Abstract

During the past few years, scholars have investigated accounting practices from different perspectives and in different contexts; however, the topics of accounting and fraud-corruption appear to be underresearched areas in accounting history literature. This article examines the case of Galliera Hospital of Genoa, established as Opera Pia De Ferrari Brignole Sale in 1877 by the Duchess Maria Brignole Sale. Currently, the Galliera Hospital is an important and specialised Italian hospital with 450 beds and almost 2,000 employees. Using the lens of Foucault’s governmentality and discipline power framework, this article explores how unforeseen events and misconduct can deeply change governance and control mechanisms, implying the adoption of empowered accounting practices. Thus, this article shows that accounting practices, when perceived as a real technology of government, allow the exercise of power. The study offers a relevant contribution to the extant accounting history literature by examining how accounting can be used as an instrument of power in the presence of misconduct.

Introduction

This study aims to analyse the relationship between accounting and power within the system of accounting practices and governance mechanisms implemented in the Italian Galliera Hospital in Genoa at the end of the nineteenth century.

According to Hopwood (1983), accounting has the power to shape and influence organisational life. Consequently, significant attention must be paid by scholars to study the possible links between accounting and power relationships within different organisations (Riccaboni et al., 2006). Following this direction, this article aims to analyse, through the lens of the Foucault’s governmentality and discipline power framework (Foucault, 1979, 1988, 1990), the accounting and power dynamics that characterised the first phase of the life of Galliera Hospital.

Foucauldian accounting theory outlines a precise focus on government technology, conceiving accounting as a control mechanism that is instrumental to the exercise of power. Accounting, understood as technology, is based on the assumption that it can generate behaviours that ‘produce certain desired effects’ (Miller and Rose, 1990: 52). As a result, accounting is widely recognised as an instrument of power and domination, among other ‘technologies of governance’ (Rose and Miller, 1992: 183).

This analysis is therefore positioned in the context of studies conducted by Foucault in the late 1980s, when the concept of power is not discarded but becomes the object of a radical theoretical shift (Lemke, 2002). Foucault adjusts the findings of his earlier studies and investigates subjectivity by emphasising aspects of discipline. In these years, Foucault uses the notion of government to investigate the relations between technologies of the self and technologies of domination (Lemke, 2002). Many studies conceive accounting as a government technology (Carnegie, 2014; Dean, 1999; Napier, 2006; Sargiacomo and Gomes, 2011), highlighting the use of accounting systems as a means of intervention in social life (Rose, 1999). Furthermore, their role as instruments of power allows them to exercise control from a distance on communities or institutions (Maran et al., 2016).

Starting from these premises, this work, adopting an etiological perspective, contributes to the literature by examining accounting, social order and control mechanisms (Ezzamel, 2012) in nineteenth-century Italy, highlighting how an unforeseen and fraudulent event significantly changed the exercising of power as adopting accounting practices becomes perceived as a real technology of government. Although recently it has seen an increase in popularity (Bailey et al., 2001; Greve et al., 2010; Liu, 2016; Miller, 2006), in the extant accounting history literature, the topic of accounting and fraud-corruption appears to be an underresearched area (Walker, 2005).

Scholars agree that fraudulent events can be considered as social constructions (Cooper et al., 2013; Greve et al., 2010). Since these differ temporally and geographically, a historical approach based on case studies seems to be useful to further investigate this topic (Van Driel, 2019).

This article contributes to the accounting history literature by analysing a thought-provoking case of misconduct by adopting a historical perspective and opening the debate on an intriguing but still neglected topic. The study shows how the consequences of such misconduct were the introduction of a systematic system of accounting and control as a form of power and knowledge (Foucault, 1980). Accounting and control systems act as real tools of technologies of power (Rose and Miller, 1992) which, in turn, modify governance (Foucault, 1979). Consequently, misconduct can be effectively analysed through the lens of Foucault’s framework on governmentality to systematically examine the misconduct and its consequences.

Because corruption is difficult to study (Neu et al., 2013), very little is known about corrupt processes in different contexts and historical periods. Even less studied is the role of accounting in these processes (Cooper et al., 2013). The research in this article is inspired by a major fraud suffered by the Duchess of Galliera at the end of the nineteenth century. This incident happened while the Duchess was carrying out her most significant philanthropic project: the construction of the Galliera Hospital in Genoa.

Fraud can be considered as a social construction (Greve et al., 2010) because of its implications for society. The effects of frauds can be circumscribed to a single organisation (Hilt, 2009) or extended to include entire states (Hansen, 2012). The literature agrees that what is generically labelled as fraud or scandal, in reality, includes even very heterogeneous phenomena. Thus, bringing focus to a singular case study in historical perspective can be extremely useful to investigate these further (Cooper et al., 2013).

This article proceeds as follows: the first section describes the theoretical background, then we briefly outline the methodology used in our study, followed by the presentation and discussion of the case study.

Theoretical background

According to Miller and Rose (2008) and Rose and Miller (1992), the problematics of government can be examined by looking at different perspectives and considering multiple elements. Their investigation of governmental technologies sheds light on ‘the complex of mundane programmes, calculations, techniques, apparatuses, documents, and procedures through which authorities seek to embody and give effect to governmental ambitions’ (Rose and Miller, 1992: 176). This perspective is useful to better understand power relations by analysing the links between the actions of individuals, groups and organisations and the aspirations of authorities. Foucault (1980) argues that ‘power relations cannot be established, consolidated or implemented without the production, accumulation, circulation and functioning of discourse’ (p. 93). Thus, it is necessary that this discourse is subsequently translated into physical practice in any place (Quattrone and Hopper, 2005).

