Abstract

The article aims to explore ways of theorizing in accounting history research. The article draws on findings originating from a semi-automated text analysis by means of topic modelling of 1,300 accounting history papers published between 1996 and 2015 across six journals most relevant to the discipline. Findings show the presence of a whole range of ways of theorizing at different levels of abstraction (from narrating to conceptualizing to theorizing settings to grand theorizing). Different ways of theorizing tend to be associated not only with specific research objects but also with specific journal types. Overall, both narrating and grand theorizing are relatively decreasing in favour of mid-range theorizing approaches, which seem to be on the rise.

Introduction

A crucial question for accounting scholars engaging with history (or wanting to do so) is how to relate history to theory. There have indeed been growing calls for more theoretical framing in historical research (Napier, 2009), suggesting that accounting/business history and organization and management theory be brought closer together (Kipping and Üsdiken, 2014; Rowlinson et al., 2014). Napier (2009: 40) makes a strong argument for a greater engagement of accounting history research with grand theories, such as ‘neo-classical economics, the ideas of Marx or Foucault, or some other source’, because ‘theory can help the researcher to clarify, even to identify, promising research questions, by suggesting influences, relationships and mechanisms’. However, others have pointed out that discussions on whether we need more theory in accounting history should recognize that there are different ways of explaining a phenomenon and that only a few draw upon some grand theory (Llewellyn, 2003).

Undoubtedly, historical research in accounting has been on the rise over the past 20 years, with an upsurge of historical subjects being investigated, scholars turning to historical research, and considerable developments in debates on methodological issues or differing schools of thought (Carnegie and Napier, 1996; Fleischman and Radcliffe, 2005; Napier, 2001; Parker, 1999). Scholars have extensively reflected on the evolving content and borders of the discipline (Baskerville et al., 2017; Carnegie and Napier, 1996, 2012), mapping areas of research, pinpointing trends (Bisman, 2012; Ferri et al., 2018; Fleischman and Radcliffe, 2005; Fowler and Keeper, 2016; Napier, 2006; Walker, 2008), and exploring patterns and variations in terms of authorship, affiliations, period, country and sectors under study (Carnegie and Potter, 2000; Coronella et al., 2018; Williams and Wines, 2006). One of the most consistent claims of these reviews relates to the issue of theory. Scholars affirm that over time, accounting history research has moved from a rather ‘antiquarian’ approach to rather theoretically informed research questions (Napier, 2009) and theoretical pluralism (Bisman, 2012), and this shift has been portrayed as part of the new accounting history trend (Carnegie, 2014; Gomes, 2008). This allegedly increased theoretical prominence is precisely the object of our study because, despite these claims, it is not clear in which ways accounting historians engage with theory as they craft their studies, that is, how they weave together empirical and theoretical stories out of historical data. In other words, we lack empirical evidence on the uses of theory in accounting history research.

This article intends to describe, categorize and account for the ways of theorizing employed in this field. To do so, we share findings originating from a semi-automated text analysis of 1,300 accounting history papers published over 20 years (1996–2015) across six journals: Journal of Accounting Historians Journal (AHJ), Accounting History Review (AHR), Accounting History (AH), Accounting, Organizations and Society (AOS), Critical Perspectives on Accounting (CPA), Accounting, Auditing and Accountability Journal (AAAJ). Empirically, we used topic modelling (Blei et al., 2003), a semi-automated technique that is used to analyse large corpora of texts based on Bayesian statistics (Hannigan et al., 2019) and which is increasingly employed to review and make sense of the evolution of fields of knowledge (e.g. Antons et al., 2019; Cho et al., 2017; Ferri et al., 2018; Wang et al., 2015).

Our analysis reports on the existence of several research objects and sources of data in accounting history research and – most notably for this study – several ways of theorizing. Differently from previous reviews, we focus specifically on the latter, drawing, as suggested by Carnegie (2019: 525), on Llewellyn’s (2003) levels of theory as a framework to ‘classify a wide array of theories for studying phenomena’ in the field of accounting history research.

We begin by addressing extant debates on the role of theory in historical research, and we introduce our research questions and analytical framework based on Llewellyn (2003). Next, after explaining our methodology, we present our main findings: while briefly reviewing the main research objects of accounting history research, we quickly move to our core issue, that is, an investigation of the main ways of theorizing and their relationship to the main objects of research as they emerge from our analysis.

Debates on theory in historical research

Empirical work and theoretical work

The value of qualitative empirical research in accounting lies in the conceptual framing of organizational actions, events, processes and structures (Llewellyn, 2003). Sound qualitative research is produced by a mix of empirical work and theoretical work. Empirical work is the process of gathering and structuring information about organizational actions, events, structures and processes, and its outcome is the production of empirical stories close to the grassroots of the data. Theoretical work is the act of understanding and explaining those actions, events, structures and processes, that is, the conceptual framing of empirical issues or the process of generating expectations about the world (Llewellyn, 2003; Weick, 1995). The outcome of theorizing is the explanation of empirical phenomena via concepts and relationships between the concepts at higher levels of abstraction.

Writing research is the work (and art) of interweaving the empirical story and the theoretical story towards the construction of an empirically grounded theoretical contribution (Golden-Biddle and Locke, 2007). There are many ways of accomplishing such endeavours. Qualitative researchers in general have long discussed the lack of a boilerplate (Pratt, 2009) for moving from empirical stories to theoretical stories towards sound conceptual contributions, especially when relying on large-scale qualitative process data (Abdallah et al., 2019).

In management and accounting history, in particular, the debate on the relationship between the role of theory and empirical historical data has been even more complicated by the holding of different epistemological views on historical research (Rowlinson et al., 2014). We will briefly review these views in what follows, reflecting on how they differ in terms of understanding empirical work, theoretical work and their connection.

The ‘history as narrative’ view

According to this view, history is essentially a study of the past, which means that the past is an object of research. This takes the form of research that collects examples of old accounting materials and of studying original accounting records or secondary sources such as books and professional journals documenting how accounting was actually undertaken in the past. As such, this view is purported to inform the so-called ‘old accounting history’ (Funnell, 1996).

This type of historical research is mainly done through narratives. Narrative is a means of organizing events and giving them coherence, providing form and giving meaning to the past, while implicitly supplying interpretations and explanations (Parker, 1999). Indeed, a commonly shared assumption underlying this view is that historical empirical evidence is revelatory of historical ‘facts’ (Fleischman et al., 1996), and the researcher’s role is one of discovering, ordering and transmitting such facts.

The researchers’ emphasis is placed on the empirical work: ‘[h]istorians are trained to the virtues of primary source material [. . .]. Historians learn to attend to concrete detail at the expense of general patterns’ (Fleischman et al., 1996: 64). However, this does not mean that theoretical work is not there. According to this view, description is already interpretation. The historical re-enactment, that is, the act of presenting information about past events, actions, structures, and processes (empirical phenomena) by giving them sense, structure and coherence is an act of the researcher’s focus of attention and is therefore in itself an act of theorizing as far as it constitutes the researcher’s explanation of those empirical phenomena.

The ‘history as social science’ view

An alternative view of historical research is concerned with the study of some social phenomenon in the past, which means that the past is essentially the research context rather than the prime object – a subtle but fundamental difference. Researchers sharing this view are primarily concerned with how accounting impacts specific individuals and organizations and more broadly how it impacts society, and they examine events in the past as a means of gaining some insight into current situations. Much of this research has been referred to as the ‘new accounting history’ (Miller et al., 1991), which is interested in understanding how individuals are controlled, restricted and in some cases enabled through the use of records and calculations (Napier, 2009).

This type of research also rests on narratives, but it is typically not limited to the narrative re-enactment of the past. Rather, it encompasses strong interpretations of the social world in the past, often through specific theoretical lenses borrowed from other fields of social science research.

The main assumption is that past events recorded in documents should be treated as primary sources of empirical evidence and that they do not constitute objective historical ‘facts’ (Napier, 2009). The implication is that the same historical event can be explained in very different ways, depending on the interpretive lens that is employed, therefore leading to a range of potential narratives and counternarratives (Funnell, 1998).

In balancing empirical work and theoretical work, research embracing this view tends to prioritize theoretical work, dedicating extra effort to noticing general patterns and generating explanations at higher levels of abstraction. Empirical work is obviously there but is less in the foreground: the role, importance and use of careful and extensive archival research are often marginalized in favour of the theoretical story (Fleischman et al., 1996).

Indeed, scholars have noted that the upsurge of the ‘new accounting history’ has come with a larger engagement with established theories from the social sciences (historical and methodological pluralization – Modell et al., 2017), with a strong prevalence of some critical paradigms, such as Foucauldian and Marxist analytical lenses (Fleischman et al., 1996; Napier, 2009).

Moving beyond dichotomies: different shades of theory

Any debate tends to polarize approaches into opposing mainstreams for the sake of conceptual clarity and analytical reflection, such that it may appear that a scholar who wishes to engage with historical research in accounting, is left with two main alternatives. Luckily, actual historical research is less black or white, as per the relationship between empirical and theoretical work.

