Abstract

The London and General Bank case is well known in auditing history. Less familiar are some of the characters involved in the group of companies financed by the Bank and its sister institution, the Liberator Building Society. At the centre of the group was a Victorian rogue, Jabez Spencer Balfour, who ensured that only those he could dominate and manipulate were chosen to take part in his complex and fraudulent schemes. Two chartered accountant brothers were drawn into Balfour’s web. One of these, Morell Theobald, had an interest in the supernatural, although his claims about supernatural activities were disputed and he was more or less branded a fraud and a liar by fellow spiritualists. Using correspondence between Balfour and Theobald and between Theobald’s wife and the Home Secretary, we reveal insights to the psychology of the main character in the scheme and one of his weak-willed disciples. The evidence shows that Theobald knew enough about accounting and finance to realize that the strategy adopted by Balfour could not be sustained.

Introduction

Recent research into the professionalization of accounting has extended our understanding of the early days of the profession. Edwards and Walker (2010) examine features of the lifestyles of Victorian accountants, identifying common traits that were intended to display to the world that they had achieved a certain status – that they were “gentlemen”. They were expected to comply with codes of behaviour, based on ideals of gentility and respectability, to be church-going and to keep a well-ordered house. Anderson and Walker (2009) examine the extent to which the professionalization of accounting tells us something about the social mobility of those drawn to this vocation. Their analysis also reveals a strong association between accountancy and non-Conformist interpretations of the Christian faith. It went without saying that the typical Victorian gentleman was expected to be a Christian of some denomination. Perhaps surprisingly, there has been little academic interest in the relationship between accounting and religion (Carmona and Ezzamel, 2006: 117) and there is a distinct “paucity of historical research connected with accounting and other religions and belief systems” (Bisman, 2012: 19). The present article does not examine religion per se, but offers an insight into how the religious beliefs of one adherent to a form of Christianity so extreme that it could easily be regarded as “an other religion” may have coloured his judgement when it came to professional matters.

The man in question was Morell Theobald, a very unusual chartered accountant. Our re-examination of some of the peculiar features of Theobald follows the suggestion of Walker (1996) that we can learn as much about the evolution of the accounting profession from the lives of the notorious as we can from the lives of the successful and famous. From his own writings on the subject of spiritualism, Theobald presents us with an opportunity to consider how his preferred belief system might have had a strong bearing on the conduct of his professional life. What we set out to show is that a man who was an outspoken member of the spiritualist movement and of some significance in commercial life displayed a remarkable degree of naivety. His natural gullibility left him ill equipped to withstand the scheming of one of the Victorian era’s outstanding rogues, Jabez Spencer Balfour.

Balfour was one of the leading financiers in Britain during the last quarter of the nineteenth century. At the centre of a web of companies, the “Balfour group”, were the London and General Bank (a name familiar to generations of auditing students) and the Liberator Building Society, the largest such institution in the country. When the group collapsed in 1892, it brought turmoil to the money markets (Ashworth, 1980), raising questions about the standards of auditing at the time and also resulting in jail sentences for both Balfour and Theobald, as well as others involved in the group.

The purpose of this article is to provide an examination of one of the accountants at the heart of this scandal, his personal beliefs and some evidence of his technical competence as an accountant. Our material comes from the archives of the Institute of Chartered Accountants in England and Wales (ICAEW) and its predecessor bodies at the Guildhall Library, the (incomplete) public filings of the Balfour group companies and related Board of Trade papers at the National Archives, law reports of the various legal actions pursued in the wake of the Liberator’s crash, contemporary general media, both British and overseas (such was the interest in the financial scandal and its aftermath), the specialist spiritual and professional journals of the time, and Theobald’s own detailed accounts of his daily life.

Our article begins with a review of Theobald’s commercial career, culminating in his partnership in a firm of chartered accountants with offices in the City of London and a client base that included at least one listed company as an audit client. We then consider the phenomenal growth in a quasi-religious movement known as spiritualism and in the following section reveal what an impact this movement had on Theobald and how he tried to make an impression on it. We believe that the evidence we produce in this connection sheds a telling light on Theobald’s conduct as an auditor and company director at the heart of the notorious Balfour group, which is the focus of the penultimate section. The article ends with concluding remarks based on the evidence presented in the earlier sections and an epilogue with a suggestion of Theobald’s lasting legacy.

The commercial life of Morell Theobald

Morell Theobald was born on 14 November 1828 in Birmingham, Warwickshire. His given name came from his maternal grandfather, the Reverend Stephen Morell. His father was a bookseller and his uncle, John Daniel Morell, was to occupy the post of Her Majesty’s Inspector of Schools. This was a solid middle-class base on which a successful career in the City could develop.

The start of Theobald’s career was as a clerk working for the Union Assurance Company. He lived at home with three siblings (Robert, Frances and William) in Clerkenwell, London. His mother had died and, as with so many Victorian families, death would continue to play a large part in the Theobald household. Ten years later in 1861, we find him (Figure 1) with his wife, Ellen, and two young children living in the Croydon home of his father-in-law, Edward Miall, the leading non-conformist MP who was also to become involved in the Balfour group, albeit in an “honorific” capacity (McKie, 2004: 21). In the same house lived Edward’s son, Arthur, who was ten years younger than Theobald but who had already begun his training as an accountant’s clerk.

Morell Theobald.

