Abstract

The purpose of this article is to present a comparative analysis of the development of the auditing profession in the United Kingdom and France. Although legal requirements for external audits of company financial statements provided an opportunity for the development of an auditing profession as early as the mid-nineteenth century, differences in the role and status of professions led to differences in the development of the auditing profession in these two countries. It is only in recent years that there have been significant efforts to harmonize the regulatory structures for the auditing profession on a more international basis. The primary argument of this article is that historical differences in the ways that auditing has developed in different countries are significant and that international harmonization of the regulation of the auditing profession may be difficult to achieve without understanding these differences.

1. Introduction

The unifying theme of this article is that different conceptions of the relationship between the individual and the state have shaped the development of the auditing profession beginning from the seventeenth century; however, differing notions regarding the individual/state relationship have created challenges in the contemporary era as the European Union (EU) tries to standardize the regulation of the auditing profession. One important difference between national traditions is that individualism has generally been more highly prized in the United Kingdom, as reflected in the writings of eighteenth- and nineteenth-century liberal philosophers (Russell, 1945). As a result, the role of the state in regulating the auditing profession in the United Kingdom remained relatively at the margins well into the twentieth century. The requirement for external audits of company financial statements was initially included in the Companies Acts during the mid-nineteenth century as a means of providing greater economic transparency and assurance about the reliability of financial information, but these requirements were later removed. Thereafter, and until recently, the British state had very little to say about the nature of auditing, leaving such matters to professional institutes of accountants and auditors. Such a laissez-faire attitude, not surprisingly, led to the proliferation of competing professional bodies (Edwards et al., 1997).

British individualistic traditions were not similarly embraced in France or other parts of Continental Europe during either the ancien régime or republican periods. In this article, France serves as a proxy for continental, Roman law countries in opposition to a more common law approach, such as in Britain. The demand for external auditing in France came primarily from the state, beginning with the Colbertian period during the seventeenth century in France under Louis XIV (Lodge, 1931). The Roman civil law tradition in which the relationships between the individual, the state and society are more precisely defined than in Britain has continued in France to the present.

Beginning in the mid-nineteenth century, a gradual removal of restrictions against the formation of limited liability companies, and other positive acts on the part of the state (Braudel, 1979, vol. 2: 24), provided linkages between political rationalities which favored economic liberalism and legal technologies which facilitated capital formation (Miller, 1990: 315). The emergence of auditing as an important component of global capitalism can therefore be traced, at least in part, to the increased use of the limited liability company as a principal form of business enterprise (Micklethwait and Wooldridge, 2003: 50).

This article also argues that historical factors which led to differences in financial reporting systems (Nobes, 1983, 1992) have led to differences in the role and status of the auditing profession in different countries. Individual shareholders have been the traditional providers of capital in the United Kingdom. Even before any involvement by the British state in the regulation of the auditing, shareholders in Britain demanded the issuance of audited financial statements (Edwards et al., 1997: 2); as a result, the auditing profession in the UK developed through individual professional partnerships and organized professional bodies.

The experience in France has been more mixed, with historical periods during which the French government encouraged capitalist development and periods in which the state nationalized major enterprises. Consequently, the regulation of the auditing profession in France has developed largely through legislation and government decrees, resulting in a role and status for professional auditors in which they function, at least in part, as agents of the French government in the regulation of corporate activity.

The remainder of this article is organized as follows. Section 2 reviews the prior literature in the sociology of professions literature and the literature in comparative financial accounting systems with regard to the development of the auditing profession. Sections 3 and 4 describe the development of the auditing profession in the United Kingdom and France. Section 5 discusses recent efforts by the Commission of the European Union to harmonize the regulation of statutory auditing within the EU and a written response to these efforts issued by the Institute of Chartered Accountants in England and Wales (ICAEW). A discussion and summary conclude the article.

2. Review of prior literature

The sociology of professions literature has contributed a great deal towards defining the characteristics, nature and functions of professional activity (see for example, Abbott, 1983, 1988; Carr-Saunders and Wilson, 1933; Etzioni, 1969; Larson, 1977; Vollmer and Mills, 1966). One of the arguments of this literature is that the role and status of professions differs among countries, and that, in particular, there is a greater expectation in code law countries (such as France) concerning the importance of the state in the regulation of professional activity. This higher expectation in code law countries regarding regulation of professional activity derives from the fact that the state has often played a role in creating professions in these countries. Arguments from the sociology of professions literature lead to the expectation that there will be differences between the United Kingdom and France with respect to the auditing profession, with the state having played a greater role in the regulation of the auditing profession in France.

Another strand of the sociology of professions literature has investigated distinctions between occupations and professions. Abbott (1988), for example, has argued that the process of professionalization involves competition among occupational groups for the right to become recognized as professions, and that professional recognition is typically achieved when the state grants such recognition. Furthermore, Abbott implies that no profession can remain completely free of external interference, particularly regulation imposed by the state (Abbott, 1988: 141). Based on Abbott’s theory of professionalization, it can argued that it was the legal designation of a monopoly in the occupational practice of auditing which led to the establishment of the auditing profession. However, this argument may not be supported in the case of the United Kingdom, in that the legal requirement for statutory audits did not come into existence until the mid-twentieth century, while the accountancy and auditing profession existed in the United Kingdom from at least the early nineteenth century.

