Abstract

Large, domestically owned and headquartered firms have been catalysts of structural transformation in several East Asian late-industrialisers. This article investigates why Nigeria’s largest domestically owned industrial conglomerates, most notably the Dangote Group, have failed to catalyse similar broad-based industrial transformation, despite their scale and entrepreneurial success. We show that such firms in Nigeria have produced limited spillovers and substantial negative effects on the wider industrial ecosystem. Theoretically, the article mobilises Myrdal’s concept of backwash and spread effects to reframe diversified business groups (DBGs) as ecosystem coordinators whose developmental role must be assessed through these effects. It shows that in Nigeria, backwash effects, stemming from market concentration, predatory behaviour, and regulatory capture, have systematically outweighed spread effects such as capability development and supplier upgrading. The findings advance the study of African capitalism by conceptualising how large firms can simultaneously stimulate and stifle industrial ecosystems, depending on the political and institutional mediation of scale. The article concludes that effective industrial policy must address not only capability failures in firms, but also the structural power of dominant conglomerates and the ecosystem-wide tensions produced by scale.

Introduction

After decades of neoliberal structural adjustment, Nigeria renewed its industrial policy efforts in the early 2000s with the introduction of the Backward Integration Policy (BIP) (Akinyoade and Uche, 2018; Itaman and Wolf, 2021; Odijie, 2020). Renewed industrial policy efforts first focussed on the cement sector, where, against the rapid increase in demand for building materials, they facilitated the meteoric rise of domestic conglomerates (Wolf, 2023a, 2023b). The Dangote Group stands out with subsidiaries across nine African countries, challenging not only the dominance of European cement manufacturers on the continent but also structures of dependency created under colonial rule reinforced under US neoliberal hegemony (Odijie, 2020). With the establishment of the Dangote Oil Refinery, Africa’s largest refinery and one of the largest in the world, Nigeria is taking critical steps towards reducing its dependence on imported refined petroleum, which accounted for over 80% of its consumption as of 2024. Domestically, these conglomerates, supported by the BIP, have diversified into a wide array of sectors, including consumer goods like sugar, salt, tomato paste and capital goods like petro-chemicals, and fertilisers.

Such Diversified Business Groups (DBGs), 1 are common in the context of developing economies and they have been critical to the success of industrialisation efforts in East Asia (Choo et al., 2009; Keister, 1998; Lee and Woo, 2002; Peng, 1999). Indeed, Lee et al. (2013) find that the presence of large, headquartered firms is a strong indicator of whether emerging economies can overcome the middle-income trap. However, in Nigeria’s case, emerging conglomerates thrive in a winner-takes-all environment, supported by rent-seeking practices that drive competitors out of the market and hinder the development of related industries.

This article asks why Nigeria’s large DBGs have failed to generate broader industrial development, despite their scale and dominance? Research on DBGs acknowledged their ambivalent role as either ‘paragons or parasites’ (Khanna and Yafeh, 2010), pointing to the potential negative implications of rentier behaviour and regulatory capture for direct competitors and consumers (Amsden, 1989; Khanna and Yafeh, 2007). We move beyond this competitor-centred perspective and theorise the role of DBGs within the wider productive ecosystem, 2 in which their developmental impact is shaped not only by relations with rivals, but also by their interactions with suppliers and complementors. To do so, we apply Gunnar Myrdal’s concept of scale-based backwash and spread effects to domestic industrial ecosystems in late-industrialising economies. Such backwash and spread effects are inherent to accumulation regimes based on increasing returns to scale and can explain spatially uneven development (Myrdal, 1957). By adapting this framework to emerging industrial ecosystems in late-industrialising economies like Nigeria, we reframe diversified business groups (DBGs) as ecosystem coordinators whose developmental role must be assessed via their backwash and spread effects. We show that large first-mover firms can produce both scale-based spread and backwash effects within national productive ecosystems, shaping the development paths of surrounding firms either positively, through skills development, knowledge and demand spillovers, or negatively, by crowding out competitors and/or subordinating suppliers and complementors.

Drawing on qualitative data from interviews with industry experts and industrialists, we examine the role of large DBGs within Nigeria’s productive ecosystem tracing backwash and spread effects. We demonstrate that backwash effects have dominated spread effects due to first the political structuring of gains from increasing return to scale (IRS), which favoured old economic elites rooted; second the stagnation of market growth, which left less room for the simultaneous expansion of several firms and increased the reliance on rent-seeking by incumbents; and third the lack of adequate support for capacity development of complementors and suppliers of large conglomerates.

Together, the findings advance our understanding of the constraints to late industrialisation in two ways. First, they substantiate the problem of ‘size failure’, that is, the absence or dysfunction of large, domestically headquartered firms capable of driving industrial upgrading of related firms. Second, they offer a new perspective on diversified business groups (DBGs), reframing them not merely as competitors or state-aligned actors, but as potential coordinators of productive ecosystems. Their developmental impact, we argue, hinges on their inter-firm relations with suppliers, complementors, and rivals. The productive ecosystem effects of corporate power asymmetries are well documented in GVC research, where multinational corporations benefit from scale, enforce intellectual property rights, and dominate high-value segments (Durand and Milberg, 2020; Lee, 2019; Lee and Malerba, 2017; Mondliwa et al., 2021; Shin et al., 2016). We find that similar dynamics emerge domestically, where first-mover advantages can similarly produce dysfunctional productive ecosystems and winner-takes-all environments. Therefore, we argue that industrial policy must actively manage scale. This involves mitigating backwash effects through competition policy as widely acknowledged in the literature on competition and corporate power (Makhaya and Roberts, 2013; Marty and Warin, 2023; Mondliwa et al., 2021) but also nurturing spread-effects to take hold.

Size-failure in late-industrialisation

The late-industrialisation problem: Firm-level capability and size failure

Structural transformation towards high value-added productive activities, especially in manufacturing remains a key developmental challenge for African economies. Latecomer industrialisation depends on industrial policy that successfully supports firm-level learning and capability accumulation. Here, political settlements theory focussed on how such capability development can be successfully supported within a given distribution of power in society (Behuria, 2019; Kelsall et al., 2022; Khan, 2013; KjÆr, 2015; Whitfield et al., 2015). Innovation studies complement this perspective by identifying sectoral priorities and ‘windows of opportunity’ for late-comers emerging through technology, demand, and public policy (Altenburg et al., 2022; Lee, 2019; Lee and Malerba 2017; Whitfield and Wuttke, 2026).

While much of the industrial policy literature concentrates on overcoming firms’ ‘capability failure’, Lee (2019) highlights ‘size failure’ as a distinct and critical constraint on industrialisation, explicitly incorporating the scale of production as a core analytical dimension. Lee et al. (2013) show that the presence of large, headquartered businesses is a good predictor of whether an economy can overcome the so-called middle-income trap. Indeed, such large, domestically headquartered firms, often operating DBGs in the developing economy context, have been central to successful industrialisation in Japan (Kobayashi, 1986), Korea (Amsden, 1989; Choo et al., 2009) and China (Keister, 1998; Lee and Woo, 2002; Peng, 1999). DBGs possess distinct advantages. Their ability to leverage economies of scale and scope means they have a unique potential to sustain productivity increases but also to overcome resource constraints. Economies of scope, for instance, allow large conglomerates to pool firm-level internal capabilities, supporting new affiliates during their initial stages by offering access to markets, capital, and established brand names. Additionally, they can collectively utilise significant intangible assets such as research and development or marketing units, promoting innovation through extensive knowledge sharing among group affiliates (Lee, 2019).

