Abstract

Within the accounting history literature, there exists a small sub-realm that focuses on the nexus between accounting and war and accounting and the military. This article is a review of 55 articles published in the new millennium (2000–2017) ranging across a 420-year period, encompassing many wars and periods of peace, and involving multiple countries. Several accounting issues including procedures, costing, budgeting, disclosure, financing, efficiency gender and culpability emerge. The availability of existing accounting knowledge forms the basis of the review, with accounting shown to be adaptive and reactive to the needs of the military (and the state) in peacetime and wartime emergency. Specifically, in applying existing accounting knowledge, accounting contributes to the military or war. Where new accounting knowledge is developed, accounting is influenced either by the needs of the military or the dictates of war.

Introduction

Within the accounting history literature, there exists a small sub-realm focused on the nexus between accounting and war (or wartime) 1 and accounting and the military. 2 Arguably war and the military are indivisible but, for the purposes of this review, differentiation is necessary. Military activity is a constant through time, whereas war is limited by time. Military activity is essentially a combination of activity during peace (or peacetime) interspersed with activity in times of war.

The post-2000 years have been characterized by war and conflict 3 on a scale not seen since the conclusion of World War 2 (WW2) (1939–1945). The reality of war, and the profile of the military in society, has been high throughout these years. The destruction of the World Trade Center in New York City in September 2001 presaged a new period in which major and lesser powers including the United States, United Kingdom, France, Germany, Canada and Australia became enmeshed in a series of difficult, protracted conflicts. Events, initially in Afghanistan (Operation Enduring Freedom, starting 2001), followed by a switch of focus to Iraq (Gulf War 2) (referred to as Operation Iraqi Freedom, 2002–2010) and then back to Afghanistan (Enduring Freedom until 2014), have drawn attention for almost the entire period. Numerous other conflicts have heightened further, the profile of war and the military. Throughout this time, war has been a staple in the print, electronic and social media. The cost to the economies of these nations has been immense, similarly the destruction and dislocation wrought on the countries in which the conflicts have occurred. Stiglitz and Bilmes (2012), for example, estimate “the true costs [to the US alone] of the Iraq and Afghanistan conflicts to be in the range of $4 to $6 trillion, or even higher” (p. 305). War and military then, are neither invisible, nor irrelevant to the public at large.

Accounting, on the other hand, has a different profile within the wider community. As a discipline deeply entrenched within the business community and public administration, its generally low profile is only disturbed when major corporate scandals erupt into the public domain (Brewster, 2003; Chandar et al., 2014). Accounting is invariably accused, by association, such that its profile goes from low-key to active, but once the scandals have receded from the public gaze, the heightened profile also recedes.

War occurs between sovereign states or parties within states as “a continuation of political intercourse, carried on by other [military] means” (Von Clausewitz, 1832: 87). Although these boundaries are neither absolute, nor clearly defined, the essential feature of war is the destructive nature of the activity, and the potential conclusions variously of decisive victory, honorable or humiliating defeat, or inconclusive stalemate. The nature of the activity, the likelihood of the devastation that follows, and the consequences for both victor and vanquished, usually mean the “events” are characterized as national emergencies and treated accordingly. With total war, where “the division between military and civilian worlds is effaced (and) the home front is integrated into warfare” (Horn, 2000: 2), the consequences may not only be catastrophic, but efforts required to prosecute war can have profound consequences for state operations at both macro and micro levels.

Wars are fought by those involved in the profession of arms, but typically managed jointly by those in that profession at various levels of command, and a disparate coterie of civilian officials and politicians. The latter group provides direction to ensure resources are maintained at levels sufficient to maximize the chances of ultimate victory while accounting for the economic resources consumed. The stark reality is that it is impossible to prosecute a war successfully without both groups striving toward the same goal. The military is the medium through which wars are prosecuted. Critical to the successful prosecution of war are the administrative preparations undertaken by parties prior to, and during, periods of conflict. The role of the military includes all activities undertaken during peacetime, either in anticipation of possible war, or as a deterrent against possible aggression, and all activities directed to the effort once conflict has started. The military exists in times of peace, in anticipation of war, as the tangible means by which war-like activities are pursued.

War and military activities are fundamentally managed within the parameters established by the state, although the purity of this position is sometimes diluted by extra-state activities. Management is exercised within the confines of institutional infrastructure of the state; accounting exists as a concomitant part of that structure. According to Burchell et al. (1980), “accounting data are … used in … the planning of national economic resources in conditions of war and peace” (p. 6). By association, accounting is utilized both within the military realm and by the private sector in connection with the supply of men and materiel 4 whenever circumstances dictate.

The linkages between accounting, the military and war stem directly from the centrality of logistics to the ongoing maintenance of the military and the day-to-day prosecution of war, and accounting’s position within that realm. As the branch of military science concerned with the economics of warfare, logistics has preoccupied military leaders for as long as there have been wars (Ohl, 1994). As the twentieth century unfolded, logistics became big business and came to encompass (1) supply, design, procurement, and distribution of military materiel; (2) transportation, the movement of materiel to the fighting forces; (3) the constitution and management of fixed and temporary installations, and (4) personnel services, the furnishing of services such as hospitalization and personnel administration. (Ohl, 1994: 3)

The scale of this is well demonstrated by Book (2002) who notes that “logistics takes roughly a third of the [US] Defense Department’s budget” (p. 37). Within this extensive domain, accounting exists as a critical element to deliver “effective management systems that include both soldiers and civilians that successfully organize armaments production and supply links with the fighting force so that forces have plentiful weapons to help them defeat (enemy forces)” (Ohl, 1994: 3). If logistics are operating effectively, in the event of war, it becomes “the responsibility of the soldier to apply most profitably, to the interest of the higher war policy, the force allotted to him within the theatre of operations assigned to him” (Liddell-Hart, 1991: 320). The force that is assigned to the individual combatant comes directly from myriad complexities that today constitute the modern (military) science of logistics. In simple yet critical terms “strategy and logistics are interdependent, for no strategic decision can be made without reference to logistical factors” (Ohl, 1994: 181). As observed earlier by Henderson (1905), “war is a matter of supply” (p. 1). Accounting then is “the mechanism for allocating resources and ensuring they are employed [deployed] in the most efficient way possible” (Funnell and Chwastiak, 2015: 1).

Further support for recognizing the critical importance of the “back office” is the notion that finance in all manifestations has long been recognized as a central tenet of defense, particularly in the context of impending or existing major conflict. The UK Treasury has long held the view that “finance constituted the fourth arm of Britain’s defence services” (Crozier, 1977: 113). However, official recognition of this principle only emerged as late as 1937 when, under the chairmanship of Sir Thomas Inskip, Minister for Co-ordination of Defence, the eponymous committee averred that national defense would never be complete without each of the four constituent arms: Army, Navy, Air Force and Finance. The committee reported that economic stability and financial strength should be viewed as “a fourth arm of defence alongside the three services.” 5 Asserting that without the fourth-arm “a purely military effort would be of no avail,” the committee sought to entrench the standing of finance in defense planning. In this context, finance is the higher-order notion that embraces, but is not limited to other disciplines including accounting, audit, supply management, procurement, funds acquisition and taxation. Research has focused on each of these areas, to investigate how, separately or in combination, they enable the state to maintain, and to a lesser extent direct, military forces through constitutional, political and financial controls (Miley and Read, 2012). Financial controls typically emerge from either third-party procurement from within or outside the state sector, or supply to military forces. The willingness of the state to strengthen administrative efficiency and embrace and adopt contemporary business technologies and practices is also critical in this context. Despite the all-consuming impact of wars on participant countries and the extraordinary costs associated with their prosecution, “this resonating historical significance has not yet found a proportionate response in the study of military accounting” (Funnell, 2009: 561).

Although the length of any war at the outset is unknown, the historical reality is that, except for contemporary ongoing conflicts, all have reached some form of finality (Iklé, 2005). Wars are interruptions to long-term commitments to maintain the military capabilities on appropriate footings and at reasonable levels of readiness. The cessation of war does not obviate the need for ongoing commitment to the military and so it exists as a continuum. In times of peace it exists in anticipation of war as the tangible means by which future wartime capabilities can be delivered or as a deterrent against potential aggression. This existence stands in contrast to war itself, which is characterized by the ability of one party to prevail over the other, or for the conflict to deteriorate to the point where a stalemate emerges and no victory is achieved. Either way, war is finite in length.