In contrast to Abbott, Larson (1977) envisioned professionalization as a process through which an occupational group achieves professional status by obtaining cognitive expertise in a particular area of practice. Larson’s theory of professionalization concerns the ability of an occupational group to obtain a state granted monopoly based on the recognition of its competence pertaining to an authoritative body of knowledge that the profession controls through education and training programs. It is argued in this article that the various recognized professional accountancy bodies in the United Kingdom have pursued the type of professionalization strategy described by Larson. The British government was persuaded from 1948 onwards that auditing constitutes an authoritative body of knowledge which requires a monopoly pursuant to the Companies Acts. In contrast to Abbott’s (1988) view about occupational competition, the recognized professional bodies in the United Kingdom did not contend with one another to gain this monopoly. Rather, the professional bodies worked together in a joint committee to establish a unified approach to government regulation in the post-World War II period (ICAEW, ICAS, ICAI, 1995). Therefore, Larson’s idea about a monopoly of competence appears to be relevant to the development of the auditing profession in the United Kingdom.

A third question that arises in a historical analysis of the development of the auditing profession relates to the origin of the profession, which in turn relates back to the distinction between an occupation and a profession. Prior to the nineteenth century, auditing was not considered to be a profession. Pursuant to the sociology of professions literature, various groups of accountancy practitioners sought to achieve recognition in the emerging industrial economies of the nineteenth century (Edwards et al., 2007). In the United Kingdom, the auditing profession developed through private sector accountancy bodies that were established before the legal requirement to have company audits (Lee and Parker, 1979). While these accountancy bodies were able to achieve recognition from the British Crown through royal charters, they were not formally regulated by the British state.

In France, the regulation of the auditing profession emerged initially through the appointment by royal edict of inspecteurs and censeurs as early as the seventeenth century. After the French Revolution, there was a period of liberalism during the nineteenth century when the French State had little involvement with the regulation of auditing (Lemarchand, 1995; Ramirez, 2001). This period of liberalism was followed in the post-World War II period by one in which the regulation of the auditing profession has been in the hands of the Compagnie Nationale des Commissaires aux Comptes (CNCC), a body created and controlled by the French state (CNCC, 1994).

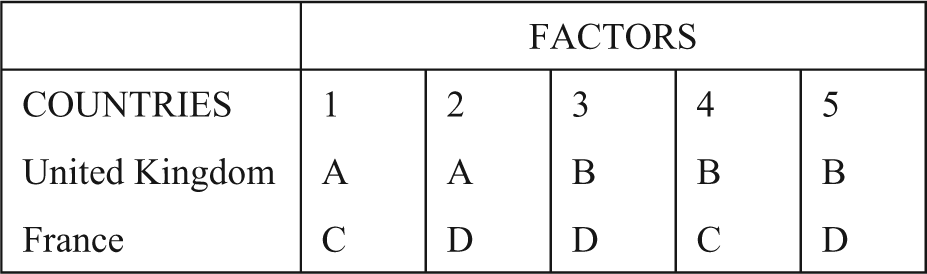

A fourth question that arises when discussing the historical development of the auditing profession relates to differences in financial accounting systems among countries. These differences are important because the primary subject matter of external auditing involves the evaluation of the truth and fairness of company financial statements in relation to financial accounting principles and standards. A great deal of prior research has compared differences in financial accounting systems among countries (see for example, Bloom and Naciri, 1989; Doupnik, 1987; Hopwood, 1989; Hopwood et al., 1979; Nobes and Parker, 1995; Taylor et al., 1986). Nobes and Parker (1995) maintain that two types of financial reporting systems have developed through time: the “micro/professional” system (Model A) and the “macro/uniform system” (Model D) (see Figure 1). Nobes and Parker have used their classification scheme to categorize the financial reporting systems of the United Kingdom and France, among other countries (see Figure 2).

Nature of regulatory environment.

Classification of countries based on regulatory environmental factors*

Pursuant to the Nobes and Parker model, the United Kingdom stands at one end of the spectrum, with the classification of France in a more intermediate position. The differences between the financial accounting systems of countries can be traced to various factors, including differences in: legal systems; traditional sources of capital; roles played by banks; accounting and auditing standards-setting practices; corporate governance practices; and the impact on financial reporting of laws regarding income taxation and dividend payments (see for example, Evans and Nobes, 1998a, 1998b; Gray, 1988; Mueller, 1967; Nair and Frank, 1980; Nobes, 1983, 1992; Perera, 1989). In summary, differences in the underlying historical factors, which led to differences in the development of financial accounting systems, have also led to differences in the regulation of the auditing profession. In the United Kingdom, the regulation of the auditing profession has been conducted primarily through private sector professional bodies, although this has been changing since the legislation enacted in 2006 which has vested greater regulatory powers in the British Parliament and the Financial Services Authority. In contrast, in France the regulation of the auditing profession has historically been conducted through law and regulation. As the auditing profession has evolved into a significant component of global capitalism, the historical distinctions between the role and status of the auditing profession in different countries has begun to diminish, and there is now an expectation of a greater degree of international harmonization of the regulation of the auditing profession by the European Union and other trans-national regulatory bodies. These efforts towards international harmonization will be addressed in a later section of this article.