As acknowledged by Carnegie (2019), Llewellyn (2003) has made an influential contribution to the uses of theory in qualitative accounting research that can be extended to accounting history research. Llewellyn’s (2003) main claim is that there are different levels of theorizing. Theory, or rather theorizing, reflects the act of giving meaning and significance to social and organizational life. Giving meaning is achieved by means of developing concepts and creating connections between elements. Giving significance is an act of elaborating on those relationships by explaining them more generally, and significance may differ across cultural and historic contexts.

These acts can be done at different levels of engagement with empirical issues in a continuum that ranges from very micro-theorizing, with maximum adherence to empirical issues (aimed at giving meaning to understand specific phenomena), to very macro-theorizing, with a maximum level of abstraction from the empirical issues (aimed at giving significance and therefore explaining general patterns – see also Layder, 1994). Llewellyn (2003) punctuates this continuum with the five main levels illustrated in Table 1.

Llewellyn’s (2003) levels of theory (authors’ elaboration).

The first level deals with the birth of concepts from a close understanding of empirical phenomena, resting on micro-levels of analysis (individuals, micro-actions and micro-processes). The mid-range level deals with concept elaboration via local explanations and the creation of meaning and significance, linking micro- and macro-levels of analysis. The higher order level deals with the networking of concepts into more abstract theories at macro levels of analysis (focusing on structures, patterns and regularities).

Relating this framework to accounting history, one may position the two main views reviewed above (history as narrative and history as social science) at the two extremes of this continuum. However, the core message of this framework is that anything that comprises this continuum is a form of theorizing, albeit at different levels of abstraction. To advance the debate on theory in accounting history research, we may therefore ask where the bulk of accounting history research is positioned across these ‘shades of theory’.

Drawing on these considerations and on Llewellyn’s (2003) framework, our goal is therefore to empirically explore the uses of theory in accounting history, describing, categorizing and accounting for them in previous research. In particular, we ask: How is accounting history theorized? Are different ways of theorizing associated with different research objects?

Methods

Sampling

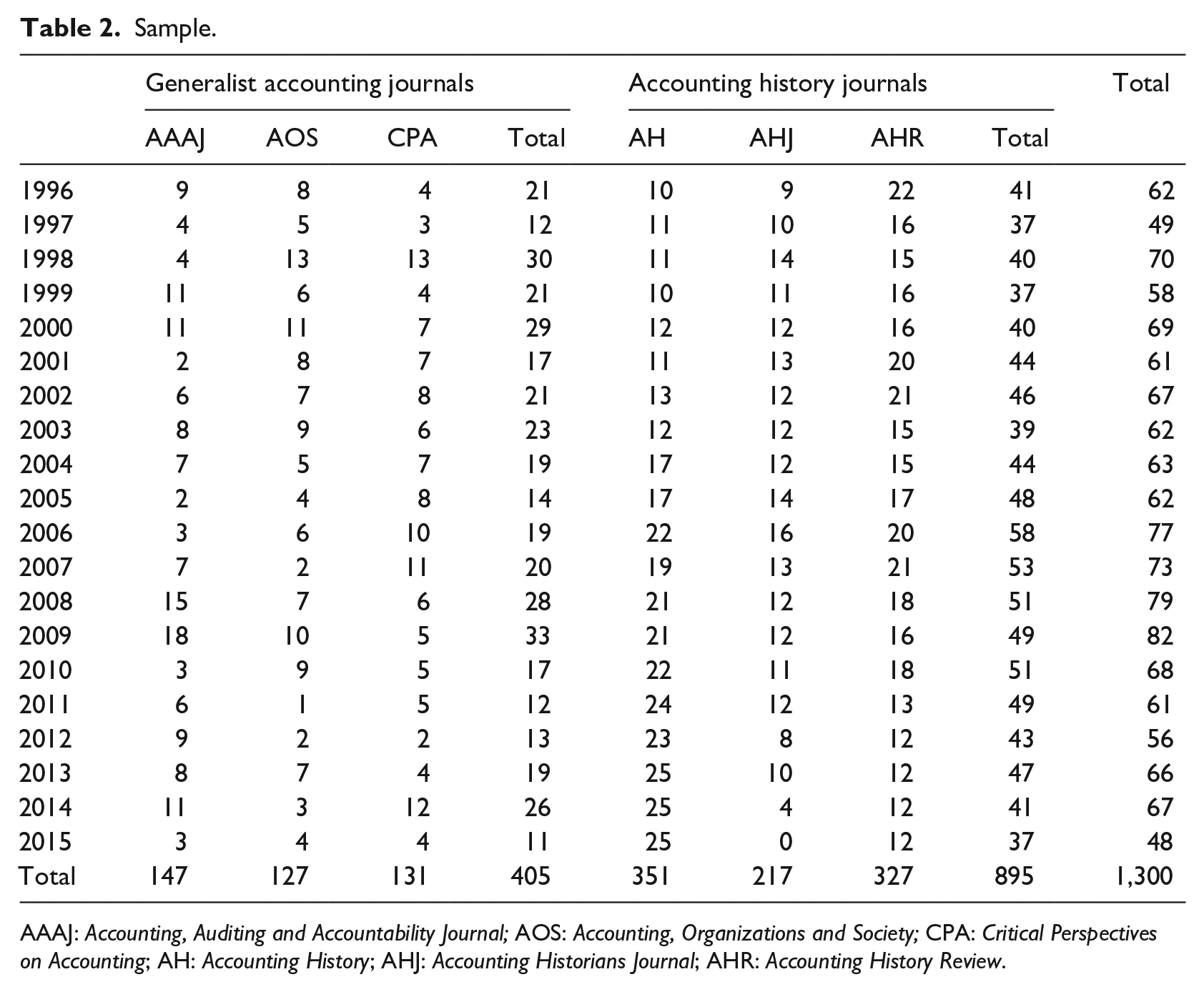

We downloaded accounting history articles published from 1996 to 2015 in six distinct journals: Accounting Historians Journal (AHJ), Accounting History Review (AHR – Accounting, Business & Financial History until 2010), Accounting History (AH), Accounting, Organizations and Society (AOS), Critical Perspectives on Accounting (CPA) and Accounting, Auditing and Accountability Journal (AAAJ). Before 1996, AH, one of the journals of our sample, did not exist. This outlet is particularly relevant for our study, as it reports a list of accounting history publications on a yearly basis that was used to pinpoint relevant additional papers to be included in the study.

In our sample, three journals specifically focus on accounting history: AHJ, AHR and AH. For these journals, we downloaded all the articles from the journals’ websites, excluding book reviews, calls for papers, publication lists/ad hoc referees lists and announcements. Moreover, we relied on the Accounting History Publication lists published annually in AH and AHR to add to our sample other relevant accounting history papers published in more generalist accounting journals: AOS, CPA and AAAJ. We focused on these generalist journals for their commitment to publishing accounting history research on a continual basis (Gomes et al., 2011; Matthews, 2017; Parker, 1999). For each paper in our sample, we also kept track of the authors, their affiliations and whether the paper was part of a special issue. We used this information later on for interpretation. Overall, our corpus is composed of 1,300 papers 1 : descriptive data are presented in Table 2.

Sample.

AAAJ: Accounting, Auditing and Accountability Journal; AOS: Accounting, Organizations and Society; CPA: Critical Perspectives on Accounting; AH: Accounting History; AHJ: Accounting Historians Journal; AHR: Accounting History Review.

Analysis

We analysed our data with topic modelling, a semi-automated content analysis technique, based on an algorithm of a Bayesian statistic called Latent Dirilecht Allocation (LDA: Blei et al., 2003). Topic modelling has been increasingly used in management studies for detecting novelties, developing inductive classification systems, understanding online audiences, analysing frames and understanding cultural dynamics (Hannigan et al., 2019). Topic modelling proved to be particularly useful for analysing the evolution of an academic journal (Antons et al., 2019; Ferri et al., 2018; Wang et al., 2015) or a field of knowledge (see Antons et al., 2019, for the field of innovation or Cho et al., 2017, for marketing) because, compared with traditional literature reviews, topic modelling is able to deal with a large corpora of data and discover less visible structures of meanings.

Topic modelling automatically codes the content of texts into a set of ‘topics’ that are containers of meaningful words (Mohr and Bogdanov, 2013), which often co-occur together in analysed documents. The researcher then inductively interprets topics. Therefore, documents pertaining to a corpus are conceptualized as a mix of different topics, and each text is defined by a particular topic distribution (Antons et al., 2016). Topic modelling permits an inductive interpretation of results and an easier reproducibility of the analysis while being able to deal with big textual data. Additionally, and more importantly, topic modelling is able to deal with polisemy: the same word can have different meanings in different contexts, as its meaning depends on the surrounding words (DiMaggio et al., 2013). Topic modelling is better suited for our purposes than traditional literature review techniques (Massaro et al., 2016), as it recognizes that papers comprise different topics and does not force univocal categorizations. For analysing our data with topic modelling, we used Mallet, a state-of-the-art software for this purpose (Hannigan et al., 2019). In the following sections, we detail our analytical and interpretive steps.

