Abstract

The roles of accountant characters in a coherent genre of entertainment media, and over time, remain surprisingly under-researched. In this study, it is argued that the roles of accountants in society can be interpreted from longitudinal analyses of the roles played by accountant characters in entertainment media narratives depicting fictional worlds. Analysis is provided of narratives in which actantial and thematic roles are played by accountants in 178 US superhero comics’ narrative sequences between 1938 and 2018. The sequences were those in which at least one character is presented as an accountant. The study reveals that accountants have increasingly been portrayed in more positive than negative roles since the beginning of the twenty-first century and have become symbolic superheroes. At the same time, this study also shows that individual accountants do not last long in these narratives, even though they have a positive role. This article shows how one genre of entertainment media has conveyed an improved image of accountants in fictional worlds, to give them progressively a place of importance comparable perhaps to the one that their professional bodies argue they occupy in modern society. Even if some negativity is still attached to the accountant, their image is progressively changing for a better one based on the roles they played because they are accountants.

Introduction

Increasingly, scholars of accounting – especially accounting in society – are using popular culture to aid their research (Jeacle, 2018). This article presents the results of a longitudinal study in which superhero comics are used to better understand the perceived roles of accountants in society. The accounting profession has attempted to craft an image of accountants that would counter negative images (Daly and Schuler, 1998; Jeacle, 2008; Picard et al., 2014). In particular, the “beancounter” image has been a target (Christensen and Rocher, 2020; Friedman and Lyne, 1997, 2001; Jui and Wong, 2013; Professional Accountants in Business Comity, 2008; Small, 2015). However, popular culture offers interesting insights that can look beyond self-interested efforts to craft an image and to see contemporary representations of accountants and changes over time.

Representations are diffused and maintained by language and communication (Maass and Arcuri, 1996; Stangor and Schaller, 1996). Mass media, especially popular media in the “entertainment age,” have helped to define modern society (Sayre and King, 2010). As such, it has provided sources for a growing number of accounting scholars to analyze the representations of accountants in society (Jeacle, 2012, 2018; Jeacle and Carter, 2014; Richardson et al., 2015). Some of the forms of media used have included movies (Beard, 1994; Dimnik and Felton, 2006; Holmes, 2002; Holt, 1994; Smith and Briggs, 1999), literature (Carnegie and Napier, 2010; Coleman, 1936; Crumbley, 1995; Czarniawska, 2008, 2012; Evans and Fraser, 2012; Finnie, 1962; Maltby, 1997; Robert, 1957; Smith, 2017; Stacey, 1958; Walker, 1995), cartoons (Bougen, 1994; Jones and Stanton, 2013), jokes (Miley and Read, 2012), comics (Christensen and Rocher, 2020), or songs (Jacobs and Evans, 2012). These various studies have explored the accountant’s image in society, yet it remains contested.

Extant studies show mixed results on whether the image of the accountant is positive or negative (Czarniawska, 2017; Dimnik and Felton, 2006; Richardson et al., 2015). In this study, we argue that one of the reasons for contrasting results is that most studies rely on a mimetic theory of fictional characters considering them as a human-like entity (Margolin, 2008) with an analysis based on their characterization to define their properties and traits (Jannidis, 2009). Thus, the transformation of the visual and behavioral traits of accountants in entertainment media has been largely studied (Richardson et al., 2015), while few studies focus on the roles that accountants play in the narratives, based on a non-mimetic theory of characters in fiction (Beard, 1994; Czarniawska, 2008, 2012, 2017; Dimnik and Felton, 2006).

This study analyzes the roles played by accountants in entertainment narratives. It does so based on the argument that the image of a character in a narrative is constructed from its behavioral and physical traits as well as from the roles it plays in the story (Bal, 2017; Barthes, 1966). Thus, the contribution of the article is to complement the portrait of accountants in entertainment media and improve understanding of how accountants are depicted in society.

Accountants will thus be considered here as characters “in action,” situated in social interaction to other protagonists and embedded within (a fictional) society. In other words, it is not the visual or behavioral characteristics of accountants that will be looked at in this study. The focus will rather be on the actions made by accountants in social situations, and on their impact on the other characters. As stated by Eder et al. (2010),

Characters do not tend to appear on their own in narratives. In most cases they are part of a constellation of at least two, and frequently many more, characters. This constellation puts all the characters of a fictional world in relation to each other. (p. 26)

Therefore, this study aims at identifying responses to the following research question: what do roles played by accountant characters in entertainment media narratives over the last nine decades, reveal of the image of accountants in society?

This study participates in the use of popular culture to better understand what accounting constitutes in our contemporary society (Jeacle, 2009, 2012; Jeacle and Carter, 2014; Jeacle and Miller, 2016), and more particularly how the accountant image has been modeled over the years by the entertainment industry. To do so, this study will rely on a narratological approach and more particularly on a combination of fictional characters’ thematic and actantial roles, applied to 162 accountant characters found in 178 sequences of superhero comic books published from 1938 to 2018.

This study reveals that, since the beginning of the twenty-first century, accountants are portrayed as playing more positive roles than negative ones in US superhero comic books. Originally accountants were mostly presented as characters whose death or personal difficulties helped initiate the plot. They needed the superhero’s help, but they have progressively become functional sidekicks and listened-to accounting advisors. Toward the end of the period studied, the accountant has become portrayed as being helpful to the superhero in overcoming some difficulties. Thus, this article shows that US superhero comic books have progressively presented an improved image of accountants’ utility. That image can be viewed as being consistent with some of the claims by professional accounting bodies regarding accountants’ roles in society (Jeacle, 2008). However, accountants in narratives continue to suffer a lack of longevity, showing that this change is not totally achieved yet.

This article is organized as follows. As a requisite foundation to understanding our approach to roles played by characters in tales and how it complements the extant literature, section “The roles played by characters in a narrative as an element of their portrait” explains the analytic model used. Characters’ roles are described and their importance in the portrayal of a character are discussed in that next section. In section “Prior research on accountants’ roles depicted in entertainment media,” extant research of roles given to characters of accountants in entertainment media are discussed. Section “Methodology of research” explains the choice to study the US superhero comic books genre and the methodology utilized in order to address the research question. The results are detailed and discussed in section “Conclusion,” before the conclusion of the article.

The roles played by characters in a narrative as an element of their portrait

In this section, a brief introduction is provided to the core model that has facilitated analysis of the superhero excerpts. According to Margolin (2008), “all the theoretical models of character divide into mimetic or representational, treating character as a human or human-like entity, and non-mimetic, reducing it to a text-grammatical, lexical, thematic or compositional unit” (p. 52). The study of a character’s traits (shaped by physical, mental, social and personality aspect(s)) belongs to the first, mimetic, category where human-like properties are assigned to characters. For Margolin (2008), this can be explained by the fact that in “everyday usage the term ‘character’ is often used to refer to someone’s personality, that is, an individual’s enduring traits and dispositions” (p. 52).

The non-mimetic approach of fictional characters finds its roots in Aristotle’s (1942 [335BC]) study of Greek tragedy where in order to understand a character in a fictional world, one needs to analyze its role in the action. 1 For Eder et al. (2010), two different types of roles of fictional characters can be identified, based on the distinction between the story level and the narrative level (p. 23). 2 The first roles are based on thematic classifications, depending on a genre and period-specific vocabulary such as the libertine and the fop in English Restoration comedy, or villain, sidekick, and henchman in twentieth century popular media (Eder et al. 2010). Such thematic roles are presented in the story, based on a combination of behavior, motivation, and action undertaken by a given character where fictional characters are seen as actors.

Eder et al.’s (2010) second category of roles relies on characters’ functions in the narrative, based on structuralist narratology and its project “to create a systematic framework for describing how characters participate in the narrated action” (Herman, 2008: 1).

The antecedent to a systematic framework of roles analysis is often considered as being the work of Propp (1958 [1928]). After having compared Russian folk tales, Propp (1958 [1928]) noted changes in names and attributes of each dramatis personae, but little change in their functions (p. 7). This led Propp (1958 [1928]) to understand an act of character as being “defined from the point of view of its significance for the course of the action” (p. 21). From this observation, Propp (1958 [1928]) inferred that a tale often attributes identical actions to various characters, and thus, he conceptualized a tale as being based on the relationship between functions and actants to which they are allocated, by regrouping functions into action spheres – each defining a specific actant.

Greimas (1966) generalized understandings of tales with his actantial model in which all narrative characters are regarded actants: “fundamental role[s] at the level of the narrative deep structure” (Prince, 1987: 1). This model is constructed around six actants ordered into pairs (the subject and its quest for an object, the sender and the receiver, the helper and the opponent) and distributed on three axes (Figure 1).

The actantial model (translated from Greimas, 1966: 180).

For Greimas (1966), the simplicity of this model lies

in the fact that it is entirely centered on the object of desire aimed at by the subject and situated, as an object of communication, between the sender and the receiver – the desire of the subject being, in its part, modulated in projections from the helper and the opponent. (p. 207)

Indeed, Axis 1 is concerned with the desire of a subject for an object. This object can be human, material, or conceptual (e.g. justice). The object is defined by Greimas and Courtès (1993) as the place of investment of valor (or determinations) with which the subject is linked or disjointed (p. 259). It is thus called “object of valor.” However, when the subject needs first to acquire a particular object to reach the desired object of valor (and in doing so, complete its quest), this particular object is called a “modal object.” Here again, this modal object could be human, material, or conceptual. The quest for this modal object is thus an intermediary quest, necessary for the subject to be able to complete its main quest.

The subject is defined by its junction with the object (Greimas, 1976: 13). Furthermore, it is possible that several subjects’ quests are opposed in a narrative. In this case, a subject which, in order to achieve its quest, opposes a second subject (i.e. the success of its quest will mean the failure of the other subject’s quest) is called an “anti-subject.”