3. United Kingdom

There have been many distinguished accounting historians who have examined the development of the accountancy and auditing professions in the United Kingdom (UK), including such authors as Kedslie (1990), Cornwell (1991, 1993), Walker (2004), Boys (1994, 2011), Maltby (1999), Edwards, Anderson and Matthews (1997), Edwards (2001, 2010), Edwards, Anderson and Chandler (2007) and Lee (2011), among others. Most of these authors have focused on the development of the accountancy profession in the United Kingdom and not on the auditing profession as a separate or distinct element of the accountancy profession. This is because, unlike France, there is no real distinction in the United Kingdom, between the accountancy and auditing professions. The remainder of this section reviews some of the findings of the prior literature, with a focus on the development of the auditing profession as a distinct element of the accountancy profession.

3.1 Historical background of professional accountancy and auditing in the United Kingdom

Micklethwait and Wooldridge (2003: 20) suggest that the practice of auditing in Great Britain may be traceable to the rise of the joint-stock company during the reign of Elizabeth I. Dobija (2011: 2) points to the separation of ownership and control in the East India Company as providing an impetus for the rise of auditing practices. Audits of joint-stock companies during the sixteenth through eighteenth centuries were primarily what may be referred to as “amateur” audits, in which certain shareholders (or members) of the company were appointed to conduct audits on behalf of their fellow shareholders.

The development of the auditing profession emerged at a later point in British history, perhaps towards the end of the eighteenth century or early in the nineteenth century. However, it is important to point out there was little recognition of either accountancy or auditing as a profession at that point and no distinction was made between accountancy and auditing; the services of accountancy and auditing were considered to be part of one occupational group. For example, based on an examination of trade directories, Edwards et al. (2007: 67) provide evidence regarding the number of “accomptants” or “accountants” offering services to the public in the larger English cities in different decades of the nineteenth century, with numbers ranging from 20 in the 1800s, to 301 in the 1830s, to 499 in the 1850s, to 1,248 in the 1870s. The listings in the trade directories often listed “accounting” rather than “auditing” services (Edwards et al., 2007: 68); thus, auditing was not distinguished as a separate aspect of accountancy services. The point is, as Boys (1994, 2011) points out, there were practicing accountants and auditors in the UK during the early nineteenth century, but these emerging professional accountants and auditors were not regulated by the British state.

Edwards et al. (2007: 82) indicate that two positive acts on the part of the British state emerged in the 1830s and 1840s which led to an increased demand for auditing services. The first was the Joint Stock Companies Act 1844 which included a requirement that joint-stock companies issue audited financial statements to their shareholders. Subsequent to this Act, there was an increased use of joint-stock companies to fund the construction of the British railway network. The second legal action on the part of the British state was the creation of municipal corporations in 1835 to supply civic improvements. Matthews et al. (1998: 139–141) indicated that audit work during this period was of great importance to the rise of the accountancy profession in Britain. Corporate failures and financial manipulations during the 1830s and 1840s with respect to the formation of capital intensive railway companies, demonstrated a need for “an expert and independent audit” (Parker, 1986: 8). Thus, there was a demand for auditing services which emerged in the 1830s and 1840s as a result of the increased use of joint-stock companies to fund rapidly expanding industrial development, which an emerging group of professional accountants attempted to serve.

Interestingly, the British state appears to have taken a relatively laissez faire approach to audit regulation during the latter half of the nineteenth century (Lee, 2013). This may have been due to the growing strength and importance of the accountancy profession in Britain, and the ability of certain professional bodies to resist regulation by the state. Rather than direct regulation by the British government, there was Crown recognition of professional bodies of accountants in different cities of the United Kingdom, who were permitted to regulate themselves. In addition to providing other professional accountancy services, the members of these recognized professional bodies also came to be acknowledged as experts in auditing (Maltby, 1999).

In 1854 the prototype of the Institute of Chartered Accountants of Scotland, called the Society of Accountants in Edinburgh, was established, followed by the Glasgow and Aberdeen societies, whose members were all known from the beginning as “chartered accountants”. These societies eventually merged to become the Institute of Chartered Accountants of Scotland (ICAS) in 1951. There was also the fusion of several English societies of accountants to form the Institute of Chartered Accountants in England and Wales (ICAEW) in 1880. With the emergence of these recognized professional bodies or institutes, the regulation of the auditing profession developed largely in the hands of the profession. Various other accounting historians have discussed the development of the accountancy and auditing profession in Britain (see for example, Walker, 1993, 2004).

It is interesting to note that while the existence of an auditing profession was evident by the end of the nineteenth century, 1 the Companies Act 1856 actually removed the requirement to have an audit for joint-stock companies, replacing this requirement with a model set of articles of incorporation which included a balance sheet format and a proposed series of procedures to audit the balance sheets. Thus, while the provisions of the 1856 Act facilitated the creation of limited liability joint-stock companies in the UK, it was not until the Companies Act 1948 that external audits were required by law to be performed by qualified professional auditors, and it was not until the Companies Act 1976 that the three primary institutes of Chartered Accountants (ICAEW, ICAS, and Institute of Chartered Accountants in Ireland - ICAI) and the Association of Chartered Certified Accountants (ACCA), were specifically mentioned by law as the only bodies whose members were recognized as qualified to perform statutory audits.

