializing of public investment policies promoted by EU budgetary integration is not inevitable, and that governments do retain levers to follow an alternative course, depending on market conditions and political dynamics.

The data are drawn from primary and secondary sources. First, in-depth documentary analysis of EU accounting rules and Eurostat publications: press releases, ad hoc decisions, manuals and reports over visits to member states. Additionally, I conducted twenty-seven semi-structured interviews between 2014 and 2016 with key informants at European level (Eurostat, European Investment Bank [EIB], cabinet of the European Commissioner in charge of Eurostat, etc.) and in Belgium (federal and regional administrations and ministerial cabinets, National Accounts Institute [NAI], National Bank of Belgium [NBB], etc.) to gather perceptions about Eurostat’s role, its evolution over time and its influence on regional investment policies. To confirm and update my findings, I conducted six additional interviews in 2022 with senior Belgian officials directly involved in federal and regional recovery plans.

The paper proceeds as follows. First, it combines the instrument-centred approach and the sociology of accounting and quantification to refine the concept of ‘fiscal ecosystem’ (Guter-Sandu and Murau, 2022), by stressing the dynamic nature and productive effects of the boundary between on- and off-balance-sheet recording (1). It then shows how the focus of EU fiscal rules on a specific accounting aggregate – the ‘general government sector’ – has favoured ‘market-based but state-led’ (Mertens and Thiemann, 2018) off-balance-sheet investment tools and the importance of Eurostat’s harmonizing and monitoring of national public finance statistics in this strategy (2). The empirical analysis stresses the relevance of the Belgian case (3), before subsequently describing the controversial off-balance-sheet investment techniques designed by Wallonia and Flanders in the 2000s (4). In 2014, Eurostat used its increased powers to reclassify them as on-balance-sheet (5). Since then, both regions have followed distinct trajectories: Flanders has further financialized its investment policy, whereas Wallonia has returned to traditional budgetary financing (6). The conclusion not only highlights the role of Eurostat and statistical harmonization in shaping a ‘market-based but state-led’ public investment regime in Europe but also the leeway kept by government to conduct alternative investment policies, depending on economic and political circumstances.

The politics of EU fiscal ecosystems: A policy instrumentation approach to off-balance-sheet policymaking

Two main theses compete in the literature on European fiscal governance. On the one hand, numerous studies have stressed the neo- (or ordo-) liberal nature of the Economic and Monetary Union (EMU) (Gill, 1998; Lovering, 2023; Ojala, 2021; Ryner, 2015). European treaties commit national governments to fiscal orthodoxy and market discipline by prohibiting monetary financing 4 and ‘excessive’ public deficits (as operationalized in the Stability and Growth Pact – SGP) and by including a strict no-bailout clause. 5 This ‘logic of discipline’ (Roberts, 2010) reflects a concern to protect private creditors, thereby relegating citizens’ demands to the second place. Deprived of monetary policy and fiscal space, ‘European consolidation states’ (Streeck, 2014) are constrained to internal devaluation policies aimed at reducing labour costs or increasing productivity. Far from putting an end to neoliberalism (Crouch, 2011), responses to the European debt crisis further strengthened the austeritarian stance of the European macroeconomic framework (Biebricher, 2017; Blyth, 2013; Morales et al., 2014; Selmic, 2016).

Other strands in the literature have been more cautious about the effects of EMU. Firstly, institutionalists have nuanced the strictness of fiscal discipline. After its first suspension in 2003, Heipertz and Verdun (2004: 776) portrayed the SGP as ‘a dog that would never bite’. Others highlighted the predominance of soft law in the EMU (Hodson, 2017). Indeed, fines have never been imposed for fiscal non-compliance, even under the strengthened fiscal framework (Sacher, 2021). 6 For the past decade, the Commission has promoted a ‘flexible’ approach to the SGP and chosen to negotiate with, rather than sanction, non-compliant states (Mérand, 2021). Economists have moreover shown how ‘creative accounting’ and ‘fiscal gimmickry’ downsized the austerity effects of the EMU – a phenomenon long stressed by international financial institutions (Brixi and Schick, 2002; Milesi-Ferretti, 2000). According to this literature, EU fiscal rules increased incentives for taking advantage of the leeway left by accounting conventions, through tools such as PPPs, capital injections and derivatives (Alt et al., 2014).

Attempting at reconciling both approaches to EU fiscal governance, Guter-Sandu and Murau (2022) coined the concept of ‘fiscal ecosystem’. The latter refers to ‘the somewhat opaque medley of treasuries and [off-balance-sheet fiscal agencies – OBFAs] on a European and a national level that has developed a specific division of labour given numerous constraints, many of them self-inflicted by the neoliberal fiscal governance logic’ (Guter-Sandu and Murau, 2022: 63). Contrary to the abovementioned literature, this concept envisions fiscal off-balance-sheet policy making not as a mere coincidental or opportunistic practice but as a ‘governance mode in its own right’ (ibid.: 75), aimed at mitigating the effects of neoliberal fiscal rules. Although it took shape during the first decade of the EMU, the Eurozone’s fiscal ecosystem has come to the fore since the global financial crisis and subsequent Eurocrisis. In an environment characterized by austerity, OBFAs have taken over tasks previously carried out by treasuries – such as public investment – to expand fiscal space by replacing actual (on-balance-sheet) liabilities by contingent (off-balance-sheet) ones. 7 Therefore, any examination of investment policies in the EU should focus on both on- and off-balance-sheet investment tools.

