Abstract

Compared to other countries, little has been written about the accounting history of Cyprus. This omission is surprising given the rich history of the island, today a Commonwealth and European Union member, with its own local accountancy body. This article aims to partly fill this vacuum. Despite Cyprus’s links to both Greece and Turkey, it was the experience of British rule that significantly influenced the development of accounting practice in Cyprus. Consequently, this article concentrates on the four decades immediately after the First World War until Cypriot independence in 1960, since this is the era in which the most notable developments in accounting practice occurred. This article traces these developments and their significant influences during that period. Like other country studies on the history of accounting, this article argues that the development of accounting evolved over time in response to the contingent political, economic, institutional and social factors, both at domestic and at international level.

Introduction

Compared to other developed and English-speaking countries little has been written about accounting history in Cyprus. This lack of attention is curious given the rich history of the island, in which the first signs of civilisation and commercial activity date back to the ninth millennium BC. At the time of writing, only two articles of relevance have been published (in English) relating specifically to accounting history in Cyprus. Recently, Clarke (2011) provided an overview of some of the main accounting changes but his article covered a lengthy period rather than focusing on a specific era. Previously, Walton (1986) described the export of British accounting legislation to a few Commonwealth countries, one of which was Cyprus, which in 1951 adopted, with minor amendments, the British Companies Act 1948. Furthermore, Cyprus was omitted from the recent and influential work edited by Poullaos and Sian (2010) on the development of the accountancy profession in key constituent territories of the British Empire, including Australia, Canada, South Africa, India, Sri Lanka, Malaysia, Jamaica, Trinidad and Tobago, Nigeria and Kenya. This study examined the formation, training and collective organisation of accounting practitioners into occupational groupings which are socially accepted as ‘professionals’. However, it should be acknowledged that the accountancy profession in Cyprus – if assumed to equate with the formation of a local, professional accountancy body in 1961 – is a relative newcomer.

This article highlights the circumstances and events which influenced the development of accounting practice in Cyprus immediately after World War I through to independence in 1960: a period corresponding, approximately, to the four decades of colonial status. Initially, to provide a backdrop, we identify aspects of the Ottoman Commercial Code, which was the prevailing commercial legislation in Cyprus prior to British administration. The early years of British administration that followed after 1878 promoted a growing awareness that book-keeping and other commercial skills, together with a knowledge of the English language, became an important source of ‘social mobility’ for the local population. The years that followed, and especially when colonial status was achieved, were characterised by commercial reforms and legislation relating to, inter alia, companies and income tax. Such legislation encouraged the development of broader accounting skills, including the preparation of financial statements, which were augmented by the need for qualified accountants as required by company legislation in 1951. By the mid-1950s, which also corresponded to the struggle for Cypriot independence, a small number of qualified accounting professionals worked on the island and they were instrumental in forming the local accountancy body. However, this article is not intended to be construed as a history of the accountancy profession in Cyprus since the precise meaning of the term ‘accountancy profession’ is debatable, especially in regard to the nature of the activities involved and the enforcement of regulations. However, it will refer to the formation of a local accountancy body in 1961, after independence was achieved.

Designing an accounting history research proposal requires identifying the appropriate conceptual framework to be used. Over the years various researchers have adopted different approaches to investigating accounting history, and, perhaps understandably, there is no consensus among historians regarding which approach is the most appropriate. For example, Napier (1989) and Loft (1995) provide different summaries of “distinctive lenses” which could be used, although Napier’s article relates to accounting research in general whereas Loft specifically focuses on researching the history of management accounting and its role within organisations. Napier (1989) suggested three approaches, namely, understanding the past, the locating of accounting in its socio-historical context, and the new positivism, but he stresses that these approaches are “interrelated but are not intended to be exhaustive” (Napier, 1989: 239). Loft (1995) suggests five approaches, namely: the traditional historians, the neo-classicalists, the Johnson and Kaplan approach and the new accounting history studies influenced by Foucault (the power-knowledge approach) and Latour (labour process theory). For the purposes of this article the eight approaches outlined by Napier and Loft can be divided into two different frameworks, namely the traditional/technical and the new accounting history approaches. 1 Napier (1989) acknowledges that much useful work in accounting history has been done, and continues to be done (at his time of writing) under the primary motivation of understanding the past, which, in many cases, emphasises the study of original accounting records. This approach has many similarities with Loft’s “traditional” and “neo-classical” approaches with their heavy emphasis on technical elaboration and subsequent revisions to previous research. (For the convenience of this article, one could also add Loft’s “Johnson and Kaplan” approach to this category, since it has a technical orientation. However, Napier (1989: 239) points out that this approach may suffer from the “danger of premature generalisations” which could potentially lead to deceptive conclusions.) The traditional approach to studying accounting history was subject to severe criticism from the late Professor Anthony Hopwood (1983, 1987), who argued that we must study accounting not as a technique practised in isolation, but in its social and organisational context. Thus, Hopwood was to the forefront of encouraging the contextualisation of accounting and the dynamics of accounting over time through a consideration of the preconditions for change, the underlying pressures and influences and the process of such change.

One of the main influences on these “contextualisers” of accounting history is the French philosopher Michel Foucault (1980) and his ideas of “governmentality”. While Foucault did not write on accounting matters per se, he argued that knowledge was power, and, therefore, accounting information can be instrumental in social control, as individuals control human behaviour and exercise power through knowledge. The power–knowledge relationship has been applied to interpreting accounting history (e.g., Miller and O’Leary, 1987) but the accounting history literature is not well developed in testing the “governmentality” perspective of Foucault to reveal the full capacity of accounting (Sánchez-Matamoros et al., 2005). In addition, the labour process theory of Latour (1987) depicts organisations as sites of persistent conflict and focuses on the micro variables of organisational control rather than the macro issues which impact on the development of general accounting practice. Likewise, while ‘institutional theory’ has been used in the field of social science and management, its main impact is located in the organisational studies area, but some contradictions are apparent (Scott, 2008).

Alternatively, management accounting researchers have (successfully) used the contingency theory as the appropriate framework in which to conduct organisational studies. As an organisational theory, it was popularised by Woodward (1965) and Lawrence and Lorsch (1967), but was not introduced into the accounting literature until the mid-1970s. At its simplest, the contingency theory of management accounting is based on the premise that there is no universally appropriate accounting system which applies equally to all organisations in all circumstances, but rather particular features of an appropriate accounting system will depend upon the specific circumstances in which an organisation finds itself (Otley, 1980). However, while based in organisational theory, a contingency approach was successfully used by Boyns and Edwards (2007) in considering factors that affected the development of business entities in Britain, together with their cost and management accounting systems and the changes to such systems over time. In a similar vein, Caramanis (1999, 2002) demonstrated that the structure of the statutory auditing profession in Greece – liberalised in 1992 – was the outcome of a dynamic interplay of economic, social and especially political forces at both the national and the international level.

Ultimately, the choice of a particular conceptual framework or ‘distinctive lens’ through which to view accounting developments over time is, itself, a subjective matter for the researcher. Some would therefore argue that the choice of such heuristics is more appropriate when the field of study is better explored and developed. However, a contingency-based framework is considered to be the most appropriate for the purpose of this pioneering article. We seek to identify, evaluate and interpret the relevant factors, circumstances and events which influenced the development of accounting in Cyprus during the period immediately after World War I through to independence in 1960 – a period corresponding to colonial status.

