Abstract

This article aims to develop our understanding of the political activity of groups and individual key-players leading to the withdrawal of the Statement of Accounting Concepts No. 4 (SAC 4). The study also examines the arguments advanced by opponents of this rule, using archival data and semi-structured interviews. The key findings of the study highlight the importance of highly motivated, influential and passionate stakeholders in lobbying against proposed accounting rules. In addition, this event raises interesting questions relating to our understanding of Capture theory. This article shows how key-players within the standard-setting environment interacted with each other and lobbied to bring about the withdrawal of the mandatory status of SAC 4. This study adds to the academic literature by allowing individual key-players to explain their motivations and activities in their own words.

Introduction

In March 1992, Statement of Accounting Concepts No. 4 (SAC 4) Definition and Recognition of the Elements of Financial Statements was published by the Australian Accounting Research Foundation (AARF). However, a bit over a year later (June 1993), this document was removed and a modified document was re-issued in 1995 (SAC 4, 1995). Accounting Policy Statement (APS) 1 Conformity with Statements of Accounting Concepts and Accounting Standards conferred ‘mandatory’ status upon SAC 4 and the other three concepts statements (AARF, 1993). This meant that members of the then Australian Society of Certified Practicing Accountants (ASCPA) (currently CPA Australia) and the Institute of Chartered Accountants in Australia (ICAA) (currently Chartered Accountants Australia and New Zealand (CAANZ)) were required to follow SAC 4 in the preparation and audit of General Purpose Financial Reports (GPFRs).

The issuance of SAC 4 with mandatory status precipitated an unprecedented political campaign. The opposition to SAC 4 was so intense that eventually the professional bodies withdrew the mandatory status of all four concepts statements 1 (Peirson, 1993). This debate was very significant at the time. Howard (1994) cites several leading accounting identities who stated that this was the biggest issue to hit the accounting profession in 1993.

The aim of this study is to develop our understanding about the use of power in making accounting rules, in particular, to understand the nature of political activity surrounding the withdrawal of the mandatory status of SAC 4 and identifying the key-players involved in this political activity. Specific research issues addressed in the study include the following:

The identification of the interest groups affected by SAC 4 and the patterns of political activities of the interest groups which enabled them to be successful in the withdrawal of the mandatory status of SAC 4. The identification of the key-players within these groups involved in the removal of the mandatory status of SAC 4 and analysis of the political actions undertaken by these actors for the withdrawal of its mandatory status. An analysis of the reasons used by the interest groups and key-players for opposing the provisions of SAC 4 and its mandatory status.

Main interest groups and key-players within those groups were identified through an analysis of submissions and other archival data. Semi-structured interviews were used to obtain insights into the motivations and actions of 32 key-players. The relevant questions in the interviews focused on eliciting their reasons for opposing the mandatory status of SAC 4 and the political activities utilised to achieve this goal. Our article reveals how key-players within the standard-setting environment interacted with each other and lobbied to bring about the withdrawal of the mandatory status of SAC 4. We suggest that a substantial number of submissions and interviewees relied on specious or inconsistent arguments to oppose SAC 4, demanding higher standards for this statement than they required for existing mandatory rules. However, some argued that SAC 4 would increase the costs of preparing GPFRs for Australian firms relying on international capital markets.

The study has value in the academic literature. Prior studies have only studied interest groups and did not get down to the level of identifying key-players and analysing their activities (Coombes and Stokes, 1985; Dyckman, 1988; Hussein and Ketz, 1980; Hope and Briggs, 1982; MacArthur, 1988; Puro, 1984). This study identifies key-players and allows them to articulate their concerns and describe their actions. This adds to our understanding of the motivations and activities of key-players. This study provides new evidence of the reasons and the ways key-players utilised their power to influence the accounting standard-setting process. Most of the key-players belonged to powerful interest groups. Some of the key-players, through their lobbying activities, did influence other members in their group to take a particular course of action such as to bring about the withdrawal of the mandatory status. Some other key-players were influential behind the scenes and some key-players commented that it was the influence of a few people who pushed the two accounting bodies into removing the mandatory status.

This article is presented as follows. Section ‘Development of SAC 4’ gives a short description of the development of SAC 4. The next section ‘Theoretical underpinning and a review of prior literature’ provides theoretical underpinning of the issues investigated in this study and a review of the literature that addresses the political aspects of accounting regulation. The research method employed in this study and an analysis of data are discussed in the section ‘Research method and data analysis’. This section is followed by the section ‘Discussion of the findings’ which provides a discussion of the findings. Finally, we discuss the conclusion and limitations of the study and possible areas for further research in the section ‘Conclusion’.

Development of SAC 4

The development of the Conceptual Framework was given a high priority by the Accounting Standards Review Board (ASRB) (1985). This importance can be seen in ASRB Release 100, ‘Criteria for the Evaluation of Accounting Standards’ which was issued in February 1985 and set out the assumptions regarding some key accounting concepts (ASRB, 1985). It was held that accounting standards if developed in accordance with a Conceptual Framework, would be more logical and consistent (Henderson and Peirson, 1994; Miller and Loftus, 1993). Accordingly, nine assumptions were developed as a preliminary step towards formulating the Conceptual Framework, which included the purpose of corporate financial reporting, the reporting entity and the concepts of asset, liability, residual equity, contributions, distributions, revenues and expenses (Robinson et al., 1994).

The accounting profession’s early approach to the development of the Conceptual Framework was in the form of accounting theory monographs and exposure drafts (EDs) issued by AARF. In December 1987, four EDs were issued by AARF, namely, ED 42A on the objective of GPFRs; ED 42B on the qualitative characteristics; ED 42C on assets; and ED 42D on liabilities. ED 46A on the definition of the reporting entity and ED 46B on expenses were issued in April 1988 and EDs 51A and 51B were issued in August 1990. These EDs became the Statements of Accounting Concepts (SAC) in August 1990; for example, ED 46A became SAC 1 ‘Definition of the Reporting Entity’; SAC 2, ‘Objectives of General Purpose Financial Reports’ comprised ED 42A; SAC 3, ‘Qualitative Characteristics of Financial Information’ was issued based on ED 42B and SAC 4, ‘Definition and Recognition of the Elements of Financial Statements’ was based on EDs 42C and 42D (Picker et al., 2009). The authoritative nature of these statements (hereafter SACs) was emphasised in paragraph 41 of SAC 1 which stated that GPFRs ‘shall be prepared in accordance with statements of accounting concepts and accounting standards’ (AARF, 1993).