3.2 Structures regulating professional auditing in the United Kingdom

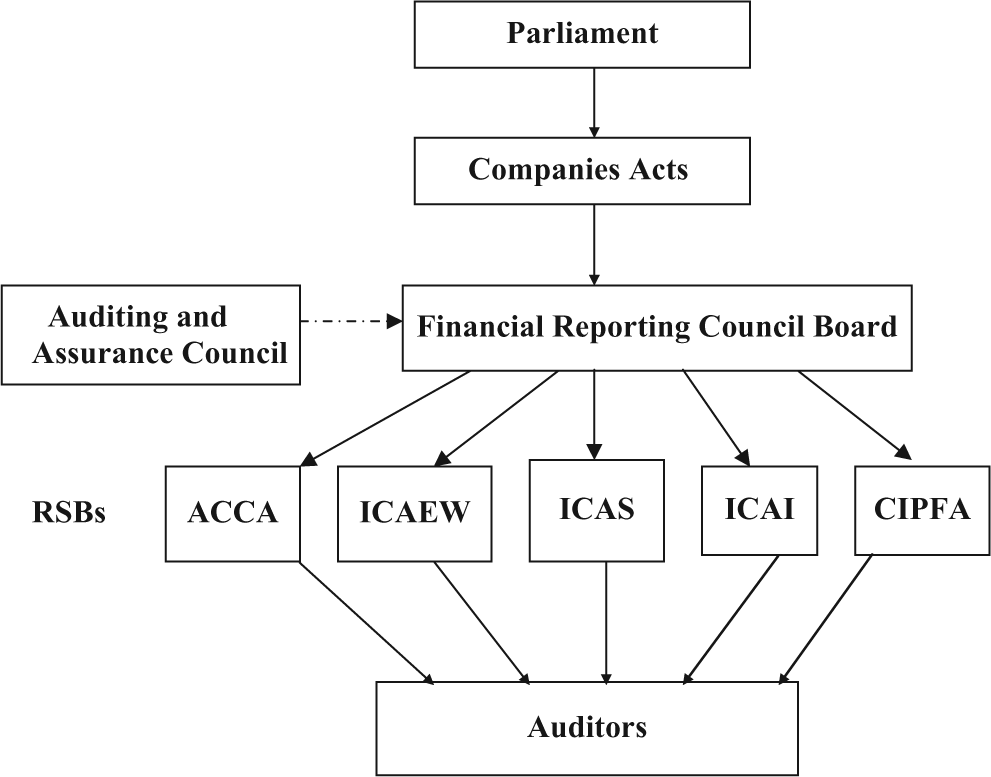

The 1989 Companies Act included provisions designed to “ensure that only persons who are properly supervised and appropriately qualified are appointed as company auditors, and that audits are carried out properly, with integrity and with a proper degree of independence”. The manner in which this was implemented in the UK was to designate certain established professional bodies as Recognized Qualifying Bodies (RQBs) and Recognized Supervisory Bodies (RSBs). The recognized professional bodies were: ICAEW, ICAS, ICAI, ACCA and the Chartered Institute of Public Finance and Accountancy (CIPFA). Through to the end of the twentieth century, the British government delegated the responsibility for determining who would be allowed to be a practicing professional auditor to the five recognized professional bodies (see Figure 3).

Regulation of statutory auditors in the United Kingdom.

The regulation of the auditing profession in the UK has been modified several times since the mid-1970s. In 1976, an Auditing Practices Committee (APC) was established in the private sector by the recognized professional bodies to formalize co-operation on auditing practices. In 1978, the APC published a preliminary codification of auditing best practices. A more formal publication of auditing standards and guidelines was published in 1980. In 1989, the APC began to issue a series of “Practice Notes” which were intended as practice guidelines to assist auditors in applying auditing standards for particular circumstances or industries. The Auditing Practices Committee (APC) was restructured in 1991 and renamed the Auditing Practices Board (APB). Regarding the issue of distinguishing between accountancy and auditing in the UK, in 1993 an auditing standard was issued that required auditors to state in their audit reports that management is responsible for the audited financial statements and the auditor for their audit report on those statements (ICAEW, ICAS, ICAI, 1995).

Following the passage of the United States Sarbanes Oxley Act of 2002, and subsequent regulatory reforms to the American auditing profession, the British Government took a decision to reorganize the regulatory structures for financial services in the UK, including those of professional auditing. This led to the UK Financial Reporting Council’s (FRC) role being expanded to become the single independent regulator of the auditing profession as well as being responsible for issuing auditing standards and dealing with their enforcement. Following the Companies Act 2006, the FRC (and its audit arm) is no longer independent of the state. It is required to report annually to the Secretary of State for Business and to Parliament on how it has conducted its oversight of the regulation of statutory auditors, including regular visits to the recognized professional bodies. Additional reforms were carried out in July 2012 to enable the FRC to operate as a unified regulatory body with enhanced independence. A new structure was implemented to ensure the effective governance of all the FRC’s regulatory activities under the responsibility of the FRC Board. As part of the reforms, the Auditing Practices Board (APB) was replaced by the Audit and Assurance Council. Responsibility for setting auditing standards was assumed by the FRC Board, with the Audit and Assurance Council acting in an advisory role to the FRC Board.

To summarize, until recently, the historical development of the auditing profession in the UK occurred primarily in the private sector, with education and admission requirements, disciplinary practices and professional standards being conducted through several recognized professional bodies. Beginning in 2006, the FRC (and effectively the British Parliament) assumed a greater role in the regulation of the auditing profession, thus confirming the predictions of both Abbott and Larson, that it is difficult for professions to maintain their independence in the face of regulation by the state.