Based on the arguments of Zeff (1971) this article presents evidence and arguments that accounting practice in Cyprus, as a British colony, developed and adapted over time in response to a variety of political, economic, institutional and social factors. Thus, accounting practice is contextual, with the significant pressures and forces on the development of accounting being contingent on a particular set of circumstances and events that facilitate and require, as Hopwood (1987) has colourfully suggested, accounting becoming what it is not. However, there is always the risk that the resulting narrative reported by the accounting researcher, especially pioneering work, may be limited either because it is incomplete or distorted by personal judgement.

The structure of this article is as follows. In order to provide an important historical backdrop, the next section outlines features of Cypriot society and governance during late Ottoman rule and the transition to British rule after 1878. This is followed by a substantial section on British reforms and their impact post-World War I. Initially, we focus on the educational system in Cyprus at the start of the twentieth century and report how the knowledge of the English language, together with competency of bookkeeping under British rule, became an important source of ‘social mobility’ for the local population in a gradually evolving commercial environment. In turn, the additional interest in education and commercial matters was largely influenced by various legislative reforms introduced by the British to encourage the economic development of the island, partly to justify the British presence (especially in view of the 1915 offer to cede Cyprus to Greece) and also to alleviate Cypriot grievances. We also include a section on the rejection and subsequent introduction of income tax and, finally, a section on the (Cyprus) Companies Law, 1951 (modelled on the UK 1948 Act), which, inter alia, specified the required qualification of auditors and, thereby, granted privilege to those accountants who had qualified in the UK. This is followed by a short section on the formation of the local accountancy body, after independence, in 1961. However, efforts to form such a local accountancy body pre-dated independence in 1960, but were delayed by the violent emergency period between 1955 and 1959, characterised by a struggle for union with Greece (Enosis) 2 and the escalation of violence between the Greek and Turkish Cypriot communities. In chronological terms, it will be argued that the British reforms and influences (post-1878) were, initially, slow to come because of the “inconsequential” nature of Cyprus’s place within the British imperial system. Yet once they did come they stimulated the need for professionals in the areas of accounting, auditing and taxation services. In turn, and after independence, these professional accountants formed their own local accountancy body in 1961. The article ends with some concluding remarks.

Cypriot society and governance during late Ottoman and early British rule

After centuries of Latin rule (1191–1571), Cyprus came under Ottoman control in 1571 and some three centuries later Cyprus was transferred to British administration in 1878. Generally speaking, Ottoman rule was hardly the story of Turkish oppression of the Greeks, as some prominent Greek, Cypriot and western authors have had people believe. Rather, it was a period of domination by a Muslim and Christian ruling elite over a Christian and Muslim peasantry, until the Ottoman reforms of the mid-nineteenth century resulted in the challenge to this system by a rising professional and middle class (Katsiaounis, 1996; Varnava, 2009).

During Ottoman rule, the Cypriot ruling elite was composed of both Muslims and Christians, with the high clergy of the Eastern Orthodox Church having a great deal of power since the Orthodox Church had become the only recognised Christian authority on the island after the Ottoman defeat of the Catholic Venetian ruler in 1571. The Ottoman millet system, which allowed for religious and communal autonomy so long as millet leaders ensured the cooperation and loyalty of their people to the Ottoman central and local government, allowed the Cypriot archbishop to become the secular as well as spiritual leader of his flock. Within the context of this ‘contract’ the archbishop received power in exchange for guaranteeing the loyalty of his people, that is, the rest of the Christian inhabitants, largely composed of the agricultural and labouring class (Varnava, 2009).

Thus, when the British arrived to “occupy and administer” Cyprus in 1878 they did not find two distinct communities divided by racial, national or even religious differences. Although religious differences existed during Ottoman rule, they had not precluded political, social and even cultural integration, and therefore Cypriot society was divided along social/class lines rather than ethnic/racial lines. Under Ottoman rule the majority of the inhabitants of Cyprus comprised Christian and Muslim small landholders who either lived off their lands, laboured on other people’s lands, or did both in order to provide for their families. The agricultural and labouring classes shared economic and social hardships, brought on by droughts, bad harvests, locust plagues, and a lack of investment by government and private investors in industry and public works. This dynamic continued under British rule for at least four decades, since the British embarked on a limited modernisation process in Cyprus and the economy remained largely unchanged (Katsiaounis, 1996; Varnava, 2009).

The British administration of the island can be, formally, traced to the Anglo-Turkish Convention of 1878 whereby the British Conservative Government of Benjamin Disraeli agreed to “occupy and administer” Cyprus in return for offering protection to Turkey from expansionist Russian ambitions. The British, initially, considered Cyprus to have a very significant strategic, military and economic value in the Near and Middle East. However, the Liberal Opposition, and many military and strategic experts, as well as the realities on the ground proved otherwise, and the island became ‘inconsequential’ and eventually a pawn which the British Government attempted to give to Greece in 1915 in return for that country’s entry into the war (Varnava, 2005, 2009). The ‘inconsequential’ nature of Cyprus’s position within the British Empire meant a much slower pace of development of the island compared to what might have been had the island been of consequence. Yet, British rule, through the introduction of a legislative council in 1882 with a local majority, equality in the courts across the religious divide, the development of internal communications, improvements to sanitation and medical treatment, increased agricultural production and other reforms, created the right conditions for the population to grow (Varnava, 2009). The official census reports for 1881, 1891, 1901 and 1911 show a very significant increase in population, from 186,173, to 209,286, to 237,023 and 274,108 respectively (Cyprus Census, 1881, 1891, 1901 and 1911). The census reports identified people according to religion and according to the 1881 census, for example, 74 per cent of the population were Eastern Orthodox Christians, 24 per cent were Muslims, and the remainder comprised Maronites, Catholics and Armenian Christians. By the time of independence, these percentages had changed little (St John-Jones, 1983). The rise in population during the first four decades (1878–1918) of British rule resulted in the development of traditional occupations, such as agriculture, and the very limited emergence of new occupations associated with finance and business, such as brokers and clerks.

The existing commercial legislation on the island was the Ottoman Commercial Code which had been introduced in 1850 and contained some basic accounting provisions (Amirayan, 1906). Its introduction was part of the basic changes in the economic, administrative and social fabric of the Ottoman Empire since its administrators realised that, in order to compete with European rivals, it had to “Europeanise” or, as they put it, to reorganise (Tanzimat) their outdated management concepts (Quataert, 2000). The Commercial Code was based on the earlier Napoleonic commercial code which had been adopted in a number of European countries during the early nineteenth century (McLeay, 1999). The Commercial Code allowed for the formation of business partnerships, which could be created through registration with the Commercial Courts but it also permitted the formation of a corporation (Société Anonyme) but this could only be formed by prior Imperial Decree (Amirayan, 1906). Of course, this was a cumbersome and lengthy process and it also had the potential to fail. Not surprisingly, partnerships were established under the framework of the Code, including the steamship, travel and forwarding firm of Mantovani and Sons in 1856, the insurance company of Pierides in 1860, the banking agency Francoudi and Stephanou in 1895, and the import-export businesses of Lanitis & Co. and Dickram Ouzounian & Co., also in 1895, to name but a few examples (for advertising material related to these companies, see Keshishian (1951: 1, 10, 12, 249, 256)).

The British accepted the Ottoman legislation then in force, and there were initially very few major commercial developments, with commercial legislation being introduced as the need arose, such as with the introduction of a law permitting the formation of Co-operative Credit Societies in 1914. Two years previously, the Cypriot Government, after some reluctance, allowed the Nicosia Savings Bank to change its name to the Bank of Cyprus and its status into a Société Anonyme, because the initial constitution with unlimited liability was no longer suitable given its increased lending to persons who were not members (Phylaktis, 1988). However, notable reforms were to take place when Britain annexed the island in 1914.