In August 1990, ASRB Release 100 was amended to set out the authority of the SACs in the context of financial reporting by companies. Paragraph 12 noted that while the concepts statements do not have the force of an approved accounting standard, application of the concepts statements by preparers and auditors would be appropriate in their endeavour to satisfy their legal obligations (Deegan, 2014). The paragraph also noted that relevant members of the ASCPA and the ICAA had a professional obligation to apply the concepts statements in the preparation, presentation or audit of GPFRs. In December 1990, the Executive Committee of the ICAA amended Rules of Ethical Conduct (REC) 1 to incorporate a reference to the mandatory status of statements of accounting concepts flowing from the reissue of APS 1.

Theoretical underpinning and a review of prior literature

Power theory

Literature suggests that regulatory activity is political in nature and political activity is complex, multi-faceted and at times invisible (Coombes and Stokes, 1985; Puro, 1984). Puro (1984) stated that a complex set of interactions influence the position adopted by audit firm respondents to draft accounting rules. Coombes and Stokes (1985) investigated the responsiveness of the accounting profession in Australia to the written submissions of respondents to EDs of accounting standards and were able to observe the influence of professional bodies on the final policy decisions.

Hussein and Ketz (1980) and Puro (1984) have established that standard setting occurs in a socio-political environment where groups and individuals engage in a broad range of lobbying activity so as to secure outcomes compatible with their interests. The concern of the public and the private sector for maintaining their interests creates the political environment in which the standard-setting board operates (Cortese et al., 2009; Dyckman, 1988; Konigsgruber, 2010). Prior studies (Dyckman, 1988; Hope and Briggs, 1982; MacArthur, 1988) have investigated the impact of political activity upon the enactment of accounting regulation. Debates over accounting policies take place not only on technical issues but more importantly such debates occur in a political environment in which the standard-setting body operates. Hope and Briggs (1982) examination of deferred taxation accounting issue in the United Kingdom provided evidence on this issue. Walker and Robinson (1993, 1994a, 1994b) mentioned in their studies that there are possible roles played by some participants in the rule-making process.

A greater understanding of the capacity of organised interests to secure more favourable regulatory outcomes and the methods used to secure agenda entrance was provided by Klumpes (1994). He investigated, through a case study approach, the overall political process which surrounds accounting rule development. It has also been suggested by Fogarty et al. (1994) that the standard-setting process can be better understood by recognising its political nature. Fairclough (2003) emphasised that it is vital to bring to light the political nature of accounting and expose the underlying institutions and arrangements of accounting to gain insight as to how accounting standards are developed.

Lukes (1974) defines power as the capacity to bring about consequences (see also Kwok and Sharp, 2005). Power theory has been used in the accounting literature across more than four decades, and Lukes (1974) explained the standard-setting process using power theory. Lukes (1974) recognised that power need not be empirically verifiable to exist and that the status quo may need to be questioned in order for the presence of power to be brought to light. A number of factors such as lobbying behaviour, control over information and financial dependency have been identified in the power theory as contributing to enable the industry to influence the standard-setting process (Lukes, 1974; Puro, 1984). Lobbying studies (Luther, 1996; Wise and Spear, 2000) examined the behaviour, particularly the decisions of rule-making bodies and the voting behaviour of their members. These studies have also looked into the processes surrounding rule-making in terms of the pluralist model of political behaviour. Also, in line with this model, previous lobbying studies in accounting have examined whether power is concentrated in the hands of elites such as Big 6 accounting firms or large corporations or is more widely distributed (Luther, 1996; Wise and Spear, 2000).

Lobbyists are adept at applying the standard-setters’ ‘accepted’ view in their lobbying strategy. Different groups of lobbyists respond in different proportions on EDs employing different strategies to influence standard-setters depending on their motivation for lobbying and perceived influence (Tutticci et al., 1994). Lobbying has also been identified by Giner and Arce (2012) as an essential part of the International Accounting Standards Board’s (IASB) standard-setting process. To analyse lobbying behaviour they conducted a content analysis of 539 letters addressing the documents issued by the IASB preceding the issue of International Financial Reporting Standards (IFRS) 2. The analysis of lobbying activity revealed that preparers constituted the most active group, particularly when the IASB started a project. However, participation of standard-setters increased at the end (Giner and Arce, 2012).

Some limitations of lobbying studies identified by Walker and Robinson (1993) are as follows: first, researchers examined only those issues which were already on the formal agenda of rule-making bodies. So, their focus was limited to only one aspect of the political processes of rule development. Second, researchers have focused only on written submissions. Reliance on evidence in the form of written submissions does not adequately reflect or may not allow other mechanisms that are used in the lobbying process to be observed. Important influences by particular groups on final decisions may not be revealed in publicly available written submissions which may themselves be incomplete and unreliable. Thus, the focus of these studies has been narrow because the researchers were looking at a later and potentially unimportant stage of rule formulation (Walker and Robinson, 1993). However, evidence about political activity other than that reflected in written submissions is often difficult to gather because members or staff of regulatory bodies may engage in oral lobbying on the telephone or during social discussions for which no written evidence may exist. It is recognised by researchers that there is still much to learn, about key aspects of the roles played and arguments employed by various constituents when employing lobbying practices (Giner and Arce, 2012).

Capture theory

Capture theory (Cortese et al., 2009) has also been used to explain the development of accounting rules. For example, Cortese et al. (2009) provide evidence that the regulatory process of setting IFRS 6 was captured by powerful extractive industries’ constituents so that it merely codified existing industry practice. Similarly, Wise and Spear (2000) commented that the disclosure practices of enterprises engaged in mining industries in Australia can at best be described as inadequate and reasonably be referred to as an outstanding example of accounting flexibility. The seeming unwillingness of legislators and accounting standard-setting bodies to regulate the reporting of companies may be because of the economic significance and associated political influence of the enterprises and the distinctive nature of their activities influencing the methods of accounting practices (Luther, 1996). Mitnick (1980) used capture theory to explain regulatory processes and identify the factors that contribute to a predisposition of regulatory bodies to take actions consistent with the preferences of the industry they were intended to regulate.