Following Foucault’s (1988) approach, accounting is used in the social context as a disciplinary and self-governing instrument that can preserve or change governance The extant literature widely recognises the importance of Foucault’s governmentality framework in the study of accounting practices (Armstrong, 1994; Bigoni and Funnell, 2015; Hoskin, 1994; Hoskin and Macve, 1986; McKinlay and Pezet, 2010; Miller, 1990; Sargiacomo, 2009; Stewart, 1992). Power relations must be analysed in the context in which they occur by considering a series of subjective determinations, such as functions, subjects, institutions and actions. In other words, accounting becomes an instrument of power that can influence and guide the conduct of individuals in organisations as well as in everyday life (Hopwood and Miller, 1994).

Foucault (1980: 52) argues that power cannot be exercised without knowledge, just as it is impossible for knowledge not to engender power. Foucault presents a framework where the notion of power is connected to:

the relationship between subjects as they act upon each other. The power-knowledge connection can be usefully employed to determine how mechanisms of power affect everyday lives. Power is not something that is acquired, seized or shared, something one holds on to or allows to slip away (p. 94).

Consequently, power is related not to a specific organisation but to the practices, techniques and procedures adopted. The impact of accounting on people’s conduct transcends the organisational confines within which accounting systems function, favouring disciplinary (supervision of the activities of the subordinate by the governing party) and self-governing actions (the subordinate defines its own conduct in the context of the degree of freedom granted by the accounting system in place) (Miller, 2001). As shown in this article, the subjective element that underlines the power expressed by the Duchess of Galliera ‘is foremost about guidance, that is, governing the forms of self-government, structuring and shaping the field of possible action of subjects’ (Lemke, 2002: 51). Accounting becomes the ‘technology’, or the ‘tool’, through which the Duchess exercises power.

This view reinforces the notion that it is appropriate to consider accounting not only as a technical practice that is applied to reveal pre-existing aspects of reality or particular truths about an organisation (Gowler and Legge, 1983; Hopwood, 2000; Miller, 1994; Potter, 2005), but also as a real technology to connect power and knowledge.

Foucault (1980) emphasises the spatial dimension of the power-knowledge relations arguing that: ‘a whole history remains to be written of spaces – which would be at the same time the history of powers [. . .] from the great strategies of geopolitics to the little tactics of the habitat’ (p. 149).

Accounting has several attributes relevant to the construction of order (Ezzamel, 2012). As Bentham (1791) observed, it is by setting barriers that actions and events can be open to wider observation and consequently to control. In the same way, accounting practices can be understood as a tool, a technology that makes it possible to highlight what the eyes cannot see. Definitively, accounting plays a powerful role by influencing perceptions and actions in organisations (Hopwood, 1988) and by serving as a vehicle for the transformation of the wider organisation (Hopwood, 1987). In such a perspective, accounting becomes a powerful tool to prevent fraud and misconduct by reducing the chances of their occurrence.

Here, misconduct is understood as a harmful or morally questionable behaviour that occurs in organisations where people are confronted with high temptations and where organisational control is poor (Greve et al., 2010). Misconducts are malpractice, a kind of fraud that involves the violation of trust (White, 2003) whose causes stem from a divergence in epistemological, ontological and moral beliefs (Rose and Miller, 1992). They can be defined as the abuse of a position for personal gain, constituting for organisations a real cancer, a disease, a scourge (Neu et al., 2013). Misconducts are based on critical issues in social studies such as compliance, punishment and social order (Coleman, 1990). In organisations, misconducts are closely linked to a lack of adequate procedures, excessive discretion and freedom and insufficient control mechanisms (Everett et al., 2007; Hamir, 1999; Harris and Bromiley, 2007; Krishnan, 2005). Accounting technologies (Everett et al., 2007; Neu et al., 2013; Sargiacomo et al., 2015) have the potential to build disciplined and ethical subjects (Hoskin and Macve, 1986; Miller and O’Leary, 1987) by organising the practices of conduct, to induce certain behaviours and outcomes (Foucault, 1990). Subjects are ‘governed’ through a set of knowledge, practices and tactics (Foucault, 1990), including accounting (Miller and Rose, 1990). As stated by Foucault (1982):

power applies itself to immediate everyday life which categorises the individual, marks him by his own individuality, attaches him to his own identity, imposes a law of truth on him which he must recognize and which others have to recognise in him . It is the form of power which makes individuals subjects. (p. 212)

There are two meanings of the word ’subject’. The first one refers to someone subjected to someone else by control and dependence; the second is tied to an individual’s own identity connoted by a conscience or self-knowledge. Both meanings suggest a form of power which subjugates and makes an individual ‘subject to’ (Foucault, 1982: 781).

The power-knowledge relationship allows preventing and detecting of misconduct by acting on the subjects, raising barriers to counteract opportunistic behaviour out of self-interest. Foucault (1977) considers the control mechanisms as an examination that ‘combines the techniques of an observing hierarchy and those of a normalizing judgement [. . .] that makes it possible to qualify, to classify and to punish’ (p. 184). Following Foucault, accounting practices create an environment to produce self-disciplined and ethical subjectivity (Neu et al., 2013). Foucault (1979) states that in discipline, ‘punishment is only one element of a double system: gratification-punishment’ operating ‘in the process of training and correction’ (p. 180).