Yet, the concept of ‘fiscal ecosystem’ currently presents two main shortcomings. A first one is its latent functionalism. Symptomatically, Guter-Sandu and Murau (2022) repeatedly claim that OBFAs ‘mitigate’ the neoliberal features of EU fiscal governance. Yet, investing through on- or off-balance-sheet techniques is not neutral. Public investment tools can be conceived as genuine ‘policy instruments’, as defined by the political sociology approach to instruments (Lascoumes and Le Galès, 2007). The latter approach was developed in opposition to functionalism, which assumes that instruments are natural and pragmatic (i.e. selected for effectiveness, in a problem-solving perspective). The instrument-centred approach states that policy tools ‘structure public policy according to their own logic’ (ibid.: 10), by producing effects (such as ‘optimizing’ fiscal rules and depoliticizing investment policy) and favouring specific actors and interests over others. Accordingly, it focuses on the actors, resources, power relations and consequences at play in the selection, construction and use of public policy tools – envisioned as conflicting processes. Over the last decade, this approach has been successfully extended to EU policy-making (Kassim and Le Galès, 2010).

In this respect, Quinn (2017) aptly put forward the constitutive properties of fiscal constraints, which not only restrict state power but also generate new government strategies. This has also been shown by Lagna (2015) with regard to the use of financial derivatives by Italian municipalities. Previous research has hinted at off-balance-sheet policymaking as a way to govern public investment through financial markets, that is, ‘to engineer and re-purpose financial instruments and markets as instruments of statecraft, with the goal of achieving economic policy goals at minimum fiscal costs’ (Braun et al., 2018: 104). Development banks play a crucial role in this ‘market-based but state-led’ way of conducting investment policies in Europe (Mertens et al., 2021; Mertens and Thiemann, 2018), along with other popular off-balance-sheet investment devices such as PPPs (Liebe and Howarth, 2020; Whiteside, 2020), public guarantees (Heald and Hodges, 2018) and financialized state-owned utilities (Deruytter et al., 2022). This mode of government might nevertheless transform the state into a mere ‘technocratic risk manager, whose investment policy becomes increasingly more dependent on investor consent than democratic control’ (Mertens and Thiemann, 2018: 187).

A second shortcoming is that little is known in practice about the moving boundary between on- and off-balance-sheet recording. Yet this delineation represents a dynamic and controversial process. As pointed out by Quinn (2017: 55), ‘even off-budget programs are beholden to budget rules, because they must be carefully designed around them. Off-budget activities are continually at risk of being pulled back into the realm of budgetary discipline and political accountability, which means that off-budget status must be defended and affirmed over time’. So, what criteria should an investment meet to be recorded off-balance-sheet and how do they impact public policies?

Scholarship on the sociology of accounting and quantification has extensively documented the constructed nature of quantitative devices such as national accounting (see Desrosières, 1998; Fioramonti, 2013), their productive impact on conducts (Chapman et al., 2009) and the reactivity to increasing demands for numbers (Espeland and Sauder, 2007; Mennicken and Espeland, 2019). Inspired by this literature, this paper argues that statistical harmonizing results from struggles between statistical agencies (like Eurostat and NSIs) and member states. Far from a self-evident compilation of ready-to-use data, it can be seen as a genuine way of governing public finance and investment policies at a distance.

In contrast with the dense body of grey literature produced by (inter)national statistical offices (e.g. Lequiller and Blades, 2014), surprisingly little scholarly attention has been paid to the harmonizing of public finance statistics carried out by Eurostat under the EMU. By way of exception, Savage (2005) retraced the debates between Eurostat, NSIs and national governments about the calculation of fiscal figures from the mid-1990s to the mid-2000s. More recent papers (Savage and Howarth, 2017; Savage and Verdun, 2016) do not tackle the recording of investment techniques.

Insights from the sociology of public policy instruments and the sociology of accounting and quantification bring a twofold contribution to the political economy of off-balance-sheet policymaking: first, by stressing the moving delineation between on- and off-balance-sheet recording; and second, by highlighting the power struggles and consequences related to this controversial process. By addressing the role of Eurostat’s work in the conduct of public investment policies, this study highlights the discreet yet crucial impact of statistical monitoring and harmonizing on the shaping of the Investor State in the fiscally constrained European polity.

In line with the abovementioned literature, the next section deciphers the accounting aggregates underlying European fiscal rules and their likely impact on investment policies. It shows that these rules encourage further marketization and privatization of public expenses (including investments) by targeting an accounting aggregate that encompasses only non-profitable public bodies: the ‘general government’ sector. Yet the effectiveness of this strategy depends on the harmonization of public finance statistics carried out by Eurostat.

Governing public investment through national accounting: The accounting underpinnings of EU fiscal rules and the role of Eurostat

Since 1992, European Treaties have stated that ‘member states shall avoid excessive government deficits’ (Art. 126 TFEU). In practice, governments are required to reduce their deficit and debt to, respectively, 3% and 60% of their gross domestic product (GDP). Moreover, a Protocol annexed to the TFEU specifies that both indicators should be understood in accordance with the European system of national and regional accounts (ESA) – thereby making the ESA a central, although discreet component of the EMU.

