Abstract

This article contributes to remedying the paucity of biographical information about Australian luminary accounting figures in the first half of the twentieth-century, a period of enormous change and development in the accounting profession, particularly in relation to its organisational structure, international links, literature, intellectual base, education and role in relation to government in both peace- and war-time. It is argued that no individual luminary is more neglected by biographers, yet deserving of extended biographical treatment, than Sir Edwin Van-der-Vord Nixon, one of the great figures in Australian accounting, whose eponymous firm was a critical antecedent to the present day EY Australia. Nixon’s career spanned the crucially important ‘coming of age’ period in Australian accounting. The key evolutionary developments in Australian accounting that provided the foundation for the modern profession are the backdrop against which Nixon’s lifelong career in accounting can be observed.

Introduction

Edwin (later Sir Edwin) Van-Der-Vord Nixon belongs to a small coterie of accountants who played key roles in what were the critical years in the development of the accounting profession in Australia: from the last decade of the nineteenth century until the end of World War 2. These years witnessed, inter alia., major developments in the organisation of the profession and its international links, the introduction of rigorous examinations, the evolution of university studies in accounting, a proliferating professional literature and the involvement of accountants in a major way in the administration of World War 2. Nixon participated in all these developments while forging his own professional reputation. This long and complex period of transition provides the backdrop against which his almost six decades in accounting can be observed.

While organised accounting in Australia traces its roots to the establishment in 1885 of the Adelaide Society of Accountants (Parker, 1987), the discipline was present in some form almost from first British settlement in 1788 (Craig and Jenkins, 1986; Gibson, 1986; Goldberg, 1956). However, it was not until well into the twentieth century that the discipline was established firmly within the commercial fabric of the country. Milestone events in this process include not only the 1885 development in Adelaide, but in 1886 the establishment of the Incorporated Institute of Accountants, Victoria (IIAV), in 1894 the Federal Institute of Accountants (FIA), in 1906 the Australasian Corporation of Practising Accountants (ACPA) and in 1910 the Association of Accountants of Australia (Inc.) (AAA). The IIAV was renamed the Commonwealth Institute of Accountants (CIA) in 1921, the same year in which the Australasian Institute of Cost Accountants was founded. Following the granting of a Royal Charter in 1928 the Institute of Chartered Accountants in Australia (ICAA) came into being. 1 As noted by Brentnall (1938: 64), Australians establishing local accountancy associations ‘followed in their [British bodies’] footsteps’. Close attention was paid to the mother-country as associations ‘were formed on the British model, but independent of British bodies’ (Parker, 1994b: 597), although there were some variations around the matters of practitioner status and membership. Most associations were ‘inclusivist’ (Carnegie and Parker, 1999: 78) with ‘open-door membership policies’, admitting both public practitioners and those engaged in other fields of accounting (Poullaos, 1994: 119). Before 1928, only the ACPA ‘modelled its exclusivist strategy on the Institute of Chartered Accountants in England and Wales’ (ICAEW) (Carnegie and Parker, 1999: 78).

Within this ‘complex genealogy’ (Carnegie et al., 2003: 794) of ‘indigenous professional bodies’ (Johnson and Caygill, 1971: 161) the only British-based association to establish branches in Australia was the Society of Accountants and Auditors (SAA) which had ‘adopted a vigorous overseas’ approach (Johnson and Caygill, 1971: 157), especially in the ‘settler’ colonies of Kenya and Australia (Parker, 2014: 176). Establishing branches in Victoria in 1886 and New South Wales in 1903, the SAA maintained a modest presence throughout the first half of the twentieth century with its requirements for membership in the colonies mirroring its inclusive approach in Britain (Garrett, 1961). In contrast, the Institute of Chartered Accountants in England and Wales (ICAEW, 1966: 173), rather than establishing formal branches in its own name, pledged to ‘foster the development of an accountancy body in any country’. In Britain, the ICAEW had a strong public-practitioner orientation with full membership restricted to practitioners qualifying in England or Wales only (ICAEW, 1966: 22–23). Although it had no branch-based presence and local practising members rarely numbered more than 30 (Johnson and Caygill, 1971), as the ‘great parent body’ (Johnson and Caygill, 1971: 160) it was ever vigilant in protecting the ‘chartered brand’ (Poullaos, 1994: 124). Its Australian-based members often acted ‘as the local representatives of large and expanding international accountancy firms’ (Johnson and Caygill, 1971: 160).

Another key marker of the development of the profession in Australia was the emergence of professional journals as a means of promoting discourse in the discipline, shown in the following chronology:

1901: Public Accountant (ACPA);

1915: Federal Accountant (FIA);

1921: Commonwealth Journal of Accountancy (later Australian Accountant) (CIA);

1930: Accountant in Australia (later Chartered Accountant in Australia) (ICAA).

Almost from the founding of the discipline in Australia, access to membership of local bodies was determined by success at regular examinations (Australian Society of Accountants, 1962; Graham, 1978). A supporting infrastructure evolved that included student societies, coaching colleges, lectures on technical topics, articles in professional journals and an extensive range of texts and monographs. 2

Exactly when the Australian discipline – and the discipline more widely – attained professional status is an open question. In a global context, Stacey (1954: 19, 176) cautioned that ‘any attempt to isolate the moment when … the profession of accountancy … sprang fully armed, into the economic area, remains a difficult task’. Nonetheless, he suggested that ‘the consolidation of the profession … during the mid-thirties [of the twentieth-century] could not have been attained without the social and economic advance of its individual members’, a conclusion arguably applicable to the Australian profession. The granting of the Royal Charter in 1928, viewed by Pouallos (1994: 3) as the culmination of ‘over forty years of effort to turn Australian accountants into professional men’ further bolsters the claim. The 1936 Australasian Accounting Congress in Melbourne was also pivotal, demonstrating the robustness and maturity of the profession and attracting extensive newspaper coverage 3 in the process (Anderson, 2002; Linn, 1996). Marshall (1978: 26) opined that as an ‘eminently successful example of co-operation between Australia’s leading, and rival, accountancy bodies’ the Congress was to be the final seminal event in the pre-World War 2 period. In summary, by the outbreak of hostilities in 1939, the discipline in Australia was in an advanced state of professionalisation. Remarkably, EV Nixon, the subject of this paper, has a presence in all the seminal events that underpin the evolution of accounting in Australia to the end of World War 2.

Biography in Australian accounting history

The assertion by Peloubet (1948) quoted by Previts et al. (1990: 137), that ‘the growth of a profession is largely the reflection of its great personalities’, is apposite in the context of the Australian profession moving from one with close links to senior bodies in Britain to one largely independent of the mother country and fully integrated into the local commercial world. While the Australian profession had established itself through the proliferation of home-grown accounting societies and activities, the ICAEW and, to a lesser degree, the SAA, were ever-present and influential (Carnegie and Parker, 1999; Poullaos, 1994). In similar vein, company law developments dating from the initial Companies Statute (Victoria) 1864 reflected legislative developments in Britain (Parker, 1994b). However, despite British influence, the progress and relative independence of the local profession also reflected Australia’s ‘growing national identity’ (Carnegie et al., 2003: 807) as it progressed from a country less dependent on Britain in the aftermath of Federation in January 1901 to one fully independent with the passing of the Statute of Westminster Adoption Act in 1942. Many advancements within accounting during these years owed much to the capacity and vision of the imposing characters who drove the process, but biographical records of their contributions and achievements are sparse, particularly for those active into the first half of the twentieth century.