Axis 2 is the axis of knowledge. On one side is the sender requesting the establishment of a junction between a subject and an object. On the other side is the receiver, who is the actant for whom the quest is being undertaken by the subject. In other words, the sender instills in the subject the will to carry out the quest, while the receiver benefits from the object of the quest.

Axis 3 is the axis of power. On one side is the helper which is an auxiliary of the subject assisting it in order to achieve its junction with the object. On the other side is the opponent hindering this junction (constraining the subject) (Greimas, 1966; Greimas and Courtès, 1993).

Finally, in Greimas’ (1966) actantial model, actants are “empty” functions that could be filled by very different characters depending on the narratives. Therefore, in different narratives, accountants could play all six functions identified by Greimas (1966).

Thematic and actantial approaches are complementary in analysis of a fictional character’s actions. The meaning of a text is constructed by the reader who unconsciously travels from the different text levels, from the content (the physical and behavioral characteristics of the characters) to the story (the actions undertaken by the characters, seen as actors, and their interacting dramatic roles) to the narrative (the roles played by the characters seen as actants). In the same vein, Greimas (1966) argued that while an articulation of actors constitutes a particular story, “a structure of actants constitutes a genre” (p. 200). Therefore, the combination of actor and actant role studies is necessary to apprehend who is the character by looking at the discursive level (the actor) as well as at the structural level (the actant) (Eder et al., 2010). While the story level reveals what she or he does, it is necessary to add a narrative analysis to assess the impact of actions on the quest of the subject (the central character). However, few studies on the accountant image in entertainment media have engaged in this direction, as is shown in the next section.

Prior research on accountants’ roles depicted in entertainment media

In this section, the extant literature that has used popular culture to understand accountant images is reviewed. Recognizing the importance taken by narrative studies in accounting research, Czarniawska (2017) identifies the analysis of the image of accounting professionals in popular culture narratives as the oldest kind of such studies, finding its source long before the narrative turn in social sciences in the 1970s (p. 185).

Among the studies of accountant representations in popular culture, two approaches can be distinguished. One approach is composed of analysis of one or a few narratives with an accountant as the main protagonist (“the hero”) of the narrative. The second approach regroups quantitative studies in order to highlight the main components of the accountant representations, as well as their evolution over time (Dimnik and Felton, 2006; Richardson et al., 2015).

The images of accountants revealed by these two approaches differ. When the accountant is studied in novels or movies in which she or he is the “hero,” the image is rather positive. However, when the image of accountants is studied in a large database of accountant character appearances in a singular popular culture medium, the stereotype appears to be mainly negative (Czarniawska, 2017).

Two explanations may illuminate how paradoxical images of accountants have arisen in popular culture studies. One reason probably resides in the deliberative choices of researchers to analyze a specific movie or novel because of the unexpected image of the accountant it contains. As an example, Czarniawska (2017) identifies Stranger than Fiction as a movie worthy of analysis because it goes strongly and successfully against the accountant stereotype (p. 186). It could also be argued that such a movie is interesting because the accountant is presented as a positive character because he is an accountant. A second reason for the paradoxical images may be that accountants are sometimes the authors of the stories studied and such stories highlight the fact that the image accountants have of themselves is far from their representations in popular culture. As Richardson et al. (2015), note, negative accountant images “persist in spite of the advent of the contemporary professional accountant who is portrayed as a confident and sociable person performing a variety of high-level complex tasks under specialist designations” (p. 29). Nevertheless, the two explanations provide evidence that the roles played by accountant characters in narratives are important constituents to understanding their image.

Several studies have analyzed the roles played by accountant characters in entertainment media, each favoring a different approach. Beard (1994) identified three dramatic functions of the accountant in 16 North American and British movies from 1957 to the end of the 1980s. She discerned: humor based on the stereotypes of the accounting profession; the accountant character being a “shortcut for narrowing the range of personality traits the audience can expect of that character” (p. 309); and functionaries where accountants are “intermediaries to introduce technical information needed to resolve the plot” (p. 309).

In addition to the three dramatic functions of accountants, Beard (1994) found more instances of accountants being used for character development (10) than those participating in plot development (3) or presenting comedy (3). Character development, however, showed an equal balance between dysfunctional, normal, and transitional depictions. These three depictions vary over time, yet the stereotype was not really modified, but instead some characters “have simply been given the freedom to exit that stereotype and enter another” (p. 312).

The study of accountant stereotypes by Richardson et al. (2015) relies on the argument by Fiske et al. (2002) that group stereotypes tend to be captured by two scales, of warmth and competence, respectively. The combination of the character’s personal attributes and his or her role (understood as his or her task performance and perception of status) are necessary for an overall view of the accounting stereotype. Based on a meta-analysis of 16 journal articles examining the accounting stereotypes in large databases, Richardson et al. (2015) identify four main stereotypes: “bookkeeper”; “scorekeeper”; “public interest guardian”; and “entrepreneur” (p. 36). However, by limiting their definition of competence to duties undertaken by accountants (p. 30), questions remain: what about an accountant character who is not in an accounting environment or for whom nothing is said of his or her accounting competencies? What about a character who is competent with warmth, in the “public interest guardian” category, but is working for a villain? What about a character who is presented as low on warmth or on competence, but who finally saves the world? For all these characters, what defines them is not only their accounting skills or their personal characteristics but the larger role(s) that they play in the narrative. Addressing that gap, our goal is to use superhero comics to better understand the accountant image. We next explain the method selected to do so.

Methodology of research

The study of US superhero comic books genre

“Born” in 1938 with the first appearance of Superman in Action Comics #1 (Coogan, 2006; Steranko, 1970), the superhero comic books genre has an important place in American society (Coogan, 2006; Duncan and Smith, 2009; Johnson, 2012) and in the worldwide entertainment business more broadly (Cawelti, 1976; Crothers, 2018; Duncan and Smith, 2009; Hassler-Forest, 2012). Johnson (2012) captured this importance when he wrote,

comic book superheroes are an important part of America’s social fabric. Since its creation in the late 1930s, the superhero has become the United States’ dominant cultural icon. Superheroes quickly expanded from their comic book origins to become a part of nearly every portion of American culture and society. Superhero films have become a Hollywood staple, numerous comic book related television shows fill the airwaves, and hundreds of other outlets showcase our fictional spandex-clad guardians . . . More importantly though, super-heroes have become part of the structure of American life. (p. 1)

Superheroes’ adventures narrated in comic books mirror the mentalities current to their creation (Johnson, 2012; Strömberg, 2003). Thus, superhero “narratives have closely mirrored and modeled American social trends and changes. This means that superhero stories are excellent primary sources for studying change in American society from 1938 until the present” (Johnson, 2012: 2).

Within the superhero narratives’ relevance to social trends is a growing influence of the economic world in the fictional worlds (Wright, 2001). There is a more global movement of situating superheroes’ adventures in more “realistic” contexts (Klock, 2002). The archnemesis of Superman was first a longtime mad scientist character, but in the 1980s was reinvented as a powerful captain of industry character (Booker, 2014; DC Comics, 2015). Similarly, increasing numbers of superheroes (and villains) became businessmen entrenched in the economic reality of their world. 3 Consequently, superheroes fight on a different ground (the economic world) than in the past, in a movement to bring superheroes stories closer to readers’ reality and to the real world (Johnson, 2012). As superhero comic books artists Morrison and Quitely (1996) stated, “The comics are just, like, crude attempts to remember the truth about reality.”

In addition to the importance and altered types of relevance of superhero comics as a genre, their use for this study is piqued by a similar narrative architecture adopted over the years. The architecture involves predefined roles at the story level (superhero, villain, needful character in danger, helping character, etc.) and an archetypal story form at the structural level (Cawelti, 1976; Eco, 1972; Eder et al., 2010). There is an adventure formula for the central fantasy with the hero (individual or group) succeeding against obstacles and dangers to accomplish some important and moral mission (Cawelti, 1976). Frequently also multiple specific cultural conventions are combined or synthesized with a more universal story form (Cawelti, 1976).

The architecture of this genre, with its limited superhero characters, provides a certain “expectability,” but this study is also enhanced by the genre’s variation over time. For this study, superhero comic books provide

flexible frameworks within which a considerable amount of deviation from prototypicality is possible: not only do some texts create blends between two or more generic traditions, which will result in the occurrence of unexpected character varieties. What is more, much variation in the representation of characters and their effects on readers and viewers results from the deviations from the established generic norms. (Eder et al., 2010: 44)

Given the interest in accountants’ images over the nine-decade period of this study, the existence of variation in an otherwise stable genre improves the richness of this study.

By studying a given formula based on stable archetypal patterns, like the superhero genre, it is possible to analyze role changes given to the accountant. Comic books in general, and its superhero genre in particular, represent “collective fantasies shared by large groups of people” (Cawelti, 1976: 7). Thus, analysis of their content – especially longitudinal analysis – should be suited to identifying change in social representations of accountants if there are sufficient representations to support meaningful analysis.

