Abstract

This study considers developments that led to the introduction and diffusion of double-entry bookkeeping in Tuscany in the late-thirteenth and fourteenth centuries. We examine the evolution of the four basic account books (debtors and creditors, cash, merchandise and moveable property), which, together with the capital account, established the basis of the accounting method. We reconstruct the social context of Tuscany to highlight how specific cultural factors, such as risk appetite and entrepreneurial spirit, fostered the creation of companies attentive to organisational modes of work and the valorisation of human capital. These elements, combined with an innate pragmatism of economic operators, produced innovation in the field of accounting as well. Accountants and firm managers were able to establish the double-entry bookkeeping method, which was not the result of abstract rules but rather of gradual evolution. Accounting systems can thus be considered as reflections of the society and the organisations in which they developed and spread.

The history of accounting has made significant advances in the choice of research topics and the sharpening of its methods of enquiry. New methodological approaches emerged in the 1990s and signposted the emergence of New Accounting History. Peter Miller, Trevor Hopper and Richard Laughlin, among other authors, defined the new developments introduced by New Accounting History as a diversification of approaches and a consolidation of historiographic analysis (Miller et al., 1991). In our view, today New Accounting History can be justly considered an open and varied assembly of interesting and stimulating research topics. Within this field, narration plays a fundamental role, one which leads to routes of enquiry freed from the obligation of following a ‘certified path to knowledge’ (Merino, 1998: 603).

While maintaining a continuous dialectical relationship to more traditional historiography, the historian of accounting cannot limit his or her attention to mere mechanisms. Each accounting system can be studied in its capacity as a mirror of the society and the organisations in which it developed and spread. Beginning in the last decade of the twentieth century, research has thus been directed towards the theoretical aspects and contexts that characterised the accounting practices of a certain historical period. In particular, greater attention has been paid to the influence of cultural and socioeconomic phenomena as well as to the language and motivations behind accounting records. 1 Accounting has thus acquired greater dignity, treated as much more than a mere technique employed by companies (Carnegie and Napier, 1996). Its history, which has been studied using methods and perspectives more akin to those of economic historians, thus appears to have been liberated from excessively technical connotations. 2

A key contribution in this regard has been and, to some extent, continues to be the study of double-entry bookkeeping, considered in all its aspects. The present study aims to add to this line of research by focussing on developments in accounting in Tuscan firms between the thirteenth and fourteenth centuries.

Benedetto Cotrugli, a merchant, and diplomat born in Ragusa in 1416, is considered the first to have written on the rules of double-entry bookkeeping. His manuscript was completed in Naples in 1458 but only became somewhat known after 1573, when it was published by Elefanta in Venice under the title ‘Della Mercatura et del Mercante perfetto’ (‘On Trade and the Ideal Merchant’, Tucci, 1990). 3

The works of friar Luca Pacioli, a Tuscan mathematician born in San Sepolcro between October 1446 and June 1447, met with greater success. In the ‘Tractatus 11: particularis de computis et scripturis’, from his ‘Summa de Arithmetica geometria proportioni et proportionalita’, Pacioli included a coherent system for the criteria of bookkeeping. Dating to 1494, the importance of this publication lies in its later becoming the point of reference for mathematicians and scholars who ushered in the so-called era of accounting manuals, a period during which Italian techniques spread throughout Europe. 4 Perhaps, the most famous example is that of the German essay, published in 1518, by Matthaeus Schwarz, head accountant of the Fugger family. To gain such precious knowledge, Schwarz had spent some time in Milan and Venice.

It is well known that neither Cotrugli nor Pacioli invented the double-entry method, 5 which had been in use many years before the fifteenth century in many different Tuscan firms. In Tuscany, double-entry bookkeeping gradually developed, often by means of small, barely perceptible changes involving many businesses, both large and small. This process must be understood as the outcome of the combined efforts of generations of accountants and merchants. Spurred by the need to measure up to new situations and to exchange information in order to work more efficiently, these economic actors created networks of relationships and goods. As we study these networks, we gain an impression of a milieu of efficiency and openness to innovation and change.

Focussing on Tuscan operators in the late Middle Ages, this article attempts to show how simple, primitive accounting methods gradually evolved into modern bookkeeping, thus providing efficient tools for managing firms (Catturi, 1992; Johnson, 1972; Riccaboni et al., 2006). As we build our argument, we will trace both the technical mechanisms and the various economic, social and cultural conditions which led to the introduction and diffusion of the double-entry method in Tuscany in the late thirteenth and fourteenth centuries. Because of its advanced level of development, this region of Italy represents a context of great importance for research on the medieval and modern eras. 6

As we will see, entrepreneurs in this region enjoyed great economic success, thanks to their solid training and to the value they attributed to knowledge and the acquisition of information. Pen in hand, these men used their account books and papers as veritable sites of memory, which, in turn, fed their curiosity and knowledge (Orlandi, 2008, 2014).