Modelling

Before analysing our data, we had to pre-process our corpora to ‘clean’ the data. First, we transformed all the papers into simple text files through conversion and (rarely, when needed) through the OCR software. Second, we retained only the meaningful part of each article: we removed the authors’ names and affiliations, the acknowledgements and the reference lists, as these parts would have produced ‘statistical noise’ (Antons et al., 2016: 731). Finally, we developed a stopword list, which is the list of the words that the software has to ignore, including English articles, prepositions, adverbs and other words with scarce substantive meaning. We choose not to stem the words in our corpus, as this operation distances the elicited topics from the original articles. As inferring meaning depends on the context created by the corpus (Hannigan et al., 2019), we extensively used the original articles to interpret topics, as we detail below. Finally, after removing stopwords, our corpus consisted of 5,978,800 words.

The algorithm asks for the number of topics to be elicited. This is a very sensible issue in topic modelling: some scholars ask the statistical analysis to determine the optimum number of topics (i.e. Mimno et al., 2011), while others highlight that topic models that have better quantitative metrics are judged as less meaningful by human experts (Chang et al., 2009). Indeed, DiMaggio et al. (2013) point out that ‘when topic modeling is used to identify themes and assist in interpretation [. . .], there is no statistical test for the optimal number of topics’, DiMaggio et al. (2013) suggest that the choice of a model should be driven by interpretative and analytical purposes only. Therefore, as we detail below, we produced several models and analysed their interpretability, analytical power and validity (Hannigan et al., 2019), comparing the meaning that we inferred for topics to articles mostly coded with those topics. Following an established procedure, we asked the algorithm to produce models with 15, 20, 25, 30, 35, 40 and 45 topics. Each model produced three main outputs:

A list of the most important words for each topic, where the prevalence of each word within a topic is adjusted for its prevalence within the corpus as a whole. Appendix 1 presents the 30 most important words for the 30-topic model.

A detailed list of the coding of each word within each paper, which we used in the inductive phase.

A ‘paper per topic’ matrix detailing the topic composition (or loading) of each paper. Thanks to this output, it is possible, for instance, to observe that in the 30-topic model, Bigoni and Funnell (2015) is composed of Topic 19 (65.5%), Topic 8 (18.3%), Topic 18 (6.2%) and so on. The output allows us to calculate the prevalence of each topic throughout the sample.

For each model, we independently analysed these outputs. In particular, we focused on the three most representative papers for each topic (we looked at 45 papers for the 15-topic model, 60 for the 20-topic model and so on) and also analysed the detailed coding of each word when needed. Each of the three co-authors analysed models independently, making a first attempt at labelling the topics produced. Upon discussion, we agreed that the 15- or 20-topic models produced topics that were too aggregated and, therefore, difficult to interpret in a univocal way. Conversely, the 45-topic solution created topics that were too specific, with too much overlap. We preferred the 30-topic solution over the 25-topic solution because the former permitted the emergence of topics that were easier to interpret, which were collapsed together in the 25-topic solution. We also tried the 31-topic and 29-topic models, but they did not improve our understanding. Therefore, we chose the 30-topic model and interpreted it as described in the following section.

Interpreting

Starting from the outputs of the 30-topic model, we then engaged in the interpretive work aimed at deepening our understanding of topics and refining the topic labels. From a practical point of view, each author had a panoply of data for interpreting topics: first, each one started from the three already described outputs (see the list of most important words and the three most important articles for each topic in Appendices 1 and 2, respectively). Additionally, we ran descriptive analyses to improve the sense-making phase. First, we identified the yearly prevalence of each topic for the period 1996–2015. Second, we analysed the differential prevalence of topics in the six different journals and in the generalist versus specialist journals. Third, we compared topic usage by author with different affiliations (i.e. scholars based in Europe vs scholars based in Australia and New Zealand). Finally, following Ferri et al. (2018), we analysed the usage of topics in the papers pertaining to our corpora and determined the quantitative indicators reported in Table 3 as follows:

The average prevalence (or loading) describes the presence of each topic across the sample. Large topics correspond to recurrent discourses (i.e. Topics 8, 7 and 21), while smaller topics suggest seldom-discussed issues (i.e. Topics 17, 22, 28);

The number of papers in which a topic is the most ‘used’ or the most important one in absolute terms (fourth column) and percentage wise (fifth column);

The number of papers in which a topic is the second- or third-most important in absolute terms (sixth column) or percentage wise (seventh column). These figures were developed from the paper per topic matrix. For instance, Topic 4 is the most important topic in 27 papers (equal to 2.1% of 1,300) and the second or third-most important topic in 20 papers (equal to 1.5% of 1,300). If read together, these two indicators give insights into topic usage (Ferri et al., 2018): a topic that is the most important one more often than it is ranked second or third is a focused topic, highly concentrated in a few papers, but not significantly present in all the others (i.e. topic 10). Conversely, a topic that appears often as the second or third most important topic suggests a more general, distributed discourse. For instance, Topic 8 is the second or third topic in many papers included in the sample (66.5% of the articles).

Topics and clusters of accounting history research.

Categories developed in prior studies (i.e. Bisman, 2012; Carnegie and Napier, 1996; Edwards and Walker, 2009; Fowler and Keeper, 2016; Previts et al., 1990; Walker, 2008; Williams and Wines, 2006) reinforced our analysis. Independent analysis was followed by an in-depth discussion during which divergences regarding the interpretation of topics were solved. In this phase, it became apparent that not all the data that informed our interpretation were always equally relevant. For some topics, the word list did suffice to suggest an interpretation. In other cases, more insights were gained from reading the most relevant papers to assess the context of the most relevant words. Sometimes trends played a crucial role in the interpretive process, as peaks corresponded to special issues on specific topics. In the most difficult cases, we proceeded by ‘testing’ tentative interpretation hypotheses against multiple evidence (the papers, the trends) or by comparing topics two-by-two as if they were different sides of the same discussion. In our presentation of the topics below, we will share this process with the reader as much as possible.

By combining qualitative and quantitative analyses and moving back and forth between the categories developed in prior studies, we were able to develop and progressively refine the interpretation of each topic and label them in a possibly univocal way. Once we were confident with our interpretation of the topics, we qualitatively clustered them based on similarities in terms of content and quantitative features (Boyatzis, 1998; Fereday and Muir-Cochrane, 2006).

Findings

To address our questions, a preliminary analysis is needed to make sense of the main research objects of the whole bulk of accounting history research under analysis. Table 3 displays, starting from the left, the emerging 30 topics with their ID and indicators, their differentiation in higher order thematic clusters and their aggregation in overarching categories (research objects, sources of data and ways of theorizing).

The category research objects comprises 21 topics aggregated into five thematic clusters, namely, Financial accounting (Topics 2 and 26); Public sector (4, 7 and 13); Profession (0, 5, 22 and 15); Regulation (3 and 20); Geographical focus (10 and 24); Specific thematic debates (12, 14, 16, 17, 19, 27, 28 and 29).

The category sources of data comprise two topics: Analysing documents (Topic 9) and Analysing the accounts (Topic 23).

The category ways of theorizing comprises seven topics aggregated by level of theory: Cost accounting concepts (Topic 1); Critics of capitalism (Topic 6); Narrating history (Topic 8); Financial accounting concepts (Topic 11); Counternarratives (Topic 18); Context-based explanations (Topic 21); and Statistical modelling (Topic 25).

Exploring research objects and sources

The topics included in this section refer to the issues of accounting studied in this body of research. Exploring the topical areas covered by this literature is a prerequisite for addressing our core research questions about the ways of theorizing. A description of the two topics referring to the sources of data is also included in this section.

Topics focusing on research objects share the following quantitative features: they are many (21 out of 30) and have a relatively low average prevalence. Almost all thematic topics appear to be the most important topics more often than they are ranked second or third. They are, therefore, highly concentrated in a few papers, but not significantly present in all the others. For space reasons, we describe only three of the clusters elicited: ‘Financial accounting’, ‘Public sector’ and ‘Specific thematic debates’.

Financial accounting: Topics 2 and 26

Two topics deal with financial accounting areas of research in the corpus of English-speaking accounting history literature: ‘Shares and shareholders’ (Topic 2) and ‘Financial accounting treatises’ (Topic 26).

Topic 2 (‘Shares and shareholders’) reflects, in general, discourses about how dividends are calculated and shared. As shown in Appendix 1, the topic is dominated by words such as shareholders, capital, dividends and stock. In addition, the three articles in which this topic is most prevalent (approximately 60% of the paper’s text is coded as ‘Topic 2’ as shown in Appendix 2) offer historical analyses of the relationship between dividends and depreciation (Pitts, 1998a), share valuation and corporate governance (Pitts, 1998b) and between investments and related returns among coal companies (Jones, 2010).

Topic 26 captures a very specific area of interest: the content of accounting treatises and the context in which they were written. Beyond the keywords, what is particularly effective for interpreting this topic is the list of the three papers in which topic 26 is more present. These papers refer to a debate about the market of Luca Pacioli’s Summa de Arithmetica and were all published in the Accounting Historians Journal (Sangster et al., 2008, 2011; Yamey, 2010).

Public sector: Topics 4, 7 and 13

The public sector cluster comprises the topics ‘Taxation’ (4), ‘Public sector governance and accountability’ (7) and ‘Education and healthcare’ (13). Words such as government or state are shared by the three topics. However, theme-specific words such as tax or taxpayers (Topic 4 – ‘Taxation’), local, reform, or national (Topic 7 – ‘Public sector governance and accountability’), and hospital, care, education (Topic 13 – ‘Education and healthcare’) are present.