Theobald’s career in insurance was to see him become manager of the fire department of the Albert Life Assurance Co (the Albert) (Daily News, 31 December 1864: 1). He wrote a slim volume on insurance (Theobald, 1868), but from this we can gain little insight into his commercial abilities in the insurance field since the book is more concerned with extolling the virtues of an individual having insurance cover rather than the intricacies of the management of insurance companies. Theobald’s choice of title “Foresight” was unfortunate, since the Albert went into liquidation in the middle of August the very next year (The London Gazette, 26 October 1869: 5755). The company’s collapse was attributed to a reckless extension of business through the acquisition of more than 25 other insurance companies over the course of the previous 20 years – when the Albert collapsed so too did its associated companies. Apparent increases in profitability were the basis on which dividends and management remuneration had been paid (Alborn, 2002). In reality, the company had been making losses estimated to have accumulated to more than £1m (The Maitland Mercury & Hunter River General Advertiser, 30 October 1869: 4). We do not know for sure whether Theobald was still involved with the Albert during the critical final year or what position he occupied at the end of his association with the company. We do know that the regulatory response to the Albert’s crash was immediate – the Life Assurance Companies Act 1870 required insurance companies to disclose more about their financial position and introduced better prudential supervision for the industry (Alborn, 2002).

It may have been this financial catastrophe which caused Theobald to change careers, for, two years later, he is entered in the 1871 census as a “public accountant”. At that time he was living in his own house in Hendon, London, with his wife and four children, a domestic servant and her eight year-old son. Also at the house was Frances, Theobald’s unmarried sister.

At some stage during the early 1870s 1 Morell Theobald formed a partnership, Theobald Bros & Miall, with his brother, William, and brother-in-law, Arthur Miall. They were based in 30 Mark Lane in the City of London and became sufficiently established to be cited in The Accountants Directory for 1877. The notion of respectability required that professional men had offices that were either prestigious or located central to the heart of city life (Edwards and Walker, 2010). We cannot say that the Theobalds’ office was impressive (their neighbours were a mixture of other accountants, lawyers, and traders such as tobacconists and grocers), but when they moved to 23 St Swithin’s Lane, they were about as central as it was possible to get – a stone’s throw from the Bank of England in Threadneedle Street and the home (at that time) of the Stock Exchange in Capel Court.

Membership of a professional body no doubt would have increased the firm’s reputation and the partners sought this elevation in status. Theobald’s two partners had both applied to become fellows of the Institute of Accountants in June 1879 (MS28405 Volume B, fo. 46) but their applications were turned down the next month on the grounds that they were not eligible under the rules (MS28405 Volume B, fo. 51). The Institute’s rules were designed to ensure that only bona fide accounting practitioners were admitted; traditionally many practitioners calling themselves “accountants” had combined that occupation with another (Anderson et al., 2007). There was a stipulation that applicants had to have been in practice for at least five years – a test which, by 1879, the Theobalds and Miall would almost certainly have met. However, there was also a requirement that members should act exclusively as accountants and this may have proved to have been more of an obstacle. The Society of Accountants in England had less stringent rules on admission – needing only three years’ practical experience and no exclusivity of practice (Anderson et al., 2005: 15). Of all the professional bodies at that time, the members of the Society were most likely to be pursuing another vocation at the same time as practising accountancy (Anderson et al., 2007: 405 fn 6).

Some indication of how members and potential members of the Institute viewed plans to establish the Society as a rival organization can be found in a letter to the Institute’s secretary from the Newcastle firm of Miller, Monkhouse and Goddard: In the first place, [the Society] has not got the right people at the head, and second, they seem disposed to admit any man who chooses to call himself an Accountant without any other test or qualification. Certainly one of the Newcastle men whose name is on the Provisional Committee should not be admitted into any Association of Public Accountants, the other[s] we don’t know much about, and generally they seem quite second-rate men, at least the provincial names, and some of the town names seem even third-rate. (MS28404: fo. 70)

The letter claims that many of the principal accountants in Liverpool, Manchester, Bradford, Sheffield and other large towns are of the same opinion. Another letter from a Liverpool accountant stated that accountants in that city had “held aloof” from joining the Society (MS28404: fo. 85). An accountant in Manchester wrote that some accountants there had joined the Society “but none of any standing” (MS28404: fo. 92–93).

It might be tempting to dismiss such comments as elitist snobbery, but these provincial accountants were not members of the Institute jealously guarding their turf. They could not become members simply because the Institute at that time only recruited London accountants. Accountants in the provinces wanted a national body – but not the Society. Fewer accountants from the upper and upper-middle classes were drawn to the Society (Anderson and Walker, 2009).

An examination of the later disciplinary records of those who joined the ICAEW from the five amalgamating bodies bears out the early suspicions about the dubious quality of those admitted to the Society. Chandler et al. (2008: 833) discovered that: In total, 44 per cent of the founders were members of the [Society]. These men account for a disproportionate number of expulsions (75 per cent of all bankruptcies and 70 per cent of all other misconduct cases). In total, more than a fifth of those admitted to the ICAEW from the [Society] were subsequently expelled.

The timing of the Theobalds’ attempts to join a professional organization is interesting but it was certainly no accident. It was known at the time that the accounting bodies were pressing for a Royal Charter and it was anticipated that gaining admission to the new body would be more difficult once it had been formed. Fortunately for the partners of Theobald Bros & Miall, all three were admitted to the Society in October 1879 (see ICAEW List of Members 1881). They were not alone in wanting to join before the Royal Charter was granted: as the move towards a government-recognised body of “official”, ultimately chartered, accountants gained pace from January 1879 onwards, significant numbers of public accountants decided to join existing associations so as to ensure that they were not excluded from what was perceived to be a more prestigious, incorporated national collective. (Edwards et al., 2005: 233)

The Society’s annual report, presented to its members at their Annual General Meeting in May 1880, referred to the great addition of members during the past year (The Accountant, 8 May 1880: 5). Indeed, the aggregate membership of the five bodies increased by nearly 30 per cent in just over a year prior to the granting of the Charter (Edwards et al., 2005: 244).

So, in May 1880, Theobald was admitted to the ranks of the newly created ICAEW. A year later, at the time of the next Census, Theobald was living with his wife, six children (including an adopted daughter), a guest (the well-known faith healer Miss Mary Godfrey) and two servants in 62 Granville Park, Lewisham, London (his residence until shortly before his death more than 25 years later). His professional life seems to have been successful and by the mid-1880s the firm of Theobald Bros & Miall could boast of one client listed on the London Stock Exchange, the Nevada Land & Cattle Co (Stock Exchange Year Book, 1887).