Given their potentially developmental roles, DBGs have been studied from three main perspectives: (1) their emergence, explained through theories of transaction costs, market failures, and institutional voids (Khanna and Palepu, 2000; Leff, 1978); (2) their financial and productive performance relative to non-group firms (Choi and Cowing, 2002; Choo et al., 2009; Keister, 1998; Lee and Woo, 2002; Shapiro et al., 2024); and (3) their political ties and the governance of market power (Amsden, 1989; Behuria, 2022; Colpan and Morck, 2021; Khanna and Yafeh, 2010; Puente and Schneider, 2020). This literature emphasises the ambivalent nature of DBGs as ‘paragons or parasites’ (Khanna and Yafeh, 2007, 2010), prone to anti-competitive behaviour and rent-seeking with negative ramifications for competitors and consumers.

From ‘paragons or parasites’ to ecosystem coordinators: Reframing the role of large-domestically owned firms in late-industrialisation

Despite these advances, several gaps remain in understanding the reasons behind ‘size failure’. The first is empirical, with most of the evidence on the positive role of large businesses coming from successful East Asian late-industrialisers, little is known about the role of DBGs in supporting late-industrialisation outside of the East Asian context. In Africa, for instance, private, state-owned and party-affiliated diversified business groups (DBGs) led by domestic capitalists are key actors in African industrialisation but their role remains largely understudied (Behuria, 2022), especially what role they play in contributing to or hindering broader industrial transformation. Second, existing conceptualisations of DBGs adopt a competitor-centred perspective, which leaves unnoticed the potential developmental role DBGs may play through their interactions with suppliers and complementors, beyond direct competitors.

This article extends the conceptualisation of DBGs by introducing the productive ecosystem as a unit of analysis. Economic geography scholarship has long shown that industrial development is organised through territorially embedded ecosystems in which inter-firm relations extend beyond competition and include symbiotic relations between large firms and their suppliers, and complementors. This constellation of competitive and (potentially) symbiotic relations can take different forms across contexts (Markusen, 1996), and it is this case-specific organisation of inter-firm relations that we conceptualise here as a productive ecosystem.

Adopting a productive ecosystem perspective is analytically valuable because there are strong reasons to view DBGs as coordinators of these ecosystems. First, large regionally headquartered firms can act as agglomeration forces, attracting and sustaining smaller firms, which specialise in related fields or cater for input demand. In doing so, they generate the conditions for expansion and influence the technological trajectories of surrounding firms (Gong et al., 2024). However, DBGs, by virtue of their economies of scale and scope, also reduce the need to develop competitive linkages with external suppliers, hampering functional upgrading of smaller firms.

Second, large regionally headquartered firms typically retain the highest value-added activities, such as goal setting, planning and research and development of proprietary technology spatially close to headquarters (Massey, 1984 [1995]; Wolf, 2025). The emergence of regionally headquartered DBGs that internalise such high-value functions offers the potential to reduce spatial asymmetries in the global distribution of value-added activities (Odijie, 2019).

Such an ecosystem approach is inherent in Global Value Chains (GVC)/(GPN) research, linking inter-firm power asymmetries between lead-firms and suppliers/complementors to firm-level capability development in late-industrialising contexts (Durand and Milberg, 2020; Mondliwa et al., 2021; Whitfield, 2023; Whitfield and Staritz, 2021). This literature shows that learning and upgrading depend on historically constituted productive capabilities, transnational networks, and the strategic alignment of interests between lead firms and suppliers (Whitfield, 2023). While this work integrates capability development and an ecosystem approach, its primary focus remains on the global scale and cross-border governance structures, leaving less explored how similar mechanisms operate within domestic productive ecosystems dominated by large national firms. This article brings these strands together by analysing how capability development, scale of production, and inter-firm relationality interact within domestic productive ecosystems. We argue that to assess whether DBGs act as ‘paragons or parasites’ (Khanna and Yafeh, 2010), it is necessary to understand the role they play in structuring inter-firm relations and enabling (or constraining) capability development across the ecosystem. Thus, the core theoretical contribution of this article is to reframe the role of large business groups in late-industrialising economies as ecosystem coordinators whose developmental impact must be evaluated through their inter-firm relations.

Mobilising Myrdal’s theory of uneven development to understand the impact of DBGs within the domestic productive ecosystem