The content of most coded articles under each topic included in this cluster can strengthen our labelling further. The most coded article under Topic 4, ‘Taxation’, provides an analysis of the role of natural law tax theory in Germany from the mid-1600s to early 1800s (Treisch, 2005). The paper by Miley and Read (2013) studies the interplay between the national and local government in the aftermath of natural disasters in New Zealand, and 56 per cent of its text is coded under Topic 7, which we named ‘Governance and accountability’. Fowler (2010: 338) investigated the ‘financing, accounting and accountability practices instituted by Nelson settlers in a not-for-profit community-based school system’. As such, 52 per cent of its text is coded under Topic 13, which partly deals with the role of accounting in education.

Specific thematic debates: Topics 12, 14, 16, 17, 19, 27, 28 and 29

This cluster includes seven small and highly focused topics. Topic 12 – ‘Military’ – covers army-related terminology (officers, soldiers, navy), and it is highly associated with the works of Warwick Funnell. Topic 14 (‘Insurance’) captures parts of texts discussing the insurance industry: 70 per cent of Keneley’s (2001) paper ‘The evolution of the Australian life insurance industry’ is coded under Topic 14. Topic 16, ‘Gender’, includes terms referring to gender issues: women, female, married, domestic. Topic 17 is the smallest of the 30 topics developed by the model and refers, in our view, to ‘Trade’. Indeed, two out of the three articles in which this topic is most heavily represented discuss fur trading at Hudson’s Bay Company (i.e. Spraakman, 1999). Topic 19 concerns discussions about ‘Religion’, as suggested by terms such as church, Islamic, God. Topic 27 ‘Corporate Social Responsibility’ (CSR hereafter) is dominated by words such as environment and report or disclosure. Topic 28, ‘British empire and colonialism’, is not only very small (mean weight of 1.4%), but it is also highly associated with the works of Dean Neu on how ‘accounting discourses and techniques were located within the logic of imperialism and enmeshed within colonial systems of government’ (Neu, 2000: 163). Not surprisingly, authors with an Australian, New Zealand, North American or British affiliation are strongly associated with Topic 28, ‘British empire and colonialism’. 2 Finally, Topic 29 characterizes papers or parts of papers that synthesize the previous accounting history literature. We therefore labelled the topic ‘Explaining the literature’. Looking at the words associated with this topic, the terms articles, journal(s), authors, published, publication and issue denote that the object of this topic is the literature itself.

Sources of data

For the sake of completeness, we present here the two further topics that, differently from the ones presented so far, are characterized by being spread across a high number of papers, while seldom being featured among the first topics in a paper. This suggests that these are topics that do not identify any specific research object but are transversal to many of them. Our interpretation of the wordlist coupled with a reading of the papers made us conclude that these topics capture words associated with sources of data used in accounting history papers. Topic 9, ‘Analysing documents’, characterizes papers that draw upon letter, minutes, proposals to analyse different events of relevance, referring also to the time when the documents were issued (June, March) and to the senders or receivers of the documents (board, chairmen, committee). On the other hand, Topic 23, ‘Analysing the accounts’, characterizes papers in which the sources of data are financial accounts, which are then analysed for purposes ranging from understanding the technicalities of financial accounting (Noke, 1996) to investigating the socio-economic conditions of specific groups (Bloom and Solotko, 2008).

Exploring ways of theorizing

Topics included within this section can be related to Llewellyn’s (2003) framework of levels of theory, as we will show, and share the following distinctive quantitative features: their mean prevalence across the corpus of a text is larger than topics relating to research objects (6.0% vs 2.4%), and they are often the second or third most important topic in the papers. Theory-related topics are not mutually exclusive: more than one theoretical topic can be present within the same paper but usually one is more present than others. After justifying our interpretation of each of these topics, we comment on their distribution across journals and their dynamics over time.

Narrating – Topic 8

Topic 8 is the largest topic in our corpus of text (14.7% of words are coded under Topic 8) and the second or third most important topic in 865 out of 1,300 papers. Topic 8 characterizes parts of the papers in which narratives are used by accounting historians to give ‘coherence to generically related historical events’ (Funnell, 1998: 145) or to make ‘facts comprehensible by identifying the whole to which they contribute’ (Polkinghorne, 1988: 18, quoted in Funnell, 1998). Topic 8 comprises verbs such as means, following, concerned, suggested and adverbs such as generally, certainly, largely that together reflect the efforts made by authors to transform a chronology into a consistent narration. Topic 8, ‘Narrating’, is employed to structure a discourse that identifies and ties together a beginning to a conclusion, also emphasizing the changes and reactions in between.

In terms of levels of theorizing, Topic 8, ‘Narrating’, mirrors attempts at understanding rather than at explaining a specific phenomenon. For Llewellyn (2003), understanding is likely to employ a lower level theorization, which links the unfamiliar to the familiar via the time and space positioning of an event, which is what Topic 8 does.

Conceptualizing: Topic 1, ‘Cost accounting concepts’, and Topic 11, ‘Financial accounting concepts’

Topic 1, ‘Cost accounting concepts’, comprises words used to describe costing techniques (cost, standard, rates), cost objects (workers, machine, manufacturing), and the locus of the analysis: the company or the factory. Topic 11 (‘Financial accounting concepts’) instead captures discussions about financial accounting concepts (income, asset, depreciation, valuation).

One could claim that these two topics represent research objects rather than ways of theorizing. However, we decided to consider Topics 1 and 11 as theoretical topics for two main reasons. First, the two topics are often the second or third most important, thus suggesting that they complement rather than substitute research-object topics. Second, as Llewellyn (2003) suggests, discourses introducing new concepts or refining the meaning of existing ones can be considered theoretical, although at a lower level compared with grand theories. Moreover, for the same author, this level of theorizing implies a focus on the agency of actors rather than on structural elements.

Papers showing a relevant presence of Topic 11, ‘Financial accounting concepts’, represent a good example of concept development or refinement conducted by investigating the agency of specific actors. Coded 70 per cent under Topic 11, Schultz and Johnson’s (1998) study on the shifting theoretical concepts and concerns relating to income tax accounting highlights the role of The Committee on Accounting Procedure, the Accounting Principles Board, and the Financial Accounting Standards Board. Moving to Topic 1, ‘Cost accounting concepts’, Vent and Milne’s (1997) paper focuses on the development of costing concepts, focusing on the agency of precious metal mining companies. Hence, Topic 1 (‘Cost accounting concepts’) reflects efforts to theorize the practices and technicalities of cost accounting.

Theorizing settings – Topic 21, ‘Context-based explanations’, and Topic 25, ‘Statistical modelling’

The topics included within this section can be understood as examples of what Llewellyn (2003) would call level 4 theorizing or theorizing settings. Level 4 theorizing works with a network of concepts rather than with single concepts. In addition, authors employing this level of theorizing are mostly interested in investigating the relationship between social actors and their environment, focusing on the conditions under which agents pursue their actions. When theorizing settings, the focus moves from understanding the constitutive features of a phenomenon to providing systematic explanations of the effects of X on Y. There are two topics that can be associated with this distinctive way of theorizing: Topic 21, ‘Context-based explanations’, and Topic 25, ‘Statistical modelling’.

Topic 21 is the second largest topic emerging from our model (the mean weight across all texts in the sample is 10.5%), and it is the second or third most important topic in almost a third of the papers. In our view, this topic reflects contextual explanations of the emergence, development or demise of accounting practices, especially in the field of management accounting. Indeed, some of the topic words relate to practices (control, performance), while others suggest an interest in contextual elements that, however, operate at different levels (organizational, social, institutional, environment). The term change also characterizes the topic, thus suggesting an interest in the evolution of accounting practices. In contrast to the papers analysed thus far, studies showing a high presence of Topic 21 explicitly acknowledge their theoretical framework, which draws on actor network theory (ANT), neo-institutionalism, contingency theory or a mix of these. Despite differences, the three theories share a common interest in taking into account contextual features, in the form of networks of relations, institutional pressures or contingent elements (Lounsbury, 2008; Modell et al., 2017).

The heterogeneity of theoretical approaches within Topic 21 is well represented by the articles most coded for this topic. Beaubien’s (2013) paper (74%, Topic 21) analyses the deployment of an ERP control system by drawing on ANT and institutional theory. On the other hand, Van der Steen’s (2009: 736) study on management accounting change is informed by ‘the institutional view on management accounting change’. Last, Chenhall and Moers (2015) draw on the prior literature to show the relationship between innovation demands at the environmental level and variations in management control systems, thus applying the contingent argument of ‘fit’ to the study of change.

Topic 25 is the smallest topic relating to ways of theorizing, accounting for only 2.1 per cent of the words in our texts. The topic is highly relevant among quantitative papers using statistical analytical tools, such as Person’s correlation (Shields and Shields, 1998) or moderated regression analysis (Hartmann and Moers, 1999), to investigate antecedents and consequences of a specific phenomenon. The most relevant words within Topic 25 are variable, sample, statistical and model. We decided to label this topic ‘Statistical modelling’ because it characterizes parts of papers where concepts are tied together to construct a broader schema based on statistical assumptions, which are then tested on a selected sample. In addition, the focus on causal explanation is explicit in papers showing a high presence of Topic 25.