The Theobalds had a keen interest in literature. They were associates of The Bacon Society, created in 1885 to promote the claim that Francis Bacon was the true author of the works of William Shakespeare; it still exists today. Theobald’s brothers, William and Robert, 2 were the Society’s auditor and honorary secretary respectively. The Theobalds were also deeply involved in the spiritualist movement.

Spiritualism

The rise of Darwinism and other scientific developments during the Victorian era led many to doubt conventional religious beliefs and paradoxically spawned a new hysteria in the form of spiritualism. In addition, a high mortality rate was just one unintended consequence of mass urbanization and industrialization. Insanitary living conditions, dangerous work practices and poor air quality contributed to a shortening of life expectancy. In turn, this led to a preoccupation with death – especially for those who had children – since infant mortality accounted for over a quarter of all deaths. Bereavement became a “national experience, and mourning a community activity” (Hazelgrove, 2000: 13). These factors produced the “supreme test of Christian faith” (Jalland, 1999: 122), which for many led to a significant move away from Christian explanations of life and death.

Beginning in the USA with the claims of the Fox sisters that the spirit of a murdered resident was communicating with them through knocking or rapping on pieces of furniture, interest in this form of spiritualism took off and spread internationally, arriving in France in 1853 after it had already made an impact in Britain and Germany (Lachapelle, 2011: 7). The notion took hold that the soul inhabited an earthly body and not only lived on after the end of that body but was able to communicate with the living. Those gifted with the ability to communicate with spirits were termed mediums and their séances in darkened rooms have been immortalized in countless dramas and melodramas set in the Victorian era. With the turn of the century, the golden age of spiritualism had passed but the movement had not died, and in fact the slaughter of so many young men during the First World War rekindled support for the idea that bereaved parents could commune with their dead sons (Field, 2012). Subsequent conflicts appear not to have produced a similar resurgence, though the movement is by no means moribund.

Spiritualism offered an alternative belief system that attracted membership from across the social spectrum. It was said that the higher the class, the more likely it would contain believers. The literati included such devotees as Sir Arthur Conan Doyle, Harriet Beecher Stowe, Elizabeth Barrett Browning, Robert Chambers, Samuel Taylor Coleridge, Alfred Lord Tennyson, William Makepeace Thackeray and Anthony Trollope (Nicol, 1982: 36). Social reformers such as John Ruskin and Robert Owen were attracted to the possibility of the soul enduring and communicating beyond death. Politicians were also represented in the form of William Gladstone, Arthur Balfour and John Hollond. Daniel Dunglas Home, 3 perhaps the most famous medium, “conducted séances for the British aristocracy and Continental royalty” (Lamont, 2004: 898). Among the aristocracy drawn to spiritualism were Lord Rayleigh and the Earl of Dunraven (1924: 10), who confessed that, despite being inclined to disbelieve reports of supernatural phenomena, he felt he must “admit the possibility of much that contrasts strongly with ordinary experience”.

Oppenheim (1985: 29) claims that the majority of active spiritualists came “from both the professional middle class and the better educated strata of the working class”. Even at this end of the social spectrum, there was money to be made by those claiming to be able to act as an intermediary between the quick and the dead. Mediums were not afraid to advertise openly that their charges could be as much as a guinea per head for private consultations (The Star, 1 February 1877: np), though critics alleged that those demanding money under such circumstances were nothing more than “impudent knaves” (The Sheffield & Rotherham Independent, 22 January 1880: 5). In the wake of Carl von Buch’s uncovering of fraudulent mediums, The Times opined that “a few good exposés of paid mediums will probably deter many from becoming victims to a fraud the worse in that it trades on the most sacred of human feelings, the sanctity of the dead” (The Times, 19 September 1882: 8).

More than two hundred organizations associated with the movement were to emerge during the Victorian era, though some included only a handful of members (Oppenheim, 1985). One of the most influential associations was the British National Association of Spiritualists (BNAS) formed in 1873 (Britten, 1884). In May 1874, the BNAS called its first public meeting where “objectors” to its principles were “specially invited” (The Examiner, 16 May 1874: 524). It was, however, a ticket-only affair and the fact that the local operatic agents, Messrs Lacon and Ollier, were responsible for ticket sales perhaps revealed the theatrical nature of these performances.

The BNAS suffered a series of controversies that by 1876 led to it “tearing itself apart” (Nelson, 1969: 107). One of the main problems was the accusation that more powerful members of the group had rigged proxy voting at council meetings. Later in 1880, after suffering a wave of prosecutions for trickery, the viability of the BNAS was called into question and its demise was eagerly anticipated by some: “[those] people who know what harm it has done among the weak minded are hoping that its work is at an end” (The Liverpool Mercury, 22 September 1880: 5).

Membership dramatically declined and the BNAS was reconstituted a number of times. In 1882 BNAS members voted to change its name to The Central Association of Spiritualists (CAS). This was a short-lived affair that was dissolved in 1883 and The London Spiritualist Alliance emerged in its place.

4

About the same time, another society, The Society for Psychical Research (SPR) began. The SPR differentiated itself from the CAS, claiming that it did “not commit itself to a belief in Spiritualism, but aims at approaching the inquiry solely from a scientific standpoint” (Britten, 1884: 186). Its membership was quite disparate (Salter, 1948: 11). Like the CAS, the SPR, popularly labelled the “Ghost Club” after a society established by a group of Cambridge intellectuals in the 1850s (McCorristine, 2012: vii), was not always well received by the press: [the SPR] was founded[,] whatever it may pretend to the contrary in its prospectus, to prove the existence of ghosts and all sorts of supernatural phenomena. It got no end of guineas on that understanding. (The Pall Mall Gazette, 6 September 1887: 2)

The SPR became “The Incorporated Society for Psychical Research” on 7 August 1895. It still exists today, as a registered charity listed under “Education and Training” by the Charity Commission. The modern SPR does not seek to cover up the frauds of the past and acknowledges that innocent audiences were often duped. 5

Our protagonist, Morell Theobald, was involved in a number of these spiritualist organizations and spiritualism was to occupy as big a part of his life as his professional career in the City.