Biographies of Australians who were instrumental in accounting’s development to this point include four ‘luminary accountants’ (Walker, 2000: 318), namely Alexander (later Sir Alec) Fitzgerald (Burrows, 1989; Carnegie and Williams, 2001; Goldberg, 1988; Goldberg and Burrows, 1996; Goldberg et al., 1994), Garrett Fitzgerald (Goldberg and Burrows, 1996; Goldberg et al., 1994), Leslie Schumer (Anderson, 2002), and, in a limited manner, Edwin Nixon (Castles, 2000; Nixon, 1976) who is the focus of this paper. Each was a part-time academic and, except for Schumer – the general manager of a major road-transport company – principals in private practice.

Paradoxically, the Australian biographical record for the same period is surprisingly strong for accounting personalities variously labelled the ‘less illustrious’ by Walker (2000: 318), ‘those beyond the limelight – the unconnected, the humble, the suppressed, the unqualified and the rogue’, (Carnegie and Potter, 2000: 305), and those engaged in ‘inglorious moments in accounting history’ (Shelton and Jacobs, 2015). These lesser lights include early authors of accounting texts, John Scouller (Goldberg, 1977, 1984), Edward Wild (Carnegie and Varker, 1995), James Dimelow (Carnegie and Parker, 1994), William Yaldwyn (Carnegie and Parker, 1996) and Francis Vigars (Carnegie et al., 2006); the first chartered accountant émigré, John Ogilvy (Carnegie et al., 2000); two early female members of the profession, Mary Hamilton (Cooper, 2008) and Harriet Amies (Hronsky et al., 2015); fraudster, William Chinnery (Scorgie, 2007); and four Irish rogues and transportees, John Kenny, Michael Hayes, Jeremiah Murphy and John Campbell (Craig, 1998a, 1998b, 1998c; Craig et al., 2004).

For Australian accountants who became active in the latter half of the twentieth-century, accounting’s biographical record is less sparse for the nation’s leading lights but barren for the less illustrious. Despite the observation by Carnegie and Potter (2000: 194) that ‘wide scope seems to exist for accounting history scholars to develop … biography’ and Bisman’s (2012: 9) opinion that ‘the call [by Carnegie and Potter, 2000] for more biographical research appears to have been taken on board by scholars’, the reality is that Australian accounting historians have mostly directed their endeavours in directions other than biography. Exceptions to this trend include six notable academic accountants, namely Louis Goldberg (Burrows, 2003; Carnegie and Williams, 2001; Kerr and Clift, 1989; Parker, 1994a), Raymond Chambers (Al-Hogail and Previtts, 2001; Barton, 1982; Bedford, 1982; Brown, 1982; Carnegie and Williams, 2001; Clarke, 2000; Gaffikin, 2000; Lee, 1982; Moonitz, 1982; Wells, 2000; Wolnizer and Dean, 2000; Whittington and Zeff, 2002), Russell Mathews (Whittington and Zeff, 2002), Reginald Gynther (Whittington and Zeff, 2002), Allan Barton (Shelton and Jacobs, 2015) and Robert (Bob) Gibson (Carnegie, 2016). With the exception of Bob Gibson each of these individuals has been honoured with membership of the Australian Accounting Hall of Fame 4 (AAHF): Chambers, Fitzgerald and Gynther in 2010, Goldberg in 2011, Mathews in 2012 and Barton in 2013 (University of Melbourne, 2016a).

The remainder of this article focuses on the life and work of Edwin Nixon (1876–1955), one of the major pioneers of Australian accounting. Nixon warrants attention for several reasons. First, as already indicated, the evolution of the Australian accounting profession and its coming of age in the first half of the twentieth century, including the battle for ascendancy between professional bodies and the internal tensions within these organisations, coincides with his working life and so provides a clear background against which his contribution can be observed. Second, the duo of existing biographies are either largely inaccessible (Nixon, 1976) or extremely concise (Castles, 2000). Third, there is every reason to document more fully his contributions as his standing in the accounting and business worlds was recognised in his lifetime by the award of two high-level Imperial honours and, posthumously, in 2012, by election to the AAHF which honoured him as a ‘pioneer, practitioner, administrator, author, educator and leader of the accounting profession’ (University of Melbourne, 2016c). This paper is thus a response not only to the call issued to expand the biographical literature on Australian accountants (Carnegie and Potter, 2000) beyond the ‘origins and firsts’ (Carnegie and Williams, 2001: 103), but also to the challenge posed by Shelton and Jacobs (2015: 21) to produce ‘further work … to reveal the biographical value and broader contribution of a number of these [AAHF] inductees’.

In his predominant professional role as a chartered accountant, we label Nixon a progressive traditionalist, a characterisation borrowed from McArthur’s (2005) depiction of celebrated Canadian architect, John M. Lyle, initially a traditional architect-practitioner who was gradually influenced by emerging avante-garde thoughts and practices. In similar vein, Nixon was firmly entrenched in traditional practice of the day, fastidious in his adherence to principles but not averse to adopting and advancing contemporary ideas and techniques as they emerged. Addressing the 1936 Australasian Congress, he observed that ‘accounting is not static, it must change with the times … whether we like it or not … the trend of commerce today increases our responsibility and demands high training’ (Nixon, 1936, as reported in the Melbourne Argus, 17 March 1936: 13).

The narrative that follows is structured thematically, the themes symbolising the evolving activities and responsibilities that contributed to Nixon’s achievements. As it happens, the themes mostly fall into a natural chronological order. Against the background of his full life of 79 years, including 58 years as an accountant of which 43 years were in private practice, we first cover his arrival in Australia, then his early school and working life, entry into the accounting profession, establishment of his own practice, involvement in professional and academic bodies and congress organisation, authorship, ethicist, advisor to governments in both peace- and war-times, and company directorships. Our coverage consolidates a range of materials contained in diverse primary and secondary sources set against a background of contemporary socio-economic, political, national-security and professional developments, to provide essential context to his achievements. We also draw on first-hand recollections of family members in attempting to provide a rounded picture of the individual behind these achievements.

Migrant/teacher/accountants’ clerk

Edwin Van-Der-Vord Nixon was born on 31 March 1876, in St Helier, Jersey, Channel Islands, to Thomas Nixon, a watchmaker, and his wife Jane, nee Vandervord (Castles, 2000). His parents accorded him the Belgian-style hyphenated version of his mother’s maiden name. The Nixon side of the family hailed from Foleshill, a village 3 km north of Coventry in Warwickshire in the English Midlands (England and Wales (EW) Census, 1861, The National Archives (TNA), RG9/2197, Folio 61: 12). Jane Vandervord’s surname indicates Flemish ancestry, although she was born in Stepney, East London in 1843. The Nixon-Vandervord marriage occurred at Witham, Essex, on 1 July 1871. Exactly when the couple moved to the Channel Islands is unclear but the 1881 census records eight occupants including Edwin at 7 Parade Place, St Helier, Jersey (EW Census, 1881, TNA, RG11/5,610, Folio 36: 3).

Within a year of the move to Jersey the family were steerage passengers aboard the 2,977-tonne S.S. Dorunda bound for Australia. The passenger manifest records them as ‘remittance’ passengers, indicating that they had been nominated by a Queensland resident, unknown (Queensland State Archives, Index to Registers of Immigrant Ships Arrivals 1842–1912: 100–102) with the cost of the passage largely remitted by the government to the ship’s owners. The Dorunda arrived at Brisbane on 8 April 1882. On arrival, Nixon as a six-year-old would have been enrolled in the state school system as compulsory primary education was already well established in Queensland (State Education Act (Queensland), 1875, s. 28).

