Abstract

In this article, we examine the role, status and autonomy of teachers at English private accountancy tuition providers from 1980 to the present. We argue that, during this period, teachers transformed from ‘rock stars’ who enjoyed significant status and autonomy over their work to ‘hygiene factors’ in a largely standardised and commodified teaching environment. Growing cost pressures on tuition providers and an increasing emphasis on the quality and consistency of the learning experience are identified as significant factors in this transformation. We discuss these findings with reference to current developments towards corporatisation and marketisation in the English higher education sector.

Keywords

Introduction

Against the background of a wider shift towards neoliberal forms of government (Miller and Rose, 2008), higher education has gradually become more managerial, corporatised and marketised in many developed countries over the last 30 years (e.g. Marginson and Considine, 2000; Tuchmann, 2009). In England, where this study is located, successive governments have sought to foster market forces in higher education by inter alia increasing tuition fees, cutting government funding, removing student recruitment caps and placing greater emphasis on teaching quality as well as student satisfaction (Browne, 2010; DfBIS, 2015). As a result of these reforms, the English higher education sector is moving towards a competitive market place where increasing emphasis is placed on delivering consistent levels of high-quality teaching at the lowest possible cost.

The corporatisation of universities and its implications for accounting education have been widely debated (e.g. Broadbent, 2011; Evans et al., 2010; Guthrie and Parker, 2014; Humphrey and Gendron, 2015; Parker, 2011, 2012, 2013). A number of studies have suggested that corporatisation would lead to more instrumental, vocational, technical and textbook-driven approaches towards teaching (e.g. Evans, 2010; Parker, 2005, 2013). Others have argued that corporatisation would result in an increasing separation between research and teaching (e.g. Hopper, 2013; Neumann and Guthrie, 2002). Concerns have also been expressed that accounting teachers would increasingly be employed on casual and part-time contracts (e.g. Churchman, 2002; Parker, 2011).

While marketisation is a relatively recent experience for English universities, private accountancy tuition companies, which provide most of the professional accountancy training in England (King and Davidson, 2009), have operated in a highly commercial environment characterised by increasing cost and quality pressures for decades. In this article, we examine the role, status and autonomy of teachers at such tuition companies from 1980 to the present, with a particular focus on the market for Institute of Chartered Accountants in England and Wales (ICAEW) tuition. We subsequently discuss our findings with reference to current developments in the English higher education sector.

This article aims to contribute to our understanding of the history of accounting education (e.g. Birkett and Evans, 2005; Clarke, 2005; Evans and Juchau, 2009; Flesher, 2010; Paisey and Paisey, 2006) in two ways. First, we seek to complement the strong focus of the extant literature in this area on the work and legacies of early pioneers and other influential historical figures in accounting education (e.g. Carnegie and Williams, 2001; Clarke, 2005; Flesher, 2010; Parker, 1994, 1995; Shelton and Jacobs, 2015; Trow and Zeff, 2010; Zeff, 2000) by examining the history of rank and file accounting educators.

Second, we seek to complement the extensive literature on the history of accounting education in the university setting (Craner and Jones, 1995; Maunders, 1997; Napier, 2011; Parker, 1997; Van Wyhe, 2007a, 2007b; Walker, 1994; Zeff, 1997) by exploring the historical role of accounting teachers in the private sector. With the exception of Edwards’ (2009, 2011) work on private accountancy schools in the early modern period, the history of accounting education in commercial settings remains largely unexplored. This is particularly unfortunate in the English context, where private sector tuition companies rather than universities dominate accountancy training (King and Davidson, 2009).

The remainder of this article is structured as follows. In the next two sections, we introduce the context of this study and discuss the methodology we adopted. In the subsequent section, we show how the role of ICAEW tutors transformed during the period investigated by this article. Finally, a concluding section summarises the findings of this article and discusses their potential implications for the higher education sector.