The spiritualist life of Morell Theobald

Theobald took an active part in some of the various organizations which evolved to promote the spiritualist movement. He, his wife and his brother were council members of the BNAS. In 1884, Theobald became Honorary Secretary to the first Council of the London Spiritualist Alliance (Theobald, 1884: 39). In the same year, he was appointed council member of the SPR. He remained an Associate member until 1896 (Proceedings of the Society for Psychical Research Vol. II (1884); Vol. VI (1890); Journal of the Society for Psychical Research Vol. VII (1895–96)). In addition, in 1884, the SPR members elected Theobald as their auditor, a post he held until he was jailed in 1896. His audit report on the SPR’s 1883 balance sheet read simply “Audited and found correct” (Journal of the Society for Psychical Research, Vol. I (1884): 7).

Superficially, the Theobald household may have appeared typical of many middle-class families of that time. In fact, it may well have been better-off than most. By 1881 Theobald was living with his wife, six children (including an adopted daughter), a guest (the well-known faith healer Miss Mary Godfrey) and two servants in 62 Granville Park, Lewisham, London. The area was becoming very fashionable among successful professional men, after John Young of the leading firm Turquand, Young, built the first house in nearby Blackheath (Edwards and Walker, 2010).

Owen (1989) devotes an entire chapter to the Theobald family, revealing some singularly unusual features of the domestic arrangements. Largely based upon the family’s own writings (which strangely make little mention of brother William), 6 Owen is generally uncritical of the conduct of the authors. Theobald himself revealed an attraction to spiritualism at an early age when his grandfather claimed to have seen and spoken to the spirit of his own dead son (Theobald, 1887: 17). Theobald’s spinster sister, Frances, who frequently visited the family, also claimed to have psychic abilities. 7 At first, Theobald played the part of sceptic, but in 1869, 8 after three of his children had died, the “table-rapping began” (Theobald, 1887: 18). In his own words, spiritualism entered “through the dark door of sorrow, as the Comforter” (Theobald, 1887: 305).

After table rapping, a less crude form of communication from the spirit world came via “passive handwriting” where a pen held in the hand of a living being was compelled to write by the guiding spirit of the departed relative. Later, the spirits sent messages via direct writing – messages would appear on paper without the involvement of a human agent; witnesses sitting in séance could not see the creation of the message since the room was darkened but all could hear the scratch of pen on paper. “Direct voice” communication used the medium as a mouth-piece for the deceased. For the distraught parents, the overriding theme of the messages was one of comfort and reassurance that the spirit of the dead child was now happy in another world and that its parents should not reproach themselves for having failed to prevent premature death.

In 1882, the Theobalds took on a new cook, Mary, and it was not long before she too began to report witnessing paranormal activity, including doors being locked, kettles boiled, fires laid and hand-written messages in a foreign language appearing on the ceilings without the aid of human intervention. Owen (1989: 90–91) explains: “Because he never seriously entertained the possibility that any member of his family might seek to impersonate a spirit, or dupe the other sitters in any way, Morell Theobald could accept the communications at face value”. In similar fashion, and again reflecting his gullibility, Theobald failed to associate the cessation of spirit activity with his children’s absence. Neither, it must be said, does Owen make anything of this coincidence.

There were those in the SPR who remained unconvinced about claims made by certain spiritualists and about Theobald in particular. Writing just after the end of the nineteenth century, Raupert (1901: 153) remarked that “the influence of the séance room is on the whole debasing”. Theobald’s main doubter was Frank Podmore, 9 who had joined the SPR a year after its formation and who was to become known as the “sceptic in chief”. Podmore was well aware of previous attempts to deceive; he dismissed most mediums as charlatans (Hazelgrove, 2000). Podmore demanded evidence of Theobald’s paranormal “guests”. Theobald resisted calls to invite an independent witness to the family séances, on the grounds that a physical guest would “prove a skeleton at the feast and frighten away the invisible guests” (Theobald, 1887: 135). Podmore explained that the writing which had mysteriously appeared on the ceiling of the Theobald home could have been done by using a pen tied on a broom-handle. He traced the text written in a mystical language to a journal which had been published only a few years earlier. To Podmore, Theobald was nothing more than a fraud and this may account for the fact that, despite his books on spiritualism and his work for various organizations, Theobald made little impact on the spiritualist movement. For example, there are no references to Theobald in books on the spiritualist movement, such as Barrett (1911), Gauld (1968), Haynes (1982), Salter (1948) and Thouless (1972).

Perhaps we can better understand Theobald’s state of mind by referring to a statement made by a fellow spiritualist, Conan Doyle, who having seen the spirit of his dead brother, said: “The objective side of it [spiritualism] ceased to interest, for having made up one’s mind that it was true there was an end of the matter” (cited in Norman, 2009: 102).

Remarking on the “extreme credulity of some of the spiritualist members of the SPR” in general and one in particular, Hamilton (2009: 160–161) observes wryly: “Poor Theobald. More sinister figures than servant girls in the guise of amiable fire-lighting spirits were later to take advantage of his trusting nature”.