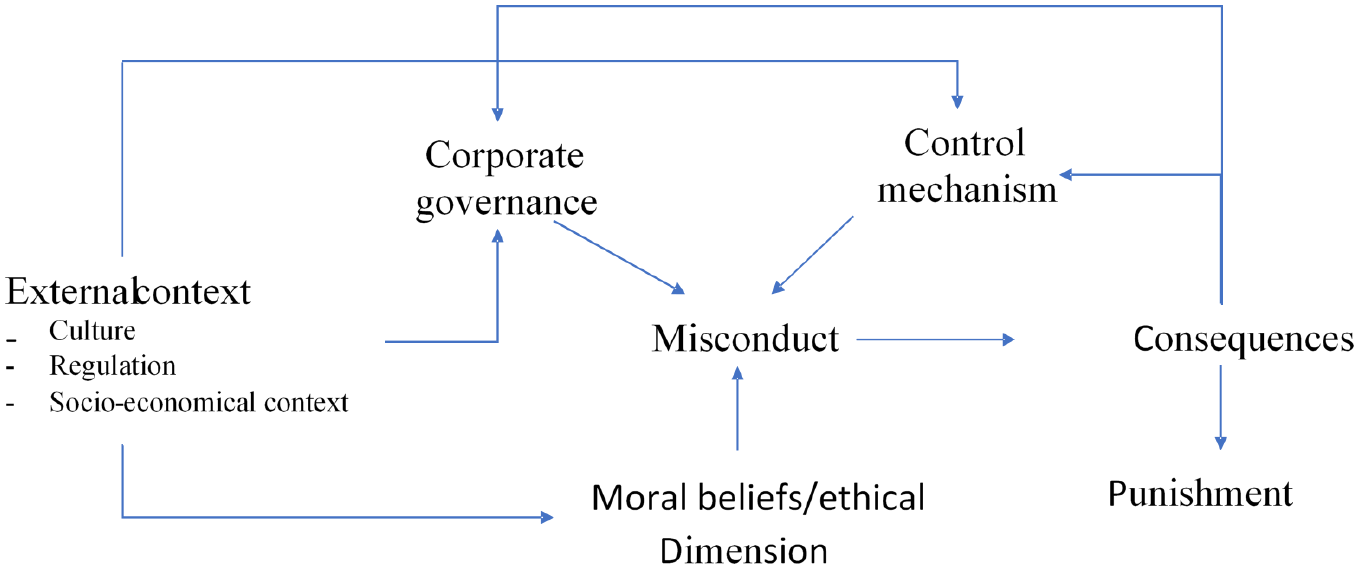

In the literature, misconducts have not been systematically connected to their determinants, consequences and the reactions to them (Cooper et al., 2013). Providing a new arrangement of the previous studies, we have formalised the conceptual framework proposed in Figure 1 and used this in the development of our research.

The conceptual framework.

The conceptual framework draws from Van Driel (2019), reinterpreted in the light of Foucault’s theories. The incentives and opportunities to commit misconducts are determined by the joint action of the external context with the specific conduct of the individual (Van Driel, 2019). The external context is conceived in its cultural connotations, in its socio-economic characteristics and in the regulatory mechanisms operating in a certain historical period. These elements influence corporate governance and control mechanisms, which, in turn, may represent more fertile or less fertile grounds for misconducts. Once the misconduct has occurred, it generates consequences that operate both at an individual level, the punishment connected to the behaviour (Foucault, 1979), and at an organisational level, influencing control and governance mechanisms.

Control mechanisms must be coupled with defined and effective penalties, to prevent and deter future possible corrupt behaviours (Thornton and Moore, 1993).

Research method

The history of Galliera Hospital has been reconstructed from archival sources. This study was conducted using material available at the extensive historic archive of the hospital, which preserves almost all the accounting documentation and historical records of the hospital since before its foundation. The primary sources are original documents from the Historical Archival of Galliera Hospital (GHA) and this study uses both primary and secondary sources appropriately integrated to give comprehensiveness to the historical approach.

The archive contains all the accounting traces, the company’s deeds, and substantial correspondence concerning documentation of the foundation and subsequent management activity. It collects all provisional documents, accounting statements and moral statements from its foundation to the present day in chronological order. The historical archive preserves the extensive correspondence that took place between the Duchess of Galliera and the governing bodies of the Opera Pia. These were fundamental to reconstructing the power relations and the modalities connected to its exercise by inserting the research into the furrow of the narrative accounting history (Carmona et al., 2002). The material at GHA constitutes the main primary source for this article, including the role of the Duchess in the administration of the Opera. The research uses the vast technical accounting material at GHA to triangulate the practices described and understand how misconduct has changed the technology of exercising power (Maran et al., 2016; Rose and Miller, 1992).

The original documents consulted are as follows:

Accounting entries, particularly those of payment and collection orders relating to variations in the budgetary chapters;

Other accounting documents: board reports and financial reports from 1888 to 1892;

the Moral Report of 1888

Letters and other writings by the Duchess of Galliera from the period between 1877 and 1888;

Statutes and regulations of the Opera Pia.

The approach adopted in this article is similar to that which accounting scholars label ‘contextual’ (Hopwood, 1983, 1987 and Napier, 1989). Bhimani (1993) believes that in contextual studies, ‘accounting is a social practice influenced by a wide range of forces’ (p. 3).

There is now a consolidated and comprehensive body of literature on accounting changes in context (Burcheil et al., 1985; Hopwood, 1987; Loft, 1986) and on the decision-making processes that can provide a more complete understanding of the changes (Bhimani, 1993; Burns, 2000; Hopwood, 1983; Ryan, 1999; Scott et al., 2003). Recognition of the change in the function of accounting is provided by Carnegie and Napier (1996), who maintain that ‘accounting must be understood in the context in which it operates, as a local phenomenon in time and space’ (p. 7).

In our research, we analyse misconduct and the role of accounting practice at the organisational level. We are especially interested in examining how accounting can be used as an instrument of power in the presence of misconduct. We focus on the accounting dynamics that characterise the first phase of the life of the Galliera Hospital through the lens of ‘accounting and power’, a paradigm based on the French philosopher, Foucault’s concepts of governmentality and discipline. This allows us to deepen the understanding of the genesis of misconduct in the Galleria Hospital and the countermeasures (control mechanisms) carried out by the Duchess of Galliera. Our analysis takes place in late-nineteenth-century Italy.