In 1891, aged 15, he was employed as a pupil-teacher at South Brisbane State School as a potential pathway into the teaching profession at a time when formal teacher-training programmes were non-existent. It was also a government strategy to staff a burgeoning school system caused by high levels of immigration into the colony (Logan and Clarke, 1984). In 1894, Nixon was appointed head-teacher at a single-teacher school near Gladstone on the central-north coast of Queensland (Castles, 2000). In 1896, he moved inland to the mining town of Mount Morgan on promotion as assistant-teacher Class III, Division 3 (Queensland Government Gazette, 1896) before returning to Brisbane in 1897 as a teacher at the State School for Boys, Kangaroo Point (Queensland Government Gazette, 1897). Nixon’s six years of relative job security in the Queensland teaching service commenced during the severe economic depression of the early 1890s (Sinclair, 1976) and ended with the resumption of economic expansion at the turn of the century (Butlin, 1955).

Accountants’ clerk to accounting practitioner

After his time in the teaching service, Nixon resigned at the tender age of 21 and four years later, in July 1901, was admitted to associate membership of the British-based SAA. Although the details are not known, he most likely completed the articles-experience and examination requirements while employed in an accountant’s office in Brisbane (Garrett, 1961). Why Nixon chose the SAA in preference to a local society such as the Queensland Institute of Accountants is a mystery. A ‘psychological allegiance to Britain’ (Parker, 1987: 135) or a simple belief that it was a more prestigious option may have been the motivation for this choice. Regardless of the reason, Nixon retained fellowship membership until his death in 1955 (Anon., 1955a, 1955b) Having qualified for admission to the SAA he must have sensed the time was right to move, in 1901, to Victoria with his ailing mother just as the state was emerging from the economic wreckage that followed the collapse of the speculative land boom and subsequent depression. The remainder of his working life was spent in Melbourne. In his new state, he also joined the ‘inclusive’ IIAV in 1906, immediately following its unsuccessful 1904 attempt to gain a Royal Charter (Poullaos, 1994). His motivation for joining the IIAV was possibly ‘to ensure that [his] professional loyalties were balanced’ (Carnegie and Parker, 1999: 95). As a member of the IIAV of two years’ standing and at 32 years of age, Nixon observed the events that led to the creation, in 1908, of the ACPA (Carnegie et al., 2003; Graham, 1978) and the second unsuccessful Charter attempt in 1909. In the new ACPA, he was a founding associate member who, by the time of the transformation of the ACPA to the ICAA two decades hence, had advanced to Fellow. He relinquished membership of the IIAV in 1914 but remained a member of the ACPA. In 1928, following the granting of the Royal Charter and the establishment of the ICAA, he was entered as a founding member at Fellowship level.

Soon after his arrival in Melbourne, Nixon gained employment as a clerk in the office of Lyell, Butler & Densham at 349 Collins Street, Melbourne where he came under the influence of Andrew Lyell, ‘an accountant of distinction’ (Falkus, 1993: 16), who had been a city practitioner since the 1860s. When Densham left to enter into partnership with Anthony Sherlock, Nixon followed progressing quickly to managing clerk in the newly created Densham & Sherlock. Following his marriage in November 1905 to Amy Mabel MacKenzie, the sister of Densham’s wife, partnership-status was undoubtedly in prospect (Nixon, 1976).

When in early 1912 Nixon was passed over for promotion to partner his reaction was swift. He severed links with Densham & Sherlock to establish the eponymous firm Edwin V. Nixon – Accountant which commenced operations on 1 April of that year at Collins House, 360 Collins Street, Melbourne, then the epicentre of the Melbourne business establishment (Nixon, 1976). Slow but steady growth followed. Over a 15-month period, he earned a modest £A200 on which he maintained a wife, two young sons and his mother who lived separately from the family (Abrahams, 2006). 5 In 1920, Nixon entered into partnership with James Ogilvy, at which point the firm’s name was changed to the long-standing Edwin V. Nixon & Partners. Under his leadership for the next 35 years, the firm evolved into one of Australia’s leading accounting firms, initially with the Melbourne office at 401 Collins Street. 6 From 1941 onwards, it developed a national profile through a series of agreements with interstate practices in Sydney, Adelaide, Perth and Brisbane.

Among the major companies that engaged the firm to undertake their annual statutory audits was the Broken Hill Proprietary Company Limited (BHP), then Australia’s largest publicly listed company, which in 1946 appointed Nixon as one of its joint auditors. The board of directors of BHP had, since 1886 and pursuant to its Articles of Association, appointed two individual practitioners rather than an audit firm per se, to conduct the audit. 7 In 1945, BHP’s incumbent auditors were George William Selby and James Leslie Balfour-Melville both members of long-established family firms. Selby had been appointed in 1886 and Balfour-Melville in 1934, replacing his father who had been in office since 1900. Following Selby’s retirement after 60 years of service Nixon was invited to join Balfour-Melville as joint auditor of BHP. That the company continued this policy and appointed Nixon speaks volumes for the reputation that he and his firm had garnered. It also indicated that BHP was finally moving, at least partially, to a top-tier audit firm following the long tenure of Selby and the Balfour-Melvilles. The extraordinary wartime public service rendered by Nixon, covered later, was arguably an important factor in the appointment. Donald Ferguson of Edwin V. Nixon & Partners retained the joint engagement with Balfour-Melville following Nixon’s death in 1955 (BHP Annual Report and Financial Statements, 1886–1956).

In 1953, Nixon and his partners all but agreed in principle to amalgamate with Cooper Brothers & Co., in London, and Cooper Brothers, Way & Hardie in Sydney, but negotiations ceased when the Nixon partners baulked at the possibility of the firm name being discontinued (Falkus, 1993). Big 8 status eventuated shortly after Nixon’s death when, in 1957, the firm became the Australian representative of the international firm, Arthur Young & Company (AY). Abrahams (2006: 46) nominates Nixon’s firm as ‘the catalyst for the foundation of Arthur Young & Company in Australia’, ahead of Fitzgerald Gunn & Partners in Melbourne, and Robertson, Darley & Wolfenden in Sydney 8 as the firm brought a formidable list of ‘blue chip’ clients when the connection was made, including the hugely prestigious BHP. 9 The presence of Nixon as senior partner at the time was of inestimable value in achieving this outcome.

Office bearer

The fact that Nixon’s professional involvement extended beyond his firm was demonstrated by his election in 1919 to the General Council of the ACPA (1926), a position retained until 1926. Wider responsibilities came with membership of the Parliamentary and Law, and Examination committees, culminating in chairmanship of the Victorian Division during 1922–1923 (ACPA, 1926). Via the ACPA, he was at the epicentre of arguably the most significant and controversial event in Australia’s organised accounting history up to that time. The ACPA was the promoter of, and key predecessor body to, the ICAA that was created in 1928 following the award of a Royal Charter (ICAA, 1932c). Nixon served on the ACPA’s Charter Committee and was involved directly in the ensuing negotiations (Poullaos, 1994). Ultimately, the Charter went not to the earlier applicant in 1904 the IIAV, but to the ACPA. It brought ‘social approbation’ (Loft, 1986: 166) and was the ‘symbol par excellence’ (Poullaos, 1994: 3) of professional status wherever British influence was strong, but the result left great bitterness and created an enduring schism in Australian accounting.

In consequence of his proximity to the events of the day, Nixon was named as a foundation Fellow and appointed General Councillor of the new Institute. His name is etched, in perpetuity, along with 29 contemporaries in the Royal Charter (ICAA, 1932c). Membership of General Council brought with it service and influence on a range of ICAA committees, notably Examinations, Library and of most significance, the four-man Executive. 10 On the Journal Committee, he was influential in the appointment in mid-1929 of his University of Melbourne colleague, Alec Fitzgerald, as the inaugural editor of the ICAA’s journal The Accountant in Australia. 11 Additional committee work extended to Applications, Indemnity Insurance, Investigations and Finance.