The Theobalds’ role in the Liberator

Those “more sinister figures” were involved with an organization that grew to become the largest building society in Britain. The Liberator Permanent Building and Investment Society was set up in June 1868 and later incorporated as the Liberator Permanent Benefit Building Society (the Liberator). The Liberator closely followed the model of another mutual society, the Alliance National Land, Building and Investment Society, formed in 1862 and so named in order to suggest a link with the leading temperance organization, the United Kingdom Alliance (McKie, 2004: 13–14). The Alliance National Land, however, was short-lived – it crashed in 1866. In a similar vein, the name “Liberator” was designed to align its ideals (or at least, to appear to do so) with those of the non-conformist Liberation Society. The mastermind behind the Liberator’s inception was Jabez Spencer Balfour, a larger than life character, whose charisma and business acumen attracted legions of followers. Sadly these attributes were not accompanied by honesty and integrity.

Balfour needed an indirect means of raising finance for building projects undertaken by the Lands Allotment Company (LAC) which he had controlled since November 1867. He used the Liberator as a conduit to pass money drawn from unsuspecting public depositors to invest in property speculation. To raise the money, Balfour created a national network of more than 500 church ministers and laymen who were paid a commission for introducing new business to the Liberator (as in fact were Theobald Brothers & Miall). An early indication of some dubious accounting practices can be found in the Liberator’s balance sheet of 1871, with the gross nominal value of shares issued appearing on the capital side and the amount unpaid on those shares, representing about 60 per cent of the total, appearing as amounts due on the asset side (Price, 1958: 285). Later manipulations became a little more sophisticated.

New companies were brought into the fold. It is worth pointing out here that although the word “group” is commonly used to describe the web of related companies which Balfour used as the vehicle for his speculative schemes, it was not a group of companies in the modern sense. There was no parent company sitting atop a pyramid of subsidiaries. It was more that a number of companies happened to have essentially the same directors. This allowed deals to be done between the companies that would never have taken place under normal market conditions. Further, as time went on, the number of companies and the scope for intra-group transactions grew. In 1875, the House and Lands Investment Trust (HLIT) was formed. Seven years later, Balfour expanded his empire with the formation of the London and General Bank. The Building Securities Company and Hobbs & Co were other entities under Balfour’s control.

Balfour used the nexus of companies to produce an appearance of prosperity when none actually existed. Robb (1992: 141) gives an illustration of how this worked: a property purchased for £52,000 by the LAC in September 1882 was sold the following January to the HLIT for £60,000 and then sold the same month to Hobbs & Co (which had been acquired by the Building Securities Company) for £134,000. At no time did any cash change hands; these were merely “paper profits”. In another case, money was siphoned out of the Liberator through overpriced purchases of land, one example of which was a property bought by Mr Alderman Newman (an associate of Balfour’s) for £16,000 which was sold eight days later to the Liberator for £26,000. Balfour’s use of what would now be considered “related party transactions” exemplified “the criminal potential of company groups” (Robb, 1992: 142).

Another device involved the valuation of unsold plots of land on the basis that each sub-plot could and would fetch the same price as had been obtained from the sale of the choicest sub-plot. This early variation on the modern approach of “marking-to-market” differed only in the treatment of the unrealized profit as available for distribution.

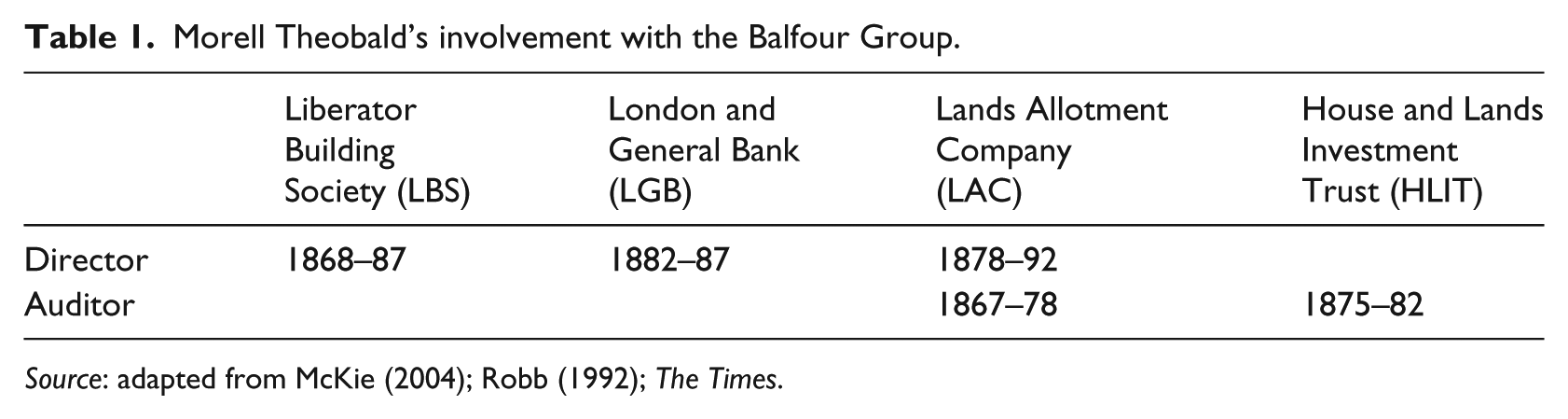

Balfour was able to get away with this because, as Ashworth (1980: 37) asserts, the directors and officers of the many companies set up by Balfour “were little more than puppets”, a claim corroborated by Price (1958: 296). Theobald too was “deeply involved” 10 (McKie, 2004: 113) in the companies in the Balfour group, as illustrated in Table 1. Theobald’s culpability lay not so much in what he did – although his conviction was for signing cheques based on fraudulent invoices from a builder – but in what he did not do. Like a few of his contemporaries and many of his successors, he failed both as auditor and as director to stand up to a dominant senior executive whose conduct he knew or ought to have known was wrong.

Morell Theobald’s involvement with the Balfour Group.

Source: adapted from McKie (2004); Robb (1992); The Times.