When we think of Tuscan archival sources, the famous ‘Fondo Datini’ 7 and other collections of great and powerful Florentine families of the era immediately come to mind. 8 We must bear in mind, though, that the whole of Tuscany contains an even greater abundance of accounting records from the thirteenth to the sixteenth centuries. 9 The archives of every city hold documents that belonged to the small and medium-sized firms, which formed the region’s economic fabric. 10 Next to the books of the great merchant and banking houses and manufacturing companies, we find the records of more modest businesses and even those of small artisans and shopkeepers, such as tailors, cobblers, leather workers, spice merchants and haberdashers. We refer here to a mass of documentation which shows that each firm and workshop kept accounts according to its capability and entrepreneurial needs. This fact allows us to refute the opinion of Hoskin and Macve (1986), who argued that a consolidation of accounting practices did not take root during the late Middle Ages and that this was the achievement of institutional elites. As we will see, although there was no standardisation of procedures, practices were common to accountants of different firms. Indeed, we must bear in mind that the strength of Florentine businesses lay in part in their participation in dense networks of economic relations. These networks facilitated the circulation of information, which included details of technical questions and accounting practices. This phenomenon explains how similar accounting methods came to be used in Florentine, Venetian and Genoese firms.

Not all firms and accountants adopted the new techniques learnt through oral or written exchanges. It is therefore natural that different accounting forms, more or less developed, were used during the same period. Indeed, nothing in history appears or disappears suddenly; novel developments coexist with traditional practices. This was certainly the case in the world of accounting in the thirteenth and fourteenth centuries Tuscany. Indeed, our analysis, while aiming to precisely locate the various innovations in their proper chronology, also finds considerable overlap of old and new techniques.

The second section examines the Tuscan context, which saw significant innovations in accounting. The third and fourth sections look at the main account books used by Tuscan merchants in the thirteenth and fourteenth centuries (the debtors and creditors, cash, merchandise and moveable property books). The fifth section discusses the emergence of two accounting innovations, namely, the secret book and the surplus and deficit account, which then leads into the conclusions.

Tuscany and the competitive advantages of its firms

Between the thirteenth and sixteenth centuries, Tuscan cities experienced a period of economic growth, which was only interrupted (significantly though only briefly) by the Black Death of 1348. In particular, Florence in the Renaissance period boasted ‘a complex combination of economic, social and cultural factors which we can concisely describe as the ‘Florence factor’ (Nigro, 2015: 40). The middle social class, made up of artisans, merchants and bankers, introduced significant social and economic mobility, leading to a more equitable distribution of wealth. The impetus behind this lively urban atmosphere came from artisan workshops, manufacturers producing woollen and silk textiles, and commercial and banking firms. The strength and confidence of these entrepreneurs was reflected in a widespread propension for risk-taking and productive investment. The continuous search for fresh opportunities for profit-making seems to have provided the necessary courage for new, risky ventures and the wish to continually reinvest money that had just been earned (Nigro, 2015: 46–47).

This milieu thus stimulated the development of entrepreneurial skills and fostered a marked inclination for innovation among Florentine firms. To begin with, from the second half of the fourteenth century, operators in the field of banking and finance shed the characteristics of the medieval bank and adopted more modern practices (Melis, 1987: 55–293). Attention was now focussed on aiding firms and workshops through the introduction of business credit, account overdrafts and bank cheques. Second, developments in the transportation sector led to a differentiation in freight charges, such that maritime commerce could be expanded to include goods of lesser value (Melis, 1985: 3–68).

In such an atmosphere, we should not be surprised to find that most young men were eager to enter workshops or commercial firms as soon as they finished their schooling. Education of the young indeed constituted another element of this vivacious milieu. Not only in Florence but in all Tuscan cities, schools could draw on a widespread cultural tradition of knowledge of applied mathematical tools for finance and accounting, which had its roots in the thought and deeds of such figures as Leonardo Fibonacci (c.1170–c.1242) and Paolo Dagomari (1328–1374) (Nigro, 2008a: 28–29). These men introduced a new way of using mathematics, employing it to quantify the value of goods and for other economic purposes. To them is also due the credit for the emergence of the first abaco schools 11 : these spread in Tuscany from the last quarter of the thirteenth century until the end of the sixteenth century, enabling a great number of individuals to acquire the training that was indispensable for founding profitable economic activities (Bonaini, 1857: 241; Nigro, 2008a: 25–38; Van Egmond, 1981: 407; Zervas, 1975: 501).

Indeed, each urban centre of a certain size had abaco schools, workshops where teachers gave elementary lessons on practical geometry and Arabic numerals, thus offering pupils training ‘sufficiens ad standum in apotecis artificis’ (‘which suffices to work in an artisan’s workshop’) (Cipolla, 2002: 52). Students learnt to master weights and measures and began to understand monetary problems. They studied how to calculate simple and compound interest, to record commercial transactions and to distribute the profits of a company or temporary partnership (Orlandi, 2008: 11–16).