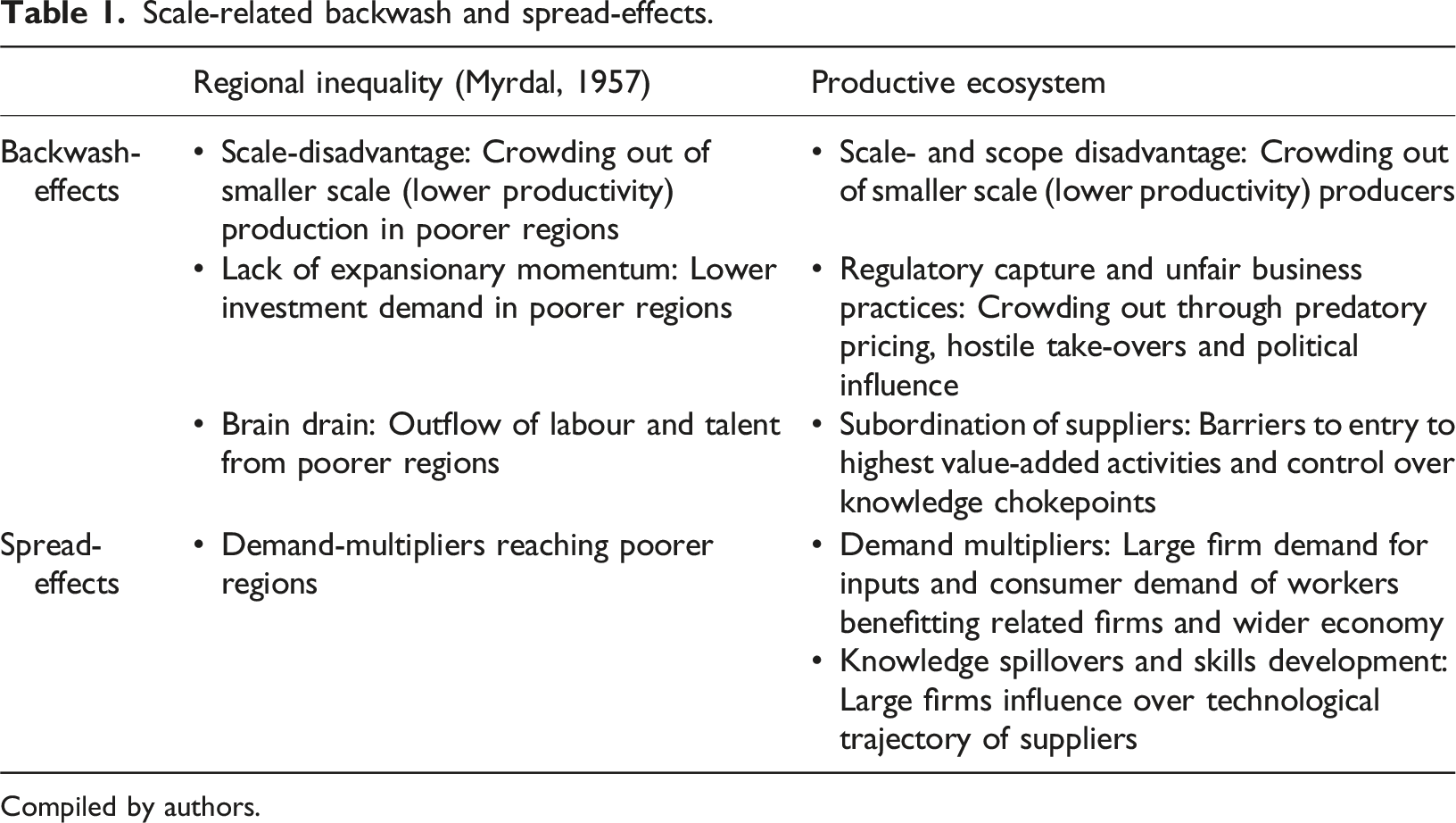

Scale-related backwash and spread-effects.

Compiled by authors.

Such backwash and spread have been well documented in the context of lead firms in Global Value Chains (GVCs). Whilst the growth of MNCs from advanced economies created windows of opportunities for late-comers (Lee, 2019; Lee and Malerba, 2017) mainly in the form of expanding markets and technology transfer (Alessandria et al., 2023), lead-firms from advanced economies use their cumulative productive advantages in ways, which hold back the development of productive capabilities of firms from emerging markets (Durand and Milberg, 2020; Lee et al., 2015; Milberg and Winkler, 2013; Shin et al., 2016).

The need to disentangle domestic institutional mediation of scale

Backwash and spread effects are equally relevant within domestic economies, especially as late-industrialisers start developing manufacturing capabilities. Gray (2025), for instance, demonstrates that small Tanzanian maize millers were unable to tap into emerging market opportunities given technological gaps and institutional biases towards large firms. This dynamic underscores that without deliberate intervention, economies of scale and pre-existing capability gaps can reinforce winner-takes-all outcomes across the productive ecosystem, where dominant firms absorb the bulk of new market opportunities while smaller firms are excluded or downgraded.

This article investigates the role of large domestic conglomerates in Nigeria’s productive ecosystem. We show that, in the Nigerian case, the political mediation of backwash and spread effects ultimately meant that backwash effects prevail. Despite their market-creating and structuring functions (spread-effects), the activities of large conglomerates became increasingly rentierist, especially when the market expansion potential for their own outputs diminished. By situating this analysis within the framework of increasing returns to scale, we show that industrial policy must not only foster firm-level capabilities, but also actively shape productive ecosystems. This includes neutralising backwash effects by holding in check rentierist tendencies of large firms and ensuring growing market size and enhancing spread-effects by supporting capability development in complementor and supplier firms.

Data and methods

This paper employs a qualitative case-study design centred on Nigeria’s most prominent diversified business group (DBG), the Dangote Group. Such an approach enables close, context-sensitive examination of complex phenomena – including the effects of DBGs on productive ecosystems – while allowing researchers to analyse sequence, contingency and causal pathways more effectively than large-N designs. It is therefore particularly well suited to exploring how and why processes unfold, rather than merely identifying statistical associations (Gerring, 2004). Although case studies have been criticised for their limited generalisability, case-study methodologists argue that they can generate generalisable insights when embedded in a clear conceptual framework, systematically compared across cases (Gomm et al., 2000), and strategically selected (Eckstein, 2000; Flyvbjerg, 2006).

Generalisation begins with theoretically informed induction, whereby researchers define the phenomenon to be explained and its causal determinants, providing the conceptual foundation for extending insights beyond a single case (Gomm et al., 2000). In this study, Myrdal’s notions of backwash and spread effects serve as analytical lenses to trace the mechanisms through which scale, vertical integration, and first-mover advantages shape inter-firm relations within Nigeria’s productive ecosystem. Interview and documentary evidence are interpreted in terms of whether they indicate capability diffusion and opportunity creation (spread effects) or resource concentration, market foreclosure, and institutional capture (backwash effects).

Strategic case selection also shapes the range of generalisations that can be drawn. Demonstrating the absence of predicted outcomes in contexts where they are ‘most likely’ to occur can help isolate key causal mechanisms (Eckstein, 2000), while appropriately chosen ‘critical cases’ can illuminate wider causal patterns and interactions (Flyvbjerg, 2006). Nigeria represents a ‘most-likely’ case given the prominence and rapid expansion of its domestic conglomerates, and the Dangote Group constitutes a critical case within this context due to its dominant scale and influence.

Finally, generalisation requires examining explanatory factors across a sufficiently large set of cases to identify when and how predicted effects occur (Gomm et al., 2000: 249). While such cross-case testing lies beyond the scope of a single article, future research could build on the approach developed here through comparative studies of DBGs across sectors and countries, helping to identify the conditions under which scale and vertical integration generate stronger spread effects rather than reinforcing backwash dynamics.

The analysis draws on thirteen semi-structured interviews and extensive desk-based research, enabling triangulation across data types and sources. Interviews were conducted between 2021 and 2024 using purposive sampling to capture actors directly involved in, or affected by, the Dangote Group’s operations, as well as those with sectoral or regulatory expertise. Participants include employees and former employees of Dangote firms, suppliers and industrial competitors, government and regulatory officials, industry analysts, and representatives of host communities. Snowball sampling was used selectively to access respondents with specialised knowledge where access to senior industry and policy actors was constrained.

13 interviews were conducted by the authors, and two draw on published interviews by PM News, included due to their unique insights from a key stakeholder (a host-community leader). All interviews were thematically analysed, with attention to recurring narratives on market power, linkages, upgrading, and institutional as well as community relations. Interviewees were anonymised as agreed. Although the number of interviews is modest, their depth and diversity provide sufficient empirical grounding for the study’s claims.

Interview findings were complemented by desk research, including company filings, policy documents, sectoral studies, media reports and relevant academic literature. Desk research served to contextualise interview evidence and to corroborate claims concerning investment patterns, sectoral dynamics, and regulatory interventions. While comparable quantitative metrics were not consistently available across subsidiaries due to uneven disclosure, qualitative material provided rich insights essential to the analysis.