ICAEW training

Since ICAEW’s creation in the late nineteenth century (Walker, 2004), its training process has developed along a different trajectory from other English professions and, indeed, accountancy bodies in other national contexts (Annisette and Kirkham, 2007). English law, medicine and engineering, as well as accountancy bodies in countries such as Australia and the United States, increasingly came to rely on universities to deliver professional training during the nineteenth and twentieth centuries (Annisette and Kirkham, 2007). The ICAEW qualification, meanwhile, remained relatively disconnected from universities. To this day, it is open to graduates of all academic disciplines as well as to non-graduates. 1 Although numerous universities have started to offer accounting degrees which grant exemptions from professional examinations, accountancy graduates still make up only a relatively small proportion of ICAEW’s student intake (Annisette and Kirkham, 2007).

The absence of universities as a central player in ICAEW training presented an opportunity for private tuition providers. Within a decade of the Institute’s creation in 1880, companies including Cloughs and Foulks Lynch started to offer correspondence courses which promised to help aspiring accountants pass their professional examinations (Foulks Lynch, 1955; Solomons and Berridge, 1974). After World War II, private tuition providers started to offer residential courses aimed at wealthy, self-funded students in London and a small number of provincial locations, including Caer Rhun Hall (Anderson-Gough, 2009; Foulks Lynch, 1955). 2 As the market for accounting work expanded in the 1960s and 1970s, accountancy firms increased their trainee intakes and suitable recruits became short in supply. In order to compete for the best candidates, firms started to fund classroom-based tuition courses for their ICAEW trainees. These developments attracted a number of new companies into the tuition industry. Financial Training (which rebranded as FTC in the 1980s) and The Accountancy Tuition Centre (which rebranded as ATC in the 1980s) were founded in the 1960s, and Brierley, Price and Prior (BPP) entered the market in 1976. All three companies offered classroom-based tuition courses in London and, to a much lesser degree, in the largest provincial cities such as Manchester.

Against the background of the deregulation of the British financial services industry initiated by the Conservative government of Margaret Thatcher in the 1980s (e.g. Barnes, 2007), the demand for accountancy services increased significantly. ATC, BPP and FTC, which dominated the ICAEW tuition market in the 1980s and 1990s, catered for the resulting increase in accounting trainees by offering courses in a wider range of provincial cities, including Newcastle and Sheffield. In 2003, ATC was taken over by FTC, which was in turn swallowed by Kaplan, an American company. Today, BPP and Kaplan remain the two largest ICAEW tuition providers in England.

The principal customers of ICAEW tuition providers are large accountancy firms, which offer actuarial, audit, consulting, legal and tax services. They recruit graduates from a wide range of disciplines and support their trainees by giving them time off to study and pay for their exam tuition. In the 1980s, eight accountancy firms dominated the audit market. After a series of mergers (KMG and Peat Marwick Mitchell in 1987, Ernst Whinney and Arthur Young in 1989, Deloitte, Haskins & Sells and Touche Ross in 1989, Price Waterhouse and Coopers & Lybrand in 1998) and the demise of Arthur Anderson in 2002, four large firms remain today: Deloitte, Ernst & Young (EY), KPMG and PricewaterhouseCoopers (PWC). They are collectively known as the ‘Big 4’ accountancy firms.

Methodology

We have adopted an oral history approach for the purposes of this study (e.g. Collins and Bloom, 1991; Hammond and Sikka, 1996; Haynes, 2010; Walker, 2008). Written sources, on one hand, often reflect the views of the powerful and privileged. Oral histories, on the other hand, give us access to the voices from below, those ideas, opinions and experiences which are often missing from official records and documents. As such, we believe that this approach is particularly well suited to our aim of exploring the role, status and autonomy of rank and file accounting teachers.