The identification of US superhero comics with at least one accountant in them

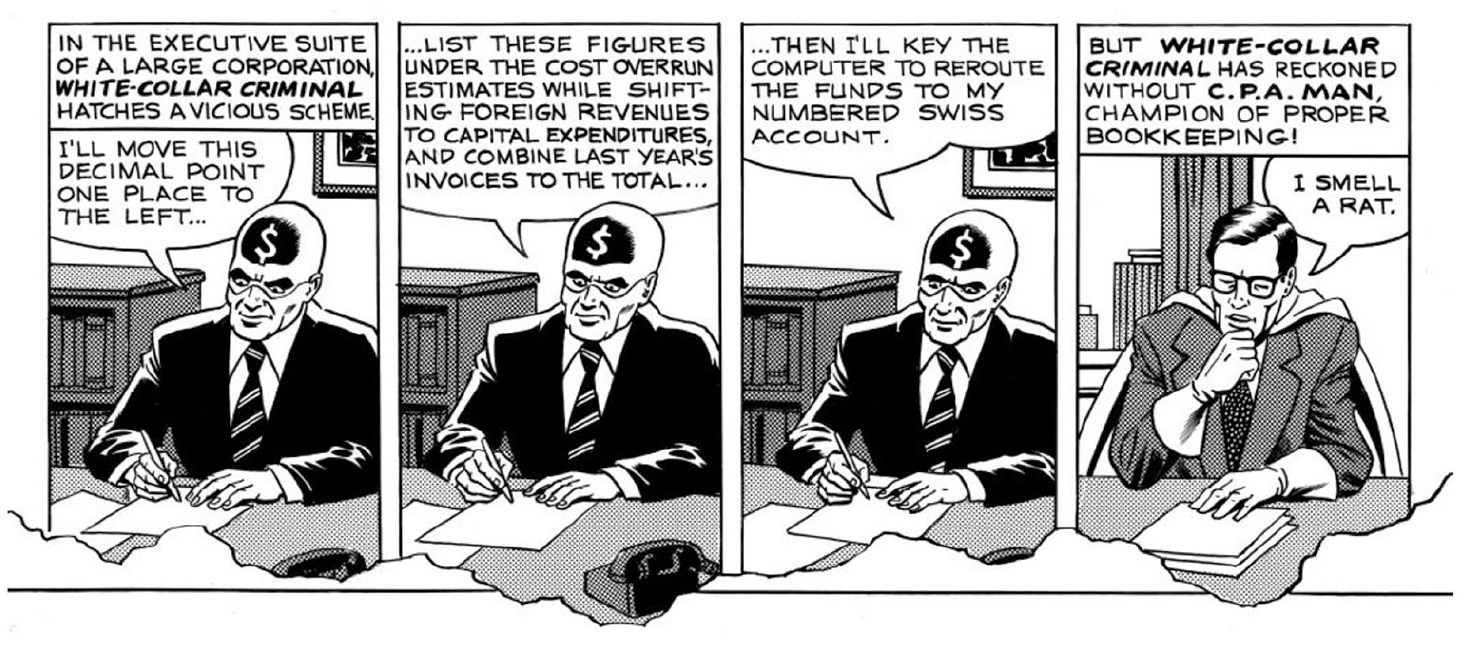

When purchasing a superhero comic, it seems unlikely that the reader is doing so for its accountant character(s). Accountants and superheroes seem to be mismatched. Indeed, this has been the subject of satire in Marvel Super Heroes That Didn’t Quite Make It (Kirchner, 1981) where a superhero idea “CPA Man” (“the champion of proper bookkeeping”) ends up in a garbage bin. We return to an extract from Kirchner’s CPA Man, but first this section explains the data selection method given the apparently counter-opposed nature of superheroes and accountants.

As noted above (section “The roles played by characters in a narrative as an element of their portrait”), the extant research has revealed accountants in literature or movies. That rebuts the expectation that popular literature will be void of accountants. Therefore, in order to find superhero comic books with at least one accountant character in them, a database of 25 Internet websites with presentations, reviews, or criticisms of US comics was analyzed for this study. The websites visited and their number were defined according to the following steps: (1) official websites of the six major US comic book publishers representing 86 percent of comic book sales in 2018; 4 (2) 14 additional websites about US comics, chosen for their relevance; (3) five additional sites in order to check that saturation was reached after analysis of the contents of the first 20 websites. In each of these websites, 12 keywords were searched for; namely, “accountant”; “accounting”; “accountancy”; “CPA”; “financial manager”; “financial director”; “financial service”; “financial office”; “financial assistant”; “financial chief”; “CFO”; and “Chief Financial Officer.”

According to Duncan and Smith (2009), US comics can be classified according to their genre (superhero, romance, mystery, detective stories, horror, science fiction, etc.). From the resultant database, superhero comics were identified as being those with one or more main characters with the following characteristics (Coogan, 2006: 30; see also Coogan, 2009): heroic with a selfless, pro-social mission; possessing of superpower/extraordinary abilities, advanced technology, or highly developed physical, mental, or mystical skills; a superhero identity embodied in a code-name and iconic costume; typically expressing their biography, character, powers, or origin (transformation from ordinary person to superhero); generally distinct from other genres (fantasy, science fiction, detective, etc.) by a preponderance of generic conventions.

Hybrid genres also exist. For example, some narratives melt the superhero genre in with a Western genre, or teen humor genre or romance genre (Duncan and Smith, 2009). Where the superhero genre was dominant in such hybrids, they were included in this study. However, satires of superhero comic books presenting the quest or the mission in a humorous and deconstructive way, have been excluded because of their double entendre hidden meanings.

For inclusion in the data set used here, the profession of accountant had to be clearly specified, by text included in the comics (e.g. dialogue; intertext; surroundings specific to the accounting profession; or the profession of the character is indicated by way of a sign indicating that the action took place in an accounting department). This assisted researchers to avoid any misinterpretation of “what is” an accountant (Bal, 2017). The goal was to retain only the characters voluntarily presented as being an accountant by the comic book’s authors. The objective was not to be exhaustive; instead it was to obtain a representative sample of accountant characters. Future researchers in this field may identify additional accountant characters.

The analytic method identifying accountants’ roles played in the story and in the narrative

The narrative level and the thematic level are discovered by the reader simultaneously. Furthermore, they together with identification of the characters both participate in constructing understanding of the narrated story. Thus, for reasons of clarity, the methodologies followed here unveil the accountants’ actantial roles and their thematic roles successively. A short example is used to illustrate both methodologies.

The narrative level: analysis of accountants’ actantial roles

To analyze the actantial functions played by accountant characters at the narrative level, the narrative analysis model developed by Greimas (1966) was applied to every sequence in which an accountant played an actantial role. In accordance with Barthes (1966), a sequence was defined as

a logical string of nuclei, linked together by a solidarity relation: the sequence opens when one of its terms is lacking an antecedent of the same kin, and it closes when another of its terms no longer entails any consequent function. (p. 13)

5

All the sequences involving an accountant in the selected superhero comics stories were analyzed individually and separately because the same accountant character could play several actantial roles in the same narrative because his 6 role could change over the course of the narrative (e.g. he could be the helper at the beginning of the narrative, but become a receiver further on). Moreover, sequences involving a character playing the same role (in the same book or in different issues) have only been counted once. This choice is explained by the fact that the objective of the study was not to know the number of times a character is presented in the same role (some characters play different roles, while others always play the same role in one or several sequences). Instead, the objective was to determine the different roles played by accountants in comics. Finally, characters without an actantial role were not included.

The methodology led to the identification of 178 sequences including 162 accountant characters. The small difference between the number of accountant characters identified and the number of sequences studied shows that a majority of accountant characters play only one formatted role. That was in accordance with the logic of the genre (Cawelti, 1976). Only a small portion of them see their role evolve over the course of the story.

Finally, these sequences were analyzed according to the different epochs that have marked the world of superhero comic books (Klock, 2002; Levitz, 2010; Morrison, 2011), namely, the “golden age” (1938–1955); the “silver age” (1956–1970); the “bronze age” (1970–1986); the “dark age” (1986–2000); and, the “modern age” (2000–present). These five epochs have been defined by comics critics based on the different views of the superhero that they convey, whether it is about identity, actions, or society’s reactions (Fingeroth, 2004).

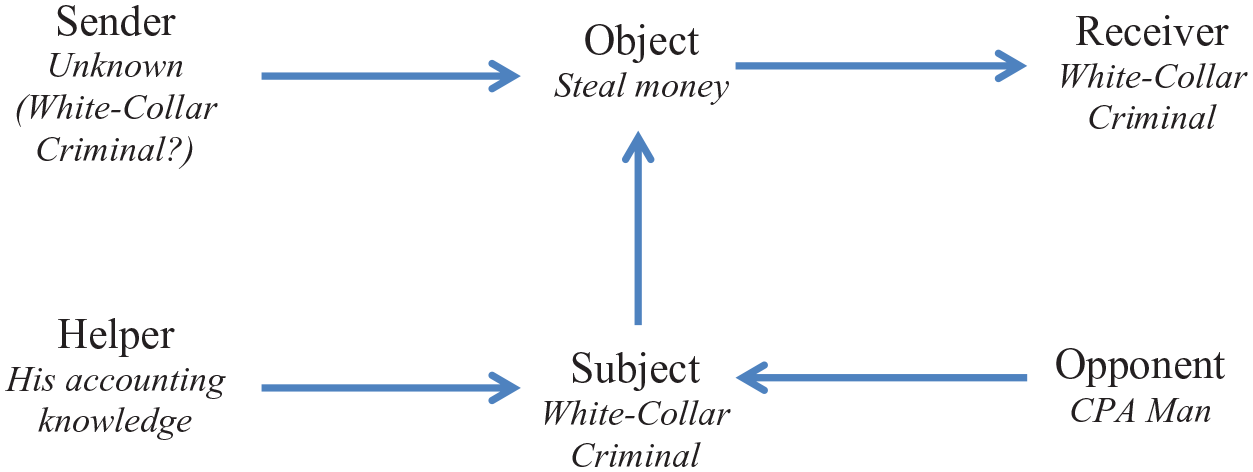

Although Kirchner’s (1981) satirical comic referred to above is not part of the comics corpus studied here, 7 it will be analyzed to provide an illustration of the methodology followed. In this sequence (refer Exhibit 1), the first character, “White-Collar Criminal,” is trying to embezzle money, which is his quest. He is the receiver of the quest (he evokes his numbered Swiss account). Maybe he is also the sender of the quest (perhaps his motivations are personal). However, nothing is said about this point. Therefore, it is not possible to conclude that he is the sender because it could also be that the embezzlement may be for external reasons (e.g. to pay for the healthcare of a beloved one). Finally, his accounting knowledge (a non-human actor) can be seen as a helper. The second character is “CPA Man.” From the first character’s perspective, he is an opponent. CPA Man can also be seen as an anti-subject looking to fulfill an opposite quest, which is respect for good bookkeeping (a quest of justice). From his perspective, White-Collar Criminal is an opponent to CPA Man as well.