Such a close relationship between accountant and client contradicts the modern concept of auditor independence, but it was by no means unusual for the late nineteenth century. Maltby (1999) considers how practitioners of the emerging accounting profession justified their alignment with the management of large companies against the demands of speculative, small investors who were in it only to make short-term gains. Such a rationale may well have been appropriate in some cases but when it came to the Balfour group, the real speculators were those on the inside and the long-term stakeholders were ordinary depositors and savers looking to make provision for their old age. Another aspect of Maltby’s analysis of the rise of the professional accountant which seems particularly apposite in our case is the development of the concept of prudence. She argues (1999: 39) that “what was needed above all by companies was advice about the basis on which accounts were to be drawn up and profits distributed”. What professional accountants, she claims, brought to this question was prudence – a badge of “distinctive competence”.

There is some evidence that Theobald exemplified this quality, albeit to a limited extent. In March 1888, Theobald wrote to George Edward Brock, the chairman of LAC, offering advice on the transfer of balances between years and highlighting relevant prescriptions within the Articles of Association; “I am anxious above all things to be exact”. That same month he wrote to the secretary of the company refusing to sign cheques for dividends which had not yet been approved, stating that such premature payment would be “immoral” and that, if he had tolerated a “lax system” in the past, it must now stop (HO144-489-X39249D, 5, 21 and 22 March 1888).

On another occasion in April 1891, the Theobald partners wrote to Brock advising that he pay less of the profits by way of dividend and put more to reserve. Such a policy, they suggested, might prompt a recovery in the LAC share price (HO144-489-X39249D, 4 April 1891). They were not writing as an ineffectual director or complicit auditor but as executors of the estate of their late uncle, Dr Morell, in which capacity they controlled one of the largest shareholdings in the LAC. 11 However, no notice was taken of this advice.

On a different matter, Theobald wrote to Balfour saying that he was unable to join a company board without his partners’ consent and they looked upon the use of non-professional auditors by the Building Securities Co as a grave mistake. He therefore asked Balfour to allow him to retire from the board (obviously already having accepted the appointment!) (HO144-489-X39249D, 25 November 1884). Balfour immediately rebuffed him saying that it was the unanimous feeling of the other directors that the “special knowledge and business qualifications of the Gentlemen named as Auditors far outweigh the advantages, if any, of having the Audit conducted by professional Accountants” (HO144-489-X39249D, 25 November 1884, emphasis added). Theobald returned to this topic some years later in concluding his letter of resignation with the belated complaint that “I should like better Auditors. The weakness of our ‘corner’ Auditors is becoming proverbial” (HO144-489-X39249D, 14 March 1892). In the same letter leading up to his resignation from the LAC, Theobald set out his objections to the accounts: profits were being anticipated, dividends were being declared without due regard to the measurement of profit, assets were overstated and new directors were needed. But even this high-minded stance could not be carried out without some subterfuge. Rather than resign, Brock suggested, why not simply not seek re-election? The compliant Theobald agreed.

Fraudulent schemes such as Balfour’s can endure when times are good but nearly always come unstuck once economic conditions harden. Such was the case with the Liberator. In 1892, the economy was in recession and the flow of savings began to dry up. Concerns were voiced about the stability of some financial institutions. When faced with searching questions, even until the very end, Balfour tried to bluster his way through the difficulties, reassuring investors that his enterprise was as safe as the Bank of England, a mere 48 hours before the Liberator’s collapse (Nottinghamshire Guardian, 18 November 1893: 5). The end came when both the London and General Bank and the Liberator suspended payment on 2 September 1892. The extent of the collapse was such that Balfour received international notoriety and somewhat deserved the soubriquet “the champion hypocrite of England” (New York Times, 15 April 1906: np).

At the time of its failure the Liberator had grown to become the largest building society in the country (Ashworth, 1980: 36). The crash cost investors and savers £8m. A public fund to help relieve the distress of the ruined depositors managed initially to raise only £114,000 (Price, 1958: 303), though repeated calls to the public were made over the next 20 years. It cost the building societies movement a loss of the trust of the investing public from which it took years to recover (Ashworth, 1980: 43) and an equally long time for shareholders to see any return on their investment. 12

For Balfour and his accomplices, the crash was to cost them their freedom. A number of criminal cases against those involved in the management of Balfour companies followed. At the end of one, Mr Justice Hawkins allowed emotional expressions regarding the resulting financial devastation to creep into his summing up: He was told that the prisoners had homes and families who would be ruined by their conviction and brought from affluence to beggary; but had it ever occurred to them to think of the many hundreds and thousands of little homes which they had been the cause of rendering desolate and wretched? Had they ever thought of those poor people whose sad losses had left them beggars in their old age, and who were now absolutely ruined by the loss of all the little treasure which they had put by for their declining years?

He admitted to feeling no sympathy for the accused as he sentenced Hobbs and the group’s solicitor, Wright, to 12 years imprisonment for forgery and Newman to five years (HO144-489-X39249B).