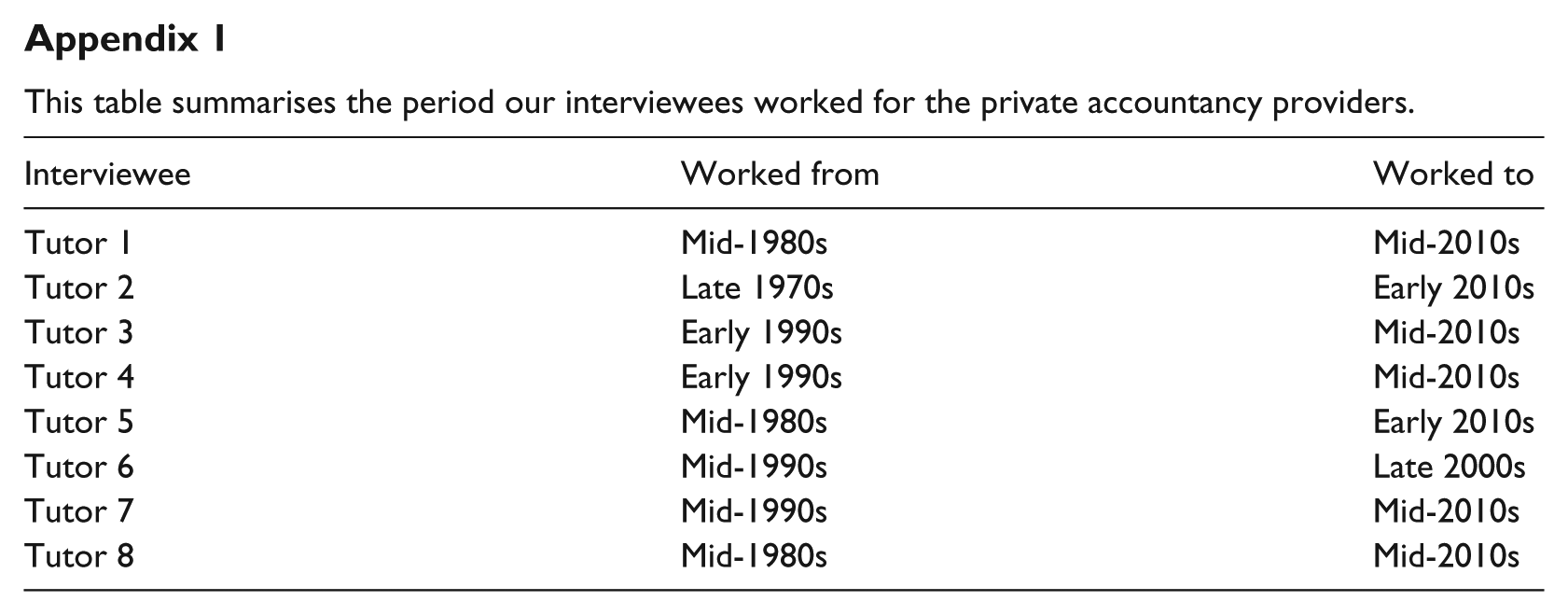

We interviewed eight tutors who had worked at private sector accounting tuition companies for significant parts of the period investigated by this article. One of the interviewees started to work for tuition providers in the late 1970s, three in the 1980s and four in the 1990s. Most were still working in the industry at the time they were interviewed or had done so until quite recently (see Appendix 1 for further details). The interviewees were selected with the help of recommendations from contacts of the authors who work at tuition companies and professional accountancy bodies. Six of the interviews were conducted by single members of the author team. The remaining two interviews were jointly conducted by two members of the team. All of the interviews took place either over the telephone or face to face at locations of the interviewees’ choosing. They lasted 64 minutes on average, with the shortest taking 36 and the longest 89 minutes. A set of semi-structured questions was designed based on our understanding of the accountancy tuition industry and our reading of relevant literatures. We assured interviewees that they would remain anonymous in order to encourage them to comment as freely and openly as possible about how various aspects of their occupation had changed during their working lives. The responses of our interviewees were electronically recorded and partially transcribed. The transcripts were subsequently subjected to a qualitative content analysis, whereby we manually coded the data according to an inductively developed set of categories. The analysis of each interview was initially performed by the author(s) who had conducted the interview and subsequently verified by at least two other members of the research team.