Florence, with a population of roughly 100,000 between 1340 and 1350, had 19 abaco schools. According to the cadastre of 1480, when the number of city’s inhabitants were about 50,000, 1,031 boys attended school; of these, at least 375 were enrolled in scuole di grammatica (‘grammar schools’) 12 and 253 in abaco schools (Ulivi, 2002).

Once basic knowledge was acquired, education continued at the workplace. In Tuscany during the late Middle Ages and early modern period, firms provided the foundation of efficient and continuous practical training. Thanks to the dynamism of the social context, this process evidently involved a relatively broad stratum of the urban population (Nigro, 2015; Orlandi, 2017).

When hired, young men were assigned a variety of tasks, without receiving any initial specialist training. By means of constant supervision of their efforts over a long period, they were able to follow all aspects of a shop’s operations, including negotiation techniques, market mechanisms, keeping an income and expenditures book, proper conduct in a business setting, and achieving positive commercial results (Orlandi, 2008: 12–13). Employees generally participated in the productive and commercial operations of their firms, and were constructively involved in the creation of end products or in the execution of business transactions (Nigro, 2015: 40). In this setting, entrepreneurs paid close attention to valorising human capital, continuing the process of developing the skills and knowledge of personnel begun in the schools.

The development of a culture of risk was another important element in the creation of this dynamic economic milieu (Orlandi, 2018: 7–16). Openness to risk-taking not only stimulated new investments but also generated a demand for new tools to assess economic results, as entrepreneurs continuously sought to maximise profits. Within this context, then, the need for innovative accounting methods is readily comprehensible. As accountants themselves, they were immersed in this atmosphere, they too aimed to sharpen their skills and improve their methods to ensure the proper functioning of their bookkeeping.

It was in this context, which characterised the operations of many workshops and fondaci 13 of various sizes, that the gradual adaptation of accounting criteria took place. Beginning in the thirteenth century, we note a change from simple and basic bookkeeping practices to more evolved techniques (Melis, 1972: 49–60). By focussing on several account books, we can trace these developments over time. 14

The evolution of the debtors and creditors book

Perusal of documents belonging to a variety of Tuscan merchants and artisans reveals that accounting techniques in thirteenth-century firms were generally quite basic. Bookkeeping in this period relied on just a few books or records, which sufficed to satisfy the basic need of recording such simple facts as credits and debits.

To this end, firms kept separate accounts for each client, whose entries were recorded a sezioni sovrapposte (one below another). After a note of the credit or debit was made, a space was left blank to record the payment or collection when this occurred. When the final transaction was recorded, the particular account was crossed off, such that those that were still open could be identified at a glance. When relations with a client were frequent, the books show a confusing alternation between entries of dee dare (‘shall give’) and ànne dato (‘has given us’).