Reforms in British Cyprus

In 1914 the Ottoman Empire entered the First World War on the side of the Central Powers, whereby Britain immediately annulled the Anglo-Turkish Convention and annexed the island on 5 November 1914. Subsequently, under the Treaty of Lausanne in 1923, the Republic of Turkey recognised British sovereignty over Cyprus, and the island became a Crown Colony in 1925. This meant that the British intended to stay in Cyprus, largely because of the perceived importance of the island in the Middle East to British imperialism, together with the uncertainties over the collapse of the Ottoman Empire. With the British deciding to stay, it also meant that reforms were needed to encourage the economic development of the island in order to justify the British presence (especially in light of the 1915 offer to cede it to Greece) and to alleviate Cypriot grievances, which Greek Cypriot political elites where trying to manipulate and capitalise on in the pursuit of their Enosis agenda (Georghallides, 1979). These reforms and changes had various impacts. We now discuss these changes under the following headings: (i) the growth in education; (ii) commercial legislation; (iii) the rejection and subsequent introduction of income tax; and (iv) the Companies Law, 1951. Finally, we briefly synthesise how these factors created a demand for professional accountants, which was filled mainly by Greek Cypriots who had trained in the UK and who were instrumental in forming their own professional accountancy body, after independence, in 1961.

The growth in education

As a practical discipline, the nature of accounting practice requires both general education and specific technical training. In 1905, after nearly three decades of British administration, it was noted that the Elementary Schools of Cyprus had made great strides since the days when a chaotic state of affairs prevailed around the late 1870s, as then evidenced by scarcely half of the children in the island receiving education (Board of Education, 1905). However, this same report commented that by 1900 commercial education had not progressed beyond the stage of suggestion, in contrast to Malta which taught the subject bookkeeping as part of the secondary (Lyceum) school curriculum. One report noted (Department of Registrar of Companies and Official Receiver, 1923) that the secondary schools were mainly classical in orientation and prepared their students for higher studies either in Constantinople or Athens, although it remarked that a large number of pupils did not proceed that far. Around that time, it is important to note that a knowledge of the English language became necessary for all those Cypriots who desired to be civil servants, or to be employed in the British military camps at Polymedia (in winter) and Troodos (in summer). Referring to commercial education, the same report (Department of Registrar of Companies and Official Receiver, 1923) noted the good ‘work’ of the American Academy at Larnaca (founded in 1908) and the Commercial Lyceum at Larnaca (founded in 1910), where special attention was paid in the curriculum of the Lyceum to languages and bookkeeping, and also the commercial school, founded in Lemythou in 1912 by D Mitsis. The English school in Nicosia was also important, because, as Sir Charles Orr (1918) claimed, this school taught modern languages and commercial subjects such as shorthand, typewriting and bookkeeping. Also the Turkish Lyceum in Nicosia provided a bookkeeping accounting curriculum and one of its graduates (c.1925), Nevvar Hickmet, was in all likelihood the first Cypriot to qualify as a Chartered Accountant, becoming a member of ICAEW in 1937 (The Accountant, 1937). It was recognised that a knowledge of bookkeeping and other commercial subjects, together with a good knowledge of the English language, was a necessary but not a sufficient condition for acquiring a secure job in government service. Under British rule, the numbers of students attending school in Cyprus were reported as increasing from 6,776 scholars in 1881 to 44,850 scholars in 1922 (Department of Registrar of Companies and Official Receiver, 1923).

The importance of being able to speak the English language, together with knowledge of bookkeeping skills and other commercial subjects, also fostered the development of private commercial colleges. One such institution, the Accounting School of Morphou, was founded in the mid-1930s and had about 50 students who studied a basic level of bookkeeping (Montis, 2010). The school was founded by Costas Sylvestros, who employed his brother-in-law, Costas Montis – one of the great Cypriot poets – as a teacher, but there is little data on this school. It is possible that the school was established, partly, because of its proximity to the Cyprus Mines Corporation, with its clerical employment possibilities in mind (Lavender, 1962). In subsequent years, another important educator was Kyziakas Neocleus, who subsequently founded a commercial institute in Nicosia in 1943 under his own name, as he recognised that there was a need for persons with knowledge of shorthand and typing and bookkeeping skills. Indeed, advertisements appeared regularly in the local newspapers for ‘Accounting Officers’ in the government. These were attractive positions since they were permanent and pensionable, but all required the Higher Examination of the London Chamber of Commerce in bookkeeping and accountancy or some other equivalent exam. The Neocleus Institute taught these subjects and had many successes in the London Chamber of Commerce and professional accountancy exams (Neocleus, 2009). Indeed, in one of his early classes, six of his 30 pupils subsequently qualified as accountants (Phillipou, 2011).

Commercial legislation

The first serious legislative reforms to boost the Cyprus economy came when the legislative council introduced the Companies (Limited Liability) Law, 1922, the Partnership Act, 1928 and the Bankruptcy Law, 1930. All these acts were firmly based on prior English legislation, thus supporting the argument that commercial law in general and company law in particular are prime subjects for legal transplantation between states. The transportation of prior English legislation to Cyprus (and elsewhere during Empire days) can be attributable to the fact that the importation of UK legislation did not conflict with local traditions because it was not intended for the general population – mainly composed of peasants and labourers – but rather for the commercial elite and the small number of foreign investors. In addition, it was administratively convenient that a relatively new and comprehensive Companies Act had been available in Britain since 1908, which could replace the existing Ottoman Commercial Code (Harris and Crystal, 2009).

The British companies legislation was consolidated in 1908. In Cyprus, the British replaced the Ottoman Commercial Code with the Companies (Limited Liability) Law, 1922, based on the British legislation of 1908. The Cyprus Gazette (18 August 1922) noted that Kingsley Willans Stead, from the UK, had been appointed to the position of Registrar of Companies in July 1922. This legislation introduced the statutory provisions for company law and financial reporting practice in Cyprus until they were replaced by reforming legislation some 30 years later. It contained sections dealing with, inter alia, a company’s constitution and incorporation, the management and administration of companies, the appointment and share qualification of directors, prospectus, winding up and audit. The accounting provisions required that the directors of every limited liability company had to “cause true accounts to be kept” of the sums of money received and expended by the company, together with the company’s assets and liabilities, and a balance sheet was to be issued in advance of the general meeting of shareholders, whereas the profit and loss account was only required to be presented at that general meeting. Furthermore, it was provided that “each company shall at each annual general meeting appoint an auditor to hold office until the next annual general meeting” (s.83) and auditors had the “right of access at all times to the books and accounts and vouchers of the company, and shall be entitled to require from the directors and officers of the company such information and explanations as may be necessary for the performance of the duties of the auditors” (s.84). The auditors were required to report to the shareholders on every balance sheet laid before the company in general meeting and this report was to:

state “whether or not they have obtained all the information and explanations they have required”;

state whether, in their opinion, the balance sheet is drawn up to “give a true and correct view of the state of the company’s affairs”; and

“be attached to the balance sheet [and] … be read before the company in general meeting” (s.84.2).

However, there was no provision regarding the qualification of auditors, and a casual review of balance sheets around that time indicates that a company’s auditors were as likely to be lawyers or doctors as businessmen, and that there was a distinct absence of individuals who described themselves as accountants. One of the earliest “accounts” complying with this legislation, including the report of the auditors in English, is that of Bank of Larnaca Limited for the financial year ended 31 December 1929 (see Figure 1), from which a number of notable features can be observed. All money items are reported to the nearest piastres – broadly equivalent to the British pence. Moreover, there are no comparative figures, the profit and loss account does not itemise expenses but reports dividends of £4,136 based on profits of about £4,800, which represents a generous dividend pay-out ratio of about 84 per cent. Also, the report of the auditors indicates that, in their opinion, the Balance Sheet provides a “true and correct view” and is signed off within one month of the financial year end.