Extract from Paul Kirchner (1981) comic Marvel Super Heroes That Didn’t Quite Make It (p. 23).

This short sequence can thus be presented according to the actantial model as shown in Figures 2 and 3, from the subject and the anti-subject perspectives.

The actantial model applied to Paul Kirchner (1981) comics Marvel Super Heroes That didn’t Quite Make It – White-Collar Criminal perspective.

The actantial model applied to Paul Kirchner (1981) comics Marvel Super Heroes That Didn’t Quite Make It – CPA Man perspective.

While this analysis helps to understand the story, it is still necessary to add a thematic analysis and emphasize the different role-played by each character for full understanding.

The story level: analysis of accountants’ thematic roles

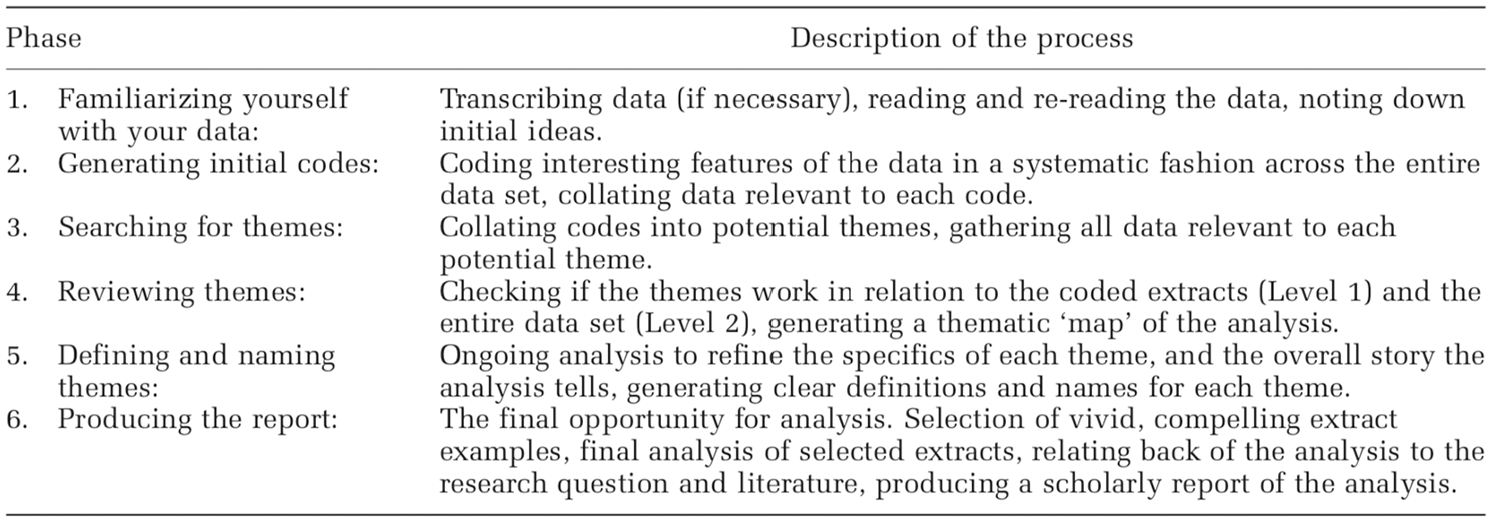

In order to study accountants’ thematic roles, their actions or the actions from which they suffer, at the discursive level, were identified. To do so, comics reading theories on the codes used in comics (Eisner, 1985, 1996; Horstkotte, 2013; Kukkonen, 2013a, 2013b; McCloud, 1993) were mobilized. Following Figure 4 (Braun and Clarke, 2006), thematic roles were created progressively, each time a new thematic role was recognized.

Phases of thematic analysis, from Braun and Clarke (2006: 87).

Continuing analysis of the extract of Kirchner’s (1981) sequence (refer Exhibit 1), we can further illustrate thematic roles. It could be analyzed as follows: in this story, there are two characters who are (indirectly) interacting. Based on their motivations, their names (White-Collar Criminal vs CPA Man), and their visual attributes (the visual code used to qualify a character such as the mask hiding a character’s face or the “good looking” face of the character, 8 as well as the cape as a symbol of the superhero), the reader understands that White-Collar Criminal is the villain (he tries to embezzle money) while CPA Man is the hero (he fights for “proper bookkeeping”). With these methodological aspects in mind, we turn to the results of the study.

Results

Accountants’ actantial roles

The finding that enables the remainder of this study is that superhero comics have sufficient images of accountants to inform on a social view of accountants. A large number of images and a wide range of diversity therein were found. With 178 actantial roles identified, the conclusion is reached that accountants, and probably the accounting craft, are sufficiently important and/or interesting for both comics artists and readers to be accorded roles within the narratives constituting superhero comics.

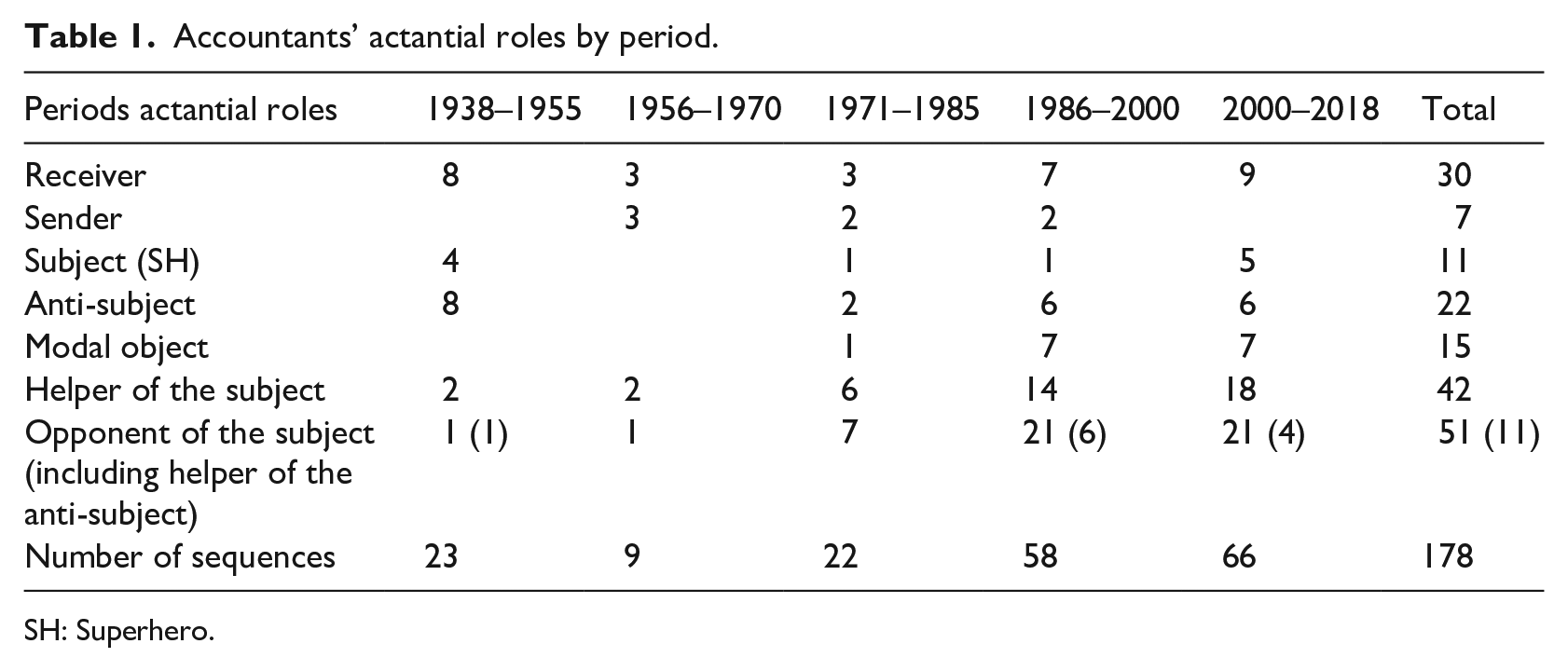

Accountants’ actantial roles found in this study can initially be overviewed by the changes observed across nine decades of data. In doing so, it is seen that a material increase in the number of accountant roles occurs from the mid-1980s to the present. We postulate that this increase reflects both a growing influence of the economic world in fictional depictions (Booker, 2014) and an increase in the number of comic books published. 9 Thus, there has been a shift in the subject matters underlying superhero comics together with an alteration in the market of ideas whereby superhero comics have attracted increased economic activity. That these changes are identifiable is an artifact of the longitudinal nature of the data but of more interest is a consideration of the actantial roles.

The most dominant role in number across the nine decades and from the mid-1980s was as an Opponent of the subject (including Helper of the anti-subject). Comparably, the role of being Helper of the subject increased substantially from the mid-1980s. Except for the Receiver role, the other roles (shown in Table 1) were not observed with much frequency across the full period. At the narrative level, actantial roles played by the accountant have evolved over the years in the superhero comics genre. While Subject and Anti-Subject roles were important roles in the first era, both have declined over the decades. Similarly, while 14 percent of accountant characters are beneficiaries of the quest of the subject, this role has decreased over the years. On the contrary, it appears that accountants more often play the role of the Helper of the superhero or the role of the modal object, that is, a necessary condition the superhero has to go through to be able to complete their quest.