During 1932–1936, while a General Councillor of the ICAA, Nixon also chaired the body’s Victorian Division. In all capacities, he was a stickler for correct process, objecting on more than one occasion to procedures adopted during meetings and withdrawing from General Council meetings on at least two occasions (Graham, 1978). The withdrawals stemmed from a belief by some members, among them Thomas Brentnall, inaugural President of the ICAA, and Nixon himself, that the absence of Bylaws to the Royal Charter when granted in 1928, and the standing of related Clauses 24 and 25 in the Royal Charter, 12 called into question all preceding decisions of General Council (Graham, 1978). In what Poullaos (1994: 219) labelled ‘the ICAA’s post-natal crisis 1928–35’, Nixon was adamant that much of the business of the General Council prior to resolution of this matter was invalid and that councillors stood personally liable for all decisions taken. This stance was subsequently vindicated when the Privy Council in London approved the Bylaws in September 1932 (ICAA, 1932a) and only finally resolved when the Privy Council issued a Supplemental Charter on 15 January 1935 (Brentnall, 1938; Poullaos, 1994). On this highly contentious matter for the fledgling institute, Nixon’s actions undoubtedly contributed to the legal clarification and finalisation of the matter.

Despite his standing within the ICAA, Nixon was never National President or Vice-President and there is no evidence that he sought high office. The presidency appears to have devolved on geographical grounds. The first president, Brentnall, was a driving figure in the quest for the Charter (Graham, 1978) and a ‘key Melbourne figure, [and] bulwark against the domination of Sydney’ (Poullaos, 1994: 248). Brentnall’s term lasted from 1928 until 1932 followed by Sydney-sider, Sir George Mason-Allard, who held office for 10 years until 1942. 13

Nixon’s involvement in accounting education came with his appointments to the Examination committees of the ACPA and then the ICAA. He brought not only a strong sense of the need to demand high standards from examinees, but also a characteristically unbending attitude to the issue of qualifications, tellingly demonstrated in mid-1939 when the Commonwealth Government was in the process of appointing an advisory accountancy panel in the Department of Supply and Development, covered later. As part of the process, the profession generally was invited to nominate members to serve. Nixon had been appointed chair of the panel but was adamant that only members of the four major accounting bodies, specifically the ICAA, CIA, FIA and AAA were acceptable on the grounds of the examinations required for membership. Objecting to participation by the International Institute of Accountants (IAA) because he felt the IAA’s examination requirements were not as rigorous as those of the nominated bodies, Nixon indicated he would be unable to serve if his expectations were not met. The government acceded to his request, but it triggered bitter recriminations and considerable correspondence and advocacy for, and on behalf of, the IAA. 14

Through his early role in the ACPA Nixon was also a member of the Joint Council of Accountancy Bodies (JCAB) in his home state of Victoria from 1920 (CIA, 1920) until the creation of the ICAA in 1928. The JCAB was established as an umbrella body to represent the ACPA, CIA, FIA and the local branches of the SAA in dealings with government, business and academia. The arrangement came to an end with the creation of the ICAA (Burrows, 2006).

Through the JCAB, Nixon established links with the University of Melbourne. In late-1924 the University established the Faculty of Commerce to undertake, among other things, the teaching of accounting. To determine the regulations that would govern the new Faculty and the curricula to be introduced, a committee was established to which the accounting profession, through the JCAB, was invited to join (Poynter and Rasmussen, 1995). Nixon was its nominee. Once the Faculty was established as the decision-making body, the accounting profession, as a stakeholder, was again asked to be represented via the JCAB. Initially as its nominee, Nixon was on Faculty during 1925–1931. When the JCAB was disbanded, membership of Faculty was ‘transferred’ to the ICAA alone with Nixon retaining the position on behalf of the chartered body. It was probably through his influence that examination exemptions, which had previously applied to members of all bodies represented by the JCAB, were restricted to ICAA members during 1930–1932, a move not surprisingly opposed by the other bodies. Whether Nixon’s conduct was opportunistic and represented a betrayal of the trust placed in him by the non-chartered bodies, or whether with the demise of the JCAB he was expected by the ICAA to advance its interests solely, even at the expense of its rivals, is not known. The university moved quickly to correct the anomaly once it became apparent that the other accounting bodies had been excluded.

Nixon’s long and extensive period of service as councillor, state chairman and committee-man for both the ACPA and ICAA meant that he had been well placed to help ‘build the profession internally’ (Previts and Robinson, 1996: 83). This period of service ended in mid-1937 as ICAA records no longer list him in any of these capacities. It appears he had made a conscious decision to withdraw from all institute-related duties, probably because of the important tasks that were in prospect with the government as the storm clouds of conflict gathered over Europe.

Academic, author and ethicist

Nixon’s involvement with the Faculty of Commerce in the University of Melbourne changed on 18 December 1924 when he was appointed as a part-time lecturer ‘to supervise’ the teaching of accounting and auditing within the then Department of Commerce (Burrows, 2006: 8). In this role, he was the first ‘head of discipline’ in accounting (248), remained on the teaching staff during 1925–1929 and holds the distinction of delivering, on 31 March 1925 – his 49th birthday – the first lecture in accounting at the university. While his teaching role was limited to 15 lectures per year, the work was delivered in addition to the heavy workload he carried as principal of his firm. Although detailed records of appointment processes cannot be located, it is likely that he was instrumental in the contemporary appointment of Alec Fitzgerald as his assistant-lecturer, the first step in Fitzgerald’s rise to becoming the university’s and Australia’s first professor of accounting (Carnegie and Williams, 2001).

Despite the evolution of university studies in accounting from the 1920s in which Nixon was an important player, the major means of entry into the accounting profession for the next four decades was examination by professional accounting bodies. His strong support for this pathway is demonstrated by lectures delivered to the Student Society of the CIA that were subsequently published in professional journals covering ‘the criticism of accounts’ and ‘holding companies’ (Nixon, 1924, 1928). In the 1924 lecture on the ‘criticism of accounts’, Nixon begins with a recitation of the nature of accounts to be found in the balance sheet and profit and loss statement then follows up with an assessment of the potential problems that might arise from each. Simple ratios were mentioned suggestive of the more complex issue of ratio analysis and interpretation of accounts. Although styled as a criticism, the lecture and the subsequent paper are not criticisms of the quality of accounts per se but more an explanation of how to critique the information with a view to extracting greater understanding. In the second of his lecture papers, Nixon (1928), reporting issues associated with the emergence of the holding and subsidiary companies is the focus. Various methods of business acquisition and subsequent combination are covered prior to outlining the possibilities for group reporting. Comparisons are made between the extant English approach that disapproved of full consolidation in favour of the inclusion of a separate schedule listing various attributes of subsidiaries controlled and the American approach that encouraged consolidation of accounts. On balance, and not surprisingly Nixon advocated for the English approach but concedes that regulatory intervention via amendment to the Companies Act would likely follow in the near future.