Monopolisation dynamics in the Nigerian manufacturing sector

Nigeria serves as an example where large domestic business groups have historically played a significant role in the manufacturing sector. Several conglomerates that emerged during the Import Substitution Industrialization (ISI) period have solidified their positions as key players in the Nigerian manufacturing industry today, particularly following the introduction of the backward integration policy in the early 2000s. During the ISI period, industrial policy measures favoured specifically large-scale, merchant capitalist interests (Biersteker, 1987; Forrest, 1987), which formed in the colonial era (Watts, 1987). A popular route taken by old merchant families, such as Dantata, Ganash, Danbappa, Rabiu, Ibeto Group or the Modanola Group, was to move from monopoly distribution of a particular product to production of the same item in Nigeria targeting the lower end of the consumer market (Biersteker, 1987: 272; Forrest, 1992).

Two large domestic business groups, in particular Dangote and BUA, that emerged during the ISI period play a key role in the Nigerian manufacturing sector today. As argued by Odijie (2020), the successful expansion of domestic lead firms such as Dangote, was essential to avoid an industrialisation path in subordinate positions in global value chains (GVCs). A descendant of the prominent Dantata merchant family, Aliko Dangote established Dangote Industries Ltd in 1978 starting out as an import business for bagged cement and other commodities including rice, sugar, flour, salt and fish (Salihu, 2023, 2025). Dangote moved into cement manufacturing when the government privatised the Benue Cement Company in 2000 (Akinyoade and Uche, 2018) and later expanded its manufacturing interests in a range of consumer goods such as salt, sugar, tomato paste, seasoning as well as more recently petro-chemicals (fertiliser and refined petroleum). Dangote’s closest competitor, the BUA Group, which operates in many of the same manufacturing sectors, is led by Abdulsamad Rabiu, also a descendant of a prominent merchant who benefited from the initial phase of ISI.

The Nigerian cement market is effectively dominated by Dangote cement with a market share around 60%, with the other two major producers BUA and Lafarge trailing with 24% and 23%, respectively. Dangote and BUA are the main conglomerates competing in the production of not only cement but also sugar, salt and food processing. However, in most of the markets for these commodities Dangote is often the first-mover with BUA following suit and providing some competition to Dangote, even if as a distant second, as it was the case in the cement market. Other conglomerates mostly owned by businesspersons of Asian descent also do exist such as those of Chief H. B. Chanrai and Mr Gilbert Chagoury. SaroAfrica International, founded by Rasheed Sarumi has business interests in agro-chemicals, consumer goods and commodity trade. However, these conglomerates – which mainly deal in real estate, textiles, insurance, hotels, furniture etc – are of relatively lesser business scope and reach compared to Dangote.

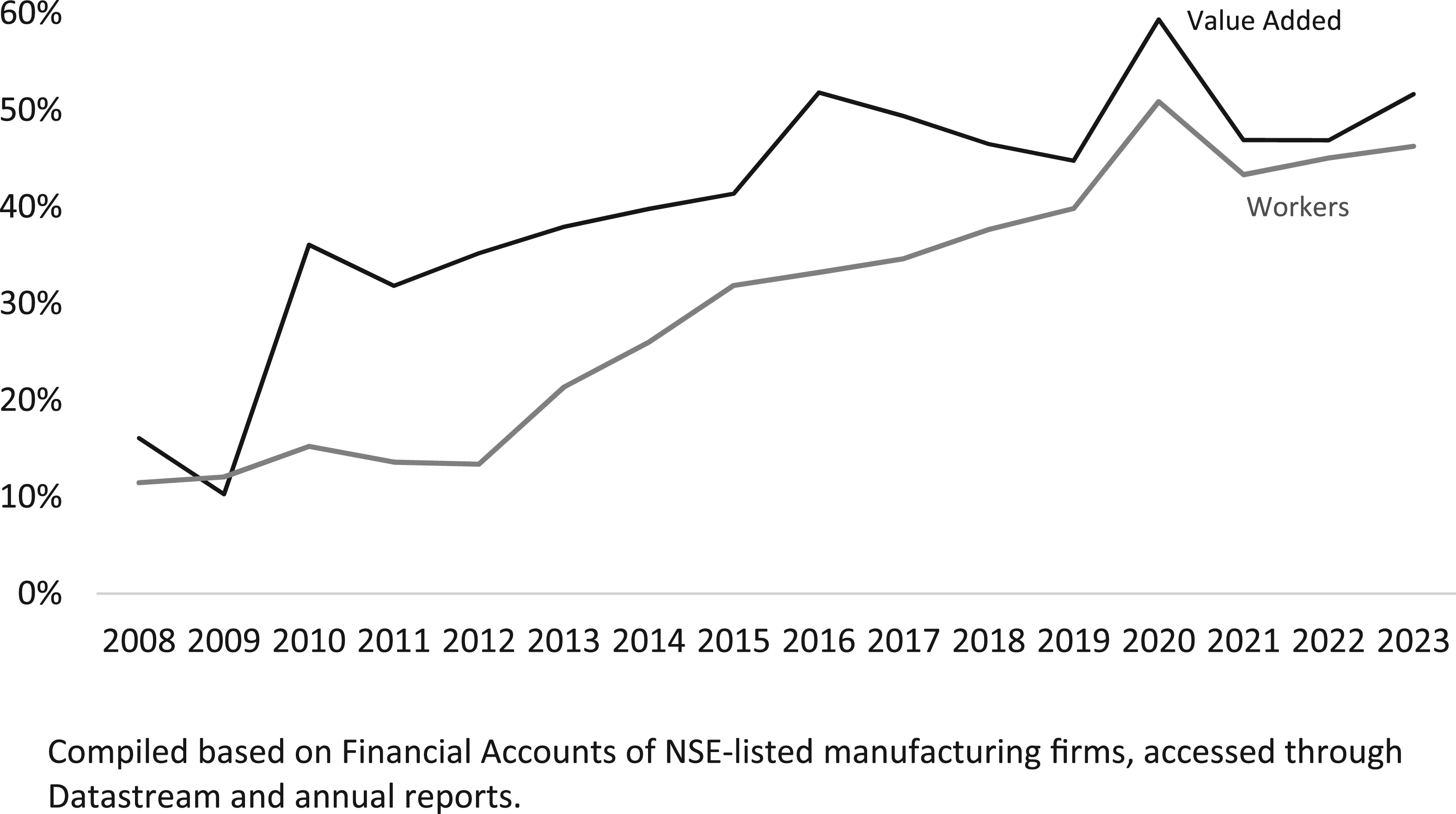

The Nigerian manufacturing sector is becoming increasingly monopolised, with a growing share of value-added and employment concentrated in a handful of dominant conglomerates. Among the 44 manufacturing companies listed in the Nigerian Stock Exchange (NSE) in 2023, three belong to the Dangote conglomerate (Dangote Cement, Dangote Sugar and Nascon) and two belong to the BUA conglomerate (BUA Cement and BUA Food). Saroafrica International has recently acquired the listed Presco Plc, the country’s biggest fully integrated agro-industrial palm processor.