Accounting’s temporal reality mirrors that of the military. As a “prevalent feature of society” (Burchell et al., 1980: 19) and a “social rather than a purely technical phenomenon” (Burchell et al., 1985: 381) accounting has been present for millennia. Active debate continues around the question of the start point and duration (De Ste Croix, 1956; Hain, 1966; Littleton, 1933; Martinelli, 1977), but in the context of this review, neither is critical. What is important is the notion that accounting is dynamic and influenced by a vast range of societal factors, while being subject to constant change, adjustment and advancement. According to Hopwood (1987), “it is not a static phenomenon … over time it has repeatedly changed (as) new techniques have been incorporated into the accounting craft” (p. 207). As also observed by Littleton (1933) in relation to the evolutionary process, “accounting is relative and progressive … The phenomenon which forms its subject matter are [sic] constantly changing” (p. 361). It can thus be of inestimable value to governments engaged in years of conflict or periods of peace.

The purpose of this article is to review research in the military-war-accounting domain published between 2000 and 2017. Drawing on research that covers a 420-year time span, the review demonstrates accounting’s contribution when existing knowledge is deployed in the service of the military in peacetime or during war. It also highlights how military activity and wartime conditions have influenced and contributed to the development of new accounting knowledge. The next section provides a brief outline of the growing presence and interests in this area of research together with an explanation of the procedures to identify the literature included in the review. Characteristics of the literature are separated into diversity and accounting themes of interest. Brief outlines are provided of each.

Identifying the literature

As observed earlier, war has a relatively high profile within society. Garfinkel and Skideras (2012) observe that “conflict is obviously costly and has economic consequence; therefore, it should have always been of at least some interest to economists” (p. 9). This observation could be readily applied to accountants yet the meager literature on accounting, the military and war dates to the period from about 1980 onwards and contains “work on highly niche topics and … studies which are intensely specific as to context, time and/or place” (Bisman, 2011: 162). The extant literature in the post-WW2 period totals fewer than 70 articles, although there are some early outliers including, Kohler and Cooper’s (1945) examination of costs and prices in the US war program during WW2, and Wright’s (1956) analysis of the cost-accounting experiment in the British Army conducted during 1919–1925. Other, often-cited earlier works such as Grimwood (1919), Harris (1911) and Young (1906) 6 were all written by participants directly involved in the events of the time.

The increasing utility attaching to research work with a military or war dimension is evidenced by recent decisions of the editors of two leading research journals, Accounting History and Accounting History Review, to schedule special editions of their journals. In the case of Accounting History in 2010, contributions to the special edition titled “Accounting and the Military” (Funnell and Chwastiak, 2010) were premised on a definition of military as extending beyond the notion of the fighting forces to include “industries and political infrastructure upon which the military depend” (Funnell, 2006a: 388). By contrast, the special edition of Accounting History Review in 2014, titled “Accounting and the First World War” (Funnell and Walker, 2014) was focused and timed to coincide with the centenary of the outbreak, in late-1914, of World War 1 (WW1) (1914–1918). The journal was devoted entirely to material on accounting and WW1, but no guidance was provided as to the boundaries for the term “military” (Anon, 2013). Interest is also evident through Edwards and Walker’s (2009) The Routledge Companion to Accounting History which included a chapter titled “Military” (Funnell, 2009). In his contribution, Funnell restricts discussion to the British experience from the end of the English Civil War (1642–1651) until WW1. More recently, the 14th World Congress of Accounting Historians, held in Pescara, Italy in June 2016 scheduled three dedicated parallel sessions to War and Military together with a plenary session, delivered at the commencement of the congress, focused on WW1 (Walker, 2016). In a similar manner the ninth Accounting History International Conference held in Verona, Italy in September 2017 scheduled two parallel sessions devoted to articles in the accounting-military-war domain.

This review, covering the period from 2000 to early-2017, includes 55 articles retrieved from full content, on-line and hardcopy searches of three specialist accounting history journals – Accounting History, Accounting History Review (formerly Accounting, Financial and Business History) and Accounting Historians Journal. Other scholarly accounting journals similarly searched included Abacus; Accounting and Business Research; Accounting and Finance; Accounting Forum; Accounting, Organizations and Society; British Accounting Review; Critical Perspectives on Accounting; European Accounting Review; Financial Accountability and Management; Journal of Accounting and Public Policy; Journal of Management Accounting Research; Management Accounting Research, and non-accounting business journals Business History; Business History Review; Financial History Review and Journal of Management History. Journals dedicated to defense issues, including Australian Defence Journal, Journal for the Study of Army Historical Research, Journal of the Royal United Services Institute (Aust), Mariner’s Mirror, Royal United Services Institute UK Journal and War and Society were hard-copy reviewed.

The body of work identified is highly specialized, and represents a small fraction 7 of the work that constitutes the wider accounting history literature over this period. It also accounts for more than 80 per cent of the accounting and the military, accounting and the war literature published since 1945. 8 The publication pattern over the review period shown in Figure 1 below, demonstrates the modest, niche character of the output. Prior to the review period, there were only 14 articles in the period 1945–1999.

Publication pattern – 2000–2017.

In identifying articles to be included in this review, the broad definition of the military, as articulated by Funnell (2006a) for the special military edition of Accounting History is used. The 55 articles identified are summarized in Appendix 1 with details of author, year of publication, journal, country of focus, specific war of interest and aftermath or period of peace, and sector. Identification of major accounting themes and summary phrases of each article are also included. In addition to these articles, two books, one book chapter and three recent doctoral theses are acknowledged in Appendix 2. The books, book chapter and theses are not included formally in this review, although both books, Funnell (2003) and Funnell and Chwastiak (2015), and book chapter Funnell (2009), are closely linked through several articles included in the review. Three doctoral theses were completed in the review period, Black (2001b) and Cobbin (2011), are also linked closely to work in the review whereas Mann (2014) does not yet appear in the scholarly literature.

Characteristics of the literature – diversity

Diversity in the literature is observed through time-period (war/peace), country, sector and theoretical frame, each of which is summarized in Table 1 below. Each measure of diversity is explained briefly following Table 1.

Literature diversity measures.

Period

The first measure of diversity is the period on which articles focus, described as either “war” or “peace.” For the review, war is not only years of actual conflict but also, on occasions years leading to the outbreak of wars and years in the aftermath of conflict where proximity is crucial. Eleven different wars have featured, ranging from the American War of Independence 9 (1775–1783) to Gulf War 2, varying in length from the lightning-fast 100 hours of Gulf War 1 (Desert Storm) in 1991 to the 44 years of the “shadow” Cold War and Nuclear Arms race (Cold War) from 1947 until 1991 (or the 13 years of the “conventional” Vietnam War [Vietnam War] from 1962 to 1975). The literature is concentrated predominately within the “European war” realm in which continental powers were the main protagonists. Works falling outside this boundary are Vietnam, and Gulf Wars 1 and 2. Most articles have a single-war focus, three are dual and one is tri-focused. Finally, one paper is general in its approach and not focused on any specific war or country but addresses war in a general manner

Peace is also complex and, in several instances, includes long periods interspersed with war(s). Twelve articles fall within this grouping. The incidence of war(s) in these latter periods tends not to complicate the analysis as the research is usually focused on the stretches of time before, during and after the wars. The concern is for the impact over an extended time frame One article, for example, looks at the impact of literacy and numeracy rates of enlisted men over the 300-year span of the seventeenth to nineteenth centuries. At the other end of the spectrum are articles that focus on projects that are precisely timed, including the building of the Rideau Canal on the Canada-United States border between 1826–1831, costing activity within a small volunteer UK militia unit during 1883–1888, reforms to the Navy Estimates in the United Kingdom in 1887–1888 and the application of New Public Management in the Department of Defence in Australia in 2001–2002.

Country

Protagonist countries include the United Kingdom, United States, France, Germany, Union of Soviet Socialist Republics (USSR) (Soviet Union), Italy, Spain, Canada, Australia, South Africa and Ireland, all of which were participants in various European wars. The United Kingdom dominates this literature with 21 instances, with the United States a distant second on 12. Two articles have a dual country focus – United Kingdom–United States and Australia-Canada, while one article has no country specificity.

Sector

The next measure of diversity is the sector within which the research is placed. The literature is overwhelmingly located in the state or public sector with nine only in the non-state or private sector and one having no state dimension. Given the close linkages between the state, the military and the prosecution of wars, this concentration is predictable.

Theoretical frame

Theoretical frames adopted by authors are the final means by which diversity of the literature can be observed. The most popular approach is descriptive-narrative but a small number of alternative frames are adopted. Nineteen articles are single-site case-study investigations, four include gender issues, two are international comparisons, one adopts an agency perspective and nine are “critical,” accusing accounting of culpability in societal “dark” issues.