Grand theorizing: Topic 6, ‘Critics of capitalism’, and Topic 18, ‘Counternarratives’

Grand theorizing implies understanding agency largely in terms of social conditions, which are regular, impersonal and large scale, and trying ‘to explain everything in terms of a comprehensive framework of concepts’ (Layder, 1994: 104). Although there are no pure grand theorists in the accounting field, for Llewellyn (2003), there are examples of authors ‘borrowing’ concepts or ideas from grand theories and applying them to the discipline. This implies bringing grand theories down to lower levels of theorizing, such as theorizing settings and conceptualizing. In our topic modelling-based investigation of the accounting history field, we observed two examples of this kind of approach.

Topic 6 is small (the mean prevalence across the texts is 1.5%) and focused (when present, it is usually the most important topic). We called Topic 6 the ‘Critics of capitalism’, as it mirrors the view of authors who, despite their undeniable differences, have much in common in their understanding of modern capitalism: Marx and Weber. Central terms within the topic are capital, labour and workers and, significantly, Marx and Weber. In our view, Rob Bryer takes the work of Marx down to level four (‘theorizing settings’) when he theorizes the role of landlords in the English Agricultural Revolution (Bryer, 2004). Similarly, Toms (2010) – 51 per cent Topic 6 – is a historical survey of profitability calculations in the context of developing capitalism informed by the theories of Weber and Sombart and by Bryer’s readings of Marx.

Larger and more diffused than Topic 6, Topic 18 features papers or parts of papers where critical perspectives on accounting are discussed and contrasted with the traditional accounting history approach. It includes terms such as discourse, critical, power and, more significantly, two author’s names: Foucault and Miller, the latter arguably being one of the authors who has contributed the most to diffusing the Foucauldian approach in the accounting field (Burchell et al., 1991). The topic is included among grand theories, as it is characterized especially, but not exclusively, by Foucauldian concepts. For instance, Kim’s (2008) critical study on the oral history method (coded 70% under Topic 18) frequently refers to the work of the French philosopher on the relationship between a writer and a reader. However, it would be reductive to consider Topic 18 as evidence of discourses featuring a strict application of Foucauldian theories. Papers with a high presence of Topic 18 reflect, either directly or indirectly, the legacy of a theoretical contribution that has provided an ‘antidote to positivistic/scientific explanations of accounting’ (Stewart, 1992: 61). To demarcate the ‘inspirational’ rather than substantial role of Foucault, we decided to label Topic 18 as ‘Counternarratives’. For Funnell (1998: 144) by producing counternarratives, new accounting historians aim at challenging the ‘naturalness and apparent neutrality of the narrative as a technique for writing accounting history’ and at unmasking the relationships of power that lies behind accepted or familiar ways of connecting historical events.

We can now compare the ways of theorizing in terms of their presence across the journals included in the sample and their dynamics over time (see Table 4). While there is no difference in the presence of Topic 8, ‘Narrating’, across journals, the use of concept theories in accounting history characterizes specialized journals, namely AHR by cost accounting concepts and AHJ by financial accounting concepts. On the other hand, papers published in generalist journals usually draw on higher levels of theorization: topics relating to theorizing settings (Topics 21 and 25) and grand theorizing (Topics 6 and 18) strongly characterize AOS, AAAJ and CPA.

Distribution of ways of theorizing by journal.

AAAJ: Accounting, Auditing and Accountability Journal; AOS: Accounting, Organizations and Society; CPA: Critical Perspectives on Accounting; AHR: Accounting History Review; AH: Accounting History; AHJ: Accounting Historians Journal.

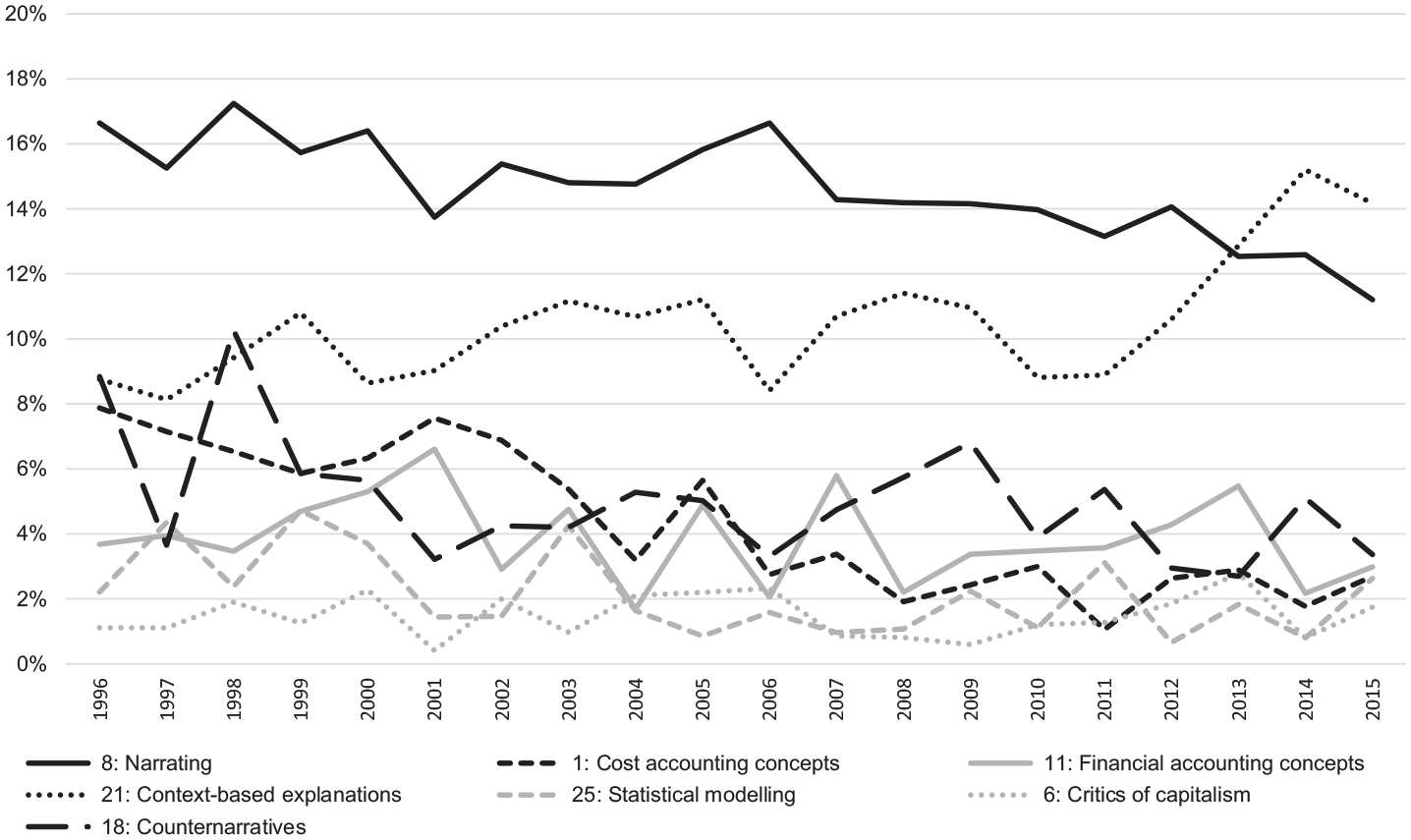

Figure 1 presents the prevalence trend over time for topics included in ‘ways of theorizing’. Values are calculated as the average prevalence of each topic for each year over our corpus and are thus independent of the number of articles published yearly. All but Topic 6, ‘Critics of capitalism’, and Topic 21, ‘Context-based explanations’, decrease in the period under analysis. The demise of Topic 1, ‘Cost accounting concepts’, is particularly dramatic: the topic decreases from 8 per cent in 1996 to 2.7 per cent in 2015. Additionally, Topic 11, ‘Financial accounting concepts’, decreases but in a lighter way. Hence, the demise of the ‘technical core of accounting’ is not just a matter of research objects but also of theoretical development. Topic 18, ‘Counternarratives’, is one of the most present topics at the beginning of the period under analysis, with a 10 per cent peak in 1998. Fifteen years later, its presence is reduced to less than 3.5 per cent. This trend could be related to the fact that the formulation and diffusion of the counternarrative approach happened during the 1990s, becoming somehow taken for granted in later stages. Additionally, Topic 25, ‘Statistical modelling’, largely decreases.

Trend over time for ‘ways of theorizing’.

It is interesting to compare the trends of Topic 8, ‘Narrating’, and Topic 21, ‘Context-based explanations’, as they are the largest topics among the 30 topics developed by our model. Topic 8 is larger than Topic 21 from 1996 to approximately 2010. Then, Topic 8 starts decreasing, with Topic 21 following the opposite trend; by 2013, Topic 21 overtakes Topic 8, also becoming the largest topic overall. Based on this trend, it could be argued that ways of connecting facts have become more theoretically informed over time. However, rather than assisting a pluralization in ways of theorizing, the data suggest a convergence towards theoretical frameworks explaining the role of contextual elements, either from an ANT, an institutional or a contingent perspective.