The role, status and autonomy of ICAEW teachers from 1980 to the present

In this section, we discuss changes in the role, status and autonomy of ICAEW tutors from the 1980s to the present. In the first sub-section, we explore the position of accounting tutors during the 1980s and early 1990s. The second sub-section subsequently examines the emergence of cost and quality pressures in the accounting tuition sector from the mid-1990s onwards as well as their implications for accounting tutors.

The 1980s and early 1990s

In the 1980s and the early 1990s, the market for ICAEW tuition services was regionally fragmented. The various training centres across the country bid directly to the local offices of large accountancy firms for tuition contracts. Tutor 6 explained that There wasn’t very much strategic management of those firms back in those days. ATC Birmingham was very different from ATC Nottingham, which was again very different from ATC London. There was no national consistency, there was no national strategy and of course there was no national client base […] you could have Price Waterhouse in Birmingham and somebody else could have Price Waterhouse in Nottingham.

3

According to Tutor 4, these contracts were won on the basis of the skills and reputations of the individual tutors employed by the local training centres. He suggested that the accountancy firms wanted to ensure that their trainees were taught by the most skilful and effective tutors, and as a result, these locally negotiated contracts often contained ‘preferred tutor lists’, which specified the tutors who would work with a particular accountancy firm. This emphasis on individual tutors meant that successful teachers could make a ‘name’ for themselves and develop considerable market power. Tutor 4 referred to these tutors as the ‘rock stars’ of the industry. Tutor 6 described them as ‘maverick superstars’.

Tutors enjoyed considerable power in these companies. The private tuition companies did not employ professional managers, so some of the tutors combined their teaching roles with management responsibilities. As Tutor 4 put it, ‘We ran the business in our lunchtimes’. Tutor 1 similarly commented, When I started there was only 5 of us [at the training centre], all ICAEW qualified and we were all of a sudden running our own business, not necessarily having had any experience of running a business before. We went there because we wanted to be tutors but actually you had to do everything; you did client liaison, you did marketing, you did everything.

Accountancy tutors also enjoyed a significant degree of autonomy during the 1980s and the early 1990s, which covered all aspects of the teaching process including course design, course duration, course content as well as discretion over the teaching materials and methods they employed in the classroom. Tutor 1 explained this situation in the following terms: ‘We told the clients how long the courses needed to be and when their students should come. We designed the courses and told them what they had to do’. She further explained that ‘there was no such thing as [standard] class notes. I decided what I was teaching. And there were quite a lot of students copying down what I was writing on the screen’. Tutor 1 also noted that with regard to the lowest level of the ICAEW qualification at the time, the Graduate Conversion Course, the autonomy of tutors even extended to course assessment, as tutors themselves were responsible for setting and marking the end of course examination.

Tutor 8 suggested that during the 1980s, some tuition companies started to introduce standardised study materials such as ‘study manuals’ and ‘question banks’, which were intended for students to use in their own time outside of class. Moreover, Tutor 5 suggested that by the late 1980s, some providers had developed standardised ‘classroom materials’, which tutors could use during their classes. According to Tutor 5, the tuition providers started producing these centrally designed materials as a potential way to differentiate their offering and attract more business. He further explained that the adoption of standardised materials in the classroom was patchy at best since it was neither enforced nor controlled.

Tutors at the time tended to only teach one particular subject area (e.g. financial accounting, audit, tax or management accounting), in which they were particularly expert. Tutor 6 remembered that when he was a trainee accountant in the early 1990s, one of his tutors was a regular and high-profile contributor to the process through which proposed new accounting and financial reporting standards were made available for public scrutiny. As a result of their expertise and reputations, students were generally respectful of the tutors and at times ‘may have felt somewhat intimidated’ (Tutor 6). Tutor 8 suggested that good tutors were ‘revered’ by students in the 1980s and early 1990s.

Tutors were not only recognised as experts of their subjects but also tended to be excellent communicators with an ability to engage their audience. As Tutor 5 explained, In the past, the skill of the tutor was being able to explain how to solve a complex problem using a simple step-by-step method: follow this method and you’ll get the right answer. The tutors in those days were much better at explaining things because they had to work it out for themselves.