The financial accounts data from the NSE-listed manufacturing firms reveals the growing dominance of individual firms, especially the Dangote business. As shown in Figure 1, the share of total value-added generated by the three Dangote companies rose from 16% in 2008 to over 51% in 2023. Similarly, by 2023, the Dangote Group accounted for 46% of all manufacturing employment among NSE-listed firms. This concentration signals a structural shift towards market dominance by a few conglomerates. NSE-listed Dangote Businesses: Value-added and number of workers as share of total NSE-listed manufacturing firms.

Spread-effects: The market-creating effects of Nigeria’s industrial conglomerates

Spread-effects: Market creation and capacity development

Interviews with stakeholders (n = 15) ranging from floor workers and top management staff at Dangote and other companies, to members of host communities, public affairs analysts and government officials have acknowledged the existence of spread effects from activities of the Dangote’s conglomerate, including market creation, capacity development and cost savings for other firms. First, the activities of the different Dangote businesses act as a market-creating force across different parts of the Nigerian economy supporting backward production linkages in mining, construction, agriculture and the chemical industry including petroleum recently. Dangote Cement sources a substantial portion of its limestone and gypsum, primary raw materials for cement production, from local quarries within Nigeria when available (Awofadeji, 2024; Salihu, 2025). Similarly, Dangote Fertilizer sources phosphate and limestone from local mines thereby supporting local mining activities. During the construction of the Dangote Refinery, one of the largest single-train refineries in the world, the company has engaged numerous local contractors and suppliers for materials like sand, gravel, steel, and other construction inputs, thereby increasing demand in the local construction and engineering sectors (Ojoye, 2019). In fact, Sunday Esan of the Dangote Group stated that Dangote Petroleum Refinery (DPR) saves Nigeria over ₦10 billion a year in foreign exchange by replacing fuel imports with locally refined products (The Cable, 2025). Asked about the importance of the DPR to the Nigerian economy, a public affairs analyst remarked thus: ‘For the first time in over two decades, Nigeria is refining fuel at scale. This has reduced imports, eased pressure on our forex [foreign exchange], and strengthened our energy security. It’s also creating jobs and giving the country greater confidence in its industrial capacity’ (Interview 15, 2026).

Also, a respondent at Obajana where Dangote’s biggest cement factory is located also observed positive effects on the productive ecosystem through wider consumption linkages: ‘The factory has created a lot of jobs here [at Obajana]. You can see the shops, restaurants and businesses that have sprung up here. This place wasn’t this lively before [the company started operation]’ (Interviewee 1, 2021). Another respondent (Interviewee 2, 2022), who is a lecturer at Federal University Lokoja, stated that Dangote also contributed in that it pays taxes to both the state and Federal government.

The Dangote Sugar Refinery engages with local sugarcane farmers for the supply of raw sugarcane thereby building a stable market for local farmers (Odijie, 2024). As part of its backward integration policy, Dangote Sugar has invested in large-scale sugarcane plantations and mills in various states across Nigeria, such as Nasarawa and Adamawa. These projects are aimed at sourcing raw materials domestically (Adenubi, 2021). A Senior Manager at Dangote’s company, Gwom (Interviewee 6, 2021) posited that people can ‘call oga [Dangote] what they want, a monopolist or whatever, but no businessman has contributed to the Nigerian economy in terms of investment in the manufacturing sector, jobs creation, and overall contribution to GDP like him! But you know, a prophet is not respected by his own people, so this is how I view all this criticism about monopoly and lack of community development’

Second, the activities of the Dangote Group support capacity development, especially in agriculture. Dangote Fertilizer works with farmer associations, corporate farms, NPK blenders, NGOs/development partners and government agencies across Nigeria and beyond Interview 12. The Dangote Group supports local farmers through outgrower schemes, a model which has been used in rice and tomato farming as well as in sugar cane production (Wada and Gbabo, 2019). Dangote Sugar Refinery has implemented outgrower schemes where smallholder farmers are provided with essential inputs such as high-yield sugarcane varieties, fertilisers, and technical support (Plaisier et al., 2019). The company then buys back the harvested sugarcane for processing. Dangote has embarked on rice cultivation projects that involve smallholder farmers under an outgrower scheme (Johnson and Masias, 2017). The company provides inputs such as seeds, fertilisers, and technical know-how. Dangote Tomato Processing Factory, located in Kano, engages local smallholder farmers to supply tomatoes. Farmers receive seedlings, fertilisers, and training on best agricultural practices. As at 2017, the factory which started in 2016 had engaged over 5000 farmers (Unah, 2021).

When in October 2022, the Kogi State government sealed off Dangote’s Obajana cement company as part of investigations on the circumstances surrounding the company’s acquisition by Dangote from the state government in 2002, locals at the mining communities of Oyo and Iwaa took sides with the company. In an interview (Interview 3 and Oluruntoba, 2022), Mr David Oluruntoba, spokesman for the Oyo mining host community remarked thus: ‘They [state-sponsored vigilantes] called us to join them. But I told them that the company has not offended us. We just signed a Community Development Agreement (CDA) and the company has been helping us and providing us with jobs. What has the government done for us, nothing. There is no basis to support the government’.

In a similar statement, Rotimi Kekereowo, the spokesperson for the Iwaa mining community, also expressed that they would not support the government on this issue, noting that ‘[E]ven when we have problems of electricity and flooding, it was Dangote that was helping us. So, I want to repeat it. We will never support them’ (Interview 4 and Kekereowo, 2002).

In another interview (Interviewee 5, 2024), a public affairs analyst, Mr Rabiu Isa, also observed the contribution of the Dangote Academy in terms of the provision of technical and vocational skills and training to Nigerians especially in communities hosting Dangote’s companies. However, the analyst added that, ‘this is seen by many as a strategy of buying up disgruntled youths in [Dangote companies’] host communities’.

Limitations to spread-effects: Stagnating markets, capacity constraints in backwardly linked sectors and power-imbalances

On balance, the spread-effects emanating from the Nigerian conglomerates have remained limited. Indeed, the manufacturing transition in Nigeria is considerably less dynamic than that historically observed in East-Asia. First, whilst Nigeria’s conglomerates and Dangote specifically, increase demand in backwardly linked sectors, the overall size of the Nigerian market remains limited, and the activities of the conglomerates have compounded these effects. Nigerian consumer goods producers have struggled under the impact of the 2015 commodity price shock, which led to inflationary pressures that severely limited consumer’s purchasing power. Macro-level distributional policies did not cushion against such uneven distributional effects of inflation. Neither wages nor daily expenditure of the lowest two income deciles have increased substantially since 2010. The wage share in Nigeria is low by absolute standards and has stagnated between 25% and 28% since 2009. Similarly, the daily expenditure that marks the cut-off point of the bottom 20% of the income distribution has barely increased since 2010. Distributional dynamics in NSE-listed firms are symptomatic for this trend and reinforce it, with limited demand multipliers emanating from the most dynamically expanding conglomerates. The three listed subsidiaries of the Dangote Industries (Dangote Cement, Dangote Sugar and Nascon) employed 51% of all workers employed in NSE-listed firms, but paid less than one third of all wages in 2020 (Wolf, 2023b). Such stagnating markets leave less space for the simultaneous expansion of competitors making it more likely for incumbents to use their first-mover advantages in predatory ways.