European fiscal indicators are generally presented as default choices, justified by alleged lack of credible or acceptable alternatives (Heipertz and Verdun, 2010; Savage, 2005). They nevertheless exert important effects on public investment policies. First, to ensure fiscal consolidation (i.e. policies intended to reduce deficits and prevent the accumulation of debt), while providing some leeway for investment, the negotiators of the Maastricht Treaty decided to limit member states’ nominal deficit (‘net borrowing’) to 3% of their GDP. In national accounts, a state’s nominal deficit corresponds to the difference between total government revenue and total government expenditure. Accordingly, this criterion does not distinguish between current (ordinary) and capital (investment) expenses. This might be detrimental to large investment projects, which disproportionately impact public deficit. To swiftly improve their public finance statistics, governments might therefore postpone or cancel such projects or have them recorded off-balance-sheet (ibid.).

Second, the accounting aggregate used to calculate public debt is the ‘government consolidated gross debt’. It is referred to as ‘gross debt’ because it does not deduct assets held by governments. In other words, this indicator only reflects the liabilities of governments, without valuing their (financial as non-financial) assets. This choice, which is generally justified by the singularity of public assets (Lequiller, 2018), does not encourage member states to maintain or even increase their assets. On the contrary, it represents a powerful incentive for their sale, with a view to transforming ‘invisible’ assets (under EU fiscal rules) into one-off revenues that might finance new (investment) projects or reduce public debt (Lemoine, 2016).

Institutional Sectors in the ESA.

Source: Eurostat (2013: 8).

The accounting aggregate underlying European fiscal rules – the general government sector – conveys an important definition of the state and ‘public’ finance insofar as it targets not all public bodies but only unprofitable ones – from an economic viewpoint. In other words, the decisive criterion of EU fiscal monitoring lies less in the public or private nature of an institutional unit, than in its economic output (market v. non-market). Yet member states do not passively comply with EU requirements. To restrict the accounting impact of their (investment) expenses under the EMU, they play at the margins of the general government sector. From a national accounting perspective, this can be achieved through outright withdrawal (privatization) or by transforming (non-market) general government units into (market-oriented) public companies (marketization).

In practice, ESA aggregates are also open to considerable room for interpretation. To ensure the reliability and comparability of national data across Europe, Eurostat was designated in 1995 as the guarantor of the quality of public finance statistics (Savage, 2005: 51–52). This marked the start of a mutual learning process between Eurostat officials and member states over the delineation of ESA categories, which has regularly been fed by the strategies designed by national governments to ‘optimize’ their (investment) expenses in relation to EU fiscal constraints. Initially, Eurostat’s resources were extremely scarce: its national accounts directorate consisted of only a dozen officials. During the convergence phase towards the EMU, it took advantage of the attention given to public finance statistics to develop a series of instruments for monitoring member states’ budgets at a distance, such as, for instance, reading national newspapers and reports from the Court of Audit and independent fiscal institutions, and occasional visits to NSIs. Eurostat’s sanctioning powers nevertheless remained merely symbolic, such as press releases without any legal consequences.

The launch of the Eurozone revealed the weakness of Eurostat’s sanctioning capabilities and the limits of the confidence-building strategy adopted, due to its scant resources. As of 2002, Eurostat publicly challenged Greek fiscal figures. Yet its requests for clarification were repeatedly ignored, thereby illustrating the obstacles faced in the absence of cooperation from member states. In 2004, European accountants accused the Greek authorities of having deliberately falsified their budget data between 1997 and 2003, with the help of investment bank Goldman Sachs (Eurostat, 2004a). In response to their pressing call for extended power, Regulation 2103/2005 enabled Eurostat to conduct biennial dialogue visits to NSIs. Exceptional methodological visits were also foreseen ‘in cases where substantial risks or potential problems with the quality of the data are identified’. However, as this reform did not grant Eurostat the auditing powers it required, power struggles continued between Eurostat, NSIs and the member states over the interpretation of the ESA.

The remainder of this paper examines such struggles over the on- or off-balance-sheet recording of investment techniques in arguably the most decentralized country of the EU: Belgium. The next section presents this case and justifies its relevance.

Public investment policy in Belgium (1960–2000): Between devolution and fiscal consolidation