The above-mentioned literature review suggests it is important to understand the roles played by groups within the political process surrounding the development of accounting rules. However, most of the above studies have focused on political activity in terms of broad interest group categorisations and have paid little attention to the role of key individuals in affecting regulatory outcomes. This study investigates the main groups and the key-players involved in the lobbying to remove the mandatory application of SAC 4. Where it differs from prior research is the attempt to identify who are the key-players that have exercised substantial influence in the withdrawal of the mandatory status of SAC 4.

Based on the gaps in prior research, the specific research questions investigated in this study are as follows:

RQ1. Who were the interest groups affected by SAC 4? What patterns of political activities did these groups use? RQ2. Who are the key-players involved in the removal of the mandatory status of SAC 4? What patterns of political activities did these key-players use? RQ3. What were the reasons for opposing the mandatory status of SAC 4?

Research method and data analysis

This study uses archival data and semi-structured interviews to investigate the research questions set out above. This article follows Walker and Robinson (1993), who noted that it is important to understand the influence of different interest groups in shaping regulatory agendas and the methods used to secure agenda entrance. In addition, Walker and Robinson (1993) suggest it is important to understand the activities these groups undertake in order to shape public opinion. Data were gathered by the following three means. First, collecting the submissions relating to EDs on the various elements of financial statements such as assets, liabilities, revenues, expenses and equities and the invitation to comment on the status of SAC 4. Second, collecting publications relating to the EDs and SAC 4 in the professional journals and the business press which we identify as media analysis. Third, interviewing interested parties who made submissions and/or media statements and members of staff at AARF, the ICAA, the ASCPA and the Australian Stock Exchange (ASX).

In an attempt to identify the key-players involved in the events surrounding the introduction and removal of the mandatory status of SAC 4, a detailed review was undertaken of the submissions made in response to ED 42, ED 46 and ED 51. The names of persons who put in submissions were collected and their positions in their respective organisations were identified. Data on the activities of key-players were obtained from written submissions made to the standard-setting bodies and also from the views expressed in the professional and business press and the views of respondents to semi-structured interviews.

A search for relevant material was made of professional accounting journals and related publications (e.g. Australian Accountant, Charter, Financial Forum and Accounting Communiqué), other professional publications (e.g. Company Director and the Company and Securities Law Journal), the business press (e.g. Accountancy News, The Australian Financial Review, Business Review Weekly, Australian Business, New Accountant) and the business pages of daily newspapers such as The Australian, The West Australian and The Age. Furthermore, the relevant press or media releases of bodies such as the Australian Accounting Standards Board (AASB), Public Sector Accounting Standard Board (PSASB), AARF, ASCPA and ICAA and archival material in the form of correspondence, reports and minutes of meetings were obtained and analysed. Finally, financial journalists were interviewed to obtain the names of individuals that the journalists thought had contributed to the debate about SAC 4.

These materials were analysed and a detailed chronology was prepared. From the chronology and the analysis of the submissions in response to ED 42, ED 46 and ED 51, a final list of potential key-players was compiled. Interviews with 32 individuals were undertaken in Sydney and Melbourne during September 1994. Follow-up telephone interviews were conducted in December 1994 with the individuals who were pivotal to the debate about the status of SAC 4. The aim of the interviews was to obtain the views of the interviewees as to their role and the role of other individuals they thought were significant in the events surrounding SAC 4. The interviews were audio taped, and over 400 typed pages of interview data were transcribed.

Discussion of the findings

We report the findings from the study under the following sections which address the three research questions.

Identification of the interest groups affected by SAC 4 (RQ1)