The historical development of professional auditing through private sector professional bodies contrasts with the way that the auditing profession developed in France, as will be seen in the following sections.

4. France

Miller (1990) provides an extensive analysis of interrelationships between accounting practices and the state during the Colbert period in France (1661–1683). The legal technologies employed during this period focused on the regulation of company accounts pursuant to the Ordinance of 1673. An official publication of instructions explaining and commenting on the Ordinance was issued by the French state in order to instruct merchants on the proper presentation of accounts. In addition, there was an enhancement of the role of intendants 2 appointed by the King, as well as the inception of systematic and detailed accounting information flows from the provinces to the center (Miller, 1990). The keeping of exact books of account (Savary, 1676) was required not only to promote the success of business enterprises, but also to enhance control over companies and promote commercial order within the French state. Miller (1990) maintains that the Colbert period (1661–1683) was a significant time of innovation in the calculative practices of accounting and for a wide range of other practices of government. He also argues that it was through a particular political rationality of creating “order” that distinct sets of accounting and governmental practices were linked (1990: 315). At the same time, it is important to acknowledge that throughout much of Louis XIV’s reign, France was the leading European military power, engaging in three major wars and two minor conflicts. Thus, an important political rationale based on military competition cannot be discounted with respect to this period. In other words, the creation of economic order and a unified set of commercial practices throughout France facilitated economic prosperity, which enhanced the military power of the French state.

4.1 Historical background of professional accountancy and auditing in France

Hilaire (1989) indicates that when the Compagnie des Indes was reorganized in 1723 during the Regency Period, “inspecteurs” were designated by royal authority, and “syndics” were elected at the general meeting of shareholders to review the stewardship of the directors. Lefebvre-Teillard (1982) states that during the nineteenth century “censeurs” were given the task of checking the operations of an enterprise, visiting locations and examining books. The censeurs reported to the members of the company (i.e. shareholders). The same author indicates that before 1863 the organizing documents of companies provided for the appointment of “commissaires” whose role was to examine the accounts and report on their findings to the members of the company.

The key legislation pertaining to the development of the auditing profession in France is as follows:

Law of 23 May 1863: created “commissaires” usually called “commissaires de surveillance” or “censeurs”;

Law of 24 July 1867: confirmed the title “commissaires”;

Decree of 8 August 1935: required competence and independence of statutory auditors and specified incompatible occupations;

Law of 24 July 1966 and the Decree of 12 August 1969: specified the organizational structure for the profession of commissaires aux comptes.

Law of 23 May 1863: provided protection for shareholders for the first time in French history.

The 1863 Act specified that: The annual general meeting designates one or more commissaires, members or not, who are given the responsibility of preparing a report to the annual general meeting of the following year on the situation of the company, on its balance sheet and on the accounts presented by the administrators. The resolution approving the balance sheet and accounts is null if it has not been preceded by the report of the commissaires (art. 15). The commissaires have the right, to be exercised whenever they think it appropriate, in the interests of the members, to review the books, to examine the operations of the company and to call for a general meeting (art. 16).

Standards of independence and competence, and a requirement for the exercise of professional secrecy were not included in 1863 Act. The Act specified only that: “the extent and the effects of the commissaires’ responsibility towards the company are determined according to the general rules of the mandate” (article 26). This article was subsequently repeated word for word in article 43 of the Law of 24 July 1867. The commissaire, usually referred to at that time as “commissaire de surveillance”, or “censeur” (Houpain and Bosvieux, 1935), could be chosen from among the shareholders, relatives of the directors, or even from the employees of the company. Members of the board of directors could not be appointed as commissaires. No knowledge of accounting and finance was required. Education in accounting was not officially recognized by the French government until the “brevet d’expert comptable” was created in 1927 by the Ministry of Public Instruction, and the “brevet professionnel de comptable” in 1931 (Bocqueraz, 2000; Degos, 2004). Leduc (1982: 9) indicates that with respect to the appointment of commissaires that: There were flagrant cases where the job was entrusted to an ageing, and particularly incompetent, shareholder, from which derives the image which is found too often, of the commissaire signing a report prepared by the accounting department of the company.

Bouteron (1953: 110) wrote that: “as far as the commissaires were concerned, it was clear that they lacked both technical training and independence from the management”. Hémard et al. (1974: 50) noted: if it is to be fulfilled in a satisfactory manner, the task entrusted to auditors requires that the individuals who undertake it should have two essential qualities: on the one hand competence, and on the other independence from those who manage the company, qualities to which one should naturally add intellectual and moral probity. Unfortunately these prerequisites completely escaped those who drafted the law.

While there was general agreement about the incompetence and lack of independence of commissaires under the 1863 act, the regulation of the auditing profession in France was not fundamentally changed until the Decree of 8 August 1935 which required publicly traded companies to select at least one of their commissaires from a list maintained by the Court of Appeal. A Decree of June 29, 1936 established the conditions for admission to the Court lists which was made dependent on a technical examination; however, many persons were exempted from the examination because of their status as practicing accountants, and the examination was not set at a high level (Bocqueraz, 2010). The 1935 Decree introduced several changes to audit regulation which remain in force today:

a definition of conflicts of interest prohibiting any employee of the company or relative of the directors from being appointed as an auditor;

a requirement that the commissaire receive no income from the firm other than that arising from the audit engagement;

a prohibition against the commissaire becoming a director of the company within five years of the expiry of the audit engagement;

an obligation for the commissaire to observe professional secrecy;

any breaches of the law on the part of audit clients were to be reported to the public prosecutor;

any publication of false information by the commissaire would be a criminal offence.