Characteristics of the literature – accounting themes

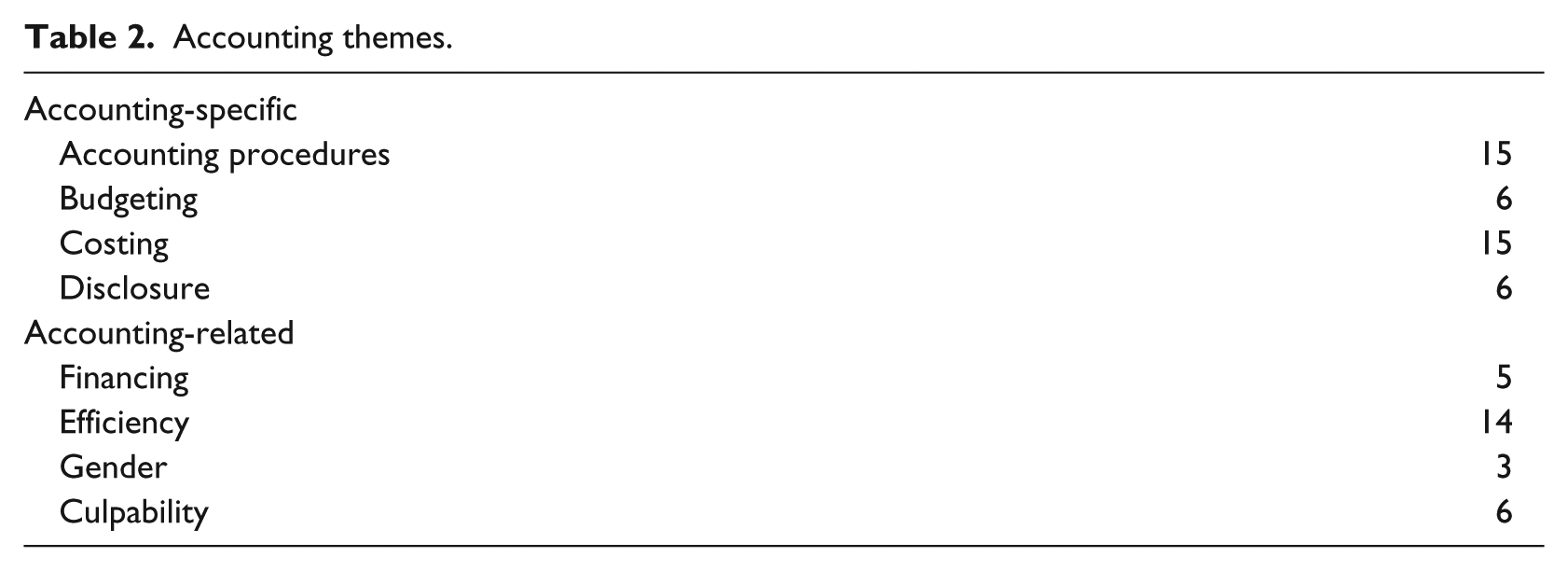

From the perspective of the accounting discipline, a small number of themes are detectable. These are subsequently referred to more generally as accounting knowledge. Accounting-specific work includes accounting procedures, budgeting, costing and disclosure; accounting-related themes include financing, efficiency, gender and culpability. Eighteen articles cover multiple themes. The distribution in Table 2 below shows the relative standings of each theme in the literature.

Accounting themes.

Accounting-specific themes

Accounting procedures

The area of accounting procedures, which is fundamental to the discipline, has been of interest over much of the period under review. The broad nature of the theme is reflected in the eclectic nature of the research activity undertaken. Each theme is given brief consideration alluding generally to the consideration that it has received in the wider accounting history literature.

Budgeting

The budget, as a tool of financial administration and central pillar of governments, has its genesis in the early evolutionary processes of the Westminster system of accountability dating from the mid-seventeenth century. As an element of accounting, it “forms part of the constitutional, hierarchical and stewardship accountability mechanisms of states” (Colquhuon, 2009: 543). Subsequently, it has been subject to constant change and refinement to the point where today, it is the primary means by which governments manage finances and the mechanism upon which judgments are based. “Perhaps every field of study fancies itself as progressing steadily toward theoretical sophistication, and public budgeting is certainly no exception … it may even be more inclined to seek linear progress than other fields of public administration” (Kelly, 2003: 309). Given its importance within the domain of the state, not surprisingly it is closely connected to the issue of efficiency that often arises in the aftermath of, for example, disastrous wars. The literature is split into content that looks at structural change and content that considers the use/abuse of budgeting procedures.

Costing

The evolution of costing principles and practices has been the subject of ongoing discourse in the accounting history literature with most attention focused on the “formalisation of the costing function” during the nineteenth and mid-twentieth centuries, up to and including WW2 (Boyns and Edwards, 2007: 994). There is scant agreement on the origins of costing principles (Boyns and Edwards, 2007; Fleischman and Tyson, 2007), with some citing the potteries of the late-eighteenth century as the key start point (McKendrick, 1973), while others nominate late-Victorian times (Dugdale and Jones, 2003; Solomons, 1952). Within this milieu there is a small contribution that focusses on the nexus between evolving costing principles and the influences of war, particularly WW1. Although outside the remit of this review, Armstrong (1987), Loft (1986) and Marriner (1980), are central in this discourse for the United Kingdom. Similar efforts have not been initiated for the United States. The review literature continues this debate and extends the focus to a small extent.

Disclosure

In the early years of the twentieth century, disclosure of information in financial reports was “minimal” (Maltby, 2005: 147). Similarly, Arnold (1997) noted “statutory disclosure requirements in financial reports were low” and “intervention on the part of the British state, marginal” as “directors and managers (often) behaved in a patrician manner and supplied shareholders with information that was thought to be good for them” (pp. 147, 164, 165). Against a background of minimal expectation, the possibility of varying approaches to disclosure was ever present, particularly in wartime. As observed by Napier (1995) “companies [and governments] that had previously disclosed a significant amount of detail … severely curtailed the level of disclosure” (p. 271). Napier’s observation is well supported by the, albeit small amount of literature.

Accounting-related themes

Financing

The funding of wars is fundamental to public finances with two options available: either through revenue via taxation or borrowings through bonds or other debt instruments. Although the accounting dimension to this theme is the way financing is recorded in accounting systems, the literature is more focused on the process and options available for raising funds to finance wars.

Efficiency

Probably, the most complex of the issues identified in the review is the desire for efficiency of operations particularly in the, at times, chaotic periods of war. The objective of efficiency within government administration should always be to the fore, but this is not always the case. Close attention often comes in the presence of national emergency or in the aftermath of catastrophe or as the consequence of earlier disastrous (mis)adventure. As a general concept, efficiency has wide reaching relevance in both the public and private sectors but, as will be seen, the review literature is heavily focused on the former.

Gender

The involvement of women in the workplace generally – the “gender question” – has been covered extensively. Zimmeck (1986), for example, observes that in late nineteenth-century Britain, as routine clerical work expanded, women were employed in ever increasing numbers. The General Post Office and the Post Office Savings Bank are cited as being among the largest employers of women at the time. In accounting, the question of “who does the accounting?” is apposite and has been of interest (Annisette, 2007; Kirkham, 1992). In the military context, WW1 and WW2 both provided major fillips for advancement of female interests and involvement in accounting.

Culpability

There is within the accounting history literature a growing body of work in the critical domain that seeks to implicate accounting and or accountants in many of the repressive regimes or dishonest practices of the past. 10 Often referred to as “accounting’s seamier side” (Fleischman, 2004: 12), much of the work infers culpability on the part of accounting. With war as the context, several articles in this review escalate the accusation.

The next section contains an explanation of the methodology used to classify the literature followed by the allocation of each article to one of four classifications. An assessment of the literature and concluding comments complete the review.