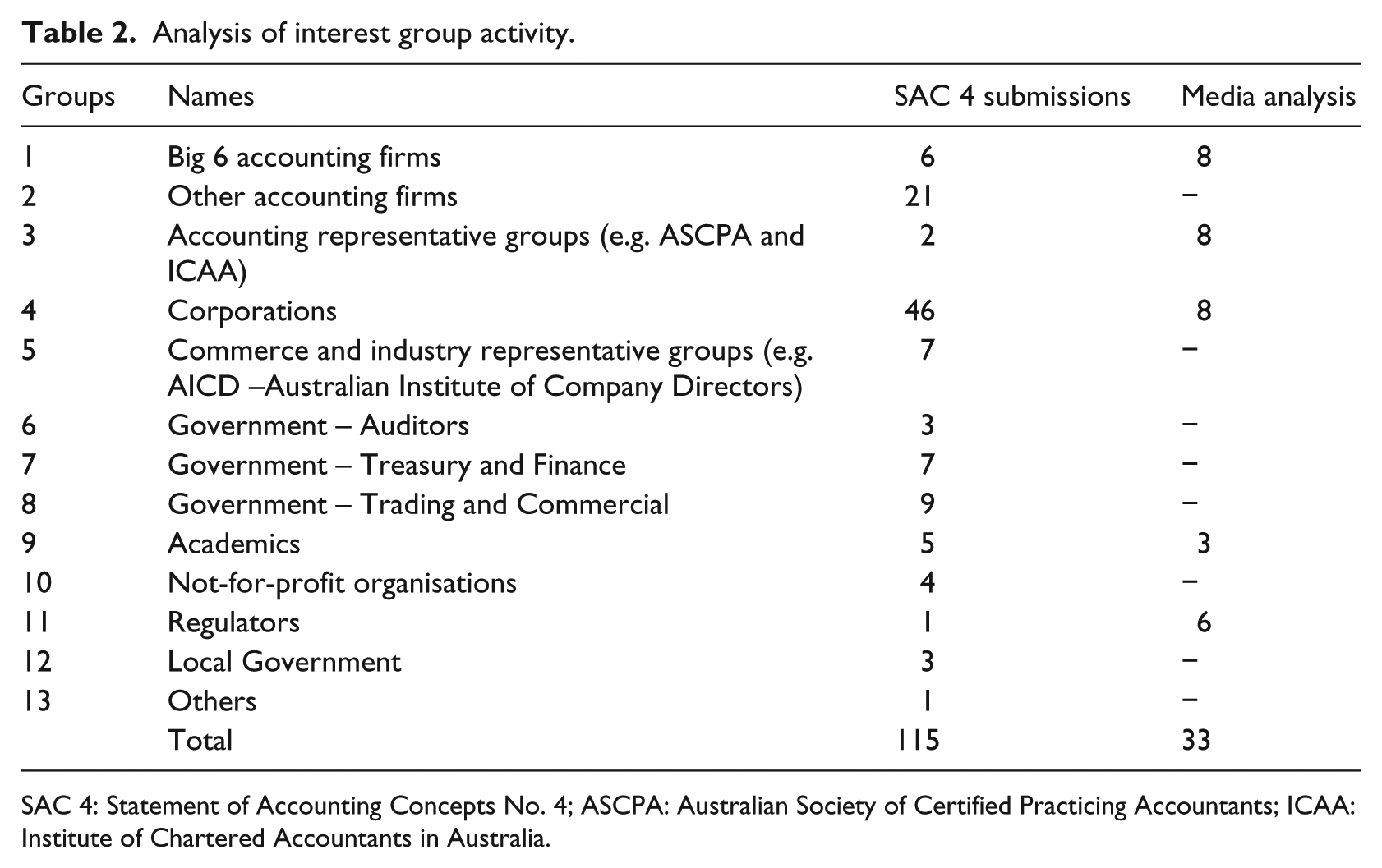

The identification of interest groups affected by SAC 4 was achieved by analysing the submissions, media analysis and the transcripts made from the interviews. We found that 13 different groups were involved in the withdrawal of the mandatory status of SAC 4 (see Table 1 for a list of these groups). In this study, we have categorised interest groups on the basis of the activity of that group, for example, the Big 6 accounting firms, commerce and industry and government agencies.

Interest groups identified as seeking to exert influence.

ASCPA: Australian Society of Certified Practicing Accountants; ICAA: Institute of Chartered Accountants in Australia; AARF: Australian Accounting Research Foundation; AASB: Australian Accounting Standards Board; ASIC: Australian Securities and Investments Commission; ASX: Australian Stock Exchange.

The patterns of political activities of the interest groups in the withdrawal of the mandatory status of SAC 4 – similarities of political activities of interest groups

Table 2 indicates the frequency of participation by interest groups in the debate about SAC 4 either by way of written submission or through media comments. There were some similarities in the political activities of the interest groups in that all of the groups identified in Table 2 took advantage of the opportunity to express their opposition to the mandatory status of SAC 4 through written submissions.

Analysis of interest group activity.

SAC 4: Statement of Accounting Concepts No. 4; ASCPA: Australian Society of Certified Practicing Accountants; ICAA: Institute of Chartered Accountants in Australia.