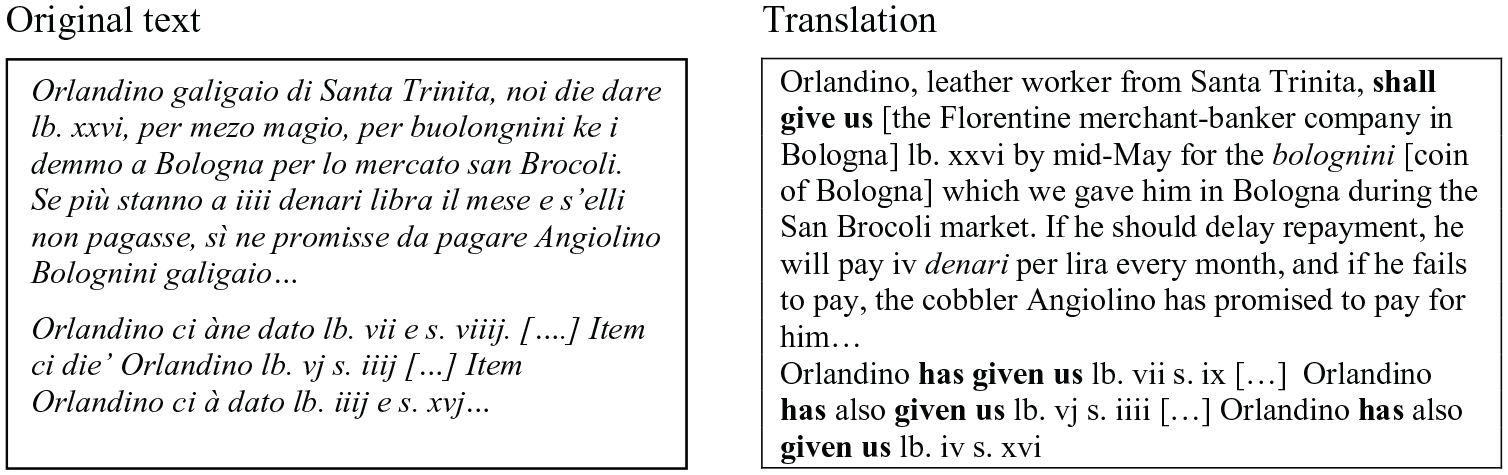

The oldest case known to us today was discovered in Florence on a parchment used to reinforce a cover of the Codice Laurenziano Aedil, 67, preserved today at the Biblioteca Medicea Laurenziana. This is a fragment of an account book that was kept by Florentine banking merchants in Bologna in 1211. Written in vernacular, the text has been of particular interest to historians of the Italian language. 15 The other surviving accounts are personal ones (that is, accounts in the name of a company’s debtors or creditors), in which entries were listed in chronological order (in forma scalare) down the two columns that divide the page. Figure 1 shows one of them (with the English translation), which bears the name of a certain Orlandino, a leather worker from the suburb of Santa Trinita in Bologna. The company of Florentine merchant-bankers operating in Bologna (whose name has not come down to us) made a loan to Orlandino.

Fragment of a transaction recording (original text and translation).

This excerpt shows us the almost spontaneous simplicity with which lending operations were recorded by a typical medieval banco. From the transcription of the original entry, we see that the sums were not arranged in an ideal external column, which allowed for immediate identification, but were rather written one after the other, creating a confused appearance.

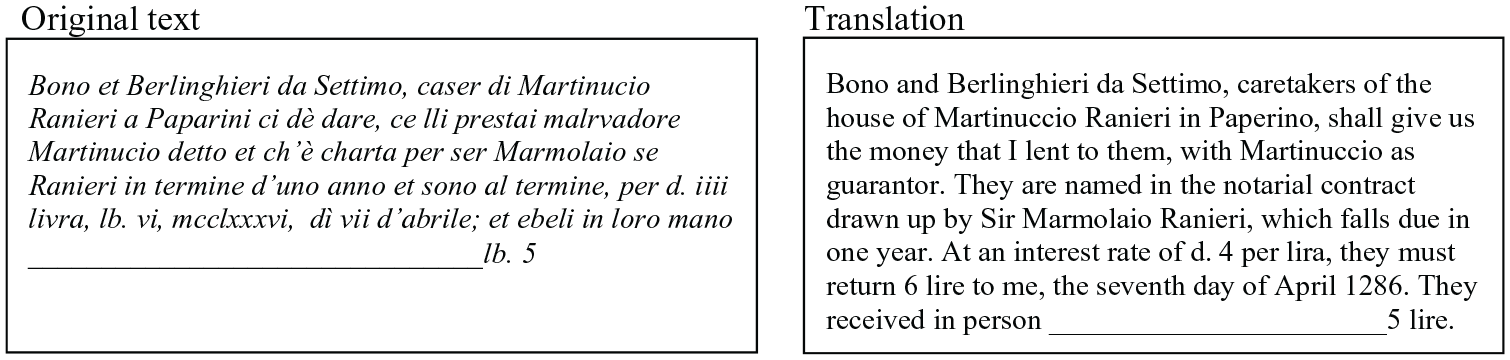

Seventy-four years later, the account book of a small money lender from Prato, Sinibaldo Angiolini, reveals that bookkeeping forms had for the most part not undergone significant changes. This is evident from comparison of the above entry with that presented below in Figure 2.

Recording of loan made by Sinibaldo Angiolini, a usurer in Prato. 16

This lender was a usurer who kept accounts in a simple quaderno di prima nota (petty cash book), listing transactions chronologically (in forma scalare) in accordance with his very basic needs (Nigro, 2008b). Angiolini’s book further includes several details which would not usually be found in a summary register. For example, he records such information as the trade and residence of the borrower, the guarantees offered (which could be tangible, such as a pawned object, or personal, in the form of a surety), the mode of repayment (directly from the borrower or from a third party on his behalf), the repayment deadline and the interest.

The main development of this rudimentary debtors and creditors book is represented by the introduction of bilateral entries: the left page records the credit, while the right indicates the corresponding repayment (and vice versa in the case of a debit). Each account still concerned an individual client and used the phrases deve dare (left page) and ànne dato (right page), the precursors of the modern meanings of ‘debit’ (increase in wealth) and ‘credit’ (decrease).

The term ànne dato, which can be traced to the twelfth century, is also found in the accounting records of some small businesses, such as those of the cheese retailer Domenico di Iacopo Giusti (1365–1408). In an account opened on 17 February 1383 for a painter, Domenico recorded a loan using the phrase dee dare and each repayment by ànne dati (Nigro, 2008b: 19).