Classifying the literature

Methodology

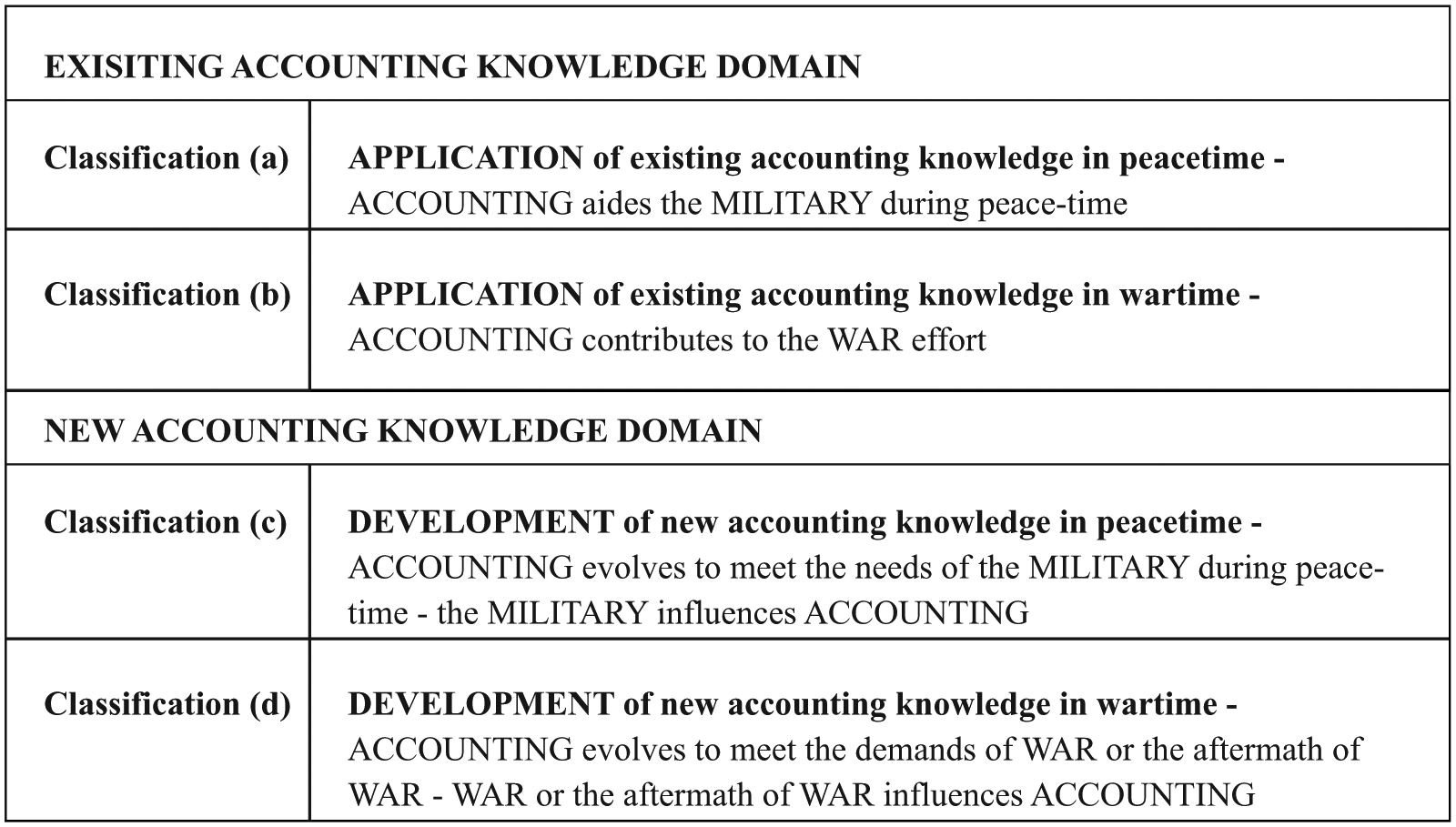

Insights into the research activity can be obtained by observing the relationship between accounting knowledge, the military and war. Using the “existing” accounting knowledge/“new” accounting knowledge dichotomy, four classifications are identified and summarized on Figure 2 below.

The relationship between accounting knowledge, the military and war.

In Figure 2, the first two panels, grouped under existing accounting knowledge – classifications (a) and (b) – focus on the role that accounting plays through the application of existing accounting knowledge required by the military in either peace or war. Panels three and four, grouped under new accounting knowledge – classifications (c) and (d) – focus on the roles that accounting plays in the development of new accounting knowledge during times of peace or war.

As with accounting history research more generally, the critical variable of interest is accounting knowledge and how it is treated. Regardless of the timing (war/peace), the expectation is that one of two outcomes will occur: either existing accounting knowledge will be sufficient or new accounting knowledge will be needed.

In the existing accounting knowledge domain, accounting knowledge is assumed to be adequate and available to solve problems or meet challenges as they emerge. During peacetime accounting acts as an aid to the military. During years of conflict, the nature of the commitment may differ in that a more timely contribution may be necessary but accounting may contribute in a tangible way, to the war effort. In the new accounting knowledge domain, existing accounting knowledge is insufficient and so through adaptation, change and evolution, advancements occur to meet challenges that emerge. In peacetime, the development of new accounting knowledge to meet the needs of the military implies the military influences accounting. In wartime, accounting evolves to meet the needs of the military and so war influences accounting.

In each grouping, accounting’s role is to provide solutions to new, and at times, urgent problems, to be innovative and responsive and to provide the wherewithal to support management decision-making (Burchell et al., 1980). Regardless of circumstance, the dynamic nature of accounting (Littleton, 1933) is the major factor that helps deliver solutions to emerging problems. Advancements emerging from the demands of the military during peacetime are likely to emerge in a measured manner unaffected by the urgencies of war and so may have lasting impacts. Developments driven by the exigencies of war are likely to emerge in a more rapid timeframe, but have only transient impacts. Expediency in the national interest may be vital in circumstances of “total war” (Copland, 1942; Horn, 2000) or the, beyond rational approach of “victory regardless of cost” (Iklé, 2005: 82). In such circumstances, accounting engagement may be premised purely on the need for national survival, arguably, as in Saritas (2009), an acceleration of Hopwood’s (1987) proposition of “accounting … conceived as being in motion” (p. 225).

While the primary objective of this review is to consider the accounting dimension of the literature, whether this accounting activity takes place in the context of war or peace requires further consideration. That circumstances in peacetime are dramatically different to wartime may explain in part, the different levels of interest. The military is simply another element of the state and, regardless of whether it consumes a significant proportion of government resources, competition is fiercer, and the claims of the military weaker, in the absence of “pressure from an external enemy” (Millar, 1965: 94). During peacetime, the military continues its primary objective of readying itself for the next conflict and providing deterrence against would-be aggressors, with varying degrees of expectations concerning when and where this might occur. Relationships with and between the elements that make up the infrastructure of state, including accounting and accounting systems, continue unabated in the absence of any military emergency or alert. In peacetime, accounting continues to serve the interests of the military as a critical element of complex management systems and much of the activity occurs on a day-to-day basis as accounting and the military go about their business. Similarly, throughout these periods, accounting will react on an as-needs-basis, if-and-when extant knowledge is insufficient to satisfy prevailing circumstances. Advances occur because of mutual interests between the parties. Peacetime, as characterized in the literature, often constitutes very long periods that make it difficult for research to be specifically focused. Instances of events in peacetime such as the building of the Rideau Canal in Canada during 1826–1831 (Bujaki, 2010, 2015) or the changes to the Royal Navy estimates in 1887–1888 (Cobbin and Burrows, 2010) are examples of events with precisely defined time periods upon which to focus compared to the long years from the mid-seventeenth to early-nineteenth centuries for the Royal Navy as in McBride et al. (2016).

The major factor driving engagement between accounting and the military in times of war is without doubt the conflict itself. Wars, as extremely complex phenomenon, have ramifications across all elements of society, including accounting. There is established, within the wider history literature, interplay between accounting and war. This exists, occasionally, in comprehensive histories of war (Butlin, 1955; Hasluck, 1952), institutional histories of accounting societies (Carey, 1969a, 1969b; Garrett, 1961; Institute of Chartered Accountants in England & Wales, 1966; Linn, 1996) and histories of major accounting firms (Abrahams, 2006; Falkus, 1993; Jones, 1981; Marshall, 1982; O’Malley, 1991; Richards, 1981). Predominantly coverages affirm accounting’s contribution but contains almost no detail of how accounting knowledge is applied or advanced. Beyond this notional acknowledgment, linkages between accounting and war, particularly the influence of war on accounting, are occasionally recognizable in the narrower accounting history literature. Hopwood et al. (1980), as cited by Walton (1995), in the context of the effects of war on accounting information and management practices, observe that “the administration of war has a[n] … influential effect on accounting practices, both directly and indirectly. The constraints which the conduct of war introduces into an economy increases the salience of many forms of economic information” (p. 8). On the more precise matter of accounting change, Walton (1995) asserts that “wars have played a surprisingly important part in generating accounting change” (p. 8). In a similar vein, Rutterford and Walton (2014: 103), citing Hopwood et al. (1980), also acknowledge “war as a phenomenon that often accelerates the development of accounting.”