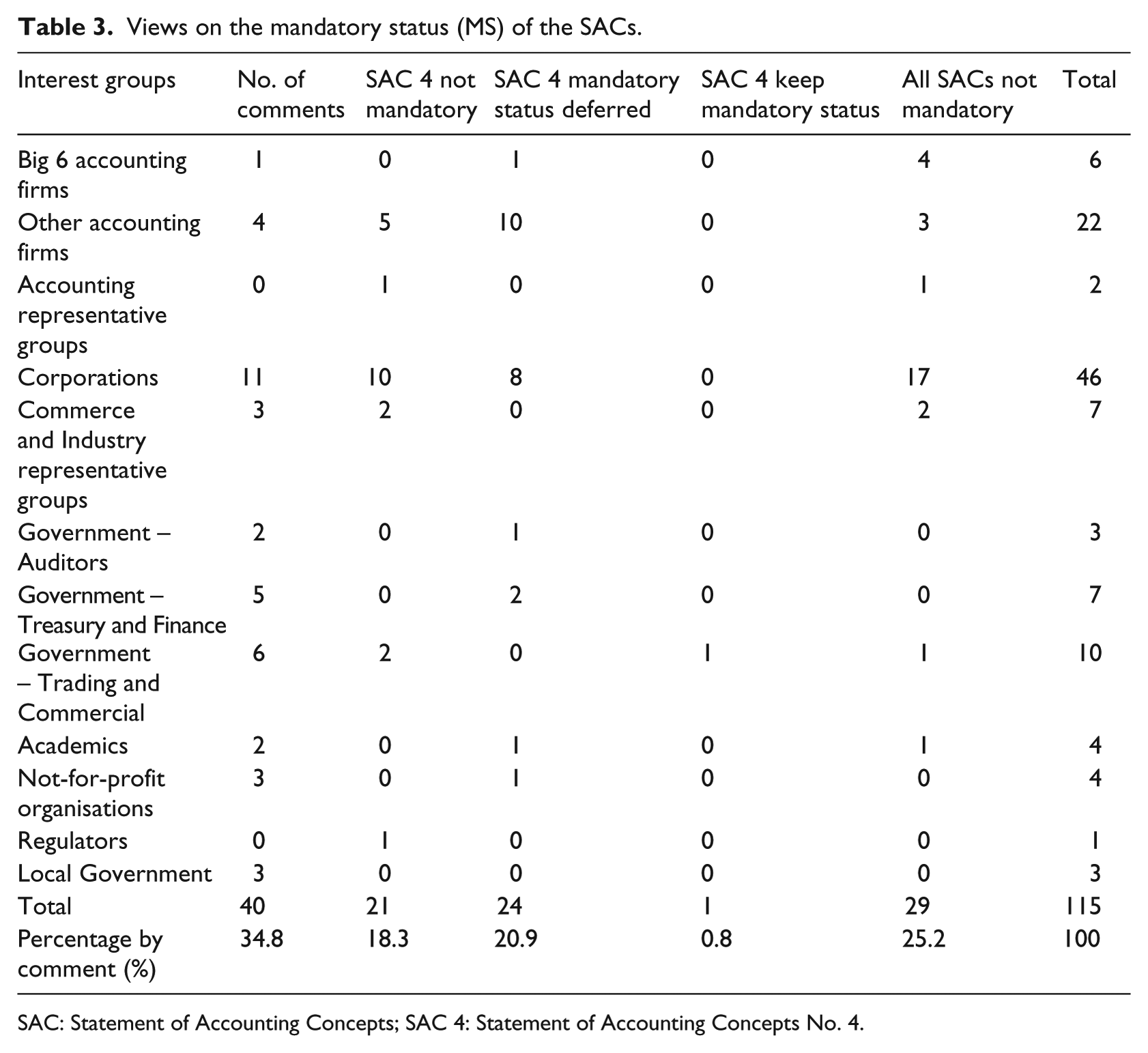

Table 3 summarises the views given by respondents to the mandatory status of SAC 4. The issue of mandatory status was commented on in 75 submissions. The views expressed in these submissions can be divided into three broad categories such as ‘retain’, ‘delay’ and ‘delete’. Only one submission supported retaining the mandatory status, 24 wanted to delay it, 21 wanted to delete the mandatory status of SAC 4, while 29 suggested removal of the mandatory status from all SACs.

Views on the mandatory status (MS) of the SACs.

SAC: Statement of Accounting Concepts; SAC 4: Statement of Accounting Concepts No. 4.

As to the issue of the influence of groups in the development of the Conceptual Framework in general in Australia, Respondent 7 (from one of the Big 6) put it in the following way: We have recently seen most of the main user groups represented in various forms dealing with the accounting rules and to some degree with the Conceptual Framework

Respondent 7 also commented that, in the past 50 to 100 individuals or entities were involved with an accounting topic, but now about 200 to 300 individuals participate in the standard withdrawal process. Although not all participants actively take part in the submissions process but in terms of the total active population of people being concerned … I think there is quite a wide range of people influencing the Framework in terms of the design of the actual accounting rules themselves or the design of the Conceptual Framework and the pressure to improve on both of those.

This respondent noted similarities in the manner in which various groups were influential, specifically, the value of persistence in arguing their case: Well, in the broader groups … the external parties to the standards setting process are becoming quite influential simply by participating in that process through expressing their views in various ways. Making submissions, attending Board (ASRB or AASB) meetings, participating in seminars, occasionally going to the press, and generally being more persistent in their views and trying to influence the direction of things. As they become more sophisticated at that and as they begin to understand more about standard setting their capacity to influence the standard setting is also becoming more acute.

Respondent 6 (from one of the Big 6) noted the value of being seen as a substantial stakeholder. He noted that the Group of 100 represented the interests of the ‘vast majority of the big business community’ and exercised influence by emphasising the size and nature of its membership. ‘They spoke with one voice saying, we don’t accept SAC 4, and [this represents] the vast majority of the users of the concepts statements’.

This quote suggests these groups leveraged their membership numbers and economic power. This is echoed in respondent 12’s comment as well: The Group of 100 was influential and was successful because members of the group were respected and they enjoyed resources and prestige.

Another aspect of similarity in group behaviour relates to the type of activity engaged in. Table 2 shows that media comments on the issue only came from the following groups: Big 6 accounting firms, corporations, the regulators, professional accounting associations and academics. Interestingly, none of the government agencies, small accounting firms or not-for-profit entities seems to have expressed their views in the media.

Differences in political activities of interest groups

There was considerable variation in the level of participation between these groups, when making submissions relating to SAC 4. For example, Table 2 shows that out of 115 submissions, 46 (40%) came from corporations. And, 27 submissions were made by accounting firms (23%). The three Government groups, Trading and Commercial, Treasury and Finance and the Auditing group, made 19 submissions (16%) of the total submissions. The rest of the submissions included academics (4%), not-for- profit organisations (3%) and local government (2%).

Some differences were also noticed in terms of the interest groups participation in the professional journals and the business press. Table 2 shows that the majority of this activity (72%) was made by three groups, namely, Big 6 accounting firms (24%), accounting representative groups (24%) and corporations (24%). This was followed by the two other groups such as regulators (AARF, AASB and Australian Securities and Investments Commission (ASIC) – 18%) and academics (9%). As was shown previously (see Table 3), five of the Big 6 accounting firms opposed the SACs having a mandatory status. Similar negative views were expressed by both members of the accounting representative group, and approximately 76 per cent of the corporations group.

Campaigns were conducted through the media by the major corporations. These groups attempted to exercise influence through submissions and media comments. They were able to exercise power by sheer size and resources (both expertise and political might). The corporations group was not well organised during the initial exposure of the concepts statements (i.e. ED 42, ED 46 and ED 51). However, subsequently, the threat of mandatory status galvanised them into action and they became organised through the Group of 100. This group started to exercise more influence by putting in submissions, participating in the Group of 100’s initiatives, organising seminars and the groups’ members worked through committees.

The Big 6 accounting firms did not hold a uniform position on the status of SAC 4. For example, only one out of the Big 6 accounting firm suggested that the mandatory status of SAC 4 should be deferred, while four of the others lobbied to ensure that none of the SACs would be mandatory. The remaining firm did not comment on the mandatory status. The professional accounting associations exercised influence by opening up the debate. The two professional accounting bodies continued to be effective through the consultative groups. The institute had very little input at the ED stage and became more involved when the mandatory status became a concern. Academics tended to be involved early in the process, such as helping to develop SAC 4 and other parts of the Conceptual Framework. However, apart from respondent 27, academics did not seem to be very involved in the debate surrounding the status of SAC 4.