In 1928, Nixon co-authored, with his university colleague, Alec Fitzgerald, the monograph Some Problems of Modern Accountancy: A Series of Four Lectures (Nixon and Fitzgerald, 1928). Each author contributed two of the four essays published. Nixon’s ‘modern developments in accountancy’ summarised developments in accounting from antiquity until the present day and then proceeded to analyse the role of the accountant in modern business to conclude that, due to the complexity of business, the role had evolved into that of a chief finance officer (or as titled in the USA, ‘controller’) who provided information to support management decision making. His second essay, ‘control through accounts’, examined the extension that had occurred with respect to the finance and accounting functions that took in, among other things, costing and budgeting. The major theme of the paper highlighted the importance of the forecasting function and the preparation and deployment of the budget as a management tool. Although a modest 35-page volume, Some Problems is one of the earliest normative research monographs in the Australian accounting literature. 15

The text of an address delivered to Queensland members of the ICAA in Brisbane in May 1932 was published that year in the Accountant in Australia, under the title ‘The shareholder’s right to information’ (Nixon, 1932). On this occasion, Nixon cited the very contemporary 1931 Royal Mail Steam Packet Case (RMSP) (Rex v. Lord Kylsant & Another) and the recently updated 1931 Companies Act to argue that a conscientious accountant would not limit his actions to the minimum prescribed by the law. In so doing, he suggested that changes incorporated in the new Companies Act were following accounting that had evolved in practice. The question of asset values is also addressed with suggestions about the potential to adjust based on values other than cost. Although the lecture was delivered in 1932 at the height of the Great Depression, Nixon chose not to add any historical context to his comments on asset valuation possibilities. The stability of historical cost, in his opinion outweighed the potential volatility associated with alternative adjustment options. In closing his address, Nixon turned his attention to the auditor suggesting the focus should be on fair presentation thus ensuring shareholders are told the truth. Finally, ‘budgetary control’ (Nixon and Fitzgerald, 1935) appearing in the Chartered Accountant in Australia, was a compilation based on the text of addresses to the ICAA’s Victorian Research Society in February 1935 by himself and his occasional collaborator, Alec Fitzgerald. On this occasion, Nixon discussed the mechanisms and processes necessary to prepare a master budget and the need for monitoring of performance and the desirability of active adjustment of the budget figures to reflect actual performance.

Notwithstanding his technical output and later publications in his government role (covered later), Nixon’s most enduring contribution was a series of seven finely crafted articles published in the Accountant in Australia during January–July 1931 on the emerging issue of professional ethics (‘Mentor’, 1931a, 1931b, 1931c, 1931d, 1931e, 1931f, 1931 g). According to LD Parker (1987: 124), this was a new area in the professional discourse as ‘virtually no evidence … of published discussion of [accounting] ethical issues [in Australia] … is detectable until the early 1920s’. Written under the pseudonym ‘Mentor’ under the title ‘The ethics of the accountancy profession’, these articles were the basis for the codified ethical pronouncements of the profession for the next 35 years. In April 1932, the series was compiled into a hardcopy booklet titled The Ethics of the Accountancy Profession and circulated to every member of the ICAA (Fitzgerald, 1932: 133; ICAA, 1932b). In the introduction to the series Nixon/‘Mentor’ (1931a: 61) acknowledged the debt owed to an earlier English monograph Etiquette of the Accountancy Profession (Anon., 1927; ICAEW, 1927) written by an anonymous chartered accountant, itself based on a series of articles in The Accountant. While there is some commonality between the two publications in chapter titles, 16 a close analysis indicates that, while Nixon may have taken Anon’s chapter headings as a guide in ordering his own work, there is no duplication of wording nor semantic resemblance in content to the ICAEW material. Nixon’s articles, which extended over 52 pages in consecutive issues of The Accountant in Australia, included chapters covering:

I. What is a profession?

II. The code of professional ethics;

III. The power of the council to impose penalties;

IV. The fundamental rules;

V. Acts or defaults discreditable to a public accountant;

VI. Advertising;

VII. Touting or the solicitation of business;

VIII. Supervising another accountant;

IX. The accountant’s certificate;

X. Contingent fees;

XI. The confidential relations of the accountant with his client and

XII. Conclusions.

In the April 1932 edition of the Accountant in Australia, timed to coincide with the distribution of the booklet, the journal’s editor, Alec Fitzgerald (1932: 133–134), drew attention to the importance of the series, particularly to the ‘admirable manner in which the articles covered the many difficult and delicate phases of the written and unwritten law on a subject of vital importance to organised accountancy’. On this occasion, Fitzgerald unmasked Nixon as the author. The series generated considerable correspondence with ‘Mentor’ providing answers and feedback to queries, via the journal (e.g. see ICAA, 1931: 481–482; ‘Mentor’, 1931h, 1932). Ex poste assessments of Nixon’s efforts in this area have largely echoed Fitzgerald’s contemporary praise. To Marshall (1978: 22) ‘they represented the first comprehensive and detailed analysis of ethical issues … undertaken in Australia at the time’. Linn (1996: 123) suggests they were ‘the first attempt to verbalise how accounting ethics were determined’. Although LD Parker (1987: 124–6) noted the existence of an earlier ‘informal code of ethics of the Australian accounting profession’, 17 he conceded the significance of the attention Nixon attracted and the influence exerted prompted other major accounting bodies to focus seriously on the matter of professional ethics for their members.

At this stage, Nixon’s articles represented a personal view on the question of ethics. In response to his initiative in this area, the ICAA’s General Council asked him ‘to draw up a Code of Rules booklet’ based on the ‘Mentor’ series. 18 The resultant Code of Ethics (Code) (ICAA, 1937) was distributed, under Council direction to all members of the ICAA and in May 1937 General Council formally adopted the Code as the Institute’s official proclamation on ethics while also minuting its appreciation for Nixon’s efforts. 19 The Code was a slim, 14-page version of the original set of articles. 20 In this format, it was amended from time to time, being last updated in 1959, 21 until finally replaced by the Code of Ethical Rules in 1967 (ICAA, 1967). 22

In a modernist context, the standards issued jointly in the name of the profession in Australia by the Accounting Professional and Ethical Standards Board (APESB) are the present-day legacies of Nixon’s efforts. The APES series that includes APES 100: Code of ethics for professional accountants, APES 200 Professional standards applicable to all members and APES 300: Professional standards for members in public practice (APESB, 2007–2015) is a complex and comprehensive set of expectations stretching to 346 pages that reflect contemporary societal and community norms and complex modern-day business and practice, many of which have changed dramatically since Nixon wrote as ‘Mentor’.

While the material in the 1937 Code has been totally subsumed within the APES series, the areas of concern to the profession in the 1930s endure indicating the present state and status is due in no small part to the initiative and work undertaken by Nixon as Australia’s first authoritative contributor on the subject and its first accounting ethicist (Graham, 1978).

A listing of his publications contained in Appendix 1 shows that, despite a busy professional and academic schedule, Nixon was keenly engaged in discourse through the professional journals. Moreover, his publications were distinguished both by their literary qualities – his simple direct prose style made the difficult look easy – and their surprising breadth. Accounting history, budgeting, financial management and professional ethics all featured as well as the more predicable matters of treatments and disclosures in financial statements that might be expected of a practitioner with a large audit practice. The breadth of topics covered is also interesting as the range is reflective of his work as practitioner heavily engaged in the market for audit services and in providing advisory services to clients.

Congress organiser and presenter

Inspired by the success of International Congresses in Accounting in 1904 (St Louis), 1926 (Amsterdam), 1929 (New York), and 1933 (London) and despite their internecine rivalries, three major Australian accounting bodies – ICAA, CIA and FIA – began planning in 1934, for an Australasian counterpart to these international events. As Vice-President of the Executive Committee, Nixon played a central role in organising the Australasian Congress on Accounting that was held in Melbourne during 16–20 March 1936. The importance of the Congress according to Linn (1996: 101) was that ‘without the stimulation of conventions, the progressive fruits of Australian accounting would wither on the branches of narrow parochialism’. The format of the Congress followed closely that of earlier international congresses held overseas with papers circulated in full to all participants. At the two technical sessions held each morning, resumes were given by authors followed by commentaries and open-forum discussions (Australasian Congress on Accounting, 1936: 3). The technical programme included papers on ‘public finance, presentation of accounts, preference shares, auditor’s report, accounting terminology, cost accounting, budgetary control, and the history of the accounting profession’ (p. ix).