Allocation

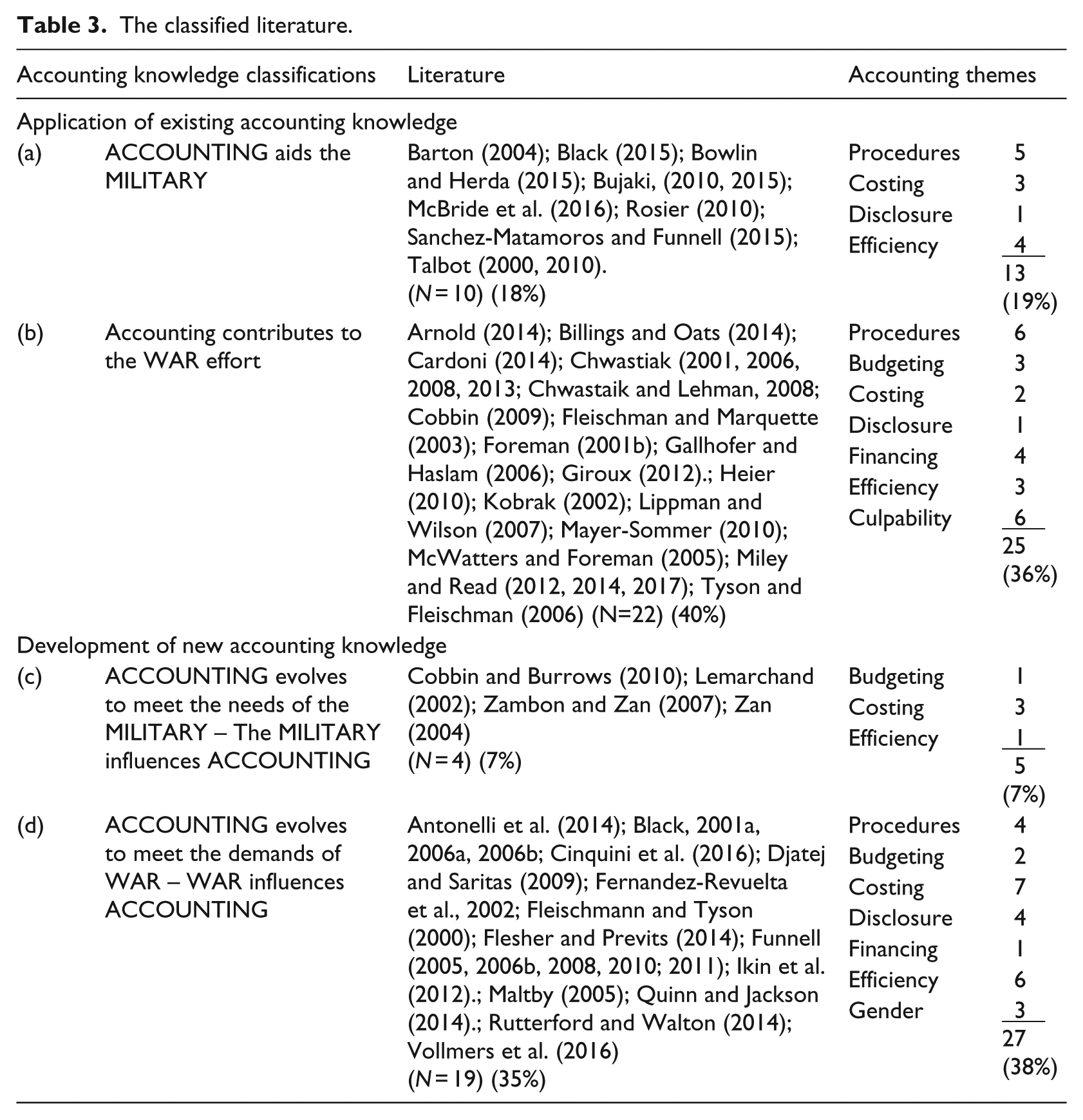

Based on detail contained in Appendix 1, each article has been examined and classified per the classifications presented in Figure 2. Each article has been allocated to one of the four classifications. Articles identified in each classification have then been grouped in Table 3, revealing the degree of concentration of research activity. Accounting themes have also been added to show the extent of coverage within each classification. Frequency counts (N) and percentages of articles and accounting themes are also recorded.

The classified literature.

Table 3 reveals a reasonably close spread between the existing accounting knowledge and the new accounting knowledge literature. The metrics associated with each classification, when aggregated, confirm the initial observation. Combining classification (a) – applying existing knowledge during peacetime, with classification (b) – applying existing accounting knowledge in wartime, accounts for 58 per cent of the literature (18% plus 40%) compared to the 42 per cent combination of new accounting knowledge developed during peacetime (classification [c] – 7%) plus new accounting knowledge developed during wartime (classification [d] – 35%). Accounting themes are similarly spread.

A secondary observation from Table 3 is the imbalance within each grouping where research activity with a peacetime dimension is significantly outweighed by research in a wartime context. Peacetime accounts for 18 per cent of the activity in the existing knowledge group compared to 40 per cent wartime. A similar pattern is discernible from new knowledge where peacetime accounts for 7 per cent of the literature compared to 35 per cent in wartime. Fixed periods of war have provided many more opportunities for research relative to the longer periods of peace.

Reviewing the literature

The existing accounting knowledge/new accounting knowledge dichotomy is applied to review the literature and so articles within the existing knowledge domain are considered first followed by those classified in the new knowledge domain. Secondary, within-domain divisions are made between peacetime and wartime.

Existing accounting knowledge domain

Classification (a) – accounting aiding the military in peacetime

The application of existing accounting knowledge to the military in peacetime is evident in a small selection of 10 articles (18%) covering four countries from the seventeenth century to the early-twenty first century. Four accounting themes – procedures, costing, disclosure and efficiency – encapsulate the areas in which the literature demonstrates accounting’s support of the military in peacetime.

Identifying the Navy Board, Victualing Board and ship’s captains as principals, McBride et al. (2016) show how, highly formatted recording processes, rudimentary costing procedures and on-board supply management techniques, which had been developed over several hundred years, were utilized by ship’s pursers as agents, to meet extensive embedded accountability demands in Royal Navy ships. Consistent with parliamentary expectations of the time, McBride et al. (2016) conclude that the accountabilities were designed to safeguard the public purse rather than promote efficiency and effectiveness in day-to-day naval activities. Also in the context of the Royal Navy, the records of costs associated with building ships in the eighteenth century provide the basis for Rosier (2010) to undertake a comparison between shipbuilding costs in royal dockyards and private yards. As overhead costs were treated differently in each location, the comparison is arguably, problematic.

Within a similar timeframe Black (2015) provides insight into the workings of the British Army in the three centuries of the seventeenth, eighteenth and nineteenth centuries. Following the English Civil War and the Revolution of 1688, control over military finance passed to civilian officials (Funnell, 2009). Although civilian control was almost absolute, some administration and procedural accounting work was carried out at unit level. Several reforms had the effect of bureaucratizing the service at unit level because the Army had, within its ranks, appropriate personnel to undertake training in finance and accounting relevant to these duties (Black, 2015).

In the latter half of the nineteenth century, provision of non-Army issue stores to soldiers located in military outposts on the American western frontier was outsourced by the War Office. As the outpost storekeeper, the sutler was required to maintain single-entry cash-based records that were subjected to considerable levels of accountability. Using Fort Abercrombie in the Dakota Territory as an illustrative case, Bowlin and Herda (2015) demonstrate how the sutler had to pay close attention to costs, manage lines of credit to soldiers and comply with heavy regulations on his record keeping.

Further evidence of rudimentary costing also emerges from a small infantry unit in the late-Victorian British Volunteer Army. Material from the first Battalion Staffordshire Volunteer Rifles indicates unofficial attention to setting standards for costs, naïve analyses of variances against standards and recording of follow-up action on variances (Talbot, 2000). The activity is (tentatively) attributed to a volunteer member who worked as a cost clerk in a Staffordshire Pottery where costing had been utilized for well over a century (McKendrick, 1973) and to the statistical accounting analysis movement championed by Colonel William Sykes at the Bass Brewery in Staffordshire at the time (Talbot, 2010).

At the start of the twenty-first century through the auspices of New Public Management, accounting and business practices in the public sectors of many countries were subject to private-sector business techniques including accrual-based accounting. Barton (2004:281) notes that because of the changes, “the Australian Defence Forces appear to be the most profitable enterprise in the nation – the profits and dividends far exceed those of the largest government business enterprises, the Reserve Bank and the largest private corporations.” He asks rhetorically “how can this be so given the Department is almost entirely dependent on an annual budget appropriation for its defence services?” (Barton, 2004: 281) and questions the substance and reality of the reforms introduced.

There is also evidence of accounting contributing to efforts to improve efficiency. Outsourcing the management of Spanish military hospitals to the St. John’s Order in the late-eighteenth century occurred because the Spanish government and the military were able, during the Enlightenment, to reconcile differences with the church and contract with an organization with a long history of helping soldiers and a capability to modify accounting and administrative processes (Sanchez-Matamoros and Funnell, 2015). Early in the following century, the British government, in Upper Canada, used state-of-the-art accounting technology to facilitate construction of key military defense infrastructure. Collaboration between Royal Engineers and civilian authorities utilized cost-benefit analysis techniques to support decision-making during construction of the Rideau Canal near the US border (Bujaki, 2010, 2015).