The relationship between research objects and ways of theorizing

The last step of our analysis investigates the association between topics representing ways of theorizing and topics representing research objects.

We focused on the three most important topics for each of the 1,300 papers that we analysed, since on average, they account for 72.7 per cent of the content of each paper. We then calculated how many times topics representing ways of theorizing co-occurred with topics representing research objects (Figure 2). For example, in 84 per cent of the cases in which ‘Military’ features among the first three most important topics, Topic 8, ‘Narrating’, is also present. Conversely, Topic 8, ‘Narrating’, co-occurs with Topic 20, ‘Accounting standards’, only in 35 per cent of the cases in which ‘Accounting standards’ appear in the three most important topics. For each research object, thus, Figure 2 reports the percentage of co-occurrence with a way of theorizing. Black bars highlight the standard deviations: the histogram in green signals the co-occurrences that happen more often than the average plus a standard deviation, while the histogram in red signals the co-occurrences that happens very rarely.

Association between ways of theorizing and research objects.

The above-displayed co-occurrences show that accounting history is a field of many ‘shades’, encompassing areas of research that are based on narratives as the main theoretical mechanism; areas of conceptual development that are nevertheless still strongly grounded in empirical description; areas of theorized settings strongly concerned about explaining how social conditions for practices emergence or change; and ultimately, areas of more abstract grand theorizing, as presented in what follows.

Narrated histories

For Funnell (1998), the ‘narrative has been accepted as the unavoidable, natural means of writing history and the preferred vehicle for accounting histories’. Our data reflect this status quo as Topic 8, ‘Narrating’, is almost always among the most important topics in a paper, irrespective of the research object. It must be emphasized, however, that four research objects are almost exclusively characterized by a narrative approach: ‘Military’ (Topic 12), ‘Financial accounting treatises’ (Topic 26), ‘Taxation’ (Topic 4) and ‘Microhistories of accountants’ (Topic 15). This suggests that alternative, higher level ways of theorizing are missing in these debates.

Areas for conceptual development

Figure 2 shows that some research fields have contributed more than others to concept development in the fields of financial and cost accounting. Reassuringly, topics often used to theorize financial accounting concepts are less frequently used to develop cost accounting concepts, and vice versa. The understanding of financial accounting concepts is highly intertwined with discussions about accounting standards, CSR and shareholders. Arguably, these debates centre upon the rules, practices and users of financial disclosure, respectively. On the other hand, the investigation of cost-accounting concepts seems much indebted to studies conducted among Italian, Spanish and French organizations such as the Venice Arsenal (Zambon and Zan, 2007) or the Royal Tobacco Factory of Seville (e.g. Carmona et al., 1997) and to studies on trade in North America (e.g. Spraakman, 1999). Consistent with Llewellyn’s (2003) expectations about the use of concept-based theorizing, the aforementioned studies deal with ‘emergent’ and ‘discontinuous’ phenomena, that is, the emergence of cost accounting at the Venice Arsenal – rather than with patterned regularities.

Theorized settings

Topic 21, ‘Context-based explanations’, is consistently present in papers dealing with public sector settings such as ‘Public sector governance and accountability’ (7) and ‘Education and healthcare’ (13). Indeed, research on these topics often entails investigating the interplay between organizations and the structures that surround them rather than issues of individual agency, which explains the engagement with context-based explanations at relatively higher levels of abstraction.

As already discussed, the presence of statistical modelling is marginal in accounting history and limited to CSR and systematic literature reviews.

Grand-theorized fields of research

Topic 6, ‘Critics of capitalism’, is so small that peaks in Figure 2 can be explained by referring to specific papers on accounting and religion (i.e. Funnell and Williams, 2014).

As a way of grand theorizing, Foucault-inspired counternarratives are more diffused than Marxian or Weberian critics of capitalism. These counternarratives inform studies on ‘British empire and colonialism’, ‘China’ and ‘Taxation’ and are especially employed to review the literature. Indeed, the high co-occurrence between Topic 18, ‘Counternarratives’, and Topic 29, ‘Explaining the literature’, can be related to one of the specific aims of new accounting history, that is, to ‘contradict the traditional stories of accounting history’ (Funnell, 1998: 156).

Discussion

The issue of theory in historical research is controversial. Theory in accounting history may minimize the value of the more traditional tasks of patiently locating and transcribing accounting records, but it may also help the researcher abstract from the particular data to understand and explain the specific phenomena of interest (Carnegie and Napier, 2012). Indeed, the accounting history discipline seems to be torn between a view of history as narrative, in which theorizing is implicitly rooted in the efficacy of evidence and the importance of time-bound, context-bound and evidence-based conclusions, and a view of history as a social science, in which established theories are explicitly mobilized to interpret historical evidence, with the expectation of bringing about lessons for change in contemporary situations as well (Carnegie, 2014; Tyson and Oldroyd, 2017). However, the issue of theory is of paramount importance for accounting history. An acknowledgement of the role of theory has the potential to shape the contours of the accounting history field’s future. To provide new insights into accounting historians’ use of theory in writing their histories, we collected 20 years of historical accounting literature across the six journals most relevant to the discipline, analysed them through topic modelling, and interpreted our findings through Llewellyn’s framework of the five levels of theory (Llewellyn, 2003).

Topic modelling rendered a picture of an academic field that addresses a range of research objects (from financial accounting to the public sector to profession to regulation to specific thematic or geographical foci), based on mainly two types of sources (accounting records and other documentary evidence) and through a whole range of ways of theorizing proposed by Llewellyn (2003). We also looked for potential relationships between these ways of theorizing and specific research objects and found that while narrating is indeed the ever-present form of historical research, there are different areas of accounting history that tend to use a different ‘shade of theory’. These findings lead to several points of discussion.

The importance of acknowledging shades of theory

The debate on theory in accounting history is quite polarized between the view of history as a narrative and history as a social science. With this article, we move beyond dichotomies by reinforcing the point that there exist different ‘shades of theory’ and by showing the proportions and dynamics of the uses of different shades of theory across 20 years of accounting history research. We show that accounting history operates in general at all of Llewellyn’s (2003) levels of theory. Only in some cases do authors rely on grand theories that theorize macro-structures (with a dominance of Foucauldian and Marxian perspectives); in many other cases, theory operates more as an analytical framework to explain specific settings, develop concepts, or simply explain a phenomenon in the past, at lower levels of abstraction. This bears important implications for a researcher engaging with accounting history: being narrative is not being a-theoretical and being theoretically informed and informing is not (only or necessarily) adopting a grand theory framework. While we embrace the call for more theoretical engagement in accounting history, we also warn that this cannot be reduced to deriving it ‘from neo-classic economics, the ideas of Marx or Foucault, or some other source’ (Napier, 2009: 40) to frame, present and interpret historical evidence. If so, there would be no more space for the birth and development of new concepts from the empirics and for an understanding of specific settings and an explanation of the emergence or change of specific practices (Llewellyn’s levels 1–4). We would risk applying already existing grand explanatory frameworks as a toolkit to comply with the demand of being more theoretical. We would also risk having an overwhelming, if not exclusive, concern with theoretically motivated and conceptual rather than ‘traditional historical’ questions (Kipping and Üsdiken, 2014). We believe that this is neither desirable for the discipline nor is this what was intended by the calls for a more theoretically informed and informing historical research in accounting.

The emergence of mid-range ways of theorizing

A second food for thought derives from a reflection on the temporal dynamics that emerge from our findings. It is now well established that the field of accounting history has been transformed with new research topics, different theoretical perspectives and different methodological approaches borrowed from other disciplines over the years (Carnegie and Napier, 1996, 2012; Fleischman and Radcliffe, 2005; Gomes, 2008; Napier, 2001; Parker, 1999). Most literature reviews also converge on the fact that in accounting history, interpretive and critical perspectives have been on the rise since the 1990s, with a prevalence of Foucauldian and Marxian views (e.g. Fleischman et al., 1996; Fleischman and Radcliffe, 2005; Gomes, 2008; Napier, 2006) and also Weberian and Latourian views (Carnegie and Napier, 2012). However, our findings tell us that while there is a sustained pluralism of research objects, there is no similar sustained pluralism in the ways of theorizing (Figure 1). Actually, an interesting dynamic emerges: in 1996, there was a predominance of narrating (level 1 of theorizing for Llewellyn, 2003) and a balanced mix of conceptualizing approaches (levels 2 and 3), theorizing settings (level 4) and grand theorizing (level 5). Twenty years later, there is a predominance of context-based explanations, such as ANT or neo-institutional perspectives (level 4), a relative decrease in narrative forms (level 1), and, most interestingly, a flattening of all the other ways of theorizing around the 2–4 per cent of the total picture. As we saw, theorizing settings comprise various ways of bridging micro- and macro-levels of analysis, linking empirical phenomena to more general, yet grounded, concepts and arguments. Is this a proof of a middle way between the two highly debated extreme views about what history and theory are or should be in accounting history? Maybe the accounting history field is in the process of finding its own way of rising from the ‘antiquarian approach’, without necessarily going to the other extreme of mobilizing grand theories to become a ‘social science’, sometimes missing being in touch with the data. Maybe, in the polarized debate around history and theory, the answer comes from the field, that is, from what accounting historians are in fact doing.