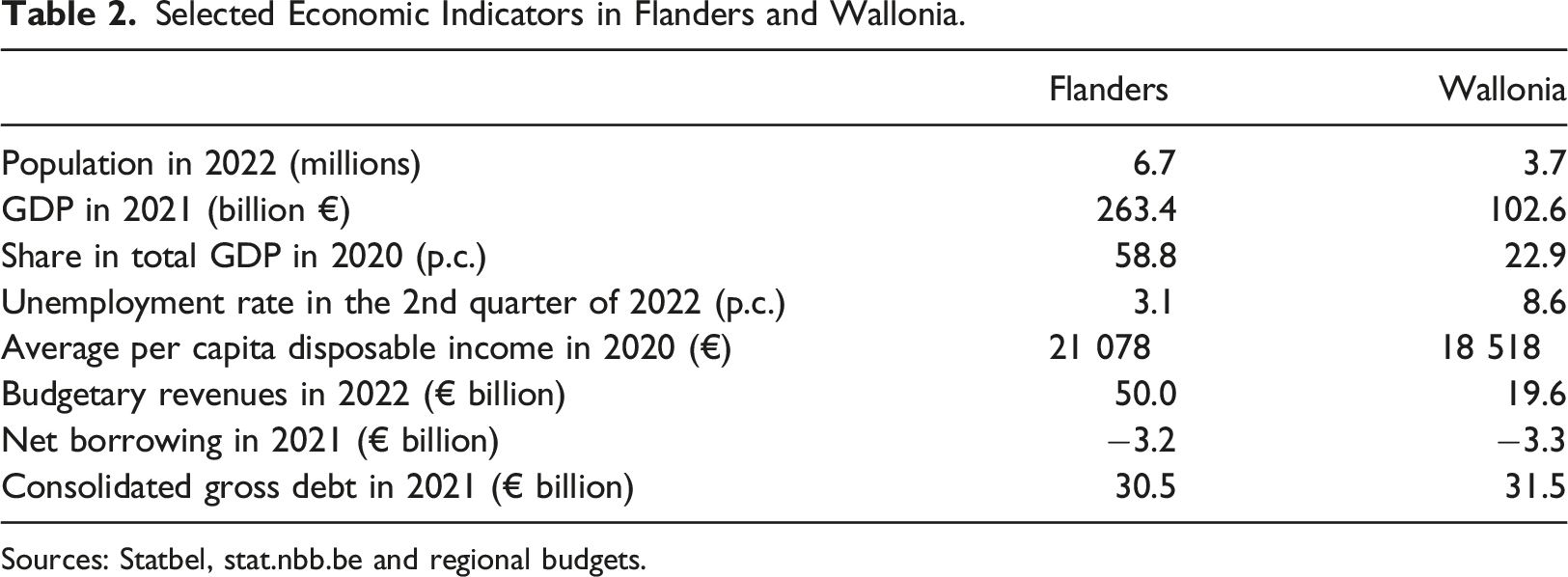

Selected Economic Indicators in Flanders and Wallonia.

Sources: Statbel, stat.nbb.be and regional budgets.

The ‘golden 1960s’ marked the starting point of Flanders’ economic dominance, as public investment attracted multinational corporations in booming sectors. In the meantime, Wallonia intended to ‘modernize’ traditional industries, especially the weakened steel industry. In the 1970s, state support for declining industrial sectors became an acute political issue. Flemish representatives increasingly depicted Wallonia as ‘a burden on economic expansion’ (Witte et al., 2009: 366), while the Walloon movement called for regional autonomy. This occurred in 1980, when economic policy was transferred to the newly created Walloon and Flemish regions. However, the five so-called ‘national’ industrial sectors (steel, coal, textile, glass and shipbuilding) remained in the hands of the central government. This again triggered acrimonious debates, as influential Flemish pressure groups demanded regionalization, claiming that Walloon companies disproportionately benefited from considerable public expenditure (Mommen, 1994). To put an end to community tensions, the third state reform (1988–1989) formally extended regional powers not only to these sectors but also to public works and some areas of transport policy. Since then, the federated entities have been responsible for a wide share (if not the majority) of public investment in Belgium (Figure 1). Government investment in Belgium by sub-sector (% of GDP). Source: Melyn et al. (2016: 100).

This massive devolution of investment policy went hand in hand with severe cuts. Throughout the 1980s, Belgian policymakers achieved public finance consolidation through a sharp decline of public investment, which fell from 5% to about 2% of the GDP, before stabilizing. Out of fear that massive devolution of power and resources would undermine public finance consolidation, the federal government structurally reduced grants to the federated entities: current expenses were cut by around 2%, whereas savings on capital expenses amounted to 14.3% – the share of public expenses then financed through borrowing (Piron, 2022b).

To summarize, in the 1980s public investment, devolution and fiscal orthodoxy in Belgium were closely intertwined. In the following decade, fiscal consolidation remained a political priority, due to Belgian authorities’ eagerness to qualify for the Eurozone. Yet, after two decades of enduring fiscal consolidation, they relaxed their fiscal policy in the 2000s. As budgetary constraints on the federated entities were eased, Wallonia and Flanders simultaneously launched massive investment programmes to spur regional economic growth. The next section examines these policies and the apparent off-balance-sheet strategies developed to finance them throughout the 2000s.

Shallow off-balance-sheet policymaking in Wallonia and Flanders (2000s)

To fund ambitious investment policies in apparent compliance with European fiscal rules in a centrifugal federal state, Flanders and Wallonia largely relied on the so-called ‘alternative’ investment techniques: PPPs and administrative decentralization, respectively. In practice though, marketization and privatization conditions set by the ESA were complied with on the surface only, as both governments endeavoured to keep tight control on the implementation of their investment policy. Off-balance-sheet recording was nevertheless made possible due to Eurostat’s restrained powers and limited data transmission to the NAI.

Flanders: Investing through ‘participative’ PPPs

Flanders is a ‘late, but committed PPP adopter’ (van Den Hurk, 2018: 278). To intensify the pro-market orientation of its investment policy, it created a PPP Knowledge Centre in 2000, before adopting a framework decree on PPPs in 2003. The advent of the Leterme Government (made up of Social-Christians, Socialists and Liberals) in 2004 marked a turning point: large PPP projects were launched in a variety of sectors (e.g. transport, sports and education) to a total value of €6 billion. This financing method explicitly aimed to renew outdated infrastructure while preserving the budgetary balance, by spreading the cost of major investments over several years.