Accounting as a technology of power: the case of Galliera Hospital

The history of the hospital and the Duchess

The Ospedali Galliera (Galliera Hospital) inaugurated its activities in March 1888. It had been established a little over a decade earlier on 22 December 1877, when, before Notary Giacomo Barsotto, the Duchess Maria Brignole Sale founded the Opera Pia De Ferrari Brignole Sale in the City of Genoa.

The original approach involved the establishment of three distinct hospitals each with a specific vocation:

The St Andrew Hospital for the treatment of acute pathologies with 300 beds (the current Ospedali Galliera): a generalist hospital for acute illnesses, aimed at helping the poor who lived in municipalities belonging to the ancient Republic of Genoa at the time of its annexation to the French Empire;

The St Philip Hospital for the care of infirm children with 36 beds;

The St Raphael Hospital for the care of poor people affected by chronic diseases with 150 beds.

The life of the Duchess was strongly characterised by painful experiences. Her first daughter, Livia, died in 1829, only four months after her birth. Her second son, Andrea, on whom the family had placed its hopes for the continuation of the dynasty, died at the age of 17 in Paris, a city beloved by the Duchess that she had chosen as the place where she wanted her son to reside and receive his education. In 1850, at almost 40 years of age, she gave birth to her third child: Filippo. He was the son destined to follow in the footsteps of his brother, whom he never knew but who loomed large as a constant figure in his life and that of his two desperate parents.

However, it soon became evident that Filippo’s disposition was far removed from his parents’ expectations. He remained indifferent to their dynastic project and even made choices that directly undermined it. He renounced his Italian citizenship, thus immediately forfeiting his father’s title. After his mother’s death, he even renounced his family name.

Currently, the Galliera Hospital is a nationally important and highly specialised hospital that has 450 beds and employs almost 2,000 people. As this article will argue, the fact that it is currently a hospital recognised and appreciated throughout the Italian healthcare system is due to the determination of the Duchess of Galliera, who, overcoming undoubted adversity, managed to achieve her greatest Opera.

Ferrari’s misconduct

The events that affected the hospital’s establishment were uneven and not without obstacles. As the Duchess herself would say, the moment of the inauguration represented great satisfaction for her and at the same time, great relief. In the handwritten letter from the GHA archives that she wrote for the inauguration of the hospital in 1888, she acknowledged that ‘from this moment on – the opening of the hospitals is a fact accomplished. It is no longer a dream’.

However, during the construction phase, this reality seemed impossible. Fewer than five years after its establishment, the great project seemed destined for inexorable disaster, quashing the dreams of the Genoese people for the new hospital.

At the end of 1882, an event as ruinous as it was unforeseen occurred. Angelo Ferrari, the Duchess’ trusted advisor, had stolen the entire sum reserved by the Opera Pia for the construction of the hospital. It was a considerable sum, 13 million lire at the time (Salidu, 2009). The Duchess had set aside a net return of 500,000 lire per year for the annual current expenses by allocating public debt securities and the proceeds of some property investments.

It was known that Angelo Ferrari enjoyed the complete trust of the Duchess. He had the task of administering a large part of her estate, dealing with assets intended for charitable and philanthropic activities (Salidu, 2018). He appears, in fact, as a witness to many acts performed by the Duchess even though he never assumed an official role in carrying out any of her activities. At the time it was common to have trustees for carrying out practices or conducting affairs and the figure of the ‘general agent’ (assumed by Ferrari) was a widespread practice among the noble and upper middle class of the Genoese community. The Duchess had a strong connection with France and Paris in particular. She spent long periods of time in Paris and decided to have her children study in France. She was also the owner of numerous properties and residences and together with her husband led many entrepreneurial activities in France (Bitossi, 1994). It was, therefore, a necessity for her to be supported by people she trusted in the administration of her many affairs.

The Duchess’ dismay at the misconduct of her agent Angelo Ferrari was so great that she had a plaque erected at the entrance to the hospital to commemorate the event. The plaque functioned as a reminder of the outrageous betrayal, but above all, it was a form of moral punishment for Ferrari and a warning for her present and future collaborators. Ferrari’s name would have been associated with behaviour of misconduct by all Genoese citizens and furthermore underlined feelings of doubt that the hospital would ever be completed (Salidu, 2018). From a letter sent by Andrea Pierano (the Duchess’s lawyer), we know that she only removed the plaque at the time of the opening of the hospitals (GHA 1.1; Folder (F) 18A; box 1).

To expose Ferrari to public blame, the Duchess published an article in the local press, which announced that on 20 March 1883 she signed a deed by the notary Ghersi, in which, to her great regret, she declared the imminent suspension of work on the hospital complexes. She communicates this postponement as an indefinite one because of the vast disruption to her assets as a result of her agent Angelo Ferrari’s disloyalty.

The situation seemed disastrous but due to the Duchess’s determination, in just a few years, she once again raised the necessary capital to build the hospitals. On 31 March 1885, at the hands of the Notary Gherzi in Genoa, the deed of foundation of the Opera was deposited. It would receive definitive approval with the emanation of the Royal Decree of 18 February 1886. This took place in March 1888. The Hospitals of St Andrew and St Philip inaugurated their healthcare activities. The Duchess lived just long enough to see the first developments of her impressive project and on 9 December of the same year, she died at her home in Paris.

The fraud suffered by the Duchess radically changed the commitment that she received for the realisation of her Opera.