Accountants’ actantial roles by period.

SH: Superhero.

These first results need to be handled with care. When considering the positive or negative influence of actantial roles on the subject quest, it appears that the accountant more often plays positive roles (subject, modal object, helper) than negative ones (anti-subject and opponent) in the modern era, and less neutral roles (refer Table 2).

Percentage of accountants based on the nature of the role-played.

However, these results leave the possibility that such indications are confounded by matters that actantial role considerations alone cannot fully reveal. These actantial roles have to be coupled with the thematic roles that accountants play in the story in order to refine this first impression. Indeed, based on how accountants are represented in the story, a positive actantial role could hide a negative image because of the thematic roles played, and in addition, a negative role could lead to a positive presentation of the character when considering its influence. Therefore, we turn next to accountants’ thematic roles.

Accountants’ thematic roles

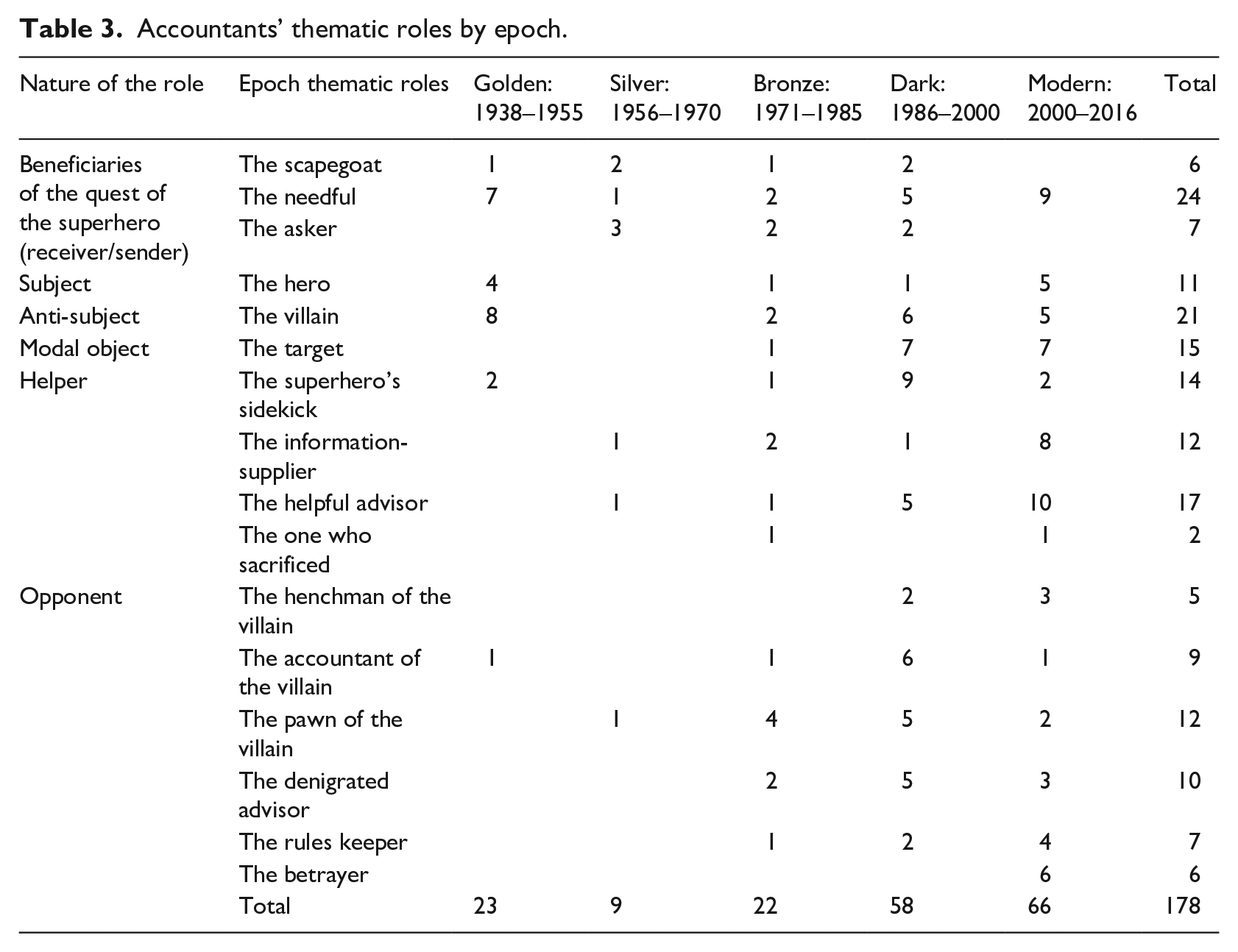

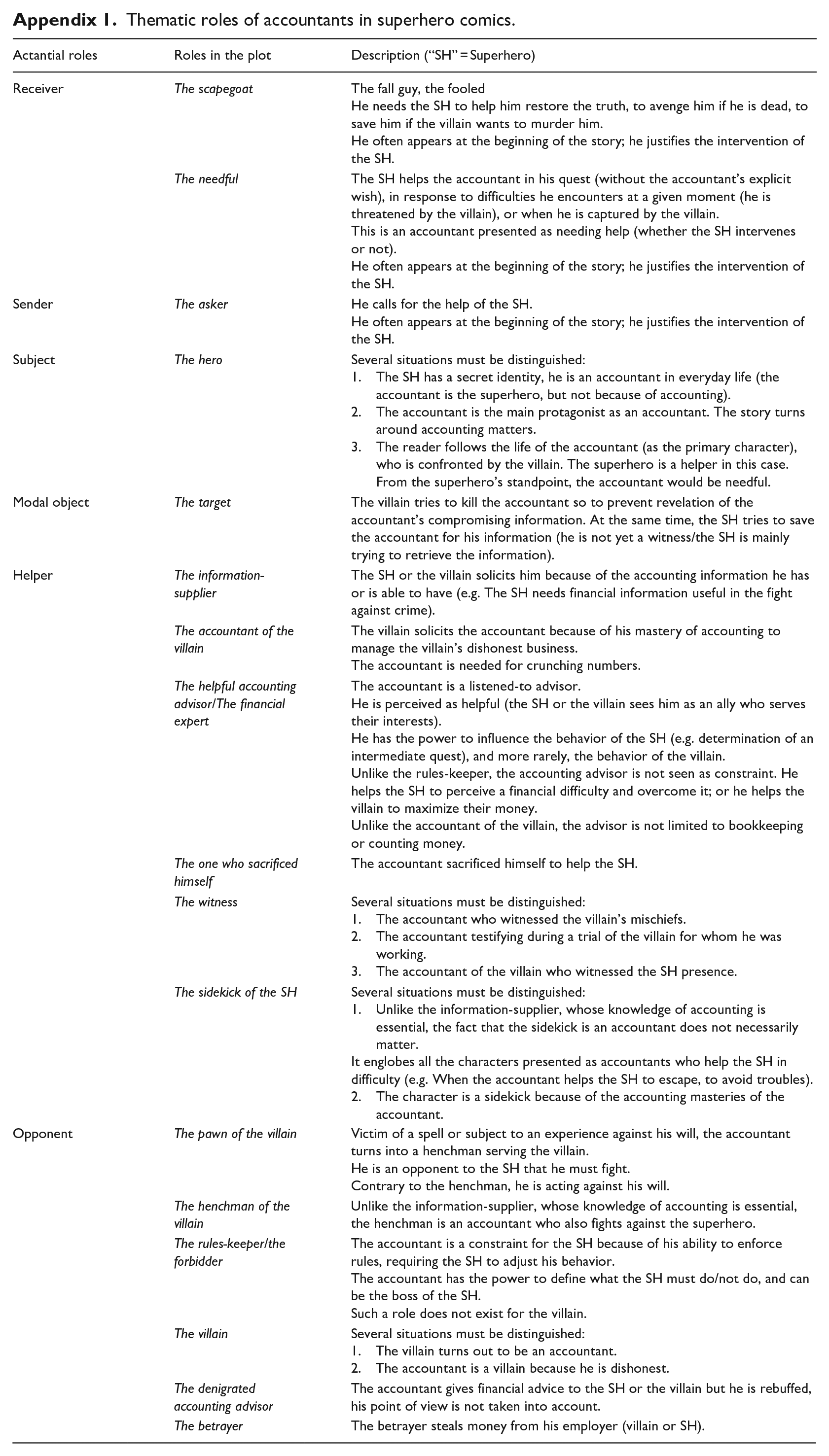

This section presents a synthesis of findings on the thematic roles found in the superhero comics. The synthesis demonstrates some of the empirical supports while also explicating the nuances of these roles and relating their occurrence to the five superhero comics epochs discussed in section “The narrative level: analysis of accountants’ actantial roles.” Following Braun and Clarke (2006), during the data analysis 17 different thematic roles were identified across the nine decades. These thematic roles are itemized and described in Appendix 1, while Table 3 presents the distribution over time of each of the identified thematic roles.

Accountants’ thematic roles by epoch.

Beneficiaries of the quest of the superhero

In all the sequences in which accountants are beneficiaries of the quest of the superhero, they are depicted as weak characters who need help (they have been fooled, aggressed, threatened, killed), and their survival or revenge requires the intervention of the superhero. One explanation of this phenomenon lies in the fact that “early Golden Age superheroes often took the side of the little guy against larger forces (including corporates)” (Booker, 2014: 502).