Second, backwardly linked sectors, particularly smallholder farmers accounting for the vast majority of agricultural production, face significant supply constraints. Consequently, the market-creating forces driven by Nigerian conglomerates are often redirected toward imports. Agricultural policies have not sufficiently addressed these supply limitations. Under the Buhari administration, agricultural policy primarily relied on trade measures and financial access initiatives. For instance, to support domestic rice production, the government imposed high import tariffs (and later a ban), restricted foreign exchange for rice imports, mandated banks to raise their loan-to-deposit ratios to 60% to encourage lending, and established credit facilities for smallholder farmers through the central bank (Nwuneli, 2019; Smith, 2019). However, these measures failed to tackle critical supply constraints faced by smallholders, such as inadequate rural roads, seeds, fertilisers, and irrigation systems. Support schemes like the central bank’s credit facilities often fail to reach their intended beneficiaries due to poor communication, leading to inconsistent registration and limited coverage, ultimately rendering these initiatives largely ineffective (Karkare et al., 2022; Nwuneli, 2019).

Third, the power dynamics between Dangote and its suppliers are highly unequal, with several instances of alleged contract breaches by Dangote companies going unprosecuted. Notable examples include the case of Plexus Cotton and several mining-related disputes. In 1996, Dangote Farms entered an agreement with Plexus Cotton, an agricultural produce supplier and trading platform, to deliver 3700 metric tonnes of raw cotton. However, Dangote Farms allegedly breached the contract, supplying only 1450 metric tonnes. In response, Plexus Cotton initiated arbitration proceedings in 1998, resulting in an award of $431,000 in compensation for the undelivered supply, plus an 8% interest rate. According to High Court of Lagos State documents (Plexus Cotton Limited V. Dangote Farms Limited, 2023), Dangote Farms wilfully ignored multiple invitations to arbitration and as of April 30, 2023, the accrued principal and interest had grown to approximately $2.3 million, a sum that continues to increase. The court documents also revealed that Dangote Farms’ refusal to settle the debt has caused significant financial hardship to Plexus Cotton.

In another case before the Federal High Court in Lokoja, the mining company Quest Two Enterprises Limited sued Dangote Cement Plc, Obajana Cement Plc, and Dangote Industries Plc for breach of contract. The court awarded Quest Two Enterprises N2.7 billion for breach of contract, special damages, and specific performance related to two memoranda of understanding signed in January and February 2014 (Onyekwere, 2017).

Dangote Coalmine’s operations in Kogi State illustrate the conglomerate’s structural power and regulatory impunity. Despite documented violations of the Nigerian Minerals and Mining Act (2007) – including water contamination linked to miscarriages, health issues, and the displacement of local residents, no prosecutions have followed. While some in Obajana recognise the benefits of the Dangote cement factory, others report severe environmental harm. As one respondent put it: ‘The company has been polluting [the] environment and our people are dying from diseases associated with the dust that is spread all over here’ (Interviewee 2, 2022).

Backwash-effects: The polarising forces of big businesses in Nigeria and how large-firm dominance is sustained in the Nigerian context

Beyond the limited spread effects, the expansion of Nigeria’s large conglomerates has produced significant backwash effects, where the growth of dominant first-movers has created structural disadvantages for smaller firms and late entrants. In the salt sector, firms like Union Dicon Salt and Royal Salt Ltd have steadily lost market share, unable to match the scale and reach of Dangote’s Nascon. By 2023, Union Dicon employed just 26 workers, compared to Nascon’s 673. Similarly, in the sugar sector, smaller producers such as Sunti Golden Sugar (owned by Flour Mills of Nigeria) have struggled to compete on pricing and distribution, resulting in financial strain and declining profitability. These patterns illustrate how the dominance of large conglomerates can suppress competition and undermine broader industrial development.

Backwash effect through leverage of economies of scale and scope

Some of the ways in which Dangote firms sustain their dominant position stem directly from their first-mover advantages and ability to internalise economies of scale and scope. Dangote’s ability to invest in large-scale production facilities allows it to achieve economies of scale that smaller competitors cannot match. This advantage can drive down production costs significantly, enabling Dangote to offer lower prices and capture greater market share (Itaman and Wolf, 2021).

Dangote Cement, for instance, operates production lines of either 1.5Mta or 3Mta, significantly bigger than the global average of 1Mta (Dangote Cement, 2016: 28), which sustains various efficiency gains including cheaper commissioning of factories and the ability to use more energy efficient technologies (Itaman and Wolf, 2021). Dangote’s extensive vertical integration, from raw material extraction to finished product manufacturing, gives it substantial control over supply chains. This control can limit competitors’ access to essential inputs, forcing them to purchase at higher prices or from less reliable sources. In 2017, for instance, Dangote Cement started sourcing coal mined in Kogi state by their parent company (DIL), providing Dangote Cement with a significant advantage over competitors who must source limestone externally (Dangote Cement, 2016: 9 and 28).

Another dimension of Dangote’s dominance is the control over distribution networks, a critical component in industries like salt, cement, and sugar. Dangote has invested heavily in its logistics and distribution networks, including owning fleets of trucks and building extensive infrastructure. This investment provides a competitive advantage in terms of distribution efficiency and cost (Dangote Industries Limited, 2024), making it difficult for smaller competitors to match. SMEs that rely on these networks find themselves excluded as Dangote exercises significant influence over distribution channels, often through exclusive contracts that cut-off market access for competitors. As a small salt producer explained: ‘We’ve faced direct pressure from distributors to exit the market. Distributors are coerced or given huge “incentives” into exclusive contracts with Dangote, cutting off smaller players like us. It is very costlier and more difficult to get our products to market because Dangote controls the supply chain’ (Interview 11, 2024).

This statement reveals the vertical integration Dangote employs, where its control extends beyond production into distribution, creating additional barriers for smaller competitors. Dangote’s monopolisation of production and distribution makes it difficult for smaller competitors to reach consumers or build sustainable business models, thus effectively shutting them out of the market. In the oil refining industry, the Dangote Petroleum Refinery (DPR) initially faced a distribution network that he neither owned nor controlled. This was swiftly changed when DPR purchased 4000 compressed natural gas-powered trucks at the cost of N720 billion (Dangote Industries Limited, 2025).

Similarly, smaller businesses often struggle to compete with Dangote Group’s ability to secure large-scale financing at favourable terms. Dangote’s established relationships with banks and financial institutions enable it to obtain capital more easily and at lower interest rates, giving it a significant advantage over smaller competitors that face higher borrowing costs and stricter lending conditions (Emejo, 2023).

Backwash effects through predatory pricing

Beyond these competitive advantages that are directly linked to Dangote’s ability to internalise the gains from IRS, Dangote also sustains its dominant market position with rentierist practices, including predatory pricing, regulatory influence and strategic acquisitions. A recurring theme throughout the interviews conducted with entrepreneurs, analysts, government officials, and industry experts is the significant market power Dangote wields, allowing the conglomerate to engage in aggressive tactics such as predatory pricing, coercion (via state agents or local vigilante groups), and strategic acquisition. These strategies have detrimental impacts on the survival and growth of SMEs and smaller competitors.