Classification (b) – accounting as a timely contributor to war

Twenty-two articles (40%) covering seven accounting themes in six countries and nine periods of war from the American Civil War to Gulf War 2 demonstrate the extensive application of existing accounting knowledge in times of war. The overwhelming focus is on the United Kingdom, United States and Australia during WW1. Accounting procedures, costing and efficiency all feature prominently. Financing war and disclosure procedures appear for the first time, as do accusations of accounting’s culpability in wartime. As noted for classification (a), the assumption underlying classification (b) is that existing accounting knowledge is made available in a timely manner.

In the mid-nineteenth century, accounting procedures were used successfully to keep the Louisville and Nashville Railroad operating during the American Civil War. Heier (2010) describes how, at a time of limited regulated accounting disclosure, a significant commitment to openness in accounting and accountability enabled the railroad to operate and service Union forces. The meatpacking industries in Australia and Canada during WW1 are the context for McWatters and Foreman (2005) to use an international comparison of the impact of war on two industry participants. Despite changed dynamics in the market place neither company made “significant changes to their accounting systems” (McWatters and Foreman, 2005: 95) suggesting arrangements in place were well attuned to the needs of war. A similar observation of useful extant procedures was made of the challenges faced by the German state during WW1 and the years immediately afterwards. Kobrak (2002) investigates the potential impact of increased complexity in foreign currency transactions on accounting procedures. Expecting some change, particularly during the hyper-inflationary years of the early 1920s, he surprisingly reports that no requirements were imposed on German industry to adjust values of assets nor were changes made to disclosure policies in consolidated accounts. The consequences of war service provide the opportunity for Miley and Read (2017) to consider the use of accounting classification techniques and procedures to support and cover government officials assessing the eligibility for pensions of shell-shocked returned soldiers.

It is also apparent in the literature that accounting makes a direct contribution to war through budgetary processes. US government budgeting has, for example, come under considerable scrutiny in recent years. In a series of articles (Chwastiak, 2001, 2006, 2008), the Vietnam War and Cold War are invoked to articulate how US government officials used this aspect of accounting to neutralize the language of war and devise technical terminology devoid of emotional consequences and impact. The introduction of Planning, Programming, Budgeting (PPB) particularly, is identified as the mechanism by which civilian officials wrested control of weapons procurement and military finance from military officials. In so doing, they employed rational economic choice and cost-effectiveness analysis as the preferred decision methodology at the expense of the judgment and heuristics of military leaders. Applying the technology, officials established and managed a goal-oriented war in Vietnam where PPB measured progress in terms of goals such as kill ratios and body counts. The underlying assumption was that when the “rational calculus [cost-benefit balance] indicated the war should be ended” (Iklé, 2005: 15), the enemy would sue for peace. The utilization of PPB techniques amply illustrates how accounting techniques were utilized directly and deliberately to manage these conflicts in a state-sanctioned manner.

Given the ongoing discourse on the evolution of cost-accounting principles that is often closely associated with the day-to-day delivery of the war effort, it is no surprise that work in this area is in a wartime setting. In a pragmatic move in the years preceding WW1, the Australian government imported, from major US government contractor, Pratt and Whitney, existing costing technology for use in government-owned factories. The motivation for this action was timely commercial efficiency in government factories through the accurate identification of costs (Foreman, 2001b). A single-site analysis of costing procedures at the Sperry Corporation during WW2 enabled Fleischman and Marquette (2003: 70) to test the proposition that the “advent of war might provide the impetus for the increased adoption of sophisticated cost accounting techniques.” Although the corporation, as a major supplier to the US armed forces, utilized advanced management techniques such as time management and sub-contracting extensively, no evidence was found to suggest the company “utilized a standard costing/variance analysis system as part of its scientific management methodologies” (Fleischman and Marquette, 2003: 97). Furthermore, Fleischman and Marquette (2003) endorse views expressed shortly after the war that the war had had a negative impact on standard costing principles.

Options for financing war available to government are limited to revenue enhancements and debt raisings, but regardless of the choice, accounting facilitates implementation of policy decisions. Only the revenue option appears in the review literature. Cardoni (2014) articulates the theory of alternative schools of thought that underpinned French decision-making during WW1. The Liberal School of Political Economy led by Paul Leroy-Beaulieu, advocated long-term borrowings that spread the cost of the war over present and future generations, whereas the alternative Social Science of Finance approach championed by Gaston Jeze, held that the cost of the war should be borne by the present population through taxation. Cardoni (2014) concludes that the French Government had no option but to utilize whatever financing options were available including revenue and debt. The revenue option in the United Kingdom during WW1 has been focused invariably on the Excess Profit Duty that was first levied in March 1915. Arnold (2014) and Billings and Oats (2014) each give prominence to profiteering and the attendant difficulties associated with defining normal and excessive profits with respect to the implementation of this tax. Earlier, during the American Civil War, the introduction for the first time by Union officials of Income Tax is the central tenet of Giroux (2012). Introduced to supplement extensive borrowings, Giroux (2012) reports the tax brought with it complexities that necessitated a series of administrative initiatives to manage collection. The Excess Profit Duty in the United Kingdom during WW1 and Income Tax in the United States during the American Civil War demonstrate how accounting facilitated the introduction of fiscal initiatives thus contributing in a tangible way to the war effort.

In Australia in the early WW2 period, huge increases in spending on the military together with Japanese forces continuing their relentless push through South East Asia, caused the Australian government great concern. Particularly troublesome was the inability of government departments to meet fully, the needs of forces in the field. Endeavoring to move to a more efficient war-footing, the government enlisted the Australian accounting profession to advise on the best way to restructure the administration and accounting procedures within the Department of the Army. The national emergency meant this was an instance where efficiency of delivery was not only desirable but an absolute necessity (Cobbin, 2009). During the later years of WW2, the US government instituted, in the wake of the Japanese attack on Pearl Harbor, a program to inter 120,000 citizens of Japanese descent. Tyson and Fleischman (2006) report how accounting was utilized effectively (and paradoxically by the internees) to manage successfully the system of 10 relocation centers during the war years.

Two articles address deployment of accounting from a different direction highlighting how, despite shortcomings with existing systems and controls, often little or no modifications are required. Mayer-Sommer (2010) shows how long-established Treasury expenditure control systems remained unaltered during the years of the American Civil War despite the greatly increased level of expenditure and the added stresses placed on systems. The priority was to ensure Congressional appropriations were being followed rigidly. Miley and Read (2012, 2014) report a similar observation regarding supply to troops in WW2. Despite the systemic problems identified by Cobbin (2009) in the Department of the Army in Australia, Miley and Read (2012, 2014) observe that senior officials drew the incorrect conclusion that processes were functioning reasonably effectively and efficiently because of inadequate feedback, poor reporting mechanisms and substandard complaints procedures.

The final issue is the “contestable” proposition of the culpability of accounting in dark issues that have had an impact on society over recent times. Chwastiak (2001, 2006, 2008, 2013), Chwastaik and Lehman (2008), Lippman and Wilson (2007), Miley and Read (2017) and Tyson and Fleischman (2006), all take the opportunity to add war to the rollcall of dark issues. As noted earlier, Chwastiak (2001, 2006, 2008) focused on US government budgetary processes in the context of the Vietnam War and the Cold War. Along with Chwastaik and Lehman (2008), the important additional aspect of this work is the critical form in which accusations of culpability are directed at government officials. Quantifying progress in war in purely economically measurable goals meant that truth was equated directly with whatever could be counted. They claim this reduces people, places and things to quantities and produces an abstract, cold and calculating reasoning bereft of human feeling. The argument was extended further with the US government (and by extension, other governments) accused of subterfuge for not disclosing the real or total cost of war. In the context of Vietnam, Gulf War 1 and Gulf War 2, the assertion is also made that the cost of war in the official budgeting process is based on the notion of “the short term incremental costs incurred” as if the war was not prosecuted (Chwastiak, 2008: 576, 577). Only direct costs of fighting were included, and no effort was made to estimate the social costs to the victor or vanquished. A radical prediction follows: that if governments were to report the total cost to the public, that is, use the full effects of accounting available, then maybe “the institution of war might well be in jeopardy of extinction” (Chwastiak, 2008: 586). Computing the real cost of war is a problematic notion according to Miller (1998: 382), who postulated, in his extensive history of the Cold War, that the “true costs of defence equipment were virtually impossible to calculate” because of the dubious and at times nefarious actions of governments. As if to show this is not a recent phenomenon, similar observations have been made about the supply of munitions to the British Army in the mid-nineteenth century (Black and Edwards, 2016).