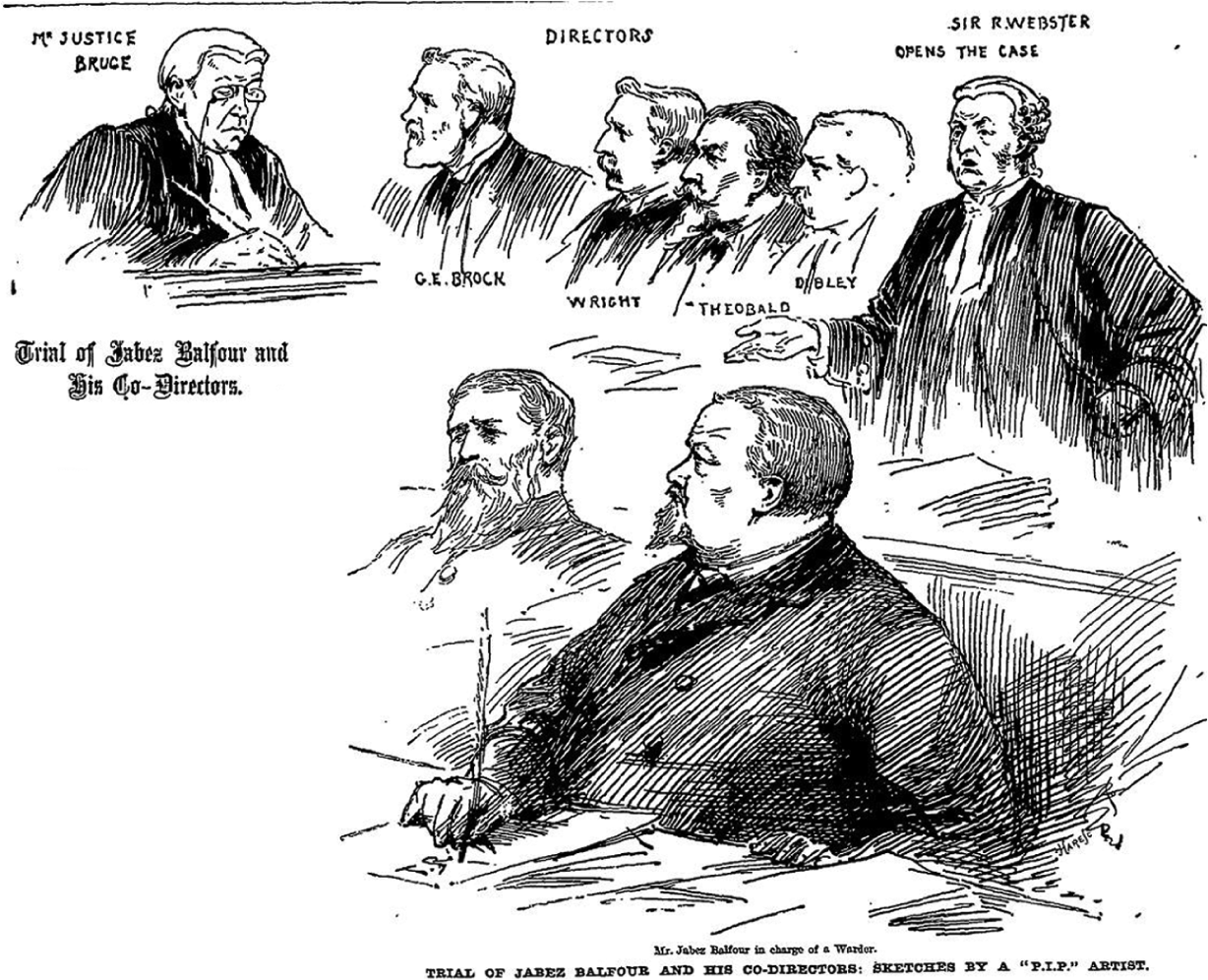

Theobald found himself accused of falsifying the books of the Lands Allotment Company. In his defence, he had argued before the court (see Figure 2 for an artist’s impression of the courtroom scene) that he was ignorant of both matters of business and accounts. The Accountant poured scorn on this admission stating that he “has doubtless during the last fifteen years gained much benefit from his association with the Institute. We suggest that it is not really open to him at this late hour to plead that he never ought to have been admitted a member” (The Accountant, 30 November 1895: 955). Subsequently, a correspondent stated that his own brother, William, had said that Theobald was not a competent accountant (The Accountant, 7 December 1895: 986). At one point during the trial Theobald appears not to have appreciated the seriousness of his situation; he was seen to smile (after attributing blame to one of his clerks), for which he was scolded by the Registrar of the court (Manchester Times, 31 March 1893: 3). Theobald was convicted and sentenced to four months’ hard labour – he was 67 at the time (The Accountant, 30 November 1895: 955; 1 February 1896: 99).

The trial.

Theobald’s conviction brought about the end of the old partnership (The London Gazette, 29 November 1895: 6944), though the remaining partners continued the practice under a new partnership. 13 Morell Theobald was expelled from the ICAEW in 1896 (The Accountant, 8 February 1896: 108). Possibly one of his final professional engagements was when he was elected as auditor for the one of the paranormal societies with which he became heavily involved (Journal for Psychical Research, Vol. VII, 1895–96: 20). 14

Legislation followed the Liberator’s collapse in the same way as greater regulation came in the wake of the fall of the Albert Life Assurance Co, although this time “Parliament passed the Building Societies Act of 1894 … stipulating that auditors be professional accountants” (Robb, 1992: 141). This of course ignored the fact that in some of the companies’ cases, at least for some of the years, a firm of chartered accountants had been involved in the audit. According to William Theobald (who audited the Liberator), apart from the audits of the HLIT and LAC, Morell Theobald “had practically no other experience as an accountant” (The Times, 12 November 1895: 3).

William Theobald escaped criminal prosecution but faced civil proceedings during which doubts began to surface about his independence, if not his competence, in connection with the Liberator group. In Re the Liberator Permanent Benefit Building Society (The Accountant Law Reports, 1893, 10 June: 73; 17 June: 80; 24 June: 82), William first stated that he was the directors’ auditor; later, when pressed, he admitted that he also had a duty to the shareholders. The disclosure that Theobald Bros & Miall had been paid commission amounting to £3,444 for introducing customers to the Society could not have added to his reputation.

Upon Morell Theobald’s imprisonment at the end of November 1895 a campaign for his release was instigated. Letters on file in the National Archives reveal a petition by his supporters who naturally include his wife and brothers. The former pleads with the Home Secretary, Sir Matthew Ridley, for her husband’s release on the grounds that she knew he could not have committed fraud and that Theobald was entirely ignorant of anything going on in the other companies. She claimed that Theobald had been a “thoroughly consistent Christian gentleman both in his dealings in the city and in connection with his private and Church life”. Furthermore, she claimed that “if he erred in his judgement and trusted those he believed to be worthy of trust, that should not be criminal”. An element of class superiority is to be seen in her petition: the jury, she claimed, could not have been capable of grasping the whole of a most complicated case being “drawn from men in an altogether different position of life”.