This image was observed in each of the epochs and across all nine decades. However, from the start of the 1990s, accountants’ relationships with the superhero have differed: they are now either colleagues in the daily life of the superhero; friends or members of the superhero’s team who need to be saved; or individuals previously revenged. This image contrasts with the image of accountants in the 1970s and the 1980s who were not linked with the superhero. This evolution indicates a turn in the perception of the accountant, from a negligible character to a character considered to have some gravitas.

The subject/the hero

Since 1938, accountants have rarely been heroes and even less superheroes. This situation could be explained by how the initial comics artists envisioned the superhero. Indeed, most of the superheroes created in the Golden Age had a secret identity and a need to be “at a hub of information so that they will know immediately about various crises” (Smith, 2009: 127). Therefore, superheroes could not be day laborers because

the secret identity must be put on hold while the fire is put out. The secret identity, therefore, must be a form of labor that is not so directly supervised that the worker cannot escape [. . .] If Superman worked on a factory assembly line, how would he punch out his timecard to save the world? The advantage of a professional job is the amount of freedom given to well trained workers who are entrusted to account for their time as they see fit. (Smith, 2009: 135)

In the first period (“Golden Age”: 1938–1955), accountants playing hero roles were in the needful category if the story was narrated from the superhero standpoint rather than the accountant standpoint, or if the superhero and the accountant were not the same character. For example, in the story Marvin the Great published in Atoman #1 (1946), Marvin Smith is an accountant at home who transforms into Marvin the Great when he looks for situations in which he could be useful. Thus, after hearing of a kidnapping news item called by a paperboy, he ended up saving his boss. However, before saving him, Marvin (in disguise) asks that the accountant (himself) be given improved work conditions. Clearly, the possibilities of similar plots are limited (the superhero has to be away from his work) – and the fact that he is an accountant adds no interest to the plot. In Marvin the Great, the concatenation of accountant and superhero was merely a mechanism to characterize ordinary Marvin as being a dominated character (by his wife, by his work, by his boss). Moreover, the image of the accountant in this sequence remains negative because he was self-serving.

Another character in the hero category during the Golden Age of comics was an accountant who dreamed of being a caped superhero fighting crime (Marvel Mystery Comics v1 #92 (1949)). Impassioned by detective stories, he grabbed the opportunity to become one when he realized that one of his neighbors had disappeared. Although the superhero did not believe in his quest at first, he finished by helping the accountant in the course of his investigation which became more dangerous than expected. After the case was resolved, thanks to the intervention of the superhero, the accountant wisely went back to his normal life, no longer dreaming of himself as a superhero.

In both of these stories and in several others over the years, the job of accountant seems only to be used to give some information about the character within the technical constraints of the medium: a limited number of panels to tell a story in the case of comics. At the same time, it created a contrast between the life of the accountant and the dangerous adventures into which he was propelled (Beard, 1994). However, in the 1990s, accountants started to become heroes because of their accounting expertise. Illustration of this change was the appearance of the character of Albert Cleary, a comptroller, on the comic book Damage Control front cover of Issue #2 (1989). 10

Previously, only characters being a pawn of the villain or a target had the “honor” of being on a front cover (e.g. The Flash #347 (1985) and The Adventures of the Outsiders #43 (1986), respectively). However, on these covers, accountants were only secondary characters; the superhero remained as the main character. In contrast, Albert Cleary is “the hero” confronting the supervillain. The story is about an unpaid bill by the villain. The image of the accountant is contrasted with the villain. As the cover shows, the words defiantly announced by the accountant (“you’ll pay for this, Doom!”) invoke the old image of the accountant attached to the rules and grasping a document with which to fight the villain without considering the consequences (he can be crushed by the villain). Within the story that image is contrasted with the superhero who fights the villain for justice. At the end of this story, the villain asks the accountant to consider working for him, thus reinforcing the image of the powerful (the villain agreed to pay the bill) and useful professional. Therefore, even though the cover could seem quite “tongue in cheek,” at the story level, the relevance of the accountant is highlighted.

The anti-subject

In the Golden Age (1938–1955), five of the eight villains were dishonest accountants. However, since the 1970s, dishonest accountants no longer appear as villains. Instead of dishonesty being the cause of villainous behavior, the villain accountants are portrayed as either deviant men or ex-accountants who have acquired superpowers (unrelated to accounting). Illustrating the deviant male accountant image is the example in Spider-Woman v1 #22 (1980) of the character Casper Whimpley. Whimpley disguises himself as a clown so as to assault women at night. However, this image of the accountant turned supervillain still maintains the implicit image of the weak and mocked weak male who can now take his revenge and express his resentment against society.

The modal object

The information possessed by accountant characters is seen as important. That utility is expressed by both the villain (who does not want this information to be known) and the superhero (who could use this information against the villain). As a result, the accountant per se becomes significant and an object of importance in the story: the superhero must find and save the accountant before the villain can get to him. In this role as an information-supplier, the accountant has appeared over the years since the 1970s.

The appearance of this role highlights a changed image for the accountant. In the information-supplier role, the accountant is needed in the superhero’s quest. In other words, with the target roles, accountants are now helpful to permit the superhero to be one. However, prior to that accountants who were being saved by superheroes as other people were helped because the superhero had to help people (he is a superhero after all).

The helper

In the 1970s, accountants as “sidekick” assistants appeared alongside the superheroes and this role increased in the 1986–2000 era. Two different kinds of sidekicks can be distinguished. One is composed of characters recruited by the superhero – especially for their mastery of accounting. All these characters had a positive image of being competent workers. The other type of sidekick is composed of characters presented as accountants, but their role is not linked to accounting. For them, the image is contrasted. For example, in Excalibur #13 and #15 (1989), and #42 and #43 (1991), the character known as “Numbers” is a big Lizard member of the superhero team and his name, timidity, and poor fighting skills, are all pointers to a negative image. However, he is the one who, at the end, “receives, as a kind of side benefit, the favors of one or more attractive young ladies” (Cawelti, 1976: 39).

A second instance is J. Pennington Pennypacker in NFL Superpro #10 (1992). He is a small, skinny accountant on a holiday camp with three college friends who also have jobs with a similarly unattractive image (actuary, mortician, and clerk). After being victimized by the villain, they all gain superpowers in relation to their jobs. The accountant was thus able to “throw money at his problem,” with rays of coins launched from his hands. He used this superpower to help the superhero to defeat the villain. Notwithstanding this success, Pennypacker is often critiqued in superhero comic websites as being one of the most lame and useless characters in comic books history.

In same vein as the sidekick role, the helpful advisor role developed during the last two periods and became dominant in the last (2000–2016). One of the main reasons for their helpfulness lies in their new role as important advisors of CEOs who are also superheroes. Indeed, there are two main types of superheroes: superheroes with supernatural abilities, like Superman, and superheroes with high physical abilities and intelligence, backed with what looks like unlimited capital, like Batman (a billionaire playboy at the head of Wayne Corporation) or Iron Man (a successful industrialist in the weapons business and then in more socially responsible activities). Superheroes with supernatural abilities are presented as disinterested superheroes known for their dual identity in order to earn money (like Superman and Spiderman), without the need of an accountant. In contrast, other superhero characters need to have financial advisors in order to protect their company (and their capital) because they depend on it to fight crime. Unlike superheroes, helpful advisors are not fighting directly against the villain. They only operate in the economic/financial sphere where accounting is also portrayed as being functional.

Finally, another positive role from the superhero’s standpoint is the accountant who sacrifices himself. Accountants are seen as heroes from their behavior and their dignity (their sacrifice helps save the world; helps the superhero). However, they are presented as being unimportant characters. At the end, their image remains ambiguous. On one hand, their death is a pointer to the negligible and replaceable accountant; on the other hand, accountants who sacrificed themselves take on the role of the martyr, devoting themselves to the superhero’s larger quest for justice. Therefore, the accountant’s death stands as a symbol of accountants’ functionality in safeguarding the public interest. Moreover, superheroes try to prevent the accountant’s sacrifice thus showing the importance of the accountants’ actions.

The opponent

Within the opponent category, six thematic roles were found. Within those six roles, the pawn of the villain role is similar to the needful role (within the beneficiary category) in that the accountant is a weak and dominated character needing help. He is acting against his will, manipulated by the villain to fight the superhero. However, the victory of the superhero helps to reveal the true identity of the accountant. Therefore, while they were opponents, it is against their will, contrary to accountants working specifically for the villain.

Unsurprisingly, the tasks undertaken by accountant characters playing the Opponent role are to launder money or fraudulently balance the books. They are only executors: it is the villain who tells the accountant what to do. The cold and authoritative interaction between the villain and his accountant serves to reinforce the power of the villain – both economically and socially. Equally, the image of the accountant as a servile employee is reinforced by the lack of consideration shown by the villain to advice that the accountant tries to pass on (the denigrated advisor).

A new category of opponent role appears in the Modern Age (2000–present): the betrayer. The betrayer differs from the villain found in prior epochs by the fact that the betrayer steals the money of the villain or the superhero who employs him. It is interesting to speculate that this new representation may be interpreted as a sign of a loss of confidence in the accounting professional in this era. As financial scandals and corporate collapses become larger with wider ramifications, it appears that comics books are connecting accountants to such scandals that have revealed fraudulent and complicit behaviors of accountants (Carnegie and Napier, 2010; Rogers et al., 2005). Such speculation and its ilk inevitably lead to what can be gleaned from this nine-decade study of superhero comics – as is discussed in the remainder of this article.

Reflections on 80 years of accountants’ roles in superhero comics

Forget the muscular body, the tights and the cape, accountants as everyman

This study highlights the difference between the image of accountants seen as superheroes (Picard et al., 2014) and the representations of accountants in superhero comics, where they are rarely superheroes. The analysis of the accountant characters in superhero comics since 1938 shows that such a difference could be explained by two main reasonings. First, comics authors have had difficulties to envision what could be accountants’ superpowers, mostly because of the negative image of the number cruncher, but also because of the difficulty to perceive what is the positive role of accountants in society. Therefore, only superheroes with a secret identity, working as an accountant in their daily lives, have been imagined. Frequently, this was in order to create a contrast between the uninteresting life of an accountant and the dangerous and successful adventures lived by the superhero.