Compared to direct funding of public investment, PPPs benefit from an advantageous accounting treatment. When outsourcing investment projects, governments are theoretically required to record all associated costs in their books at the inception of the contract. However, PPPs bundle both capital and current expenses in a single contract, which includes the completion of an asset and the delivery of a service. Due to this distinctive feature, and with no mention of this topic in the ESA 1995 (then in force), Eurostat (2004b) decided to equate PPPs with lease contracts. Consequently, PPPs could be recorded off-balance-sheet, provided that the private operator effectively bore the ‘majority’ of the risks and rewards arising from the contract. This implied, among others, that the construction risk (including its financing component) was effectively transferred to the private partner.

Eurostat’s ruling was a compromise between three parties: European institutions eager to stimulate growth through public investment (like the EIB) or to secure fiscal discipline (such as the Commission’s Directorate-General for Economic and Financial Affairs and Eurostat); governments seeking to downplay the accounting impact of investments; and large private groups (e.g. public works companies and credit institutions) whose growth had been driven by public procurement (Heald and Georgiou, 2011).

This decision nevertheless prompted criticism. The International Monetary Fund (IMF)’s Fiscal Affairs Department deemed it ‘problematic’, fearing that it ‘could open the door to PPPs that are intended mainly to circumvent the SGP’ (IMF, 2004: 22). In a context of strict fiscal monitoring, Eurostat’s ‘liberal’ stance towards PPPs accelerated their development in Europe. Several interviewees confirmed the decisive influence of Eurostat’s case law on Flemish investment policy (Piron, 2020).

The ‘Scholen van Morgen’ (Schools of tomorrow) project is illustrative of Flanders’ distinctive ‘participatory PPP’ model. With an investment volume of €1.5 billion, this ambitious PPP attempted to reconcile off-balance-sheet recording with clear public involvement (Van Gestel et al., 2014). Consortia created to manage PPPs typically involve financial intermediaries and operational players. To enable the Flemish government to keep control, two regional public companies – including the Flemish Participation Company (Participatiemaatschappij Vlaanderen – PMV) 10 – participated in the special purpose vehicle (SPV) in charge of implementing the project and were granted a blocking minority. Such mechanisms reflected the Flemish authorities’ distrust of private actors, according to an employee of AG Real Estate, one of the two private companies involved in the SPV (December 2015). 11

As governments generally enjoy more favourable funding conditions than private companies, PPPs are more expensive than debt. Therefore, one of the challenges faced by the Flemish government was to transfer sufficient risk to the private partner to safeguard off-balance-sheet recording, while containing additional costs as much as possible. To ‘de-risk’ (Gabor, 2021) this huge investment, it offered guarantees on the liabilities of the SPV, at the request of the private partners. However, these atypical features caught the attention of Eurostat officials, as will be shown later (Section 5).

Wallonia: Investing through semi-autonomous public agencies

To reconnect with its glorious industrial past, the Walloon Region initiated a series of economic recovery programs in the late 1990s. The so-called ‘Marshall Plan for Wallonia’, adopted in 2005 and extended several times since then, mobilized more than €1 billion to promote regional growth, entrepreneurship and jobs (Van Oudheusden et al., 2017). This investment strategy rested extensively on the financial intervention of diverse public agencies, including its regional development bank, the Société régionale d’investissement de Wallonie (SRIW). 12

Such extensive decentralization of public investment policy can partly be explained by Belgium’s tradition of agencification, which federalization has even strengthened. At regional level, the number of public-law agencies increased sharply in the wake of the abovementioned 1988-89 state reform. In 1999, a Walloon decree allowed the creation of specialized agencies with a hybrid legal status. Although characterized by ‘a huge diversity of autonomy and control arrangements’, these vehicles – such as the SRIW and its subsidies – quickly ‘became a popular device to stimulate the Walloon economy’. In 2010, they accounted for a quarter of all Walloon agencies (Verhoest et al., 2012: 92).

Budgetary considerations are not foreign to this trend either, as administrative decentralization served to downplay the accounting impact of public investments. To spread their cost over time, the Walloon authorities used to outsource major investment programmes (e.g. roads and subsidized municipal works) to a wide range of autonomous agencies. In practice, the latter remained under the supervision of the government, as witnessed by the appointment of managers and board members close to the parties in power. On the grounds of their legal autonomy, most of these government-backed agencies were nevertheless classified outside the general government sector by the Walloon authorities. In addition, some of them were instructed to pre-fund vast investments, before subsequently being paid back through regional subsidies. Although not legally responsible for borrowing, the Walloon government still bore the economic responsibility of these ‘delegated missions’.

This strategy of investing through decentralized public units was in line with Wallonia’s tradition of economic dirigisme, which had taken shape in the 1960s to rescue failing industries (see Section 3). Its raison d’être was to support economic recovery while ‘mitigating’ European fiscal rules, by recording strategic investment expenses off-balance-sheet. Accordingly, it did not intend to turn involved agencies into ‘market producers’, as required by the ESA.