In addition to his organisational role, Nixon delivered the penultimate technical paper and chaired one of the technical sessions. His paper, ‘the history of the accounting profession, and the position of the accountant in commerce’, presented to over 800 delegates in the Melbourne Town Hall was subsequently published in the Congress Proceedings (Nixon, 1936). This was the last article published by Nixon in the profession arena. In what was largely an historical paper ranging over the evolution of accounting from the early-middle ages to the present, Nixon recorded his debt to seminal accounting-history works by Brown (1905) and Littleton (1933). In addition to the historical material, the RMSP Case was cited again to demonstrate that accountants and auditors should consider carefully disclosure in financial statements and the question of fairness and truth to shareholders. Finally, he turned his attention to the matter of education and the syllabus confronted by candidates for membership of the profession, opined the lack of engagement with candidates by the various institutes and called for greater engagement between the profession and university sector.

Peacetime advisor to government

When establishing Royal Commissions, governments turn to the most highly respected and capable individuals or

Together with the Hon. David Ferguson, retired judge of the Supreme Court of NSW, he was appointed, in October 1932, to conduct the Royal Commission on Taxation (Commonwealth of Australia, 1932), an enquiry which reported in March 1934. In this period, the Australian states levied their own income taxes and the Commission’s terms of reference were, inter alia., to inquire into and report upon the simplification of the taxation laws of the Commonwealth and of the States in so far as they relate substantially to the same subject matters of taxation … [and] to make recommendations for the purpose of obtaining uniformity in legislative provisions including provisions relating to procedure and forms of Return.

The commissioners’ recommendations regarding uniformity between the jurisdictions were praised by contemporary observer, White (1934: 73), for ‘the manner in which they have handled this most difficult subject’. According to Ferguson’s biographer, Arthur (1981), all recommendations of the Commission were ‘largely accepted by all Australian governments’. The recommendations relating to the taxation of company profits and dividends largely endured until the advent of dividend imputation in 1987. The commissioners’ involvement did not go unrewarded: Ferguson was created Knight Bachelor in 1934 for his chairmanship (Australian Government, 2016a) and Nixon made a Commander of the Order of St. Michael and St. George (CMG) in 1935 (Australian Government, 2016b).

The Royal Commission into the Monetary and Banking System which sat from November 1935 until August 1937 (Commonwealth of Australia, 1935) was established in the aftermath of the banking and financial-system failures which occurred during the depression years of the 1930s (Sinclair, 1976: 195). On this occasion, Nixon was one of six commissioners under the chairmanship of John (later Sir John) Napier, then a judge of the Supreme Court of South Australia. Future prime-minister, Ben Chifley, was also a member. Ultimately – and several important recommendations were only adopted as part of wartime financial controls – the Commission influenced the increased power of the Central Bank over trading banks through minimum liquidity and deposit requirements. It was also the catalyst for the Commonwealth Bank of Australia establishing a mortgage department designed to provide long-term finance to the rural sector, the lack of which department had become evident in the course of the Commission’s hearings.

Nixon also sat on three additional public enquiries in 1938, at the national level examining the film industry, the granting of small loans, and other aspects of taxation. Earlier in 1932–1933, the Victorian Government called upon him to investigate the finances of the Victorian Railways with a view to advising particularly on the prospects for re-capitalisation of that undertaking. Nixon recommended a £A30 million reduction in the Capital Account of the Railways that was subsequently accepted by government (Victorian Railway Commissioners, 1936: 9).

Wartime adviser to government – the advent of war

Of critical importance in a national security context was Nixon’s services to government made immediately prior to and during the dark years of World War 2. In late-1938, the Commonwealth Government decided that to be fully self-sufficient in the supply of munitions during the impending conflict, private industry would be permitted to manufacture, for the first time, munitions for a profit (Street, 1938). This change of policy brought with it a decision to utilise potentially troublesome cost-plus contracts as the means of rewarding private contractors. Government was aware of the potential for abuse on the part of contractors if stringent cost identification and control measures were not implemented and, with its pro-business leanings, was attuned to the political cost of any perception that private contractors were engaging in war profiteering. 23

In 1938, Nixon was appointed to the Contract Board that oversaw all contract negotiations and delivery of all contracts with private interests. 24 Next, in June 1939, the government established the Advisory Accountancy Panel in the Department of Supply and Development (AAP-SD) to provide advice on costs and profits in munitions manufacturing that were being established in private premises. 25 Nixon, a confidant of then prime-minister Robert Menzies, was appointed to chair the panel made up of four other senior accountants 26 all well versed in the field of cost accounting. 27 Under his chairmanship, the panel produced five reports and a Costing Compendium, 28 which was used in all munitions-manufacturing facilities for the remaining years of the war. The Compendium was euphemistically referred to as the ‘Yellow Peril’ partially because of the colour of the paper on which it was printed and more particularly because of the hostility that it generated. The panel’s basic brief was, per the medium of cost-plus contracts, to advise on the best way to limit war profiteering without denying private manufacturers a reasonable level of profit with the identification of reimbursable costs as the centre-point. The tenure of the panel lasted nine months, ending in June 1940 with the establishment, within the newly created Ministry of Munitions, of the Directorate of Finance. At this point, Nixon’s role changed dramatically from advisor to government to one engaged directly in the public administration of munitions contracts, effectively regulator of costs. On the recommendation of Essington Lewis, Director-General of Munitions, Nixon was appointed to the post of Finance Director of the Finance Directorate 29 retaining the post for the remaining years of war through a period of unprecedented expansion in munitions manufacturing in both government-owned facilities and private annexes.

While a comprehensive history of the contribution of accountants and the accounting profession to Australia’s war effort has yet to be published, references to Nixon’s leadership of the Finance Directorate in three separate volumes of Australia’s official World War 2 history (Butlin, 1955; Butlin and Schedvin, 1977; Mellor, 1958) and one unpublished history of the Ministry of Munitions (Jensen, 1964) indicate that he made an enormous contribution to public life and the national war effort. As one of seven directors supporting Lewis, he was responsible for the design, codification and monitoring of procurement contracts written by the department with private-sector munitions manufacturers who established annexes to their premises to contribute to the war effort. Contracts that were written on a cost-plus basis raised a range of definitional, incentive and measurement problems that ultimately required the adoption of different versions of cost-plus. The Costing Compendium produced by the AAP-SD in 1940 under his chairmanship was adopted enthusiastically by the new Directorate. Contemporaneously, Nixon also issued under his name, and for the benefit of annexe owners, the first version of a 40-page pamphlet titled Financial Assistance to Contractors for the Production of Munitions (Nixon, 1940 at NAA: P2571, 12 C). The booklet, subsequently updated on several occasions, provided a detailed account of the procedures required to establish annexes on private premises. It included an outline of the facilities for the provision of working capital, erection of buildings, supply of plant and machinery together with the stringent government regulations associated with the provision of financial and non-financial government resources. Along with the oversight management of these annexes, Nixon as Finance Director oversaw the financial administration of all munitions-manufacturing activities in government factories.

Under Lewis’s leadership, the Ministry of Munitions was a great success and all indications are that Nixon and his staff handled the costing-related matters with considerable competence. Lewis, the peacetime Chief General Manager of BHP, worked closely with Nixon throughout the war and Nixon’s appointment as joint auditor of BHP in 1946 referred to earlier, should be interpreted not as cronyism, but evidence of Lewis’s high regard for Nixon’s capacities. As with Lewis, Nixon performed his wartime duties at no cost to the Government. In addition to his position as Finance Director, Nixon was also a member of the Board of Business Administration in the Department of Defence Co-ordination in 1940 30 (Commonwealth of Australia, 1940) and a member of the Co-ordination Committee for Aircraft Manufacture in the Department of Aircraft Production in 1941. 31 For his work as Director General, Lewis was made a Companion of Honour in 1943 (Australian Government, 2016c). 32 Nixon had to wait until 1951 for his efforts in Munitions, together with his other work in a lifetime in accounting, to be rewarded with appointment as Knight Bachelor (Australian Government, 2016d).