Tutor 2 felt that the teacher’s ability to engage students was a significant factor: To my mind the most important thing about recruiting a new teacher was always that they had a certain charisma […], it’s about having that spark, having that something to engage people.

The power and status of tutors was reflected in the salaries they earned. In the 1980s and early 1990s, the salaries of new tutors were superior to other opportunities available for recently qualified accountants. Tutor 1, for example, commented on her own experience when she started working as a tutor in the mid-1980s: ‘When I left [large accountancy firm], I had a massive pay rise and a company car. It was financially attractive’. Tutor 4 even suggested that he received a small pay rise when he left a well-paid job with a London investment bank to become an accountancy tutor in the early 1990s. The opportunities and financial rewards on offer attracted many highly ambitious, intelligent and entrepreneurial people into the private accountancy tuition sector. Tutor 8, for example, suggested that one of his fellow tutors from the 1980s subsequently went on to serve as a Cabinet Minister in the British government.

Not all tutors, however, succeeded in this environment. New tutors received relatively little by way of structured support and training to prepare for the role. Instead, new tutors would spend their first month or so observing more experienced tutors to learn first-hand from their approach and to develop their own lecture notes. Once tutors started teaching in class, regular feedback from students who typically had very high expectations of the quality of tuition meant that only the most effective teachers survived. As Tutor 2 explained, ‘It was a sink or swim situation’. Those tutors who did not perform well in the classroom generally left of their own accord. As Tutor 1 remembered, ‘It was such an unpleasant experience if it wasn’t going down well that they didn’t stay’. Tutor 3 suggested that teachers could also be ‘red-carded’ if they were deemed to be underperforming: Students talk about the tutors and word of mouth spreads positive attitudes, and also bad perceptions of poor tutors. A bad tutor would be red-carded – if students complained the tutor would be taken off the course and replaced […] This was not common but happened especially if there was a group of students from one employer who ganged up on a tutor.

Tutor 4 similarly remarked that students from one of the big chartered accountancy firms in particular were known to ‘hunt in packs’.

The mid-1990s to the present

From approximately the mid-1990s onwards, large accountancy firms became increasingly dissatisfied with the tuition providers. Our interviewees indicated that there were two principal reasons for this. First, the accountancy firms felt that the quality of the tuition their trainees received was too variable. According to Tutor 6, ‘the accountancy firms noticed that there was a postcode lottery with student experience and pass rates depending on the approach taken by the various tutors’. Second, they felt that tuition was becoming too expensive. Tutor 8 explained that at times in the 1980s and 1990s, representatives of the tuition companies ‘used to stroll into their clients’ offices and tell them that fees are going up 15 per cent next year – there came a point when the accountancy firms said enough is enough’. 4

In response to these concerns, the large accountancy firms put pressure on the tuition providers to offer a less expensive and more consistent tuition experience. Tutor 4 explained that the principal mechanisms whereby large accountancy firms put pressure on tuition providers were the introduction of national training policies and the ‘single sourcing’ of exam tuition. He suggested that the accountancy firms wanted their trainees to have a similar tuition experience across the country; that they wanted students to spend less time in the classroom and to enjoy the same teaching approach and amount of teaching time regardless of where in the United Kingdom they were located. Tutor 4 further explained that in order to achieve this, the accountancy firms moved away from the then established practice that their regional offices procured tuition through locally negotiated contracts and towards awarding a national contract to a single tuition provider, which would cover the exam training of all their trainees. The single sourcing of tuition seemingly strengthened the bargaining power of the large accountancy firms and allowed them to enter into tough negotiations on both the price and the nature of the service provided by tuition companies. Tutor 2 summarised these developments in the following terms: The tuition firms used to dictate everything – times of courses, what was happening. There was no liaison with the accounting firms with regard to content or timing. That started to change with cataclysmic changes in the ‘90s and ‘00s so that now the power relationship is completely the other way around.