Effects on corporate governance and control mechanisms

According to Miller and Rose (1990), governmentality is characterised by a discursive dimension, oriented towards conceptualising and explaining political rationalities, and a technological dimension. The latter, the technology of government, deals with the development of bureaucratic and administrative apparatus (Dean, 1999) and is, therefore, how an apparatus establishes its own rules of operation to achieve a given system of order. The accounting control system is a typical technology of government conceived as a means of intervention in the social context ‘with aspirations for the shaping of conduct in the hope of producing certain desired effects’ (Rose, 1999: 52).

Before the theft, the Duchess had been directly involved in the construction of the hospital complex, and anything related to the operational aspects of the institution. She relied heavily on her ‘trustee’, Angelo Ferrari. The fraud that the Duchess suffered proved essential in changing the way in which power was exercised through another ‘government technology’, the accounting control system. According to Miller and Rose (1990), accounting technologies are techniques ‘of notation, computation, calculations, the procedures of examination and assessment, [and] the invention of devices such as surveys and presentational forms such as tables . . .’ (p. 8). The Duchess decided to use accounting as a tool to induce certain behaviours and, particularly, to prevent misconduct by emphasising an element of control that had been substantially absent until then.

The central element leading to the moment of change in the government following the misconduct is in a letter from the Duchess addressed to Archbishop Magnasco on 15 October 1883. She renounces direct control of the construction of the hospitals and asks the archbishop to proceed with the formation of the board of directors (GHA 2.1- F. 2b–Box 1).

Before the theft the statute of Article 9 of the deed founding the Opera Pia De Ferrari Brignole Sale stated that the superintendence of the construction was to be in the hands of the Duchess and that only once the structures had been completed would they be transferred to the Opera and their management entrusted to the board of directors. The same statute in Art. 17 established that as long as the Duchess was alive, the Opera Pia

was not subject to any interference of governmental authority, nor to the protection of the provincial deputation, nor to the obligation of the presentation of its financial statement and approval of its accounts; intending to preserve intact and whole, during her life, the quality and power of the Founder and maintain the most absolute freedom of action, to change and modify to her consent [. . .] the bases and conditions of the Opera Pia. (GHA, Deed of foundation of the Opera, 1978, F. 1, Box 3)

At the time of the foundation of the Opera the Duchess, therefore, considered the accounting control system an obstacle to her exercise of power and reaffirmed in the statute the centrality of her role and the absolute prerogative to modify, according to her own will, the conditions of operation of the institution. Because of the theft, she decided to resign from her role and immediately set up the board of directors, believing that a collegiate and autonomous body could better perform this onerous task.

The letter is reproduced in its entirety in Volume 1 of the Register of Minutes of the Board of Directors Resolutions. The Chairman of the board read it aloud to the other members on the day the board took office. The letter communicates the Duchess’s disappointment and disheartened feelings about the fraud but also the new governmentality that she expresses in placing the accounting control system at the centre of the mode of exercise of power:

It was not so far, and it would not even be the case today of this convocation, because according to Article 9 of this act (the Statute), the Council could not interfere in the construction of hospitals while I am still alive. They are not yet complete and cannot be unfortunate if not after a long time. The enormous decrease in my assets suffered by the infidelity of my agent, Angelo Ferrari, forced me, last December, to suspend the completion, and as far as possible, also the construction work, in order to have time to put my assets in a position to bear the costs of the Foundation. [. . .] Today I have thought that it would be better to provide perhaps for the interest of the Opera Pia if [. . .] the completion and opening of the Hospitals were entrusted to the care of the board of directors: and I have therefore decided to resign from the possession and administration of the endowment assets, [. . .] placing the Council from now on in the exercise of all the powers that it would have at the time of my death, for the formation of the multiplication, and for the completion of the construction, and the installation of the hospitals. (GHA, Vol. 1, Minutes collection, 1888)

This letter underlines the need to ‘communicate the fundamental acts of Opera Pia’, reiterates the commitment of the board of directors to ‘take over the management of the assets assigned to it’ and to comply with ‘all the provisions’ laid down by the regulations for the management of the Opera Pia and those deemed necessary to ensure the best feedback regarding the management carried out. Thus, the accounting system becomes the fulcrum for the exercising of power and the central element of knowledge about the activities of the institution as well as an expression of the change in the Duchess’s approach.

The fraud suffered therefore changed the ‘governmentality’ expressed by the Duchess.

The semantic link ‘of governing (governor) and modes of thought (mentalitè)’ expressed by Foucault represents the central element in understanding the ‘technologies of power’ (Lemke, 2002: 50) and the implications of the accounting system as a technical element of the exercise of power. On 18 October 1885, the board of directors was therefore given the task of completing the construction of the hospitals and managing the assets, with an additional task of configuring the accounting control system of the entity, as described in the letter.

The Duchess, while declaring her resignation from the ‘possession and administration of the endowment assets’, would continue to maintain her interest in the institution and to exercise her influence, but with a fundamentally different attitude. There was no further direct exercise of power on her part but rather an ‘indirect’ referent for the remote control of the entity operated through the accounting technology. Along with the board of directors, this became the vector of information for the Duchess. A great deal of evidence testifies to the close correspondence between the Duchess and the members of the board of directors on many aspects of hospital management.

About a year later, in a letter dated 21 April 1887, the Duchess replied to the vice president, Mr Edoardo Pizzorni. In a previous letter, Edoardo Pizzorni had asked the Duchess for clarification on ‘the provisions that she considered appropriate to give on the drafting of internal regulations’. She expressed the opinion that the responsibility of executive power should be concentrated in a few hands ‘to ensure a well-ordered administration’, but at the same time, this requirement should not lead to situations that could result in dominant positions of power. Therefore, the peculiar system of governance of the institution was conceived (GHA, Common Correspondences Found, 1885–1892).