One of the most pressing issues raised by interviewees was the use of predatory pricing by the Dangote Group, which involves lowering prices to unsustainable levels to drive competitors out of the market. This practice was frequently cited as a major threat to the survival of competitors across different sectors like cement, sugar and salt. For instance, a CEO of a small cement company described the challenge of competing with Dangote: ‘The Dangote Group has drastically undercut our prices. We can’t compete with their economies of scale and massive distribution networks. Our margins are shrinking by the day’ (Interview 7, 2024).

This statement highlights the inability of smaller firms to match the low prices Dangote can afford due to its large-scale operations and efficient production capabilities. SMEs, with their limited resources, find it difficult to survive in such an environment, as they lack the necessary scale to compete on price alone. But even Dangote’s larger competitors like the BUA Group struggle under Dangote’s predatory pricing strategies (Ubochioma, 2021). Economies of scale realised by the Dangote firms enable them to reduce costs in any of the industries they operate in, which it can pass on to consumers through lower prices. However, these pricing strategies are predatory in nature aiming at pushing competitors out of the market, as highlighted by this analyst: ‘The Dangote Group has become a market giant in sectors like cement, sugar, and salt. While this has benefits, such as increased local production, it has negative consequences too. The company’s dominance enables them to engage in practices that can stifle competition. Their control over pricing often leads to price manipulation, where they can afford to lower prices temporarily, driving out competition, and then raise prices once they're the sole player’ (Interviewee 8, 2024).

Price wars between the Dangote refinery and the state-owned oil company NNPC has also been raging from the late 2025 to date (The Africa Report, 2026). In fact, Dangote Refinery filed a lawsuit (which it later withdrew in July 2025) against Nigeria’s midstream and downstream petroleum regulator and several fuel importers, including state-owned NNPC Ltd, over fuel imports (Reuters, 2025). In fact, in the suit, Dangote had not only sought to nullify fuel import licences issued to NNPC Ltd, AYM Shafa Ltd, A.A. Rano Ltd, T. Time Petroleum Ltd, 2015 Petroleum Ltd, and Matrix Petroleum Services Ltd, but also sought 100 billion naira ($66 million) in damages (ibid).

In addition to predatory pricing, the interviews revealed that the fear of litigation and other aggressive tactics further discourages SMEs from entering markets where Dangote is a dominant player. Many members of the Manufacturers’ Association of Nigeria (MAN) expressed concerns about the use of litigations to intimidate smaller companies and prevent them from competing. One entrepreneur from an agro-allied company reflected on this dynamic, stating: ‘We were planning to enter the sugar and cement market, but after witnessing the aggressive tactics used by the Dangote Group against Clestus Ibeto and even his own brother Abdussamad [Isyaka Rabiu], we reconsidered our stand. The fear of being crushed by their massive resources and legal actions is real. We’ve seen his [Dangote’s] competitors getting entangled in long, costly litigations that they can’t afford’ (Interview 9, 2024).

This quote illustrates how the mere prospect of competing with Dangote dissuades potential entrants from even attempting to enter certain industries. The legal intimidation strategies employed by Dangote further solidify its market dominance, as SMEs often lack the financial capacity to engage in drawn-out legal battles, forcing them to either settle or exit the market altogether.

In fact, the threat of litigation is not just theoretical for many SMEs. A source close to a famous Nigerian industrialist recounted their own experience with Dangote’s legal machinery: ‘Litigations are another tool used by large companies like Dangote to suppress competition. We faced a lawsuits form mining rights infringement, which was completely unjustified but drained our resources for months. It’s hard to compete when you’re fighting a legal battle with a behemoth like Dangote’ (Interview 10, 2024).

This strategic use of the legal system as a coercive tool demonstrates the power asymmetry between a massive conglomerate like Dangote and smaller players, making it nearly impossible for SMEs to thrive in industries where Dangote operates.

Backwash effects through regulatory influence: Dangote’s preferential access to government incentives and foreign exchange

Several analysts and industry experts also pointed to an institutional bias in favour of large corporations, which are often seen as drivers of industrialisation and economic growth, as highlighted by this economic policy expert: ‘The Nigerian market is structured in a way that favours large conglomerates. Dangote, in particular, has benefited from favourable government policies, access to credit or subsidized forex, and sometimes tariff exemptions that smaller businesses don’t enjoy. This creates an uneven playing field, making it difficult for SMEs to grow’ (Interviewee 5, 2024).

For example, 52 companies, including the Dangote Group, have benefited from preferential access to foreign exchange at favourable rates from the Central Bank of Nigeria (CBN) (Salihu, 2025). This advantage enables these companies to import raw materials and equipment at significantly lower costs than competitors who must acquire foreign exchange at higher rates from the open market. This practice creates an uneven playing field, particularly in sectors heavily reliant on imports (Adeoye and Pilling, 2024).

Among large companies, there is a bias of regulatory authorities in favour of the Dangote conglomerate. 3 Apart from first-mover advantages and possession of huge investable capital, Dangote has, leveraging his family connection, deployed the rents he extracts from the cement and other sectors/businesses to establish extensive networks of influence through political financing, co-optation and other means, enabling him to wield enormous influence to be able to successfully support, distort or block policies (un)favourable to him. For instance, acting upon a petition by Dangote alleging the violations of the BIP by one of his then cement importer competitor, Cletus Ibeto, the Federal Government under Obasanjo swiftly moved in to seal off Ibeto’s Port Harcourt cement bagging warehouses in November 2005. Initially, Ibeto thought this was a minor communication gap that would soon be sorted out upon his reaching out to government officials, but this was not so, as the Obasanjo government locked up his warehouses till the end of its tenure and handing over of power to the new Yar Adua administration in 2007 (Salihu, 2025).

In 2020, BUA Cement accused Dangote Cement of influencing regulatory authorities to delay the commissioning of BUA’s new cement plant in Sokoto. BUA claimed this was an attempt by Dangote to maintain its dominance in the northern Nigerian cement market (Mbachu, 2023). In 2021, the BUA Group accused Dangote Sugar of attempting to manipulate the sugar market by leveraging its influence to secure government policies favourable to its interests. Specifically, BUA alleged that Dangote Sugar was pushing for higher import tariffs and restrictive import quotas on raw sugar, which would raise costs for competitors reliant on imported raw materials. BUA also claimed that Dangote Sugar colluded with Flour Mills of Nigeria to influence sugar import quotas and tariffs, seeking higher quotas for themselves while limiting BUA’s imports. The regulatory bias in favour of the Dangote Group becomes evident when considering the lack of any investigation by the Federal Competition and Consumer Protection Commission (FCCPC) into allegations of price fixing raised by the BUA Group. Instead, the Dangote Group leveraged its influence to redirect attention by petitioning the Minister of Trade and Investment, accusing the BUA Group of violating the National Sugar Master Plan (NSMP) by selling products locally rather than exporting them (Ubochioma, 2021).