The concept of a co-commissariat (i.e. two auditors for each annual audit) was also established in 1935 with respect to financial institutions accepting savings from the public. The 1935 decree mandated that there should be two auditors, including one who was considered to be competent by virtue of having been registered with the Appeal Court. It was possible, therefore, for a company, to have several commissaires. However, it was only with the law of 24 July 1966 that listed companies were explicitly obligated to appoint two qualified commissaires. Nevertheless, this was already the practice of most big French companies (Bennecib, 2004).

4.2 Structures regulating professional auditing in France

In 1967, beginning with the creation of the Commission des opérations de bourse (COB, the French equivalent of the US Securities and Exchange Commission), now replaced by the Autorité des Marchés Financiers (AMF), discussions emerged regarding the competence of auditors and the effectiveness of the co-commissariat (COB, 1994). It was believed that the co-commissariat provided a high level of audit quality. In addition, elimination of the co-commissariat could have led to a loss of audit engagements by French auditors in favor of the large international accounting firms. Consequently, even though the idea of a co-commissariat arose initially in 1935 because of a perceived lack of competence among auditors, the requirement was maintained because removing it would be detrimental to French audit firms, particularly with respect to large audit clients.

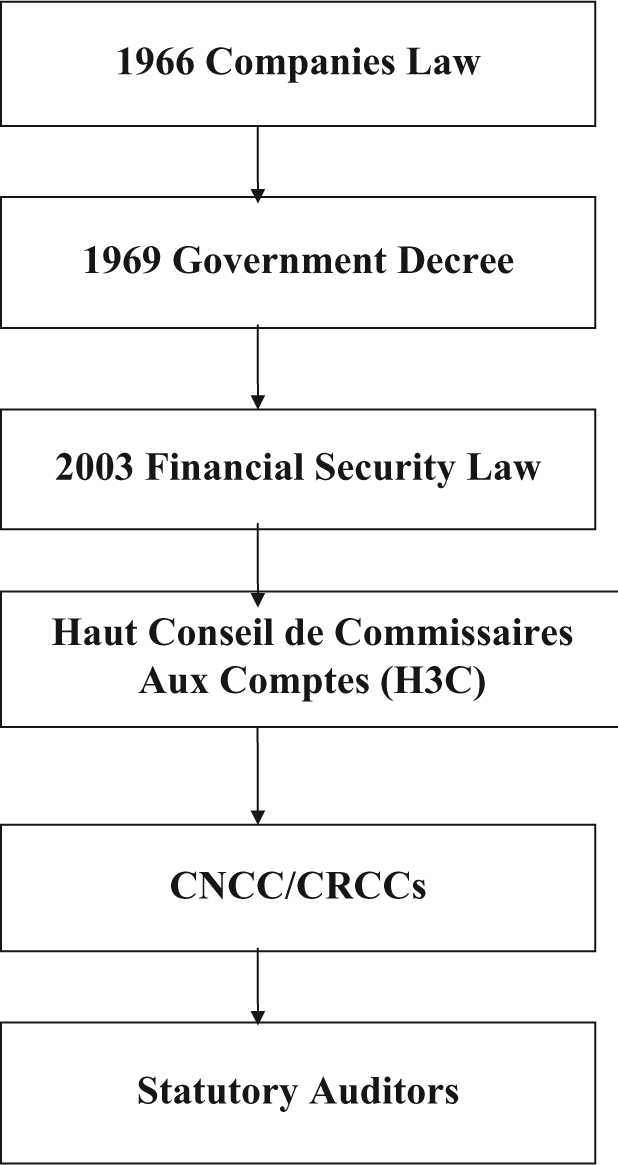

It was with the Law of 24 July 1966 and the Decree of 12 August 1969 that the role, duties and status of the statutory auditor in France were significantly modified. The requirement to preserve professional secrecy was retained, independence was reinforced, entry to the profession was made conditional upon passing exams of a very high level, and the purpose of the audit was clearly defined. In short, the 1966 Law marked the end of amateur auditors. As far as competence and independence were concerned, the Decree of 12 August 1969, and the modifications of the Law of 24 July 1966, anticipated the Eighth European Company Law Directive of 1984 concerning the qualification of statutory auditors. The Law of 24 July 1966 maintained the obligation to have two commissaires for listed companies and for limited-liability companies with capital of more than five million francs. In addition, there was a requirement for a change of statutory auditors every six years.

An important historical event which has had significant impact on statutory auditing in France was the creation of the Plan Comptable. This legal requirement established a specific chart of accounts and a mandatory format for financial statements. Thus, what was to be audited became specified by law. The origins of the Plan Comptable are interesting in that it was in effect a “cultural intrusion” imposed by the Goering Plan during the German occupation of France in the 1940s (Standish, 1990). The Plan Comptable continued to be the legal framework for accounting standards in France into the post World War II period. Following various amendments it is now called the Plan Comptable Générale (PCG), as defined by Regulation 99-03 of the Comité de la Réglementation Comptable (CRC), and validated by the Ministry of the Budget. Changes to the PCG are now recommended by the Autorité des normes Comptables (ANC) which was created by the Ordonnance No. 2009-79.