The governance system was based on a combination of representatives of local institutions, people from civil society and the ecclesiastical power. The appointed members of the board of directors consisted of the Archbishop of Genoa, who was entrusted with the higher level superintendence of the Opera, the Prior of the Magistrato della Misericordia (Magistrate of Charity) and a representative from the Municipality of Genoa. The Magistrate of Charity (Office of Charity) is an institution dating back to 1419, established during the Republic of Genoa. The magistrate’s task was to manage the legacies of the important noble families of the Republic to aid and support to the poor. The institution still exists in Genoa, operating as a foundation under private law (Petti Balbi, 2013). The six elective members were, however, appointed by co-optation.

The appointment mechanism (still in force today) is intended to guarantee the replacement of the members without undermining the continuity of governance. The appointment of the elected board members is the responsibility of the board in such a way that the remaining members in office elect a replacement after a member’s term expires or when a member is missing. Each year, one of the six elected board members terminates his or her membership based on seniority in office under a mandate of six years, and the remaining members co-opt a new board member. In this way, the Duchess hoped that the governing body could reconcile the rightful need for continuity of management with that of ensuring a continuous rotation among the members of the board so that no situation of power would be consolidated.

The impacts on accounting

The vastness of the correspondence and the care with which these documents have been stored enables us to reconstruct the entire life of this historic Genoese institution, providing a snapshot of not only the social system of the regional capital but also the entire healthcare system.

The document analysis focuses on documentation that refers to the period between 1877 and 1900. As per the accounting records, the analysis covers the period from 1886, the year of the first report, to 1900. From 1888 to 1900, it is possible to distinguish two sub-periods from an accounting approach. The first can be defined as from the hospital’s origins until 1891, and the second extends from 1892 to beyond the turn of the century.

Italian Law 6972 from 17 July 1890 and the subsequent Administrative Regulation no. 90 of 5 February 1891 introduced the obligation for public charity institutions to disclose the treasurer’s financial records by May that year. These should have been submitted to the prefect for the approval of the Provincial Council alongside the final balance and a report on the moral actions of management of the past year. This was an opportunity for the Genoese Opera to redesign its accounting system. In 1892, in addition to the accounting books already in use, the Till Journal was established. On a sheet with opposing sections, it enabled the income and expenses arising from management operations to be highlighted from month to month.

The two periods share the presence of financial records kept with the single-entry method. However, their documentation approach differs, as, from 1892 onwards, the institution decided to use a highly structured reporting system in which a series of books whose function was to use the balancing mechanism to guarantee the validity of the records, was added to the traditional financial accounting documents.

The accounting system was established in 1886. It consisted of the ‘budget’, understood as a planning document with authoritative functions, while the related accounts were kept by means of consolidating the journal of income and expenses and the ledger of income and expenses by chapter and article. For both the income and expense sections, the forecast financial statements were structured into titles, categories, parts, chapters and articles, thus constituting a framework based on five partition levels with a hierarchical structure. The budget had only one title for both assets and liabilities. The first title was divided into two categories: ‘ordinary income’ and ‘extraordinary income’.

The ordinary income category was divided into three parts and 10 chapters for 1886. The first part contained capital income, and the second contained income derived from the operation of the foundation. This section featured chapters related to rental income, pharmacy products, income from patients who paid per day of hospitalisation and revenues from internal manufacturers. The last part of the first category included random income such as security deposits, advances or refunds in the current account. The second asset category, extraordinary income, was divided into two parts: capital transformations and price of extraordinary forest felling.

The synoptic system was structured into columns that, when read from left to right, featured the description of the type of income or expense (designation) and then the indication of the amount based on the previous year that was envisaged for the current year by chapter and article, the positive or negative difference, the causes of the difference and, in the last column, the variation following approval of the financial statements.

The prospective phase was therefore highly detailed and at the same time, it was able to keep track of factors that impacted allocations, as well as the causes of variations, both in the phase of approval by the board of directors and in the phases following approval of the budget. The text of the designation column also contained references to the annexes and supporting documents related to specific management events.