Identification of individual key-players (RQ2)

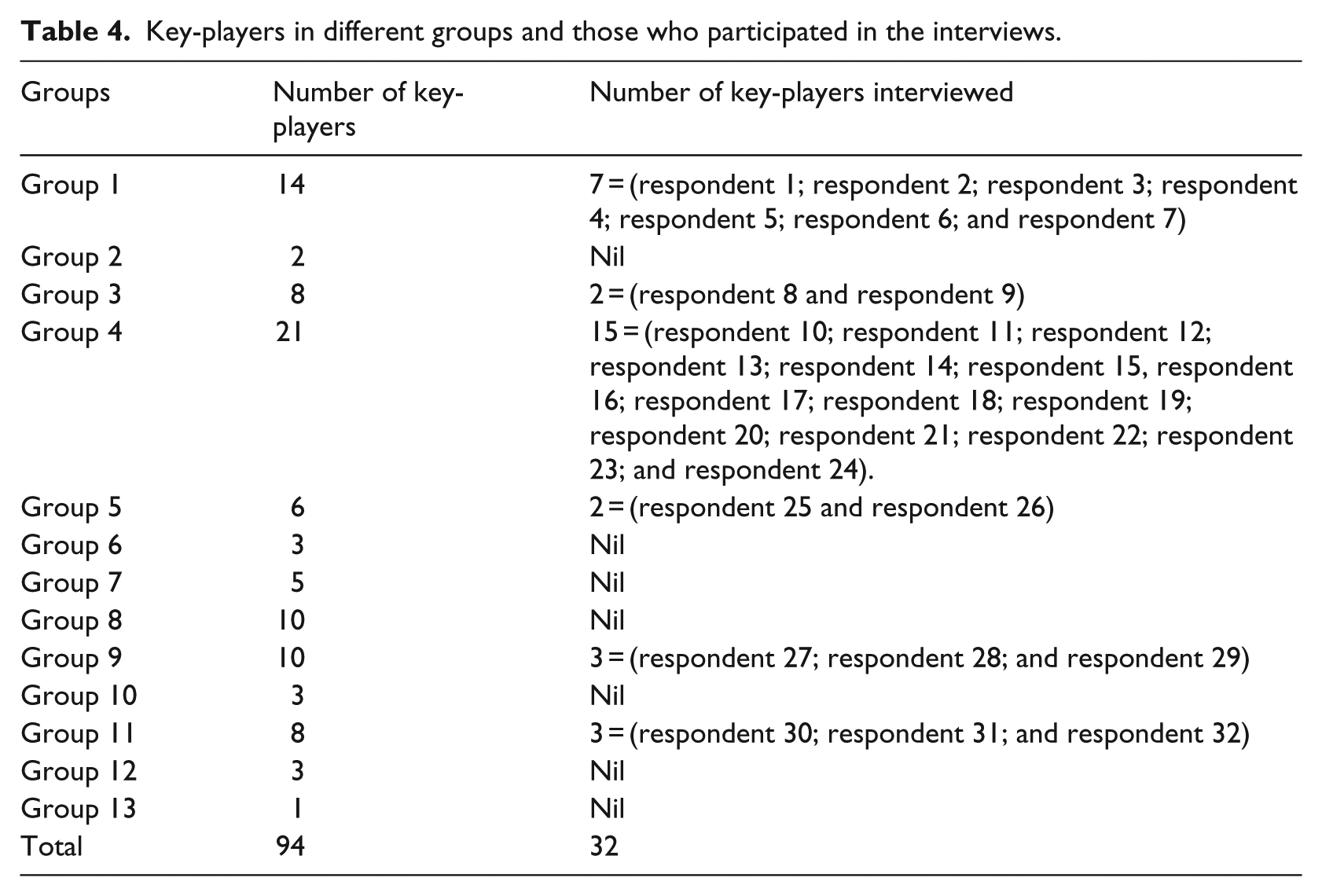

An analysis of submissions on SAC 4 and the interviews revealed that 94 key-players from various groups were involved in the events surrounding the removal of SAC 4. Table 4 lists the number of key-players identified, the number of key-players interviewed and indicates the different groups to which they belonged. The key-players interviewed were from diverse sources. With some notable exceptions (the academics), most of the key-players belonged to the major accounting firms and corporations and were able to get involved by virtue of their positions of responsibility.

Key-players in different groups and those who participated in the interviews.

Patterns of the political activities of the key-players in removing the mandatory status of SAC 4 (RQ2) – similarities

This study found clear evidence that all key-players actively lobbied using similar tactics, such as making submissions, participating in seminars, using resources and their time for lobbying and actively campaigning through the media. Another similarity relates to the power of the entities they represented, as well as their own personal standing. The value of being seen as a leader within an influential group was commented on by respondent 12, who stated that ‘Because of the positions they hold within those groups, I think they are well respected’.

Respondent 1, a partner in one of the Big 6 firms, was involved in professional accounting circles. Additionally, respondent 1 served on the AARF and on the AASB, as well as being actively involved in the International Accounting Standards Committee (IASC). Some respondents suggested that respondent 1 had exerted influence over the development of SAC 4. Respondent 12 (from the Corporations group) in identifying respondent 1 as a key-player, stated, ‘I always regard him as one of the leading members of the profession in this area’ …

Respondent 30 from the regulators’ group commented on the significance of personal branding and reputation. This prestige allowed a person to exercise power to persuade other stakeholders in the debate relating to SAC 4. Respondent 30 stated, They have the benefit of significant contact with the overseas bodies, and participation in the project advisory panels, the steering committees etc. at the international level and therefore they’re recipients of a great volume of information and they’re therefore at a considerable advantage to the rest of us … They’re highly qualified, competent people, and in that key position, they’re able to influence significantly the direction of things.

Patterns of the political activities of the key-players in removing the mandatory status of SAC 4 (RQ2) – differences

In terms of pattern of political lobbying activities, there were some fundamental differences in the roles played by the key-players. A major difference in political lobbying included using formal as well as informal methods to exert influence. Reference was made in the interviews as to the ‘informal’ or ‘disguised’ method of activity as suggested by Sutton (1984).

Formal activities include making submissions, attending seminars or Board meetings and engaging with the media. Some key-players such as respondent 10 from the Corporations group thought formal methods of communication, such as seminars, were quite effective in educating the constituency. Respondent 10 also attempted to influence the removal of the mandatory status by running seminars, organising groups to deal with issues and going to people and explaining the implications of SAC 4 to them. Informal activities included attending luncheons, informal conversations and attending informal meetings. Nevertheless, only more active and highly positioned key-players such as respondent 15 and respondent 10 (from the Corporations group) participated in such informal activities.