The large accountancy firms also put pressure on ICAEW to address their concerns regarding the cost and quality of exam tuition. ICAEW was initially slow to respond to these concerns. However, after EY decided to have their recruits train towards the Institute of Chartered Accountants of Scotland (ICAS) rather than the ICAEW qualification in 1998, ICAEW responded by taking control of their educational materials, including the study texts, progress tests and question banks which had to be used in class. In this way, ICAEW was able to accommodate the concerns of large accountancy firms as well as ensure the quality and consistency of the study materials. Tutor 5 felt that this development also weakened the position of the tuition providers: By 1998 ICAEW were producing their own materials and ICAS was being offered as an alternative qualification. This was all about taking the power off the tutor firms.

5

In order to comply with the demands of the national training contracts, mandate the use of ICAEW’s educational materials and remain profitable in an increasingly competitive environment, the tuition providers started to standardise their teaching practices. To this end, the tuition providers created ‘subject specialist’ roles. Tutor 7 explained that subject specialists were assigned national responsibility for deciding how a particular subject should be taught within a particular tuition company. She suggested that subject specialists dictated precisely how many hours tutors should spend on each topic, which examples and questions to practise in class and which exercises should be given as homework. They were also responsible for developing ‘prepped files’, which gave tutors ideas of stories to tell and ways to put across complex ideas (Tutor 7).

The consistency of the learning experience became an important priority for the tuition providers. Tutor 7 commented that ‘if we are running a national contract our company needs to be certain that everyone gets the same level of service’, while Tutor 4 suggested that inconsistencies came to be seen as a ‘nightmare’. This emphasis on consistency is further exemplified by the fact that tuition providers forbade tutors to give students any personally developed handouts in addition to the standardised learning materials so as to ensure that no student would get an advantage over their peers.

With this emphasis on consistency and standardised learning processes, the technical expertise of tutors became less important. Tutor 5 explained that while teachers had historically specialised in one particular subject in which they were particularly knowledgeable, the advent of standardised learning materials enabled them to teach a wider range of subjects. Standardised materials also helped new teachers, who moreover started to benefit from formal induction schemes in the 2000s and 2010s. Tutor 7, for example, explained that new recruits are now put on 2-year-long training and mentoring programmes and that they are given carefully calibrated timetables that allow them to develop their technical and teaching skills. Thus, the tuition providers moved away from the ‘sink or swim’ (Tutor 2) attitude towards new staff which they had displayed in the 1980s.

From the mid-2000s onwards, online teaching and examinations started to play an increasing role in the ICAEW tuition market. This development once again appeared to be motivated by economic reasons. Tutor 2, for example, suggested, I don’t think that online exams improve students’ ability to do tax or their knowledge of tax. I think the drive for online exams is purely to reduce the turnaround time of marking and to reduce the cost of marking. I don’t think it’s anything to do with educating students or producing better qualified accountants.

Tutor 1 highlighted positive and negative effects of the adoption of new technologies. On the plus side, she noted that they made it possible ‘to get through things quicker’. On the minus side, she suggested that the rise of online multiple choice exams in particular had resulted in ‘dumbed-down’ teaching approaches which were even more ‘exam-driven’ than in the past. Moreover, Tutor 4 noted that the emergence of online teaching required different skills from tutors than those required in the traditional classroom setting. Specifically, he argued that the online format put more emphasis on delivering the teaching content in a structured and coherent manner, while the ability to ‘engage in banter’ with the students, which had been a key component of success in the physical classroom, was much less important.

Overall, many of our interviews suggested that the role of the teacher in private accountancy tuition had become ‘commodified’ since the mid-1990s (see Lawrence and Sharma, 2002; Milton and O’Connell, 2009). As the large accountancy firms started to single source their tuition requirements and ICAEW took control of their learning materials, tutors lost much of the power and autonomy they had enjoyed in the 1980s and the early 1990s. In the face of strong pressures to reduce the cost and increase the consistency of accountancy tuition, the providers standardised almost all aspects of the tuition process. The ‘name’, personality, charisma and expertise of the tutor no longer mattered, and ‘preferred tutor lists’ started to disappear as the role of the tutor was largely reduced to delivering a standardised set of learning materials in as consistent a manner as possible. According to Tutor 4, the teacher had become a ‘hygiene factor’, 6 while Tutor 7 described the role of the teacher from the mid-1990s onwards in the following manner: ‘You are part of a big machine. It is the machine that the students will remember’.