Three additional account books to record assets: cash, merchandise and moveable property

The cash book

Regarding the recording of cash transactions, we find that the income and expenditures books were kept separately, preserved in the strongbox where money was safeguarded. The oldest exemplar of a private cash account (1277) is preserved in Siena (Melis, 1972: 382); it belonged to the important merchant company of the Ugolini family. It is divided into two parts, the first for income and the other for expenditures. In this case as well, entries were sovrapposti, or mingled, with debits and credits entered vertically. They were kept in a particularly simple form, with a description of successive operations but without the use of an external column for figures. Beginning in the fifteenth century, this record was more frequently called cassa, often taking the form of an account opened in the debtors and creditors book, in which entries were usually made contrapposti, or bilaterally (Melis, 1972: 63–64).

The merchandise book

Beginning in the second half of the thirteenth century, the merchandise book (libro mercanzie) was also used in Tuscany. Here again, accountants did not adopt uniform recording techniques. In some cases, a specific book was used, while in others these accounts formed part of the debtors and creditors book. The choice, it seems, depended on the preferences of each firm and its accountants. In any case, the merchandise book was important for those merchants who acted as commercial intermediaries, purchasing and reselling goods for themselves and for third parties. This book indeed emerged from the need to keep track of the principal element of a company’s expansion (namely, the analysis of all purchase costs) on the basis of which sale prices were determined, together with gross and net revenues.

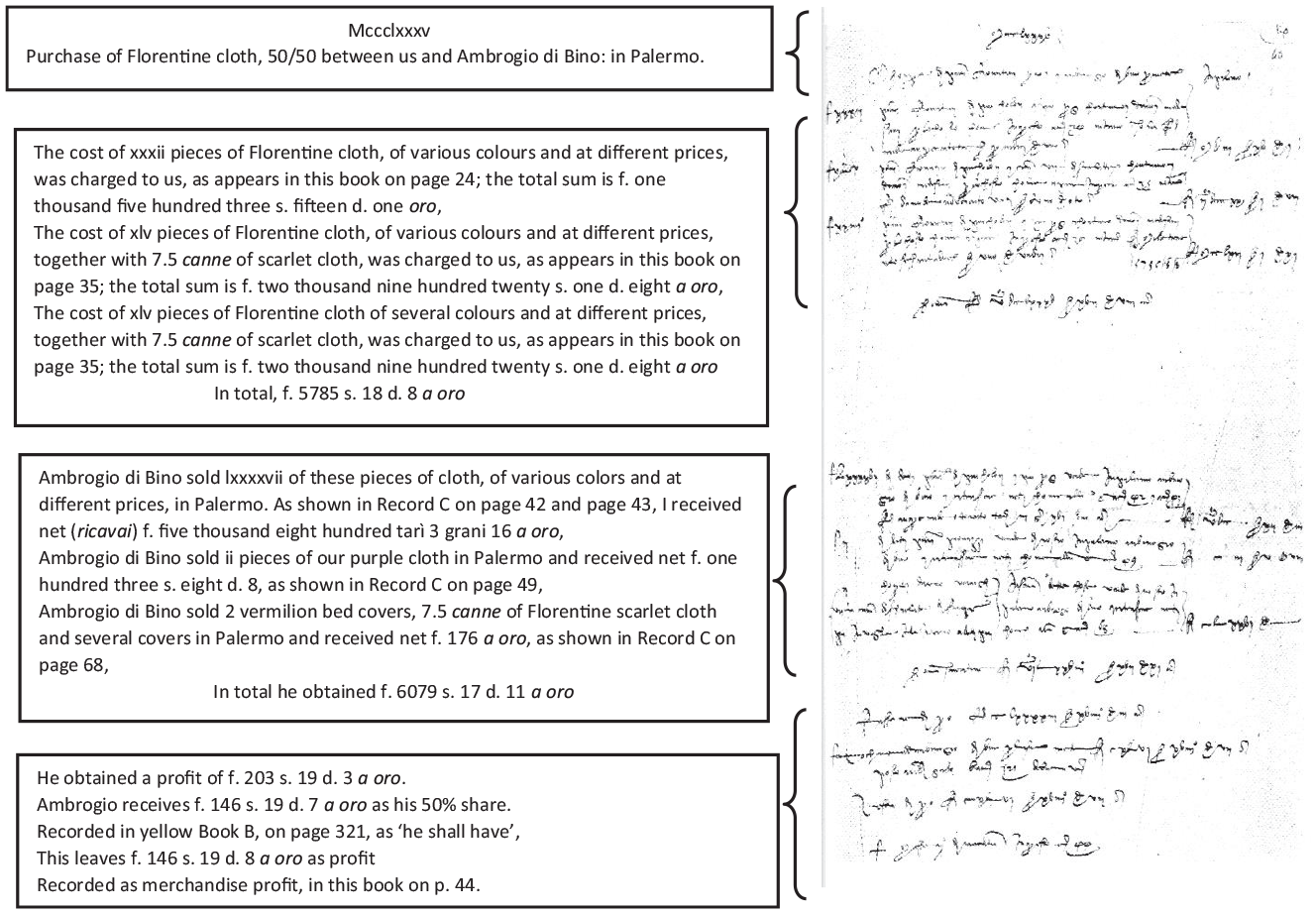

An account for each lot of goods was opened in the merchandise book, a practice which is evident from the document shown in Figure 3. In this case, the first entry indicated the quantity purchased, the unit price paid and the overall price. Then, all additional costs were recorded (fees for carriage, insurance, taxes, storage, others), such that the total purchase costs could be calculated. Later, the income from the sale of the goods was noted, from which sales costs were subtracted. The difference between the two totals represented the profit from the sale of the merchandise lot. This analytical method of accounting was the result of specific entrepreneurial needs and methods. Such a perspective allows us to account for the non-linear progression of accounting systems among the various firms.