Financial statements (1929) of the Bank of Larnaca Limited.

Almost immediately existing and new companies began to take advantage of the law. In 1923 the important Cyprus Mines Corporation became the first overseas company to register its activities in Cyprus (Department of Registrar of Companies and Official Receiver, n.d.). In 1924 the initially named Popular Savings Bank of Limassol, which had been established in July 1901, became the first limited liability entity registered in Cyprus as ‘The People’s Bank Limassol Limited’ with the registration number ‘1’ (Department of Registrar of Companies and Official Receiver, n.d.). 3 By February 1937, in the space of 15 years, the 92nd limited liability company was incorporated (Department of Registrar of Companies and Official Receiver, 1937), a moderate number for an island with a small business class. In turn, within a few years a number of legal firms were established, stimulated by the 1922 and other commercial legislation. For example, the legal firm Christos P Mitsides and Co. indicate that they are one of the oldest law firms in Cyprus, having being founded in 1923 (Mitsides and Co., n.d.).

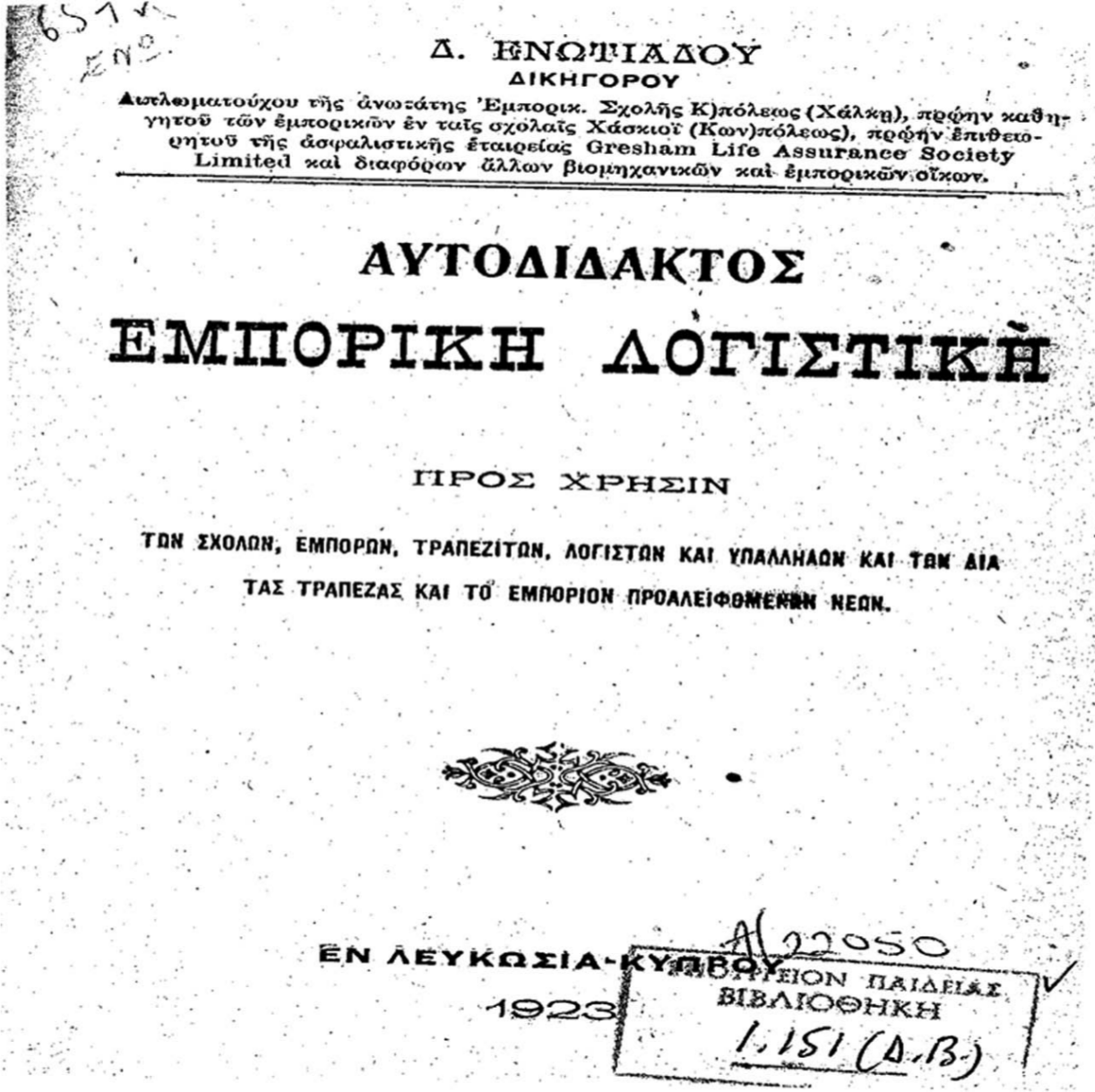

The 1922 Companies legislation was quickly followed by the publication of the first bookkeeping/accounting text in Cyprus (in Greek) by Enotiades (1923), titled Self-Teaching Commercial Accountancy with a Commercial Guide to the Island of Cyprus (see Figure 2). It is likely that similar texts published (in English) in other countries were available for sale in Cyprus prior to this, or brought into Cyprus by individuals taking up positions as government accountants or similar commercial personnel on the island. Enotiades’s book, in excess of 300 pages, had a large print run of 2,000 copies and the selling price was five shillings, which was expensive relative to other books published that year. It contained basic accounting and commercial terms, examples of commercial documents, a comprehensive list of transactions/events which were then recorded by way of journal entries and subsequently in ledger accounts, together with end of period financial statements. It also contained names of business firms, together with advertisements for many commercial firms and merchants (some in Greek and English) and a list of prominent individuals and their role in the administration of Cyprus. According to the book’s Prologue, it is based on the works of Decio de Rezo, Giorgio Marchesini and two Greek writers, Saradou and Iakovidou. It should be noted that the absence of income tax in Cyprus – it was not introduced until 1941 – meant that the preparation of a basic profit and loss account for tax purposes was not required. Thus, in the commercial world of Cyprus around that time, with the exception of banks and possibly a few large companies, such as the Cyprus Mines Corporation, which employed accountants from around 1919 (Lavender, 1962), accounting practice within most business enterprises was likely to have been focused mainly on keeping track of accounts receivable, accounts payable, cash received and paid. Such accounting records would provide necessary evidence if trade disputes arose regarding unpaid amounts or if the business became bankrupt. Also, such basic accounting records would have been useful for the owner in preventing fraud among employees.

Enotiades (1923): The first accounting book published in Cyprus.

It is interesting to note that the first professional accountancy firm founded in Cyprus was Russell and Company, which was formed in 1937 and acted as auditors to most of the major companies including, for example, the Bank of Cyprus and the Cyprus Mines Corporation (Papakyriacou, 2011). In relation to this firm’s formation in Cyprus, a front-page letter to the editor in the inaugural edition of the Embros newspaper reported that a member of a “good British firm of Chartered Accountants who are well established in Egypt, Palestine and Syria visited Cyprus lately, with the object of sounding out the place to see whether there would be any prospects for his firm to open a branch here and it appears that after approaching the Government he went away somewhat disappointed” (Embros, 1937: 1). In addition, the (anonymous) letter-writer indicated the necessity for the establishment of a chartered accountancy firm in Cyprus which could render “good services to the shareholders of limited liability companies and to the Government at large since the audit of accounts of limited companies is done by persons who no doubt have not the knowledge and experience of chartered accountants”. It appears that the local letter-writer was misinformed, since Russell and Company were registered as a partnership in Cyprus on 10 May 1937 under the Partnership Law of 1928. Its first partners were John Charles Sidley FCA (Cairo), William Gibson Carmichael CA (Alexandria), Robert Rainie Brewis CA (Cairo), Sherley Dale ACA (Cairo), Oscar Couldrey ACA (Alexandria) and Alfred Nicholson Young ACA (Jerusalem). Unfortunately, none of these individuals are listed in the obituaries published by the Institute of Chartered Accountants in England and Wales (ICAEW, 1874–1965), and there is a meagre amount of information available on them. However, the introduction of income tax would further stimulate the need for accounting professionals and this is now discussed.