At least from the mid-1980s, accountant images seem to have taken on increased importance to superhero narratives as told in comic books. The economy-related contextualization of superhero comic book narratives has been related to the observation that accountants have incrementally taken a major importance for superheroes and villains. Progressively, the positive roles played by accountants outnumbered negative roles. Indeed, the combined analysis of actantial and thematic roles shows that in the last era studied (the Modern Age: 2000–2016), accountants are now playing positive roles because they are accountants.

Looking at narratives with advisors or sidekicks chosen for their accounting competencies, which emerged in the 1990s, it became apparent that accountants are now presented as men or women who can make a difference when the superhero cannot. In such narratives, while they don’t have superpowers, nor the superhero costume, accountants are still the real (super)heroes. They appear better equipped to handle a certain type of crisis than the super-heroic individual, whose physical superpowers are inadequate. For the sidekicks and the heroes, accounting knowledge is a superpower per se. Accountants are now shown as functional helpers serving the public interest via their important role in the superhero’s quest. While the alter ego of Superman, Clark Kent, would see a challenge and quickly think “This looks like a job for Superman!” before hurriedly changing into Superman to fight crime, the data suggest that his mantra could equally be accompanied or even replaced by “this is a job for an accountant!”

Even characters playing negative roles do not have an entirely negative image. The pawns of the villain manipulated into fighting the superhero are portrayed as acting against their natural will. The accountant working to improve the financial situation of the villain is equally portrayed as being a functional and competent character. Moreover, in the Modern Age (2000–2016), more accountant characters are seen as helpful advisors than denigrated professionals and so this is seen as a marked change in the depiction of accountants within this genre of popular culture.

This conclusion is coherent with Eco’s (1993) observation that since the 1990s, the everyman has overcome the superman (p. 157). The model offered is no longer the exceptional man, but a character not necessarily beautiful, athletic, or heroic with whom everyone can identify. The maintenance of a contrasting image of the accountant (functional but weak, important but killed) is therefore a way to incarnate the Everyman. The everyman is seen as useful but weak while also being important but disposable with a consequential lack of longevity.

Longevity is a troubling matter: accountant death as a means to define the superhero or the villain

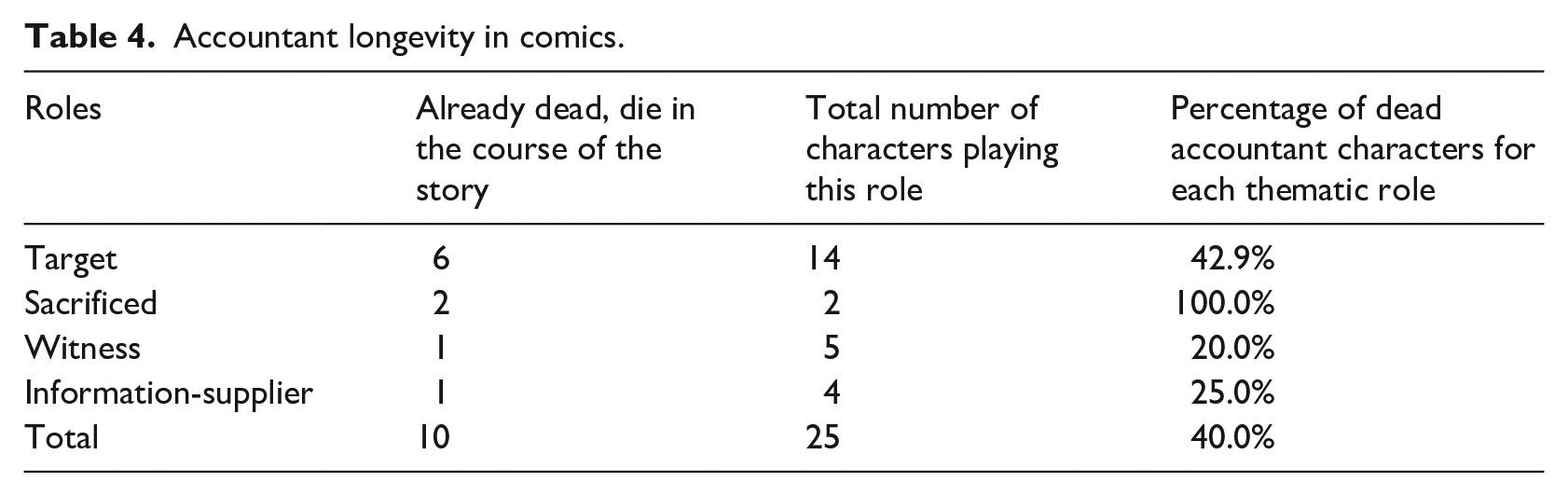

A notable feature of accountant characters in superhero comics is that they do not last long. Their longevity can be measured in numbers of episodes in which they appear or in terms of the story length in which they participate. On both counts, the accountants need good funeral insurance. They are frequently either already dead and thus referred to in flashbacks to the past or are likely to die – often in murders at the hands of others – within a short period. Whereas some superhero characters have existed for decades, accountant characters are not so lucky.

All the characters playing roles of information-supplier, target, and the sacrificed share the image of being weak. One indicator of this conclusion is the number of accountant characters playing these roles who are either already dead at the beginning of the story or are going to die at one point or another in the story (refer Table 4), revealing the accountant as a negligible – indeed, disposable – character.

Accountant longevity in comics.

To these first group of characters, could also be added the denigrated accounting advisors. Whether these characters are explicitly killed or they suffer a symbolic death, when the hero or villain reject them, the consequence is the same: more dead accountants who disappear from the story. Their “annoying power” is shut down.

The explanation of this situation lies in the dramatic roles of these characters. Indeed, they all participate in the characterization of the hero or the villain. The cold and violent murder of the accountant by the villain is a way to show the depth of evil in this character, while the superhero’s protection is contributing to the kind of stories constructed on the theme of “defense of the little guy” that have largely characterized superhero stories over the years (Booker, 2014). Accountants are thus a means to justify (and reveal) the superhero. Similarly, the death of the accountant is sometimes also a means to help the reader appreciate that the superhero falls into the “outlaw hero” category (Smith, 2009). In that category, a hero serving justice does so with unconventional or immoral methods contrary to the “official hero.” Therefore, accountants are back to their status of the irrelevant professional in their accomplished “role.” For example, in Black Widow #14 (2014), the superhero throws out of a plane, the accountant she was interrogating for information on the villain. However, she does so while he holds a parachute and thus the frontier between the outlaw hero and the villain is demonstrated. Such behaviors and unexpected endings create a “humoristic” kind of situation where humor is not the genre, but slight twists can enliven the plot and characterizations. Similarly, in Harley Quinn #12 (2015), the accountant is a good-looking young man, in the role of the information-supplier to the villain. Even though he appears to be a prisoner, chained to his desk behind a calculating machine, he is the lover of the alien who has captured him. However, Harley Quinn (the outlaw hero) kills the accountant by mistake and thus accidentally starts a war. Thus, the accountant seems to be a disposable stratagem to allow introduction of gratuitous violence and a battle between superhero and villain.

The absence of longevity may be a characteristic of comics in that other professional groups equally do not appear across generations (where are the architects? the lawyers? the engineers?). However, the willingness of comics authors to have accountants die in comics seems to indicate a basic lack of gravitas and respect toward accountants. Consistent with the point made above about the importance of the work – not the worker – the “turnover” of accountant characters revealed here can be taken to reinforce the longevity of accounting as an aspect of our society that has achieved recognition in this genre of popular literature.

When considering the real or symbolic death of accountants, one could ask if it is not also a way for an artist to take revenge on the constraining business side of their artistic work. Very few characters expressed regret upon an accountant’s death. The extant scholarly literature on superhero comic book artists’ use of characters is scant. However, the point of view of other comic books artists provide some interesting insights: Scott Adams (2008), the creator of the worldwide known comic strips Dilbert, recognized that two of the greatest things about being a cartoonist are “killing people who have demonstrated they deserve it” (p. 182) and “the opportunity to get revenge without risking jail time” (p. 248). Similarly, in the action-based comic book Watson and Holmes #1 (Bollers et al., 2012), when two characters hear on a radio that an accountant has been murdered, one of them expresses no real surprise and goes further: “who hasn’t wanted to kill their accountant at one time or another? It’s all about follow-through.” In the same vein, superhero comic book artist Erik Larsen questions the idea of killing characters, “except if it’s a character I want to kill, of course” (Fingeroth, 2002). Was the accountant he killed in The Savage Dragon #3 (Larsen, 1993) one of his exceptions?

Linkage between the economic context of publishing companies for whom artists work and the image and roles given to accountants is an intriguing topic. The death of accountant characters could be a means to express an artist critique against the bourgeois world (Christensen and Rocher, 2020; Jacobs and Evans, 2012). In that light, accountants may be “scapegoats” more than the real target of artists, who may use them as a stratagem to obscure the artists’ core concern. Similarly, killing the accountant may be a way to generate an image of art for art’s sake (Jacobs and Evans, 2012). Such speculation goes beyond this article’s goal, but it opens up avenues for further research which are broached in the final section together with conclusions to the article and acknowledgment of its limitations.