When to embrace a different shade of theory?

A third element of discussion is what drives the engagement with more or less abstract shades of theory in accounting history research. Carnegie and Napier (2012) maintained that operating at different levels of theory depends on the problem under consideration. Based on our findings, we can say that this is quite true. For example, the study of treatises, or of micro-histories, continues to call for a strong narrative approach, while the study of public sector accounting in the past is generally associated with context-based explanations

However, based on our findings, we can also say that the orientation towards one or another way of theorizing might in part also depend on the publication outlet. We found that specialized accounting history journals are the ones that most welcome theorizing at lower levels of abstraction (narrative or concept theories), while generalist journals (AOS, AAAJ, CPA) are rather associated with theorizing at higher levels of abstraction. Arguably, these journals address a broader audience, which may be interested in the general implications of a historical study (De Villiers and Dumay, 2014). The impression is that generalist journals may consider accounting history worth publishing when it helps to ‘resolve technical accounting problems of the present’ or ‘to develop general theories of accounting change in terms of response to environmental change’ (Napier, 2006: 453). This has interesting implications for accounting scholars, because it becomes clear that embracing a different ‘shade of theory’ depends on the research design and the researcher’s interest and – partly – on the choice of the publication outlet.

Methodological contributions

Prior research has pointed out that topics can be ontologically different in topic modelling (DiMaggio et al., 2013; Ferri et al., 2018). Our study confirms this finding, as three ontologically distinct clusters of topics emerged: research objects, sources of data and ways of theorizing. In addition, our article provides guidelines on how to leverage this feature of topics, especially in the areas of topic interpretation and analysis.

The study shows that ontologically different clusters require different interpretative efforts. The topic modelling outputs (list of words, coding of each word within each paper, paper per topic matrix) may not be enough to interpret complex topics such as ways of theorizing. Going back to the original documents may be necessary in these cases as part of the iterative sense-making process. While some authors prefer relying on quantitative methods for defining the ‘right’ number of topics and interpreting them, we stress the importance of the inductive phase, especially when difficult-to-label topics emerge. We believe that to avoid using topic modelling as a ‘black box’ (Hannigan et al., 2019), researchers should complement two of the best features of these methods: the possibility of dealing with large corpora of texts and the possibility to preserve induction (DiMaggio et al., 2013).

In terms of analysis, in this article, we developed a methodology for analysing the co-occurrences between topics pertaining to ontologically different clusters – namely, research objects and ways of theorizing. This represents a promising analytical tool to investigate in more depth the features of a field of knowledge or a debate.

Conclusion and directions for future research

This article has provided some answers on the role of theory in accounting history research. Essentially, the field is characterized by shades of theory, ranging from very narrative accounts to very abstract theorizations about the past, but mid-range ways of theorizing are seemingly becoming the predominant approach embraced by accounting historians, beyond the dualism of the scholarly debate. It should be noted that a limitation of the analysis is looking only at journals as much history appears in books and monographs.

This article also raises some further questions about the issue of history and theory in this field. First, does the evidence of the relative decrease in the narrative approach, which has so deeply characterized historical research for centuries, mark a dismissal of this form of research? What are the implications, both intended and unintended, and what is the responsibility of the research community in this sense? Does grand theorizing have a similar destiny and with what implications?

Second, scholars have extensively reviewed the accounting history literature, engaging, in some cases, with thematic reviews or thematic calls for empirical research (see, for instance, Cobbin and Burrows, 2018, for accounting history and the military). We are missing an in-depth engagement with conceptual reviews, such as ‘accounting history and ANT’, or ‘accounting history and neo-institutionalism’ and the like, as some scholars have started doing in general accounting research (Justesen and Mouritsen, 2011; Modell et al., 2017). It would be interesting to inquire, for example, what kind of a contribution has been made to the field with the adoption of particular perspectives positioned at different levels of theory.

Third, future research could deepen some issues that emerge from the associations between the research object and the ways of theorizing that we have uncovered in this article. For example, why is a context-based explanation, such as ANT, used for certain research objects rather than for others? Vice versa, why is a particular research object, such as the military one, essentially researched through a narrative approach?

To conclude, the role of theory in historical research is not only a fundamental issue but also an evolving one. For this reason, despite the specific position that different scholars might have on the topic, we believe that keeping up a reflective debate on this issue within the accounting historians’ community is a duty for all of us, and that reaching a conclusive point is not only unlikely but also not even desirable.

Footnotes

Appendix

Three main articles per topic.

In this appendix, for each topic, we list the three articles which are most constituted by that topic. We list author(s), journal, year, article and the percentage of topic composition. Although in the inductive labelling of topic we analysed five to ten papers per topic, we list here only three for the sake of space.

| Topic | Most coded articles per topic | Topic composition (%) | ||||

|---|---|---|---|---|---|---|

| Author(s) | Title | Journal | Year | |||

| 0 | Professional bodies | Parker | Naming and branding: Accountants and accountancy bodies in the British Empire and Commonwealth, 1853-2003 | AH | 2005 | 58.2 |

| Birkett, Evans | Control of accounting education within Australian universities and technical colleges 1944–1951: A uni-dimensional consideration of professionalism | ABFH | 2005 | 55.6 | ||

| Carnegie, Parker | Accountants and Empire: The case of co-membership of Australian and British accountancy bodies, 1885 to 1914 | ABFH | 1999 | 54.1 | ||

| 1 | Cost accounting concepts | Vent, Milne | Cost accounting practices at precious metal mines: A comparative study, 1869–1905 | AH | 1997 | 62.8 |

| Mclean, Tyson | Standard costs, standard costing and the introduction of scientific management and new technology into the post-Second World War Sunderland shipbuilding industry | ABFH | 2006 | 58.5 | ||

| Yoshikawa | Cost accounting standard and cost accounting systems in Japan. Lessons from the past recovering lost traditions | ABFH | 2001 | 57.4 | ||

| 2 | Share and shareholders | Pitts | Did dividends dictate depreciation in British coal companies 1864 - 1914? | AH | 1998 | 68.1 |

| Pitts | Victorian share-pricing–a problem in thin trading | ABFH | 1998 | 63.2 | ||

| Jones | Was the nineteenth-century Denbighshire coalfield a worthwhile investment? An analysis of the investors and their returns | ABFH | 2010 | 63.0 | ||

| 3 | Auditing | Baker, Prentice | The origins of auditor liability to third parties under United States common law | AH | 2008 | 61.4 |

| Young | Defining auditors’ responsibilities | AHJ | 1997 | 59.6 | ||

| Holm | Civil and common law influences on the Danish auditor’s responsibilities in relation to fraud | AHR | 2014 | 57.1 | ||

| 4 | Taxation | Treisch | Taxable treatment of the subsistence level of income in German Natural Law | ABFH | 2005 | 59.2 |

| Giroux | Financing the American Civil War: Developing new tax sources | AH | 2012 | 56.9 | ||

| Barney, Flesher | A study of the impact of special interest groups on major tax reform: Agriculture and the 1913 Income Tax Law | AHJ | 2008 | 52.9 | ||

| 5 | Accounting firms | Wootton, Wolk, Normand | An historical perspective on mergers and acquisitions by major US accounting firms | AH | 2003 | 59.1 |

| Hollingsworth | Examining Frank Adair Jr. as an African American CPA pioneer: A historical note | AHJ | 2012 | 55.5 | ||

| Baskerville, Hay | The impact of globalization on professional accounting firms: Evidence from New Zealand | AH | 2010 | 53.9 | ||

| 6 | Critics of capitalism | Bryer | The roots of modern capitalism: A Marxist accounting history of the origins and consequences of capitalist landlords in England. | AHJ | 2004 | 64.9 |

| Bryer | The history of accounting and the transition to capitalism in England. Part one: theory | AOS | 2000 | 63.1 | ||

| Bryer | Americanism and financial accounting theory – Part 1: Was America born capitalist? | CPA | 2012 | 57.0 | ||

| 7 | Governance and accountability | Miley, Read | After the quake: The complex dance of local government, national government and accounting | AH | 2013 | 55.9 |

| Yamamoto, Noguchi | Different scenarios for accounting reform in non-Anglophone contexts: The case of Japanese local governments since the 1990s | AH | 2013 | 48.6 | ||

| Senarath Yapa | In whose interest? An examination of public sector governance in Brunei Darussalam | CPA | 2014 | 48.4 | ||

| 8 | Narrating | Funnell | Evidence, Myths and Informed Debate in Accounting History: A Response to Arnold and McCartney | CPA | 2007 | 47.2 |

| Radcliffe | It’s oysters, dear! Professor Carnegie’s prescription and the seeming fate of accounting history in the United States | AHJ | 2006 | 44.8 | ||

| Mattessich | ‘Forensic’ accounting in Spanish belles-lettres of the nineteenth century | AAAJ | 2000 | 41.1 | ||

| 9 | Analysing documents | Noke | Advising on the Act: The UK Companies Act Consultative Committee and Accountancy Advisory Committee 1948–72 | AH | 2007 | 54.5 |