The rejection and subsequent introduction of income tax

In 1925 Cyprus became a Crown Colony, a decision which meant that the British Government had no intention of relinquishing control of the island to Turkey. A number of reports were subsequently commissioned by the British colonial authorities, one of which dealt with (the absence of) income tax (Report of the Commission, 1930). This Commission was established to “enquire into the present system of taxation, its nature and incidence, with special reference to the condition and interests of agriculture, commerce and industry; to report whether the burden of taxation is equitably distributed and, if not, to make recommendations for its adjustment” (p.3). The report noted the absence of accounting records in most businesses and, based on this consideration, admitted that while

there is no fairer tax than an income tax we have reluctantly come to the conclusion that it is difficult in the present somewhat backward state of the island in regard to keeping of commercial accounts to impose such a tax [as] there were very few traders who keep proper accounts. This would make it difficult to arrive at their incomes, and it would not be fair to tax those whose incomes could be easily ascertained and allow others to evade taxation. Moreover, uneasiness is felt that examination of books and documents of merchants by a Board of Assessors would result in leakage of information and in certain cases affect the credit of the person whose books have been examined. (Report of the Commission, 1930: 8–9)

To support this argument, two (unnamed) British experts reported that they knew of “no country in the world less suitable for the imposition of income tax than Cyprus” (Report of the Commission, 1930: 8–9).

It would require the severe economic crisis on the island as a result of World War II to bring about the imposition of income tax (from 1 January 1941). Specifically, Italy’s entry into the war in summer 1940 hindered Cypriot trade and closed most of the normal markets for the colony’s produce, with a significant, adverse effect on its shipping industry. The advent of income tax was announced in the address of the Governor to the Advisory Council, and the Cyprus Post (1941b) noted that unemployment was high “due to the loss of export markets, the inevitable closing down of the mines [and] the failure to sell much of the agricultural produce of the island”. The dominant industry in Cyprus, agriculture, was depressed and the Government actively purchased domestic crops in order to support local prices: this, of course, increased overall government expenditure. However, not all members of Cypriot society struggled financially during those lean war years. In particular, some money lenders and commodity speculators exploited the situation and operated very lucrative, if slightly unethical, businesses. Furthermore, the many years of immunity from income tax enjoyed by Cyprus had attracted a “small and leisured class to reside in this island” (Cyprus Post, 1941a). Introducing income tax was considered the most equitable way to eliminate the government’s financial crisis at that time, with initial projections estimating that income tax receipts would amount to about £50,000 per annum (about 5 per cent of total revenue).

The legislation which introduced income tax (Income Tax, 1941) contained less than 60 sections and is remarkably simple compared to present day legislation. The essential thrust of the legislation was that income tax was payable in respect of gains or profits from any trade, business, profession or vocation and also on income arising from dividends, interest, pensions, rents and royalties. Some of the income tax provisions in the legislation created a demand for accounting services and tax professionals in Cyprus. These provisions were innovative in that those subject to income tax would have had no prior experience of compliance. A former income tax assessor opined that taxpayers would be likely to consult their tax advisers when dealing with the Inland Revenue and that a good living could be earned by those who represented their clients’ interests (Papakyriacou, 2011). The legislation also required accounting expertise be held by income tax officials within the Inland Revenue Department in order to assess income tax. The Inland Revenue Department soon advertised for both assessors and accountants, with an annual salary of £300, and applicants were required to possess an accounting qualification and have a good knowledge of English (Cyprus Gazette, 1943: 198).

The Income Tax Act provided for the deduction of “all outgoings and expenses wholly and exclusively incurred during the year” in ascertaining chargeable income – a standard clause used in tax legislation in general. Such deductions included, for example, expenditure on repair of premises, plant and machinery employed in acquiring the income, and bad debts incurred in any trade, business, profession or vocation proved to the satisfaction of the commissioner to have become bad during the year. Deductions were also allowed for wear and tear (i.e. annual allowances) on property, plant and equipment. 4 However, the legislation also provided that these deductions would not be allowed unless proper accounts, to the satisfaction of the Commissioner, together with a computation showing the assessable profits of the trade, business or vocation were produced to the Commissioner. Also, a deduction for trading losses, either in the form of immediate set-off against other income or subsequent carry-forward against the same source of income, was allowed, but only where the taxpayer kept proper books of account. Moreover, the legislation required that where a taxpayer appealed their assessment, the Commissioner had the power to require any person assessed to produce all accounts, books or other documents in their custody or under their control relating to such income. Clearly, the services of a professional accountant, especially for preparing and submitting business accounts, was beneficial for the tax payer in order to interpret and comply with this unprecedented legislation, and effectively prove their circumstances to the “satisfaction of the Commissioner”.