Conclusion

As noted by Cawelti (1976), “one cannot write a successful adventure story about a social character type that the culture cannot conceive in heroic terms; this is why we have so few adventure stories about plumbers, janitors, or streetsweepers” (p. 6). Accountants and bookkeepers could also have been included in this list. This is consistent with Beard’s (1994) observation that “the vigilante accountant in Brian Garfield’s novel Death Wish is changed to a more credible professional – an architect – in the 1974 movie version” (p. 309). Further and more recent illustration of this can be found when, the US movie The Accountant, had a change of title for its release in France to a less evocative title (Mr. Wolff).

Cultural change is always possible. For Mario and Luigi, the two emblematic fictional plumbers “born” in a Nintendo video game back in the 1980s were turned into US movie heroes in the 1990s and are now famous worldwide. It is the same for accountants as revealed in this study. 11 Indeed, since 2000, accountant characters are playing more positive than negative roles in the superhero genre and have progressively become heroes because of their accounting competencies. Even though their image remains characterized by negative traits, the narrative and thematic roles they play give a more positive impression. While they are not superheroes with superpowers and flashy costumes, their accounting competencies sometimes exceed superhero superpowers. Albeit that the accountants seem to be disposable to the authors of the stories.

There are two ways for the accounting profession to consider the broad results of this study. First is to see the glass half empty: a lot of time is needed before accountants do not appear to be weak and negligible characters, if ever. Second is to see the glass as being half full in that these results show change. According to Smith (2009) who studied the importance of the corporate (wo)man appearing in comics, “Young readers for whom the work sphere is a mysteriously fantastic future world can feel ‘realistic’ about their aspirations (‘I know that I’ll never be able to fly’) while simultaneously ‘settling’ for what is a dream job” (p. 129). The change of roles given to accountants, highlighting the functionality of their craft in society as well as in organizations, participates in such a movement.

This study is not exempt of limitations. The results need to be couched within the caveat that the study sought to contribute to its research question rather than to find the holy grail that may hold the definitive answer that could quench our curiosity. One limitation relates to the chosen genre of comics: superhero. While that choice brought with it notable advantages (refer to section “The study of US superhero comic books genre”), the cultural change identified herein is probably not made at the same rate in every part of the world whereas the data used here is particularly US-centric. Although superhero comic books (and their related movie outputs) are an influential media worldwide, comparative studies focusing on different cultures could lead to different conclusions to those found here. Moreover, as stated by Cawelti (1976),

there are in general two primary ways in which the hero can be characterized: as a superhero, with exceptional strength or ability or as “one of us,” a figure marked, at least at the beginning of the story, by flawed abilities and attitudes presumably shared by the audience. (p. 40)

While the superhero genre is the most developed, it could be interesting to study other kinds of adventure stories, in comic books or in other entertainment media, to test the results of this study. Similarly, other genres, like romance, which were very popular in the 1950s and the 1960s, could also offer interesting insights on past accountant images for a particular type of public (e.g. female adolescent and young women). Furthermore, this article calls for further studies relying first on narrative analysis as well as roles analysis in order to better understand the perceived roles of the accountant in Society.

A further limitation to note relates to usage of Greimas’ actantial model. While its application appears to be useful to understand the roles that accountant characters play in fictions, it is also the target of several criticisms. It has been argued elsewhere that by relying solely on the roles’ oppositions, this approach does not explain the psychological development of characters and does aid understanding of why some characters are invested with a psychological essence, while others are not (Fokkema, 1991). In addition, concepts of actant and actor do not facilitate recognition of a description, traits, psychological essence, or names as conventionally constitute a character in its full depth. Such criticisms call for further research based simultaneously on traits, psychological characteristics, and roles played in the narrative to fully understand the construction of a character. With respect to this study, it could thus be useful to undertake further research on the specific characters and primary sources identified herein.

Intriguing further research is available in this field. Aligned with the abovementioned conjectures regarding the lack of accountant longevity (refer section “Reflections on 80 years of accountants’ roles in superhero comics”), explicit consideration of comics artists’ motivations in their craft is a topic likely to be fruitful in understanding of the appearance of accountants in superhero comics. Comparisons of changes in the accountant image could also be generated by including other, perhaps allied, professionals such as lawyers, financial advisors, and bankers. From such comparisons, it may be possible to identify further insights about accountants as well as the comparator profession(s) and the motives of the artists. Other comparisons could enlighten the image of accountants where studied in other genres of comics without a superhero present. Genre of comics might also have a relationship with national/regional culture (such as the American centricity of superhero comics used herein); arising, it may be that by varying the genre, insights about cultural impacts on the image of accountants could be yielded.

Why does this research of superhero comics matter? Primarily, it is argued that the answer lies in the revelation that this genre of popular literature is indicating change in the broad image of the accountant – and the craft of the accountant. Accountants are arguably the “human face” of business/commerce and even the neo-liberal public sector. They represent the claims toward evidence-gathering and evidence-based decision-making in business and other goal-seeking entities. It is significant if the accountants’ doings are increasingly seen as being helpful in a popular literature rooted in its history to a Manichean focus on light and dark, good and evil, in our society.

It is not argued that there is a nexus between this history’s findings and the accounting professions’ various national-based strategic efforts to create an image of colorful accountants (Carnegie and Napier, 2010; Jeacle, 2008). However, it is possible that the findings here, together with the remarkable growth of superhero-based entertainment, may portend the beginnings of an epoch-defining change to societal representations of the accounting profession.

Footnotes

Appendix

Thematic roles of accountants in superhero comics.

| Actantial roles | Roles in the plot | Description (“SH” = Superhero) |

|---|---|---|

| Receiver | The scapegoat | The fall guy, the fooled He needs the SH to help him restore the truth, to avenge him if he is dead, to save him if the villain wants to murder him. He often appears at the beginning of the story; he justifies the intervention of the SH. |

| The needful | The SH helps the accountant in his quest (without the accountant’s explicit wish), in response to difficulties he encounters at a given moment (he is threatened by the villain), or when he is captured by the villain. This is an accountant presented as needing help (whether the SH intervenes or not). He often appears at the beginning of the story; he justifies the intervention of the SH. |

|

| Sender | The asker | He calls for the help of the SH. He often appears at the beginning of the story; he justifies the intervention of the SH. |

| Subject | The hero | Several situations must be distinguished: 1. The SH has a secret identity, he is an accountant in everyday life (the accountant is the superhero, but not because of accounting). 2. The accountant is the main protagonist as an accountant. The story turns around accounting matters. 3. The reader follows the life of the accountant (as the primary character), who is confronted by the villain. The superhero is a helper in this case. From the superhero’s standpoint, the accountant would be needful. |

| Modal object | The target | The villain tries to kill the accountant so to prevent revelation of the accountant’s compromising information. At the same time, the SH tries to save the accountant for his information (he is not yet a witness/the SH is mainly trying to retrieve the information). |

| Helper | The information-supplier | The SH or the villain solicits him because of the accounting information he has or is able to have (e.g. The SH needs financial information useful in the fight against crime). |

| The accountant of the villain | The villain solicits the accountant because of his mastery of accounting to manage the villain’s dishonest business. The accountant is needed for crunching numbers. |

|

| The helpful accounting advisor/The financial expert | The accountant is a listened-to advisor. He is perceived as helpful (the SH or the villain sees him as an ally who serves their interests). He has the power to influence the behavior of the SH (e.g. determination of an intermediate quest), and more rarely, the behavior of the villain. Unlike the rules-keeper, the accounting advisor is not seen as constraint. He helps the SH to perceive a financial difficulty and overcome it; or he helps the villain to maximize their money. Unlike the accountant of the villain, the advisor is not limited to bookkeeping or counting money. |

|

| The one who sacrificed himself | The accountant sacrificed himself to help the SH. | |

| The witness | Several situations must be distinguished: 1. The accountant who witnessed the villain’s mischiefs. 2. The accountant testifying during a trial of the villain for whom he was working. 3. The accountant of the villain who witnessed the SH presence. |

|

| The sidekick of the SH | Several situations must be distinguished: 1. Unlike the information-supplier, whose knowledge of accounting is essential, the fact that the sidekick is an accountant does not necessarily matter. It englobes all the characters presented as accountants who help the SH in difficulty (e.g. When the accountant helps the SH to escape, to avoid troubles). 2. The character is a sidekick because of the accounting masteries of the accountant. |

|

| Opponent | The pawn of the villain | Victim of a spell or subject to an experience against his will, the accountant turns into a henchman serving the villain. He is an opponent to the SH that he must fight. Contrary to the henchman, he is acting against his will. |

| The henchman of the villain | Unlike the information-supplier, whose knowledge of accounting is essential, the henchman is an accountant who also fights against the superhero. | |

| The rules-keeper/the forbidder | The accountant is a constraint for the SH because of his ability to enforce rules, requiring the SH to adjust his behavior. The accountant has the power to define what the SH must do/not do, and can be the boss of the SH. Such a role does not exist for the villain. |

|

| The villain | Several situations must be distinguished: 1. The villain turns out to be an accountant. 2. The accountant is a villain because he is dishonest. |

|

| The denigrated accounting advisor | The accountant gives financial advice to the SH or the villain but he is rebuffed, his point of view is not taken into account. | |

| The betrayer | The betrayer steals money from his employer (villain or SH). |

Acknowledgements

This paper has benefited from comments and critiques offered through its presentation at the 2019 Asia-Pacific Interdisciplinary Research in Accounting Conference, Auckland, as well as from Professor Ingrid Jeacle. Mr Paul Kirchner is also acknowledged and thanked for his generous permission to include a copy of his work as Exhibit 1 herein. The insightful and encouraging advice from two anonymous reviewers are also gratefully acknowledged.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Sébastien Rocher acknowledges with gratitude the financial support from the CEREFIGE in the form of copyright payments in association with publication of this article. Mark Christensen acknowledges with gratitude the financial support persuant to ESSEC Business School institutional suport of schollarly research and publication of this article.