Company director

Given that he retained his interest in his firm for 43 years until his death in 1955 and that he was senior partner with an extensive involvement in the audit field, the final dimension to Nixon’s life in business is, curiously, his portfolio of directorships in listed companies. Abrahams (2006) observes that Nixon’s corporate involvements at board level occurred at a time when independence and other ethical issues associated with audit clients were not as closely prescribed as they are today. Nixon’s own writings on ethics contain no reference to positions such as these or the potential conflicts they may cause, matters that had not fully crystallised in the corporate, professional or regulatory minds at that time.

Nixon’s son, Noel Nixon (1976), provided a detailed account of his father’s corporate directorships. One was with heavy-engineering concern, Thompson’s Engineering and Pipe Ltd of Castlemaine. First appointed to the board in 1925, he was chairman during 1931–1955. In addition, he was a director and chairman (and his firm was the auditor) of flour-miller Noske Ltd from 1931 to 1955 and chairman of Moulded Products Australasia (later Nylex Ltd) from 1936 until 1955. All these offices ceased with his death in 1955. Service on the boards of Thompsons’s Engineering and Noske came at the behest of the then National Bank of Australasia (now National Australia Bank) as the bank’s nominee following his involvement in rescuing these companies from serious financial trouble.

Drug House of Australia Ltd (DHA) is another former Australian company that benefitted from Nixon’s involvement. He was instrumental in the creation and listing, in 1930, of the entity that resulted from a merger of seven pharmaceutical manufacturing and distribution companies located in various Australian capital cities. His role was critical in the structuring of the new enterprise as it involved complex work on the valuation bases for the shares that were to be allocated to each of the different parties (Grimwade, 1974: 27; Nixon, 1976). Interestingly, this work was done while serving as the company’s auditor (Grimwade, 1974: 28). DHA subsequently had a long life as a listed public company before succumbing to severe financial pressure in 1974 following takeover in 1970 by British investment bank, Slater Walker.

Private individual

While the formal record of Nixon’s contributions and achievements is impressive, it still raises the questions of what sort of man he was in relation to his personal qualities, attitudes, habits and beliefs. Castles (2000) wrote only that he was ‘shy and reserved in manner’. Nixon’s 1950 Who’s Who entry is a little more forthcoming, stating that his recreations were ‘motoring and golf’ (Alexander, 1950: 533). The sometime registrar of the ICAA, Stan Walton, recorded that he had the ‘misfortune to lack a sense of humour’, and that he had a ‘saturnine countenance giving an impression of impending doom’ (Graham, 1978: 117). His high principles and unbending manner were demonstrated by his actions on the General Council of the ICAA and his vetoing in mid-1939 of members of the IAA serving on a government advisory panel. His academic subordinate, Alec Fitzgerald, would later recount how at the first lecture Fitzgerald gave at the university in 1925, Nixon ‘ostentatiously sat in the front row observing, but also perusing business papers which he occasionally tore up to Fitzgerald’s intense irritation’ (Burrows, 2006: 22).

While the recollections of Nixon’s son, Noel Nixon (1976) and grandsons, Ted Nixon (2013, personal communication (letter Nixon to Burrows), 15 November 2013) and Chris Nixon (2013, personal communication (letter Nixon to Burrows), 17 November 2013) mostly confirm this picture of a humourless workaholic, there are some points of difference. Noel Nixon described his father as a shy modest man, which was the reason for his quietness and reticence. He found it difficult to make intimate friends: there was an air of reserve about him that was sometimes mistaken for aloofness. I think he might have wished he could mix more easily with people and in his younger days he may have: he reached the rank of Major in the Militia and was Master of his Masonic Lodge, but by nature he was self-contained and even his hobbies – cabinet making, photography and reading – were solitary ones. (Nixon, 1976: 4)

Chris Nixon’s (2013) impression is that his grandfather’s ‘work was his life’ and with his directorships, ‘Sunday morning meetings were the norm’. Similarly, Ted Nixon (2013) recalls that on family visits, his grandfather ‘was always to be found in his inner sanctum’. Chris Nixon’s (2013) recollection of family Christmases was that his grandfather ‘would sit in his chair, with numerous unopened presents, clearly not interested either in the present or what the giver thought’.

Perhaps surprisingly for such an establishment figure, within the setting of his family, Nixon was something of an aggressive atheist. Ted Nixon (2013) remembers his own father (Noel Nixon) reporting that Sir Edwin ‘scorned the piety of his [wife] … and muttered darkly as she slunk off to church’. Curiously, Edwin V. Nixon & Partners was well known within the Melbourne business establishment as a ‘Presbyterian’ firm (Abrahams, 2006: 67). Religious and other ‘favouritisms’ were a matter of course in many business of the day – although under-researched – and Nixon’s known attitude to religion, particularly that practised by his wife, stands in contrast to the approach adopted by and within his firm.

While Nixon may not have been the life of the party, his lack of charm was no impediment to the importance of his networking which may reflect positive qualities identified by his son, Noel Nixon (1976), such as his patience and methodical approach when dealing with problems and his ability to quickly get to the heart of any problem, which impressed those with whom he worked. Despite Alec Fitzgerald’s irritation with Nixon’s conduct in the lecture theatre and their differences in temperament and professional orientations, the pair’s collaborations in relation to accounting education, publications and congress participation were enormously beneficial to accounting practitioners and students. Fittingly, Nixon’s firm’s telegraphic address remained ‘Methodical’ for the whole of his career and beyond.