| Noguchi | Corporatism and unavoidable imperatives: Recommendations on accounting priciples and the ICAEW memorandum to the Cohen committee | AHJ | 2004 | 52.9 | ||

| Keenan | Between anarchy and authority: The New Zealand Society of Accountants’ management of crisis, 1989-1993 | AH | 2000 | 50.5 | ||

| 10 | China | Lu, Aiken | Origins and evolution of Chinese writing systems and preliminary counting relationships | AH | 2004 | 68.2 |

| Ji, Lu | The evolution of bookkeeping methods in China: A Darwinist analysis of developments during the twentieth-century | AH | 2013 | 59.4 | ||

| Lin | Chinese bookkeeping systems: A study of accounting adaptation and change | ABFH | 2003 | 54.3 | ||

| 11 | Financial accounting concepts | Schultz, Johnson | Income tax allocation: The continuing controversy in historical perspective | AHJ | 1998 | 69.7 |

| Nurnberg | Objectives of financial reporting, aboriginal cost, and pooling of interests accounting | AHJ | 2012 | 68.9 | ||

| Nurnberg | Conceptual nature of the Corporate Income Tax | AHJ | 2009 | 66.9 | ||

| 12 | Military | Funnell | The ‘Proper Trust of Liberty’: Economical reform, the English constitution and the protections of accounting during the American War of Independence | AH | 2008 | 59.9 |

| Funnell | On his majesty’s secret service: Accounting for the secret service in a time of national peril 1782-1806 | AHJ | 2010 | 58.4 | ||

| Funnell | Social reform, military accounting and the pursuit of economy during the liberal apotheosis, 1906–1912 | AHR | 2011 | 57.9 | ||

| 13 | Education and healthcare | Fowler | Financing, accounting and accountability in colonial New Zealand: The case of the Nelson School Society (1842-52) | AH | 2010 | 51.8 |

| Robbins, Lapsley | Irish voluntary hospitals: An examination of a theory of voluntary failure | ABFH | 2008 | 51.4 | ||

| Fowler, Cordery | From community to public ownership: A tale of changing accountabilities | AAAJ | 2015 | 47.5 | ||

| 14 | Insurance | Van Der Eng | Consumer credit in Australia during the twentieth century | ABFH | 2008 | 71.2 |

| Keneley | The evolution of the Australian life insurance industry | ABFH | 2001 | 70.4 | ||

| Thomson, Abbott | The life and death of the Australian permanent building societies | ABFH | 1998 | 67.6 | ||

| 15 | Microhistories of accountants | Lee | British public accountants in America: A historical study of social mobility and fluidity associated with élite immigration | AAAJ | 2009 | 70.6 |

| Lee | Paul and Mackersy, accountants, 1818–34: Public accountancy in the early nineteenth century | AHR | 2011 | 69.7 | ||

| Lee | A social network analysis of the founders of institutionalized public accountancy | AHJ | 2000 | 69.0 | ||

| 16 | Gender | Walker | Identifying the woman behind the ‘railed-in desk’: The proto feminisation of bookkeeping in Britain | AAAJ | 2003 | 50.9 |

| Virtanen | Revealing financial accounting in Finland under five historical themes | AH | 2009 | 48.5 | ||

| Roberts | Women in accounting occupations in the 1880 US Census | AHR | 2013 | 47.1 | ||

| 17 | Trade | Spraakman | Management accounting at the historical Hudson’s Bay Company: A comparison to the 20th century practices | AHJ | 1999 | 58.6 |

| McWatters, Lemarchand | Accounting for triangular trade | ABFH | 2009 | 56.0 | ||

| Roy, Spraakman | Transaction cost economics and nineteenth century fur trade accounting: relevance of a contemporary theory | AH | 1996 | 54.9 | ||

| 18 | Counternarratives | Kim | Whose voice is it anyway? Rethinking the oral history method in accounting research on race, ethnicity and gender | CPA | 2008 | 70.0 |

| Funnell | The narrative and its place in the new accounting history: The rise of the counternarrative | AAAJ | 1998 | 66.3 | ||

| Funnell | Preserving history in accounting: seeking common ground between ‘new’ and ‘old’ accounting history | AAAJ | 1996 | 61.0 | ||

| 19 | Religion | Funnell | Ancestors of governmentality: Accounting and pastoral power in the 15th century | CPA | 2015 | 65.6 |

| Bigoni, Deidda, Gagliardo, Funnell | Rethinking the sacred and secular divide: Accounting and accountability practices in the Diocese of Ferrara (1431–1457) | AAAJ | 2013 | 63.7 | ||

| Liyanarachchi | Accounting in ancient Sri Lanka: Some evidence of the accounting and auditing practices of Buddhist monasteries during 815–1017 AD | AH | 2009 | 63.0 | ||

| 20 | Accounting standards | Eierle | Differential reporting in Germany – A historical analysis | ABFH | 2005 | 55.1 |

| Chiba | The designing of corporate accounting law in Japan after the Second World War | ABFH | 2001 | 53.1 | ||

| Elitaş, Üç | The change on the foundations of the Turkish accounting system and the future perspective | CPA | 2009 | 45.5 | ||

| 21 | Context-based explanations | Beaubien | Technology, change, and management control: A temporal perspective | AAAJ | 2013 | 74.4 |

| van der Steen | Inertia and management accounting change: The role of ambiguity and contradiction between formal rules and routines | AAAJ | 2009 | 71.6 | ||

| Chenhall, Moers | The role of innovation in the evolution of management accounting and its integration in management control | AOS | 2015 | 68.9 | ||

| 22 | Profession and the State | Constable | Accounting for the nation-state in mid-nineteenth-century Thailand | AAAJ | 2007 | 55.3 |

| Bakre | Second attempt at localizing imperial accountancy: The case of the Institute of Chartered Accountants of Jamaica (ICAJ) (1970s–1980s) | CPA | 2006 | 46.0 | ||

| Kuasirikun, Constable | The cosmology of accounting in mid 19th-century Thailand | AOS | 2010 | 45.5 | ||

| 23 | Analysing accounts | Hollister, Schultz | The Elting and Hasbrouck store accounts: A window into eighteenth-century commerce | AH | 2007 | 73.0 |

| Noke | Respites in charge and discharge statements | ABFH | 1996 | 71.4 | ||

| Baker, Eadsforth | Agency reversal and the steward’s lot when discharge exceeds charge: English archival evidence, 1739-1890 | AH | 2011 | 68.7 | ||

| 24 | Italy, Spain and France | Zambon, Zan | Controlling expenditure, or the slow emergence of costing at the Venice Arsenal, 1586–1633 | ABFH | 2007 | 69.6 |

| Oldroyd | Through a glass clearly: Management practice on the Bowes family estates c.1700-70 as revealed by the accounts | ABFH | 1999 | 68.9 | ||

| Baxter | McKesson & Robbins: a milestone in auditing | ABFH | 1999 | 68.4 | ||

| 25 | Statistical modelling | Shields, Shields | Antecedents of participative budgeting | AOS | 1998 | 81.8 |

| Hartmann, Moers | Testing contingency hypotheses in budgetary research: An evaluation of the use of moderated regression analysis | AOS | 1999 | 81.5 | ||

| Smith Bamber, Christensen, Gaver | Do we really ‘know’ what we think we know? A case study of seminal research and its subsequent overgeneralization | AOS | 2000 | 68.2 | ||

| 26 | Financial accounting treatises | Sangster, Stoner, McCarthy | The market for Luca Pacioli’s Summa Arithmetica | AHJ | 2008 | 64.7 |

| Yamey | The market for Luca Pacioli’s Summa De Arithmetica: Some comments | AHJ | 2010 | 63.4 | ||

| Sangster, Stoner, McCarthy | In defence of Pacioli | AHJ | 2011 | 58.5 | ||

| 27 | Corporate Social Responsibility (CSR) | Deegan, Rankin, Tobin | An examination of the corporate social and environmental disclosures of BHP from 1983-1997: A test of legitimacy theory | AAAJ | 2002 | 56.1 |

| Campbell, Moore, Shrives | Cross-sectional effects in community disclosure | AAAJ | 2006 | 52.4 | ||

| Neu, Warsame, Pedwell | Managing public impressions: Environmental disclosures in annual reports | AOS | 1998 | 51.4 | ||

| 28 | British empire and colonialism | Neu | ‘Presents’ for the ‘Indians’: Land, colonialism and accounting in Canada | AOS | 2000 | 54.0 |

| Neu, Heincke | The subaltern speaks: Financial relations and the limits of governmentality | CPA | 2004 | 50.9 | ||

| Neu | Discovering indigenous peoples: Accounting and the machinery of empire | AHJ | 1999 | 47.8 | ||

| 29 | Explaining the literature | Baños-Sánchez Matamoros, Gutiérrez-Hidalgo | Patterns of accounting history literature: Movements at the beginning of the 21st century | AHJ | 2010 | 83.1 |

| Baños-Sánchez Matamoros, Gutiérrez Hidalgo | Publishing patterns of accounting history research in generalist journals: Lessons from the past | AH | 2011 | 82.9 | ||