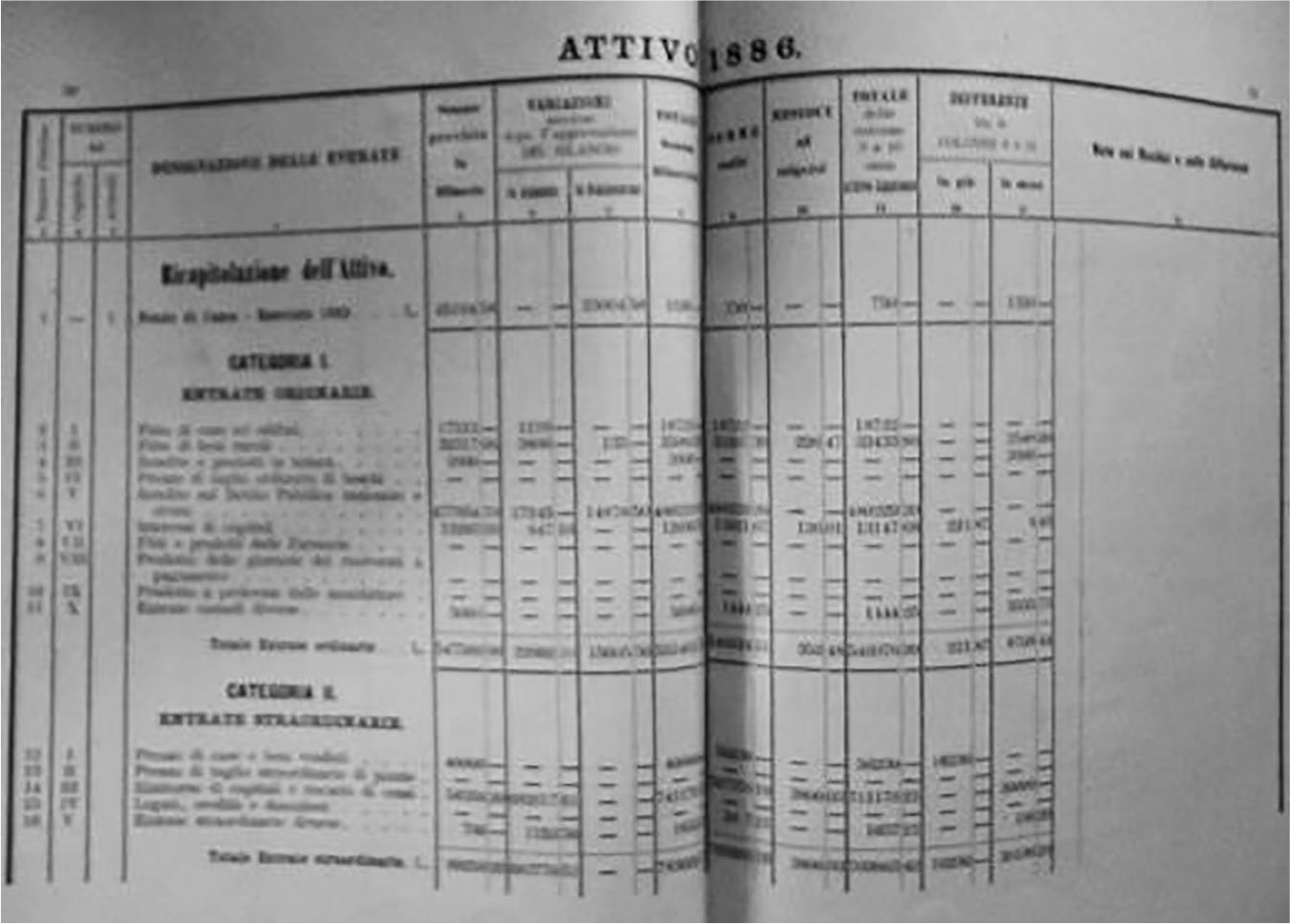

The last part of the accounting system contained the final accounts, which were displayed in the Resoconto Materiale del Tesoriere (The Treasury Final Report). The final report provided initial documentary evidence called ‘recapitulation’ that enabled it to be read at different levels of summarisation. The report taken as a constant reference was the category around which the analysis pivoted, enabling an initial summary of the variables at the article level and a later grouping of the various articles into their respective chapters. Regarding recapitulation, the final report was conceived in full logical continuity with the forecast financial statements (see Figure 2). The sheet in Figure 2 highlights the recapitulation of the assets at the chapter level, but the synoptic structure of the tables remains the same, even for the recapitulation at the article level.

Annual Accounts 1886.

Specifically, the first column recalls the order numbers connected to the forecast financial statements, while the second, in turn, divided into two sections, uses numbering referring to the individual chapter and/or article. The following column shows the designation of the income, as shown in the financial statements. These first columns act as a connection with the forecast document. Columns 6 and 7 show the positive or negative variations, respectively, that occurred following approval of the financial statements, while Column 8 shows the definitive forecast amounts attributed to the year following the various adjustments made. The document continues with evidence of the year-end results. Column 9 reports the sums collected, and Column 10 reports the amount of the ‘residual sums to be recovered’. Column 11 is the sum of the two previous columns and shows the ‘realised assets’, or how much of the relevant income the administration had recorded during the year. Columns 12 and 13 show the positive or negative ‘differences’, respectively, regarding the expected values and the settled allocations. The same synoptic system is also applied to the outgoings section.

The final report was the responsibility of the Treasurer of the Opera Pia, who addressed it to the board of directors (see Figure 3). This report was merged into a larger document containing the board’s ‘Moral Report’ and the Treasurer’s ‘Material Report’. The first moral account was presented in 1888 and refers to the exercises of 1886 and 1887. In its ‘Moral Report’ the board provided a detailed relation of the most important occurrences that characterised the management.

Frontpage Moral Report 1887.

The first ‘Moral Report’, although referring to 1887, also contemplates all the events of management that occurred in 1886. In this way, it provides a precise descriptive representation of all the most significant operating events that occurred in the previous two years and the size of the capital of the Opera. In the document, the vice president of the board and author of the report, Edoardo Pizzorni, expresses the hope that the report ‘will demonstrate that the economic and administrative performance of the Opera Pia has proceeded with the regularity and accuracy required by the importance of the great Foundation established by the munificent Duchess of Galliera’ (Moral Report, 1887).

Discussion

The case of the Genoese hospital can be seen as an embodiment of the more general view of accounting as an instrument of power in the Foucauldian paradigm. In this case, the holder of power (the Duchess) decided to create a hospital establishment to achieve a specific goal: to ensure healthcare and welfare protection for all Genoese citizens. This mission went beyond her personal interest as the power holder. However, her philanthropic action meets a very serious obstacle in the fraud perpetrated by her trustee Angelo Ferrari.

Until this misconduct, the exercise of power by the Duchess was carried out through a fiduciary mandate which was the technology used to remotely control her activities. Immediately after the foundation of her institution, the Duchess expressed her opinion that the creation of an accounting system was completely superfluous and she considered it a hindrance to the construction of the new hospital. After the fraud, the Duchess’ governance changed completely. She set up and convened the board of directors for the first time and acted on the mechanisms for appointing its members. She prefigured a nomination process that provided different periods of time for the terms of office of the members. The option for renewal only applied to some board members, making it possible to avoid the formation of dominant positions. Second, she established the accounting control system, which became the ‘technology’ for the exercising of power, encouraging an accountability of the institution’s directors that goes well beyond what was required by the regulations. No less, she punishes Ferrari by exposing him to public blame. The plaque she had affixed at the entrance to the building brought all Genoese citizens’ attention to the outrage suffered.