The sectoral classification of specialized public agencies at the edge of the general government sector provoked serious conflicts between the Walloon executive and statistical authorities in the second half of the 2000s. While the regional government used to calculate public finance statistics on the basis of a restricted consolidation scope, made up exclusively of general administrative services (i.e. the regional administration in a narrow, legal sense), the NAI adopted a broader perspective. This was based on the ‘substance over form’ principle contained in the ESA, according to which the economic substance prevails over legal form. Following Eurostat’s first dialogue visits in 2006 and 2008, the NAI started to include (‘consolidate’) several major agencies, such as the SRIW, into the Walloon general government sector. In so doing, it worsened Walloon fiscal indicators and limited opportunities for ‘alternative financing’ of public investments. The Walloon authorities rejected the NAI’s decisions as unacceptable federal interference in regional affairs, as a close advisor to a former Walloon Minister of Budget explained: ‘There is no denying that the fact that all this came from a federal structure addressing the federated entities, was perceived at certain times, in certain games, as forms of investigation, with politically tainted approaches’. 13

The next section shows how Eurostat gained power in the wake of the Eurozone crisis and used it to tighten its grip on Belgian public finance statistics.

Regional investment policies put to the test of Eurostat’s increased powers (2010 onwards)

In October 2009, Eurostat officials used a second major revision of Greece’s public deficit to request genuine audit powers. Against the backdrop of the emerging sovereign debt crisis, they successfully convinced national governments to increase their sanctioning powers. First, Regulation 679/2010 granted Eurostat the right to access the accounts of all public bodies in the (exceptional) context of the so-called ‘methodological visits’. Second, its staff dedicated to monitoring government finance statistics grew from 15 to about 50 between 2010 and 2014 (Savage and Verdun, 2016). Third, Eurostat was granted the power to fine states for statistical manipulation. A European accountant whom I met in February 2016 emphasized how exceptional this prerogative was in the European context: ‘Now, if a country sends me data that I consider are not accurate, I can change them. Previously, I used to put footnotes, but now I also have the power to change the data [...]. And above all, the big difference [is] these increased investigative powers and the power we have to impose fines. Only we and DG Competition have this power. The only DGs in the Commission’.

14

Eurostat officials would not wait long to use their new tools. In May 2012, they launched an investigation due to suspicions of statistical manipulation in the Region of Valencia. This would result in the Council sentencing Spain to the first fine ever under the SGP, in July 2015 (Savage and Howarth, 2017). In 2018, Austria was likewise fined, on similar grounds (Piron, 2022a). It was no coincidence that both fines involved federal countries. Eurostat pays particular attention to federations, suspecting that devolution might affect data transmission, as highlighted in an interview with a European accountant. 15

A similar situation occurred in Belgium, where the long-lasting controversy between Eurostat, the NAI and regional governments eventually resulted in stricter implementation of European statistical requirements. In the past, Eurostat had repeatedly called for fundamental changes to address shortcomings in the Belgian statistical apparatus. One of them was the NAI’s lack of resources: until the early 2010s, only three civil servants monitored the entire Belgian public finance statistics. In February 2014, senior European accountants convened a series of meetings with representatives from all governments of the Belgian federation to put an end to the lack of cooperation of the federated entities, as explained by the same Eurostat official: ‘We asked so many times: “what about this, and this, and this, concerning the regions?”. And the NAI said: “we don’t have the data, we don’t have it, we don’t have it.” “Why don’t you have it?”. And then we started to understand that the data were not available because the regions were not cooperative. They were just ignoring the requests made by the NAI’.

16

It appeared that out of fear that massive consolidation of public agencies with the general government sector would jeopardize its investment policy, the Walloon government would only send limited information to the NAI. Its requests were treated as merely ‘incidental’ or ‘cosmetic’, as the abovementioned advisor to the Walloon Minister of Budget puts it. 17 Although at odds with its legal duties, such partial transmission of data was facilitated by the NAI’s understaffing.

Following this visit, Eurostat listed 53 action points to be implemented urgently. These included, for example, the nomination by each region of a ‘single point of contact’ for all exchanges with the NAI, as well as the provision of ‘an exhaustive list of government-controlled units’ and ‘all the information needed’ to perform sector classification analysis (Eurostat, 2014: 57–58). It also threatened Belgian governments to launch an investigation into possible manipulation of statistical data, similar to the one underway at the time in Spain. Belgian authorities eventually decided to comply with Eurostat’s injunctions, to avoid the fallout of such an investigation which was perceived as an ‘atomic bomb’, 18 according to an advisor to a former Walloon Regional Minister whom I met shortly after Eurostat’s visit. A senior official of the Belgian federal budget administration, who reported having been ‘slapped in the face’ during these meetings, stressed the attention that Belgian policymakers subsequently paid to European statistical requirements: ‘It’s the internal life that has changed. This whole thing helped to increase the politicians’ awareness, by saying “don’t do anything stupid because at the end of the day, it’s Eurostat and NAI statistics that count”’. 19

Stricter enforcement of the ESA led to the reclassification of many investment vehicles and expenses within the general government sector, and therefore to the upward revision of Belgian public debt by more than €26 billion (6.8% of GDP). This rise was significantly higher than the eurozone average (1.2%) and mostly concentrated in federated entities, which accounted for just under 70% of total changes (NAI, 2014: 51). For instance, Flemish debt increased by nearly €11 billion (to €16.6 billion), mostly due to Eurostat’s stricter case-law on PPPs. After extensive negotiations with Flemish authorities, Eurostat ultimately decided to reclassify most Flemish PPPs into public accounts due to insufficient risk transfer to the private partner.