Extract and translation of a transaction from the merchandise book of the Datini company in Pisa.

Other accounts emerged over time, particularly the conto di costi e spese (costs and expenses account) and the conto di netto ricavo (net profit account), which contained detailed descriptions of purchase and sales costs. These values were then transferred in summary form to the merchandise book.

Commercial ventures required substantial investments, especially when they involved sources of raw materials and costly finished products. In the initial phases of the development of trade, such ventures were realised through temporary business associations, such as the commenda. (Cipolla, 1997: 193–199). Later, with the emergence of partnerships, mutual financial support was based on commerce conducted through ownership of variable shares or on behalf of third parties. In either case, everything depended on the merchandise lot, which had to be tracked at every stage. Firms therefore exchanged their costi e spese and netto ricavo accounts for each lot of goods.

Using an extract from the merchandise book of the Datini company in Pisa, in Figure 3 we show an example of a sovrapposto merchandise account which does not provide a detailed recording of additional costs, but only the balances. This particular transaction concerns the purchase of a lot of Florentine cloth for Palermo (Sicily). The operation was a 50–50 joint venture with the firm of the Florentine Ambrogio di Bino, who was active in Palermo. It shows how the old system of accounts opened for single lots coexisted with a clear application of the double-entry method. 17

It is interesting to note that in Figure 3, the accountant recorded the quantity of purchased cloth in the external margin (right column), thus facilitating the reading of the account.

In the late fourteenth century, instead of being kept sovrapposti, merchandise accounts began to be recorded bilaterally, supported by descriptive details. The typical merchandise account of a Datini company allowed accountants to track the transactions of each merchandise lot step by step: on the debit side, it showed all purchase costs and expenses, and then sales costs; on the credit side, it indicated the gross revenue from the sale.

The moveable property book

The moveable property book probably originated together with that for merchandise. The book recorded purchases, sales and depreciation costs of furnishings and shop equipment. The debit side noted purchases, while the credit side indicated any sales of such property. As the double-entry method became prevalent, depreciation charges were recorded at the end of the fiscal year.

The oldest case of depreciation on moveable property is found in the accounts of the company of Giovanni Farolfi, dating to 1299–1300 (Melis, 1950: 486–492).

The emergence of the secret book and the surplus and deficit account

The expansion of commerce saw an increased need for new and more complex ways of recording economic transactions, a process which gave rise to novel forms of analytical and synthetic bookkeeping. Nonetheless, by the end of the thirteenth century all accountants were still able to keep an adequate record of each positive or negative variation in a firm’s assets using the four books that we have seen thus far (the debtors and creditors, cash, merchandise and moveable property books). We agree with Federigo Melis (1950, 1972) that we cannot yet speak of double-entry bookkeeping, which only comes into being with the introduction of the surplus and deficit account. For the moment, we may find dual recording but not double entry in the true sense of the term.

Asset variations in the accounts of the debtors and creditors book, which contained accounts opened for individual clients, were indicated by the phrases deve dare (‘shall give’) and deve avere (‘shall have’). In the merchandise and moveable property books, these transactions were noted by comprammo (‘we bought’) or vendemmo (‘we sold’), and in the cash book, finally, most frequently by da (‘received’ or ‘from’) or a (‘delivered’ or ‘to’). As long as accounts were recorded sovrapposti, the meaning of an accounting transaction was clearly expressed through these terms. With the introduction of contrapposti, or bilateral, accounts, debit and credit operations were noted on the left and right pages, respectively. In an equally natural way, some accountants tended to make less use of the older phrases, beginning rather to employ the terms dee dare (or deve dare) and dee avere (or deve avere) in the modern sense of ‘debit’ and ‘credit’.

Since their emergence, it is evident that the complementary use of the four basic account books gave rise to a spontaneous dual recording. It was, for example, completely natural that a purchase of merchandise with fixed-term payments was recorded both in the merchandise book (with the phrase ‘we bought’) and in the accounts of the debtors and creditors book (with the phrase ‘X shall have’). Annual profit or loss, meanwhile, was calculated by using the account balances for each merchandise lot. Operating and general expenses which were not recorded in the merchandise book could be deduced from the cash book, where they were noted without any corresponding entry. Not all asset variations, then, were recorded in double entry. On the contrary, some parts or elements of a company’s assets had to be deduced indirectly, as they were not recorded in a truly systematic manner.