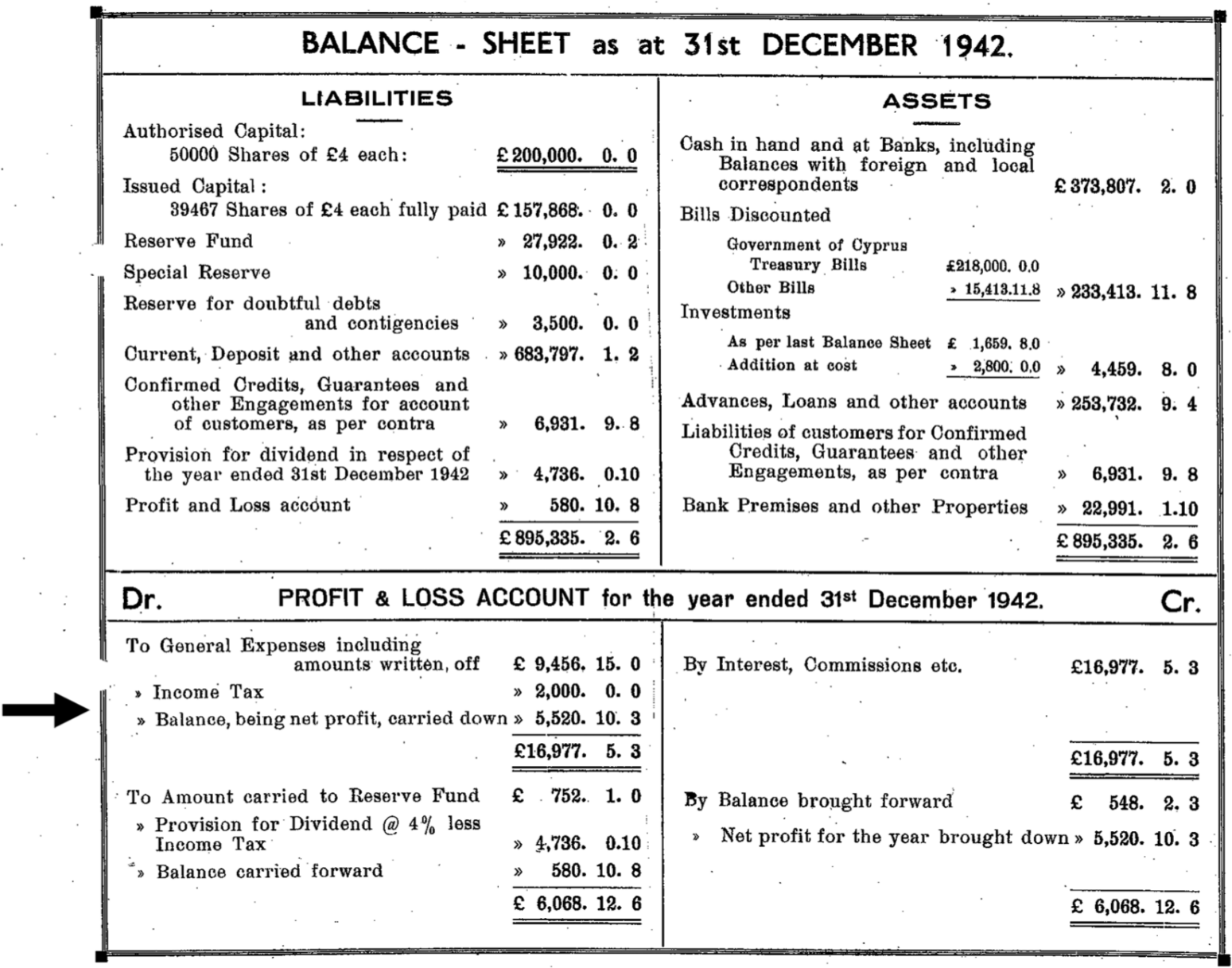

The 1941 legislation made individuals, partnerships and limited liability companies liable for income tax. Individuals were subject to a graduated rate of tax, with those with chargeable income of less than £150 per annum being exempt, while the marginal rate for top incomes was, effectively, 60 per cent. Furthermore, the amount of tax payable by a bachelor or a spinster was increased, within limits, by 50 per cent, making marriage a rather convenient and financially attractive tax planning exercise. In contrast, limited liability companies were at that time liable for a flat-rate of tax at the rate of three shillings and three piastres in every pound – equivalent to about 16 per cent. The necessity of good tax advice in forming a limited liability company – to take advantage of a flat rate structure – in contrast to trading as a sole trader (or partnership), where profits would be taxed at progressively higher rates, was obvious. The impact of the tax charge and its disclosure can be illustrated with reference to the Profit and Loss Account for 1942 of the Bank of Cyprus Limited (see Figure 3). However, this income tax charge of £2000.0.0, being approximately 26 per cent of the Bank’s pre-tax profits, seems rather severe.

Bank of Cyprus (1942): Disclosure of income tax provision.

The 1941 income tax legislation also contained several anti-avoidance provisions. For example, one provision (s.44i) allowed the Commissioner, in relation to a company controlled by not more than five persons, to treat undistributed profits as a dividend payment in circumstances where a dividend “could be distributed to shareholders without detriment to the company’s existing business or without detriment to the future expansion or development of the Company’s business”. The practical implication of this (subjective) section meant that individual shareholders of (family) companies would be assessed as if they were in receipt of dividends and the persons concerned would be assessed accordingly, even though no dividend was actually received. Therefore, it would not be possible for (family) shareholders to avoid a liability for personal income tax by not paying dividends. Effectively, from a personal income tax point of view, it made no difference whether the after-tax profits of a family company were paid by way of dividend to individual shareholders or retained by the company. A more general anti-avoidance (and subjective) provision followed (s.44ii), which specified that “where the Commissioner is of opinion that any transaction which reduces or would reduce the amount of tax payable by any person is artificial or fictitious he may disregard any such transaction and the persons concerned shall be assessable accordingly”. The extent to which the Commissioner utilised these stringent powers is not known. However, they had the potential to cause difficulties for taxpayers trying to cope with these subjective sections within the income tax code. Professional accountants and tax consultants became a useful link in negotiation between the tax authorities and taxpayers – both individuals and companies.

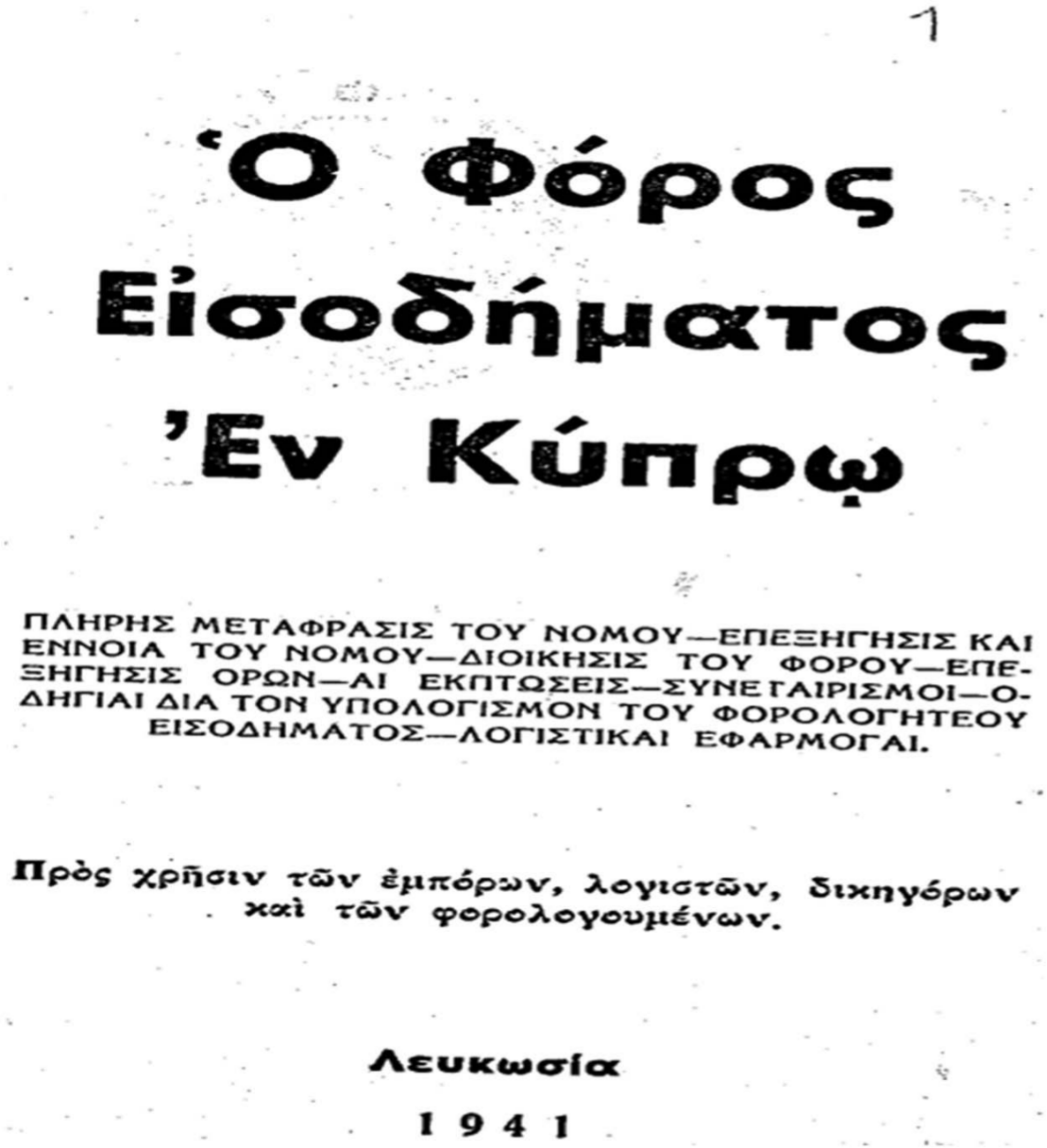

Therefore, it is no coincidence that the first formal explanation of Cypriot income tax taxation was published (in Greek) in 1941 in Nicosia and included worked examples in English and Greek (Antoniades, 1941). Translated into English, the title was Income Tax in Cyprus: Complete Translation of the Law, Explanation and Meaning of the Law. Antoniades indicated (in translation) that he had graduated from Montpellier and Liege Universities with a degree in Economics and Management and was a member of the Royal Economics Society of England. He intended that his publication be used by tradesmen, accountants, lawyers and taxpayers (see Figure 4). The (translated) Preface states:

… examples that we use were taken from the everyday life of Cyprus [and] in our effort to make this project even more complete we have drawn help from studying and consulting various English, Greek and other studies relevant to the subject [since] this is the first time that a law is being discussed, analysed and explained.