Regularly confronted with practices deemed incompatible with its 2004 case law, Eurostat officials decided to clarify its understanding in 2010 (Eurostat, 2010), with a view to putting an end to what they considered ‘abusive’ interpretations, according to an EIB official: ‘Often, governments would set something together, but behind it they would give guarantees, some comfort. So it was a sort of classic procurement, but with a PPP label, with the advantage of not having to record the debt on their books. And so, there were many reclassifications. At that point, Eurostat took a harder line’.

20

As for Wallonia’s debt, it increased by more than €12 billion (to €18 billion) between September 2013 and September 2014. After a comprehensive report by the Court of Auditors had ‘opened the eyes’ 21 of statistical authorities to the magnitude of the issue, the NAI reclassified no fewer than 115 agencies within the Walloon general government sector (which serves as the basis for calculating regional deficit and debt), due to a lack of autonomy, public control or insufficient market output. This list included many agencies investing in a wide variety of policy fields – from roads to decontamination of soil, through social housing and airports (Piron, 2019).

The last section explains the contrasting responses of these two Belgian regions to Eurostat’s increased monitoring.

Consolidating or resisting financialization: Divergent regional investment policies (2014 onwards)

The two main Belgian regions reacted very differently to Eurostat’s growing scrutiny: while Flanders further sharpened the financializing of its investment policy, Wallonia has so far stood against this trend and has even returned to traditional budgetary financing, for economic and political motives.

Flanders: Consolidating the financialization of public investment

In Flanders, the right-wing government installed after the 2014 elections reaffirmed its commitment to both fiscal discipline and dynamic public investment. To insulate the latter from budgetary cuts, it intended to draw lessons from the on-balance-sheet reclassification of its ‘first generation’ of PPPs, by designing a new PPP model that would be compatible with Eurostat’s case law. Basically, this implied eliminating any public participation in the SPV and public financing, as illustrated by the Flemish government’s strategy since 2016 regarding school buildings. In a letter to Eurostat (2016: 3), the Flanders’ executive expressly committed to ‘a very pure DBFM [Design-Build-Finance-Maintain]-construction contract’, where ‘no financial interest – directly or indirectly – will be held in the SPV in terms of participation, financing, provision of guarantees, control or otherwise’.

Faced with increased risk, private partners might in turn raise their returns on investment, as explained by a PMV employee in December 2015 – at a time when the Flemish government and its regional development bank were still reconsidering their PPP strategy following Eurostat’s intervention: ‘If the operator must carry all the risks on an ongoing basis, will they still be willing to invest? Will the bankers still be willing to invest? Because then you must start tinkering with things that will be riskier for them as well. Are the operators willing to carry all this? And if they do, well, what price are we going to have to pay?’.

22

With this logic, the funding of PPPs ultimately depends on the financial appraisal of private investors, erected as ultimate judges of investment projects – instead of the political choice of elected representatives. Off-balance-sheet policymaking therefore appears far less neutral towards public investment than (implicitly) envisioned by the current functionalist uses of the concept of ‘fiscal ecosystem’. Since their off-balance-sheet recording is conditional on (quasi-)privatization and marketization, public investment policies in the EU are increasingly subordinated to a financialized logic (Chiapello, 2017; Epstein, 2005).

To contain costs, Flemish authorities have moved away from ‘mammoth’ 23 projects and have started to put small-scale clusters (amounting to between €30 and €60 million capital expenditure) on the market. By splitting the overall risk into a series of smaller and hence more manageable risks under standardized contracts, they have intended to foster competition between private operators, with a view to generating savings. In parallel, in March 2019 the Flemish Parliament passed a new decree providing for increased supervision, standardization and monitoring of large investment projects, including PPPs. Procedural and financial safeguards were also set to limit their potential adverse effects (Willems and Bruyninckx, 2020).

The Flemish Recovery Plan designed to absorb the consequences of the COVID-19 pandemic confirms the growing financializing of Flemish investment policy. Next to a ‘one-off’ budgetary provision (€3.4 billion, including European subsidies worth €2.3 billion), contingent liabilities play a crucial role in ‘Flemish resilience’: in addition to over €3 billion dedicated to renovating school buildings through off-balance-sheet PPPs, the Flemish regional development bank, PMV, has also mobilized over €4 billion to manage the fallout of the sanitary crisis and Brexit, through loans, equity investments and guarantees. It has furthermore created a ‘welfare fund’ aiming to leverage €500 million out of €240 million of public money (Court of Auditors, 2022).

By contrast, the case of Wallonia illustrates that the financializing of public investment policy encouraged by European fiscal and accounting rules is not inexorable and can be opposed by governments.

Wallonia: Reverting to budgetary financing of public investment

In Wallonia, the consolidation of many agencies into the general government sector threatened to jeopardize regional investment policy and reinforce the focus on fiscal sustainability. Stating that ‘the new European rules for fiscal discipline impose[d] reinforced and tightly controlled rigor’, the Socialist-Social-Christian executive formed after the 2014 elections undertook to implement ‘unprecedented fiscal consolidation’ (Walloon Government, 2014: 6). At the same time, it reaffirmed the importance of economic recovery – even though it remained silent about its funding. For instance, an administrator of the Walloon public agency in charge of funding road investments (‘Société de financement complémentaire des infrastructures’ – SOFICO), whom I met in January 2015, feared the ‘risk’ 24 of the government privatizing this unit with a view to ensuring off-balance-sheet recording of its huge investment expenses. Another scenario under study would be to increase the revenues of selected non-market public units, with a view to transforming them into market-oriented public companies – and therefore classified outside the general government sector.