Such a system entailed complex calculations to make periodic assessments of profit or loss; these limitations were overcome in various ways. The demand for more advanced methods emerged in Tuscany (Melis, 1950, 1972); and in particular in the larger companies that were involved internationally with capital entrusted to them by their partners. It was regarding partners that the need to provide an exact and prompt report on the state of certain economic transactions arose. For this reason, a new development took place in the second half of the thirteenth century: alongside those books that specifically concerned the firm (the debtors and creditors, cash, merchandise, and moveable property books), additional ones were created for individual shareholders

18

or for the entire company. These books made evident the personal standing of each partner, or all of them, vis-à-vis the firm. Capital accounts thus came into being, whose purpose was to record the debts of the firm towards the partners. The following translated extract is a hypothetical example of a credit entry in an account opened in the name of a company, which we can define as a capital account: Domenico Giusti and partners shall have f. (florins) 1,500. This money is the amount they must keep in the corpo di compagnia (share capital).

Initially, the capital account might be found in the debtors and creditors book, which was gradually being transformed into the ledger. As a surplus and deficit account which enabled accountants to calculate final earnings or losses had not yet come into being, costs and gross revenues from the merchandise book, together with all other general expenditures and revenues, were recorded as debits or credits in the capital account. With this development, the distinction between personal wealth and company wealth was a fait accompli. Partners or an individual owner and the firm had rights to distinct and mutual relations of debits and credits, which needed to be recorded.

The capital account was included in the secret book (also known as the libro della Ragione or dei Ragionamenti, [‘book of calculations’]), which often opened with a transcription of the firm’s partnership contract. This book contained all the elements that regulated the partnership contract, including the total amount of share capital (called Corpo di Compagnia), the termination date of the partnership, the shares possessed by each partner, and so on. Neither in this case can we speak of a uniform process. In firms which did not have a secret book, we find accounts in the names of the partners, to whom profits were credited and losses charged. In other businesses, the secret book was kept independently by the majority shareholder, 19 while the firm’s accountants kept the surplus and deficit account.

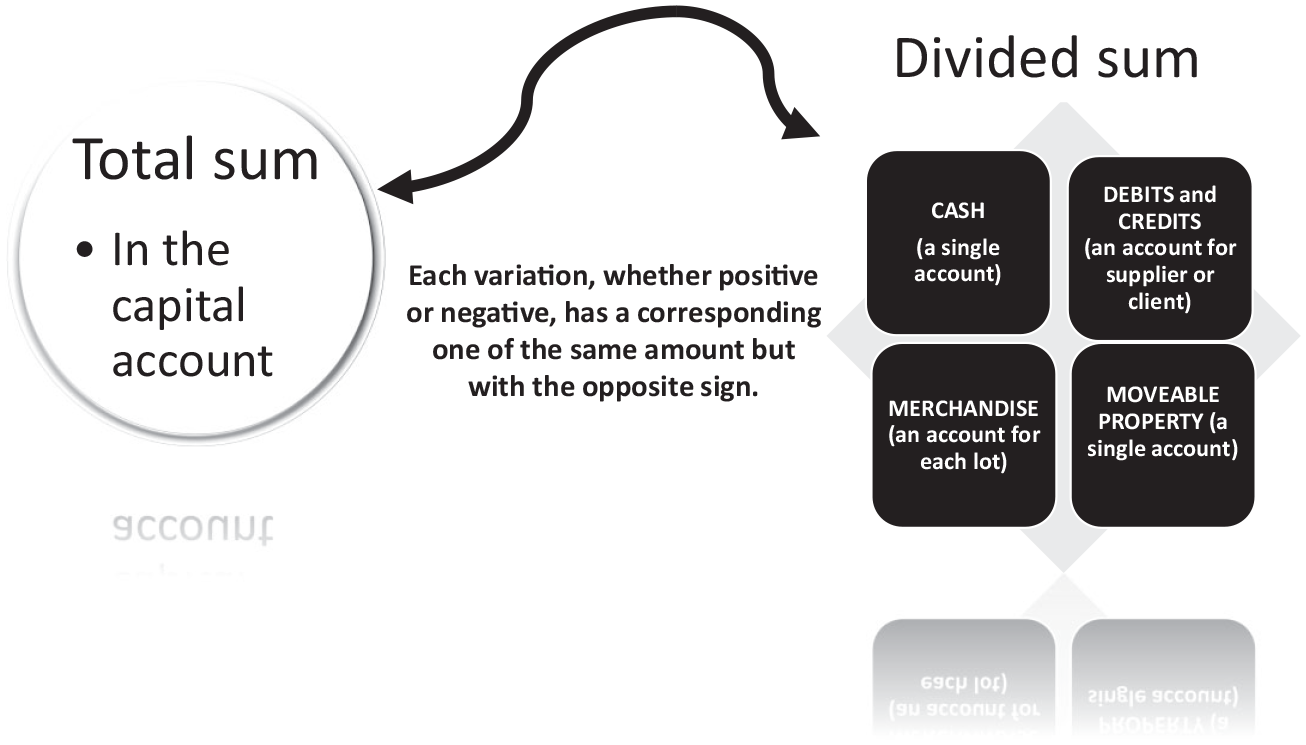

The introduction of the capital account, then, had the effect that assets were considered twice: in the total sum of the capital account (the partners’ accounts) and in the sum split among the four basic books (Figure 4). Each positive or negative variation appearing in the capital account required a corresponding positive or negative variation in one of the four books. This is the basis of double-entry bookkeeping, which we must not confuse with dual recording.