Another form of difference arises when it is realised that even though many of the protagonists represented substantial entities (the elites), the influence of key-players was exercised unevenly. Furthermore, it is important to recognise the critical impact a well-connected and passionate advocate had on the debate. Respondent 9 from the Accounting Representative group gives some insight into the passion this debate unleashed: (I) guess the mandatory status issue has taken a lot of time and energy. And whilst the debate at the end of the day ended up being constructive, we did spend a lot of time and effort arguing around the toss and it became very political and at times personal. I mean even quotes saying ‘the forces of darkness and evil ranged up. (Respondent 9) In total, 12 interviewees (approximately 40%) noted that respondent 10 (a member of the Group of 100) was a key-player. Respondent 30 spoke of the significant role respondent 10 played ‘He put a lot of work into it and made a significant contribution to the debate in (the Corporations group)’. Respondent 9 said that ‘ … respondent 10 had the running of SAC 4’. Respondent 13 (from the Corporations group) spoke about respondent 10’s role as well, he sort of started a one man campaign and then got the Group of 100 revved up, and there was a fairly lengthy paper written which was then condensed into three or four hard hitting points which were released on the accounting world in terms of press releases and articles and various presentations in early 1993. This tended to shift debate and successfully lobbied the whole thing in the progress of SAC 4.

Respondent 24 (from the Corporations group) observed that ‘I think you’d have to agree the debate was carried about 75 per cent by respondent 10’.

Another interesting aspect relates to key-players who were previously members of the various boards (ASRB, AARF and AASB), such as respondent 1 and respondent 26. Despite this association, they lobbied against SAC 4 publicly. Respondent 1 felt that the position he held within both the National Council of the accounting representative group, the regulatory group and internationally (e.g. IASC) gave him the leverage to argue against SAC 4. In respect of SAC 4 he stated, I pushed very hard to get rid of the mandatory status … my own view was that it was a big mistake to have the SACs mandatory. (Respondent 1)

In this regard, respondent 26 stated, After standing down from the ASRB, I became President of the Group of 100. There I had some influence over the forming of the Group of 100’s position on SAC 4 … I believe that I was able to draw the attention of the AASB and AARF to the concerns of the Group of 100 preparers.

Their behaviour may be contrasted with that of respondent 7. Unlike respondent 26 and respondent 1, respondent 7 does not appear to have lobbied against SAC 4 after his tenure as the Executive Director of a regulatory body. As Executive Director, respondent 7 presided over the development and release of the accounting theory monographs and the EDs of the concept statements. In total, 10 interviewees cited him as having exerted some influence over the development of SAC 4.

Some key-players such as respondent 3 adopted a middle position with regard to the withdrawal of the mandatory status of SAC 4. As to respondent 3’s role, respondent 20 commented that ‘I think this person tried to be quite fair in the assessment of SAC 4, and tried to find some middle ground’. The desire to find ‘middle ground’ may have been affected by respondent 3’s position on the AASB at the time of the debate.

There were also some differences in perceptions of the value of formal communication methods compared to informal methods. Respondent 15 suggested that stakeholders used informal luncheons and conversations as informal communication methods. Respondent 25 (from the Commerce and Industry Representative group) also gave an example of an informal meeting in Sydney in which the mood of the Group of 100 in relation to SAC 4 was made quite clear. Some thought informal methods of communication, such as seminars, were quite effective in educating the constituency. Respondent 25 was of the opinion that some of the formal methods, such as consultative groups, were a more effective means of communication because there was two-way communication between the members of the consultative groups and the boards. Some (e.g. respondent 7) also expressed the view that informal means of communication were not very effective. For example, they said that in the informal seminars not everybody spoke or expressed themselves. Respondent 27 gave some insights into the way power was used and impacted through informal lobbying: Some of them were influential behind the scenes, in trying to knock off people from boards, or support other people, and trying to change the status of a board.

Additionally, respondent 9 provided some support for the view that informal methods were seen as legitimate and effective. His use of language suggests the use and value of hidden power as a way to shape the debate. ‘ … in particular some in the Group of 100 engaged in guerilla warfare against SAC 4’.

Reasons for removing the mandatory status (RQ3)

An analysis of the arguments presented by critics of SAC 4 in interviews and submissions suggests a strong aversion to changing existing accounting practices. That is, many of the arguments did not address specific weaknesses in SAC 4. Rather, they essentially argued that it represented a change to existing practice, and this alone seemed to justify opposition. This is very similar to the experience faced by other researchers (see Moonitz, 1961; Sprouse and Moonitz, 1962).

For example, respondent 30 did not want companies to ‘adopt the provisions of SAC 4 which are inconsistent with generally accepted accounting conventions’ (Submission 1). This view was supported by members of a small accounting firm, which stated in its submission (Submission 28) that, We are not aware that the concepts exposed within SAC 4 have acceptance or are being commonly applied by any of our major trading partners.

The Federal Airports Corporation (Submission 40) was concerned that SAC 4 would change the accounting treatment of agreements equally proportionately unperformed (AEPUs) and that this change would constitute a breach of the existing Generally Accepted Accounting Principles (GAAP). The submission by one of the Big 6 accounting firms (Submission 21) went further and argued that SAC 4 would lead to a reduction in the quality of GPFRs: The term ‘probable’ is defined to mean ‘more likely rather than less likely’. We are concerned that this term is too vague and may lead to a wide range of possible interpretations. At worst this will lead to opinion-shopping for the interpretation that best suits the needs of the reporting entity in question. Opinion shopping is undesirable for the accounting profession. We believe that SACs should aim to achieve consistency in financial reporting, not promote inconsistencies.

This particular argument is quite revealing, as accounting standards that were in force at the time of this submission, and some years beforehand, used similar ‘vague’ language. For example, in AASB 1011 Accounting for Research and Development Costs (1987), it is stated that Research and Development (R&D) costs would be capitalised when there was an expectation ‘beyond any reasonable doubt’ (AASB 1011, para. 31) that the benefits of the expenditures would be recoverable (AASB, 1987). This term (beyond any reasonable doubt) was not defined. It is hard to see how changing from this undefined, subjective rule, to the ‘probability test’ would give rise to opinion shopping and an increase in the inconsistent application of the proposed rule. AASB 1011 was not the only rule in existence at that time which used text which could be subjectively interpreted. For example, in AASB 1024 (1992) Consolidated Accounts, the definition of ‘control’ is given as, ‘the capacity of an entity to dominate decision making directly or indirectly, in relation to the financial and operating policies of another entity so as to enable that other entity to operate with it in pursuing the objectives of the controlling entity’ (AASB 1024: 9) can also be subject to interpretation (AASB, 1992).