In summary, the evolution of the auditing profession in France has been associated with legal requirements for the appointment of various types of auditors, ranging from inspecteurs to syndics to censeurs, and finally to commissaires. The Law of 23 May 1863 required limited liability companies to appoint a commissaire to audit the accounts and report to the shareholders; however, there were no requirements concerning who could be appointed to this position, nor any education and experience requirements. It was not until 1935 that a legal requirement specified that two commissaires must be appointed, at least one of whom must be enrolled in a list of professional auditors maintained by the Court of Appeal. Finally, the Law of 1966 marked the end of the amateur auditor, with commissaires required to be enrolled in an organization that subsequently came to be named the Compagnie National des Commissaire aux Comptes (CNCC), operating under the direct supervision of the Ministry of Justice. Consequently, the evolution of the auditing profession in France has been closely associated with political rationalities and legal technologies related to the goals and objectives of the state. Figure 4 shows the regulatory context of the statutory auditor in France.

Regulation of the statutory auditor in France.

Table 1 summarizes the regulatory structures for the auditing profession in the United Kingdom and France. Based on the discussion of the historical evolution of the auditing profession in these countries, it can be seen that the regulatory structures differ in substantial ways. During the last twenty years, however, there have been efforts to harmonize the regulatory structures for the auditing profession throughout the European Union.

Differences in regulation of the auditing profession in the United Kingdom and France.

5. Initiatives to harmonize regulation of the auditing profession in the European Union

The regulation of the auditing profession was impacted by the Eighth Directive of the European Commission (European Commission, 1984; Evans and Nobes 1998a) issued in 1984. The purpose of the Eighth Directive was to harmonize regulation within the EU, in particular with regard to access to the auditing profession and prerequisites to become a statutory auditor. In response to the Eighth Directive, the member states of the EU modified their company laws and state regulations (i.e. government decrees) to comply with the provisions of the Directive (Cooper et al., 1996; Evans and Nobes, 1998a). However, compliance with the Directive does not mean that regulation of professional auditors is the same in every country (Buijink et al., 1996; Margerison and Moizer, 1996). Moreover, the Eighth Directive did not cover all aspects of audit regulation; it focused primarily on reducing barriers to intra-European trade in audit services. A subsequent Council Directive of 21 December 1988 required mutual recognition of higher education diplomas and mandated professional training of at least three years’ duration.

In October 1996, the European Commission issued a Green Paper entitled The Role, the Position and the Liability of the Statutory Auditor within the European Union (European Commission, 1996). Green Papers of the Commission provide the basis for discussion of issues among the member states of the EU. Following the issuance of the Green Paper, a conference on the role, position and the liability of the statutory audit within the EU was held in Brussels in December 1996. The objective of the conference was to discuss the regulation of professional auditors in Europe. There was general agreement that the EU should provide a common regulatory framework (European Commission, 1998). Among the topics discussed in the Green Paper and at the conference were the following: the definition of the statutory audit; contents of the audit report; the competence of the statutory auditor; the independence of the statutory auditor; the role of the statutory auditor in corporate governance; auditors’ civil liability; and the freedom of establishment and the freedom to provide services across national borders. One important point contained in the first paragraph of the Green Paper was as follows: The requirement to have the annual and consolidated accounts of certain companies audited by a qualified professional which was introduced for the Community as a whole by the Accounting Directives, is designed to protect the public interest. (European Commission, 1996: 4)

It is precisely in defining what constitutes the public interest that the regulation of statutory auditing comes to be of great importance. The protection of the public interest is viewed somewhat differently in different countries. In the United Kingdom the public interest is defined primarily in terms of a well-functioning capital market, whereas in France the statutory auditor is deemed to act on behalf of the state in certain circumstances.

In late 2010, the European Commission addressed the regulation of the statutory auditor in a more direct manner by issuing another Green Paper which called for consultation on the role of statutory audit as well the wider environment within which statutory audits are conducted (European Commission, 2010). The purpose of the Green Paper was to question whether the role of auditors could be enhanced to mitigate financial crises. In particular, the Commission wanted to address whether financial audits provide the right kind of information for participants in capital markets, whether there are issues regarding the independence of audit firms, whether there are risks linked to a concentrated market for audit services, and whether supervision at a European level might be useful and how to best meet the specific needs of small and medium sized businesses.

The EU Green Paper made several statements about statutory audits which may or may not be generally accepted. The Green Paper defined statutory audits as audits of company accounts as required by EU law. Auditors are entrusted by law to conduct statutory audits. The aim of an audit is to offer an opinion on the truth and fairness of the financial statements of the companies audited in complete independence of the audited company. To this extent, the independence of auditors should be the bedrock of the audit environment. In the wake of the banking crisis of 2008–2009, questions arose as to whether the role of auditors could be enhanced to mitigate financial risks in the future. There are a number of areas that the Commission believed should be explored, in particular:

The independence of auditors – it is unclear if auditors are truly detached and critical when examining the financial statements of a company when that same company is an existing or potential client for non-audit services.