The effects of the introduction of the capital account.

As we have seen, by this method asset variations in terms of profit or loss were accredited or charged to shareholders as soon as they occurred.

All of this was still quite cumbersome, such that the need naturally and quickly arose for the creation of a new account able to indicate daily changes in assets. In many firms, this was called the ‘surplus and deficit account’. Here a company’s earnings were determined by the algebraic sum of the increases and decreases in the company’s wealth resulting from its operations. We have evidence that the surplus and deficit account was present in Tuscany by the late-thirteenth century. 20

The creation of the ledger, also known as the Libro grande (‘great book’), represented the definitive simplification of the procedure. It emerged from the old debtors and creditors book, which contained the merchandise book and, over time, basic accounts, and elementary or derivative accounts.

From the last decades of the fourteenth century, we have evidence of a double-entry journal which indicated how to post values each time to the ledger accounts, in chronological order. Federigo Melis published the oldest example of a double-entry journal in Tuscany, which dates to 1391. This account book of the company Del Bene and Lippi shows entries introduced by the word a (‘to’) followed by accounts to be recorded as debits in the ledger, as well as others beginning with da (‘from’), which precedes those to be entered as credits. The account in which the corresponding entry was to be recorded was indicated in each description, with the left margin showing the respective page numbers of the ledger. 21 In firms which did not keep this journal, we find a series of large and small preparatory books that gave rise to entries in the ledger. For example, the Memoriale 22 (‘diary’) contained the first recording of credit and debit operations together with many qualitative descriptions, while the libro di Ricevute e Mandate di Balle (‘book of bales received and dispatched’) contained descriptive notations of the movement of goods with the relevant costs.

In light of the above considerations, we may conclude that the double-entry method had already come into being by the end of the thirteenth century. Indeed, in 1299–1300, accountants at another company, Farolfi, used the capital account and the surplus and deficit account, which had the characteristics and functions that we have noted. 23 In the following decades, this accounting method spread among companies and merchant-banking houses, with gradual improvements in its efficiency leading to the milestone of the introduction of the double-entry journal. There is no evidence that this method emerged within banks 24 : while we cannot exclude this possibility, we must recall that in that historical period the specialised function of the bank had not yet taken root and that companies themselves carried out other operations, including those of a commercial nature.

Conclusion

We have seen that the expansion and the nature of economic activity had an impact on accounting systems, shaping them according to various needs. This process evolved through forms of pragmatic adaptation, which had an impact on various aspects of bookkeeping. This development did not produce a clear distinction between new and old accounting methods, as Basil Yamey (1949: 127–128) argued. Instead, it was characterised by gradual and contradictory changes that spread the double-entry method among accountants and managers. This process was influenced by the conditions of economic growth in Tuscany between the thirteenth and sixteenth centuries. Here, a social and economic model was founded on factors such as risk culture and entrepreneurial spirit, elements which contributed to the creation of companies that paid great attention to ways of organising work and to the valorisation of human capital. In addition, the pragmatism of economic operators played an important role. In short, as commerce intensified and merchant companies expanded, questions of efficient bookkeeping became tantamount, forcing accountants to build a pragmatic model that was not the result of abstract rules.

From the first half of the fourteenth century, the double-entry method was prevalent in Tuscan companies, although certain limitations are evident: a lack of manuals, together with the character and restricted knowledge of accountants, meant that bookkeeping operations were marked by differing degrees of development. 25 In the same way that the social and cultural context played a role in the gradual formation of bookkeeping systems, accounting was in turn an influential instrument for the entrepreneur, who carefully preserved its methods once he understood their importance.

After the close of each fiscal year, when all the lists of balances had been completed, Francesco Datini had the papers and accounts collected by each of his companies sent to him. Letters and books arrived in Prato, where Datini was based; here the merchant duly double-checked the figures. This scrupulous verification of the accuracy of the calculations not only shows that accounting methods were important tools for controlling business operations but also reveals how accounting had the capability of influencing the organisational life of a company.

Footnotes

Acknowledgements

The author is very grateful to the Joint Editor Professor Carolyn Fowler and the Editorial Assistant Anna Burnett-Howard as well as to the two anonymous referees for their useful and constructive comments.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.