Foucault has always recognised that personal conduct can be a defiance of power, an inescapable response to the exercise of power (Lemke, 2002). Such a change operated directly on the individual modalities of the exercise of power and the mentality of the Duchess. That is, there is a link of immediate determination between the act of misconduct and the limitation of the sphere of power.

In this study, we draw on a framework that reinterprets the idea of Van Driel (2019) by incorporating Foucault’s theories. In this conceptual model, the incentives and opportunities to commit misconduct are determined by the joint action of the external context with the specific conduct of the individual. The external context is conceived in its cultural connotations, in its socio-economic characteristics and in the regulatory mechanisms operating in a certain historical period. These elements influence corporate governance and control mechanisms, which in turn may encourage or discourage misconducts.

In our case, the context is represented by the economic well-being of the Genoese nobility, strongly internationalised and glad to leave a tangible sign of their attachment to the city and its citizens. The Genoese entrepreneurial system was growing sustainably, supported by successful commercial activity and an important nucleus of industrial manufacturing. Regulations allowed for the creation of institutions intended to administer large assets for specific social and welfare purposes. These elements are associated with the personal commitment of the Duchess, animated by a deep sensitivity towards social needs and oriented towards an intense philanthropic activity driven by a deep ethical and moral sense.

Following the conceptual framework, once the misconduct occurred, it generated consequences that operate both at an individual level, the punishment connected to the behaviour (Foucault, 1979), and at an organisational level, influencing the control and governance mechanisms. In our case, the individual consequence was the punishment inflicted on Angelo Ferrari, through the affixing of the plaque which, in addition to inflicting a serious shame on the person who carried out the fraud, was also a warning to the population not to commit other such acts. At an organisational level, the case study highlighted consequences on three sides: the corporate governance (through the establishment of a board of directors), the control mechanisms (coupled with defined and effective penalties, to prevent and deter future possible corrupt behaviours) and the accounting, which is the fulcrum of the exercise of power.

Conclusion

This article contributes to the accounting history literature by analysing a case of misconduct and showing, according to Foucault (1980), how the consequences of that misconduct enacted the introduction of a structured system of accounting and control as a form of power and knowledge.

In our case of study, the Duchess decided to change how power was exercised, using the ‘privilege of status’ to guide the development of the institution, but from a distance through the accounting control system. The accounting system played no role within the board of directors; therefore, the exercise of its power derived not from a hierarchical position within the organisation but from the privileges connected to its status that allowed it to orient governance, drafting the regulations and characteristics of the control system. The accounting control system and audit of the Galliera Hospital was conceived as a formal mechanism of continuous verification of the use of resources, but it became a real mechanism for the exercise of the power by the Duchess.

At the same time, the Duchess feared that once she died, there would be a natural distraction from the initial objective among future generations. To counter this or, in Foucauldian terms, to dampen the resistance to power, the accounting and governance mechanisms came into play.

Linking our results to Rose and Miller (1992), accounting and control systems act as real tools of technologies of power by which to modify the governance situation. Consequently, the misconduct of Ferrari is a case study that can be examined using Foucault’s framework on governmentality (Foucault, 1979) to systematically study the misconduct and its consequences. Before the fraud, the Duchess had not yet decided to develop a control system. Her authority and the relationship of trust that she had established with her collaborators were themselves a form of exercising power based on personal legitimacy. After the fraud, the way in which the Duchess exercised her power changed, compelling her to reconfigure certain aspects of it, as demonstrated by the fact that the accounting system plays a fundamental role in the exercise of power.

Therefore, following the work of Miller and Rose (1990) and Napier (2006), we can outline that fraud represents a discontinuity that introduces a change. At the centre of the change there is the introduction of accounting as a new form of government, which, linking to the idea of Preston (2006), is no longer exercised directly but rather remotely through the accounting tool.

Considering this article in terms of the previous literature on accounting and fraud-corruption (Bailey et al., 2001; Greve et al., 2010; Liu, 2016; Miller, 2006), we find that the case of Galliera Hospital is fully in line with Heller’s idea (1996) that Foucault’s theory conceives power as ‘exercised’ by drawing a clear distinction between the pluralist and functionalist conceptions of power. The focus on the accounting dynamics that characterised the first phase of the life of the Galliera Hospital allows us to deepen the genesis of misconduct in and the countermeasures (control mechanisms) carried out by the Duchess of Galliera, through the lens of the ‘accounting and power’ paradigm based on the concepts of governmentality and discipline. Indeed, Foucault argues that ‘power is not an institution, and not a structure; neither is it a certain strength we are endowed with’ (Foucault, 1990: 93). ‘Power is employed and exercised through a net-like organization’ (Foucault, 1980: 98). This net-like organisation consists of ‘the system of differentiations which permits one to act upon the actions of others: differentiations determined by the law or by traditions of status and privileges’ (Foucault, 1980: 98).

The limitation of our work is that we only use ‘corporate’ sources contained in the GHA in this article. Following the seminal work by Rowlinson et al. (2014), our article falls within the literature on ‘corporate history’. This represents the form of organisational history that most closely resembles a stylised conventional narrative history, combining narrative with documentary sources and a periodisation derived from the corporate entity itself.

These limitations also represent the main future direction of the work, since we believe we can intensify the archival research in the search for new documents, outside the GHA (e.g. documents from Genoa’s public and private archives) that further support the main theses presented here.