Theobald’s own solicitor felt the need to point out the injustice of having men on the jury who would be unlikely to understand accounts; they included six publicans and several other tradesmen “none of whom could fairly be said to be in the same station of life”. The Treasury solicitor was forced to admit that Theobald had borne a “high character” but at the trial he appeared to be a “very broken man”. 15 However, at the time the offences were committed Theobald had not a feeble mind, but a weak character. His offences were committed not through ignorance but through a lack of “sufficient moral fibre”. Theobald had protested against the accounting treatments being adopted; his objections had been ignored yet he remained a director until the final year and even then he allowed the balance sheet for 1891 to be published. It is only because men of “character” lent their names to dubious transactions that the fraud could have been carried out and the public’s confidence maintained in the companies. On balance, in the view of the Treasury solicitor, the sentence was lenient.

Concluding remarks

The association with fraud was a feature of the development of the modern accounting profession. Though professional claims to be able to prevent and detect fraud may have been exaggerated at the start, auditing practitioners soon began to enjoy a reputation for honesty and integrity as well as an ability to assist clients in avoiding becoming the victims of fraud. Occasionally, as Chandler et al. (2008) have shown, chartered accountants were themselves implicated in the sort of deceit and dishonesty against which they claimed to offer some protection. The case of Morell Theobald is more or less unique in that his own accounts of the paranormal activities which are supposed to have happened in his home provide us with sufficient evidence to question whether he is likely to have been effectual in his professional capacity. We are unable to conclude whether he was complicit in manipulating either the manifestations of the supernatural events themselves or the reports of the events – or whether he was simply very gullible. Whatever the truth may have been, that the word “fraud” should be used so frequently by others in referring to Theobald in the non-professional aspect of his life must cast further doubt on his ability to conduct himself professionally according to the principles expected of a chartered accountant.

Although at the time that Theobald was a practising accountant, the term “professional scepticism” had not yet been coined, nevertheless accountants were expected to bring a degree of enquiry to their work. We have presented evidence that shows that he was aware of at least some of the unacceptable practices in the Balfour group, that he tried to put an end to them but what he did was too little, and too late to be effective in preventing the loss of millions of pounds of investors’ money.

It is possible, but it seems unlikely, that one could be questioning in a professional capacity while being entirely gullible in a personal capacity, at least to the extent of Theobald’s credulity. In fact, Theobald appears to have been a weak individual in both aspects of his life. It is perhaps as well for the accounting profession that his name is today more likely to be remembered for his belief in matters spiritual than for his lack of ability as a professional auditor. In making such a judgement, we intend no disrespect to those who hold spiritual beliefs. It is possible to have religious and spiritual faith while at the same time being prepared to question matters of an earthly and materialistic nature. There have even been successful accountants since Theobald who have taken up the spiritualists’ cause. One noteworthy example is James Arthur Findlay CA, OBE, JP (1883–1964) of the firm Findlay, Kidston & Goff who retired from business at the age of 40, wrote several books on spiritualism, 16 founded the International Institute of Psychical Research, and on his death bequeathed his large country house, Stansted Hall, to the Spiritualists’ National Union and the Arthur Findlay College.

Few now subscribe to spiritualism. Data from the British Election Study 2009–2010 reveal that out of nearly 17,000 people who completed an on-line survey, just over 500 indicated their religious affiliation as “Other”, that is, not belonging to one of the mainstream religious groups. Research by the University of Manchester analysed those respondents in the “Other” category and found that spiritualism was the third largest group behind non-denominational Christians and Pagans, but ranked above better known religious minorities such as the Salvation Army, Mormons, Lutherans, Jehovah’s Witnesses, and Quakers (McAndrew and Clements, 2011), though this may well be attributed to the respondents mistaking “spiritualist” for “being spiritual”, a far more nebulous concept (http://www.vexen.co.uk/UK/religion.html #CensusResults).

However, while spiritualism still has its adherents, its heyday was the second half of the nineteenth century. Its decline is attributed to growing scepticism amid clear evidence of fraud on the part of its leading practitioners (Lamont, 2004: 915). Quite simply, even those who had suffered serious bereavement were no longer prepared to take things at face value.

Epilogue

The 1901 Census records Morell Theobald, at 72 years of age, as an insurance broker living at the same Blackheath, London address, with his wife, his daughter Ellen – now 37 years old – and one servant. He lived long enough to celebrate his golden wedding anniversary (The Times, 5 June 1906: 1) but died two years later on 24 July 1908 in Lee, Kent, leaving an estate of just over £1,330. His brother, William, also became an insurance broker, though he did not resign from the ICAEW until December 1911. He died on 7 September 1912 leaving an estate valued at £3,175. His wife, Louisa, had died less than two months earlier leaving an estate of £4,551. The various court cases would have involved the Theobald brothers in great expense, but their days in court did not ruin them.

Theobald’s books on the subject of spiritualism (Theobald, 1884 and 1887) have long been forgotten and perhaps deservedly so since large tracts are little more than catalogues of daily activity within his household. Although he may have intended some of the events to have appeared wondrous, the fact that they all were capable of rational explanation is likely either to frustrate or to bore the modern reader. A more enduring and possibly more fitting tribute to such an odd character as Morell Theobald may be that his books are said to have provided the inspiration for a chapter on séances in the Grossmiths’ much-loved and still popular 1892 satire of Victorian life, The Diary of a Nobody.

Footnotes

Acknowledgements

We are extremely grateful to the anonymous reviewers for their very helpful comments on earlier drafts and the unstinting support of the editorial team. Our thanks also go to Ms Jo Thompson for supplying us with the photo of Morell Theobald from her family tree.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.