These changes in the role, status and autonomy of tutors had implications for their remuneration, working conditions and promotion opportunities. Regarding remuneration, the circumstance that tuition programmes were no longer sold on the basis of tutors’ reputations meant that the tuition companies no longer had to offer large salaries to ‘rock star’ tutors. Instead, they could hire ‘generic young professionals’ (Tutor 6) to communicate the high-quality, standardised learning materials to the students. These ‘generic’ tutors could easily be replaced and had much less market power than the ‘rock stars’, which had significant implications for their salaries. While in the 1980s and early 1990s, tutor salaries had compared favourably with practice and even investment banking, Tutor 2 suggested that in the early 2010s, ‘you would have to take a pay cut, generally, to move [from practice] into accountancy tuition’. Tutor 3 even remarked that the pay differential between private accountancy tuition firms and universities, which had been large in the past, had decreased to such an extent that by the mid-2010s, some of the ‘better people are being taken into the university sector’.

In addition to deteriorating pay, teachers found fewer opportunities for promotion and advancement in the 2000s and 2010s as a strong separation between teaching and managerial staff emerged at accountancy tuition firms. According to Tutor 8, At BPP and Kaplan they have now consciously separated teaching from management – so the managers manage and the teachers teach, whereas back in the old days the route to a good job in management was to be a good teacher to begin with.

The cost and quality pressures that emerged in the industry from the 1990s onwards not only had implications for tutors’ salaries and career opportunities but also for their workloads. Tutor 7 explained that single-sourced, national contracts often stipulated longer teaching days and required tutors to provide regular feedback on students’ performance in, for example, practice tests and mock exams, which added to the reporting and marking requirements of tutors. As a result, she suggested that teaching workloads had increased significantly from the early 2000s onwards.

As the power, autonomy and remuneration of accountancy tutors declined, the industry started to attract a new type of tutor in the 2000s and 2010s. Many of the ‘rock stars’, the charismatic, entrepreneurial individuals who had thrived in accountancy tuition during the 1980s and the early 1990s, left the big tuition providers. Tutor 6 suggested that for ‘rock star’ tutors, ‘teaching to standard Powerpoint presentations was pretty grim’. The ‘rock stars’ were replaced by a new kind of tutor, which Tutor 4 characterised as ‘teacher types’. Tutor 8 offered the following assessment of the latest generation of accountancy tutors: By and large accountancy tutors are a little bit disappointing compared to how they were 30 years ago […] there seemed to be more go-getters in the 1980s, [now] the job seems to be attracting less ambitious, slightly less able people […] you don’t quite find that level of ambition.

Interestingly, while our interviewees generally suggested that the standardisation and commodification of accountancy tuition had negative implications for the role of the teacher, they felt that it had by and large been a good thing for the students. Tutor 3, for example, suggested that The lecture notes and question banks are now produced nationally and are very good, comprehensive and cover the whole syllabus. Students trust the material and think they had a good chance of passing the exams because of the material.

Tutor 7 similarly noted that ‘the syllabus coverage is now guaranteed by the materials. In the past, it was down to an excellent tutor to ensure they covered the full extent of the syllabus’, while Tutor 1 commented that ‘I think it is also important that you have got standardisation around the country so that you have not got a tutor teaching something that is wrong’.

Finally, it should be noted that although ‘rock star’ tutors have all but disappeared from the nationwide ICAEW contracts negotiated between large accountancy firms and the bigger tuition providers, they have not died out entirely. Rather, many of them have started small, independent training centres, which compete with BPP and Kaplan for the custom of (usually self-paying) students studying towards Chartered Institute of Management Accountants (CIMA) or Association of Chartered Certified Accountants (ACCA) qualifications. According to Tutor 1, these small, independent providers are reminiscent of the accountancy tuition industry in the 1980s and early 1990s: ‘It has come in full circle – the small colleges now are very much like the big tuition providers were 25 years ago – small centres set up by an entrepreneur’. Thus, it would appear that the ‘rock star’ tutor has found a new habitat in the CIMA and ACCA markets.