More generally, Odijie and Onofua (2020) have highlighted Dangote’s ability to co-opt opposition groups and rivalling civil society groups to guarantee the continuation of industrial policy, of which the Dangote group was the main beneficiary. While government officials acknowledge the negative impacts of Dangote’s dominance on SMEs and larger competitors, they are often caught in a dilemma. A senior official from the Ministry of Trade and Investment remarked: ‘Dangote has contributed significantly to Nigeria’s industrialisation, but the government is aware of concerns about its dominance. We are considering policies that could ensure a more level playing field, especially for SMEs. It’s important that we support small businesses while also encouraging large investments. However, it’s a balancing act, and Dangote’s role in economic growth cannot be ignored’ (Interview 13, 2024).

This reflects the policy challenges that governments face when dealing with large corporations that are key to national industrialisation efforts. While conglomerates like Dangote are crucial for reducing import dependence and driving local production, their unchecked dominance raises questions about long-term economic growth, competition and consumer welfare.

Backwash-effects through hostile take-overs/strategic acquisition

Finally, several interviewees (Interviews 2, 5, 11 and 14) pointed to strategic acquisitions as key tactics Dangote employs to maintain market dominance. While there are instances in which Dangote has used acquisitions to strategically strengthen and expand core technological competences as in the case of the acquisition of Twister B.V. – a Dutch engineering company that specialises in advanced gas processing technologies (Africa News, 2019), entrepreneurs and analysts alike emphasised how the conglomerate seeks to neutralise potential competitors by either acquiring them outright or using aggressive takeover strategies. An industrialist in the cement sector detailed how Dangote’s acquisition of a key competitor disrupted the industry: ‘When Dangote acquired Benue Cement, it wasn’t just about expanding capacity – it was a calculated move to eliminate a strong competitor. With Benue Cement gone, many other smaller players simply couldn’t sustain themselves in the face of such overwhelming market consolidation’ (Interview 14, 2024).

Another interviewee who is an entrepreneur in the sugar industry reinforced this view, highlighting how Dangote’s acquisition of competitors served to pre-emptively curtail any potential threats to its market share: ‘We heard rumours that Dangote was eyeing our company. They had already taken over several medium-sized sugar producers, and we feared we might be next. It’s not about growing the industry – it’s about making sure no one else grows’.

However, despite Dangote’s dominance in the Nigerian manufacturing sector, vested interests remain strong around refined petroleum production/imports making Dangote’s advance into petroleum processing uniquely challenging. Despite Dangote wielding disproportionate market power and dominating supply in the manufacturing sub-sectors he operates in through first-mover advantage, low competition, access to huge investable capital and political connection, the recent challenges faced in the petroleum industry reveal that these factors which drive his success in the manufacturing industry can be met with tensions from powerful interests in other sectors. Competition policies, intended to mediate these tensions are rendered ineffective as they are often captured by the most powerful interests, ultimately becoming instruments for political settlements.

Conclusion

This article explored the phenomenon of ‘size failure’ within Nigeria’s industrial ecosystem, focussing on the role of large domestic conglomerates and their implications for the productive ecosystem. The renewal of industrial policy measures in the early 2000s, set against the backdrop of rapidly expanding markets for construction materials, facilitated the rise of dominant players such as Dangote. These firms have achieved notable productivity gains and market dominance through economies of scale and scope. Historically, such large firms have been central in driving structural transformation, as evidenced by the role played by large conglomerates in East Asia. Yet in Nigeria, their success at the firm level has not translated into broad-based industrial development. The article therefore set out to understand why large, domestically owned industrial conglomerates failed to drive broader industrial transformation in Nigeria, despite their own scale and entrepreneurial success.

While scholarship on DBGs explicitly incorporates the scale and scope of production, and their relationality to the state and to rival firms, it pays little attention to how DBGs structure supplier, complementor, and ecosystem-wide capability trajectories. Consequently, DBGs are typically analysed either as efficient internal markets or as politically connected competitors, rather than as actors that actively coordinate – or distort – broader productive ecosystems. We mobilised Myrdal’s framework of backwash and spread effects to demonstrate how accumulation regimes based on increasing returns to scale can create both opportunities and distortions in industrial ecosystems of late-industrialising economies. While Myrdal developed this framework to explain regional disparities, we extended it to the inter-firm level, arguing that increasing returns to scale produce ecosystem-level effects that require active governance. This lens helps explain why large firms, despite their potential, may ultimately fail to catalyse broader structural transformation in the absence of deliberate governance of scale-related power dynamics.

Nigeria’s industrial conglomerates have produced modest spread effects. Whilst there are some spread effects that could support growth of complementor and supplier firms, including through local sourcing, and capacity development through outgrower schemes, the expansion of Nigeria’s conglomerates has not led to widespread benefits for the productive ecosystem, failing to generate the positive externalities observed in East Asia.

Instead, backwash effects, characterised by the monopolisation and dominance of first-movers, have prevailed. Large conglomerates, foremost the Dangote Group, have employed monopolistic practices, including predatory pricing, strategic acquisitions, and regulatory capture, to consolidate their market position. These practices have marginalised smaller firms, restricted competition, and suppressed the dynamism of Nigeria’s industrial sector. Consequently, the industrial landscape has become increasingly concentrated, with limited opportunities for new entrants and smaller players.

The dominance of backwash over spread-effects is due to the political structuring of IRS gains, which favoured old economic elites rooted in the colonial era and before; the stagnation of market growth, which left less room for the simultaneous expansion of competing firms and increased the reliance on rent-seeking by incumbents; and the lack of adequate support for capacity development in backwardly linked industries.

By reframing DBGs as ecosystem coordinators whose developmental role can be assessed through backwash and spread-effects, the article opens up new avenues for comparative and theoretical research on late industrialisation including in the African context. Our findings suggest that industrial policy needs to not only support firm-level capability, but also actively govern the ecosystemic dynamics of accumulation by amplifying spread effects while constraining backwash effects.

This involves actively managing inter-firm relations, power asymmetries, and learning opportunities across productive ecosystems. First, industrial incentives should be conditioned on ecosystem-level outcomes, not firm size or investment scale alone. Access to protection, finance, or other rents should be linked to demonstrable spillovers, such as supplier upgrading, skills development, and fair contracting practices, rather than assumed to follow automatically from large-firm expansion. Second, competition policy needs to address ecosystem power, not only market rivalry. This requires closer scrutiny of exclusionary practices, strategic acquisitions, and control over distribution and input access that allow dominant firms to crowd out rivals or subordinate suppliers, even in the absence of overt monopoly pricing. Third, policy should directly support suppliers and complementors, recognising persistent power asymmetries within productive ecosystems. Targeted capability-building programmes, shared infrastructure, and credible mechanisms for contract enforcement are essential to enable smaller firms to participate in learning and upgrading. Finally, governing scale requires sustaining market growth and demand multipliers. Wage, procurement, and sectoral policies that expand domestic demand and allow parallel firm expansion reduce the tendency for increasing returns to translate into zero-sum dominance.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.