Further support for the accusation of culpability comes in Chwastiak (2013) with a stark illustration in the contemporary setting of Gulf War 2 where it is argued the reconstruction of Iraq in the aftermath of Iraqi Freedom was abused financially by contractors who extracted huge profits in the absence of rigorous oversight from government officials. To minimize the impact of the “corporate malfeasance (fraud)” officials are accused of disaggregating events to limit the financial impact and portraying frauds as losses due to waste. The charge was that “accounting was not an innocent bystander … but the means by which this form of corporate welfare … became institutionalized, rationalized and normalized” (Chwastiak, 2013: 34). Through inadequate audit and oversight functions, accounting is accused of acquiescing.

Using WW1 as context, Gallhofer and Haslam (2006) adopt a different approach where the media is used to demonstrate how “factual accounting” in the form of published accounts can be used to push different political agendas through varying manipulations of financial numbers. Of interest was how the radical left-wing Glasgow-based publication Forward, manipulated facts to advance the case of workers in the face of the hegemonic (establishment) press whose views sided with capitalist interests. Alternative establishment views, for example, The Economist, provide a contrast, but the article is primarily focused on how hegemonic interests were advanced. It also advances the argument that WW1 was a great swindle facilitated by accounting, perpetrated on the working classes by capitalist forces. Miley and Read (2017) consider a different “swindle” with the awarding of pensions to UK veterans of WW1. They accuse the British Government of deliberately distorting and manipulating accounting techniques to discriminate against and deny pensions to victims of shell shock. Decision-makers using accounting classification techniques were “distanced from the morality of their decisions” (Miley and Read, 2017: 21) and were free to reject claims for pensions safe in the knowledge that they were insulated at least one step removed from the consequences of adverse decision about the awarding of pensions.

Two further accusations of culpability emerge from WW2. Tyson and Fleischman (2006) record a scathing observation of US officials and accounting in the management of Japanese internment camps during WW2. Conceding that these camps were run very successfully, due to the initiative of the Japanese-American “evacuees,” they opine that this “remains one of the most shameful events in race relations in recent history of the United States” (Tyson and Fleischman, 2006: 199). Finally, accounting activities that helped facilitate the horrors of the Holocaust during WW2 by Nazi Germany are used by Lippman and Wilson (2007) to level the accusation of the culpability of accounting in this darkest of dark episodes in recent world history.

The evidence that accounting provides existing accounting knowledge in peacetime or is actively and directly involved in the prosecution of wars through the provision of existing accounting knowledge is extensive and corroborative of Burchell et al.’s (1980: 6) earlier cited assertion that accounting plays a role “in conditions of war and peace.” The observation is particularly apt though weighted heavily in favor of war over peace.

New accounting knowledge domain – classifications (c) and (d)

Classification (c) – accounting evolves to meet the needs of the military in peacetime

Military influences on accounting in peacetime reflect the reality that existing accounting knowledge is/was not sufficiently developed to be of immediate use and so an “evolution” or “development” occurred. This small classification contains four articles (7%) covering three countries from the late-sixteenth century through to the mid-twentieth century. Three accounting themes – budgeting, costing and efficiency – give some clue as to how accounting has evolved to meet the needs of the military in peacetime.

Refinement and the pursuit of greater efficiency motivated changes to the Royal Navy’s budgetary estimates in late-Victorian Britain. Moving from a subject-based compilation of expenditures to an object-based approach, two senior reformist politicians 11 engineered, in the face of trenchant opposition from Treasury, a major advance in the methodology of producing the estimates (Cobbin and Burrows, 2010).

The accounting-military-war contribution to the modern debate on the origins of costing and costing procedures is almost exclusively placed in the wartime context. Zan (2004) and Zambon and Zan (2007) are exceptions with Zan (2004) using archival records of the Venice Arsenal in the late-sixteenth and early-seventeenth centuries to demonstrate the emergence of early accounting processes in place and speculate about the use of naïve notions of cost as distinct from expenses and value. Furthermore, Zambon and Zan (2007) analyze two major reports of the time into the Arsenal that investigated cost identification. However, they were not confident enough to link the analysis to later developments in cost allocation. Lemarchand (2002) focuses on state-owned French military arsenals in the mid-nineteenth to mid-twentieth centuries paying particular attention to pressure placed on management to achieve efficiency in production and the most effective means of establishing manufacturing costs. These directives were not designed to maximize the benefit to the state but as a counter to sustained agitation from private interests to have manufacturing transferred to private facilities.

Classification (d) – accounting evolves as a contributor to war

In the highly stressful circumstances of war, solutions to problems are often not afforded the luxury of time as responses may be required almost immediately. From an accounting point of view, this classification is premised on the assumption, as with classification (c), that existing accounting knowledge may not be adequate or sufficient, and so a timely evolution or development may be necessary. The literature contains 19 articles (35%) covering seven countries over seven different war periods from the American War of Independence to WW2. Seven accounting areas are included within the classification – accounting procedures, budgeting, costing, disclosure, efficiency, financing and, for the first time, gender.

The introduction of major pay accounting technology in 1904 shortly after the conclusion of the Boer War was timely as the British Army underwent a dramatic expansion in the lead up to the outbreak of WW1 (Black, 2006a, 2006b). Introduction of the “Dover system’ provided a sound foundation for an improved pay system” (Black, 2006b: 199) which lasted until late into the twentieth century. The advent of war in 1914 brought with it a vastly expanded regime of accounting processes and duties together with a huge expansion in personnel, both military and civilian. At an individual entity level, wartime conditions caused the Guinness Brewing Company in Ireland to rethink its approach to risk assessments with delivery of beer products to markets on mainland Britain. The dangers that lurked in the Irish Sea forced the company to self-insure inventory and in so doing, record a system of reserve funds to meet any exogenous threats to company ships from German U-boats (Quinn and Jackson, 2014).

The Soviet Union during WW2 provides the impetus for Djatej and Saritas (2009) to show how extreme political conditions in times of war can force change regardless of the technical veracity of the outcome. The totalitarian Soviet state threatened draconian consequences on accountants and accounting if changes were not implemented in accordance with state dictates. Managers in state-owned enterprises were subject to “extraordinary and ruthless authoritarian oversight with the threat of execution ever present if a failure occurred” (Djatej and Saritas, 2009: 41). A “total war” mind-set prevailed which led to the simplification of accounting procedures and adoption of “innovative soviet accounting” strategies with most decisions based on an “ends justifies the means” philosophy pursued in the interests of national survival and salvation. This was accounting evolving at the extreme edge.

Changes to budgetary processes driven by wartime conditions are less conspicuous in the literature. The approach adopted by the Italian Government during WW1 is examined by Antonelli et al. (2014) who note, with respect to content in budgets, “when war broke out only one additional category was added to the document ‘War Expenses’ even though this comprised 90 per cent of total costs by the end of the conflict” (p. 139). “The government, the military high command and the main defence contractors preferred concealment” (Antonelli et al., 2014: 151). Manipulation of the expense items through extremely limited disclosure was an important aspect of this action.

The literature demonstrates the interest in costing in the years following the Boer War and the steps taken to remedy deficiencies before the outbreak of WW1. Evidence is also presented of varying attitudes and approaches to costing during the years of WW1, although there is some reservation as to the extent of advancement of costing in the United States and United Kingdom. The dearth of work on war costing in the United States is a phenomenon observed by Fleischmann and Tyson (2000) who review the parallels in costing practices between the United Kingdom and the United States during WW1 and assess the legacy in the immediate post-war years. They document institutional arrangements to manage prices and costs, as instituted by the US government in contrast to the “puffery” (Fleischmann and Tyson, 2000: 197) expressed by the Ministry of Munitions about the standing and state of costing in the United Kingdom. Overall, Fleischman and Tyson (2000) doubt the influence of the war years on costing into the 1920s, a view consistent with that of Boyns and Edwards (2007). As observed by Vollmers et al. (2016), the Italian state in WW1 was particularly vulnerable to opportunistic, fraudulent or illegal activities because there was virtually no oversight or accountability over munitions contracts written on a cost-plus basis. To complicate matters, it appears that private interests appeared to have little understanding or appreciation of their costs, particularly overheads, which perversely, caused some contractors to grossly underestimate true cost to the point that almost culminated in bankruptcy.

As with WW1, WW2 provides excellent opportunities for examination of costing in a wartime setting. There is evidence of poor policy and meddling by the totalitarian Italian state resulting in delivery of problematic accounting outcomes. Cinquini et al. (2016) report how a uniform approach to costing based on a flawed Nazi Germany model during the middle years of the war, was mandated by the fascist state for use in all industries, including munitions. An extension to the work on state control by Djatej and Saritas (2009) cites action by the totalitarian state in the Soviet Union to dictate costing practice. The State had no hesitation in directing simplification of costing particularly the allocation of common costs regardless of the veracity of the process demanded. In this circumstance, production budgets were supreme.