It is important to note that we are not trying to present an argument which promotes a ‘race to the bottom’. That is, we are not saying that because one rule had subjective text, then all rules should have subjective text. Rather, we are emphasising that accounting firms at the time were used to dealing with this sort of rule and did not seem to struggle with it. None of the submissions, to our knowledge, stated that this sort of language was a problem with existing rules that needed to be fixed. However, the submission by one of the Big 6 accounting firms asserted that the language in the probability rule was different from the existing language and that this justified the removal of SAC 4’s mandatory status.

A similar inconsistency in argument relates to concerns about the lack of a measurement concept in SAC 4. This argument was utilised by many key-players from different groups, such as the Big 6 accounting firms, Commerce and Industry Representative Groups, academics and not-for-profit organisations. For example, respondent 30 in Submission 1 stated that, It is critical that a Concepts Statement on Measurement is drafted and debated prior to SAC 4 becoming mandatory and before companies are permitted to adopt the provisions of SAC 4 which are inconsistent with generally accepted accounting conventions. Without a consistent measurement base, it is difficult to debate logically and rationally the concepts promoted within SAC 4, as it is not easy to understand or assess the financial impact of those concepts.

Some of the groups and interviewees used a different approach, essentially arguing that SAC 4 would have negative consequences for Australian firms, as they would have to prepare more reconciliations to bring them into line with GPFRs presented under different accounting frameworks. For example, respondent 9 from the accounting representative group commented, I guess that the major firms within the Group of 100 are multinationals and/or are listed on a United States Exchange and the last thing these companies want is to have to do more reconciliation as a result of the deviations between the Australian reporting framework and US generally accepted accounting principles. Thus they campaigned actively against SAC 4.

This is supported by respondent 30 in his submission, The mandatory adoption of SAC 4 by Australian companies would mean significant and numerous adjustments to Australian financial statements to meet the requirements of the United States Securities and Exchange Commission (SEC), other regulatory authorities and to satisfy international rating agencies … Under SAC 4 these adjustments will be more frequent, more significant and … add further costs to Australian corporations for uncertain benefit.

Our overall findings suggest that these stakeholders acted as would be expected under power theory, specifically in the way they exercised their power and influence when lobbying in relation to SAC 4. Our study suggests that highly motivated key-players were able to galvanise support for their view. With the benefit of hindsight, it is surprising how effective these players were, given the apparent inconstancies and weaknesses in their arguments. This surprise grows when it is realised that most of the controversial aspects of SAC 4 (such as AEPUs and the probability test) were adopted with minimal fuss, over the next 20 years or so. At the same time, we still do not have a consistent measurement model.

We also believe this event throws up some interesting light on capture theory. It seems strange that a ‘captured’ Board would release such a controversial rule, if its ‘captors’ were going to lobby against it so passionately. Perhaps, this suggests that the ‘captors’ are not representative of the external entities they represent. This could be a fertile area for future research. That is, how does capture theory apply in cases where proposed mandatory accounting pronouncements are modified or withdrawn, due to intense opposition from stakeholders?

Conclusion

In this study, we aimed to develop our understanding of the political activity surrounding the withdrawal of the mandatory status of SAC 4. The relevant questions addressed in the study include the identification of the interest groups affected by SAC 4, the identification of the key-players, the political actions undertaken by the interest groups, the key-players for the removal of the mandatory status of SAC 4 and investigating the reasons argued by the interest groups and key-players for opposing the provisions of SAC 4 and its mandatory status.

The study reveals how key-players within the standard-setting environment interacted with each other and lobbied to bring about the withdrawal of the mandatory status of SAC 4. We suggest that a substantial number of submissions and interviewees relied on specious or inconsistent arguments to oppose SAC 4, demanding higher standards for this pronouncement than they required for existing mandatory rules. However, some argued convincingly that SAC 4 would increase the costs of preparing GPFR for Australian firms relying on international capital markets.

This study adds to the academic literature with regard to accounting regulation by its emphasis on political activities of interest groups as well as key-players with regard to standard setting. This can be significantly distinguished from most of the prior studies which emphasised only analysing political activities of interest groups with regard to standard setting. However, in this study, we sought to identify the prominent participants in the debate over the removal of the mandatory status of SAC 4 which was a significant historical event in the context of standard setting in Australia.

The findings of the study should be interpreted by taking into account some limitations in this study. First, the conclusions arrived on the issue of the removal of the mandatory status of SAC 4 in Australia may not hold true over time. Therefore, it lacks generalisability of the findings. This is because key-players may be different in each case and in different settings. Second, the interview data may have been confounded by the problems of selective recalling by the interviewees and the benefit of hindsight. One way to have avoided such a problem would have been to look at the personal diaries and notes maintained by interviewees at the time the events took place. However, such documents may not exist for all parties and, if in existence, still may not be made available to the researchers. In a limited sense, media comments provided some insight into the views held by the key-players at the time the status of SAC 4 was being debated.

The identification of key-players and their influence can be investigated in future studies of historical events in standard setting at the IASB level. At that level, the influence of different players from different countries can be investigated. Such future studies can further clarify and lead to a deeper understanding of the role and political activities of key-players in the setting of international accounting standards.

There is an interesting postscript to this debate. The most controversial parts of SAC 4 have been made mandatory in subsequently issued accounting standards. For example, the role of the probability concept has increased and is no longer confined to recognition of elements in the financial statements. It is now specifically included in the measurement of various elements, such as income in IFRS 15 Revenues from Contracts with Customers and liabilities under IAS 18 Employee Benefits. It is intriguing to note how little controversy these changes have caused, given the passions they generated about 25 years ago.

Footnotes

Acknowledgements

The authors recognise the contribution of Mr Peter Robinson of Curtin Business School for his guidance in this research project. The authors also acknowledge the invaluable time and support given by the respondents during their interviews.

Disclaimer statement

At the time of the interviews reported upon in this contribution, verbal consent was gained from the interviewees to quote from the interview transcripts. No Ethics Committee approval was obtained around the time of undertaking the study as it was not needed.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.