Discussion and conclusion

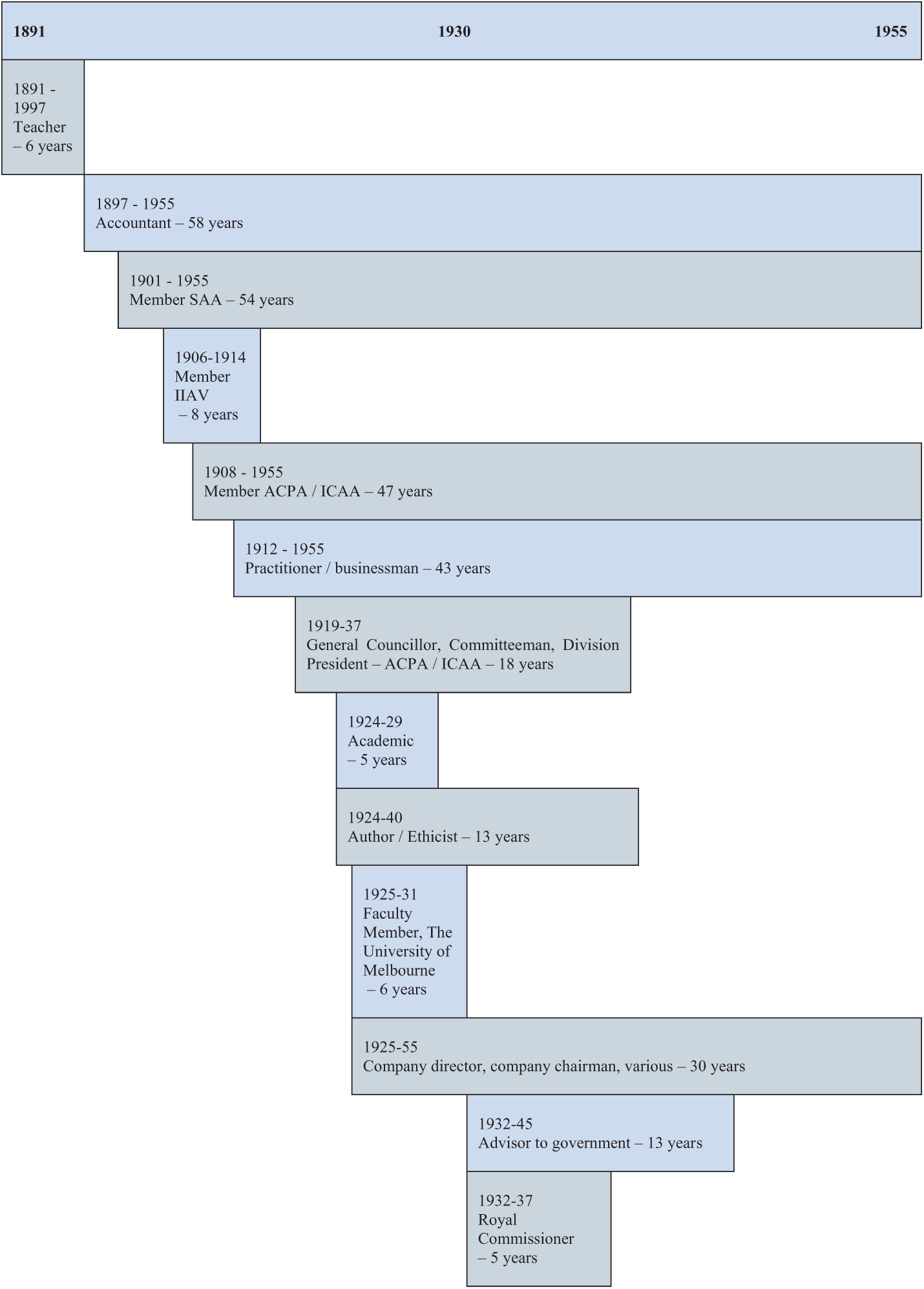

In his history of EY Australia, Abrahams (2006: 45) describes Edwin Nixon as a ‘colossus of the accounting profession’. Ordinarily, such a statement may be interpreted as hyperbole or hagiographic, but in Nixon’s case, there seems to be little if any exaggeration. He was present and, more importantly, active during many of the seminal moments in the emergence of the profession in Australia. He was not merely an observer of these events but a participant engaged in the coming of age of the accounting profession in Australia. Among his approximate contemporaries, he is arguably only matched by Alec Fitzgerald for the comprehensive nature, scope and impact of his contributions. A visual representation of the complexity of his working life illustrated in Figure 1 below reveals the complexity of that working life.

Timeline of the working life of Edwin Van-der-Vord Nixon.

His decision to leave the Queensland teaching service and navigate the challenges of professional examinations and an accountant’s clerkship and the unexpected denial of a partnership were the catalysts for his career-defining decision in 1912 to establish the eponymous firm that eventually became a top-tier presence in the Australian accounting market-place. At the time of his death, Edwin V. Nixon & Partners’ prestigious client list meant it was ideally positioned for the internationalisation of accounting practice that began in the late 1950s (Hanlon, 1994). Related to accounting practice and his standing in the business community were the substantial directorships he held in major public companies, in at least two cases resulting from successfully rescuing them from financial distress.

Throughout his busy practising life Nixon was always ready to serve the profession. His election in 1919 to the General Council of the ACPA was to be the genesis of a long and distinguished period of official service to the ACPA and then ICAA as General Councillor, Division Chairman and committeeman, positioning him as one of the shepherds in the ACPA’s transformation from the old corporation to the new, chartered body. While his role in the fractious Sydney-Melbourne divide over the absence of Bylaws to the ICAA’s Royal Charter can be depicted as nit-picking, divisive and uncompromising, the outcome – the issue in 1935 of a Supplemental Charter – was a vindication of his principled stand. In recognition of an extraordinary period of service, General Council of the ICAA honoured him in 1937 with ‘a Vote of Appreciation as a General Councillor’ (ICAA General Council Minutes #1972, 19 May 1937).

It is as an educator that Nixon’s progressive and traditional traits are most clearly revealed. As faculty member and lecturer, he was an instrumental figure in the development of accounting education at the University of Melbourne. His reputation as one of Melbourne’s leading practitioners undoubtedly helped establish the credibility of the new Bachelor of Commerce qualification and the status of accounting as a specialisation within the degree. As an inaugural member of the Examinations Committee of the ICAA in 1929, he played a leading role in designing the syllabi required for qualification. As an author, sometimes in collaboration with Fitzgerald, he was an early contributor in the era of normative research and surprisingly prolific given the scope of his other activities. His seminal series of articles on professional ethics led to the ICAA promulgating the first codified set of rules in this area by a professional body in Australia and he can be rightly credited with stimulating the debate on professional ethical conduct and placing it as an enduring element of the agenda of all accounting bodies in Australia.

The staging of the International Congress of Accountants in Melbourne in 1936, at which he was both organiser and presenter, demonstrated further Nixon’s commitment to his chosen profession. Linn’s (1996: 106) verdict six decades later of the impact of the Congress, reflecting contemporary newspaper commentary, was that it ‘was a watershed for Australian accounting and in some ways marked the genesis of the modern era for the profession’.

There is perhaps no better indication of the reputation that he had acquired by the early 1930s than the extent to which his expertise was tapped by the Commonwealth and State governments, particularly his appointments to Royal Commissions into Australia’s taxation and financial systems. The legacy of both Commissions persists to this day in the taxation and banking systems. At a time when Australia was engaged in a major world conflict, he volunteered his energies and abilities in ways that significantly benefitted the war effort. Ultimately as Director of Finance in the Ministry of Munitions, but without monetary reward from government, he worked tirelessly to ensure that the financial relationship between government and private munitions contractors was equitable and that the potential for war-profiteering was minimised. In effect, he became the nation’s wartime costing supremo.

Given the achievements made consistently throughout his long career, it is not surprising that he was possessed of a range of personal characteristics and traits that enabled him to achieve so much. As a stickler for procedure, he maintained a proper personal decorum and had similar expectations of others. In many respects, he was a ‘meticulous professional’ (Picard et al., 2014: 73). While his severe and inflexible persona in some respects reflects the unfortunate stereotypical portrayal of accountants in film and television (Evans and Fraser, 2012; Miley and Read, 2012; Smith and Jacobs, 2011; Willmott, 1986) his work ethic, discipline and application were traits possibly shared with eminent contemporaries in other professions and activities.

Other aspects of Nixon’s life, contributions and character suggest opportunities for further research. One obvious area warranting fuller coverage is not only his wartime work in the Ministry of Munitions as Director of Finance but also the administrative and advisory contributions of other individual accountants, and the profession more generally to the World War 2 effort. Similar opportunities exist in relation to World War 1 and for accountants and the accounting professions in other nations in times of war. In addition, the field of biography is, as observed by Carnegie and Potter (2000), still wide open in the Australian context and beyond. Australian contemporaries of Nixon such as A.D. Lyell, Thomas Brentnall, Sir George Mason-Allard, F.N. Yarwood and T.D. Hadley, among others, whose contributions are similarly multi-dimensional, well deserve biographical enquiry. Significant individuals in the second half of the twentieth-century are similarly worthy of biographical representation in the literature including recent practitioner inductees into the AAHF.

Edwin Nixon was a man of serious ability, unbounding ambition and strong sense of duty who was fortunate, though the quirk of history, for his long period of endeavour to coincide with an extended period of unparalleled progression and advancement in his chosen profession of accounting. What sets him apart from most of his contemporaries is not only the length of service, but the breadth and depth of the contribution made. When his multi-faceted working life is observed against the ever-changing political and economic conditions and emerging national identity, he is well placed within the pantheon of eminent twentieth-century Australian accountants.

Footnotes

Appendix 1

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.