Antoniades (1941): The first book on taxation in Cyprus.

The following year, D Th Antoniades, who was not a qualified accountant, formed his own accounting firm. This is the second oldest accountancy firm in Cyprus and is now part of Grant Thornton (Michaelides, 2010).

The subsequent introduction of Estate Duty in Cyprus further stimulated the demand for professionals with appropriate accounting knowledge and skills. This tax applied to the estate of every person dying on or after 1 December 1942 (Estate Duty Law, 1942) who, at the time of death, was domiciled in Cyprus, and, in the case of deceased persons who were not domiciled in Cyprus, on all property in Cyprus which passed on death. This complex legislation, which was innovative to Cyprus, further stimulated the demand for accounting professionals, because the legislation required all property passing on death to be valued, including business interests, and returns to be made by the executor of the estate. While the rates of estate duty payable were initially around 1 per cent on small estates, a rate of 30 per cent was levied on the amount of the estate in excess of £100,000.

The Companies Law, 1951

The development of accounting practice and the need for accounting professionals with relevant accountancy qualifications was further stimulated by two provisions, one of which was contained in the original UK 1948 Act and the other in the amending company legislation which was enacted in 1951 (Companies Law, 1951) and which was modelled on an earlier UK Act (Companies Act, 1948). The British legislation was influenced by the changing perception of the social responsibility of companies, and the fact that the Cohen (Company Law Amendment) Committee had finally rejected the notion that accounting was a matter concerning only directors and shareholders (e.g., Bircher, 1988). The prior UK legislation had an unintended accounting consequence for Cyprus, and indeed for accountancy practice in the colonies in general, since the ninth schedule of the 1948 Act required auditors to state in their audit report whether, “in their opinion … proper returns adequate for the purposes of their audit have been received from branches not visited by them” (Companies Act, 1948: 348). It is probable, as noted by Wallace (1992) in Nigeria, that the requirement for “proper returns” would have been satisfied by local professional persons and firms with the appropriate accounting skills.

The second provision was contained in the 1951 legislation and dealt with the qualifications of auditors. The 1951 budget address of Sir Andrew Wright, the Governor, stated that the (pending) Companies Law would “bring the law in Cyprus into line with the law regarding companies in the United Kingdom” (Cyprus Mail, 1951a). This can also be interpreted as a statement of intent by the British to retain the island in spite of growing opposition to their occupation and the increasing support of Enosis. The 1951 legislation introduced to Cyprus additional provisions relating to the disclosure of accounting information in the profit and loss account, the balance sheet and group accounts, and was based on the British 1948 Act (Walton, 1986). The requirement of the 1922 legislation that every company must keep “proper books of account” was retained, with the clarification that “proper books of account shall not be deemed to be kept (unless they) give a true and fair view of the state of the company’s affairs and … explain its transactions” (s.140).

Specific provisions were introduced regarding auditors, including the requirement for the audit report to express an opinion as to whether the accounts show “a true and fair view” (Seventh Schedule). Additional provisions were introduced regarding the qualification of auditors and the Act (s.155) provided that a person could not automatically qualify for appointment as auditor of a company unless they were a member of a body of accountants established in the United Kingdom. It was subsequently clarified (Cyprus Gazette, 1951a) that the recognised accountancy bodies comprised: The Institute of Chartered Accountants in England and Wales; The Society of Incorporated Accountants and Auditors; The Association of Certified and Corporate Accountants; The Society of Accountants in Edinburgh; The Institute of Accountants and Actuaries in Glasgow; The Society of Accountants in Aberdeen; and The Institute of Chartered Accountants in Ireland. This auditor qualification presented an auditing monopoly in Cyprus to those individuals who had obtained the relevant accountancy qualification in the UK (or Ireland). Thus, British (and Irish) persons who were members of the above accountancy bodies continued to provide professional auditing services in Cyprus, and these included Paul Graham (ICAEW) and Wilfred Normand (CAS). However, one chartered accountant (Frank Hiscocks in Nicosia) was formally reprimanded by the Institute of Chartered Accountants of England and Wales for referring to his firm as “Chartered Accountants” when his partner was not a chartered accountant (Cyprus Mail, 1951b).

This auditing monopoly was not exploited by British firms, who only began to enter the Cyprus market after independence. It should be noted that around this time Russell and Company was the dominant professional (chartered) accountancy firm operating in Cyprus – its partners were all chartered accountants qualified in the UK who had extensive Middle East experience. Therefore, Greek or Turkish Cypriots with UK accounting qualifications would have been the immediate beneficiaries of the 1951 legislation. However, the 1951 legislation also provided that other (non-qualified) persons who had obtained adequate knowledge and experience, or by having before the commencement of the law practised in the colony as an accountant, could also be approved by the Governor to act as auditor (Companies Law, 1951). It is likely that the first recipient of the Governor’s discretion was the previously mentioned D Th Antoniades, who was authorised by the Governor to act as an auditor of companies in 1951 (Cyprus Gazette, 1951b).

The legislative provisions relating to the qualification of auditors (in addition to the understandable lure of the UK for those living in the colonies) encouraged some Cypriots to qualify as accountants in Britain during the 1950s or study for ACCA examinations (including English law and taxation) while remaining in Cyprus and utilising distance education facilities (Papakyriacou, 2011). Coinciding with the 1951 legislation, Greek Cypriots George Syrimis and Xantos Sarris had both qualified as Certified Accountants – then referred to as Certified and Corporate Accountants (ACCA, 2010). Syrimis, who subsequently acted as Finance Minister between 1988 and 1993, had offices in Nicosia and Limassol and his is the third longest surviving accountancy firm in Cyprus, having become part of Peat Marwick, which is now part of KPMG International (KPMG, n.d.). Xantos Sarris – a noted footballer – had offices in Famagusta but subsequently pursued a successful industrial career. After the 1951 legislation other professional accountancy firms were formed, and these include Hassapis and Co., established in 1954 (Hassapis and Co., n.d.) and Kyprianides, Nicolaou & Associates, established in 1955 (Kyprianides, Nicolaou & Associates, n.d.). Two notable Turkish Cypriots qualified as accountants and were employed in government service. Rustem Tatar qualified as a Chartered Accountant (ICAEW) in 1955. He had studied industrial economics at Nottingham University, England, graduating with a first class degree, and was trained in accountancy at Moore & Morell, a provincial firm of Chartered Accountants in Nottingham, subsequently becoming Auditor General of the Republic of Cyprus (Tatar, 2011). Also, Mustafe Guven qualified as a Certified Accountant in 1956 and worked in the Treasury Government of Cyprus (ACCA, 2012).