The degree of reliance stakeholders can place on audited financial statements. Does an “expectation gap” exist amongst stakeholders with regard to the scope and the methodology of audit?

The potential for systemic risk because of the strong concentration in the audit sector. What consequences might there be for the wider financial system if one of the big audit firms fails?

The role played by national regulators, and whether national supervision is fully effective.

The potential for a competitive internal market for auditing and the removal of barriers which make auditing primarily a national market.

The specific needs of small businesses and ensuring proportional application of rules to SMEs.

The global context – audit firms operate as global networks; to this extent it is important to co-ordinate efforts at an international level.

5.1 Response of professional bodies to the EU Commission Green Paper

Various professional bodies have responded to the EU Commission Green Paper, including the Institute of Chartered Accountants in England and Wales (ICAEW). In a document entitled International Consistency: Global Challenges Initiative: Providing Direction, issued by the ICAEW in 2010, the ICAEW (2010) concluded that there were limits to the international regulation of auditing because of historical and cultural differences among countries. The ICAEW further concluded that historical differences in the ways that auditing has been practiced in different countries are quite important. These comments from the ICAEW correspond with the primary argument of the current article, that there are limits to the international regulation of auditing because of historical and cultural differences among countries.

In France, the response to the European Commission Green Paper has been muted, with the Compagnie Nationale des Commissaires aux Comptes (CNCC) stating that it works closely with the Federation des Experts Comptables Europénnes (FEE) to influence European Regulations for statutory auditing. However, it should be noted that a “justification of assessments” was introduced in France by the Financial Security Act of 2003 which became mandatory in auditors’ reports in 2004 with respect to the 2003 accounts. This requirement has been codified in the French Commercial Code (Code de commerce) (article L.823-9). Initially, the “justification of assessments” was introduced to remove constraints imposed on auditors and to allow them to express themselves freely in their reports. However, in 2006, a related professional standard was introduced (NEP 705 (87)), which required auditors to justify their assessments and opinions. This requirement has been cited by the European Commission as best practice for statutory auditors (http://www.cncc.fr/download/footprintconsultant_reportstudy_va_cncc_fev2011.pdf).

6. Summary and conclusion

The purpose of this article has been to present a comparative historical analysis of the development of the auditing profession in the United Kingdom and France. A historical analysis of the development of the auditing profession in these two countries indicates that the state has played a role in the emergence of the auditing profession, but that the nature of the state’s involvement in the emergence of the auditing profession has differed between the countries. Beginning in the mid-nineteenth century, a gradual removal of restrictions against the formation of limited liability companies, and other positive acts on the part of the state, provided linkages between political rationalities which favored economic liberalism and legal technologies which facilitated capital formation. Thus, the origins of company auditing as an important component of capitalism appears to be linked with the emergence of the limited liability company as a principal form of business enterprise. Legal requirements for audited financial statements provided an opportunity for the growth of an auditing profession, but historical differences regarding the role and status of professions led to differences in the ways that the auditing profession developed in the countries examined. These differences have constituted the primary focus of this article.

Abbott (1988) has argued that professional recognition is normally achieved when the governing authority in a nation state grants recognition as a profession. Abbot has also indicated that the regulation of professional activity differs among countries, and that, in particular, there is a higher expectation in code law countries (such as France) regarding the importance of the state in the regulation of professions. The findings of this article confirm Abbott’s contention that professions seek state support to confirm their legitimacy, and that expectations regarding the regulation of professions will vary between code and common law countries. The restriction of the right to perform audits has characterized the auditing profession. No other aspect of the profession is similarly recognized or regulated by the state. The findings of the article also confirm that there is a distinction between the role and status of professions in code law countries such as France and common law countries such as the United Kingdom, with the state playing a more prominent role in the regulation of the auditing profession in code law countries. In addition the differences in historical sources of capital (private individuals or banks) among countries has had an impact on the development of the auditing profession, with members of the profession in the United Kingdom having been oriented more to individual providers of capital. In contrast, it appears that the French may wish to see more uniform requirements for conducting an audit than the British. This may mean that the historical differences in the distinctions between the two traditions may lessen as the British profession becomes more subject to greater state oversight.

The importance of this topic lies in its implications for international regulatory harmonization. If the differences in regulation of the auditing profession are based on established laws and historical traditions relating to the training of auditors and their role in corporate governance, then expectations for increased regulatory harmonization may be difficult to achieve. Moreover, the meaning of external auditing may actually differ among countries. In particular, there may be different definitions of stakeholders, and different beliefs about the role and purpose of independent auditors. More fundamentally, as long as the definition of the purpose of regulating corporate activity differs among countries, then regulatory structures for statutory auditing will most likely differ. Nevertheless, as the importance of global capital market activity increases, there will be a continuing emphasis on regulatory harmonization of statutory auditing. The primary argument of this article has been that international regulatory harmonization of the auditing profession may be difficult to achieve without understanding differences in the historical development of the auditing profession in different countries.

Footnotes

Acknowledgements

The helpful comments of the Editor of the Special Issue, Paul Miranti, are greatly appreciated, as well as the comments of the anonymous reviewers. I would also like to thank the participants at the World Congress of Accounting Historians 2012 in Newcastle, the Association Francophone de Comptabilité 2012 in Grenoble, as well as seminars at HEC Paris, CNAM Paris, and the American Accounting Association Annual Meeting 2013.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.