Disclosure has also come under consideration with several examples indicating how wartime impacts on management practice. Despite a reluctance to increase disclosure in financial reports, Maltby (2005) records how company chairmen in the United Kingdom during WW1 used Annual General Meetings and media reporting thereof, to make financial and other disclosures in an opportunistic and at times personally beneficial manner. Rutterford and Walton (2014) cite the Blackpool Tower Company using differential disclosure decisions by directors of new taxes levied during WW1. Entertainments Tax, levied on customer revenue at the point-of-sale of seats, was fully disclosed, whereas the opposite decision was made when it came to Excess Profits Duty levied on “excess profits” (Rutterford and Walton, 2014: 114). Liability for the latter tax presupposed the company making excess profits “calculated under the tax legislation” (Arnold, 1997: 791), but no clarity is provided nor is there generalization of the observation to industry. The Italian WW1 budget (Antonelli et al., 2014) noted earlier, is an example of maximum aggregation that facilitated very limited disclosure. Moving from a full-disclosure model with 114 separate line items, the Italian government added a single line item to the existing budget to cover “War Expenses” providing no detail as to the composition of the number. Conflicting approaches of Nationalists and Republicans before, during and after the Spanish Civil War provides the context to assess the differential approach to accounting and financial reporting. Fernandez-Revuelta et al. (2002: 364) point to the “intersection of political beliefs and ideologies of both Republican [communist] and Nationalist [fascist] with accounting” highlighting how the changing circumstances of the progress of the civil war affected the way accounting disclosure was carried out in a state-controlled power utility in the Almeria Granada region of southern Spain.

Difficulties that the post-English Civil War constitutional arrangements posed to the Army surfaced initially in the aftermath of the American War of Independence (Funnell, 2008) and later Crimean War. The national humiliation and financial ruin in Britain in the aftermath of the American War of Independence is cited by Funnell (2008) as the catalyst for scrutiny of the Civil List and military accounts. Although parliament controlled the finance flowing to the Army, it “had no information as to whether [Army] Imprests were fully expended and whether they had been used for the purposes proposed” (Funnell, 2008: 20). Reformist parliamentarians 12 sought to regain parliamentary control over expenditures from the crown and the executive through the Civil List together with strengthened accountabilities for Army finance, including appointing Commissioners for Examining the Public Accounts and Commissioners of Audit. Scrutiny of the Civil List that followed in the wake of the American War of Independence enabled parliament to extend financial authority over the executive along with reforms to financing of the Secret Service. Increased allocations and enhanced audit oversight placed on the service through the Civil Establishments Act of 1782 brought expenditure on the Secret Service under strict parliamentary control for the first time (Funnell, 2010).

Efficiency in the United Kingdom reached a nadir in the years leading to WW1. The abject lack of efficiency with supply and logistics during the Boer War and the scandals that followed that were subject to high-level public enquiry (Elgin Report, 1903; Esher Report, 1904) provide the background for work that shows how accounting systems, regardless of their underlying quality, can produce unimaginably bad outcomes, precipitate public outcry and facilitate dramatic change (Black, 2001a; Funnell, 2005, 2006b, 2011). The Boer War demonstrated the untenable state of readiness of the British Army to manage financial aspects of the war due to entrenched civilian control. The civilian goal “of economy was incompatible with military efficiency” and “government accounting systems had never been designed with the intention to promote military effectiveness” (Funnell, 2005: 323, 312). The lack of accounting knowledge and particularly costing skills were significant factors in the poor performance of the Army Service Corps and the Army Pay Corps during the Boer War and the years following when vast amounts of surplus war supplies were disposed of in an un-businesslike manner. The inevitable outcome was that military personnel had to acquire financial and accounting skills through enhanced training schemes for there to be a successful transformation. While the civilian service resisted change, the prospect of impending conflict that was to be WW1 changed the dynamics dramatically. “A constitutionally safe Army that denied the Army control over its finances” (Funnell, 2006b: 723) and restricted its ability to wage war was no longer considered tenable in the context of modern warfare. Reforms designed to equip Army officers and men with financial administrative and accounting skills and responsibilities to meet the new order involved new structural and training arrangements. At the organizational level, the Army Pay Department was initially disbanded then reinstated in 1909 and the centralized system of Accountant-General to the Army was replaced by the Assistant Financial Secretary to the Army with the earlier mentioned, Sir Charles Harris appointed. The establishment of the Army Class at the London School of Economics and Political Science (LSE) in 1912 that lasted until 1932 (Funnell, 2006b), and later the Army Costing Experiment that incorporated the Corps of Military Accountants from 1919 to 1926 (Black, 2001a; Funnell, 2006b) provided the training and advanced skills dimension of the reforms.

Although the timing of these changes appeared to be fortuitous for the military with expenditure at an historical high, the years between the Boer War and WW1 witnessed dramatic societal shifts and close examination of government expenditure. Government was under pressure to institute social reforms and a peoples’ budget had been introduced in 1909. 13 Army finance came under great scrutiny with the transfer of control over military finance from civilian to military officials agreed, subject to significant conditions. Robert Haldane, Secretary of State for War (and keen supporter of the forces), required the Army to agree a covenant whereby it undertook to “keep spending under control, introduce objects-based business and accounting principles with a view to efficiency and economy and [at the same time] remain fully prepared for war” (Funnell, 2011: 84, 87).

The final issue that gains significant traction from the exigencies of war is that of gender and gender equity. The movement of men into the fighting services, the freeing up of positions that needed to be back-filled and the growing number of positions created by the expansion of various war economies created conditions for women to undertake roles previously unavailable to them. Black (2006b) cites these factors as reasons for the increase in the number of women joining the Army Pay Department in the United Kingdom in WW1. The trend also saw large increases in the number of military male paymasters, male civilian paymasters, and most interestingly, lady superintendents (female paymasters) (Black, 2006a). Similar employment trends were observed in WW2 in Australia with women again providing much of the manpower to backfill roles as men left to join the armed forces (Ikin et al., 2012). This process was not confined to accounting, but Ikin et al. (2012) use the phenomenon to demonstrate the enduring influence and ever-growing presence of women in the accounting profession in the years since the conclusion of the war. A brief insight into the accounting profession at the firm level in the United States during WW1 is offered by Flesher and Previts (2014) who investigated the impact of the war on top-tier firm Deloitte, Haskins and Sells – present-day Deloitte. They report how the war provided the opportunity for the firm to employ the first female who went on to qualify as a CPA and rise to the level of principal.

The evolution of new accounting knowledge in circumstances where existing accounting knowledge is insufficient is a phenomenon readily observable in the literature and provides ample evidence of the capacity of the discipline to generate new knowledge during peacetime or during wartime. The exigencies of war challenge many disciplines to meet every problem confronted. The accounting discipline has been shown to support Hopwood’s 1987 contention of accounting being “in [constant] motion” and Walton’s 1995 assertion that “wars generate accounting change.” In both time perspectives, but more substantially in the wartime setting, accounting is revealed as a discipline that reacts to the environment within which it is engaged and seeks solutions to challenges and problems that arise. As such it is not only influenced by the military in peacetime but to a much greater extent, by war, demonstrative of the “demand/response theory of accounting development” (Edwards and Newell, 1991: 35).

Concluding comments and further research opportunities

The literature in this review covers more than 400 years, stretching from the Venetian Empire of the late-sixteenth century to the present day, a period that includes extended periods of peace and many major conflicts. Although the literature is compact relative to the wider accounting history literature, it none-the-less, demonstrates variety across this long period. The range of countries covered draws in many of the major protagonists with the state sector predictably, predominant. A range of theoretical frames have also been utilized with descriptive narratives and case studies predominating.

Besides diversity measures, several accounting themes have been identified as either accounting-specific or accounting-related. Accounting procedures, budgeting, costing and disclosure fall within the accounting-specific theme, while financing and efficiency are described as accounting-related. Also within the latter group, research has contributed to the wider work on gender in accounting and the more controversial matter of accounting’s role in some of the darker activities in the recent past. Although most articles are single-themed, a significant minority (33%) are multi-themed. Accounting procedures, costing and contribution to enhancing efficiency within government are where most effort had been directed.

The review is focused primarily on the status of accounting knowledge at the time when accounting engages with the military either in peacetime or during years of war. As to whether accounting knowledge exists in a state fit for purpose or requires further advancement to meet the terms of the engagement is the fundamental question underpinning the review. The existing versus new accounting knowledge divide is the primary means of classifying the literature and the primary variable of interest in the examination process. This divide reveals a relatively even spread between the “existing” and “new” knowledge domains. Within each grouping, a further divide based on whether the research is set within a peacetime setting or years of war provides a stark contrast with the overwhelming proportion of the research focused in wartime settings.