Concluding discussion

In this article, we have argued that a series of developments towards greater economy, quality and consistency in the private accountancy tuition industry had profound implications for teachers working in this sector. Specifically, we have argued that their role, status and autonomy changed significantly during this period – from powerful ‘rock stars’ who enjoyed great freedom in designing and delivering learning materials to interchangeable ‘hygiene factors’ whose role was largely restricted to communicating centrally produced, standardised content. As such, this article has made a contribution towards taking the historical study of accounting education into commercial settings (e.g. Edwards, 2009, 2011) and provided insights into the work of rank and file accounting teachers rather than the achievements of pioneering individuals (e.g. Carnegie and Williams, 2001; Flesher, 2010; Parker, 1994, 1995; Zeff, 2000).

While this article has focussed on teachers at private sector tuition companies, its findings will resonate with many accounting teachers working at universities in England (and possibly beyond). Many will recognise an increasing focus on costs, as huge cuts to central government funding for English universities have only been partially offset by higher tuition fees. Further significant cuts to the higher education teaching budget have recently been announced (HMT, 2015). The focus on the quality and consistency of the student experience will also have a familiar ring to many accounting teachers working in the English higher education sector. Good results in the National Student Survey, the government’s preferred quality measure, have become a central strategic objective for many universities. As a result, increasing pressure is put on teachers to achieve higher student satisfaction scores. A perceived need for consistency is also increasingly emphasised by the government and individual institutions. Jo Johnson, the Minister for Higher Education, has recently suggested that there was ‘too much variability in the student experience within and between universities’ (Morgan, 2015), while a senior management figure at our home institution recently warned us that ‘everybody needs to adopt best practice, we need consistency, we cannot afford inconsistencies’. 7

The findings of our article indicate that significant challenges may lie ahead for teachers in the higher education sector if the increasing emphases on costs and consistency lead to similar levels of standardisation and commodification as is evident in private accountancy tuition providers. Such developments could further reduce the power of university teachers (see Tuchmann, 2009) and accentuate existing trends towards casualisation (see Churchman, 2002; Parker, 2011). University teachers without a research profile, in particular, could find themselves at risk of sharing the fate of present-day private accountancy tutors and become ‘hygiene factors’.

Developments towards standardisation and commodification may not only pose challenges to university teachers but also to university education more generally. Standardised approaches work well in professional exam tutoring, where the ultimate aims and objectives of education are very narrow, clear and unequivocal. Passing a set of standardised exams is the be all and end all of accountancy tuition – the examination defines the very purpose of education (see Anderson-Gough, 2009). The goals and objectives of university education, however, are broad and loosely defined, ranging from personal intellectual development to improving one’s employability. Standardised and commodified approaches to higher education are unlikely to do this broad set of objectives justice and may have detrimental implications for intellectual diversity.

Footnotes

Appendix

This table summarises the period our interviewees worked for the private accountancy providers.

| Interviewee | Worked from | Worked to |

|---|---|---|

| Tutor 1 | Mid-1980s | Mid-2010s |

| Tutor 2 | Late 1970s | Early 2010s |

| Tutor 3 | Early 1990s | Mid-2010s |

| Tutor 4 | Early 1990s | Mid-2010s |

| Tutor 5 | Mid-1980s | Early 2010s |

| Tutor 6 | Mid-1990s | Late 2000s |

| Tutor 7 | Mid-1990s | Mid-2010s |

| Tutor 8 | Mid-1980s | Mid-2010s |

Acknowledgements

We would like to thank our interviewees for contributing their time and their invaluable insights to this project. We would also like to thank Elaine Evans, Catriona Paisey, three anonymous reviewers and the participants of the MARG Management Accounting Education Seminar (Aston Business School, November 2015) for their helpful comments on this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.