When the centre-left Walloon government fell in 2017 due to internal conflicts, the dominant Socialist Party joined the regional opposition for the second time only in four decades. The short-lived centre-right government in power until the 2019 elections opened new perspectives for ‘a stronger partnership with the private sector’ (Walloon Government, 2017: 7). However, this has not materialized. Unlike Flanders, financialized investment tools remain marginal in Wallonia. For instance, the governing coalition since 2019 (Socialists, Liberals and Greens) adopted in October 2021 a ‘Recovery Plan for Wallonia’, 25 with the help of an academic advisory group. The bulk of investment projects contained in this plan (worth €7.6 billion) are funded through traditional budgetary tools, such as subsidies directly stemming from regional resources (including €1.48 billion EU subsidies).

Several reasons explain this choice. First, low interest rates have made debt financing of investments particularly attractive. Senior Walloon officials contrast the apparent simplicity of this practice with ‘the new complexity of off-balance-sheet operations’ 26 and the financial and organizational pitfalls likely to result from Eurostat’s requirements – as experienced with the enduring implementation problems faced with the first (and thus far the only) PPP ever launched by the Walloon government: Liège’s tramway. This project, decided in 2011, eventually started in 2019 – among others due to four amendments to secure its off-balance-sheet recording by Eurostat. Due to be completed in October 2022, it is currently over 2 years behind schedule, leading to major conflicts between the Walloon government and the private operator, Tram Ardent. 27

Second, this strategy has been facilitated by the Commission’s ‘flexible’ reading of the SGP prior to its outright suspension since March 2020. Under the Juncker Commission (2014–2019), the Commissioner for Economic and Monetary Affairs, French Socialist Pierre Moscovici, was prone to favour negotiations rather than sanctions with non-compliant member states (Mérand, 2021).

Finally, Wallonia’s return to traditional funding techniques also reflects the desire of regional authorities to maintain strategic control over their investment policy. According to an actor involved in drafting the regional recovery plan (predominantly left-wing), Walloon policymakers remain ‘very strongly suspicious’

28

about private finance – in contrast to their (predominantly right-wing) Flemish counterparts. Consequently, neither the academic expert group nor the members of the Walloon government could agree on greater involvement of financial actors and instruments in regional recovery policies, as stressed in the following quote: ‘We insisted a lot on the Flemish model, where the state gives the impulse, but is not afraid, after a while, to let the private sector get more involved and even to sell shares to the private sector to develop. This was a very sensitive issue. [...] It’s complicated to get this message across here in Wallonia. There is still a great deal of reluctance to accept the idea that public money can, at some point, be used to develop private sector activities which, in the end, will develop on their own’.

29

Conclusion

This paper has highlighted the influence of Eurostat’s statistical harmonizing and monitoring of public finance statistics on (sub)national investment policies in the EU. Combining insights from the policy instrumentation approach and the sociology of accounting and quantification, it critically refines the concepts of ‘fiscal ecosystems’ (Guter-Sandu and Murau, 2022) and ‘off-balance-sheet policymaking’ (Mertens and Thiemann, 2018; Quinn, 2017), by stressing the dynamic nature of the boundary between on- and off-balance-sheet recording and the productive effects of this contested process on public investment policies.

EU fiscal rules target a precise accounting aggregate, namely, the ‘general government sector’, which exclusively encompasses non-market public producers (as opposed to private producers and public companies). Hence, they encourage ‘market-based but state-led’ (Mertens and Thiemann, 2018) off-balance-sheet investment tools, like PPPs and financialized state-owned utilities. This pro-market stance has consolidated the financialization of investment policymaking in Europe, that is, its growing subordination to financial actors, logics and tools (Chiapello, 2017; Epstein, 2005).

The examination of a long-lasting controversy between Eurostat, the NAI and the two main Belgian regions has highlighted the instrumental role of statistical harmonization in shaping such a ‘market-based but state-led’ public investment regime in the multilevel EU. Yet Flanders and Wallonia adopted contrasting responses to the rise of Eurostat’s power. Eager to combine dynamic public investment and fiscal discipline, right-wing Flemish governments have resolutely consolidated the financialization of their investment policy, as witnessed by their recent recovery plan. By contrast, centre-left Wallonia has so far resisted this trend and even decided to fund its recovery policy through debt, due to low interest rates, the suspension of fiscal rules and wariness of private finance.

The Walloon case calls into question the conditions of resistance to the governing public investment through financial markets rooted in European fiscal and accounting rules. It demonstrates that the growing financialization of public investment at the core of the EIS is no fatality and that governments keep some room to manoeuvre and might follow an alternative investment strategy. However, the Walloon government also benefited from extraordinary political and economic circumstances until recently. The distinctiveness of its investment policy is now being put to the test of more adverse circumstances, characterized by rising interest rates and the return of tighter European fiscal constraints. Against this backdrop, will Wallonia withstand or – eventually – favour the path of the EIS?

Footnotes

Acknowledgements

The author thanks Matthias Thiemann, Ulrike Lepont, Daniel Mertens, Zoé Evrard, Catherine Fallon, the participants to the workshop ‘Public investment policies in Europe’ held on 5th and 6th September 2021 in Sciences Po Paris and the two anonymous reviewers for insightful comments on previous versions of this paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.