The formation of the local accountancy body in 1961

Thus, by the mid-1950s a small number of qualified accountants, mainly members of ICAEW and ACCA, had established themselves as professionally qualified accountants working in Cyprus. While students of ICAEW had to study in England, ACCA students could study and sit their exams in Cyprus, and around this time it was estimated that there were about 40 ACCA students on the island (Papakyriacou, 2011). During 1955/56, the ACCA members on the island, led by Alan Bates and John Papakyriacou from the Income Tax office, together with their ACCA colleague George Syrimis, received permission from ACCA to form a regional Society in Cyprus. The first meeting of the Provisional Committee was held on 15 March 1956: a permit under the Emergency Powers Regulations, 1955, for holding such a meeting was first obtained! Subsequently, the first meeting of the Committee of the Cyprus Society of the Association of Certified and Corporate Accountants was held on 27 May 1957, with Alan Bates being elected Chairman, John Papakyriacou elected Honorary Secretary and George Syrimis elected Honorary Treasurer (Papakyriacou, 2011). However, the Society did not function. The increasing curfew and other restrictions imposed from 1956 due to the violent struggle for Enosis waged by EOKA – the National Organisation of Cypriot Fighters – made it difficult, if not impossible, to run lectures for students or for the society to operate (Papakyriacou, 2011).

Nevertheless, the idea of forming a body of professional accountants in Cyprus did not evaporate, and came to fruition after political independence was achieved. The first Pancyprian meeting of the Cypriot Accountants and Certified Auditors of Cyprus took place in the Ledra Palace Hotel, Nicosia, on 12 June 1960 and listed 17 (Cypriot) individuals, of which five were members of ICAEW, nine were members of ACCA and three were auditors approved by the Government (Papakyriacou, 2011). A Provisional Committee, including Messrs Papakyriacou and Syrimis (from the earlier ACCA Society), was elected and mandated to draft a Memorandum and Articles of Association of the proposed (translated) “Institute of Certified Public Accountants of Cyprus” and these were presented at the subsequent general meeting of the members on 20 November, 1960. The Institute of Certified Public Accountants of Cyprus (ICPAC) was formally incorporated in April 1961 with Messrs Papakyriacou and Syrimis and prominent others, including British citizens and accountants (Paul Graham and Wilfred Norman), as founding members; and the ICPAC list of their 21 founding members is provided on the ICPAC website. As Parker (2005) notes, the choice of the CPA designation in Cyprus was consistent with that of the non-Commonwealth Middle Eastern countries of Greece, Jordan, Israel, Saudi Arabia and Turkey. Coincidentally, of the 21 founding members listed by ICPAC there was not one Turkish Cypriot. This may be a reflection of the economic separatism, leading to economic dualism, which gained momentum after 1957, and of the exclusionary politics of Greek Cypriot political elites and the separation politics of Turkish Cypriot elites (Meyer, 1962; Varnava and Yakinthou, 2011).

With independence, the demand for professional accountants and accountancy students continued as new limited liability companies were registered and as economic development was promised. The Cyprus Mail (1961a) reported that 41 new limited liability companies had been registered in Cyprus in the year after independence, which would have reflected the general economic optimism among the residents of and overseas investors in the island. In the same year, President Archbishop Makarios, in his address to the House of Representatives, expressed confidence that the first five-year plan (1961–1966) would increase annual GNP by 6 per cent per annum (Cyprus Mail, 1961b). Anticipating future prosperity, the first private third-level college, Cyprus College, was founded by Ioannis Gregoriou in order to provide a well-rounded education so that students could acquire the necessary academic and practical knowledge in the field of business and accounting (Cyprus College, n.d.). Other third-level colleges were to follow, as was the establishment of universities, which would provide trainees for the expanding accountancy firms, both local and international; however the establishment of universities would have to wait for another four decades. These local educational institutions can be considered as the final steps in the transition from primitive accounting skills to a sustainable local, professional accountancy body.

Concluding remarks

This article has provided insights into the significant influences of British rule on accounting practice and its development, in the context of colonial Cyprus during the last four decades (1918–1960). One consequence of these influences was the formation of a local professional accountancy body on the island in 1961. It has highlighted how the significant local political, economic, institutional and social developments, within the wider imperial and colonial contexts, brought about accounting change in Cyprus during the period commencing after World War I through to Cyprus’s independence in 1960. Three phases can be identified. Initially, after the First World War, the Government’s efforts to encourage the economy, particularly business, through various legislative reforms stimulated the need for personnel with bookkeeping and other commercial skills. Possession of these skills was an important source of “social mobility” for local inhabitants of the island, but this aspect is not unique to Cyprus (e.g. Clarke, 2008). Secondly, commercial legislation during the 1920s and the subsequent introduction of income tax in 1941 extended the range of accounting skills needed by individuals and business with its emphasis on the preparation of “accounts”. Finally, the era of the professionally qualified accountant was stimulated with the provisions of the 1951 Companies legislation. The culmination of these phases resulted in the formation of a local, professional accountancy body after independence, in 1961.

Throughout these phases, the colonial dimension for understanding the development of accounting in Cyprus is significant and supports Parker’s (2005) argument that the growth of the accountancy profession worldwide cannot be properly understood without an imperial dimension, and that the true effects of the British Empire on accounting practice is within the pre-independence rather than the post-independence era. This article also supports the observation of Sian and Poullaos (2010) that British accountancy associations trained colonial accountants both in Britain and in the colonies, and also inspired the formation of similar-but-different versions of themselves, often aided and abetted by British immigrant accountants.

Additional work on accounting history in Cyprus needs to be undertaken. For example, one could study the financial reporting practices of individual companies, such as the influential Cyprus Mines Corporation, through time, or examine the archives of long-established companies operating in Cyprus, such as Lanitis Bros, KEO, and the Cyprus Trading Corporation, or review the many files relating to the entire period of British rule – all in English, and readily available in the State Archives in Nicosia. Indeed, it may be possible to identify the internal costing systems of such entities. In a separate vein, the work on Waqf 5 accounting and auditing under Ottoman rule (Cavlan et al., 2008) could be extended using, for example, the research framework and other topics of Yayla (2011). Such records can be accessed in the National Archives of the Turkish Republic of Northern Cyprus. Furthermore, rich insights could be obtained by researching the teaching of accounting at various commercial schools after the Second World War. In addition, it would be worthwhile to investigate the occupational backgrounds and status of accountants and tax professionals who practised around that time in order to prepare an oral history, which is bound to contain interesting and colourful stories. Also, following Carnegie and Edwards (2001), it would be revealing to investigate the “signals of movement” and “occupational ascendency” associated with the formation of the local accountancy body with its formal designation as “Institute” in 1961. Furthermore, one could pursue the approach of, for example, Chua and Poullaos (1993) to investigate the micropolitics of how this professional accountancy group organised to define and extend their domain of practice, reputation and influence. There is a great deal of literature available that examines the pre-formation activities of professional bodies, their genesis and their continued development after their formation. However, as West (1996) notes, there is no one theory which explains exclusively how all professions arise, and Walker’s (1995) study of the genesis of professional accountancy in Scotland confirms that the development of any individual profession cannot be examined without taking account of the economic, political and legal context of its formation. One could also investigate whether the formation of a local professional accountancy body was a natural consequence of Cypriot nationalism during that period. Finally, as was noted by Carnegie and Napier (2002), the study of the evolution of accounting practice cannot be confined to a single country or culture. Thus, a comparative international study with other Mediterranean colonies, namely Malta and Gibraltar, but particularly the former, in which professional accountancy firms were formed during the 1960s, would be particularly interesting.

Footnotes

Acknowledgements

The authors are grateful to three anonymous reviewers for their constructive comments on earlier drafts of this article.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.